Earnings Review Third Quarter 2008 October 30, 2008 Exhibit 99.3 |

2 Important Disclosures This presentation may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 which, by their nature, are subject to risks and uncertainties. We intend for these forward-looking statements to be covered by the safe harbor provisions of the federal securities laws relating to forward-looking statements. These include statements relating to trends in, or representing management’s beliefs about, our future transactions, strategies, operations and financial results, as well as other statements including words such as “anticipate,” “believe,” “plan,” “estimate,” “expect,” “intend,” “may,” “should” and other similar expressions. Forward-looking statements are made based upon our current expectations and beliefs concerning trends and future developments and their potential effects on the company. They are not guarantees of future performance. Actual results may differ materially from those suggested by forward-looking statements as a result of risks and uncertainties, which include, among others: (i) the effects of recent adverse market and economic developments on all aspects of our business; (ii) changes in general market and business conditions, interest rates and the debt and equity markets; (iii) the possibility that mortality rates, persistency rates or funding levels may differ significantly from our pricing expectations; (iv) the availability, pricing and terms of reinsurance coverage generally and the inability or unwillingness of our reinsurers to meet their obligations to us specifically; (v) our dependence on non-affiliated distributors for our product sales, (vi) downgrades in our debt or financial strength ratings; (vii) our dependence on third parties to maintain critical business and administrative functions; (viii) the ability of independent trustees of our mutual funds and closed-end funds, intermediary program sponsors, managed account clients and institutional asset management clients to terminate their relationships with us; (ix) our ability to attract and retain key personnel in a competitive environment; (x) the poor relative investment performance of some of our asset management strategies and the resulting outflows in our assets under management; (xi) the possibility that the goodwill or intangible assets associated with our asset management business could become impaired, requiring a charge to earnings; (xii) the strong competition we face in our business from mutual fund companies, banks, asset management firms and other insurance companies; (xiii) our reliance, as a holding company, on dividends and other payments from our subsidiaries to meet our financial obligations and pay future dividends, particularly since our insurance subsidiaries’ ability to pay dividends is subject to regulatory restrictions; (xiv) the potential need to fund deficiencies in our Closed Block; (xv) tax developments that may affect us directly, or indirectly through the cost of, the demand for or profitability of our products or services; (xvi) other legislative or regulatory developments; (xvii) legal or regulatory actions; (xviii) changes in accounting standards; (xix) the potential effects of the spin-off of our asset management subsidiary on our expense levels, liquidity and third-party relationships; and (xx) other risks and uncertainties described herein or in any of our filings with the SEC. We undertake no obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future events or otherwise. In managing our business, we analyze our performance on the basis of “operating income” which does not equate to net income as determined in accordance with GAAP. Rather, it is the measure of profit or loss used by our management to evaluate performance, allocate resources and manage our operations. We believe that operating income, and measures that are derived from or incorporate operating income, are appropriate measures that are useful to investors as well, because they identify the earnings of, and underlying profitability factors affecting, the ongoing operations of our business. Operating income is calculated by excluding realized investment gains (losses) and certain other items because we do not consider them to be related to our operating performance. The size and timing of realized investment gains (losses) are often subject to our discretion. Certain other items are also excluded from operating income if, in our opinion, they are not indicative of overall operating trends. The criteria used to identify an item that will be excluded from operating income include: whether the item is infrequent and is material to our income; or whether it results from a change in regulatory requirements, or relates to other unusual circumstances. Items excluded from operating income may vary from period to period. Because these items are excluded based on our discretion, inconsistencies in the application of our selection criteria may exist. Some of these items may be significant components of net income in accordance with GAAP. Accordingly, operating income, and other measures that are derived from or incorporate operating income, are not substitutes for net income, or measures that are derived from or incorporate net income, determined in accordance with GAAP and may be different from similarly titled measures of other companies. Within our Asset Management segment, we also consider earnings before interest, taxes, depreciation and amortization (“EBITDA”). Our management believes EBITDA provides additional perspective on the operating efficiency and profitability of the Asset Management segment. EBITDA represents pre-tax operating income before depreciation and amortization of goodwill and intangibles. Total operating return on equity (“ROE”) is an internal performance measure used in the management of our operations, including our compensation plans and planning processes. Our management believes that this measure provides investors with a useful metric to assess our performance and the effectiveness of our use of historic capital. ROE is calculated by dividing (i) total operating income, by (ii) average equity, excluding accumulated OCI, FIN 46-R and discontinued operations. Total operating return on tangible equity ("return on tangible equity") is also an internal performance measure used in the evaluation of our operations. Our management believes that this measure provides investors with a useful metric to assess our performance and the effectiveness of our use of current capital. Return on tangible equity is calculated by dividing (i) total operating income, by (ii) average equity, excluding accumulated OCI, FIN 46-R, discontinued operations and the carrying value of goodwill and intangible assets. More detailed financial information, including reconciling information regarding our non-GAAP financial measures, can be found in our financial supplement for the third quarter of 2008, which is available on our Web site, www.phoenixwm.com in the Investor Relations section. |

