UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-10123

The North Country Funds

(Exact name of Registrant as specified in charter)

250 Glen Street, Glens Falls, NY | | 12801 |

| (Address of principal executive offices) | | (Zip code) |

James Colantino

c/o Ultimus Fund Solutions, LLC., 4221 North 203rd Street, Suite 100 Elkhorn, Nebraska 68022-3474

(Name and address of agent for service)

| Registrant’s telephone number, including area code: | 631-470-2600 | |

| Date of fiscal year end: | 11/30 | |

| | | |

| Date of reporting period: | 11/30/24 | |

Item 1. Reports to Stockholders.

(a)

North Country Large Cap Equity Fund

Annual Shareholder Report - November 30, 2024

This annual shareholder report contains important information about North Country Large Cap Equity Fund for the period of December 1, 2023 to November 30, 2024. You can find additional information about the Fund at www.northcountryfunds.com. You can also request this information by contacting us at (888) 350-2990. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund’s costs for the last year?

(based on a hypothetical $10,000 investment)

| Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

| North Country Large Cap Equity Fund | $127 | 1.07% |

|---|

How did the Fund perform during the reporting period?

The Equity Fund’s outperformance against its benchmark index over the one-year time period can primarily be attributed to a combination of active management of mega cap exposure as well as strong stock selection across the rest of the portfolio. The “Magnificent 7” mega cap tech stocks – Apple, Amazon, Alphabet, Nvidia, Meta Platforms, Microsoft and Tesla – remain an outsized factor in today’s market environment and account for over 33% of the S&P 500.

The slight overweight to the Magnificent 7, combined with exposure to good businesses outside of the group provided positive contribution as we continued to see more broad based performance participation in the second half of the year. As positions in the Magnificent 7 grew, we tactically trimmed many of the positions to manage position sizing and to fund opportunities in more attractively priced areas of the S&P 500.

Growth stocks’ year-to-date and one-year performance edge on value stocks remains substantial. Throughout the period, investors navigated earnings seasons, which for companies within the Equity Fund was largely in line with its share of positives, but also some disappointments. In general, companies that beat expectations and issued strong guidance were met with a sigh of relief, which was a stark contrast to the pullback firms encountered when coming up short – especially in terms of outlooks.

Many of the select names across the portfolio generated strong relative returns during the year, as these companies with unique products and services have been widely viewed as beneficiaries of the new global economic environment. Monetary easing should act to stabilize equities as economic growth slows and the late-cycle expansion seeks its next catalyst. Whether growth reaccelerates or recession risk increases, the focus on quality factors has benefited the relative performance of the portfolio in times of stress, and the Fund’s cyclical exposure should be beneficial if the former scenario occurs.

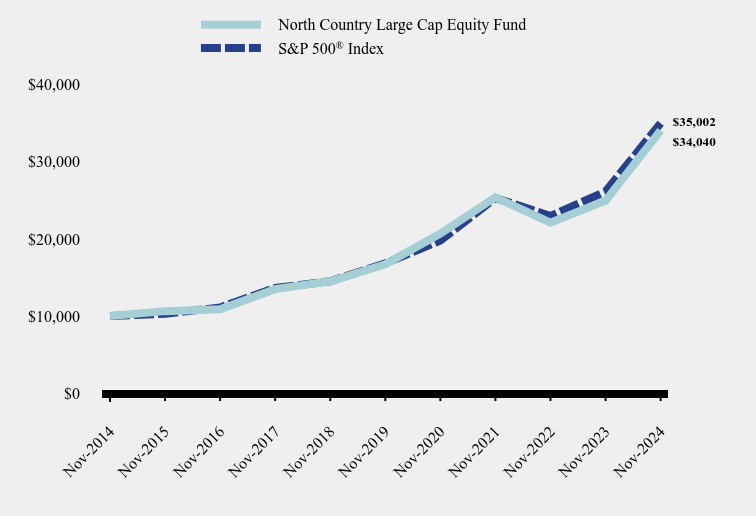

How has the Fund performed over the last ten years?

Total Return Based on $10,000 Investment

| North Country Large Cap Equity Fund | S&P 500® Index |

|---|

| Nov-2014 | $10,000 | $10,000 |

|---|

| Nov-2015 | $10,624 | $10,275 |

|---|

| Nov-2016 | $10,871 | $11,103 |

|---|

| Nov-2017 | $13,477 | $13,642 |

|---|

| Nov-2018 | $14,490 | $14,498 |

|---|

| Nov-2019 | $16,700 | $16,834 |

|---|

| Nov-2020 | $20,691 | $19,773 |

|---|

| Nov-2021 | $25,394 | $25,294 |

|---|

| Nov-2022 | $22,088 | $22,964 |

|---|

| Nov-2023 | $24,949 | $26,142 |

|---|

| Nov-2024 | $34,040 | $35,002 |

|---|

Average Annual Total Returns

| 1 Year | 5 Years | 10 Years |

|---|

| North Country Large Cap Equity Fund | 36.44% | 15.31% | 13.03% |

|---|

S&P 500® Index | 33.89% | 15.77% | 13.35% |

|---|

The Fund's past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

- Net Assets$129,102,366

- Number of Portfolio Holdings63

- Advisory Fee (net of waivers)$870,048

- Portfolio Turnover3%

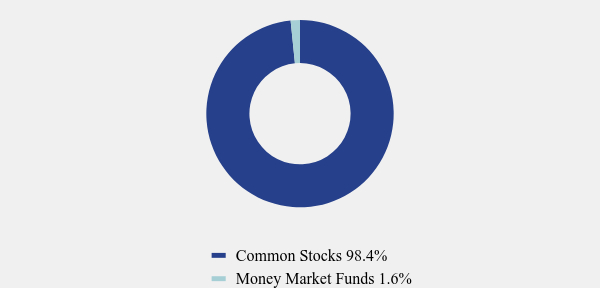

Asset Weighting (% of total investments)

| Value | Value |

|---|

| Common Stocks | 98.4% |

| Money Market Funds | 1.6% |

What did the Fund invest in?

