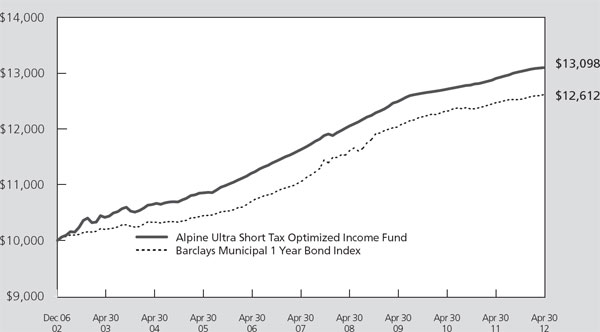

|

UNITED STATES |

SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

|

FORM N-CSR |

|

CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

MANAGEMENT INVESTMENT COMPANIES |

|

Investment Company Act file number: 811-10405 |

|

|

Alpine Series Trust |

|

(Exact name of registrant as specified in charter) |

|

2500 Westchester Avenue, Suite 215 |

Purchase, New York 10577 |

|

(Address of principal executive offices)(Zip code) |

|

|

(Name and Address of Agent for | Copy to: |

|

|

Samuel A. Lieber | Rose DiMartino |

Alpine Woods Capital Investors, LLC | Attorney at Law |

2500 Westchester Avenue, Suite 215 | Willkie Farr & Gallagher |

Purchase, New York 10577 | 787 7th Avenue, 40th Floor |

| New York, New York 10019 |

Registrant’s telephone number, including area code: (914) 251-0880

Date of fiscal year end: October 31

Date of reporting period: November 1, 2011 - April 30, 2012

Item 1: Shareholder Report

Equity & Income Funds

Alpine Dynamic Dividend Fund

Alpine Transformations Fund

Institutional Class (ADVDX)

Institutional Class (ADTRX)

Class A (ADAVX)

Class A (ADATX)

Alpine Accelerating Dividend Fund

Alpine Foundation Fund

Institutional Class (AADDX)

Institutional Class (ADBYX)

Class A (AAADX)

Class A (ADABX)

Alpine Financial Services Fund

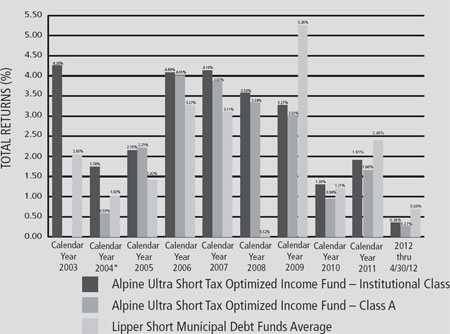

Alpine Ultra Short Tax Optimized Income Fund

Institutional Class (ADFSX)

Institutional Class (ATOIX)

Class A (ADAFX)

Class A (ATOAX)

Alpine Innovators Fund

Alpine Municipal Money Market Fund

Institutional Class (ADINX)

Institutional Class (AMUXX)

Class A (ADIAX)

April 30,

2012

Semi-Annual Report

|

Table of Contents |

|

|

|

|

|

|

| |

|

|

|

|

| 7 |

| |

|

|

|

|

| 14 |

| |

|

|

|

|

| 19 |

| |

|

|

|

|

| 24 |

| |

|

|

|

|

| 28 |

| |

|

|

|

|

| 32 |

| |

|

|

|

|

|

|

| |

|

|

|

|

| 37 |

| |

|

|

|

|

| 40 |

| |

|

|

|

|

| 46 |

| |

|

|

|

|

| 50 |

| |

|

|

|

|

| 78 |

| |

|

|

|

|

| 81 |

| |

|

|

|

|

| 84 |

| |

|

|

|

|

| 92 |

| |

|

|

|

|

| 107 |

| |

|

|

|

|

| 123 |

|

|

Additional Alpine Funds are offered in the Alpine Equity Trust. These funds include: |

|

Alpine International Real Estate Equity Fund |

Alpine Realty Income Growth Fund |

Alpine Cyclical Advantage Property Fund |

Alpine Emerging Markets Real Estate Fund |

Alpine Global Infrastructure Fund |

Alpine Global Consumer Growth Fund |

Alpine’s Real Estate Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing in funds of the Alpine Series Trust and Alpine Income Trust. The statutory and summary prospectuses contain this and other important information about the investment company, and it may be obtained by calling 1-888-785-5578, or visiting www.alpinefunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible.

|

|

| Alpine’s Investment Outlook |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dear Investor:

Beneath the day-to-day noise of news and data, there is a dialogue playing out in the capital markets which questions (a) whether an effective fiscal European Union (EU) can emerge from the current stresses brought on by a decade of imprudent fiscal laxity, and (b) what are the broader global economic implications whether or not the EU succeeds. Complicating these scenarios are the ongoing after effects of the financial crisis of 2008, which have highlighted the constraints on how countries provide a broad array of health, education and social services when the population is aging or even declining and productivity growth slows. Most of the developed economies have known such issues for years, but this ongoing slowdown may force a restructuring of revenue collection and the availability of those services. This issue is not about big vs. limited government, or socialist vs. laissez-faire ideologies. Rather, it should be about how much of a base shall a country provide and how best to pay for it. Revenues from gambling, tolls, asset sales, licenses, fees, consumption taxes, asset taxes as well as income and transaction taxes are, globally, all part of the possible sources which have varying economic and societal impacts.

Where Is The Train Heading?

Much of the fear and uncertainty in the market revolves around who is conducting the course and pace of response to today’s economic dilemmas. Europe’s leaders have fallen behind the pace of events. The markets have lost patience with EU politicians and bankers who failed to achieve much in the way of labor and business reforms, economic restructuring, or balance sheet recapitalizations between 2008 through this summer. Potential scenarios range from the hopeful implementation of constructive reforms, which may take a long time to implement, to the uncertain implications of Greece’s potential exit from the Euro. Perhaps the most benign scenario would be a decisive U.S. election followed by minimal political brinksmanship regarding budget/tax reform while, at the same time, sovereign debt burdens stabilize and confidence improves that Europe can muddle through their problems. Further

comfort could be derived if China would achieve a soft landing before resuming growth, and the risk of war in the Middle East and/or potential disruption of oil flows would lessen as a factor. This scenario assumes a rational world motivated by mutual interest, and more than a little good luck. On the other hand, misfortune, combined with a panicked and protectionist environment motivated by self preservation could also emerge.

The most pessimistic scenarios depict a world where confidence in institutions and societal or economic structures which worked for over sixty years fail to perform. Bank runs, margin calls, credit withdrawals, currency collapses, all reflect the sort of contagion that could be imagined to spring from a worst case collapse of the Euro. Such fears are reminiscent of late 2008, when the genuine dysfunction and lack of tools to address the structural problems contributed to the crisis at that time. Now, fears of societal unrest or further external conflicts in the Middle East, Asia or Africa, could create another desperate dimension in extreme circumstances.

Unfortunately, investors can only model scenarios of what might happen along each route as the journey unfolds over time, and then weigh the probabilities as we evaluate portfolio positioning in terms of potential risk or reward. Potential reward can be measured in terms of growth and value metrics. Current valuations vary by country or industry, but many individual stocks are priced at valuations similar to early 2009. Yet economic measures of demand, financial stability and overall integrity are far better than 2008 or 2009, so if the political and economic concerns begin to align into action, then equity valuations could prove compelling.

We believe the market has already discounted some percentage of both best and worst scenarios, with a higher likelihood that a messy, muddled, mix of positive actions, fearful reactions and modicum of inaction will carry the day. Since the collapse of Lehman Brothers, the fear and loathing trade has over-emphasized the negative ‘risk’ scenarios, by inducing the withdrawal of equity capital into bonds and alternative investments. The subsequent reduction in both breadth and depth of market participation and liquidity has aggravated

1

|

volatility, both on the downsizing and on the rebound. Compounding this has been the so called “risk on, risk off” trades driven by quantitative algorithms which tend to exacerbate shifts in market sentiment.

