Exhibit 99.23

Project Island –Discussion MaterialsDecember 23, 2015

Table of Contents ConfidentialI. Review of T-Co Investment in TahitiII. Comments on Merger Agreement Draft Mark-UpIII. Updated Merger AnalysisIV. Potential Alternative Scenarios – Discussion and AnalysisV. Updated Tahiti Pro Forma EPS Accretion/Dilution AnalysisThis document and any other materials accompanying this document (collectively, the “Materials”) are provided for general informational purposes only. By accepting any Materials, the recipient acknowledges and agrees to keep the Materials confidential and not to distribute the Materials to any other party. ©2015 Wells Fargo Securities. All Rights Reserved.Project Island 2

Review of T-Co Investment in Tahiti

T-Co PIPE Investment in Tahiti - Transaction Summary ConfidentialPartiesType of SecuritiesPurchase PricePro Forma CommonStock OwnershipUse of ProceedsBoard RepresentationPublic OfferingMerger DilutionTransferRestrictionsConditions to ClosingShare Subscription Agreement Overview? “Tahiti”, a Taiwanese corporation and “T-Co” (the “Subscriber”), a Chinese corporation? Common stock of Tahiti? NT$11,970,080,000 (~US$368,200,000) at NT$40 (~US$1.22) per share for 299,252,000 shares? 25% of Tahiti’s shares outstanding? R&D and production capacity, investment in Tahiti Shanghai and support of the Tahiti-Barbados merger and merger strategy in the semiconductor industry? 1 Board seat as long as T-Co’s pro forma ownership interest in Tahiti does not fall below 5%? Three years after the closing, Tahiti will seek to file for a public offering related to the private placement shares on the Taiwan Exchange if required conditions for the shares by the exchange are met? T-Co’s 25% stake is not to be diluted as a result of any subsequent merger between Tahiti and Barbados? 1 month notice required before transferring shares to a 3rd party during which Tahiti may attempt to purchase shares from T-Co? T-Co may not sell to specified 3rd parties without Tahiti consent? Transfer restrictions will not be imposed on T-Co if they own less than 5% of Tahiti or T-Co does not have a Board seat? Tahiti shareholder approval? Relevant government approvalSources: Tahiti – T-Co Subscription Agreement dated 12/11/2015Project Island 4

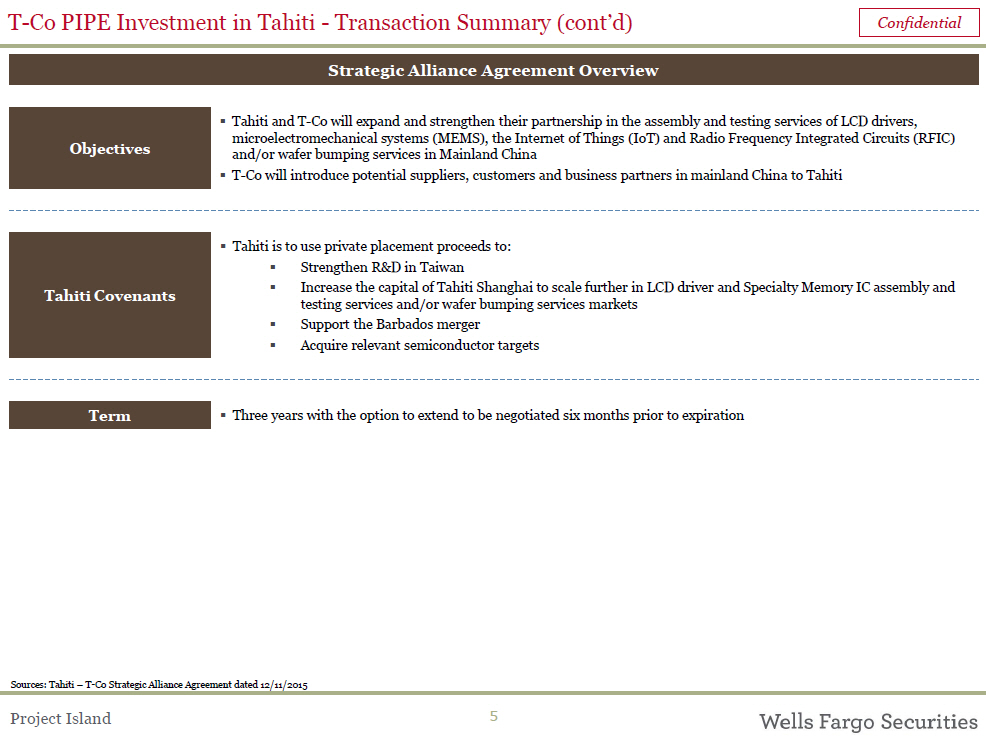

T-Co PIPE Investment in Tahiti - Transaction Summary (cont’d) ConfidentialObjectivesTahiti CovenantsTermStrategic Alliance Agreement Overview? Tahiti and T-Co will expand and strengthen their partnership in the assembly and testing services of LCD drivers, microelectromechanical systems (MEMS), the Internet of Things (IoT) and Radio Frequency Integrated Circuits (RFIC)and/or wafer bumping services in Mainland China ? T-Co will introduce potential suppliers, customers and business partners in mainland China to Tahiti? Tahiti is to use private placement proceeds to:? Strengthen R&D in Taiwan? Increase the capital of Tahiti Shanghai to scale further in LCD driver and Specialty Memory IC assembly and testing services and/or wafer bumping services markets? Support the Barbados merger? Acquire relevant semiconductor targets? Three years with the option to extend to be negotiated six months prior to expirationSources: Tahiti – T-Co Strategic Alliance Agreement dated 12/11/2015Project Island 5

