UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-10067

Eaton Vance Variable Trust

(Exact Name of Registrant as Specified in Charter)

Two International Place, Boston, Massachusetts 02110

(Address of Principal Executive Offices)

Maureen A. Gemma

Two International Place, Boston, Massachusetts 02110

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

December 31

Date of Fiscal Year End

December 31, 2015

Date of Reporting Period

Item 1. Reports to Stockholders

Eaton Vance

VT Floating-Rate Income Fund

Annual Report

December 31, 2015

Commodity Futures Trading Commission Registration. Effective December 31, 2012, the Commodity Futures Trading Commission (“CFTC”) adopted certain regulatory changes that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. The Fund has claimed an exclusion from the definition of the term “commodity pool operator” under the Commodity Exchange Act. Accordingly, neither the Fund nor the adviser with respect to the operation of the Fund is subject to CFTC regulation. Because of its management of other strategies, the Fund’s adviser is registered with the CFTC as a commodity pool operator and a commodity trading advisor.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

This report is prepared for the general information of contract owners. It is authorized for distribution to prospective investors only when preceded or accompanied by a current summary prospectus or prospectus. Before investing, investors should consider carefully the investment objective, risks, and charges and expenses of the Fund. This and other important information is contained in the summary prospectus and prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing. For further information, please call 1-800-262-1122.

Annual Report December 31, 2015

Eaton Vance

VT Floating-Rate Income Fund

Table of Contents

| | | | |

Management’s Discussion of Fund Performance | | | 2 | |

| |

Performance | | | 3 | |

| |

Fund Profile | | | 4 | |

| |

Endnotes and Additional Disclosures | | | 5 | |

| |

Fund Expenses | | | 6 | |

| |

Financial Statements | | | 7 | |

| |

Report of Independent Registered Public Accounting Firm | | | 31 | |

| |

Management and Organization | | | 32 | |

| |

Important Notices | | | 35 | |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Management’s Discussion of Fund Performance1

Economic and Market Conditions

During the fiscal year ended December 31, 2015, the U.S. floating-rate loan market experienced broadly declining loan prices only partially offset by interest income. As a result, the S&P/LSTA Leveraged Loan Index,2 a loan market barometer, returned –0.69% for the 12-month period.

The period was dominated by risk-averse sentiment among investors. Slowing growth in China, declining prices for oil and other commodities, weakness in the global economic recovery and uncertainty regarding the Federal Reserve’s expected rate hike all dragged on returns of most asset classes across capital markets, including floating-rate loans.

Loan prices edged lower in the secondary market as retail investors exited loan-focused investments. Further downward pressure on loan prices came from high-yield bond funds that sold floating-rate loan holdings to cover redemptions. Meanwhile, institutional loan investors generally stayed the course, with strong demand exhibited in both collateralized loan obligations and traditional institutional channels.

Performance trends within the loan market were bifurcated in a number of ways during the period. Of note, larger and more actively traded loans underperformed less liquid loans, resulting from selling pressure in retail products. Loans in industries affected by declining commodity prices — including oil & gas, metals & mining and utilities — were among the worst performing loans during the period. Meanwhile, investor preference for quality showcased itself in credit tier performance, with higher-quality loans generally outperforming lower-rated issues.

With the U.S. economy continuing its uneven but gradual recovery, the default rate, a measure of corporate health and credit risk in the market, was 1.54%, well below the market’s 10-year average of 2.59%, according to Standard & Poor’s Leveraged Commentary & Data.

Fund Performance

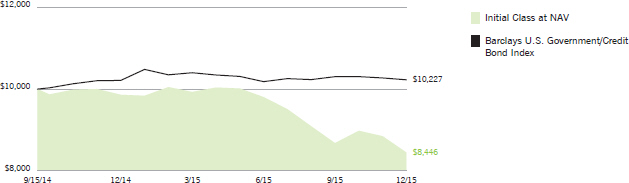

For the fiscal year ended December 31, 2015, Eaton Vance VT Floating-Rate Income Fund (the Fund) Initial Class shares at net asset value (NAV) had a total return of –0.99%. By comparison, the Fund’s benchmark, the S&P/LSTA Leveraged Loan Index (the Index), returned –0.69% for the same period. Index returns do not reflect the effect of any applicable sales charges, commissions, or expenses.

The Fund has historically tended to overweight higher-rated loans relative to the Index. This strategy may help the Fund experience limited credit losses over the long run, but it may detract from relative performance versus the Index in times when lower-rated loans perform well. By contrast, the strategy may aid relative returns versus the Index in times when higher-rated loans perform well, as was the fact over the course of the period.

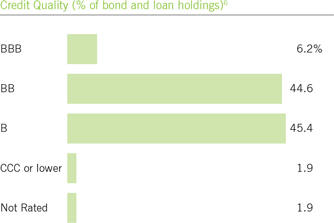

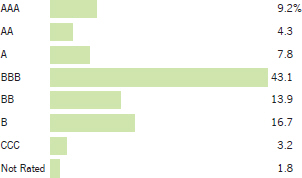

For the 12-month period, BB-rated6 loans in the Index returned 2.23%, B-rated loans in the Index returned -0.82%, CCC-rated loans in the Index returned -8.43% and D-rated (defaulted) loans in the Index returned -42.86%. The negative performance of the D-rated category was due in large part to the continued decline of the defaulted loan issued by Energy Future Holdings (“EFH”), also known as TXU, a major Index component that defaulted during the Fund’s previous fiscal year but was not held by the Fund. Across the ratings tiers, the Fund’s overweight to higher-quality BB-rated loans, a ratings category that outperformed the overall Index during the period, and underweight to poorly performing CCC and D-rated loans, helped Fund performance versus the Index. (The Fund’s weighting in B-rated loans was nearly the same as that of the Index, and thus did not materially affect Fund performance versus the Index.) The Fund’s lack of exposure to the defaulted EFH loan was the largest individual contributor to performance versus the Index.

In contrast, a headwind related to issuer size detracted from Fund performance versus the Index. As the period was marked by heightened volatility and risk aversion by retail investors, more widely held and actively traded issues took the brunt of selling pressure from investors exiting the asset class. As these loans tend to be issued by the larger and more durable companies that the Fund has tended to favor, positioning in larger loans was a relative detractor to Fund performance versus the Index. By way of example, the S&P/LSTA U.S. Leveraged Loan 100 Index, a barometer of the largest loans within the broad Index, returned -2.75% for the one-year period, well below the return of the market at large as represented by the Index.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance less than one year is cumulative. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than quoted. Returns are before taxes unless otherwise noted.

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Performance2,3

Portfolio Managers Scott H. Page, CFA, Craig P. Russ and Andrew Sveen, CFA

| | | | | | | | | | | | | | | | | | | | |

| % Average Annual Total Returns | | Class

Inception Date | | | Performance

Inception Date | | | One Year | | | Five Years | | | Ten Years | |

Initial Class at NAV | | | 05/02/2001 | | | | 05/02/2001 | | | | –0.99 | % | | | 2.62 | % | | | 3.41 | % |

ADV Class at NAV | | | 04/15/2014 | | | | 05/02/2001 | | | | –0.63 | | | | 2.70 | | | | 3.46 | |

S&P/LSTA Leveraged Loan Index | | | — | | | | — | | | | –0.69 | % | | | 3.41 | % | | | 4.31 | % |

| | | | | |

| | | | | | | | | | | | | | | | | | | | |

| % Total Annual Operating Expense Ratios4 | | | | | | | | | | | Initial Class | | | ADV Class | |

| | | | | | | | | | | | | | | 1.16 | % | | | 0.91 | % |

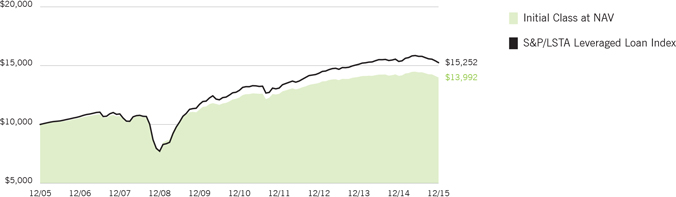

Growth of $10,000

This graph shows the change in value of a hypothetical investment of $10,000 in Initial Class of the Fund for the period indicated. For comparison, the same investment is shown in the indicated index.

| | | | | | | | | | | | | | | | |

| Growth of Investment | | Amount Invested | | | Period Beginning | | | At NAV | | | With Maximum Sales Charge | |

ADV Class | | $ | 10,000 | | | | 12/31/2005 | | | $ | 14,049 | | | | N.A. | |

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance less than one year is cumulative. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than quoted. Returns are before taxes unless otherwise noted.