Outside of big picture news flow, the important factors driving underlying business performance and, hence, the fundamental drivers of equity performance have been pretty spotty but generally solid in the U.S., and selectively stronger in Asia and Latin America, although the Euro area slowdown is affecting these economies as well. While liquidity is still difficult in some markets and for certain industries, the flow of capital has improved over the past fifteen months, although European credit is understandably more difficult to come by. That said, large private equity funds have been raised to participate in potential European recapitalizations or mergers and acquisitions (M&A), which we believe could play a significant role over the next 12 to 24 months. In general, high commodity prices have also declined with the ongoing slowdown of marginal global demand, which should have a positive effect upon corporate profitability around the world, mitigating the top line impact of an economic slowdown.

Signals Say “Proceed Cautiously” Avoid Congestion

For the U.S., the trend in costs is particularly positive for ongoing economic activity given the abundance of natural gas and our existing infrastructure to distribute it and cut back on coal and oil. However, after a six month run of good economic data through April, the latest (May) reviews of purchasing managers’ orders books, consumer confidence, industrial production and, notably, leading indicators reveal a weakening trend is emerging. Admittedly, while job growth is positive, it is diminishing and far below a desirable 300+ thousand per month. Improvement in the housing statistics is also supportive as new home sales begins to rise off a very low base and, barring any significant downturn, should enhance economic activity and job growth after over five years of negative contribution. Even Fannie Mae produced positive earnings in the first quarter of this year after eighteen negative quarters suggesting that the poor performing financial underpinnings of the past have worked their way through the system and that even the system itself is healing without having been significantly restructured. Combine this with the current strong balance sheet strength of large public companies and historically strong profit margins, and it suggests that it is a matter of time before America’s private sector increases capital spending and starts adding jobs.

Given the continued support of the Federal Reserve, it appears clear that a cheap monetary policy will continue

to keep the flame of economic potential burning. In this context it is encouraging to see that Central Banks around the world, from Beijing to Oslo, and Bangkok to Brasília, continue to provide low cost liquidity to their domestic sectors. Given the global output gap, it is reasonable to assume that the potential creation of an inflation bubble is still a long way off, and certainly not a foregone conclusion. Thus, we remain confident in our belief that given this global cyclical upturn, albeit slow and narrow so far, and constrained by fragile confidence, that growth can continue in many countries. Notably, global growth and demand is staggered by region with projections that emerging economies will create 80% of global growth over the next few years. That said, there are many companies in the already developed economies that produce much of their revenue from growing countries.

Mind The Gap, Before Boarding The Train

The ‘gap’ between demand and productive capability may change the trend of globalization which previously emphasized cheap exports. Production may become more focused on the domestic needs of individual countries. While this may prove inflationary for specific goods in certain countries or regions, the output gap will likely have a moderating effect on global inflation for several years.

We should also be mindful that a gap still exists between the traditional sources of economic growth. Typically, the manufacturing or private sector and the government or public sector have evolved in most economies to either supplement or offset each other during weak phases of the business cycle. However, during a protracted downturn, such as we are currently experiencing, resources can be exhausted or stretched beyond comfortable norms. In the U.S., for example, corporate spending, while improving, has yet to recover from the downdraft of 2008. The balance sheets for large corporations are in great shape, because many smaller firms are still constrained, allowing big or public companies to grow market share at low cost. However, this period of improving margins and low cost growth may begin to fade. Meanwhile, the Government’s spending on transfer payments, including unemployment benefits and municipal support has offset the impact of reduced corporate capex and employment declines since 2008. Significant supplemental spending packages have made up for revenue shortfalls at both the state and municipal levels of government and minimized the potential for further layoffs and service reductions brought on by diminished local tax receipts. Alas, this is not just an American problem. After four years with total Federal government outlays far exceeding tax receipts

2

|

already diminished by slower economic activity, governments around the world have fallen into excessive fiscal deficits which have overloaded debt burdens. This has been especially prevalent in most developed countries with established social services covering health, education and welfare.

Significantly, these fiscal deficiencies cannot be fixed by just raising taxes and cutting spending without creating other problems. Now the gap between corporate capital spending on plant equipment and employment must shift back to the corporate sector if these countries hope to maintain economic momentum. Recent increases in corporate spending, with the U.S. leading European companies, has been primarily limited to technology, marketing and sales, as opposed to new production, but this may not be enough to stimulate employment gains before the stimulus gap begins to widen. The rapid expansion of shale and coal seam gas extraction, initially in the U.S., to be followed by Australia and China, could lower fuel costs in many countries, stimulating large infrastructure spending and supporting further business activity. We think investors will have to “watch the gap” between corporate and Federal spending trends as a precursor to our getting the global economy back on track.

Even though so called ‘Emerging Market’ (EM) economies have maintained fiscal capacity through both lower debt levels and superior economic growth, those with export oriented economies such as China, Taiwan and Korea are not immune to falling or stagnant demand from Europe, Japan and, possibly, the U.S.A. While this has reduced EM Gross Domestic Product (GDP) growth potential, economic forecasts still remain well ahead of those for developed economies. The combination of population growth, expanding proportion of middle class people, aggregate wealth accumulation and continued corporate expansion

would likely lead to extending the rising trends in income and consumption. Nonetheless, we believe the prospect of the emerging middle class consumer in EM’s fully offsetting the decline in buying power of developed economies is unlikely for the next decade or so, until median incomes begin to approach ours and the number of people included is far in excess. Thus, the U.S. and Europe must take rational steps to stabilize the balance sheets of both the public and private sectors of their economies.

While Europe’s troubles and the U.S. ‘fiscal cliff’ have received the most attention, perhaps of greater importance to the global economy is the transition of the Chinese economy from an export-led, low cost production model towards a broader focus on services and capabilities to meet the demands of a growing middle class. We are seeing a similar effort take place in Brazil where the middle class has grown from the ranks of impoverished masses. As incomes and standards of living rise, people in these countries will likely aspire to lifestyles similar to those which we have enjoyed for decades. This is the direction in which the global locomotive of growth will be traveling. As Alpine’s analysts and managers annually participate in over 1,000 company meetings, and visits, we will continue to assess whether different countries, companies or industries are positioned at the front of the train or towards the caboose. Over time, perhaps the biggest risk to investors during these volatile times of economic transition would be staying put when the train leaves the station.

Sincerely,

Samuel A. Lieber

President

|

|

|

|

Past performance is not a guarantee of future results. The specific market, sector or investment conditions that contribute to a Fund’s performance may not be replicated in future periods. | |

|

|

Mutual fund investing involves risk. Principal loss is possible. Please refer to the individual fund letters for risks specific to each fund. | |

|

|

This letter and the letters that follow represent the opinion of Alpine Funds’ management and are subject to change, are not guaranteed, and should not be considered investment advice. | |

|

|

Please refer to the schedule of investments for fund holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. Current and future portfolio holdings are subject to risk. | |

3

|

|

Disclosures and Definitions |

|

Disclosure

Mutual fund investing involves risk. Principal loss is possible. Please refer to the individual fund letters for risks specific to each fund.

The President’s Letter and those that follow represent the opinion of the Funds’ management and are subject to change, are not guaranteed, and should not be considered investment advice. The information provided is not intended to be a forecast of future events. Views expressed may vary from those of the firm as a whole.

Past performance is not a guarantee of future results.

Please refer to the schedule of investments for each fund’s holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. Current and future portfolio holdings are subject to risk.

Favorable tax treatment of Fund distributions may be adversely affected, changed or repealed by future changes in tax laws. Alpine may not be able to anticipate the level of dividends that companies will pay in any given timeframe.

Neither the Fund nor any of its representatives may give tax advice. Investors should consult their tax advisor for information concerning their particular situation.

Diversification does not assure a profit or protect against loss in a declining market.

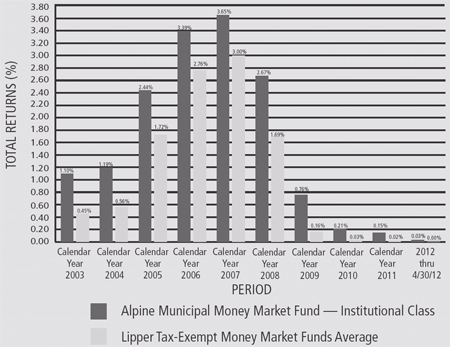

An investment in the Alpine Municipal Money Market Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund. Must be preceded or accompanied by a prospectus.