Market Reaction to T-Co’s NT$12.0 Billion Investment in Tahiti at NT$40.0 per Common Share Confidential Barbados Stock Price Reaction ($ in USD) $20.50 Barbados closed at $19.48; up 4.5% from prior day’s close, up 6.4% against S&P 500 $20.00 Transaction announced before U.S. market opened on $19.50 December 11$19.00$18.58$18.50$18.0012/7/15 12/8/15 12/9/15 12/10/15 12/11/15 12/14/15 12/15/15 12/16/15 12/17/15 12/18/15Tahiti Stock Price Reaction($ in NTD) $36.00 Tahiti closed at NT$34.75; up 8.1% from prior day’s close, up9.0% against Taiwan TAIEX $35.00 $34.00 Transaction announced after Taiwan market closed onDecember 11 $33.00 $32.00 $32.05$31.00 12/6/15 12/7/15 12/8/15 12/9/15 12/10/15 12/13/15 12/14/15 12/15/15 12/16/15 12/17/15Source: Wall Street research and FactSet; Note: As of 12/18/15Project Island 6

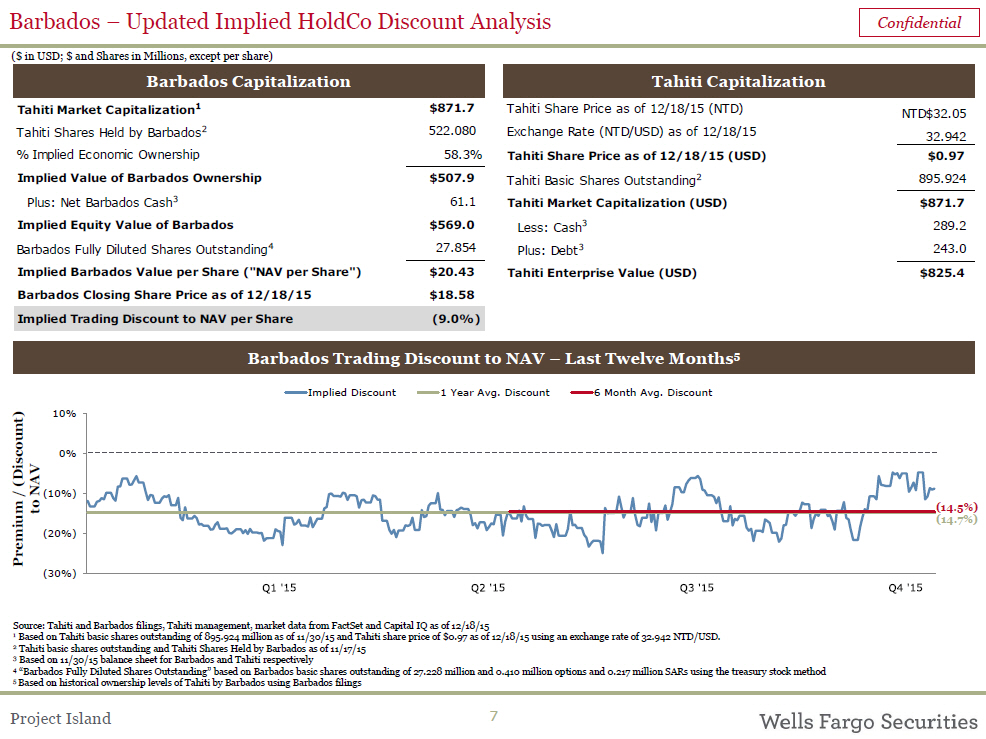

Barbados – Updated Implied HoldCo Discount Analysis Confidential($ in USD; $ and Shares in Millions, except per share)Barbados Capitalization Tahiti Capitalization Tahiti Market Capitalization1 $871.7 Tahiti Share Price as of 12/18/15 (NTD) NTD$32.05Tahiti Shares Held by Barbados2 522.080 Exchange Rate (NTD/USD) as of 12/18/15 32.942% Implied Economic Ownership 58.3% Tahiti Share Price as of 12/18/15 (USD) $0.97Implied Value of Barbados Ownership $507.9 Tahiti Basic Shares Outstanding2 895.924 Plus: Net Barbados Cash3 61.1 Tahiti Market Capitalization (USD) $871.7 Implied Equity Value of Barbados $569.0 Less: Cash3 289.2 Barbados Fully Diluted Shares Outstanding4 27.854 Plus: Debt3 243.0 Implied Barbados Value per Share ("NAV per Share") $20.43 Tahiti Enterprise Value (USD) $825.4 Barbados Closing Share Price as of 12/18/15 $18.58 Implied Trading Discount to NAV per Share (9.0%)Barbados Trading Discount to NAV – Last Twelve Months5Implied Discount 1 Year Avg. Discount 6 Month Avg. Discount (Discount) 10% 0%/NAV (10%) to (14.5%) Premium (14.7%) (20%)(30%)Source: Tahiti and Barbados filings, Tahiti management, market data from FactSet and Capital IQ as of 12/18/15 1 Based on Tahiti basic shares outstanding of 895.924 million as of 11/30/15 and Tahiti share price of $0.97 as of 12/18/15 using an exchange rate of 32.942 NTD/USD.2 Tahiti basic shares outstanding and Tahiti Shares Held by Barbados as of 11/17/153 Based on 11/30/15 balance sheet for Barbados and Tahiti respectively4 “Barbados Fully Diluted Shares Outstanding” based on Barbados basic shares outstanding of 27.228 million and 0.410 million options and 0.217 million SARs using the treasury stock method5 Based on historical ownership levels of Tahiti by Barbados using Barbados filingsProject Island 7

