United States

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F/A

Amendment No. 1

| | | | | | | | | | | | |

(Mark One) | |

| | | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | | OR |

| X | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | | For the fiscal year ended____November 30, 2007__________________________________ |

| | | OR |

| | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | | OR |

| | | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | | Date of event requiring this shell company report . . . . . . . . . . . . . . . . . . . |

| | | |

| | | For the transition period from ________________ to ______________________ |

| | | |

Commission file number | 0-31172 | | |

| | | |

ALBERTA STAR DEVELOPMENT CORP. |

(Exact name of registrant as specified in this charter) |

Province of Alberta, Canada |

(Jurisdiction of incorporation or organization) |

506 – 675 West Hastings Street, Vancouver, British Columbia V6B 1N2 Canada |

(Address of principal executive offices) |

Securities registered or to be registered pursuant to section 12(b) of the Act:

|

| Title of each Class | | Name of each exchange on which registered | |

| None | | Not Applicable | |

|

Securities registered or to be registered pursuant to Section 12(g) of the Act:

|

| Common Shares Without Par Value | |

| (Title of Class) | |

Securities registered or to be registered pursuant to Section 15(D) of the Act:

|

| None | |

| (Title of Class) |

|

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close |

1

| | | | | | | | | | | | | | | |

Of the period covered by the annual report. | 104,536,561 |

| |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. |

| Yes | | | No | X |

If this report is an annual or transitional report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. |

| Yes | | | No | X |

| |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. |

| Yes | X | | No | |

| |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” on Rule 12b-2 of the Exchange Act. (Check One): |

|

Large accelerated filer | | | Accelerated filer | | | Non-accelerated filer | X |

|

Indicate by check mark which financial statement item the registrant has elected to follow. |

| Item 17 | X | | Item 18 | |

|

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). |

| Yes | | | No | X |

2

TABLE OF CONTENTS

| PART I | | 5 |

| |

| ITEM 1 – IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 5 |

| ITEM 2 – OFFER STATISTICS AND EXPECTED TIMETABLE | 5 |

| ITEM 3 – KEY INFORMATION | 5 |

| A. | Selected Financial Data | 5 |

| B. | Capitalization and Indebtedness | 6 |

| C. | Reasons for the Offer and Use of Proceeds | 6 |

| D. | Risk Factors | 6 |

| ITEM 4 – INFORMATION ON THE COMPANY | 10 |

| A. | History and Development of the Company | 10 |

| B. | Business Overview | 11 |

| C. | Organizational Structure | 12 |

| D. | Property, Plants and Equipment | 12 |

| ITEM 4A - UNRESOLVED STAFF COMMENTS | 51 |

| ITEM 5 - OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 52 |

| A. | Operating Results | 53 |

| B. | Liquidity and Capital Resources | 54 |

| C. | Research and Development, Patents and Licenses, etc | 58 |

| D. | Trend Information | 58 |

| E. | Off-balance Sheet Arrangements | 58 |

| F. | Tabular Disclosure of Contractual Obligations | 58 |

| G. | Safe Harbour | 58 |

| ITEM 6 - DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 58 |

| A. | Directors and Senior Management | 58 |

| B. | Compensation | 61 |

| C. | Board Practices | 62 |

| D. | Employees | 63 |

| E. | Share Ownership | 64 |

| ITEM 7 - MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 65 |

| A. | Major Shareholders | 65 |

| B. | Related Party Transactions | 66 |

| C. | Interests of Experts and Counsel | 67 |

| ITEM 8 - FINANCIAL INFORMATION | 68 |

| A. | Consolidated Statements and Other Financial Information | 68 |

| B. | Significant Changes | 68 |

| ITEM 9 - THE OFFER AND LISTING | 68 |

| A. | Offer and Listing Details | 68 |

| B. | Plan of Distribution | 70 |

| C. | Markets | 70 |

| D. | Selling Shareholders | 70 |

| E. | Dilution | 70 |

| F. | Expenses of the Issue | 70 |

| ITEM 10 - ADDITIONAL INFORMATION | 70 |

| A. | Share Capital | 70 |

| B. | Memorandum and Articles of Association | 70 |

| C. | Material Contracts | 70 |

| D. | Exchange Controls | 71 |

| E. | Taxation | 71 |

| F. | Dividends and Paying Agents | 72 |

| G. | Statement by Experts | 72 |

| H. | Documents on Display | 72 |

| I. | Subsidiary Information | 72 |

| ITEM 11 - QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 72 |

| ITEM 12 - DESCRIPTIONS OF SECURITIES OTHER THAN EQUITY SECURITIES | 73 |

| |

| PART II | | 73 |

| |

| ITEM 13 - DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 73 |

3

| |

| ITEM 14 - MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 73 |

| ITEM 15 - CONTROLS AND PROCEDURES | 73 |

| A. | Disclosure Controls and Procedures | 73 |

| B. | Management’s Annual Report on Internal Control over Financial Reporting | 73 |

| C. | Attestation Report of the Registered Public Accounting Firm | 74 |

| D. | Changes in Internal Control Over Financial Reporting | 74 |

| ITEM 16A - AUDIT COMMITTEE FINANCIAL EXPERT | 74 |

| ITEM 16B - CODE OF ETHICS | 74 |

| ITEM 16C - PRINCIPAL ACCOUNTANT FEES AND SERVICES | 74 |

| ITEM 16D - EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 76 |

| ITEM 16E - PURCHASES OF EQUITY SECURITIES BY THE ISSUERS AND AFFILIATED PURCHASERS |

| | | 76 |

| |

| PART III | | 76 |

| |

| ITEM 17 - FINANCIAL STATEMENTS | 76 |

| ITEM 18 - FINANCIAL STATEMENTS | 124 |

| ITEM 19 - EXHIBITS | 124 |

| SIGNATURE | 125 |

4

FORWARD-LOOKING STATEMENTS

We caution you that certain important factors (including without limitation those set forth in this Form 20-F) may affect our actual results and could cause such results to differ materially from any forward-looking statements that may be deemed to have been made in this Form 20-F annual report, or that are otherwise made by or on our behalf. For this purpose, any statements contained in this annual report that are not statements of historical fact may be deemed to be forward-looking statements. Without limiting the generality of the foregoing, words such as “may,” “except,” “believe,” “anticipate,” “intend,” “could,” estimate,” or “continue,” or the negative or other variations of comparable terminology, are intended to identify forward-looking statements.

PART I

ITEM 1 – Identity of Directors, Senior Management and Advisers

All items in this section are not required, as this 20-F filing is made as an annual report.

ITEM 2 – Offer Statistics and Expected Timetable

All items in this section are not required, as this 20-F filing is made as an annual report.

ITEM 3 – Key Information

A.

Selected Financial Data

The following tables set forth the data of our fiscal years ended November 30, 2007, 2006, 2005, 2004, and 2003. We derived all figures from our financial statements as prepared by our management, approved by our audit committee and audited by our independent auditor. This information should be read in conjunction with our financial statements included in this annual report.

Our financial statements included in this annual report have been prepared in accordance with accounting principles generally accepted (“GAAP”) in Canada. All amounts are expressed in Canadian dollars. The first table presents this financial data in accordance with United States (“US”) GAAP; the second table presents the data in accordance with Canadian GAAP.

All amounts within this annual report are in Canadian funds (CDN), unless otherwise indicated.

| US GAAP | | | | | Fiscal Year Ended November 30 | | | | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Net operating revenue | | Nil | | | Nil | | | Nil | | | Nil | | | Nil | |

| Loss from operations | ($ | 14,784,688 | ) | ($ | 13,060,169 | ) | ($ | 2,832,810 | ) | ($ | 1,889,340 | ) | ($ | 2,043,936 | ) |

| Loss from continuing operations | ($ | 14,784,688 | ) | ($ | 13,060,169 | ) | ($ | 2,832,810 | ) | ($ | 1,889,340 | ) | ($ | 2,043,936 | ) |

| Comprehensive loss for the year | ($ | 14,870,688 | ) | ($ | 13,022,169 | ) | ($ | 2,784,810 | ) | ($ | 1,889,340 | ) | ($ | 2,043,936 | ) |

| Loss from operations per share | ($ | 0.15 | ) | ($ | 0.16 | ) | ($ | 0.06 | ) | ($ | 0.07 | ) | ($ | 0.13 | ) |

| Loss from continuing operations per share | ($ | 0.15 | ) | ($ | 0.16 | ) | ($ | 0.06 | ) | ($ | 0.07 | ) | ($ | 0.13 | ) |

| Total assets | $ | 24,384,800 | | $ | 30,798,020 | | $ | 11,978,824 | | $ | 2,155,878 | | $ | 442,927 | |

| Net assets | $ | 22,758,444 | | $ | 30,332,098 | | $ | 11,899,236 | | $ | 2,071,876 | | $ | 157,242 | |

| Capital stock | $ | 59,680,456 | | $ | 52,469,422 | | $ | 20,976,391 | | $ | 8,316,221 | | $ | 4,512,247 | |

| Number of shares | | 104,536,561 | | | 96,251,717 | | | 70,914,983 | | | 37,527,290 | | | 20,735,499 | |

| Dividends per common share | | Nil | | | Nil | | | Nil | | | Nil | | | Nil | |

| Diluted net income (loss) per share | ($ | 0.15 | ) | ($ | 0.16 | ) | ($ | 0.06 | ) | ($ | 0.07 | ) | ($ | 0.13 | ) |