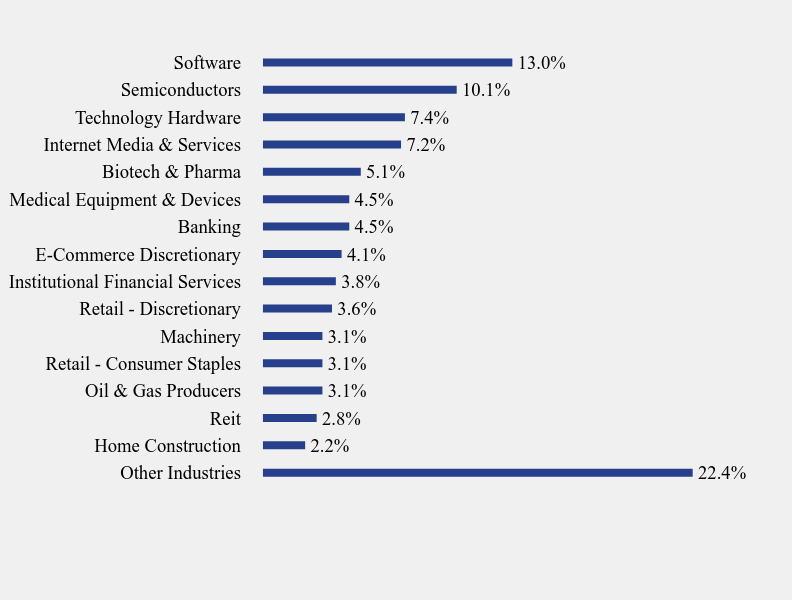

Industry Weighting (% of net assets)

| Value | Value |

|---|

| Other Industries | 22.4% |

| Home Construction | 2.2% |

| Reit | 2.8% |

| Oil & Gas Producers | 3.1% |

| Retail - Consumer Staples | 3.1% |

| Machinery | 3.1% |

| Retail - Discretionary | 3.6% |

| Institutional Financial Services | 3.8% |

| E-Commerce Discretionary | 4.1% |

| Banking | 4.5% |

| Medical Equipment & Devices | 4.5% |

| Biotech & Pharma | 5.1% |

| Internet Media & Services | 7.2% |

| Technology Hardware | 7.4% |

| Semiconductors | 10.1% |

| Software | 13.0% |

Top 10 Holdings (% of net assets)

| Holding Name | % of Net Assets |

| NVIDIA Corporation | 8.3% |

| Apple, Inc. | 7.4% |

| Microsoft Corporation | 6.7% |

| Amazon.com, Inc. | 4.1% |

| Alphabet, Inc., Class A | 3.6% |

| Home Depot, Inc. (The) | 2.6% |

| Salesforce, Inc. | 2.5% |

| Meta Platforms, Inc., Class A | 2.5% |

| JPMorgan Chase & Company | 2.4% |

| Eli Lilly & Company | 2.1% |

This is a summary of certain planned changes to the Fund that were approved by the Board at a meeting on January 2, 2025, subject to shareholder approval. For more complete information, you may review the Fund's current prospectus dated March 31, 2024, as supplemented, and the Fund's next prospectus, which we expect to be available March 31, 2025, at www.northcountryfunds.com or upon request at (888) 350-2990.

At a meeting held on January 2, 2025, the Trust’s Board of Trustees (the “Board”) unanimously approved a new investment advisory agreement (the “New Investment Advisory Agreement”) for the Fund with Advisors Preferred, LLC (“Advisors Preferred”) that will, subject to shareholder approval, replace the Fund’s current investment advisory agreement with North Country Investment Advisers, Inc. In connection with the proposed transition of investment advisory services to Advisors Preferred, the Board also approved the nomination of five new trustees for the Trust to be elected by shareholders to replace the current Trustees: Charles R. Ranson, Felix Rivera, David M. Feldman, Brian S. Humphrey, and Catherine Ayers-Rigsby (the “New Trustees”). At a special meeting of shareholders of the Fund expected to occur on or about February 26, 2025, shareholders of record as of January 7, 2025 will receive a proxy statement authorized by the Board and be asked to consider and approve both the New Investment Advisory Agreement and New Trustees.

North Country Large Cap Equity Fund (NCEGX)

Annual Shareholder Report - November 30, 2024

Where can I find additional information about the Fund?

Additional information is available on the Fund's website (www.northcountryfunds.com), including its:

Prospectus

Financial information

Holdings

Proxy voting information

Item 2. Code of Ethics.

| (a) | The registrant has, as of the end of the period covered by this report, adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, and principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party. |

| (c) | During the period covered by this report, there were no amendments to any provision of the code of ethics. |

| (d) | During the period covered by this report, there were no waivers or implicit waivers of a provision of the code of ethics. |

Item 3. Audit Committee Financial Expert.

| (a)(1) | The Registrant’s Board of Trustees has determined that James E. Amell is an audit committee financial expert, as defined in Item 3 of Form N-CSR. Mr. Amell is independent for purposes of this Item. |

Item 4. Principal Accountant Fees and Services.

| (a) | Audit Fees. The aggregate fees billed for each of the last two fiscal years for professional services rendered by the registrant’s principal accountant for the audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years are as follows: |

| (b) | Audit-Related Fees. There were no fees billed in each of the last two fiscal years for assurances and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under paragraph (a) of this Item. |

| (c) | Tax Fees. The aggregate fees billed in each of the last two fiscal years for professional services rendered by the principal accountant for tax compliance are as follows: |

Preparation of Federal & State income tax returns, assistance with calculation of required income, capital gain and excise distributions and preparation of Federal excise tax returns.

| (d) | All Other Fees. The aggregate fees billed in each of the last two fiscal years for products and services provided by the registrant’s principal accountant, other than the services reported in paragraphs (a) through (c) of this item were $0 and $0 for the fiscal years ended November 30, 2024 and 2023 respectively. |

| (e)(1) | The audit committee does not have pre-approval policies and procedures. Instead, the audit committee or audit committee chairman approves on a case-by-case basis each audit or non-audit service before the principal accountant is engaged by the registrant. |

| (e)(2) | There were no services described in each of paragraphs (b) through (d) of this Item that were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X. |

| (f) | Not applicable. |

| | |

| (g) | All non-audit fees billed by the registrant’s principal accountant for services rendered to the registrant for the fiscal years ended November 30, 2024 and 2023 respectively are disclosed in (b)-(d) above. There were no audit or non-audit services performed by the registrant’s principal accountant for the registrant’s adviser. |

| | |

| (h) | Not applicable. |

| | |

| (i) | Not applicable. |

| | |

| (j) | Not applicable. |

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

The Registrant’s schedule of investments in unaffiliated issuers is included in the Financial Statements under Item 7 of this form.

Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

(a)

| | The North Country Funds |

| | |

| | Large Cap Equity Fund |

| | |

| |  |

| | |

| | |

| | |

| | |

| | |

| | Annual Financial Statements and Additional Information |

| | November 30, 2024 |

| | |

| Investment Adviser | |

| North Country Investment Advisers, Inc. | |

| 250 Glen Street | |

| Glens Falls, NY 12801 | |

| | |

Administrator and Fund Accountant Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246 Investor Information: (888) 350-2990 | This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing herein contained is to be considered an offer of sale or solicitation of an offer to buy shares of The North Country Funds. Such offering is made only by prospectus, which includes details as to offering price and other material information. Investors should consider the Fund’s investment objectives, risks, charges and expenses carefully before investing. The prospectus contains this and other important information about the Fund. Please read the prospectus carefully before investing. |

NORTH COUNTRY LARGE CAP EQUITY FUND

SCHEDULE OF INVESTMENTS

November 30, 2024

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 98.4% | | | | |

| | | | | ASSET MANAGEMENT - 1.7% | | | | |

| | 2,200 | | | Blackrock, Inc. | | $ | 2,250,160 | |

| | | | | | | | | |

| | | | | AUTOMOTIVE - 1.1% | | | | |

| | 4,200 | | | Tesla, Inc.(a) | | | 1,449,672 | |

| | | | | | | | | |

| | | | | BANKING - 4.5% | | | | |

| | 55,500 | | | Bank of America Corporation | | | 2,636,805 | |

| | 12,500 | | | JPMorgan Chase & Company | | | 3,121,500 | |

| | | | | | | | 5,758,305 | |

| | | | | BEVERAGES - 0.9% | | | | |

| | 7,000 | | | PepsiCo, Inc. | | | 1,144,150 | |

| | | | | | | | | |

| | | | | BIOTECH & PHARMA - 5.1% | | | | |

| | 4,700 | | | Amgen, Inc. | | | 1,329,489 | |

| | 3,400 | | | Eli Lilly & Company | | | 2,704,190 | |

| | 9,500 | | | Johnson & Johnson | | | 1,472,595 | |

| | 2,200 | | | Vertex Pharmaceuticals, Inc.(a) | | | 1,029,886 | |

| | | | | | | | 6,536,160 | |

| | | | | CHEMICALS - 1.7% | | | | |

| | 2,700 | | | Air Products and Chemicals, Inc. | | | 902,691 | |

| | 1,500 | | | Ecolab, Inc. | | | 373,155 | |

| | 2,150 | | | Sherwin-Williams Company (The) | | | 854,410 | |

| | | | | | | | 2,130,256 | |

| | | | | COMMERCIAL SUPPORT SERVICES - 1.4% | | | | |

| | 8,000 | | | Waste Management, Inc. | | | 1,825,760 | |

| | | | | | | | | |

| | | | | CONSTRUCTION MATERIALS - 0.2% | | | | |

| | 1,100 | | | Vulcan Materials Company | | | 316,943 | |

| | | | | | | | | |

| | | | | DATA CENTER REIT - 1.9% | | | | |

| | 12,300 | | | Digital Realty Trust, Inc. | | | 2,406,987 | |

The accompanying notes are an integral part of these financial statements.

NORTH COUNTRY LARGE CAP EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued)

November 30, 2024

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 98.4% (Continued) | | | | |

| | | | | DIVERSIFIED INDUSTRIALS - 1.6% | | | | |

| | 9,000 | | | Honeywell International, Inc. | | $ | 2,096,370 | |

| | | | | | | | | |

| | | | | E-COMMERCE DISCRETIONARY - 4.1% | | | | |

| | 25,300 | | | Amazon.com, Inc.(a) | | | 5,259,617 | |

| | | | | | | | | |

| | | | | ELECTRIC UTILITIES - 1.0% | | | | |

| | 5,500 | | | NextEra Energy, Inc. | | | 432,685 | |

| | 9,150 | | | Southern Company (The) | | | 815,540 | |

| | | | | | | | 1,248,225 | |

| | | | | ELECTRICAL EQUIPMENT - 1.5% | | | | |

| | 26,000 | | | Amphenol Corporation, Class A | | | 1,888,900 | |

| | | | | | | | | |

| | | | | ENTERTAINMENT CONTENT - 0.6% | | | | |

| | 6,300 | | | Walt Disney Company (The) | | | 740,061 | |

| | | | | | | | | |

| | | | | FOOD - 0.4% | | | | |

| | 2,600 | | | Hershey Company (The) | | | 457,938 | |

| | | | | | | | | |

| | | | | GAS & WATER UTILITIES - 0.3% | | | | |

| | 3,000 | | | American Water Works Company, Inc. | | | 410,820 | |

| | | | | | | | | |

| | | | | HEALTH CARE FACILITIES & SERVICES - 1.5% | | | | |

| | 3,200 | | | UnitedHealth Group, Inc. | | | 1,952,640 | |

| | | | | | | | | |

| | | | | HOME CONSTRUCTION - 2.2% | | | | |

| | 3,300 | | | Lennar Corporation, Class A | | | 575,487 | |

| | 27,500 | | | Masco Corporation | | | 2,215,400 | |

| | | | | | | | 2,790,887 | |

| | | | | HOUSEHOLD PRODUCTS - 1.7% | | | | |

| | 12,125 | | | Procter & Gamble Company (The) | | | 2,173,528 | |

The accompanying notes are an integral part of these financial statements.

NORTH COUNTRY LARGE CAP EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued)

November 30, 2024

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 98.4% (Continued) | | | | |

| | | | | INFRASTRUCTURE REIT - 0.4% | | | | |

| | 2,350 | | | American Tower Corporation, Class A | | $ | 491,150 | |

| | | | | | | | | |

| | | | | INSTITUTIONAL FINANCIAL SERVICES - 3.8% | | | | |

| | 2,600 | | | Goldman Sachs Group, Inc. (The) | | | 1,582,282 | |

| | 11,350 | | | Intercontinental Exchange, Inc. | | | 1,826,896 | |

| | 11,300 | | | Morgan Stanley | | | 1,487,193 | |

| | | | | | | | 4,896,371 | |

| | | | | INSURANCE - 1.9% | | | | |

| | 5,100 | | | Berkshire Hathaway, Inc., Class B(a) | | | 2,463,402 | |

| | | | | | | | | |

| | | | | INTERNET MEDIA & SERVICES - 7.2% | | | | |

| | 27,800 | | | Alphabet, Inc., Class A | | | 4,696,810 | |

| | 5,500 | | | Meta Platforms, Inc., Class A | | | 3,158,760 | |

| | 1,700 | | | Netflix, Inc.(a) | | | 1,507,577 | |

| | | | | | | | 9,363,147 | |

| | | | | LEISURE FACILITIES & SERVICES - 0.6% | | | | |

| | 2,600 | | | McDonald’s Corporation | | | 769,626 | |

| | | | | | | | | |

| | | | | MACHINERY - 3.1% | | | | |

| | 6,300 | | | Caterpillar, Inc. | | | 2,558,493 | |

| | 14,300 | | | Ingersoll Rand, Inc. | | | 1,489,631 | |

| | | | | | | | 4,048,124 | |

| | | | | MEDICAL EQUIPMENT & DEVICES - 4.5% | | | | |

| | 13,000 | | | Abbott Laboratories | | | 1,544,010 | |

| | 3,800 | | | Danaher Corporation | | | 910,822 | |

| | 4,300 | | | Stryker Corporation | | | 1,686,245 | |

| | 3,100 | | | Thermo Fisher Scientific, Inc. | | | 1,641,853 | |

| | | | | | | | 5,782,930 | |

| | | | | OIL & GAS PRODUCERS - 3.1% | | | | |

| | 6,600 | | | Chevron Corporation | | | 1,068,738 | |

| | 8,200 | | | Exxon Mobil Corporation | | | 967,272 | |

| | 34,400 | | | Williams Companies, Inc. (The) | | | 2,013,088 | |

| | | | | | | | 4,049,098 | |

The accompanying notes are an integral part of these financial statements.

