UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-10263

GuideStone Funds

(Exact name of registrant as specified in charter)

5005 Lyndon B. Johnson Freeway, Suite 2200

Dallas, TX 75244-6152

(Address of principal executive offices) (Zip code)

Matthew A. Wolfe, Esq.

GuideStone Financial Resources of the Southern Baptist Convention

5005 Lyndon B. Johnson Freeway, Suite 2200

Dallas, TX 75244-6152

(Name and address of agent for service)

Registrant’s telephone number, including area code: 214-720-4640

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

| | (a) | The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1) |

GuideStone Funds

Privacy Notice

NOTICE CONCERNING OUR PRIVACY PRACTICES

This notice provides you with information concerning our policies with respect to non-public personal information that we collect about you in connection with the following financial products and services provided and/or serviced by the entities listed below: Individual Retirement Accounts (“IRAs”), personal mutual fund accounts and/or GuideStone Personal Advisory Services.

The confidentiality of your information is important to us, as we recognize that you depend on us to keep your information confidential, as described in this notice.

We collect non-public personal information about you with regard to the products and services listed above from the following sources:

| • | Information we receive from you on applications or other forms |

| • | Information about your transactions with us, our affiliates or others (including our third-party service providers) |

| • | Information we receive from others, such as service providers, broker-dealers and your personal agents or representatives |

| • | Information you and others provide to us in correspondence sent to us, whether written, electronic or by telephone |

We may disclose such non-public personal financial information about you to one or more of our affiliates as permitted by law. An affiliate of an organization means any entity that controls, is controlled by or is under common control with that organization. GuideStone Funds, GuideStone Financial Resources of the Southern Baptist Convention, GuideStone Capital Management, LLC, GuideStone Resource Management, Inc., GuideStone Investment Services, GuideStone Trust Services, GuideStone Financial Services, GuideStone Advisors and GuideStone Advisors, LLC (collectively “GuideStone”) are affiliates of one another. GuideStone does not sell your personal information to non-affiliated third parties.

We may also disclose any of the personal information that we collect about you to non-affiliated third parties as permitted by law. For example, we may provide your information to non-affiliated companies that provide account services or that perform marketing services on our behalf. We restrict access to non-public personal information about you to those of our employees who need to know that information in order for us to provide products and services to you. We also maintain physical, electronic and procedural safeguards to guard your personal information.

We may continue to maintain and disclose non-public personal information about you after you cease to receive financial products and services from us.

If you have any questions concerning our customer information policy, please contact a customer solutions specialist at 1-888-GS-FUNDS (1-888-473-8637).

This report has been prepared for shareholders of GuideStone Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current prospectus, which contains more complete information about the Funds. Investors are reminded to read the prospectus carefully before investing.

LETTER FROM THE PRESIDENT

Dear Shareholder:

We are pleased to present you with the 2022 GuideStone Funds Annual Report. This report reflects our unwavering commitment to integrity in financial reporting so you may stay fully informed of your investments. We trust that you will find this information valuable when making investment decisions.

2022 offered many opportunities for the GuideStone Funds team to demonstrate its commitment to work on behalf of the investors who entrust us with their hard-earned resources. Despite the challenges brought on by economic headwinds of inflation and volatile markets, all of the people who make up GuideStone Funds worked diligently, as we have since 2001, to continue to earn your trust each day.

We invite you to learn more about GuideStone Funds and the various investment options available by visiting our website, GuideStoneFunds.com/Fund-Literature, or contacting us at 1-888-GS-FUNDS (1-888-473-8637).

Thank you for choosing to invest in GuideStone Funds.

Sincerely,

John R. Jones, CFA

President

FROM THE CHIEF INVESTMENT OFFICER

Market Recap

One word describes the past 12 months: volatility. Between geopolitical events, worldwide inflation and an unprecedented wave of monetary tightening by global central banks, markets whipsawed back and forth.

The year began with a historic level of inflation (at least at that time), but the war between Russia and Ukraine quickly garnered global attention. Soon after the February invasion of Ukraine, nations worldwide imposed punitive sanctions on Russia, essentially turning it into a pariah state. The ongoing conflict has exacerbated inflation and supply chain problems, as both countries are significant producers of critical commodities like oil, natural gas and fertilizer. As the war approaches its first anniversary, we expect to see elevated prices and extreme volatility within commodity markets for the foreseeable future, and the economic consequences of the war are likely to resonate for years to come.

The world’s attention soon returned to the global inflation problem. In the United States, the Consumer Price Index1 (“CPI”) climbed steadily to a peak in June at a year-over-year rate of 9.1%, the highest since 1981. (By December, the CPI had dropped to 6.5% year-over-year, an improvement, but still intolerably high.) In March, the Federal Reserve (“Fed”) made the first of many moves against inflation by ending the quantitative easing program it had started in 2020. Then less than a week after its last bond purchase, it raised the fed funds rate for the first time since 2018. Additional increases followed throughout the year. By the end of December, the Fed had raised the fed funds rate from 0.25% to 4.50%, a far cry from the beginning of the year estimates of a 0.75% increase. Such a rapid increase over so short a time was unprecedented and accounted for much of the market’s volatility last year. The Fed also employed a rarely used tactic and further reduced liquidity in the economy by allowing maturing bonds to roll off without replacing them with other assets. After a seemingly endless climb in 2021, the past year in equity markets was characterized by repeated cycles of declines and rallies as investors carefully parsed every statement from the Fed, looking for signs of a pivot towards an easing of monetary policy.

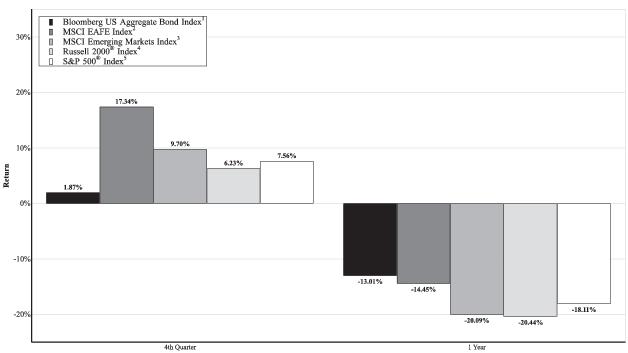

The following table summarizes the calendar year 2022 returns for each major broad-based market index or market indicator.

| Index | 3 rd Quarter

2022 Return | 4 th Quarter

2022 Return | YTD Return as of December 31, 2022 |

| U.S. Equities |

| S&P 500® | -4.88% | 7.56% | -18.11% |

| Russell 2000® | -2.19% | 6.23% | -20.44% |

| International Equities |

| MSCI EAFE | -9.36% | 17.34% | -14.45% |

| MSCI Emerging Markets | -11.57% | 9.70% | -20.09% |

| U.S. Fixed Income |

| Bloomberg US Aggregate Bond | -4.75% | 1.87% | -13.01% |

| Bloomberg US High Yield Corporate | -0.65% | 4.17% | -11.19% |

| Global Fixed Income |

| Bloomberg Global Aggregate Bond | -6.94% | 4.55% | -16.25% |

Looking ahead, here are three things we expect to see in 2023.

Continued Tight Monetary Policy by the Federal Reserve

The Fed has staked its credibility on reducing inflation to a 2.0% target. To do so, it must remain in tightening mode to slow economic activity and lower consumer demand. In every cycle since 1974, the Fed has had to raise the fed funds rate above the inflation rate to bring inflation down to its preferred level. With CPI at 6.5% and the fed funds rate at 4.5%, it still has a way to go. But the ultra-tight labor market (unemployment was 3.5% at the end of December) and wage gains have given the Fed the green

light to continue ratcheting interest rates higher. Economies typically do not feel the full effects of monetary policy tightening until 10 to 24 months after implementation, so we have yet to fully feel the impact of the initial rate hike from last March. Barring financial or market instability, a material increase in the unemployment rate or a sustainable trend of falling inflation, a pivot to lower rates is unlikely anytime soon. In short, expect a higher rate for longer than typically seen in prior cycles. Current projections have the fed funds rate hitting a terminal rate of around 5% in the early second quarter of 2023 and staying above 4% through 2024.

