UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09721

Allianz Global Investors Managed Accounts Trust

(Exact name of registrant as specified in charter)

1633 Broadway, New York, New York 10019

(Address of principal executive offices) (Zip code)

Lawrence G. Altadonna — 1633 Broadway, New York, New York 10019

(Name and address of agent for service)

Registrant’s telephone number, including area code: 212-739-3371

Date of fiscal year end: October 31, 2012

Date of reporting period: April 30, 2012

ITEM1. REPORT TO SHAREHOLDERS

Semi-Annual Report

April 30, 2012

Allianz Global Investors Managed Accounts Trust

Fixed Income SHares: Series C, M, R

Contents

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 1 | |

Hans W. Kertess

Chairman

Brian S. Shlissel

President & CEO

Dear Shareholder:

The U.S. economy expanded throughout the six-month reporting period ended April 30, 2012, although the growth rate slowed during the latter half of the period, amid reduced government spending and ongoing geopolitical concerns.

Six Months in Review

For the six-month reporting period ended April 30, 2012:

| • | | Fixed Income SHares: Series C returned 6.94% prior to the deduction of fees. |

| • | | Fixed Income SHares: Series M returned 6.18% prior to the deduction of fees. |

| • | | Fixed Income SHares: Series R returned 6.92% prior to the deduction of fees. |

During the first half of the reporting period, gross domestic product (“GDP”), the value of goods and services produced in the country, the broadest measure of economic activity and the principal indicator of economic performance, expanded at an annual rate of 3.0%. This growth, the strongest since 2010, eased to a 1.9% annual pace during the first quarter of 2012.

A decline in government spending at the federal, state and local level acted as an economic headwind during the six-month reporting period. Business spending also eased, growing at a 1.7% annual rate between January and March 2012, down from double-digits during mid-2011. These declines were offset by increased consumer spending, which accounts for approximately two-thirds of U.S. economic activity. Manufacturing, representing approximately 10% of the U.S. economy, reported gains and the housing sector showed signs of improvement. The U.S. unemployment rate fell to 8.1%, the lowest level in three years.

Despite record low yields, many investors continued to park assets in U.S. Treasury bonds. The benchmark ten-year bond began the six-month reporting period yielding 2.01% and stood at 1.95% at April 30, 2012. Investors also sought greater returns in higher-yielding corporate bonds during the six-month period.

Federal Reserve (the “Fed”) Chairman Ben Bernanke gave no indication that interest rates would rise anytime soon. He revealed that the Fed’s closely-watched Federal Funds rate (the interest rate at which depository institutions trade funds held by the

| | | | |

| 2 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fed with each other, usually on an overnight basis) would remain in the 0.0% to 0.25% range through late 2014. He also indicated that the Fed might unveil future measures to stimulate the U.S. economy.

Outlook

In addition to its revelation that it plans to keep interest rates low through 2014, the Fed warned of “significant downside risks to the economic outlook, including strains in global financial markets.” This caution has found validation in one significant instance, the fiscal crisis in the European Union (“E.U.”), as the sovereign debt crisis in the E.U., now in its fourth year, appeared to

deepen, particularly subsequent to the end of the six-month reporting period. The E.U. is in or close to recession and unemployment is 10.8%. The current state of the E.U. will adversely impact the U.S., which in recent years has sent approximately 20% of its exports to the continent.

“Significant downside risk” to the economy also resides in the U.S. A series of tax cuts are scheduled to expire on December 31, 2012 and major spending reductions are planned to commence in January 2013. Either or both would almost certainly have a negative impact on the economy in 2013. The current partisan divide in Washington is such that any attempt to mitigate either is unlikely to happen smoothly.

Together with Allianz Global Investors Fund Management LLC, the Portfolios’ investment manager and Pacific Investment Management Company LLC, the Portfolios’ sub-adviser, we thank you for investing with us.

We remain dedicated to serving your investment needs.

Sincerely,

| | |

| |  |

Hans W. Kertess Chairman | | Brian S. Shlissel President & Chief Executive Officer |

Receive this report electronically and eliminate paper mailings. To enroll, go to www.allianzinvestors.com/ edelivery.

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 3 | |

Allianz Global Investors Managed Accounts Trust

Fixed Income SHares: Series C, M, R

Important Information

April 30, 2012 (unaudited)

In an economic environment where interest rates may trend upward, rising rates will negatively impact the performance of most bond funds and fixed income securities held by a fund and are likely to cause these instruments to decrease in value. Bond funds and individual bonds with a longer duration (a measure of the expected life of a security) tend to be more sensitive to changes in interest rates, usually making them more volatile than securities with shorter durations.

Fixed Income SHares: Series C, M and R (the “Portfolios”) may be subject to various risks as described in the Portfolios’ prospectus. Some of these risks may include, but are not limited to, the following: derivatives risk, foreign (non-U.S.) investment risk, high-yield security risk, counterparty risk and issuer non-diversification risk. The Portfolios may use derivative instruments for hedging purposes or as part of an investment strategy. Use of these instruments may involve certain costs and risks, such as liquidity risk, interest rate risk, market risk, credit risk, management risk and the risk that a Portfolio could not close out a position when it would be most advantageous to do so. Portfolios investing in derivatives could lose more than the principal amount invested in these instruments. Investing in non-U.S. securities may entail risk due to non-U.S. economic, political and other developments. This risk may be enhanced when a Portfolio invests in emerging markets. High-yield bonds typically have a lower credit rating than other bonds. Lower rated bonds generally involve a greater risk to principal than higher rated bonds. Concentrating investments in individual sectors may add additional risk and volatility compared to a diversified Portfolio. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall Portfolio.

Allianz Global Investors Fund Management LLC (the “Investment Manager”) serves as the Portfolios’ Investment Manager and Pacific Investment Management Company LLC (“PIMCO” or the “Sub-Adviser”) serves as the sub-adviser. The Portfolios’ Investment Manager and Sub-Adviser have adopted written proxy voting policies and procedures (the “Proxy Policy”) as required by Rule 206(4)-6 under the Investment Advisers Act of 1940, as amended. The Proxy Policy has been adopted by the Portfolios as the policies and procedures that the Sub-Adviser will use when voting proxies on behalf of the Portfolios. Copies of the written Proxy Policy and the factors that the Sub-Adviser may consider in determining how to vote proxies for each Portfolio, and information about how each Portfolio voted proxies relating to portfolio securities held during the most recent twelve-month period ended June 30, are available without charge, upon request, by calling the Portfolios’ shareholder servicing agent at (800) 628-1237, on the Allianz Global Investors Distributors’ website at www.allianzinvestors.com and on the Securities and Exchange Commission’s (the “SEC”) website at http://www.sec.gov.

Past performance is no guarantee of future results. Total return is calculated by subtracting the value of an investment in each Portfolio at the beginning of each specified period from its value at the end of the period and dividing the remainder by the value of the investment at the beginning of the period and expressing the result as a percentage. The calculation assumes that all income dividends and capital gain distributions, if any, have been reinvested. Total return does not reflect broker commissions or “wrap fee” charges. Total return for a period of more than one year represents the average annual total return during the period. Total return for a period of less than one year is not annualized.

An investment in the Portfolios involves risk, including the loss of principal. Total return, distribution yield, net asset value and duration will fluctuate with changes in market conditions. The following data is provided for informational purposes only and is not intended for trading purposes. Net asset value is equal to total assets less total liabilities divided by the number of shares outstanding.

This report, including the financial information herein, is transmitted to the shareholders of Allianz Global Investors Managed Accounts Trust for their information. It is not a prospectus, circular or representation intended for use in the purchase of shares of the Portfolios or any other securities mentioned in this report.

| | | | |

| 4 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Allianz Global Investors Managed Accounts Trust

Fixed Income SHares: Series C Portfolio Insights

April 30, 2012 (unaudited)

| | | | |

| Symbol: | | Primary Investments: | | Inception Date: |

| FXICX | | Intermediate maturity fixed income securities. | | 3/17/00 |

| | |

| | | | Net Assets: |

| | | | $3.9 billion |

| | |

| | | | Portfolio Managers: |

| | | | Curtis Mewbourne |

After a spike in volatility and general unease in late 2011, the markets reflected optimism over short-term measures taken by European policymakers to prevent an expansion of the European sovereign debt crisis as the European Central Bank’s (“ECB’s”) Longer-Term Refinancing Operations (LTROs) and a Greek Private Sector Investment (“PSI”) deal appear to have calmed Eurozone fears. Throughout the six-month period, U.S. economic data continued to improve while European growth remained sluggish. Unemployment rates declined in the U.S. and Latin America, while the unemployment rates in the U.K. and Eurozone continued to reach new cycle highs.

During the reporting period, bond markets posted positive returns. Volatility declined in the second half of the period as investors nerves seemed to settle down and the growing desire to “reach for yield” helped riskier fixed income markets. Improving sentiment also sent investors back into emerging markets; local assets, in particular, benefitted from strong currency appreciation in early 2012.

Performance, Statistics & Drivers

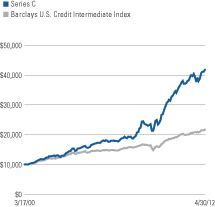

For the six-month reporting period ended April 30, 2012, Series C returned 6.94% prior to the deduction of fees, outperforming the unmanaged Barclays U.S. Credit Intermediate Index (the “benchmark index”), which returned 3.40%.

An overweighting to U.S. duration contributed to Series C’s performance as the 10-year U.S. Treasury yield fell 20 basis points during the six-month reporting period. Tactical curve strategies, implemented through the use of Eurodollar futures, contributed to returns as these contracts rose in price during the period. Non-U.S. interest rate exposure, particularly to Australia and the U.K., also enhanced performance, as yields declined in these countries during the reporting period.

On a duration-adjusted basis, sectors within the Barclays U.S. Aggregate Index that trade to U.S. Treasuries outperformed. An emphasis on bonds of financial companies within the corporate debt market added to returns as financials outperformed the broader investment grade corporate market on investor demand for higher yielding assets. Exposure to high yield securities contributed to performance as this asset class also outperformed Treasuries of similar duration. Holdings of agency mortgage-backed securities (“MBS”) detracted from relative performance as this asset class underperformed the Barclays U.S. Aggregate Index. An allocation to emerging market external debt added to returns as external emerging market debt outperformed like-duration Treasuries as measured by the Barclays Emerging Market (U.S. Dollar) Index. Exposure to select emerging market local rates, particularly Brazil, was positive for returns as yields declined. Currency strategies designed to benefit from a decline in the euro were positive for performance as the euro fell versus the U.S. dollar.