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Fund Profile

Top 10 Issuers (% of total investments)5

| | | | |

Avago Technologies Cayman Ltd. | | | 1.3 | % |

Asurion, LLC | | | 1.3 | |

Community Health Systems, Inc. | | | 1.3 | |

TransDigm, Inc. | | | 1.1 | |

Berry Plastics Holding Corporation | | | 1.1 | |

Reynolds Group Holdings, Inc. | | | 1.0 | |

First Data Corporation | | | 1.0 | |

Michaels Stores, Inc. | | | 1.0 | |

Supervalu, Inc. | | | 1.0 | |

Infor (US), Inc. | | | 0.9 | |

Total | | | 11.0 | % |

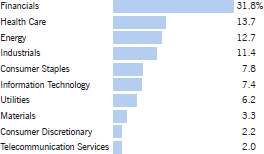

Top 10 Sectors (% of total investments)5

| | | | |

Health Care | | | 10.9 | % |

Electronics/Electrical | | | 9.9 | |

Business Equipment and Services | | | 6.3 | |

Chemicals and Plastics | | | 6.1 | |

Retailers (Except Food and Drug) | | | 6.1 | |

Financial Intermediaries | | | 4.1 | |

Leisure Goods/Activities/Movies | | | 3.8 | |

Automotive | | | 3.6 | |

Lodging and Casinos | | | 3.4 | |

Utilities | | | 3.1 | |

Total | | | 57.3 | % |

See Endnotes and Additional Disclosures in this report.

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Endnotes and Additional Disclosures

| 1 | The views expressed in this report are those of the portfolio manager(s) and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance and the Fund(s) disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This commentary may contain statements that are not historical facts, referred to as “forward looking statements”. The Fund’s actual future results may differ significantly from those stated in any forward looking statement, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission. |

| 2 | S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market. S&P/LSTA U.S. Leveraged Loan 100 Index is an unmanaged index of the largest 100 facilities in the institutional leveraged loan market. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 3 | There is no sales charge. Insurance-related charges are not included in the calculation of returns. If such charges were reflected, the returns would be lower. Please refer to the report for your insurance contract for performance data reflecting insurance-related charges. |

| | Performance prior to the inception date of a class may be linked to the performance of an older class of the Fund. This linked performance is not adjusted for class expense differences. If adjusted for such differences, the performance would be different. Performance presented in the financial highlights included in the financial statements is not linked. In the performance table, the performance of ADV Class is linked to Initial Class. Performance since inception for an index, if presented, is the performance since the Fund’s or oldest share class’ inception, as applicable. |

| 4 | Source: Fund prospectus. |

| 5 | Excludes cash and cash equivalents. |

| 6 | Credit ratings are categorized using S&P. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” are not rated by S&P. |

| | Fund profile subject to change due to active management. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Fund Expenses

Example: As a Fund shareholder, you incur ongoing costs, including management fees; distribution and/or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of Fund investing and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2015 – December 31, 2015).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual Fund return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect expenses and charges which are, or may be imposed under the variable annuity contract or variable life insurance policy (variable contracts) (if applicable) through which your investment in the Fund is made. Therefore, the second section of the table is useful in comparing ongoing costs associated with an investment in vehicles which fund benefits under variable contracts and to qualified pension and retirement plans, and will not help you determine the relative total costs of investing in the Fund through variable contracts. In addition, if these expenses and charges imposed under the variable contracts were included, your costs would be higher.

| | | | | | | | | | | | | | | | |

| | | Beginning

Account Value

(7/1/15) | | | Ending

Account Value

(12/31/15) | | | Expenses Paid

During Period*

(7/1/15 – 12/31/15) | | | Annualized

Expense

Ratio | |

| | | | |

| | | | | | | | | | | | | | | | |

Actual | | | | | | | | | | | | | | | | |

Initial Class | | $ | 1,000.00 | | | $ | 969.60 | | | $ | 5.81 | | | | 1.17 | % |

ADV Class | | $ | 1,000.00 | | | $ | 970.90 | | | $ | 4.57 | | | | 0.92 | % |

| | | | | | | | | | | | | | | | | |

| | | | |

| | | | | | | | | | | | | | | | |

Hypothetical | | | | | | | | | | | | | | | | |

(5% return per year before expenses) | | | | | | | | | | | | | | | | |

Initial Class | | $ | 1,000.00 | | | $ | 1,019.30 | | | $ | 5.95 | | | | 1.17 | % |

ADV Class | | $ | 1,000.00 | | | $ | 1,020.60 | | | $ | 4.69 | | | | 0.92 | % |

| * | Expenses are equal to the Fund’s annualized expense ratio for the indicated Class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on June 30, 2015. Expenses shown do not include insurance-related charges. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments

| | | | | | | | |

| Senior Floating-Rate Loans — 90.9%(1) | |

| | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Aerospace and Defense — 1.8% | | | | | | | | |

BE Aerospace, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing December 16, 2021 | | $ | 704 | | | $ | 705,176 | |

IAP Worldwide Services, Inc. | | | | | | | | |

Revolving Loan, Maturing

July 18, 2018(2) | | | 133 | | | | 119,087 | |

Term Loan - Second Lien, 8.00%, Maturing July 18, 2019(3) | | | 181 | | | | 144,515 | |

Silver II US Holdings, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing December 13, 2019 | | | 3,134 | | | | 2,682,215 | |

TransDigm, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing February 28, 2020 | | | 5,067 | | | | 4,960,594 | |

Term Loan, 3.75%, Maturing June 4, 2021 | | | 1,182 | | | | 1,154,173 | |

| | | | | | | | | |

| | | $ | 9,765,760 | |

| | | | | | | | | |

| | |

Automotive — 3.3% | | | | | | | | |

Affinia Group Intermediate Holdings, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing April 27, 2020 | | $ | 399 | | | $ | 399,534 | |

Chrysler Group, LLC | | | | | | | | |

Term Loan, 3.50%, Maturing May 24, 2017 | | | 2,726 | | | | 2,720,942 | |

Term Loan, 3.25%, Maturing December 31, 2018 | | | 1,806 | | | | 1,793,166 | |

CS Intermediate Holdco 2, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing April 4, 2021 | | | 2,389 | | | | 2,357,771 | |

Dayco Products, LLC | | | | | | | | |

Term Loan, 5.25%, Maturing December 12, 2019 | | | 614 | | | | 609,073 | |

Federal-Mogul Holdings Corporation | | | | | | | | |

Term Loan, 4.75%, Maturing April 15, 2021 | | | 2,592 | | | | 2,292,790 | |

Goodyear Tire & Rubber Company (The) | | | | | | | | |

Term Loan - Second Lien, 3.75%, Maturing April 30, 2019 | | | 1,988 | | | | 1,991,624 | |

Horizon Global Corporation | | | | | | | | |

Term Loan, 7.00%, Maturing June 30, 2021 | | | 293 | | | | 282,262 | |

MPG Holdco I, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing October 20, 2021 | | | 1,493 | | | | 1,461,801 | |

Schaeffler AG | | | | | | | | |

Term Loan, 4.25%, Maturing May 15, 2020 | | | 245 | | | | 246,121 | |

TI Group Automotive Systems, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing June 30, 2022 | | | 748 | | | | 733,162 | |

Tower Automotive Holdings USA, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing April 23, 2020 | | | 2,475 | | | | 2,376,001 | |

Visteon Corporation | | | | | | | | |

Term Loan, 3.50%, Maturing April 9, 2021 | | | 379 | | | | 376,619 | |

| | | | | | | | | |

| | | $ | 17,640,866 | |

| | | | | | | | | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Beverage and Tobacco — 0.3% | | | | | | | | |

Flavors Holdings, Inc. | | | | | | | | |

Term Loan, 6.75%, Maturing April 3, 2020 | | $ | 539 | | | $ | 482,461 | |

Term Loan - Second Lien, 11.00%, Maturing October 3, 2021 | | | 1,000 | | | | 945,000 | |

| | | | | | | | | |

| | | $ | 1,427,461 | |

| | | | | | | | | |

|

Brokerage / Securities Dealers / Investment Houses — 0.1% | |

Astro AB Borrower, Inc. | | | | | | | | |

Term Loan, 5.50%, Maturing April 30, 2022 | | $ | 224 | | | $ | 221,776 | |

Salient Partners L.P. | | | | | | | | |

Term Loan, 7.50%, Maturing May 19, 2021 | | | 493 | | | | 477,725 | |

| | | | | | | | | |

| | | $ | 699,501 | |

| | | | | | | | | |

| | |

Building and Development — 2.5% | | | | | | | | |

ABC Supply Co., Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing April 16, 2020 | | $ | 525 | | | $ | 520,614 | |

Auction.com, LLC | | | | | | | | |

Term Loan, 6.00%, Maturing May 8, 2022 | | | 645 | | | | 639,480 | |

CPG International, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing September 30, 2020 | | | 391 | | | | 369,495 | |

DTZ U.S. Borrower, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing November 4, 2021 | | | 1,617 | | | | 1,580,495 | |

Gates Global, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing July 5, 2021 | | | 963 | | | | 905,846 | |

Headwaters Incorporated | | | | | | | | |

Term Loan, 4.50%, Maturing March 24, 2022 | | | 124 | | | | 124,634 | |

Ply Gem Industries, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing February 1, 2021 | | | 2,462 | | | | 2,416,236 | |

Quikrete Holdings, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing September 28, 2020 | | | 591 | | | | 585,856 | |

RE/MAX International, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing July 31, 2020 | | | 1,762 | | | | 1,733,412 | |

