Table of Contents

Filed Pursuant to Rule 424(h)

Registration Nos. 333-226529 and 333-226529-01

The information in this preliminary prospectus is not complete and may be changed. We may not deliver the notes described in this preliminary prospectus until we deliver a final prospectus. This preliminary prospectus is not an offer to sell these notes nor is it seeking an offer to buy these notes in any state where the offer or sale is not permitted.

Subject to Completion, dated May 14, 2019

PROSPECTUS

$1,123,489,000

Capital One Prime Auto Receivables Trust 2019-1

Issuing Entity

Central Index Key Number: 0001766004

Capital One Auto Receivables, LLC Depositor

Central Index Key Number: 0001133438 | Capital One, National Association Sponsor and Servicer

Central Index Key Number: 0000047288 |

You should carefully read the risk factors set forth under “Risk Factors” beginning on page 13 of this prospectus.

The notes are asset-backed securities. The notes will be the obligation of the issuing entity solely and will not be obligations of or guaranteed by any other person or entity.

Capital One Prime Auto Receivables Trust 2019-1 will issue the following asset-backed notes:

| | Initial Note Balance(1) |

| | Offered Amount |

| Interest Rate | Final Scheduled Payment Date | Price to Public(3) | Underwriting Discount | Proceeds to the Depositor | ||||||||

Class A-1 Notes | $238,000,000 | $226,100,000 | % | June 15, 2020 | % | % | % | |||||||||||

Class A-2 Notes | $410,000,000 | $389,500,000 | % | April 15, 2022 | % | % | % | |||||||||||

Class A-3 Notes | $410,000,000 | $389,500,000 | % | November 15, 2023 | % | % | % | |||||||||||

Class A-4 Notes | $124,620,000 | $118,389,000 | % | October 15, 2024 | % | % | % | |||||||||||

Class B Notes(2) | $18,390,000 | $0 | % | October 15, 2024 | % | % | % | |||||||||||

Class C Notes(2) | $12,260,000 | $0 | % | December 16, 2024 | ||||||||||||||

Class D Notes(2) | $12,260,000 | $0 | % | August 15, 2025 | ||||||||||||||

|

|

|

|

|

|

| ||||||||||||

Total | $1,225,530,000 | $1,123,489,000 | $ | $ | $ | |||||||||||||

|

|

|

|

|

|

|

| (1) | Not less than 5% of each class of notes will be retained by the sponsor or one or more majority-owned affiliates of the sponsor to satisfy the credit risk retention obligations of the sponsor as described under “Credit Risk Retention” and “EU Risk Retention” in this prospectus. |

| (2) | The Class B notes, the Class C notes and the Class D notes are not being offered hereby and will be retained by the sponsor or another majority-owned affiliate of the sponsor, but will be entitled to certain payments as described herein. |

| (3) | Plus accrued interest, if any, from the closing date. |

| • | The notes are payable solely from the assets of the issuing entity, which consist primarily of receivables which are motor vehicle retail installment sale contracts that are secured by new and used automobiles, light-duty trucks, SUVs and vans, and funds on deposit in the reserve account. |

| • | The issuing entity will pay interest on and principal of the notes on the 15th day of each month, or, if the 15th is not a business day, the next business day, starting on June 17, 2019. |

| • | Credit enhancement for the notes will consist of (i) a reserve account with an initial deposit of approximately $3,063,835.05, (ii) excess interest on the receivables, (iii) overcollateralization, (iv) the yield supplement overcollateralization amount, and (v) in the case of the Class A notes, Class B notes and Class C notes, the subordination of certain payments to the noteholders of less senior classes of notes. |

| • | The issuing entity will also issue non-interest bearing certificates representing the equity interest in the issuing entity, which initially will be issued to the depositor and are not being offered hereby. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these notes or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The issuing entity is being structured so as not to constitute a “covered fund” as defined in the final regulations issued December 10, 2013, implementing Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, commonly known as the “Volcker Rule.”

| J.P. Morgan | Barclays | Credit Suisse | ||

| Capital One Securities | ||||

The date of this prospectus is May , 2019

Table of Contents

Prospectus

| v | ||||

| vi | ||||

| vii | ||||

| vii | ||||

| viii | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 2 | ||||

| 2 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 7 | ||||

| 7 | ||||

| 10 | ||||

CERTAIN CONSIDERATIONS FOR ERISA AND OTHER U.S. BENEFIT PLANS | 10 | |||

| 10 | ||||

| 10 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| 37 | ||||

| 37 | ||||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 39 | ||||

| 40 | ||||

| 40 | ||||

| 41 | ||||

| 41 | ||||

| 42 | ||||

| 44 | ||||

| 44 | ||||

i

Table of Contents

| 45 | ||||

| 46 | ||||

| 46 | ||||

| 46 | ||||

| 47 | ||||

| 47 | ||||

| 47 | ||||

| 49 | ||||

| 49 | ||||

| 49 | ||||

| 49 | ||||

| 51 | ||||

| 52 | ||||

| 58 | ||||

| 61 | ||||

| 61 | ||||

| 62 | ||||

| 62 | ||||

| 63 | ||||

| 78 | ||||

| 78 | ||||

| 78 | ||||

| 78 | ||||

| 80 | ||||

| 80 | ||||

| 80 | ||||

| 81 | ||||

| 82 | ||||

| 83 | ||||

| THE TRANSFER AGREEMENTS, THE SERVICING AGREEMENT, THE ADMINISTRATION AGREEMENT AND THE ASSET REPRESENTATIONS REVIEW AGREEMENT | 85 | |||

Sale and Assignment of Receivables and Related Security Interests | 85 | |||

| 85 | ||||

| 86 | ||||

| 89 | ||||

| 92 | ||||

| 92 | ||||

| 93 | ||||

| 93 | ||||

| 94 | ||||

| 94 | ||||

| 94 | ||||

| 95 | ||||

| 96 | ||||

| 96 | ||||

| 96 | ||||

| 97 | ||||

| 99 | ||||

| 100 | ||||

| 100 | ||||

Indemnification of the Indenture Trustee and the Owner Trustee | 100 | |||

| 101 | ||||

ii

Table of Contents

| 101 | ||||

Modifications of Receivables and Extensions of Receivables Final Payment Dates | 101 | |||

| 104 | ||||

| 104 | ||||

| 105 | ||||

| 106 | ||||

| 106 | ||||

| 107 | ||||

| 107 | ||||

| 108 | ||||

| 108 | ||||

| 108 | ||||

| 109 | ||||

| 109 | ||||

| 109 | ||||

| 109 | ||||

| 110 | ||||

Priority of Payments Will Change Upon Events of Default that Result in Acceleration | 111 | |||

| 112 | ||||

| 113 | ||||

| 114 | ||||

| 114 | ||||

| 115 | ||||

| 117 | ||||

| 117 | ||||

| 118 | ||||

| 118 | ||||

| 119 | ||||

| 120 | ||||

| 120 | ||||

| 123 | ||||

| 124 | ||||

| 126 | ||||

| 127 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 131 | ||||

Characterization of the Issuing Entity and the Offered Notes | 132 | |||

| 133 | ||||

| 136 | ||||

| 137 | ||||

CERTAIN CONSIDERATIONS FOR ERISA AND OTHER U.S. BENEFIT PLANS | 137 | |||

| 139 | ||||

| 140 | ||||

| 141 | ||||

| 141 | ||||

| 141 | ||||

| 141 | ||||

iii

Table of Contents

Table of Contents

WHERE TO FIND INFORMATION IN THIS PROSPECTUS

This prospectus provides information about the issuing entity, Capital One Prime Auto Receivables Trust 2019-1, including terms and conditions that apply to the notes to be offered by this prospectus.

In this prospectus, the terms “we,” “us,” and “our” refer to Capital One Auto Receivables, LLC, the depositor.

You should rely only on the information provided in this prospectus, including the information incorporated by reference. We have not authorized anyone to provide you with other or different information. If you receive any other information, you should not rely on it. We are not offering the notes in any jurisdiction where the offer is not permitted. We do not claim that the information in this prospectus is accurate on any date other than the date stated on the cover.