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 5 | |

Allianz Global Investors Managed Accounts Trust

Fixed Income SHares: Series M Portfolio Insights

April 30, 2012 (unaudited)

| | | | |

| Symbol: | | Primary Investments: | | Inception Date: |

| FXIMX | | Intermediate maturity mortgage-backed securities. | | 3/17/00 |

| | |

| | | | Net Assets: |

| | | | $3.9 billion |

| | |

| | | | Portfolio Managers: |

| | | | Curtis Mewbourne |

Performance, Statistics & Drivers

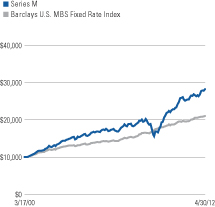

For the six-month reporting period ended April 30, 2012, Series M returned 6.18% prior to the deduction of fees, outperforming the unmanaged Barclays U.S. MBS Fixed Rate Index (the “benchmark index”), which returned 2.13%.

While policy-related developments, including implementation of the Home Affordable Refinance Program (“HARP”) 2.0, continued to influence the agency mortgage-backed securities (“MBS”) market, this sector benefitted from strong demand from banks and mortgage REITs. The MBS sector, as measured by the benchmark index, returned 2.13% during the six months ended April 30, 2012. While HARP 2.0 has resulted in a moderate increase in prepayment speeds among certain higher coupons, stringent lending standards, gridlock in Washington, and a lack of capacity in the mortgage finance system remain significant barriers to a widespread increase in refinancing activity.

An overweighting to U.S. duration contributed to Series M’s performance as the 10-year U.S. Treasury yield fell 20 basis points during the six-month period. Tactical curve strategies, implemented through the use of Eurodollar futures, contributed to returns as these contracts rose in price during the period. Non-U.S. interest rate exposure, especially to Australia, Canada, and the U.K., enhanced performance, as yields generally declined in these countries during the reporting period.

An allocation to commercial mortgage-backed securities (“CMBS”) added to returns amid strong demand for higher yielding assets. An underweight position to Ginnie Mae (“GNMA”) MBS slightly added to returns, as GNMA modestly underperformed conventional Fannie Mae and Freddie Mac. An overall underweighting to Agency MBS, in favor of other sectors, was generally positive for performance during the period. Within the corporate sector, an emphasis on bonds of financial companies contributed to returns as financials outperformed the broader investment grade corporate market and like-duration Treasuries. Exposure to select emerging market local rates, particularly Brazil, was positive for returns as yields declined.

| | | | |

| 6 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Allianz Global Investors Managed Accounts Trust

Fixed Income SHares: Series R Portfolio Insights

April 30, 2012 (unaudited)

| | | | |

| Symbol: | | Primary Investments: | | Inception Date: |

| FXIRX | | Inflation-indexed fixed income securities. | | 4/15/04 |

| | |

| | | | Net Assets: |

| | | | $546.7 million |

| | |

| | | | Portfolio Manager: |

| | | | Mihir Worah |

Performance, Statistics & Drivers

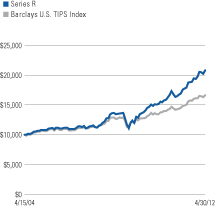

For the six-month reporting period ended April 30, 2012, Series R returned 6.92% prior to the deduction of fees, outperforming the unmanaged Barclays U.S. TIPS Index (the “benchmark index”), which returned 3.74%.

Real U.S. yields fell for all maturities. Treasury Inflation Protected Securities (“TIPS”) gained amid positive U.S. economic data, which reflected an improved short-term economic outlook in addition to optimism over measures taken by European policymakers to prevent an expansion of the European sovereign debt crisis. Breakeven inflation levels, a measure of market inflation expectations which is calculated as the difference between nominal yields and real yields, widened across the maturity curve as improved U.S. economic prospects leaning more towards reflation favored TIPS over nominal Treasuries.

An underweighting to real duration, in favor of nominal duration, was negative for returns as breakeven inflation levels widened across the curve. Tactical curve strategies, implemented through the use of Eurodollar futures, contributed to returns as these contracts rose in price during the period. Modest exposure to Australian real duration contributed to performance, as real yields declined in this market during the period.

Within the corporate sector, an emphasis on bonds of financial companies contributed to returns as financials outperformed the broader investment grade corporate market and like-duration Treasuries on investor demand for higher yielding assets. Exposure to commercial mortgage-backed securities (“CMBS”) enhanced returns as CMBS outperformed Treasuries with similar durations during the period. An allocation to emerging-market external debt added to returns as external emerging market debt outperformed like-duration Treasuries as measured by the Barclays Emerging Market (U.S. Dollar) Index. Exposure to select emerging market local rates, particularly Brazil, was positive for returns as yields declined. Currency strategies designed to benefit from a decline in the euro were positive for performance as the euro fell versus the U.S. dollar.

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 7 | |

Allianz Global Investors Managed Accounts Trust

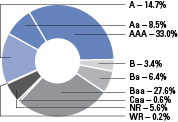

Fixed Income SHares: Series C Performance & Statistics

April 30, 2012 (unaudited)

| | | | |

| Total Returns (Six Months ended 4/30/12) | | | |

Series C | | | 6.94% | |

Barclays U.S. Credit Intermediate Index | | | 3.40% | |

Change in Value of $10,000 Investments in Series C and the Barclays U.S. Credit Intermediate Index

Moody’s Ratings

(as a % of total investments,

before options written)

Past performance is no guarantee of future results. Returns presented do not reflect the deduction of taxes that a shareholder would pay on fund distribution or the redemption of fund shares.

| | | | |

| Shareholder Expense Example | | Actual | | Hypothetical |

| | | | | (5 % return before expenses) |

Beginning Account Value (11/1/11) | | $1,000.00 | | $1,000.00 |

Ending Account Value (4/30/12) | | $1,069.40 | | $1,024.86 |

Expenses Paid During Period | | $0.01 | | $0.01 |

Expenses are equal to the annualized expense ratio of 0.0012%, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

| | | | |

| 8 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Allianz Global Investors Managed Accounts Trust

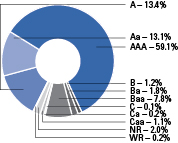

Fixed Income SHares: Series M Performance & Statistics

April 30, 2012 (unaudited)

| | | | |

| Total Returns (Six Months ended 4/30/12) | | | |

Series M | | | 6.18% | |

Barclays U.S. MBS Fixed Rate Index | | | 2.13% | |

Change in Value of $10,000 Investments in Series M and the Barclays U.S. MBS Fixed Rate Index

Moody’s Ratings

(as a % of total investments,

before options written)

Past performance is no guarantee of future results. Returns presented do not reflect the deduction of taxes that a shareholder would pay on fund distribution or the redemption of fund shares.

| | | | |

| Shareholder Expense Example | | Actual | | Hypothetical |

| | | | | (5 % return before expenses) |

Beginning Account Value (11/1/11) | | $1,000.00 | | $1,000.00 |

Ending Account Value (4/30/12) | | $1,061.80 | | $1,024.86 |

Expenses Paid During Period | | $0.00 | | $0.00 |

Expenses are equal to the annualized expense ratio of 0.0007%, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 9 | |

Allianz Global Investors Managed Accounts Trust

Fixed Income SHares: Series R Performance & Statistics

April 30, 2012 (unaudited)

| | | | |

| Total Returns (Six Months ended 4/30/12) | | | |

Series R | | | 6.92% | |

Barclays U.S. TIPS Index | | | 3.74% | |

Change in Value of $10,000 Investments in Series R and the Barclays U.S. TIPS Index

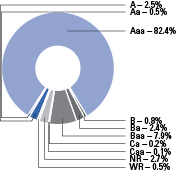

Moody’s Ratings

(as a % of total investments,

before options written )

Past performance is no guarantee of future results. Returns presented do not reflect the deduction of taxes that a shareholder would pay on fund distribution or the redemption of fund shares.

| | | | |

| Shareholder Expense Example | | Actual | | Hypothetical |

| | | | | (5 % return before expenses) |

Beginning Account Value (11/1/11) | | $1,000.00 | | $1,000.00 |

Ending Account Value (4/30/12) | | $1,069.20 | | $1,024.84 |

Expenses Paid During Period | | $0.03 | | $0.03 |

Expenses are equal to the annualized expense ratio of 0.005%, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

| | | | |

| 10 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Allianz Global Investors Managed Accounts Trust

Benchmark Descriptions

April 30, 2012 (unaudited)

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

Index/Description

| • | | Barclays U.S. MBS Fixed Rate Index |

The Barclays U.S. MBS Fixed Rate Index is an unmanaged index comprised of fixed rate mortgage pass through securities issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC), with a Weighted Average Maturity (WAM) of at least one year and at least $250 million par outstanding.

| • | | Barclays U.S. Credit Intermediate Index |

The Barclays U.S. Credit Intermediate Index is an unmanaged index of publicly issued U.S. corporate and specified foreign debentures and secured notes with intermediate maturities ranging from 1 to 10 years. Securities must also meet specific liquidity and quality requirements.

| • | | Barclays U.S. TIPS Index |

The Barclays U.S. TIPS Index is an unmanaged market index comprised of all U.S. Treasury Inflation Protected Securities rated investment grade (Baa3 or better), having at least one year to final maturity, and at least $250 million par amount outstanding. Performance data for this index prior to October 1997 represents returns of the Barclays Inflation Notes Index.

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 11 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| CORPORATE BONDS & NOTES–47.9% | | | | |

| | | | | | | | | | |

| | | | Airlines–1.1% | | | | | | |

| $ | 90 | | | American Airlines Pass Through Trust, 10.375%, 1/2/21 | | | | $ | 96,777 | |

| | 1,373 | | | Northwest Airlines, Inc., | | | | | | |

| | | | 7.041%, 10/1/23 | | | | | 1,509,946 | |

| | 41,706 | | | 7.15%, 4/1/21 (MBIA) | | | | | 42,123,607 | |

| | 54 | | | United Air Lines Pass Through Trust, 10.125%, 3/22/15 (b)(f) | | | | | 19,190 | |

| | | | | | | | | | |

| | | | | | | | | 43,749,520 | |

| | | | | | | | | | |

| | | |

| | | | Automotive–0.2% | | | | | | |

| | 9,100 | | | Volkswagen International Finance NV, 4.00%, 8/12/20 (a)(d) | | | | | 9,660,615 | |

| | | | | | | | | | |

| | | |

| | | | Banking–6.4% | | | | | | |

| | 16,200 | | | Abbey National Treasury Services PLC, 2.046%, 4/25/14, FRN | | | | | 15,575,555 | |

| | 5,200 | | | Banco do Brasil S.A., 4.50%, 1/22/15 (a)(d) | | | | | 5,460,000 | |

| | | | Banco Santander Brasil S.A., | | | | | | |

| | 1,000 | | | 4.50%, 4/6/15 | | | | | 1,005,000 | |

| | 3,500 | | | 4.50%, 4/6/15 (a)(d) | | | | | 3,517,500 | |

| | 30,200 | | | Banco Santander Brazil S.A., 2.574%, 3/18/14, FRN (a)(d) | | | | | 30,023,451 | |

