B E R M U D A I R E L A N D U N I T E D S T A T E S LLOYD’S Creating a World Class Specialty Insurer and Reinsurer Investor Presentation May 27, 2009 Filed by Max Capital Group Ltd. pursuant to Rule 425 under the Securities Act of 1933, as amended and deemed filed pursuant to Rule 14a-12 under the Securities and Exchange Act of 1934, as amended. Subject Company: Max Capital Group Ltd. (Commission File No.: 000-33047) |

2 INFORMATION CONCERNING FORWARD LOOKING STATEMENTS CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION This presentation includes statements about future economic performance, finances, expectations, plans and prospects of both IPC Holdings, Ltd. (“IPC”) and Max Capital Group Ltd. (“Max”) that constitute forward-looking statements for purposes of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to certain risks and uncertainties, including the risks described in the definitive joint proxy statement/prospectus of IPC and Max that has been filed with the Securities and Exchange Commission (“SEC”) under “Risk Factors,” many of which are difficult to predict and generally beyond the control of IPC and Max, that could cause actual results to differ materially from those expressed in or suggested by such statements. For further information regarding cautionary statements and factors affecting future results, please also refer to the most recent Annual Report on Form 10-K, Quarterly Reports on Form 10-Q filed subsequent to the Annual Report and other documents filed by each of IPC or Max, as the case may be, with the SEC. Neither IPC nor Max undertakes any obligation to update or revise publicly any forward-looking statement whether as a result of new information, future developments or otherwise. This presentation contains certain forward-looking statements within the meaning of the U.S. federal securities laws. Statements that are not historical facts, including statements about our beliefs, plans or expectations, are forward-looking statements. These statements are based on our current plans, estimates and expectations. Some forward-looking statements may be identified by our use of terms such as “believes,” “anticipates,” “intends,” “expects” and similar statements of a future or forward looking nature. In light of the inherent risks and uncertainties in all forward-looking statements, the inclusion of such statements in this presentation should not be considered as a representation by us or any other person that our objectives or plans will be achieved. A non-exclusive list of important factors that could cause actual results to differ materially from those in such forward-looking statements includes the following: (a) the occurrence of natural or man-made catastrophic events with a frequency or severity exceeding our expectations; (b) the adequacy of our loss reserves and the need to adjust such reserves as claims develop over time; (c) any lowering or loss of financial ratings of any wholly-owned operating subsidiary; (d) the effect of competition on market trends and pricing; (e) changes in general economic conditions, including changes in interest rates and/or equity values in the United States of America and elsewhere and continued instability in global credit markets; and (f) other factors set forth in the definitive joint proxy statement/prospectus of IPC and Max, the most recent reports on Form 10-K, Form 10-Q and other documents of IPC or Max, as the case may be, on file with the SEC. Risks and uncertainties relating to the proposed transaction include the risks that: the parties will not obtain the requisite shareholder or regulatory approvals for the transaction; the anticipated benefits of the transaction will not be realized; and/or the proposed transactions will not be consummated. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. We do not intend, and are under no obligation, to update any forward looking statement contained in this presentation. ADDITIONAL INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION AND WHERE TO FIND IT: This presentation relates to a proposed business combination between IPC and Max. On May 7, 2009, IPC and Max filed with the SEC a definitive joint proxy statement/prospectus of IPC and Max. This presentation is not a substitute for the definitive joint proxy statement/prospectus or any other document that IPC or Max may file with the SEC or send to their respective shareholders in connection with the proposed transaction. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DEFINITIVE JOINT PROXY STATEMENT/PROSPECTUS AND ALL OTHER RELEVANT DOCUMENTS FILED OR THAT WILL BE FILED WITH THE SEC AS THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION. All such documents, if filed, would be available free of charge at the SEC’s website (www.sec.gov) or by directing a request to IPC, at Jim Bryce, President and Chief Executive Officer, or John Weale, Executive Vice President and Chief Financial Officer, at 441-298-5100, in the case of IPC’s filings, or Max, at Joe Roberts, Chief Financial Officer, or Susan Spivak Bernstein, Senior Vice President, Investor Relations at 441-295-8800, in the case of Max’s filings. PARTICIPANTS IN THE SOLICITATION: IPC and Max and their directors, executive officers and other employees may be deemed to be participants in any solicitation of IPC and Max shareholders, respectively, in connection with the proposed business combination. Information about IPC’s directors and executive officers is available in the definitive joint proxy statement/prospectus filed with the SEC on May 7, 2009, relating to IPC’s 2009 annual meeting of shareholders; information about Max’s directors and executive officers is available in the amendment to its annual report on Form-10K, filed with the SEC on April 1, 2009. |

3 Why Shareholders Should Vote For The IPC / Max Merger Offers superior value to IPC / Max shareholders Compelling strategic combination Speed and certainty of closing – all regulatory approvals are in place Result of a thorough and robust process Max transaction and the Validus offer are NOT “either or" options |

4 Key Considerations Validus Hostile Takeover of IPC IPC / Max Merger Compelling strategic rationale Accretive to IPC book value Delivers greater book value to IPC shareholders Historical track record of strong risk management Better timing and certainty of completion Greater upside and long-term value creation Choice for IPC Shareholders – Vote to Approve Max Merger or NO Transaction |

5 IPC / Max – A World Class Specialty Company |

6 IPC’s Strategic Review – A Path to Superior Value Since its inception in 1993, IPC has successfully operated as a property catastrophe reinsurer Following KRW hurricane losses in 2005, IPC reevaluated its business model Rating agencies increased capital requirements for property catastrophe business Lowered premiums for a given amount of capital resulted in lower ROEs for monoline property catastrophe companies IPC’s Board reviewed strategic options to achieve superior shareholder value creation: Diversification beyond IPC’s monoline property catastrophe business to achieve more consistent earnings, a more efficient use of capital and higher returns on equity IPC’s Board determined a merger-of-equals was the best way to achieve its goals A comprehensive range of alternatives, including run-off and organic growth was actively considered A merger of equals preserves the value of IPC’s franchise in property catastrophe built over 15 years Max best achieved IPC’s goals and provided a clear path to create significant value IPC completed a thorough diligence process on Max |

7 Strong capital base with over $3 billion in equity and minimal leverage Greater size enhances “margin of safety” and financial flexibility A truly diversified, balanced global underwriting platform Strong and vibrant franchise serving both property & casualty markets Multiple operating platforms – Bermuda, Dublin, U.S. and Lloyd’s More efficient use of capital - $300 to $400 million of excess capital Increased ability to accelerate growth in a hardening market Both property & casualty markets currently provide attractive opportunities Strong and deep management and underwriting teams IPC/Max Creates A World Class Specialty Company An IPC/Max merger brings together the upside of the short-tail market and the stability of returns of long-tail business to create value for shareholders |

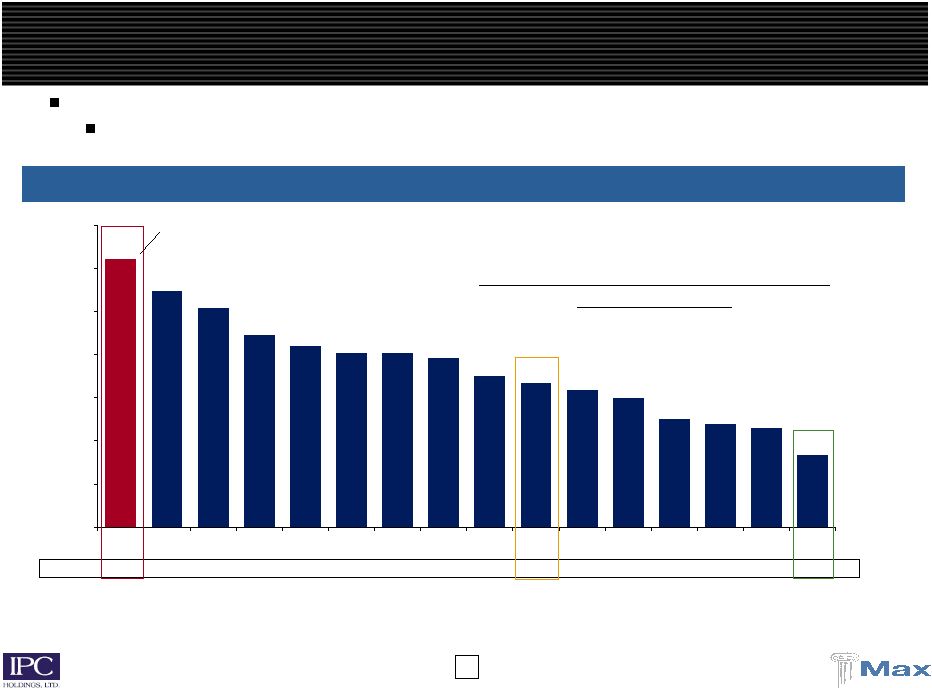

8 A Combination Creates Size and Scale Combination provides greater size and scale Enhances valuation and ratings profile Better positioning with clients and brokers Platform/underwriters are in place ____________________ (1) Includes RE, AXS, PRE, ACGL, TRH and RNR. (2) Includes ORH, AHL, AWH, ENH, VR, IPCR, PTP, MRH and MXGL. (3) Based on A.M. Best financial strength ratings. 12/31/2008 Company Equity 1 Everest Re $4,960 2 AXIS 4,461 3 PartnerRe 4,199 4 Arch Capital 3,433 5 Transatlantic 3,198 IPC + Max 3,131 6 RenaissanceRe 3,033 7 OdysseyRe 2,828 8 Aspen 2,779 9 Allied World 2,417 10 Endurance 2,207 11 Validus 1,939 12 IPC Holdings 1,851 13 Platinum Re 1,809 14 Montpelier Re 1,358 15 Max Capital 1,280 16 FlagstoneRe 986 17 Greenlight Capital 485 Average Price / Book Multiple 3-Year 2007 2008 Current Rating (3) > $3.0 billion of equity (1) 1.26x 1.39x 1.09x 0.93x A to A+ < $3.0 billion of equity (2) 1.04x 1.16x 0.89x 0.77x A- to A |