3 Overview of Investment in Virtus > Harris Bankcorp will make a $45 million investment in Virtus 8% convertible preferred stock > Preferred stock is convertible into 23% of Virtus common stock at an aggregate equity value for Virtus of $195.6 million ($45 million / 23%) > Redeemable at the end of 6 years; putable at the end of year 7 at liquidation preference > 8% preferred dividend payable in cash or additional securities Benefits to Phoenix > Supports successful separation of Asset Management > Provides valuation benchmark for Phoenix and Virtus shareholders > Provides additional financial flexibility Benefits to Virtus > Provides sponsorship and valuation benchmark > Provides capital to successfully launch new company > Extends existing strategic relationship |

4 Financial Highlights > Net loss of $339.5 million or, $2.97 per share driven by goodwill and intangible impairment in Asset Management > Operating earnings of $15 million or $0.13 per share excluding impairment • Stable life insurance earnings • Annuities affected by market decline • Asset Management affected by market impact on AUM • Unusual transaction costs of $5.1 million; severance and restructuring costs of $3.0 million > Book value post-impairment of $1.53 billion or $13.35 per share ($2.11 billion or $18.46 per share ex AOCI) > Realized investment losses after offsets of $21.0 million |

5 1 Includes net earnings of debt securities pledged as collateral and non-recourse collateralized obligations (421.7) - (10.5) - - Asset Management impairment (5.1) (8.7) (7.5) - - Transaction & Proxy Expenses $0.13 $0.13 - $0.24 $0.29 Operating Income (Loss) Per Share excl. impairment $(2.97) $0.05 $(0.13) $0.03 $0.30 Net Income (Loss) Per Share - - - (4.7) - Discontinued Operations Income (Loss) (6.0) (4.0) (2.8) 1.9 2.6 Asset Management excl. impairment $6.2 (8.6) $14.8 5.6 $20.4 $33.1 (12.4) 1.1 $44.4 2Q08 $(339.5) (21.9) $(317.6) (93.1) $(410.7) $22.1 (11.2) (9.5) $42.8 3Q08 $(14.4) (14.3) $(0.1) (0.5) $(0.6) $20.2 (13.1) (4.1) $37.4 1Q08 $34.8 1.3 $33.5 6.3 $39.8 $37.2 (11.4) 5.3 $43.3 3Q07 $3.2 (20.5) $28.4 13.1 $41.5 $39.6 (10.8) 3.1 $47.3 4Q07 Net Income (Loss) Net Realized Gains (Losses) Operating Income (Loss) Sub Total Life Insurance Income Tax expense (Benefit) Pretax Operating Income Corporate & Other (ex. transaction & proxy expenses) Annuity Earnings Summary $ in millions except per share amounts 1 |

6 3Q07 4Q07 1Q08 2Q08 3Q08 Closed Block Other Traditional 3Q07 4Q07 1Q08 2Q08 3Q08 UL VUL Other $ in millions Traditional Life Pre-tax Operating Income Core Life Pre-tax Operating Income Earnings Review: Life Insurance $21.0 $20.5 $14.6 $20.5 $22.3 $26.8 $22.8 $23.9 $19.5 $23.3 |

7 Earnings Review: Life Insurance 71% 68% 49% 50% 70% 3Q07 4Q07 1Q08 2Q08 3Q08 39% 44% 45% 54% 61% 3Q07 4Q07 1Q08 2Q08 3Q08 VUL Mortality Margin UL Mortality Margin 1 Excludes private placements 1 |

