As filed with the Securities and Exchange Commission on March 5, 2004.

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549

FORM 20-F

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE

SECURITIES EXCHANGE ACT OF 1934

or

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2003

or

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from N/A to N/A

Commission file number: 1-14930

HSBC Holdings plc (Exact name of Registrant as specified in its charter)

N/A

United Kingdom

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organisation)

8 Canada Square London E14 5HQ United Kingdom (Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

Title of each class

Name of each exchange on which registered

Ordinary Shares, nominal value US$0.50 each.

American Depository Shares, each representing 5 Ordinary Shares of nominal value US$0.50 each.

London Stock Exchange Hong Kong Stock Exchange Euronext Paris New York Stock Exchange

Securities registered or to be registered pursuant to Section 12(g) of the Securities Exchange Act of 1934:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Securities Exchange Act of 1934:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the period covered by the annual report:

Ordinary Shares, nominal value US$0.50 each

10,998,301,166

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes

No

Indicate by check mark which financial statements Item the registrant has elected to follow:

Unless the context requires otherwise, ‘HSBC Holdings’ means HSBC Holdings plc and ‘HSBC’ or the ‘Group’ means HSBC Holdings together with its subsidiary undertakings. Within this document the

Hong Kong Special Administrative Region of the People’s Republic of China is referred to as ‘Hong Kong’.

HSBC’s Financial Statements and Notes thereon, as set out on pages 233 to 366, are prepared in accordance with UK Generally Accepted Accounting Principles (‘UK GAAP’). HSBC uses the US dollar as its reporting currency because the US dollar and currencies linked to it form the major currency bloc in which HSBC transacts its business. As HSBC is listed on the New York Stock Exchange, it also reconciles certain financial information to US Generally Accepted Accounting Principles (‘US GAAP’), which differ in certain respects from UK GAAP as explained on page 326 and reconciled in Note 50 of the ‘Notes on the Financial Statements’. Unless otherwise stated, the numbers presented in this document have been prepared in accordance with UK GAAP.

HSBC judges its own performance by comparing returns before goodwill amortisation on cash invested as HSBC believes this gives an important measure of its underlying performance and facilitates comparison with its peer group. Profit before goodwill amortisation is derived by adjusting reported earnings to eliminate the impact of the amortisation of goodwill arising on acquisitions. The derivation of non-GAAP measures from the equivalent reported measures is explained in the ‘Footnotes to Financial Highlights’ on page 4.

2003

2002

US$m

US$m

For the year (excluding goodwill amortisation)

Operating profit before provisions1

19,990

11,641

Profit on ordinary activities before tax2

14,401

10,513

Profit attributable to shareholders2

10,359

7,102

For the year (as reported)

Operating profit before provisions

18,540

10,787

Profit on ordinary activities before tax

12,816

9,650

Profit attributable to shareholders

8,774

6,239

Dividends

(6,532

)

(5,001

)

At year-end

Shareholders’ funds3

74,473

51,765

Capital resources

74,042

57,430

Customer accounts and deposits by banks

643,556

548,371

Total assets3

1,034,216

758,605

Risk-weighted assets

618,662

430,551

US$

US$

Per ordinary share4

Basic earnings

0.84

0.67

Earnings excluding goodwill amortisation5

0.99

0.76

Diluted earnings

0.83

0.66

Dividends

0.60

0.53

Net asset value at year end

6.79

5.46

At 31 December 2003

At 31 December 2002

Share information

US$0.50 ordinary shares in issue

10,960

m

9,481

m

Market capitalisation

US$172

bn

US$105

bn

Closing market price per ordinary share:

– London

£8.78

£6.87

– Hong Kong

HK$122.50

HK$85.25

Closing market price per American Depositary Share (‘ADS’)6

US$78.82

US$54.98

HSBC

Benchmark

Total shareholder return to 31 December 20037

–over 1 year

136

132

–since 1 January 19998

211

126

For the above footnotes, see ‘Footnotes to Financial Highlights’ on page 4.

Provisions for bad and doubtful debts as a percentage of operating profits before goodwill amortisation and provisions

30.5

11.3

Provisions for bad and doubtful debts as a percentage of average gross customer advances:

– in aggregate

1.2

0.4

– Consumer Finance (Household)12

5.2

n/a

– other HSBC

0.4

0.4

Total provisions outstanding as a percentage of non-performing loans at year end:

– in aggregate

91.0

86.7

– Consumer Finance (Household)12

110.5

n/a

– other HSBC

82.1

86.7

Efficiency and revenue mix ratios

Cost:income ratio (excluding goodwill amortisation)13

51.3

56.2

As a percentage of total operating income:

– net interest income

62.3

58.1

– other operating income

37.7

41.9

– net fees and commissions

25.3

29.4

– dealing profits

5.3

4.9

Constant currency

Constant currency comparatives in respect of 2002 and 2001, used in the 2003 and 2002 commentaries respectively, are computed by retranslating into US dollars:

•

the profit and loss accounts for 2002 and 2001 of non-US dollar branches, subsidiary undertakings, joint ventures and associates at the average rates of exchange for 2003 and 2002 respectively; and

•

the balance sheets at 31 December 2002 and 2001 for non-US dollar branches, subsidiary undertakings, joint ventures and associates at the rates of exchange ruling at 31 December 2003 and 2002 respectively.

No adjustment is made to the exchange rates used to translate foreign currency denominated assets and liabilities into the functional currency of any HSBC branches, subsidiary undertakings, joint ventures and associates.

2003 compared with 2002

2002 compared with 2001

As

reported

Constant

currency

As

reported

Constant

currency

%

%

%

%

Operating income and cost growth

Net interest income

66

58

5

6

Fees and commissions (net)

33

24

5

4

Dealing profits

66

58

(22

)

(23

)

Total operating income

54

46

3

3

Administrative expenses (excluding goodwill

amortisation)

41

32

2

(4

)

For the above footnotes, see ‘Footnotes to Financial Highlights’ on page 4.

Operating profit before provisions and excluding goodwill amortisation can be reconciled to the equivalent reported measure by deducting goodwill amortisation of US$1,450 million ( 2002: US$854 million).

2

The profit on ordinary activities before tax and the profit attributable to shareholders excluding, in each case, goodwill amortisation, can be reconciled to the equivalent reported measures by deducting goodwill amortisation, including that attributable to joint ventures and associates, of US$1,585 million (2002: US$863 million).

3

The figures for shareholders’ funds, total assets and average total assets for 2002 and, in the Five-year comparison, 2001 and 2000, have been restated to reflect the adoption of Urgent Issues Task Force (‘UITF’) Abstracts 37 ‘Purchases and sales of own shares’, and 38 ‘Accounting for ESOP trusts’, details of which are set out in Note 1 of the ‘Notes on the Financial Statements’ on pages 239 to 240. The 1999 comparatives in the Five-year comparison have not been restated as any adjustment would not significantly alter the figures. Therefore, any benefit to be obtained from restatement would be outweighed by the cost of the exercise.

4

Per ordinary share amounts reported here and throughout the document reflect the share capital reorganisation on 2 July 1999.

5

Earnings excluding goodwill amortisation per ordinary share are calculated by dividing profit excluding goodwill amortisation attributable to shareholders (as explained in note 2 above) by the weighted average number of ordinary shares in issue and held outside the Group during the year, which is the same number used in the calculation of basic earnings per share on a reported basis.

6

Each ADS represents 5 ordinary shares.

7

Total shareholder return (‘TSR’) is defined on page 218.

8

HSBC’s governing objective for its five year strategic plan ended 31 December 2003 was to beat the TSR of its defined peer group benchmark. An additional target objective was set to achieve a doubling of TSR over the five years beginning on 1 January 1999.