More Downside Ahead for Equity Markets

Though the market has dropped sharply over the year, we believe equity valuations are still too high and have further to fall. Much of the recent decline in equities has stemmed from price-to-earnings2 (P/E) multiple compression. Over the past several years, the Fed flooded the market with liquidity by keeping interest rates low, driving multiples up. Now, the Fed has been pulling liquidity from the markets, thus pushing multiples down and lowering the value of equities. We anticipate a decrease in corporate earnings to add further pressure to stocks over the next 12 months. Earnings growth has already started to show signs of decay, but the equity market is currently trading at a level that has yet to factor in the anticipated decline. As earnings fall, the market will continue to trend downward next year. However, the market rarely travels in a straight line, and bear market rallies (like those we saw in the latter half of last year) are likely to occur along the way.

A Mild to Moderate Recession

Our highest probability outcome and the best-case scenario for the U.S. economy is a mild to moderate recession next year. Rising rates and oil prices typically cause recessions, both of which are in play now. (A recession is an extended period of employment, real income and aggregate demand decline.) Though growth has slowed, the U.S. economy must decline further before hitting recessionary levels. Consumer spending has been resilient as savings and a strong employment market with historically high job openings have cushioned consumers. However, housing and commodity prices have fallen recently due to recession fears and rising interest rates. Additionally, the U.S. Treasury 2/10-year yield curve remains inverted, indicating that investors are becoming more pessimistic about the economic prospects for the near future – a clear recession signal.

But on a positive note – and one we mentioned many times last year – recessions are a normal part of the economic cycle. They effectively correct economic imbalances (such as too-high housing prices and a too-tight labor market) while reducing inflation to a more tolerable level. A mild to moderate recession is preferable to a sustained stagflationary period of sub-par growth and high inflation. Additionally, stock and bond valuations are already much improved, leading to a better opportunity for gains in all asset classes in 2023.

We are likely in store for additional volatility as rate hikes make their impact and markets begin to factor in earnings declines and a recession. So as a reminder to investors: with market volatility comes the temptation to make investment decisions as a reaction to the headlines. But investment decisions should always be strategic and based on long-term goals. We believe that following a disciplined, long-term approach to investing is the key to riding out turbulent market periods.

Thank you for allowing GuideStone to serve you through managing your hard-earned financial assets. We appreciate your continued confidence in us. Please feel free to contact us if you have any comments, questions or concerns. For additional information on GuideStone Funds, we invite you to visit our website at GuideStoneFunds.com.

Sincerely,

David S. Spika, CFA

President and Chief Investment Officer

GuideStone Capital Management, LLC

1The Consumer Price Index (CPI) is a measure of the average change in prices over time in a fixed market basket of goods and services.

2The price-to-earnings (P/E) ratio is the ratio for valuing a company that measures its current share price relative to its per-share earnings, computed by dividing the price of the stock by the company's annual earnings per share.

Past performance does not guarantee future results and the Funds may experience negative performance. There can be no guarantee that any strategy (risk management or otherwise) will be successful. All investing involves risk, including potential loss of principal. You cannot invest directly into an index.

Asset Class Performance Comparison

The following graph illustrates the performance of the major assets classes during 2022.

1The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

2The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure equity market performance of developed markets, excluding the United States & Canada. The index consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom.

3The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The index consists of the following 24 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

4The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® Index is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure that larger stocks do not distort the performance and characteristics of the actual small-cap opportunity set.

5The S&P 500® Index is a market capitalization-weighted equity index composed of approximately 500 U.S. companies, representing all major industries and captures approximately 80% coverage of available market capitalization. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of its constituents.

S&P 500® Index Returns

Despite a rally in the fourth quarter, the U.S. large-cap equity market, as measured by the S&P 500® Index, finished the year down -18.1%. The index return was the worst result since 2008 (amid the Great Financial Crisis) as investors were focused on China’s new Covid policy, the ongoing war in Ukraine, persistently higher inflation, the U.S. midterm elections and fears that the Fed tightening would hinder economic growth. All sectors were negative with the exception of utilities (+1.6) which was slightly positive and energy which posted an astounding +65.7% return for the year. The communication services (-39.9%), consumer discretionary (-37.0%) and information technology (-28.2%) sectors were the weakest performers and significantly underperformed the overall index during the calendar year 2022.

The S&P 500® Index is a market capitalization-weighted equity index composed of approximately 500 U.S. companies, representing all major industries and captures approximately 80% coverage of available market capitalization. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of its constituents.

Data Source: Dow Jones Indices LLC

Russell 2000® Index Returns

The U.S. small cap equity market, as measured by the Russell 2000® Index, declined by -20.4% in 2022. The index posted negative returns during the first three quarters of the year and advanced in the fourth quarter. Smaller capitalization stocks lagged their larger capitalization brethren as the Russell 2000® Index finished roughly -2.3% below the S&P 500® Index for the year. Both posted double-digit losses during a period where the market punished stocks with lower dividend yields, lower quality and higher growth characteristics within the index. All sectors were negative, with the exception of energy which was up a whopping +53% for the year. The information technology (-34.0%), communication services (-30.7%) and consumer discretionary (-30.1%) sectors posted the weakest performance returns within the index during the calendar year 2022.

The Russell 2000® Index measures the performance of the small capitalization segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® Index is constructed to provide a comprehensive and unbiased small capitalization barometer and is completely reconstituted annually to ensure that larger stocks do not distort the performance and characteristics of the actual small capitalization opportunity set.

Data Source: Russell Investments, Bloomberg

MSCI EAFE Index Returns

In 2022, developed-country international stocks posted weak returns, reversing 2021’s strong double-digit performance. The MSCI EAFE Index was down -14.45% for the year after an 11.26% return in 2021. Following a strong market in 2021, international investors saw yet another eventful year, with geopolitical and economic concerns around the world. The Russia/Ukraine war stoked fear into markets as investors searched to grapple with an energy crisis. Inflation soared across borders and central banks raised interest rates for the first time in years. Global recession fears drove the index down nearly -28% through the third quarter. However, in the fourth quarter, as inflation cooled and warmer than expected winter temperatures in Europe forced energy prices lower, the index quickly reversed itself, finishing the year on a strong note. Every country in the MSCI EAFE Index, except for Portugal, posted negative returns in 2022 with Ireland, Sweden and the Netherlands posting the greatest losses and Australia and the U.K. weathering the storm the best. Sector performance was negative across all sectors except for energy, with energy posting the highest returns and information technology and consumer discretionary detracting the most from index performance.

The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure equity market performance of developed markets, excluding the U.S. & Canada. The index consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom.

Data Source: FactSet

MSCI Emerging Markets Index Returns

The broad Emerging Market Equity, as measured by the MSCI Emerging Market Index, was down -20.1% for 2022, its second year of negative returns following a weak 2021, where the index was down by -2.5%. Emerging Market Equity had several strong headwinds in 2022. The China zero-covid policy was a strong burden for the Chinese economy and equity. China had the largest weight in the MSCI Emerging Market Index, and its underperformance led to the underperformance of Emerging Market Equity overall. In addition, a strong USD in 2022 was also very challenging for all Emerging Market Equity sectors.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The index consists of the following 24 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

Data Source: FactSet

Bloomberg US Aggregate Bond Index Returns

The broad U.S. bond market, as measured by the Bloomberg US Aggregate Bond Index, was down -13.01% for 2022, its second year of negative returns following a weak 2021, where the index was down by -1.54%. Rates were substantially higher this year as the Fed and markets grappled with higher inflation, as prices continued to rise in a range of sectors and the transitory narrative was abandoned. This was the first time the index was negative two years in a row since its inception in the mid-70s. All major sectors of the index were down significantly as rates reset higher and spreads widened on a year over year basis. Investment grade credit, agency mortgages and treasuries were all down double digits in the worst year for the index on record.

The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

Data Source: FactSet

Federal Reserve

The Fed reversed course and committed to bringing inflation back to its targeted levels. They increased the targeted Fed Funds rate from 0.00% – 0.25% at the end of 2021 to 4.25% – 4.50% at the end of 2022. This included several outsized hikes of 0.50% - 0.75% in an attempt to prevent inflation from becoming entrenched. The Fed also continued with its balance sheet runoff plan targeting a roll off of $95 billion in assets per month ($60 billion in treasuries and $35 billion in mortgages). The balance sheet ended the year at $8.1 trillion and remains near all time highs.