Realogy Corporation | | | | | | | | |

Term Loan, 3.75%, Maturing March 5, 2020 | | | 3,673 | | | | 3,655,561 | |

Summit Materials Companies I, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing July 17, 2022 | | | 373 | | | | 369,744 | |

WireCo WorldGroup, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing February 15, 2017 | | | 274 | | | | 264,145 | |

| | | | | | | | | |

| | | $ | 13,165,518 | |

| | | | | | | | | |

| | |

Business Equipment and Services — 6.0% | | | | | | | | |

Acosta Holdco, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing September 26, 2021 | | $ | 2,475 | | | $ | 2,366,160 | |

| | | | |

| | 7 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Business Equipment and Services (continued) | |

AlixPartners, LLP | | | | | | | | |

Term Loan, 4.50%, Maturing July 28, 2022 | | $ | 374 | | | $ | 371,725 | |

Altisource Solutions S.a.r.l. | | | | | | | | |

Term Loan, 4.50%, Maturing December 9, 2020 | | | 1,623 | | | | 1,420,396 | |

Brock Holdings III, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing March 16, 2017 | | | 472 | | | | 440,795 | |

CCC Information Services, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing December 20, 2019 | | | 218 | | | | 215,065 | |

Ceridian, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing September 15, 2020 | | | 1,889 | | | | 1,622,139 | |

Corporate Capital Trust, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing May 15, 2019 | | | 614 | | | | 606,755 | |

CPM Holdings, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing April 11, 2022 | | | 174 | | | | 173,145 | |

Crossmark Holdings, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing December 20, 2019 | | | 1,262 | | | | 946,847 | |

Education Management, LLC | | | | | | | | |

Term Loan, 5.50%, Maturing

July 2, 2020(3) | | | 196 | | | | 90,251 | |

Term Loan, 8.50%, (2.00% Cash, 6.50% PIK), Maturing July 2, 2020(3) | | | 344 | | | | 84,882 | |

EIG Investors Corp. | | | | | | | | |

Term Loan, 5.00%, Maturing November 9, 2019 | | | 2,702 | | | | 2,639,074 | |

Emdeon Business Services, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing November 2, 2018 | | | 3,646 | | | | 3,586,580 | |

Extreme Reach, Inc. | | | | | | | | |

Term Loan, 6.75%, Maturing February 7, 2020 | | | 882 | | | | 869,547 | |

Garda World Security Corporation | | | | | | | | |

Term Loan, 4.00%, Maturing November 6, 2020 | | | 70 | | | | 66,966 | |

Term Loan, 4.00%, Maturing November 6, 2020 | | | 2,616 | | | | 2,507,527 | |

IG Investment Holdings, LLC | | | | | | | | |

Term Loan, 5.25%, Maturing October 31, 2019 | | | 997 | | | | 994,520 | |

Term Loan, 6.00%, Maturing October 29, 2021 | | | 1,003 | | | | 998,419 | |

IMS Health Incorporated | | | | | | | | |

Term Loan, 3.50%, Maturing March 17, 2021 | | | 507 | | | | 493,129 | |

Information Resources, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing September 30, 2020 | | | 758 | | | | 756,282 | |

ION Trading Finance Limited | | | | | | | | |

Term Loan, 4.25%, Maturing June 10, 2021 | | | 1,091 | | | | 1,058,641 | |

KAR Auction Services, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing March 11, 2021 | | | 1,336 | | | | 1,335,486 | |

Kronos Incorporated | | | | | | | | |

Term Loan, 4.50%, Maturing October 30, 2019 | | | 1,955 | | | | 1,928,291 | |

Match Group, Inc. | | | | | | | | |

Term Loan, 5.50%, Maturing November 16, 2022 | | | 725 | | | | 719,562 | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Business Equipment and Services (continued) | |

MCS AMS Sub-Holdings, LLC | | | | | | | | |

Term Loan, 7.50%, Maturing October 15, 2019 | | $ | 326 | | | $ | 267,141 | |

Monitronics International, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing March 23, 2018 | | | 274 | | | | 266,809 | |

Term Loan, 4.50%, Maturing April 2, 2022 | | | 347 | | | | 332,611 | |

National CineMedia, LLC | | | | | | | | |

Term Loan, 3.18%, Maturing November 26, 2019 | | | 250 | | | | 248,437 | |

PGX Holdings, Inc. | | | | | | | | |

Term Loan, 5.75%, Maturing September 29, 2020 | | | 380 | | | | 378,455 | |

RCS Capital Corporation | | | | | | | | |

Term Loan, 7.50%, Maturing April 29, 2019(3) | | | 1,340 | | | | 938,166 | |

Sensus USA, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing May 9, 2017 | | | 333 | | | | 325,895 | |

ServiceMaster Company | | | | | | | | |

Term Loan, 4.25%, Maturing July 1, 2021 | | | 1,555 | | | | 1,545,592 | |

TNS, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing February 14, 2020 | | | 351 | | | | 346,916 | |

Travelport Finance (Luxembourg) S.a.r.l. | | | | | | | | |

Term Loan, 5.75%, Maturing September 2, 2021 | | | 866 | | | | 849,828 | |

WASH Multifamily Laundry Systems, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing May 14, 2022 | | | 30 | | | | 28,971 | |

Term Loan, 4.25%, Maturing May 14, 2022 | | | 169 | | | | 165,427 | |

| | | | | | | | | |

| | | | | | $ | 31,986,432 | |

| | | | | | | | | |

| | |

Cable and Satellite Television — 1.1% | | | | | | | | |

MCC Iowa, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing June 30, 2021 | | $ | 566 | | | $ | 562,363 | |

Mediacom Illinois, LLC | | | | | | | | |

Term Loan, 3.50%, Maturing June 30, 2021 | | | 321 | | | | 317,792 | |

Neptune Finco Corp. | | | | | | | | |

Term Loan, 5.00%, Maturing October 9, 2022 | | | 2,475 | | | | 2,474,780 | |

Numericable Group SA | | | | | | | | |

Term Loan, 4.56%, Maturing July 31, 2022 | | | 250 | | | | 240,000 | |

Virgin Media Investment Holdings Limited | | | | | | | | |

Term Loan, 3.50%, Maturing June 30, 2023 | | | 2,188 | | | | 2,145,441 | |

| | | | | | | | | |

| | | | | | $ | 5,740,376 | |

| | | | | | | | | |

| | |

Chemicals and Plastics — 5.3% | | | | | | | | |

A. Schulman, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing June 1, 2022 | | $ | 995 | | | $ | 988,781 | |

Allnex (Luxembourg) & Cy S.C.A. | | | | | | | | |

Term Loan, 4.50%, Maturing October 3, 2019 | | | 144 | | | | 144,194 | |

Allnex USA, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing October 3, 2019 | | | 75 | | | | 74,815 | |

| | | | |

| | 8 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Chemicals and Plastics (continued) | |

Aruba Investments, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing February 2, 2022 | | $ | 208 | | | $ | 205,288 | |

Axalta Coating Systems US Holdings, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing February 1, 2020 | | | 2,575 | | | | 2,558,311 | |

AZ Chem US, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing June 12, 2021 | | | 408 | | | | 407,554 | |

Chemours Company (The) | | | | | | | | |

Term Loan, 3.75%, Maturing May 12, 2022 | | | 1,642 | | | | 1,510,410 | |

ECO Services Operations, LLC | | | | | | | | |

Term Loan, 4.75%, Maturing December 4, 2021 | | | 297 | | | | 293,937 | |

Emerald Performance Materials, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing August 1, 2021 | | | 363 | | | | 357,815 | |

Flint Group GmbH | | | | | | | | |

Term Loan, 4.50%, Maturing September 7, 2021 | | | 252 | | | | 246,326 | |

Flint Group US, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing September 7, 2021 | | | 1,525 | | | | 1,477,040 | |

Gemini HDPE, LLC | | | | | | | | |

Term Loan, 4.75%, Maturing August 7, 2021 | | | 815 | | | | 809,605 | |

Huntsman International, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing October 1, 2021 | | | 1,238 | | | | 1,229,766 | |

Ineos US Finance, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing May 4, 2018 | | | 4,112 | | | | 4,014,171 | |

Term Loan, 4.25%, Maturing March 31, 2022 | | | 447 | | | | 432,267 | |

Kronos Worldwide, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing February 18, 2020 | | | 197 | | | | 178,651 | |

MacDermid, Inc. | | | | | | | | |

Term Loan, 5.50%, Maturing June 7, 2020 | | | 349 | | | | 338,913 | |

Term Loan, 5.50%, Maturing June 7, 2020 | | | 421 | | | | 407,602 | |

Term Loan, 5.50%, Maturing June 7, 2020 | | | 1,282 | | | | 1,244,181 | |

Minerals Technologies, Inc. | | | | | | | | |

Term Loan, 3.77%, Maturing May 9, 2021 | | | 815 | | | | 817,038 | |

Omnova Solutions, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing May 31, 2018 | | | 1,355 | | | | 1,337,627 | |

Orion Engineered Carbons GmbH | | | | | | | | |

Term Loan, 5.00%, Maturing July 25, 2021 | | | 388 | | | | 389,578 | |

OXEA Finance, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing January 15, 2020 | | | 343 | | | | 331,424 | |