| | | | Barclays Bank PLC, | | | | | | |

| | 24,000 | | | 6.05%, 12/4/17 (a)(d) | | | | | 24,183,576 | |

| £ | 3,300 | | | 14.00%, 6/15/19 (h) | | | | | 6,426,683 | |

| $ | 23,900 | | | BPCE S.A., 2.277%, 2/7/14, FRN (a)(d) | | | | | 23,772,350 | |

| AUD | 2,600 | | | Commonwealth Bank of Australia, 4.50%, 2/20/14 | | | | | 2,737,372 | |

| $ | 20,000 | | | Cooperatieve Centrale Raiffeisen-Boerenleenbank BA,

11.00%, 6/30/19 (a)(d)(h) | | | | | 25,530,120 | |

| | 5,000 | | | HBOS Capital Funding L.P., 6.071%, 6/30/14 (a)(d)(h) | | | | | 3,375,000 | |

| | 30,600 | | | HBOS PLC, 6.75%, 5/21/18 (a)(d) | | | | | 28,144,625 | |

| | | | HSBC Capital Funding L.P. (a)(d)(h), | | | | | | |

| | 13,900 | | | 4.61%, 6/27/13 | | | | | 13,063,345 | |

| | 1,350 | | | 10.176%, 6/30/30 | | | | | 1,768,500 | |

| | | | ICICI Bank Ltd., | | | | | | |

| | 5,900 | | | 4.75%, 11/25/16 (a)(d) | | | | | 5,866,034 | |

| | 2,500 | | | 5.00%, 1/15/16 | | | | | 2,567,667 | |

| | 700 | | | 5.50%, 3/25/15 | | | | | 725,920 | |

| | 900 | | | Korea Exchange Bank, 4.875%, 1/14/16 | | | | | 958,601 | |

| | 29,300 | | | Lloyds TSB Bank PLC, 12.00%, 12/16/24 (a)(d)(h) | | | | | 30,987,475 | |

| | 2,400 | | | RBS Capital Trust I, 4.709%, 7/1/13 (h) | | | | | 1,536,000 | |

| | | | State Bank of India, | | | | | | |

| | 1,300 | | | 4.50%, 10/23/14 | | | | | 1,342,938 | |

| | 1,000 | | | 4.50%, 7/27/15 (a)(d) | | | | | 1,032,528 | |

| | | | |

| 12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Banking (continued) | | | | | | |

| | | | | | | | | | |

| | AUD 20,000 | | | Westpac Banking Corp., 4.75%, 3/5/14 | | | | $ | 21,156,898 | |

| | | | | | | | | | |

| | | | | | | | | 250,757,138 | |

| | | | | | | | | | |

| | | |

| | | | Biotechnology–0.1% | | | | | | |

| $ | 1,700 | | | Amgen, Inc., 5.70%, 2/1/19 | | | | | 2,010,396 | |

| | | | | | | | | | |

| | | |

| | | | Computers–0.1% | | | | | | |

| | 5,000 | | | Lexmark International, Inc., 5.90%, 6/1/13 | | | | | 5,204,775 | |

| | | | | | | | | | |

| | | |

| | | | Diversified Manufacturing–0.5% | | | | | | |

| | 15,000 | | | Tyco Electronics Group S.A., 6.55%, 10/1/17 | | | | | 17,938,035 | |

| | | | | | | | | | |

| | | |

| | | | Drugs & Medical Products–0.3% | | | | | | |

| | 1,800 | | | Abbott Laboratories, 5.125%, 4/1/19 | | | | | 2,148,800 | |

| | 100 | | | Biomet, Inc., 10.00%, 10/15/17 | | | | | 108,375 | |

| | 3,400 | | | GlaxoSmithKline Capital, Inc., 5.65%, 5/15/18 | | | | | 4,129,800 | |

| | 1,700 | | | Hospira, Inc., 6.05%, 3/30/17 | | | | | 1,915,030 | |

| | 1,300 | | | Pfizer, Inc., 6.20%, 3/15/19 | | | | | 1,639,325 | |

| | | | | | | | | | |

| | | | | | | | | 9,941,330 | |

| | | | | | | | | | |

| | | |

| | | | Electronics–0.0% | | | | | | |

| | 150 | | | Sanmina-SCI Corp., 8.125%, 3/1/16 | | | | | 155,437 | |

| | | | | | | | | | |

| | | |

| | | | Financial Services–18.5% | | | | | | |

| | | | Ally Financial, Inc., | | | | | | |

| | 13,894 | | | 2.688%, 12/1/14, FRN | | | | | 13,021,457 | |

| | 21,075 | | | 3.874%, 6/20/14, FRN | | | | | 20,872,258 | |

| | 1,000 | | | 6.75%, 12/1/14 | | | | | 1,052,920 | |

| | 10,500 | | | 7.50%, 12/31/13 | | | | | 11,235,000 | |

| | 17,300 | | | 8.00%, 3/15/20 | | | | | 19,860,832 | |

| | 19,100 | | | 8.30%, 2/12/15 | | | | | 21,010,000 | |

| | 11,000 | | | American Express Co., 7.25%, 5/20/14 | | | | | 12,280,576 | |

| | | | Bank of America Corp., | | | | | | |

| | 3,800 | | | 5.65%, 5/1/18 | | | | | 4,023,071 | |

| | 4,300 | | | 5.75%, 12/1/17 | | | | | 4,564,330 | |

| | 2,715 | | | 6.00%, 9/1/17 | | | | | 2,907,018 | |

| | | | Bear Stearns Cos. LLC, | | | | | | |

| | 1,500 | | | 5.30%, 10/30/15 | | | | | 1,647,345 | |

| | 17,265 | | | 7.25%, 2/1/18 | | | | | 21,022,883 | |

| | 39,800 | | | BNP Paribas S.A., 5.00%, 1/15/21 | | | | | 40,194,259 | |

| | 5,700 | | | Caterpillar Financial Services Corp., 7.15%, 2/15/19 | | | | | 7,415,181 | |

| | | | Citigroup, Inc., | | | | | | |

| | 12,350 | | | 4.75%, 5/19/15 | | | | | 12,984,123 | |

| | 700 | | | 5.50%, 10/15/14 | | | | | 746,377 | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 13 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Financial Services (continued) | | | | | | |

| | | | | | | | | | |

| $ | 11,718 | | | 6.00%, 8/15/17 | | | | $ | 12,999,305 | |

| | 13,500 | | | 6.125%, 11/21/17 | | | | | 14,992,101 | |

| | 8,260 | | | Citigroup Capital XXI, 8.30%, 12/21/77, (converts to FRN on 12/21/37) | | | | | 8,409,712 | |

| | | | Ford Motor Credit Co. LLC, | | | | | | |

| | 49,300 | | | 5.625%, 9/15/15 | | | | | 53,557,104 | |

| | 16,900 | | | 7.00%, 10/1/13 | | | | | 18,124,270 | |

| | 20,750 | | | 8.00%, 6/1/14 | | | | | 23,093,775 | |

| | 7,900 | | | 8.00%, 12/15/16 | | | | | 9,454,286 | |

| | 2,700 | | | 8.125%, 1/15/20 | | | | | 3,427,669 | |

| | 3,400 | | | 8.70%, 10/1/14 | | | | | 3,901,157 | |

| | | | General Electric Capital Corp., | | | | | | |

| € | 10,000 | | | 4.625%, 9/15/66, (converts to FRN on 9/15/16) (a)(d) | | | | | 11,198,386 | |

| € | 19,100 | | | 5.50%, 9/15/67, (converts to FRN on 9/15/17) | | | | | 21,869,515 | |

| $ | 5,000 | | | 6.15%, 8/7/37 | | | | | 5,809,695 | |

| £ | 1,400 | | | 6.50%, 9/15/67, (converts to FRN on 9/15/17) | | | | | 2,147,096 | |

| | | | Goldman Sachs Group, Inc., | | | | | | |

| € | 10,000 | | | 1.376%, 5/23/16, FRN | | | | | 11,842,048 | |

| $ | 15,200 | | | 6.15%, 4/1/18 | | | | | 16,561,540 | |

| | 2,000 | | | HSBC Finance Corp., 0.918%, 6/1/16, FRN | | | | | 1,841,202 | |

| | | | HSBC Holdings PLC, | | | | | | |

| | 700 | | | 6.50%, 5/2/36 | | | | | 773,524 | |

| | 400 | | | 7.625%, 5/17/32 | | | | | 454,782 | |

| | | | International Lease Finance Corp. (a)(d), | | | | | | |

| | 4,000 | | | 6.75%, 9/1/16 | | | | | 4,340,000 | |

| | 3,000 | | | 7.125%, 9/1/18 | | | | | 3,315,000 | |

| | 14,800 | | | JPMorgan Chase & Co., 6.00%, 1/15/18 | | | | | 17,117,147 | |

| | | | LBG Capital No.1 PLC, | | | | | | |

| € | 2,825 | | | 7.375%, 3/12/20 | | | | | 3,037,558 | |

| £ | 9,402 | | | 7.588%, 5/12/20 | | | | | 12,732,001 | |

| £ | 1,000 | | | 7.869%, 8/25/20 | | | | | 1,371,350 | |

| $ | 3,400 | | | 7.875%, 11/1/20 (a)(d) | | | | | 3,001,061 | |

| | 22,200 | | | 8.50%, 12/17/21 (a)(d)(h) | | | | | 20,646,000 | |

| | | | LBG Capital No.2 PLC, | | | | | | |

| £ | 2,331 | | | 9.00%, 12/15/19 | | | | | 3,423,596 | |

| £ | 4,500 | | | 9.334%, 2/7/20 | | | | | 6,773,622 | |

| € | 2,180 | | | 15.00%, 12/21/19 | | | | | 3,477,228 | |

| | | | Merrill Lynch & Co., Inc., | | | | | | |

| $ | 500 | | | 5.00%, 1/15/15 | | | | | 522,380 | |

| | 22,700 | | | 6.40%, 8/28/17 | | | | | 24,561,241 | |

| | 40,100 | | | 6.875%, 4/25/18 | | | | | 44,729,344 | |

| | | | |

| 14 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Financial Services (continued) | | | | | | |

| | | | | | | | | | |

| | | | Morgan Stanley, | | | | | | |

| € | 10,000 | | | 1.177%, 1/16/17, FRN | | | | $ | 11,239,209 | |

| $ | 2,800 | | | 5.375%, 10/15/15 | | | | | 2,890,684 | |

| € | 5,000 | | | 5.375%, 8/10/20 | | | | | 6,551,615 | |

| $ | 900 | | | 5.95%, 12/28/17 | | | | | 926,366 | |

| | 3,700 | | | 6.625%, 4/1/18 | | | | | 3,871,173 | |

| £ | 550 | | | MUFG Capital Finance 5 Ltd., 6.299%, 1/25/17 (h) | | | | | 894,648 | |

| $ | 1,000 | | | Novatek Finance Ltd., 5.326%, 2/3/16 (a)(d) | | | | | 1,046,920 | |

| | 540 | | | Preferred Term Securities XIII Ltd., 1.024%, 3/24/34, FRN (a)(b)(d)(l) (acquisition cost–$539,995; purchased 3/9/04) | | | | | 318,597 | |