In its December meeting, members of the Fed provided forward guidance in the form of a new dot plot. The consensus view for the committee was for rates to peak at 5% sometime in 2023. Fed Chairman Powell further indicated that rates would likely remain elevated and restrictive until economic data provided confidence that inflation was under control and heading back toward the stated target of 2%.

The Fed is the central bank of the United States. It was created by Congress to provide the nation with a safer, more flexible and more stable monetary and financial system. The federal funds rate is the interest rate at which depository institutions lend balances at the Fed to other depository institutions overnight. The rate is one tool the Fed can use in their efforts of controlling the supply of money. Changes in the federal funds rate trigger a chain of events that affect other short-term interest rates, foreign exchange rates, long-term interest rates, the amount of money and credit and, ultimately, a range of economic variables, including employment, output and prices of goods and services.

Data Source: Bloomberg, Federal Reserve

U.S. Treasury Yield Curve

The Fed increased its target for the Fed Funds rate by 4.25% in 2022 in response to persistent inflation. Balance sheet normalization also continued and ultimately ended the year with the Fed targeting a runoff of $95 billion in assets per month. Rates increased significantly across the curve. Front end rates rose more rapidly than the long end, and the benchmark 2s/10s curve inverted in July. The curve remained inverted for the rest of the year, going as low as -0.84% and ending the year at -0.54%. The benchmark 10-year U.S. Treasury began the year at 1.51% and ended 1.97% higher at 3.48% peaking at 4.24% in October.

Inflation concerns continued throughout the year and the Fed attempted to catch up after characterizing it as transitory in 2021. Aggressively hiking the Fed Funds rate, persisting in balance sheet runoff and publicly committing to combatting inflation led to higher rates on the front end as markets moved to price in aggressive monetary policy.

The Treasury yield curve illustrates the relationship between yields on short-term, intermediate-term and long-term Treasury securities. Normally, the shape of the yield curve is upward sloping with rates increasing from the short end of the curve moving higher to the long end. The short end of the curve is impacted more by monetary policy (demand for money) while inflationary expectations and market forces impact the long end of the curve.

Data Source: Bloomberg

About Your Expenses (Unaudited)

As a shareholder of the Funds, you incur ongoing costs, including advisory fees and to the extent applicable, shareholder services fees, as well as other Fund expenses. This example is intended to help you to understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. It is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2022, to December 31, 2022. The Annualized Expense Ratio may be different from the expense ratio in the Financial Highlights which is for the fiscal year ended December 31, 2022.

Actual Expenses

The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you incurred over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses attributable to your investment during this period.

Hypothetical Example for Comparison Purposes

The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. Thus, you should not use the hypothetical account values and expenses to estimate the actual ending account balance or your expenses for the period. Rather, these figures are provided to enable you to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. Please note that the expenses shown in the table are meant to highlight your ongoing costs only. Therefore, the second section of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds.

| Actual |

| Fund | | Class | | Beginning

Account Value

07/01/22 | | Ending

Account Value

12/31/22 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

MyDestination 2015

| | Institutional | | $ 1,000.00 | | $ 1,003.40 | | 0.11% | | $ 0.53 |

| | | Investor | | 1,000.00 | | 1,001.80 | | 0.35 | | 1.78 |

MyDestination 2025

| | Institutional | | 1,000.00 | | 1,007.50 | | 0.10 | | 0.49 |

| | | Investor | | 1,000.00 | | 1,004.90 | | 0.35 | | 1.75 |

MyDestination 2035

| | Institutional | | 1,000.00 | | 1,013.00 | | 0.13 | | 0.64 |

| | | Investor | | 1,000.00 | | 1,012.60 | | 0.38 | | 1.91 |

MyDestination 2045

| | Institutional | | 1,000.00 | | 1,020.70 | | 0.13 | | 0.67 |

| | | Investor | | 1,000.00 | | 1,018.20 | | 0.39 | | 1.96 |

MyDestination 2055

| | Institutional | | 1,000.00 | | 1,021.50 | | 0.15 | | 0.78 |

| | | Investor | | 1,000.00 | | 1,020.60 | | 0.40 | | 2.05 |

Conservative Allocation

| | Institutional | | 1,000.00 | | 1,002.70 | | 0.17 | | 0.85 |

| | | Investor | | 1,000.00 | | 1,001.00 | | 0.42 | | 2.12 |

Balanced Allocation

| | Institutional | | 1,000.00 | | 1,005.50 | | 0.13 | | 0.66 |

| | | Investor | | 1,000.00 | | 1,003.80 | | 0.39 | | 1.95 |

Growth Allocation

| | Institutional | | 1,000.00 | | 1,016.80 | | 0.14 | | 0.69 |

| | | Investor | | 1,000.00 | | 1,015.10 | | 0.39 | | 1.99 |

Aggressive Allocation

| | Institutional | | 1,000.00 | | 1,029.80 | | 0.14 | | 0.70 |

About Your Expenses (Unaudited) (Continued)

| Actual |

| Fund | | Class | | Beginning

Account Value

07/01/22 | | Ending

Account Value

12/31/22 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

| | | Investor | | $1,000.00 | | $1,028.30 | | 0.39% | | $2.00 |

Money Market

| | Institutional | | 1,000.00 | | 1,013.40 | | 0.15 | | 0.75 |

| | | Investor | | 1,000.00 | | 1,012.00 | | 0.41 | | 2.10 |

Low-Duration Bond

| | Institutional | | 1,000.00 | | 996.00 | | 0.34 | | 1.73 |

| | | Investor | | 1,000.00 | | 993.90 | | 0.62 | | 3.11 |

Medium-Duration Bond

| | Institutional | | 1,000.00 | | 973.40 | | 0.39 | | 1.94 |

| | | Investor | | 1,000.00 | | 972.10 | | 0.66 | | 3.30 |

Global Bond

| | Institutional | | 1,000.00 | | 1,006.10 | | 0.57 | | 2.89 |

| | | Investor | | 1,000.00 | | 1,004.20 | | 0.87 | | 4.39 |

Defensive Market Strategies®

| | Institutional | | 1,000.00 | | 1,020.20 | | 0.66 | | 3.37 |

| | | Investor | | 1,000.00 | | 1,019.20 | | 0.93 | | 4.74 |

Global Impact

| | Institutional | | 1,000.00 | | 1,002.60 | | 0.98 | | 4.94 |

| | | Investor | | 1,000.00 | | 1,000.50 | | 1.41 | | 7.09 |

Equity Index

| | Institutional | | 1,000.00 | | 1,021.50 | | 0.13 | | 0.64 |

| | | Investor | | 1,000.00 | | 1,020.30 | | 0.39 | | 2.01 |

Value Equity Index (3)

| | Institutional | | 1,000.00 | | 1,018.40 | | 0.20 | | 0.69 |

| | | Investor | | 1,000.00 | | 1,017.70 | | 0.48 | | 1.60 |

Value Equity

| | Institutional | | 1,000.00 | | 1,068.50 | | 0.65 | | 3.38 |

| | | Investor | | 1,000.00 | | 1,067.20 | | 0.91 | | 4.76 |

Growth Equity Index (3)

| | Institutional | | 1,000.00 | | 923.20 | | 0.20 | | 0.65 |

| | | Investor | | 1,000.00 | | 922.40 | | 0.48 | | 1.53 |

Growth Equity

| | Institutional | | 1,000.00 | | 1,003.00 | | 0.66 | | 3.31 |

| | | Investor | | 1,000.00 | | 1,002.00 | | 0.92 | | 4.66 |

| Small Cap Equity | | Institutional | | 1,000.00 | | 1,045.70 | | 0.92 | | 4.77 |

| | | Investor | | 1,000.00 | | 1,044.00 | | 1.20 | | 6.17 |

| International Equity Index | | Institutional | | 1,000.00 | | 1,053.60 | | 0.21 | | 1.10 |

| | | Investor | | 1,000.00 | | 1,052.40 | | 0.50 | | 2.52 |

| International Equity (4) | | Institutional | | 1,000.00 | | 1,045.50 | | 0.85 | | 4.36 |