Comments on Merger Agreement Draft Mark-Up

Comments on Merger Agreement Draft Mark-Up Confidential? Article 1. Definitions:? Added a note to draft that ChipMOS Taiwan is to determine the share/ADS ratio – we should discuss appropriate ratio targeted to appropriate share price range once ADRs start trading in the open market? To discuss with counsel and/or CS? Added back in the concept of the extra-ordinary dividend and reference technical issues under Bermuda and ROC law which complicates disclosure. Language also added in Section 6.05? To discuss with counsel and/or CS. Need to research tax implications? Noted that the exchange ratio should be updated prior to signing? To discuss with counsel and/or CS? Added the concept of disclosure schedules to the agreement? TBD – Based on level of disclosure required? Changed the definition of “Per Share Value” to be based on prior 10 trading days (vs 30 prior days in previous version). There is a note that this change should be discussed? To discuss with counsel and/or CSProject Island 9

Comments on Merger Agreement Draft Mark-Up (Continued) Confidential? Article 2:? There is a note requesting IMOS to confirm Appleby has started the process of having the merger “recognized” in Bermuda? Appleby to follow up? 2.07: Noted that cashing out the IMOS Share Plans is not an adverse change and there are significant challenges to rolling plans into Taiwan? To discuss with Tahiti counsel and/or CS given we view consents as necessary? 2.07(b): They view the ChipMOS Taiwan Equity Award Contribution as fixed and not subject to adjustment? To discuss with counsel and/or CS? 2.07(b): Changed the payment of the Equity Award Payments to be the responsibility of the surviving company via the payroll process after closing? To discuss with Tahiti counsel? 10.01(b)(iv): Removed IMOS ability to solicit additional acquisition proposals if a Superior Proposal is received? Suggest pushing back on this so additional interest can be solicited as part of fiduciary process? 11.04(b): They have asked to discuss the Termination Fee and proposed the Reverse Termination Fee equate to 2x the Termination Fee? To discuss with counsel and/or CSProject Island 10