Quasar Distributors, LLC, distributor.

Definitions

Average Weight refers to the average weight of the holding in the portfolio during the reporting period.

Book value is the net asset value of a company, calculated by subtracting total liabilities from total assets.

Build America Bonds are taxable municipal bonds that carry special tax credits and federal subsidies for either the bond issuer or the bondholder. Build America Bonds were created under Section 1531 of Title I of Division B of the American Recovery and Reinvestment Act that U.S. President Barack Obama signed into law on February 17, 2009.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

Dividend Yield (Funds) represents the trailing 12-month dividend yield aggregating all income distributions per share over the past year, divided by the period ending fund share price. It does not reflect capital gains distributions.

Dividend Yield: The yield a company pays out to its shareholders in the form of dividends. It is calculated by taking the amount of dividends paid per share over a specific period of time and dividing by the stock’s price.

Earnings or Earnings Per Share Growth is a measure of a company’s net income over a specific period, generally one year, is a key indicator for measuring a company’s success, and the driving force behind stock price appreciation.

Free cash flow is a measure of financial performance calculated as operating cash flow minus capital expenditures. Free cash flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base. Free cash flow is important because it allows a company to pursue opportunities that enhance shareholder value.

LTRO is Long Term Refinancing Operation.

Price/Earnings Ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings. Normalized earnings – earnings metric that shows you want earnings look like smoothed out in the long run, taking into account the cyclical changes in an economy or stock.

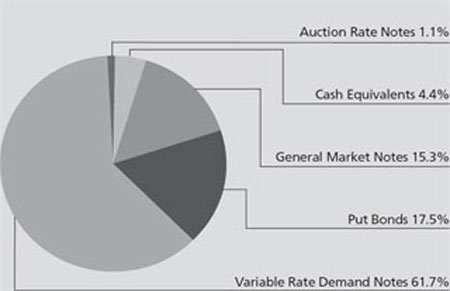

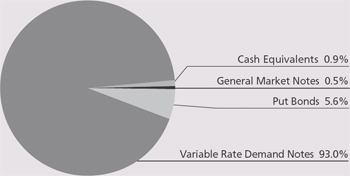

Variable Rate Demand Note (VRDN): A debt instrument that represents borrowed funds that are payable on demand and accrue interest based on a prevailing money market rate, such as the prime rate. The interest rate applicable to the borrowed funds is specified from the outset of the debt, and is typically equal to the specified money market rate plus an extra margin.

Dow Jones Industrial Average – is a price-weighted average of 30 blue-chip stocks that are generally the leaders in their industry.

Each Lipper Average represents a universe of Funds with similar invest objectives.

MSCI World Index USD is a free float-adjusted market cap weighted index that is designed to measure the equity market performance of developed markets. Source: MSCI. MSCI data may not be reproduced or used for any other purpose. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

The NASDAQ Financial-100 Index includes 100 of the largest domestic and international financial securities listed on The NASDAQ Stock Market based on market

4

|

|

Disclosures and Definitions |

|

capitalization. They include companies classified according to the Industry Classification Benchmark as Financials, which are included within the NASDAQ Bank, NASDAQ Insurance, and NASDAQ Other Finance Indexes.

KBW Bank Index is a modified cap-weighted index consisting of 24 exchange-listed and National Market System stocks, representing national money center banks and leading regional institutions.

The S&P 500® Index is float-adjusted market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance.

The MSCI AC World Ex Japan Index Gross USD is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets, excluding Japan. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with

respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

The STOXX Europe 600 (Price) Index is a broad based capitalization-weighted index of European stocks designed to provide a broad yet liquid representation of companies in the European region. The equities use free float shares in the index calculation. The index was developed with a base value of 100 as of December 31, 1991. This index uses float shares.

The Bovespa Index is a total return index weighted by traded volume and is comprised of the most liquid stocks traded on the Sao Paulo Stock Exchange.

The Hang Seng Property Index is a capitalization-weighted index of all the stocks designed to measure the performance of the property sector of the Hang Seng Index.

5

|

|

| Alpine Dynamic Dividend Fund |

|

|

| Alpine Accelerating Dividend Fund |

|

|

| Alpine Financial Services Fund |

|

|

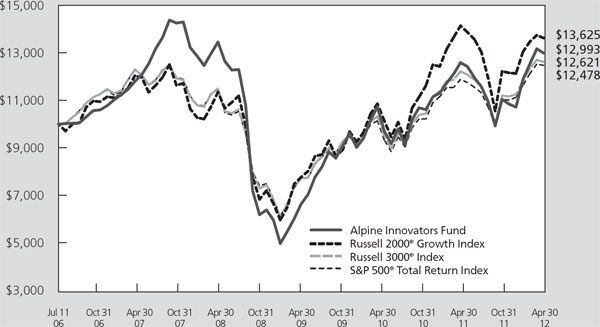

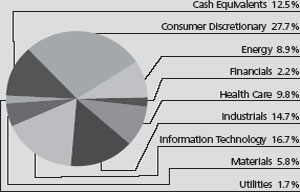

| Alpine Innovators Fund |

|

|

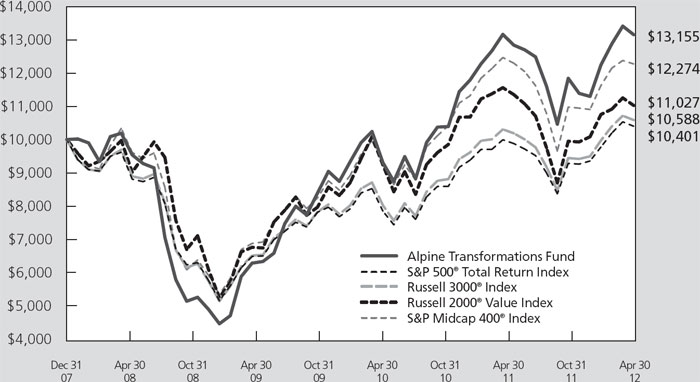

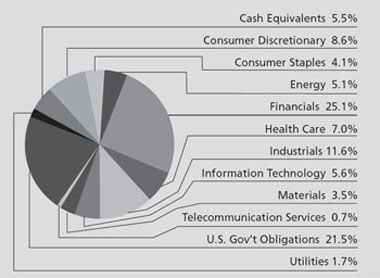

| Alpine Transformations Fund |

|

|

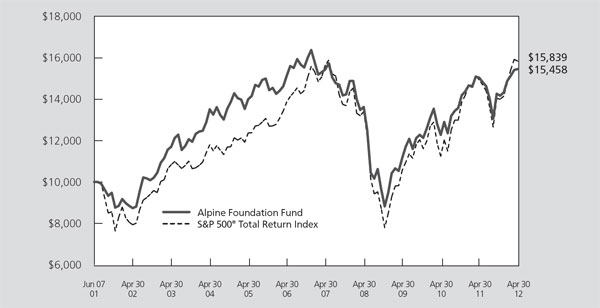

| Alpine Foundation Fund |

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Comparative Annualized Returns as of 4/30/12 (Unaudited) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 6 Months(1) |

| 1 Year |

| 3 Years |

| 5 Years |

| Since Inception |

| |||||

Alpine Dynamic Dividend Fund – Institutional |

| 3.61 | % |

| -17.86 | % |

| 9.99 | % |

| -8.63 | % |

| 3.28 | % |

|

S&P 500® TR (Total Return) Index |

| 12.77 | % |

| 4.76 | % |

| 19.46 | % |

| 1.00 | % |

| 5.65 | % |

|

STOXX Europe 600 Index(2) |

| 2.26 | % |

| -15.76 | % |

| 12.85 | % |

| -4.90 | % |

| 7.22 | % |

|

Lipper Global Multi-Cap Core Funds Average(3) |

| 6.64 | % |

| -5.80 | % |

| 16.37 | % |

| -1.21 | % |

| 5.56 | % |

|

Lipper Global Multi-Cap Core Funds Ranking(3) |

| N/A(4) |

| 158/159 |

| 128/130 |

| 95/95 |

| 44/47 |

| |||||

Gross Expense Ratio: 1.21%(5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.21%(5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