9

The definition of return on invested capital and a reconciliation to the equivalent GAAP measures are set out on page 58.

10

The return on average net tangible equity is defined as attributable profit excluding goodwill amortisation of US$10,359 million (2002: US$7,102 million) divided by average shareholders’ funds after deduction of average purchased goodwill of US$42.0 billion (2002: US$35.3 billion).

11

Average net tangible equity and average tangible assets are calculated by deducting average purchased goodwill net of cumulative amortisation of US$25.4 billion (2002: US$15.0 billion). The calculation of average risk-weighted assets is the same for both the reported basis and that excluding goodwill amortisation.

12

Annualised on the basis of the period of ownership in the year of acquisition.

13

The cost:income ratio, excluding goodwill amortisation, is defined as operating expenses excluding goodwill amortisation of US$1,450 million (2002: US$854 million) divided by operating income.

14

Capital resources are defined on page 173. A detailed computation for 2003 and 2002 is provided on page 175.

15

Net of suspended interest and provisions for bad and doubtful debts

16

Dividends per share expressed as a percentage of earnings per share (excluding goodwill amortisation)

17

Apart from shareholders’ funds and total assets at the 1999 year-end, the 1999 comparatives have not been restated to reflect the adoption of UK Financial Reporting Standard 19 ‘Deferred tax’ in 2002 as any adjustment made would not significantly alter the figures. Therefore, any benefit to be obtained from restatement would be outweighed by the cost of the exercise.

This Annual Report contains certain forward-looking statements with respect to the financial condition, results of operations and business of HSBC.

Statements that are not historical facts, including statements about HSBC’s beliefs and expectations, are forward-looking statements. Words such as ‘expects’, ‘anticipates’, ‘intends’, ‘plans’, ‘believes’, ‘seeks’, ‘estimates’, ‘potential’, ‘reasonably possible’ and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are based on current plans, estimates and projections, and therefore undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made, and it should not be assumed that they have been revised or updated in the light of new information or future events.

Written and/or oral forward-looking statements may also be made in the periodic reports to the US Securities and Exchange Commission, summary financial statements to shareholders, proxy statements, offering circulars and prospectuses, press releases and other written materials, and in oral statements made by HSBC’s Directors, officers or employees to third parties, including financial analysts.

Forward-looking statements involve inherent risks and uncertainties. Readers are cautioned that a number of factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. These factors include, among others:

·

changes in general economic conditions in the markets in which HSBC operates, such as:

-

changes in foreign exchange rates, in both market exchange rates (for example, between the US dollar and the pound sterling) and government-established exchange rates (for example, between the Hong Kong dollar and the US dollar);

-

volatility in interest rates;

-

volatility in equity markets, including in the smaller and less liquid trading markets in Asia and South America;

-

lack of liquidity in wholesale funding markets in periods of economic or political crisis;

-

volatility in national real estate markets, particularly consumer-owned real estate markets;

-

continuing or deepening recessions and employment fluctuations; and

-

consumer perception as to the continuing availability of credit, and price competition in the market segments served by HSBC.

·

changes in governmental policy and regulation, including:

-

the monetary, interest rate and other policies of central banks and bank and other regulatory authorities, including the UK Financial Services Authority, the Bank of England, the Hong Kong Monetary Authority, the US Federal Reserve, the European Central Bank, the People’s Bank of China and the central banks of other leading economies and markets where HSBC operates;

-

expropriation, nationalisation, confiscation of assets and changes in legislation relating to foreign ownership;

-

initiatives by local, state and national regulatory agencies or legislative bodies to revise the practices, pricing or responsibilities of financial institutions serving their consumer markets;

-

changes in personal bankruptcy legislation in the principal markets in which HSBC operates and the consequences thereof;

-

general changes in governmental policy that may significantly influence investor decisions in particular markets in which HSBC operates;

-

other unfavourable political or diplomatic developments producing social instability or legal uncertainty which in turn may affect demand for HSBC’s products and services;

-

the costs, effects and outcomes of regulatory reviews, actions or litigation, including any additional compliance requirements;

the ability of the Government of Argentina to attract international support for the measures necessary to restructure its debt obligations and create a viable financial system with stability in monetary, fiscal and exchange rate policies; and

-

the effects of competition in the markets where HSBC operates including increased competition resulting from new types of affiliations between banks and financial services companies, including securities firms, particularly in the United States.

·

factors specific to HSBC:

-

the success of HSBC in adequately identifying the risks it faces, such as the incidence of loan losses or delinquency, and

managing those risks (through account management, hedging and other techniques). Effective risk management depends on, among other things, HSBC’s ability through stress testing and other techniques to prepare for events that cannot be captured by the statistical models it uses; and

-

the success of HSBC in integrating the recently acquired Grupo Financiero Bital S.A. de C.V. (now Grupo Financiero HSBC S.A. de C.V. (‘HSBC Mexico’)), Household International, Inc. (‘Household’), Losango Promotora de Vendas, and The Bank of Bermuda Limited.

Information About the Enforceability of Judgements made in the United States

HSBC Holdings is a public limited company incorporated in England and Wales. Most of HSBC Holdings’ Directors and executive officers live outside the United States. As a result, it may not be possible to serve process on such persons or HSBC Holdings in the United States or to enforce judgements obtained in US courts against them or HSBC Holdings based on civil liability provisions of the securities laws of the United States. There is doubt as to whether English courts would enforce:

·

certain civil liabilities under US securities laws

in original actions; or

·

judgements of US courts based upon these civil liability provisions.

In addition, awards of punitive damages in actions brought in the United States or elsewhere may be unenforceable in the United Kingdom. The enforceability of any judgement in the United Kingdom will depend on the particular facts of the case as well as the laws and treaties in effect at the time.

Exchange Controls and Other Limitations Affecting Equity Security Holders

There are currently no UK laws, decrees or regulations which would prevent the transfer of capital or remittance of distributable profits by way of dividends and other payments to holders of HSBC Holdings’ equity securities who are not residents of the United Kingdom. There are also no restrictions

under the laws of the United Kingdom or the terms of the Memorandum and Articles of Association of HSBC Holdings concerning the right of non-resident or foreign owners to hold HSBC Holdings’ equity securities or, when entitled to vote, to do so.

HSBC is one of the largest banking and financial services organisations in the world, with a market capitalisation of US$172 billion at 31 December 2003.

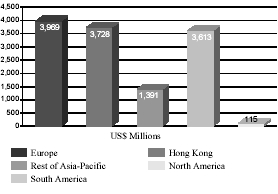

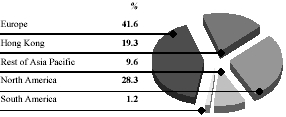

Headquartered in London, HSBC operates through long-established businesses and has an international network of over 9,500 offices in 79 countries and territories in five regions: Europe; Hong Kong; the rest of Asia-Pacific, including the Middle East and Africa; North America; and South America. Within these geographical regions, a comprehensive range of financial services is offered to personal, commercial, corporate, institutional, investment and private banking clients. HSBC manages its business through the following customer groups: Personal Financial Services; Commercial Banking; Corporate, Investment Banking and Markets; and Private Banking. Whilst part of Personal Financial Services, the consumer finance operations of Household are currently a distinct business and have been separately identified accordingly. Services are delivered through businesses which usually operate as domestic banks, typically with large retail deposit bases and strong liquidity and capital ratios. In North America, Household is one of the largest consumer finance companies in the US, and is substantially funded in the wholesale market. By using HSBC’s extensive technological links, businesses are able to access its wide range of products and services and adapt them to local customer needs.

The establishment of HSBC and its hexagon symbol as a uniform, international brand has ensured that it has become an increasingly familiar sight across the world.