9 Strong Balance Sheet and Capital Base Combined (2) ____________________ (1) Investment portfolio includes cash. (2) Does not reflect GAAP purchase accounting adjustments. For more information, see the joint proxy statement/prospectus filed with the SEC by IPC on May 7, 2009. (3) Max corporate debt excludes $150 million of borrowings under primary credit facility, which were repaid in April 2009. Balance sheet strength and liquidity positions the combined company for future opportunities As of March 31, 2009 ($mm) Investment Portfolio (1) $2,190.0 $5,036.0 $7,225.9 Total Assets $2,453.1 $7,177.4 $9,630.5 Loss & LAE Reserves $354.5 $4,311.7 $4,666.2 Stockholders' Equity $1,849.5 $1,262.9 $3,112.3 Corporate Debt (3) $0.0 $91.4 $91.4 Total Debt / Capitalization 0.0% 6.7% 2.9% Investments / Equity 1.18x 3.99x 2.32x |

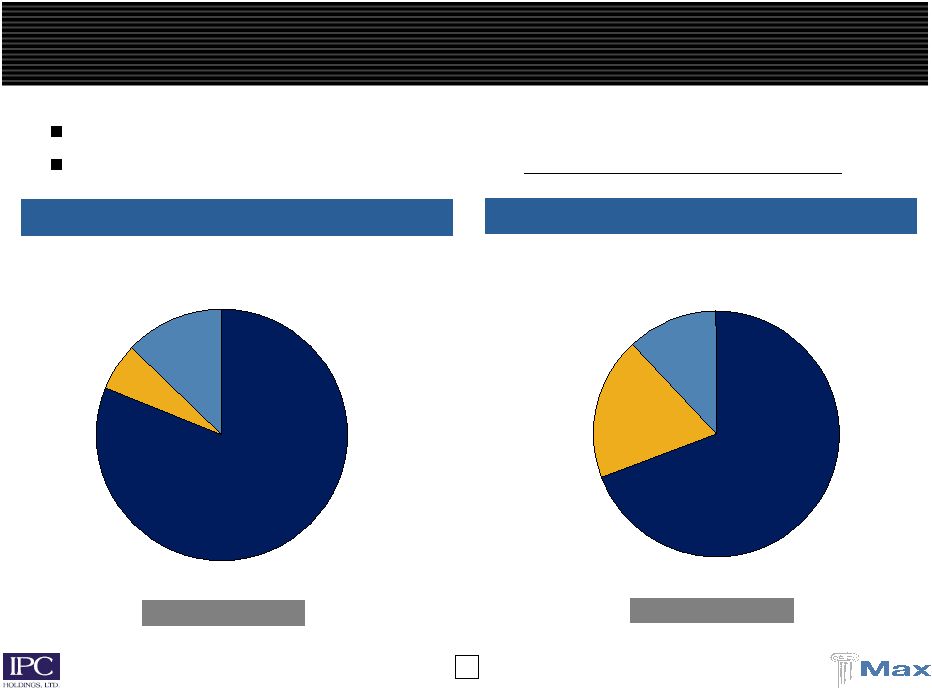

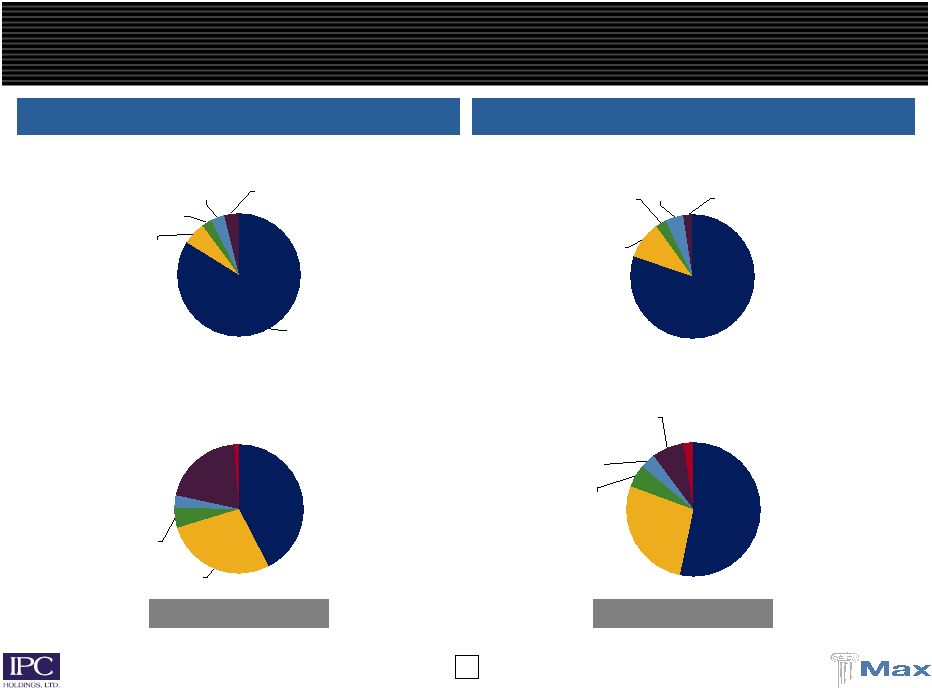

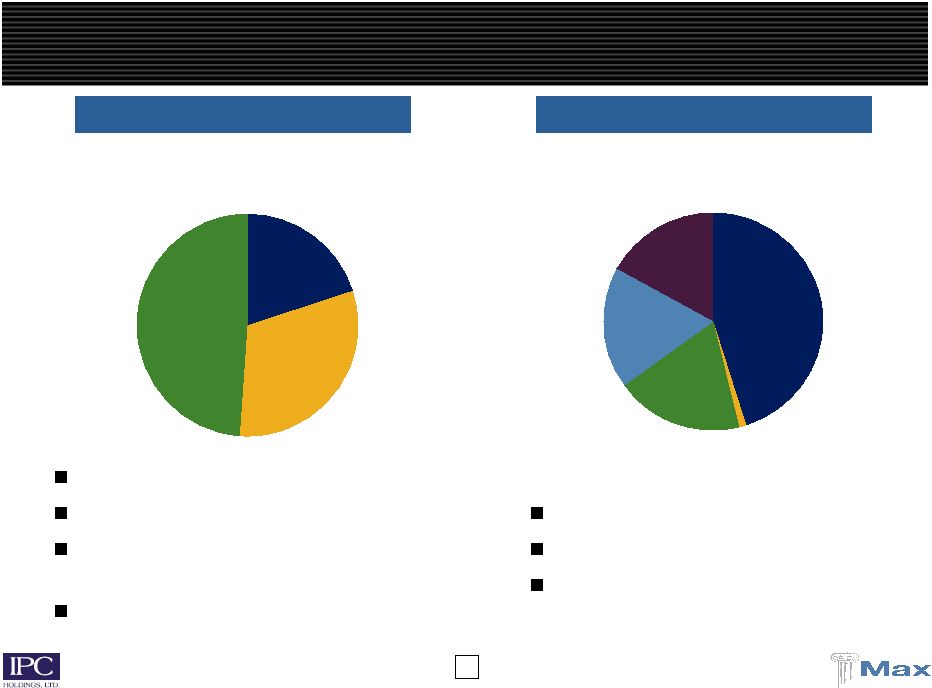

10 Fixed Income 81% Alternatives / Equities 13% Cash 6% 3/31/09 - $5.0 billion 3/31/09 - $2.2 billion IPC and Max Maintain a High Quality Investment Portfolio Max Capital IPC Holdings IPC and Max currently have similarly positioned investment portfolios Alternatives / equities of combined portfolio to be reduced to 5%-7% of total Fixed income 69% Cash 19% Alternative investments 12% |

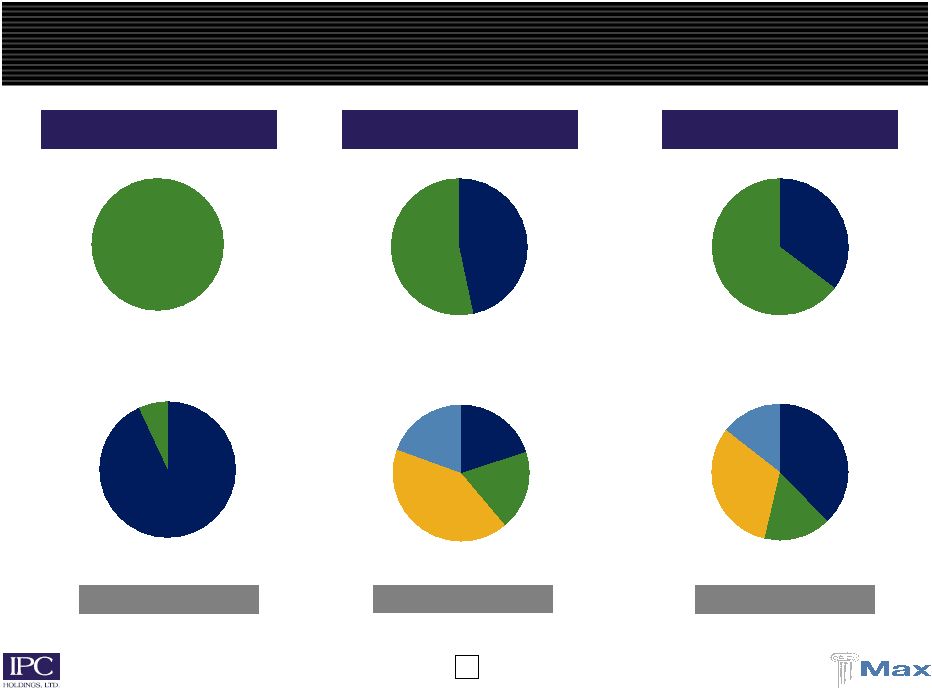

11 2008 GPW = $403 million Reinsurance Insurance 47% 53% Reinsurance Insurance 35% 65% 2008 GPW = $1,254 million 2008 GPW = $1,658 million Max Capital Combined Reinsurance 100% IPC Holdings A Truly Diversified Underwriting Platform Property / property cat Other short-tail 93% 7% Life & annuity Casualty long-tail Other short-tail Property / property cat 20% 19% 42% 19% Property / property cat Other short-tail Casualty long-tail Life & annuity 38% 16% 32% 15% |