(1) Not annualized. | ||||||||||||||||

(2) The since inception return represents the annualized return for the period beginning 9/30/2003. | ||||||||||||||||

(3) The since inception return represents the annualized return for the period beginning 9/25/2003. | ||||||||||||||||

(4) FINRA does not recognize rankings for less than one year. | ||||||||||||||||

(5) As disclosed in the prospectus dated February 28, 2012. | ||||||||||||||||

| ||||||||||||||||

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 60 days. If it did, total returns would be reduced. | ||||||||||||||||

| ||||||||||||||||

Performance of Class A shares is not shown because this share class commenced operations on December 30, 2011. | ||||||||||||||||

| ||||||||||||||||

The S&P 500® TR (Total Return) Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The STOXX Europe 600 Index is derived from the STOXX Europe Total Market Index (TMI) and is a subset of the STOXX Global 1800 Index. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. The Lipper Global Multi-Cap Core Funds Average is an average of funds that, by portfolio practice, invest in a variety of market capitalization ranges without concentrating 75% of their equity assets in any one market capitalization range over an extended period of time. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500® TR (Total Return) Index, the STOXX Europe 600 Index and the Lipper Global Multi-Cap Core Funds Average are unmanaged and do not reflect the deduction of direct fees associated with a mutual fund, such as investment adviser fees; however, the Lipper Global Multi-Cap Core Funds Average reflects fees charged by the underlying funds. The performance for the Dynamic Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index. | ||||||||||||||||

| ||||||||||||||||

Expense Ratios reflect the ratios reported in the Fund’s most recent prospectus. The Alpine Dynamic Dividend Fund has a contractual expense waiver that continues through February 28, 2013. Where a Fund’s gross and net expense ratio are the same for the period reported, the contractual expense reimbursement level was not reached as of the end of that period. To the extent the Fund’s expenses were reduced by waivers, the Fund’s total returns were increased. In these cases, in the absence of the expense waivers, the Fund’s total returns would have been lower. | ||||||||||||||||

| ||||||||||||||||

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”) and/or secondary offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary allocations in the future. | ||||||||||||||||

7

|

|

Alpine Dynamic Dividend Fund |

|

|

|

|

|

|

|

|

|

|

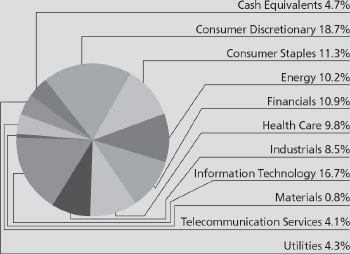

Portfolio Distributions* (Unaudited) | Top 10 Holdings* (Unaudited) |

|

| |||||

|

| 1. |

| Seadrill, Ltd. | 2.63% |

| ||

| 2. |

| Sara Lee Corp. | 2.60% |

| |||

3. |

| McDonald’s Corp. | 2.36% |

| ||||

4. |

| International Business |

|

| ||||

|

| Machines Corp. | 2.34% |

| ||||

5. |

| ITC Holdings Corp. | 2.22% |

| ||||

6. |

| QUALCOMM, Inc. | 2.16% |

| ||||

7. |

| JPMorgan Chase & Co. | 2.13% |

| ||||

8. |

| Tele2 AB-B Shares | 2.02% |

| ||||

9. |

| Wells Fargo & Co. | 2.01% |

| ||||

10. |

| Telefonaktiebolaget LM |

|

| ||||

|

| Ericsson-B Shares | 1.90% |

| ||||

|

|

|

| |||||

|

|

|

| |||||

| * | Top 10 Holdings do not include short-term investments and percentages are based on total net assets. Portfolio Distributions percentages are based on total investments. Portfolio holdings and sector distributions are as of 4/30/12 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. |

| |||||

|

|

|

|

| ||||

|

|

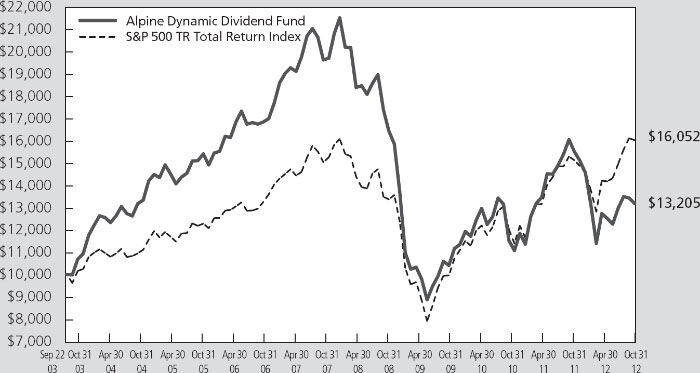

Value of a $10,000 Investment (Unaudited) |

|

|

|

|

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

8

|

|

Alpine Dynamic Dividend Fund |

|

|

Commentary |

PERFORMANCE

The Alpine Dynamic Dividend Fund completed first half fiscal 2012 with a total return of 3.61% including dividend reinvestments. The comparative returns of broad-based global indices for the same time period were +12.77% for the Standard & Poor’s 500 TR Total Return Index, +2.26% for the STOXX Europe 600 Index, and +7.66% return for the MSCI All Country World ex-Japan Index in U.S. dollar terms.

Our U.S. based holdings, which represented over 70% of the Fund’s assets on April 30, 2012, provided a solid return of 10.3% during the six months ended April 30, 2012. Our worst performing country was Brazil with only a 4.1% weighting in the Fund but a negative 20.88% return for the six months ended April 30, 2012. Even though our international weightings were not large, the correction in these markets in March and April has been deep and detrimental to the Fund.

DRIVERS OF PERFORMANCE

The performance of the Fund during the first half of fiscal 2012 could be attributed primarily to strong overall appreciation in our U.S. based assets but continued challenging performance in our investment positions in international markets. In comparison to the S&P 500 TR Total Return Index and many of our equity income peers, the Fund has a large portion of its assets invested overseas to help achieve our goal of high dividends and capital appreciation since the U.S. is one of the lowest yielding global equity markets. We do not actively manage our country weightings – we pick our holdings on a stock by stock basis based on dividend potential and total return. This bottom-up approach has historically taken a portion of our holdings to Europe, as the dividend payout ratios remain higher than any other region, in addition to finding what we believe are numerous compelling growth and income stories that have led us to invest in Asia and Latin America.

The U.S. and international markets reached the lows of the semi-annual reporting period in late November 2011 on fears of a global double dip recession and an escalation of the European sovereign debt crisis, The European Central Bank stepped in to prevent a worsening crisis by providing favorable financing to European banks on December 21, 2011 and again on February 29, 2012, known as the Long Term Refinancing Operation (or “LTRO”). This buoyed the international markets during that time period and stocks rallied. However, renewed concerns about the longer term

structural problems in Europe followed the second LTRO payment. Additionally, the slowdown in economic growth in countries like China and Brazil led to overall negative performance in many of the international and cyclical holdings in the portfolio in March and April, 2012, with the U.S. being viewed as a safe haven. From March 1, 2012, the day after the last LTRO payment, through the end of the first fiscal half of 2012 on April 30, 2012, the S&P 500 TR Total Return Index increased 2.01% versus the Brazilian Bovespa Index which declined 16.29%, the STOXX Europe 600 Index – which declined 3.25%, and the Hang Seng Index which declined by 1.01%. This particularly impacted the portfolio because of our long term emphasis on the search for high yielding, high quality securities overseas that were sold off despite attractive fundamentals and positive longer term growth and income opportunities.

We responded to the volatility in the markets and the outlook for subdued global economic growth by bringing more assets back to the U.S. We believe that many U.S. companies will continue to report strong earnings and cash flow in the months ahead and the U.S. will likely maintain its safe haven status. We ended fiscal first half 2012 with 70.6% of assets in U.S. based companies and 23.7% in companies based in 11 different countries, with 5.7% in cash and equivalents. Following the U.S., our top five countries by weight on April 30, 2012 were:

|

|

Sweden | 4.9% |

|

|

United Kingdom | 4.3% |

|

|

Brazil | 4.1% |

|

|

Norway | 2.6% |

|

|

Israel | 2.0% |

In addition, we shifted to higher quality and larger capitalization stocks, reviewed our economically sensitive stocks to look for growth based more on secular forces or innovation and less economic growth, and searched for companies we believe will continue to have strong margin improvements and productivity initiatives.

