UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09721

AllianzGI Managed Accounts Trust

(Exact name of registrant as specified in charter)

1633 Broadway, New York, New York 10019

(Address of principal executive offices) (Zip code)

Lawrence G. Altadonna — 1633 Broadway, New York, New York 10019

(Name and address of agent for service)

Registrant’s telephone number, including area code: 212-739-3371

Date of fiscal year end: October 31, 2013

Date of reporting period: April 30, 2013

ITEM1. REPORT TO SHAREHOLDERS

Semiannual Report

April 30, 2013

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series C, M, R, TE

Contents

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 1 | |

Hans W. Kertess

Chairman

Brian S. Shlissel

President & CEO

Dear Shareholder:

The US economy expanded during the six-month fiscal reporting period ended April 30, 2013. However, growth was uneven and unemployment remained a concern. Despite this, many US stock market indices reached record highs and lower rated corporate bonds produced strong results.

Six Months in Review

For the six-month fiscal reporting period ended April 30, 2013:

| • | | Fixed Income SHares: Series C returned 4.81% prior to the deduction of fees. |

| • | | Fixed Income SHares: Series M returned 3.56% prior to the deduction of fees. |

| • | | Fixed Income SHares: Series R returned 1.96% prior to the deduction of fees. |

| • | | Fixed Income SHares: Series TE returned 2.57% prior to the deduction of fees. |

The US economy continued to grow during the fiscal six-month reporting period, but the pace of the expansion was far from robust. Gross domestic product (“GDP”), the value of goods and services produced in the country, the broadest measure of US economic activity and the principal indicator of economic performance, grew at an annual pace of 0.4% during the fourth quarter of 2012 and accelerated to an annual rate of 2.5% (preliminary estimate) during the first quarter of 2013.

The Federal Reserve (the “Fed”) took a number of actions to support the economy and reduce unemployment. In September 2012, prior to the beginning of the fiscal reporting period, the Fed introduced a third round of “quantitative easing” which entailed the purchase of $40 billion of mortgage securities each month. Toward the end of 2012, the Fed revealed that it would continue the purchase of $40 billion mortgage securities each month, in addition to purchasing $45 billion per month of longer-term Treasuries on an open-ended basis. At its meeting in December, the Fed said that it expected to keep the Fed Funds rate in the 0.0% to 0.25% range “…as long as the unemployment rate remains above 6.5%,” provided that inflation remains well contained.

Yields on US Treasury bonds trended lower during the six-months ended April 30, 2013. The benchmark ten-year Treasury bond commenced the fiscal period yielding 1.72% and ended the period at 1.70%. Continued low yields reflected a variety of concerns, including Europe’s ongoing sovereign debt crisis, uncertainties regarding fiscal policy and decelerating global economic growth.

| | | | |

| 2 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Outlook

Recent US economic data has generally been weaker than anticipated, leading to concerns of another spring/summer slowdown. At the conclusion of its meeting in March 2013, the Fed stated that it was seeing “a return to moderate economic growth following a pause late last year.” However, the Fed also acknowledged that “fiscal

policy is restraining economic growth.” Whether the economy is currently experiencing a temporary “soft patch” or larger setback remains to be seen. Given this uncertainty and continued high unemployment, we expect the Fed will maintain an accommodative monetary stance.

Concerns related to the European sovereign debt crisis reemerged during the reporting period amid inconclusive election results in Italy and a banking crisis in Cyprus. In addition, austerity measures remain a headwind for European Union countries. Elsewhere, while growth in China has decelerated, a “soft landing” for China’s economy looks likely.

Together with Allianz Global Investors Fund Management LLC, the Portfolios’ investment manager, and Pacific Investment Management Company LLC, the Portfolios’ sub-adviser, we thank you for investing with us.

We remain dedicated to serving your investment needs.

Sincerely,

| | |

| |  |

Hans W. Kertess Chairman of the Board of Trustees | | Brian S. Shlissel President & Chief Executive Officer |

Receive this report electronically and eliminate paper mailings. To enroll, go to us.allianzgi.com/edelivery.

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 3 | |

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series C, M, R, TE

Important Information

April 30, 2013 (unaudited)

In an economic environment where interest rates may trend upward, rising rates will negatively impact the performance of most bond funds and fixed income securities held by a fund and are likely to cause these instruments to decrease in value. Bond funds and individual bonds with a longer duration (a measure of the expected life of a security) tend to be more sensitive to changes in interest rates, usually making them more volatile than securities with shorter durations.

Fixed Income SHares: Series C, M, R and TE (the “Portfolios”) may be subject to various risks as described in their prospectuses. The risk associated with one or more Portfolios may include, but are not limited to, the following: derivatives risk, foreign (non-U.S.) investment risk, high yield risk, credit risk and issuer non-diversification risk. The Portfolios may use derivative instruments for hedging purposes or as part of an investment strategy. Use of these instruments may involve certain costs and risks, such as liquidity risk, leverage risk, market risk, credit risk, management risk and the risk that a Portfolio could not close out a position when it would be most advantageous to do so. Portfolios investing in derivatives could lose more than the principal amount invested in these instruments. Investing in non-U.S. securities may entail risk due to non-U.S. economic, political and other developments. This risk may be enhanced when a Portfolio invests in emerging markets. High-yield bonds typically have a lower credit rating than other bonds. Lower rated bonds generally involve a greater risk to principal than higher rated bonds. Concentrating investments in individual sectors may add additional risk and volatility compared to a diversified Portfolio. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall Portfolio.

Allianz Global Investors Fund Management LLC (the “Investment Manager”) serves as the Portfolios’ Investment Manager and Pacific Investment Management Company LLC (“PIMCO” or the “Sub-Adviser”) serves as the sub-adviser. The Portfolios’ Investment Manager and Sub-Adviser have adopted written proxy voting policies and procedures (the “Proxy Policy”) as required by Rule 206(4)-6 under the Investment Advisers Act of 1940, as amended. The Proxy Policy has been adopted by the Portfolios as the policies and procedures that the Sub-Adviser will use when voting proxies on behalf of the Portfolios. Copies of the written Proxy Policy and the factors that the Sub-Adviser may consider in determining how to vote proxies for each Portfolio, and information about how each Portfolio voted proxies relating to portfolio securities held during the most recent twelve-month period ended June 30, are available without charge, upon request, by calling the Portfolios’ shareholder servicing agent at (800) 628-1237, on the Allianz Global Investors Distributors’ website at us.allianzgi.com and on the Securities and Exchange Commission’s (the “SEC”) website at http://www.sec.gov.

Past performance is no guarantee of future results. Total return is calculated by subtracting the value of an investment in each Portfolio at the beginning of each specified period from its value at the end of the period and dividing the remainder by the value of the investment at the beginning of the period and expressing the result as a percentage. The calculation assumes that all income dividends and capital gain distributions, if any, have been reinvested. Total return does not reflect broker commissions or “wrap fee” charges. Total return for a period of more than one year represents the average annual total return during the period. Total return for a period of less than one year is not annualized.

An investment in the Portfolios involves risk, including the loss of principal. Total return, distribution yield, net asset value and duration will fluctuate with changes in market conditions. The following data is provided for informational purposes only and is not intended for trading purposes. Net asset value is equal to total assets less total liabilities divided by the number of shares outstanding. The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

This report, including the financial information herein, is transmitted to the shareholders of AllianzGI Managed Accounts Trust for their information. It is not a prospectus, circular or representation intended for use in the purchase of shares of the Portfolios or any other securities mentioned in this report.

| | | | |

| 4 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series C Portfolio Insights

April 30, 2013 (unaudited)

| | | | |

| Symbol: | | Primary Investments: | | Inception Date: |

| FXICX | | Intermediate maturity fixed income securities. | | 3/17/00 |

| | |

| | | | Net Assets: |

| | | | $3.9 billion |

| | |

| | | | Portfolio Managers: |

| | | | Curtis Mewbourne |

Portfolio Commentary, Performance Statistics & Drivers

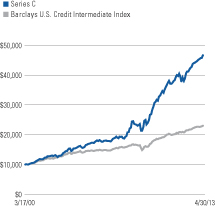

For the six months ended April 30, 2013, Series C returned 4.81%, prior to the deduction of fees, outperforming the unmanaged Barclays US Credit Intermediate Index (the “benchmark index”), which returned 1.68% during the reporting period.

Non-US interest rate exposure, particularly to Canada, enhanced Series C’s performance, as yields declined during the reporting period. A modest exposure to non-agency mortgage-backed securities (“MBS”), which are not guaranteed by the government, contributed to performance as the sector was positively impacted by generally strong demand and improvements in the housing market. Exposure to high yield corporate bonds was additive to performance due to strong demand from investors looking to generate incremental yield in the low interest rate environment. An allocation to emerging market debt was rewarded as this asset class outperformed similar duration Treasuries. Specifically, Mexican local rates enhanced returns as yields fell in this country. Exposure to select currencies, such as the Brazilian real and Mexican peso, enhanced returns as these currencies rallied versus the US dollar. Elsewhere, an overweighting to US duration did not meaningfully impact performance, as the 10-year US Treasury yield fell only modestly during the six-month reporting period. However, the yield curve steepening by nine basis points was beneficial for performance during the reporting period.

An overall underweighting to corporate bonds negatively impacted performance, as investors continued to seek higher yielding sectors due to continued low rates.

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 5 | |

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series M Portfolio Insights

April 30, 2013 (unaudited)

| | | | |

| Symbol: | | Primary Investments: | | Inception Date: |

| FXIMX | | Intermediate maturity mortgage-backed securities. | | 3/17/00 |

| | |

| | | | Net Assets: |

| | | | $3.9 billion |

| | |

| | | | Portfolio Managers: |

| | | | Curtis Mewbourne |

Portfolio Commentary, Performance Statistics & Drivers

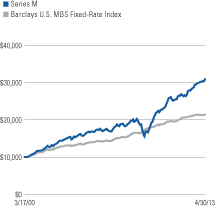

For the six months ended April 30, 2013, Series M returned 3.56%, prior to the deduction of fees, outperforming the unmanaged Barclays US MBS Fixed-Rate Index (the “benchmark index”), which returned 0.45% during the reporting period.

An overweighting to US duration contributed positively to performance. The 10-year US Treasury yield fell two basis points during the six-month reporting period. Non-US interest rate exposure, particularly in Italy, also enhanced performance, as yields in the country declined during the reporting period. An underweighting to agency mortgage-backed securities (“MBS”) was beneficial as MBS lagged similar duration Treasuries. An allocation to commercial mortgage-backed securities was additive, due to robust demand from investors looking to generate incremental yield. Non-agency MBS, which are not guaranteed by the government, contributed to performance as the sector was positively impacted by solid demand and improvements in the housing market. Investment-grade corporate financials enhanced performance given their strong earnings and continued balance sheet strengthening. An allocation to Build America Bonds (BABs) added to returns as these securities outperformed the benchmark index during the period. Currency strategies, designed to benefit from a depreciation of the Japanese yen, were positive for performance as the yen depreciated versus the US dollar during the reporting period.

