SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) | |

| þ | OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| | For the Fiscal Year Ended: December 31, 2008 | |

| | OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) | |

| o | OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| | For the transition period from . . . . to . . . . | |

Commission File Number: 1-7627

FRONTIER OIL CORPORATION

(Exact name of registrant as specified in its charter)

| Wyoming | | 74-1895085 |

| (State or other jurisdiction of | | (I.R.S. Employer |

| incorporation or organization) | | Identification No.) |

| | | |

| 10000 Memorial Drive, Suite 600 | | 77024-3411 |

| Houston, Texas | | (Zip Code) |

| (Address of principal executive offices) | | |

Registrant’s telephone number, including area code: (713) 688-9600

Securities registered pursuant to Section 12(b) of the Act:

| | Name of Each Exchange |

| Title of Each Class | | on Which Registered |

| Common Stock | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to rule 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ü

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one)

Large accelerated filer þ Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of June 30, 2008 was $2.1 billion.

The number of shares of common stock outstanding as of February 20, 2009 was 103,919,472.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Annual Proxy Statement for the registrant’s 2009 annual meeting of shareholders are incorporated by reference into Items 10 through 14 of Part III.

Forward-Looking Statements

This Form 10-K contains “forward-looking statements” as defined by the Securities and Exchange Commission (“SEC”). Such statements are those concerning contemplated transactions and strategic plans, expectations and objectives for future operations. These include, without limitation:

| · | statements, other than statements of historical fact, that address activities, events or developments that we expect, believe or anticipate will or may occur in the future; |

| · | statements relating to future financial performance, future capital sources and other matters; and |

| · | any other statements preceded by, followed by or that include the words “anticipates,” “believes,” “expects,” “plans,” “intends,” “estimates,” “projects,” “could,” “should,” “may,” or similar expressions. |

Although we believe that our plans, intentions and expectations reflected in or suggested by the forward-looking statements we make in this Form 10-K are reasonable, we can give no assurance that such plans, intentions or expectations will be achieved. These statements are based on assumptions made by us based on our experience and perception of historical trends, current conditions, expected future developments and other factors that we believe are appropriate in the circumstances. Such statements are subject to a number of risks and uncertainties, many of which are beyond our control. You are cautioned that any such statements are not guarantees of future performance and that actual results or developments may differ materially from those projected in the forward-looking statements.

All forward-looking statements contained in this Form 10-K only speak as of the date of this document. We undertake no obligation to update or revise publicly any revisions to any such forward-looking statements that may be made to reflect events or circumstances after the date of this Form 10-K, or to reflect the occurrence of unanticipated events.

The terms “Frontier,” “we,” “us” and “our” as used in this Form 10-K refer to Frontier Oil Corporation and its subsidiaries, except where it is clear that those terms mean only the parent company. When we use the term “Rocky Mountain region,” we refer to the states of Colorado, Wyoming, western Nebraska, Montana and Utah, and when we use the term “Plains States,” we refer to the states of Kansas, Oklahoma, eastern Nebraska, Iowa, Missouri, North Dakota and South Dakota.

Overview

We are an independent energy company, organized in the State of Wyoming in 1977, engaged in crude oil refining and the wholesale marketing of refined petroleum products. We operate refineries (the “Refineries”) in Cheyenne, Wyoming and El Dorado, Kansas with a total annual average crude oil capacity of approximately 182,000 barrels per day (“bpd”). Both of our Refineries are complex refineries, which means that they can process heavier, less expensive types of crude oil and still produce a high percentage of gasoline, diesel fuel and other high value refined products. We focus our marketing efforts in the Rocky Mountain region and the Plains States, which we believe are among the most attractive refined products markets in the United States. The operations of refining and marketing of petroleum products are considered part of one reporting segment.

Cheyenne Refinery. Our Cheyenne Refinery has a permitted crude oil capacity of 52,000 bpd on a twelve-month average. We market its refined products primarily in the eastern slope of the Rocky Mountain region, which encompasses eastern Colorado (including the Denver metropolitan area), eastern Wyoming and western Nebraska (the “Eastern Slope”). The Cheyenne Refinery has a coking unit, which allows the refinery to process extensive amounts of heavy crude oil for use as a feedstock. The ability to process heavy crude oil lowers our raw material costs because heavy crude oil is generally less expensive than lighter types of crude oil. For the year ended December 31, 2008, heavy crude oil constituted approximately 76% of the Cheyenne Refinery’s total crude oil charge. For the year ended December 31, 2008, the Cheyenne Refinery’s product yield included gasoline (45%), diesel fuel (31%) and asphalt and other refined petroleum products (24%).

El Dorado Refinery. The El Dorado Refinery is one of the largest refineries in the Plains States and the Rocky Mountain region with crude oil capacity of 130,000 bpd. The El Dorado Refinery can select from many different types of crude oil because of its direct access to Cushing, Oklahoma, which is connected by pipelines to the Gulf Coast and to Canada. This access, combined with the El Dorado Refinery’s complexity (including a coking unit), gives it the flexibility to refine a wide variety of crude oils. In connection with our acquisition of the El Dorado Refinery in 1999, we entered into a 15-year refined product offtake agreement for gasoline and diesel production at this refinery with Shell Oil Products US (“Shell”). Shell has also agreed to purchase all jet fuel production until the end of the product offtake agreement. As our deliveries to Shell have declined per the terms of the refined product offtake agreement, we have marketed an increasing portion of the El Dorado Refinery’s gasoline and diesel in the same markets where Shell currently sells the El Dorado Refinery’s products, primarily in Denver and throughout the Plains States. For the year ended December 31, 2008, the El Dorado Refinery’s product yield included gasoline (50%), diesel and jet fuel (40%) and chemicals and other refined petroleum products (10%).

Other Assets. The Company owns Ethanol Management Company (“EMC”) which is a 25,000 bpd products terminal and blending facility located near Denver, Colorado.

Varieties of Crude Oil and Products. Traditionally, crude oil has been classified within the following types:

· sweet (low sulfur content),

· sour (high sulfur content),

· light (high gravity),

· heavy (low gravity) and

· intermediate (if gravity or sulfur content is in between).

For the most part, heavy crude oil tends to be sour and light crude oil tends to be sweet. When refined, light crude oil produces a higher proportion of high value refined products such as gasoline, diesel and jet fuel and, as a result, is more expensive than heavy crude oil. In contrast, heavy crude oil produces more low value by-products and heavy residual oils. The discount at which heavy crude oil sells compared to light crude oil is known in the industry as the light/heavy spread or differential, while the discount at which sour crude oil sells compared to light crude oil is known as the sweet/sour, or WTI/WTS, spread or differential. Coking units, such as the ones at our Refineries, can process certain by-products and heavy residual oils to produce additional volumes of gasoline and diesel, thus increasing the aggregate yields of higher value refined products from the same initial barrel of crude oil.

Refineries are frequently classified according to their complexity, which refers to the number, type and capacity of processing units at the refinery. Each of our Refineries possesses a coking unit, which provides substantial upgrading capacity and generally increases a refinery’s complexity rating. Upgrading capacity refers to the ability of a refinery to produce high yields of high value refined products such as gasoline and diesel from heavy and intermediate crude oil. In contrast, refiners with low upgrading capacity must process primarily light, sweet crude oil to produce a similar yield of gasoline and diesel. Some low complexity refineries may be capable of processing heavy and intermediate crude oil, but they will produce large volumes of by-products, including heavy residual oils and asphalt. Because gasoline, diesel and jet fuel sales generally achieve higher margins than are available on other refined products, we expect that these products will continue to make up the majority of our production.

Refinery Maintenance. Each of the processing units at our Refineries requires scheduled significant maintenance and repair shutdowns (referred to as “turnarounds”) during which the unit is not in operation. Turnaround cycles vary for different units but are generally required every one to five years. In general, turnarounds at our Refineries are managed so that some units continue to operate while others are down for scheduled maintenance. We also coordinate operations by staggering turnarounds between our two Refineries. Turnarounds are implemented using our regular personnel as well as additional contract labor. Once started, turnaround work typically proceeds 24 hours per day to minimize unit downtime. We defer the costs of turnarounds, reflected as “Deferred turnaround costs” on the Consolidated Balance Sheets, and subsequently amortize them on a straight-line basis over the period of time estimated to lapse until the next turnaround occurs. We normally schedule our turnaround work during the spring or fall of each year. When we perform a turnaround, we may increase product inventories prior to the turnaround to minimize the impact of the turnaround on our sales of refined products.