| | 1,500 | | | Qatari Diar Finance QSC, 5.00%, 7/21/20 | | | | | 1,642,500 | |

| | 500 | | | QNB Finance Ltd., 3.125%, 11/16/15 | | | | | 505,750 | |

| | | | Royal Bank of Scotland Group PLC, | | | | | | |

| € | 1,000 | | | 4.625%, 9/22/21, (converts to FRN on 9/22/16) | | | | | 999,394 | |

| $ | 273 | | | 5.00%, 11/12/13 | | | | | 274,747 | |

| | 22,200 | | | 6.99%, 10/5/17 (a)(d)(h) | | | | | 17,649,000 | |

| | 5,000 | | | 7.648%, 9/30/31 (h) | | | | | 4,131,250 | |

| | | | RSHB Capital S.A. for OJSC Russian Agricultural Bank, | | | | | | |

| | 500 | | | 7.125%, 1/14/14 | | | | | 536,250 | |

| | 1,500 | | | 9.00%, 6/11/14 (a)(d) | | | | | 1,678,125 | |

| | | | SLM Corp., | | | | | | |

| € | 2,950 | | | 1.206%, 6/17/13, FRN | | | | | 3,806,602 | |

| $ | 750 | | | 5.00%, 10/1/13 | | | | | 770,625 | |

| | 400 | | | 5.375%, 5/15/14 | | | | | 418,023 | |

| | 36,000 | | | 6.25%, 1/25/16 | | | | | 37,260,000 | |

| | 9,555 | | | 8.45%, 6/15/18 | | | | | 10,510,500 | |

| | | | Teco Finance, Inc., | | | | | | |

| | 983 | | | 6.572%, 11/1/17 | | | | | 1,160,137 | |

| | 2,000 | | | 6.75%, 5/1/15 | | | | | 2,220,946 | |

| | 6,800 | | | TransCapitalInvest Ltd. for OJSC AK Transneft, 5.67%, 3/5/14 | | | | | 7,235,200 | |

| | | | UBS AG, | | | | | | |

| | 500 | | | 4.875%, 8/4/20 | | | | | 524,085 | |

| | 1,000 | | | 5.875%, 12/20/17 | | | | | 1,109,535 | |

| | 6,700 | | | USB Capital IX, 3.50%, 5/29/12, VRN (h) | | | | | 5,115,584 | |

| | 2,050 | | | Wachovia Corp., 5.75%, 2/1/18 | | | | | 2,393,492 | |

| | 19,217 | | | Wells Fargo & Co., 7.98%, 3/15/18 (h) | | | | | 20,946,530 | |

| | 4,200 | | | White Nights Finance BV for Gazprom, 10.50%, 3/25/14 | | | | | 4,799,382 | |

| | 7,400 | | | Xstrata Finance Canada Ltd., 5.80%, 11/15/16 (a)(d) | | | | | 8,392,518 | |

| | | | | | | | | | |

| | | | | | | | | 726,161,712 | |

| | | | | | | | | | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 15 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Food & Beverage–0.2% | | | | | | |

| | | | | | | | | | |

| $ | 6,700 | | | Kraft Foods, Inc., 6.50%, 8/11/17 | | | | $ | 8,137,257 | |

| | 1,100 | | | Tate & Lyle International Finance PLC, 6.625%, 6/15/16 (a)(d) | | | | | 1,271,660 | |

| | | | | | | | | | |

| | | | | | | | | 9,408,917 | |

| | | | | | | | | | |

| | | |

| | | | Healthcare & Hospitals–0.2% | | | | | | |

| | | | HCA, Inc., | | | | | | |

| | 3,200 | | | 7.25%, 9/15/20 | | | | | 3,560,000 | |

| | 4,000 | | | 7.875%, 2/15/20 | | | | | 4,460,000 | |

| | | | | | | | | | |

| | | | | | | | | 8,020,000 | |

| | | | | | | | | | |

| | | |

| | | | Holding Companies–0.2% | | | | | | |

| | | | Hutchison Whampoa International Ltd., | | | | | | |

| | 100 | | | 5.75%, 9/11/19 | | | | | 113,227 | |

| | 1,000 | | | 7.625%, 4/9/19 | | | | | 1,239,412 | |

| | 6,300 | | | Sinochem Overseas Capital Co., Ltd., 4.50%, 11/12/20 (a)(d) | | | | | 6,233,755 | |

| | | | | | | | | | |

| | | | | | | | | 7,586,394 | |

| | | | | | | | | | |

| | | |

| | | | Insurance–4.1% | | | | | | |

| | | | American International Group, Inc., | | | | | | |

| | 1,900 | | | 3.65%, 1/15/14 | | | | | 1,941,764 | |

| | 7,600 | | | 5.05%, 10/1/15 | | | | | 8,140,086 | |

| | 2,000 | | | 5.45%, 5/18/17 | | | | | 2,172,436 | |

| | 900 | | | 5.60%, 10/18/16 | | | | | 984,258 | |

| | 30,600 | | | 5.85%, 1/16/18 | | | | | 33,727,871 | |

| | 17,200 | | | 6.25%, 5/1/36 | | | | | 19,285,758 | |

| £ | 1,456 | | | 6.765%, 11/15/17 (a)(d) | | | | | 2,584,302 | |

| € | 5,557 | | | 6.797%, 11/15/17 (a)(b)(d)(l) (acquisition cost–$10,216,616; purchased 3/8/07) | | | | | 8,109,773 | |

| $ | 70,000 | | | 8.25%, 8/15/18 | | | | | 85,007,230 | |

| | | | | | | | | | |

| | | | | | | | | 161,953,478 | |

| | | | | | | | | | |

| | | |

| | | | Metals & Mining–0.9% | | | | | | |

| | 2,900 | | | CSN Islands XI Corp., 6.875%, 9/21/19 (a)(d) | | | | | 3,291,500 | |

| | | | Gerdau Holdings, Inc., | | | | | | |

| | 3,950 | | | 7.00%, 1/20/20 | | | | | 4,512,875 | |

| | 11,800 | | | 7.00%, 1/20/20 (a)(d) | | | | | 13,481,500 | |

| | 1,000 | | | Gerdau Trade, Inc., 5.75%, 1/30/21 (a)(d) | | | | | 1,064,000 | |

| | 5,000 | | | Gold Fields Orogen Holding BVI Ltd., 4.875%, 10/7/20 (a)(d) | | | | | 4,738,720 | |

| | 1,600 | | | Newmont Mining Corp., 5.125%, 10/1/19 | | | | | 1,806,469 | |

| | 800 | | | Teck Resources Ltd., 4.50%, 1/15/21 | | | | | 850,381 | |

| | | | Vale Overseas Ltd., | | | | | | |

| | 2,790 | | | 6.875%, 11/10/39 | | | | | 3,359,584 | |

| | | | |

| 16 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Metals & Mining (continued) | | | | | | |

| | | | | | | | | | |

| $ | 2,000 | | | 8.25%, 1/17/34 | | | | $ | 2,675,536 | |

| | | | | | | | | | |

| | | | | | | | | 35,780,565 | |

| | | | | | | | | | |

| | | |

| | | | Multi-Media–1.9% | | | | | | |

| | 1,000 | | | Comcast Cable Communications LLC, 7.125%, 6/15/13 | | | | | 1,071,015 | |

| | | | Comcast Corp., | | | | | | |

| | 10,600 | | | 5.875%, 2/15/18 | | | | | 12,602,139 | |

| | 1,700 | | | 5.90%, 3/15/16 | | | | | 1,973,615 | |

| | 700 | | | 6.30%, 11/15/17 | | | | | 849,925 | |

| | | | CSC Holdings LLC, | | | | | | |

| | 7,850 | | | 7.625%, 7/15/18 | | | | | 8,733,125 | |

| | 810 | | | 7.875%, 2/15/18 | | | | | 903,150 | |

| | 7,500 | | | 8.625%, 2/15/19 | | | | | 8,550,000 | |

| | | | DISH DBS Corp., | | | | | | |

| | 3,700 | | | 7.00%, 10/1/13 | | | | | 3,972,875 | |

| | 4,200 | | | 7.125%, 2/1/16 | | | | | 4,672,500 | |

| | 19,200 | | | 7.75%, 5/31/15 | | | | | 21,696,000 | |

| | | | Time Warner Cable, Inc., | | | | | | |

| | 6,940 | | | 5.85%, 5/1/17 | | | | | 8,135,137 | |

| | 1,500 | | | 8.25%, 4/1/19 | | | | | 1,955,646 | |

| | | | | | | | | | |

| | | | | | | | | 75,115,127 | |

| | | | | | | | | | |

| | | |

| | | | Oil & Gas–5.8% | | | | | | |

| | 300 | | | Anadarko Petroleum Corp., 5.95%, 9/15/16 | | | | | 347,114 | |

| | 1,100 | | | BP Capital Markets PLC, 3.625%, 5/8/14 | | | | | 1,156,816 | |

| | 2,400 | | | Canadian Natural Resources Ltd., 6.00%, 8/15/16 | | | | | 2,830,942 | |

| | 10,400 | | | Canadian Oil Sands Ltd., 7.75%, 5/15/19 (a)(d) | | | | | 12,869,490 | |

| | 2,900 | | | DCP Midstream LLC, 5.375%, 10/15/15 (a)(d) | | | | | 3,141,358 | |

| | 846 | | | Devon Energy Corp., 7.95%, 4/15/32 | | | | | 1,214,536 | |

| | 1,300 | | | Devon Financing Corp. ULC, 7.875%, 9/30/31 | | | | | 1,848,504 | |

| | 1,330 | | | Ecopetrol S.A., 7.625%, 7/23/19 | | | | | 1,676,465 | |

| | | | El Paso Corp., | | | | | | |

| | 1,789 | | | 7.00%, 6/15/17 | | | | | 2,020,541 | |

| | 19,700 | | | 7.25%, 6/1/18 | | | | | 22,632,404 | |

| | 4,800 | | | Enbridge Energy Partners L.P., 5.875%, 12/15/16 | | | | | 5,538,067 | |

| | | | EnCana Corp., | | | | | | |

| | 2,000 | | | 5.90%, 12/1/17 | | | | | 2,315,714 | |

| | 4,700 | | | 6.50%, 8/15/34 | | | | | 5,156,732 | |

| | | | Energy Transfer Partners L.P., | | | | | | |

| | 2,100 | | | 6.125%, 2/15/17 | | | | | 2,343,564 | |

| | 2,600 | | | 6.625%, 10/15/36 | | | | | 2,723,919 | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 17 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Oil & Gas (continued) | | | | | | |

| | | | | | | | | | |

| | | | Gaz Capital S.A. for Gazprom, | | | | | | |

| $ | 6,500 | | | 6.212%, 11/22/16 | | | | $ | 7,121,985 | |

| | 1,300 | | | 6.51%, 3/7/22 | | | | | 1,433,510 | |

| | 14,000 | | | 8.146%, 4/11/18 (a)(d) | | | | | 16,587,900 | |

| | 1,551 | | | Gazprom International S.A. for Gazprom, 7.201%, 2/1/20 | | | | | 1,717,874 | |