| | | Investor | | 1,000.00 | | 1,043.50 | | 1.12 | | 5.77 |

| Emerging Markets Equity | | Institutional | | 1,000.00 | | 973.10 | | 1.15 | | 5.71 |

| | | Investor | | 1,000.00 | | 971.20 | | 1.45 | | 7.22 |

| Global Real Estate Securities | | Institutional | | 1,000.00 | | 938.40 | | 0.85 | | 4.15 |

| | | Investor | | 1,000.00 | | 937.10 | | 1.14 | | 5.59 |

| Strategic Alternatives (4) | | Institutional | | 1,000.00 | | 1,009.10 | | 1.15 | | 5.83 |

| | | Investor | | 1,000.00 | | 1,008.60 | | 1.46 | | 7.37 |

| Hypothetical (assuming a 5% return before expenses) |

| Fund | | Class | | Beginning

Account Value

07/01/22 | | Ending

Account Value

12/31/22 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

MyDestination 2015

| | Institutional | | $ 1,000.00 | | $ 1,024.68 | | 0.11% | | $ 0.54 |

| | | Investor | | 1,000.00 | | 1,023.43 | | 0.35 | | 1.80 |

MyDestination 2025

| | Institutional | | 1,000.00 | | 1,024.71 | | 0.10 | | 0.50 |

| | | Investor | | 1,000.00 | | 1,023.46 | | 0.35 | | 1.76 |

| Hypothetical (assuming a 5% return before expenses) |

| Fund | | Class | | Beginning

Account Value

07/01/22 | | Ending

Account Value

12/31/22 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

MyDestination 2035

| | Institutional | | $1,000.00 | | $1,024.57 | | 0.13% | | $0.64 |

| | | Investor | | 1,000.00 | | 1,023.31 | | 0.38 | | 1.92 |

MyDestination 2045

| | Institutional | | 1,000.00 | | 1,024.55 | | 0.13 | | 0.67 |

| | | Investor | | 1,000.00 | | 1,023.26 | | 0.39 | | 1.97 |

MyDestination 2055

| | Institutional | | 1,000.00 | | 1,024.44 | | 0.15 | | 0.78 |

| | | Investor | | 1,000.00 | | 1,023.18 | | 0.40 | | 2.05 |

Conservative Allocation

| | Institutional | | 1,000.00 | | 1,024.36 | | 0.17 | | 0.86 |

| | | Investor | | 1,000.00 | | 1,023.09 | | 0.42 | | 2.14 |

Balanced Allocation

| | Institutional | | 1,000.00 | | 1,024.54 | | 0.13 | | 0.67 |

| | | Investor | | 1,000.00 | | 1,023.26 | | 0.39 | | 1.97 |

Growth Allocation

| | Institutional | | 1,000.00 | | 1,024.52 | | 0.14 | | 0.69 |

| | | Investor | | 1,000.00 | | 1,023.24 | | 0.39 | | 1.99 |

Aggressive Allocation

| | Institutional | | 1,000.00 | | 1,024.51 | | 0.14 | | 0.70 |

| | | Investor | | 1,000.00 | | 1,023.24 | | 0.39 | | 1.99 |

Money Market

| | Institutional | | 1,000.00 | | 1,024.46 | | 0.15 | | 0.75 |

| | | Investor | | 1,000.00 | | 1,023.12 | | 0.41 | | 2.11 |

Low-Duration Bond

| | Institutional | | 1,000.00 | | 1,023.47 | | 0.34 | | 1.75 |

| | | Investor | | 1,000.00 | | 1,022.08 | | 0.62 | | 3.16 |

Medium-Duration Bond

| | Institutional | | 1,000.00 | | 1,023.24 | | 0.39 | | 1.99 |

| | | Investor | | 1,000.00 | | 1,021.86 | | 0.66 | | 3.38 |

Global Bond

| | Institutional | | 1,000.00 | | 1,022.32 | | 0.57 | | 2.92 |

| | | Investor | | 1,000.00 | | 1,020.82 | | 0.87 | | 4.43 |

Defensive Market Strategies®

| | Institutional | | 1,000.00 | | 1,021.87 | | 0.66 | | 3.37 |

| | | Investor | | 1,000.00 | | 1,020.51 | | 0.93 | | 4.74 |

Global Impact

| | Institutional | | 1,000.00 | | 1,020.27 | | 0.98 | | 4.98 |

| | | Investor | | 1,000.00 | | 1,018.11 | | 1.41 | | 7.16 |

Equity Index

| | Institutional | | 1,000.00 | | 1,024.57 | | 0.13 | | 0.64 |

| | | Investor | | 1,000.00 | | 1,023.22 | | 0.39 | | 2.01 |

Value Equity Index (3)

| | Institutional | | 1,000.00 | | 1,016.03 | | 0.20 | | 0.69 |

| | | Investor | | 1,000.00 | | 1,015.12 | | 0.48 | | 1.60 |

Value Equity

| | Institutional | | 1,000.00 | | 1,021.93 | | 0.65 | | 3.31 |

| | | Investor | | 1,000.00 | | 1,020.60 | | 0.91 | | 4.65 |

Growth Equity Index (3)

| | Institutional | | 1,000.00 | | 1,016.03 | | 0.20 | | 0.69 |

| | | Investor | | 1,000.00 | | 1,015.12 | | 0.48 | | 1.60 |

Growth Equity

| | Institutional | | 1,000.00 | | 1,021.90 | | 0.66 | | 3.34 |

| | | Investor | | 1,000.00 | | 1,020.55 | | 0.92 | | 4.70 |

Small Cap Equity

| | Institutional | | 1,000.00 | | 1,020.55 | | 0.92 | | 4.71 |

| | | Investor | | 1,000.00 | | 1,019.17 | | 1.20 | | 6.09 |

International Equity Index

| | Institutional | | 1,000.00 | | 1,024.13 | | 0.21 | | 1.09 |

| | | Investor | | 1,000.00 | | 1,022.68 | | 0.50 | | 2.52 |

International Equity (4)

| | Institutional | | 1,000.00 | | 1,020.94 | | 0.85 | | 4.31 |

| | | Investor | | 1,000.00 | | 1,019.56 | | 1.12 | | 5.70 |

Emerging Markets Equity

| | Institutional | | 1,000.00 | | 1,019.41 | | 1.15 | | 5.85 |

| | | Investor | | 1,000.00 | | 1,017.88 | | 1.45 | | 7.40 |

About Your Expenses (Unaudited) (Continued)

| Hypothetical (assuming a 5% return before expenses) |

| Fund | | Class | | Beginning

Account Value

07/01/22 | | Ending

Account Value

12/31/22 | | Annualized

Expense

Ratio (1) | | Expenses

Paid During

Period (2) |

| Global Real Estate Securities | | Institutional | | $1,000.00 | | $1,020.93 | | 0.85% | | $4.32 |

| | | Investor | | 1,000.00 | | 1,019.44 | | 1.14 | | 5.82 |

| Strategic Alternatives (4) | | Institutional | | 1,000.00 | | 1,019.81 | | 1.15 | | 5.45 |

| | | Investor | | 1,000.00 | | 1,018.27 | | 1.46 | | 7.00 |

(1) Expenses include the effect of contractual waivers by GuideStone CapitalManagement, LLC. The Target Date Funds’ and the Target Risk Funds’ proportionate share of the operating expenses of the Select Funds is not reflected in the tables above.

(2) Expenses are equal to the Fund’s annualized expense ratios for the period July 1, 2022, through December 31, 2022, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

(3) The expense ratios for the Value Equity Index Fund and Growth Equity Index Fund are equal to the class’s annualized expense ratios for the period August 31, 2022, through December 31, 2022, multiplied by the average account value over the period, multiplied by 123/365.

(4) The expense ratios for the International Equity Fund and the Strategic Alternatives Fund include the impact of dividend or interest expense on securities sold short.