During 2008, the major turnaround work at the El Dorado Refinery involved the crude unit, the coker and the reformer. The timing of the 2008 El Dorado Refinery turnarounds coincided with the completion of the crude unit and vacuum expansion and the coker expansion projects. We are planning turnaround work and catalyst replacement on a distillate hydrotreater at the El Dorado Refinery in March 2009. We also have major turnaround work scheduled on the gofiner, fluid catalytic cracking unit (“FCCU”) and related units at the El Dorado refinery in the fall of 2009.

At the Cheyenne Refinery, 2008 turnaround work was modest in scope and involved a naphtha hydrotreater and its associated reformer, diesel hydrotreater, and sulfur recovery unit. The Cheyenne Refinery has no major turnaround work planned for 2009.

Cheyenne Refinery. The primary market for the Cheyenne Refinery’s refined products is the Eastern Slope. For the year ended December 31, 2008, we sold approximately 87% of the Cheyenne Refinery’s gasoline volumes in Colorado and 11% in Wyoming. For the year ended December 31, 2008, we sold approximately 69% of the Cheyenne Refinery’s diesel in Wyoming and 25% in Colorado. Because of the location of the Cheyenne Refinery, we are able to sell a significant portion of its diesel product from the truck rack at the Refinery, thereby eliminating transportation costs. The gasoline and remaining diesel produced by this Refinery are primarily shipped via pipeline to terminals for distribution by truck or rail. Pipeline shipments from the Cheyenne Refinery are handled mainly by the Plains All American Pipeline (formerly Rocky Mountain Pipeline), serving Denver and Colorado Springs, Colorado, and the ConocoPhillips Pipeline, serving Sidney, Nebraska.

We sell refined products from our Cheyenne Refinery to a broad base of independent retailers, jobbers and major oil companies. Refined product prices are determined by local market conditions at distribution centers known as “terminal racks,” and prices at the terminal racks are posted daily by sellers. The customer at a terminal rack typically supplies its own truck transportation. In the year ended December 31, 2008, approximately 87% of the Cheyenne Refinery’s sales were made to its 25 largest customers compared to the year ended December 31, 2007, when approximately 91% of the Cheyenne Refinery’s sales were made to its 25 largest customers. Occasionally, volumes sold exceed the Refinery’s production, in which case we purchase product in the spot market as needed.

El Dorado Refinery. The primary markets for the El Dorado Refinery’s refined products are Colorado and the Plains States, which include the Kansas City metropolitan area. The gasoline, diesel and jet fuel produced by the El Dorado Refinery are primarily shipped via pipeline to terminals for distribution by truck or rail. The NuStar Pipeline Operating Partnership L.P. Pipeline, serving the northern Plains States, the Magellan Pipeline Company, L.P. (“Magellan”) mountain pipeline serving Denver, Colorado, and the Magellan mid-continent pipeline serving the Plains States handle shipments from our El Dorado Refinery.

For the year ended December 31, 2008, Shell was the El Dorado Refinery’s largest customer, and our only customer which represented more than 10% of our total consolidated sales. For 2008, sales to Shell represented approximately 50% of the El Dorado Refinery’s total sales and 37% of our total consolidated sales. Under the offtake agreement, Shell purchases gasoline, diesel and jet fuel produced by the El Dorado Refinery at market-based prices. Initially in 1999, Shell purchased all of the El Dorado Refinery’s production of these products. Beginning in 2000, we retained and marketed 5,000 bpd of the Refinery’s gasoline and diesel production, and the retained portion increases by 5,000 bpd each year through 2009. In 2008, the Company entered into an amendment to the offtake agreement that allowed the Company to retain and market an additional 10,000 bpd of diesel production due to the coker expansion project and improved refinery efficiencies. In aggregate during 2008, we retained and marketed 55,000 bpd of the Refinerys’ gasoline and diesel production. As our sales to Shell under this agreement decrease, we intend to sell the gasoline and diesel produced by the El Dorado Refinery in the same general markets currently served by Shell, as previously described.

Cheyenne Refinery. The most competitive market for the Cheyenne Refinery’s products is the Denver metropolitan area. Other than the Cheyenne Refinery, three principal refineries serve the Denver market: an approximate 70,000 bpd refinery near Rawlins, Wyoming and an approximate 25,000 bpd refinery in Casper, Wyoming, both owned by Sinclair Oil Company (“Sinclair”); and a 90,000 bpd refinery located in Denver and owned by Suncor Energy (U.S.A.) Inc. (“Suncor”). Five product pipelines also supply Denver, including three from outside the region that enable refined products from other regions to be sold in the Denver market. Refined products shipped from other regions typically bear the burden of higher transportation costs.

The Suncor refinery located in Denver has lower product transportation costs to serve the Denver market than we do. However, the Cheyenne Refinery has lower crude oil transportation costs because of its proximity to the Guernsey, Wyoming hub, the major crude oil pipeline hub in the Rocky Mountain region. Moreover, unlike Sinclair and Suncor, we only sell our products to the wholesale market. We believe that our commitment to the wholesale market gives us certain marketing advantages over our principal competitors in the Eastern Slope area, all of which also have retail outlets, because we do not compete directly with independent retailers of gasoline and diesel.

El Dorado Refinery. The El Dorado Refinery faces competition from other Plains States and mid-continent refiners, but the principal competitors for the El Dorado Refinery are Gulf Coast refiners. Although our Gulf Coast competitors typically have lower production costs because of their size (economies of scale) than the El Dorado Refinery, we believe that our competitors’ higher refined product transportation costs allow our El Dorado Refinery to compete effectively in the Plains States and Rocky Mountain region with the Gulf Coast refineries. The Plains States and mid-continent regions are supplied by three product pipelines (Magellan Midstream Partners, L.P., Explorer Pipeline and Nustar Energy L.P.) that originate from the Gulf Coast.

We purchase crude oil from numerous suppliers, including major oil companies, marketing companies and large and small independent producers, under arrangements which contain market-responsive pricing provisions. Most of these arrangements are subject to cancellation by either party or have terms that are not in excess of one year and are subject to periodic renegotiation. We intend to continue purchasing crude oil from a variety of suppliers and typically under short-term commitments. In the event we become unable to purchase crude oil from any one of these sources, we believe that adequate alternative supplies of crude oil would be available. Crude oil charges are the quantity of crude oil and other feedstock processed through Refinery units.

Cheyenne Refinery. In the year ended December 31, 2008, we obtained approximately 64% of the Cheyenne Refinery’s crude oil charge from Canada, 15% from Wyoming, 16% from Colorado and 5% from other domestic sources. During the same period, heavy crude oil constituted approximately 76% of the Cheyenne Refinery’s total crude oil charge, compared to 72% in 2007. Cheyenne is 88 miles south of Guernsey, Wyoming, the main hub and crude oil trading center for the Rocky Mountain region. We transport crude oil from Guernsey to the Cheyenne Refinery via common carrier pipelines owned by Plains All American Pipeline and Suncor Energy. Ample quantities of heavy crude oil are available at Guernsey, including both locally produced Wyoming general sour and imported Canadian heavy crude oil, which is supplied by the Express pipeline system. This type of crude oil typically sells at a discount from lighter crude oil prices.