| | 1,800 | | | Halliburton Co., 6.15%, 9/15/19 | | | | | 2,219,301 | |

| | 923 | | | Kern River Funding Corp., 4.893%, 4/30/18 (a)(d) | | | | | 1,021,949 | |

| | | | Kinder Morgan Energy Partners L.P., | | | | | | |

| | 700 | | | 5.00%, 12/15/13 | | | | | 741,327 | |

| | 5,800 | | | 6.00%, 2/1/17 | | | | | 6,747,488 | |

| | 3,800 | | | 6.95%, 1/15/38 | | | | | 4,492,911 | |

| | 5,500 | | | 7.30%, 8/15/33 | | | | | 6,491,430 | |

| | 11,900 | | | Midcontinent Express Pipeline LLC, 5.45%, 9/15/14 (a)(d) | | | | | 12,143,188 | |

| | 3,400 | | | NGPL PipeCo LLC, 7.119%, 12/15/17 (a)(d) | | | | | 3,290,843 | |

| | 1,700 | | | Northwest Pipeline GP, 7.00%, 6/15/16 | | | | | 2,005,390 | |

| | 294 | | | Odebrecht Drilling Norbe VIII/IX Ltd., 6.35%, 6/30/21 (a)(d) | | | | | 314,580 | |

| | 500 | | | Pemex Project Funding Master Trust, 5.75%, 12/15/15 | | | | | 562,500 | |

| | 15,250 | | | Petrobras International Finance Co., 7.875%, 3/15/19 | | | | | 18,922,322 | |

| | | | Petroleos Mexicanos, | | | | | | |

| | 18,700 | | | 5.50%, 1/21/21 | | | | | 20,906,600 | |

| | 14,550 | | | 6.50%, 6/2/41 | | | | | 16,950,750 | |

| | 7,500 | | | 8.00%, 5/3/19 | | | | | 9,562,500 | |

| | 2,600 | | | Plains All American Pipeline L.P., 6.65%, 1/15/37 | | | | | 3,107,626 | |

| | 1,200 | | | Plains Exploration & Production Co., 7.00%, 3/15/17 | | | | | 1,242,000 | |

| | 2,939 | | | Ras Laffan Liquefied Natural Gas Co., Ltd. II, 5.298%, 9/30/20 | | | | | 3,185,613 | |

| | | | Ras Laffan Liquefied Natural Gas Co., Ltd. III, | | | | | | |

| | 1,400 | | | 5.50%, 9/30/14 (b) | | | | | 1,515,570 | |

| | 1,778 | | | 5.832%, 9/30/16 (b) | | | | | 1,915,526 | |

| | 3,000 | | | 6.75%, 9/30/19 | | | | | 3,555,000 | |

| | 1,800 | | | Reliance Holdings USA, Inc., 4.50%, 10/19/20 (b) | | | | | 1,736,320 | |

| | 100 | | | Rockies Express Pipeline LLC, 5.625%, 4/15/20 (a)(d) | | | | | 91,000 | |

| | 4,400 | | | Southern Natural Gas Co. LLC, 5.90%, 4/1/17 (a)(d) | | | | | 5,040,209 | |

| | 1,950 | | | Tennessee Gas Pipeline Co., 7.50%, 4/1/17 | | | | | 2,331,500 | |

| | 1,100 | | | TransCanada PipeLines Ltd., 3.80%, 10/1/20 | | | | | 1,200,173 | |

| | | | | | | | | | |

| | | | | | | | | 225,971,051 | |

| | | | | | | | | | |

| | | |

| | | | Paper & Forest Products–0.2% | | | | | | |

| | 5,000 | | | Weyerhaeuser Co., 7.375%, 10/1/19 | | | | | 5,897,820 | |

| | | | | | | | | | |

| | | |

| | | | Paper/Paper Products–0.2% | | | | | | |

| | 1,000 | | | Fibria Overseas Finance Ltd., 7.50%, 5/4/20 (a)(d) | | | | | 1,052,500 | |

| | | | |

| 18 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Paper/Paper Products (continued) | | | | | | |

| | | | | | | | | | |

| $ | 6,300 | | | Georgia-Pacific LLC, 5.40%, 11/1/20 (a)(d) | | | | $ | 7,188,911 | |

| | | | | | | | | | |

| | | | | | | | | 8,241,411 | |

| | | | | | | | | | |

| | | |

| | | | Retail–1.0% | | | | | | |

| | | | CVS Pass Through Trust, | | | | | | |

| | 8,054 | | | 6.943%, 1/10/30 | | | | | 9,511,508 | |

| | 22,868 | | | 7.507%, 1/10/32 (a)(d) | | | | | 28,421,808 | |

| | | | | | | | | | |

| | | | | | | | | 37,933,316 | |

| | | | | | | | | | |

| | | |

| | | | Road & Rail–0.1% | | | | | | |

| | 1,800 | | | Canadian National Railway Co., 5.55%, 3/1/19 | | | | | 2,188,181 | |

| | | | | | | | | | |

| | | |

| | | | Technology–0.1% | | | | | | |

| | 1,800 | | | International Business Machines Corp., 8.375%, 11/1/19 | | | | | 2,544,579 | |

| | 1,800 | | | Oracle Corp., 5.00%, 7/8/19 | | | | | 2,139,860 | |

| | | | | | | | | | |

| | | | | | | | | 4,684,439 | |

| | | | | | | | | | |

| | | |

| | | | Telecommunications–2.9% | | | | | | |

| | | | America Movil SAB De C.V., | | | | | | |

| | 42,800 | | | 5.00%, 3/30/20 | | | | | 48,539,822 | |

| | 21,400 | | | 6.125%, 3/30/40 | | | | | 25,884,456 | |

| | | | AT&T, Inc., | | | | | | |

| | 1,718 | | | 5.35%, 9/1/40 | | | | | 1,882,603 | |

| | 5,000 | | | 5.50%, 2/1/18 | | | | | 5,903,090 | |

| | 1,100 | | | 5.80%, 2/15/19 | | | | | 1,323,781 | |

| | 51 | | | AT&T Corp., 8.00%, 11/15/31 | | | | | 73,256 | |

| | 1,000 | | | Axiata SPV1 Labuan Ltd., 5.375%, 4/28/20 | | | | | 1,076,723 | |

| | 4,500 | | | Deutsche Telekom International Finance BV, 6.75%, 8/20/18 | | | | | 5,435,384 | |

| | | | Qtel International Finance Ltd. (a)(d), | | | | | | |

| | 3,000 | | | 3.375%, 10/14/16 | | | | | 3,067,500 | |

| | 7,300 | | | 5.00%, 10/19/25 | | | | | 7,500,750 | |

| | 5,000 | | | Qwest Communications International, Inc., 7.50%, 2/15/14 | | | | | 5,025,000 | |

| | | | Qwest Corp., | | | | | | |

| | 2,000 | | | 3.724%, 6/15/13, FRN | | | | | 2,037,500 | |

| | 1,250 | | | 6.50%, 6/1/17 | | | | | 1,436,211 | |

| | 4,800 | | | Sprint Capital Corp., 8.75%, 3/15/32 | | | | | 4,092,000 | |

| | 1,100 | | | Verizon Communications, Inc., 8.75%, 11/1/18 | | | | | 1,504,151 | |

| | | | | | | | | | |

| | | | | | | | | 114,782,227 | |

| | | | | | | | | | |

| | | |

| | | | Tobacco–0.7% | | | | | | |

| | 10,000 | | | Altria Group, Inc., 10.20%, 2/6/39 | | | | | 16,055,180 | |

| | 1,400 | | | Philip Morris International, Inc., 5.65%, 5/16/18 | | | | | 1,676,768 | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 19 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Tobacco (continued) | | | | | | |

| | | | | | | | | | |

| $ | 8,130 | | | Reynolds American, Inc., 7.75%, 6/1/18 | | | | $ | 10,208,760 | |

| | | | | | | | | | |

| | | | | | | | | 27,940,708 | |

| | | | | | | | | | |

| | | |

| | | | Utilities–2.2% | | | | | | |

| | 2,618 | | | Bruce Mansfield Unit, 6.85%, 6/1/34 | | | | | 2,814,553 | |

| | 2,000 | | | Consumers Energy Co., 5.15%, 2/15/17 | | | | | 2,306,594 | |

| | 5,000 | | | DTE Energy Co., 6.35%, 6/1/16 | | | | | 5,796,270 | |

| | 14,200 | | | EDF S.A., 6.50%, 1/26/19 (a)(d) | | | | | 16,782,469 | |

| | 27,500 | | | Entergy Corp., 3.625%, 9/15/15 | | | | | 28,087,400 | |

| | 174 | | | GG1C Funding Corp., 5.129%, 1/15/14 (a)(d) | | | | | 173,490 | |

| | | | Korea Hydro & Nuclear Power Co., Ltd., | | | | | | |

| | 300 | | | 3.125%, 9/16/15 (a)(d) | | | | | 306,163 | |

| | 4,450 | | | 6.25%, 6/17/14 | | | | | 4,817,054 | |

| | 1,000 | | | Majapahit Holding BV, 7.25%, 6/28/17 | | | | | 1,150,000 | |

| | | | Nevada Power Co., | | | | | | |

| | 100 | | | 5.875%, 1/15/15 | | | | | 112,515 | |

| | 1,600 | | | 5.95%, 3/15/16 | | | | | 1,841,016 | |

| | 3,000 | | | 6.50%, 5/15/18 | | | | | 3,698,202 | |

| | 900 | | | Nisource Finance Corp., 6.40%, 3/15/18 | | | | | 1,061,805 | |

| | 6,100 | | | NRG Energy, Inc., 7.625%, 1/15/18 | | | | | 6,206,750 | |

| | 1,700 | | | Ohio Edison Co., 5.45%, 5/1/15 | | | | | 1,869,488 | |

| | 2,900 | | | Public Service Co. of Oklahoma, 6.15%, 8/1/16 | | | | | 3,350,060 | |

| | 1,900 | | | Sierra Pacific Power Co., 6.00%, 5/15/16 | | | | | 2,217,893 | |

| | 4,500 | | | Toledo Edison Co., 6.15%, 5/15/37 | | | | | 5,422,684 | |

| | 54 | | | W3A Funding Corp., 8.09%, 1/2/17 | | | | | 54,949 | |

| | | | | | | | | | |

| | | | | | | | | 88,069,355 | |

| | | | | | | | | | |

| | | | Total Corporate Bonds & Notes (cost–$1,721,982,712) | | | | | 1,879,151,947 | |