History and development

The founding member of HSBC, The Hongkong and Shanghai Banking Corporation Limited (‘The Hongkong and Shanghai Banking Corporation’), was established in Hong Kong and Shanghai in 1865. The bank expanded rapidly, with an emphasis on building up representation in China and the rest of the Asia-Pacific region, whilst also establishing a presence in the major financial and trading centres in Europe and America.

In the mid-1950s, The Hongkong and Shanghai Banking Corporation embarked on a strategy of pursuing profitable growth through acquisition as well as organic development – a combination that has remained a key feature of HSBC’s approach ever since.

As each acquisition has been made, HSBC has focused on integrating its newly acquired operations with its existing businesses with a view to maximising the synergy between the various components. Key to this integration process is to blend local and international expertise.

The most significant developments are described below. Other acquisitions in 2003 are discussed in the section headed ‘Business highlights in 2003’ under the relevant geographical region on pages 15 to 26.

The Hongkong and Shanghai Banking Corporation purchased The Mercantile Bank of India Limited and The British Bank of the Middle East (now HSBC Bank Middle East Limited) in 1959. In 1965, The Hongkong and Shanghai Banking Corporation acquired a 51 per cent interest (subsequently increased to 62.14 per cent) in Hang Seng Bank Limited (‘Hang Seng Bank’), consolidating its position in Hong Kong. Hang Seng Bank is the second-largest listed bank in Hong Kong by market capitalisation.

From the beginning of the 1980s, The Hongkong and Shanghai Banking Corporation began to focus its acquisition strategy on the UK. In 1987, it purchased a 14.9 per cent interest in Midland Bank plc, now HSBC Bank plc (‘HSBC Bank’), one of the UK’s principal clearing banks. In 1991, HSBC Holdings plc was established as the parent company of HSBC and, in 1992, HSBC Holdings purchased the remaining interests in HSBC Bank. In connection with this acquisition, HSBC’s head office was transferred from Hong Kong to London in January 1993. To expand its base in the euro zone, in October 2000 HSBC completed its acquisition of 99.99 per cent of the issued share capital of CCF S.A. (‘CCF’), a major French banking group.

The Hongkong and Shanghai Banking Corporation entered the US market in 1980 by acquiring a 51 per cent interest in Marine Midland Banks, Inc. (now HSBC USA Inc.). The remaining interest was acquired in 1987.

In 1981, The Hongkong and Shanghai Banking Corporation incorporated its extant Canadian operations. HSBC Bank Canada has since made numerous acquisitions, expanding rapidly to become the largest foreign-owned bank in Canada and the seventh-largest overall at 31 December 2003.

In 1997, HSBC assumed selected assets, liabilities and subsidiaries of Banco Bamerindus do Brasil S.A. following the intervention of the Central Bank of Brazil, and completed the acquisition of Grupo Roberts in Argentina.

In December 1999, HSBC acquired Republic New York Corporation, subsequently merged with HSBC USA Inc., and Safra Republic Holdings S.A. (together ‘Republic’).

In 2002, HSBC made further steps in expanding its presence in North America, completing the acquisition of 99.59 per cent of Grupo Financiero Bital S.A. de C.V. (now ‘HSBC Mexico’), the fifth-largest banking group in Mexico measured by deposits and assets.

Mainland China remains a critical long-term growth area for the Group. In 2002, HSBC completed the acquisition of a 10 per cent equity stake in Ping An Insurance Company of China Limited. Ping An Insurance is the second-largest life insurer and the third-largest insurer in mainland China.

In March 2003, HSBC acquired Household International, Inc. (‘Household’) for a consideration of approximately US$14.8 billion. The acquisition has significantly increased the contribution from HSBC’s North American business. In particular, Household offers HSBC national coverage in the US for consumer lending, credit cards and credit insurance through varied distribution channels, including over 1,300 branch offices in 45 states.

In October 2003, HSBC agreed to acquire The Bank of Bermuda Limited for US$1.3 billion, adding a strong position in the local banking market in Bermuda and significant scale and geographical spread to HSBC’s existing international fund administration, private banking, trust and payments, and cash management businesses. The acquisition was completed on 18 February 2004.

In December 2003, HSBC acquired substantially all of Lloyds TSB Group plc’s onshore and offshore businesses and assets related to Brazil for US$745 million. Included in the transaction was the

acquisition of all the shares of Banco Lloyds TSB S.A. – Banco Múltiplo and a consumer finance company, Losango Promotora de Vendas (‘Losango’).

Outlook

In 2004, the Group has already seen growth in consumer spending and borrowing, in increased merger and acquisition activity, and a modest resumption of growth in demand for equity investment products. The Group also sees improving prospects for economic growth and private sector employment, particularly in the US and in Hong Kong.

In emerging markets, such as Brazil, Mexico and the ASEAN countries, relatively stable currencies and historically low interest rates are promoting consumer activity, fuelling domestic growth and reducing export dependence. China plays an increasingly important role, not only through its export growth, but also as the fastest growing market for commodity producing countries and for those developed countries which are supplying the technology, equipment and services to support its economic expansion.

The Group is conscious of the changing nature of the global economy and the speed of change and continues to monitor the impact on sentiment and consumer spending of globally strong property prices, which continue to rise faster than underlying wage growth in many developed markets. While such rises are understandable in the context of low interest rates and limited appetite for alternative investment opportunities, in the long run property prices have to be linked to income growth.

The picture for 2004 therefore is one of improving sentiment and stronger growth prospects in the near term, but with the potential risk of an unexpected shock as a result of circumstances which would cause a spike in either short-term interest rates or commodity prices.

Against this backdrop HSBC expects to concentrate on building its businesses steadily. HSBC expects to see lending to consumers around the world rise as a proportion of our total lending, with the emphasis on real estate secured lending. The Group also expect to see business in the US grow in importance to HSBC as the potential of the

Household acquisition is realised and as the US economy shows its flexibility and responds to the lower value of the dollar.

Strategy

At the end of 1998, HSBC launched Managing for Value, a five-year plan to take the Group into the 21st Century. Over the life of the plan, HSBC made significant progress against the eight strategic imperatives included therein.

Under Managing for Value, HSBC established HSBC and its hexagon symbol as a globally recognised brand and greatly increased the scope and penetration of its wealth management services in a number of key markets. Corporate, Investment Banking and Markets operations were completely integrated, enabling the Group to pursue a strategy of seamlessly servicing the needs of the largest international companies and institutions, and build corporate origination and cross-selling capabilities. A risk adjusted cost of capital methodology was introduced and applied. (For the application of economic profit in HSBC and its results for 2003 see page 58.) Good progress was made against the other strategic imperatives announced under the initiative.

In financial terms, HSBC achieved its objective of doubling Total Shareholder Return (‘TSR’) and beating the TSR performance of a peer group of leading banks over the period. TSR is a measure of the growth in the value of a share over a specific period with dividends reinvested. Starting with a benchmark of 100 on 31 December 1998, HSBC’s TSR more than doubled to 211 on 31 December 2003, while that of its peer group stood at 126.

As HSBC worked on its strategic plan for the next five years it was clear that there were many opportunities to develop HSBC’s businesses further, and also that HSBC could build more from the structural and business changes achieved in the recent past. For instance, during the five years of Managing for Value, HSBC made investments in the US (Republic and Household), France (CCF) and Mexico (HSBC Mexico), as a result of which an additional 100,000 employees joined the Group. This expansion changed the profile of HSBC’s business, increased the complexity of the Group and brought new management and business challenges as well as exciting opportunities.

The new plan, developed to build on the achievements of the Managing for Value strategy and take the Group forward, is now being implemented. This plan, called Managing for Growth, was launched at the end of 2003. It provides HSBC with a blueprint for growth and development during the next five years. The plan is an evolutionary, not revolutionary, strategy. It builds on HSBC’s strengths and it addresses the areas where further improvement is considered both desirable and attainable.