Updated Merger Analysis

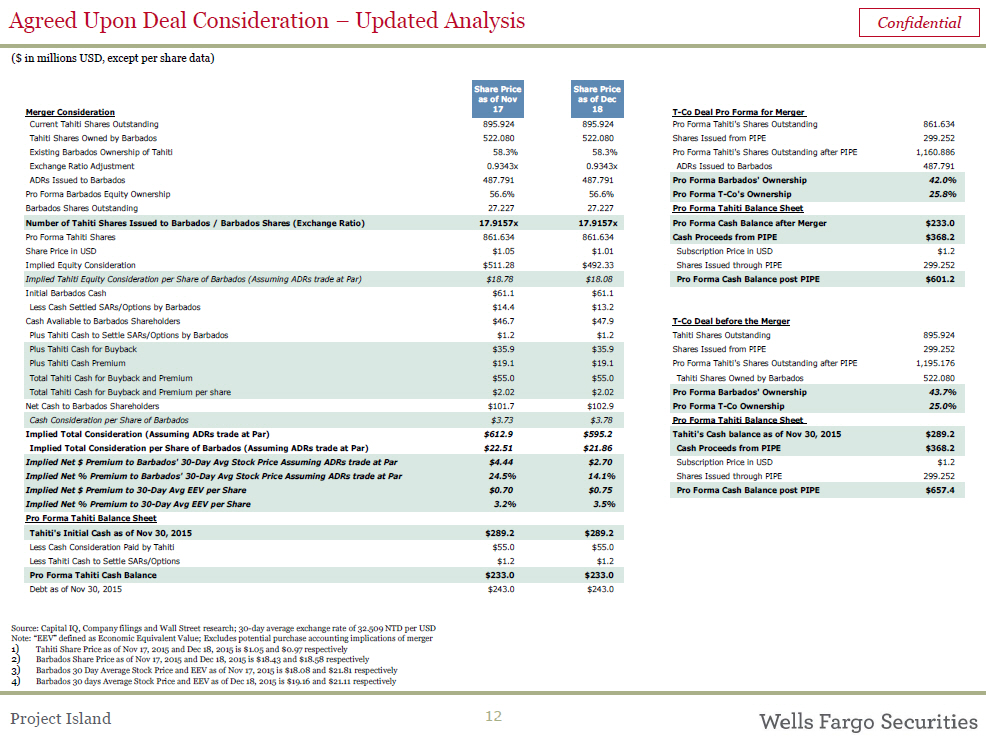

Agreed Upon Deal Consideration – Updated Analysis Confidential($ in millions USD, except per share data)Share Price Share Price as of Nov as of Dec Merger Consideration 17 18Current Tahiti Shares Outstanding 895.924 895.924 Tahiti Shares Owned by Barbados 522.080 522.080 Existing Barbados Ownership of Tahiti 58.3% 58.3% Exchange Ratio Adjustment 0.9343x 0.9343x ADRs Issued to Barbados 487.791 487.791 Pro Forma Barbados Equity Ownership 56.6% 56.6% Barbados Shares Outstanding 27.227 27.227 Number of Tahiti Shares Issued to Barbados / Barbados Shares (Exchange Ratio) 17.9157x 17.9157x Pro Forma Tahiti Shares 861.634 861.634 Share Price in USD $1.05 $1.01 Implied Equity Consideration $511.28 $492.33 Implied Tahiti Equity Consideration per Share of Barbados (Assuming ADRs trade at Par) $18.78 $18.08 Initial Barbados Cash $61.1 $61.1 Less Cash Settled SARs/Options by Barbados $14.4 $13.2 Cash Avaliable to Barbados Shareholders $46.7 $47.9 Plus Tahiti Cash to Settle SARs/Options by Barbados $1.2 $1.2 Plus Tahiti Cash for Buyback $35.9 $35.9 Plus Tahiti Cash Premium $19.1 $19.1 Total Tahiti Cash for Buyback and Premium $55.0 $55.0 Total Tahiti Cash for Buyback and Premium per share $2.02 $2.02 Net Cash to Barbados Shareholders $101.7 $102.9 Cash Consideration per Share of Barbados $3.73 $3.78 Implied Total Consideration (Assuming ADRs trade at Par) $612.9 $595.2 Implied Total Consideration per Share of Barbados (Assuming ADRs trade at Par) $22.51 $21.86 Implied Net $ Premium to Barbados' 30-Day Avg Stock Price Assuming ADRs trade at Par $4.44 $2.70 Implied Net % Premium to Barbados' 30-Day Avg Stock Price Assuming ADRs trade at Par 24.5% 14.1% Implied Net $ Premium to 30-Day Avg EEV per Share $0.70 $0.75 Implied Net % Premium to 30-Day Avg EEV per Share 3.2% 3.5% Pro Forma Tahiti Balance Sheet Tahiti's Initial Cash as of Nov 30, 2015 $289.2 $289.2 Less Cash Consideration Paid by Tahiti $55.0 $55.0 Less Tahiti Cash to Settle SARs/Options $1.2 $1.2 Pro Forma Tahiti Cash Balance $233.0 $233.0 Debt as of Nov 30, 2015 $243.0 $243.0Source: Capital IQ, Company filings and Wall Street research; 30-day average exchange rate of 32.509 NTD per USDNote: “EEV” defined as Economic Equivalent Value; Excludes potential purchase accounting implications of merger 1) Tahiti Share Price as of Nov 17, 2015 and Dec 18, 2015 is $1.05 and $0.97 respectively2) Barbados Share Price as of Nov 17, 2015 and Dec 18, 2015 is $18.43 and $18.58 respectively3) Barbados 30 Day Average Stock Price and EEV as of Nov 17, 2015 is $18.08 and $21.81 respectively4) Barbados 30 days Average Stock Price and EEV as of Dec 18, 2015 is $19.16 and $21.11 respectivelyT-Co Deal Pro Forma for Merger Pro Forma Tahiti's Shares Outstanding 861.634 Shares Issued from PIPE 299.252 Pro Forma Tahiti's Shares Outstanding after PIPE 1,160.886 ADRs Issued to Barbados 487.791 Pro Forma Barbados' Ownership 42.0% Pro Forma T-Co's Ownership 25.8% Pro Forma Tahiti Balance Sheet Pro Forma Cash Balance after Merger $233.0 Cash Proceeds from PIPE $368.2 Subscription Price in USD $1.2 Shares Issued through PIPE 299.252 Pro Forma Cash Balance post PIPE $601.2 T-Co Deal before the Merger Tahiti Shares Outstanding 895.924 Shares Issued from PIPE 299.252 Pro Forma Tahiti's Shares Outstanding after PIPE 1,195.176 Tahiti Shares Owned by Barbados 522.080 Pro Forma Barbados' Ownership 43.7% Pro Forma T-Co Ownership 25.0% Pro Forma Tahiti Balance Sheet Tahiti's Cash balance as of Nov 30, 2015 $289.2 Cash Proceeds from PIPE $368.2 Subscription Price in USD $1.2 Shares Issued through PIPE 299.252 Pro Forma Cash Balance post PIPE $657.4Project Island 12