| | | | | | | | | | |

| | | | | | | | | | |

| SOVEREIGN DEBT OBLIGATIONS–13.6% | | | | |

| | | | Australia–7.1% | | | | | | |

| | | | Australia Government Bond (i), | | | | | | |

| | AUD 110,800 | | | 3.00%, 9/20/25, Ser. 25-CI | | | | | 151,804,955 | |

| | AUD 61,700 | | | 4.00%, 8/20/20, Ser. 20-CI | | | | | 120,556,592 | |

| | AUD 5,400 | | | Queensland Treasury Corp., 6.00%, 9/14/17, Ser. 17 | | | | | 6,161,135 | |

| | | | | | | | | | |

| | | | | | | | | 278,522,682 | |

| | | | | | | | | | |

| | | |

| | | | Brazil–5.0% | | | | | | |

| | | | Brazil Notas do Tesouro Nacional, Ser. F, | | | | | | |

| | BRL 24,573 | | | 10.00%, 1/1/14 | | | | | 13,122,295 | |

| | BRL 164,206 | | | 10.00%, 1/1/17 | | | | | 86,032,378 | |

| | | | |

| 20 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Brazil (continued) | | | | | | |

| | | | | | | | | | |

| | BRL 147,171 | | | 10.00%, 1/1/21 | | | | $ | 74,750,912 | |

| | $ 3,300 | | | Brazilian Development Bank, 6.369%, 6/16/18 | | | | | 3,873,540 | |

| | | | Brazilian Government International Bond, | | | | | | |

| | 1,600 | | | 4.875%, 1/22/21 | | | | | 1,844,800 | |

| | 12,176 | | | 8.875%, 10/14/19 | | | | | 17,387,328 | |

| | | | | | | | | | |

| | | | | | | | | 197,011,253 | |

| | | | | | | | | | |

| | | |

| | | | Canada–0.3% | | | | | | |

| | CAD 2,400 | | | Province of Ontario Canada, 6.50%, 3/8/29 | | | | | 3,350,146 | |

| | $ 7,800 | | | Province of Quebec Canada, 3.50%, 7/29/20 | | | | | 8,523,450 | |

| | | | | | | | | | |

| | | | | | | | | 11,873,596 | |

| | | | | | | | | | |

| | | |

| | | | Colombia–0.1% | | | | | | |

| | 2,000 | | | Colombia Government International Bond, 7.375%, 1/27/17 | | | | | 2,486,000 | |

| | | | | | | | | | |

| | | |

| | | | Indonesia–0.1% | | | | | | |

| | 3,100 | | | Indonesia Government International Bond, 6.875%, 1/17/18 | | | | | 3,677,375 | |

| | | | | | | | | | |

| | | |

| | | | Korea (Republic of)–0.4% | | | | | | |

| | 10,800 | | | Export-Import Bank of Korea, 4.00%, 1/29/21 | | | | | 10,835,316 | |

| | | | Korea Development Bank, | | | | | | |

| | 3,950 | | | 4.00%, 9/9/16 | | | | | 4,154,902 | |

| | 300 | | | 8.00%, 1/23/14 | | | | | 329,886 | |

| | | | | | | | | | |

| | | | | | | | | 15,320,104 | |

| | | | | | | | | | |

| | | |

| | | | Mexico–0.3% | | | | | | |

| | 10,000 | | | Mexico Government International Bond, 6.05%, 1/11/40 | | | | | 12,525,000 | |

| | | | | | | | | | |

| | | |

| | | | Qatar–0.3% | | | | | | |

| | | | Qatar Government International Bond (a)(d), | | | | | | |

| | 3,300 | | | 4.00%, 1/20/15 | | | | | 3,494,700 | |

| | 6,100 | | | 5.25%, 1/20/20 | | | | | 6,855,180 | |

| | | | | | | | | | |

| | | | | | | | | 10,349,880 | |

| | | | | | | | | | |

| | | |

| | | | Russian Federation–0.0% | | | | | | |

| | 1,610 | | | Russian Federation Bond, 7.50%, 3/31/30, VRN | | | | | 1,934,012 | |

| | | | | | | | | | |

| | | |

| | | | South Africa–0.0% | | | | | | |

| | 300 | | | South Africa Government International Bond, 6.875%, 5/27/19 | | | | | 368,625 | |

| | | | | | | | | | |

| | | | Total Sovereign Debt Obligations (cost–$527,310,342) | | | | | 534,068,527 | |

| | | | | | | | | | |

| | | | | | | | | | |

| U.S. GOVERNMENT AGENCY SECURITIES–13.2% | | | | |

| | | | Fannie Mae–12.0% | | | | | | |

| | 1,489 | | | 2.165%, 5/1/35, FRN, MBS | | | | | 1,567,238 | |

| | 3,820 | | | 2.391%, 11/1/35, FRN, MBS | | | | | 4,063,385 | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 21 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Fannie Mae (continued) | | | | | | |

| | | | | | | | | | |

| $ | 3 | | | 2.456%, 8/25/18, CMO, FRN | | | | $ | 2,742 | |

| | 5 | | | 3.089%, 2/1/18, FRN, MBS | | | | | 5,099 | |

| | 2,327 | | | 4.00%, 11/1/40, MBS | | | | | 2,465,097 | |

| | 3 | | | 4.095%, 4/1/17, FRN, MBS | | | | | 3,367 | |

| | 287,356 | | | 4.50%, 3/1/29 - 11/1/41, MBS | | | | | 308,542,153 | |

| | 143,000 | | | 4.50%, MBS, TBA, 30 Year (e) | | | | | 153,080,313 | |

| | 1,217 | | | 5.29%, 11/25/33, CMO | | | | | 1,261,763 | |

| | | | | | | | | | |

| | | | | | | | | 470,991,157 | |

| | | | | | | | | | |

| | | |

| | | | Freddie Mac–0.0% | | | | | | |

| | 8 | | | 2.50%, 12/1/18, FRN, MBS | | | | | 8,008 | |

| | 2 | | | 2.575%, 6/1/30, FRN, MBS | | | | | 1,995 | |

| | 456 | | | 6.50%, 1/1/38 - 10/1/38, MBS | | | | | 514,605 | |

| | | | | | | | | | |

| | | | | | | | | 524,608 | |

| | | | | | | | | | |

| | | |

| | | | Ginnie Mae–0.0% | | | | | | |

| | 13 | | | 2.375%, 1/20/22, FRN, MBS | | | | | 13,455 | |

| | | | | | | | | | |

| | | |

| | | | Small Business Administration Participation Certificates–1.2% | | | | | | |

| | 233 | | | 4.504%, 2/10/14 | | | | | 240,051 | |

| | 3,606 | | | 4.77%, 4/1/24, ABS | | | | | 3,960,132 | |

| | 21,945 | | | 5.32%, 1/1/27, ABS | | | | | 24,686,274 | |

| | 16,239 | | | 5.70%, 8/1/26, ABS | | | | | 18,372,238 | |

| | | | | | | | | | |

| | | | | | | | | 47,258,695 | |

| | | | | | | | | | |

| | | | Total U.S. Government Agency Securities (cost–$501,834,023) | | | | | 518,787,915 | |

| | | | | | | | | | |

| | | | | | | | | | |

| MUNICIPAL BONDS–9.7% | | | | |

| | | | Arizona–0.1% | | | | | | |

| | 2,000 | | | Univ. of Arizona Rev., 6.423%, 8/1/35, Ser. A | | | | | 2,231,660 | |

| | | | | | | | | | |

| | | |

| | | | California–5.5% | | | | | | |

| | 2,400 | | | Golden State Tobacco Securitization Corp. Rev., | | | | | | |

| | | | 5.75%, 6/1/47, Ser. A-1 | | | | | 1,977,720 | |

| | 15,000 | | | Infrastructure & Economic Dev. Bank Rev., 6.486%, 5/15/49 | | | | | 18,105,450 | |

| | | | Los Angeles Cnty. Public Works Financing Auth. Rev., | | | | | | |

| | 7,400 | | | 7.488%, 8/1/33 | | | | | 9,193,686 | |

| | 14,300 | | | 7.618%, 8/1/40 | | | | | 18,372,640 | |

| | 25,000 | | | Los Angeles Community College Dist., GO, 6.75%, 8/1/49 | | | | | 33,637,250 | |

| | 3,000 | | | Los Angeles Department of Water & Power Rev., 5.516%, 7/1/27, Ser. C | | | | | 3,360,300 | |

| | 1,300 | | | Los Angeles Unified School Dist., GO, 6.758%, 7/1/34 | | | | | 1,676,974 | |

| | 13,600 | | | Northern California Power Agcy. Rev., 7.311%, 6/1/40 | | | | | 15,943,280 | |

| | 300 | | | Palomar Community College Dist., GO, 7.194%, 8/1/45, Ser. B-1 | | | | | 350,400 | |

| | 1,000 | | | San Diego Cnty. Water Auth. Rev., 6.138%, 5/1/49 | | | | | 1,299,650 | |

| | | | |

| 22 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | California (continued) | | | | | | |

| | | | | | | | | | |

| | | | State, GO, | | | | | | |

| $ | 800 | | | 4.85%, 10/1/14 | | | | $ | 872,184 | |

| | 400 | | | 6.20%, 10/1/19 | | | | | 478,896 | |

| | 1,500 | | | 6.65%, 3/1/22 | | | | | 1,823,805 | |

| | 8,550 | | | 7.55%, 4/1/39 | | | | | 11,201,269 | |

| | 36,400 | | | 7.60%, 11/1/40 | | | | | 48,242,012 | |

| | 12,000 | | | 7.70%, 11/1/30 | | | | | 14,229,240 | |

| | 23,500 | | | 7.95%, 3/1/36 | | | | | 27,675,950 | |

| | 7,500 | | | Univ. of California Rev., 0.887%, 7/1/13, Ser. AA-2 | | | | | 7,535,325 | |

| | | | | | | | | | |

| | | | | | | | | 215,976,031 | |

| | | | | | | | | | |

| | | |

| | | | Illinois–0.5% | | | | | | |

| | 10,500 | | | Chicago Transit Auth. Rev., 6.20%, 12/1/40, Ser. B | | | | | 12,089,910 | |

| | 1,600 | | | Finance Auth. Rev., Univ. of Chicago, 5.50%, 7/1/37, Ser. B | | | | | 1,792,832 | |

| | 2,500 | | | Greater Chicago Metropolitan Water Reclamation Dist., GO, 5.72%, 12/1/38 | | | | | 3,157,625 | |

| | | | | | | | | | |

| | | | | | | | | 17,040,367 | |

| | | | | | | | | | |

| | | |

| | | | Iowa–0.0% | | | | | | |

| | 725 | | | Tobacco Settlement Auth. Rev., 6.50%, 6/1/23, Ser. A | | | | | 689,838 | |

| | | | | | | | | | |

| | | |

| | | | Massachusetts–0.5% | | | | | | |

| | 17,000 | | | School Building Auth. Rev., 5.468%, 6/15/27 | | | | | 20,107,770 | |