Given the continued uncertain outlook that still remains for the Euro region, we have strived to diversify our exposure in the region by moving away from companies with Euro denominated currencies. On April 30, 2012, approximately 13.6% of the Fund’s assets were invested in Europe, but only 1.2% in Euro denominated currencies, with the rest being in Norway, Sweden, Switzerland, and the UK. Our dividend capture strategy

9

|

|

Alpine Dynamic Dividend Fund |

|

tends to be seasonally focused in Europe in the spring and we hedged the currency exposure related to our dividend capture trades in Europe during this time. We have also continued to employ leverage in the execution of the Fund’s strategy both to increase returns and to manage unexpected cash inflows and outflows.

The Fund’s sector exposures and stock selection were also drivers of returns during the first half of fiscal 2012. We had eight sectors that provided positive total returns in the portfolio with the top two being Consumer Staples and Financials, with two sectors having negative performance – Materials and Telecom – which represented less than 7% of net assets combined.

TOP FIVE CONTRIBUTORS

The top five contributors to the Fund’s performance in first half fiscal 2012 based on contribution to total return were Sara Lee (25.33%), JPMorgan Chase (25.17%), Yum! Brands (36.64%), Seadrill (21.65%), and Wells Fargo (30.57%), with four of these five issues (excluding Yum!) included in the top 10 holdings;

|

|

|

| • | Sara Lee Corp. (average weight 2.22%) is a global food manufacturer that has plans to split into two companies on June 30, 2012 – a faster growing coffee business and a more mature meats business –and will pay shareholders a $3 special dividend at the time of the split. The stock has appreciated into the split as investors realize the value that will be unlocked by the action. In addition, we have a favorable view on the growth potential for the coffee business and the cost cutting potential at the meat company. |

|

|

|

| • | JPMorgan Chase (average weight 2.28%) and Wells Fargo (average weight 1.72%) are two of the largest banks in the U.S. and both benefited in first half fiscal 2012 from a rebound in financial stocks following the European Central Bank’s LTRO. Also, better economic data in the U.S. and a stabilization of the housing market also helped propel these financial stocks from the fears of a double dip recession in late 2011. |

|

|

|

| • | Seadrill (average weight 2.37%) is a global leader in the high-growth and technologically advanced deepwater and ultra-deepwater rig markets which are benefitting from strong demand in regions like Brazil, West Africa, and the Gulf of Mexico as oil is getting harder to find and exploration is moving further out to sea. With its new building program completed, Seadrill has committed to returning its strong free cash flow back to investors with very attractive dividend yields. |

|

|

|

| • | Yum! Brands (average weight 1.52%) operates a worldwide system of over 36,000 quick serve restaurants with their main brands being Taco Bell, Pizza Hut, and KFC. With about 75% of profits generated from international markets and substantial growth opportunities in countries like China, we believe YUM offers attractive access to the emerging consumer growth markets. |

|

|

|

| • | Wells Fargo (average weight 1.63%) is one of the largest banks in the U.S. that benefited in first half fiscal 2012 from a rebound in financial stocks following the European Central Bank’s LTRO. Also, better economic data in the U.S. and a stabilization of the housing market also helped propel these financial stocks from the fears of a double dip recession in late 2011. |

BOTTOM FIVE CONTRIBUTORS

The bottom five contributors that had the largest adverse impact on the performance of the Fund during fiscal first half 2012 were primarily international holdings in PDG Realty (-46.49%), Daqing Dairy (-47.06%), Suncor Energy (-18.16), Wynn Resorts (-13.37%), and MRV Engenharia e Participacoes (-17.93%). Unlike our top five performers, these underperformers represented relatively smaller positions in the portfolio, with four of the five (excluding PDG) having an average weight of less than 0.65% in the portfolio.

|

|

|

| • | PDG (average weight 1.66%) and MRV (average weight 0.44%) are two of Brazil’s largest home builders. We believe the home building sector in Brazil is an attractive high growth market due to rising discretionary income and subsidized government financing. Both companies experienced weak share performance in first half 2012 due to fears of rising interest rates and cost overruns which impacted profitability. We sold the shares in MRV but we believe PDG will have a turnaround in profitability in second half 2012 and we continue to hold the position. |

|

|

|

| • | Daqing Dairy (average weight 0.65%) is an ex-state owned enterprise that sells baby milk products in Tier 2 and Tier 3 cities in China. The company’s auditor resigned in March and the company’s shares have not traded since that time. The majority of the decline in value during the period is attributable to a 40% discount to its last traded price we have taken due to our concerns about the company’s disclosures and issues raised by their former auditors. Prior to the suspension of trading, the shares had declined by approximately 12%. |

10

|

|

Alpine Dynamic Dividend Fund |

|

|

|

|

| • | Wynn Resorts (average weight 0.20%) operates casinos and resorts in Las Vegas and Macau. We purchased the stock following its announcement of a special dividend payment of $5 per share, or about 4% of the stock price, in November 2011. However, the company has a higher percentage of VIP versus mass gaming exposure that was slower than expected in first half 2012 on the economic slowdown in China and there was more competitive pressure than anticipated. We no longer hold the shares. |

|

|

|

| • | Suncor Energy (average weight 0.31%) is an integrated energy company with a focus on developing the oil sands basin in Canada. We believed the company would benefit from the rise in crude prices at the time and its positive impact on the profitability of the oil sands region. However, as concerns of a double dip recession set in at the end of 2011, the stock sold off and we exited the stock. |

SUMMARY & OUTLOOK FOR THE MARKET AND ECONOMY

We remain cautious as we enter second half of 2012 based on uncertainty surrounding global economic growth and European financial risks, but we believe that the longer term outlook for dividend paying equities remains positive especially in the U.S. We expect continued volatility in the near term in equity markets as the four of the main pillars of global economic growth – the U.S., Europe, China, and Latin America – face significant challenges. We do see a number of positives offsetting these challenges, such as a decline in commodity and energy prices versus the first half of fiscal 2012 which should be a benefit for consumer spending and business input costs. In addition, the housing market in the U.S., which has been a drag on the economy for several years, appears to be stabilizing. And while sovereign nations are struggling with large debt burdens, corporate balance sheet quality is high and companies are sitting on record amounts of cash which should support capital growth initiatives, mergers and acquisitions, and the return of cash to shareholders via share buybacks and dividend increases, if we can see some clarity coming out of Europe and volatility declines.

Over the long term, we continue to remain optimistic that dividend stocks will attract increasing amounts of capital as investors around the world search for income. Global demographics point to an aging population in the industrialized world and these millions of savers are facing zero to low interest rates for quarters or potentially years to come. For example, the U.S. in the 1930’s and Japan in the past 20 years have shown that when interest rates go close to zero they can stay there for extended periods of time until structural economic issues are resolved. Since the year 2000, dividends (including the reinvestment of those dividends) – not stock price appreciation – are the reasons for the S&P 500’s positive return. Without these dividends, the price of the S&P 500 Index declined by -4.86% but with reinvested dividends the total return for the S&P 500 is 19.47%.

The Fund was initiated in September 2003 to provide investors with a vehicle to benefit from the reduced U.S. Federal tax rates on dividends or Qualified Dividend Income (“QDI”). This tax benefit is set to expire on December 31, 2012, and there is uncertainty on the level of taxation for dividends going forward. However, even if the tax benefits are not renewed, we do not intend to materially change our strategy. If the QDI benefit is eliminated, we will not have the constraint of the 61-day holding period required to be eligible for the tax benefit. In addition, we could look to expand our dividend capture opportunities in different non-tax qualified equity markets (i.e. Hong Kong, Taiwan) or non-qualified equity payers such as most Real Estate Investment Trusts (“REITS”) and Master Limited Partnerships (“MLPs”).

Our goals remain clear. We intend to continue to seek to provide high current income and grow our Net Asset Value over the long term and we seek to achieve these goals with lower volatility than we have seen over the past several years as we strive to be the dividend income fund of choice for investors. Thank you for your support of the Alpine Dynamic Dividend Fund.