NORTH COUNTRY LARGE CAP EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued)

November 30, 2024

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 98.4% (Continued) | | | | |

| | | | | RETAIL - CONSUMER STAPLES - 3.1% | | | | |

| | 1,400 | | | Costco Wholesale Corporation | | $ | 1,360,632 | |

| | 28,200 | | | Walmart, Inc. | | | 2,608,500 | |

| | | | | | | | 3,969,132 | |

| | | | | RETAIL - DISCRETIONARY - 3.6% | | | | |

| | 7,800 | | | Home Depot, Inc. (The) | | | 3,347,214 | |

| | 10,600 | | | TJX Companies, Inc. (The) | | | 1,332,314 | |

| | | | | | | | 4,679,528 | |

| | | | | SELF-STORAGE REIT - 0.5% | | | | |

| | 1,900 | | | Public Storage | | | 661,295 | |

| | | | | | | | | |

| | | | | SEMICONDUCTORS – 10.1% | | | | |

| | 20,000 | | | Marvell Technology, Inc. | | | 1,853,800 | |

| | 77,000 | | | NVIDIA Corporation | | | 10,645,250 | |

| | 5,000 | | | Teradyne, Inc. | | | 550,000 | |

| | | | | | | | 13,049,050 | |

| | | | | SOFTWARE - 13.0% | | | | |

| | 4,400 | | | Adobe, Inc.(a) | | | 2,270,092 | |

| | 20,350 | | | Microsoft Corporation | | | 8,617,410 | |

| | 11,000 | | | Oracle Corporation | | | 2,033,240 | |

| | 1,600 | | | Palo Alto Networks, Inc.(a) | | | 620,512 | |

| | 9,900 | | | Salesforce, Inc. | | | 3,266,901 | |

| | | | | | | | 16,808,155 | |

| | | | | SPECIALTY FINANCE - 1.0% | | | | |

| | 6,800 | | | Capital One Financial Corporation | | | 1,305,668 | |

| | | | | | | | | |

| | | | | TECHNOLOGY HARDWARE - 7.4% | | | | |

| | 40,200 | | | Apple, Inc. | | | 9,540,666 | |

| | | | | | | | | |

| | | | | TECHNOLOGY SERVICES - 1.4% | | | | |

| | 5,700 | | | Visa, Inc., Class A | | | 1,795,956 | |

| | | | | | | | | |

| | | | | WHOLESALE - CONSUMER STAPLES - 0.3% | | | | |

| | 7,500 | | | Sysco Corporation | | | 578,325 | |

| | | | | | | | | |

| | | | | TOTAL COMMON STOCKS (35,464,362) | | | 127,089,002 | |

The accompanying notes are an integral part of these financial statements.

NORTH COUNTRY LARGE CAP EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued)

November 30, 2024

| Shares | | | | | Fair Value | |

| | | | | SHORT-TERM INVESTMENTS — 1.6% | | | | |

| | | | | MONEY MARKET FUNDS - 1.6% | | | | |

| | 2,014,959 | | | BlackRock Liquidity Funds Treasury Trust Fund Portfolio, Institutional Class, 4.54%(b) (Cost $2,014,959) | | $ | 2,014,959 | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 100.0% (Cost $37,479,321) | | $ | 129,103,961 | |

| | | | | LIABILITIES IN EXCESS OF OTHER ASSETS - 0.0% | | | (1,595 | ) |

| | | | | NET ASSETS - 100.0% | | $ | 129,102,366 | |

ETF - Exchange-Traded Fund

REIT - Real Estate Investment Trust

| (a) | Non-income producing security. |

| (b) | Rate disclosed is the seven day effective yield as of November 30, 2024. |

The accompanying notes are an integral part of these financial statements.

STATEMENT OF ASSETS AND LIABILITIES

November 30, 2024

| | | Large Cap

Equity Fund | |

| ASSETS: | | | | |

| Investments in securities, at fair value (Cost $37,479,321) | | $ | 129,103,961 | |

| Dividends and interest receivable | | | 124,357 | |

| Receivable for fund shares sold | | | 150 | |

| Receivable for legal fees (See Note 3) | | | 53,223 | |

| Prepaid expenses and other assets | | | 8,596 | |

| Total Assets | | | 129,290,287 | |

| | | | | |

| LIABILITIES: | | | | |

| Accrued advisory fees | | | 72,831 | |

| Accrued audit fees | | | 17,981 | |

| Payable for fund shares redeemed | | | 16,813 | |

| Payable to related parties | | | 15,744 | |

| Accrued expenses and other liabilities | | | 64,552 | |

| Total Liabilities | | | 187,921 | |

| Net Assets | | $ | 129,102,366 | |

| | | | | |

| NET ASSETS CONSIST OF: | | | | |

| Paid in capital | | $ | 23,446,458 | |

| Accumulated earnings | | | 105,655,908 | |

| Net Assets | | $ | 129,102,366 | |

| | | | | |

| Shares outstanding (unlimited number of shares authorized; no par value) | | | 5,332,156 | |

| | | | | |

| Net asset value, offering and redemption price per share ($129,102,366/5,332,156) | | $ | 24.21 | |

The accompanying notes are an integral part of these financial statements

STATEMENT OF OPERATIONS

For the Year Ended November 30, 2024

| | | Large Cap

Equity Fund | |

| INVESTMENT INCOME: | | | | |

| Dividends | | $ | 1,409,304 | |

| Interest | | | 132,341 | |

| Total investment income | | | 1,541,645 | |

| | | | | |

| EXPENSES: | | | | |

| Investment advisory fees | | | 910,394 | |

| Administration and fund accounting fees | | | 185,686 | |

| Legal fees | | | 142,062 | |

| Transfer agency fees | | | 40,246 | |

| Audit fees | | | 20,998 | |

| Registration and filing fees | | | 17,001 | |

| Chief Compliance Officer fees | | | 16,455 | |

| Printing expense | | | 15,999 | |

| Trustees’ fees | | | 15,543 | |

| Custody fees | | | 11,799 | |

| Insurance expense | | | 11,502 | |

| Shareholder Service fees | | | 10 | |

| Miscellaneous expenses | | | 4,244 | |

| Total expenses | | | 1,391,939 | |

| | | | | |

| Less: Advisory fee waiver | | | (40,346 | ) |

| Less: Voluntary Reimbursement - Legal Fees (See Note 3) | | | (53,223 | ) |

| Net expenses | | | 1,298,370 | |

| | | | | |

| Net investment income | | | 243,275 | |

| | | | | |

| NET REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | | | | |

| Net realized gain from investment transactions | | | 14,963,733 | |

| Net change in unrealized appreciation of investments | | | 22,773,863 | |

| Net realized and unrealized gain on investments | | | 37,737,596 | |

| | | | | |

| Net increase in net assets resulting from operations | | $ | 37,980,871 | |

The accompanying notes are an integral part of these financial statements

LARGE CAP EQUITY FUND

STATEMENTS OF CHANGES IN NET ASSETS

| | | For the

Year Ended

November 30,

2024 | | | For the

Year Ended

November 30,

2023 | |

| FROM OPERATIONS: | | | | | | | | |

| Net investment income | | $ | 243,275 | | | $ | 691,849 | |

| Net realized gain from investment transactions | | | 14,963,733 | | | | 18,747,047 | |