5

| Canadian GAAP | | | | | Fiscal Year Ended November 30 | | | | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

| Net operating revenue | | Nil | | | Nil | | | Nil | | | Nil | | | Nil | |

| Loss from operations | ($ | 7,916,250 | ) | ($ | 11,630,209 | ) | ($ | 2,832,810 | ) | ($ | 957,202 | ) | ($ | 1,941,606 | ) |

| Loss from continuing operations | ($ | 7,916,250 | ) | ($ | 11,630,209 | ) | ($ | 2,832,810 | ) | ($ | 957,202 | ) | ($ | 1,941,606 | ) |

| Comprehensive loss for the year | ($ | 7,916,250 | ) | ($ | 11,630,209 | ) | ($ | 2,832,810 | ) | ($ | 957,202 | ) | ($ | 1,941,606 | ) |

| Loss from operations per share | ($ | 0.079 | ) | ($ | 0.139 | ) | ($ | 0.064 | ) | ($ | 0.035 | ) | ($ | 0.123 | ) |

| Loss from continuing operations per share | ($ | 0.079 | ) | ($ | 0.139 | ) | ($ | 0.064 | ) | ($ | 0.035 | ) | ($ | 0.123 | ) |

| Total assets | $ | 24,384,800 | | $ | 30,798,020 | | $ | 11,978,824 | | $ | 2,155,878 | | $ | 442,927 | |

| Net assets | $ | 22,758,444 | | $ | 30,332,098 | | $ | 11,899,236 | | $ | 2,071,876 | | $ | 224,842 | |

| Capital stock | $ | 50,118,414 | | $ | 49,775,818 | | $ | 19,712,747 | | $ | 7,052,577 | | $ | 4,248,341 | |

| Number of shares | $ | 104,536,561 | | | 96,251,717 | | | 70,914,983 | | | 37,527,290 | | | 20,735,499 | |

| Dividends per share | | Nil | | | Nil | | | Nil | | | Nil | | | Nil | |

| Diluted net income (loss) per share | ($ | 0.079 | ) | ($ | 0.139 | ) | ($ | 0.064 | ) | ($ | 0.035 | ) | ($ | 0.123 | ) |

Since June 1, 1970, the Government of Canada has permitted a floating exchange rate to determine the value of the Canadian dollar as compared to the US dollar. On March 5, 2008, the exchange rate in effect for Canadian dollars exchanged for US dollars, expressed in terms of Canadian dollars was $1.0103. This exchange rate is based on the noon buying rates of the Bank of Canada, as obtained from the websitewww.bankofcanada.ca.

For the past five fiscal years ended November 30, 2007 and for the three month period between December 31, 2007 and February 29, 2008, the following exchange rates were in effect for Canadian dollars exchanged for US dollars, calculated in the same manner as above:

| Period | | Average |

| Year ended November 30, 2003 | $ | 1.4216 |

| Year ended November 30, 2004 | $ | 1.3093 |

| Year ended November 30, 2005 | $ | 1.2163 |

| Year ended November 30, 2006 | $ | 1.1350 |

| Year ended November 30, 2007 | $ | 1.0865 |

| Period | | Low | | High |

| Month ended February 29, 2008 | $ | 0.9952 | $ | 1.0035 |

| Month ended January 31, 2008 | $ | 1.0060 | $ | 1.0149 |

| Month ended December 31, 2007 | $ | 0.9987 | $ | 1.0073 |

| Month ended November 30, 2007 | $ | 0.9617 | $ | 0.9716 |

| Month ended October 31, 2007 | $ | 0.9725 | $ | 0.9786 |

| Month ended September 30, 2007 | $ | 1.0220 | $ | 1.0286 |

B.

Capitalization and Indebtedness

Not required, as this 20-F filing is made as an annual report.

C.

Reasons for the Offer and Use of Proceeds

Not required, as this 20-F filing is made as an annual report.

D.

Risk Factors

Any investment in our common shares involves a high degree of risk. You should consider carefully the following information before you decide to buy our common shares.

6

If any of the events discussed in the following risk factors actually occurs, our business, financial condition or results of operations would likely suffer. In this case, the market price of our common shares could decline, and you could lose all or part of your investment in our shares. In particular, you should consider carefully the following risk factors:

We have a history of losses.

We have incurred losses in our business operations since inception, and we expect that we will continue to lose money for the foreseeable future. Since our incorporation on September 6, 1996 to November 30, 2007, we incurred losses determined under United States GAAP totalling $36,922,012. Very few junior mining resource companies ever become profitable. Failure to achieve and maintain profitability may adversely affect the market price of our common stock.

We generally have limited financial resources and no source of cash flow.

With the exception of funds recently raised through private placements and the exercise of options and warrants, we generally have limited financial resources, no source of operating cash flow and no assurance that additional funding will be available to us for further exploration of our projects or to fulfil our obligations under any applicable agreements. Failure to obtain such additional financing could result in delay or indefinite postponement of further exploration of our projects with the possible loss of such properties. We have secured funds that will enable us to meet our current obligations. Raising additional capital resources in the future can not be depended upon.

Very few mineral properties are ultimately developed into producing mines.

The business of exploration for minerals and mining involves a high degree of risk. Few properties that are explored are ultimately developed into producing mines. At present, our mineral properties have no known significant body of commercial ore. Most exploration projects do not result in the discovery of commercially mineable deposits of ore. The occurrence of unsuccessful exploration efforts may eventually lead to us needing to cease operations.

Substantial expenditures are required for us to establish ore reserves through drilling, to develop metallurgical processes, to extract the metal from the ore and, in the case of new properties, to develop the mining and processing facilities and infrastructure at any site chosen for mining.

Although substantial benefits may be derived from the discovery of a major mineral deposit, no assurance can be given that we will discover minerals in sufficient quantities to justify commercial operations or that we can obtain the funds required for development on a timely basis.

The economics of developing precious and base metal mineral properties is affected by many factors including the cost of operations, variations in the grade of ore mined, fluctuations in metal markets, costs of processing equipment and other factors such as government regulations, including regulations relating to royalties, allowable production, importing and exporting of minerals and environmental protection. We have no producing mines at this time.

If we do not obtain additional financing, our business will fail.

Our current operating funds are less than necessary to complete exploration of our mineral claims, and therefore we will need to obtain additional financing in order to complete our business plan. As at November 30, 2007, we had $23,151,345 in cash on hand. Cash on hand at the date of filing this annual report is approximately $21,000,000.

Our business plan calls for significant expenses in connection with the exploration of our mineral claims. We will require additional financing in order to complete these activities. In addition, we will require additional financing to sustain our business operations if we are not successful in earning revenues once exploration is complete. We do not currently have any arrangements for financing and we can provide no assurance to investors that we will be able to find such financing if required.

7

We believe the only realistic source of future funds presently available to us is through the sale of equity capital. Any sale of equity capital will result in dilution to existing shareholders. The only other alternative for the financing of further exploration would be the offering by us of an interest in our properties to be earned by another party or parties carrying out further exploration thereof.

Dilution through contractor, director and consultant options could adversely affect our stockholders.

Because our success is highly dependant on our contractors, we grant some or all of our key contractors, officers, directors and consultants options to purchase common shares, as non-cash incentives. If significant numbers of these options are granted and exercised, the interests of other stockholders may be diluted.

There are currently options outstanding to purchase an additional 5,850,000 common shares, which upon exercise would result in a total of 110,386,561 common shares being issued and outstanding.

Because management has only limited experience in resource exploration, the business has a higher risk of failure.

Our management, while experienced in business operations, has only limited experience in resource exploration. While we try to hire and maintain management with the proper expertise, as we have management with diverse business backgrounds, none of our directors or officers have any significant technical training or experience in resource exploration or mining. Management may not fully be aware of the specific requirements related to working in mineral exploration, whether technical or operational. Therefore, our managerial decisions and choices may not always reflect standard engineering or mineral exploration practices commonly used. We rely on the opinions of consulting geologists and mining experts that we retain from time to time for specific exploration projects or property reviews.

We cannot be certain that the measures we take will ensure that we implement and maintain adequate financial resources or profitability. Management’s lack of experience may cause failure to implement appropriate financial decisions, or cause difficulties in implementing proper decisions, ultimately harming our operating results.

As a foreign private issuer, our shareholders may have less complete and timely data.

The submission of proxy and annual meeting of shareholder information (prepared to Canadian standards) in Form 6-K may result in shareholders having less complete and timely information in connection with shareholder actions. The exemption from Section 16 rules regarding reports of beneficial ownership and purchases and sales of common shares by insiders and restrictions on insider trading in our securities may result in shareholders having less data and there being fewer restrictions on insiders’ activities in our securities.

Mineral exploration involves a high degree of risk against which we are not currently insured.

Unusual or unexpected rock formations, formation pressures, fires, power outages, labour disruptions, flooding, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labour are risks involved in the operation of mines and the conduct of exploration programs. We have relied on and will continue to rely upon consultants and others for exploration expertise.

It is not always possible to fully insure against such risks and we may decide not to take out insurance against such risks as a result of high premiums or other reasons. Should such liabilities arise, they could reduce or eliminate any future profitability and result in increasing costs and a decline in the value of our common shares. We do not currently maintain insurance against environmental risks relating to our mineral property interests, though we have obtained third party liability insurance, to counter the effects of these risks.

There is no assurance of the title to or boundaries of our resource properties.