PolyOne Corporation | | | | | | | | |

Term Loan, 3.75%, Maturing November 11, 2022 | | | 325 | | | | 324,594 | |

PQ Corporation | | | | | | | | |

Term Loan, 4.00%, Maturing August 7, 2017 | | | 2,014 | | | | 2,001,378 | |

Solenis International L.P. | | | | | | | | |

Term Loan, 4.25%, Maturing July 31, 2021 | | | 222 | | | | 213,670 | |

Sonneborn Refined Products B.V. | | | | | | | | |

Term Loan, 4.75%, Maturing December 10, 2020 | | | 48 | | | | 48,051 | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Chemicals and Plastics (continued) | |

Sonneborn, LLC | | | | | | | | |

Term Loan, 4.75%, Maturing December 10, 2020 | | $ | 273 | | | $ | 272,291 | |

Tata Chemicals North America, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing August 7, 2020 | | | 665 | | | | 648,768 | |

Trinseo Materials Operating S.C.A. | | | | | | | | |

Term Loan, 4.25%, Maturing November 5, 2021 | | | 1,393 | | | | 1,375,588 | |

Tronox Pigments (Netherlands) B.V. | | | | | | | | |

Term Loan, 4.50%, Maturing March 19, 2020 | | | 1,995 | | | | 1,779,643 | |

Univar, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing July 1, 2022 | | | 2,020 | | | | 1,962,044 | |

Zep, Inc. | | | | | | | | |

Term Loan, 5.75%, Maturing June 27, 2022 | | | 224 | | | | 221,916 | |

| | | | | | | | | |

| | | | | | $ | 28,643,237 | |

| | | | | | | | | |

| | |

Clothing / Textiles — 0.2% | | | | | | | | |

Ascena Retail Group, Inc. | | | | | | | | |

Term Loan, 5.25%, Maturing August 21, 2022 | | $ | 1,025 | | | $ | 963,500 | |

| | | | | | | | | |

| | | | | | $ | 963,500 | |

| | | | | | | | | |

| | |

Conglomerates — 0.4% | | | | | | | | |

RGIS Services, LLC | | | | | | | | |

Term Loan, 5.50%, Maturing October 18, 2017 | | $ | 1,557 | | | $ | 1,148,058 | |

Spectrum Brands, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing June 23, 2022 | | | 1,182 | | | | 1,179,116 | |

| | | | | | | | | |

| | | | | | $ | 2,327,174 | |

| | | | | | | | | |

| | |

Containers and Glass Products — 2.6% | | | | | | | | |

Berry Plastics Holding Corporation | | | | | | | | |

Term Loan, 3.50%, Maturing February 8, 2020 | | $ | 3,093 | | | $ | 3,042,738 | |

Term Loan, 3.75%, Maturing January 6, 2021 | | | 1,989 | | | | 1,964,446 | |

Term Loan, 4.00%, Maturing October 1, 2022 | | | 706 | | | | 701,205 | |

Hilex Poly Co., LLC | | | | | | | | |

Term Loan, 6.00%, Maturing December 5, 2021 | | | 1,067 | | | | 1,067,382 | |

Libbey Glass, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing April 9, 2021 | | | 271 | | | | 267,489 | |

Onex Wizard US Acquisition, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing March 13, 2022 | | | 844 | | | | 832,704 | |

Owens-Illinois, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing August 6, 2022 | | | 773 | | | | 772,096 | |

Pelican Products, Inc. | | | | | | | | |

Term Loan, 5.25%, Maturing April 10, 2020 | | | 1,625 | | | | 1,598,502 | |

Reynolds Group Holdings, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing December 1, 2018 | | | 3,524 | | | | 3,493,682 | |

| | | | |

| | 9 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Containers and Glass Products (continued) | | | | | | | | |

TricorBraun, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing May 3, 2018 | | $ | 275 | | | $ | 273,198 | |

| | | | | | | | | |

| | | | | | $ | 14,013,442 | |

| | | | | | | | | |

| | |

Cosmetics / Toiletries — 0.9% | | | | | | | | |

Coty, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing October 27, 2022 | | $ | 550 | | | $ | 550,344 | |

Galleria Co. | | | | | | | | |

Term Loan, Maturing

October 22, 2022(2) | | | 1,100 | | | | 1,092,438 | |

KIK Custom Products, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing August 26, 2022 | | | 973 | | | | 936,091 | |

Prestige Brands, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing September 3, 2021 | | | 632 | | | | 629,848 | |

Revlon Consumer Products Corporation | | | | | | | | |

Term Loan, 4.00%, Maturing October 8, 2019 | | | 698 | | | | 695,761 | |

Sun Products Corporation (The) | | | | | | | | |

Term Loan, 5.50%, Maturing March 23, 2020 | | | 1,116 | | | | 1,049,287 | |

| | | | | | | | | |

| | | | | | $ | 4,953,769 | |

| | | | | | | | | |

| | |

Drugs — 1.7% | | | | | | | | |

Alkermes, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing September 18, 2019 | | $ | 194 | | | $ | 193,379 | |

AMAG Pharmaceuticals, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing August 13, 2021 | | | 667 | | | | 643,649 | |

DPx Holdings B.V. | | | | | | | | |

Term Loan, 4.25%, Maturing March 11, 2021 | | | 1,281 | | | | 1,237,283 | |

Endo Luxembourg Finance Company I S.a.r.l. | | | | | | | | |

Term Loan, 3.75%, Maturing September 26, 2022 | | | 1,650 | | | | 1,631,094 | |

Horizon Pharma, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing May 7, 2021 | | | 149 | | | | 139,922 | |

Mallinckrodt International Finance S.A. | | | | | | | | |

Term Loan, 3.50%, Maturing March 19, 2021 | | | 864 | | | | 846,241 | |

Valeant Pharmaceuticals International, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing December 11, 2019 | | | 853 | | | | 823,213 | |

Term Loan, 3.75%, Maturing August 5, 2020 | | | 1,190 | | | | 1,144,190 | |

Term Loan, 4.00%, Maturing April 1, 2022 | | | 2,382 | | | | 2,301,112 | |

| | | | | | | | | |

| | | | | | $ | 8,960,083 | |

| | | | | | | | | |

| | |

Ecological Services and Equipment — 0.8% | | | | | | | | |

ADS Waste Holdings, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing October 9, 2019 | | $ | 3,984 | | | $ | 3,890,726 | |

EnergySolutions, LLC | | | | | | | | |

Term Loan, 6.75%, Maturing May 29, 2020 | | | 716 | | | | 554,761 | |

| | | | | | | | | |

| | | | | | $ | 4,445,487 | |

| | | | | | | | | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Electronics / Electrical — 9.4% | | | | | | | | |

Answers Corporation | | | | | | | | |

Term Loan, 6.25%, Maturing October 3, 2021 | | $ | 792 | | | $ | 542,520 | |

Avago Technologies Cayman Ltd. | | | | | | | | |

Term Loan, 3.75%, Maturing May 6, 2021 | | | 7,075 | | | | 7,070,386 | |

Campaign Monitor Finance Pty. Limited | | | | | | | | |

Term Loan, 6.25%, Maturing March 18, 2021 | | | 463 | | | | 456,514 | |

CommScope, Inc. | | | | | | | | |

Term Loan, 3.31%, Maturing January 14, 2018 | | | 362 | | | | 360,733 | |

Term Loan, 3.83%, Maturing December 29, 2022 | | | 574 | | | | 570,784 | |

CompuCom Systems, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing May 11, 2020 | | | 398 | | | | 254,878 | |

Dell International, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing April 29, 2020 | | | 3,706 | | | | 3,688,614 | |

Deltek, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing June 25, 2022 | | | 1,224 | | | | 1,216,326 | |

Entegris, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing April 30, 2021 | | | 218 | | | | 216,664 | |

Excelitas Technologies Corp. | | | | | | | | |

Term Loan, 6.00%, Maturing October 31, 2020 | | | 508 | | | | 453,797 | |

Eze Castle Software, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing April 6, 2020 | | | 318 | | | | 312,121 | |

FIDJI Luxembourg (BC4) S.a.r.l. | | | | | | | | |

Term Loan, 6.25%, Maturing December 24, 2020 | | | 349 | | | | 348,750 | |

Go Daddy Operating Company, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing May 13, 2021 | | | 3,194 | | | | 3,179,730 | |

Hyland Software, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing July 1, 2022 | | | 1,177 | | | | 1,158,599 | |

Infor (US), Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing June 3, 2020 | | | 238 | | | | 224,340 | |

Term Loan, 3.75%, Maturing June 3, 2020 | | | 4,961 | | | | 4,680,633 | |

Informatica Corporation | | | | | | | | |

Term Loan, 4.50%, Maturing August 5, 2022 | | | 1,397 | | | | 1,347,332 | |

Lattice Semiconductor Corporation | | | | | | | | |

Term Loan, 5.25%, Maturing March 10, 2021 | | | 373 | | | | 354,469 | |

M/A-COM Technology Solutions Holdings, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing May 7, 2021 | | | 320 | | | | 319,325 | |