| Net change in unrealized appreciation (deprecation) | | | 22,773,863 | | | | (4,498,320 | ) |

| Net increase in net assets resulting from operations | | | 37,980,871 | | | | 14,940,576 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | |

| Total distributions to shareholders | | | (16,891,475 | ) | | | (14,322,130 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS (Note 4) | | | (8,724,616 | ) | | | (15,452,119 | ) |

| | | | | | | | | |

| NET ASSETS: | | | | | | | | |

| Net increase (decrease) in net assets | | | 12,364,780 | | | | (14,833,673 | ) |

| Beginning of year | | | 116,737,586 | | | | 131,571,259 | |

| | | | | | | | | |

| End of year | | $ | 129,102,366 | | | $ | 116,737,586 | |

The accompanying notes are an integral part of these financial statements

LARGE CAP EQUITY FUND

FINANCIAL HIGHLIGHTS

(For a fund share outstanding throughout each year)

| | | For the Year Ended November 30, | |

| | | 2024 | | | 2023 | | | 2022 | | | 2021 | | | 2020 | |

| Net asset value, beginning of year | | $ | 20.77 | | | $ | 20.73 | | | $ | 25.86 | | | $ | 23.48 | | | $ | 20.32 | |

| | | | | | | | | | | | | | | | | | | | | |

| INCOME (LOSS) FROM INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (1) | | | 0.04 | | | | 0.11 | | | | 0.11 | | | | 0.07 | | | | 0.08 | |

| Net realized and unrealized gain (loss) on investments | | | 6.41 | | | | 2.19 | | | | (3.16 | ) | | | 4.74 | | | | 4.44 | |

| Total from investment operations | | | 6.45 | | | | 2.30 | | | | (3.05 | ) | | | 4.81 | | | | 4.52 | |

| | | | | | | | | | | | | | | | | | | | | |

| LESS DISTRIBUTIONS: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.12 | ) | | | (0.12 | ) | | | (0.07 | ) | | | (0.10 | ) | | | (0.08 | ) |

| Distribution from net realized gains | | | (2.89 | ) | | | (2.14 | ) | | | (2.01 | ) | | | (2.33 | ) | | | (1.28 | ) |

| Total distributions | | | (3.01 | ) | | | (2.26 | ) | | | (2.08 | ) | | | (2.43 | ) | | | (1.36 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net asset value, end of year | | $ | 24.21 | | | $ | 20.77 | | | $ | 20.73 | | | $ | 25.86 | | | $ | 23.48 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total return (2) | | | 36.44 | % | | | 12.95 | % | | | (13.02 | )% | | | 22.73 | % | | | 23.90 | % |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in 000’s) | | $ | 129,102 | | | $ | 116,738 | | | $ | 131,571 | | | $ | 170,626 | | | $ | 151,343 | |

| Ratios to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Expenses, before waiver | | | 1.10 | %* | | | 1.08 | % | | | 1.02 | % | | | 0.99 | % | | | 1.02 | % |

| Expenses, after waiver | | | 1.07 | %* | | | 1.08 | % | | | 1.02 | % | | | 0.99 | % | | | 1.02 | % |

| Net investment income | | | 0.20 | % | | | 0.56 | % | | | 0.51 | % | | | 0.31 | % | | | 0.40 | % |

| Portfolio turnover rate | | | 3 | % | | | 8 | % | | | 7 | % | | | 7 | % | | | 5 | % |

| (1) | Net investment income per share is based on average shares outstanding during the year. |

| (2) | Total returns are historical and assume changes in share price and reinvestment of dividends and capital gain distributions, if any. Total return does not reflect the deductions of taxes that a shareholder would pay on distributions or on the redemption of shares. |

| * | Includes voluntary reimbursement from the advisor for legal fees. Had the advisor not reimbursed legal expenses ratios wold have been as follows: |

| Expenses, before waiver | | | 1.14 | % | | | | | | | | | | | | | | | | |

| Expenses, after waiver | | | 1.11 | % | | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these financial statements

NOTES TO FINANCIAL STATEMENTS

November 30, 2024

NOTE 1. ORGANIZATION

The North Country Funds (the “Trust”) was organized as a Massachusetts business trust on June 1, 2000, and registered under the Investment Company Act of 1940 (the “1940 Act”) as an open-end, diversified, management investment company on September 11, 2000. The Trust currently offers one series: the North Country Large Cap Equity Fund (the “Fund”). The Fund’s principal investment objective is to provide investors with long-term capital appreciation. The Fund commenced operations on March 1, 2001.

The Fund was initially organized on March 26, 1984 under New York law as a Collective Investment Trust sponsored by Glens Falls National Bank & Trust Company. Prior to its conversion to a regulated investment company (mutual fund), investor participation was limited to qualified employee benefit plans.

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of the significant accounting policies followed by the Trust in the preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in conformity with these generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the year. Actual results could differ from these estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 Financial Services - Investment Companies.

Security Valuation – Securities which are traded on a national securities exchange are valued at the last quoted sale price. NASDAQ traded securities are valued using the NASDAQ official closing price (“NOCP”). Investments for which no sales are reported are valued at the mean between the current bid and ask prices on the day of valuation. To the extent these securities are actively traded and valuation adjustments are not applied, they are categorized in level 1 of the fair value hierarchy described below. When an equity security is valued by the independent pricing service using factors other than market quotations or the market is considered inactive, they will be categorized in level 2.