Our mineral property interests may be subject to prior unregistered agreements of transfers or native land claims and title may be affected by undetected defects. We have not conducted surveys on the property and there is a risk that the boundaries could be challenged.

8

We may require permits and licenses that we may not be able to obtain.

Our operations may require licenses and permits from various governmental authorities. There can be no assurance that we will be able to obtain all of the necessary licenses and permits that may be required to conduct exploration, development and mining operations at our projects on certain properties in the Northwest Territories.

Metal prices fluctuate widely.

Factors beyond our control may affect the marketability of any resource we discover. Metal prices have fluctuated widely, particularly in recent years. The effect of these factors cannot accurately be predicted.

The resource industry is very competitive.

The resource industry is intensely competitive in all its phases. We compete with many companies possessing greater financial resources and technical facilities than us for the acquisition of mineral concessions, claims, leases and other mineral interests as well as for the recruitment and retention of qualified exploration personnel and independent contractors.

Our operations may be adversely affected by government and environmental regulations.

Our operations may be subject to environmental regulations promulgated by government agencies from time to time. Environmental legislation provides for restrictions and prohibitions on spills, release or emissions of various substances produced in association with certain mining industry operations, such as seepage from tailings disposal areas, which would result in environmental pollution. A breach of such legislation may result in the imposition of fines and penalties. In addition, certain types of operations require the submission and approval of environmental impact assessments.

Environmental legislation is evolving in a manner which means that standards, enforcements, fines and penalties for non-compliance are more stringent. Environmental assessments of proposed projects carry a heightened degree of responsibility for us and our directors, officers and consultants. The cost of compliance with changes in governmental regulations has a potential to reduce the profitability of our operations. We do not maintain environmental liability insurance.

The trading market for our shares is not always liquid.

Although our shares trade on the TSX Venture Exchange (“TSX-V”) and the NASD Over the Counter Bulletin Board (“OTCBB”) and the Frankfurt Exchange (“QLD”), the volume of shares traded at any one time can be limited, and, as a result, there may not be a liquid trading market for our shares.

Our securities may be subject to penny stock regulation in the US.

Because the current market price of our common stock is below US $5.00 per share, we are subject to "penny stock" regulation under US securities laws. "Penny stock" rules impose additional sales practice requirements on broker-dealers who sell such securities to persons other than established customers and accredited investors (generally those with assets in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 together with a spouse).

For transactions covered by these rules, the broker-dealer must make a special suitability determination for the purchase of such securities and have received the purchaser's written consent to the transaction prior to the purchase. Additionally, for any transaction involving a penny stock, unless exempt, the rules require the delivery, prior to the transaction, of a disclosure schedule prescribed by the Securities and Exchange Commission (“SEC”) relating to the penny stock market. The broker-dealer also must disclose the commissions payable to both the broker-dealer and the registered representative and current quotations for the securities. Finally, monthly statements must be sent disclosing recent price information on the limited market in penny stocks. Consequently, the "penny stock" rules restrict the ability of broker-dealers to sell our shares of common stock.

9

Certain directors may be in a position of conflicts of interest.

Certain members of our board also serve as directors of other companies involved in natural resource exploration and development. Consequently, there exists the possibility that those directors may be in a position of conflict. Any decision made by those directors will be made in accordance with their duties and obligations to deal fairly and in good faith of our company and such other companies. In addition, such directors will declare, and refrain from voting on, any matter in which such directors may have a conflict of interest.

Enforcement of legal process may be difficult.

All members of our board of directors and management reside in Canada. As well, our address for service is a Canadian address. Accordingly, service of process upon us, or upon individuals related to us, may be difficult or impossible to obtain within the US.

All of our assets are located outside of the US. Any judgment obtained in the US against us may not be collectible within the US.

As we are incorporated pursuant to the laws of the Province of Alberta, Canada, duties of our directors and officers, and the ability of shareholders to initiate a lawsuit on our behalf, are governed by the AlbertaBusiness Corporations Act.

ITEM 4 – Information on the Company

A.

History and Development of the Company

We were incorporated under the name “Alberta Star Mining Corp.” pursuant to theBusiness Corporations Actin the Province of Alberta, Canada by registration of our articles of incorporation and the issuance by the Registrar of Corporations of a Certificate of Incorporation on September 6, 1996. On September 20, 2001, we consolidated our share capital such that every five common shares in our capital stock pre-consolidation were exchanged for one post-consolidation common share. Concurrently, we changed our name to “Alberta Star Development Corp.”

Our head office is located at 506 – 675 West Hastings Street, Vancouver, British Columbia, Canada, V6B 1N2. Our telephone number is (604) 488 0860.

We have not been involved in any bankruptcy, receivership or similar proceedings, nor have we been a party to any material reclassification, merger, consolidation or purchase or sale of a significant amount of assets.

We are engaged in the business of the acquisition, exploration and development of resource properties. At present, our properties are in the exploration stage and further exploration will be required before final evaluations as to the economic and legal feasibility can be determined.

Our properties have no known significant body of commercial ore, nor are any such properties at the commercial development or production stage. No assurance can be given that commercially viable mineral deposits exist on any of our properties. Further, our interest in joint ventures which own properties will be subject to dilution if we fail to expend further funds on the projects. We have not generated cash flows from operations. These facts increase the uncertainty and risks faced by investors in our company. For more information see Item 3D – Risk Factors.

10

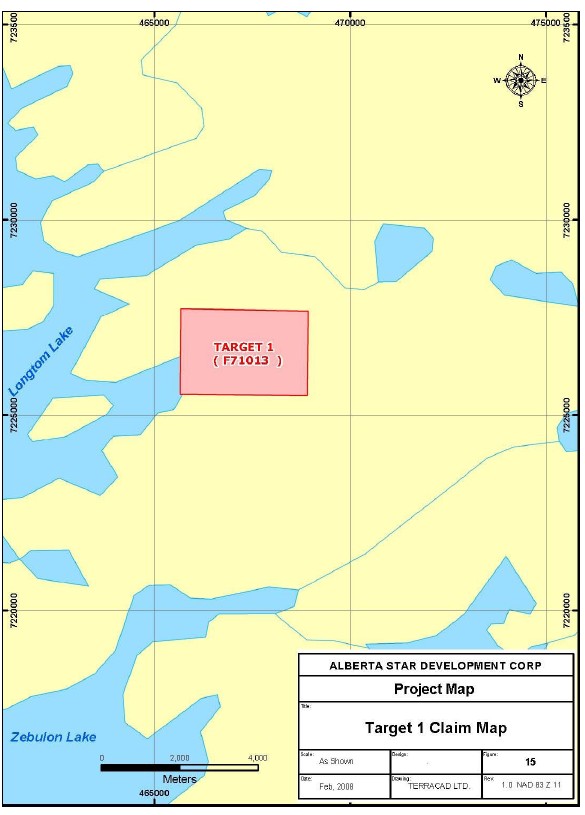

Our principal mineral property assets are located in the Northwest Territories and include an interest in:

·

the Contact Lake Mineral Claims;

·

the Glacier Lake Mineral Claims;

·

the Port Radium – Crossfault Lake Mineral Claims;

·

the Eldorado Uranium Mineral Claims;

·

the North Contact Lake Mineral Claims;

·

the South Eldorado Uranium Project;

·

the Longtom Property;

·

the Longtom Property (Target 1); and

·

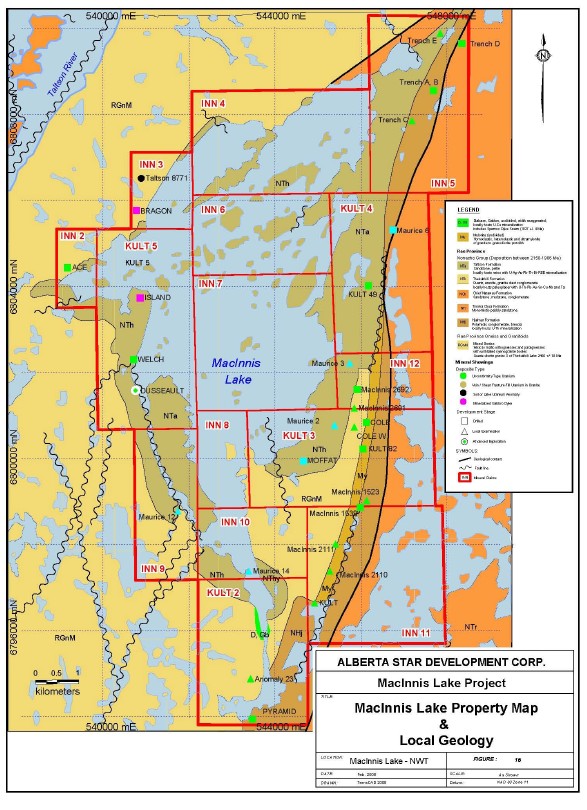

the MacInnis Lake Uranium Claims.

As these projects are in the exploration stage, we have no current operating income or cash flow.

B.

Business Overview

Background

All disclosure about our exploration properties in this annual report conforms to the standards of US SEC Industry Guide 7,Description of Property by Issuers Engaged or to be Engaged in Significant Mining Operations, other than disclosure of “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource”, which are geological and mining terms as defined in accordance with Canadian National Instrument 43-101 under the guidelines adopted by the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”), as CIM Standards in Mineral Resources and Reserve Definition and Guidelines adopted by the CIM. US investors in particular are advised to read carefully the definitions of these terms as well as the cautionary notes below, regarding use of these terms.