We have started with two introductory sections in this prospectus describing the notes and the issuing entity in abbreviated form, followed by a more complete description of the terms of the offering of the notes. The introductory sections are:

| • | Summary of Terms—provides important information concerning the amounts and the payment terms of each class of notes and gives a brief introduction to the key structural features of the issuing entity; and |

| • | Risk Factors—describes briefly some of the risks to investors in the notes. |

We include cross-references in this prospectus to captions in these materials where you can find additional related information. You can find the page numbers on which these captions are located under the Table of Contents in this prospectus. You can also find a listing of the pages where the principal terms are defined under “Index” beginning on page 147 of this prospectus.

If you have received a copy of this prospectus in electronic format, and if the legal prospectus delivery period has not expired, you may obtain at no cost a paper copy of this prospectus from the depositor or from the underwriters upon request.

v

Table of Contents

After the notes are issued, unaudited monthly reports containing information concerning the issuing entity, the notes and the receivables will be prepared by Capital One, National Association (“CONA”), as the servicer, and sent on behalf of the issuing entity to the indenture trustee, which will forward the same to Cede & Co. (“Cede”), as nominee of The Depository Trust Company (“DTC”).

The indenture trustee will also make such reports (and, at its option, any additional files containing the same information in an alternative format) available to noteholders each month via its website, which is presently located at http://www.wilmingtontrustconnect.com. Assistance in using this website may be obtained by calling the indenture trustee’s customer service desk at (866) 829-1928. The indenture trustee will notify the noteholders in writing of any changes in the address or means of access to the website where the reports are accessible.

The reports do not constitute financial statements prepared in accordance with generally accepted accounting principles. CONA, the depositor and the issuing entity do not intend to send any of their financial reports to the beneficial owners of the notes. The issuing entity will file with the Securities and Exchange Commission (the “SEC”) all required annual reports on Form 10-K, distribution reports on Form 10-D and current reports on Form 8-K. Those reports will be filed with the SEC under the name “Capital One Prime Auto Receivables Trust 2019-1” and file number 333-226529-01. The issuing entity incorporates by reference any current reports on Form 8-K filed after the date of this prospectus by or on behalf of the issuing entity before the termination of the offering of the notes. The issuing entity’s annual reports on Form 10-K, distribution reports on Form 10-D and current reports on Form 8-K, and amendments to those reports filed with, or otherwise furnished to, the SEC will not be made available on CONA’s website because those reports are made available to the public on the SEC website as described below.

The depositor has filed with the SEC a Registration Statement on Form SF-3 that includes this prospectus and certain amendments and exhibits under the Securities Act of 1933, as amended, relating to the offering of the notes described herein. This prospectus does not contain all of the information in the Registration Statement. The SEC maintains a website (http://www.sec.gov) that contains reports, registration statements, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

vi

Table of Contents

NOTICE TO RESIDENTS OF THE UNITED KINGDOM

THIS PROSPECTUS MAY ONLY BE COMMUNICATED OR CAUSED TO BE COMMUNICATED IN THE UNITED KINGDOM TO PERSONS AUTHORIZED TO CARRY ON A REGULATED ACTIVITY UNDER THE FINANCIAL SERVICES AND MARKETS ACT 2000, AS AMENDED (“FSMA”), OR TO PERSONS OTHERWISE HAVING PROFESSIONAL EXPERIENCE IN MATTERS RELATING TO INVESTMENTS AND QUALIFYING AS INVESTMENT PROFESSIONALS UNDER ARTICLE 19 (INVESTMENT PROFESSIONALS) OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (FINANCIAL PROMOTION) ORDER 2005, AS AMENDED (THE “ORDER”), OR TO PERSONS WHO FALL WITHIN ARTICLE 49(2)(A)-(D) (HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS, ETC.) OF THE ORDER OR TO ANY OTHER PERSON TO WHOM THIS PROSPECTUS MAY OTHERWISE LAWFULLY BE COMMUNICATED OR CAUSED TO BE COMMUNICATED.

NEITHER THIS PROSPECTUS NOR THE NOTES ARE OR WILL BE AVAILABLE TO OTHER CATEGORIES OF PERSONS IN THE UNITED KINGDOM AND NO ONE IN THE UNITED KINGDOM FALLING OUTSIDE SUCH CATEGORIES IS ENTITLED TO RELY ON, AND THEY MUST NOT ACT ON, ANY INFORMATION IN THIS PROSPECTUS. THE COMMUNICATION OF THIS PROSPECTUS TO ANY PERSON IN THE UNITED KINGDOM OTHER THAN PERSONS IN THE CATEGORIES STATED ABOVE IS UNAUTHORIZED AND MAY CONTRAVENE THE FSMA.

NOTICE TO RESIDENTS OF THE EUROPEAN ECONOMIC AREA

THIS PROSPECTUS IS NOT A PROSPECTUS FOR THE PURPOSE OF THE PROSPECTUS DIRECTIVE (AS DEFINED BELOW). THE NOTES ARE NOT INTENDED TO BE OFFERED, SOLD OR OTHERWISE MADE AVAILABLE TO AND SHOULD NOT BE OFFERED, SOLD OR OTHERWISE MADE AVAILABLE TO ANY RETAIL INVESTOR IN THE EUROPEAN ECONOMIC AREA. FOR THESE PURPOSES, A RETAIL INVESTOR MEANS A PERSON WHO IS ONE (OR MORE) OF: (I) A RETAIL CLIENT AS DEFINED IN POINT (11) OF ARTICLE 4(1) OF DIRECTIVE 2014/65/EU (AS AMENDED, “MIFID II”); OR (II) A CUSTOMER WITHIN THE MEANING OF DIRECTIVE (EU) 2016/97, WHERE THAT CUSTOMER WOULD NOT QUALIFY AS A PROFESSIONAL CLIENT AS DEFINED IN POINT (10) OF ARTICLE 4(1) OF MIFID II; OR (III) NOT A QUALIFIED INVESTOR AS DEFINED IN THE PROSPECTUS DIRECTIVE.

CONSEQUENTLY, NO KEY INFORMATION DOCUMENT REQUIRED BY REGULATION (EU) NO 1286/2014 (AS AMENDED, THE “PRIIPS REGULATION”) FOR OFFERING OR SELLING THE NOTES OR OTHERWISE MAKING THEM AVAILABLE TO RETAIL INVESTORS IN THE EUROPEAN ECONOMIC AREA HAS BEEN PREPARED AND THEREFORE OFFERING OR SELLING THE NOTES OR OTHERWISE MAKING THEM AVAILABLE TO ANY RETAIL INVESTOR IN THE EUROPEAN ECONOMIC AREA MAY BE UNLAWFUL UNDER THE PRIIPS REGULATION.

THIS PROSPECTUS HAS BEEN PREPARED ON THE BASIS THAT ANY OFFERS OF NOTES IN ANY MEMBER STATE OF THE EUROPEAN ECONOMIC AREA WHICH HAS IMPLEMENTED THE PROSPECTUS DIRECTIVE (EACH, A “RELEVANT MEMBER STATE”) WILL BE MADE ONLY TO A PERSON OR LEGAL ENTITY QUALIFYING AS A QUALIFIED INVESTOR (AS SUCH TERM IS DEFINED IN THE PROSPECTUS DIRECTIVE, A “QUALIFIED INVESTOR”). ACCORDINGLY, ANY PERSON MAKING OR INTENDING TO MAKE AN OFFER IN A RELEVANT MEMBER STATE OF NOTES WHICH ARE THE SUBJECT OF THE OFFERING CONTEMPLATED IN THIS PROSPECTUS MAY ONLY DO SO TO ONE OR MORE QUALIFIED INVESTORS. NONE OF THE ISSUING ENTITY, THE DEPOSITOR OR ANY OF THE UNDERWRITERS HAS AUTHORIZED, NOR DO THEY AUTHORIZE, THE MAKING OF ANY OFFER OF NOTES OTHER THAN TO QUALIFIED INVESTORS. THE EXPRESSION “PROSPECTUS DIRECTIVE” MEANS DIRECTIVE 2003/71/EC (AS AMENDED OR SUPERSEDED), AND INCLUDES ANY RELEVANT IMPLEMENTING MEASURE IN THE RELEVANT MEMBER STATE.

vii

Table of Contents

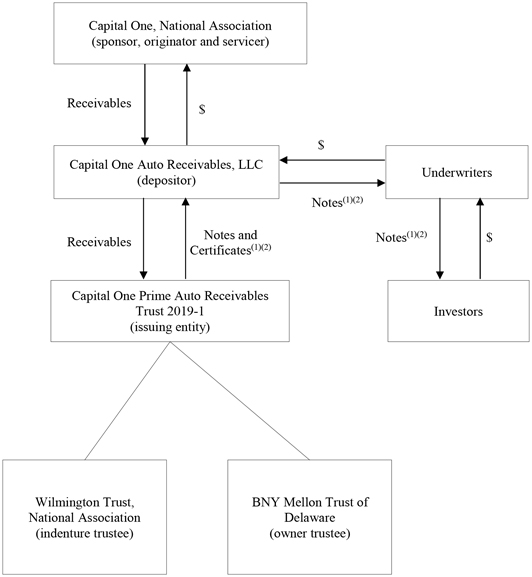

SUMMARY OF STRUCTURE AND FLOW OF FUNDS

This structural summary briefly describes certain major structural components, the relationship among the parties, the flow of funds prior to an acceleration after an event of default and certain other material features of the transaction. This structural summary does not contain all of the information that you need to consider in making your investment decision. You should carefully read this entire prospectus to understand all the terms of this offering.