El Dorado Refinery. In the year ended December 31, 2008, we obtained approximately 57% of the El Dorado Refinery’s crude oil charge from Texas, 26% from Canada, 5% from Kansas, 10% from the Gulf of Mexico, and the remaining 2% from other foreign and domestic locations. El Dorado is 125 miles north of Cushing, Oklahoma, a major crude oil hub. The Cushing hub is supplied by the Seaway Pipeline, which runs from the Gulf Coast; the Basin Pipeline, which runs through Wichita Falls, Texas from West Texas; the Sun Pipeline, which originates at the Gulf Coast and connects to the Basin Pipeline at Wichita Falls; and the Spearhead Pipeline, which connects at Griffith, Indiana with the Enbridge Pipeline to bring crude oil from Canada. The Osage Pipeline runs from Cushing to El Dorado and transported approximately 95% of our crude oil charge during the year ended December 31, 2008. The remainder of our crude oil charge was transported to the El Dorado Refinery through Kansas gathering system pipelines. We have a Transportation Services Agreement to transport up to 38,000 bpd of crude oil on the Spearhead Pipeline from Griffith, Indiana to Cushing, Oklahoma, enabling us to transport heavy Canadian crude oil to our El Dorado Refinery. The initial term of this agreement expires in 2016. We have the right to extend the agreement for an additional ten years and increase the volume transported under a preferential tariff to 50,000 bpd.

Environmental Matters. See “Environmental” in Note 12 in the “Notes to Consolidated Financial Statements.”

We are subject to the requirements of the federal Occupational Safety and Health Act (“OSHA”) and comparable state occupational safety statutes.

The Cheyenne Refinery’s OSHA recordable incident rate in 2008 of 2.52 is higher than the latest reported U.S. refining industry average of 1.6 as compiled by the United States Department of Labor. While the frequency of injuries at the Cheyenne Refinery has risen above the industry average, we continue to emphasize safety at all levels of the Cheyenne Refinery organization. The Cheyenne Refinery’s 2008 contractor recordable rate was 2.9, representing six recordable injuries. Overall contractor work and, thus, man-hours was lower at the Cheyenne Refinery. As a result, the incidence rate is then significantly increased with any single recordable injury that occurs at the Refinery. During 2009, we intend to focus on safety by improving procedures and training for all Refinery workers in the coming year. These efforts include programs in both areas of occupational and process safety initiatives and are comprehensive across all areas of the Refinery.

The El Dorado Refinery’s OSHA recordable incident rate of 0.67 in 2008 is a significant improvement from the rate of 0.95 for 2007, and compares favorably to the U.S. refining average of 1.6. Management and employees at the El Dorado Refinery remain committed to programs, processes and behaviors that drive safety excellence. Improvement in contractor safety continued to be a key initiative for the El Dorado Refinery during 2008. Behavior-based safety programs were introduced in 2004 for our own employees. During 2006, we began including the majority of our contractor base in these programs as well. These efforts have resulted in a significant increase in contractor safety awareness and much improved contractor safety results. Our employees and management continue to dedicate their efforts to a balanced safety program that combines individual behavioral elements in a safety-coaching environment with structured, management-driven programs to improve the safety of our facilities and operating procedures. Our objective is to provide a safe working environment for employees and contractors and continue educating them about how to work safely. Encouraging all employees and contractors to contribute toward improving safety performance through personal involvement in safety-related activities is an industry-proven method of reducing injuries.

At December 31, 2008, we employed approximately 860 full-time employees: 95 in the Houston and Denver offices, 350 at the Cheyenne Refinery, and 415 at the El Dorado Refinery. The Cheyenne Refinery employees included approximately 130 administrative and technical personnel and approximately 220 union members. The El Dorado Refinery employees included 155 administrative and technical personnel and approximately 260 union members. The union members at our El Dorado Refinery are represented by the United Steel, Paper and Forestry, Rubber, Manufacturing, Energy, Allied Industrial and Service Workers International Union (“USW”). The union members at our Cheyenne Refinery are represented by seven bargaining units, the largest being the USW and the others with various craft unions.

For our Cheyenne Refinery, the current contract between the Company, the USW, and its Local 8-0574 expires in July 2009. The current contract between the Company, the craft unions, and its various local chapters expires in June 2009.

At our El Dorado Refinery, the current contract between the Company, the USW, and its Local 5-241 expires in January 2012.

Item 1A. Risk Factors Relating to Our Business Crude oil prices and refining margins significantly impact our cash flow and have fluctuated substantially in the past.Our cash flow from operations is primarily dependent upon producing and selling refined products at margins that are high enough to cover our fixed and variable expenses. In recent years, crude oil costs and crack spreads (the difference between refined product sales prices and crude oil prices) have fluctuated substantially. Factors that may affect crude oil costs and refined product prices include:

· overall demand for crude oil and refined products;

· general economic conditions;

· the level of foreign and domestic production of crude oil and refined products;

· the availability of imports of crude oil and refined products;

· the marketing of alternative and competing fuels;

· the extent of government regulation;

· global market dynamics;

· product pipeline capacity;

· local market conditions; and

· the level of operations of competing refineries.

Crude oil supply contracts are generally short-term contracts with price terms that change as market prices change. Our crude oil requirements are supplied from sources that include:

· major oil companies;

· crude oil marketing companies;

· large independent producers; and

· smaller local producers.

The price at which we can sell gasoline and other refined products is strongly influenced by the price of crude oil. Generally, an increase or decrease in the price of crude oil results in a corresponding increase or decrease in the price of gasoline and other refined products. However, if crude oil prices increase significantly, our operating margins would fall unless we could pass along these price increases to our customers.

Our Refineries maintain inventories of crude oil, intermediate products and refined products, the value of each being subject to fluctuations in market prices. Our inventories of crude oil, unfinished products and finished products are recorded at the lower of cost on a first-in, first-out (“FIFO”) basis or market prices. As a result, a rapid and significant increase or decrease in the market prices for crude oil or refined products could have a significant short-term impact on our earnings and cash flow.

Our profitability is affected by crude oil differentials, which may decline and accordingly decrease our profitability.

The light/heavy crude oil differentials that we report are the average differential between the benchmark West Texas Intermediate (“WTI”) crude oil priced on the New York Mercantile Exchange and the heavy crude oil priced as delivered to our Cheyenne Refinery or El Dorado Refinery, respectively. The WTI/WTS (sweet/sour) crude oil differential is the average differential between benchmark WTI crude oil priced on the New York Mercantile Exchange and West Texas sour crude oil priced at Midland, Texas. Our profitability at our Cheyenne Refinery is affected by the light/heavy crude oil differential, and our profitability at our El Dorado Refinery is affected by the WTI/WTS crude oil differential. Starting in March 2006, when our El Dorado Refinery began receiving heavy Canadian crude oil through the Spearhead Pipeline, its profitability also began benefiting from the light/heavy crude oil differential. We typically prefer to refine heavy sour crude oil at the Cheyenne Refinery and intermediate sour crude oil at the El Dorado Refinery because these crudes provide a higher refining margin than light or sweet crude oil does. Accordingly, any reduction of these crude oil differentials will reduce our profitability. The Cheyenne Refinery light/heavy crude oil differential averaged $17.15 per barrel in the year ended December 31, 2008, compared to $18.95 per barrel in the same period in 2007. The El Dorado Refinery light/heavy crude oil differential averaged $17.85 per barrel in the year ended December 31, 2008 compared to $21.00 per barrel in 2007. The WTI/WTS crude oil differential averaged $3.92 per barrel in the year ended December 31, 2008, compared to $5.02 per barrel in the same period in 2007. Crude oil prices were historically high during the first seven months of 2008, contributing to higher light/heavy crude oil differentials and WTI/WTS crude oil differentials. Crude oil prices dropped dramatically during the latter part of 2008, which resulted in significant narrowing of the light/heavy crude oil differentials and WTI/WTS crude oil differentials.

Our risk management activities may generate substantial losses and limit potential gains.