We are engaged in the exploration and acquisition of mineral properties in Canada, and specifically, hold a majority of our interests in the Northwest Territories. We are a junior mining company in the exploration stage and none of our properties are currently beyond the initial exploration stage. There is no assurance that a commercially viable mineral deposit exists on any of our properties and further exploration work may be required before a final evaluation as to the economic and legal feasibility is determined. For further information, see Item 3D – Risk Factors.

We have conducted acquisitions and initial surveys for the purpose of determining the viability of exploration work on properties located in the Northwest Territories, Canada. We intend to develop our IOCG and uranium exploration projects in Canada. The equity markets for junior mineral exploration companies are unpredictable. We may also and have historically entered into cost sharing arrangements through joint venture agreements and interest agreements in the form of letters of intent. For detailed property descriptions please refer to Item 4D – Property, Plants and Equipment.

At present we have no income from our operations and none of our properties have significant reserves nor are in production. Our ability to finance the future acquisition, exploration and development, if warranted, of our mineral properties, to make concession payments and to fund general and administrative expenses is therefore dependent upon our ability to secure additional financing.

11

Competition

The mineral property exploration business, in general, is intensively competitive and there is not any assurance that even if commercial quantities of ore are discovered, a ready market will exist for sale of same. Numerous factors beyond our control may affect the marketability of any substances discovered. These factors include market fluctuations; the proximity and capacity of natural resource markets and processing equipment; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of mineral and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may make it difficult for us to receive an adequate return on investment.

We compete with many companies possessing greater financial resources and technical facilities for the acquisition of mineral concessions, claims, leases and other mineral interests as well as for the recruitment and retention of qualified employees.

Office Space

We utilize about 1,467 square feet of office space in Vancouver, British Columbia. On April 1, 2006, we entered into a five year lease (expires 1 March 2011) with a property management firm with minimum lease commitments of approximately $3,575 per month.

Environmental Regulations

Mineral property exploration in the Northwest Territories is governed by Indian and Northern Affairs Canada, a Federal Government office which is responsible for negotiating the development of healthy and sustainable communities on behalf of the Native and Inuit peoples. Applicable statutes are the Canadian Environmental Assessment Act and the Canadian Environmental Protection Act.

In order to conduct exploration on any of our properties, we obtain land use permits. When exploration ceases on a Northwest Territories property, the land affected needs to be reclaimed in order to protect public health and safety, to reduce or prevent environmental degradation and to allow future productive land use of the property.

The reclamation plan for any property is site specific. In general, the reclamation plan consists of ensuring that the physical structures that remain do not impose a long-term hazard to public health and safety and the environment, which includes ensuring that the land and watercourses are returned to a safe and environmentally sound state. We do not anticipate incurring any reclamation costs in connection with our other mineral property interests.

C.

Organizational Structure

This item is not applicable, as we are not part of a group, nor do we hold any subsidiary companies.

D.

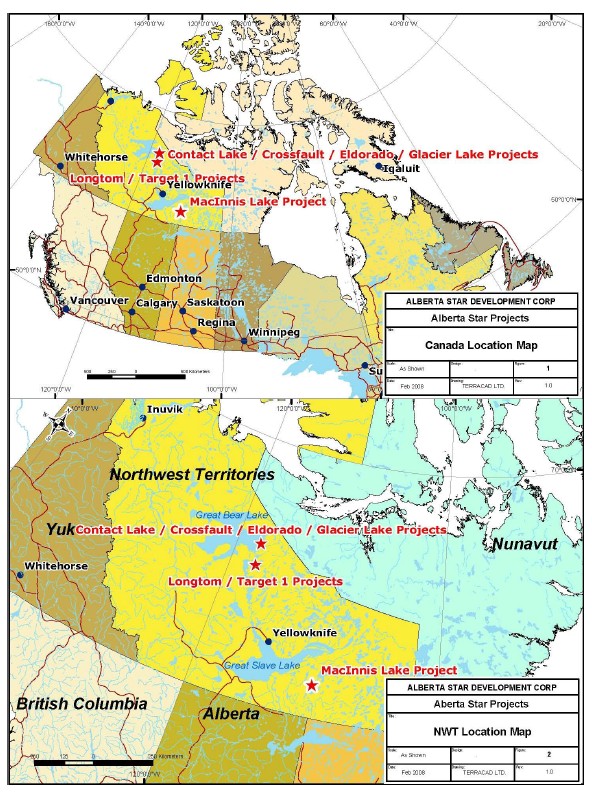

Property, Plants and Equipment

We are engaged in the acquisition and exploration of mineral property interests in Canada, and specifically hold all of our current property interests within the Northwest Territories, Canada (figures 1 and 2). What follows is a description of our current and former properties, including information on expenses for the years ended November 30, 2007 and, if applicable, November 30, 2006. We have also included information on exploration work completed and if applicable, planned for the upcoming fiscal year.

12

Figures 1 and 2

13

Contact Lake – Eldorado Area Geological Setting

1. Regional Geology

Adapted from Hildebrand, 1981; Hildebrand et al.1987; and Hoffman and Hall, 1993

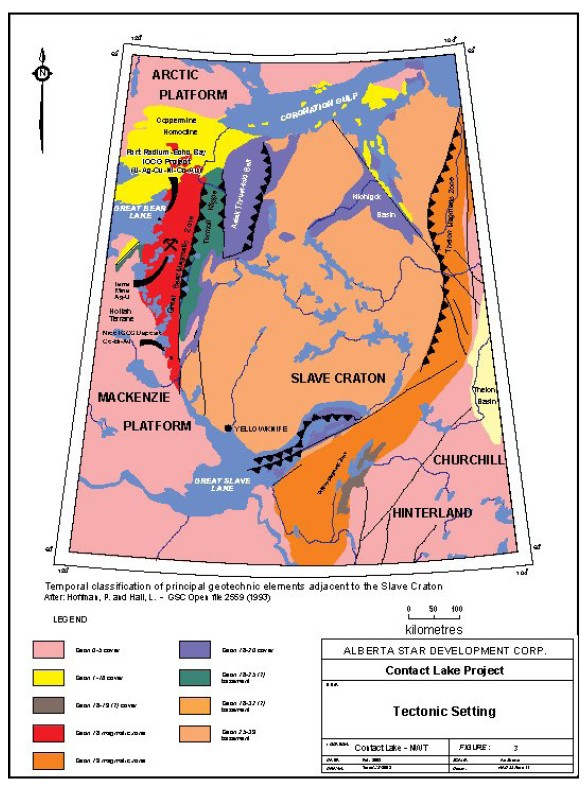

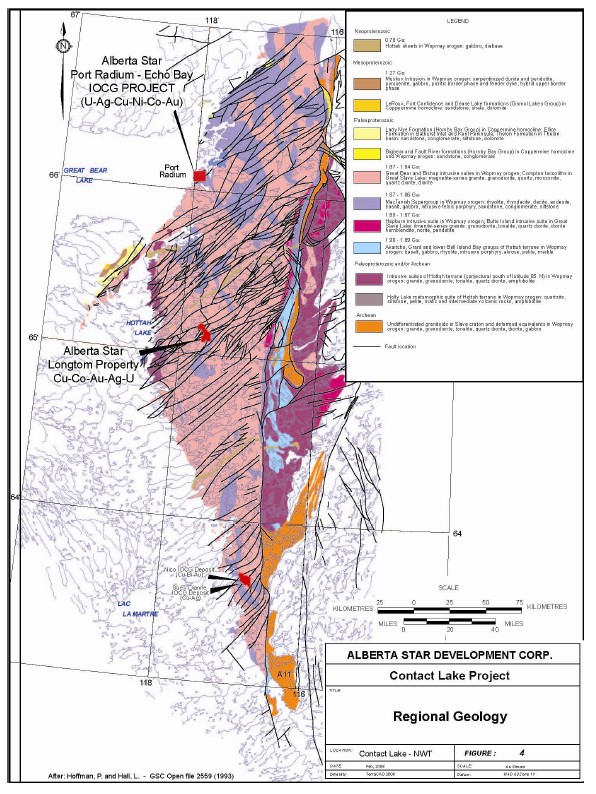

The Port Radium-Echo Bay Project is located in the northern portion of the Great Bear Magmatic Zone (GBMZ), part of the Bear Structural Province of the Canadian Shield (figure 3). The Bear province covers some 40,000 square kilometres (100 x 400 km) and consists of the gneissic Coronation Geosyncline to the east, and the GBMZ to the west, with the long-lived, polyphase Wopmay Deformation Zone (WDZ) separating the two terranes (Hildebrand, 1986) (figure 4). This orogenic zone developed on the western side of the Archean Slave craton between 2.1 and 1.8 Ga. Hoffman (1980a) divided the Wopmay Deformation Zone into four distinct tectonic zones: (1) a thin autochthonous cratonic cover and foreland basal sequence overlies the northwestern area of the Slave Craton (2) the Asiak fold and thrust belt of of continental shelf and carbonate sequences overthrust on the Craton (3) the Hepburn orthotectonic zone of deformed rift sediment-volcanic sequences intruded by post tectonic S-type plutons (4) the little deformed GBMZ, of subgreenschist facies volcano-sedimentary sequences intruded by I-type plutons. The GBMZ is onlapped by platformal Paleozoic cover sequences to the west. The Port Radium-Echo Bay Property is situated in the western part of the GBMZ.