12 Opportunistic Expansion in a Hardening Market A merger creates excess capital of $300 to $400 million through diversification Ability to profitably deploy capital for new business and capital management Total property / property catastrophe premiums of over $550 million Peak catastrophe risk (1 in 250 PML) presently targeted at 20% of capital Retentions on Max’s seasoned casualty insurance business expected to increase Lloyd’s expected to contribute approximately $150 million in gross premiums in 2009 ____________________ (1) Does not reflect GAAP purchase accounting adjustments. For more information, see the joint proxy statement/prospectus filed with the SEC by IPC on May 7, 2009. ($mm) Combined (1) 2008 GPW $403 $1,254 $1,658 2008 NPW $397 $840 $1,237 12/31/2008 Equity $1,851 $1,280 $3,131 NPW / Equity 0.21x 0.66x 0.40x |

13 Diversified Business = More Stable Underwriting Returns Each $1 of property catastrophe business requires as much capital as writing $2.5 to $3.0 of casualty business, depending on the class Aggregate underwriting profit is similar – but more stable results 50% to 60% combined ratio in property is equivalent to achieving a 80% to 87% combined ratio in casualty based on higher (2.5x - 3.0x) premium leverage Current casualty business written is in line with these underwriting levels Earnings enhanced by higher investment income due to longer duration of liabilities Capital to be opportunistically deployed to generate highest risk adjusted returns Segments of the casualty market currently offer attractive opportunities A diversified portfolio of risks allows capital to be deployed more efficiently Diversified mix of business = lower underwriting volatility and more efficient utilization of capital |

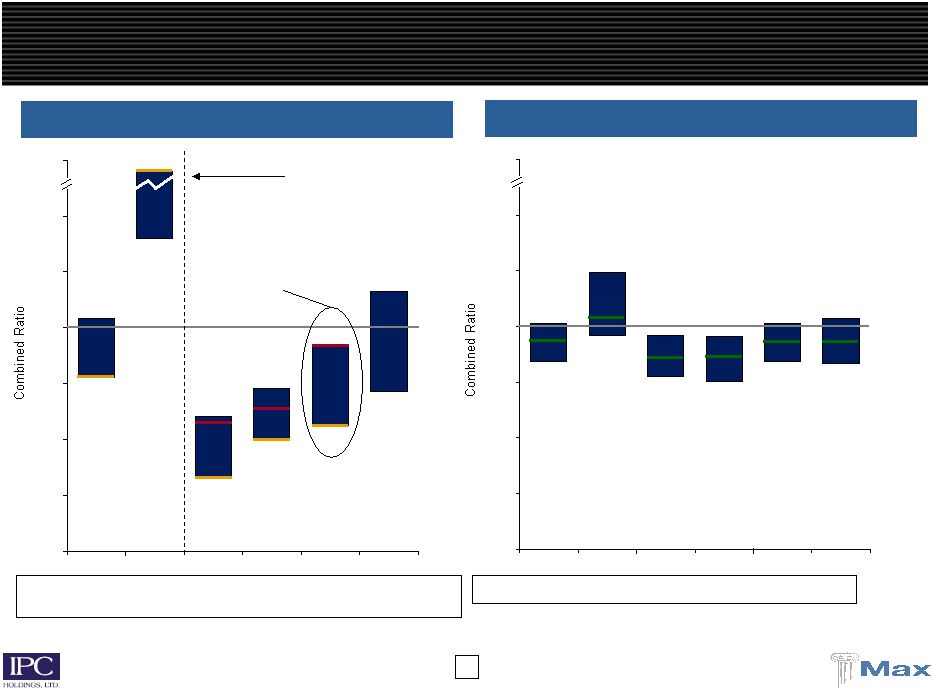

14 78% 140% 33% 50% 56% 71% 104% 252% 60% 73% 92% 116% 0% 25% 50% 75% 100% 125% 150% 300% 2004 2005 2006 2007 2008 Average 83% 84% 75% 77% 96% 84% 104% 101% 96% 96% 124% 102% 0% 25% 50% 75% 100% 125% 150% 300% 2004 2005 2006 2007 2008 Average ____________________ Source: Company filings. Property focused reinsurers include RNR, IPC, VR, MRH and FSR. Diversified reinsurers include RE, AXS, ACGL, TRH, PRE, ORH, AWH, ENH, AHL, PTP and MXGL. Validus had the worst combined ratio relative to its mono-line peers Validus began operations following Hurricanes Katrina, Rita and Wilma Diversified Platforms Generate More Consistent Margins Diversified Reinsurers Property Focused Reinsurers Validus has underperformed its peers over the last 3 years Median 94% 116% 85% 83% 94% 94% Max 94% 106% 86% 88% 92% 93% Median 78% 201% 55% 61% 89% 97% 68% IPC 78% 252% 33% 50% 56% 94% 46% VR 57% 62% 92% NA 70% 3 year Average |

15 Validus has significant volatility embedded in its underwriting operations Validus indicates its 1 in 250 year peak PML represents 33% of equity…whereas Validus lost 12.4% of its equity in Ike/Gustav, a 1:10-15 year event? Validus Has Significant Exposure to Catastrophes Ike/Gustav Ultimate Net Losses as a % of 6/30/08 Common Equity ($ in millions) 3.4% 12.4% 11.0% 10.1% 8.9% 8.4% 8.1% 8.1% 7.8% 7.0% 6.7% 6.3% 6.0% 5.0% 4.8% 4.6% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% VR FSR RNR MRH PTP ACGL AXS PRE AHL IPCR ENH ORH TRH AWH RE MXGL (1) (2) (2) (3) Losses $256 $140 $276 $140 $165 $287 $384 $305 $171 $135 $148 $155 $113 $257 $50 $170 ____________________ Source: Company filings as of 12/31/08. Losses are generally disclosed net of reinstatement premiums. (1) Results reflect Ike only. (2) Equity includes preferred, which subsequently converted to common. (3) TRH does not disclose specific losses but disclosed “$169.7 million principally relating to Hurricane Ike” or 5.0% of 6/30/08 common equity. VR increased its Ike reserves by 42% in Q4 2008 Validus had the greatest loss among its broad peer group |

16 The IPC / Max Superior Value Proposition |

17 Valuation is a Function of Book Value “Investors mostly look at insurance stocks on a price / book basis. The average price / book for our property /casualty stocks have ranged between 1.0 times to 2.0 times book.” - Bank of America Merrill Lynch, Industry Primer, February 20, 2009 “Why focus on book value? Book value, while largely meaningless for those investing in the stocks of many industries, is an important benchmark in valuing property-casualty related insurers for two reasons: (1) insurance is a promise and (2) book value provides stability in an industry setting where earnings can be volatile.” - Credit Suisse, Charles Gates, September 14, 2006 “[T]he per share ‘consideration’ to IPCRe shareholders from either deal will continue to change at any point in time as market pricing changes…Accordingly, we continue to believe that the value to IPC shareholders is a combination of their share in the pro forma tangible book value of the combined entity, and what the ultimate P/B valuation the market will afford the new entity (both are equally important).” - Dowling & Partners Securities, LLC May 22, 2009 As Validus states - “Diluted book value per common share is considered by management to be an appropriate measure of our returns to common shareholders, as we believe growth in our book value on a diluted basis ultimately translates into growth of our stock price” — Validus 2008 10-K, page 48 |

18 The IPC/Max Superior Value Proposition Combined business plan will provide more stable and enhanced returns Building on increased scale and diversification while retaining franchise value of property cat business Generation of $300 to $400 million of excess capital for deployment or capital management programs will increase ROE Ability to allocate capital to lines of business as and when opportunities arise Significant book value multiple expansion IPC and Max are both trading at discounts to current book values Resolution of current valuation pressures for IPC (monoline business model) and Max (alternative investment allocation) Larger cap, diversified companies trade at higher multiples than smaller cap, monoline companies The IPC/Max Combination Provides Significant Value Creation |

19 IPC / Max Offers Significant Value to Shareholders Valuation of IPC / Max Is Opportunistic Significant Value Creation — IPC Implied Price Per Share 0.77x 0.72x Max IPC +46% +56% +31% IPC / Max Delivers Higher ROE +55% 2009E – 2013E Average ROE (1) (1) ____________________ (1) Based on the "combined entity case 1" referred to in the joint registration statement/proxy of IPC and Max under the heading "The Amalgamation--Opinion of J.P. Morgan Securities Inc., Financial Advisor to IPC's Board”. Price / Book Value Per Share Prior to Merger (at 2/27/09) (1) (1) (1) $26 $28 $31 $41 $26.49 IPC Price 05/08/09 IPC Run-Off Case IPC Monoline Case IPC Organic Growth Case IPC/Max Combined 14% 11% IPC Monoline Case Combined |

20 The IPC / Max Merger Delivers Superior Value to IPC Delivers greater tangible book value per share and book value per share Max delivers book value accretion – Validus is dilutive Delivers a superior value creation opportunity Historical multiple implies a greater historical premium to IPC over time Market has not endorsed the Validus proposal Market is expecting the successful closing of the IPC / Max merger Equity research analysts support the IPC / Max merger IPC / Max merger is ready to close immediately after shareholder votes |

