Filed by Max Capital Group Ltd. pursuant to Rule 425 under the Securities Act of 1933, as amended, and deemed filed pursuant to Rule 14a-12 under the Securities Exchange Act of 1934, as amended. Subject Company: Max Capital Group Ltd. (Commission File No.: 000-33047) |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING INFORMATION

This filing includes statements about future economic performance, finances, expectations, plans and prospects of both IPC Holdings, Ltd. (“IPC”) and Max Capital Group Ltd. (“Max”) that constitute forward-looking statements for purposes of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to certain risks and uncertainties, including the risks described in the definitive joint proxy statement/prospectus of IPC and Max that has been filed with the Securities and Exchange Commission (“SEC”) under “Risk Factors,” many of which are difficult to predict and generally beyond the control of IPC and Max, that could cause actual results to differ materially from those expressed in or suggested by such statements. For further information regarding cautionary statements and factors affecting future results, please also refer to the most recent Annual Report on Form 10-K, Quarterly Reports on Form 10-Q filed subsequent to the Annual Report and other documents filed by each of IPC or Max, as the case may be, with the SEC. Neither IPC nor Max undertakes any obligation to update or revise publicly any forward-looking statement whether as a result of new information, future developments or otherwise.

This filing contains certain forward-looking statements within the meaning of the U.S. federal securities laws. Statements that are not historical facts, including statements about our beliefs, plans or expectations, are forward-looking statements. These statements are based on our current plans, estimates and expectations. Some forward-looking statements may be identified by our use of terms such as “believes,” “anticipates,” “intends,” “expects” and similar statements of a future or forward looking nature. In light of the inherent risks and uncertainties in all forward-looking statements, the inclusion of such statements in this filing should not be considered as a representation by us or any other person that our objectives or plans will be achieved. A non-exclusive list of important factors that could cause actual results to differ materially from those in such forward-looking statements includes the following: (a) the occurrence of natural or man-made catastrophic events with a frequency or severity exceeding our expectations; (b) the adequacy of our loss reserves and the need to adjust such reserves as claims develop over time; (c) any lowering or loss of financial ratings of any wholly-owned operating subsidiary; (d) the effect of competition on market trends and pricing; (e) changes in general economic conditions, including changes in interest rates and/or equity values in the United States of America and elsewhere and continued instability in global credit markets; and (f) other factors set forth in the definitive joint proxy statement/prospectus of IPC and Max, the most recent reports on Form 10-K, Form 10-Q and other documents of IPC or Max, as the case may be, on file with the SEC. Risks and uncertainties relating to the proposed transaction include the risks that: the parties will not obtain the requisite shareholder or regulatory approvals for the transaction; the anticipated benefits of the transaction will not be realized; and/or the proposed transactions will not be consummated. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. We do not intend, and are under no obligation, to update any forward looking statement contained in this filing.

ADDITIONAL INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION AND WHERE TO FIND IT:

This filing relates to a proposed business combination between IPC and Max. On May 7, 2009, IPC and Max filed with the SEC a definitive joint proxy statement/prospectus, which was first mailed to shareholders of IPC and Max on May 7, 2009. This filing is not a substitute for the definitive joint proxy statement/prospectus or any other document that IPC or Max may file with the SEC or send to their respective shareholders in connection with the proposed transaction

INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DEFINITIVE JOINT PROXY STATEMENT/PROSPECTUS AND ALL OTHER RELEVANT DOCUMENTS FILED OR THAT WILL BE FILED WITH THE SEC AS THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION.All such documents, if filed, would be available free of charge at the SEC’s website (www.sec.gov) or by directing a request to IPC, at Jim Bryce, President and Chief Executive Officer, or John Weale, Executive Vice President and Chief Financial Officer, at 441-298-5100, in the case of IPC’s filings, or Max, at Joe Roberts, Chief Financial Officer, or Susan Spivak Bernstein, Senior Vice President, Investor Relations at 441-295-8800, in the case of Max’s filings.