The Hottah Terrane is a basement continental calc-alkaline volcano-plutonic arc and associated sedimentary rocks which formed above an eastward subducting plate along the western margin of the Slave Province (Hildebrand et al. 1987; Clowes, 1997). The volcano-sedimentary rocks of this terrane were cut by calc-alkaline biotite-hornblende bearing plutons with ages ranging from 1.914 Ga to 1.902 Ga.. A depositional prism of geosynclinal shelf and slope sediments (Epworth, Snare and Akaitcho Groups) of the Coronation Supergroup formed at the edge of the continental margin and at about 1.90 Ga, arc magmatism stopped and a bimodal suite of submarine volcanic rocks erupted onto the block faulted and subsided sediments of the margin. This tectono-magmatic episode lasted only 5-10 Ma, related to intra-arc extension which also generated a marginal basin originally to the east of the Hottah arc. The basin filled with siliciclastic and carbonate rocks overlying the volcanic succession and lapping on to the Slave Craton to the east.

Within 5-10 Ma, the sedimentary basin was simultaneously shortened and intruded by peraluminous to metalumious plutons of the Hepburn intrusive suite (1.896-1.879 Ma). The shortening resulted in detachment and eastward thrusting of the imbricated basinal sediments into the Calderian accretionary wedge forming the Asiak Fold belt in the east and the Hepburn plutonic and metamorphic zone (Turmoil Klippe) in the west part of the former basin. As the hot plutons of the Hepburn suite were emplaced over the colder authochton of the western Slave Craton, inverted metamorphic isograds developed.

The 1.878 Ga closure of the marginal basin resulted in the initiation and growth of the 1.876 -1.850 Ga continental, arc complex of the GBMZ at the suture between the Hottah arc to the west and the Hepburn suite to the east. The Great Bear Magmatic Zone is a 100 x 400 km wide corridor which is the product of the final stages of continental volcanism and related plutonic activity.

It consists of low titanium/high aluminum calc-alkaline volcano-plutonic rocks which have been intruded by a suite of hornblende and biotite bearing plutons of similar age (Hoffman and Bowring, 1984; Hildebrand and Bowring, 1084). The thick supracrustal sequences are referred to as the McTavish Supergroup, and consist of sub-greenschist facies, calc-alkaline andesitic to rhyolitic volcanic, volcaniclastic and sedimentary rocks, which have been interpreted as remnants of ancient stratovolcanoes and the products of caldera collapse (Hildebrand, 1984).

14

The occurrence of these sequences as isolated roof pendants within larger batholiths of the GBMZ hinders regional stratigraphic correlations between widely spaced regions. The northern part of the GBMZ is underlain by a 10 km thick section of supracrustal rocks of the MacTavish Supergroup, which comprises three Groups: the Labine, Dumas and Sloan, in ascending order. The southern part of the GBMZ is underlain by a 5 km thick section of the Faber Group, which has been interpreted as broadly correlatable with the Sloan Group. These units occupy the central core of the GBMZ, and are flanked to the west and east, by rocks of the Labine and Dumas Groups, respectively. Cannuli (1989) also suggested that the Labine and Dumas may be broadly correlative and that the distribution of supracrustal sequences define a regional scale syncline within the GBMZ volcano-plutonic complex. Ghandi (1994) noted that synvolcanic quartz monzonitic plutons within the strat igraphy of both the Labine and Faber Groups were closely coeval; however, the predominantly basaltic and less andesitic strata of the Labine Group contrasts with the more felsic strata of the Faber and Sloan Groups. The Faber Group volcanic sequences were suggested to be texturally and chemically similar to products formed in anorogenic extensional settings, such as in the Missouri granite-rhyolite terrane and the Gawler ranges of South Australia, rather than a subduction setting (Ghandi, 1994).

The Labine Group, which represents the main magmatic arc in the western part of the GBMZ, consists of a 7 km thick section of volcanic-derived rocks which is exposed in the Port Radium-Echo Bay area. The Labine Group consists of the lower Port Radium Formation and the overlying Echo Bay and Cameron Bay Formations, which collectively define a minimum of two caldera collapse sequences. The rocks of the Labine Group have been intruded along a minimum of two stratigraphic levels, by intermediate plutons and largely concordant sills of the Mystery Island Intrusive Complex. The lower sheet includes the Bertrand and Mystery Island plutons and the upper sheet includes the Contact Lake and Glacier/Tut plutons. These intrusive typically have pronounced zoned alteration haloes within the intrusions and/or their flanking host rocks. Large, felsic syn- to post-volcanic, granite to monzonite plutons of the Great Bear batholith also intrude this sequence. These intrusions have locally de veloped hornfels aureoles but lack the strong alteration associated with the earlier intermediate sills.

The cessation of volcanism in the GBMZ may have been the result of subduction of an oceanic spreading ridge or other high topographic features such as remnant arcs. Gravity studies have suggested the presence of another arc further to the west (Fort Simpson arc) existed on the western side of the ocean, and now under Paleozoic cover. The cessation of arc magmatism due to ridge subduction is common to Mesozoic-Cenozoic volcanic arcs worldwide, such as in South America, where the Chile Rise and Nazca Ridge were subducted into the Peru-Chile Trench and in California, where the East Pacific Rise was subducted under North America (Hildebrand, et al. 1987). Such an event may also have resulted in a change in plate motion in the GBMZ, to transpression (dextral wrenching) and folding oblique to the original subduction direction (Bowring, 1984). As a result, the concordant plutons and their host rocks were folded around NW trending axes at about 1.843 Ga (Bowring, 1984), exposing t he plutons and their altered waIlrocks in oblique cross-section.

Post-dating the development of the northwest trending folds, large, discordant, epizonal, biotite bearing granites and quartz diorites were emplaced between about 1.858 and 1.843 Ga (Bowring and van Schmus, 1987), formed as a result of melting due to crustal thickening from folding (Hildebrand et al, 1987). Bodies of this syenogranitic suite are also offset by continued movement on a swarm of later transcurrent, predominantly north to northeast trending faults. These structures were developed as a result of east-west shortening which generated the northeast trending, dextral strike-slip structures (Hoffman, 1980; Hildebrand et al., 1987). Evidence of plutonism in this setting is noted as swarms of related northeast trending dykes.

Movement on these northeast faults is related to displacement on north-south, transcurrent fault zones, parallel to the Wopmay Deformation Zone. Displacement along these structures continued after the development of the igneous and sedimentary rock assemblages in the GBMZ, commonly resulting in kilometre scale offset of units.

The northeast trending faults are also cut by Cleaver diabase (Hoffman, 1984; Hildebrand, 1982), and both are unconformably overlain by the sedimentary basin of the 1.663 Ga Hornby Bay Group (McGrath and Hildebrand, 1984; Bowring and Ross, 1985) . Hildebrand (1988) noted that many of the northeasterly faults were reactivated during a period of normal faulting which occurred during the late stages of, or after, the deposition of the Hornby Bay Group (Hildebrand, 1988). Gabbro sills known as Western Channel diabase are considered to be the youngest rocks in the area (Hildebrand, 1982).

15

Figure 3

16

Figure 4

17

2. Local Geology

Adapted from Hoffman & McGlynn, 1977;Hildebrand, 1981; Reardon, 1992; Robinson & Ohmoto, 1971. The geology of the Port Radium-Echo Bay area, as shown infigure 5, has been compiled from mapping completed by Hildebrand, 1981 and Reardon, 1992.

18

Figure 5

19

Stratigraphy

The Port Radium-Echo Bay area is underlain by volcano-sedimentary rocks of the Labine Group, which is subdivided into 3 main formations: Port Radium, Echo Bay, Cameron Bay. These are further subdivided into members which represent two main eruptive caldera phases: an early phase characterized by relatively gas-poor eruptions of andesitic lavas (Port Radium and Echo Bay Formations) and a younger, more gas-charged phase of voluminous siliceous volcanics and volcaniclastics (within the Cameron Bay and Feniak Formations) (Hildebrand, 1981). The stratigraphy can be locally isolated into distinct calderas, 3 to 5 km in diameter. The two cycles of caldera collapse, resurgence and intermediate plutonism are characterized by cone facies andesite, marr diatreme breccias and caldera fill sediments.

Lithogeochemical studies indicate that the Labine sequence is high in potassium (K), calc-alkaline belt of stratavolcanoes similar to Andean continental arc sequences (Ewart and LeMaitre, 1980). The sequence has only been subjected to low grade metamorphism (zeolite facies), with local contact metamorphic effects (i.e. hornfels) noted in supracrustal rocks flanking large plutons of the Great Bear Batholith series.