There were no meaningful detractors from performance during the reporting period.

| | | | |

| 6 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series R Portfolio Insights

April 30, 2013 (unaudited)

| | | | |

| Symbol: | | Primary Investments: | | Inception Date: |

| FXIRX | | Inflation-indexed fixed income securities. | | 4/15/04 |

| | |

| | | | Net Assets: |

| | | | $591.2 million |

| | |

| | | | Portfolio Manager: |

| | | | Mihir Worah |

Portfolio Commentary, Performance Statistics & Drivers

For the six months ended April 30, 2013, Series R returned 1.96%, prior to the deduction of fees, outperforming the unmanaged Barclays US TIPS Index (the “benchmark index”), which returned 0.25% during the reporting period.

An underweighting to shorter maturity real rates in the US in favor of nominal rates was positive for performance, as short-term breakeven inflation levels narrowed during the reporting period. Exposure to real rates in the U.K. also contributed to performance. Breakeven inflations levels widened during the period and real yields rallied in response to the decision to leave the U.K.’s retail price index calculation unchanged. Tactical exposure to rates in core Europe, namely France and Italy, as well as in Mexico, added to returns as yields fell in these countries during the reporting period. Exposure to non-agency mortgage-backed securities (“MBS”), which are not guaranteed by the government, contributed to performance as the sector was positively impacted by generally strong demand and improvements in the housing market. An overall allocation to investment-grade corporate financials positively impacted performance due to strong earnings and continued balance sheet strengthening.

Strategies designed to benefit from a decline in the euro detracted from performance as the euro appreciated versus the US dollar. However, this was more than offset by an exposure to a basket of emerging market currencies, namely the Mexican peso and Brazilian real, as these currencies appreciated versus the US dollar during the six-month reporting period.

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 7 | |

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series TE Portfolio Insights

April 30, 2013 (unaudited)

| | | | |

| Symbol: | | Primary Investments: | | Inception Date: |

| FXIEX | | High yield municipal securities | | 6/26/12 |

| | |

| | | | Net Assets: |

| | | | $39.8 million |

| | |

| | | | Portfolio Managers: |

| | | | Joseph Deane |

| | | | Julie Callahan |

Portfolio Commentary, Performance Statistics & Drivers

For the six months ended April 30, 2013, Series TE returned 2.57%, prior to the deduction of fees, outperforming the unmanaged Barclays Municipal Bond 1-Year Index (the “benchmark index”), which returned 0.40% during the reporting period.

An overweighting to US duration contributed to Series TE’s performance as municipal yields fell across the curve. An emphasis on revenue bonds versus general obligation bonds was positive for performance as revenue bonds outperformed general obligation securities during the reporting period. An overweighting to industrial revenue and transportation bonds contributed to returns as these sectors outperformed the broader municipal market. Elsewhere, a short Treasury futures position contributed to returns during the period.

An underweighting to the Tobacco sector detracted from performance, as this higher yielding portion of the municipal market outperformed the benchmark index during the reporting period. An underweighting to pre-refunded securities was also a drag on performance.

| | | | |

| 8 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series C Performance & Statistics

April 30, 2013 (unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Total Returns (Period ended 4/30/13) | | Six Months | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception

(3/17/00) | |

Series C | | | 4.81% | | | | 11.52% | | | | 14.79% | | | | 12.06% | | | | 12.45% | |

Barclays U.S. Credit Intermediate Index | | | 1.68% | | | | 5.99% | | | | 6.70% | | | | 5.36% | | | | 6.53% | |

Change in Value of $10,000 Investments in Series C and the Barclays U.S. Credit Intermediate Index

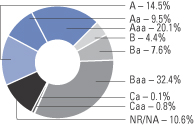

Moody’s Ratings

(as a % of total investments,

before options written and securities sold short)

Past performance is no guarantee of future results. Returns presented do not reflect the deduction of taxes that a shareholder would pay on fund distribution or the redemption of fund shares.

| | | | |

Shareholder Expense Example | | Actual | | Hypothetical |

| | | | | (5% return before expenses) |

Beginning Account Value (11/1/12) | | $1,000.00 | | $1,000.00 |

Ending Account Value (4/30/13) | | $1,048.10 | | $1,024.79 |

Expenses Paid During Period | | $0.00 | | $0.00 |

Expenses are equal to the annualized expense ratio of 0.0003%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 9 | |

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series M Performance & Statistics

April 30, 2013 (unaudited)

| | | | | | | | | | | | | | | | | | | | |

| Total Returns (Period ended 4/30/13) | | Six Months | | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Inception

(3/17/00) | |

Series M | | | 3.56% | | | | 9.46% | | | | 8.85% | | | | 7.37% | | | | 8.99% | |

Barclays U.S. MBS Fixed-Rate Index | | | 0.45% | | | | 1.86% | | | | 5.30% | | | | 5.02% | | | | 5.97% | |

Change in Value of $10,000 Investments in Series M and the Barclays U.S. MBS Fixed-Rate Index

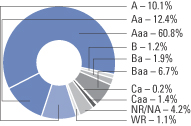

Moody’s Ratings

(as a % of total investments,

before options written)

Past performance is no guarantee of future results. Returns presented do not reflect the deduction of taxes that a shareholder would pay on fund distribution or the redemption of fund shares.

| | | | |

Shareholder Expense Example | | Actual | | Hypothetical |

| | | | | (5% return before expenses) |

Beginning Account Value (11/1/12) | | $1,000.00 | | $1,000.00 |

Ending Account Value (4/30/13) | | $1,035.60 | | $1,024.79 |

Expenses Paid During Period | | $0.01 | | $0.01 |

Expenses are equal to the annualized expense ratio of 0.001%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

| | | | |

| 10 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

AllianzGI Managed Accounts Trust

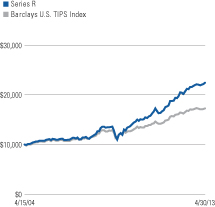

Fixed Income SHares: Series R Performance & Statistics

April 30, 2013 (unaudited)

| | | | | | | | | | | | | | | | |

| Total Returns (Period ended 4/30/13) | | Six Months | | | 1 Year | | | 5 Years | | | Since

Inception

(4/15/04) | |

Series R | | | 1.96% | | | | 8.00% | | | | 10.82% | | | | 9.36% | |

Barclays U.S. TIPS Index | | | 0.25% | | | | 4.41% | | | | 6.51% | | | | 6.29% | |

Change in Value of $10,000 Investments in Series R and the Barclays U.S. TIPS Index

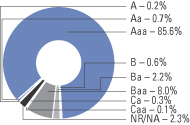

Moody’s Ratings

(as a % of total investments,

before options written)

Past performance is no guarantee of future results. Returns presented do not reflect the deduction of taxes that a shareholder would pay on fund distribution or the redemption of fund shares.

| | | | |

Shareholder Expense Example | | Actual | | Hypothetical |

| | | | | (5% return before expenses) |

Beginning Account Value (11/1/12) | | $1,000.00 | | $1,000.00 |

Ending Account Value (4/30/13) | | $1,019.60 | | $1,024.50 |

Expenses Paid During Period | | $0.30 | | $0.30 |

Expenses are equal to the annualized expense ratio of 0.06%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 11 | |

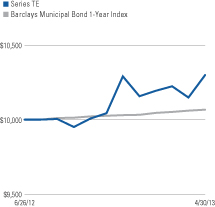

AllianzGI Managed Accounts Trust

Fixed Income SHares: Series TE Performance & Statistics

April 30, 2013 (unaudited)

| | | | | | | | |

| Total Returns (Period ended 4/30/13) | | Six Months | | | Since

Inception

(6/26/12) | |

Series TE | | | 2.57% | | | | 3.01% | |

Barclays Municipal Bond 1-Year Index | | | 0.40% | | | | 0.65% | |

Change in Value of $10,000 Investments in Series TE and the Barclays Municipal Bond 1-Year Index

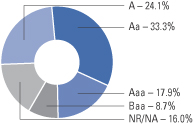

Moody’s Ratings

(as a % of total investments)

Past performance is no guarantee of future results. Returns presented do not reflect the deduction of taxes that a shareholder would pay on fund distribution or the redemption of fund shares.

| | | | |

Shareholder Expense Example | | Actual | | Hypothetical |

| | | | | (5% return before expenses) |

Beginning Account Value (11/1/12) | | $1,000.00 | | $1,000.00 |

Ending Account Value (4/30/13) | | $1,025.70 | | $1,024.78 |

Expenses Paid During Period | | $0.01 | | $0.01 |

Expenses are equal to the annualized expense ratio of 0.002%, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

| | | | |

| 12 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

AllianzGI Managed Accounts Trust

Benchmark Descriptions

April 30, 2013 (unaudited)

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

| • | | Barclays Municipal Bond 1-Year Index |

The Barclays Municipal Bond 1-Year Index is an unmanaged index comprised of national municipal bond issues having a maturity of at least one year and less than two years.

| • | | Barclays US Credit Intermediate Index |

The Barclays US Credit Intermediate Index is an unmanaged index of publicly issued US corporate and specified foreign debentures and secured notes with intermediate maturities ranging from 1 to 10 years. Securities must also meet specific liquidity and quality requirements.

| • | | Barclays US MBS Fixed-Rate Index |

The Barclays US MBS Fixed-Rate Index is an unmanaged index comprised of fixed rate mortgage pass through securities issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC), with a Weighted Average Maturity (WAM) of at least one year and at least $250 million par outstanding.

| • | | Barclays U.S. TIPS Index |

The Barclays US TIPS Index is an unmanaged market index comprised of all US Treasury Inflation Protected Securities rated investment grade (Baa3 or better), having at least one year to final maturity, and at least $250 million par amount outstanding. Performance data for this index prior to October 1997 represents returns of the Barclays Inflation Notes Index.

