| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| FORM N-CSR |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

| Investment Company Act file number 811-09903 |

| Mellon Funds Trust |

| (Exact name of Registrant as specified in charter) |

| c/o The Dreyfus Corporation |

| 200 Park Avenue |

| New York, New York 10166 |

| (Address of principal executive offices) (Zip code) |

| Mark N. Jacobs, Esq. |

| 200 Park Avenue |

| New York, New York 10166 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: (212) 922-6000 |

| Date of fiscal year end: | 08/31 | |

| Date of reporting period: | 02/28/2007 |

FORM N-CSR

| Item 1. | Reports to Stockholders. |

The Mellon Funds

| Mellon Large Cap Stock Fund |

| Mellon Income Stock Fund |

| Mellon Mid Cap Stock Fund |

| Mellon Small Cap Stock Fund |

| Mellon International Fund |

| Mellon Emerging Markets Fund |

| Mellon Balanced Fund |

SEMIANNUAL REPORT February 28, 2007

| Contents | ||

| The Funds | ||

| Letter from the President | 2 | |

| Discussion of Funds’ Performance | ||

| Mellon Large Cap Stock Fund | 3 | |

| Mellon Income Stock Fund | 5 | |

| Mellon Mid Cap Stock Fund | 7 | |

| Mellon Small Cap Stock Fund | 9 | |

| Mellon International Fund | 11 | |

| Mellon Emerging Markets Fund | 13 | |

| Mellon Balanced Fund | 15 | |

| Understanding Your Fund’s Expenses | 17 | |

| Comparing Your Fund’s Expenses | ||

| With Those of Other Funds | 18 | |

| Statements of Investments | 19 | |

| Statements of Assets and Liabilities | 46 | |

| Statements of Operations | 48 | |

| Statements of Changes in Net Assets | 50 | |

| Financial Highlights | 55 | |

| Notes to Financial Statements | 70 | |

For More Information

Back cover

The views expressed herein are current to the date of this report. These views and the composition of the funds’ portfolios are subject to change at any time based on market and other conditions.

| • Not FDIC-Insured |

| • Not Bank-Guaranteed |

| • May Lose Value |

The Funds

| LETTER FROM |

| THE PRESIDENT |

Dear Shareholder:

We are pleased to present this semiannual report for the Mellon Funds Trust, covering the six-month period from September 1, 2006, through February 28, 2007.

Despite a sudden bout of market volatility near the end of February 2007, the U.S. stock market fared relatively well. Domestic stock prices generally were propelled higher by stabilized short-term rates, moderate inflationary pressures, and robust corporate earnings. In international markets, the European and Asian markets posted very strong returns as well, boosted by fiscal reforms in many emerging markets and a surge in mergers-and-acquisitions activity and corporate reorganizations. Although the U.S. and other developed economies have shown signs of decelerating, many economists currently feel the risk of a full-blown recession is extremely small.

We remain optimistic about the sustainability of the current economic expansion. Productivity has increased as modern technologies and efficient business practices helped to limit cyclical inflation pressures around the world. Over the more immediate term, a warm winter in the U.S. and rapidly declining energy prices have mitigated the risks that weakness in the U.S. housing sector might derail business and consumer confidence.The overall result has been to bolster investor sentiment and stock prices.

For information about how each fund performed during the reporting period, as well as market perspectives, we have provided a Discussion of Fund Performance.

As always, we encourage you to talk with your portfolio manager to help ensure that your portfolio remains aligned with your current financial needs and future investment goals.

Thank you for your continued confidence and support.

| Christopher E. Sheldon |

| President |

| Mellon Funds Trust | ||

| March 15, 2007 |

| DISCUSSION OF FUND PERFORMANCE |

Michael D. Weiner, Portfolio Manager

How did Mellon Large Cap Stock Fund perform relative to its benchmark?

For the six-month period ended February 28, 2007, the fund’s Class M shares produced a total return of 7.81% while its Investor shares produced a total return of 7.66% .1 In comparison, the total return of the Standard & Poor’s 500 Composite Stock Price Index (“S&P 500 Index”), the fund’s benchmark, was 8.93% for the same period.2

Stocks were driven higher during the reporting period by continued U.S. economic growth, stable short-term interest rates and rising corporate earnings. The fund participated in the market’s rise to a significant degree, producing particularly strong returns in the materials, telecommunications services, consumer discretionary, utilities and financial services sectors. However, relatively weak returns in the health care and technology areas undermined the fund’s performance compared to the benchmark.

In addition, on February 23, 2007, Sean P. Fitzgibbon became the fund’s primary portfolio manager. The fund will continue to seek capital appreciation as its investment objective.

What is the fund’s investment approach?

The fund seeks capital appreciation.To pursue its goal, the fund normally invests at least 80% of its assets in stocks of large-cap companies. We choose stocks through a disciplined investment process that uses computer modeling techniques to identify and rank companies based on value, growth and other financial characteristics. Next, we use fundamental analysis to select the most attractive of the higher ranked securities, drawing on a variety of internal and Wall Street research sources. We also attempt to manage risks by diversifying the fund’s investments across companies and industries, maintaining weightings and risk characteristics that generally are similar to those of the S&P 500 Index.

What other factors influenced the fund’s performance?

While the market’s advance was broadly based, high levels of volatility and short-term stock price fluctuations were a significant influence on fund performance. Price volatility proved to be detrimental during the final months of 2006, but it worked in the fund’s favor during January and February 2007, nearly making up for the fund’s earlier underperfor-mance relative to the benchmark.

The fund produced some of its greater gains in the basic materials sector, where top performers included raw materials producers, such as Freeport-McMoRan Copper & Gold, industrial gas producer Air Products and Chemical, Inc. and nickel mining company Inco, which merged with another of the fund’s holdings, iron producer Companhia Vale do Rio Doce. In the telecommunications services area, gains in stocks such as Sprint Nextel enabled the fund to roughly match the benchmark’s strong returns from the sector.

The fund also derived robust gains from consumer discretionary holdings such as motorcycle maker Harley-Davidson, residential homebuilder D. R. Horton and automobile products producer Harman International Industries. These winners largely compensated for weaker returns from other consumer discretionary holdings, such as Starbucks, and from the fund’s lack of exposure to strong-performing cable service providers. Among utilities stocks, the fund’s position in Dynegy Cl. A performed well, due to an increase in private equity investment in energy generation and transmission companies. Finally, in the finan-

The Funds 3

DISCUSSION OF FUND PERFORMANCE (continued)

cial services sector, the fund delivered relatively positive performance through its emphasis on brokerage firms, such as Goldman Sachs Group, Lehman Brothers Holdings and JPMorgan Chase & Co.

On the negative side, health care and technology holdings detracted from the fund’s relative performance. Biotechnology giant Amgen was hurt by concerns regarding competitive issues and government reimbursement rates. In the technology area, the fund’s performance was hurt by significant exposure to Motorola, which dropped sharply when the company lost ground in the cellular handset market.

What is the fund’s current strategy?

As of the end of the reporting period, we have allocated a slightly greater percentage of the fund’s assets to technology stocks than the benchmark in light of attractive valuations, favorable product cycles and a positive corporate spending environment. Similarly, in the health care sector, a slightly overweight position reflects our favorable view of the sector’s long-term prospects as the U.S. population ages. We also have placed modest emphasis on energy stocks, where we see strong business fundamentals for drillers and oilfield services companies.

On the other hand, we have slightly reduced the fund’s consumer discretionary exposure in response to the potential for weakening consumer spending given current turmoil in the mortgage lending market.The fund also holds underweight exposure to the telecommunications services sector, where the competitive landscape appears uncertain and many companies face the need to make significant capital expenditures. It should be noted, however, that these over- and underweight positions were mild. In general, the fund remained true to its disciplined, sector-neutral investment approach.

More broadly, we believe current market valuations and economic trends toward slowing, but reasonable, growth are likely to favor the kinds of large-cap, high-quality, financially sound companies in which the fund invests.

March 15, 2007

| 1 | Total return includes reinvestment of dividends and any capital gains paid. | |

| Past performance is no guarantee of future results. Share price and investment | ||

| return fluctuate such that upon redemption, fund shares may be worth more or | ||

| less than their original cost. | ||

| 2 | SOURCE: LIPPER INC. — Reflects the monthly reinvestment of | |

| dividends and, where applicable, capital gain distributions.The Standard & | ||

| Poor’s 500 Composite Stock Price Index is a widely accepted, unmanaged | ||

| index of U.S. stock market performance. Index return does not reflect fees and | ||

| expenses associated with operating a mutual fund. |

| 4 |

| DISCUSSION OF |

| FUND PERFORMANCE |

Brian Ferguson, Portfolio Manager

Note to Shareholders: On February 23, 2007, D. Gary Richardson was replaced as the fund’s primary portfolio manager.

How did Mellon Income Stock Fund perform relative to its benchmark?

For the six-month period ended February 28, 2007, the fund’s Class M shares produced a total return of 7.33%, and its Investor shares produced a total return of 7.17% .1 In comparison, the Russell 1000 Value Index, the fund’s benchmark, provided a total return of 9.82% .2

Continued economic growth and strong corporate earnings drove stocks higher over the reporting period. The market’s performance proved to be broadly based, with most industry groups generating gains. The fund participated in the stock market’s advance to a significant degree, achieving notably good returns in the consumer staples sector and roughly matching the benchmark in several other key areas. However, relatively weak stock selection within the health care, financials and industrials sectors caused the fund’s returns to lag the benchmark.

What is the fund’s investment approach?

The fund seeks total return consisting of capital appreciation and income.To pursue its goal, the fund normally invests at least 80% of its assets in stocks. The fund seeks to focus on dividend-paying stocks and other investment techniques that produce income.We choose stocks through a disciplined investment process that combines computer modeling techniques, fundamental analysis and risk management. While we attempt to manage risks by diversifying broadly across companies and industries, the fund may at times overweight certain sectors in an attempt to earn higher yields.The fund may also use derivatives as a substitute for taking a position in an underlying asset, to increase returns or income, or as part of a hedging strategy.

What other factors influenced the fund’s performance?

In an environment characterized by moderate economic growth, subdued inflation and stable interest rates, market sentiment tended to favor relatively speculative issues rather than the income-producing, value-oriented stocks on which the fund focused. Even within the fund’s benchmark, lower-yielding, more volatile stocks produced stronger returns during the reporting period.