The Eldorado & Contact Lake IOCG & Uranium Projects 2008 Explorations Program

Proposed personnel requirements and budgets for the 2008 drilling and exploration programs are illustrated in the Tables below.

| | # Personnel | Days |

| Diamond Drillers (two drills) | 8 | 120 |

| Drill Foreman | 1 | 120 |

| Geologists - Drill support | 2 | 120 |

| Core samplers, splitters, sawers, geo-assistants | 3 | 120 |

| Field Geologists - experienced | 2 | 60 |

| Student geo-assistants | 2 | 30 |

| Geophysics crew | 2 | 60 |

| Line cutters | 2 | 30 |

| Cook | 2 | 120 |

| Camp Manager and Logistics | 1 | 120 |

| Helicopter Pilot | 2 | 120 |

| Miscellaneous Project Support (helicopter-mechanic, Government geologists, | | variable |

| remote sensing mechanics, etc) | 2 | |

| Visitors (government, geologists, community leaders, etc) | 2 | variable |

| Project Manager | 1 | 120 |

| |

| Total | 32 | |

20

The Eldorado & Contact Lake IOCG & Uranium Projects 2008 - Budget

| Field Geology | | |

| | Geologists, line cutting | | 450,000 |

| | Reconnaissance mapping, sampling, ground I.P. | | |

| Detailed mapping and sampling, geological support | | |

| Geophysics | | |

| | IP and surveying | | 50,000 |

| |

| |

| Camp Operations, Logistics, Fixed-Wing and Air Support | | 750,000 |

| |

| Diamond Drilling | | |

| | 3,000 to 5,000 meters (20 holes) | | |

| | Sampling and assaying | | |

| | Helicopter support | | 1,100,000 |

| |

| Program Total | $ | 2,350,000 |

Mineral Claim and Lease Claim Payments in the Northwest Territories

In order to retain property title or mineral claims in the Northwest Territories, the Company must file at least $4 per acre during the two-year period immediately following the date the claim is recorded. In respect to the representation of work, the types of undertakings on the claims are as follows:

·

Drilling

·

Trenching

·

Sinking shafts

·

Geochemical and geophysical investigation made on the ground or by aircraft

·

Surveyor claims must be proved by the surveyor general

·

Work done in constructing roads and airstrips

The Company must pay annual payments to the federal government in order to maintain lease claims.

21

1.

Contact Lake Mineral Claims – Contact Lake, Northwest Territories

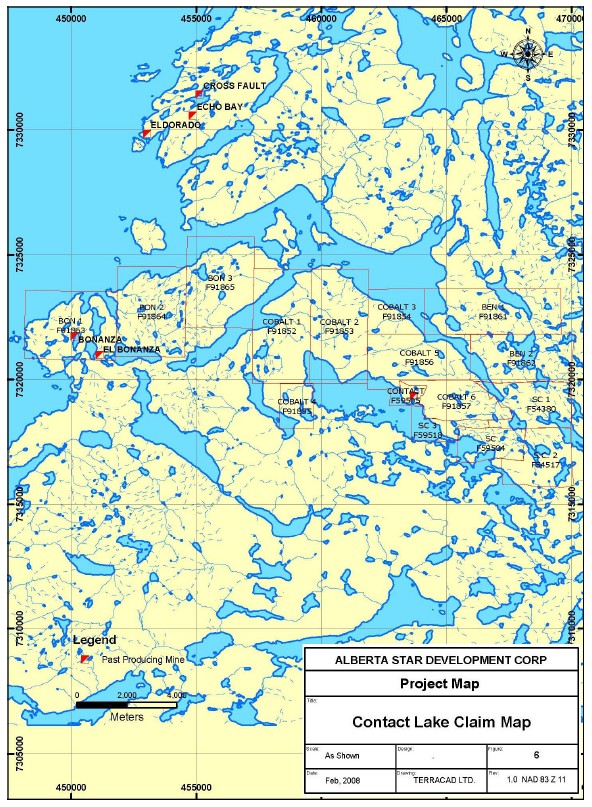

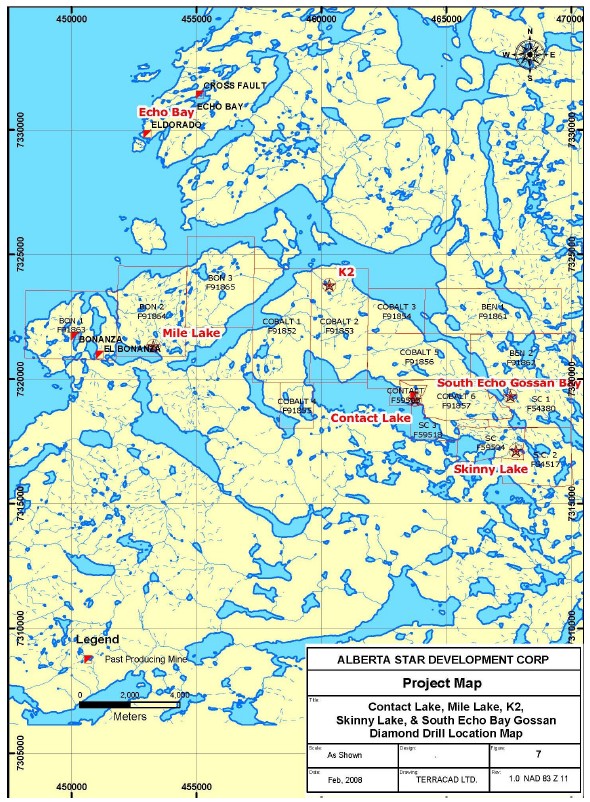

During the year ended November 30, 2005, we acquired a 100% undivided right, title and interest, subject to a 1% net smelter return royalty (“NSR”), in five mineral claims totalling 1,801.82 hectares (“ha”) (4,450.50 acres) located five miles southeast of Port Radium on Great Bear Lake, NT for cash payments of $60,000 (paid) and 300,000 common shares (issued and valued at $72,000). We may purchase the NSR for a one-time payment of $1,000,000. We completed additional staking in the area in order to increase the project size to 16 mineral claims, totalling 10,601.57 ha (26,185.88 acres). Collectively the properties are known as the Contact Lake Mineral Claims (figure 6).

The area has traditionally been underexplored, but encompasses a mineral rich portion of the Great Bear Magmatic Zone, and includes the Contact Lake Mineral Belt itself, approximately 15 km long and the same belt whose northern extension hosts Fortune Minerals NICO Gold deposit.

A summary of our claims can be found below:

| Name | Tag Number | Size (ha) |

| CONTACT | F59505 | 100.33 |

| SC | F59504 | 376.24 |

| SC 1 | F54380 | 582.75 |

| SC 2 | F54517 | 501.65 |

| SC 3 | F59518 | 240.85 |

| COBALT 1 | F91852 | 1,045.10 |

| COBALT 2 | F91853 | 1,045.10 |

| COBALT 3 | F91854 | 250.82 |

| COBALT 4 | F91855 | 418.04 |

| COBALT 5 | F91856 | 752.47 |

| COBALT 6 | F91857 | 522.55 |

| BEN 1 | F91861 | 1,003.30 |

| BEN 2 | F91862 | 752.47 |

| BON 1 | F91863 | 1,003.30 |

| BON 2 | F91864 | 1,003.30 |

| BON 3 | F91865 | 1,003.30 |

| |

| | | 10,601.57 |

22

Figure 6

23

Our expenditures related to the Contact Lake Mineral Claims can be summarized as follows:

| | Cumulative | | | |

| | amounts from | For the year | For the year | For the year |

| | inception to | ended 30 | ended 30 | ended 30 |

| | 30 November | November | November | November |

| | 2007 | 2007 | 2006 | 2005 |

| | $ | $ | $ | $ |

| |

| Exploration operating expenses | | | | |

| Amortization | 84,574 | 84,574 | - | - |

| Assaying and geochemical | 317,993 | 126,745 | 180,351 | 10,897 |

| Camp costs and field supplies | 1,288,275 | 499,322 | 671,577 | 117,376 |

| Claim maintenance and permitting | 82,983 | 13,452 | 69,531 | - |

| Community relations and government | 124,917 | 50,603 | 74,314 | - |

| Drilling | 3,199,850 | 1,741,790 | 1,458,060 | - |

| Equipment rental | 197,081 | 75,693 | 121,388 | - |

| Geology and engineering | 408,538 | 171,399 | 52,673 | 184,466 |

| Orthophotography | 199,451 | 103,306 | 96,145 | - |

| Staking and line cutting | 332,660 | - | 332,660 | - |

| Surveying | 1,473,493 | 336,349 | 908,846 | 228,298 |

| Transportation and fuel | 4,437,007 | 1,357,400 | 2,874,802 | 204,805 |

| Wages, consulting and management fees | 3,135,462 | 1,407,434 | 1,519,578 | 208,450 |

| |

| | 15,282,284 | 5,968,067 | 8,359,925 | 954,292 |

| |

| Acquisition of mineral property interests | 132,000 | - | - | 132,000 |

| |

| | 15,414,284 | 5,968,067 | 8,359,925 | 1,086,292 |

Accessibility, Local Resources and Infrastructure

The best access to the area is from Yellowknife, NT, using charter fixed wing aircraft which can land at the 900 meter long unmaintained gravel airstrip at the western shore of Glacier Lake, which lies in the centre of the project area. A road extends west from the airstrip to the area of the Echo Bay and Eldorado Mines. Bulk freight has also previously been mobilized by seasonal barging along the Mackenzie River, from Alberta to Tulita (Fort Norman), NT, on the western shore of Great Bear Lake. When mining was active in the area, a barge service also operated along the Bear River from Tulita to Deline, and across Great Bear Lake to the various mining operations. Lake barging service is in limited operation.

Currently, the Northwest Territories Department of Transport maintains a winter road from Yellowknife to Rae-Edzo and beyond, to Rae Lakes which is approximately 100 km south of the property. Recent records indicate that local conditions have allowed this road to be open for a period of approximately 6 weeks, from mid- February to late March/early April. During operation of the silver mines at Camsell River and Echo Bay prior to 1984, the winter road was extended to Port Radium, via Marian Lake and Camsell River.