PARTICIPANTS IN THE SOLICITATION:

IPC and Max and their directors, executive officers and other employees may be deemed to be participants in any solicitation of IPC and Max shareholders, respectively, in connection with the proposed business combination.

Information about IPC’s directors and executive officers is available in the definitive joint proxy statement/prospectus filed with the SEC on May 7, 2009, relating to IPC’s 2009 annual meeting of shareholders; information about Max’s directors and executive officers is available in the amendment to its annual report on Form-10K, filed with the SEC on April 1, 2009.

Max Capital Group Ltd.

Susan Spivak Bernstein

+1-212-898-6640

Kekst and Company

Roanne Kulakoff or Peter Hill

+1-212-521-4800

Delroy Alexander Group managing editor

Bermuda Re/insurance

©iStockphoto.com / P_Wei

8 Bermuda Re/insurance . June 2009

THE DEAL DECADE OF

Max Capital celebrates its 10th anniversary this year.

Delroy | Alexander looks at a mainstay of the Bermuda |

landscape and its proposed deal with IPC Holdings.

As Max Capital turns 10 this the midst of a proposed merger combined company into the big

From its 1999 inception as a company offering structured and utilising an investment to hedge funds, Max has been re/insurance company, most and chief executive officer W. helm in October 2006.

It is now the centre of a reinsurer IPC Holdings. If will vault the new combination based re/insurers, with more debt-free concern.

“In the last two years, we our underwriting platforms,” robust platforms in Bermuda

year, But now the we fast-growing have expanded re/insurer recently, with IPC Holdings at Lloyd’s. that We will have league write insurance of Bermuda or insurers. reinsurance a wide variety of classes. relatively marketplace small wherever Bermuda it seems from alternative time to time. risk “ reinsurance that included a significant transformed A far cry from into Max’s global humble under the leadership of Marston In 2000, “Marty” the then Becker, Max Re who Capital in 2007) commenced underwriting and alternative risk reinsurance was talked to write about products merger with successful, as annuities, the share-for-share structured workers’ into the compensation ranks of the and top 10 than $3.0 billion of equity in a A series of joint ventures and expand to writing both insurance have which really it also accelerated launch edits the said and consolidated Becker recently. its Bermuda “We had House, Dublin, the our current original building two

Bermuda Re/insurance . June 2009 9

More recently, under Becker’s excess and surplus speciality the giant North American divisions—brokerage, contract of property, ocean and inland umbrella insurance products.

And in the fourth quarter of acquisition of Max at Lloyd’s Lloyd’s insurance operation in Denmark and Japan. Max at specialty insurance and financial institutions, and business through Lloyd’s

“Along this path of expansion, it would also be desirable for to Becker. “It wasn’t a

$3. guidance 0 billion in2007, and up Max in formed capital lines in the carrier investor that world, gave and it rating Max Specialty agencies. operates So we had across binding that, but and really marine—offering had not found a until marine, the casualty, IPC situation. excess “

Those options also included last companies year, suggesting the reinsurer a range (formerly details filed Imagine recently Group with (UK) the In in the London, first quarter which included of 2008, Lloyd’s re/insurer, underwrites which ultimately portfolio in the risks fourth from quarter property of last Max, offering accident itself to professional as a 1400, 2525 and 2526.

But it is the IPC deal that IPC we chairman recognised Ken that, Hammond. at some Max to be larger in scale,” “It’s a but merger it’s of clear equals,” that review a couple of years ago, its appropriateness, our and also our capital utilisation, exposed. In looking at that, very important, especially in towards catastrophe exposure. capital, and a merger would that existed in our business.”

IPC’s board looked at a number Hammond says. These included rival, and being acquired by a was the clear choice of the

“We identified a number of screens,” says Hammond. “We down to eight and then three. we got down to the shorter addition to that was the first knew who we were negotiating

The deal with Max came number of parallel negotiations made initial contact with talking to seven other potential 2009, other contenders had had agreed to an exclusivity between the two.