Any securities or other assets for which market quotations are not readily available, or securities for which the last bid price does not accurately reflect the current value, are valued at fair value pursuant to the Fund’s fair value pricing policies and procedures, as approved by the Board (the “Valuation Policy”). The Board has designated North Country Investment Advisers, Inc., the Fund’s investment adviser (the “Adviser”), as the “Valuation Designee” pursuant to Rule 2a-5 under the 1940 Act to make fair value determinations for all of the Fund’s investments for which market quotations are not readily available (or are deemed unreliable). The Board will oversee the Adviser’s fair value determinations and the Adviser’s performance as Valuation Designee. Pursuant to the Valuation Policy, the Valuation Designee will take into account all relevant factors and circumstances in determining the fair value of a security, which may include: (i) the nature and pricing history (if any) of the security; (ii) whether any dealer quotations for the security are available; (iii) possible valuation methodologies that could be used to determine the fair value of the security; (iv) the recommendation of the portfolio manager of the Fund with respect to the valuation of the security; (v) whether the same or similar securities are held by other funds managed

NOTES TO FINANCIAL STATEMENTS (Continued)

November 30, 2024

by the Adviser or other funds and the method used to price the security in those funds; (vi) the extent to which the fair value to be determined for the security will result from the availability and use of data, reports or formulae produced by third parties independent of the Adviser; (vii) the liquidity or illiquidity of the market for the security; (viii) the size of the Fund’s holdings; (ix) the existence of any extraordinary event relating to the security; (x) changes in the market environment; and (xi) any other matters considered relevant by the Valuation Designee. In the absence of readily available market quotations, or other observable inputs, securities valued at fair value pursuant to the Procedures would be categorized as level 3.

Money market funds are valued at their net asset value of $1.00 per share and are categorized as level 1. Securities with maturities of 60 days or less may be valued at amortized cost, which approximates fair value and would be categorized as level 2. The ability of issuers of debt securities held by the Fund to meet its obligations may be affected by economic or political developments in a specific country or region.

The Fund utilizes various methods to measure the fair value of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, including the Valuation Designee’s assumptions used in determining the fair value of priced instruments.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

NOTES TO FINANCIAL STATEMENTS (Continued)

November 30, 2024

The following is a summary of inputs used as of November 30, 2024, in valuing the Fund’s assets carried at fair value.

North Country Large Cap Equity Fund:

| | Assets | | Level 1 | | | Level 2 | | | Level 3* | | | Total | |

| | Common Stocks ** | | $ | 127,089,002 | | | $ | - | | | $ | - | | | $ | 127,089,002 | |

| | Money Market Fund | | | 2,014,959 | | | | - | | | | - | | | | 2,014,959 | |

| | Total | | $ | 129,103,961 | | | $ | - | | | $ | - | | | $ | 129,103,961 | |

| * | The Fund did not hold any Level 3 investments during the period. |

| ** | See Schedule of Investments for industry classifications. |

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund intends to qualify each year as regulated investment companies (“RICs”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

Management has analyzed the Fund’s tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years November 30, 2021, to November 30, 2023, or expected to be taken in the Fund’s November 30, 2024, year-end tax returns.

The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statements of Operations. During the year, the Fund did not incur any interest or penalties.

During the fiscal year ended November 30, 2024, the Fund utilized tax equalization which is the use of earnings and profits distributions to shareholders on redemption of shares as part of the dividends paid deduction for income tax purposes. Permanent book and tax differences, primarily attributable to the book/tax treatment of use of tax equalization credits, resulted in reclassifications for the Fund for the fiscal year ended November 30, 2024, as follows:

Paid In

Capital | | | Distributable

Earnings | |

| $ | 1,218,214 | | | $ | (1,218,214 | ) |

Dividends and Distributions – The Fund will pay dividends from net investment income, if any, on an annual basis. The Fund will declare and pay distributions from net realized capital gains, if any, annually. Income and capital gain distributions to shareholders are recorded on the ex-dividend date and are determined in accordance with income tax regulations, which may differ from generally accepted accounting principles.

NOTES TO FINANCIAL STATEMENTS (Continued)

November 30, 2024

Security Transactions – Securities transactions are recorded no later than the first business day after the trade date, except for reporting purposes when trade date is used. Realized gains and losses on sales of securities are calculated on the identified cost basis. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Discounts and premiums on securities purchased are amortized over the life of the respective securities using the effective yield method. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Indemnification – The Trust indemnifies its officers and trustees for certain liabilities that may arise from the performance of their duties to the Trust. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be remote.

Cash and cash equivalents – Cash and cash equivalents are held with a financial institution. The assets of the Fund may be placed in deposit accounts at U.S. banks and such deposits generally exceed Federal Deposit Insurance Corporation (“FDIC”) insurance limits. The FDIC insures deposit accounts up to $250,000 for each accountholder. The counterparty is generally a single bank rather than a group of financial institutions; thus there may be a greater counterparty credit risk. The Fund places deposits only with those counterparties which are believed to be creditworthy and there has been no history of loss.

NOTE 3. INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES

The Trust has entered into an investment advisory agreement (the “Advisory Agreement”) with North Country Investment Advisers, Inc. (the “Adviser”). Pursuant to the Advisory Agreement, the Adviser is responsible for formulating the Trust’s investment programs, making day-to-day investment decisions and engaging in portfolio transactions, subject to the authority of the Board of Trustees. Under the terms of the agreement, the Fund pays a fee, calculated daily and paid monthly, at an annual rate of 0.75% of the average daily net assets of the Fund. For the year ended November 30, 2024, the Adviser received advisory fees of $910,394.

Effective April 1, 2024 the Adviser has agreed to waive, through March 31, 2025, a portion of its advisory fees, which will reduce the 0.75% contractual fee rate by 0.05% to 0.70%. This waiver may not be terminated prior to that date without the approval of the Board of Trustees of The North Country Funds. For the year ended November 30, 2024 the Adviser waived $40,346 in fees.

The Advisor has agreed to voluntarily reimburse legal fees associated with a transaction involving the Advisor, the Fund and Advisors Preferred LLC. (the “Purchaser”). The Advisor will seek reimbursement of these legal fees from the Purchaser at a later date. For the year ended November 30, 2024 the amount of legal fees to be reimbursed by the Advisor amount to $53,223 and are not recoupable.

The Trust has entered into an Underwriting Agreement with Northern Lights Distributors, LLC (“the Distributor”) to serve as the principal underwriter for the Fund and distributor for the Fund’s shares.

NOTES TO FINANCIAL STATEMENTS (Continued)

November 30, 2024

In addition, certain affiliates of the Distributor provide services to the Fund as follows:

Ultimus Fund Solutions, LLC (“UFS”) – UFS, an affiliate of the Distributor, provides administration, fund accounting, and transfer agent services to the Trust. Pursuant to separate servicing agreements with UFS, the Fund pays UFS customary fees for providing administration, fund accounting, and transfer agency services to the Fund. Certain officers of the Trust are also officers of UFS, and are not paid any fees directly by the Fund for serving in such capacities.

Northern Lights Compliance Services, LLC (“NLCS”) – NLCS, an affiliate of UFS and the Distributor, provides a Chief Compliance Officer to the Trust, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Trust. Under the terms of such agreement, NLCS receives customary fees from the Fund.