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 13 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| CORPORATE BONDS & NOTES–53.7% | | | | |

| | | | Airlines–1.2% | | | | | | |

| $ | 82 | | | American Airlines Pass-Through Trust, 10.375%, 1/2/21 | | | | $ | 86,340 | |

| | 3,000 | | | Continental Airlines Pass-Through Trust, 4.00%, 4/29/26 | | | | | 3,157,500 | |

| | | | Northwest Airlines, Inc., | | | | | | |

| | 1,335 | | | 7.041%, 10/1/23 | | | | | 1,485,213 | |

| | 37,547 | | | 7.15%, 4/1/21 (MBIA) | | | | | 41,114,280 | |

| | 46 | | | United Air Lines Pass-Through Trust, 10.125%, 3/22/15 (b)(f) | | | | | 28,958 | |

| | | | | | | | | | |

| | | | | | | | | 45,872,291 | |

| | | | | | | | | | |

| | | |

| | | | Auto Manufacturers–0.2% | | | | | | |

| | 9,100 | | | Volkswagen International Finance NV, 4.00%, 8/12/20 (a)(d) | | | | | 10,146,919 | |

| | | | | | | | | | |

| | | |

| | | | Banking–15.2% | | | | | | |

| | 16,200 | | | Abbey National Treasury Services PLC, 1.856%, 4/25/14 (m) | | | | | 16,321,824 | |

| | | | Ally Financial, Inc., | | | | | | |

| | 21,075 | | | 3.68%, 6/20/14 (m) | | | | | 21,601,243 | |

| | 800 | | | 4.625%, 6/26/15 | | | | | 843,433 | |

| | 14,486 | | | 7.50%, 9/15/20 | | | | | 17,944,533 | |

| | 28,969 | | | 8.00%, 3/15/20 | | | | | 36,573,362 | |

| | 25,200 | | | Banco do Brasil S.A., 4.50%, 1/22/15 (a)(d) | | | | | 26,460,000 | |

| | | | Banco Santander Brasil S.A., | | | | | | |

| | 30,200 | | | 2.38%, 3/18/14 (a)(d)(m) | | | | | 30,134,557 | |

| | 3,500 | | | 4.50%, 4/6/15 (a)(d) | | | | | 3,671,500 | |

| | 1,000 | | | 4.50%, 4/6/15 | | | | | 1,049,000 | |

| | | | Bank of America Corp., | | | | | | |

| | 1,000 | | | 5.625%, 7/1/20 | | | | | 1,188,687 | |

| | 3,800 | | | 5.65%, 5/1/18 | | | | | 4,416,675 | |

| | 4,300 | | | 5.75%, 12/1/17 | | | | | 5,003,798 | |

| | 2,715 | | | 6.00%, 9/1/17 | | | | | 3,160,423 | |

| £ | 3,300 | | | Barclays Bank PLC, 14.00%, 6/15/19 (h) | | | | | 7,127,163 | |

| $ | 8,236 | | | BNP Paribas S.A., 5.00%, 1/15/21 | | | | | 9,459,515 | |

| | 23,900 | | | BPCE S.A., 2.046%, 2/7/14 (a)(d)(m) | | | | | 24,151,213 | |

| | | | Citigroup, Inc., | | | | | | |

| | 12,350 | | | 4.75%, 5/19/15 | | | | | 13,272,841 | |

| | 700 | | | 5.50%, 10/15/14 | | | | | 745,901 | |

| | 11,718 | | | 6.00%, 8/15/17 | | | | | 13,806,112 | |

| | 13,500 | | | 6.125%, 11/21/17 | | | | | 16,071,534 | |

| | 20,000 | | | Cooperatieve Centrale Raiffeisen-Boerenleenbank BA, 11.00%, 6/30/19 (a)(d)(h) | | | | | 27,019,440 | |

| | | | Goldman Sachs Group, Inc., | | | | | | |

| € | 10,000 | | | 0.57%, 5/23/16 (m) | | | | | 12,944,583 | |

| $ | 15,200 | | | 6.15%, 4/1/18 | | | | | 17,979,320 | |

| | | | |

| 14 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Banking (continued) | | | | | | |

| $ | 5,000 | | | HBOS Capital Funding L.P., 6.071%, 6/30/14 (a)(d)(h) | | | | $ | 4,631,250 | |

| | 30,600 | | | HBOS PLC, 6.75%, 5/21/18 (a)(d) | | | | | 34,305,017 | |

| | | | HSBC Capital Funding L.P. (a)(d)(h), | | | | | | |

| | 13,900 | | | 4.61%, 6/27/13 | | | | | 13,894,079 | |

| | 1,350 | | | 10.176%, 6/30/30 (b)(l) (acquisition cost–$1,545,528; purchased 5/30/02-10/10/08) | | | | | 1,960,875 | |

| | | | HSBC Holdings PLC, | | | | | | |

| | 700 | | | 6.50%, 5/2/36 | | | | | 885,322 | |

| | 400 | | | 7.625%, 5/17/32 | | | | | 562,952 | |

| | | | ICICI Bank Ltd., | | | | | | |

| | 5,900 | | | 4.75%, 11/25/16 (a)(d) | | | | | 6,355,905 | |

| | 2,500 | | | 5.00%, 1/15/16 | | | | | 2,684,008 | |

| | 700 | | | 5.50%, 3/25/15 | | | | | 743,476 | |

| | 14,800 | | | JPMorgan Chase & Co., 6.00%, 1/15/18 | | | | | 17,661,846 | |

| | 900 | | | Korea Exchange Bank, 4.875%, 1/14/16 | | | | | 980,332 | |

| | | | LBG Capital No. 1 PLC, | | | | | | |

| € | 2,825 | | | 7.375%, 3/12/20 | | | | | 3,878,687 | |

| £ | 9,552 | | | 7.588%, 5/12/20 | | | | | 15,802,041 | |

| | 1,000 | | | 7.869%, 8/25/20 | | | | | 1,667,521 | |

| $ | 3,400 | | | 7.875%, 11/1/20 (a)(b)(d)(l) (acquisition cost–$2,788,000; purchased 12/7/09) | | | | | 3,746,800 | |

| | 22,200 | | | 8.50%, 12/17/21 (a)(d)(h) | | | | | 23,833,987 | |

| | | | LBG Capital No. 2 PLC, | | | | | | |

| £ | 2,331 | | | 9.00%, 12/15/19 | | | | | 4,038,307 | |

| | 4,500 | | | 9.334%, 2/7/20 | | | | | 7,877,758 | |

| € | 2,180 | | | 15.00%, 12/21/19 | | | | | 4,213,122 | |

| $ | 29,300 | | | Lloyds TSB Bank PLC, 12.00%, 12/16/24 (a)(d)(h) | | | | | 39,921,250 | |

| | | | Morgan Stanley, | | | | | | |

| € | 10,000 | | | 0.63%, 1/16/17 (m) | | | | | 12,801,220 | |

| $ | 2,800 | | | 5.375%, 10/15/15 | | | | | 3,058,885 | |

| € | 5,000 | | | 5.375%, 8/10/20 | | | | | 7,875,673 | |

| $ | 900 | | | 5.95%, 12/28/17 | | | | | 1,051,452 | |

| | 3,700 | | | 6.625%, 4/1/18 | | | | | 4,440,744 | |

| | 2,400 | | | RBS Capital Trust I, 4.709%, 7/1/13 (h) | | | | | 1,974,000 | |

| | | | Royal Bank of Scotland Group PLC, | | | | | | |

| | 273 | | | 5.00%, 11/12/13 | | | | | 277,846 | |

| | 22,200 | | | 6.99%, 10/5/17 (a)(b)(d)(h)(l) (acquisition cost–$22,553,947; purchased 10/25/07-10/26/07) | | | | | 21,978,000 | |

| | 5,000 | | | 7.648%, 9/30/31 (h) | | | | | 5,275,000 | |

| | | | RSHB Capital S.A. for OJSC Russian Agricultural Bank, | | | | | | |

| | 500 | | | 7.125%, 1/14/14 | | | | | 520,550 | |

| | 1,500 | | | 9.00%, 6/11/14 (a)(d) | | | | | 1,622,025 | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 15 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Banking (continued) | | | | | | |

| | | | State Bank of India, | | | | | | |

| $ | 1,300 | | | 4.50%, 10/23/14 | | | | $ | 1,352,568 | |

| | 1,000 | | | 4.50%, 7/27/15 (a)(d) | | | | | 1,053,962 | |

| | | | UBS AG, | | | | | | |

| | 250 | | | 4.875%, 8/4/20 | | | | | 292,988 | |

| | 582 | | | 5.875%, 12/20/17 | | | | | 693,439 | |

| | 6,700 | | | USB Capital IX, 3.50%, 5/31/13 (h) | | | | | 6,298,000 | |

| | 2,050 | | | Wachovia Corp., 5.75%, 2/1/18 | | | | | 2,449,475 | |

| | 19,217 | | | Wells Fargo & Co., 7.98%, 3/15/18 (h) | | | | | 22,303,731 | |

| | | | | | | | | | |

| | | | | | | | | 595,910,750 | |

| | | | | | | | | | |

| | | |

| | | | Biotechnology–0.1% | | | | | | |

| | 1,700 | | | Amgen, Inc., 5.70%, 2/1/19 | | | | | 2,047,772 | |

| | | | | | | | | | |

| | | |

| | | | Computers–0.1% | | | | | | |

| | 1,800 | | | International Business Machines Corp., 8.375%, 11/1/19 | | | | | 2,515,484 | |

| | | | | | | | | | |

| | | |

| | | | Diversified Financial Services–12.4% | | | | | | |

| | 11,000 | | | American Express Co., 7.25%, 5/20/14 | | | | | 11,765,347 | |

| | | | Bear Stearns Cos. LLC, | | | | | | |

| | 1,500 | | | 5.30%, 10/30/15 | | | | | 1,655,751 | |

| | 17,265 | | | 7.25%, 2/1/18 | | | | | 21,524,017 | |

| | 5,700 | | | Caterpillar Financial Services Corp., 7.15%, 2/15/19 | | | | | 7,392,695 | |

| | | | Ford Motor Credit Co. LLC, | | | | | | |

| | 49,300 | | | 5.625%, 9/15/15 | | | | | 53,927,051 | |

| | 2,000 | | | 5.875%, 8/2/21 | | | | | 2,337,916 | |

| | 16,900 | | | 7.00%, 10/1/13 | | | | | 17,349,760 | |

| | 20,750 | | | 8.00%, 6/1/14 | | | | | 22,245,390 | |

| | 7,900 | | | 8.00%, 12/15/16 | | | | | 9,529,099 | |

| | 22,700 | | | 8.125%, 1/15/20 | | | | | 29,298,459 | |

| | 3,400 | | | 8.70%, 10/1/14 | | | | | 3,763,491 | |

| | | | General Electric Capital Corp., | | | | | | |

| € | 10,000 | | | 4.625%, 9/15/66 (converts to FRN on 9/15/16) (a)(d) | | | | | 13,314,106 | |

| | 19,100 | | | 5.50%, 9/15/67 (converts to FRN on 9/15/17) (k) | | | | | 26,454,731 | |

| $ | 5,000 | | | 6.15%, 8/7/37 | | | | | 6,236,680 | |

| £ | 1,400 | | | 6.50%, 9/15/67 (converts to FRN on 9/15/17) | | | | | 2,315,884 | |

| $ | 2,000 | | | HSBC Finance Corp., 0.717%, 6/1/16 (m) | | | | | 1,981,556 | |

| | | | International Lease Finance Corp. (a)(d), | | | | | | |

| | 4,000 | | | 6.75%, 9/1/16 | | | | | 4,570,000 | |

| | 3,000 | | | 7.125%, 9/1/18 | | | | | 3,585,000 | |

| | 1,000 | | | Majapahit Holding BV, 7.25%, 6/28/17 | | | | | 1,171,250 | |

| | | | |

| 16 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Diversified Financial Services (continued) | | | | | | |