MA FinanceCo., LLC | | | | | | | | |

Term Loan, 4.50%, Maturing November 20, 2019 | | | 760 | | | | 753,192 | |

Term Loan, 5.25%, Maturing November 19, 2021 | | | 702 | | | | 695,565 | |

Magic Newco, LLC | | | | | | | | |

Term Loan, 5.00%, Maturing December 12, 2018 | | | 1,728 | | | | 1,727,247 | |

MH Sub I, LLC | | | | | | | | |

Term Loan, 4.75%, Maturing July 8, 2021 | | | 765 | | | | 743,452 | |

| | | | |

| | 10 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Electronics / Electrical (continued) | | | | | | | | |

NXP B.V. | | | | | | | | |

Term Loan, 3.25%, Maturing January 11, 2020 | | $ | 1,197 | | | $ | 1,181,571 | |

Term Loan, 3.75%, Maturing December 7, 2020 | | | 1,125 | | | | 1,121,484 | |

Orbotech, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing August 6, 2020 | | | 280 | | | | 275,380 | |

Renaissance Learning, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing April 9, 2021 | | | 467 | | | | 448,215 | |

Rocket Software, Inc. | | | | | | | | |

Term Loan, 5.75%, Maturing February 8, 2018 | | | 214 | | | | 213,020 | |

RP Crown Parent, LLC | | | | | | | | |

Term Loan, 6.00%, Maturing December 21, 2018 | | | 3,284 | | | | 2,939,229 | |

SGS Cayman L.P. | | | | | | | | |

Term Loan, 6.00%, Maturing April 23, 2021 | | | 140 | | | | 139,498 | |

SkillSoft Corporation | | | | | | | | |

Term Loan, 5.75%, Maturing April 28, 2021 | | | 1,481 | | | | 1,155,375 | |

Smart Technologies ULC | | | | | | | | |

Term Loan, 10.50%, Maturing January 31, 2018 | | | 333 | | | | 321,627 | |

Southwire Company | | | | | | | | |

Term Loan, 3.25%, Maturing February 10, 2021 | | | 246 | | | | 240,712 | |

SS&C Technologies, Inc. | | | | | | | | |

Term Loan, 4.01%, Maturing July 8, 2022 | | | 1,234 | | | | 1,227,905 | |

Term Loan, 4.02%, Maturing July 8, 2022 | | | 182 | | | | 180,706 | |

SunEdison Semiconductor B.V. | | | | | | | | |

Term Loan, 6.50%, Maturing May 27, 2019 | | | 437 | | | | 432,881 | |

SurveyMonkey, Inc. | | | | | | | | |

Term Loan, 6.25%, Maturing February 5, 2019 | | | 1,247 | | | | 1,225,429 | |

Sutherland Global Services, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing April 23, 2021 | | | 601 | | | | 599,276 | |

Sybil Software, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing March 20, 2020 | | | 1,538 | | | | 1,531,769 | |

Vantiv, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing June 13, 2021 | | | 505 | | | | 504,652 | |

VeriFone, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing July 8, 2021 | | | 1,970 | | | | 1,955,225 | |

Vertafore, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing October 3, 2019 | | | 456 | | | | 453,051 | |

Wall Street Systems Delaware, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing April 30, 2021 | | | 2,283 | | | | 2,257,881 | |

Zebra Technologies Corporation | | | | | | | | |

Term Loan, 4.75%, Maturing October 27, 2021 | | | 1,411 | | | | 1,414,042 | |

| | | | | | | | | |

| | | | | | $ | 50,494,899 | |

| | | | | | | | | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Financial Intermediaries — 3.8% | | | | | | | | |

Armor Holding II, LLC | | | | | | | | |

Term Loan, 5.75%, Maturing June 26, 2020 | | $ | 1,342 | | | $ | 1,304,625 | |

Citco Funding, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing June 29, 2018 | | | 1,006 | | | | 1,000,640 | |

Clipper Acquisitions Corp. | | | | | | | | |

Term Loan, 3.00%, Maturing February 6, 2020 | | | 267 | | | | 261,469 | |

First Data Corporation | | | | | | | | |

Term Loan, 3.92%, Maturing March 24, 2018 | | | 3,455 | | | | 3,415,656 | |

Term Loan, 3.92%, Maturing September 24, 2018 | | | 1,125 | | | | 1,112,484 | |

Term Loan, 4.17%, Maturing July 8, 2022 | | | 475 | | | | 468,723 | |

Grosvenor Capital Management Holdings, LLP | | | | | | | | |

Term Loan, 3.75%, Maturing January 4, 2021 | | | 2,544 | | | | 2,455,373 | |

Guggenheim Partners, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing July 22, 2020 | | | 858 | | | | 854,507 | |

Hamilton Lane Advisors, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing July 9, 2022 | | | 299 | | | | 297,754 | |

Harbourvest Partners, LLC | | | | | | | | |

Term Loan, 3.25%, Maturing February 4, 2021 | | | 1,055 | | | | 1,049,948 | |

LPL Holdings, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing March 29, 2021 | | | 894 | | | | 887,310 | |

Term Loan, 4.75%, Maturing November 9, 2022 | | | 1,000 | | | | 1,001,250 | |

Medley, LLC | | | | | | | | |

Term Loan, 6.50%, Maturing June 15, 2019 | | | 367 | | | | 372,551 | |

MIP Delaware, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing March 9, 2020 | | | 490 | | | | 486,584 | |

NXT Capital, Inc. | | | | | | | | |

Term Loan, 6.25%, Maturing September 4, 2018 | | | 74 | | | | 73,679 | |

Term Loan, 6.25%, Maturing September 4, 2018 | | | 422 | | | | 421,754 | |

Term Loan, 6.25%, Maturing September 4, 2018 | | | 440 | | | | 439,864 | |

Ocwen Financial Corporation | | | | | | | | |

Term Loan, 5.50%, Maturing February 15, 2018 | | | 808 | | | | 808,703 | |

Starwood Property Trust, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing April 17, 2020 | | | 1,561 | | | | 1,532,350 | |

Walker & Dunlop, Inc. | | | | | | | | |

Term Loan, 5.25%, Maturing December 11, 2020 | | | 385 | | | | 385,947 | |

Walter Investment Management Corp. | | | | | | | | |

Term Loan, 4.75%, Maturing December 19, 2020 | | | 2,052 | | | | 1,777,362 | |

| | | | | | | | | |

| | | | | | $ | 20,408,533 | |

| | | | | | | | | |

| | |

Food Products — 2.8% | | | | | | | | |

AdvancePierre Foods, Inc. | | | | | | | | |

Term Loan, 5.75%, Maturing July 10, 2017 | | $ | 2,576 | | | $ | 2,575,149 | |

Charger OpCo B.V. | | | | | | | | |

Term Loan, 4.25%, Maturing July 2, 2022 | | | 1,795 | | | | 1,784,409 | |

| | | | |

| | 11 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Food Products (continued) | | | | | | | | |

Del Monte Foods, Inc. | | | | | | | | |

Term Loan, 4.26%, Maturing February 18, 2021 | | $ | 936 | | | $ | 901,529 | |

Diamond Foods, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing August 20, 2018 | | | 1,081 | | | | 1,079,162 | |

Dole Food Company, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing November 1, 2018 | | | 670 | | | | 666,687 | |

High Liner Foods Incorporated | | | | | | | | |

Term Loan, 4.25%, Maturing April 24, 2021 | | | 540 | | | | 533,620 | |

JBS USA, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing May 25, 2018 | | | 2,593 | | | | 2,584,266 | |

Term Loan, 3.75%, Maturing September 18, 2020 | | | 953 | | | | 947,702 | |

Term Loan, 4.00%, Maturing October 30, 2022 | | | 425 | | | | 419,018 | |

NBTY, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing October 1, 2017 | | | 3,582 | | | | 3,507,173 | |

Post Holdings, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing June 2, 2021 | | | 89 | | | | 88,913 | |

| | | | | | | | | |

| | | | | | $ | 15,087,628 | |

| | | | | | | | | |

| | |

Food Service — 2.3% | | | | | | | | |

1011778 B.C. Unlimited Liability Company | | | | | | | | |

Term Loan, 3.75%, Maturing December 12, 2021 | | $ | 3,390 | | | $ | 3,373,686 | |

Aramark Services, Inc. | | | | | | | | |

Term Loan, 3.69%, Maturing July 26, 2016 | | | 50 | | | | 49,466 | |

Term Loan, 3.70%, Maturing July 26, 2016 | | | 11 | | | | 11,109 | |

Landry’s, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing April 24, 2018 | | | 1,476 | | | | 1,470,512 | |

NPC International, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing December 28, 2018 | | | 1,293 | | | | 1,281,972 | |

P.F. Chang’s China Bistro, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing July 2, 2019 | | | 189 | | | | 180,612 | |

Seminole Hard Rock Entertainment, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing May 14, 2020 | | | 146 | | | | 143,691 | |

US Foods, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing March 31, 2019 | | | 3,388 | | | | 3,360,596 | |