Management’s vision for the Group remains unchanged: HSBC aims to be the world’s leading financial services company. In this context, ‘leading’ means preferred, admired and dynamic, and being recognised for giving the customer a fair deal. HSBC will strive to secure and maintain a leading position within each of its customer groups in selected markets.

HSBC will remain focused on growing its TSR. In an era of low interest rates and low nominal growth rates, HSBC remains committed to exceeding a benchmark based on peer group comparison. For full details of the benchmark, see page 217. The peer group of banks has been updated to include HSBC’s current principal competitors, and HSBC will chart its TSR progress on a three-year rolling basis and over the five-year plan period.

HSBC’s core values are integral to its strategy, and communicating them to shareholders, customers and employees is intrinsic to the plan. These values comprise a preference for long-term, ethical client relationships; high productivity through teamwork; a confident and ambitious sense of excellence; being international in outlook and character; prudence; creativity and strong marketing.

In the plan, HSBC also recognises its corporate social responsibility (‘CSR’), which is essential to sustaining the Group’s long-term success in the community. HSBC has always had a strong sense of corporate social responsibility, and believes that there is no fundamental conflict between being a good corporate citizen and being sustainably profitable. Moreover, the pressures to comply with public expectations across a wide spectrum of social, ethical and environmental issues are growing rapidly. The strategy therefore calls for a renewed recognition of HSBC’s wider obligations to society and for increased external communication of the Group’s CSR policies and performance, particularly on education and the environment, which will remain

the principal beneficiaries of HSBC’s philanthropic activities.

HSBC’s new plan is led by customer groups, and specific strategies will be implemented for each of them. The expression ‘customer group’ is new in 2003. Previously ‘customer groups’ were called ‘lines of business’, but HSBC believes the new term reinforces more accurately to all its employees the Group’s customer focus.

The acquisition of Household in 2003 highlighted the importance within Personal Financial Services of a distinctive customer group, Consumer Finance, to augment HSBC’s existing activities in Personal Financial Services. HSBC’s other customer groups are Corporate, Investment Banking and Markets; Commercial Banking; and Private Banking.

Key elements in achieving HSBC’s objectives for its customer groups will be accelerating the rate of growth of revenue; developing the brand strategy further; improving productivity; and maintaining the Group’s prudent risk management and strong financial position. Developing the skills of HSBC’s staff will also be critical and it will be necessary to ensure that all employees understand how they can contribute to the successful achievement of the Group’s objectives. Employees who achieve this contribution will be rewarded accordingly.

Operating management will continue to be organised geographically under four regional intermediate head offices, with business activities concentrated in locations where growth and critical mass are to be found.

The plan contains eight strategic imperatives:

•

Brand: make HSBC and its hexagon symbol one of the world’s leading brands for customer experience and corporate social responsibility;

•

Personal Financial Services (‘PFS’): drive growth in key markets and through appropriate channels to make HSBC the strongest global player in PFS;

•

Consumer Finance: extend HSBC’s new business to existing customers and penetrate new markets;

•

Corporate, Investment Banking and Markets: accelerate growth through enhanced capital markets and advisory capabilities focused on the client;

•

Commercial Banking: make the most of HSBC’s international customer base through effective customer relationship management and improved product offering in all the Group’s markets;

•

Private Banking: serve the Group’s highest value personal clients around the world, utilising the investments already made;

•

Attract, develop and motivate HSBC’s people, rewarding success and rejecting mediocrity; and

•

TSR: fulfil HSBC’s TSR target by achieving strong competitive performances in earnings per share growth and efficiency.

Employees and management

At 31 December 2003, HSBC’s customers were served by 232,000 employees (including part-time employees) worldwide, compared with 192,000 at 31 December 2002 and 180,000 at 31 December 2001. The main centres of employment are the UK with 56,000 employees, the US (43,000), Hong Kong (24,000), Brazil (25,000), Mexico (18,500) and France (14,000). HSBC negotiates with recognised unions, and estimates that approximately 44 per cent of its employees are unionised. The highest concentrations of union membership are in Brazil, France, India, Malaysia, Malta, Mexico, the Philippines, Singapore and the UK. HSBC has not experienced any material disruptions to its operations from labour disputes during the past five years.

In support of its new strategy, HSBC continues to focus on attracting, developing and motivating the very best individuals. Emphasis is therefore given to performance management; reward; talent management, including graduate recruitment and international secondments; diversity; and learning and development. Ensuring that employee satisfaction with the working experience is kept as high as possible is seen as beneficial to shareholders, employees and customers alike.

HSBC is proud of its diverse workforce, which is able to communicate with HSBC’s customers in local languages and dialects across 79 countries and territories. A continuing focus on policies that encourage an inclusive working environment and the development of career opportunities for all, regardless of ethnicity, gender or grade, is a key part of positioning HSBC as an employer of choice.

HSBC operates in a highly competitive and international business environment and as such is obliged to manage its costs realistically, responding to the availability of talent pools which are proven to be both efficient and cost effective. This can lead to the migration of tasks to different geographical locations as education levels improve, and as investments in technology and telecommunications facilitate access to those locations. As a result, job losses can arise. HSBC has a good record of communicating openly and sensitively in these circumstances and of reassigning employees and minimising compulsory redundancies, wherever possible.

The quality of HSBC’s employees represents a significant competitive advantage. The international mix of staff, working in a meritocracy, enables HSBC to resource operations with employees who have a detailed knowledge of local markets, whilst maintaining a global perspective. To maintain this balance, international mobility is seen as vital to sharing best practice and is actively encouraged and managed. HSBC promotes and recruits the most able and attaches great importance to cultivating its own talent. It values teamwork and collective management. Senior management succession is planned to be as seamless as possible.

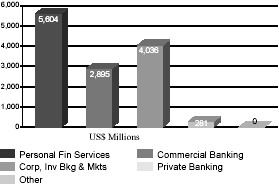

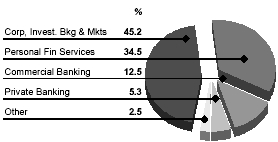

Customer Groups

Profit before tax by customer group

Year ended 31 December 2003

Total assets by customer group Year ended 31 December 2003

*

excludes Hong Kong Government certificates of indebtedness

Personal Financial Services

Personal Financial Services provides some 39 million individual and self-employed customers with a wide range of banking and related financial services. Customer Relationship Management (‘CRM’) systems and processes are used by HSBC employees to recognise and fulfil customer needs by identifying appropriate products and services and delivering them to the customer through their channel of preference. Examples include current, cheque and savings accounts; loans and home finance; cards; payments; insurance; and investment services, including securities trading. Insurance products sold and distributed by HSBC through its branch networks include loan and health protection; life, property, casualty and health insurance; and pensions. HSBC acts as both a broker and an underwriter, and sees continuing opportunities to deliver insurance products to its personal customer base.

Personal Financial Services are increasingly delivered via self-service terminals, the telephone and the internet. Comprehensive financial planning services, covering customers’ investment, retirement, personal and asset protection needs are offered through specialist financial planning managers.

High net worth individuals and their families who choose the differentiated services offered within Private Banking are not included in this segment.

The most valuable of the 39 million Personal Financial Service customers worldwide are offered HSBCPremier. HSBC currentlyhas more than 880,000HSBC Premier customers, who have access to more than 250 specialisedPremier centres located in 31 countries. In addition to the standard range of personal banking products and services, HSBCPremier customers receive dedicated relationship

management and 24 hour priority telephone access and global travel assistance. In 2003 HSBCPremierInternational Services were introduced in eight countries, providing seamless account opening and credit history transfer across borders for HSBCPremier customers.