Structural Diagram

(1) Neither the certificates, which represent an equity interest in the issuing entity, nor the Class B notes, the Class C notes or the Class D notes are being offered hereby.

(2) Not less than 5% of each class of notes and the certificates will be retained by CONA or one or more majority-owned affiliates of CONA to satisfy the credit risk retention obligations of CONA described under “Credit Risk Retention” and “EU Risk Retention” in this prospectus.

viii

Table of Contents

Flow of Funds

ix

Table of Contents

This summary provides an overview of selected information from this prospectus and does not contain all of the information that you need to consider in making your investment decision. This summary provides an overview of certain information to aid your understanding. You should carefully read this entire prospectus to understand all of the terms of this offering.

Issuing Entity

Capital One Prime Auto Receivables Trust 2019-1, a Delaware statutory trust, will be the “issuing entity” of the notes and the certificates. The primary assets of the issuing entity will be a pool of receivables, which are motor vehicle retail installment sale contracts that are secured by new and used automobiles, light-duty trucks, SUVs and vans.

Depositor

Capital One Auto Receivables, LLC, a Delaware limited liability company and a wholly-owned special purpose subsidiary of Capital One, National Association, is the “depositor.” The depositor will sell the receivables to the issuing entity. The depositor will be the initial holder of the issuing entity’s certificates. The certificates are not being offered by this prospectus.

You may contact the depositor by mail at 1600 Capital One Drive, Room 27907B, McLean, Virginia 22102.

Sponsor

Capital One, National Association, a national banking association, known as “CONA” will be the “sponsor” of the transaction described in this prospectus.

Servicer

CONA, operating through its Capital One Auto Finance division and in its capacity as the “servicer,” will service the receivables held by the issuing entity. The servicer will be entitled to receive a servicing fee for each collection period. The “servicing fee” for any payment date will be an amount equal to the product of (1) 1.00%, (2) one-twelfth, and (3) the net pool balance of the receivables as of the first day of the related collection period (or, for the first payment date, as of the cut-off date). As additional compensation, the servicer will be entitled to retain all supplemental servicing fees and reimbursements

and investment earnings (net of investment losses and expenses) from amounts on deposit in the collection account. The servicing fee, together with any portion of the servicing fee that remains unpaid from prior payment dates, will be payable on each payment date from funds on deposit in the collection account with respect to the collection period preceding such payment date, including funds, if any, deposited into the collection account from the reserve account.

Originator

CONA, operating through its Capital One Auto Finance division, acquired the receivables from motor vehicle dealers. We refer to CONA as the “originator.”

CONA will sell all of the receivables to be included in the receivables pool to the depositor and the depositor will sell those receivables to the issuing entity.

Administrator

CONA will be the “administrator” of the issuing entity, and, in such capacity, will provide administrative and ministerial services for the issuing entity.

Trustees

Wilmington Trust, National Association, a national banking association, will be the “indenture trustee.”

BNY Mellon Trust of Delaware, a Delaware banking corporation, will be the “owner trustee.”

Asset Representations Reviewer

Clayton Fixed Income Services LLC, a Delaware limited liability company, will be the “asset representations reviewer.”

The issuing entity will issue and offer the following notes:

1

Table of Contents

| Class | Initial Note Balance(1) | Interest Rate | Final Scheduled Payment Date | |||||

|

|

| ||||||

Class A-1 Notes | $ | 226,100,000 | % | June 15, 2020 | ||||

Class A-2 Notes | $ | 389,500,000 | % | April 15, 2022 | ||||

Class A-3 Notes | $ | 389,500,000 | % | November 15, 2023 | ||||

Class A-4 Notes | $ | 118,389,000 | % | October 15, 2024 | ||||

(1) Not less than 5% of each class of notes will be retained by CONA or one or more majority-owned affiliates of CONA to satisfy the credit risk retention obligations of CONA described under “Credit Risk Retention” and “EU Risk Retention” in this prospectus. $11,900,000 of the Class A-1 notes, $20,500,000 of the Class A-2 notes, $20,500,000 of the Class A-3 notes and $6,231,000 of the Class A-4 notes are not being offered hereunder.

The issuing entity will also issue $18,390,000 of Class B % asset-backed notes, $12,260,000 of Class C % asset-backed notes and $12,260,000 of Class D % asset-backed notes, which are not being offered by this prospectus.

The final scheduled payment date for the Class B notes is October 15, 2024. The final scheduled payment date for the Class C notes is December 16, 2024. The final scheduled payment date for the Class D notes is August 15, 2025.

The Class B notes, Class C notes and the Class D notes are not being publicly registered and will be retained by the sponsor or another majority-owned affiliate of the sponsor. Information about the Class B notes, Class C notes and the Class D notes is set forth herein solely to provide a better understanding of the Class A notes.

We refer to the Class A-1 notes, the Class A-2 notes, the Class A-3 notes and the Class A-4 notes as the “Class A notes.” We refer to the Class A notes, the Class B notes, the Class C notes and the Class D notes, collectively as the “notes.” The Class A notes, which we refer to as the “offered notes,” are the only securities that are being offered by this prospectus.

The notes are issuable in a minimum denomination of $1,000 and integral multiples of $1,000 in excess thereof.

So long as the Class A notes are outstanding, the Class A notes will be the “controlling class.” After the Class A notes have been paid in full, the Class B notes will be the controlling class; after the Class B notes have been paid in full, the Class C notes will be the controlling class; and after the Class C notes have been paid in full, the Class D notes will be the controlling class.

The issuing entity expects to issue the notes on or about May , 2019, which we refer to as the “closing date.”

On the closing date, the issuing entity will issue subordinated and non-interest bearing “certificates” in a nominal aggregate principal amount of $100,000, which represent the equity interest in the issuing entity and are not offered hereby. The “certificateholders” will be entitled on each payment date only to amounts remaining after payments on the notes and payments of issuing entity expenses and other required amounts on such payment date. The certificates will initially be held by the depositor. The portion of the certificates retained by the depositor to satisfy U.S. and EU credit risk retention rules will not be sold or transferred except as permitted under those rules. See “—Credit Risk Retention” and “—EU Risk Retention.”

To the extent of funds available therefor and prior to an acceleration of the notes following an event of default, after payment of certain amounts to the servicer, the issuing entity will pay interest and principal on the notes monthly, on the 15th day of each month (or, if the 15th day is not a business day, on the next business day), which we refer to as the “payment date.” The first payment date is June 17, 2019. On each payment date, payments on the notes will be made to holders of record as of the close of business on the business day immediately preceding that payment date (except in limited circumstances where definitive notes are issued), which we refer to as the “record date.”

Interest Payments

The issuing entity will pay interest on the Class A-1 notes on the basis of the actual number of days elapsed during the period for which interest is payable and a 360-day year. This means that the interest due on each payment date for the Class A-1 notes will be the product of (i) the outstanding principal balance of the related class of notes, (ii) the applicable interest rate and (iii) the actual number of days from and including the previous payment date (or, in the case of the first payment date, from and including the closing date) to but excluding the current payment date divided by 360.