Weight Watchers International, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing April 2, 2020 | | | 3,209 | | | | 2,362,810 | |

| | | | | | | | | |

| | | | | | $ | 12,234,454 | |

| | | | | | | | | |

| | |

Food / Drug Retailers — 2.3% | | | | | | | | |

Albertsons, LLC | | | | | | | | |

Term Loan, 5.50%, Maturing March 21, 2019 | | $ | 1,112 | | | $ | 1,107,519 | |

Term Loan, 5.13%, Maturing August 25, 2019 | | | 1,612 | | | | 1,599,088 | |

Term Loan, 5.50%, Maturing August 25, 2021 | | | 670 | | | | 665,332 | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Food / Drug Retailers (continued) | | | | | | | | |

General Nutrition Centers, Inc. | | | | | | | | |

Term Loan, 3.25%, Maturing March 4, 2019 | | $ | 2,544 | | | $ | 2,483,098 | |

Rite Aid Corporation | | | | | | | | |

Term Loan - Second Lien, 5.75%, Maturing August 21, 2020 | | | 250 | | | | 251,302 | |

Term Loan - Second Lien, 4.88%, Maturing June 21, 2021 | | | 1,000 | | | | 999,063 | |

Supervalu, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing March 21, 2019 | | | 5,323 | | | | 5,260,957 | |

| | | | | | | | | |

| | | | | | $ | 12,366,359 | |

| | | | | | | | | |

| | |

Health Care — 10.1% | | | | | | | | |

Acadia Healthcare Company, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing February 11, 2022 | | $ | 173 | | | $ | 173,683 | |

ADMI Corp. | | | | | | | | |

Term Loan, 5.50%, Maturing April 30, 2022 | | | 224 | | | | 223,968 | |

Akorn, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing April 16, 2021 | | | 667 | | | | 650,732 | |

Albany Molecular Research, Inc. | | | | | | | | |

Term Loan, 5.75%, Maturing July 16, 2021 | | | 923 | | | | 918,074 | |

Alere, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing June 18, 2022 | | | 1,020 | | | | 1,012,706 | |

Alliance Healthcare Services, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing June 3, 2019 | | | 627 | | | | 598,411 | |

Amneal Pharmaceuticals, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing November 1, 2019 | | | 1,203 | | | | 1,181,267 | |

AmSurg Corp. | | | | | | | | |

Term Loan, 3.50%, Maturing July 16, 2021 | | | 468 | | | | 464,496 | |

Ardent Legacy Acquisitions, Inc. | | | | | | | | |

Term Loan, 6.50%, Maturing July 21, 2021 | | | 324 | | | | 322,567 | |

ATI Holdings, Inc. | | | | | | | | |

Term Loan, 5.25%, Maturing December 20, 2019 | | | 218 | | | | 217,216 | |

Auris Luxembourg III S.a.r.l. | | | | | | | | |

Term Loan, 4.25%, Maturing January 15, 2022 | | | 546 | | | | 543,721 | |

CareCore National, LLC | | | | | | | | |

Term Loan, 5.50%, Maturing March 5, 2021 | | | 1,317 | | | | 1,126,135 | |

CeramTec Acquisition Corporation | | | | | | | | |

Term Loan, 4.25%, Maturing August 30, 2020 | | | 89 | | | | 88,915 | |

CHG Healthcare Services, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing November 19, 2019 | | | 1,465 | | | | 1,440,930 | |

Community Health Systems, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing December 31, 2019 | | | 2,050 | | | | 2,001,805 | |

Term Loan, 4.00%, Maturing January 27, 2021 | | | 3,772 | | | | 3,712,152 | |

| | | | |

| | 12 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Health Care (continued) | | | | | | | | |

Concentra, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing June 1, 2022 | | $ | 199 | | | $ | 198,005 | |

Convatec, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing June 15, 2020 | | | 482 | | | | 475,755 | |

CPI Buyer, LLC | | | | | | | | |

Term Loan, 5.50%, Maturing August 18, 2021 | | | 741 | | | | 712,853 | |

DaVita HealthCare Partners, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing June 24, 2021 | | | 2,069 | | | | 2,062,284 | |

DJO Finance, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing June 8, 2020 | | | 1,421 | | | | 1,384,718 | |

Envision Healthcare Corporation | | | | | | | | |

Term Loan, 4.25%, Maturing May 25, 2018 | | | 2,345 | | | | 2,337,273 | |

Faenza Acquisition GmbH | | | | | | | | |

Term Loan, 4.25%, Maturing August 30, 2020 | | | 261 | | | | 259,716 | |

Term Loan, 4.25%, Maturing August 30, 2020 | | | 858 | | | | 853,473 | |

Global Healthcare Exchange, LLC | | | | | | | | |

Term Loan, 5.50%, Maturing August 15, 2022 | | | 673 | | | | 669,315 | |

Greatbatch Ltd. | | | | | | | | |

Term Loan, 5.25%, Maturing October 27, 2022 | | | 625 | | | | 621,680 | |

Grifols Worldwide Operations USA, Inc. | | | | | | | | |

Term Loan, 3.42%, Maturing February 27, 2021 | | | 3,144 | | | | 3,118,848 | |

Halyard Health, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing November 1, 2021 | | | 413 | | | | 412,502 | |

Hill-Rom Holdings, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing September 8, 2022 | | | 875 | | | | 876,339 | |

Iasis Healthcare, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing May 3, 2018 | | | 786 | | | | 773,273 | |

Indivior Finance S.a.r.l. | | | | | | | | |

Term Loan, 7.00%, Maturing December 19, 2019 | | | 641 | | | | 607,584 | |

inVentiv Health, Inc. | | | | | | | | |

Term Loan, 7.75%, Maturing May 15, 2018 | | | 331 | | | | 326,318 | |

Term Loan, 7.75%, Maturing May 15, 2018 | | | 1,340 | | | | 1,322,393 | |

Jaguar Holding Company II | | | | | | | | |

Term Loan, 4.25%, Maturing August 18, 2022 | | | 2,761 | | | | 2,690,026 | |

Kindred Healthcare, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing April 9, 2021 | | | 1,484 | | | | 1,431,804 | |

Kinetic Concepts, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing May 4, 2018 | | | 1,310 | | | | 1,262,971 | |

Knowledge Universe Education, LLC | | | | | | | | |

Term Loan, 6.00%, Maturing July 28, 2022 | | | 698 | | | | 680,794 | |

LHP Hospital Group, Inc. | | | | | | | | |

Term Loan, 9.00%, Maturing July 3, 2018 | | | 351 | | | | 343,881 | |

MedAssets, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing December 13, 2019 | | | 173 | | | | 171,666 | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Health Care (continued) | | | | | | | | |

MMM Holdings, Inc. | | | | | | | | |

Term Loan, 9.75%, Maturing December 12, 2017(3) | | $ | 258 | | | $ | 141,765 | |

MSO of Puerto Rico, Inc. | | | | | | | | |

Term Loan, 9.75%, Maturing December 12, 2017(3) | | | 187 | | | | 103,063 | |

National Mentor Holdings, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing January 31, 2021 | | | 344 | | | | 335,135 | |

New Millennium HoldCo, Inc. | | | | | | | | |

Term Loan, 7.50%, Maturing December 21, 2020 | | | 465 | | | | 425,328 | |

Onex Carestream Finance L.P. | | | | | | | | |

Term Loan, 5.00%, Maturing June 7, 2019 | | | 1,278 | | | | 1,176,523 | |

Opal Acquisition, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing November 27, 2020 | | | 2,220 | | | | 1,878,440 | |

Ortho-Clinical Diagnostics, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing June 30, 2021 | | | 1,526 | | | | 1,302,409 | |

Physio-Control International, Inc. | | | | | | | | |

Term Loan, 5.50%, Maturing June 6, 2022 | | | 275 | | | | 270,531 | |

PRA Holdings, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing September 23, 2020 | | | 2,179 | | | | 2,159,591 | |

Radnet Management, Inc. | | | | | | | | |

Term Loan, 4.27%, Maturing October 10, 2018 | | | 1,003 | | | | 995,393 | |

RCHP, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing April 23, 2019 | | | 1,503 | | | | 1,485,823 | |

Sage Products Holdings III, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing December 13, 2019 | | | 896 | | | | 886,757 | |

Select Medical Corporation | | | | | | | | |

Term Loan, 5.00%, Maturing June 1, 2018 | | | 1,038 | | | | 1,034,712 | |

Sterigenics-Nordion Holdings, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing May 15, 2022 | | | 449 | | | | 437,653 | |

Steward Health Care System, LLC | | | | | | | | |

Term Loan, 6.75%, Maturing April 12, 2020 | | | 1,442 | | | | 1,405,994 | |

Tecomet, Inc. | | | | | | | | |

Term Loan, 5.75%, Maturing December 5, 2021 | | | 817 | | | | 751,410 | |

Truven Health Analytics, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing June 6, 2019 | | | 1,297 | | | | 1,245,129 | |

| | | | | | | | | |

| | | | | | $ | 54,305,905 | |

| | | | | | | | | |

| | |

Home Furnishings — 0.6% | | | | | | | | |

Serta Simmons Holdings, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing October 1, 2019 | | $ | 3,215 | | | $ | 3,205,224 | |

| | | | | | | | | |

| | | | | | $ | 3,205,224 | |

| | | | | | | | | |

| | | | |

| | 13 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Industrial Equipment — 2.7% | | | | | | | | |