Consumer Finance

Within Personal Financial Services, Household’s operations in the US, the UK and Canada make credit available to customer groups not well catered for by traditional banking operations, facilitate point of sale credit in support of retail trading purchases and support major affiliate credit card programmes. At 31 December 2003 Household had over 60 million customers with total gross advances of US$121.7 billion. Consumer Finance products are offered through the following businesses:

Household’sconsumer lendingbusiness is one of the largest sub-prime home equity originators in the US, marketed under the HFC and Beneficial brand names through a network of over 1,300 branches in 45 states, direct mail, telemarketing, strategic alliances and the internet. ‘Sub-prime’ is a US categorisation which describes customers who have limited credit histories, modest incomes, high debt-to-income ratios, high loan-to-value ratios (for real estate secured products) or have experienced credit problems caused by occasional delinquencies, prior charge-offs, bankruptcy or other credit related actions. Consumer lending products include secured and unsecured loans such as first and second lien closed-end mortgages, open-ended home equity loans, personal loans and retail finance contracts.

Household’s mortgage servicesbusiness purchases first and second lien residential mortgage loans from a network of over 200 unaffiliated third party lenders (‘correspondents’) in the US. Purchases are either of pools of loans (‘bulk acquisitions’) or individual loan portfolios (‘flow acquisitions’) made under predetermined underwriting guidelines. Forward commitments are offered to selected correspondents to strengthen relationships and create a sustainable growth channel for this business. Household, through its subsidiary Decision One, also offers mortgage loans referred by mortgage brokers.

Household’sretail servicesbusiness is one of the largest providers of third party private label credit cards (or store cards) in the US based on receivables

outstanding, with over 60 merchant relationships and 14 million active customer accounts.

In addition to originating and refinancing motor vehicle loans, Household’s motor vehicle financebusiness purchases retail instalment contracts of US customers who do not have access to traditional prime based lending sources. The loans are largely sourced from a network of approximately 5,000 motor dealers.

Household’scredit card services business is the seventh largest issuer of MasterCard1 and Visa1credit cards in the US, and also includes affiliation cards such as the GM Card ® and the AFL-CIO Union Plus2 ® credit card. Also, credit cards issued in the name of Household’s Household Bank and Orchard Bank brands ar e offered to customers under-served by traditional providers, or are marketed primarily through merchant relationships established by the retail services business.

A wide range ofinsurance services is offered by Household to customers in the US, the UK and Canada who are typically under-insured by traditional sources. The purchase of insurance is never a condition of any loan or credit advanced by Household.

Therefund lending business accelerates access to funds for US taxpayers who are entitled to tax refunds. The business is seasonal with most revenues generated in the first three months of the year.

Household’s business in the UK provides mid-market consumers with mortgages, secured and unsecured loans, insurance products, credit cards and retail finance products. It concentrates on customer service through its 216 HFC Bank and Beneficial branches, and finances consumer electronics through its retail finance operations. In Canada, similar products are offered and, deposits are taken through Household’s trust operations there.

Commercial Banking

HSBC is one of the world’s leading banks in the

1

MasterCard is a registered trademark of MasterCard International, Incorporated and Visa is a registered trademark of Visa USA, Inc.

2

The Union plus MasterCard and Visa credit card programme is an affinity arrangement with Union Privilege under which credit cards are offered to members of unions affiliated with the American Federation of Labor and Congress of Industrial organisations (‘AFL-CIO’).

provision of financial services and products to small and medium-sized businesses, with over 2 million business customers including sole proprietors, partnerships, clubs and associations, incorporated businesses and publicly quoted companies.

At 31 December 2003, HSBC had total commercial customer deposits of US$111.5 billion and total commercial customer loans and advances, net of suspended interest and provisions for bad and doubtful debts, of US$103.5 billion.

The Commercial Banking segment places particular emphasis on multi-disciplinary and geographical collaboration in meeting its commercial customers’ needs. This differentiated service allows HSBC to broaden and enhance its offering to its Commercial Banking customers. The range of products includes:

Payments and cash management: HSBC is a leading provider of payments, collections, liquidity management and account services worldwide, enabling financial institutions and corporate customers to manage their cash efficiently on a global basis. HSBC’s extensive network of offices and strong domestic capabilities in many countries, including direct access to local clearing systems, enhance its ability to provide high-quality cash management services.

e-banking: A key component of HSBC’s provision of financial services to commercial customers is continuing innovation and flexibility in electronic delivery solutions.

Wealth management services: These include advice and products related to savings and investments. They are provided to commercial banking customers and their employees through HSBC’s worldwide network of branches and business banking centres.

Insurance: HSBC offers insurance protection, employee benefits programmes and pension schemes designed to meet the needs of businesses and their employees, and to help fulfill the applicable statutory obligations of client companies. These products are provided by HSBC either as an intermediary (broker, agent or consultant) or as a supplier of in-house or third party offerings. Products and services include a full range of commercial insurance, including pension schemes; healthcare schemes; ‘key man’ life insurance; car fleet; goods in transit; trade credit protection; risk management and insurance due

diligence reviews; and actuarial/employee benefit consultancy.

Trade services: HSBC has more than 130 years of experience in trade services. A complete range of traditional documentary credit, collections and financing products is offered, as well as specialised services such as insured export finance, international factoring and forfaiting. HSBC’s expertise is supported by highly automated systems.

Leasing, finance and factoring: HSBC provides leasing, finance (including instalment and invoice finance) and domestic factoring services, primarily to commercial customers in the UK, Hong Kong and France. Special divisions have been established to finance vehicles, plant and equipment, materials handling, machinery and large complex leases.

Corporate, Investment Banking and Markets

HSBC’s Corporate, Investment Banking and Markets business provides tailored financial solutions to major government, corporate and institutional clients worldwide. Managed as a global business, this customer group operates a long-term relationship management approach to build a full understanding of clients’ financial requirements. Sectoral client service teams comprising relationship managers and product specialists develop financial solutions to meet individual client needs. With dedicated offices in over 50 countries and with access to HSBC’s worldwide presence and capabilities, this business serves subsidiaries and offices of these clients on a global basis.

Products and services offered include:

Global Markets: HSBC’s operations in Global Markets consist of treasury and capital markets services for supranationals, central banks, corporations, institutional and private investors, financial institutions and other market participants. Products include:

•

foreign exchange;

•

currency, interest rate, bond, credit, equity and other specialised derivatives;

•

government and non-government fixed income and money market instruments;

trading for institutional, corporate, private clients and asset management services, including global investment advisory and fund management services; and

•

capital raising, both publicly and privately, including debt and equity capital, structured finance and syndicated finance, and distribution of these instruments utilising links with HSBC’s global networks.

Global Transaction Banking: This includes international, regional and ‘in-country’ payments and cash management services; trade services, particularly the specialised ‘supply chain’ product; and securities services, where HSBC is one of the world’s leading custodians providing custody and clearing services and funds administration to both domestic and cross-border investors. Factoring and banknotes services are also provided by specialist units.

Corporate and Institutional Banking: This includes:

•

direct lending, including structured finance for complex investment facilities;

•

leasing finance with an emphasis on ‘large ticket’ transactions; and

•

deposit-taking.

Global Investment Banking: This comprises:

•

corporate finance and advisory services for mergers and acquisitions, asset disposals, stock exchange listings, privatisations and capital restructurings;

•

project and export finance services providing non-recourse finance to exporters, importers and financial institutions, and working closely with all major export credit agencies; and

•

financing and risk advisory services.

Asset management services: This comprises Asset Management products and services for institutional investors, intermediaries and individual investors and their advisors.

Private Banking

HSBC is one of the world’s leading international private banking groups with total client funds under management of US$169 billion at 31 December 2003. In December 2003, HSBC announced the

adoption of HSBC Private Bank as the worldwide marketing name for its principal private banking business.