The impact of this trend was most evident in three sectors. In the health care sector, where the fund maintained mildly overweight exposure, dividend-paying pharmaceutical companies, such as Eli Lilly and GlaxoSmithKline, suffered declines due to concerns regarding the companies’ new product pipelines.While the fund invested in some of the sector’s better performers, such as Bristol-Myers Squibb, these stocks failed to make up for other, more disappointing stock selections. Among financial stocks, the fund invested in relatively few brokerage firms due to what we believed were the group’s high valuations and poor record of dividend growth; however, brokerage firms proved to be among the sector’s best performers during the reporting period. Finally, in the industrials sector, the fund emphasized major dividend-paying stocks, such as 3M, General Electric and United Technologies, at a time when smaller, more speculative stocks produced greater gains.

The fund matched or exceeded the benchmark’s performance in several sectors. Strong individual stock selections in the consumer discretionary sector enabled the fund to match the benchmark’s returns despite an underweight position in the high-flying cable industry. Top holdings included media giant News Corp. and casino and resort operator Harrah’s Entertainment. In the telecommunications services sector, strong stock selection and an overweight position in the sector helped produce competitive returns

The Funds 5

DISCUSSION OF FUND PERFORMANCE (continued)

among holdings such as AT&T, which benefited from rising earnings forecasts, and Verizon, which generated excitement over its deployment of fiber optic services to its customers’ homes.

Among basic materials stocks, the fund roughly matched the benchmark’s robust returns with holdings such as Monsanto and DuPont, which prospered as a result of greater emphasis in the United States on ethanol as a petroleum substitute; and Temple-Inland, which announced plans to divest its financial holdings to focus more intently on its core containerboard business. In the utilities sector, strong industrial demand and limited energy supplies broadly bolstered returns. Finally, in the consumer staples sector, the fund outperformed the benchmark primarily on the strength of Avon Products, which generated higher revenues from existing operations as well as expanding its presence in China.

What is the fund’s current strategy?

We continue to focus on what we believe are attractively valued, large-cap stocks with strong growth rates that are generating consistent cash flows. In addition, we have emphasized companies that either pay dividends or offer prospects for paying dividends in the near future.

As of the reporting period’s end, we have found a relatively large number of what we believe are attractively valued investments meeting our criteria in the technology sector, where we see opportunities for potential growth.The fund also holds relatively sizeable exposure to health care stocks, with an emphasis on pharmaceutical companies that are cutting costs to improve earnings in the face of competition from generic drugs. On the other hand, the fund holds a mildly underweight position in the energy sector, where growth opportunities currently appear to us limited.The fund’s financial sector exposure is somewhat light as well, particularly among, in our view, richly valued real estate investment trusts and regional banks, which appear vulnerable to credit problems.

March 15, 2007

| 1 | Total return includes reinvestment of dividends and any capital gains paid. | |

| Past performance is no guarantee of future results. Share price and investment | ||

| return fluctuate such that upon redemption, fund shares may be worth more or | ||

| less than their original cost. | ||

| 2 | SOURCE: LIPPER INC. — Reflects the reinvestment of dividends and, | |

| where applicable, capital gain distributions.The Russell 1000 Value Index is | ||

| an unmanaged index that measures the performance of those Russell 1000 | ||

| companies with lower price-to-book ratios and lower forecasted growth values. | ||

| Index return does not reflect fees and expenses associated with operating a | ||

| mutual fund. |

| 6 |

| DISCUSSION OF |

| FUND PERFORMANCE |

James C. Wadsworth, Portfolio Manager

How did Mellon Mid Cap Stock Fund perform relative to its benchmark?

For the six-month period ended February 28, 2007, the fund produced total returns of 11.16% for its Class M shares, 10.98% for its Investor shares and 10.62% for its Dreyfus Premier shares.1 In comparison, the Standard & Poor’s MidCap 400 Index (“S&P 400 Index”), the fund’s benchmark, produced a total return of 12.44% for the same period.2

Midcap stocks generally gained value over the reporting period as investors responded favorably to moderating economic growth, diminishing inflationary pressures, stable interest rates and rising corporate earnings.While the fund participated in the market’s rally to a significant degree, individual disappointments in the information technology, health care, consumer staples and energy sectors caused the fund’s returns to lag the benchmark.

What is the fund’s investment approach?

The fund seeks capital appreciation by normally investing at least 80% of its assets in stocks of domestic companies with market capitalizations between $1 billion and $10 billion at the time of purchase.When selecting securities, we begin with quantitative analysis to screen and rank stocks within each industry and sector based on valuation, earnings growth and financial health.We then use fundamental analysis to evaluate and select individual stocks, drawing on research by internal analysts and external Wall Street sources. Finally, we use portfolio construction techniques to manage sector and industry risks. Our goal is to keep those risks at levels that are similar to those of the S&P 400 Index.

What other factors influenced the fund’s performance?

Early in the reporting period, investors’ concerns regarding robust economic growth and higher inflation began to subside as housing markets cooled and energy prices fell.The Federal Reserve Board lent credence to a more benign inflation outlook when it refrained from raising short-term interest rates after more than two years of rate hikes. These factors, together with expectations of an economic “soft landing” and strong corporate earnings, helped fuel a stock market rally through the end of February, when turbulence in Chinese equity markets triggered a sharp U.S. market correction.

In this generally favorable market environment, investors apparently felt comfortable assuming the risks that midcap companies typically entail. As a result, midcap stocks generally produced higher returns than their large-cap counterparts, extending a cycle of smaller-stock dominance that has persisted for the better part of six years.

The fund received especially strong contributions to its relative performance from the industrials sector, where specialty metals producer Precision Castparts benefited from better-than-expected earnings and new orders from industrial giant General Electric. In the materials area, metals producer Allegheny Technologies saw its stock price advance strongly due to robust earnings stemming from rising stainless steel and titanium sales. In addition, a number of construction aggregate providers prospered in a consolidating industry amid greater federal highway spending and ongoing recovery efforts in areas affected by Hurricane Katrina in 2005.

Among financial stocks, investments in securities exchanges enabled the fund to benefit from intensifying mergers-and-acquisitions (“M&A”) activity, including the acquisition of New York Board of Trade by electronic futures exchange Intercontinental Exchange. Utilities holdings Dynegy, Cl A. and Northeast Utilities were rewarded with higher valuations for achieving improved revenues and earnings. In the consumer discretionary sector, the fund received positive contributions to relative performance from lodging chain Hilton Hotels, apparel retailer Urban Outfitters and superstore Dick’s Sporting Goods.

The Funds 7

DISCUSSION OF FUND PERFORMANCE (continued)

Gains in these market sectors were offset by lagging returns in other areas. In the information technology sector, strong results from outsourcer Cognizant Technology Solutions, Cl. A, and communications equipment maker Polycom were more than offset by weakness in Linux software developer Red Hat, which encountered greater competitive pressures, and semiconductor manufacturer Microsemi, which made an acquisition that many analysts considered expensive. Consequently, we sold our Red Hat and Microsemi positions early in the reporting period. In the health care sector, contract research organization Pharmaceutical Product Development and medical services provider Omnicare were hurt by the loss of major contracts and lower-than-expected earnings. Pepsi Bottling Group undermined results in the consumer staples sector when earnings came in lower than anticipated. Finally, declining commodity prices and unusually warm winter weather in many parts of the United States hurt returns of stocks comprising the energy sector.

What is the fund’s current strategy?

Although we have maintained the fund’s sector-neutral allocation strategy, we have identified a number of trends

within certain industry groups that we believe may send stock prices of individual companies higher. These trends include the impending retirement of the baby boom generation, the need for construction materials to build and maintain the nation’s infrastructure, strong federal spending on aerospace and defense, the need for new power plants and transmission lines, and growth in the delivery of broadband-intensive applications on the Internet. In our judgment, long-term secular trends such as these may fuel the growth of midcap companies. In addition, midcap businesses rank among the main candidates for purchase by larger enterprises in an environment that we expect to be characterized by additional M&A activity.

March 15, 2007

| 1 | Total return includes reinvestment of dividends and any capital gains paid. | |

| Past performance is no guarantee of future results. Share price and investment | ||

| return fluctuate such that upon redemption, fund shares may be worth more or | ||

| less than their original cost. | ||

| 2 | SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where | |

| applicable, capital gain distributions.The Standard & Poor’s MidCap 400 Index | ||

| is a widely accepted, unmanaged total return index measuring the performance of | ||

| the midsize company segment of the U.S. stock market. Index return does not | ||

| reflect the fees and expenses associated with operating a mutual fund. |

| 8 |

| DISCUSSION OF |

| FUND PERFORMANCE |

Dwight E. Cowden, Portfolio Manager

How did Mellon Small Cap Stock Fund perform relative to its benchmark?

For the six-month period ended February 28, 2007, the fund’s Class M shares produced a total return of 8.50%, and its Investor shares produced a total return of 8.38%.1 In comparison, the fund’s benchmark, the Standard & Poor’s SmallCap 600 Index (the “Index”), produced a total return of 10.46% for the same period.2

As they have for some time, small-cap stocks continued to produce generally higher returns than their large-cap counterparts during the reporting period. Investors responded positively to moderate economic growth, subdued inflation, steady interest rates and rising corporate earnings.The fund achieved lower returns than the Index, primarily due to disappointing returns from consumer-oriented stocks early in the reporting period.

What is the fund’s investment approach?

The fund seeks capital appreciation.To pursue its goal, the fund normally invests at least 80% of its assets in stocks of small capitalization companies whose market capitalizations generally range between $100 million and $3 billion at the time of purchase. We choose growth and value stocks using a disciplined process that combines computer modeling, fundamental analysis and risk management. We use a computer model to rank stocks within an industry or sector based on valuation, earnings growth and the company’s financial profile.We examine the fundamentals of the higher-ranked securities, and we select those we believe to be the most attractive.We use portfolio construction techniques to manage sector and industry risks, and we attempt to keep those risks at levels that are similar to those of the Index.

What other factors influenced the fund’s performance?

Small-cap stocks posted relatively strong returns over the reporting period, achieving gains in every market sector of the Index.As previous concerns over higher inflation and volatile energy prices began to ease, investors looked forward to more moderate economic growth and stable interest rates. In addition, small-cap stocks benefited from ample global liquidity as risk-tolerant investors sought high returns. Other positive factors included rising mergers-and-acquisitions (“M&A”) activity, including several large leveraged buyouts, and persistently low yields on 10-year U.S. Treasury securities, which helped keep borrowing costs affordable.