The issuing entity will pay interest on the Class A-2 notes, the Class A-3 notes, the Class A-4 notes, the Class B notes, the Class C notes and the Class D notes on the basis of a 360-day year consisting of twelve 30-day months. This means that the interest

2

Table of Contents

due on each payment date for the Class A-2 notes, the Class A-3 notes, the Class A-4 notes, the Class B notes, the Class C notes and the Class D notes will be the product of (i) the outstanding principal balance of the related class of notes, (ii) the applicable interest rate and (iii) 30 (or, in the case of the first payment date, the number of days from and including the closing date to but excluding June 15, 2019 (assuming a 30-day calendar month)), divided by 360. Interest payments on all Class A notes will have the same priority. Interest payments on the Class B notes will be subordinated to interest payments and, in specified circumstances, principal payments on the Class A notes. Interest payments on the Class C notes will be subordinated to interest payments and, in specified circumstances, principal payments on the Class A notes and the Class B notes. Interest payments on the Class D notes will be subordinated to interest payments and, in specified circumstances, principal payments on the Class A notes, the Class B notes and the Class C notes.

A failure to pay the interest due on the notes of the controlling class on any payment date that continues for a period of five (5) business days or more will result in an event of default under the indenture.

Principal Payments

The issuing entity will generally pay principal sequentially to the earliest maturing class of notes monthly on each payment date in accordance with the payment priorities described below under “—Priority of Payments.”

The issuing entity will make principal payments of the notes based on the amount of collections and defaults on the receivables during the prior collection period. This prospectus describes how available funds and amounts on deposit in the reserve account are allocated to principal payments of the notes.

On each payment date, prior to the acceleration of the notes following an event of default, which is described below under “—Interest and Principal Payments after an Event of Default,” the issuing entity will distribute funds available to pay principal of the notes in the following order of priority:

| ● | first, to the Class A-1 noteholders, until the Class A-1 notes are paid in full; |

| ● | second, to the Class A-2 noteholders until the Class A-2 notes are paid in full; |

| ● | third, to the Class A-3 noteholders, until the Class A-3 notes are paid in full; |

| ● | fourth, to the Class A-4 noteholders, until the Class A-4 notes are paid in full; |

| ● | fifth, to the Class B noteholders, until the Class B notes are paid in full; |

| ● | sixth, to the Class C noteholders, until the Class C notes are paid in full; and |

| ● | seventh, to the Class D noteholders, until the Class D notes are paid in full. |

All unpaid principal of a class of notes will be due on the final scheduled payment date for that class.

Interest and Principal Payments after an Event of Default

If an event of default under the indenture were to occur and the maturity of the notes were to be accelerated, the priority of payments of principal and interest will change from the description in “—Interest Payments” above, “—Principal Payments” above and “Priority of Payments” below. The priority of payments of principal and interest after an event of default under the indenture and acceleration of the notes will depend on the nature of the event of default.

On each payment date after an event of default under the indenture occurs as a result of a payment default or a bankruptcy event relating to the issuing entity and the notes are accelerated, after payment of certain amounts to the trustees, the asset representations reviewer and the servicer, interest on the Class A notes will be paid ratably to each class of Class A notes and then principal payments will be made first to Class A-1 noteholders until the Class A-1 notes are paid in full. Next, the noteholders of each class of the Class A-2 notes, the Class A-3 notes and the Class A-4 notes will receive principal payments, ratably, based on the outstanding principal balance of each remaining class of Class A notes until each such class of notes is paid in full. After interest on and principal of all of the Class A notes are paid in full, interest and principal payments will be made to noteholders of the Class B notes. After interest on and principal of all of the Class B notes are paid in full, interest and principal payments will be made to noteholders of the Class C notes. After interest on and principal of all of the Class C notes are paid in full, interest and

3

Table of Contents

principal payments will be made to noteholders of the Class D notes.

On each payment date after an event of default under the indenture occurs as a result of the issuing entity’s breach of a covenant (other than a payment default), representation or warranty and the maturity of the notes is accelerated, after payment of certain amounts to the trustees, the asset representations reviewer and the servicer, interest on the Class A notes will be paid ratably to each class of Class A notes followed by interest on the Class B notes, then followed by interest on the Class C notes and then followed by interest on the Class D notes. After the payments described in the previous sentence, principal payments of each class of notes will then be made first to the Class A-1 noteholders until the Class A-1 notes are paid in full. Next, the noteholders of all other classes of Class A notes will receive principal payments, ratably, based on the outstanding principal balance of each remaining class of Class A notes until those other classes of Class A notes are paid in full. Next, the Class B noteholders will receive principal payments until the Class B notes are paid in full. Next, the Class C noteholders will receive principal payments until the Class C notes are paid in full. Finally, the Class D noteholders will receive principal payments until the Class D notes are paid in full.

See “The Indenture—Rights Upon Event of Default” in this prospectus.

If an event of default has occurred but the notes have not been accelerated, then interest and principal payments will be made in the priority set forth below under “—Priority of Payments.”

Optional Redemption of the Notes

The servicer will have the right at its option to exercise a “clean-up call” to purchase (and/or designate one or more persons to purchase) the receivables and the other issuing entity property (other than the reserve account) from the issuing entity on any payment date if both of the following conditions are satisfied: (a) as of the last day of the related collection period, the net pool balance has declined to 10% or less of the net pool balance as of the cut-off date and (b) the purchase price (as defined below) and the available funds for such payment date would be sufficient to pay (i) the amounts required to be paid under clauses first through ninth and eleventh in accordance with “—Priority of Payments” below (assuming that such payment date is not a redemption date) and (ii) the aggregate unpaid note balance of all

of the outstanding notes (after giving effect to the payments described in the preceding clause (i)). We use the term “net pool balance” to mean, as of any date, the aggregate outstanding principal balance of all receivables (other than defaulted receivables) owned by the issuing entity on that date. If the servicer (or its designee) purchases the receivables and other issuing entity property (other than the reserve account), the “purchase price” will equal the net pool balance plus accrued and unpaid interest on the receivables as of the last day of the collection period immediately preceding the redemption date, which amount (net of any collections deposited into the collection account after the last day of the collection period immediately preceding the redemption date) will be deposited by the servicer (or its designee) into the collection account on or prior to noon, New York City time, on the redemption date.

It is expected that at the time this option becomes available to the servicer, the Class A-4 notes, Class B notes, Class C notes and Class D notes will be outstanding.

Additionally, each of the notes is subject to redemption in whole, but not in part, on any payment date on which the sum of the amounts on deposit in the reserve account and remaining available funds after the payments under clauses first through ninth and eleventh set forth in “—Priority of Payments” below would be sufficient to pay in full the aggregate unpaid note balance of all of the outstanding notes as determined by the servicer. On such payment date, the outstanding notes shall be redeemed in whole, but not in part.

Notice of redemption under the indenture must be given by the indenture trustee prior to the applicable redemption date to each holder of notes as of the close of business on the record date preceding the applicable redemption date. All notices of redemption will state: (i) the redemption date; (ii) the redemption price; (iii) that the record date otherwise applicable to that redemption date is not applicable and that payments will be made only upon presentation and surrender of those notes, and the place where those notes are to be surrendered for payment of the redemption price; (iv) that interest on the notes will cease to accrue on the redemption date; and (v) the CUSIP numbers (if applicable) for the notes. Notice of redemption of the notes shall be given by the indenture trustee in the name and at the expense of the issuing entity.

4

Table of Contents

The occurrence of any one of the following events will be an “event of default” under the indenture:

| ● | a default in the payment of any interest on any note of the controlling class when the same becomes due and payable, and such default continues for a period of five (5) business days or more; |

| ● | default in the payment of the principal of any note at the related final scheduled payment date or the redemption date; |

| ● | any failure by the issuing entity to duly observe or perform in any material respect any of its covenants or agreements in the indenture (other than (i) a covenant or agreement, a default in the observance or performance of which is elsewhere specifically addressed or (ii) a covenant or agreement pursuant to the FDIC Rule Covenant (as defined below)), which failure materially and adversely affects the interests of the noteholders, and which continues unremedied for ninety (90) days after receipt by the issuing entity of written notice thereof from the indenture trustee or noteholders evidencing at least a majority of the outstanding principal amount of the notes of the controlling class; |

| ● | any representation or warranty of the issuing entity made in the indenture proves to be incorrect in any material respect when made, which failure materially and adversely affects the interests of the noteholders, and which failure continues unremedied for ninety (90) days after receipt by the issuing entity of written notice thereof from the indenture trustee or noteholders evidencing at least a majority of the outstanding principal amount of the notes of the controlling class; or |

| ● | the occurrence of certain events (which, if involuntary, remain unstayed for more than ninety (90) days) of bankruptcy, insolvency, receivership or liquidation of the issuing entity. |

Notwithstanding the foregoing, a delay in or failure of performance referred to under the first four bullet points above for a period of one-hundred twenty

(120) days will not constitute an event of default if that delay or failure was caused by force majeure or other similar occurrence.