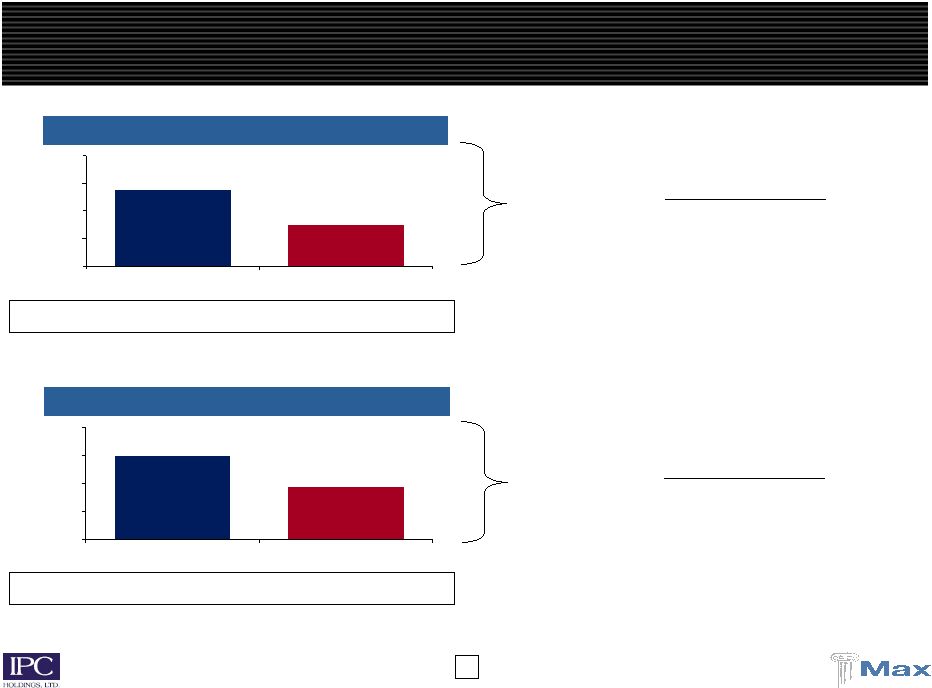

21 Max Provides IPC Shareholders More Value than Validus Diluted Tangible Book Value per IPC Share Diluted Book Value per IPC Share Max delivers 23% more value to IPC’s shareholders vs. Validus Max delivers 19% more value to IPC’s shareholders vs. Validus As of December 31, 2008 ____________________ Note : See appendix for book value per share calculations included herein. As a multiple of IPC 1.03x 0.84x As a multiple of IPC 1.06x 0.90x $27.44 $33.83 $20.00 $25.00 $30.00 $35.00 $40.00 Max Validus $34.93 $29.46 $20.00 $25.00 $30.00 $35.00 $40.00 Max Validus |

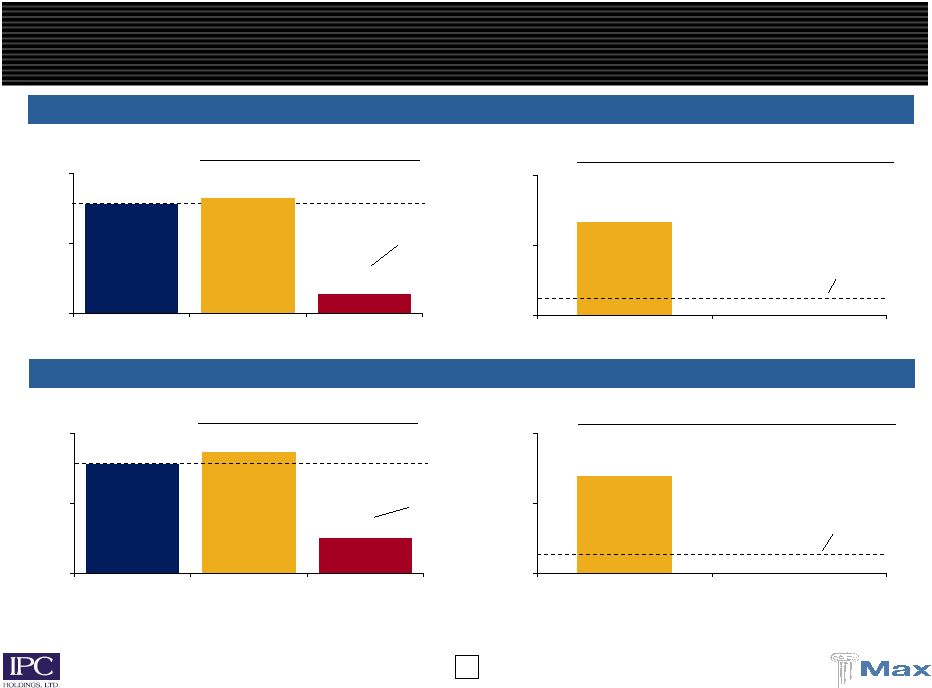

22 $27.55 $33.67 $32.85 $25.00 $30.00 $35.00 IPC Standalone Max Validus $31.67 $25.00 $30.00 $35.00 Max Validus $31.97 $25.00 $30.00 $35.00 Max Validus ____________________ Note: Validus book value includes the impact of $3.00 dividend per share to IPC shareholders. (1) Excludes purchase accounting adjustments and transaction expenses. For more information, see joint proxy statement/prospectus filed with the SEC by IPC on May 7, 2009. Max Transaction is Accretive to IPC – Validus is Dilutive Diluted Tangible Book Value per IPC Share (12/31/08) As a multiple of IPC 0.96x Pro Forma for PGAAP Combined (1) Diluted Book Value per IPC Share (12/31/08) As a multiple of IPC 0.97x Combined (1) Pro Forma for PGAAP ? ? As a multiple of IPC 1.03x 0.84x 19.6% dilutive to IPC As a multiple of IPC 1.01x 0.80x No higher than $26.10 No higher than $27.24 16.1% dilutive to IPC Less than 0.79x Less than 0.83x $26.41 $33.23 $32.85 $25.00 $30.00 $35.00 IPC Standalone Max Validus |