ABBREVIATIONS, FOOTNOTES AND INDEX DEFINITIONS

| INVESTMENT ABBREVIATIONS: |

| 10Y | — | 10 Year |

| 12Y | — | 12 Year |

| 1M | — | 1 Month |

| 1Y | — | 1 Year |

| 2M | — | 2 Month |

| 3M | — | 3 Month |

| 5Y | — | 5 Year |

| 6M | — | 6 Month |

| ABS | — | Asset-Backed Security |

| ACES | — | Alternative Credit Enhancement Securities |

| ADR | — | American Depositary Receipt |

| AEX | — | Amsterdam Exchange |

| AGM | — | Assured Guarantee Municipal Corporation |

| ARM | — | Adjustable Rate Mortgage |

| ASX | — | Australian Securities Exchange |

| BAM | — | Build America Mutual |

| BBR | — | Bank Bill Rate |

| BBSW | — | Bank Bill Swap Rate |

| Bobl | — | Bundesobligation ("federal government bond") |

| Bund | — | Bundesanleihe ("federal bond") |

| CDI | — | Crest Depository Interest |

| CDO | — | Collateralized Debt Obligation |

| CDOR | — | Canadian Dollar Offered Rate |

| CDX | — | A series of indexes that track North American and emerging market credit derivative indexes. |

| Cetip | — | Central of Custody and Financial Settlement of Securities |

| CFETS | — | China Foreign Exchange Trade System |

| CLP-TNA | — | Chilean Pesos Floating Rate Index |

| CLO | — | Collateralized Loan Obligation |

| CME | — | Chicago Mercantile Exchange |

| CMT | — | Constant Maturity |

| CONV | — | Convertible |

| COP-IBR-OIS | — | Certificate of Participation - Income-based Repayment - Overnight Indexed Swap |

| COPS | — | Certificates of Participation |

| CVA | — | Dutch Certificate |

| DAC | — | Designated Activity Company |

| DAX | — | Deutscher Aktien Index |

| ESTR | — | Euro Short-Term Rate |

| ETF | — | Exchange Traded Fund |

| EURIBOR | — | Euro Interbank Offered Rate |

| Fannie Mae | — | Federal National Mortgage Association |

| FHA | — | Federal Housing Administration |

| FHLMC | — | Federal Home Loan Mortgage Corporation |

| FRA | — | Forward Rate Agreements |

| FTSE | — | Financial Times Stock Exchange |

| GDR | — | Global Depositary Receipt |

| Gtd. | — | Guaranteed |

| HIBOR | — | Hong Kong Interbank Offered Rate |

| HTS | — | Harmonized Tariff Schedule |

| HY | — | High Yield |

| IBEX | — | Iberia Index |

| ICE | — | Intercontinental Exchange |

| IG | — | Investment Grade |

| IO | — | Interest Only (Principal amount shown is notional) |

| JIBAR | — | Johannesburg Interbank Average Rate |

| JSC | — | Joint Stock Company |

| KLCI | — | Kuala Lumpur Composite Index |

| KWCDC | — | Korean Won Certificate of Deposit |

| LIBOR | — | London Interbank Offered Rate |

| LLC | — | Limited Liability Company |

| LP | — | Limited Partnership |

| MIBOR | — | Mumbai Inter-Bank Overnight Rate |

| MSCI | — | Morgan Stanley Capital International |

| NIBOR | — | Norwegian Interbank Offered Rate |

| NVDR | — | Non-Voting Depository Receipt |

| OAT | — | Obligations Assimilables du Trésor |

| PCL | — | Public Company Limited |

| PIK | — | Payment-in-Kind Bonds |

| PJSC | — | Public Joint Stock Company |

| PLC | — | Public Limited Company |

| PRIBOR | — | Prague Inter-bank Offered Rate |

| PSF | — | Permanent School Fund |

| Q-SBLF | — | Qualified School Bond Loan Fund |

| QPSC | — | Qualified Personal Service Corporation |

| QSC | — | Qatar Shareholder Company |

| REIT | — | Real Estate Investment Trust |

| REMIC | — | Real Estate Mortgage Investment Conduit |

| SA | — | Societe Anonyme |

| SAE | — | Societe Anonyme Egyptienne |

| SBA | — | Small Business Administration |

| SDR | — | Special Drawing Rights |

| SGX | — | Singapore Stock Exchange |

| SOFR | — | Secured Overnight Financing Rate |

| SONIA | — | Sterling Overnight Index Average Rate |

| SonyMA | — | State of New York Mortgage Agency |

| STACR | — | Structured Agency Credit Risk |

| STEP | — | Stepped Coupon Bonds: Interest rates shown reflect the rates currently in effect. |

| STIBOR | — | Stockholm Interbank Offered Rate |

| STRIP | — | Stripped Security |

| TBA | — | To be announced |

| Tbk | — | Terbuka |

| TELBOR | — | Tel Aviv Inter-Bank Offered Rate |

| TIIE | — | The Equilibrium Interbank Interest Rate |

| TSX | — | Toronto Stock Exchange |

| 144A | — | Security was purchased pursuant to Rule 144A under the Securities Act of 1933 and may not be resold subject to that rule except to qualified institutional buyers. As of December 31, 2022, the total market values and percentages of net assets for 144A securities by fund were as follows: |

| Fund | | Value of

144A Securities | | Percentage of

Net Assets |

| Low-Duration Bond | | $305,291,734 | | 30.98% |

| Medium-Duration Bond | | 460,520,070 | | 22.91 |

| Global Bond | | 89,059,414 | | 16.74 |

| Defensive Market Strategies® | | 43,084,382 | | 3.41 |

| Global Impact | | 5,835,923 | | 4.82 |

| International Equity Index | | 10,083,939 | | 1.27 |

| International Equity | | 14,304,290 | | 1.40 |

| Emerging Markets Equity | | 25,579,029 | | 3.61 |

| Global Real Estate Securities | | 954,738 | | 0.39 |

| Strategic Alternatives | | 5,146,180 | | 1.79 |

ABBREVIATIONS, FOOTNOTES AND INDEX DEFINITIONS

| INVESTMENT FOOTNOTES: |

| π | — | Century bond maturing in 2115. |

| ‡‡ | — | All or a portion of the security was held as collateral for open futures, options, securities sold short and/or swap agreements. |

| ‡ | — | Security represents underlying investment on open options contracts. |

| * | — | Non-income producing security. |

| # | — | Security in default. |

| § | — | Security purchased with the cash proceeds from securities loaned. |

| ^ | — | Variable rate security. Security issued at a fixed coupon rate, which converts to a variable rate at a specified date. Rate shown is the rate in effect as of year end. |

| † | — | Variable rate security. Rate shown reflects the rate in effect as of December 31, 2022. |

| γ | — | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

| Ξ | — | Variable or floating rate security, the interest rate of which adjusts periodically and is linked to changes in current local market conditions. |

| γ | — | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

| Ω | — | Rate shown reflects the effective yield as of December 31, 2022. |

| ∞ | — | Affiliated fund. |

| Δ | — | Security either partially or fully on loan. |

| Σ | — | All or a portion of this position has not settled. Full contract rates do not take effect until settlement date. |

| ††† | — | Security is a Level 3 investment (see Note 2 in Notes to Financial Statements). |

| Ø | — | 7-day current yield as of December 31, 2022 is disclosed. |

| ρ | — | Perpetual bond. Maturity date represents the next call date. |

| ~ | — | Century bond maturing in 2121. |

| ◊ | — | Current yield is disclosed. Dividends are calculated based on a percentage of the issuer’s net income. |

| ≈ | — | Unfunded loan commitment. An unfunded loan commitment is a contractual obligation for future funding at the option of the borrower. The Fund receives a stated coupon rate until the borrower draws on the loan commitment, at which time the rate will become the stated rate in the loan agreement. |