Drawing on the strength of the HSBC Group and utilising the best products from the marketplace, Private Banking works with its clients to offer both traditional and innovative ways to manage and preserve wealth whilst optimising returns. Products and services offered include:

Investment services: These comprise both advisory and discretionary investment services. A wide range of investment vehicles is covered, including bonds, equities, derivatives, structured products, mutual funds and hedge funds. Supported by five major advisory centres in Hong Kong, Singapore, Geneva, New York and London, Private Banking selects and validates the most suitable investments for clients’ needs and investment strategies.

Global wealth solutions: These comprise planning, trustee and other fiduciary services designed to protect existing wealth and create tailored structures to preserve wealth for future generations. Areas of expertise include trusts, foundations, charitable trusts, private investment companies, insurance vehicles and offshore structures.

Specialist advisory services: Private Banking offers expertise in several specialist areas of wealth management including tax advisory, family office advisory, charities and foundations, media, diamonds and jewellery, and real estate. Such specialist advisers are available to deliver products and services which are tailored to meet the full range of high net worth clients’ individual financial needs.

General banking services: These are the ancillary services necessary for the management of clients’ finances. They include treasury and foreign exchange, offshore and onshore deposits, tailor-made loans and internet banking. The skills and products available in HSBC’s other customer groups, such as corporate banking, investment banking and insurance are also offered to Private Banking clients.

HSBC Private Bank is the marketing name for the private banking business conducted by the principal private banking subsidiaries of the HSBC Group worldwide. Private Banking services are also provided by HSBC Guyerzeller and HSBC Trinkaus & Burkhardt.

Excludes Hong Kong Government certificates of indebtedness.

Business highlights in 2003

For additional information regarding business developments in 2003, as well as comparative information relating to developments in 2002 and 2001, please refer to the ‘Financial Review’ on pages 36-117.

Europe

HSBC’s principal banking subsidiaries in Europe are HSBC Bank, CCF and HSBC Private Bank. HSBC provides a wide range of banking, treasury and financial services to personal, commercial and corporate customers in the UK, France, and across continental Europe, with strong coverage in Malta and Turkey. The bank’s strategy is to build long-term relationships attracting customers through value-for-money products and high-quality service.

General

•

The remarkable efforts of colleagues in Turkey ensured that business returned to normal following the two bomb blasts on 20 November, 2003 which severely damaged the Head Office and a branch in Istanbul. All branches were operating as normal the day after, with the exception of Beyoglu, which was damaged by the bomb at the British Consulate. Head Office employees relocated to a contingency site and the bank’s business recovery planning proved both highly effective and invaluable. In the face of the terrible events, colleagues responded with incredible courage and commitment. HSBC immediately launched support initiatives for the bereaved and those most impacted by the tragic events.

•

In March, HSBC added the consumer finance business, HFC Bank plc (‘HFC Bank’), to its European network as a consequence of the Household acquisition. HFC Bank provides a range of loan and insurance products to over 3.5 million customers throughout the UK, making it one of the country’s largest pure consumer finance businesses.

Personal Financial Services

•

For the second year running, HSBC won a major category of the ‘What Mortgage?’ award in the UK and was the Mortgage Magazine winner of the ‘Lender of the Year’ award. First Direct won the Mortgage Advisor and Home Buyer Magazine award for ‘Offset Mortgage of the Year’.

•

In July, HSBC became the first British high street bank to offer an Islamic mortgage to the estimated UK Muslim population of 1.8 million. The Amanah Home Finance product was launched with the backing of HSBC's Dubai-based Amanah Finance division.

•

The Premier customer base in the UK grew by 57 per cent to over 280,000. Premier International, offering credit history transfer across borders and seamless account opening, was launched in the UK, Jersey (Offshore) and France, while Malta and Greece became the 30th and 31st countries to offer the HSBC Premier service.

In July, HSBC launched HSBC InvestDirect, a new online and telephone investment service in the UK. This provides internet and telephone share-dealing and price information across a broad range of UK equities and gilts.

•

HSBC in the UK was awarded the coveted ‘Five Star Award’ from Money Management magazine for its regular premium stakeholder pensions.

•

HSBC’s Private Clients service was ranked the number one UK Independent Financial Adviser (‘IFA’) in a survey of the top 50 IFAs by Professional Advisor Magazine again in 2003.

•

In the UK, individual service reviews (a review of a customer’s financial service needs) were completed for more than 800,000 customers during the year, an increase of 67 per cent on 2002.

•

By the end of 2003, over 2 million customers in the UK were registered for personal internet banking and over 4.7 million customers are now registered for telephone banking.

•

Significant progress was made in migrating the UK card issuing business onto Household’s credit card system, improving both operational and cost efficiency. HSBC Card Services issued its highest ever number of new credit cards and gained a record number of competitor balance transfers in the UK, boosted by the introduction of a ‘0%’ balance transfer offer in July.

•

Following successful participation in the UK ‘chip and pin’ trials earlier in the year, HSBC will begin issuing chip and pin enabled credit and debit cards in 2004, delivering greater security for card users and reducing exposure to fraud costs.

•

HSBC expanded its UK debt counselling service for customers with potential repayment difficulties. The service works with customers to construct plans to manage debt more effectively ahead of possible problems.

Consumer Finance

•

In June, HFC Bank announced a long-term agreement with the John Lewis Partnership, the employee-owned UK department store and supermarket group, for the joint management and operation of the John Lewis, Peter Jones and Waitrose store card business. The agreement

•

involves the transfer of US$400 million of loans and 1.8 million cardholders to HFC Bank on a revenue-sharing basis. The bank will work with the John Lewis Partnership to enhance its credit card offering to existing and potential customers.

Commercial Banking

•

HSBC’s commitment to supporting new businesses in the UK helped in the formation of over 102,000 start-ups during the year through its ‘Start-up Stars’ programme. Additionally, the bank attracted more than 23,000 new competitor balance transfers in 2003.

•

The Chartered Institute of Management Accountants (‘CIMA’) voted HSBC ‘Best Small Business Bank’ following feedback from its Members in Practice Group. The CIMA recognition follows the Forum of Private Business’s announcement of HSBC as the ‘Best High Street Clearing Bank for Small Businesses’, while the UK 200 Group, a consortium of leading accountants, also named HSBC the best bank for business.

•

A new Business Money Manager deposit product was launched in January, attracting an average of 1,700 new accounts per week.

•

During 2003, in response to depolarisation in the UK investments market, the bank introduced a number of Commercial Independent Financial Advisors to provide quality independent financial advice to business customers. Based on the success of the initial pilot, the initiative is being expanded across the network. HSBC is now the number one provider of income protection products in the UK.

HSBC DriverQuote won the award for the ‘most innovative e-delivery channel’ at the Institute of Financial Services’ Financial Innovation Awards 2003. HSBC DriverQuote is the UK bank’s online quotation and ordering system and allows businesses to manage their company car policy over the internet.

•

HSBC Invoice Finance (UK) Limited was awarded the Best Factoring Award by Trade Finance Magazine in 2003.

•

Business Moneyfacts, a leading independent finance guide, named HSBC the UK’s ‘Best Computer Banking Provider’. Over 130,000

customers in the UK registered for business internet banking in 2003. Fifty-four per cent of all new business customers register for internet banking at the time of account opening. The value of payments generated using business internet banking now exceeds US$786 million per month. At the Institute of Financial Services’ Financial Innovation Awards HSBC won the award for the ‘Best Internet Banking Service’ and the ‘Grand Prix Award’ for general innovation in the financial services industry.