Apex Tool Group, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing January 31, 2020 | | $ | 2,755 | | | $ | 2,635,985 | |

Delachaux S.A. | | | | | | | | |

Term Loan, 4.50%, Maturing October 28, 2021 | | | 301 | | | | 300,256 | |

Doosan Infracore International, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing May 28, 2021 | | | 2,973 | | | | 2,935,973 | |

Filtration Group Corporation | | | | | | | | |

Term Loan, 4.25%, Maturing November 21, 2020 | | | 169 | | | | 164,427 | |

Gardner Denver, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing July 30, 2020 | | | 1,075 | | | | 971,757 | |

Husky Injection Molding Systems Ltd. | | | | | | | | |

Term Loan, 4.25%, Maturing June 30, 2021 | | | 1,793 | | | | 1,732,356 | |

Milacron, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing September 28, 2020 | | | 759 | | | | 753,146 | |

Paladin Brands Holding, Inc. | | | | | | | | |

Term Loan, 7.25%, Maturing August 16, 2019 | | | 398 | | | | 373,938 | |

Rexnord, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing August 21, 2020 | | | 2,737 | | | | 2,659,453 | |

Signode Industrial Group US, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing May 1, 2021 | | | 600 | | | | 577,804 | |

STS Operating, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing February 12, 2021 | | | 197 | | | | 185,692 | |

Tank Holding Corp. | | | | | | | | |

Term Loan, 5.25%, Maturing March 16, 2022 | | | 750 | | | | 740,043 | |

VAT Lux III S.a.r.l. | | | | | | | | |

Term Loan, 4.25%, Maturing February 11, 2021 | | | 215 | | | | 212,254 | |

| | | | | | | | | |

| | | | | | $ | 14,243,084 | |

| | | | | | | | | |

| | |

Insurance — 2.9% | | | | | | | | |

Alliant Holdings I, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing August 12, 2022 | | $ | 1,169 | | | $ | 1,146,839 | |

AmWINS Group, LLC | | | | | | | | |

Term Loan, 5.25%, Maturing September 6, 2019 | | | 2,290 | | | | 2,288,595 | |

AssuredPartners, Inc. | | | | | | | | |

Term Loan, 5.75%, Maturing October 21, 2022 | | | 475 | | | | 473,219 | |

Asurion, LLC | | | | | | | | |

Term Loan, 5.00%, Maturing May 24, 2019 | | | 2,675 | | | | 2,529,459 | |

Term Loan, 5.00%, Maturing August 4, 2022 | | | 3,383 | | | | 3,126,457 | |

Term Loan - Second Lien, 8.50%, Maturing March 3, 2021 | | | 1,400 | | | | 1,201,375 | |

CGSC of Delaware Holding Corporation | | | | | | | | |

Term Loan, 5.00%, Maturing April 16, 2020 | | | 268 | | | | 258,741 | |

Cunningham Lindsey U.S., Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing December 10, 2019(3) | | | 452 | | | | 309,441 | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Insurance (continued) | | | | | | | | |

Hub International Limited | | | | | | | | |

Term Loan, 4.00%, Maturing October 2, 2020 | | $ | 1,981 | | | $ | 1,869,420 | |

USI, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing December 27, 2019 | | | 2,264 | | | | 2,188,187 | |

| | | | | | | | | |

| | | | | | $ | 15,391,733 | |

| | | | | | | | | |

|

Leisure Goods / Activities / Movies — 3.6% | |

AMC Entertainment, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing December 15, 2022 | | $ | 1,375 | | | $ | 1,375,172 | |

Ancestry.com, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing August 17, 2022 | | | 1,397 | | | | 1,391,263 | |

Bombardier Recreational Products, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing January 30, 2019 | | | 1,603 | | | | 1,588,432 | |

CDS U.S. Intermediate Holdings, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing July 8, 2022 | | | 274 | | | | 259,568 | |

ClubCorp Club Operations, Inc. | | | | | | | | |

Term Loan, Maturing December 15, 2022(2) | | | 1,225 | | | | 1,220,406 | |

Emerald Expositions Holding, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing June 17, 2020 | | | 546 | | | | 539,032 | |

Fender Musical Instruments Corporation | | | | | | | | |

Term Loan, 5.75%, Maturing April 3, 2019 | | | 133 | | | | 131,132 | |

Live Nation Entertainment, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing August 16, 2020 | | | 169 | | | | 169,176 | |

LTF Merger Sub, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing June 10, 2022 | | | 846 | | | | 824,600 | |

Nord Anglia Education Finance, LLC | | | | | | | | |

Term Loan, 5.00%, Maturing March 31, 2021 | | | 1,824 | | | | 1,778,391 | |

Regal Cinemas Corporation | | | | | | | | |

Term Loan, 3.80%, Maturing April 1, 2022 | | | 2,477 | | | | 2,475,504 | |

Sabre, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing February 19, 2019 | | | 631 | | | | 624,983 | |

SeaWorld Parks & Entertainment, Inc. | | | | | | | | |

Term Loan, 3.00%, Maturing May 14, 2020 | | | 1,467 | | | | 1,377,717 | |

SRAM, LLC | | | | | | | | |

Term Loan, 4.02%, Maturing April 10, 2020 | | | 1,389 | | | | 1,152,757 | |

Town Sports International, Inc. | | | | | | | | |

Term Loan, 4.50%, Maturing November 15, 2020 | | | 728 | | | | 294,724 | |

WMG Acquisition Corp. | | | | | | | | |

Term Loan, 3.75%, Maturing July 1, 2020 | | | 1,015 | | | | 964,973 | |

Zuffa, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing February 25, 2020 | | | 3,410 | | | | 3,331,293 | |

| | | | | | | | | |

| | | $ | 19,499,123 | |

| | | | | | | | | |

| | | | |

| | 14 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Lodging and Casinos — 2.6% | | | | | | | | |

Amaya Holdings B.V. | | | | | | | | |

Term Loan, 5.00%, Maturing August 1, 2021 | | $ | 2,843 | | | $ | 2,663,202 | |

Boyd Gaming Corporation | | | | | | | | |

Term Loan, 4.00%, Maturing August 14, 2020 | | | 244 | | | | 242,757 | |

Caesars Entertainment Operating Company | | | | | | | | |

Term Loan, 0.00%, Maturing March 1, 2017(4) | | | 785 | | | | 690,727 | |

CityCenter Holdings, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing October 16, 2020 | | | 488 | | | | 485,667 | |

Four Seasons Holdings, Inc. | | | | | | | | |

Term Loan, 3.50%, Maturing June 27, 2020 | | | 390 | | | | 385,395 | |

Golden Nugget, Inc. | | | | | | | | |

Term Loan, 5.50%, Maturing November 21, 2019 | | | 86 | | | | 85,189 | |

Term Loan, 5.50%, Maturing November 21, 2019 | | | 200 | | | | 198,775 | |

Hilton Worldwide Finance, LLC | | | | | | | | |

Term Loan, 3.50%, Maturing October 26, 2020 | | | 3,144 | | | | 3,140,933 | |

MGM Resorts International | | | | | | | | |

Term Loan, 3.50%, Maturing December 20, 2019 | | | 1,892 | | | | 1,870,813 | |

Pinnacle Entertainment, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing August 13, 2020 | | | 172 | | | | 171,477 | |

Playa Resorts Holding B.V. | | | | | | | | |

Term Loan, 4.00%, Maturing August 9, 2019 | | | 1,273 | | | | 1,238,187 | |

RHP Hotel Properties L.P. | | | | | | | | |

Term Loan, 3.50%, Maturing January 15, 2021 | | | 419 | | | | 418,167 | |

Scientific Games International, Inc. | | | | | | | | |

Term Loan, 6.00%, Maturing October 18, 2020 | | | 1,862 | | | | 1,717,229 | |

Term Loan, 6.00%, Maturing October 1, 2021 | | | 619 | | | | 566,930 | |

Tropicana Entertainment, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing November 27, 2020 | | | 220 | | | | 218,838 | |

| | | | | | | | | |

| | | $ | 14,094,286 | |

| | | | | | | | | |

| | |

Nonferrous Metals / Minerals — 1.4% | | | | | | | | |

Alpha Natural Resources, LLC | | | | | | | | |

DIP Loan, 10.00%, Maturing January 31, 2017 | | $ | 200 | | | $ | 191,000 | |

Term Loan, 3.50%, Maturing May 22, 2020 | | | 1,393 | | | | 625,662 | |

Arch Coal, Inc. | | | | | | | | |

Term Loan, 6.25%, Maturing May 16, 2018 | | | 2,394 | | | | 1,105,337 | |

Dynacast International, LLC | | | | | | | | |

Term Loan, 4.50%, Maturing January 28, 2022 | | | 422 | | | | 411,267 | |

Fairmount Santrol, Inc. | | | | | | | | |

Term Loan, 3.88%, Maturing March 15, 2017 | | | 244 | | | | 172,895 | |

Term Loan, 4.50%, Maturing September 5, 2019 | | | 2,202 | | | | 1,103,665 | |

Murray Energy Corporation | | | | | | | | |

Term Loan, 7.00%, Maturing April 16, 2017 | | | 199 | | | | 159,853 | |

Term Loan, 7.50%, Maturing April 16, 2020 | | | 1,219 | | | | 785,495 | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Nonferrous Metals / Minerals (continued) | | | | | | | | |