Although there lacks major infrastructure in the immediate area of the property, significant logistical support and supplies are available from Yellowknife. Established fishing camps on the eastern side of Great Bear Lake also provide some support. The town of Yellowknife has a long history of mining, where the services of many experienced explorers can be obtained. As well, personnel may be available from several smaller communities within the Great Bear Lake area.

24

In 2006 the Company undertook a successful exploratory drill program (Phase 1) on the Company’s Eldorado & Contact Lake projects. From June to October, 2006, 14,475 metres of NQ drill core was recovered, and 6,470 samples including 289 standards were assayed. The 2006 drill program targeted seven areas, 1) the K2 area in which there is a low-grade Cu+ Co, Au and Ag mineralized breccia system that has strong affinities to an IOCG system, 2) the Echo Bay gossan at the end of the southeast arm of Echo Bay which marks the location of a newly discovered silver zone; 3) a high-grade Cu-Ag-Mo-Zn-Pb-W mineralized hydrothermal breccia at Mile Lake, 4) uranium, nickel, cobalt and silver mineralized zones adjacent to the past producing Eldorado mine site, 5) uranium, nickel, cobolt and silver mineralized zones adjacent to the past producing Echo Bay mine site, 6) an area centered on a strong VTEM plus magnetic anomaly near the sou theast end of Echo Bay; and 7) the Thompson Showing of a high-grade Cu-Ag-Co-Ni-Au-U polymetallic vein. Highlights from the 2006 Phase 1 program on the Company’s Eldorado & Contact Lake projects are included in a Technical Report prepared in accordance with National Instrument 43-101 and is accessible on SEDAR.

In 2007 the Company completed Phase 2 of the exploratory drill program based on the preliminary investigations from the 2006 drill program at the Eldorado & Contact Lake project areas. The Company’s two base exploration camps, personnel and supporting infrastructures were fully operational from May to October, 2007. The Company completed almost 20,000 meters of drilling in 72 drill holes (37 reported) and collected over 10,000 surface samples. The 2007 drill program targeted ten areas; K2, Echo Bay South, Mag Hill, Glacier Creek, Breccia Island, Camelback, Skinny Lake and Contact Lake, located on the Contact Lake Mineral Claims and Eldorado and Echo Bay, located on the Glacier Lake Mineral Claims. Highlights from the 37 drill holes reported to date are discussed below.

The K2-IOCG target

The K2-IOCG target area is a target area in which drilling encountered significant IOCG style poly-metallic copper, gold, silver and cobalt mineralization. The mineralized zone is part of a regionally extensive zone of phyllic, potassic, hematite and magnetite, magnetite-actinolite alteration zones, often appearing at surface as phyllic-potassic pyritic gossans. The mineralization occurs within the same suite of volcano-plutonic rocks that host other poly-metallic zones in the Eldorado & Contact lake mineral belt, including the former El Bonanza Silver- Uranium (U-Ag) and the Eldorado Uranium (U-Ag- Cu- Co- Ni- Bi) mines (figure 7).

The latest results from the first six holes of a nine hole 2007 program confirm the initial drill results whereby the Company announced that it had discovered a zone of hydrothermal and structurally controlled poly-metallic breccias that are enriched in copper and locally in gold, silver and cobalt. The K2-IOCG target is located on the Contact Lake property, on the south side of Echo Bay. All eight drill holes from the 2006 drill program intersected multiple zones of altered and mineralized breccias with disseminated and vein hosted copper, gold, silver and cobalt sulphide mineralization.

Highlights from significant mineralized down hole intervals from the six three holes of a nine hole 2007 program include:

25

·

K2-07-11 intersected 60.20 meters of 0.37% copper including 3.10 meters of 0.93% copper. Other mineralized zones in this drill hole includes 13.14 meters of 0.30% copper including 1.50 meters of 0.60% copper, 0.12% zinc and 12 g/ton silver. Other zones of 24.70 meters of 0.27% copper and 30.23 meters of 0.17% copper were intersected in this drill hole.

·

K2-07-12 intersected 93.00 meters of 0.35% copper including 1.35 meters of 1.45% copper. Other mineralized zones of 44.52 meters of 0.33% copper and 42.50 meters of 0.32% copper were intersected in this drill hole. Also 2.97 meters of 27.3 g/ton silver including 0.77 meter of 69.0 g/ton silver was intersected in this hole.

·

K2-07-13 intersected 36.70 meters of 1.11% copper including 0.90 meter of 5.45% copper, 5.20 meters of 1.31% copper, 7.40 meters of 2.96% copper and 3.00 meters of 0.45% copper.

·

K2-07-16 intersected 1.5 meters of 1,467 g/ton silver and 0.32% copper.

·

K2-07-18 intersected 5.5 meters of 0.143% copper as well as 1.5 meters of 0.134% cobalt.

·

K2-07-19 intersected 0.3 meters of 0.93% copper as well as 1.5 meters of 0.25% copper and another interval of 1.0 meter of 0.23% copper.

The Skinny Lake IOCG target

The Skinny Lake IOCG target is the site of extensive hydrothermal magnetite-actinolite- feldspar-apatite plus sulphide alteration along the Contact Lake Mineral Belt in the northern part of the Great Bear Magmatic Zone. The host rocks are alkali (sodic or potassic) and or actinolite-epidote altered andesites. The core zone comprises a pervasive alkali feldspar-scapolite-magnetite-actinolite-apatite hydrothermal assemblage.

The alteration signature and zone at Skinny Lake is similar to that of the Port Radium- Eldorado uranium mine area situated on Labine Point, NT. Also the metal assemblage is very similar to the Echo Bay silver mine. The Skinny Lake discovery zone and target area is defined by predominately pyrite mineralization, which is present intermittently throughout the Skinny Lake region and in an extensive gossan at the southeast end of Echo Bay, with visible sulphide mineralization at the surface. In addition, uranium, cobalt, nickel, copper, silver, lead and zinc enrichments are present locally as veins, veinlets and disseminations that extend outward in the southern and eastern extensions of the Skinny Lake and Mag Hill target areas (figure 7).

Highlights from significant mineralized down hole intervals from the first hole of a two hole 2007 program include:

·

SL-07-01 intersected 22.50 meters of 2.24% zinc, 0.23% lead and 18.35 g/ton silver and 0.025% cobalt. Including 7.40 meters of 5.64% zinc, 0.45% lead, 0.20% copper, 45.93 g/ton silver and 0.042% cobalt as well as 1.1 meters of 0 10.82% zinc, 0.29% lead, 0.22% copper and 38.52 g/ton silver. Also including 2.3 meters of 4.48% zinc, 0.47% lead and 75.01 g/ton silver and 0.053% cobalt.

26

Figure 7

27

2.

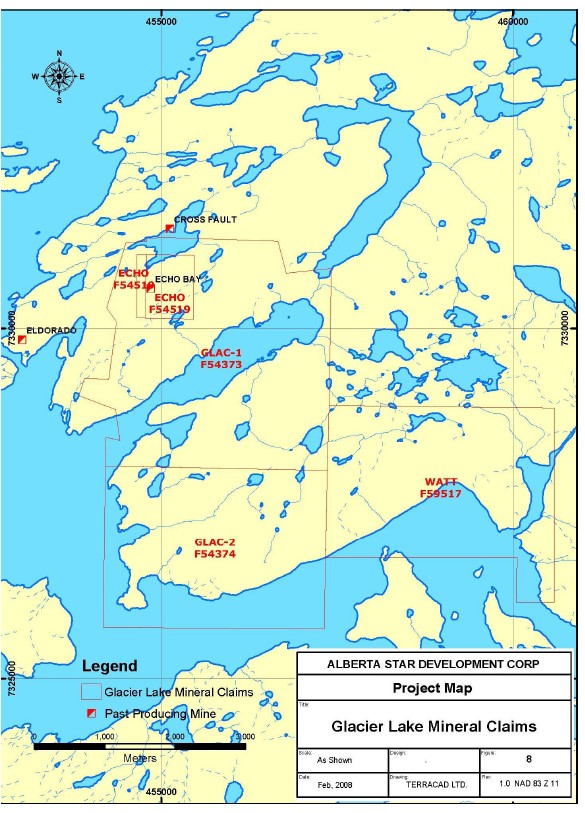

Glacier Lake Mineral Claims, Northwest Territories

During the year ended November 30, 2005, we acquired a 100% undivided right, title and interest, subject to a 2% NSR in four mineral claims, totalling 2,424.23 ha (5,987.85 acres) (the “Glacier Lake Mineral Claims”) located one mile east of Port Radium on Great Bear Lake, NT. For cash payments of $30,000 (paid) and 360,000 common shares (issued and valued at $72,000) of the Company. We may purchase one-half of the NSR for a one-time payment of $1,000,000(figure 8).

Two former past-producing silver and radium mines, Echo Bay (produced 23,779,178 ounces of silver) and Eldorado (produced 15 million pounds of uranium and 8 million ounces of silver) are situated on claims, which the Company owns. The claim is comprised of extensive alteration zones that include intensely mineralized gossans, traceable for over one km in length and 200 meters in lateral extent.

The property contains a fully operational all-season airstrip and base camp, situated at Glacier Lake. The Echo Bay claim (produced 23,779,178 ounces of silver) and the Port Radium – Eldorado claim (produced 15 million pounds of uranium and 8 million ounces of silver) are situated on property owned by the Company. The Port Radium uranium belt was formerly one of Canada’s principal producers of Pitchblende uranium during the 1930s and 1940s.