| » | — | Zero coupon bond. |

| FOREIGN BOND FOOTNOTES: |

| (A) | — | Par is denominated in Australian Dollars (AUD). |

| (B) | — | Par is denominated in Brazilian Reals (BRL). |

| (C) | — | Par is denominated in Canadian Dollars (CAD). |

| (D) | — | Par is denominated in Danish Krone (DKK). |

| (E) | — | Par is denominated in Euro (EUR). |

| (I) | — | Par is denominated in Indonesian Rupiahs (IDR). |

| (J) | — | Par is denominated in Japanese Yen (JPY). |

| (M) | — | Par is denominated in Mexican Pesos (MXN). |

| (P) | — | Par is denominated in Polish Zloty (PLN). |

| (Q) | — | Par is denominated in Russian Rubles (RUB). |

| (S) | — | Par is denominated in South African Rand (ZAR). |

| (U) | — | Par is denominated in British Pounds (GBP). |

| (Y) | — | Par is denominated in Chinese Yuan (CNY). |

| (Z) | — | Par is denominated in New Zealand Dollars (NZD). |

| (ZB) | — | Par is denominated in Peruvian Sol (PEN). |

| (ZC) | — | Par is denominated in Israeli Shekels (ILS). |

| (ZE) | — | Par is denominated in Czech Koruna (CZK). |

| (ZF) | — | Par is denominated in Thai Baht (THB). |

| COUNTERPARTY ABBREVIATIONS: |

| BAR | — | Counterparty to contract is Barclays Capital. |

| BNP | — | Counterparty to contract is BNP Paribas. |

| BOA | — | Counterparty to contract is Bank of America. |

| CITI | — | Counterparty to contract is Citibank NA London. |

| DEUT | — | Counterparty to contract is Deutsche Bank AG. |

| GSC | — | Counterparty to contract is Goldman Sachs Capital Markets, LP. |

| HSBC | — | Counterparty to contract is HSBC Securities. |

| JPM | — | Counterparty to contract is JPMorgan Chase Bank. |

| MSCS | — | Counterparty to contract is Morgan Stanley Capital Services. |

| RBC | — | Counterparty to contract is Royal Bank of Canada. |

| RBS | — | Counterparty to contract is Royal Bank of Scotland. |

| SC | — | Counterparty to contract is Standard Chartered PLC. |

| SS | — | Counterparty to contract is State Street Global Markets. |

| TD | — | Counterparty to contract is Toronto-Dominion Bank. |

| UBS | — | Counterparty to contract is UBS AG. |

ABBREVIATIONS, FOOTNOTES AND INDEX DEFINITIONS

INDEX DEFINITIONS:

The Bloomberg Global Aggregate Bond Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers.

The Bloomberg US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass- throughs), ABS and CMBS (agency and non-agency).

The Bloomberg US Corporate High Yield 2% Issuer Capped Bond Index is an issuer- constrained version of the flagship US Corporate High Yield Index, which measures the USD-denominated, high yield, fixed-rate corporate bond market. The index follows the same rules as the uncapped version, but limits the exposure of each issuer to 2% of the total market value and redistributes any excess market value index-wide on a pro rata basis.

The Bloomberg Global Aggregate Bond Index (USD-Hedged) is a flagship measure of global investment grade debt from twenty-four local currency markets. This benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. All foreign currency exposure is hedged back to USD.

The FTSE EPRA/NAREIT Developed Index is designed to track the performance of listed real estate companies and REITS worldwide. By making the index constituents free-float adjusted, liquidity, size and revenue screened, the series is suitable for use as the basis for investment products.

The Bloomberg US Treasury: 1-3 Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with 1-2.999 years to maturity. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index. STRIPS are excluded from the index because their inclusion would result in double-counting. (Future Ticker: I00055US)

The Bloomberg 1-3 Month US Treasury Bill Index tracks the market for treasury bills with 1 to 2.9999 months to maturity issued by the US government. US Treasury bills are issued in fixed maturity terms of 4-, 13-, 26- and 52-weeks. (Future Ticker: I00078US)

The J.P. Morgan Emerging Markets Bond Index (EMBI) Plus is a traditional, market-capitalization weighted index comprised of U.S. dollar denominated Brady bonds, Eurobonds and traded loans issued by sovereign entities.

The MSCI ACWI (All Country World Index) Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets.

The MSCI ACWI (All Country World Index) ex USA Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed (excluding U.S.) and emerging markets.

The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of developed markets, excluding the U.S. & Canada. The index consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The index consists of the following 24 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

The Russell 1000® Growth Index is a large-cap index consisting of those Russell 1000® Index securities with greater-than-average growth orientation. Companies in this index tend to exhibit higher price-to- book and price-to-earnings-ratios, lower dividend yields and higher forecasted growth values than the value universe.

The Russell 1000® Value Index is a large-cap index consisting of those Russell 1000® Index securities with a less-than-average growth orientation. Companies in this index tend to exhibit lower price-to-book and price-to-earnings ratios, higher dividend yields and lower forecasted growth values than the growth universe.

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® Index is

ABBREVIATIONS, FOOTNOTES AND INDEX DEFINITIONS

constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure that larger stocks do not distort the performance and characteristics of the actual small-cap opportunity set.

The Russell 3000® Index is composed of approximately 3,000 large U.S. companies. This portfolio of securities represents approximately 98% of the investable U.S. equity market.

The S&P 500® Index is a market capitalization-weighted equity index composed of approximately 500 U.S. companies representing all major industries. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of its constituents.

“Bloomberg®”, Bloomberg Global Aggregate Bond Index, Bloomberg US Aggregate Bond Index, Bloomberg US Corporate High Yield 2% Issuer Capped Bond Index, Bloomberg Global Aggregate Bond Index (USD-Hedged), Bloomberg US Treasury 1-3 Year Index, and Bloomberg 1-3 Month US Treasury Bill Index are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by GuideStone Funds. Bloomberg is not affiliated with GuideStone Funds, and Bloomberg does not approve, endorse, review, or recommend GuideStone Funds. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to GuideStone Funds.

GuideStone Funds are not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings, including FTSE International Limited (collectively, the “LSE Group”), European Public Real Estate Association (“EPRA”), or the National Association of Real Estate Investments Trusts (Nareit) (and together the “Licensor Parties”). FTSE Russell is a trading name of certain of the LSE Group Companies. All rights in the FTSE Russell Indexes vest in the Licensor Parties. “FTSE®” and “FTSE Russell®” are a trademark(s) of the relevant LSE Group company and are used by any other LSE Group company under license. “Nareit®” is a trademark of Nareit, “EPRA®” is a trademark of EPRA and all are used by the LSE Group under license. The FTSE Russell Indexes are calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The Licensor Parties do not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in the FTSE Russell Indexes or (b) investment in or operation of the GuideStone Funds. The Licensor Parties make no claim, prediction, warranty or representation either as to the results to be obtained from the GuideStone Funds or the suitability of the FTSE Russell Indexes for the purpose to which it is being put by GuideStone Funds.

The funds or securities referred to herein are not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities or any index on which such funds or securities are based. The prospectus contains a more detailed description of the limited relationship MSCI has with GuideStone Funds. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

“Standard & Poor’s®”, “S&P®”, and “S&P 500®” are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use by GuideStone Funds. The Funds are not sponsored, endorsed, sold or promoted by Standard & Poor’s and Standard & Poor’s makes no representation regarding the advisability of investing in the Funds.

MyDestination 2015 Fund (Unaudited)

The Fund, through investments primarily in the Select Funds, combined a greater percentage of exposure to fixed income securities with smaller percentages allocated to equity securities and alternative investments. The Fund followed an allocation glide path designed to become more conservative over time, and the targeted allocations were approximately 52% fixed income securities, 45% equity securities and 3% alternative investments as of December 31, 2022.

As a fund of funds, the Fund’s performance was based on the performance of its underlying investments. The Investor Class of the Fund generated a return of -13.10% for the one-year period ended December 31, 2022. Contribution to absolute performance from each major asset class was negative, as the year was one of the worst for both equity and fixed income drawdowns. Exposure to non-U.S. equity securities produced relatively stronger performance than funds with primarily U.S. equity securities exposure. During the year, the downside in markets primarily emanated from lingering supply chain and supply/demand imbalances resulting from the COVID-19 pandemic, which created the strongest increase in inflation the United States has experienced in decades; the resultant global central bank actions to tame inflation, which manifested itself as one of the fastest paces of globally-coordinated interest rate hikes; Russia’s invasion of Ukraine, which not only caused geopolitical angst, but also distorted energy delivery and pricing; and ongoing economic disruptions caused by China’s COVID-lockdown policies as well as the country’s unilateral interventions in China-based global businesses. Lastly, the strength of the U.S. dollar made investing internationally a more difficult proposition for U.S.-based investors. The Equity Index Fund was the largest equity detractor to Fund performance due to its broad exposure to the weakness of stocks in the S&P 500® Index. Broadly, fixed income markets experienced their first back-to-back years of declines and suffered alongside equity markets as uncertainty abounded. As such, the contribution to performance emanating from the fixed income Funds, while relatively more attractive than the equity Funds, was not the typical uncorrelated offset that investors have grown accustomed to experiencing in a diversified portfolio construct. The contribution to absolute performance by the Fund’s exposure to real assets, via exposure to the Global Real Estate Securities Fund as well as Treasury Inflation Protected Securities (TIPS), which were a drag to a lesser degree, was also negative. Exposure to the Strategic Alternatives Fund and Defensive Market Strategies® Fund were strongly positive contributors to Fund performance on a relative basis, particularly when viewed through the lens of the Funds’ roles in augmenting traditional fixed income and broad U.S. equities, respectively. For more information on a Select Fund’s performance, please refer to that Select Fund’s section in this Annual Report.