| | | | Merrill Lynch & Co., Inc., | | | | | | |

| $ | 500 | | | 5.00%, 1/15/15 | | | | $ | 531,904 | |

| | 22,700 | | | 6.40%, 8/28/17 | | | | | 26,739,510 | |

| | 99,300 | | | 6.875%, 4/25/18 | | | | | 120,859,420 | |

| £ | 550 | | | MUFG Capital Finance Ltd., 6.299%, 1/25/17 (h) | | | | | 946,184 | |

| $ | 515 | | | Preferred Term Securities XIII Ltd., 0.83%, 3/24/34 (a)(b)(d)(l)(m) (acquisition cost–$515,073; purchased 3/9/04) | | | | | 399,503 | |

| | 500 | | | QNB Finance Ltd., 3.125%, 11/16/15 | | | | | 521,375 | |

| | | | SLM Corp., | | | | | | |

| € | 2,950 | | | 0.533%, 6/17/13 (m) | | | | | 3,888,341 | |

| $ | 750 | | | 5.00%, 10/1/13 | | | | | 763,125 | |

| | 400 | | | 5.375%, 5/15/14 | | | | | 417,120 | |

| | 1,400 | | | 5.50%, 1/25/23 | | | | | 1,408,599 | |

| | 36,000 | | | 6.25%, 1/25/16 | | | | | 39,285,000 | |

| | 17,700 | | | 7.25%, 1/25/22 | | | | | 19,779,750 | |

| | 1,100 | | | 8.00%, 3/25/20 | | | | | 1,275,759 | |

| | 24,455 | | | 8.45%, 6/15/18 | | | | | 28,841,518 | |

| | | | | | | | | | |

| | | | | | | | | 486,075,291 | |

| | | | | | | | | | |

| | | |

| | | | Electric Utilities–2.5% | | | | | | |

| | 2,497 | | | Bruce Mansfield Unit, 6.85%, 6/1/34 | | | | | 2,776,714 | |

| | 2,000 | | | Consumers Energy Co., 5.15%, 2/15/17 | | | | | 2,299,240 | |

| | 5,000 | | | DTE Energy Co., 6.35%, 6/1/16 | | | | | 5,788,405 | |

| | 14,200 | | | Electricite de France S.A., 6.50%, 1/26/19 (a)(d) | | | | | 17,462,350 | |

| | 27,500 | | | Entergy Corp., 3.625%, 9/15/15 | | | | | 28,699,000 | |

| | 5,700 | | | FirstEnergy Corp., 7.375%, 11/15/31 | | | | | 6,843,295 | |

| | 99 | | | GG1C Funding Corp., 5.129%, 1/15/14 (a)(b)(d)(l) (acquisition cost–$98,616; purchased 4/16/04) | | | | | 99,526 | |

| | | | Korea Hydro & Nuclear Power Co., Ltd., | | | | | | |

| | 300 | | | 3.125%, 9/16/15 (a)(d) | | | | | 312,688 | |

| | 4,550 | | | 6.25%, 6/17/14 | | | | | 4,805,569 | |

| | | | Nevada Power Co., | | | | | | |

| | 100 | | | 5.875%, 1/15/15 | | | | | 108,576 | |

| | 1,600 | | | 5.95%, 3/15/16 | | | | | 1,816,760 | |

| | 3,000 | | | 6.50%, 5/15/18 | | | | | 3,719,469 | |

| | 900 | | | Nisource Finance Corp., 6.40%, 3/15/18 | | | | | 1,089,672 | |

| | 6,100 | | | NRG Energy, Inc., 7.625%, 1/15/18 | | | | | 7,098,875 | |

| | 1,700 | | | Ohio Edison Co., 5.45%, 5/1/15 | | | | | 1,854,821 | |

| | 2,900 | | | Public Service Co. of Oklahoma, 6.15%, 8/1/16 | | | | | 3,322,121 | |

| | 1,900 | | | Sierra Pacific Power Co., 6.00%, 5/15/16 | | | | | 2,191,593 | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 17 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Electric Utilities (continued) | | | | | | |

| | | | Teco Finance, Inc., | | | | | | |

| $ | 983 | | | 6.572%, 11/1/17 | | | | $ | 1,184,607 | |

| | 2,000 | | | 6.75%, 5/1/15 | | | | | 2,199,894 | |

| | 4,500 | | | Toledo Edison Co., 6.15%, 5/15/37 | | | | | 5,724,486 | |

| | 48 | | | W3A Funding Corp., 8.09%, 1/2/17 | | | | | 50,012 | |

| | | | | | | | | | |

| | | | | | | | | 99,447,673 | |

| | | | | | | | | | |

| | | |

| | | | Food & Beverage–0.2% | | | | | | |

| | 6,700 | | | Mondelez International, Inc., 6.50%, 8/11/17 | | | | | 8,096,240 | |

| | 1,100 | | | Tate & Lyle International Finance PLC, 6.625%, 6/15/16 (a)(b)(d)(l) (acquisition cost–$957,637; purchased 3/12/09) | | | | | 1,244,638 | |

| | | | | | | | | | |

| | | | | | | | | 9,340,878 | |

| | | | | | | | | | |

| | | |

| | | | Healthcare-Products–0.0% | | | | | | |

| | 1,700 | | | Hospira, Inc., 6.05%, 3/30/17 | | | | | 1,936,873 | |

| | | | | | | | | | |

| | | |

| | | | Healthcare-Services–0.2% | | | | | | |

| | | | HCA, Inc., | | | | | | |

| | 3,200 | | | 7.25%, 9/15/20 | | | | | 3,556,000 | |

| | 4,000 | | | 7.875%, 2/15/20 | | | | | 4,445,000 | |

| | | | | | | | | | |

| | | | | | | | | 8,001,000 | |

| | | | | | | | | | |

| | | |

| | | | Holding Companies-Diversified–0.2% | | | | | | |

| | | | Hutchison Whampoa International Ltd., | | | | | | |

| | 100 | | | 5.75%, 9/11/19 | | | | | 119,317 | |

| | 1,000 | | | 7.625%, 4/9/19 | | | | | 1,290,666 | |

| | 6,300 | | | Sinochem Overseas Capital Co., Ltd., 4.50%, 11/12/20 (a)(d) | | | | | 6,953,549 | |

| | | | | | | | | | |

| | | | | | | | | 8,363,532 | |

| | | | | | | | | | |

| | | |

| | | | Insurance–4.4% | | | | | | |

| | | | American International Group, Inc., | | | | | | |

| | 3,000 | | | 4.875%, 6/1/22 | | | | | 3,462,597 | |

| | 4,600 | | | 5.05%, 10/1/15 | | | | | 5,036,765 | |

| | 2,000 | | | 5.45%, 5/18/17 | | | | | 2,293,756 | |

| | 900 | | | 5.60%, 10/18/16 | | | | | 1,025,845 | |

| | 30,600 | | | 5.85%, 1/16/18 | | | | | 35,972,779 | |

| | 17,200 | | | 6.25%, 5/1/36 | | | | | 22,234,560 | |

| £ | 1,456 | | | 6.765%, 11/15/17 | | | | | 2,728,302 | |

| € | 5,557 | | | 6.797%, 11/15/17 | | | | | 8,928,458 | |

| $ | 70,000 | | | 8.25%, 8/15/18 | | | | | 90,986,420 | |

| | | | | | | | | | |

| | | | | | | | | 172,669,482 | |

| | | | | | | | | | |

| | | | |

| 18 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Iron/Steel–0.5% | | | | | | |

| $ | 200 | | | CSN Islands XI Corp., 6.875%, 9/21/19 (a)(d) | | | | $ | 220,000 | |

| | | | Gerdau Holdings, Inc., | | | | | | |

| | 11,800 | | | 7.00%, 1/20/20 (a)(d) | | | | | 13,599,500 | |

| | 3,950 | | | 7.00%, 1/20/20 | | | | | 4,552,375 | |

| | 800 | | | Gerdau Trade, Inc., 5.75%, 1/30/21 (a)(d) | | | | | 865,600 | |

| | | | | | | | | | |

| | | | | | | | | 19,237,475 | |

| | | | | | | | | | |

| | | |

| | | | Media–1.9% | | | | | | |

| | 1,000 | | | Comcast Cable Communications LLC, 7.125%, 6/15/13 | | | | | 1,008,054 | |

| | | | Comcast Corp., | | | | | | |

| | 10,600 | | | 5.875%, 2/15/18 | | | | | 12,846,659 | |

| | 1,700 | | | 5.90%, 3/15/16 | | | | | 1,944,530 | |

| | 700 | | | 6.30%, 11/15/17 | | | | | 857,714 | |

| | | | CSC Holdings LLC, | | | | | | |

| | 7,850 | | | 7.625%, 7/15/18 | | | | | 9,263,000 | |

| | 810 | | | 7.875%, 2/15/18 | | | | | 955,800 | |

| | 7,500 | | | 8.625%, 2/15/19 | | | | | 9,168,750 | |

| | | | DISH DBS Corp., | | | | | | |

| | 15,667 | | | 5.00%, 3/15/23 (a)(d) | | | | | 15,275,325 | |

| | 6,615 | | | 5.875%, 7/15/22 | | | | | 6,780,375 | |

| | 4,200 | | | 7.125%, 2/1/16 | | | | | 4,662,000 | |

| | | | Time Warner Cable, Inc., | | | | | | |

| | 6,940 | | | 5.85%, 5/1/17 | | | | | 8,105,927 | |

| | 1,500 | | | 8.25%, 4/1/19 | | | | | 1,971,072 | |

| | | | | | | | | | |

| | | | | | | | | 72,839,206 | |

| | | | | | | | | | |

| | | |

| | | | Mining–0.6% | | | | | | |

| | 5,000 | | | Gold Fields Orogen Holding BVI Ltd., 4.875%, 10/7/20 (a)(d) | | | | | 4,817,565 | |

| | 1,600 | | | Newmont Mining Corp., 5.125%, 10/1/19 | | | | | 1,811,771 | |

| | 800 | | | Teck Resources Ltd., 4.50%, 1/15/21 | | | | | 859,253 | |

| | | | Vale Overseas Ltd., | | | | | | |

| | 2,790 | | | 6.875%, 11/10/39 | | | | | 3,360,792 | |

| | 2,000 | | | 8.25%, 1/17/34 | | | | | 2,687,316 | |

| | 7,400 | | | Xstrata Finance Canada Ltd., 5.80%, 11/15/16 (a)(d) | | | | | 8,418,928 | |

| | | | | | | | | | |

| | | | | | | | | 21,955,625 | |

| | | | | | | | | | |

| | | |

| | | | Miscellaneous Manufacturing–2.6% | | | | | | |

| | 70,000 | | | General Electric Co., 5.25%, 12/6/17 | | | | | 82,624,150 | |

| | 15,000 | | | Tyco Electronics Group S.A., 6.55%, 10/1/17 | | | | | 17,986,200 | |

| | | | | | | | | | |

| | | | | | | | | 100,610,350 | |

| | | | | | | | | | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 19 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Oil & Gas–3.6% | | | | | | |