The amount of principal required to be paid to noteholders under the indenture generally will be limited to amounts available to make such payments in accordance with the priority of payments. Thus, the failure to pay principal on a class of notes due to a lack of amounts available to make such payments will not result in the occurrence of an event of default until the final scheduled payment date or redemption date for that class of notes.

The primary assets of the issuing entity will be a pool of motor vehicle retail installment sale contracts secured by new and used automobiles, light-duty trucks, SUVs and vans. We refer to these contracts as “receivables,” to the pool of those receivables as the “receivables pool” and to the persons who financed their purchases with these contracts as “obligors.”

The receivables identified on the schedule of receivables delivered by CONA on the closing date will be transferred by CONA to the depositor and then transferred by the depositor to the issuing entity. The issuing entity will grant a security interest in the receivables and the other issuing entity property to the indenture trustee on behalf of the noteholders.

The “issuing entity property” will include the following:

| ● | the receivables, including collections on the receivables after April 30, 2019, which we refer to as the “cut-off date”; |

| ● | security interests in the vehicles financed by the receivables, which we refer to as the “financed vehicles”; |

| ● | all receivable files relating to the original motor vehicle retail installment sale contracts evidencing the receivables; |

| ● | rights to proceeds under insurance policies that cover the obligors under the receivables or the financed vehicles and refunds in connection with extended service agreements relating to receivables which became defaulted receivables after the cut-off date; |

5

Table of Contents

| ● | any other property securing the receivables; |

| ● | rights to amounts on deposit in the collection account, the principal distribution account, the reserve account and any other accounts owned by the issuing entity (other than the certificate distribution account), and permitted investments of those accounts; |

| ● | rights under the administration agreement, the sale agreement, the servicing agreement and the purchase agreement; and |

| ● | the proceeds of any and all of the above. |

Receivable Representations and Warranties

CONA will make certain representations and warranties regarding the characteristics of the receivables as of the cut-off date. Breach of these representations may, subject to certain conditions, result in CONA being obligated to repurchase the related receivable. See “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Representations and Warranties.” This repurchase obligation will constitute the sole remedy available to the noteholders or the issuing entity for any uncured breach by CONA of those representations and warranties.

If an investor in the notes requests that CONA repurchase any receivable due to a breach of a representation or warranty as described above, and the repurchase request has not been fulfilled or otherwise resolved to the reasonable satisfaction of the requesting party within one-hundred eighty (180) days of the receipt of notice of the request by CONA, the requesting party will have the right to refer the matter, at its discretion, to either mediation (including nonbinding arbitration) or third-party arbitration. The terms of the mediation or arbitration, as applicable, are described under “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Dispute Resolution” in this prospectus.

Review of Asset Representations

As more fully described in “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Asset Representations Review” in this prospectus, if the

aggregate amount of delinquent receivables exceeds a specified threshold, then investors holding at least 5% of the aggregate outstanding principal amount of the notes may elect to initiate a vote to determine whether the asset representations reviewer will conduct a review. If investors representing at least a majority of the voting investors vote in favor of directing a review, then the asset representations reviewer will perform a review of specified delinquent receivables for compliance with the representations and warranties made by CONA. See “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Asset Representations Review” in this prospectus.

The statistical information in this prospectus is based on the pool of receivables as of the cut-off date.

As of the close of business on the cut-off date, the receivables in the pool had an aggregate initial principal balance of $1,250,000,000.97 and had:

| • | an average original principal balance of $22,206.94; |

| • | a weighted average contract rate of approximately 4.43%(1); |

| • | a weighted average original term of approximately 66 months(1); |

| • | a weighted average remaining term of approximately 58 months(1); |

| • | a minimum FICO® score at origination of 700; |

| • | a maximum FICO® score at origination of 882; |

| • | a weighted average FICO® score at origination of approximately 779(1); and |

| • | a weighted average loan-to-value ratio at origination of approximately 92.21%(1). |

For more information about the characteristics of the receivables in the pool, see “The Receivables Pool” in this prospectus. In connection with the offering of the notes, the depositor has performed a review of the receivables in the pool as of the cut-off date and

1 Weighted by outstanding principal balance as of the cut-off date.

6

Table of Contents

certain disclosure in this prospectus relating to the receivables, as described under “The Receivables Pool—Review of the Receivables Pool” in this prospectus.

As described under “The Originator—Underwriting” in this prospectus, in limited circumstances, some contracts may be approved by CONA under an exception to CONA’s underwriting criteria based on a judgmental evaluation. The originator’s credit risk management monitors exceptions to the underwriting criteria continuously using an automated tracking tool.

None of the receivables to be sold to the issuing entity on the closing date were approved as an exception to CONA’s underwriting criteria.

In addition to the purchase of receivables from the issuing entity in connection with the servicer’s exercise of its “clean-up call” option as described above under “Interest and Principal—Optional Redemption of the Notes,” receivables may be purchased from the issuing entity by the sponsor, in connection with the breach of certain representations and warranties concerning the characteristics of the receivables, and by the servicer, in connection with certain specified modifications to the receivables or the breach of certain servicing covenants, as described under “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Representations and Warranties” in this prospectus.

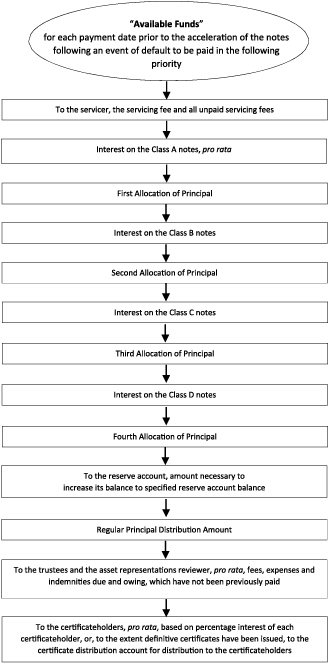

On each payment date, except after the acceleration of the notes following an event of default, the paying agent will make the following payments and deposits from available funds in the collection account (including funds, if any, deposited into the collection account from the reserve account to the extent described in “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Reserve Account” in this prospectus) in the following amounts and order of priority:

| ● | first, to the servicer, the servicing fee (including servicing fees not previously paid); |

| ● | second, pro rata to the Class A noteholders, accrued interest on the Class A notes; |

| ● | third, to the principal distribution account for distribution to the noteholders, the First Allocation of Principal; |

| ● | fourth, to the Class B noteholders, accrued interest on the Class B notes; |

| ● | fifth, to the principal distribution account for distribution to the noteholders, the Second Allocation of Principal; |

| ● | sixth, to the Class C noteholders, accrued interest on the Class C notes; |

| ● | seventh, to the principal distribution account for distribution to the noteholders, the Third Allocation of Principal; |

| ● | eighth, to the Class D noteholders, accrued interest on the Class D notes; |

| ● | ninth, to the principal distribution account for distribution to the noteholders, the Fourth Allocation of Principal; |

| ● | tenth, to the reserve account, any additional amounts required to cause the amount of cash on deposit in the reserve account to equal the specified reserve account balance; |

| ● | eleventh, to the principal distribution account for distribution to the noteholders, the Regular Principal Distribution Amount; |

| ● | twelfth, to the indenture trustee, the owner trustee and the asset representations reviewer, pro rata, fees, expenses and indemnification amounts due and owing which have not been previously paid; and |

| ● | thirteenth, to the certificateholders, pro rata based on the percentage interest of each certificateholder, or, to the extent definitive certificates have been issued, to the certificate distribution account for distribution to the certificateholders. |

Amounts deposited in the principal distribution account will be paid to the noteholders of the notes as described under “The Notes—Payment of Principal.”

Credit enhancement provides protection for the notes against losses and delays in payment on the

7

Table of Contents

receivables or other shortfalls of cash flow. The credit enhancement for the notes will be the reserve account, overcollateralization (in addition to the yield supplement overcollateralization amount), the yield supplement overcollateralization amount, the excess interest on the receivables and, in the case of the Class A notes, the Class B notes and the Class C notes, subordination of certain payments as described below. If the credit enhancement is not sufficient to cover all amounts payable on the notes, notes having a later final scheduled payment date generally will bear a greater risk of loss than notes having an earlier final scheduled payment date. See also “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Overcollateralization” and “—Excess Interest” in this prospectus.