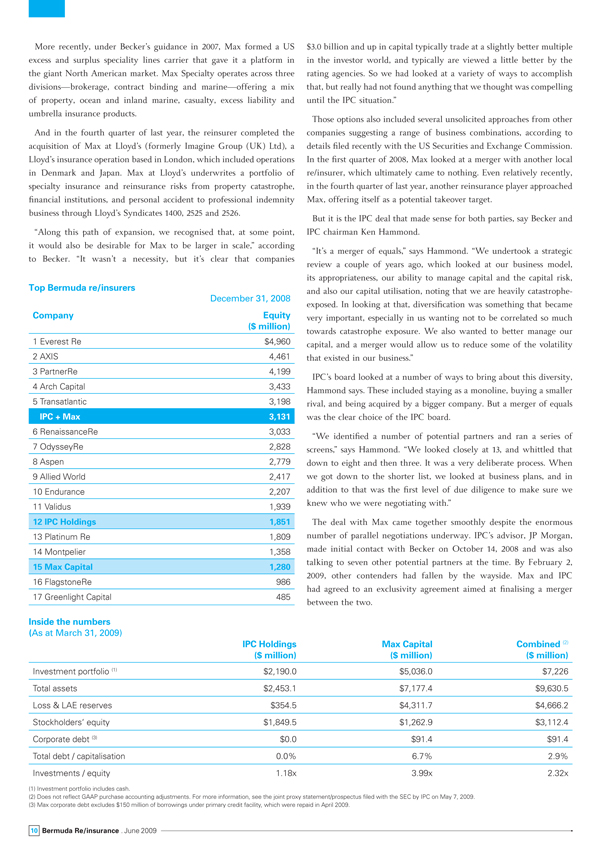

Top Bermuda re/insurers

December 31, 2008

Company Equity ($ million)

1 Everest Re $4,960

2 AXIS 4,461

3 PartnerRe 4,199

4 Arch Capital 3,433

5 Transatlantic 3,198

IPC + Max 3,131

6 Renaissance Re 3,033

7 Odyssey Re 2,828

8 Aspen 2,779

9 Allied World 2,417

10 Endurance 2,207

11 Valid us 1,939

12 IPC Holdings 1,851

13 Platinum Re 1,809

14 Montpelier 1,358

15 Max Capital 1,280

16 Flagstone Re 986

17 Green light Capital 485

Inside the numbers (As at March 31, 2009)

IPC Holdings Max Capital Combined (2) ($ million) ($ million) ($ million)

Investment portfolio (1) $2,190.0 $5,036.0 $7,226 Total assets $2,453.1 $7,177.4 $9,630.5 Loss & LAE reserves $354.5 $4,311.7 $4,666.2 Stockholders’ equity $1,849.5 $1,262.9 $3,112.4 Corporate debt (3) $0.0 $91.4 $91.4 Total debt / capitalisation 0.0% 6.7% 2.9% Investments / equity 1.18 x 3.99 x 2.32 x

(1) Investment portfolio includes cash.

(2) Does not reflect GAAP purchase accounting adjustments. For more information, see the joint proxy statement/prospectus filed with the SEC by IPC on May 7, 2009. (3) Max corporate debt excludes $150 million of borrowings under primary credit facility, which were repaid in April 2009.

10 Bermuda Re/insurance . June 2009

Max at 10 2001

A joint venture with Bayerische Hypo- und Vereinsbank in early 2001 “It’s sometimes easy to forget the rapid transformation of Max saw Grand Central Re formed, a Class 4 Bermuda insurance company from a Bermuda reinsurance player to a global traditional insurance with an initial shareholders’ equity of $200 million. HypoVereinsbank and reinsurance company,” says Angelo Guagliano, the current chief brought its asset management and banking experience to the new executive officer of Max Bermuda. company, while Max added its insurance management and underwriting “As we started out as a reinsurance company, that’s how some expertise. On September 11, 2001, US terrorist attacks severely tested people still see us,” says Guagliano, who took over the top job at Max risk management practices and controls.