Sincerely,

Jill K. Evans and Kevin Shacknofsky

Co-Portfolio Managers

11

|

|

Alpine Dynamic Dividend Fund |

|

|

|

| |

Mutual fund investing involves risk. Principal loss is possible. The Fund is subject to the following risks: | |

Credit Risk – Credit risk refers to the possibility that the issuer of a security will not be able to make payments of interest and principal when due. Changes in an issuer’s credit rating or the market’s perception of an issuer’s creditworthiness may also affect the value of the Fund’s investment in that issuer. The degree of credit risk depends on both the financial condition of the issuer and the terms of the obligation.

Dividend Strategy Risk – The Fund’s strategy of investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperforms the market. Companies that issue dividend paying-stocks are not required to continue to pay dividends on such stocks. Therefore, there is the possibility that such companies could reduce or eliminate the payment of dividends in the future or the anticipated acceleration of dividends could not occur.

Emerging Market Securities Risk – The risks of investing in foreign securities can be intensified in the case of investments in issuers domiciled or operating in emerging market countries. These risks include lack of liquidity and greater price volatility, greater risks of expropriation, less developed legal systems and less reliable custodial services and settlement practices.

Equity Securities Risk – The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company (such as poorer than expected earnings or certain management decisions) or to the industry in which the company is engaged (such as a reduction in the demand for products or services in a particular industry).

Foreign Currency Transactions Risk – Foreign securities are often denominated in foreign currencies. As a result, the value of the Fund’s shares is affected by changes in exchange rates. A Fund may enter into foreign currency transactions to try to manage this risk. A Fund’s ability to use foreign currency transactions successfully depends on a number of factors, including the foreign currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the portfolio managers to accurately predict the direction of changes in currency exchange rates.

Foreign Securities Risk – Public information available concerning foreign issuers may be more limited than would be with respect to domestic issuers. Different accounting standards may be used by foreign issuers, and foreign trading markets may not be as liquid as U.S. markets. Currency fluctuations could erase investment gains or add to investment losses. Additionally, foreign securities also involve possible imposition of withholding or confiscatory taxes and adverse political or economic developments. These risks may be greater in emerging markets.

Growth Stock Risk – Growth stocks are stocks of companies believed to have above-average potential for growth in revenue and earnings. Growth stocks typically are very sensitive to market movements because their market prices tend to reflect future expectations. When it appears those expectations will not be met, the prices of growth stocks typically fall. Growth stocks as a group may be out of favor and underperform the overall equity market while the market concentrates on undervalued stocks.

Leverage Risk – The Fund may use leverage to purchase securities. Increases and decreases in the value of the Fund’s portfolio will be magnified when the Fund uses leverage.

Management Risk – The Adviser’s judgment about the quality, relative yield or value of, or market trends affecting, a particular security or sector, or about interest rates generally, may be incorrect. The Adviser’s security selections and other investment decisions might produce losses or cause the Fund to underperform when compared to other funds with similar investment objectives and strategies.

Market Risk – The price of a security held by the Fund may fall due to changing market, economic or political conditions.

Micro Capitalization Company Risk – Investments in micro-cap companies are associated with similar risks as investments in small and medium capitalization companies, but these risks may be even greater with respect to investments in micro-cap companies.

Portfolio Turnover Risk – High portfolio turnover necessarily results in greater transaction costs which may reduce Fund performance.

12

|

|

Alpine Dynamic Dividend Fund |

|

Qualified Dividend Tax Risk – Favorable U.S. federal tax treatment of Fund distributions may be adversely affected, changed or repealed by future changes in tax laws. Under current law, favorable U.S. federal tax treatment of Fund distributions as qualified dividend income will expire as of December 31, 2012 unless new legislations extending that deadline is enacted.

Small and Medium Capitalization Company Risk – Securities of small or medium capitalization companies are more likely to experience sharper swings in market values, less liquid markets, in which it may be more difficult for the Adviser to sell at times and at prices that the Adviser believes appropriate and generally are more volatile than those of larger companies.

Swaps Risk – Swap agreements are derivative instruments that can be individually negotiated and structured to address exposure to a variety of different types of investments or market factors. Depending on their structure, swap agreements may increase or decrease a Fund’s exposure to long- or short-term interest rates, foreign currency values, mortgage securities, corporate borrowing rates, or other factors such as security prices or inflation rates. A Fund also may enter into swaptions, which are options to enter into a swap agreement. Since these transactions generally do not involve the delivery of securities or other underlying assets or principal, the risk of loss with respect to swap agreements and swaptions generally is limited to the net amount of payments that the Fund is contractually obligated to make. There is also a risk of a default by the other party to a swap agreement or swaption, in which case a Fund may not receive the net amount of payments that such Fund contractually is entitled to receive.

Undervalued Stock Risk – Undervalued stocks may perform differently from the market as a whole and may continue to be undervalued by the market for long periods of time. Although the Fund will not concentrate its investments in any one industry or industry groups, it may weigh its investments towards certain industries, thus increasing its exposure to factors adversely affecting issues within these industries.

Please refer to pages 4-5 for other important disclosures and definitions.

13

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Comparative Annualized Returns as of 4/30/12 (Unaudited) | |||||||||||||

|

| 6 Months(1) |

| 1 Year |

| 3 Years |

| Since Inception |

| ||||

Alpine Accelerating Dividend Fund – Institutional |

| 10.24 | % |

| 0.79 | % |

| 16.60 | % |

| 13.67 | % |

|

S&P 500® TR (Total Return) Index |

| 12.77 | % |

| 4.76 | % |

| 19.46 | % |

| 12.38 | % |

|

Dow Jones Industrial Average |

| 12.04 | % |

| 5.98 | % |

| 20.65 | % |

| 12.72 | % |

|

Lipper Equity Income Funds Average(2) |

| 10.34 | % |

| 2.51 | % |

| 18.21 | % |

| 14.45 | % |

|

Lipper Equity Income Funds Ranking(2) |

| N/A(3) |

| 211/296 |

| 209/250 |

| 169/248 |

| ||||

Gross Expense Ratio: 2.64%(4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.35%(4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) Not annualized. |

(2) The since inception data represents the period beginning 11/6/2008. |

(4) As disclosed in the prospectus dated February 28, 2012. |

|

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 60 days. If it did, total returns would be reduced. |

|

Performance of Class A shares is not shown because this share class commenced operations on December 30, 2011. |

|

The S&P 500® TR (Total Return) Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Dow Jones Industrial Average is a price weighted average of 30 actively traded shares of large cap U.S. industrial corporations. The Lipper Equity Income Funds Average is an average of Funds that seek relatively high current income and income growth through investing 60% or more of their respective portfolios in equities. Lipper rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500® TR (Total Return) Index, the Dow Jones Industrial Average, and the Lipper Equity Income Funds Average are unmanaged and do not reflect direct fees associated with a mutual fund, such as investment adviser fees; however, the Lipper Equity Income Funds Average reflects fees charged by the underlying funds. The performance for the Accelerating Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index. |

|

Expense Ratios reflect the ratios reported in the Fund’s most recent prospectus. The Accelerating Dividend Fund has a contractual expense waiver that continues through February 28, 2013. Where a Fund’s gross and net expense ratio are the same for the period reported, the contractual expense reimbursement level was not reached as of the end of that period. To the extent the Fund’s expenses were reduced by waivers, the Fund’s total returns were increased. In these cases, in the absence of the expense waivers, the Fund’s total returns would have been lower. |

|

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”) and/or secondary offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary allocations in the future. |