| $ | 300 | | | Anadarko Petroleum Corp., 5.95%, 9/15/16 | | | | $ | 345,233 | |

| | 1,100 | | | BP Capital Markets PLC, 3.625%, 5/8/14 | | | | | 1,134,993 | |

| | 2,400 | | | Canadian Natural Resources Ltd., 6.00%, 8/15/16 | | | | | 2,769,494 | |

| | 10,400 | | | Canadian Oil Sands Ltd., 7.75%, 5/15/19 (a)(d) | | | | | 13,159,495 | |

| | 846 | | | Devon Energy Corp., 7.95%, 4/15/32 | | | | | 1,207,405 | |

| | 1,300 | | | Devon Financing Corp. LLC, 7.875%, 9/30/31 | | | | | 1,810,882 | |

| | 1,330 | | | Ecopetrol S.A., 7.625%, 7/23/19 | | | | | 1,702,400 | |

| | | | Encana Corp., | | | | | | |

| | 2,000 | | | 5.90%, 12/1/17 | | | | | 2,362,512 | |

| | 4,700 | | | 6.50%, 8/15/34 | | | | | 5,694,271 | |

| | | | Gaz Capital S.A. for Gazprom, | | | | | | |

| | 6,500 | | | 6.212%, 11/22/16 | | | | | 7,316,400 | |

| | 1,300 | | | 6.51%, 3/7/22 | | | | | 1,522,625 | |

| | 14,000 | | | 8.146%, 4/11/18 (a)(d) | | | | | 17,220,000 | |

| | 1,800 | | | Halliburton Co., 6.15%, 9/15/19 | | | | | 2,278,751 | |

| | 1,000 | | | Novatek Finance Ltd., 5.326%, 2/3/16 (a)(d) | | | | | 1,081,250 | |

| | 500 | | | Pemex Project Funding Master Trust, 5.75%, 12/15/15 | | | | | 552,500 | |

| | | | Petrobras International Finance Co.–Pifco, | | | | | | |

| | 300 | | | 5.875%, 3/1/18 | | | | | 342,786 | |

| | 15,250 | | | 7.875%, 3/15/19 | | | | | 19,041,104 | |

| | | | Petroleos Mexicanos, | | | | | | |

| | 18,700 | | | 5.50%, 1/21/21 | | | | | 22,019,250 | |

| | 10,850 | | | 6.50%, 6/2/41 | | | | | 13,535,375 | |

| | 7,500 | | | 8.00%, 5/3/19 | | | | | 9,787,500 | |

| | 2,640 | | | Ras Laffan Liquefied Natural Gas Co., Ltd. II, 5.298%, 9/30/20 | | | | | 2,937,056 | |

| | | | Ras Laffan Liquefied Natural Gas Co., Ltd. III, | | | | | | |

| | 1,400 | | | 5.50%, 9/30/14 | | | | | 1,489,250 | |

| | 1,454 | | | 5.832%, 9/30/16 (b) | | | | | 1,574,226 | |

| | 3,000 | | | 6.75%, 9/30/19 | | | | | 3,757,500 | |

| | 1,800 | | | Reliance Holdings USA, Inc., 4.50%, 10/19/20 (b) | | | | | 1,935,880 | |

| | 4,200 | | | White Nights Finance BV for Gazprom, 10.50%, 3/25/14 | | | | | 4,554,480 | |

| | | | | | | | | | |

| | | | | | | | | 141,132,618 | |

| | | | | | | | | | |

| | | |

| | | | Paper & Forest Products–0.3% | | | | | | |

| | 9,300 | | | Georgia-Pacific LLC, 5.40%, 11/1/20 (a)(d) | | | | | 11,134,183 | |

| | | | | | | | | | |

| | | |

| | | | Pharmaceuticals–0.1% | | | | | | |

| | 3,400 | | | GlaxoSmithKline Capital, Inc., 5.65%, 5/15/18 | | | | | 4,127,383 | |

| | 1,300 | | | Pfizer, Inc., 6.20%, 3/15/19 | | | | | 1,639,296 | |

| | | | | | | | | | |

| | | | | | | | | 5,766,679 | |

| | | | | | | | | | |

| | | | |

| 20 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Pipelines–2.3% | | | | | | |

| $ | 7,200 | | | AK Transneft OJSC Via TransCapitalInvest Ltd., 8.70%, 8/7/18 | | | | $ | 9,216,000 | |

| | 2,900 | | | DCP Midstream LLC, 5.375%, 10/15/15 (a)(d) | | | | | 3,148,385 | |

| | | | El Paso LLC, | | | | | | |

| | 1,789 | | | 7.00%, 6/15/17 | | | | | 2,067,363 | |

| | 17,500 | | | 7.25%, 6/1/18 | | | | | 20,548,185 | |

| | 4,800 | | | Enbridge Energy Partners L.P., 5.875%, 12/15/16 | | | | | 5,539,603 | |

| | | | Energy Transfer Partners L.P., | | | | | | |

| | 2,100 | | | 6.125%, 2/15/17 | | | | | 2,438,955 | |

| | 2,600 | | | 6.625%, 10/15/36 | | | | | 3,099,015 | |

| | 804 | | | Kern River Funding Corp., 4.893%, 4/30/18 (a)(b)(d)(l) (acquisition cost–$813,093; purchased 4/28/03) | | | | | 878,721 | |

| | | | Kinder Morgan Energy Partners L.P., | | | | | | |

| | 700 | | | 5.00%, 12/15/13 | | | | | 719,517 | |

| | 5,800 | | | 6.00%, 2/1/17 | | | | | 6,755,742 | |

| | 5,500 | | | 7.30%, 8/15/33 | | | | | 7,287,566 | |

| | 11,900 | | | Midcontinent Express Pipeline LLC, 5.45%, 9/15/14 (a)(b)(d)(l) (acquisition cost–$11,879,413; purchased 9/9/09) | | | | | 12,354,354 | |

| | 3,400 | | | NGPL PipeCo LLC, 7.119%, 12/15/17 (a)(d) | | | | | 3,557,250 | |

| | 1,700 | | | Northwest Pipeline GP, 7.00%, 6/15/16 | | | | | 2,001,685 | |

| | 2,600 | | | Plains All American Pipeline L.P., 6.65%, 1/15/37 | | | | | 3,460,491 | |

| | 100 | | | Rockies Express Pipeline LLC, 5.625%, 4/15/20 (a)(d) | | | | | 94,125 | |

| | 4,400 | | | Southern Natural Gas Co. LLC, 5.90%, 4/1/17 (a)(b)(d)(l) (acquisition cost–$4,392,696; purchased 3/14/07) | | | | | 5,168,196 | |

| | 1,950 | | | Tennessee Gas Pipeline Co. LLC, 7.50%, 4/1/17 | | | | | 2,400,368 | |

| | 1,100 | | | TransCanada PipeLines Ltd., 3.80%, 10/1/20 | | | | | 1,223,076 | |

| | | | | | | | | | |

| | | | | | | | | 91,958,597 | |

| | | | | | | | | | |

| | | |

| | | | Real Estate–0.0% | | | | | | |

| | 1,500 | | | Qatari Diar Finance QSC, 5.00%, 7/21/20 | | | | | 1,726,500 | |

| | | | | | | | | | |

| | | |

| | | | Real Estate Investment Trust–0.2% | | | | | | |

| | 5,000 | | | Weyerhaeuser Co., 7.375%, 10/1/19 | | | | | 6,333,420 | |

| | | | | | | | | | |

| | | |

| | | | Retail–1.0% | | | | | | |

| | | | CVS Pass-Through Trust, | | | | | | |

| | 7,814 | | | 6.943%, 1/10/30 | | | | | 9,809,521 | |

| | 22,332 | | | 7.507%, 1/10/32 (a)(d) | | | | | 29,678,991 | |

| | | | | | | | | | |

| | | | | | | | | 39,488,512 | |

| | | | | | | | | | |

| | | |

| | | | Software–0.1% | | | | | | |

| | 1,800 | | | Oracle Corp., 5.00%, 7/8/19 | | | | | 2,149,270 | |

| | | | | | | | | | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 21 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Telecommunications–2.9% | | | | | | |

| | | | America Movil S.A.B. de C.V., | | | | | | |

| $ | 42,800 | | | 5.00%, 3/30/20 | | | | $ | 49,490,624 | |

| | 21,400 | | | 6.125%, 3/30/40 | | | | | 26,991,585 | |

| | | | AT&T, Inc., | | | | | | |

| | 80 | | | 4.30%, 12/15/42 (a)(d) | | | | | 78,823 | |

| | 1,718 | | | 5.35%, 9/1/40 | | | | | 1,949,452 | |

| | 5,000 | | | 5.50%, 2/1/18 | | | | | 5,917,270 | |

| | 1,100 | | | 5.80%, 2/15/19 | | | | | 1,339,191 | |

| | 1,000 | | | Axiata SPV1 Labuan Ltd., 5.375%, 4/28/20 | | | | | 1,151,523 | |

| | 4,500 | | | Deutsche Telekom International Finance BV, 6.75%, 8/20/18 | | | | | 5,581,656 | |

| | | | Qtel International Finance Ltd. (a)(d), | | | | | | |

| | 3,000 | | | 3.375%, 10/14/16 | | | | | 3,191,250 | |

| | 7,300 | | | 5.00%, 10/19/25 | | | | | 8,103,000 | |

| | | | Qwest Corp., | | | | | | |

| | 2,000 | | | 3.53%, 6/15/13 (m) | | | | | 2,005,708 | |

| | 1,250 | | | 6.50%, 6/1/17 | | | | | 1,450,511 | |

| | 4,800 | | | Sprint Capital Corp., 8.75%, 3/15/32 | | | | | 5,700,000 | |

| | 715 | | | Verizon Communications, Inc., 8.75%, 11/1/18 | | | | | 967,118 | |

| | | | | | | | | | |

| | | | | | | | | 113,917,711 | |

| | | | | | | | | | |

| | | |

| | | | Tobacco–0.8% | | | | | | |

| | | | Altria Group, Inc., | | | | | | |

| | 1,689 | | | 9.25%, 8/6/19 | | | | | 2,359,758 | |

| | 10,000 | | | 10.20%, 2/6/39 | | | | | 17,095,770 | |

| | 1,400 | | | Philip Morris International, Inc., 5.65%, 5/16/18 | | | | | 1,688,271 | |

| | 8,130 | | | Reynolds American, Inc., 7.75%, 6/1/18 | | | | | 10,353,303 | |

| | | | | | | | | | |

| | | | | | | | | 31,497,102 | |

| | | | | | | | | | |

| | | |

| | | | Transportation–0.1% | | | | | | |

| | 1,800 | | | Canadian National Railway Co., 5.55%, 3/1/19 | | | | | 2,193,964 | |

| | | | | | | | | | |

| | | | Total Corporate Bonds & Notes (cost–$1,855,093,514) | | | | | 2,104,269,157 | |