In order to hedge and limit potential financial losses on certain of our inventories, we from time to time enter into derivative contracts to make forward sales or purchases of crude oil, refined products, natural gas and other commodities. We may also use options or swaps to accomplish similar objectives. Our inventory hedging strategies generally produce losses when hedged crude oil or refined products increase in value. During the year ended December 31, 2008, we incurred a pre-tax hedging gain of $146.5 million recorded in “Other revenues” in the Consolidated Statements of Income. Offsetting the benefit of our hedges is the economic loss realized when we liquidate inventory which had been hedged. The value of the hedged inventory generally moves in an opposite direction to the value of the hedge contract. However, due to mark to market accounting requirements and cash margin requirements of commodities exchanges and various counterparties, there may be timing differences between when hedging losses are incurred and when the related physical inventories are sold. In certain instances, these derivative contracts are accounted for as hedges, but there is potential risk that these hedges may not be considered effective from an accounting perspective and would be marked to market in our financial statements. To the extent we use progressively more Canadian crude oil at our Refineries, both our total crude oil inventories and the amount of hedged inventories are likely to increase in future periods. See “Quantitative and Qualitative Disclosures about Market Risk” in Part II, Item 7A.

Instability and volatility in the financial markets could have a negative impact on our business, financial condition, results of operations and cash flows.

The financial markets have recently experienced substantial and unprecedented volatility as a result of dislocations in the credit markets. Market disruptions such as those currently being experienced in the United States and abroad may increase our cost of borrowing or adversely affect our ability to access sources of liquidity upon which we may rely to finance our operations and satisfy our obligations as they become due, and capital may not be available on terms that are reasonably acceptable to us, or at all. These disruptions may include turmoil in the financial services industry, including substantial uncertainty surrounding particular lending institutions with which we do business, reduction in available trade credit due to counterparties liquidity concerns, more strict lending requirements, unprecedented volatility in the markets where our outstanding securities trade, and general economic downturns in the areas where we do business. In addition, a general economic slowdown or the lack of liquidity may result in contractual counterparties with which we do business being unable to satisfy their obligations to us in a timely manner, or at all.

We maintain significant amounts of cash and cash equivalents at several financial institutions that are in excess of federally insured limits. During the year ended December 31, 2008, we recorded a loss of $499,000 on money market funds that had investments in Lehman Brothers, which filed for bankruptcy. Given the current instability of financial institutions, we may experience further losses on our cash and cash equivalents.

External factors beyond our control can cause fluctuations in demand for our products, prices and margins, which may negatively affect income and cash flow.

Among these factors is the demand for crude oil and refined products, which is largely driven by the conditions of local and worldwide economies as well as by weather patterns and the taxation of these products relative to other energy sources. Governmental regulations and policies, particularly in the areas of taxation, energy and the environment, also have a significant impact on our activities. Operating results can be affected by these industry factors, by competition in the particular geographic areas that we serve. The demand for crude oil and refined products can also be reduced due to a local or national recession or other adverse economic condition that results in lower spending by businesses and consumers on gasoline and diesel fuel, a shift by consumers to more fuel-efficient vehicles or alternative fuel vehicles (such as ethanol or wider adoption of gas/electric hybrid vehicles), or an increase in vehicle fuel economy, whether as a result of technological advances by manufacturers, legislation mandating or encouraging higher fuel economy or the use of alternative fuel.

In addition, our profitability depends largely on the spread between market prices for refined petroleum products and crude oil prices. This margin is continually changing and may fluctuate significantly from time to time. Crude oil and refined products are commodities whose price levels are determined by market forces beyond our control. Due to the seasonality of refined products markets and refinery maintenance schedules, results of operations for any particular quarter of a fiscal year are not necessarily indicative of results for the full year. In general, prices for refined products are influenced by the price of crude oil. Although an increase or decrease in the price of crude oil may result in a similar increase or decrease in prices for refined products, there may be a time lag in the realization of the similar increase or decrease in prices for refined products. The effect of changes in crude oil prices on operating results therefore depends in part on how quickly refined product prices adjust to reflect these changes. A substantial or prolonged increase in crude oil prices without a corresponding increase in refined product prices, a substantial or prolonged decrease in refined product prices without a corresponding decrease in crude oil prices, or a substantial or prolonged decrease in demand for refined products could have a significant negative effect on our results of operations and cash flows.

We are dependent on others to supply us with substantial quantities of raw materials.

Our business involves converting crude oil and other refinery charges into liquid fuels. We own no crude oil or natural gas reserves and depend on others to supply these feedstocks to our Refineries. We use large quantities of natural gas and electricity to provide heat and mechanical energy required by our processing units. Disruption to our supply of crude oil, natural gas or electricity, or the continued volatility in the costs thereof, could have a material adverse effect on our operations. In addition, our investment in inventory is affected by the general level of crude oil prices, and significant increases in crude oil prices could result in substantial working capital requirements to maintain inventory volumes.

Our Refineries face operating hazards, and the potential limits on insurance coverage could expose us to significant liability costs.

Our operations could be subject to significant interruption, and our profitability could be impacted if either of our Refineries experienced a major accident or fire, was damaged by severe weather or other natural disaster, or was otherwise forced to curtail its operations or shut down. If a crude oil pipeline that supplies crude oil to our Refineries became inoperative, crude oil would have to be supplied to our Refineries through an alternative pipeline or from additional tank truck deliveries to the Refineries. Alternative supply arrangements could require additional capital expenditures, hurt our business and profitability and cause us to operate the affected Refinery at less than full capacity until pipeline access was restored or crude oil transportation was fully replaced. In addition, a major accident, fire or other event could damage our Refineries or the environment or cause personal injuries. If either of our Refineries experiences a major accident or fire or other event or an interruption in supply or operations, our business could be materially adversely affected if the damage or liability exceeds the amounts of business interruption, property, terrorism and other insurance that we maintain against these risks.

Our Refineries consist of many processing units, a number of which have been in operation for many years. One or more of the units may require additional unscheduled down time for unanticipated maintenance or repairs that are more frequent than our scheduled turnaround for such units. Scheduled and unscheduled maintenance could reduce our revenues during the period of time that our units are not operating.

We face substantial competition from other refining companies, and greater competition in the markets where we sell refined products could adversely affect our sales and profitability.

The refining industry is highly competitive. Many of our competitors are large, integrated, major or independent oil companies that, because of their more diverse operations, larger refineries and stronger capitalization, may be better positioned than we are to withstand volatile industry conditions, including shortages or excesses of crude oil or refined products or intense price competition at the wholesale level. Many of these competitors have financial and other resources substantially greater than ours.

We are not engaged in the petroleum exploration and production business and therefore do not produce any of our crude oil feedstocks. We do not have a retail business and therefore are dependent upon others for outlets for our refined products. Certain of our competitors, however, obtain a portion of their feedstocks from company-owned production and have retail outlets. Competitors that have their own crude oil production or extensive retail outlets, with brand-name recognition, are at times able to offset losses from refining operations with profits from producing or retailing operations, and may be better positioned to withstand periods of depressed refining margins or feedstock shortages. In addition, we compete with other industries, such as wind, solar and hydropower, that provide alternative means to satisfy the energy and fuel requirements of our industrial, commercial and individual consumers. If we are unable to compete effectively with these competitors, both within and outside our industry, there could be a material adverse effect on our business, financial condition and results of operations.

Our operations involve environmental risks that may require us to make substantial capital expenditures to remain in compliance or that could give rise to material liabilities.

Our results of operations may be affected by increased costs of complying with the extensive environmental laws to which our business is subject and from any possible contamination of our facilities as a result of accidental spills, discharges or other releases of petroleum or hazardous substances.

Our operations are subject to extensive federal, state and local environmental and health and safety laws and regulations relating to the protection of the environment, including those governing the emission or discharge of pollutants into the air and water, product specifications and the generation, treatment, storage, transportation, disposal or remediation of solid and hazardous waste and materials. Environmental laws and regulations that affect the operations, processes and margins for our refined products are extensive and have become progressively more stringent. Additional legislation or regulatory requirements or administrative policies could be imposed with respect to our products or activities. Compliance with more stringent laws or regulations or more vigorous enforcement policies of the regulatory agencies could adversely affect our financial position and results of operations and could require us to make substantial expenditures. Any noncompliance with these laws and regulations could subject us to material administrative, civil or criminal penalties or other liabilities. For examples of existing and potential future regulations and their possible effects on us, please see “Environmental” in Note 12 in the “Notes to Consolidated Financial Statements.”