| | | | | | | | | | |

| | | |

| | | | New Jersey–0.3% | | | | | | |

| | | | State Turnpike Auth. Rev., | | | | | | |

| | 5,000 | | | 7.102%, 1/1/41, Ser. A | | | | | 7,002,250 | |

| | 3,900 | | | 7.414%, 1/1/40, Ser. F | | | | | 5,600,790 | |

| | 250 | | | Tobacco Settlement Financing Corp. Rev., 5.00%, 6/1/41, Ser. 1-A | | | | | 198,285 | |

| | | | | | | | | | |

| | | | | | | | | 12,801,325 | |

| | | | | | | | | | |

| | | |

| | | | New York–0.8% | | | | | | |

| | 5,500 | | | Metropolitan Transportation Auth. Rev., 5.871%, 11/15/39 | | | | | 6,304,430 | |

| | 3,000 | | | New York City, GO, 4.769%, 10/1/23, Ser. A-2 | | | | | 3,416,130 | |

| | | | New York City Municipal Water Finance Auth. Rev., | | | | | | |

| | 3,640 | | | 5.79%, 6/15/41 | | | | | 3,987,220 | |

| | 1,445 | | | 6.011%, 6/15/42 | | | | | 1,894,944 | |

| | | | New York City Transitional Finance Auth. Rev., | | | | | | |

| | 400 | | | 4.325%, 11/1/21 | | | | | 450,904 | |

| | 800 | | | 4.525%, 11/1/22 | | | | | 908,368 | |

| | 3,000 | | | 5.267%, 5/1/27, Ser. G-3 | | | | | 3,606,570 | |

| | 700 | | | 5.572%, 11/1/38 | | | | | 848,596 | |

| | 800 | | | 5.932%, 11/1/36 | | | | | 898,136 | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 23 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | New York (continued) | | | | | | |

| | | | | | | | | | |

| | | | State Dormitory Auth. Rev., | | | | | | |

| $ | 1,600 | | | 5.289%, 3/15/33 | | | | $ | 1,850,528 | |

| | 2,700 | | | 5.389%, 3/15/40 | | | | | 3,193,992 | |

| | 4,000 | | | State Urban Dev. Corp. Rev., 5.77%, 3/15/39 | | | | | 4,783,040 | |

| | | | | | | | | | |

| | | | | | | | | 32,142,858 | |

| | | | | | | | | | |

| | | |

| | | | Ohio–0.4% | | | | | | |

| | | | American Municipal Power-Ohio, Inc. Rev., | | | | | | |

| | 3,600 | | | 5.939%, 2/15/47 | | | | | 3,999,060 | |

| | 1,400 | | | Comb Hydroelectric Projects, 7.834%, 2/15/41, Ser. B | | | | | 1,904,140 | |

| | | | Buckeye Tobacco Settlement Financing Auth. Rev., Ser. A-2, | | | | | | |

| | 11,700 | | | 5.75%, 6/1/34 | | | | | 9,110,673 | |

| | 900 | | | 5.875%, 6/1/47 | | | | | 702,567 | |

| | | | | | | | | | |

| | | | | | | | | 15,716,440 | |

| | | | | | | | | | |

| | | |

| | | | Texas–1.6% | | | | | | |

| | 43,800 | | | Dallas Area Rapid Transit Rev., 5.022%, 12/1/48 | | | | | 51,678,744 | |

| | 4,400 | | | Dallas Cnty. Hospital Dist., GO, 5.621%, 8/15/44, Ser. C | | | | | 5,448,212 | |

| | 4,100 | | | North Texas Tollway Auth. Rev., 6.718%, 1/1/49, Ser. B | | | | | 5,330,246 | |

| | | | | | | | | | |

| | | | | | | | | 62,457,202 | |

| | | | | | | | | | |

| | | | Total Municipal Bonds (cost–$316,338,507) | | | | | 379,163,491 | |

| | | | | | | | | | |

| | | | | | | | | | |

| MORTGAGE-BACKED SECURITIES–4.5% | | | | |

| | 197 | | | Banc of America Funding Corp., 5.739%, 1/20/47, CMO, FRN | | | | | 120,445 | |

| | 204 | | | Banc of America Large Loan, Inc., 0.75%, 8/15/29, CMO, FRN (b) | | | | | 195,362 | |

| | 4,400 | | | Banc of America Merrill Lynch Commercial Mortgage, Inc., | | | | | | |

| | | | 5.889%, 7/10/44, CMO, VRN | | | | | 4,990,218 | |

| | | | Bear Stearns Adjustable Rate Mortgage Trust, CMO, FRN, | | | | | | |

| | 1,494 | | | 2.25%, 8/25/35 | | | | | 1,380,654 | |

| | 1,680 | | | 2.57%, 3/25/35 | | | | | 1,633,947 | |

| | 118 | | | 2.681%, 10/25/35 | | | | | 117,337 | |

| | 124 | | | 2.689%, 10/25/33 | | | | | 124,777 | |

| | 354 | | | 3.078%, 3/25/35 | | | | | 346,605 | |

| | 84 | | | 3.189%, 5/25/34 | | | | | 72,507 | |

| | | | Bear Stearns Alt-A Trust, CMO, FRN, | | | | | | |

| | 1,360 | | | 2.777%, 2/25/36 | | | | | 612,375 | |

| | 4,389 | | | 2.794%, 11/25/36 | | | | | 2,423,288 | |

| | 5,676 | | | 2.863%, 11/25/36 | | | | | 3,066,691 | |

| | | | Bear Stearns Commercial Mortgage Securities, CMO, | | | | | | |

| | 1,600 | | | 5.54%, 9/11/41 | | | | | 1,828,281 | |

| | 7,500 | | | 5.694%, 6/11/50, VRN | | | | | 8,659,099 | |

| | | | |

| 24 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Citigroup Mortgage Loan Trust, Inc., CMO, FRN, | | | | | | |

| | | | | | | | | | |

| $ | 645 | | | 2.23%, 9/25/35 | | | | $ | 599,632 | |

| | 578 | | | 2.45%, 9/25/35 | | | | | 509,290 | |

| | | | Citigroup/Deutsche Bank Commercial Mortgage Trust, CMO, | | | | | | |

| | 4,400 | | | 5.322%, 12/11/49 | | | | | 4,895,715 | |

| | 8,000 | | | 5.505%, 1/15/46, VRN | | | | | 8,905,012 | |

| € | 265 | | | Cordusio RMBS SRL, 0.927%, 6/30/35, CMO, FRN | | | | | 325,777 | |

| | | | Countrywide Alternative Loan Trust, CMO, | | | | | | |

| $ | 2,217 | | | 0.429%, 11/25/46, FRN | | | | | 1,339,229 | |

| | 632 | | | 0.439%, 5/25/36, FRN | | | | | 354,034 | |

| | 10,944 | | | 6.25%, 8/25/37 | | | | | 6,801,759 | |

| | | | Countrywide Home Loan Mortgage Pass Through Trust, CMO, FRN, | | | | | | |

| | 309 | | | 0.559%, 3/25/35 | | | | | 168,144 | |

| | 68 | | | 2.798%, 8/25/34 | | | | | 49,905 | |

| | 20 | | | Credit Suisse First Boston Mortgage Securities Corp., | | | | | | |

| | | | 2.481%, 7/25/33, CMO, FRN | | | | | 19,162 | |

| | | | Credit Suisse Mortgage Capital Certificates, CMO, | | | | | | |

| | 2,600 | | | 5.311%, 12/15/39 | | | | | 2,903,399 | |

| | 7,300 | | | 5.867%, 6/15/39, VRN | | | | | 7,950,890 | |

| | | | Downey Savings & Loan Assoc. Mortgage Loan Trust, CMO, FRN, | | | | | | |

| | 2,264 | | | 0.50%, 8/19/45 | | | | | 1,510,039 | |

| | 1,328 | | | 2.466%, 7/19/44 | | | | | 1,098,309 | |

| | 118 | | | First Horizon Asset Securities, Inc., 2.541%, 12/25/33, CMO, FRN | | | | | 107,479 | |

| | 3,641 | | | Greenpoint Mortgage Funding Trust, 0.469%, 6/25/45, CMO, FRN | | | | | 2,164,838 | |

| | 15 | | | Greenpoint Mortgage Pass Through Certificates, | | | | | | |

| | | | 3.13%, 10/25/33, CMO, FRN | | | | | 12,886 | |

| | | | GSR Mortgage Loan Trust, CMO, FRN, | | | | | | |

| | 119 | | | 1.93%, 3/25/33 | | | | | 115,295 | |

| | 893 | | | 2.653%, 9/25/35 | | | | | 870,147 | |

| | 2,088 | | | 2.671%, 9/25/35 | | | | | 2,005,158 | |

| | | | Harborview Mortgage Loan Trust, CMO, FRN, | | | | | | |

| | 320 | | | 0.43%, 1/19/38 | | | | | 205,772 | |

| | 558 | | | 0.58%, 6/20/35 | | | | | 448,163 | |

| | 236 | | | 3.029%, 5/19/33 | | | | | 229,736 | |

| | 368 | | | Homebanc Mortgage Trust, 5.593%, 4/25/37, CMO, FRN | | | | | 320,151 | |

| € | 32 | | | IntesaBci Sec 2 SRL, 1.286%, 8/28/23, CMO, FRN | | | | | 42,684 | |

| | | | JPMorgan Chase Commercial Mortgage Securities Corp., CMO, | | | | | | |

| $ | 12,500 | | | 3.341%, 7/15/46 (a)(d) | | | | | 13,162,525 | |

| | 20,600 | | | 4.106%, 7/15/46 (a)(d) | | | | | 22,406,260 | |

| | 1,000 | | | 5.336%, 5/15/47 | | | | | 1,105,748 | |

| | 6,600 | | | 5.42%, 1/15/49 | | | | | 7,385,888 | |

| | 2,200 | | | 5.44%, 6/12/47 | | | | | 2,477,302 | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 25 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | JPMorgan Mortgage Trust, CMO, FRN, | | | | | | |

| | | | | | | | | | |

| $ | 116 | | | 2.245%, 11/25/33 | | | | $ | 110,666 | |

| | 1,675 | | | 2.85%, 7/25/35 | | | | | 1,628,812 | |

| | 175 | | | 5.003%, 2/25/35 | | | | | 174,384 | |

| | 5,357 | | | 5.235%, 2/25/36 | | | | | 4,152,631 | |

| | 1,761 | | | 5.315%, 7/25/35 | | | | | 1,771,335 | |

| | | | Merrill Lynch/Countrywide Commercial Mortgage Trust, CMO, VRN, | | | | | | |

| | 1,200 | | | 5.172%, 12/12/49 | | | | | 1,328,975 | |

| | 1,600 | | | 6.165%, 8/12/49 | | | | | 1,784,036 | |

| | 555 | | | Morgan Stanley Dean Witter Capital I, 4.74%, 11/13/36, CMO | | | | | 562,759 | |

| | 1,500 | | | Morgan Stanley Reremic Trust, 5.98%, 8/15/45, CMO, VRN (a)(d) | | | | | 1,699,468 | |