Small-cap stocks achieved some of their stronger gains in the materials and industrials sectors, as robust global demand and lower raw materials costs boosted earnings. Particularly strong contributions to the fund’s performance came from chemical producers Terra Industries and Nalco Holding. Terra Industries, a fertilizer producer, benefited from strong sales and profit growth arising from above-average corn planting, price increases and falling natural gas costs. Nalco’s stock price appreciated as investors gained greater confidence in management’s ability to cut costs while realigning the sales force to improve organic growth. Among steel producers, global industry consolidation and price increases helped boost returns from RTI International and AK Steel.

The fund also derived competitive results from the utilities sector. Electricity generator Dynegy Cl A. benefited from M&A activity within its industry as well as the sale of non-strategic assets. Management continued to rationalize the company’s portfolio of power plants, alleviating investor concerns regarding the company’s balance sheet.

The Funds 9

DISCUSSION OF FUND PERFORMANCE (continued)

On the other hand, the fund’s relative returns fell short of the Index in the health care sector, where disappointing stock selections in the biotechnology industry weighed on performance. Foxhollow Technologies reported a slowdown in sales of its leading product for arterial plaque removal. Panacos Pharmaceuticals announced delays in the launch of a key drug. Finally, Advanced Medical Optics was hurt by lower-than-expected laser vision sales and subdued forward earnings guidance.As a result, we sold our positions of these companies throughout the reporting period.

In the consumer discretionary sector, retailers encountered difficulties due to weather-related issues and slower holiday spending. Coldwater Creek, one of the fund’s larger holdings, suffered from disappointing same-store sales and increased inventories as warm weather held back shopping for winter-related merchandise. Bebe Stores suffered from similar problems, resulting in weaker-than-expected sales and increased markdowns. Nutrisystems announced higher marketing costs and a disappointing outlook for Internet sales of its products.

Finally, results from the financials sector were hurt by the fund’s relatively light exposure to real estate investment trusts (REITs). Surprisingly strong gains in the office and entertainment areas of the REIT sub-sector outpaced the fund’s overweight positions in lodging-related companies.

What is the fund’s current strategy?

We have continued to employ our longstanding investment approach, which combines quantitative screens with fundamental analysis to find what we believe are opportunities for growth. While our sector-neutral risk management strategy has remained intact, our “bottom-up” process has identified a greater number of opportunities in the consumer discretionary sector, where lagging performance over the reporting period has, in our view, created more attractive risk/reward profiles for many companies. Conversely, we have found fewer stocks meeting our criteria in the materials sector due to strong recent performance and typical seasonal weak-ness.We also have continued to focus on several investment themes — healthy living, consolidating industries, internet growth beneficiaries and global growth — that we believe will help propel the growth of certain companies and industries.

March 15, 2007

| 1 | Total return includes reinvestment of dividends and any capital gains paid. | |

| Past performance is no guarantee of future results. Share price and investment | ||

| return fluctuate such that upon redemption, fund shares may be worth more or | ||

| less than their original cost. | ||

| 2 | SOURCE: LIPPER INC. — Reflects the reinvestment of dividends and, | |

| where applicable, capital gain distributions.The Standard & Poor’s SmallCap | ||

| 600 Index is a broad-based index and a widely accepted, unmanaged index of | ||

| overall small-cap stock market performance.The Index does not take into | ||

| account fees and expenses to which the fund is subject. |

10

| DISCUSSION OF |

| FUND PERFORMANCE |

D. Kirk Henry and Remi J. Browne, Portfolio Managers

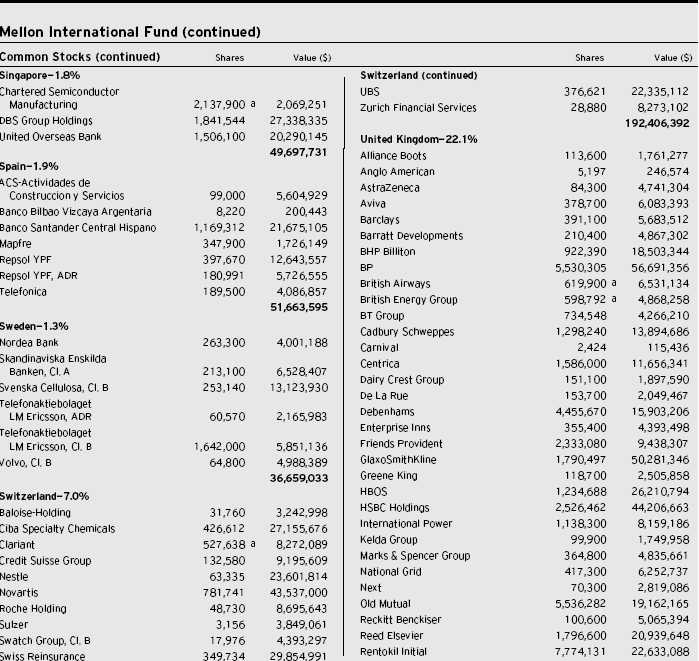

How did Mellon International Fund perform relative to its benchmark?

For the six-month period ended February 28, 2007, the fund’s Class M shares produced a total return of 10.16%, and its Investor shares produced a total return of 10.02% .1 The fund’s benchmark, the Morgan Stanley Capital International Europe, Australasia, Far East Index (“MSCI EAFE Index”), produced a total return of 12.17% for the same period.2

In an environment of strong global economic growth and favorable business dynamics, international stock markets continued to gain value throughout the reporting period. Although the fund was able to participate in the global markets’ rise to a degree, its returns lagged the benchmark, primarily due to an overweight position in Japanese financial and consumer-related stocks, which suffered during the reporting period due to the region’s slower-than-expected economic recovery.

What is the fund’s investment approach?

The fund seeks long-term capital growth. To pursue this goal, the fund normally invests at least 65% of its total assets in equity securities of foreign issuers.

Since June 30, 2005, the fund generally invests most of its cash inflows (purchases of fund shares and reinvested distributions) in accordance with a core investment style under the direction of the fund’s co-primary portfolio manager, Remi J. Browne.The fund’s portfolio as of June 30, 2005, will continue to be managed in accordance with the value-oriented investment style under the direction of the fund’s other co-primary portfolio manager, D. Kirk Henry. The allocation of cash inflows and outflows will be at the discretion of the investment adviser depending on the circumstances; however, under normal circumstances, generally between 90% and 100% of cash inflows will be allocated to the core investment style.We believe that by implementing a core investment style with respect to such assets, the fund may take advantage of investment opportunities in international markets that may not fall within the value-oriented investment style previously employed for the fund’s entire portfolio.

Pursuant to the core investment style, under normal circumstances, at least 80% of the fund’s cash inflows allocated to this style is invested in equity securities of companies located in the foreign countries represented in the Index and Canada.

The fund will continue to invest in stocks that appear to be undervalued (as measured by their price/earnings ratios), but stocks purchased pursuant to the core investment style may have value and/or growth char-acteristics.The core investment style portfolio manager employs a “bottom-up” investment approach, which emphasizes individual stock selection.The core investment style stock selection process is designed to produce a diversified portfolio that, relative to the Index, has a below-average price/earnings ratio and an above-average earnings growth trend.

The fund’s investment approach for the portion of the fund using the value-oriented investment style is research-driven and risk-averse. When selecting stocks, we identify potential investments through extensive quantitative and fundamental research. Emphasizing individual stock selection over economic or industry trends, the fund focuses on three key factors: value, business health and business momentum.

What other factors influenced the fund’s performance?

During the reporting period, international equity markets posted generally strong gains fueled by corporate restructuring and mergers-and-acquisitions activities throughout much of Europe. High levels of busi-

The Funds 11

DISCUSSION OF FUND PERFORMANCE (continued)

ness confidence, positive earnings announcements and favorable economic growth forecasts in most countries also supported stock prices. Even a modest global stock market correction during the summer had little effect as international stocks quickly recovered and generally continued to gain value through the balance of the reporting period.

While the fund also benefited from these conditions, its lagging relative performance can be attributed primarily to its overweight position in Japan, where we emphasized companies that were closely tied to the domestic economy, which has not yet accelerated. In addition, two Japanese consumer lenders, Takefuji and Aiful, fell sharply following the adoption of new government regulations designed to lower the debt burden of lower income borrowers. Japan’s domestic economy remains in a recovery phase, but it has been slow to gain momentum. Financial and consumer-related stocks also fell in this environment, including shares of Dentsu Corporation, a large advertising firm. In addition, the fund’s limited exposure to a number of Japanese auto and technology exporters that performed well also hurt its relative performance.

The fund enjoyed better results in Europe, where aggressive corporate restructuring efforts, strong export activities and improving domestic economic conditions bolstered a number of the fund’s German holdings. Notable performers included E.On AG., one of the country’s top electricity suppliers; Siemens AG, the electronics and electrical engineering giant; and Deutsche Post, whose

DHL arm has expanded to become well positioned in Asia and Russia. In the United Kingdom, the fund benefited from its overweight positions in Centrica, the private gas supplier and distributor, and Smiths Group, the industrial giant whose stock price rose sharply on news of a buyout of its aerospace division from General Electric. Also in the U.K., wireless carrier Vodafone Group flourished during the fourth quarter of 2006 as part of an industry-wide rebound in the telecommunications services sector.

What is the fund’s current strategy?

As of the end of the reporting period, we have found a number of investment opportunities in the health care, energy and consumer discretionary areas,where we believe stock prices have fallen to more attractive valuations. On the other hand, we are seeing fewer opportunities in the utilities industry, where valuations appear too high to meet our investment criteria. In our judgment, the fund remains well positioned to potentially capture value-oriented opportunities in international markets.