Bermuda in 2007, when it was relinquished by group boss W. Marston 2002 “Marty” Becker. “Since the company was formed in 1999, it has been transformed from an organisation providing structured reinsurance only In January 2002, Max helped fund DaVinci Re Holdings, and its operating into a traditional specialty reinsurance and insurance company.” subsidiary DaVinci Reinsurance, a global property catastrophe reinsurance company. The move was partly prompted by the improvement of rates Max has built a solid underwriting base, which remains its strength, for traditional business in the aftermath of the events of 9/11. says Guagliano.

2003

“Our strength is having small teams of experienced underwriters, with Max Re launched a new business unit to provide insurance to larger the appropriate authority to make underwriting decisions. This allows public companies. An excess liability department was established in us to be responsive to the market,” says the Max Bermuda CEO. “A January, followed by a professional liability department in April. This core principle is that we are an underwriting company that is willing to additional capability proved timely. In May 2003, Max Re House, the new understand a client’s needs, and tailor a programme that works for both building on Hamilton Harbour, consolidated all activities in Bermuda. them and us.”

2004

Guagliano joined Max in January 2003, at the start of the company’s In September, Max Re added a dedicated property insurance department, push into general insurance underwriting. He has seen the Bermuda providing cover to large multinational clients on a worldwide basis, platform increase, alongside growth in Europe through Max Europe’s focused on commercial, industrial and technical risks.

Dublin office, and, more recently, through the additions of Max

2005

Specialty—a US excess and surplus lines operation—and Max Hurricanes Katrina, Rita and Wilma made 2005 an extraordinary at Lloyd’s. year, costing the industry an estimated $65 billion. Max Re’s multi-line “We still have virtually all the same underwriters that we hired in 2003 underwriting portfolio was inevitably impacted, but the company still working for us in every insurance line that Max Bermuda offers,” he recorded a small net income for 2005. adds. “I think that says something about how we operate and the type 2006 of commitment we have to doing the job properly. As the transformation has occurred, the premiums generated by our Bermuda/Dublin insurance Max began to reduce the alternative investment segment of its segment have grown to about $400 million, from zero in 2003, and our invested asset portfolio to between 15 and 20 percent of invested track record shows we have been operating profitably.” assets, to reflect the change in risk profile of the transformed traditional specialty insurance and reinsurance underwriter. In December 2006, the DaVinci Re investment liquidated. Aviation insurance department Timeline established. Max USA Holdings incorporated.

1999 2007

Max Capital Group was incorporated as Maximus Capital Holdings in Max posted outstanding financial results. Max Re Capital changed its July 1999. name to Max Capital Group to better reflect its new role. Max Specialty Insurance Company, a US excess and surplus insurance platform with The company’s initial strategy included investing in a combination of headquarters in Richmond, Virginia, is established. traditional fixed income securities and a portfolio of alternative investments managed by Moore Capital Management. The company completed first 2008 private placement and ended the year with a headcount of six. Max posted good operating results in 2008, overshadowed by unprecedented investment volatility and losses on its alternative investment

2000 portfolio. Saw favourable performance from its underwriting units. Max Established in Bermuda, underwriting commenced with operating acquired new Lloyd’s platform, managing three Lloyd’s syndicates with a activity focused on structured and specialty risk reinsurance of 2008 combined stamp capacity of approximately £200 million. long-tailed liabilities, such as annuities, structured settlements, life insurance, disability income, workers’ compensation and medical 2009 malpractice insurance. Max Re Europe was incorporated and the Max Capital turned 10. Headcount topped 330. Company agreed to merger company name was changed from Maximus Capital Holdings to Max with IPC, which is set to see W. Marston “Marty” Becker CEO of the new Re Capital. combination, which is expected to have more than $3.0 billion in assets.