The credit enhancement for the notes will be as follows:

| Class A notes: | Subordination of payments on the Class B notes, the Class C notes and the Class D notes, overcollateralization (in addition to the yield supplement overcollateralization amount), the yield supplement overcollateralization amount, the reserve account and excess interest on the receivables. | |

| Class B notes: | Subordination of payments on the Class C notes and the Class D notes, overcollateralization (in addition to the yield supplement overcollateralization amount), the yield supplement overcollateralization amount, the reserve account and excess interest on the receivables. | |

| Class C notes: | Subordination of payments on the Class D notes, overcollateralization (in addition to the yield supplement overcollateralization amount), the yield supplement overcollateralization amount, the reserve account and excess interest on the receivables. | |

| Class D notes: | Overcollateralization (in addition to the yield supplement overcollateralization amount), the yield supplement overcollateralization amount, the reserve account and excess interest on the receivables. | |

Subordination of Payments on the Class B Notes

As long as the Class A notes remain outstanding, payments of interest on any payment date on the Class B notes will be subordinated to payments of interest on the Class A notes and certain other payments on that payment date (including principal payments of the Class A notes in specified circumstances), and payments of principal of the Class B notes will be subordinated to all payments of principal of and interest on the Class A notes and certain other payments on that payment date. If the notes have been accelerated after an event of default under the indenture, the priority of payments will change. For a description of these changes in priority, see “—Interest and Principal— Interest and Principal Payments after an Event of Default” above and “The Indenture—Priority of Payments Will Change Upon Events of Default That Result in Acceleration.”

Subordination of Payments on the Class C Notes

As long as the Class A notes and the Class B notes remain outstanding, payments of interest on any payment date on the Class C notes will be subordinated to payments of interest on the Class A notes and the Class B notes and certain other payments on that payment date (including principal payments of the Class A notes and the Class B notes in specified circumstances), and payments of principal of the Class C notes will be subordinated to all payments of principal of and interest on the Class A notes and the Class B notes and certain other payments on that payment date. If the notes have been accelerated after an event of default under the indenture, the priority of payments will change. For a description of these changes in priority, see “—Interest and Principal—Interest and Principal Payments after an Event of Default” above and “The Indenture—Priority of Payments Will Change Upon Events of Default That Result in Acceleration.”

Subordination of Payments on the Class D Notes

As long as the Class A notes, the Class B notes and the Class C notes remain outstanding, payments of interest on any payment date on the Class D notes will be subordinated to payments of interest on the Class A notes, the Class B notes and the Class C notes and certain other payments on that payment date (including principal payments of the Class A

8

Table of Contents

notes, the Class B notes and the Class C notes in specified circumstances), and payments of principal of the Class D notes will be subordinated to all payments of principal of and interest on the Class A notes, the Class B notes and the Class C notes and certain other payments on that payment date. If the notes have been accelerated after an event of default under the indenture, the priority of payments will change. For a description of these changes in priority, see “—Interest and Principal—Interest and Principal Payments after an Event of Default” above and “The Indenture—Priority of Payments Will Change Upon Events of Default That Result in Acceleration.”

Overcollateralization

Overcollateralization is the amount by which the adjusted pool balance exceeds the outstanding principal balance of the notes. (We use the term “adjusted pool balance” to mean, as of any date of determination, the net pool balance at that date, minus the yield supplement overcollateralization amount (as described below) as of that date.) The initial overcollateralization level on the closing date will be approximately 0.00% of the adjusted pool balance as of the cut-off date and is expected to build to a target overcollateralization level equal to 0.25% of the adjusted pool balance as of the cut-off date. See “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Overcollateralization” in this prospectus.

Reserve Account

On the closing date, the reserve account will initially be funded by a deposit of proceeds from the sale of the notes in an amount not less than 0.25% of the adjusted pool balance as of the cut-off date.

On each payment date, after giving effect to any withdrawals from the reserve account, if the amount of cash on deposit in the reserve account is less than the specified reserve account balance, the deficiency will be funded by the deposit of available funds to the reserve account in accordance with the priority of payments described above. The “specified reserve account balance” will be, on any payment date while the notes are outstanding, 0.25% of the adjusted pool balance as of the cut-off date.

On each payment date, the indenture trustee will withdraw funds from the reserve account to cover any shortfall in the amounts required to be paid on that payment date with respect to clauses first through ninth under “Priority of Payments” above.

On each payment date, after giving effect to any withdrawals from the reserve account on that

payment date, any amounts of cash on deposit in the reserve account in excess of the specified reserve account balance for that payment date will constitute available funds and will be distributed in accordance with the priority of payments. See “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Reserve Account.”

Yield Supplement Overcollateralization Amount

The yield supplement overcollateralization amount, as calculated by the servicer, is a specified amount for each payment date based on a schedule determined as of the cut-off date.

As of the closing date, the yield supplement overcollateralization amount will equal $24,465,979.96, which is approximately 2.00% of the initial adjusted pool balance. The yield supplement overcollateralization amount for each payment date approximates the present value of the amount by which future payments on receivables with contract rates below a required rate of 5.00% are less than future payments would be on those receivables if their contract rates were equal to the required rate. The yield supplement overcollateralization amount will decline on each payment date. Because the receivables include a substantial number of low contract rate receivables, the receivables could generate less collections of interest than the sum of the amount necessary to pay the servicing fee, interest on the notes, fees, expenses and indemnification amounts required to be paid to the indenture trustee, the owner trustee and the asset representations reviewer and any required deposits into the reserve account if low contract rate receivables are not adequately offset by high contract rate receivables. The yield supplement overcollateralization amount is intended to compensate for low contract rates and is in addition to the overcollateralization referred to above.

See “The Transfer Agreements, the Servicing Agreement, the Administration Agreement and the Asset Representations Review Agreement —Credit and Cash Flow Enhancement—Yield Supplement Overcollateralization Amount” in this prospectus for more detailed information about the yield supplement overcollateralization amount.

Excess Interest

Because more interest is expected to be paid by the obligors in respect of the receivables than is

9

Table of Contents

necessary to pay the servicing fee, trustee fees, expenses and indemnity amounts (to the extent not otherwise paid by the servicer), asset representations reviewer fees, expenses and indemnity amounts (to the extent not otherwise paid by the sponsor), amounts required to be deposited in the reserve account, if any, and interest on the notes each month, there is expected to be “excess interest.” Any excess interest will be applied on each payment date as an additional source of available funds for distribution in accordance with “Priority of Payments” above.

On the closing date, Mayer Brown LLP, special federal tax counsel to the depositor and the issuing entity, will deliver its opinion, assuming compliance with the trust agreement, the indenture and certain other transaction documents, and subject to the assumptions and qualifications therein, to the effect that, for United States federal income tax purposes, the issuing entity will not be classified as an association or a publicly traded partnership taxable as a corporation, and the offered notes (other than any notes, if any, held by (A) the issuing entity or a person that beneficially owns more than 99% of the issuing entity for United States federal income tax purposes, (B) a member of an expanded group (as defined in Treasury Regulation Section 1.385-1(c)(4) or any successor regulation then in effect) that includes the issuing entity or a person beneficially owning a certificate, (C) a “controlled partnership” (as defined in Treasury Regulation Section 1.385-1(c)(1) or any successor regulation then in effect) of such expanded group or (D) a disregarded entity owned directly or indirectly by a person described in preceding clause (B) or (C)) will be characterized as debt for United States federal income tax purposes.

Each holder of a note, by acquiring a note or an interest therein, will agree to treat the note as indebtedness for federal, state and local income and franchise tax purposes.

We encourage you to consult your own tax advisor regarding the United States federal income tax consequences of the purchase, ownership and disposition of the notes and the tax consequences arising under the laws of any state or other taxing jurisdiction.

See “Material United States Federal Income Tax Consequences” in this prospectus.