March 15, 2007

| 1 | Total return includes reinvestment of dividends and any capital gains paid. | |

| Past performance is no guarantee of future results. Share price and investment | ||

| return fluctuate such that upon redemption, fund shares may be worth more or | ||

| less than their original cost. | ||

| 2 | SOURCE: LIPPER INC.— Reflects reinvestment of net dividends and, | |

| where applicable, capital gain distributions.The Morgan Stanley Capital | ||

| International Europe, Australasia, Far East (MSCI EAFE) Index is an | ||

| unmanaged index composed of a sample of companies representative of the | ||

| market structure of European and Pacific Basin countries. Index return does | ||

| not reflect fees and expenses associated with operating a mutual fund. |

12

| DISCUSSION OF |

| FUND PERFORMANCE |

D. Kirk Henry and Daniel B. LeVan, Portfolio Managers

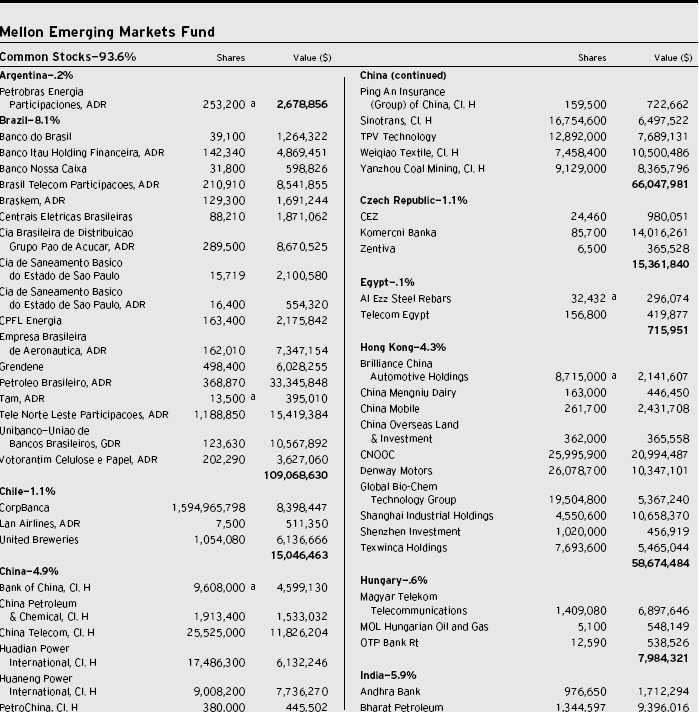

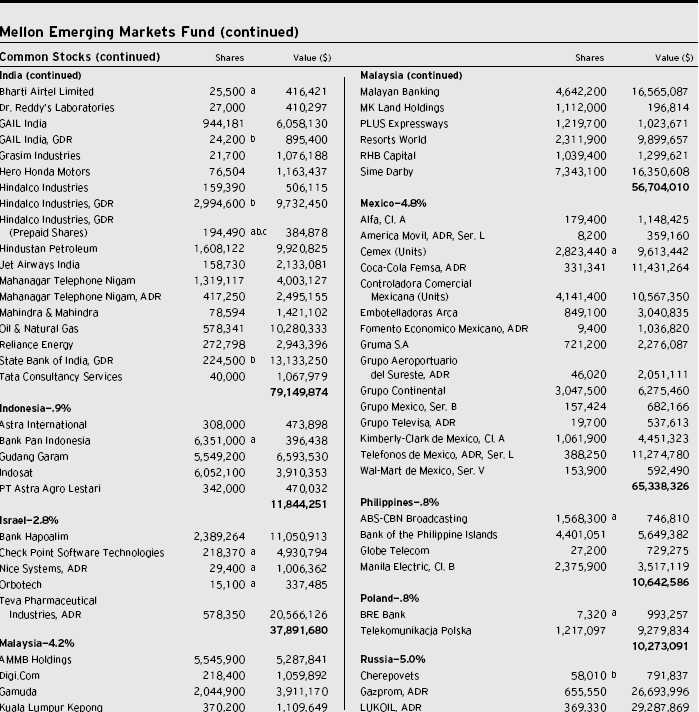

How did Mellon Emerging Markets Fund perform relative to its benchmark?

For the six-month period ended February 28, 2007, the fund’s Class M shares produced a total return of 14.67%, and the fund’s Investor shares produced a total return of 14.52% .1 In comparison, the Morgan Stanley Capital International Emerging Markets (Free) Index (the “Index”), the fund’s benchmark, provided a total return of 16.61% for the same period.2

We attribute the emerging markets’ strong performance to growing global demand for the natural resources produced by many developing nations. The fund’s returns fell short of the benchmark, primarily due to its lack of exposure to better-performing companies in China, India and Brazil.

What is the fund’s investment approach?

The fund seeks long-term capital growth.To pursue its goal, the fund invests at least 80% of its assets in equity securities of companies organized, or with a majority of assets or operations, in countries considered to be emerging markets.

The fund invests most of its cash inflows received since June 30, 2005, in accordance with a core investment style. The fund’s portfolio as of June 30, 2005, was invested in companies the investment adviser considered to be “value” companies. Pursuant to the core investment style, under normal circumstances, at least 80% of the fund’s cash inflows allocated to this style are invested in equity securities of companies located in the foreign countries represented in the Index.

The allocation of cash inflows and outflows will be at the discretion of the investment adviser depending on the circumstances; however, under normal circumstances, generally between 90% and 100% of cash inflows will be allocated to the core investment style.

We believe that by implementing a core investment style with respect to such assets, the fund may take advantage of investment opportunities in emerging markets that may not fall within the value-oriented investment style previously employed for the fund’s entire portfolio.

The fund will continue to invest in stocks that appear to be undervalued (as measured by their price/earnings ratios), but stocks purchased pursuant to the core investment style may have value and/or growth characteristics. The core investment style portfolio manager employs a “bottom-up” investment approach, which emphasizes individual stock selection. The core investment style stock selection process is designed to produce a diversified portfolio that, relative to the Index, has a below-average price/earnings ratio and an above-average earnings growth trend.

When choosing stocks for the portion of the fund using the value-oriented investment style, we use a research-driven and risk-averse approach. We identify potential investments through extensive quantitative and fundamental research. Emphasizing individual stock selection rather than economic and industry trends, we focus on three key factors: value, business health and business momentum.

What other factors influenced the fund’s performance?

The emerging markets continued to post strong gains during the reporting period in a decidedly upbeat global economic environment. Rich in iron ore, oil, copper and other natural resources, many emerging markets’ countries continued to benefit from rising global demand for the commodities and construction materials needed to build the world’s industrial infrastructures.

While the fund participated in the market’s gains to a substantial degree, it modestly underperformed its benchmark due to its limited exposure to stocks in China, India and Brazil that we deemed too richly

The Funds 13

DISCUSSION OF FUND PERFORMANCE (continued)

valued. For example, in China, the fund’s relatively light exposure to financial services companies hindered returns during a period of increased consumer lending. In India, a lack of exposure to industrial firms and software developers detracted from performance. In Brazil, an underweight position in Companhia Vale do Rio Doce (CVRD), the world’s largest iron ore miner, held back returns, as did relatively heavy exposure to integrated oil and gas producer Petrobras, which fell sharply when oil prices retreated.

The fund achieved better success with its holdings in the Philippines, Malaysia and Russia.The Philippines benefited from strong intra-Asian trade as well as lower prices for imported oil. In addition, utility Manila Electric advanced during the reporting period on the heels of governmental reforms that could allow it to pass higher costs along to consumers. In Malaysia, the recent passage of the “Ninth Malaysian Plan,” a comprehensive expansion of government investment in various infrastructure projects and public works, helped fuel gains in Sime Darby, an industrial conglomerate, and Gamuda, a large construction firm. Significantly underweight exposure

to stocks in Russia also benefited the fund, including relatively light holdings of oil and gas companies hurt by falling commodity prices.

What is the fund’s current strategy?

As of the end of the reporting period, we have found what we believe to be attractive investment opportunities in Taiwan and South Korea. Conversely, we have identified fewer opportunities in Russia and China. On a sector basis, we have favored stocks of consumer discretionary companies and utilities over shares of companies in the materials and energy sectors.

March 15, 2007

| 1 | Total return includes reinvestment of dividends and any capital gains paid. | |

| Past performance is no guarantee of future results. Share price and investment | ||

| return fluctuate such that upon redemption, fund shares may be worth more or | ||

| less than their original cost. | ||

| 2 | SOURCE: LIPPER INC. — Reflects reinvestment of gross dividends and, | |

| where applicable, capital gain distributions.The Morgan Stanley Capital | ||

| International Emerging Markets (Free) Index is a market capitalization- | ||

| weighted index composed of companies representative of the market structure of | ||

| 26 emerging market countries in Europe, Latin America and the Pacific Basin. | ||

| Index return does not reflect fees and expenses associated with operating a | ||

| mutual fund. |

| 14 |

| DISCUSSION OF |

| FUND PERFORMANCE |

Sean P. Fitzgibbon and John F. Flahive, Portfolio Managers

Note to Shareholders: On February 23, 2007, Sean Fitzgibbon replaced Michael Wiener as the primary portfolio manager of the fund’s equity portfolio.

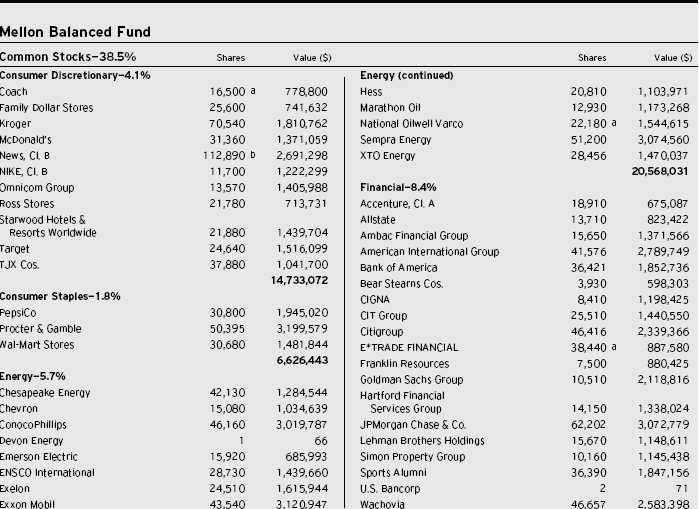

How did Mellon Balanced Fund perform relative to its benchmark?

For the six-month period ended February 28, 2007, the fund’s Class M shares produced a total return of 6.83%, while its Investor shares produced a total return of 6.76% .1 In comparison, the fund’s benchmark, a blended index composed of 60% Standard & Poor’s 500 Composite Stock Price Index (“S&P 500 Index”) and 40% Lehman Brothers U.S.Aggregate Index, produced a 6.82% total return for the same period.2 Separately, the S&P 500 Index and the Lehman Brothers U.S. Aggregate Index produced total returns of 8.93% and 3.66%, respectively, for the same period.

Stocks and bonds were driven higher during the reporting period by moderating U.S. economic growth, diminishing inflationary pressures, stable short-term interest rates and robust corporate earnings. As a result, the fund produced returns that were in line with the blended benchmark index.