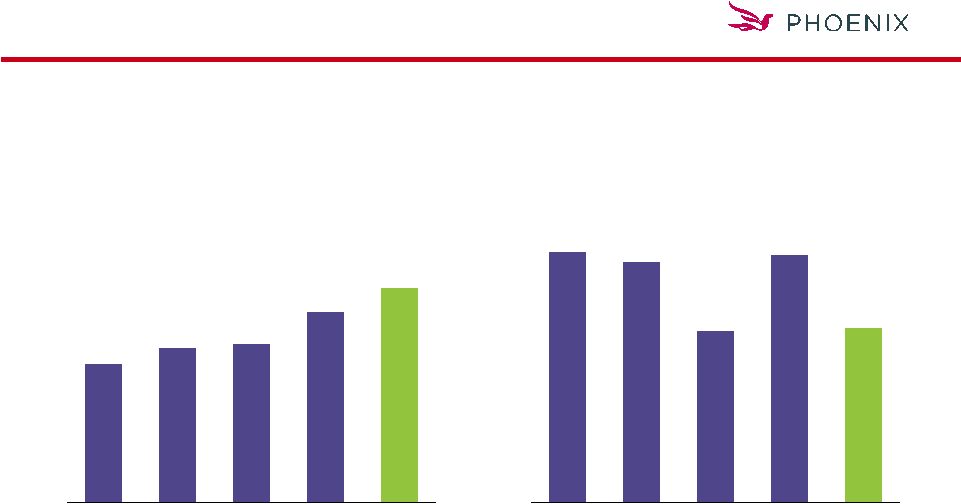

8 $96 $141 $113 $69 $56 3Q07 4Q07 1Q08 2Q08 3Q08 $ in millions Life Insurance Sales Annualized Life Sales Policies Sold and Inforce 3,551 5,659 4,541 4,311 4,523 $160.6 $147.5 $152.6 $156.0 $158.4 3Q07 4Q07 1Q08 2Q08 3Q08 Policy Count Sold Total Life Insurance Inforce 1 Excludes private placements $ in billions 1 |

9 3Q07 4Q07 1Q08 2Q08 3Q08 3Q07 4Q07 1Q08 2Q08 3Q08 $5.3 $3.1 $1.1 Pre-tax Operating Income Funds Under Management 1 Excludes private placements & discontinued products $ in millions except for FUM chart which is in billions 3Q07 4Q07 1Q08 2Q08 3Q08 3Q07 4Q07 1Q08 2Q08 3Q08 Inflows Outflows Earnings Review: Annuities $(4.1) $141 $196 $176 $169 $4.3 $4.3 $4.1 $(152) $(149) $(134) $(136) Net flows $(11) $47 $33 $42 $35 $4.1 $(9.5) $154 $(120) $3.7 1 1 1 1 |

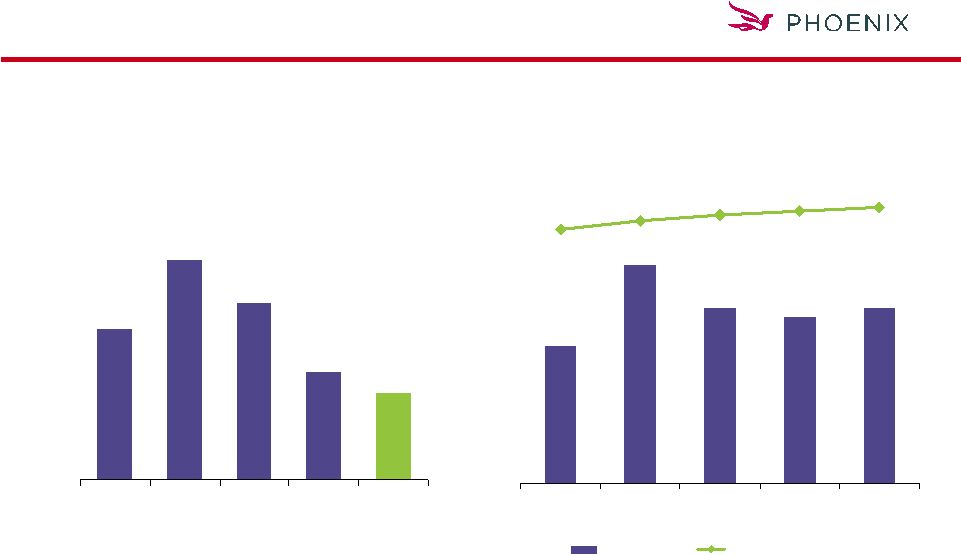

10 Terminated account $1.30 $1.20 $1.30 $0.99 $0.94 3Q07 4Q07 1Q08 2Q08 3Q08 Outflows $46.5 $42.5 $34.5 $33.4 $28.7 3Q07 4Q07 1Q08 2Q08 3Q08 Assets Under Management Inflows $ in billions ($2.1) ($2.0) ($3.2) ($1.6) (5.7) 3Q07 4Q07 1Q08 2Q08 3Q08 Earnings Review: Asset Management Net flows $(0.8) $(0.9) $(4.4) $(2.2) $(0.7) |