•

By the end of 2003, over 280,000 UK customers were registered for business telephone banking, utilising the bank’s telephone centres in the UK and India. These handle some 3,000 sales and more than 100,000 in-bound calls per month, leaving relationship managers to focus on customer service.

•

Group ‘Secure E-Payments’ remote payments solution successfully launched in June 2003. HSBC’s offering has enhanced security features over other providers and includes compliance with MasterCard ‘Securecode’ and verification by Visa standards for internet merchants.

Corporate, Investment Banking and Markets

•

In June, HSBC announced the appointment of co-heads of its global Corporate, Investment Banking and Markets business. Under this new management structure, HSBC combined its origination capabilities with its broad-based trading and sales platform to ensure a seamless banking, financing and investor service for the Group’s corporate and institutional clients.

•

During 2003, the business strengthened its client coverage model, adopting a sector-based relationship approach to client servicing. The origination businesses were restructured to reflect this sectoral approach and reinforced through selective recruitment. As a result of this investment, HSBC strengthened its corporate client service offering, winning a number of notable contracts.

•

In March 2003, the payments and cash management, trade services, securities services and banknotes businesses were brought together under a single management and organisation structure, Global Transaction Banking.

•

In September, HSBC commenced the integration

of its equities business into the Global Markets business, creating a single platform for all trading and sales operations. In addition, HSBC announced the restructuring of the research offering so as to align macro, sectoral and price driven research with both institutional investor and corporate client needs.

•

In the international bond market, HSBC’s market share rose to 4.4 per cent, and in the fourth quarter, HSBC came third in the international bond bookrunner league table.

•

HSBC was joint adviser to Safeway on its £3 billion recommended merger with Morrison in the UK and advised LNM Holdings on its US$1.2 billion acquisition of Polish steel maker Polski Huty Stali.

•

The London and Paris dealing rooms were fully integrated with each site taking a lead role in specific product areas. This dual-hub structure in Europe has proved to be a key competitive advantage.

•

HSBC won a five-year contract to support British Telecommunications plc’s (‘BT’) corporate card programme. The BT programme is the largest in both the UK and Europe with more than 35,000 corporate cards in issue and an annual spend of over £100 million (US$164 million).

•

The Universities Superannuation Scheme, the UK’s third largest pension fund, appointed HSBC Global Fund Services Limited as sole provider of a full range of investment accounting and performance measurement services.

•

In response to the anticipated growth in employee share saving schemes and personal retirement schemes, CCF created HSBC CCF Épargne Enterprise, following the acquisition of minority shareholdings in Elysees Gestion and Elysees Fonds

.

Private Banking

•

HSBC Private Bank was rated among the top three ‘Best Global Private Banks’ in Euromoney’s first annual survey of wealth management providers published in January 2004.

•

HSBC Private Bank’s alternative investments attracted in excess of US$3 billion new assets,

raising total client assets invested in hedge funds to US$14 billion. In Switzerland, four new hedge funds were launched. HSBC Private Bank was voted ‘Best European High Net Worth/Retail Hedge Fund of Funds Product Provider’ for 2003 at the ‘Hedge Funds Review’ and received Financial Adviser magazine’s gold award as a ‘Top Provider’ in the long/short funds of funds sector.

•

Strategic Investment Solutions (‘SIS’) was launched in July, providing clients with externally managed multi-manager investment portfolios.

•

The Family Office Advisory team launched Consolidation and Analysis of Investment Portfolios providing wealthy clients and their families with a single set of statements covering all their wealth. For clients with more complex portfolios, the service provides a means of developing coherent tax and investment management strategies.

•

The Group’s four French private banking subsidiaries combined into a single operating unit, HSBC Private Bank France, to create a major player in the French private banking market, with over US$15 billion in assets under management. The new unit comprises three divisions: resident private clients, international clients and institutional clients.

Other

•

HSBC Actuaries and Consultants Limited were appointed as actuarial consultant for a UK pension fund, The Pensions Trust. With assets approaching £2 billion (US$3.6 billion), The Pensions Trust is the leading multi-employer occupational pension fund for employees involved in the charitable, social, educational, voluntary and not-for-profit sectors.

Hong Kong

HSBC’s principal banking subsidiaries in Hong Kong are The Hongkong and Shanghai Banking Corporation and Hang Seng Bank, in which HSBC has a 62.14 per cent stake. The Hongkong and Shanghai Banking Corporation is the largest bank incorporated in Hong Kong and is HSBC’s flagship bank in the Asia-Pacific region. It is one of Hong Kong’s three note-issuing banks, accounting for more than 62 per cent by value of banknotes in

circulation in 2003.

General

•

Surveys indicated that HSBC has the strongest brand equity amongst all banks in Hong Kong. With its ‘The world's local bank’ positioning, HSBC combines a strong global brand with local reach and knowledge.

•

To support the recovery of the Hong Kong economy post-SARS (severe acute respiratory syndrome), HSBC launched the ‘HSBC Supports Hong Kong’ campaign, investing up to HK$100 million (US$12.8 million) to provide financial assistance to those affected by atypical pneumonia, and to stimulate local consumer spending. This leadership position received a very positive reaction from all sectors of the community.

•

Hang Seng Bank celebrated its 70th anniversary on 3 March 2003. The anniversary tagline, ‘70 Years of Excellence’, highlighted the bank’s commitment to providing high quality services that exceed customer expectations.

Personal Financial Services

•

HSBC’s position as one of the leading providers of wealth management services was sustained amid keen competition. Income from wealth management, including commissions on sales of unit trust products, funds under management, and securities transactions, grew by 38 per cent to US$408 million. A wide range of new retail unit trusts, certificates of deposit, bonds and structured deposits were launched to provide products to meet customers’ needs in the low-interest rate environment.

•

HSBC increased sales of new regular premium individual life insurance by 59 per cent, growing its market share from 13.9 per cent to 18.6 per cent.

•

On the back of this success, HSBC continued to add to its dedicated sales force, and the number of sales staff gaining professional qualifications in investment and insurance business also rose.

•

HSBC maintained its position as the number one credit card issuer in Hong Kong and, through strong and targeted customer marketing, increased card usage despite the subdued economy.

HSBC continued to focus on operational efficiency, with the Group Service Centres in mainland China expanding to provide about half the operational support for credit cards in Hong Kong.

•

HSBC continues to have the largest market share in online banking in Hong Kong, with more than 665,000 registered users at December 2003, up by 41 per cent on 2002. A 62 per cent increase in monthly website visits was achieved in 2003, following the introduction of tailored web pages for customer segments, alert services and market information.

•

HSBC was judged the best consumer internet bank in Hong Kong for the second year in a row by Global Finance and also won awards for the best consumer online securities trading service; the best consumer online credit service in Asia, and the best consumer web site design in Asia.

•

Hang Seng Bank continued to enhance its internet banking services, launching the e-Fund Supermarket in July to provide customers with comprehensive one-stop online investment fund services. By the year-end the number of Hang Seng customers registered for Personal e-Banking services in Hong Kong had risen by 34 per cent to 337,000, and internet transactions represented 20 per cent of total transactions.

•

HSBC increased the number of Premier centres in Hong Kong to 36, which support an enlarged Premier customer base of 224,000.

•

HSBC was named the Best Bank in Hong Kong in 2003 by Euromoney, The Asset, and The Banker, and Best Local Bank in Hong Kong by Finance Asia. HSBC was also named as the Best Managed Company in Hong Kong for the second consecutive year by Asiamoney, and won the Hong Kong Retail Management Association’s 2003 Award for Services: Customer Service Grand Award.

•

Hang Seng Bank was named the Best Domestic Commercial Bank in Hong Kong by The Asset and Asiamoney.