Certain derivatives were utilized to provide market exposure for the cash positions held in the Fund. These derivative positions primarily included stock index futures and fixed income futures. Overall, derivative exposure had a negative impact on Fund performance for the year.

The Fund attempted to achieve its objective by investing in a diversified portfolio of primarily the Select Funds that represent various asset classes. The Fund is managed to the specific year included in its name (“Target Date”) and assumes a retirement age of 65. The Target Date refers to the approximate year an investor in the Fund would plan to retire and likely stop making any new investments in the Fund. The Fund is designed for an investor who anticipates retiring at or near the Target Date and who plans to withdraw the value of the account in the Fund gradually after retirement. Over time, the allocation to asset classes will change according to a predetermined “glide path,” which adjusts the percentage of fixed income securities and equity securities to become more conservative each year until 15 years after Target Date. The Fund’s value will fluctuate due to changes in interest rates. There is a risk that the issuer of a fixed income investment may fail to pay interest or even principal due in a timely manner or at all. The Fund’s value will fluctuate due to business developments concerning a particular issuer, industry or country, as well as general market and economic conditions. Securities of foreign issuers may be negatively impacted by political events, economic conditions or inefficient, illiquid or unregulated markets in foreign countries, and they also may be subject to inadequate regulatory or accounting standards, which may increase investment risk. By investing in this Fund, you will incur the expenses of the Fund in addition to those of the underlying Select Funds. You may directly invest in the Select Funds. The Fund’s value will go up and down in response to changes in the share prices of the investments that it owns. The amount invested in the Fund is not guaranteed to increase, is not guaranteed against loss nor is the amount of the original investment guaranteed at the Target Date. It is possible to lose money by investing in the Fund.

MyDestination 2015 Fund (Unaudited)

At December 31, 2022, the portfolio holdings of the Fund, as a percentage of net assets, is shown in the following table. Portfolio holdings are subject to risk and may change at any time.

| | % |

| Fixed Income Select Funds | 46.1 |

| U.S. Equity Select Funds | 31.0 |

| Non-U.S. Equity Select Funds | 11.2 |

| U.S. Treasury Obligations | 6.8 |

| Alternative Select Funds | 3.0 |

| Money Market Funds | 1.1 |

| Real Assets Select Funds | 0.8 |

| | 100.0 |

| Average Annual Total Returns as of 12/31/22 | |

| | | Institutional Class* | | Investor Class* | |

| One Year | | (12.87)% | | (13.10)% | |

| Five Year | | 2.60% | | 2.34% | |

| Ten Year | | N/A | | 4.18% | |

| Since Inception | | 3.51% | | 3.88% | |

| Inception Date | | 05/01/17 | | 12/29/06 | |

| Total Fund Operating Expenses (May 1, 2022 Prospectus)(1) | | 0.52% | | 0.77% | |

(1)The Fund’s shareholders indirectly bear the expenses of the Institutional Class shares of the Select Funds in which the Fund invests. Current information regarding the Fund’s Operating Expenses can be found in the Financial Highlights.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained at GuideStoneFunds.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The Adviser has agreed to waive fees and/or reimburse expenses to the extent needed to limit total annual operating expenses to 0.50% for the Institutional Class and 0.75% for the Investor Class. This contractual waiver and reimbursement applies to Fund operating expenses only and will remain in place until April 30, 2023.

MyDestination 2015 Fund (Unaudited)

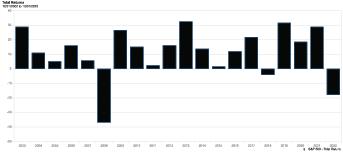

The graph illustrates the results of a hypothetical $10,000 investment in the Investor Class of the Fund for the 10-year period from December 31, 2012 to December 31, 2022, with all dividends and capital gains reinvested.

*These returns reflect investment advisory and shareholder servicing fee waivers, if applicable, during the reported time periods.

Unlike a mutual fund, the performance of an index assumes no taxes, transaction costs, management fees or other expenses.

| | | Shares | | Value |

| MUTUAL FUNDS — 92.1% |

GuideStone Low-Duration Bond Fund

(Institutional Class)∞ | 8,136,999 | | $102,607,558 |

GuideStone Medium-Duration Bond Fund

(Institutional Class)∞ | 12,638,187 | | 158,609,252 |

GuideStone Global Bond Fund

(Institutional Class)∞ | 4,155,306 | | 34,696,805 |

GuideStone Defensive Market Strategies® Fund

(Institutional Class)∞ | 6,631,421 | | 70,293,061 |

GuideStone Equity Index Fund

(Institutional Class)∞ | 2,853,219 | | 114,185,842 |

GuideStone International Equity Index Fund

(Institutional Class)∞ | 5,040,229 | | 49,747,057 |

GuideStone Small Cap Equity Fund

(Institutional Class)∞ | 930,733 | | 14,230,912 |

GuideStone Emerging Markets Equity Fund

(Institutional Class)∞ | 2,687,489 | | 22,064,281 |

GuideStone Global Real Estate Securities Fund

(Institutional Class)∞ | 625,888 | | 5,194,872 |

GuideStone Strategic Alternatives Fund

(Institutional Class)∞ | 1,982,103 | | 19,464,251 |

Total Mutual Funds

(Cost $644,149,359) | | 591,093,891 |

| MONEY MARKET FUNDS — 1.1% |

GuideStone Money Market Fund, 3.97%

(Institutional Class)Ø∞ | 7,072,440 | | 7,072,440 |

| Northern Institutional U.S. Government Portfolio (Shares), 3.73%Ø | 153,590 | | 153,590 |

Total Money Market Funds

(Cost $7,226,030) | | 7,226,030 |

| | | Par | | Value |

| U.S. TREASURY OBLIGATIONS — 6.8% |

| U.S. Treasury Bill | | | | |

| 3.97%, 01/31/23 | $ 1,400,000 | | $ 1,395,715 |

| U.S. Treasury Inflationary Index Bonds | | | | |

| 0.13%, 07/15/24 | 6,724,665 | | 6,511,676 |

| 0.13%, 07/15/26 | 11,388,262 | | 10,744,062 |

| 0.38%, 07/15/27 | 1,991,871 | | 1,879,902 |

| 3.88%, 04/15/29 | 9,444,688 | | 10,628,342 |

| 3.38%, 04/15/32 | 4,751,400 | | 5,447,800 |

| 0.63%, 07/15/32 | 1,420,581 | | 1,303,677 |

| 0.63%, 02/15/43 | 3,415,513 | | 2,760,657 |

| 1.00%, 02/15/48 | 1,770,453 | | 1,493,027 |

| 0.13%, 02/15/51 | 2,003,138 | | 1,293,329 |

Total U.S. Treasury Obligations

(Cost $50,143,878) | | 43,458,187 |

TOTAL INVESTMENTS — 100.0%

(Cost $701,519,267) | | | 641,778,108 |

Other Assets in Excess of

Liabilities — 0.0% | | | 60,834 |

| NET ASSETS — 100.0% | | | $641,838,942 |

VALUATION HIERARCHY

The following is a summary of the inputs used, as of December 31, 2022, in valuing the Fund’s investments carried at fair value:

| | Total

Value | | Level 1

Quoted Prices | | Level 2

Other Significant

Observable Inputs | | Level 3

Significant

Unobservable Inputs |

| Assets: | | | | | | | |

| Investments in Securities: | | | | | | | |

| Money Market Funds | $ 7,226,030 | | $ 7,226,030 | | $ — | | $ — |

| Mutual Funds | 591,093,891 | | 591,093,891 | | — | | — |

| U.S. Treasury Obligations | 43,458,187 | | — | | 43,458,187 | | — |

| Total Assets - Investments in Securities | $641,778,108 | | $598,319,921 | | $43,458,187 | | $ — |

See Notes to Financial Statements.