BluGiant, LLC (“BluGiant”), an affiliate of UFS and the Distributor, provides EDGAR conversion and filing services as well as print management services for the Fund on an ad-hoc basis. For the provision of these services, BluGiant receives customary fees from the Fund.

Certain officers and/or trustees of the Adviser are also officers/trustees of the Trust.

NOTE 4. CAPITAL SHARE TRANSACTIONS

At November 30, 2024, there were an unlimited number of shares authorized with no par value.

Transactions in capital shares were as follows:

| | | | For the

Year Ended

November 30,

2024 | | | For the

Year Ended

November 30,

2023 | |

| | | | Shares | | | Amount | | | Shares | | | Amount | |

| | Shares sold | | | 64,296 | | | $ | 1,366,346 | | | | 223,652 | | | $ | 4,042,425 | |

| | Shares issued for reinvestment of dividends | | | 926,183 | | | | 16,328,622 | | | | 772,470 | | | | 13,688,179 | |

| | Shares redeemed | | | (1,280,096 | ) | | | (26,419,584 | ) | | | (1,721,579 | ) | | | (33,182,723 | ) |

| | Net decrease | | | (289,617 | ) | | $ | (8,724,616 | ) | | | (725,457 | ) | | $ | (15,452,119 | ) |

NOTE 5. INVESTMENTS

The cost of purchases and proceeds from the sales of securities, other than short-term investments, for the year ended November 30, 2024, amounted to $3,107,711 and $27,259,462, respectively.

NOTES TO FINANCIAL STATEMENTS (Continued)

November 30, 2024

NOTE 6. AGGREGATE UNREALIZED APPRECIATION AND DEPRECIATION – TAX BASIS

The identified cost of investments in securities owned by the Fund for federal income tax purposes, and its gross unrealized appreciation and depreciation at November 30, 2024, were as follows:

| | Tax

Cost | | | Gross

Unrealized

Appreciation | | | Gross

Unrealized

Depreciation | | | Net Unrealized

Appreciation

(Depreciation) | |

| | $ | 37,421,284 | | | $ | 91,747,338 | | | $ | (64,661 | ) | | $ | 91,682,677 | |

NOTE 7. TAX INFORMATION

The tax character of distributions paid during the fiscal year ended November 30, 2024, and fiscal year ended November 30, 2023, was as follows:

| | | | Fiscal Year Ended

November 30,

2024 | | | Fiscal Year Ended

November 30,

2023 | |

| | Ordinary Income | | $ | 730,479 | | | $ | 732,450 | |

| | Long-Term Capital Gain | | | 16,160,996 | | | | 13,589,680 | |

| | Return of Capital | | | - | | | | - | |

| | | | $ | 16,891,475 | | | $ | 14,322,130 | |

As of November 30, 2024, the components of distributable earnings/ (deficit) on a tax basis were as follows:

| | Undistributed

Ordinary

Income | | | Undistributed

Long-Term

Gains | | | Post October

Loss and Late

Year Loss | | | Capital Loss

Carry

Forwards | | | Other

Book/Tax

Differences | | | Unrealized

Appreciation/

(Depreciation) | | | Total

Distributable

Earnings/

(Accumulated Deficit) | |

| | $ | 854,490 | | | $ | 13,118,741 | | | $ | - | | | $ | - | | | $ | - | | | $ | 91,682,677 | | | $ | 105,655,908 | |

The difference between book basis and tax basis unrealized appreciation/(depreciation) from investments is primarily attributable to the adjustments for C-Corporation return of capital distributions.

NOTE 8. CONTROL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a Fund creates presumption of control of the Fund, under Section 2(a) 9 of the 1940 Act. As of November 30, 2024, Arrow Financial Corporation, an account holding shares for the benefit of others in nominee name, held approximately 83% of the voting securities of the Fund.

NOTES TO FINANCIAL STATEMENTS (Continued)

November 30, 2024

NOTE 9. SUBSEQUENT EVENTS

Subsequent events after the date of the Statement of Assets and Liabilities have been evaluated through the date the financial statements were issued. Except as noted below, management has concluded that there are no events requiring additional adjustment or disclosure in the financial statements. On December 6, 2024, the Fund paid an ordinary income dividend of $0.049 per share, a short-term capital gain dividend of $0.1185 per share and a long-term capital gain dividend of $2.4604 per share to shareholders of record on December 5, 2024. At a meeting held on January 2, 2025, the Trust’s Board of Trustees (the “Board”) unanimously approved a new investment advisory agreement (the “New Investment Advisory Agreement”) for the Fund with Advisors Preferred, LLC (“Advisors Preferred”) that will, subject to shareholder approval, replace the Fund’s current investment advisory agreement with North Country Investment Advisers, Inc. In connection with the proposed transition of investment advisory services to Advisors Preferred, the Board also approved the nomination of five new trustees for the Trust to be elected by shareholders to replace the current Trustees: Charles R. Ranson, Felix Rivera, David M. Feldman, Brian S. Humphrey, and Catherine Ayers-Rigsby (the “New Trustees”). At a special meeting of shareholders of the Fund expected to occur on or about February 26, 2025, shareholders of record as of January 7, 2025 will receive a proxy statement authorized by the Board and be asked to consider and approve both the New Investment Advisory Agreement and New Trustees.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Trustees of

The North Country Funds

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of The North Country Funds comprising North Country Large Cap Equity Fund (the “Fund”) as of November 30, 2024, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of November 30, 2024, the results of its operations for the year then ended, the changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of November 30, 2024, by correspondence with the custodian. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

Emphasis of Matter

As discussed in Note 9 to the financial statements, the Board of Trustees unanimously approved a new investment advisory agreement and the nomination of five new trustees. Our opinion is not modified with respect to this matter.

We have served as the Fund’s auditor since 2004.

COHEN & COMPANY, LTD.

Milwaukee, Wisconsin

January 24, 2025

ADDITIONAL INFORMATION (Unaudited)

Changes in and Disagreements with Accountants

There were no changes in or disagreements with accountants during the period covered by this report.

Proxy Disclosures

Not applicable.

Remuneration Paid to Directors, Officers and Others

Refer to the financial statements included herein.