| | | | | | | | | | |

| | | | | | | | | | |

| SOVEREIGN DEBT OBLIGATIONS–14.1% | | | | | | |

| | | | Australia–7.5% | | | | | | |

| | | | Australia Government Bond (i), | | | | | | |

| AUD | 110,800 | | | 3.00%, 9/20/25, Ser. 25-CI | | | | | 161,550,841 | |

| | 61,700 | | | 4.00%, 8/20/20, Ser. 20-CI | | | | | 124,015,721 | |

| | 5,400 | | | Queensland Treasury Corp., 6.00%, 9/14/17, Ser. 17 | | | | | 6,244,631 | |

| | | | | | | | | | |

| | | | | | | | | 291,811,193 | |

| | | | | | | | | | |

| | | | |

| 22 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Brazil–5.1% | | | | | | |

| | | | Brazil Notas do Tesouro Nacional, Ser. F, | | | | | | |

| BRL | 40,777 | | | 10.00%, 1/1/14 | | | | $ | 20,632,886 | |

| | 176,575 | | | 10.00%, 1/1/17 | | | | | 91,339,331 | |

| | 153,313 | | | 10.00%, 1/1/21 | | | | | 79,173,257 | |

| | 6,144 | | | 10.00%, 1/1/23 | | | | | 3,154,292 | |

| $ | 3,300 | | | Brazilian Development Bank, 6.369%, 6/16/18 | | | | | 3,894,000 | |

| | | | | | | | | | |

| | | | | | | | | 198,193,766 | |

| | | | | | | | | | |

| | | |

| | | | Canada–0.3% | | | | | | |

| CAD | 2,400 | | | Province of Ontario Canada, 6.50%, 3/8/29 | | | | | 3,380,676 | |

| $ | 7,800 | | | Province of Quebec Canada, 3.50%, 7/29/20 | | | | | 8,727,014 | |

| | | | | | | | | | |

| | | | | | | | | 12,107,690 | |

| | | | | | | | | | |

| | | |

| | | | Colombia–0.1% | | | | | | |

| | 2,000 | | | Colombia Government International Bond, 7.375%, 1/27/17 | | | | | 2,444,000 | |

| | | | | | | | | | |

| | | |

| | | | Indonesia–0.1% | | | | | | |

| | 3,100 | | | Indonesia Government International Bond, 6.875%, 1/17/18 | | | | | 3,751,000 | |

| | | | | | | | | | |

| | | |

| | | | Korea (Republic of)–0.4% | | | | | | |

| | | | Export-Import Bank of Korea, | | | | | | |

| | 10,900 | | | 4.00%, 1/29/21 | | | | | 11,879,888 | |

| | 250 | | | 5.125%, 6/29/20 | | | | | 290,924 | |

| | | | Korea Development Bank, | | | | | | |

| | 3,950 | | | 4.00%, 9/9/16 | | | | | 4,289,005 | |

| | 300 | | | 8.00%, 1/23/14 | | | | | 314,904 | |

| | | | | | | | | | |

| | | | | | | | | 16,774,721 | |

| | | | | | | | | | |

| | | |

| | | | Mexico–0.3% | | | | | | |

| | 10,000 | | | Mexico Government International Bond, 6.05%, 1/11/40 | | | | | 13,200,000 | |

| | | | | | | | | | |

| | | |

| | | | Qatar–0.3% | | | | | | |

| | | | Qatar Government International Bond (a)(d), | | | | | | |

| | 3,500 | | | 4.00%, 1/20/15 (b)(l) (acquisition cost–$3,507,960; purchased 11/17/09-9/17/12) | | | | | 3,687,950 | |

| | 6,400 | | | 5.25%, 1/20/20 | | | | | 7,600,000 | |

| | | | | | | | | | |

| | | | | | | | | 11,287,950 | |

| | | | | | | | | | |

| | | |

| | | | Russia–0.0% | | | | | | |

| | 1,490 | | | Russian Federation Bond, 7.50%, 3/31/30 | | | | | 1,877,400 | |

| | | | | | | | | | |

| | | |

| | | | South Africa–0.0% | | | | | | |

| | 300 | | | South Africa Government International Bond, 6.875%, 5/27/19 | | | | | 375,750 | |

| | | | | | | | | | |

| | | | Total Sovereign Debt Obligations (cost–$532,405,484) | | | | | 551,823,470 | |

| | | | | | | | | | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 23 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| MUNICIPAL BONDS–13.8% | | | | | | |

| | | | Arizona–0.1% | | | | | | |

| $ | 2,000 | | | Univ. of Arizona Rev., 6.423%, 8/1/35, Ser. A | | | | $ | 2,420,940 | |

| | | | | | | | | | |

| | | |

| | | | California–5.8% | | | | | | |

| | 2,400 | | | Golden State Tobacco Securitization Corp. Rev., 5.75%, 6/1/47, Ser. A-1 | | | | | 2,276,640 | |

| | 15,000 | | | Infrastructure & Economic Dev. Bank Rev., 6.486%, 5/15/49 | | | | | 18,689,400 | |

| | | | Los Angeles Cnty. Public Works Financing Auth. Rev., | | | | | | |

| | 6,900 | | | 7.488%, 8/1/33 | | | | | 9,140,637 | |

| | 12,300 | | | 7.618%, 8/1/40 | | | | | 16,920,372 | |

| | 25,000 | | | Los Angeles Community College Dist., GO, 6.75%, 8/1/49 | | | | | 36,440,250 | |

| | | | Los Angeles Department of Water & Power Rev., | | | | | | |

| | 3,000 | | | 5.516%, 7/1/27, Ser. C | | | | | 3,727,800 | |

| | 5,000 | | | 6.574%, 7/1/45 | | | | | 7,316,400 | |

| | 1,300 | | | Los Angeles Unified School Dist., GO, 6.758%, 7/1/34 | | | | | 1,810,393 | |

| | 300 | | | Palomar Community College Dist., GO, 7.194%, 8/1/45, Ser. B-1 | | | | | 357,021 | |

| | 1,000 | | | San Diego Cnty. Water Auth. Rev., 6.138%, 5/1/49 | | | | | 1,368,960 | |

| | | | State, GO, | | | | | | |

| | 800 | | | 4.85%, 10/1/14 | | | | | 849,224 | |

| | 400 | | | 6.20%, 10/1/19 | | | | | 492,756 | |

| | 1,500 | | | 6.65%, 3/1/22 | | | | | 1,928,820 | |

| | 8,550 | | | 7.55%, 4/1/39 | | | | | 12,794,477 | |

| | 36,400 | | | 7.60%, 11/1/40 | | | | | 55,265,392 | |

| | 12,000 | | | 7.70%, 11/1/30 | | | | | 15,333,600 | |

| | 27,250 | | | 7.95%, 3/1/36 | | | | | 34,746,202 | |

| | 7,500 | | | Univ. of California Rev., 0.887%, 7/1/13, Ser. AA-2 | | | | | 7,505,775 | |

| | | | | | | | | | |

| | | | | | | | | 226,964,119 | |

| | | | | | | | | | |

| | | |

| | | | Illinois–0.4% | | | | | | |

| | 10,500 | | | Chicago Transit Auth. Rev., 6.20%, 12/1/40, Ser. B | | | | | 12,646,095 | |

| | 1,600 | | | Finance Auth. Rev., Univ. of Chicago, 5.50%, 7/1/37, Ser. B | | | | | 1,897,424 | |

| | | | | | | | | | |

| | | | | | | | | 14,543,519 | |

| | | | | | | | | | |

| | | |

| | | | Iowa–0.0% | | | | | | |

| | 680 | | | Tobacco Settlement Auth. Rev., 6.50%, 6/1/23, Ser. A | | | | | 680,435 | |

| | | | | | | | | | |

| | | |

| | | | Massachusetts–0.5% | | | | | | |

| | 17,000 | | | School Building Auth. Rev., 5.468%, 6/15/27 | | | | | 21,001,290 | |

| | | | | | | | | | |

| | | |

| | | | New Jersey–0.3% | | | | | | |

| | | | State Turnpike Auth. Rev., | | | | | | |

| | 5,000 | | | 7.102%, 1/1/41, Ser. A | | | | | 7,347,750 | |

| | 3,900 | | | 7.414%, 1/1/40, Ser. F | | | | | 5,920,551 | |

| | | | | | | | | | |

| | | | | | | | | 13,268,301 | |

| | | | | | | | | | |

| | | | |

| 24 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | New York–3.2% | | | | | | |

| $ | 5,500 | | | Metropolitan Transportation Auth. Rev., 5.871%, 11/15/39 | | | | $ | 6,726,665 | |

| | 3,000 | | | New York City, GO, 4.769%, 10/1/23, Ser. A-2 | | | | | 3,524,280 | |

| | | | New York City Municipal Water & Sewer System Finance Auth. Rev., | | | | | | |

| | 3,640 | | | 5.79%, 6/15/41 | | | | | 4,258,363 | |

| | 1,445 | | | 6.011%, 6/15/42 | | | | | 1,996,195 | |

| | | | New York City Transitional Finance Auth. Rev., | | | | | | |

| | 400 | | | 4.325%, 11/1/21 | | | | | 463,516 | |

| | 800 | | | 4.525%, 11/1/22 | | | | | 939,120 | |

| | 10,000 | | | 5.00%, 11/1/38, Ser. D-1 | | | | | 11,473,700 | |

| | 3,000 | | | 5.267%, 5/1/27, Ser. G-3 | | | | | 3,660,900 | |

| | 700 | | | 5.572%, 11/1/38 | | | | | 891,184 | |

| | 200 | | | 5.932%, 11/1/36 | | | | | 230,540 | |

| | 11,000 | | | Port Auth. of New York & New Jersey Rev., 4.458%, 10/1/62, Ser. 174 | | | | | 11,502,040 | |

| | | | State Dormitory Auth. Rev., | | | | | | |

| | 10,000 | | | 5.00%, 3/15/27, Ser. A | | | | | 11,798,500 | |

| | 20,345 | | | 5.00%, 2/15/30, Ser. D | | | | | 23,998,962 | |

| | 1,600 | | | 5.289%, 3/15/33, Ser. H | | | | | 1,970,704 | |

| | 2,700 | | | 5.389%, 3/15/40, Ser. H | | | | | 3,466,827 | |

| | 20,550 | | | 5.50%, 3/15/30 | | | | | 25,997,394 | |

| | 3,180 | | | State Thruway Auth. Rev., 5.00%, 3/15/25, Ser. A | | | | | 3,851,553 | |

| | | | State Urban Dev. Corp. Rev., | | | | | | |

| | 1,500 | | | 5.00%, 3/15/23, Ser. A | | | | | 1,833,345 | |

| | 4,000 | | | 5.77%, 3/15/39 | | | | | 5,016,120 | |

| | | | | | | | | | |

| | | | | | | | | 123,599,908 | |

| | | | | | | | | | |

| | | |

| | | | Ohio–0.6% | | | | | | |

| | | | American Municipal Power, Inc. Rev., | | | | | | |

| | 3,600 | | | 5.939%, 2/15/47 | | | | | 4,300,272 | |

| | 4,400 | | | Comb Hydroelectric Projects, 7.834%, 2/15/41, Ser. B | | | | | 6,397,292 | |