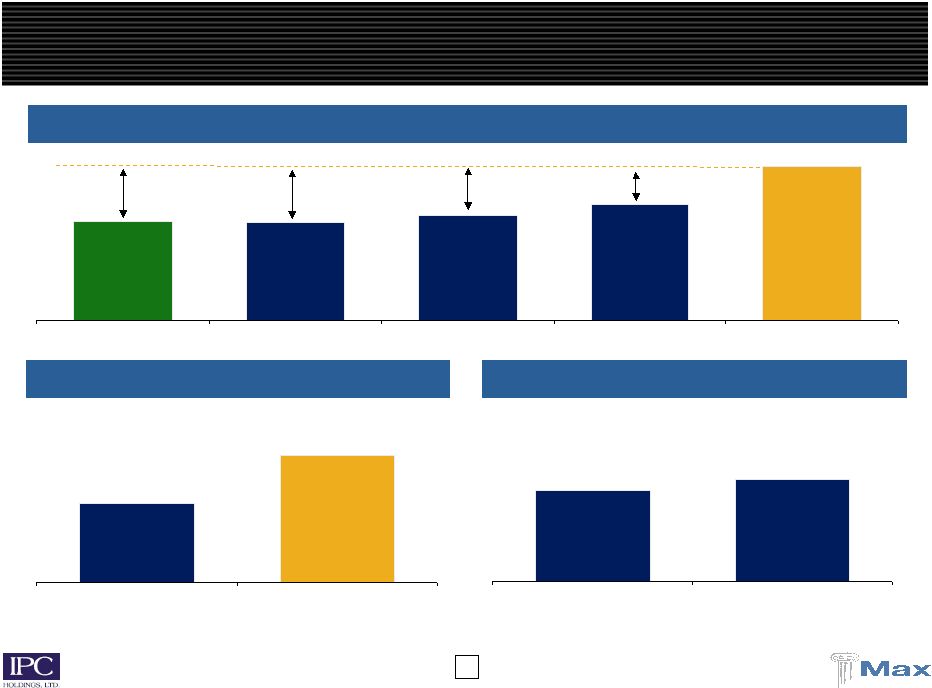

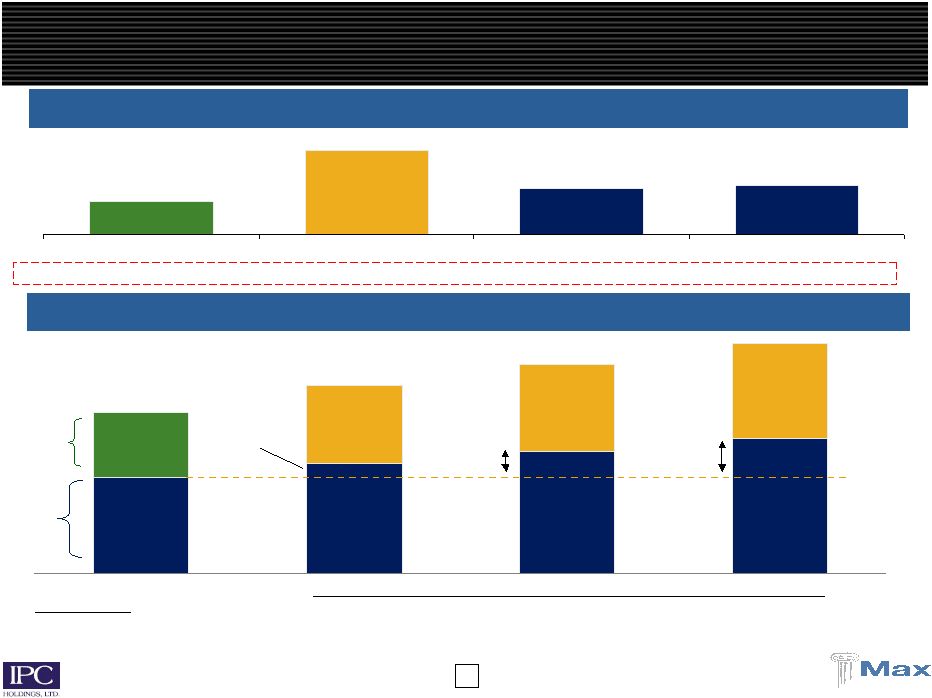

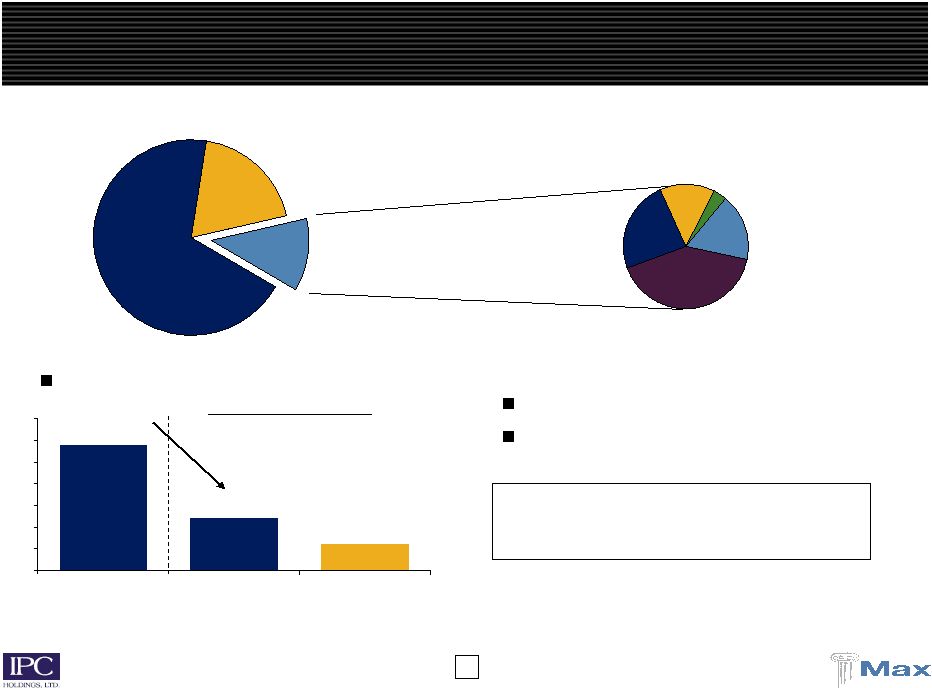

23 $925 $1,019 $1,280 $1,035 Implied Value At Announcement Book Value 60-Day Avg. 1-Year Avg. Combined Market Cap 0.90x 1.00x 1.10x IPC / Max Has Significant Upside Potential Max Offers a Diversified Franchise with Significant Upside (1) Value Creation Opportunity (2) P/B multiple: 0.72x 0.80x 0.81x Pro forma price to book value multiple Max IPC (3) $2,801 $3,112 $3,424 $2,395 $1,432 $25.35 / share $1,638 $29.00 / share $1,820 $32.22 / share $2,002 $35.45 / share $963 $1,163 $1,292 $1,421 Implied 0.77x PF multiple +14.4% +27.1% +39.8% (1) Based on share counts as of December 31, 2008, diluted using the treasury stock method with average prices as of February 27, 2009. (3) Based on share counts as of March 31, 2009, fully diluted with share prices as of May 21, 2009. (2) Does not reflect GAAP purchase accounting adjustments. |

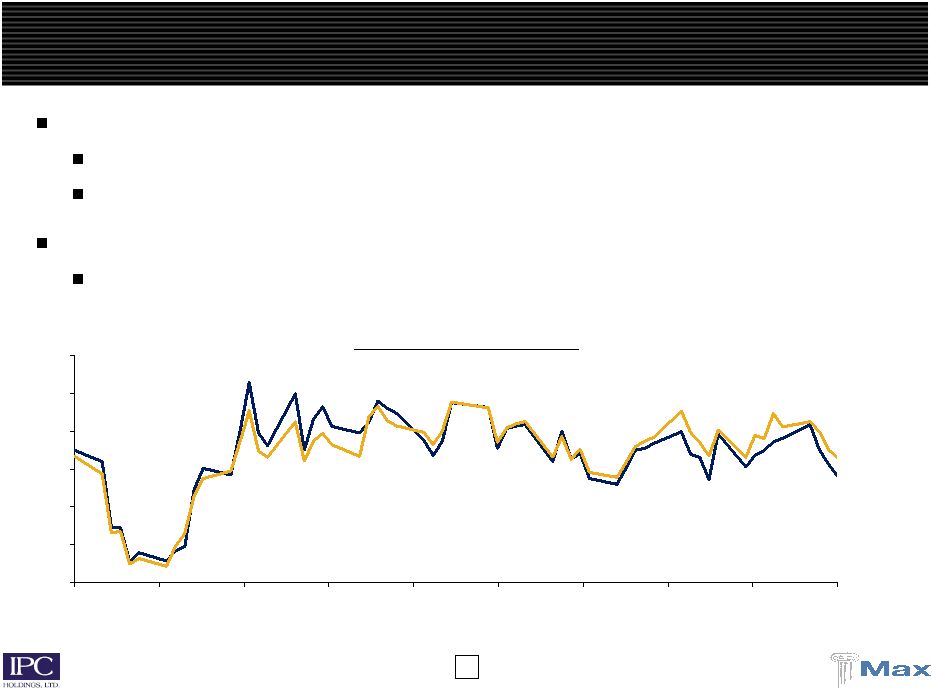

24 Max Offers a Higher Implied Price to IPC Shareholders ____________________ (1) Exchange ratio of 0.6429 IPC shares per Max share implies 1.5555 Max shares per IPC share. (2) Exchange ratio of 1.1234 Validus shares per IPC share plus $3.00 dividend per IPC share. Validus Average Max Average $10.0 $15.0 $20.0 $25.0 $30.0 $35.0 $40.0 $45.0 $50.0 7/25/07 10/7/07 12/20/07 3/3/08 5/16/08 7/29/08 10/11/08 12/24/08 3/8/09 5/21/09 Average Implied Price to IPC Since VR IPO 2007 2008 52-Week Max Capital (1) $35.34 $41.72 $35.61 $29.71 % Premium to IPC 28% 44% 27% 8% Validus (2) $29.07 $30.38 $28.32 $28.18 % Premium to IPC 5% 5% 1% 2% |

25 th The Market Has Not Endorsed Validus’ Hostile Proposal 3-Day VR Performance Following 03/30/09 Proposal 05/15/09 Proposal (5.7%) (7.5%) Validus’ stock under significant pressure after each hostile offer Massive underperformance against composite group Reasons are clear and simple – NO strategic element to the transaction Validus using its overpriced stock to achieve a “change of control” Revised offer now lower than original proposal (at time of announcement) Validus’ stock declined 7.5% on the 3 days following its May 15 proposal Downside risks to the trading value of Validus are significant Hurricanes Ike/Gustav demonstrated high risk nature of underwriting platform |

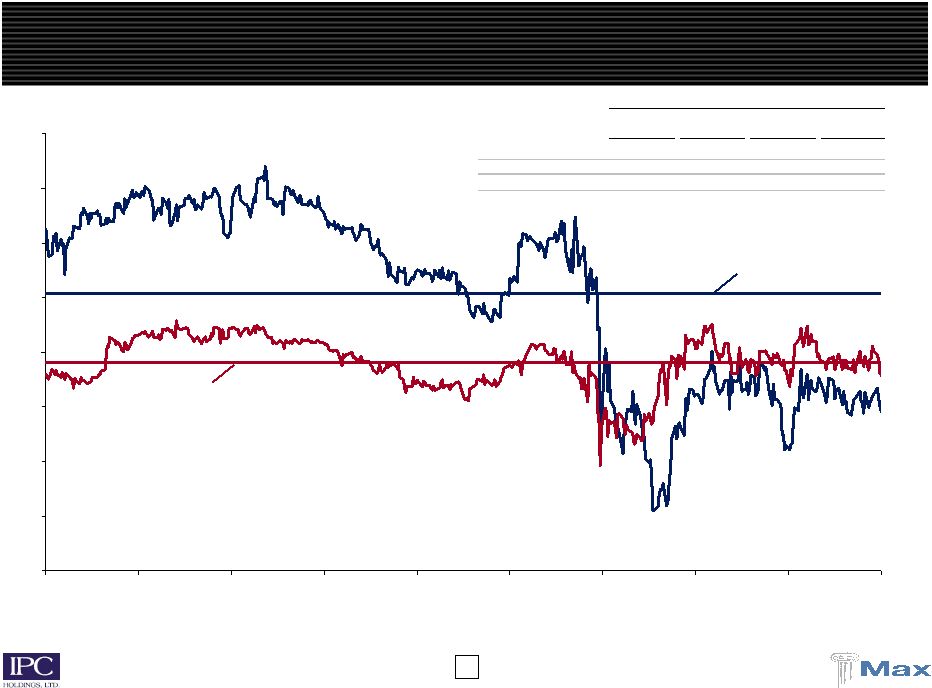

26 $13.00 $14.00 $15.00 $16.00 $17.00 $18.00 $19.00 2/27/09 3/8/09 3/17/09 3/26/09 4/4/09 4/14/09 4/23/09 5/2/09 5/11/09 5/21/09 The Market Expects the IPC / Max Merger to Close The market expects the IPC / Max merger to close when IPC shareholders vote on June 12 th Since the merger was announced, IPC and Max’s stock prices have traded in a narrow band Insurance investors understand that the IPC / Max merger makes strategic sense The market has rejected Validus’s hostile offer IPC and Max’s stock prices demonstrate that the market views Validus’ hostile offer as improbable Implied to Max (1) Max ____________________ (1) Implied to Max reflects an exchange ratio of 0.6429 IPC shares per Max share. Implied Deal Price to Max |

27 “An IPCR/MXGL merger has strategic advantages in our view including: 1) increased diversification, 2) ability to free up excess capital (est. at $300-$400mm) and 3) improved likelihood of ultimately achieving an A rating.” - Fox-Pitt Kelton Cochran Caronia Waller, Daniel Farrell April 7, 2009 Research Analysts Strongly Endorse the IPC / Max Merger “Max Capital’s management estimates the excess capital generated from the diversification credits of the combined entity at $300–400 million. The merged entity’s larger balance sheet and more diverse operations may provide more security and attract more business just as a flight to quality is prevailing among clients. We note that S&P placed Max Capital’s credit rating on CreditWatch with positive implications following the announced merger, citing the “creation of a larger and well- capitalized company, with a more diversified book of business… and reduced earnings/capital volatility.” - Citi, Joshua Shanker May 13, 2009 “We would support the IPC-Max deal. We believe the proposed deal makes sense and would create value for shareholders by virtue of its strong capital position and diversified business mix. We don’t believe 90% of shareholders will tender to the Validus offer and as such believe that rejecting the IPC-Max deal injects a considerable degree of uncertainty without necessarily creating additional value… Regardless of any other considerations, we believe this is the choice which offers shareholders the greatest certainty.” - RBC Capital Markets, Mark A. Dwelle May 13, 2009 “We do not like the potential IPCR merger for VR, as we believe the resulting combination would have too large a concentration of catastrophe exposed business (particularly heading into Atlantic Hurricane season), as well as increased investment risk and an uncertain rating agency reaction. We continue to believe that the IPCR/MXGL merger will be approved by IPCR shareholders when they vote in June.” - Keefe, Bruyette & Woods, Dean Evans May 5, 2009 |