Our business is inherently subject to accidental spills, discharges or other releases of petroleum or hazardous substances. Past or future spills related to any of our operations, including our Refineries, pipelines or product terminals, could give rise to liability (including potential cleanup responsibility) to governmental entities or private parties under federal, state or local environmental laws, as well as under common law. This could involve contamination associated with facilities that we currently own or operate, facilities that we formerly owned or operated and facilities to which we sent wastes or by-product for treatment or disposal and other contamination. Accidental discharges could occur in the future, future action may be taken in connection with past discharges, governmental agencies may assess penalties against us in connection with past or future contamination and third parties may assert claims against us for damages allegedly arising out of any past or future contamination. The potential penalties and clean-up costs for past or future releases or spills, the failure of prior owners of our facilities to complete their clean-up obligations, the liability to third parties for damage to their property, or the need to address newly-discovered information or conditions that may require a response could be significant, and the payment of these amounts could have a material adverse effect on our business, financial condition and results of operations.

Our operations are subject to various laws and regulations relating to occupational health and safety, which could give rise to increased costs and material liabilities.

The nature of our business may result from time to time in industrial accidents. Our operations are subject to various laws and regulations relating to occupational health and safety. Continued efforts to comply with applicable health and safety laws and regulations, or a finding of non-compliance with current regulations, could result in additional capital expenditures or operating expenses, as well as fines and penalties.

We could incur substantial costs or disruptions in our business if we cannot obtain or maintain necessary permits and authorizations.

Our operations require numerous permits and authorizations under various laws and regulations, including environmental and health and safety laws and regulations. These authorizations and permits are subject to revocation, renewal or modification and can require operational changes, which may involve significant costs, to limit impacts or potential impacts on the environment and/or health and safety. A violation of these authorization or permit conditions or other legal or regulatory requirements could result in substantial fines, criminal sanctions, permit revocations, injunctions and/or refinery shutdowns. In addition, major modifications of our operations could require changes to our existing permits or expensive upgrades to our existing pollution control equipment, which could have a material adverse effect on our business, financial condition or results of operations.

Hurricanes along the Gulf Coast could disrupt our supply of crude oil and our ability to complete capital investment projects in a timely manner.

In 2005 and 2008, tropical hurricanes and related storm activity, such as windstorms, storm surges, floods and tornadoes, caused extensive and catastrophic physical damage in and to coastal and inland areas located in the Gulf Coast region of the United States (parts of Texas, Louisiana, Mississippi and Alabama) and certain other parts of the southeastern parts of the United States. Some of the materials we use for our capital projects are fabricated at facilities located along the Gulf Coast. Should other storms of this nature occur in the future, it is possible that the storms and their collateral effects could result in delays or cost increases for our capital investment projects.

In addition, supplies of crude oil to our El Dorado Refinery are sometimes shipped from Gulf Coast production or terminaling facilities. This crude oil supply source could be potentially threatened in the event of future catastrophic damage to such facilities.

We may have labor relations difficulties with some of our employees represented by unions.

Approximately 56 percent of our employees were covered by collective bargaining agreements at December 31, 2008. Our El Dorado Refinery union contract expires in 2012 and our Cheyenne Refinery union contracts expire by July 2009, and there is no assurance that we will be able to enter into new contracts on terms acceptable to us or at all. A failure to do so may increase our costs or result in an interruption of our business. See Item 1 “Business-Employees.” In addition, employees may conduct a strike at some time in the future, which may adversely affect our operations.

Terrorist attacks and threats or actual war may negatively impact our business.

Terrorist attacks in the United States and the war in Iraq, as well as events occurring in response to or in connection with them, including future terrorist attacks against U.S. targets, rumors or threats of war, actual conflicts involving the United States or its allies, or military or trade disruptions affecting our suppliers or our customers, could adversely impact our operations. In addition, any terrorist attack could have an adverse impact on energy prices, including prices for our crude oil and refined products, and an adverse impact on the margins from our refining and marketing operations. As a result, there could be delays or losses in the delivery of supplies and raw materials to us, decreased sales of our products and extensions of time for payment of accounts receivable from our customers.

None.

Refining and Terminal Operations We own an approximately 255 acre site on which the Cheyenne Refinery is located in Cheyenne, Wyoming and an approximately 1,000 acre site on which the El Dorado Refinery is located in El Dorado, Kansas. We lease the approximately two acre site in Henderson, Colorado on which our products and blending terminal is located.

Other Properties

We lease approximately 6,500 square feet of office space in Houston, Texas for our corporate headquarters under a lease expiring in October 2009. We also lease approximately 28,000 square feet of office space in Denver, Colorado under a lease expiring in April 2012 for our refining, marketing and raw material supply operations.

See “Litigation” and “Environmental” in Note 12 in the “Notes to Consolidated Financial Statements.”

Item 4. Submission of Matters to a Vote of Security Holders

None.

We file reports with the SEC, including annual reports on Form 10-K, quarterly reports on Form 10-Q and other reports from time to time. The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, DC, 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. We are an electronic filer, and the SEC’s Internet site at http://www.sec.gov contains the reports, proxy and information statements, and other information filed electronically.

As required by Section 402 of the Sarbanes-Oxley Act of 2002, we have adopted a code of ethics that applies to our chief executive officer, chief financial officer and principal accounting officer. This code of ethics is posted on our web site. Our web site address is: http://www.frontieroil.com. We make our web site content available for informational purposes only. It should not be relied upon for investment purposes, nor is it incorporated by reference in this Form 10-K. We make available on this web site under “Investor Relations,” free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports as soon as reasonably practicable after we electronically file those materials with, or furnish those materials to, the SEC.

We filed our 2008 annual CEO certification with the New York Stock Exchange (“NYSE”) on April 23, 2008. We anticipate filing our 2009 annual CEO certification with the NYSE on or about May 8, 2009. In addition, we filed with the SEC as exhibits to our Form 10-K for the year ended December 31, 2008 the CEO and CFO certifications required under Section 302 of the Sarbanes-Oxley Act of 2002.

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities Our common stock is listed on the New York Stock Exchange under the symbol FTO. The quarterly high and low sales as reported on the New York Stock Exchange for 2008 and 2007 are shown in the following table:

| 2008 | | High | | | Low | |

| Fourth quarter | | $ | 18.38 | | | $ | 7.51 | |

| Third quarter | | | 24.26 | | | | 16.49 | |

| Second quarter | | | 33.00 | | | | 23.03 | |

| First quarter | | | 41.00 | | | | 25.22 | |

| 2007 | | High | | | Low | |

| Fourth quarter | | $ | 49.13 | | | $ | 39.54 | |

| Third quarter | | | 49.10 | | | | 31.61 | |

| Second quarter | | | 45.75 | | | | 31.95 | |

| First quarter | | | 33.75 | | | | 25.47 | |

The approximate number of holders of record for our common stock as of February 20, 2009 was 912. The quarterly cash dividend on our common stock was $0.03 per share for the quarters ended June 30, 2006 through March 31, 2007. The quarterly cash dividend was $0.05 per share for the quarters ended June 30, 2007 through March 31, 2008. The quarterly cash dividend was $0.06 per share for the quarters ended June 30, 2008 through December 31, 2008. Our 6.625% Senior Notes, our 8.5% Senior Notes and our Revolving Credit Facility may restrict dividend payments based on the covenants related to interest coverage and restricted payments. See Notes 6 and 7 in the “Notes to Consolidated Financial Statements.”