Potential Alternative Scenarios – Discussion and Analysis

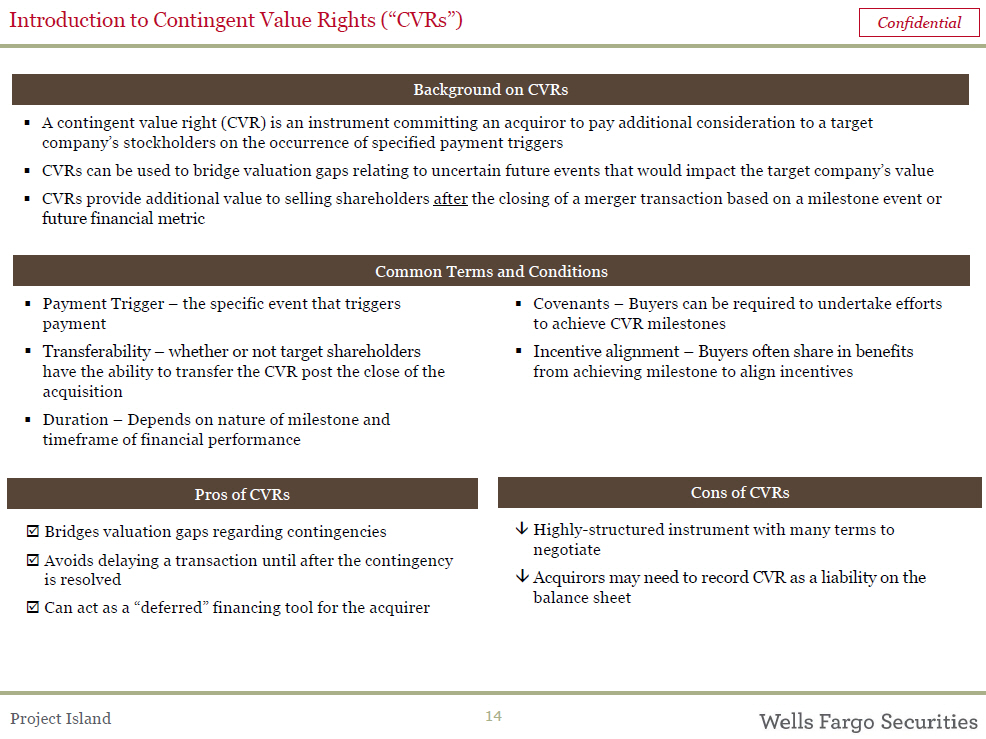

Introduction to Contingent Value Rights (“CVRs”) ConfidentialBackground on CVRs? A contingent value right (CVR) is an instrument committing an acquiror to pay additional consideration to a target company’s stockholders on the occurrence of specified payment triggers? CVRs can be used to bridge valuation gaps relating to uncertain future events that would impact the target company’s value? CVRs provide additional value to selling shareholders after the closing of a merger transaction based on a milestone event or future financial metricCommon Terms and Conditions? Payment Trigger – the specific event that triggers payment? Transferability – whether or not target shareholders have the ability to transfer the CVR post the close of the acquisition? Duration – Depends on nature of milestone and timeframe of financial performancePros of CVRs? Bridges valuation gaps regarding contingencies? Avoids delaying a transaction until after the contingency is resolved? Can act as a “deferred” financing tool for the acquirer? Covenants – Buyers can be required to undertake efforts to achieve CVR milestones? Incentive alignment – Buyers often share in benefits from achieving milestone to align incentivesCons of CVRs? Highly-structured instrument with many terms to negotiate? Acquirors may need to record CVR as a liability on the balance sheetProject Island 14

Hypothetical Sensitivity Analysis Including CVRs – At Current Stock Price Confidential($ in USD million, except per share data) Contingent Value Rights CVR / Share Analysis at Various Price $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 CVR Cash per Share $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 Total Tahiti Cash for CVR $0.00 $13.61 $27.23 $40.84 $54.45 $68.07 $81.68 $95.29 Initial Barbados Cash $61.1 $61.1 $61.1 $61.1 $61.1 $61.1 $61.1 $61.1 Less Cash Settled SARs/Options by Barbados $13.2 $13.8 $14.4 $15.0 $15.9 $16.5 $18.3 $19.6 Barbados Cash Avaliable to Barbados Shareholders - Per Merger $47.9 $47.3 $46.7 $46.1 $45.2 $44.5 $42.8 $41.5 Plus Tahiti Cash to Barbados Shareholders - Per Merger $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 Total Cash to Barbados Shareholders from Merger $102.9 $102.3 $101.7 $101.1 $100.2 $99.5 $97.8 $96.5 Total Cash to Barbados Shareholders - including CVR $102.9 $115.9 $128.9 $141.9 $154.6 $167.6 $179.5 $191.8 Net Cash Consideration / Share - including CVR $3.78 $4.26 $4.73 $5.21 $5.68 $6.16 $6.59 $7.04 Tahiti Share Price in USD $1.01 $1.01 $1.01 $1.01 $1.01 $1.01 $1.01 $1.01 ADRs Issued to Barbados $487.79 $487.79 $487.79 $487.79 $487.79 $487.79 $487.79 $487.79 Implied Tahiti Equity Consideration (Assuming ADRs trade at Par) $492.33 $492.33 $492.33 $492.33 $492.33 $492.33 $492.33 $492.33 Implied Tahiti Equity Consideration per Share of Barbados (Assuming ADRs trade at Par) $18.08 $18.08 $18.08 $18.08 $18.08 $18.08 $18.08 $18.08 Implied Total Consideration (Assuming ADRs Trade at Par & CVR) $595.21 $608.20 $621.23 $634.26 $646.95 $659.94 $671.82 $684.13 Implied Total Consideration per Share of Barbados (Assuming ADRs trade at Par & CVR) $21.86 $22.34 $22.82 $23.30 $23.76 $24.24 $24.67 $25.13 Implied Net $ Premium to Barbados' 30-Day Avg Stock Price Assuming ADRs trade at Par & CVR ($19.16) $2.70 $3.17 $3.65 $4.13 $4.60 $5.07 $5.51 $5.96 Implied Net % Premium to Barbados' 30-Day Avg Stock Price Assuming ADRs trade at Par & CVR ($19.16) 14.1% 16.6% 19.1% 21.6% 24.0% 26.5% 28.8% 31.1% Implied Net $ Premium to 30-Day Avg EEV per Share ($21.11) $0.75 $1.23 $1.70 $2.18 $2.65 $3.13 $3.56 $4.01 Implied Net % Premium to 30-Day Avg EEV per Share ($21.11) 3.5% 5.8% 8.1% 10.3% 12.5% 14.8% 16.9% 19.0% Pro Forma Tahiti Balance Sheet Tahiti's Initial Cash as of Nov 30, 2015 $289.2 $289.2 $289.2 $289.2 $289.2 $289.2 $289.2 $289.2 Plus Cash Proceeds from PIPE $368.2 $368.2 $368.2 $368.2 $368.2 $368.2 $368.2 $368.2 Less Cash to Barbados Shareholders - Per Merger $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 Less Tahiti Cash to Settle SARs/Options $1.2 $1.2 $1.2 $1.2 $1.2 $1.2 $1.2 $1.2 Less Cash used for CVR $0.0 $13.6 $27.2 $40.8 $54.5 $68.1 $81.7 $95.3 Total Cash Used from Tahiti $56.2 $69.8 $83.4 $97.1 $110.7 $124.3 $137.9 $151.5 Pro Forma Tahiti Cash Position $601.2 $587.6 $574.0 $560.4 $546.7 $533.1 $519.5 $505.9Source: CapitalIQ and Company filings; Market data as of 12/18/15; based on a 30 day average FX rate of NWT32.509/USD 1) Tahiti Share Price as of Dec 18, 2015 is $0.972) Barbados Share Price as of Dec 18, 2015 is $18.583) Barbados 30 days Average Stock Price and EEV as of Dec 18, 2015 is $19.16 and $21.11 respectivelyProject Island 15