11 (3.7) (3.7) (4.5) - - Indirect Expenses 0.2 0.8 0.3 0.6 0.4 Other Income – Net $41.9 $44.9 $47.4 $53.1 $53.9 Revenues (36.8) (38.3) (38.4) (43.8) (44.0) Direct Expenses (ex depreciation) $(427.7) $(4.0) $(13.3) $1.9 $2.6 Operating Income Before Taxes 429.3 7.7 18.1 8.0 7.7 Amortization & Depreciation $1.6 $3.7 $4.8 $9.9 $10.3 EBITDA 2Q08 1Q08 4Q07 3Q07 3Q08 $ in millions Earnings Review: Asset Management |

12 (4.6) 0.2 (3.6) - - Fair Value Option Securities (0.6) - - - - Debt Securities Pledged as Collateral $(8.5) 17.7 $(26.2) 0.1 $(26.5) 2Q08 $(16.6) 30.9 $(47.5) (3.5) $(40.4) 1Q08 $(21.9) 11.4 $(33.3) (2.3) $(31.0) 4Q07 $1.7 (2.2) $3.9 9.2 $(5.3) 3Q07 $(21.0) Realized Gains/Losses After Offsets (39.6) Offsets (PDO, DAC, Taxes) $(60.6) Total Realized Gains/Losses (17.2) Transaction Gains/Losses $(38.2) 3Q08 Gross Impairments $ in millions Realized Loss Trend 1 Excluding debt securities pledged as collateral 1 1 |

13 19.4% $(399.7) Total Gross Unrealized Losses After Offsets 11.4 (235.6) Gross Unrealized Losses After Offsets – Closed Block 8.0% $(164.1) Gross Unrealized Losses After Offsets – Open Block 51.8% $(1,096.1) Total Gross Unrealized Losses 27.4 (580.1) Gross Unrealized Losses – Closed Block 24.4% % of GAAP equity $(516.0) $ millions Gross Unrealized Losses – Open Block Unrealized Losses As of September 30, 2008 1 Based on total stockholders’ equity excluding accumulated other comprehensive income (loss) 2 Gross unrealized losses after offsets for deferred policy acquisition cost adjustments and taxes 3 Gross unrealized losses after offsets for policyholder dividend obligation and taxes $ in millions 1 2 3 |

14 Strong Liquidity Position > Phoenix has modest redemption/liquidity risk • No GICs • No institutional funding agreements • No bank-owned life insurance • No securities lending • No material rating triggers > We have added high quality, liquid positions to the investment portfolio > Holding company requirements are modest and predictable |

15 Phoenix Life Statutory Results > Statutory surplus of $835 million > Estimated RBC >325% > Year-to-date statutory gain from operations of $20.7 million Leverage > Debt/capital: 18.1% Additional Metrics |

16 Appendix Investment Portfolio Update |

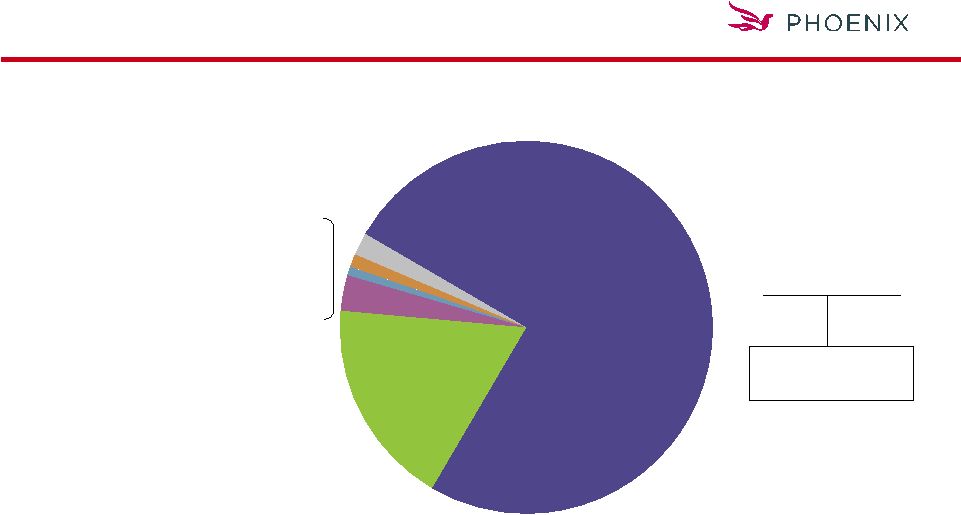

17 Investment Portfolio Public 72% Private 28% Bonds $10,699 75% Policy Loans $2,490 18% Cash & Short-Term $312 2% Venture Capital $202 1% Stock $166 1% Mortgages & Real Estate $12 0% Other Invested Assets $475 3% Invested Assets: $14.4 Billion Market value as of September 30, 2008 $ in millions |