|

|

|

|

|

|

|

|

| |||||||

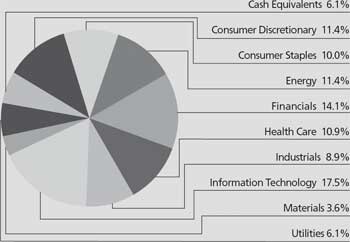

Portfolio Distributions* (Unaudited) |

| Top 10 Holdings* (Unaudited) |

|

| |||

|

| 1. |

| Teva Pharmaceutical |

|

| |

|

|

| Industries, Ltd.-ADR | 2.03% |

| ||

| 2. |

| QUALCOMM, Inc. | 1.89% |

| ||

| 3. |

| Abbott Laboratories | 1.83% |

| ||

| 4. |

| PepsiCo, Inc. | 1.83% |

| ||

| 5. |

| General Mills, Inc. | 1.80% |

| ||

| 6. |

| OGE Energy Corp. | 1.79% |

| ||

| 7. |

| Intel Corp. | 1.78% |

| ||

| 8. |

| Microsoft Corp. | 1.77% |

| ||

| 9. |

| International Business |

|

| ||

|

|

| Machines Corp. | 1.76% |

| ||

| 10. |

| Becton, Dickinson & Co. | 1.74% |

| ||

|

|

|

|

| |||

|

|

|

| ||||

| * | Top 10 Holdings do not include short-term investments and percentages are based on total net assets. Portfolio Distributions percentages are based on total investments. Portfolio holdings and sector distributions are as of 4/30/12 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. |

| ||||

|

|

|

|

|

|

| |

14

|

|

Alpine Accelerating Dividend Fund |

|

|

|

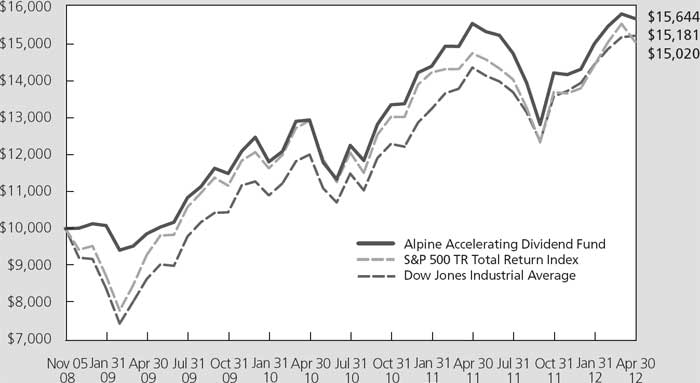

Value of a $10,000 Investment (Unaudited) |

|

|

|

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

|

Commentary |

For the six months ended April 30, 2012 the Alpine Accelerating Dividend Fund generated a total return of 10.24%. This compares with a total return of 12.77% for the Standard & Poor’s 500 TR Total Return Index for the same period. Since inception, the Alpine Accelerating Dividend Fund has generated an annualized total return of 13.67% versus an annualized return of 12.38% for the Standard & Poor’s 500. During the last six months, the Fund steadily increased its monthly payout from $0.0385 to $0.0391 per share.

PERFORMANCE DRIVERS

The Fund generally prefers to take a conservative investment stance with regard to portfolio construction and security selection during times of economic and geopolitical uncertainty. For example, the Fund had an average cash holding of 7.2% during the six months ended April 30, 2012 and a portfolio beta of less than 1.0 during the same span. While this conservative investment posture may perform well in choppy markets, it is also likely to lag a broader market rally such as the one that unfolded during the first half of the fiscal year.

|

|

|

| • | The 7.2% average cash holding detracted from the Fund’s performance relative to the S&P 500, its benchmark, in the first half of fiscal 2012. |

|

|

|

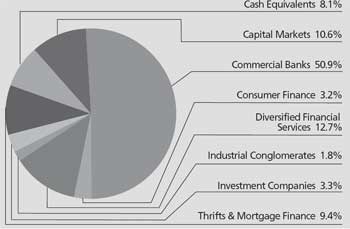

| • | On a sector basis, the financial sector (average weight 13.82%) enjoyed a strong rally and was the Fund’s top contributor. The Information Technology (average weight 16.59%) and Health Care (average weight 10.66%) sectors were also strong performers in the period. Meanwhile, Materials (average weight 4.09%) and Consumer Discretionary (average weight 11.19%) were among our worst performing groups. Utilities (average weight 5.79%) also underperformed during the period as investors took profits after a strong 2011. |

PORTFOLIO ANALYSIS

The top five contributors to the Fund’s performance during the six months ended April 30, 2012, based on contribution to total return were Anheuser-Busch InBev (+33.73%), Huntington Bancshares (+32.58%), Dick’s Sporting Goods (+45.47%), Comcast (+30.08%), and Visa (+32.59%).

15

|

|

Alpine Accelerating Dividend Fund |

|

|

|

|

| • | Anheuser Busch InBev N.V. (average weight 1.67%) was the top contributor to the Fund’s performance over the period as the company executed on its cost improvement plan and began to generate volume growth in many of its markets. |

|

|

|

| • | A better than expected first quarter earnings report highlighted by strong loan growth along with an attractive valuation helped Huntington Bancshares (average weight 1.57%) shake off some investor disappointment from the prior quarter’s results and led to a strong rally in the shares. |

|

|

|

| • | Dick’s Sporting Goods (average weight 0.80%) was able to post strong earnings results despite warm weather throughout the winter selling season. The company continues to benefit from the strength of the athletic cycle in apparel and footwear. |

|

|

|

| • | Comcast’s (average weight 1.66%) core cable operations continue to generate strong results, with stable subscriber additions and rising average revenue per user. Meanwhile, the acquired NBCU assets are largely integrated into the business and some progress toward a turnaround at the unit is being made. |

|

|

|

| • | Visa (average weight 1.47%) registered above plan financial results driven by strong global transaction volume growth. Near term, there may be some confusion in the numbers due to the changing regulatory landscape but as the world transitions to digital payments, Visa’s network is poised to benefit. |

|

|

|

PDG Realty (-47.28%), Pace PLC (-52.16%), Potash Corporation of Saskatchewan (-9.32%), Ceradyne (-15.55%), and Guess? (-4.33%) had the largest adverse impact on the performance of the Fund over the first half of the fiscal year. | ||

|

|

|

| • | PDG Realty (average weight 0.79%), suffered a combination of falling earnings estimates and multiple contraction due to poor management of its outsourced construction projects. This margin pressure, along with a slower pace of new launches has led to a reduced earnings growth profile for this Brazilian homebuilder. |

|

|

|

| • | Pace PLC (average weight 0.06%), one of the leading set-top box manufacturers for digital television was negatively impacted by the floods in Thailand that dramatically reduced the availability and supply of hard disk drives, leading to reduced sales and lower margins. |

|

|

|

| • | Potash Corporation of Saskatchewan (average weight 1.52%) declined as the fertilizer market struggled to find equilibrium with large buyers such as China and India delaying purchases and customers working down inventories, causing the company to curtail potash production at some of its mines. |

|

|

|

| • | Ceradyne’s (average weight 0.19%) crucible business serving the solar industry has been hard hit by the oversupply of solar wafer inventory at its customers that has yet to be worked down to normal levels. The decline in solar sales together with some delayed shipments of body armor to the US military led to disappointing first quarter results for the company. |

|

|

|

| • | Guess? (average weight 0.57%), with over a quarter of its sales in Southern Europe, continues to languish under a tepid consumer spending atmosphere in the region. In addition, a highly promotional pricing environment in the US has hampered sales domestically. |

SUMMARY & OUTLOOK

The Accelerating Dividend Fund seeks to invest in dividend-paying companies which we believe have the potential to increase or accelerate their dividends in the future, based on our analysis of their growth prospects and cash flow generating capabilities. The Fund aims to achieve a sustainable and rising stream of dividend income as well as long-term capital appreciation. We believe that companies with strong franchises characterized by defensible margins and a solid balance sheet are best positioned to increase, and even accelerate, their dividends over time. While the Fund concentrates its investment in the US, we believe there is also great potential for accelerating dividend ideas in the developing world. In the first half of fiscal year 2012, the Fund had an average exposure to Brazil of 3.60%. Overall, we aim to manage the fund conservatively by limiting our international exposure, eschewing the use of leverage, and avoiding large sector bets when possible.