28 IPC / Max Merger Is Ready to Close All regulatory approvals are in place - closing expected immediately after the June 12 th vote, prior to the 2009 hurricane season Completion Hart-Scott-Rodino Lloyd’s UK FSA Ireland Delaware Insurance Department Regulatory Approval Indiana Insurance Department A.M. Best Moody’s Joint Rating Agency Meetings Standard & Poor’s IPC lenders Credit Facilities Max lenders Proxy statement effective IPC shareholders June 12 th Shareholder Approvals Max shareholders June 12 th |

29 The Validus Proposal Is Not Superior |

30 IPC / Max - A Compelling Value Enhancing Transaction Validus Unsolicited Offer IPC / Max Validus’ private equity-dominated Board will control direction of the company – not always best for public shareholders Continued IPC Board representation ensures implementation of shared strategic vision Financially-driven transaction Strategically-driven transaction Validus does not intend to offer a role to IPC management despite IPC’s longstanding relationships and highly regarded underwriting culture Combined management team leverages skill sets from both IPC and Max Focus on short-tail lines that exhibited strong correlation when tested by hurricanes Ike and Gustav Diversified global platform provides flexibility to deploy capital opportunistically to take advantage of favorable markets Significant overlap would lead to excessive risk concentration and require a reduction in the property book Complementary businesses with limited overlap, combining IPC’s property cat expertise with Max’s diversified insurance and reinsurance platforms Compounding two large catastrophe exposed books would not lead to capital efficiencies and be viewed negatively by rating agencies Generates excess capital of $300 to $400 million to deploy in new businesses or for capital management purposes Validus does not value IPC’s franchise - views acquiring IPC as a way to raise capital at a deep discount to book value at the expense of IPC shareholders Preserves IPC’s property catastrophe franchise writing $550 million of property catastrophe premiums annually on a combined basis Hostile takeover with no intention to preserve IPC’s business Combined business plan developed jointly by the management of Max and IPC |

31 IPC / Max Has Certainty of Close — Validus Does Not Exchange Offer Scheme of Arrangement Amalgamation Offer Validus’ Hostile Offer Cannot Close Early in Hurricane Season And Hurricane Season Can Change Validus’ Plans Complex and time consuming “Offer” is highly conditional, resulting in substantial uncertainty for IPC shareholders Conditions include tender of 90% of IPC’s shares, which is impracticable IPC’s Bye - Laws prevent a single owner of 10% or more of IPC’s common shares Those who attempt to acquire more than 10% are subject to a voting cutback Unprecedented in Bermuda and never successful in England Not expected to be permitted by the Supreme Court of Bermuda Long process that requires multiple shareholder meetings Does not meet IPC’s strategic objectives – highly correlated risk concentration, – significant risk and uncertainty Value and terms are unacceptable to IPC – financial deal at a significant discount to book – IPC would need to perform diligence on Validus offer IPC needs satisfactory ratings agency feedback to continue serving its clients |

32 IPC / Max Merger Is The Result Of A Thorough Process |

33 Max Transaction Result of A Thorough and Robust Process The merger with Max resulted from a lengthy and careful process where the IPC Board considered organic growth, and a possible combination with a significant number of counterparties, including some who were invited to submit proposals and others that approached IPC IPC established a Business Development Committee IPC engaged J.P. Morgan to assist with the strategic review process in determining whether to pursue an organic growth plan or a business combination IPC reviewed a broad list of potential counterparties, including Validus IPC authorized J.P. Morgan to contact a select number of potential counterparties IPC also received inbound calls from various parties, some of whom were invited in the process IPC entered into confidentiality and standstill agreements with eight potential counterparties, including Max IPC engaged in discussions with six potential counterparties, including Max, and for formal merger proposals IPC received four written proposals and one oral proposal IPC decided to pursue further discussions with three potential counterparties IPC developed counter proposals IPC engaged in detailed negotiations and diligence with Max and another potential counterparty, which included the development of combined business plans IPC determined that pursuing exclusive discussions with Max would be in its best interest IPC and Max engaged in additional due diligence and finalized negotiations before executing the amalgamation agreement January 29 — March 1, 2009 January 2009 December 2008 November — December 2008 October — November 2008 Early 2008 2007 |

34 Four Month Due Diligence Process November – December 2008: exchanged non-public information and engaged in discussions January 2009: IPC and its outside advisors engaged in due diligence on threshold items Outside advisors – (i) independent consulting firm, (ii) independent investment advisory firm, (iii) independent accounting firm, (iv) J.P. Morgan as financial advisor, (v) Sullivan & Cromwell and Mello Jones & Martin as legal advisors Key due diligence items included Evaluation of management Valuation and liquidity of Max’s investment portfolio Loss reserves Ability to manage the initial aggregation of catastrophe risk Enterprise risk management Collectability of ceded reinsurance Accounting Information technology Change in control provisions Pending litigation and claims and other contingencies February 2009: Continued IPC’s detailed due diligence investigation into Max on an exclusive basis As a result of the due diligence process, IPC was able to gain comfort with Max as an amalgamation partner and build a combined business plan |

35 Consideration of Validus in the Process In early October 2008, IPC selected 12 parties who were most likely to satisfy IPC’s strategic objectives, and excluded those that IPC believed were not appropriate potential counterparties Although IPC had previously identified Validus as a potential counterparty because of its similar size to IPC, after careful consideration IPC did not include Validus in its select list of potential counterparties to contact because of the following: Validus’s catastrophe exposure Level of Validus’s goodwill and intangible assets Validus’s relative lack of seasoning as compared to other alternatives, given its formation in 2005 and acquisition of substantial assets in 2007 Other parties that had not been included on the initial list of selected potential counterparties contacted IPC, and the Company’s board considered every credible proposal On November 3, 2008, IPC received an unsolicited proposal from a large, publicly-traded insurance company proposing that IPC and the company enter into an exclusivity agreement to discuss an acquisition of IPC in a stock-for-stock transaction. As the proposal was based on an unsatisfactory valuation of IPC’s book value and was subject to detailed due diligence, IPC’s board of directors declined to grant exclusivity but invited the company to participate in the process. The counterparty declined Another company contacted IPC and made a business case to be included in the process. IPC agreed and held discussions with that counterparty over several months until it entered into an exclusivity agreement with Max IPC also received unsolicited indications of interest from parties referred to as Party H and Party I in the proxy statement, and met with and received a formal proposal from Party K |

36 Diversification beyond IPC’s monoline property catastrophe business to achieve, consistent long-term earnings and higher returns on equity Excess capital of $300 to $400 million to deploy in new businesses or for capital management purposes Diversify to Improve Earnings and Returns Increased flexibility to deploy capital opportunistically to take advantage of favorable pricing and underwriting developments across a greater number of business lines and regions Highly Complementary Businesses Limited overlap between IPC’s strength in property catastrophe reinsurance and Max’s diversified insurance and reinsurance platforms Preserve IPC’s Existing Franchise Value Maintain position as leading property catastrophe reinsurer writing over $550 million of property catastrophe premiums annually, on a combined basis Increased Scale and Scope Approximately $3 billion of capital, providing a larger buffer to protect IPC’s capital from catastrophe events and enhancing IPC’s ability to achieve better ratings Increase Management Depth Top-notch management team with a proven ability to manage a more diversified business, led by Marty Becker Max Transaction In-Line with IPC’s Strategic Objectives Significant Shareholder Value Creation Both IPC and Max are at historical low trading valuation and currently at a discount to book value Larger, more diversified companies typically trade at a higher multiple |

37 IPC Strategic Objectives are Complementary to Max IPC allows Max to accelerate its build out Max provides IPC with real diversification IPC adds high quality property catastrophe reinsurance franchise Capital to support growth of Max’s well established and diversified platforms Ability to increase retentions on Max’s business and expand capacity where appropriate Adds size and scale to both companies at a time when cost of capital is at a relative high point Similar transaction valuations allows both shareholders to be fairly rewarded Deal protections designed to reflect planned “merger-of-equals” rather than a “change in control” Max considered other diversification alternatives but did not conduct a process |

38 Why Shareholders Should Vote For The IPC / Max Merger Compelling strategic combination Leading specialty insurance/reinsurance business Global platform with enhanced size and scale Diversification into complementary and non-correlated business lines Well established, entrepreneurial management team Offers significant value to shareholders Speed and certainty of closing Result of a thorough and robust process The Max transaction and the Validus offer are NOT “either or" options Choice for IPC Shareholders – Vote to Approve Max Merger or NO Transaction Closing expected immediately after the June 12 th shareholder vote, before hurricane season |

39 Appendix - Overview of IPC |

40 Reinsurance Industry Overview Reinsurance is a form of insurance for insurance companies Allows clients to transfer risk to the reinsurance market and more efficiently manage capital Reinsurer’s obligation is to the insurance company not the policyholder Insurance company inherently assumes some degree of credit risk Reinsurers principally generate income through underwriting and investment income Coverage provided across diverse business lines Coverage includes “short-tail” lines such as property cat and “long-tail” lines such as general liability The “tail” refers to the amount of time until a claim is paid Long-tail reinsurers generally have higher investment leverage as invested assets grow Short-tail reinsurers can have significant earnings volatility due to property cat exposure Bermuda is on of the world's largest reinsurance centers |