18 Residential MBS by Rating As of September 30, 2008 Percentages based on market value $ in millions 0.5% 0.8% 3.0% 0.2% - BB & Below 53.1% 5.0% 34.7% 39.6% 76.6% % in Closed Block 1.5% 0.5% 3.7% 93.8% 12.8% $1,839.9 $2,043.7 Total 4.7% 1.3% 6.4% 86.8% 1.4% 201.9 247.9 Subprime 1.3% 2.6% 12.9% 80.2% 1.6% 231.5 302.0 Alt-A 3.0% - 4.9% 91.9% 3.6% 513.4 594.7 Prime - - - 100.0% 6.2% $893.1 $899.1 Agency BBB A AA AAA % General Account Market Value Book Value Rating |

19 Residential MBS Subprime Collateral As of September 30, 2008 Percentages based on market value $ in millions - - 29.2% 70.8% - - 1.6 2.4 BB & Below Year of Issue 8.5% 22.6% 29.8% 17.0% 22.1% 1.4% $201.9 $247.9 Total 7.0% 43.4% 9.3% 40.3% - 0.1% 9.6 21.2 BBB - - - 100.0% - - 2.7 6.3 A 46.4% - 1.0% - 52.6% 0.1% 12.8 19.8 AA 6.1% 23.7% 33.5% 15.1% 21.6% 1.2% $175.2 $198.2 AAA 2003 & Prior 2004 2005 2006 2007 % General Account Market Value Book Value Rating |

20 Residential MBS ALT-A Collateral As of September 30, 2008 Percentages based on market value $ in millions - - - 100% - - 7.0 7.0 BB & Below Year of Issue 8.5% 27.1% 25.9% 34.4% 4.1% 1.6% $231.5 $302.0 Total - - 100% - - - 3.0 3.0 BBB 53.2% 12.0% 34.8% - - 0.1% 5.9 8.3 A 47.5% 52.5% - - - 0.2% 29.9 43.6 AA 1.3% 25.0% 29.6% 39.0% 5.1% 1.3% $185.7 $240.1 AAA 2003 & Prior 2004 2005 2006 2007 % General Account Market Value Book Value Rating |

21 CMBS by Year of Origination Year of Issue 5.2% - 3.9% 8.1% 4.9% 2007 8.1% - 10.0% 10.8% 7.5% 2006 5.9% 32.5% - 6.5% 6.1% 2005 80.8% 67.5% 86.1% 74.6% 81.5% 2004 & Prior 70.2% 9.0% $1,285.3 $1,372.2 Total - 0.1% 7.9 10.3 BBB 52.0% 0.5% 74.5 87.4 A 61.3% 1.1% 151.7 172.8 AA 73.3% 7.3% $1,051.2 $1,101.7 AAA % in Closed Block % General Account Market Value Book Value Rating As of September 30, 2008 Percentages based on market value $ in millions |

22 CDO Holdings As of September 30, 2008 Percentages based on market value $ in millions 11.3% 100% - - - 13.7% BB & Below 41.3% - 55.3% 100.0% 51.1% 36.9% % in Closed Block 15.7% 22.8% 34.9% 26.6% 0.3% 50.2 72.9 CMBS 36.6% 28.7% 19.5% 3.9% 2.3% $340.7 $389.6 Total - - - - - 4.6 4.6 RMBS - - 100% - - 3.7 3.9 High-Yield Debt 10.2% 3.9% 85.9% - 0.3% 36.4 36.5 Inv Grade Debt 46.1% 34.5% 5.7% - 1.7% $245.8 $271.7 Bank Loans BBB A AA AAA % General Account Market Value Book Value Collateral - - BB & Below - - % in Closed Block 100% - - - 0.1% $8.1 $16.9 Total 100% - - - 0.1% $8.1 $16.9 Bank Loans BBB A AA AAA % General Account Market Value Book Value Collateral |

23 Financial Sector Holdings $ in millions 40.2% 0.4% 51.6 64.2 Consumer Finance 53.5% 11.1% $1,590.9 $1,845.5 Total - - 4.3 4.2 Project Finance 54.5% 1.5% 216.9 240.1 REITS 52.9% 0.6% 88.4 93.0 Leasing/Rental 60.9% 2.4% 344.7 385.6 Insurance 33.2% 1.9% 272.4 322.6 Diversified Financial 45.5% 0.6% 83.6 98.2 Commercial Finance 58.9% 1.0% 146.8 158.5 Broker-Dealer 63.1% 2.7% $382.2 $479.1 Bank Book Value Market Value % General Account % in Closed Block Sector As of September 30, 2008 Percentages based on market value |

|