| | | | Buckeye Tobacco Settlement Financing Auth. Rev., Ser. A-2, | | | | | | |

| | 11,700 | | | 5.75%, 6/1/34 | | | | | 10,239,372 | |

| | 900 | | | 5.875%, 6/1/47 | | | | | 800,847 | |

| | | | | | | | | | |

| | | | | | | | | 21,737,783 | |

| | | | | | | | | | |

| | | |

| | | | Texas–2.8% | | | | | | |

| | | | Conroe Independent School Dist., GO, Ser. A (GTD-PSF), | | | | | | |

| | 1,000 | | | 5.00%, 2/15/24 | | | | | 1,251,190 | |

| | 2,610 | | | 5.00%, 2/15/25 | | | | | 3,239,663 | |

| | 2,905 | | | 5.00%, 2/15/26 | | | | | 3,577,246 | |

| | 3,115 | | | 5.00%, 2/15/27 | | | | | 3,802,948 | |

| | 5,000 | | | 5.00%, 2/15/28 | | | | | 6,064,000 | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 25 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | Texas (continued) | | | | | | |

| $ | 4,520 | | | 5.00%, 2/15/29 | | | | $ | 5,438,554 | |

| | 21,200 | | | Dallas, GO, 5.00%, 2/15/23 | | | | | 26,570,808 | |

| | 23,250 | | | Dallas Area Rapid Transit Rev., 5.022%, 12/1/48 | | | | | 28,593,082 | |

| | 4,400 | | | Dallas Cnty. Hospital Dist., GO, 5.621%, 8/15/44, Ser. C | | | | | 5,741,208 | |

| | 18,960 | | | Municipal Gas Acquisition & Supply Corp. III Rev., 5.00%, 12/15/25 | | | | | 21,215,292 | |

| | 4,100 | | | North Texas Tollway Auth. Rev., 6.718%, 1/1/49, Ser. B | | | | | 5,811,340 | |

| | | | | | | | | | |

| | | | | | | | | 111,305,331 | |

| | | | | | | | | | |

| | | |

| | | | Virginia–0.1% | | | | | | |

| | 2,000 | | | Richmond Rev., 5.00%, 1/15/29, Ser. A (e) | | | | | 2,412,920 | |

| | | | | | | | | | |

| | | | Total Municipal Bonds (cost–$453,712,849) | | | | | 537,934,546 | |

| | | | | | | | | | |

| | | | | | | | | | |

| U.S. GOVERNMENT AGENCY SECURITIES–8.2% | | | | | | |

| | | | Fannie Mae–7.1% | | | | | | |

| | 2 | | | 2.249%, 8/25/18, CMO (m) | | | | | 2,194 | |

| | 1,007 | | | 2.468%, 5/1/35, MBS (m) | | | | | 1,066,560 | |

| | 3,307 | | | 2.711%, 11/1/35, MBS (m) | | | | | 3,539,453 | |

| | 4 | | | 3.078%, 2/1/18, MBS (m) | | | | | 3,798 | |

| | 1,476 | | | 4.00%, 11/1/40, MBS | | | | | 1,580,456 | |

| | 3 | | | 4.095%, 4/1/17, MBS (m) | | | | | 2,661 | |

| | 103,800 | | | 4.50%, MBS, TBA, 30 Year (e) | | | | | 111,876,937 | |

| | 147,269 | | | 4.50%, 3/1/29-11/1/41, MBS | | | | | 159,064,213 | |

| | 620 | | | 5.29%, 11/25/33, CMO | | | | | 631,647 | |

| | | | | | | | | | |

| | | | | | | | | 277,767,919 | |

| | | | | | | | | | |

| | | |

| | | | Freddie Mac–0.0% | | | | | | |

| | 1 | | | 1.95%, 6/1/30, MBS (m) | | | | | 957 | |

| | 7 | | | 2.25%, 12/1/18, MBS (m) | | | | | 7,045 | |

| | 322 | | | 6.50%, 1/1/38-10/1/38, MBS | | | | | 366,234 | |

| | | | | | | | | | |

| | | | | | | | | 374,236 | |

| | | | | | | | | | |

| | | |

| | | | Ginnie Mae–0.0% | | | | | | |

| | 11 | | | 1.625%, 1/20/22, MBS (m) | | | | | 11,394 | |

| | | | | | | | | | |

| | | |

| | | | Small Business Administration Participation Certificates–1.1% | | | | | | |

| | 110 | | | 4.504%, 2/10/14, ABS | | | | | 111,846 | |

| | 2,767 | | | 4.77%, 4/1/24, ABS | | | | | 3,027,478 | |

| | 19,451 | | | 5.32%, 1/1/27, ABS | | | | | 22,315,911 | |

| | 13,340 | | | 5.70%, 8/1/26, ABS | | | | | 15,319,426 | |

| | | | | | | | | | |

| | | | | | | | | 40,774,661 | |

| | | | | | | | | | |

| | | | Total U.S. Government Agency Securities (cost–$307,298,104) | | | | | 318,928,210 | |

| | | | | | | | | | |

| | | | |

| 26 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| MORTGAGE-BACKED SECURITIES–3.6% | | | | | | |

| $ | 4,400 | | | Banc of America Commercial Mortgage Trust, 5.889%, 7/10/44 CMO (m) | | | | $ | 4,993,039 | |

| | 163 | | | Banc of America Funding Trust, 5.618%, 1/20/47 CMO (m) | | | | | 128,492 | |

| | 1,000 | | | BCAP LLC Trust, 0.368%, 9/26/35 CMO (a)(b)(d)(g)(l)(m) (acquisition cost–$946,250; purchased 4/3/13) | | | | | 946,103 | |

| | | | Bear Stearns Adjustable Rate Mortgage Trust, CMO (m), | | | | | | |

| | 1,231 | | | 2.32%, 8/25/35 | | | | | 1,253,798 | |

| | 1,362 | | | 2.60%, 3/25/35 | | | | | 1,376,042 | |

| | 105 | | | 2.792%, 10/25/33 | | | | | 106,420 | |

| | 271 | | | 2.793%, 3/25/35 | | | | | 273,872 | |

| | 74 | | | 2.907%, 5/25/34 | | | | | 71,448 | |

| | | | Bear Stearns ALT-A Trust, CMO (m), | | | | | | |

| | 1,189 | | | 2.635%, 2/25/36 | | | | | 793,347 | |

| | 4,105 | | | 2.87%, 11/25/36 | | | | | 3,024,384 | |

| | 5,312 | | | 2.89%, 11/25/36 | | | | | 3,781,008 | |

| | | | Bear Stearns Commercial Mortgage Securities Trust, CMO, | | | | | | |

| | 1,600 | | | 5.54%, 9/11/41 | | | | | 1,812,555 | |

| | 7,500 | | | 5.694%, 6/11/50 (m) | | | | | 8,803,680 | |

| | | | Citigroup Mortgage Loan Trust, Inc., CMO (m), | | | | | | |

| | 526 | | | 2.24%, 9/25/35 | | | | | 523,825 | |

| | 464 | | | 2.29%, 9/25/35 | | | | | 458,660 | |

| | | | Citigroup/Deutsche Bank Commercial Mortgage Trust, CMO, | | | | | | |

| | 4,400 | | | 5.322%, 12/11/49 | | | | | 5,025,568 | |

| | 8,000 | | | 5.484%, 1/15/46 (m) | | | | | 8,829,756 | |

| € | 217 | | | Cordusio RMBS SRL, 0.353%, 6/30/35 CMO (m) | | | | | 272,999 | |

| | | | Countrywide Alternative Loan Trust, CMO, | | | | | | |

| $ | 1,900 | | | 0.39%, 11/25/46 (m) | | | | | 1,347,213 | |

| | 557 | | | 0.40%, 5/25/36 (m) | | | | | 411,128 | |

| | 9,089 | | | 6.25%, 8/25/37 | | | | | 7,450,021 | |

| | | | Countrywide Home Loan Mortgage Pass-Through Trust, CMO (m), | | | | | | |

| | 274 | | | 0.52%, 3/25/35 | | | | | 198,128 | |

| | 61 | | | 3.061%, 8/25/34 | | | | | 56,426 | |

| | 17 | | | Credit Suisse First Boston Mortgage Securities Corp., 2.505%, 7/25/33 CMO (m) | | | | | 17,308 | |

| | | | Credit Suisse Mortgage Capital Certificates Mortgage-Backed Trust, CMO, | | | | | | |

| | 2,600 | | | 5.311%, 12/15/39 | | | | | 2,927,226 | |

| | 7,300 | | | 5.869%, 6/15/39 (m) | | | | | 8,441,461 | |

| | | | Downey Savings & Loan Assoc. Mortgage Loan Trust, CMO (m), | | | | | | |

| | 2,003 | | | 0.459%, 8/19/45 | | | | | 1,773,398 | |

| | 1,200 | | | 2.514%, 7/19/44 | | | | | 1,204,957 | |

| | 3,286 | | | Greenpoint Mortgage Funding Trust, 0.43%, 6/25/45 CMO (m) | | | | | 2,673,274 | |

| | 13 | | | Greenpoint Mortgage Pass-Through Certificates, 2.92%, 10/25/33 CMO (m) | | | | | 12,809 | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 27 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | GSR Mortgage Loan Trust, CMO (m), | | | | | | |

| $ | 80 | | | 1.94%, 3/25/33 | | | | $ | 79,227 | |

| | 772 | | | 2.662%, 9/25/35 | | | | | 798,597 | |

| | 1,776 | | | 2.677%, 9/25/35 | | | | | 1,793,699 | |

| | | | Harborview Mortgage Loan Trust, CMO (m), | | | | | | |

| | 285 | | | 0.389%, 1/19/38 | | | | | 235,157 | |

| | 482 | | | 0.539%, 6/20/35 | | | | | 462,787 | |

| | 186 | | | 2.602%, 5/19/33 | | | | | 187,450 | |

| | | | HomeBanc Mortgage Trust, CMO (m), | | | | | | |

| | 2,770 | | | 0.46%, 1/25/36 | | | | | 2,250,130 | |

| | 345 | | | 5.478%, 4/25/37 | | | | | 285,499 | |

| | | | JPMorgan Chase Commercial Mortgage Securities Trust, CMO, | | | | | | |

| | 1,000 | | | 5.336%, 5/15/47 | | | | | 1,137,411 | |

| | 6,600 | | | 5.42%, 1/15/49 | | | | | 7,575,437 | |

| | 2,200 | | | 5.44%, 6/12/47 | | | | | 2,519,992 | |

| | | | JPMorgan Mortgage Trust, CMO (m), | | | | | | |

| | 99 | | | 2.232%, 11/25/33 | | | | | 99,640 | |

| | 4,718 | | | 2.841%, 2/25/36 | | | | | 4,252,160 | |

| | 1,342 | | | 3.003%, 7/25/35 | | | | | 1,384,600 | |

| | 98 | | | 4.722%, 2/25/35 | | | | | 100,777 | |

| | 1,378 | | | 5.264%, 7/25/35 | | | | | 1,431,450 | |

| | | | Merrill Lynch/Countrywide Commercial Mortgage Trust, CMO (m), | | | | | | |