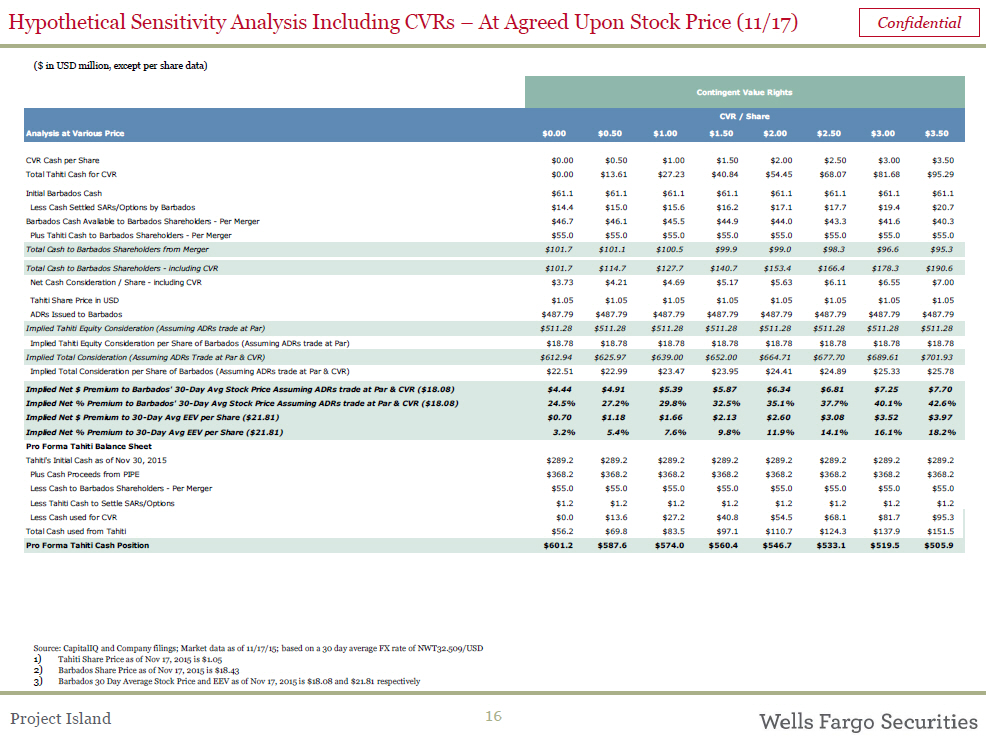

Hypothetical Sensitivity Analysis Including CVRs – At Agreed Upon Stock Price (11/17) Confidential($ in USD million, except per share data) Contingent Value Rights CVR / Share Analysis at Various Price $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 CVR Cash per Share $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 Total Tahiti Cash for CVR $0.00 $13.61 $27.23 $40.84 $54.45 $68.07 $81.68 $95.29 Initial Barbados Cash $61.1 $61.1 $61.1 $61.1 $61.1 $61.1 $61.1 $61.1 Less Cash Settled SARs/Options by Barbados $14.4 $15.0 $15.6 $16.2 $17.1 $17.7 $19.4 $20.7 Barbados Cash Avaliable to Barbados Shareholders - Per Merger $46.7 $46.1 $45.5 $44.9 $44.0 $43.3 $41.6 $40.3 Plus Tahiti Cash to Barbados Shareholders - Per Merger $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 Total Cash to Barbados Shareholders from Merger $101.7 $101.1 $100.5 $99.9 $99.0 $98.3 $96.6 $95.3 Total Cash to Barbados Shareholders - including CVR $101.7 $114.7 $127.7 $140.7 $153.4 $166.4 $178.3 $190.6 Net Cash Consideration / Share - including CVR $3.73 $4.21 $4.69 $5.17 $5.63 $6.11 $6.55 $7.00 Tahiti Share Price in USD $1.05 $1.05 $1.05 $1.05 $1.05 $1.05 $1.05 $1.05 ADRs Issued to Barbados $487.79 $487.79 $487.79 $487.79 $487.79 $487.79 $487.79 $487.79 Implied Tahiti Equity Consideration (Assuming ADRs trade at Par) $511.28 $511.28 $511.28 $511.28 $511.28 $511.28 $511.28 $511.28 Implied Tahiti Equity Consideration per Share of Barbados (Assuming ADRs trade at Par) $18.78 $18.78 $18.78 $18.78 $18.78 $18.78 $18.78 $18.78 Implied Total Consideration (Assuming ADRs Trade at Par & CVR) $612.94 $625.97 $639.00 $652.00 $664.71 $677.70 $689.61 $701.93 Implied Total Consideration per Share of Barbados (Assuming ADRs trade at Par & CVR) $22.51 $22.99 $23.47 $23.95 $24.41 $24.89 $25.33 $25.78 Implied Net $ Premium to Barbados' 30-Day Avg Stock Price Assuming ADRs trade at Par & CVR ($18.08) $4.44 $4.91 $5.39 $5.87 $6.34 $6.81 $7.25 $7.70 Implied Net % Premium to Barbados' 30-Day Avg Stock Price Assuming ADRs trade at Par & CVR ($18.08) 24.5% 27.2% 29.8% 32.5% 35.1% 37.7% 40.1% 42.6% Implied Net $ Premium to 30-Day Avg EEV per Share ($21.81) $0.70 $1.18 $1.66 $2.13 $2.60 $3.08 $3.52 $3.97 Implied Net % Premium to 30-Day Avg EEV per Share ($21.81) 3.2% 5.4% 7.6% 9.8% 11.9% 14.1% 16.1% 18.2% Pro Forma Tahiti Balance Sheet Tahiti's Initial Cash as of Nov 30, 2015 $289.2 $289.2 $289.2 $289.2 $289.2 $289.2 $289.2 $289.2 Plus Cash Proceeds from PIPE $368.2 $368.2 $368.2 $368.2 $368.2 $368.2 $368.2 $368.2 Less Cash to Barbados Shareholders - Per Merger $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 $55.0 Less Tahiti Cash to Settle SARs/Options $1.2 $1.2 $1.2 $1.2 $1.2 $1.2 $1.2 $1.2Less Cash used for CVR $0.0 $13.6 $27.2 $40.8 $54.5 $68.1 $81.7 $95.3 Total Cash used from Tahiti $56.2 $69.8 $83.5 $97.1 $110.7 $124.3 $137.9 $151.5 Pro Forma Tahiti Cash Position $601.2 $587.6 $574.0 $560.4 $546.7 $533.1 $519.5 $505.9Source: CapitalIQ and Company filings; Market data as of 11/17/15; based on a 30 day average FX rate of NWT32.509/USD 1) Tahiti Share Price as of Nov 17, 2015 is $1.052) Barbados Share Price as of Nov 17, 2015 is $18.433) Barbados 30 Day Average Stock Price and EEV as of Nov 17, 2015 is $18.08 and $21.81 respectivelyProject Island 16

Updated Tahiti Pro Forma EPS Accretion/Dilution Analysis

Illustrative Tahiti 2016E Accretion / Dilution Analysis Confidential(USD and Shares in Millions, except per share data) BASIC EPS METHOD Fiscal Year Ending 2016 Adjustments Tahiti Interco Others Total Adj. Combined Notes Total Net Sales $610.1 - - - $610.1 Cost of Goods Sold (Excluding D&A) 394.4 (1.4) - (1.4) 393.0 Licensing Fees Paid by Bermuda to Taiwan (1.0) - (1.0) • Licensing fees paid by Bermuda to Taiwan pursuant to use of technology patent right dated 4/7/2014 will be cancelled Licensing Fees Paid by Bermuda to Shanghai (0.4) - (0.4) • Licensing fees paid by Bermuda to Shanghai pursuant to use of technology patent right dated 10/2011 will be cancelled Gross Profit 215.7 1.4 - 1.4 217.1 Total SG&A1 48.1 - 2.0 2.0 50.2 Bermuda Personnel Expenses - 1.6 1.6 • Salary and benefits for CEO, CFO and Assistant to Chairman will be transferred to Taiwan Estimated ADR Listing Costs - 0.2 0.2 Others - 0.2 0.2 • Miscellaneous Bermuda advertising, travel expenses, etc will continue to be incurred at the Taiwan level EBITDA 167.5 1.4 (2.0) (0.6) 166.9 Depreciation & Amortization 108.3 - - - 108.3 EBIT 59.2 1.4 (2.0) (0.6) 58.6 Interest Income 2.3 - (0.2) (0.2) 2.1 • Interest income forgone due to reduction in cash Foreign Exchange Gain (Loss) - - - - - Other Gain (Loss) 2.4 (2.8) - (2.8) (0.4) Royalty Income of ChipMOS Taiwan (1.0) - (1.0) • Income received from Bermuda pursuant to sale of technology patent right dated 4/7/2014 will be cancelled Royalty Income of ChipMOS Taiwan (0.7) - (0.7) • Income received from Bermuda pursuant to sale of 50% technology patent right dated 4/12/2007 will be cancelled Patent Co-Development Contract (1.2) - (1.2) • Cost reimbursement received from Bermuda pursuant to patent co-development contract dated 1/1/2007 will be cancelled Interest Expenses (6.1) - - - (6.1) Pre-Tax Income 57.8 (1.4) (2.2) (3.6) 54.2 Income Taxes Expense 14.7 (0.3) (0.5) (0.9) 13.8 Consolidated Net Income 43.2 (1.0) (1.7) (2.7) 40.5 Attributable to Non-Controlling Interests - - - - - Net Income Available to Common $43.2 ($1.0) ($1.7) ($2.7) $40.5 Weighted Average Fully Diluted Shares Outstanding 896.304 (34.670) 861.634 Normalized Earnings per Share $0.048 $0.047 ($0.001) (2.5%)Source: Tahiti management Note:1. SG&A excludes one time merger expensesProject Island 18