CERTAIN CONSIDERATIONS FOR ERISA AND OTHER U.S. BENEFIT PLANS

Subject to the considerations described in “Certain Considerations for ERISA and Other U.S. Benefit Plans” in this prospectus, the offered notes may be purchased by employee benefit plans and other retirement accounts. An employee benefit plan, any other retirement plan and any entity deemed to hold “plan assets” of any employee benefit plan or other plan should consult with its counsel before purchasing the offered notes.

See “Certain Considerations for ERISA and Other U.S. Benefit Plans” in this prospectus.

The Class A-1 notes will be structured to be “eligible securities” for purchase by money market funds as defined in paragraph (a)(11) of Rule 2a-7 under the Investment Company Act of 1940, as amended (the “Investment Company Act”). Rule 2a-7 includes additional criteria for investments by money market funds, including requirements and clarifications relating to portfolio credit risk analysis, maturity, liquidity and risk diversification. If you are a money market fund contemplating a purchase of Class A-1 notes, you or your advisor should consider these requirements before making a purchase.

The transaction contemplated by this prospectus is intended to comply with the Federal Deposit Insurance Corporation regulatory safe harbor entitled “Treatment of financial assets transferred in connection with a securitization or participation” (the “FDIC Rule”). For more information, see “Risk Factors—FDIC receivership or conservatorship of CONA could result in delays in payments or losses on your notes” and “The Indenture—FDIC Rule Covenant” and “Material Legal Aspects of the Receivables—FDIC Rule.”

Pursuant to the SEC’s credit risk retention rules, 17 C.F.R. Part 246 (“Regulation RR”), CONA, as the sponsor, is required to retain an economic interest in the credit risk of the receivables, either directly or through a majority-owned affiliate. CONA intends to satisfy this obligation through the retention by CONA and/or one or more of its majority-owned affiliates (which for EU risk retention purposes will be a wholly-owned special purpose subsidiary of CONA)

10

Table of Contents

of an “eligible vertical interest” of at least 5% of each class of notes and the certificates to be issued by the issuing entity.

The retained eligible vertical interest will take the form of at least 5% of each class of notes and certificates issued by the issuing entity, though CONA and/or one or more of its majority-owned affiliates may retain more than 5% of one or more classes of notes or of the certificates. The material terms of the notes are described in this prospectus under “The Notes,” and the material terms of the certificates are described in this prospectus under “The Sponsor—Credit Risk Retention.

CONA does not intend to transfer or hedge the portion of its retained economic interest that is intended to satisfy the requirements of Regulation RR except as permitted under Regulation RR.

See “The Sponsor—Credit Risk Retention” in this prospectus.

CONA, as “originator,” will agree to retain a material net economic interest of not less than 5% in the securitization transaction described in this prospectus, in the form of retention of at least 5% of the nominal value of each of the tranches sold or transferred to investors in accordance with the text of option (a) of Article 6(3) of the EU Securitization Regulation. Initially, CONA intends to satisfy this obligation by holding at least 5% of the nominal value of each class of notes and by holding all the membership interest in the depositor (or one or more other wholly-owned special purpose subsidiaries of CONA), which in turn will retain at least 5% of the nominal value of the certificates. Each prospective investor is required, where relevant, to independently assess and determine the scope and applicability of the EU Retention Rules, and (if applicable) whether the agreement by CONA to retain an economic interest as described above, and the information provided in this prospectus or otherwise, are or will be sufficient for the purposes of such prospective investor’s compliance with the EU Retention Rules. None of CONA, the depositor, the issuing entity, the underwriters, the indenture trustee, their respective affiliates or any other party to the transactions described in this prospectus makes any representation that such agreement and such information are or will be sufficient for purposes of any person’s compliance with the EU Retention Rules. See “The Sponsor—EU Risk Retention” and “Legal Investment—

Requirements for Certain European Regulated Persons” in this prospectus.

CERTAIN VOLCKER RULE CONSIDERATIONS

The issuing entity will rely on an exclusion or exemption from the definition of “investment company” under the Investment Company Act contained in Section 3(c)(5) of the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” as defined in the final regulations issued December 10, 2013, implementing Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, commonly known as the “Volcker Rule”.

The depositor expects that each class of notes will receive credit ratings from one or more credit rating agencies hired by the sponsor to rate the notes (the “hired agencies”).

Although the hired agencies are not contractually obligated to monitor the ratings on the notes, we believe that the hired agencies will continue to monitor the transaction while the notes are outstanding. The hired agencies’ ratings on the notes may be lowered, qualified or withdrawn at any time. In addition, a rating agency not hired by the sponsor to rate the transaction or a particular class of notes may provide an unsolicited rating that differs from (or is lower than) the ratings provided by the hired agencies. A rating is based on each rating agency’s independent evaluation of the receivables and the availability of any credit enhancement for the notes. A rating, or a change or withdrawal of a rating, by one rating agency will not necessarily correspond to a rating, or a change or a withdrawal of a rating, from any other rating agency. See “Risk Factors—The ratings of the notes may be withdrawn or lowered, or the notes may receive an unsolicited rating, which may have an adverse effect on the liquidity or the market price of the notes” in this prospectus.

REGISTRATION UNDER THE SECURITIES ACT

The depositor has filed a registration statement relating to the notes with the SEC on Form SF-3. The depositor has met the registrant requirements contained in General Instruction I.A.1 to Form SF-3.

11

Table of Contents

Our affiliate, Capital One Securities, Inc., is participating in this offering as an underwriter. Accordingly, this offering is being conducted in compliance with the provisions of FINRA Rule 5121. Capital One Securities, Inc. is not permitted to sell the notes in this offering to an account over which it exercises discretionary authority without the prior specific written approval of the customer to which the account relates.

12

Table of Contents

An investment in the notes involves significant risks. Before you decide to invest, we recommend that you carefully consider the following risk factors.

| The notes may not be a suitable investment for you |

The notes are not a suitable investment for you if you require a regular or predictable schedule of payments or payment on any specific date. The notes are complex investments that should be considered only by investors who, either alone or with their financial, tax and legal advisors, have the expertise to analyze the prepayment, reinvestment, default and market risks, the tax consequences of an investment in the notes and the interaction of these factors. | |

| You must rely for repayment only upon the issuing entity’s assets, which may not be sufficient to make full payments on your notes |

Your notes are secured solely by the assets of the issuing entity. The sponsor, the servicer and the depositor are not obligated to make any payments to you on your notes and do not guarantee payments on the receivables. Further, neither the notes nor the receivables will be insured or guaranteed by the United States or any governmental entity. Distributions on any class of notes will depend on the amount and timing of payments and other collections in respect of the receivables and any credit enhancement for the notes and distributions from the reserve account. These amounts may not be sufficient to make full and timely distributions on your notes. If delinquencies and losses on the receivables create shortfalls which exceed the available credit enhancement, you may experience delays in payments due to you and you could suffer a loss. | |

| Repurchase obligations are limited, and do not protect the issuing entity from all risks that may impact the performance of the receivables |

The sponsor will make limited representations and warranties regarding the characteristics of the receivables to be transferred to the depositor, which will then transfer the receivables and assign the sponsor’s representations to the issuing entity. The sponsor will be obligated to repurchase from the issuing entity (as assignee of the depositor) a receivable if there is a breach of the representations or warranties regarding the eligibility of such receivable (and such breach is not cured and materially and adversely affects the interest of the issuing entity, the noteholders or the certificateholders in such receivable). Additionally, CONA, as servicer, will be obligated to repurchase from the issuing entity a receivable if the servicer makes certain modifications to the receivable or if the servicer breaches certain servicing covenants (and such breach is not cured and materially and adversely affects the interest of the issuing entity, the noteholders or the certificateholders in such receivable). However, the representations and warranties made by the sponsor are not a guarantee of performance and do not protect the issuing entity from all risks that could impact the performance of the receivables. Further, the representations and warranties are made as of the cut-off date or closing date, as applicable, | |

13

Table of Contents

| and are not ongoing representations or warranties with respect to the eligibility of the receivables. While the sponsor is obligated to repurchase any receivable if there is a breach of any of its representations and warranties or covenants regarding the eligibility of such receivable (but only if such breach is not cured and materially and adversely affects the interest of the issuing entity, the noteholders or certificateholders in such receivable), the sponsor may not be financially in a position to fund its repurchase obligation and you could suffer a loss. | ||

| Credit scores and historical loss experience may not accurately predict the likelihood of delinquencies, defaults and losses on the receivables |