Noranda Aluminum Acquisition Corporation | | | | | | | | |

Term Loan, 5.75%, Maturing February 28, 2019 | | $ | 481 | | | $ | 245,037 | |

Novelis, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing June 2, 2022 | | | 1,667 | | | | 1,595,273 | |

Oxbow Carbon, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing July 19, 2019 | | | 1,385 | | | | 1,299,737 | |

| | | | | | | | | |

| | | | | | $ | 7,695,221 | |

| | | | | | | | | |

| | |

Oil and Gas — 2.4% | | | | | | | | |

Ameriforge Group, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing December 19, 2019 | | $ | 2,170 | | | $ | 672,796 | |

Bronco Midstream Funding, LLC | | | | | | | | |

Term Loan, 5.00%, Maturing August 15, 2020 | | | 939 | | | | 774,541 | |

CITGO Holding, Inc. | | | | | | | | |

Term Loan, 9.50%, Maturing May 12, 2018 | | | 643 | | | | 641,883 | |

CITGO Petroleum Corporation | | | | | | | | |

Term Loan, 4.50%, Maturing July 29, 2021 | | | 716 | | | | 694,459 | |

Crestwood Holdings, LLC | | | | | | | | |

Term Loan, 7.00%, Maturing June 19, 2019 | | | 1,178 | | | | 747,766 | |

Drillships Ocean Ventures, Inc. | | | | | | | | |

Term Loan, 5.50%, Maturing July 25, 2021 | | | 790 | | | | 379,200 | |

Energy Transfer Equity L.P. | | | | | | | | |

Term Loan, 3.25%, Maturing December 2, 2019 | | | 1,025 | | | | 925,916 | |

Term Loan, 4.00%, Maturing December 2, 2019 | | | 256 | | | | 233,065 | |

Fieldwood Energy, LLC | | | | | | | | |

Term Loan, 3.88%, Maturing September 28, 2018 | | | 636 | | | | 435,489 | |

Term Loan - Second Lien, 8.38%, Maturing September 30, 2020 | | | 425 | | | | 66,937 | |

Floatel International Ltd. | | | | | | | | |

Term Loan, 6.00%, Maturing June 27, 2020 | | | 1,673 | | | | 756,902 | |

MEG Energy Corp. | | | | | | | | |

Term Loan, 3.75%, Maturing March 31, 2020 | | | 3,176 | | | | 2,786,761 | |

Paragon Offshore Finance Company | | | | | | | | |

Term Loan, 3.75%, Maturing July 18, 2021 | | | 642 | | | | 187,748 | |

Samson Investment Company | | | | | | | | |

Term Loan - Second Lien, 0.00%, Maturing September 25, 2018(4) | | | 1,425 | | | | 71,250 | |

Seadrill Partners Finco, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing February 21, 2021 | | | 2,427 | | | | 1,004,135 | |

Seventy Seven Operating, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing June 25, 2021 | | | 345 | | | | 253,104 | |

Sheridan Investment Partners II L.P. | | | | | | | | |

Term Loan, 4.25%, Maturing December 16, 2020 | | | 22 | | | | 13,055 | |

Term Loan, 4.25%, Maturing December 16, 2020 | | | 60 | | | | 35,005 | |

Term Loan, 4.25%, Maturing December 16, 2020 | | | 432 | | | | 251,637 | |

| | | | |

| | 15 | | See Notes to Financial Statements. |

Eaton Vance

VT Floating-Rate Income Fund

December 31, 2015

Portfolio of Investments — continued

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Oil and Gas (continued) | | | | | | | | |

Sheridan Production Partners I, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing October 1, 2019 | | $ | 77 | | | $ | 45,689 | |

Term Loan, 4.25%, Maturing October 1, 2019 | | | 127 | | | | 74,801 | |

Term Loan, 4.25%, Maturing October 1, 2019 | | | 957 | | | | 564,500 | |

Southcross Energy Partners L.P. | | | | | | | | |

Term Loan, 5.25%, Maturing August 4, 2021 | | | 493 | | | | 353,369 | |

Southcross Holdings Borrower L.P. | | | | | | | | |

Term Loan, 6.00%, Maturing August 4, 2021 | | | 296 | | | | 160,309 | |

Targa Resources Corp. | | | | | | | | |

Term Loan, 5.75%, Maturing February 25, 2022 | | | 177 | | | | 171,884 | |

Tervita Corporation | | | | | | | | |

Term Loan, 6.25%, Maturing May 15, 2018 | | | 764 | | | | 594,733 | |

| | | | | | | | | |

| | | | | | $ | 12,896,934 | |

| | | | | | | | | |

| | |

Publishing — 1.4% | | | | | | | | |

682534 N.B., Inc. | | | | | | | | |

Term Loan, 12.00%, (8.00% Cash, 4.00% PIK), Maturing October 1, 2020(3) | | $ | 227 | | | $ | 181,107 | |

Ascend Learning, LLC | | | | | | | | |

Term Loan, 5.50%, Maturing July 31, 2019 | | | 808 | | | | 806,816 | |

Getty Images, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing October 18, 2019 | | | 3,764 | | | | 2,387,565 | |

Laureate Education, Inc. | | | | | | | | |

Term Loan, 5.00%, Maturing June 15, 2018 | | | 2,277 | | | | 1,912,553 | |

McGraw-Hill Global Education Holdings, LLC | | | | | | | | |

Term Loan, 4.75%, Maturing March 22, 2019 | | | 354 | | | | 349,783 | |

Merrill Communications, LLC | | | | | | | | |

Term Loan, 6.25%, Maturing June 1, 2022 | | | 373 | | | | 341,073 | |

Penton Media, Inc. | | | | | | | | |

Term Loan, 4.75%, Maturing October 3, 2019 | | | 377 | | | | 375,208 | |

ProQuest, LLC | | | | | | | | |

Term Loan, 5.75%, Maturing October 24, 2021 | | | 495 | | | | 481,998 | |

Springer Science+Business Media Deutschland GmbH | | | | | | | | |

Term Loan, 4.75%, Maturing August 14, 2020 | | | 858 | | | | 825,162 | |

| | | | | | | | | |

| | | | | | $ | 7,661,265 | |

| | | | | | | | | |

| | |

Radio and Television — 2.4% | | | | | | | | |

ALM Media Holdings, Inc. | | | | | | | | |

Term Loan, 5.50%, Maturing July 31, 2020 | | $ | 315 | | | $ | 284,241 | |

AP NMT Acquisition B.V. | | | | | | | | |

Term Loan, 6.75%, Maturing August 13, 2021 | | | 321 | | | | 287,239 | |

Block Communications, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing November 7, 2021 | | | 148 | | | | 147,014 | |

| | | | | | | | |

| Borrower/Tranche Description | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

| | |

Radio and Television (continued) | | | | | | | | |

CCO Safari III, LLC | | | | | | | | |

Term Loan, 3.50%, Maturing January 24, 2023 | | $ | 1,275 | | | $ | 1,274,044 | |

Cumulus Media Holdings, Inc. | | | | | | | | |

Term Loan, 4.25%, Maturing December 23, 2020 | | | 2,609 | | | | 1,987,200 | |

Entercom Radio, LLC | | | | | | | | |

Term Loan, 4.00%, Maturing November 23, 2018 | | | 162 | | | | 161,024 | |

Entravision Communications Corporation | | | | | | | | |

Term Loan, 3.50%, Maturing May 31, 2020 | | | 2,005 | | | | 1,958,116 | |

Gray Television, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing June 10, 2021 | | | 156 | | | | 154,283 | |

Hubbard Radio, LLC | | | | | | | | |

Term Loan, 4.25%, Maturing May 27, 2022 | | | 415 | | | | 386,988 | |

iHeartCommunications, Inc. | | | | | | | | |

Term Loan, 7.17%, Maturing January 30, 2019 | | | 453 | | | | 319,276 | |

Term Loan, 7.92%, Maturing July 30, 2019 | | | 146 | | | | 102,806 | |

MGOC, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing July 31, 2020 | | | 870 | | | | 860,246 | |

Mission Broadcasting, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing October 1, 2020 | | | 424 | | | | 421,850 | |

Nexstar Broadcasting, Inc. | | | | | | | | |

Term Loan, 3.75%, Maturing October 1, 2020 | | | 481 | | | | 478,385 | |

Raycom TV Broadcasting, LLC | | | | | | | | |

Term Loan, 3.75%, Maturing August 4, 2021 | | | 431 | | | | 428,889 | |

TWCC Holding Corp. | | | | | | | | |

Term Loan - Second Lien, 7.00%, Maturing June 26, 2020 | | | 375 | | | | 374,414 | |

Univision Communications, Inc. | | | | | | | | |

Term Loan, 4.00%, Maturing March 1, 2020 | | | 486 | | | | 476,700 | |