Illustrative Tahiti 2016E Accretion / Dilution Analysis Confidential(NTD and Shares in Millions, except per share data) BASIC EPS METHOD Fiscal Year Ending 2016 Adjustments Tahiti Interco Others Total Adj. Combined Notes Total Net Sales $19,833.9 - - - $19,833.9 Cost of Goods Sold (Excluding D&A) 12,823.2 (46.8) - (46.8) 12,776.4 Licensing Fees Paid by Bermuda to Taiwan (33.0) - (33.0) • Licensing fees paid by Bermuda to Taiwan pursuant to use of technology patent right dated 4/7/2014 will be cancelled Licensing Fees Paid by Bermuda to Shanghai (13.8) - (13.8) • Licensing fees paid by Bermuda to Shanghai pursuant to use of technology patent right dated 10/2011 will be cancelled Gross Profit 7,010.7 46.8 - 46.8 7,057.5 Total SG&A1 1,565.2 - 65.6 65.6 1,630.8 Bermuda Personnel Expenses - 51.2 51.2 • Salary and benefits for CEO, CFO and Assistant to Chairman will be transferred to Taiwan Estimated ADR Listing Costs - 7.8 7.8 Others - 6.5 6.5 • Miscellaneous Bermuda advertising, travel expenses, etc will continue to be incurred at the Taiwan level EBITDA 5,445.5 46.8 (65.6) (18.8) 5,426.7 Depreciation & Amortization 3,521.4 - - - 3,521.4 EBIT 1,924.1 46.8 (65.6) (18.8) 1,905.3 Interest Income 75.1 - (6.9) (6.9) 68.2 • Interest income forgone due to reduction in cash Foreign Exchange Gain (Loss) - - - - - Other Gain (Loss) 78.5 (91.2) - (91.2) (12.8) Royalty Income of ChipMOS Taiwan (32.5) - (32.5) • Income received from Bermuda pursuant to sale of technology patent right dated 4/7/2014 will be cancelled Royalty Income of ChipMOS Taiwan (21.2) - (21.2) • Income received from Bermuda pursuant to sale of 50% technology patent right dated 4/12/2007 will be cancelled Patent Co-Development Contract (37.5) - (37.5) • Cost reimbursement received from Bermuda pursuant to patent co-development contract dated 1/1/2007 will be cancelled Interest Expenses (197.6) - - - (197.6) Pre-Tax Income 1,880.1 (44.5) (72.4) (116.9) 1,763.2 Income Taxes Expense 476.8 (11.3) (17.7) (29.0) 447.8 Consolidated Net Income 1,403.2 (33.2) (54.7) (87.9) 1,315.3 Attributable to Non-Controlling Interests - - - - - Net Income Available to Common $1,403.2 ($33.2) ($54.7) ($87.9) $1,315.3 Weighted Average Fully Diluted Shares Outstanding 896.304 (34.670) 861.634 Normalized Earnings per Share $1.566 $1.527 ($0.039) (2.5%)Source: Tahiti management Note:1. SG&A excludes one time merger expensesProject Island 19

Disclaimer ConfidentialThis document and any other materials accompanying this document (collectively, the “Materials”) are provided for general informational purposes. By accepting any Materials, the recipient thereof acknowledges and agrees to the matters set forth below in this notice.Wells Fargo Securities makes no representation or warranty (express or implied) regarding the adequacy, accuracy or completeness of any information in the Materials. Information in the Materials is preliminary and is not intended to be complete, and such information is qualified in its entirety. Any opinions or estimates contained in the Materials represent the judgment of Wells Fargo Securities at this time, and are subject to change without notice. Interested parties are advised to contact Wells Fargo Securities for more information. The Materials are not an offer to sell, or a solicitation of an offer to buy, the securities or instruments named or described herein. The Materials are not intended to provide, and must not be relied on for accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. No person providing any Materials is acting as fiduciary or advisor with respect to the Materials. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the Materials.Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.Notwithstanding anything to the contrary contained in the Materials, all persons may disclose to any and all persons, without limitations of any kind, the U.S. federal, state or local tax treatment or tax structure of any transaction, any fact that may be relevant to understanding the U.S. federal, state or local tax treatment or tax structure of any transaction, and all materials of any kind (including opinions or other tax analyses) relating to such U.S. federal, state or local tax treatment or tax structure, other than the name of the parties or any other person named herein, or information that would permit identification of the parties or such other persons, and any pricing terms or nonpublic business or financial information that is unrelated to the U.S. federal, state or local tax treatment or tax structure of the transaction to the taxpayer and is not relevant to understanding the U.S. federal, state or local tax treatment or tax structure of the transaction to the taxpayer.IRS Circular 230 Disclosure:To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in the Materials is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein. © 2015 Wells Fargo. All Rights Reserved.Project Island 20