| | 443 | | | Ocwen Residential MBS Corp., 7.00%, 10/25/40, CMO, VRN (a)(d)(g) | | | | | 39,662 | |

| | | | RBSSP Resecuritization Trust, CMO, FRN (a)(d), | | | | | | |

| | 1,455 | | | 0.519%, 5/26/37 | | | | | 1,368,359 | |

| | 14,792 | | | 0.559%, 3/26/37 | | | | | 13,529,246 | |

| | 6,990 | | | 0.739%, 9/26/34 | | | | | 6,440,873 | |

| | 9,606 | | | 0.739%, 3/26/36 | | | | | 8,945,250 | |

| | 6,391 | | | 0.739%, 4/26/37 | | | | | 5,874,209 | |

| | 1,541 | | | Residential Accredit Loans, Inc., 0.449%, 4/25/46, CMO, FRN | | | | | 617,213 | |

| | 149 | | | Structured Adjustable Rate Mortgage Loan Trust, | | | | | | |

| | | | 2.728%, 2/25/34, CMO, FRN | | | | | 145,695 | |

| | 4,114 | | | Structured Asset Mortgage Investments, Inc., | | | | | | |

| | | | 0.459%, 5/25/36, CMO, FRN | | | | | 2,079,826 | |

| | | | Wachovia Bank Commercial Mortgage Trust, CMO, | | | | | | |

| | 355 | | | 0.32%, 6/15/20, FRN (a)(d) | | | | | 329,531 | |

| | 700 | | | 5.416%, 1/15/45, VRN | | | | | 784,611 | |

| | 1,300 | | | 5.678%, 5/15/46 | | | | | 1,496,851 | |

| | | | WaMu Mortgage Pass Through Certificates, CMO, FRN, | | | | | | |

| | 222 | | | 0.549%, 1/25/45 | | | | | 187,094 | |

| | 2,482 | | | 0.62%, 11/25/34 | | | | | 2,061,498 | |

| | 1,260 | | | 1.158%, 2/25/46 | | | | | 979,225 | |

| | 727 | | | Wells Fargo Mortgage-Backed Securities Trust, | | | | | | |

| | | | 2.637%, 3/25/36, CMO, FRN | | | | | 556,431 | |

| | | | | | | | | | |

| | | | Total Mortgage-Backed Securities (cost–$159,198,303) | | | | | 174,710,554 | |

| | | | | | | | | | |

| | | | | | | | | | |

| U.S. TREASURY OBLIGATIONS (j)–1.9% | | | | |

| | 11,259 | | | U.S. Treasury Inflation Indexed Bonds, 3.625%, 4/15/28 (i) | | | | | 17,106,704 | |

| | 55,900 | | | U.S. Treasury Notes, 2.00%, 11/15/21 | | | | | 56,480,857 | |

| | | | | | | | | | |

| | | | Total U.S. Treasury Obligations (cost–$70,471,603) | | | | | 73,587,561 | |

| | | | | | | | | | |

| | | | |

| 26 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| SENIOR LOANS (a)(c)–0.6% | |

| | | | | | | | | | |

| | | | Financial Services–0.6% | | | | | | |

| $ | 23,000 | | | Springleaf Financial Corp., 5.50%, 5/10/17 | | | | $ | 21,832,750 | |

| | | | | | | | | | |

| | | |

| | | | Healthcare & Hospitals–0.0% | | | | | | |

| | | | HCA, Inc., | | | | | | |

| | 370 | | | 2.489%, 11/17/13, Term B1 | | | | | 369,160 | |

| | 886 | | | 3.72%, 3/31/17, Term B2 | | | | | 874,214 | |

| | | | | | | | | | |

| | | | | | | | | 1,243,374 | |

| | | | | | | | | | |

| | | | Total Senior Loans (cost–$24,157,867) | | | | | 23,076,124 | |

| | | | | | | | | | |

| | | | | | | | | | |

| ASSET-BACKED SECURITIES–0.2% | |

| | 2,000 | | | Bear Stearns Asset-Backed Securities Trust, FRN, | | | | | 1,334,281 | |

| | | | 0.439%, 12/25/36 | | | | | | |

| | 596 | | | 1.239%, 10/25/37 | | | | | 383,337 | |

| | 334 | | | BNC Mortgage Loan Trust, 0.339%, 5/25/37, FRN | | | | | 301,319 | |

| | | | Conseco Financial Corp., | | | | | | |

| | 282 | | | 6.22%, 3/1/30 | | | | | 306,973 | |

| | 4,203 | | | 6.53%, 2/1/31, VRN | | | | | 4,199,432 | |

| | 141 | | | JPMorgan Mortgage Acquisition Corp., 0.319%, 3/25/37, FRN | | | | | 137,607 | |

| | 3 | | | Keystone Owner Trust, 9.00%, 1/25/29 (a)(d) | | | | | 1,340 | |

| | 520 | | | MASTR Asset-Backed Securities Trust, 0.319%, 5/25/37, FRN | | | | | 489,721 | |

| | 258 | | | Merrill Lynch Mortgage Investors, Inc., 0.359%, 2/25/37, FRN | | | | | 118,080 | |

| | 206 | | | Morgan Stanley Mortgage Loan Trust, 0.599%, 4/25/37, FRN | | | | | 78,112 | |

| | 292 | | | Popular ABS Mortgage Pass Through Trust, 0.329%, 6/25/47, FRN | | | | | 249,804 | |

| | | | | | | | | | |

| | | | Total Asset-Backed Securities (cost–$7,182,020) | | | | | 7,600,006 | |

| | | | | | | | | | |

| | | | | | | | | | |

| Shares | | | | | | | | |

| COMMON STOCK–0.0% | |

| | | | Insurance–0.0% | | | | | | |

| | 451 | | | American International Group, Inc. (k) (cost–$13,115) | | | | | 15,347 | |

| | | | | | | | | | |

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | | |

| SHORT-TERM INVESTMENTS–11.3% | |

| | | | U.S. Treasury Obligations (j)(m)–7.9% | | | | | | |

| $ | 309,505 | | | U.S. Treasury Bills, 0.048%-0.163%, 5/3/12-4/4/13 (cost–$309,353,153) | | | | | 309,367,758 | |

| | | | | | | | | | |

| | | |

| | | | Corporate Notes–1.7% | | | | | | |

| | | | Banking–0.1% | | | | | | |

| | 5,000 | | | American Express Bank FSB, 5.50%, 4/16/13 | | | | | 5,222,375 | |

| | | | | | | | | | |

| | | | | | |

| 4.30.12 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | | 27 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Financial Services–1.6% | | | | | | |

| | | | | | | | | | |

| $ | 800 | | | AK Transneft OJSC Via TransCapitalInvest Ltd., 6.103%, 6/27/12 (a)(d) | | | | $ | 804,324 | |

| | 2,300 | | | BRFkredit A/S, 2.05%, 4/15/13 (a)(d) | | | | | 2,326,951 | |

| | 700 | | | Citigroup, Inc., 5.50%, 4/11/13 | | | | | 724,458 | |

| | 4,700 | | | Ford Motor Credit Co. LLC, 7.50%, 8/1/12 | | | | | 4,775,068 | |

| | | | Merrill Lynch & Co., Inc., | | | | | | |

| € | 2,150 | | | 1.558%, 9/27/12, FRN | | | | | 2,842,734 | |

| $ | 7,470 | | | 6.05%, 8/15/12 | | | | | 7,578,741 | |

| | 200 | | | 6.15%, 4/25/13 | | | | | 208,157 | |

| | 15,700 | | | Morgan Stanley, 1.446%, 4/29/13, FRN | | | | | 15,498,349 | |

| | | | SLM Corp., | | | | | | |

| € | 1,600 | | | 3.125%, 9/17/12 | | | | | 2,123,076 | |

| £ | 500 | | | 4.875%, 12/17/12 | | | | | 807,799 | |

| $ | 2,650 | | | 5.125%, 8/27/12 | | | | | 2,678,029 | |

| | 11,200 | | | 5.375%, 1/15/13 | | | | | 11,450,813 | |

| | 7,700 | | | TNK-BP Finance S.A., 7.50%, 3/13/13 | | | | | 8,085,000 | |

| | | | | | | | | | |

| | | | | | | | | 59,903,499 | |

| | | | | | | | | | |

| | | |

| | | | Food & Beverage–0.0% | | | | | | |

| | 400 | | | Kroger Co., 6.20%, 6/15/12 | | | | | 402,525 | |

| | | | | | | | | | |

| | | |

| | | | Oil & Gas–0.0% | | | | | | |

| | 600 | | | Enterprise Products Operating LLC, 4.60%, 8/1/12 | | | | | 606,047 | |

| | | | | | | | | | |

| | | |

| | | | Utilities–0.0% | | | | | | |

| | 1,100 | | | Consumers Energy Co., 5.375%, 4/15/13 | | | | | 1,149,729 | |

| | 200 | | | Midamerican Energy Holdings Co., 5.875%, 10/1/12 | | | | | 204,352 | |

| | | | | | | | | | |

| | | | | | | | | 1,354,081 | |

| | | | | | | | | | |

| | | | Total Corporate Notes (cost–$66,927,606) | | | | | 67,488,527 | |

| | | | | | | | | | |

| | | |

| | | | Sovereign Debt Obligations–0.1% | | | | | | |

| | | | Brazil–0.1% | | | | | | |

| BRL | 8,390 | | | Brazil Notas do Tesouro Nacional, 10.00%, 1/1/13, Ser. F (cost–$5,276,067) | | | | | 4,446,360 | |

| | | | | | | | | | |

| | | |

| | | | Repurchase Agreements–1.6% | | | | | | |

| $ | 5,500 | | | Bank of America Corp.,

dated 4/30/12, 0.21%, due 5/1/12, proceeds

$5,500,032; collateralized by U.S. Treasury

Notes, 0.875%, due 2/28/17, valued at

$5,615,050 including accrued interest | | | | | 5,500,000 | |

| | 5,000 | | | Barclays Capital, Inc.,

dated 4/30/12, 0.21%, due 5/1/12, proceeds

$5,000,029; collateralized by Ginnie Mae,

5.00%, due 6/20/40, valued at $5,163,559

including accrued interest | | | | | 5,000,000 | |

| | | | |

| 28 | | Allianz Global Investors Managed Accounts Trust Semi-Annual Report | | 4.30.12 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2012 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Repurchase Agreements (continued) | | | | | | |

| | | | | | | | | | |

| $ | 5,500 | | | Citigroup Global Markets, Inc.,

dated 4/30/12, 0.21%, due 5/1/12, proceeds

$5,500,032; collateralized by Federal Home

Loan Bank, 1.00%, due 2/13/17, valued at

$5,656,140 including accrued interest | | | | $ | 5,500,000 | |

| | 5,000 | | | JPMorgan Securities, Inc.,

dated 4/30/12, 0.22%, due 5/1/12 proceeds

$5,000,031; collateralized by Fannie Mae,

1.00%, due 12/5/14, valued at $5,107,477