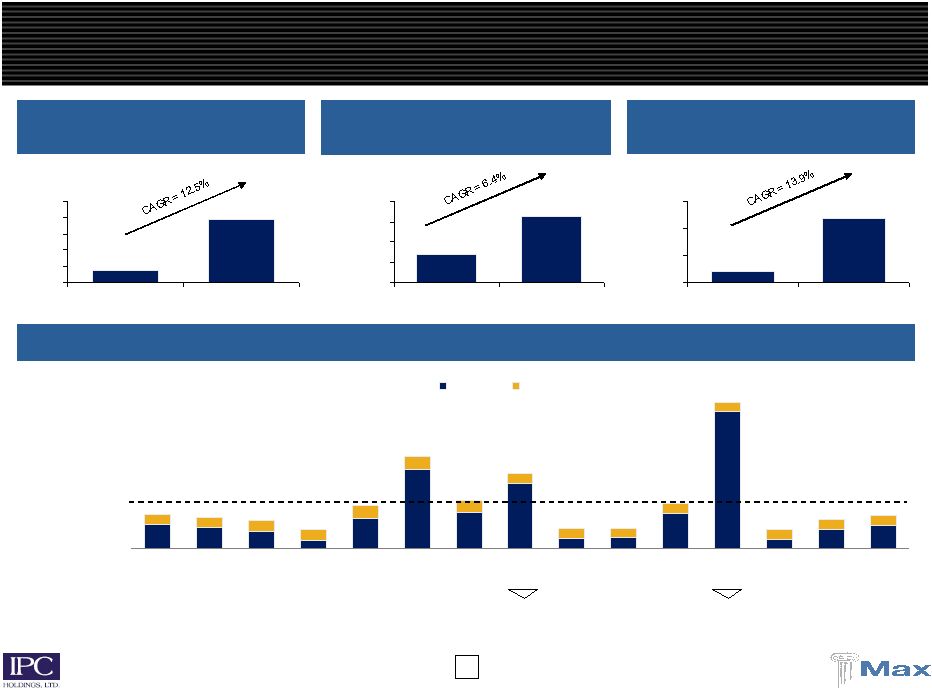

41 Established in 1993, sponsored by AIG, listed on Nasdaq since 1996 Focused on property catastrophe reinsurance Majority written on an excess of loss basis for primary insurers rather than reinsurers Subject to aggregate limits on exposure to losses Approximately 258 clients during 2008 (36% U.S.-based), including many of the leading insurance companies around the world No single ceding insurer accounted for more than 3.7% of GPW, excluding reinstatement premiums IPC Overview ($mm) 2007 2008 Gross premiums written $404.1 $403.4 Net premiums earned 391.4 387.4 Net income (Loss) $385.4 $90.4 Operating earnings per common share (diluted) $4.56 $4.36 Assets $2,627.7 $2,388.7 Shareholders’ equity 2,125.7 1,850.9 Book value per share (diluted) $32.42 $32.85 Operating return on average common equity 15.4% 13.0% Loss & LAE ratio 31.9% 40.2% Expense ratio 18.0% 16.2% Combined ratio 49.9% 56.4% A.M. Best FSR rating (outlook) A (Neg) A (Neg) Standard & Poor’s FSR rating (outlook) A- (Stable) A- (Stable) |

42 Europe 28% U.S. 53% Australasia 3% Worldwide 8% Japan 6% Other 3% U.S. 42% Australasia 3% Worldwide 21% Other 1% Japan 5% Europe 28% Catastrophe 80% Retro 10% Risk Excess 3% Aviation 5% Other 2% Other 4% Aviation 4% Risk Excess 3% Retro 6% Catastrophe 84% Established and Consistent Business Risk type 2003 2008 Risk type Geography Geography ____________________ (1) Excludes reinstatement premiums GPW (1) = $315.5 million GPW (1) = $370.9 million |

43 42 36 29 13 51 136 62 112 17 18 61 237 15 32 40.2 17 17 19 20 23 24 21 18 17 17 17 15 18 18 16.2 59% 54% 48% 33% 74% 160% 83% 129% 34% 35% 78% 252% 33% 50% 56.4% 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 Loss ratio Expense ratio IPC Performance NPE growth ($mm) Book value per share growth (1) Asset growth ($mm) $74.7 $387.4 $0 $100 $200 $300 $400 $500 1994 2008 $13.76 $32.85 $0.0000 $10.0000 $20.0000 $30.0000 $40.0000 1994 2008 $387.0 $2,388.7 $0 $1,000 $2,000 $3,000 1994 2008 ____________________ (1) Represents diluted book value per common share. (2) Calculated as net income (loss), available to common shareholders divided by the average common shareholders’ equity (excluding convertible preferred shares). Underwriting performance WTC: $116mm loss Hurricanes Katrina, Rita, Wilma: $977mm loss 20% 24% (38%) 9% 18% 17% (1%) 8% 1% 12% 20% 20% 19% ROAE² Average loss ratio 60.1% Average expense ratio 18.5% 15% 4% Average combined ratio 78.5% |

44 Appendix - Overview of Max Capital |

45 Global underwriter of specialty insurance and reinsurance Multiple operating platforms - Bermuda, Dublin, United States, and Lloyd’s Diversified business profile across specialty classes of business Highly experienced management with proven track record Opportunistic and disciplined underwriting strategy Analytical and quantitative underwriting orientation 5 year average combined ratio, with cats, of 93% Strong, liquid balance sheet with conservative reserving track record Gross premiums written (2008) of $1.3 billion and 3/31/09 equity of $1.3 billion Prudent capital management - $305 million in dividends/repurchases over last 5 years Significant expansion of underwriting platforms with minimal goodwill High quality investment portfolio repositioned to reflect traditional underwriting base Alternative investments are now a much smaller part of Max’s asset base at 11.9% and are to be reduced to 5% to 7% Max has evolved and repositioned itself since its formation in 1999 Overview of Max Capital Short-Tail Long-Tail 62% 38% Insurance Reinsurance 53% 47% |

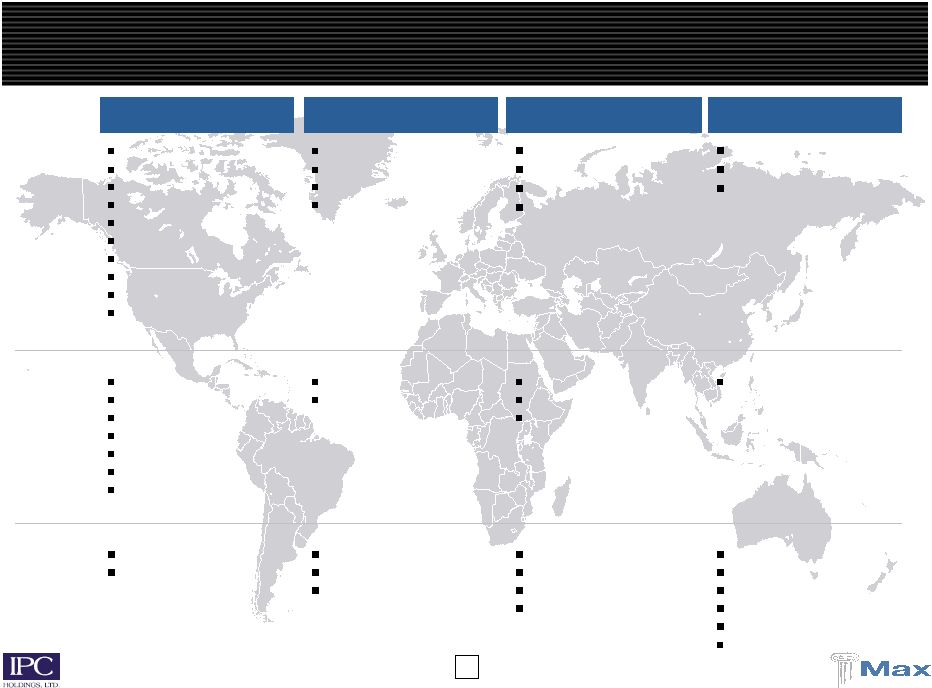

46 Global Reach Through Established Platforms Bermuda / Dublin Reinsurance Bermuda / Dublin Insurance Lloyd’s U.S Specialty Insurance Major Classes Agriculture Aviation Excess liability Medical malpractice Professional liability Property Marine and energy Whole account Workers’ comp Life and annuity Aviation Excess liability Professional liability Property Personal accident Financial institutions Professional liability Property General liability Marine Property Operating Regions United States Latin America Canada European Union Japan Australia New Zealand United States European Union United Kingdom Japan Denmark United States Offices Bermuda Dublin Bermuda Dublin Hamburg London Leeds Tokyo Copenhagen New York Philadelphia Richmond Atlanta Dallas San Francisco |

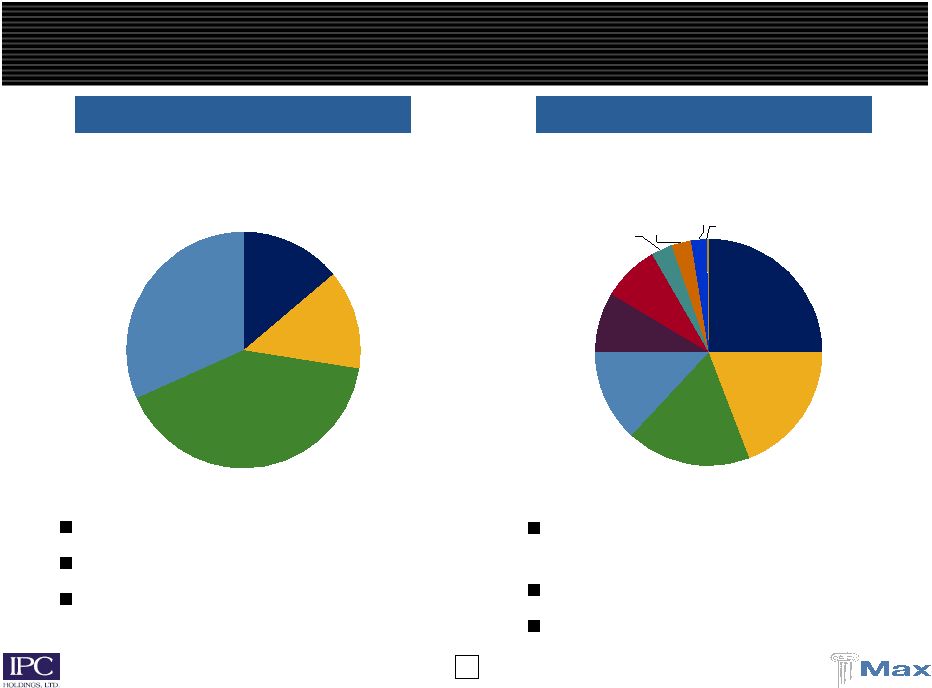

47 Max Has a Strong Market Position in Specialty Classes … Working layer excess business Focus on Fortune 1000 customers 2008 combined ratio = 88% 2008 GPW - $389 million 2008 GPW - $420 million Bermuda / Dublin Insurance Bermuda / Dublin Reinsurance Working layer excess / quota share business Cross class capability 2008 combined ratio = 87% Excess Liability Professional Liability Aviation Property 14% 14% 41% 32% Other General Liability Marine & Energy Whole Account Aviation Prof. Liabliity Workers Comp Med. Mal. Agriculture Property 25% 19% 18% 13% 9% 8% 3% 3% |