12 Bermuda Re/insurance . June 2009

“We were both well positioned in to June. move forward,” “I was really says not Hammond. “They had a complementary business this procedure plan, which was a means ‘getting the implementation and execution risks through were a minimised series of as meetings a result. think that, on a combined basis, was both a good companies fit.” will benefit and the shareholders will benefit greatly.” Hammond agrees: “I knew of Marty Becker says it wasn’t only the but business I had mix never between met him the prior that made sense; both teams were the convinced early stages that were the like people an work well together.

Becker echoes Hammond’s view “A unique characteristic of this able transaction to come together. is that it of the risk that has caused many insurance mergers and transactions in the past to not” The work deal out well,” works both says ways, Becker. so portfolio of IPC is very short-tail The diversification and, therefore, of has their very for surprises. And the IPC leadership, with Max because will give they their kept the in a single line of business, had From been our prudent shareholders’ when it point came of to management. As a result, the people IPC’s global integration knowledge issues from are its In fact, we have committed that business everyone is who predominantly wants to have in a the the new company will have a job, the because world—the there combination is plenty of of the everyone to do.” generates is extremely attractive generate about $300 to $400 February was spent finalising the capital negotiations in the world and doing of today is diligence so that “by the time we announced the transaction in our two organisations had researched But it each hasn’t other all thoroughly, been smooth and convinced of the benefits of this surprise newly combined hostile offer for IPC publicly revealed their merger. Several observers also warmed to the proposed merger.

“It was a surprise,” says “We believe this merger of Max surprise. with IPC is We positive had looked to at the Max,” said Standard & Poor’s in Valid us April.” The is primarily transaction a is property a merger, with the new company becoming determined the that combination Valid us, of given IPC and Max. Although some overlap appropriate exists between potential the two partner—a companies terms of employees, property catastrophe exposures and the post-merger company will basically Hammond reiterates be the combination that it’s of relatively intact stand-alone entities. shareholders, who now have two negotiated deal with Max, and a “The merger is not driven by expense savings, but rather by creation of a larger and well-capitalised “Under the agreement, company, with the a diversified book of business (mainly for approval. through Should IPC’s they vote presence and Max’s diversified business June closing lines) before and the reduced hurricane earnings/capital volatility.” is rejected, that is the end of driver’s seat, as it does not The deal was made all the more addition surprising to that, by the there fact would that be party knew the other particularly well prior to the start of in October last year. On May 14, IPC and Max all regulatory hurdles in “I did not know the IPC employees shareholder or the board vote is of directors June 12. If all prior to this process,” says closure Becker, on who the will deal remain will chief occur the combined organisation if shareholders giant, under vote the to familiar approve ‘Max’ the

Valid us ups offer The bid’s implied value of $30.14 per share represented a 16 cents per share, or less than one percent, increase over the value of the original On May 21, as Bermuda Re/insurance was going to press, IPC Holdings’ offer of $29.98 per share, IPC said. board rejected a sweetened takeover offer from Valid us Holdings, and reiterated its backing for a proposed merger with Max Capital Group. “This increase underscores our strong commitment to the acquisition IPC once again turned down overtures from its hostile suitor. Valid us of IPC,” stated Ed Noon an, Valid us’ chairman and chief executive officer. had increased its rival bid for the Bermuda reinsurer to $1.69 billion, or “Following numerous meetings with IPC shareholders, we believe there $30.14 per share, on Monday, May 18. The latest offer included $3.00 is widespread support for our acquisition of IPC.” of cash and 1.1234 Valid us shares for each IPC share. “[It’s] not a lot of money,” Morningstar analyst William Bergman told However, the IPC board said the fresh offer terms did not constitute a Reuters about the offer. “Valid us sees this as a cost-effective way to superior proposal and were not in the company’s best interests. It again gain scale. At the same time, the relationships between IPC and Max’s recommended that IPC shareholders reject the Valid us exchange offer. corporate guys are also very valuable relative to the Valid us offer.”

Bermuda Re/insurance . June 2009 13