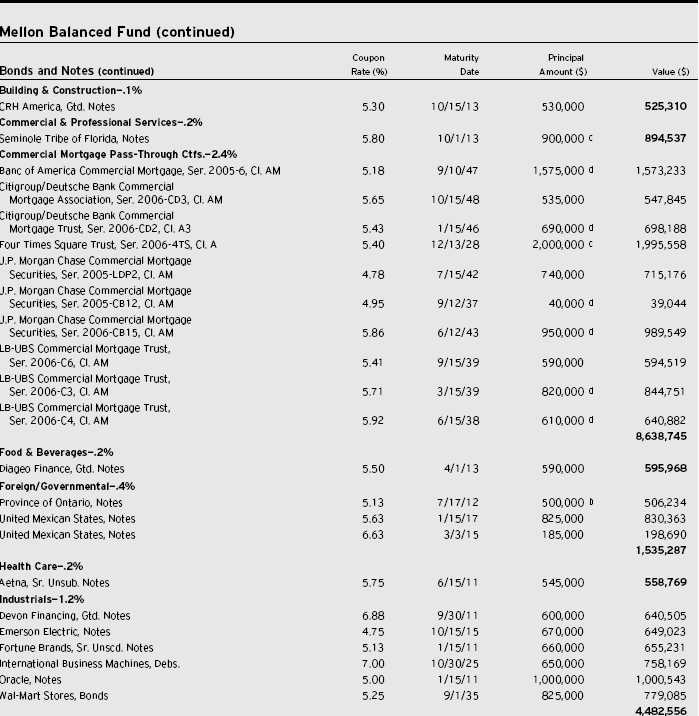

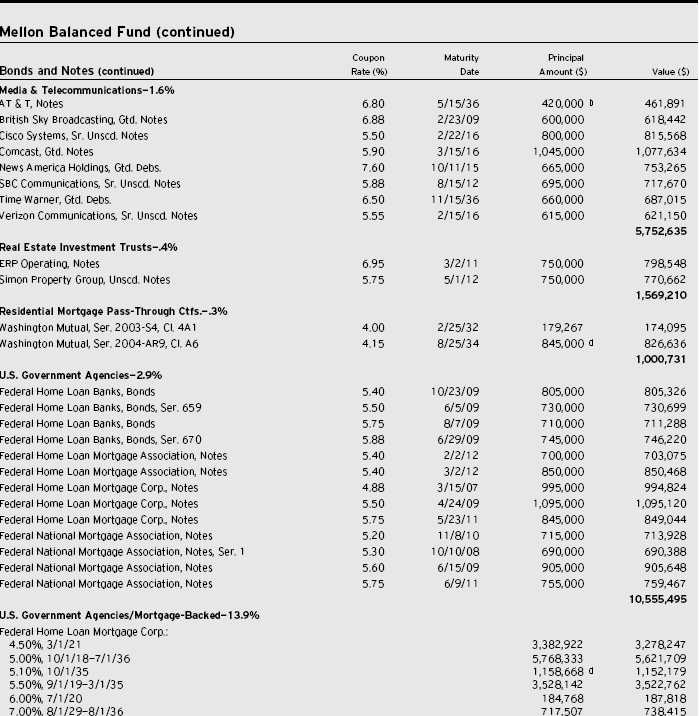

What is the fund’s investment approach?

The fund seeks long-term growth of principal in conjunction with current income. To pursue its goal, the fund may invest in equity securities, income producing bonds, Mellon Small Cap Stock Fund, Mellon Mid Cap Stock Fund, Mellon International Fund and Mellon Emerging Markets Fund (collectively, the “Mellon Funds”).The fund has established target allocations of 60% to equity securities and 40% to bonds and money market instruments.The fund may deviate from these targets within ranges of 15% above or below the target amount. The fund’s investments in

each of the Mellon Funds are subject to a separate limit of 20% of the fund’s total assets, as is the fund’s investment in money market instruments.

In the fund’s equity portfolio, individual stocks are chosen using a computer model, fundamental analysis and risk management techniques. Our computer model identifies and ranks stocks within each industry or sector based on value, earnings growth and the financial health of the company.

In the fund’s fixed-income portfolio, investments in debt securities must be of investment-grade quality at the time of purchase3 or, if unrated, deemed of comparable quality by the investment adviser. Generally, the fund’s average effective portfolio duration of bonds will not exceed eight years.We choose debt securities based on their yields, credit quality, the level of interest rates and inflation, general economic and financial trends and our outlook for the securities markets.

What other factors influenced the fund’s performance?

Investors’ concerns regarding robust economic growth, intensifying inflationary pressures and rising interest rates began to subside early in the reporting period as housing markets cooled and energy prices fell. The Federal Reserve Board (the “Fed”) lent credence to a more benign inflation outlook when it refrained from raising short-term interest rates after more than two years of rate hikes. These factors, together with expectations of an economic “soft landing” and strong corporate earnings, helped fuel rallies in U.S. stock and bond markets through the end of February, when turbulence in the Chinese equity markets triggered a global market correction.

Among equities, the fund produced some of its greater gains during the reporting period in the basic materials sector, where top performers included Freeport-

The Funds 15

DISCUSSION OF FUND PERFORMANCE (continued)

McMoRan Copper & Gold, industrial gas producer Air Products and Chemical, Inc. and nickel mining company Inco. In the telecommunications services sector, gains in Sprint Nextel enabled the fund to roughly match the benchmark’s strong returns from the sector.The fund also derived robust gains from consumer discretionary holdings Harley-Davidson, residential homebuilder D. R. Horton and automobile products producer Harman International Industries. Some of the fund’s utilities stocks, such as Dynegy Cl A., benefited from an increase in private equity investment in the sector.The fund delivered positive relative performance in the financial services area through holdings such as Goldman Sachs Group, Lehman Brothers Holdings and JPMorgan Chase & Co.

On the negative side, health care and technology holdings detracted from the fund’s relative performance. Biotechnology giant Amgen was hurt by concerns regarding competitive issues and government reimbursement rates. In the technology area, the fund’s performance was hurt by significant exposure to Motorola, which dropped sharply when the company lost ground in the cellular handset market.

The fund’s fixed-income component benefited from a relatively short average duration during temporary market weakness early in the reporting period.We subsequently shifted to a more neutral posture as inflation concerns eased, enabling the fund to participate more fully in the ensuing rally.The fund also benefited from its holdings of investment-grade corporate bonds, where we focused primarily on credits with short maturities that tend to be less sensitive to adverse developments. Because we regarded most bond market sectors as neither over- nor undervalued, we generally maintained a sector allocation strategy that was similar to that of the benchmark.

What is the fund’s current strategy?

In the fund’s equity portfolio, we have maintained slightly heavier-than-average exposure to technology companies in light of what we believe are attractive valuations, favorable product cycles and rising corporate spending. A slightly overweight position in the health care sector reflects our positive view of the area’s prospects as the U.S. population ages.We also see strong business fundamentals for drillers and oilfield services companies in the energy area. We have slightly reduced the fund’s consumer discretionary exposure due to the potential for weaker consumer spending amid rising mortgage defaults. The fund also holds mildly underweight exposure to the telecommunications services sector, where the competitive landscape appears uncertain.

Among bonds, we have emphasized broad diversification, and we have maintained the fund’s average duration and sector allocations in the neutral range. We believe these are prudent strategies until we see clearer signs of the economy’s health and the direction of Fed policy.

March 15, 2007

| 1 | Total return includes reinvestment of dividends and any capital gains paid. | |

| Past performance is no guarantee of future results. Share price and investment | ||

| return fluctuate such that upon redemption, fund shares may be worth more or | ||

| less than their original cost. | ||

| 2 | SOURCE: LIPPER INC. — Reflects reinvestment of dividends and, where | |

| applicable, capital gain distributions.The Standard & Poor’s 500 Composite | ||

| Stock Price Index is a widely accepted, unmanaged index of U.S. stock market | ||

| performance.The Lehman Brothers U.S. Aggregate Index is a widely accepted, | ||

| unmanaged total return index of corporate, U.S. government and U.S. | ||

| government agency debt instruments, mortgage-backed securities and asset- | ||

| backed securities with an average maturity of 1-10 years.The indices returns | ||

| do not reflect the fees and expenses associated with operating a mutual fund. | ||

| 3 | The fund may continue to own investment grade bonds (at the time of | |

| purchase), which are subsequently downgraded to below investment grade. |

| 16 |

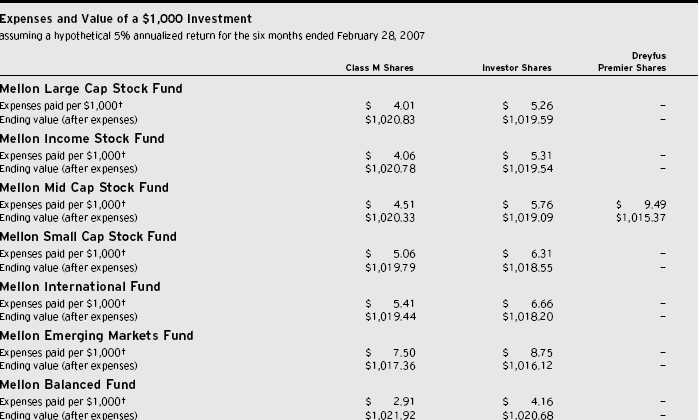

UNDERSTANDING YOUR FUND’S EXPENSES ( U n a u d i t e d )

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemptions fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in each class of each Mellon equity fund from September 1, 2006 to February 28, 2007. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

† Expenses are equal to the Mellon Large Cap Stock Fund’s annualized expense ratio of .80% for Class M and 1.05% for Investor Shares, Mellon Income Stock Fund ..81% for Class M and 1.06% for Investor Shares, Mellon Mid Cap Stock Fund .90% for Class M, 1.15% for Investor Shares and 1.90% for Dreyfus Premier Shares, Mellon Small Cap Stock Fund 1.01% for Class M and 1.26% for Investor Shares, Mellon International Fund 1.08% for Class M and 1.33% for Investor Shares, Mellon Emerging Markets Fund 1.50% for Class M and 1.75% for Investor Shares and Mellon Balanced Fund .58% for Class M and .83% for Investor Shares, multiplied by the respective fund's average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

The Funds 17

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investores assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return.You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