Information regarding credit scores for the obligors under the receivables in the pool as of the cut-off date obtained at the time of acquisition from the originating dealer of their contracts is presented in “The Receivables Pool” in this prospectus. A credit score purports only to be a measurement of the relative degree of risk a borrower represents to a lender, i.e., that a borrower with a higher score is statistically expected to be less likely to default on its payment obligations than a borrower with a lower score. Neither the sponsor nor any other party makes any representations or warranties as to any obligor’s current credit score or actual performance of any motor vehicle receivable or that a particular credit score should be relied upon as a basis for an expectation that a receivable will be paid in accordance with its terms. | |

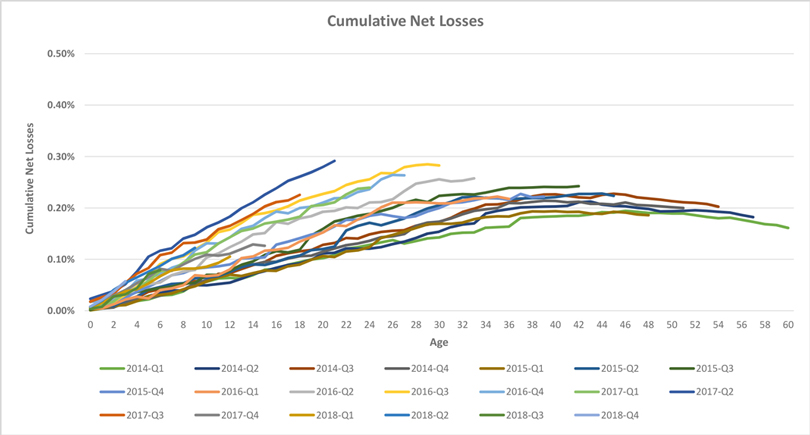

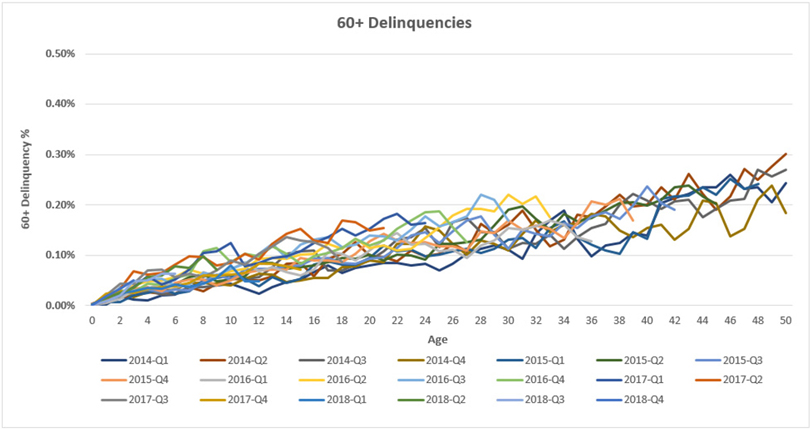

| Historical loss and delinquency information set forth in this prospectus under “The Receivables Pool” was affected by several variables, including general economic conditions and market interest rates, that are likely to differ in the future. Consequently, the net loss experience calculated and presented in this prospectus with respect to the sponsor’s managed portfolio of motor vehicle retail installment sale contracts categorized as “prime” and which are considered eligible for securitization in the Capital One Prime Auto Receivables (“COPAR”) program based on CONA’s internal scoring model may not reflect actual experience with respect to the receivables in the receivables pool. The sponsor has experienced variability (including increases) in delinquencies and repossessions on its motor vehicle receivables portfolio, which variability may continue. Additionally, the prices of used vehicles, including the prices at which the servicer is able to sell repossessed vehicles, are variable and can decline over periods of time, resulting in increased credit losses on defaulted receivables. In addition, future delinquency rates, rates of repossession, recovery rates on repossessed vehicles or loss experience of the servicer with respect to the receivables may be better or worse than that set forth in the static pool information and historical delinquency and loss information contained in this prospectus. | ||

14

Table of Contents

| The rate of depreciation of a financed vehicle could exceed the amortization of the outstanding principal amount of the related receivable, which may result in losses on the receivables |

The value of any financed vehicle may be less than the outstanding principal balance of the related receivable. For example, new vehicles normally experience an immediate decline in value after purchase because they are no longer considered to be new. As a result, it is highly likely that the principal balance of a receivable will exceed the value of the related financed vehicle during the early years of a receivable’s term. The lack of any significant equity in their vehicles may make it more likely that those obligors will default in their payment obligations if their personal financial conditions change. Defaults during these earlier years are likely to result in losses because the proceeds of repossession of the related financed vehicle are less likely to pay the full amount of interest and principal owed on the related receivable. Further, the frequency and amount of losses may be greater for receivables with longer terms because these receivables tend to have a somewhat greater frequency of delinquencies and defaults and because the slower rate of amortization of the principal balance of a longer term receivable may result in a longer period during which the value of the related financed vehicle is less than the remaining principal balance of the receivable. See “The Receivables Pool—Pool Stratifications” in this prospectus for the percentage of receivables with original terms greater than 72 months. None of the receivables will have an original term greater than 75 months. Additionally, although the frequency of delinquencies and defaults tends to be greater for receivables secured by used vehicles, loss severity tends to be greater with respect to receivables secured by new vehicles because of the higher rate of depreciation described above and the decline in used vehicle prices. Similarly, receivables with a higher loan-to-value ratio tend to have higher severity of loss. Furthermore, specific makes, models and vehicle types may experience a higher rate of depreciation and a greater than anticipated decline in used vehicle prices under certain market conditions including, but not limited to, the discontinuation of a brand by a manufacturer, material vehicle recalls or the termination of dealer franchises by a manufacturer. | |

| The pricing of used vehicles is affected by the supply and demand for those vehicles, which, in turn, is affected by consumer tastes, economic factors (including the price of gasoline), the introduction and pricing of new vehicle models and other factors, including the impact of vehicle recalls or the discontinuation of vehicle models or brands. Decisions by a manufacturer with respect to new vehicle production, pricing and incentives may affect used vehicle prices, particularly those for the same or similar models. Further, the insolvency of a manufacturer may negatively affect used vehicle prices for vehicles manufactured by that company. An increase in the supply or a decrease in the demand for used vehicles may impact the resale value of the financed vehicles securing the receivables. Decreases in the value of those vehicles may, in turn, reduce the incentive of obligors to make payments on the receivables and decrease the proceeds realized by the issuing entity from repossessions of financed vehicles. In any of the foregoing cases, the delinquency, repossession and credit loss figures, shown in the tables appearing under “The Receivables Pool—Delinquencies, | ||

15

Table of Contents

| Repossessions and Net Credit Losses” in this prospectus, might be a less reliable indicator of the rates of delinquencies, repossessions and losses that could occur on the receivables than would otherwise be the case. | ||

| You may experience delays in payments or losses on your notes resulting from a vehicle recall |

Obligors on receivables related to financed vehicles affected by a vehicle recall may be more likely to be delinquent in, or default on, payments on their receivables. Significant increases in the inventory of used motor vehicles subject to a recall may also depress the prices at which repossessed motor vehicles may be sold or delay the timing of those sales. If the default rate on the receivables increases and the price at which the related vehicles may be sold declines or if a recall delays the timing of sales, you may experience losses with respect to your notes. If any of these events materially affect collections on the receivables, you may experience delays in payments or losses on your notes. | |

| The geographic concentration of the obligors in the receivables pool and varying economic circumstances may increase the risk of losses or reduce the return on your notes |

The concentration of the receivables in specific geographic areas may increase the risk of loss. A deterioration in economic conditions in the states where obligors reside may adversely affect the ability and willingness of obligors to meet their payment obligations under the receivables and may consequently affect the delinquency, default, loss and repossession experience of the issuing entity with respect to the receivables of the obligors in such states. See “—The return on your notes may be reduced due to varying economic circumstances and/or an economic downturn.” As a result, you may experience payment delays and losses on your notes. An improvement in economic conditions could result in prepayments by the obligors of their payment obligations under the receivables. As a result, you may receive principal payments of your notes earlier than anticipated. No prediction can be made as to the effect of an economic downturn or economic growth on the rate of delinquencies, prepayments and/or losses on the receivables. See “—Your yield to maturity may be reduced by prepayments on the receivables, events of default, optional redemption of the notes or repurchases of receivables from the issuing entity.” | |