| | 1,200 | | | 5.172%, 12/12/49 | | | | | 1,350,168 | |

| | 1,600 | | | 6.13%, 8/12/49 | | | | | 1,888,612 | |

| | | | Morgan Stanley Re-Remic Trust, CMO (a)(d)(m), | | | | | | |

| | 3,400 | | | 5.982%, 8/12/45 | | | | | 3,938,111 | |

| | 1,500 | | | 5.982%, 8/15/45 | | | | | 1,737,402 | |

| | 52 | | | Ocwen Residential MBS Corp., 7.00%, 10/25/40 CMO (a)(b)(d)(g)(l)(m) (acquisition cost–$40,562; purchased 11/15/04) | | | | | 2,878 | |

| | | | RBSSP Resecuritization Trust, CMO (a)(d)(m), | | | | | | |

| | 1,026 | | | 0.48%, 5/26/37 | | | | | 986,922 | |

| | 11,387 | | | 0.52%, 3/26/37 | | | | | 10,900,658 | |

| | 5,765 | | | 0.698%, 9/26/34 | | | | | 5,529,746 | |

| | 6,900 | | | 0.698%, 3/26/36 | | | | | 6,779,728 | |

| | 5,201 | | | 0.698%, 4/26/37 | | | | | 5,044,012 | |

| | 1,415 | | | Residential Accredit Loans, Inc., 0.41%, 4/25/46 CMO (m) | | | | | 751,115 | |

| | 137 | | | Structured Adjustable Rate Mortgage Loan Trust, 2.583%, 2/25/34 CMO (m) | | | | | 138,713 | |

| | 3,628 | | | Structured Asset Mortgage Investments II Trust, 0.42%, 5/25/36 CMO (m) | | | | | 2,560,800 | |

| | | | Wachovia Bank Commercial Mortgage Trust, CMO, | | | | | | |

| | 229 | | | 0.279%, 6/15/20 (a)(d)(m) | | | | | 226,502 | |

| | 700 | | | 5.416%, 1/15/45 (m) | | | | | 783,425 | |

| | 1,300 | | | 5.678%, 5/15/46 | | | | | 1,514,973 | |

| | | | |

| 28 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| | | | WaMu Mortgage Pass-Through Certificates, CMO (m), | | | | | | |

| $ | 196 | | | 0.51%, 1/25/45 | | | | $ | 189,230 | |

| | 2,205 | | | 0.62%, 11/25/34 | | | | | 2,129,865 | |

| | 1,137 | | | 1.178%, 2/25/46 | | | | | 1,070,972 | |

| | 648 | | | Wells Fargo Mortgage-Backed Securities Trust, 2.652%, 3/25/36 CMO (m) | | | | | 609,149 | |

| | | | | | | | | | |

| | | | Total Mortgage-Backed Securities (cost–$117,340,847) | | | | | 141,715,339 | |

| | | | | | | | | | |

| | | | | | | | | | |

| U.S. TREASURY OBLIGATIONS–3.3% | | | | | | |

| | | | U.S. Treasury Inflation Indexed Bonds–0.5% | | | | | | |

| | 11,480 | | | 3.625%, 4/15/28 (i)(j) | | | | | 18,210,657 | |

| | | | | | | | | | |

| | | |

| | | | U.S. Treasury Notes–2.8% | | | | | | |

| | 522 | | | 0.25%, 1/31/14 (j) | | | | | 522,571 | |

| | 205 | | | 0.25%, 2/28/14 (j) | | | | | 205,232 | |

| | 5,900 | | | 0.25%, 3/31/14 (j) | | | | | 5,906,915 | |

| | 6,945 | | | 1.00%, 1/15/14 (j) | | | | | 6,989,219 | |

| | 60,000 | | | 1.125%, 5/31/19 (j)(k) | | | | | 60,815,640 | |

| | 543 | | | 1.25%, 3/15/14 (j) | | | | | 548,367 | |

| | 610 | | | 1.25%, 4/15/14 | | | | | 616,576 | |

| | 20 | | | 1.75%, 3/31/14 | | | | | 20,298 | |

| | 30,600 | | | 3.625%, 2/15/21 (j) | | | | | 36,009,988 | |

| | | | | | | | | | |

| | | | | | | | | 111,634,806 | |

| | | | | | | | | | |

| | | | Total U.S. Treasury Obligations (cost–$125,737,080) | | | | | 129,845,463 | |

| | | | | | | | | | |

| | | | | | | | | | |

| SENIOR LOANS (a)(c)–0.5% | | | | | | |

| | | | Financial Services–0.5% | | | | | | |

| | 18,615 | | | Springleaf Finance Corp., 5.50%, 5/10/17 | | | | | 18,719,760 | |

| | | | | | | | | | |

| | | |

| | | | Healthcare-Services–0.0% | | | | | | |

| | 886 | | | HCA, Inc., 3.534%, 3/31/17, Term B2 | | | | | 889,787 | |

| | | | | | | | | | |

| | | | Total Senior Loans (cost–$19,437,797) | | | | | 19,609,547 | |

| | | | | | | | | | |

| | | | | | | | | | |

| ASSET-BACKED SECURITIES–0.4% | | | | | | |

| | | | Bear Stearns Asset-Backed Securities I Trust (m), | | | | | | |

| | 2,000 | | | 0.40%, 12/25/36 | | | | | 1,814,607 | |

| | 531 | | | 1.20%, 10/25/37 | | | | | 460,427 | |

| | 274 | | | BNC Mortgage Loan Trust, 0.30%, 5/25/37 (m) | | | | | 267,588 | |

| | | | Conseco Financial Corp., | | | | | | |

| | 243 | | | 6.22%, 3/1/30 | | | | | 265,984 | |

| | 3,817 | | | 6.53%, 2/1/31 (m) | | | | | 3,925,977 | |

| | 1,500 | | | First Frankin Mortgage Loan Trust, 0.69%, 9/25/35 (m) | | | | | 1,319,404 | |

| | 1,468 | | | First NLC Trust, 0.905%, 12/25/35 (m) | | | | | 1,394,163 | |

| | 979 | | | Home Equity Asset Trust, 1.40%, 10/25/33 (m) | | | | | 933,311 | |

| | | | | | |

| 4.30.13 | | AllianzGI Managed Accounts Trust Semiannual Report | | | 29 | |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)

| | | | | | | | | | |

Principal

Amount

(000s) | | | | | | | Value | |

| $ | 21 | | | JPMorgan Mortgage Acquisition Corp., 0.28%, 3/25/37 (m) | | | | $ | 21,318 | |

| | 3 | | | Keystone Owner Trust, 9.00%, 1/25/29 (a)(b)(d)(l) (acquisition cost–$1,680; purchased 11/21/00) | | | | | 1,365 | |

| | 138 | | | MASTR Asset-Backed Securities Trust, 0.28%, 5/25/37 (m) | | | | | 137,744 | |

| | 242 | | | Merrill Lynch Mortgage Investors Trust, 0.32%, 2/25/37 (m) | | | | | 95,879 | |

| | 500 | | | Morgan Stanley ABS Capital I, Inc. Trust, 0.63%, 9/25/35 (m) | | | | | 402,048 | |

| | 187 | | | Morgan Stanley Mortgage Loan Trust, 0.56%, 4/25/37 (m) | | | | | 101,977 | |

| | 1,000 | | | Nomura Home Equity Loan, Inc. Home Equity Loan Trust, 0.79%, 9/25/35 (m) | | | | | 740,461 | |

| | 238 | | | Popular ABS Mortgage Pass-Through Trust, 0.29%, 6/25/47 (m) | | | | | 214,661 | |

| | 1,000 | | | Structured Asset Investment Loan Trust, 0.66%, 6/25/35 (m) | | | | | 920,568 | |

| | | | Structured Asset Securities Corp. Mortgage Loan Trust (m), | | | | | | |

| | 1,000 | | | 0.54%, 2/25/36 | | | | | 813,851 | |

| | 1,200 | | | 0.65%, 11/25/35 | | | | | 996,641 | |

| | 1,500 | | | Wells Fargo Home Equity Asset-Backed Securities Trust, 0.79%, 11/25/35 (m) | | | | | 1,298,220 | |

| | | | | | | | | | |

| | | | Total Asset-Backed Securities (cost–$14,741,937) | | | | | 16,126,194 | |

| | | | | | | | | | |

| | | | | | | | | | |

| SHORT-TERM INVESTMENTS–4.7% | |

| | | | Repurchase Agreements–4.4% | | | | | | |

| | 18,600 | | | Banc of America Securities LLC,

dated 4/26/13-4/30/13, 0.11%-0.17%, due 5/1/13, proceeds $18,600,257; collateralized by U.S. Treasury Notes, 0.25%-1.875%, due 6/30/15-4/30/18, valued at $19,056,680 including accrued interest | | | | | 18,600,000 | |

| | 35,100 | | | Barclays Capital, Inc.,

dated 4/29/13, 0.09%, due 5/6/13, proceeds $35,100,614; collateralized by Federal Farm Credit Bank, 0.18%, due 7/15/14, valued at $36,523,582 including accrued interest | | | | | 35,100,000 | |

| | 61,100 | | | Citigroup Global Markets, Inc.,

dated 4/30/13, 0.18%-0.19%, due 5/1/13, proceeds $61,100,322; collateralized by Freddie Mac, 1.02%, due 10/16/17, valued at $60,741,754 and U.S. Treasury Notes, 2.125%, due 2/29/16, valued at $1,635,593 including accrued interest | | | | | 61,100,000 | |

| | 56,500 | | | JPMorgan Securities, Inc.,

dated 4/26/13, 0.08%, due 5/3/13, proceeds $56,500,879; collateralized by Federal Home Loan Bank, 0.125%, due 1/22/14, valued at $57,660,953 including accrued interest | | | | | 56,500,000 | |

| | 2,876 | | | State Street Bank and Trust Co.,

dated 4/30/13, 0.01%, due 5/1/13, proceeds $2,876,001; collateralized by Freddie Mac, 2.08%, due 10/17/22, valued at $2,935,194 including accrued interest | | | | | 2,876,000 | |

| | | | | | | | | | |

| | | | Total Repurchase Agreements (cost–$174,176,000) | | | | | 174,176,000 | |

| | | | | | | | | | |

| | | |

| | | | U.S. Treasury Obligations (j)(n)–0.2% | | | | | | |

| | 7,279 | | | U.S. Treasury Bills, 0.086%-0.137%, 10/17/13-4/3/14 (cost–$7,273,055) | | | | | 7,273,938 | |

| | | | | | | | | | |

| | | | |

| 30 | | AllianzGI Managed Accounts Trust Semiannual Report | | 4.30.13 |

Fixed Income SHares: Series C Schedule of Investments

April 30, 2013 (unaudited) (continued)