† Expenses are equal to the Mellon Large Cap Stock Fund’s annualized expense ratio of .80% for Class M and 1.05% for Investor Shares, Mellon Income Stock Fund ..81% for Class M and 1.06% for Investor Shares, Mellon Mid Cap Stock Fund .90% for Class M, 1.15% for Investor Shares and 1.90% for Dreyfus Premier Shares, Mellon Small Cap Stock Fund 1.01% for Class M and 1.26% for Investor Shares, Mellon International Fund 1.08% for Class M and 1.33% for Investor Shares, Mellon Emerging Markets Fund 1.50% for Class M and 1.75% for Investor Shares and Mellon Balanced Fund .58% for Class M and .83% for Investor Shares, multiplied by the respective fund's average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

| 18 |

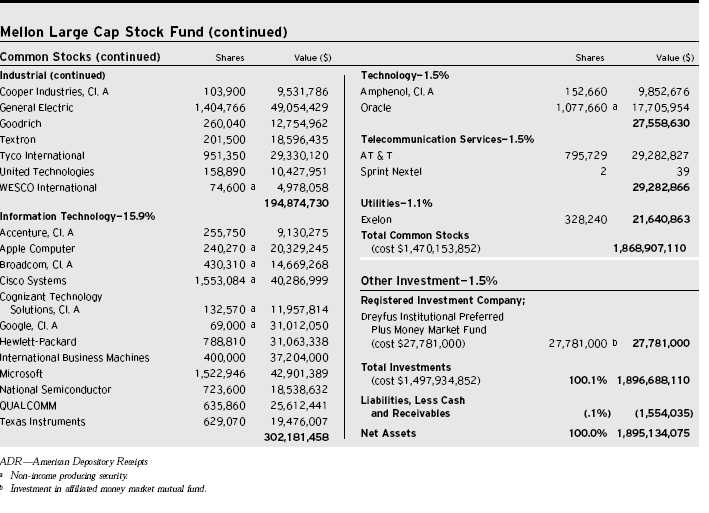

| STATEMENT OF INVESTMENTS |

| February 28, 2007 (Unaudited) |

The Funds 19

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| Portfolio Summary | (Unaudited) † | |||||||

| Value (%) | Value (%) | |||||||

| Financial | 21.0 | Capital Goods | 2.9 | |||||

| Consumer Discretionary | 19.4 | Money Market Investment | 1.5 | |||||

| Information Technology | 15.9 | Telecommunication Services | 1.5 | |||||

| Energy | 13.0 | Technology | 1.5 | |||||

| Health Care | 12.0 | Utilities | 1.1 | |||||

| Industrial | 10.3 | 100.1 | ||||||

| † Based on net assets. | ||||||||

| See notes to financial statements. | ||||||||

| 20 |

| STATEMENT OF INVESTMENTS |

| February 28, 2007 (Unaudited) |

| Mellon Income Stock Fund | ||||||||||

| Common Stocks—99.5% | Shares | Value ($) | Shares | Value ($) | ||||||

| Banks—8.3% | Financial (continued) | |||||||||

| Freddie Mac | 114,100 | 7,322,938 | Capital One Financial | 66,197 | 5,102,465 | |||||

| SunTrust Banks | 40,500 | 3,414,555 | Chubb | 44,580 | 2,275,809 | |||||

| U.S. Bancorp | 97,006 | 3,459,234 | Citigroup | 393,775 | 19,846,260 | |||||

| Wachovia | 151,190 | 8,371,390 | Fidelity National Financial, Cl. A | 89,870 | 2,156,880 | |||||

| Washington Mutual | 117,200 a | 5,048,976 | Goldman Sachs Group | 11,030 | 2,223,648 | |||||

| Wells Fargo & Co. | 234,200 | 8,126,740 | JPMorgan Chase & Co. | 279,599 | 13,812,191 | |||||

| 35,743,833 | Lincoln National | 94,310 | 6,427,226 | |||||||

| Consumer Discretionary—7.8% | Merrill Lynch & Co. | 39,760 | 3,327,117 | |||||||

| Cadbury Schweppes, ADR | 76,740 | 3,302,122 | Morgan Stanley | 64,420 | 4,826,346 | |||||

| CBS, Cl. B | 86,300 | 2,619,205 | PNC Financial Services Group | 30,280 | 2,219,827 | |||||

| Federated Department Stores | 79,200 | 3,537,072 | ProLogis | 89,600 | 5,925,248 | |||||

| Home Depot | 79,400 | 3,144,240 | Prudential Financial | 24,610 | 2,238,033 | |||||

| McDonald’s | 90,100 | 3,939,172 | Simon Property Group | 25,860 | 2,915,456 | |||||

| News, Cl. A | 374,900 | 8,446,497 | Travelers Cos. | 86,451 | 4,388,253 | |||||

| Omnicom Group | 41,730 | 4,323,645 | 100,152,280 | |||||||

| PMI Group | 47,280 | 2,216,014 | Health Care—9.5% | |||||||

| TJX Cos. | 80,860 | 2,223,650 | Abbott Laboratories | 186,420 | 10,182,260 | |||||

| 33,751,617 | Baxter International | 66,230 | 3,312,162 | |||||||

| Consumer Staples—9.4% | Bristol-Myers Squibb | 184,800 | 4,876,872 | |||||||

| Altria Group | 157,090 | 13,239,545 | Eli Lilly & Co. | 102,570 | 5,399,285 | |||||

| Merck & Co. | 102,840 | 4,541,414 | ||||||||

| Clorox | 67,830 | 4,297,709 | ||||||||

| Pfizer | 343,458 | 8,572,712 | ||||||||

| Coca-Cola | 70,440 | 3,288,139 | ||||||||

| Wyeth | 87,789 | 4,294,638 | ||||||||

| Colgate-Palmolive | 64,990 | 4,377,726 | ||||||||

| 41,179,343 | ||||||||||

| Procter & Gamble | 169,720 | 10,775,523 | Industrial—9.0% | |||||||

| SUPERVALU | 117,840 | 4,355,366 | 3M | 56,000 | 4,148,480 | |||||

| 40,334,008 | Eaton | 26,650 | 2,158,916 | |||||||

| Energy—11.8% | Emerson Electric | 55,000 | 2,369,950 | |||||||

| Chevron | 157,166 | 10,783,159 | General Electric | 248,692 | 8,684,325 | |||||

| ConocoPhillips | 99,640 | 6,518,449 | Honeywell International | 80,200 | 3,724,488 | |||||

| EOG Resources | 32,800 | 2,221,872 | Johnson Controls | 33,580 | 3,149,804 | |||||

| Exxon Mobil | 266,276 | 19,086,664 | Lockheed Martin | 32,810 | 3,191,757 | |||||

| Marathon Oil | 24,110 | 2,187,741 | Raytheon (warrants 6/16/2011) | 299 b | 5,346 | |||||

| NRG Energy | 89,070 b | 5,899,997 | Textron | 27,100 | 2,501,059 | |||||

| Occidental Petroleum | 86,220 | 3,981,640 | United Technologies | 67,696 | 4,442,888 | |||||

| 50,679,522 | Waste Management | 126,100 | 4,293,705 | |||||||

| Financial—23.2% | 38,670,718 | |||||||||

| Accenture, Cl. A | 87,000 | 3,105,900 | Information Technology—6.0% | |||||||

| American International Group | 64,070 | 4,299,097 | Automatic Data Processing | 87,260 | 4,344,675 | |||||

| Bank of America | 248,188 | 12,625,324 | Cisco Systems | 162,140 b | 4,205,912 | |||||

| Bank of New York | 60,000 | 2,437,200 | Hewlett-Packard | 136,170 | 5,362,375 | |||||

The Funds 21

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| Mellon Income Stock Fund (continued) | ||||||||||

| Common Stocks (continued) | Shares | Value ($) | Shares | Value ($) | ||||||

| Information Technology (continued) | Utilities (continued) | |||||||||

| International Business Machines | 22,550 | 2,097,376 | FPL Group | 82,200 | 4,855,554 | |||||

| Lucent Technologies | PPL | 115,040 | 4,373,821 | |||||||

| (warrants 12/10/2007) | 2,788 b | 488 | 22,054,848 | |||||||

| Microchip Technology | 96,100 a | 3,421,160 | Total Common Stocks | |||||||

| Microsoft | 151,160 | 4,258,177 | (cost $343,625,477) | 429,059,456 | ||||||

| QUALCOMM | 57,000 | 2,295,960 | ||||||||

| 25,986,123 | Other Investment—1.3% | |||||||||

| Materials—2.3% | Registered Investment Company; | |||||||||

| Air Products & Chemicals | 33,360 | 2,495,995 | Dreyfus Institutional Preferred | |||||||

| E.I. du Pont de Nemours & Co. | 43,530 | 2,209,148 | Plus Money Market Fund | |||||||

| Monsanto | 28,500 | 1,501,665 | (cost $5,575,000) | 5,575,000 c | 5,575,000 | |||||

| Temple-Inland | 61,820 | 3,696,836 | Investment of Cash Collateral | |||||||

| 9,903,644 | for Securities Loaned—.7% | |||||||||

| Telecommunication Services—7.1% | ||||||||||

| Registered Investment Company; | ||||||||||

| Alltel | 30,450 | 1,844,966 | ||||||||

| Dreyfus Institutional Cash | ||||||||||

| AT & T | 539,595 | 19,857,096 | Advantage Plus Fund | |||||||

| Verizon Communications | 202,251 | 7,570,255 | (cost $3,138,000) | 3,138,000 c | 3,138,000 | |||||

| Windstream | 88,452 | 1,331,203 | ||||||||

| 30,603,520 | Total Investments | |||||||||

| (cost $352,338,477) | 101.5% | 437,772,456 | ||||||||

| Utilities—5.1% | ||||||||||

| Dominion Resources/VA | 41,200 | 3,523,836 | Liabilities, Less Cash | |||||||

| Entergy | 44,450 | 4,387,215 | and Receivables | (1.5%) | (6,362,667) | |||||

| Exelon | 74,540 | 4,914,422 | Net Assets | 100.0% | 431,409,789 | |||||

| ADR—American Depository Receipts |

| a All or a portion of these securities are on loan. At February 28,2007, the total market value of the fund’s securities on loan is $3,062,616 and the total market value of the |