MyDestination 2025 Fund (Unaudited)

The Fund, through investments primarily in the Select Funds, combined a greater percentage of exposure to equity securities with smaller percentages allocated to fixed income securities, real assets and alternative investments. The Fund followed an allocation glide path designed to become more conservative over time, and the targeted allocations were approximately 42% fixed income securities, 55% equity securities, 1% real assets and 2% alternative investments as of December 31, 2022.

As a fund of funds, the Fund’s performance was based on the performance of its underlying investments. The Investor Class of the Fund generated a return of -14.40% for the one-year period ended December 31, 2022. Contribution to absolute performance from each major asset class was negative, as the year was one of the worst for both equity and fixed income drawdowns. Exposure to non-U.S. equity securities produced relatively stronger performance than funds with primarily U.S. equity securities exposure. During the year, the downside in markets primarily emanated from lingering supply chain and supply/demand imbalances resulting from the COVID-19 pandemic, which created the strongest increase in inflation the United States has experienced in decades; the resultant global central bank actions to tame inflation, which manifested itself as one of the fastest paces of globally-coordinated interest rate hikes; Russia’s invasion of Ukraine, which not only caused geopolitical angst, but also distorted energy delivery and pricing; and ongoing economic disruptions caused by China’s COVID-lockdown policies as well as the country’s unilateral interventions in China-based global businesses. Lastly, the strength of the U.S. dollar made investing internationally a more difficult proposition for U.S.-based investors. The Equity Index Fund was the largest equity detractor to Fund performance due to its broad exposure to the weakness of stocks in the S&P 500® Index. Broadly, fixed income markets experienced their first back-to-back years of declines and suffered alongside equity markets as uncertainty abounded. As such, the contribution to performance emanating from the fixed income Funds, while relatively more attractive than the equity Funds, was not the typical uncorrelated offset that investors have grown accustomed to experiencing in a diversified portfolio construct. The contribution to absolute performance by the Fund’s exposure to real assets, via exposure to the Global Real Estate Securities Fund as well as Treasury Inflation Protected Securities (TIPS), which were a drag to a lesser degree, was also negative. Exposure to the Strategic Alternatives Fund and Defensive Market Strategies® Fund were strongly positive contributors to Fund performance on a relative basis, particularly when viewed through the lens of the Funds’ roles in augmenting traditional fixed income and broad U.S. equities, respectively. For more information on a Select Fund’s performance, please refer to that Select Fund’s section in this Annual Report.

Certain derivatives were utilized to provide market exposure for the cash positions held in the Fund. These derivative positions primarily included stock index futures and fixed income futures. Overall, derivative exposure had a negative impact on Fund performance for the year.

The Fund attempted to achieve its objective by investing in a diversified portfolio of primarily the Select Funds that represent various asset classes. The Fund is managed to the specific year included in its name (“Target Date”) and assumes a retirement age of 65. The Target Date refers to the approximate year an investor in the Fund would plan to retire and likely stop making any new investments in the Fund. The Fund is designed for an investor who anticipates retiring at or near the Target Date and who plans to withdraw the value of the account in the Fund gradually after retirement. Over time, the allocation to asset classes will change according to a predetermined “glide path,” which adjusts the percentage of fixed income securities and equity securities to become more conservative each year until 15 years after Target Date. The Fund’s value will fluctuate due to changes in interest rates. There is a risk that the issuer of a fixed income investment may fail to pay interest or even principal due in a timely manner or at all. The Fund’s value will fluctuate due to business developments concerning a particular issuer, industry or country, as well as general market and economic conditions. Securities of foreign issuers may be negatively impacted by political events, economic conditions or inefficient, illiquid or unregulated markets in foreign countries, and they also may be subject to inadequate regulatory or accounting standards, which may increase investment risk. By investing in this Fund, you will incur the expenses of the Fund in addition to those of the underlying Select Funds. You may directly invest in the Select Funds. The Fund’s value will go up and down in response to changes in the share prices of the investments that it owns. The amount invested in the Fund is not guaranteed to increase, is not guaranteed against loss nor is the amount of the original investment guaranteed at the Target Date. It is possible to lose money by investing in the Fund.

See Notes to Financial Statements.

MyDestination 2025 Fund (Unaudited)

At December 31, 2022, the portfolio holdings of the Fund, as a percentage of net assets, is shown in the following table. Portfolio holdings are subject to risk and may change at any time.

| | % |

| Fixed Income Select Funds | 39.0 |

| U.S. Equity Select Funds | 38.5 |

| Non-U.S. Equity Select Funds | 14.6 |

| U.S. Treasury Obligations | 3.3 |

| Alternative Select Funds | 2.1 |

| Money Market Funds | 1.4 |

| Real Assets Select Funds | 1.1 |

| | 100.0 |

| Average Annual Total Returns as of 12/31/22 | |

| | | Institutional Class* | | Investor Class* | |

| One Year | | (14.11)% | | (14.40)% | |

| Five Year | | 3.28% | | 3.02% | |

| Ten Year | | N/A | | 5.28% | |

| Since Inception | | 4.47% | | 4.28% | |

| Inception Date | | 05/01/17 | | 12/29/06 | |

| Total Fund Operating Expenses (May 1, 2022 Prospectus)(1) | | 0.51% | | 0.76% | |

(1)The Fund’s shareholders indirectly bear the expenses of the Institutional Class shares of the Select Funds in which the Fund invests. Current information regarding the Fund’s Operating Expenses can be found in the Financial Highlights.

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained at GuideStoneFunds.com. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The Adviser has agreed to waive fees and/or reimburse expenses to the extent needed to limit total annual operating expenses to 0.50% for the Institutional Class and 0.75% for the Investor Class. This contractual waiver and reimbursement applies to Fund operating expenses only and will remain in place until April 30, 2023.

See Notes to Financial Statements.

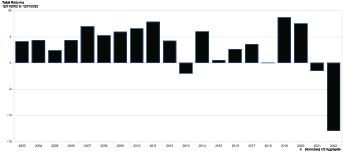

MyDestination 2025 Fund (Unaudited)

The graph illustrates the results of a hypothetical $10,000 investment in the Investor Class of the Fund for the 10-year period from December 31, 2012 to December 31, 2022, with all dividends and capital gains reinvested.

*These returns reflect investment advisory and shareholder servicing fee waivers, if applicable, during the reported time periods.

Unlike a mutual fund, the performance of an index assumes no taxes, transaction costs, management fees or other expenses.

See Notes to Financial Statements.

| | | Shares | | Value |

| MUTUAL FUNDS — 95.3% |

GuideStone Low-Duration Bond Fund

(Institutional Class)∞ | 13,074,611 | | $ 164,870,850 |

GuideStone Medium-Duration Bond Fund

(Institutional Class)∞ | 30,336,080 | | 380,717,807 |

GuideStone Global Bond Fund

(Institutional Class)∞ | 10,778,227 | | 89,998,195 |

GuideStone Defensive Market Strategies® Fund

(Institutional Class)∞ | 18,972,837 | | 201,112,070 |

GuideStone Equity Index Fund

(Institutional Class)∞ | 9,444,405 | | 377,965,070 |

GuideStone International Equity Index Fund

(Institutional Class)∞ | 16,785,907 | | 165,676,898 |

GuideStone Small Cap Equity Fund

(Institutional Class)∞ | 3,022,768 | | 46,218,124 |

GuideStone Emerging Markets Equity Fund

(Institutional Class)∞ | 8,736,698 | | 71,728,287 |

GuideStone Global Real Estate Securities Fund

(Institutional Class)∞ | 2,102,812 | | 17,453,341 |

GuideStone Strategic Alternatives Fund

(Institutional Class)∞ | 3,437,660 | | 33,757,824 |

Total Mutual Funds

(Cost $1,664,787,878) | | 1,549,498,466 |

| MONEY MARKET FUNDS — 1.4% |

GuideStone Money Market Fund, 3.97%