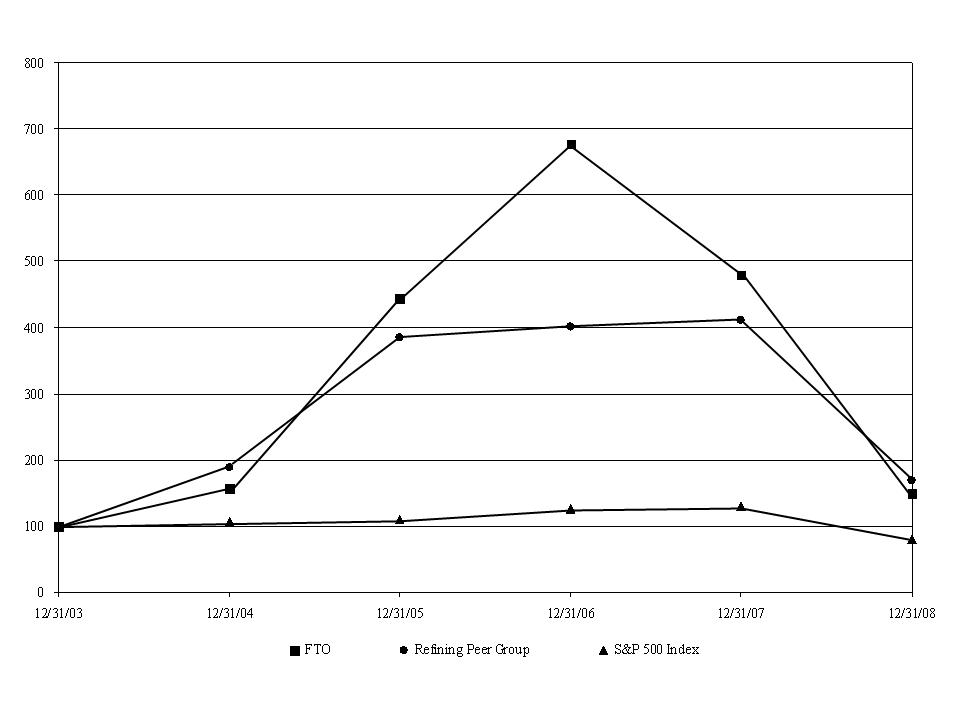

The following graph indicates the performance of our common stock against the S&P 500 Index and against a refining peer group which is comprised of Sunoco Inc., Holly Corporation, Valero Energy Corporation and Tesoro Corporation. The following information in this Item 5 of this Annual Report on Form 10-K is not deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate it by reference into such a filing.

| Five Year Financial Data | | | | | | | | | | | | | | | |

| (Unaudited) | | Years Ended December 31, | |

| | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | (Dollars in thousands, except per share amounts) | |

| | | | | | | | | | | | | | | | |

| Revenues | | $ | 6,498,780 | | | $ | 5,188,740 | | | $ | 4,795,953 | | | $ | 4,001,162 | | | $ | 2,861,716 | |

| | | | | | | | | | | | | | | | | | | | | |

| Operating income | | | 116,753 | | | | 755,795 | | | | 574,194 | | | | 450,013 | | | | 142,903 | |

| | | | | | | | | | | | | | | | | | | | | |

Cumulative effect of accounting change, net of income taxes (1) | | | - | | | | - | | | | - | | | | (2,503 | ) | | | - | |

| | | | | | | | | | | | | | | | | | | | | |

| Net income | | | 80,234 | | | | 499,125 | | | | 379,277 | | | | 275,158 | | | | 69,392 | |

| | | | | | | | | | | | | | | | | | | | | |

| Basic earnings per share: | | | | | | | | | | | | | | | | | | | | |

Before cumulative effect of accounting change | | $ | 0.78 | | | $ | 4.67 | | | $ | 3.40 | | | $ | 2.51 | | | $ | 0.65 | |

Cumulative effect of accounting change (1) | | | - | | | | - | | | | - | | | | (0.02 | ) | | | - | |

| Net income | | $ | 0.78 | | | $ | 4.67 | | | $ | 3.40 | | | $ | 2.49 | | | $ | 0.65 | |

| | | | | | | | | | | | | | | | | | | | | |

| Diluted earnings per share: | | | | | | | | | | | | | | | | | | | | |

Before cumulative effect of accounting change | | $ | 0.77 | | | $ | 4.62 | | | $ | 3.37 | | | $ | 2.44 | | | $ | 0.63 | |

Cumulative effect of accounting change (1) | | | - | | | | - | | | | - | | | | (0.02 | ) | | | - | |

| Net income | | $ | 0.77 | | | $ | 4.62 | | | $ | 3.37 | | | $ | 2.42 | | | $ | 0.63 | |

| | | | | | | | | | | | | | | | | | | | | |

Working capital (current assets less current liabilities) | | $ | 651,352 | | | $ | 529,510 | | | $ | 479,518 | | | $ | 270,145 | | | $ | 106,760 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total assets | | | 2,018,469 | | | | 1,863,848 | | | | 1,523,925 | | | | 1,223,057 | | | | 770,177 | |

| | | | | | | | | | | | | | | | | | | | | |

| Long-term debt | | | 347,220 | | | | 150,000 | | | | 150,000 | | | | 150,000 | | | | 150,000 | |

| | | | | | | | | | | | | | | | | | | | | |

| Shareholders' equity | | | 1,051,140 | | | | 1,038,614 | | | | 775,854 | | | | 478,692 | | | | 271,120 | |

| | | | | | | | | | | | | | | | | | | | | |

Dividends declared per common share | | $ | 0.230 | | | $ | 0.180 | | | $ | 0.100 | | | $ | 0.575 | | | $ | 0.055 | |

| | | | | | | | | | | | | | | | | | | | | |

(1) As of December 31, 2005, we adopted FASB Interpretation No. 47, "Accounting for Conditional Asset Retirement Obligations." | |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

General

Frontier operates Refineries in Cheyenne, Wyoming and El Dorado, Kansas as previously discussed in Part I, Item 1 of this Form 10-K. We focus our marketing efforts in the Rocky Mountain and Plains States regions of the United States. We purchase crude oil to be refined and market refined petroleum products, including various grades of gasoline, diesel, jet fuel, asphalt and other by-products.

Results of Operations

To assist in understanding our operating results, please refer to the operating data at the end of this analysis which provides key operating information for our Refineries. Refinery operating data is also included in our quarterly reports on Form 10-Q and on our web site at http://www.frontieroil.com. We make our web site content available for informational purposes only. It should not be relied upon for investment purposes, nor is it incorporated by reference in this Form 10-K.

Overview

Our Refineries have a total annual average crude oil capacity of approximately 182,000 bpd. The four significant indicators of our profitability, which are reflected and defined in the operating data at the end of this analysis, are the gasoline crack spread, the diesel crack spread, the light/heavy crude oil differential and the WTI/WTS crude oil differential. Other significant factors that influence our financial results are refinery utilization, crude oil price trends, asphalt and by-product margins and refinery operating expenses (including natural gas and maintenance). Under our first-in, first-out (“FIFO”) inventory accounting method, crude oil price trends can cause significant fluctuations in the inventory valuation of our crude oil, unfinished products and finished products, thereby resulting in inventory gains (lowering “Raw material, freight and other costs”) when crude oil prices increase and inventory losses (increasing “Raw material, freight and other costs”) when crude oil prices decrease during the reporting period. As crude prices rose during the first seven months of 2008; we realized inventory gains; however, as crude prices declined quickly during the latter part of the year and gasoline and diesel margins contracted, we realized significant inventory losses resulting in an overall inventory loss for the year. We typically do not use derivative instruments to offset price risk on our base level of operating inventories. See “Price Risk Management Activities” under Item 7A for a discussion of our utilization of futures trading.

Crude oil market fundamentals, changes in the macro-economy and geopolitical considerations have caused crude oil prices to be highly volatile. Our results for the year ended December 31, 2008 were negatively impacted by several factors, the primary ones being the rapid increase in crude oil prices during the first seven months of 2008 followed by a rapid decline in crude oil prices the remainder of the year and the weakening U.S. economy. These factors reduced the demand for gasoline, causing a substantial drop in gasoline margins. In addition, our margins on asphalt and other products declined substantially during the first seven months of 2008 as sales prices for these products increased only modestly compared to the significant increase in crude prices.

2008 Compared with 2007

Overview of Results

We had net income for the year ended December 31, 2008, of $80.2 million, or $0.77 per diluted share, compared to net income of $499.1 million, or $4.62 per diluted share, for the same period in 2007. Our operating income of $116.8 million for the year ended December 31, 2008 reflected a decrease of $639.0 million from the $755.8 million operating income for the comparable period in 2007. The average gasoline crack spread was significantly lower during 2008 ($4.75 per barrel) than in 2007 ($17.99 per barrel), and the light/heavy crude oil differentials decreased. The average diesel crack spread was higher during 2008 ($24.59 per barrel) than in 2007 ($22.19 per barrel).