| collateral held by the fund is $3,138,000. |

| b Non-income producing security. |

| c Investment in affiliated money market mutual fund. |

| Portfolio Summary | (Unaudited) † | |||||||

| Value (%) | Value (%) | |||||||

| Financial | 23.2 | Telecommunication Services | 7.1 | |||||

| Energy | 11.8 | Information Technology | 6.0 | |||||

| Health Care | 9.5 | Utilities | 5.1 | |||||

| Consumer Staples | 9.4 | Materials | 2.3 | |||||

| Industrial | 9.0 | Money Market Investments | 2.0 | |||||

| Banks | 8.3 | |||||||

| Consumer Discretionary | 7.8 | 101.5 | ||||||

| † Based on net assets. | ||||||||

| See notes to financial statements. | ||||||||

22

| STATEMENT OF INVESTMENTS |

| February 28, 2007 (Unaudited) |

| Mellon Mid Cap Stock Fund | ||||||||||

| Common Stocks—98.9% | Shares | Value ($) | Shares | Value ($) | ||||||

| Consumer Discretionary—16.8% | Energy (continued) | |||||||||

| Abercrombie & Fitch, Cl. A | 237,400 | 18,557,558 | Southwestern Energy | 343,500 a | 13,396,500 | |||||

| Advance Auto Parts | 372,400 | 14,020,860 | Superior Energy Services | 261,500 a | 8,014,975 | |||||

| bebe Stores | 410,400 | 7,543,152 | Tesoro | 98,300 | 8,959,062 | |||||

| Children’s Place Retail Stores | 467,600 a | 25,465,496 | 129,169,967 | |||||||

| Coldwater Creek | 481,850 a | 8,866,040 | Financial—16.4% | |||||||

| D.R. Horton | 562,740 | 14,276,714 | AllianceBernstein Holding, LP | 112,100 | 9,618,180 | |||||

| Dick’s Sporting Goods | 227,140 a | 11,888,508 | Allied World Assurance Holdings | 232,800 | 9,705,432 | |||||

| Dollar Tree Stores | 237,500 a | 8,101,125 | AMB Property | 227,900 | 13,395,962 | |||||

| Domino’s Pizza | 40,400 | 1,246,744 | AmeriCredit | 346,500 a | 8,461,530 | |||||

| Focus Media Holding, ADR | 110,800 a | 8,875,080 | Arthur J. Gallagher & Co. | 315,500 | 9,032,765 | |||||

| Gentex | 674,500 | 11,270,895 | Axis Capital Holdings | 147,000 | 4,970,070 | |||||

| Hansen Natural | 214,100 a | 7,493,500 | City National/Beverly Hills, CA | 174,700 | 12,609,846 | |||||

| Harman International Industries | 109,000 | 10,808,440 | Compass Bancshares | 96,300 | 6,645,663 | |||||

| Hilton Hotels | 448,440 | 15,829,932 | Cullen/Frost Bankers | 172,100 | 9,307,168 | |||||

| ITT Educational Services | 184,800 a | 14,780,304 | Developers Diversified Realty | 195,740 | 12,832,714 | |||||

| Life Time Fitness | 154,000 a | 7,361,200 | Eaton Vance | 384,200 | 13,327,898 | |||||

| NutriSystem | 164,800 a,b | 7,440,720 | FelCor Lodging Trust | 386,700 | 9,118,386 | |||||

| Penn National Gaming | 187,200 a | 8,729,136 | Huntington Bancshares/OH | 373,300 | 8,641,895 | |||||

| Regis | 218,700 | 9,202,896 | IntercontinentalExchange | 104,600 a | 15,778,910 | |||||

| Ruby Tuesday | 247,300 | 7,245,890 | Jefferies Group | 281,600 | 7,617,280 | |||||

| Scientific Games, Cl. A | 370,700 a | 12,121,890 | Lazard, Cl. A | 262,800 | 13,531,572 | |||||

| Sotheby’s, Cl. A | 356,800 | 12,973,248 | Nasdaq Stock Market | 179,000 a | 5,357,470 | |||||

| Thor Industries | 243,090 | 10,170,886 | People’s Bank | 214,300 | 9,512,777 | |||||

| Urban Outfitters | 564,570 a | 14,012,627 | Radian Group | 114,346 | 6,569,178 | |||||

| Virgin Media | 298,400 | 7,821,064 | Rayonier | 303,986 | 13,576,015 | |||||

| VistaPrint | 158,200 a | 5,888,204 | SL Green Realty | 69,400 | 10,122,684 | |||||

| 281,992,109 | Sunstone Hotel Investors | 301,460 | 8,543,376 | |||||||

| Consumer Staples—1.4% | Taubman Centers | 172,470 | 10,256,791 | |||||||

| Performance Food Group | 320,500 a | 9,445,135 | TCF Financial | 438,100 | 11,583,364 | |||||

| Smithfield Foods | 456,400 a | 13,331,444 | TD Ameritrade Holding | 291,700 | 4,667,200 | |||||

| 22,776,579 | W.R. Berkley | 551,050 | 17,964,230 | |||||||

| Energy—7.7% | Webster Financial | 243,500 | 12,026,465 | |||||||

| Cameron International | 338,800 a | 19,206,572 | 274,774,821 | |||||||

| Consol Energy | 219,100 b | 7,815,297 | Health Care—10.7% | |||||||

| Denbury Resources | 462,600 a | 13,341,384 | Barr Pharmaceuticals | 153,800 a | 8,151,400 | |||||

| FMC Technologies | 215,800 a | 14,195,324 | C.R. Bard | 98,570 | 7,865,886 | |||||

| Grant Prideco | 193,900 a | 8,417,199 | Cephalon | 203,800 a | 14,486,104 | |||||

| Newfield Exploration | 355,860 a | 15,380,269 | Community Health Systems | 320,400 a | 11,934,900 | |||||

| Quicksilver Resources | 89,400 a | 3,448,158 | Cytyc | 434,900 a | 13,177,470 | |||||

| Range Resources | 265,900 | 8,490,187 | Dentsply International | 229,600 | 7,241,584 | |||||

| Smith International | 207,440 | 8,505,040 | Health Management Associates, Cl. A | 411,700 | 8,217,532 | |||||

| The Funds | 23 |

STATEMENT OF INVESTMENTS (Unaudited) (continued)

| Mellon Mid Cap Stock Fund (continued) | ||||||||||

| Common Stocks (continued) | Shares | Value ($) | Shares | Value ($) | ||||||

| Health Care (continued) | Information Technology (continued) | |||||||||

| Health Net | 354,200 a | 18,939,074 | Amphenol, Cl. A | 276,060 | 17,816,912 | |||||

| Henry Schein | 272,100 a | 14,195,457 | Avnet | 185,900 a | 6,798,363 | |||||

| Hologic | 156,400 a | 8,609,820 | CheckFree | 66,000 a | 2,502,720 | |||||

| MGI Pharma | 191,700 a | 4,067,874 | Citrix Systems | 130,700 a | 4,208,540 | |||||

| Omnicare | 526,800 | 21,883,272 | Cognizant Technology Solutions, | |||||||

| Pharmaceutical Product Development | 393,000 | 12,493,470 | Cl. A | 104,200 a | 9,398,840 | |||||

| Varian Medical Systems | 370,310 a | 17,015,745 | Comtech Telecommunications | 212,120 a | 7,286,322 | |||||

| Vertex Pharmaceuticals | 378,771 a | 11,624,482 | Digital River | 164,600 a | 9,117,194 | |||||

| 179,904,070 | F5 Networks | 143,200 a | 10,399,184 | |||||||

| Industrial—16.7% | FactSet Research Systems | 97,920 | 5,959,411 | |||||||

| Aircastle | 220,000 | 7,574,600 | Fairchild Semiconductor | |||||||

| AMETEK | 404,450 | 13,832,190 | International | 380,900 a | 7,126,639 | |||||

| Canadian Pacific Railway | 146,200 | 7,808,542 | Fortress Investment Group | 5,000 | 151,000 | |||||

| Chicago Bridge & Iron (NY Shares) | 264,200 | 7,854,666 | Harris | 155,800 | 7,646,664 | |||||

| Cintas | 156,900 | 6,335,622 | Integrated Device Technology | 690,200 a | 11,195,044 | |||||

| Corrections Corp. of America | 177,500 a | 9,293,900 | Intersil, Cl. A | 529,800 | 14,013,210 | |||||

| DRS Technologies | 233,600 | 12,378,464 | Lam Research | 226,500 a | 10,115,490 | |||||

| Dun & Bradstreet | 135,200 | 11,935,456 | Macrovision | 236,500 a | 5,834,455 | |||||

| Equifax | 205,300 | 7,949,216 | ManTech International, Cl. A | 237,100 a | 8,168,095 | |||||

| Expeditors International | McAfee | 549,800 a | 16,559,976 | |||||||

| Washington | 513,000 | 23,008,050 | MEMC Electronic Materials | 312,700 a | 16,125,939 | |||||

| Goodrich | 234,600 | 11,507,130 | Microchip Technology | 563,800 | 20,071,280 | |||||

| Jacobs Engineering Group | 188,700 a | 17,047,158 | Polycom | 343,600 a | 10,960,840 | |||||

| Joy Global | 185,275 | 8,215,094 | Synopsys | 456,000 a | 11,664,480 | |||||

| Kansas City Southern | 269,900 a | 8,647,596 | 252,184,885 | |||||||

| L-3 Communications Holdings | 100,600 | 8,762,260 | Materials—5.7% | |||||||

| Manpower | 221,300 | 16,442,590 | Albemarle | 155,100 | 12,694,935 | |||||

| NCI Building Systems | 149,000 a | 8,320,160 | Allegheny Technologies | 124,300 | 12,734,535 | |||||

| Oshkosh Truck | 236,300 | 12,677,495 | Ashland | 116,800 | 7,659,744 | |||||

| Precision Castparts | 326,000 | 29,656,220 | Florida Rock Industries | 88,100 | 5,936,178 | |||||

| Republic Services | 431,320 | 18,145,632 | Freeport-McMoRan | |||||||

| Robert Half International | 194,600 | 7,603,022 | Copper & Gold, Cl. B | 91,500 | 5,253,015 | |||||

| Shaw Group | 215,800 a | 6,642,324 | IPSCO | 81,400 | 8,877,484 | |||||

| Textron | 97,100 | 8,961,359 | Martin Marietta Materials | 144,300 | 18,083,676 | |||||

| WESCO International | 123,900 a | 8,267,847 | RPM International | 509,300 | 11,917,620 | |||||

| 278,866,593 | Vulcan Materials | 111,000 | 12,930,390 | |||||||

| Information Technology—15.1% | 96,087,577 | |||||||||

| Activision | 681,700 a | 11,398,024 | Telecommunication Services—1.1% | |||||||