•

Hang Seng Bank strengthened its suite of insurance and investment products by widening its product range. The number of funds under the Hang Seng Investment series launched by Hang Seng Bank rose from 60 to 90 in 2003, and funds under management increased by 30 per

cent to HK$30 billion (US$3.9 billion) at the year end.

•

Hang Seng Investment Management Limited introduced the first exchange traded fund tracking the Hang Seng China Enterprises Index. This fund was listed on the Hong Kong stock exchange in December 2003.

•

Hang Seng Bank launched Leisure Class in June 2003, a new service which offers retirees and those who are planning to retire, comprehensive investment services and benefits and a range of leisure activities including Chinese painting and calligraphy classes and seminars on Chinese medicine.

•

Following the relaxation of restrictions on individual travel to Hong Kong by mainland China visitors, the People’s Bank of China and the Hong Kong Monetary Authority announced consent at the end of 2003 for Hong Kong banks to commence specified renminbi services, including exchange, deposit taking, remittances and renminbi credit cards. HSBC and Hang Seng Bank launched renminbi services in February 2004.

Commercial Banking

•

HSBC maintained its position as the leading trade services bank in 2003, growing market share and being named the Best Trade Finance Bank in Asia by Global Finance. With 80 per cent of HSBC’s substantial trade income coming from Commercial Banking customers, instant@dvice, an internet based service which supports electronic documentary credits advising, was launched.

•

Launched in August 2001, HSBC’s Business Internet Banking service continued to be well received in the market. HSBC was recognised by Global Finance as the Best Corporate/ Institutional Internet Bank in Hong Kong in 2003. Surveys indicated that HSBC had the largest online business banking market share in Hong Kong with over 31,000 companies registered as users. In addition, Hang Seng Bank had some 13,000 business e-banking customers by the year-end compared with 5,000 at the end of 2002.

•

Hang Seng Bank launched the Integrated Business Solutions Account in September 2003,

offering small and medium-sized enterprises one-stop financial services to facilitate their business growth.

•

Hang Seng Bank opened its first branch in the Macau SAR in December 2003 to serve the trade finance needs of its customers with business operations there.

Corporate, Investment Banking and Markets

•

HSBC increased its market share in G3 and local currency bond issuance in the Hong Kong market from 33 per cent in 2002 to 45 per cent in 2003, with 249 issues totalling US$11 billion. It was named Best Hong Kong Bond House by IFR.

•

HSBC was a joint bookrunner on Hutchison Whampoa’s US$5 billion global bond issue, the largest bond issue in Asia to date.

•

The debt finance group set up Cheung Kong’s HK$10 billion (US$1.3 billion) retail bond programme and led Hong Kong’s largest retail bond to date, for Kowloon-Canton Railway Corporation.

•

The securitisation team led the industry’s first securitisation of taxi and public light bus loans and the first synthetic securitisation of non-mortgage consumer and small and medium-sized enterprise (‘SME’) obligors in Hong Kong and the rest of Asia-Pacific.

•

The equity capital markets team executed equity placements amounting to US$576 million.

•

HSBC Asset Management celebrated its 30th anniversary on 4 September 2003, with the theme ‘Your Advantage in Investment In Asia and Around the World’, highlighting its commitment to providing investment solutions and delivering results.

•

By the end of 2003, HSBC Asset Management had launched 14 capital guaranteed funds, covering a wide range of sector and country themes, with US$3.5 billion in assets at the year-end, which represented more than 80 per cent of the guaranteed fund market in Hong Kong.

Private Banking

•

HSBC Private Bank was named the Best Private Bank in Hong Kong in 2003 by Euromoney.

•

HSBC Private Bank continued to expand its family office capabilities with the relaunch of its tax consulting service as Wealth and Tax Advisory Services (‘WTAS’) (Asia) Limited.

•

In October 2003, HSBC and Hang Seng Bank launched one-stop private banking services to cater to the needs of applicants to the Hong Kong Government’s Capital Investment Entrant Scheme.

Rest of Asia-Pacific (including the Middle East)

The Hongkong and Shanghai Banking Corporation offers personal, commercial, corporate and investment banking and markets services in mainland China. The bank’s network spans 11 major cities, comprising nine branches and two representative offices. Hang Seng Bank offers personal and commercial banking services and operates five branches, a sub-branch, and two representative offices in seven cities.

Outside Hong Kong and mainland China, the HSBC Group conducts business in the Asia-Pacific region primarily through branches and subsidiaries of The Hongkong and Shanghai Banking Corporation, with particularly strong coverage in India, Indonesia, Korea, Singapore, Taiwan and Thailand. HSBC’s presence in the Middle East is led by HSBC Bank Middle East Limited, the largest foreign-owned bank in the region; in Australia by HSBC Bank Australia Limited; and in Malaysia by HSBC Bank Malaysia Berhad, which has the second largest presence of any foreign-owned bank in the country.

General

•

In 2003 HSBC celebrated 150 years of doing business in India.

•

HSBC remains committed to the local communities in which it operates across the region. With the World Health Organization declaring the SARS virus contained worldwide in July, HSBC launched the ‘Shop Asia, Dine Asia’ programme to stimulate affected industries. Over 2,500 outlets across Asia-Pacific joined with HSBC to support the programme.

•

HSBC entered into an agreement to acquire a 14.71 per cent stake in UTI Bank Limited, an Indian retail bank, for a consideration of

Rs3.1 billion (US$66 million), with the option to acquire a further 5.37 per cent stake. UTI has some 200 branches and extension counters and over 1,000 ATMs nationwide, and offers a comprehensive range of corporate banking, retail lending and deposit products, and an internet banking service, to its one million customers.

•

In New Zealand, HSBC purchased the retail banking business of AMP Bank Limited, which comprised mortgage lending of US$1.1 billion and deposits of US$122 million. The purchase, which complements HSBC’s existing retail franchise in New Zealand, involved the acquisition of approximately 25,000 customer accounts and substantially increased HSBC’s mortgage and deposit business.

•

In October, HSBC Insurance Brokers Limited entered into a joint venture agreement to offer insurance broking and risk management services to domestic and international clients in mainland China, the first foreign joint venture in China to obtain such a licence. HSBC holds a 24.9 per cent stake in the new company, Beijing HSBC Insurance Brokers Limited.

•

In December, HSBC and China Ping An Trust & Investment Co. Limited (‘Ping An’) announced an agreement to acquire 50 per cent each of Fujian Asia Bank Limited for not more than US$20 million in cash. Completion of the transaction is expected to be at the end of March 2004, by which time Ping An is committed to injecting a further US$23 million into Fujian Asia bank, diluting HSBC’s share to 27 per cent.

•

Also in December, Hang Seng Bank signed an agreement to acquire 15.98 per cent of Industrial Bank Co. Limited’s (‘Industrial Bank’) enlarged capital for a consideration of 1.7 billion renminbi (US$208 million) in cash, subject to regulatory and shareholder approval. With this transaction, Hang Seng Bank will become the first foreign bank to acquire more than 15 per cent of a mainland Chinese bank. Industrial Bank has assets of 190 billion renminbi (US$23 billion).

•

In January 2004, HSBC and the Bank of Shanghai launched the Shanghai International Credit Card, which enables mainland Chinese customers to make purchases when travelling outside the mainland at any merchant accepting

Visa credit cards, and settle their payments in renminbi through a Bank of Shanghai account.

•

Six new branches were opened during the year, one in Bangladesh, one in New Zealand and four in India, further building HSBC’s position in the region.

•

In March, HSBC was among the first foreign banks in mainland China to receive full approval to offer custodian services to Qualified Foreign Institutional Investors (‘QFII’s) in China’s A-share market. HSBC also provides custodian services for China’s B-share market, in which it has a leading market position.

•

HSBC obtained approval for its QFII licence in August and as a result is able to invest in renminbi-denominated securities in China’s A-share market.

•