Specific Variances

Refined product revenues. Refined product revenues increased $1.07 billion, or 20%, from $5.27 billion to $6.34 billion for the year ended December 31, 2008 compared to 2007. This increase was due to an increase in average product sales prices ($19.30 higher per sales barrel) partially offset by lower product sales volumes in 2008 (3,776 fewer bpd). Sales prices increased primarily because of higher average crude oil prices in 2008 compared to 2007.

Manufactured product yields. Manufactured product yields (“yields”) are the volumes of specific materials obtained through the distilling of crude oil and the operations of other refinery process units. Yields decreased 5,139 bpd at the El Dorado Refinery and increased 1,773 bpd at the Cheyenne Refinery for the year ended December 31, 2008 compared to 2007. The decrease in yields at the El Dorado Refinery was due to the planned major turnaround work on the crude unit, the coker and the reformer during March and April of 2008.

Other revenues. Other revenues increased $237.6 million to a $156.6 million gain for the year ended December 31, 2008 compared to an $80.9 million loss for 2007, the primary source of which was $146.5 million in net realized and unrealized gains from derivative contracts to hedge in-transit crude oil and excess inventories during the year ended December 31, 2008 compared to $86.4 million in net realized and unrealized losses from derivative contracts to hedge in-transit crude oil and excess inventories in 2007. See “Price Risk Management Activities” under Item 7A and Note 11 in the “Notes to Consolidated Financial Statements” for a discussion of our utilization of commodity derivative contracts. We had gasoline sulfur credit sales of $4.6 million in 2008 compared to $4.8 million in 2007 and $4.5 million of ethanol Renewable Identification Number (“RIN”) sales in 2008 (none in 2007). Ethanol RINs were created to assist in tracking the compliance with national EPA regulations for blending of renewable fuels.

Raw material, freight and other costs. Raw material, freight and other costs include crude oil and other raw materials used in the refining process, purchased products and blendstocks, freight costs for FOB destination sales, as well as the impact of changes in inventory. Raw material, freight and other costs increased by $1.91 billion, or 47%, during the year ended December 31, 2008, from $4.04 billion in 2007 to $5.95 billion in 2008. The increase in raw material, freight and other costs when compared to 2007 was due to higher average crude prices, increased purchased products, lower light/heavy crude oil differentials and inventory losses in 2008 compared to inventory gains in 2007, partially offset by decreased overall crude oil charges during the year ended December 31, 2008 compared to 2007. The average NYMEX WTI priced on the New York Mercantile Exchange was $99.75 per barrel for the year ended December 31, 2008 compared to $72.39 per barrel for the year ended December 31, 2007. Average crude oil charges were 142,938 bpd for the year ended December 31, 2008 compared to 146,046 bpd in 2007. For the year ended December 31, 2008, we realized an increase in raw material, freight and other costs as a result of net inventory losses of approximately $157.4 million after tax ($254.7 million pretax, comprised of a $184.5 million loss at the El Dorado Refinery and a $70.2 million loss at the Cheyenne Refinery) due to decreasing crude oil and refined product prices during the latter part of 2008. For the year ended December 31, 2007, we realized a decrease in raw material, freight and other costs as a result of net inventory gains of approximately $78.4 million after tax ($126.3 million pretax, comprised of a $84.9 million gain at the El Dorado Refinery and a $41.4 million gain at the Cheyenne Refinery) due to increasing crude oil and refined product prices during 2007.

The Cheyenne Refinery raw material, freight and other costs of $92.58 per sales barrel for the year ended December 31, 2008 increased from $62.08 per sales barrel in the same period in 2007 due to higher average crude oil prices, increased purchased products, lower light/heavy crude oil differentials and inventory losses in 2008 compared to inventory gains in 2007. Average crude oil charges of 43,590 bpd for the year ended December 31, 2008 were higher than the 41,778 bpd in 2007 because of a spring 2007 turnaround, a temporary shutdown of the FCCU in the third quarter of 2007, and a December 2007 fire in the coker unit at the Cheyenne Refinery. The heavy crude oil utilization rate at the Cheyenne Refinery expressed as a percentage of the total crude oil charge increased to 76% in the year ended December 31, 2008, from 72% in 2007. The light/heavy crude oil differential for the Cheyenne Refinery averaged $17.15 per barrel in the year ended December 31, 2008 compared to $18.95 per barrel in 2007.

The El Dorado Refinery raw material, freight and other costs of $99.94 per sales barrel for the year ended December 31, 2008 increased from $66.25 per sales barrel in the same period in 2007 due to higher average crude oil prices, lower light/heavy differentials and inventory losses in 2008 compared to inventory gains in 2007 partially offset by decreased overall crude oil charges. Average crude oil charges were 99,347 bpd for the year ended December 31, 2008, compared to 104,268 bpd in 2007. The decrease in average crude oil charges was due to the planned major turnaround work on the crude unit, the coker and the reformer during March and April of 2008. We realized a light/heavy crude oil differential of $17.85 per barrel during 2008 compared to $21.00 per barrel in 2007. For the year ended December 31, 2008, the heavy crude oil utilization rate at our El Dorado Refinery expressed as a percentage of the total crude oil charge was approximately 17%, compared to 15% in 2007. The WTI/WTS crude oil differential decreased from an average of $5.02 per barrel in the year ended December 31, 2007 to an average of $3.92 per barrel in 2008.

Refinery operating expenses. Refinery operating expenses, excluding depreciation, include both the variable costs (energy and utilities) and the fixed costs (salaries, taxes, maintenance costs and other) of operating the Refineries. Refinery operating expenses, excluding depreciation, increased $20.8 million, or 7%, to $321.4 million in the year ended December 31, 2008 from $300.5 million in 2007.

The Cheyenne Refinery operating expenses, excluding depreciation, were $116.7 million in the year ended December 31, 2008 compared to $109.2 million in 2007. The increased expenses and the 2008 compared to 2007 variances included: increased additives and chemicals costs ($4.4 million due to both price and volume increases), higher turnaround amortization ($2.8 million due to amortization of costs of 2007 turnarounds), higher electricity costs ($1.1 million due to both price and volume increases), increased natural gas costs ($819,000 due to increased prices partially offset by lower volumes), higher property and other taxes ($720,000 due to refinery additions), demurrage ($443,000) and training ($397,000). These increases were partially offset by decreased maintenance costs ($3.8 million) as 2007 maintenance costs included $3.8 million of costs relating to repairs from the December 2007 coker unit fire, and decreased environmental costs ($879,000).

The El Dorado Refinery operating expenses, excluding depreciation, were $204.7 million in the year ended December 31, 2008, increasing from $191.3 million for the year ended December 31, 2007. The primary areas of increased costs and the variance amounts for the 2008 period compared to the 2007 period were: increased maintenance costs ($9.5 million, primarily related to demolition, catalyst and repair costs incurred during the March 2008 turnaround), increased salaries and benefits expenses ($3.0 million, mostly due to increased overtime in relation to the March 2008 turnaround), higher electricity costs ($1.5 million), increased operating supplies costs ($710,000) and higher turnaround amortization ($571,000). These increases were partially offset by decreased environmental costs of $1.6 million because 2007 included $1.2 million in environmental penalties and there were no penalties in 2008.

Selling and general expenses. Selling and general expenses, excluding depreciation, decreased $11.2 million, or 20%, from $55.3 million for the year ended December 31, 2007 to $44.2 million for the year ended December 31, 2008, primarily due to the $6.3 million recognition of the loss on the Beverly Hills settlement during the year ended December 31, 2007. In addition, salaries and benefits expense (including stock-based compensation expense) during the year ended December 31, 2008 decreased $3.8 million compared to the same period in 2007. See Note 9 under “Stock-based Compensation” in the “Notes to Consolidated Financial Statements” for a detailed discussion of our stock-based compensation. Stock-based compensation expense was $17.2 million for the year ended December 31, 2008 compared to $20.0 million in 2007.