Statement Regarding Basis for Approval of Investment Advisory Agreement

FACTORS CONSIDERED BY THE INDEPENDENT TRUSTEES IN APPROVING THE INVESTMENT ADVISORY AGREEMENT

At a meeting (the “Meeting”) of the Board of Trustees (the “Board” or the “Trustees”) held on July 16, 2024, a majority of the Board, including a majority of trustees who are not “interested persons” of the Trust, as that term is defined in Section 2(a)(19) of the Investment Company Act of 1940, as amended (hereafter, the “Independent Trustees”), unanimously approved the continuance of the investment advisory agreement (the “Advisory Agreement”) between North Country Investment Advisers, Inc. (“NCIA” or the “Adviser”) and the North Country Large Cap Equity Fund (the “Large Cap Fund” or “Fund”). Fund counsel discussed with the Board its fiduciary responsibility to shareholders and the importance of assessing certain specific factors in its deliberations. Prior to the Meeting, the Adviser provided the Board with a number of written materials, including information relating to: a) the terms of the Advisory Agreement and fee arrangements with the Fund; b) the Adviser’s management and investment personnel; c) the financial condition and stability of the Adviser; d) data comparing the Fund’s fees, operating expenses and performance with that of a group of mutual funds in the same category, that the Adviser determined were similar in size to the Fund (the “Peer Group”); and e) past performance of the Fund as compared to its benchmark. In addition, the Board engaged in in-person discussions with representatives of the Adviser. The Board also met outside the presence of the Adviser to consider this matter and consulted with independent counsel and the Fund’s Chief Compliance Officer.

The Board, including the Independent Trustees, unanimously approved continuance of the Advisory Agreement based upon its review of the written materials provided at the Meeting, the reports provided at each quarterly meeting of the Board, the Board’s discussions with key personnel of the Adviser, and the Board’s deliberations. In their deliberations, the Trustees did not identify any particular information that was all-important or controlling, and individual Trustees may have attributed different weights to the various factors. Below is a summary of the Board’s conclusions regarding various factors relevant to approval of continuance of the Advisory Agreement:

Nature, Extent and Quality of Services. In considering the renewal of the Advisory Agreement, the Board considered the nature, extent and quality of services that the Adviser provided to the Fund, including, without limitation, the nature and quality of the investment advisory services since the Fund’s inception, its coordination of services for the Fund by the Fund’s service providers, its compliance procedures and practices, and the Adviser’s personnel and resources. The Board reviewed the backgrounds of the personnel providing services to the Fund, including the Fund’s portfolio managers and their compensation structure. They also reviewed information provided regarding trading and brokerage practices, risk management, and compliance and regulatory matters. After reviewing the foregoing information, the Board concluded that the quality, extent, and nature of the services the Adviser provided were satisfactory.

ADDITIONAL INFORMATION (Unaudited)(Continued)

Performance of the Adviser. The Board reviewed performance information for the Fund compared to the Benchmark Index and Peer Group for the one-, two-, three-, four-, five- and ten-year periods ended May 31, 2024. The Board also reviewed information on the construction of the Fund’s Peer Group. The Board reviewed the Fund’s total returns compared to the total returns of its Peer Group and Benchmark Index (Lipper Large Cap Core Funds Index). The Board also considered the success and consistency of the Adviser’s management of the Fund in implementing the Fund’s investment objective and policies, as well as the consistency of the Adviser’s management of the Fund with the management expected from value-focused managers generally. The Board concluded that the performance of the Fund was consistent with the Fund’s investment objective and policies and was satisfactory.

Cost of Services. The Board considered the Adviser’s staffing, personnel, and methods of operating; the Adviser’s compliance policies and procedures; the financial condition of the Adviser and the level of commitment to the Fund; the asset levels of the Fund; and the overall expenses of the Fund, including certain fee waivers by the Adviser on behalf of the Fund. The Board considered the nature and scope of the services provided by the Adviser, including supervision of outside service providers. In light of the nature, quality and extent of services the Adviser provided, the Board concluded that the Fund’s advisory fee was appropriate. The Board discussed the Fund’s current fee waiver arrangement with the Adviser, and considered the Adviser’s past fee waivers with respect to the Fund. The Board compared the fees and expenses of the Fund (including the management fee) to the Peer Funds. Upon further consideration and discussion of the foregoing, the Board concluded that the fees to be paid to the Adviser by the Fund are appropriate and within the range of what would have been negotiated at arm’s length.

Profitability. The Board reviewed the profitability of NCIA with respect to the Fund. The Board considered the methodology for calculating profitability. Using such methodology, the Board noted that NCIA earned a profit from the Fund. The Board concluded that the profitability of NCIA in connection with the management of the Fund was not excessive given the nature, extent and quality of the services provided.

Economies of Scale. The Trustees noted that the Adviser represented that certain efficiencies may be realized when the level of assets under management in the Fund nears $500 million. The Trustees concluded that they would re-visit the issue of certain benefits to the Fund’s shareholders that might ensue from economies of scale following any significant growth in Fund assets or other change in circumstances.

Fallout Benefits. The Board considered that, because of its relationship with the Fund, the Adviser and its affiliates may derive ancillary benefits from Fund operations, including those derived from the allocation of Fund brokerage and the use of commission dollars to pay for research and other similar services. The Board noted that the Adviser did not anticipate any fallout benefits at this time.

Conclusion. Based on all of the information considered and the conclusions reached, the Board determined that the compensation to be paid under the Advisory Agreement is appropriate in light of the nature, quality and extent of services provided by the Adviser, and that the continuance of the Advisory Agreement be approved.

Item 8. Changes in and Disagreements with Accountants for Open-End Management Investment Companies.

Not applicable.

Item 9. Proxy Disclosures for Open-End Management Investment Companies.

Not applicable.

Item 10. Remuneration Paid to Directors, Officers, and Others of Open-End Management Investment Companies.

Included under Item 7

Item 11. Statement Regarding Basis for Approval of Investment Advisory Contract.

Included under Item 7

Item 12. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 13. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 14. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 15. Submission of Matters to a Vote of Security Holders.

None.

Item 16. Controls and Procedures

| (a) | The registrant’s Principal Executive Officer and Principal Financial Officer have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a-3(c) under the Act) are effective in design and operation and are sufficient to form the basis of the certifications required by Rule 30a-(2) under the Act, based on their evaluation of these disclosure controls and procedures as of a date within 90 days of this report on Form N-CSR. |

| (b) | There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the Act) during the period covered by this report that have materially affected, or are reasonably likely to materially affect, the registrant’s internal control over financial reporting. |

Item 17. Disclosure of Securities Lending Activities for Closed-End Management Investment Companies.

Not applicable.

Item 18. Recovery of Erroneously Awarded Compensation.

Item 19. Exhibits.

| (a)(3) | A separate certification for each principal executive officer and principal financial officer of the registrant as required by Rule 30a-2(a) under the Act (17 CFR 270.30a-2(a)): Attached hereto. |

| (b) | Certifications required by Rule 30a-2(b) under the Act (17 CFR 270.30a-2(b)): Attached hereto. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

The North Country Funds

| By | /s/ James Colantino | |

| James Colantino | |

| Principal Executive Officer | |

| Date: | 2/3/2025 | | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By | /s/ James Colantino | |

| James Colantino | |

| Principal Executive Officer | |

| Date: | 2/3/2025 | | |

| By | /s/ Rich Gleason | |

| Rich Gleason | |

| Principal Financial Officer | |

| Date: | 2/3/2025 | | |