As we look towards the balance of 2012, we remain cautious in our investment stance. The geopolitical environment remains unsettled and there is a great deal of uncertainty as to the strength and durability of the economic recovery underway in the US and Europe. As such, we believe that dividend income may become a key signpost for investors to gauge the true financial strength of companies. In a world currently offering low single digit yields on safe investments, companies with

16

|

|

Alpine Accelerating Dividend Fund |

|

track records of increasing dividends could be the winners in the equity market, in our view. As a result, we are sticking to our knitting – we believe a strategy that seeks to identify stocks with rising dividends as well as those with the potential to not only increase the dividend, but to do so at an accelerating pace, is well positioned to succeed in the uncertain market environment in which we currently find ourselves and to potentially outperform over time. Likewise, we think the Fund offers investors an attractive combination of

current yield with the potential for increasing payouts over time.

We thank our shareholders for their support and look forward to continued success over the next year.

Sincerely,

Bryan Keane

Andrew Kohl

Co-Portfolio Managers

|

|

| |

Mutual fund investing involves risk. Principal loss is possible. The Fund is subject to the following risks: | |

Dividend Strategy Risk – The Fund’s strategy of investing in dividend-paying stocks involves the risk that such stocks may fall out favor with investors and underperforms the market. Companies that issue dividend paying-stocks are not required to continue to pay dividends on such stocks. Therefore, there is the possibility that such companies could reduce or eliminate the payment of dividends in the future or the anticipated acceleration of dividends could not occur.

Equity Securities Risk – The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company (such as poorer than expected earnings or certain management decisions) or to the industry in which the company is engaged (such as a reduction in the demand for products or services in a particular industry).

Foreign Currency Transactions – Foreign securities are often denominated in foreign currencies. As a result, the value of the Fund’s shares is affected by changes in exchange rates. A Fund may enter into foreign currency transactions to try to manage this risk. A Fund’s ability to use foreign currency transactions successfully depends on a number of factors, including the foreign currency transactions being available at prices that are not too costly, the availability of liquid markets and the ability of the portfolio managers to accurately predict the direction of changes in currency exchange rates.

Foreign Securities Risk – Public information available concerning foreign issuers may be more limited than would be with respect to domestic issuers. Different accounting standards may be used by foreign issuers, and foreign trading markets may not be as liquid as U.S. markets. Currency fluctuations could erase investment gains or add to investment losses. Additionally, foreign securities also involve possible imposition of withholding or confiscatory taxes and adverse political or economic developments. These risks may be greater in emerging markets.

Growth Stock Risk – Growth stocks typically are very sensitive to market movements because their market prices tend to reflect future expectations. When it appears those expectations will not be met, the prices of growth stocks typically fall. Growth stocks as a group may be out of favor and underperform the overall equity market while the market concentrates on undervalued stocks. Although the Fund will not concentrate its investments in any one industry or industry group, it may, like many growth funds, weight its investments toward certain industries, thus increasing its exposure to factors adversely affecting issuers within those industries.

Management Risk – The Adviser’s judgment about the quality, relative yield or value of, or market trends affecting, a particular security or sector, or about interest rates generally, may be incorrect. The Adviser’s security selections and other investment decisions might produce losses or cause the Fund to underperform when compared to other funds with similar investment objectives and strategies.

Market Risk – The price of a security held by the Fund may fall due to changing market, economic or political conditions.

Micro Capitalization Company Risk – The Fund may invest in the stocks of micro-cap companies with capitalizations under $100 million. Investments in micro-cap companies are associated with similar risks as investments in small and medium capitalization companies, but these risks may be even greater with respect to investments in micro-cap companies. Accordingly, the stocks of micro-cap companies may be more volatile and more thinly traded, and therefore more illiquid, than stocks of companies with larger capitalizations.

Portfolio Turnover Risk – High portfolio turnover necessarily results in greater transaction costs which may reduce Fund performance.

17

|

|

Alpine Accelerating Dividend Fund |

|

Small and Medium Capitalization Company Risk – Securities of small or medium capitalization companies are more likely to experience sharper swings in market values, less liquid markets, in which it may be more difficult for the Adviser to sell at times and at prices that the Adviser believes appropriate and generally are more volatile than those of larger companies.

Undervalued Stock Risk – Undervalued stocks may perform differently from the market as a whole and may continue to be undervalued by the market for long periods of time. Although the Fund will not concentrate its investments in any one industry or industry groups, it may weigh its investments towards certain industries, thus increasing its exposure to factors adversely affecting issues within these industries.

Please refer to pages 4-5 for other important disclosures and definitions.

18

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Comparative Annualized Returns as of 4/30/12 (Unaudited) | ||||||||||||||||

|

| 6 Months(1) |

| 1 Year |

| 3 Years |

| 5 Years |

| Since Inception |

| |||||

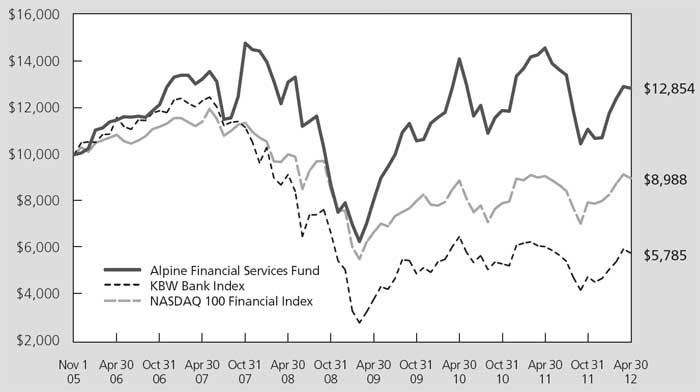

Alpine Financial Services Fund – Institutional |

| 15.94 | % |

| -11.81 | % |

| 16.85 | % |

| -0.60 | % |

| 3.94 | % |

|

KBW Bank IndexSM |

| 21.69 | % |

| -4.39 | % |

| 15.34 | % |

| -13.95 | % |

| -8.08 | % |

|

NASDAQ 100 Financial Services IndexSM |

| 13.00 | % |

| -1.06 | % |

| 10.45 | % |

| -4.66 | % |

| -1.63 | % |

|

S&P 500® TR (Total Return) Index |

| 12.77 | % |

| 4.76 | % |

| 19.46 | % |

| 1.00 | % |

| 4.47 | % |

|

Lipper Financial Services Funds Average(2) |

| 14.79 | % |

| -3.37 | % |

| 12.23 | % |

| -8.44 | % |

| -3.82 | % |

|

Lipper Financial Services Funds Ranking(2) | N/A | (3) |

| 75/78 |

|

| 7/69 |

|

| 4/64 |

|

| 3/53 |

| ||

Gross Expense Ratio: 1.86%(4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.45%(4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) Not annualized. |

(2) The since inception data represents the period beginning 11/03/2005. |

(3) FINRA does not recognize rankings for less than one year. |

(4) As disclosed in the prospectus dated February 28, 2012. |

|

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 60 days. If it did, total returns would be reduced. |

|

Performance of Class A shares is not shown because this share class commenced operations on December 30, 2011. |

|

The KBW Bank IndexSM is a modified cap-weighted index consisting of 24 exchange-listed and National Market System stocks, representing national money center banks and leading regional institutions. The NASDAQ 100 Financial Services IndexSM is a capitalization-weighted index of the 100 largest financial companies, as well as foreign issues, including American Depository Receipts (ADRs), traded on the NASDAQ National Market System (NASDAQ/NMS) and Small Cap Market. The S&P 500® TR (Total Return) Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Lipper Financial Services Funds Average is an average of funds whose primary objective is to invest primarily in equity securities of companies engaged in providing financial services. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The KBW Bank IndexSM, the NASDAQ 100 Financial Services IndexSM, the S&P 500® TR (Total Return) Index and the Lipper Financial Services Funds Average are unmanaged and do not reflect the deduction of direct fees associated with a mutual fund, such as investment adviser fees; however, the Lipper Financial Services Fund Average reflects fees charged by the underlying funds. The performance for the Dynamic Financial Services Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index. |

|

Expense Ratios reflect the ratios reported in the Fund’s most recent prospectus. The Financial Services Fund has a contractual expense waiver that continues through February 28, 2013. Where a Fund’s gross and net expense ratio are the same for the period reported, the contractual expense reimbursement level was not reached as of the end of that period. To the extent the Fund’s expenses were reduced by waivers, the Fund’s total returns were increased. In these cases, in the absence of the expense waivers, the Fund’s total returns would have been lower. |

|