| Akamai Technologies | 169,600 a | 8,746,272 | NII Holdings | 154,000 a | 10,909,360 | |||||

| Alliance Data Systems | 204,800 a | 12,236,800 | SBA Communications, Cl. A | 272,300 a | 7,343,931 | |||||

| Amdocs | 193,100 a | 6,683,191 | 18,253,291 | |||||||

| 24 |

| Mellon Mid Cap Stock Fund (continued) | ||||||||||

| Common Stocks (continued) | Shares | Value ($) | Other Investment—1.0% | Shares | Value ($) | |||||

| Utilities—7.3% | Registered Investment Company; | |||||||||

| Allegheny Energy | 171,300 a | 8,092,212 | Dreyfus Institutional Preferred | |||||||

| Alliant Energy | 425,500 | 17,794,410 | Plus Money Market Fund | |||||||

| (cost $16,677,000) | 16,677,000 c | 16,677,000 | ||||||||

| Aqua America | 566,600 | 12,912,814 | ||||||||

| DPL | 459,800 | 13,872,166 | Investment of Cash Collateral | |||||||

| Dynegy, Cl. A | 1,117,300 a | 9,173,033 | for Securities Loaned—.5% | |||||||

| Energen | 181,900 | 8,818,512 | Registered Investment Company; | |||||||

| Northeast Utilities | 554,600 | 16,116,676 | Dreyfus Institutional Cash | |||||||

| Advantage Plus Fund | ||||||||||

| (cost $8,946,720) | 8,946,720c | |||||||||

| OGE Energy | 347,800 | 13,428,558 | > | 8,946,720 | ||||||

| PPL | 224,200 | 8,524,084 | ||||||||

| Questar | 152,600 | 12,839,764 | Total Investments | |||||||

| (cost $1,405,376,590) | 100.4% 1,681,205,841 | |||||||||

| 121,572,229 | ||||||||||

| Total Common Stocks | Liabilities, Less Cash and Receivables | (.4%) | (6,668,636) | |||||||

| (cost $1,379,752,870) | 1,655,582,121 | Net Assets | 100.0% 1,674,537,205 | |||||||

| ADR—American Depository Receipts |

| a Non-income producing security. |

| b All or a portion of these securities are on loan. At February 28, 2007, the total market value of the fund’s securities on loan is $8,801,178 and the total market value of the |

| collateral held by the fund is $8,946,720. |

| c Investment in affiliated money market mutual fund. |

| Portfolio Summary | (Unaudited) † | |||||||

| Value (%) | Value (%) | |||||||

| Consumer Discretionary | 16.8 | Utilities | 7.3 | |||||

| 25 | ||||||||

| Industrial | 16.7 | Materials | 5.7 | |||||

| Financial | 16.4 | Money Market Investments | 1.5 | |||||

| Information Technology | 15.1 | Consumer Staples | 1.4 | |||||

| Health Care | 10.7 | Telecommunication Services | 1.1 | |||||

| Energy | 7.7 | 100.4 | ||||||

| † Based on net assets. | ||||||||

| See notes to financial statements. | ||||||||

The Funds 25

| STATEMENT OF INVESTMENTS |

| February 28, 2007 (Unaudited) |

| Mellon Small Cap Stock Fund | ||||||||||

| Common Stocks—95.9% | Shares | Value ($) | Shares | Value ($) | ||||||

| Consumer Discretionary—15.0% | Financial—18.0% | |||||||||

| Charter Communications, Cl. A | 1,541,400 a,b | 4,639,614 | Annaly Capital Management | 326,200 | 4,573,324 | |||||

| Children’s Place Retail Stores | 144,800 b | 7,885,808 | Apollo Investment | 282,043 a | 6,396,735 | |||||

| Coldwater Creek | 517,325 a,b | 9,518,780 | Aspen Insurance Holdings | 116,500 | 3,087,250 | |||||

| Life Time Fitness | 159,100 b | 7,604,980 | Asta Funding | 92,800 | 3,069,824 | |||||

| Live Nation | 223,500 b | 5,171,790 | Boston Private | |||||||

| Meritage Homes | 100,900 b | 3,909,875 | Financial Holdings | 220,100 | 6,349,885 | |||||

| NutriSystem | 99,000 a,b | 4,469,850 | Christopher & Banks | 337,200 | 6,261,804 | |||||

| Penn National Gaming | 103,200 b | 4,812,216 | Downey Financial | 85,300 a | 5,590,562 | |||||

| PEP Boys-Manny Moe & Jack | 260,600 a | 3,948,090 | East West Bancorp | 65,100 | 2,426,277 | |||||

| Phillips-Van Heusen | 59,800 a | 3,279,432 | Essex Property Trust | 27,100 | 3,763,919 | |||||

| Regis | 117,400 | 4,940,192 | FelCor Lodging Trust | 279,520 a | 6,591,082 | |||||

| Smith & Wesson Holding | 426,100 a,b | 5,292,162 | First Midwest Bancorp/IL | 81,140 a | 3,052,487 | |||||

| Sonic Automotive, Cl. A | 183,700 a | 5,400,780 | FirstFed Financial | 87,700 a,b | 5,016,440 | |||||

| Sotheby’s, Cl. A | 202,900 a | 7,377,444 | Innkeepers USA Trust | 369,000 | 6,162,300 | |||||

| Standard-Pacific | 132,300 a | 3,377,619 | International Securities | |||||||

| TiVo | 883,700 a,b | 5,187,319 | Exchange Holdings, Cl. A | 80,100 a | 3,704,625 | |||||

| Tractor Supply | 95,200 b | 4,871,384 | Investment Technology Group | 53,500 b | 2,189,755 | |||||

| Vail Resorts | 101,300 a,b | 5,263,548 | Kilroy Realty | 38,400 | 3,162,240 | |||||

| 96,950,883 | Knight Capital Group, Cl. A | 163,100 a,b | 2,578,611 | |||||||

| Consumer Staples—3.2% | National Financial Partners | 96,700 | 4,463,672 | |||||||

| Briggs & Stratton | 159,400 a | 4,660,856 | Ohio Casualty | 105,000 | 3,131,100 | |||||

| Chiquita Brands International | 198,900 a | 2,884,050 | Philadelphia | |||||||

| Consolidated Holding | 151,200 b | 6,941,592 | ||||||||

| Flowers Foods | 57,600 a | 1,692,864 | ||||||||

| Prosperity Bancshares | 174,700 | 6,074,319 | ||||||||

| Hain Celestial Group | 41,500 a,b | 1,203,915 | ||||||||

| SVB Financial Group | 101,500 b | 4,902,450 | ||||||||

| Jones Soda | 322,800 a,b | 3,973,668 | ||||||||

| Umpqua Holdings | 207,900 a | 5,615,379 | ||||||||

| Performance Food Group | 97,640 a,b | 2,877,451 | ||||||||

| Webster Financial | 93,400 | 4,613,026 | ||||||||

| Sanderson Farms | 99,000 a | 3,202,650 | ||||||||

| Whitney Holding | 67,400 | 2,137,928 | ||||||||

| 20,495,454 | ||||||||||

| Zenith National Insurance | 108,200 | 5,209,830 | ||||||||

| Energy—5.8% | ||||||||||

| 117,066,416 | ||||||||||

| Cabot Oil & Gas | 62,500 | 4,222,500 | ||||||||

| Health Care—13.2% | ||||||||||

| Forest Oil | 88,900 b | 2,835,910 | ||||||||

| Alpharma, Cl. A | 70,800 | 1,866,288 | ||||||||

| Helix Energy Solutions Group | 87,500 a,b | 2,937,375 | ||||||||

| American Medical | ||||||||||

| Input/Output | 356,100 a,b | 4,832,277 | Systems Holdings | 154,700 a,b | 3,146,598 | |||||

| Lone Star Technologies | 61,100 b | 2,904,083 | AMERIGROUP | 60,800 b | 2,011,264 | |||||

| Massey Energy | 113,900 | 2,763,214 | AMN Healthcare Services | 247,400 a,b | 6,877,720 | |||||

| Oceaneering International | 158,300 b | 6,243,352 | ARIAD Pharmaceuticals | 605,700 a,b | 2,925,531 | |||||

| St. Mary Land & Exploration | 142,890 a | 5,145,469 | Cooper Cos. | 53,400 | 2,450,526 | |||||

| Tetra Technologies | 75,600 a,b | 1,680,588 | Digene | 63,900 b | 3,021,192 | |||||

| Unit | 53,830 b | 2,634,978 | Five Star Quality Care | 466,900 a,b | 5,336,667 | |||||

| W-H Energy Services | 37,700 b | 1,583,400 | Hologic | 153,800 b | 8,466,690 | |||||

| 37,783,146 | ||||||||||

| 26 |

| Mellon Small Cap Stock Fund (continued) | ||||||||||

| Common Stocks (continued) | Shares | Value ($) | Shares | Value ($) | ||||||

| Health Care (continued) | Industrial (continued) | |||||||||

| IDEXX Laboratories | 32,640 b | 2,812,915 | Watson Wyatt | |||||||

| Immucor | 75,300 b | 2,239,422 | Worldwide, Cl. A | 46,200 | 2,220,834 | |||||

| Merit Medical Systems | 1 b | 14 | 96,226,255 | |||||||

| MGI Pharma | 148,300 b | 3,146,926 | Information Technology—15.0% | |||||||

| Par Pharmaceutical Cos. | 294,700 b | 7,155,316 | ANSYS | 82,280 b | 4,197,926 | |||||

| PDL BioPharma | 218,700 a,b | 4,174,983 | Avocent | 127,700 a,b | 4,064,691 | |||||

| Pediatrix Medical Group | 52,140 b | 2,820,774 | BearingPoint | 561,500 a,b | 4,492,000 | |||||

| Psychiatric Solutions | 180,020 a,b | 7,193,599 | Benchmark Electronics | 80,100 b | 1,720,548 | |||||

| Regeneron Pharmaceuticals | 67,100 b | 1,331,264 | CommScope | 101,010 a,b | 3,885,855 | |||||

| Respironics | 80,290 b | 3,289,481 | ECI Telecommunications | 533,500 b | 4,278,670 | |||||

| Sierra Health Services | 84,100 b | 3,125,156 | Esterline Technologies | 53,260 b | 2,179,399 | |||||

| Sirona Dental Systems | 128,900 | 4,797,658 | FactSet Research Systems | 40,650 | 2,473,959 | |||||