48 … With an Attractive Position in the U.S. Market and Lloyd’s Launched in 2007 Nationwide niche E&S underwriter Growing into expense base – target combined ratio of 85% to 90% Expected GPW of $250 million in 2009 2008 GPW - $194 million 2008 GPW - £65 million (1) U.S. Insurance Max at Lloyd’s Acquired in November 2008 Direct and reinsurance Expected GPW of $150 million in 2009 ____________________ (1) GPW reflects full year of business, which includes periods prior to the acquisition by Max. Marine General Casualty Property 20% 31% 49% Accident & Health Fin. Institutions Prof. Indemnity / Med. Mal. Employers' Public Liability Property Treaty 45% 1% 19% 18% 17% |

49 As % of Total Investments Max Investment Portfolio Highlights ____________________ (1) Peers include: IPCR, PRE, ORH, ACGL, RE, RNR, MRH, ENH, TRH, AXS, AWH, PTP, VR, AHL, FSR, and GLRE. Peer average represents 3/31/09 allocation of preferred / equities and “other investments” as % of total investments. Alternatives allocation is decreasing Alternative investments 12% Cash 19% Fixed income 69% Long / Short funds 41% Opportunistic 3% Distressed Securities 14% Arbitrage strategies 24% Emerging / Global Markets 18% 5%-7% 12% 29% 0% 5% 10% 15% 20% 25% 30% 35% Max 12/31/05 Max 3/31/09 Target Market neutral / absolute return focus Max alternatives in line with Bermuda peers Max / IPC alternatives target = 5%-7% Peer group (1) (average) = 10% |

50 Appendix - Book Value Calculations |

51 Calculation of Combined Book Value Per Share (IPC / Max) As of December 31, 2008 Combined (a) (per IPC share) Max IPC Value Delivered by Max per IPC Share (0.6429) 2.5% accretive to IPC 1.2% accretive to IPC ____________________ (a) “Combined” figures exclude impact of purchase accounting adjustments. Shares outstanding Basic shares 55,855,103 (7) 55,805,790 (10) 35,877,542 91,732,645 Warrants (net) 0 635,728 (11) 408,710 408,710 Stock options (net) 18,608 (8) 120,685 (12) 77,589 96,197 Restricted stock awards 474,987 (8) 447,195 (12) 287,502 762,489 Diluted shares outstanding (1) 56,348,698 57,009,398 36,651,342 93,000,040 Book value per share Shareholders' equity $1,850,947 (9) $1,280,331 (13) $1,280,331 $3,131,278 Book value per share (2) $33.14 $22.94 $35.69 $34.13 Diluted book value per share Shareholders' equity $1,850,947 (9) $1,280,331 (13) $1,280,331 $3,131,278 Proceeds from exercise of Warrants and stock options (3) 0 0 0 0 Diluted book value $1,850,947 $1,280,331 $1,280,331 $3,131,278 Diluted book value per share (4) $32.85 $22.46 (14) $34.93 $33.67 Tangible book value per share Shareholders' equity $1,850,947 (9) $1,280,331 (13) $1,280,331 $3,131,278 Goodwill and other intangible assets 0 (40,488) (15) (40,488) (40,488) Tangible shareholders' equity $1,850,947 $1,239,843 $1,239,843 $3,090,790 Tangible book value per share (5) $33.14 $22.22 $34.56 $33.69 Diluted tangible book value per share Diluted book value $1,850,947 $1,280,331 $1,280,331 $3,131,278 Goodwill and other intangible assets 0 (40,488) (15) (40,488) (40,488) Diluted tangible book value $1,850,947 $1,239,843 $1,239,843 $3,090,790 Diluted tangible book value per share (6) $32.85 $21.75 $33.83 $33.23 |

52 Calculation of Combined Book Value Per Share (IPC / VR) As of December 31, 2008 Validus IPC Termination Fee Combined (b) (per IPC share) 16.1% dilutive to IPC 19.6% dilutive to IPC ____________________ (a) In order to place figures on a comparative basis, “combined” figures are shown per share of IPC by converting the exchange ratio of 1.1234 VR shares per IPC share to 0.8902 (1 ÷ 1.1234) IPC shares per VR share, including the impact of $3.00 per share of cash consideration. (b) “Combined” figures exclude impact of purchase accounting adjustments. Value Delivered by VR per IPC Share (1/1.1234) (a) Shares outstanding Basic shares 55,855,103 (7) 75,624,697 (16) 67,317,694 123,172,797 Warrants (net) 0 2,856,884 (16) 2,543,069 2,543,069 Stock options (net) 18,608 (8) 848,758 (16) 755,526 774,134 Restricted stock awards 474,987 (8) 2,986,619 (16) 2,658,553 3,133,540 Diluted shares outstanding (1) 56,348,698 82,316,958 73,274,842 129,623,540 Book value per share Shareholders' equity $1,850,947 (9) $1,938,734 (16) $1,769,744 $(50,000) $3,570,691 Book value per share (2) $33.14 $25.64 $26.29 $28.99 Diluted book value per share Shareholders' equity $1,850,947 (9) $1,938,734 (16) $1,769,744 $(50,000) $3,570,691 Proceeds from exercise of Warrants and stock options (3) 0 0 0 0 Diluted book value $1,850,947 $1,938,734 $1,769,744 $(50,000) $3,570,691 Diluted book value per share (4) $32.85 $23.55 $24.15 $27.55 Tangible book value per share Shareholders' equity $1,850,947 (9) $1,938,734 (16) $1,769,744 $(50,000) $3,570,691 Goodwill and other intangible assets 0 (147,610) (17) (147,610) (147,610) Tangible shareholders' equity $1,850,947 $1,791,124 $1,622,134 $(50,000) $3,423,081 Tangible book value per share (5) $33.14 $23.68 $24.10 $27.79 Diluted tangible book value per share Diluted book value $1,850,947 $1,938,734 $1,769,744 $(50,000) $3,570,691 Goodwill and other intangible assets 0 (147,610) (17) (147,610) (147,610) Diluted tangible book value $1,850,947 $1,791,124 $1,622,134 $(50,000) $3,423,081 Diluted tangible book value per share (6) $32.85 $21.76 $22.14 $26.41 |

53 Purchase Accounting Adjustments Reserve adjustment of $130 million does not represent a change in the amount of reserves established by Max Represents fair value purchase accounting adjustment, solely as a result of the merger Discount rates are applied to the underlying cash flows, combined with an estimated risk premium Reserve adjustment will be reversed into income each year, increasing net income Increases net income by $13 million (10% of total) in year one Cumulative increase of $130 million over the payout period Reserve adjustment has no economic impact – represents only a timing difference Does not impact ultimate losses and loss adjustment expenses IPC 12/31/08 shareholders' equity $1,850.9 Plus: Max 12/31/08 shareholders' equity 1,280.3 Combined 12/31/08 shareholders' equity $3,131.3 Purchase accounting adjustments Less: Adjustment to reserves ($130.0) Less: Transaction expenses (40.0) Plus: Other purchase accounting adjustments 12.1 Pro forma 12/31/08 shareholders' equity $2,973.4 Less: Goodwill and intangibles (28.5) Pro forma 12/31/08 tangible shareholders' equity $2,944.9 IPC 12/31/08 fully diluted book value per share $32.85 Pro forma 12/31/08 fully diluted book value per share $31.97 Pro forma 12/31/08 fully diluted tangible book value per share $31.67 |

54 Footnotes Note: Book value per share, diluted book value per share, tangible book value per share, and diluted tangible book value per share are all “non-GAAP financial measures” as defined in Regulation G. Combined figures exclude purchase accounting adjustments. For more information on GAAP purchase accounting adjustments, see the joint proxy statement/prospectus filed with the SEC by IPC on May 7, 2009. 1. Calculations are based on treasury stock method for warrants and stock options; and includes all restricted stock and RSUs outstanding as of the 12/31/2008 balance sheet date. Validus’ publicly disclosed calculations are based on the "as-if-converted" method, assuming all proceeds received upon exercise of warrants and stock options will be retained by the Company, and the resulting common shares from exercise remain outstanding. 2. Shareholders’ equity divided by basic shares outstanding. 3. Calculations are based on treasury stock method, assuming the proceeds received upon exercise of warrants and stock options are used to repurchase shares at the 12/31/2008 closing market price. 4. Diluted book value divided by diluted shares outstanding as of the 12/31/2008 balance sheet date. 5. Tangible shareholders’ equity divided by common shares outstanding as of the 12/31/2008 balance sheet date. 6. Diluted tangible book value divided by diluted shares outstanding as of the 12/31/2008 balance sheet date. 7. Common shares outstanding as of 12/31/08 per the IPCR Consolidated Balance Sheet contained within the IPC 2008 Form 10-K. Adjusted to exclude certain restricted stock awards included in shares outstanding. 8. Note 7 in the IPC 2008 Form 10-K Notes to the Consolidated Financial Statements. Adjusted to exclude certain restricted stock awards included in shares outstanding. 9. Per the IPC Consolidated Balance Sheet included in the IPC 2008 Form 10-K. 10. Common shares outstanding as of 12/31/08 per the MXGL Consolidated Balance Sheet contained within the Max 2008 Form 10-K filed 2/19/2009. 11. Note 12 in the Max 2008 Form 10-K Notes to the Consolidated Financial Statements. Based on the treasury stock method. 12. Note 13 in the Max 2008 Form 10-K Notes to the Consolidated Financial Statements. Based on the treasury stock method. 2,021,631 non-vested restricted stock awards included in basic shares outstanding. 13. Per the Max Consolidated Balance Sheet included in the 2008 Form 10-K. 14. As disclosed in Max’s fourth quarter 2008 earnings press release, dated 2/11/2009. 15. Note 5 in the Max 2008 Form 10-K Notes to the Consolidated Financial Statements. 16. Based on page 6 of the Validus Investor Financial Supplement as of 12/31/2008 filed 2/12/2009. 17. Note 6 in the Validus 2008 Form 10-K Notes to the Consolidated Financial Statements. |