Depreciation, amortization and accretion. Depreciation, amortization and accretion increased $12.7 million, or 24%, from $53.0 million for the year ended December 31, 2007 to $65.8 million in 2008 because of increased capital investments in our Refineries, including our El Dorado Refinery crude unit and vacuum tower expansion project placed into service in the second quarter of 2008.

Net gains on sales of assets. The $44,000 gain on the sale of assets during the year ended December 31, 2008 compares to a $15.2 million gain on sale of assets in 2007. The 2007 gain resulted from a gain of $17.3 million from the sale of our 34.72% interest in a crude oil pipeline in Wyoming and a 50% interest in two crude oil tanks in Guernsey, Wyoming in September 2007, partially offset by the buyout and sale of a leased aircraft.

Interest expense and other financing costs. Interest expense and other financing costs of $15.1 million for the year ended December 31, 2008 increased $6.4 million, or 72%, from $8.8 million in 2007. The increase in interest expense related to interest of $4.9 million on the new 8.5% Senior Notes offering, $540,000 higher interest expense on the Utexam Master Crude Oil Purchase and Sale Contract (“Utexam Arrangement”) (see “Leases and Other Commitments” in Note 12 in the “Notes to Consolidated Financial Statement”), and $711,000 increased interest and facility fees on our revolving credit facility. Capitalized interest for the year ended December 31, 2008 was $6.6 million compared to $8.1 million in 2007. These increased expenses were partially offset by a $1.2 million reversal of prior years interest expenses for 2004 income tax contingency interest accruals due to the statute of limitations expiring. Average debt outstanding (excluding amounts payable under the Utexam Arrangement) increased to $398.1 million during the year ended December 31, 2008 from $150.0 million for the same period in 2007.

Interest and investment income. Interest and investment income decreased $16.4 million, or 75%, from $21.9 million in the year ended December 31, 2007 to $5.4 million in the year ended December 31, 2008, due to lower cash balances during the first eight months (prior to receiving the proceeds from our 8.5% Senior Notes offering) of 2008 and lower interest rates on invested cash.

Provision for income taxes. The provision for income taxes for the year ended December 31, 2008 was $26.8 million on pretax income of $107.0 million (or 25.0%) compared to $269.7 million on pretax income of $768.9 million (or 35.1%) in 2007. The effective tax rate for the year ended December 31, 2008 was lower than the effective tax rate in the comparable period in 2007 primarily from recognizing the benefit from $23.3 million of Kansas income tax credits for expansion projects at our El Dorado Refinery which reduced the effective tax rate (net of federal tax impact) by approximately 14%. The American Jobs Creation Act of 2004 (“the Act”) created Internal Revenue Code Section 199 (“Section 199”), which provides an income tax benefit to domestic manufacturers. We recorded income tax benefits under Section 199 of approximately $15.4 million and $5.7 million, in our 2007 and 2006 income tax provisions, respectively. The effective tax rate in 2008 was increased by approximately 2.9% due to reversing previously recognized 2007 and 2006 production activities deductions from filing an amended 2006 return in 2008 and the planned carryback of the 2008 taxable loss. The Company did not recognize a benefit from the production activities deduction in 2008, as it had a taxable loss. The Act also benefited our 2006 current income taxes payable by allowing us an accelerated depreciation deduction of 75% of qualified capital costs incurred to achieve low sulfur diesel fuel requirements (See “Environmental” under Note 12 in the “Notes to Consolidated Financial Statements”). The Act also provided for a $0.05 per gallon federal income tax credit on compliant diesel fuel up to an amount equal to the remaining 25% of these qualified capital costs. The $0.05 per gallon federal income tax credit allowed us to realize an $8.5 million federal income tax credit ($5.5 million excess tax benefit) and a $22.4 million federal income tax credit ($14.5 million excess tax benefit) in the years ended December 31, 2007 and 2006, respectively. This credit reduced our 2007 and 2006 income taxes payable and reduced our overall effective income tax rate for those years. The Energy Policy Act of 2005 added Section 179C to the Internal Revenue Code which provides an accelerated deduction for qualified capital costs incurred to expand an existing refinery. This accelerated deduction allows an expense deduction of 50% of such costs in the year the qualified projects are placed in service with the remaining costs depreciable under regular tax depreciation rules. This Section 179C deduction has benefited our cash flow for income taxes by reducing our taxable income for 2006 and 2007 and is a primary factor in our 2008 taxable loss. See “Income Taxes” in Note 8 in the “Notes to Consolidated Financial Statements” for more information on our income taxes and detailed information on our deferred tax assets.

2007 Compared with 2006

Overview of Results

We had net income for the year ended December 31, 2007, of $499.1 million, or $4.62 per diluted share, compared to net income of $379.3 million, or $3.37 per diluted share, in 2006. Our operating income of $755.8 million for the year ended December 31, 2007, reflected an increase of $181.6 million from the $574.2 million operating income for the comparable period in 2006. The average diesel crack spread was higher during 2007 ($22.19 per barrel) than in 2006 ($20.13 per barrel). The average gasoline crack spread was also higher during 2007 ($17.99 per barrel) than in 2006 ($12.82 per barrel), and the light/heavy crude oil differentials improved.

Specific Variances

Refined product revenues. Refined product revenues increased $510.0 million, or 11%, from $4.8 billion to $5.3 billion for the year ended December 31, 2007 compared to 2006. This increase was due to an increase in average product sales prices ($9.05 higher per sales barrel) partially offset by lower product sales volumes in 2007 (1,890 fewer bpd). Sales prices increased primarily as a result of increased crude oil prices and improvements in the gasoline and diesel crack spreads.

Manufactured product yields. Yields decreased 1,826 bpd at the El Dorado Refinery and 4,067 bpd at the Cheyenne Refinery for the year ended December 31, 2007 compared to 2006. Planned and unplanned shut downs at the Cheyenne Refinery during 2007 caused yields to be lower during 2007 than 2006. At the El Dorado Refinery, we processed more heavy crude oils during 2007 than in 2006, which resulted in decreased yields.

Other revenues. Other revenues decreased $117.2 million to an $80.9 million loss for the year ended December 31, 2007, compared to a $36.3 million gain in 2006, the sources of which were $86.4 million in net losses from derivative contracts in the year ended December 31, 2007 compared to net derivative gains of $34.6 million for the same period in 2006 offset by $4.8 million in gasoline sulfur credit sales in 2007 ($1.5 million in 2006). See “Price Risk Management Activities” under Item 7A and Note 11 in the “Notes to Consolidated Financial Statements” for a discussion of our utilization of commodity derivative contracts.

Raw material, freight and other costs. Raw material, freight and other costs increased by $188.3 million, or 5%, during the year ended December 31, 2007, from $3.9 billion in 2006 to $4.0 billion in 2007. The increase in raw material, freight and other costs when compared to 2006 was due to higher average crude prices, offset by lower crude oil charges and inventory gains in the year ended December 31, 2007 compared to inventory losses in the year ended December 31, 2006. We benefited from improved light/heavy crude oil differentials during the year ended December 31, 2007 compared to 2006. The average WTI crude oil priced on the New York Mercantile Exchange was $72.39 for the year ended December 31, 2007 compared to $66.22 for the year ended December 31, 2006. Average crude oil charges were 146,046 bpd for the year ended December 31, 2007, compared to 154,473 bpd in 2006. For the year ended December 31, 2007, we realized a decrease in raw material, freight and other costs as a result of net inventory gains of approximately $78.4 million after tax ($126.3 million pretax, comprised of an $84.9 million gain at the El Dorado Refinery and a $41.4 million gain at the Cheyenne Refinery) due to increasing crude oil and refined product prices during 2007. For the year ended December 31, 2006, we realized an increase in raw material, freight and other costs as a result of net inventory losses of approximately $16.1 million after tax ($25.7 million pretax, comprised of a $31.7 million loss at the El Dorado Refinery and a $6.0 million gain for the Cheyenne Refinery) due to decreasing crude oil and refined product prices during the latter part of 2006.