A summary of our claims can be found below:

| Name | Tag Number | Size (ha) |

| GLAC 1 | F54373 | 835.68 |

| GLAC 2 | F54374 | 731.57 |

| ECHO | F54519 | 83.61 |

| WATT | F59517 | 773.37 |

| |

| | | 2,424.23 |

28

Figure 8

29

Our expenditures related to the Port Radium – Glacier Lake Mineral Claims can be summarized as follows:

| | Cumulative | | | | | | |

| | amounts from | | For the year | | For the year | | For the year |

| | inception to | | ended 30 | | ended 30 | | ended 30 |

| | 30 November | | November | | November | | November |

| | 2007 | | 2007 | | 2006 | | 2005 |

| | $ | | $ | | $ | | $ |

| |

| Exploration operating expenses | | | | | | | |

| Amortization | 7,796 | | 7,796 | | - | | - |

| Assaying and geochemical | 143,177 | | 143,177 | | - | | - |

| Camp costs and field supplies | 382,311 | | 256,581 | | 125,730 | | - |

| Claim maintenance and permitting | 7,130 | | 6,867 | | 263 | | - |

| Community relations and government | 21,472 | | 21,472 | | - | | - |

| Drilling | 758,681 | | 758,681 | | - | | - |

| Equipment rental | 58,038 | | 45,643 | | 12,395 | | - |

| Geology and engineering | 33,673 | | 33,673 | | - | | - |

| Metallurgical studies | 62,977 | | 62,977 | | - | | - |

| Orthophotography | 25,522 | | 25,522 | | - | | - |

| Staking and line cutting | 88,335 | | 88,335 | | - | | - |

| Surveying | 17,309 | | - | | 17,309 | | - |

| Transportation and fuel | 4,685,859 | | 3,754,918 | | 930,941 | | - |

| Wages, consulting and management fees | 680,818 | | 505,775 | | 175,043 | | - |

| |

| | 6,973,098 | | 5,711,417 | | 1,261,681 | | - |

| |

| Acquisition of mineral propertyinterests | 102,000 | | - | | - | | 102,000 |

| Recovery of mineral property costs | (603,750 | ) | (186,651 | ) | (417,099 | ) | - |

| |

| | 6,471,348 | | 5,524,766 | | 844,582 | | 102,000 |

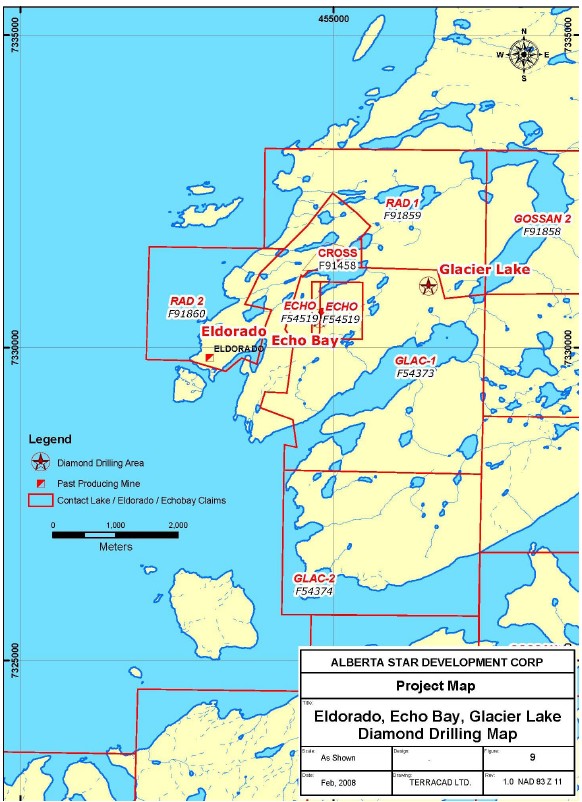

The Eldorado IOCG and Uranium target

In 2006, the Company discovered a new zone of hydrothermal and structurally controlled poly-metallic vein breccias at Eldorado on the North side of Echo Bay. The 2006-2007 programs were designed to re-evaluate the economic potential of the former Eldordo-Echo Bay silver and uranium mines (figure 9).

The results of the seventeen hole 2007 program confirmed additional widespread poly-metallic and uranium mineralization. The Company has encountered uranium mineralization in three of the 2007 drill holes released to date, which assayed 0.25 meters of 1.41 % U3O8, 0.53 meters of 0.17% U3O8 and 0.30 meters 0.21% U3O8within poly-metallic core.

Highlights from significant mineralized down hole intervals from the seventeen hole 2007 program include:

·

PR-07-11 intersected 0.5 meters of 2.3 g/ton gold as well as another 0.3 meters of 2.3 g/ton gold

·

PR-07-12 intersected 0.47 meter 0.22% lead, 0.9% zinc, 0.5 % cobalt and 7.7 g/tonne silver.

·

PR-07-13 intersected 0.25 meter of 1.45% copper and 1.41% U3O8.

·

PR-07-14 intersected 1.49 meters of 0.44% copper and 0.30 meter of 0.21% U3O8.

30

·

PR-07-15 intersected 8.14 meters of 0.68% copper, 22.9 g/tonne silver. This included 2.26 meters of 2.02% copper, 73.4 g/tonne silver. Subsequent sections comprised 0.25 meters of 2.5% cobalt with 1.7% bismuth and 0.53 meters of 0.17% U3O8 and 0.98% cobalt.

·

PR-07-16 intersected 4.82 meters of 0.47% copper, and also several vanadium-bearing zones including 25.51 meters of 0.22% vanadium (as V205) and also 45.22 meters of 0.20% vanadium (as V205).

·

PR-07-17 intersected 15.46 meters of 0.27% lead, 1.67% zinc including 7.67 meters of 0.43% lead and 2.93% zinc, 4.51 meters of 1.42% lead and 0.93% zinc including 1.51 meters of 3.81% lead and 1.22% zinc.

·

PR-07-18 intersected 1.5 meters of 0.25% zinc and 0.23% V2O5; 4.5 meters of 0.31% copper, 0.28% lead and 0.35% zinc including 1.5 meters of 0.87% copper, 0.66% lead, 0.65% zinc and 6.5 g/ton silver; 1.26 meters of 1.01% lead and 0.51% zinc; 10.74 meters of 0.12% copper, 0.72% zinc including 1.74 meters of 2.45% zinc, 12.30 g/ton silver and 0.16% V2O5 and 1.50 meters of 0.13% lead, 0.31% zinc, and 0.12% V2O5.

·

PR-07-19 intersected several zones of zinc mineralization including 4.5 meters of 0.17% zinc, 1.5 meters of 0.14% zinc and 4.5 meters of 0.14% zinc.

·

PR-07-20 intersected 9.0 meters of 0.25% zinc including 1.49 meters of 1.0% zinc. 31.65 meters of 0.22% copper and 24.2 g/ton silver, including: 0.57 meter of 4.4% copper, 0.11% lead, 0.39% zinc, 46.8 g/ton silver and 0.21% V2O5, 3.0 meters of 0.39% copper and 206.5 g/ton silver and 4.5 meters of 0.18% V2O5.

·

PR-07-21 intersected 12.34 meters of 1.01% zinc and 0.25% lead; 15.0 meters of 0.12% zinc and 0.15% V2O5 and 4.9 meters of 0.22% lead, 0.44% zinc and 0.11% V2O5.

·

PR-07-22 include 21.08 meters of 2.23% copper, 65.21 g/ton silver and 0.20% V2O5 including 7.50 meters of 2.74% copper, 102.09 g/ton silver and 0.19% V2O5 and 3.58 meters of 3.90% copper, 66.37 g/ton silver and 0.13% V205 as well as 1.50 meters of 4.77% copper, 168.07 g/ton silver and 0.58meters of 9.47% copper and 182.40 g/ton silver. 0.70 meter of 1.49% copper 52.0 g/ton. 0.41 meter of 2.86% copper, 123 g/ton silver and 0.14% V2O5. 15 meters of 0.14% copper, 0.33% zinc and 0.12% V2O5.

·

PR-07-23 intersected 185.4 meters of 0.12% V2O5 including 28.24 meters of 0.21% V2O5; 34.20 meters of 0.26% zinc; 8.82 meters of 0.21% zinc and 11 g/ton silver including 2 meters of 0.25% zinc and 30.2 g/ton silver and 0.10% nickel

·

PR-07-24 intersected 18.45 meters of 0.453% copper, 0.249% lead, 0.480% zinc, 42.6 g/ton silver including 1.82 meter of 2.485% copper, 0.525% lead and 200.8 g/ton silver;1.50 meters of 2.190% zinc, 1.060% lead and 21.9 g/ton silver: 14.50 meter of 0.480% zinc, 0.116% lead and 6.1 g/ton silver: 9.37 meters of 0.573% copper, 0.043% uranium (U3O8) and 0.089% vanadium (V2O5) including 1.50 meter of 0.097% uranium (U3O8) as well as 1.06 meter of: 1.85% copper, 0.142% uranium (U3O8) and 0.110% vanadium (V2O5).

·

PR-07-25 intersected 1.45 meters of 39.9 g/ton silver, 0.403% copper, 0.333% lead, 0.207% zinc, 0.123% nickel, and 0.126% cobalt; 1.5 meters of 1.89% zinc, 1.04% lead and 14.2 g/ton silver; 49.7 meters of 0.145% zinc and 212.05 meters of vanadium (V2O5)

·

PR-07-26 intersected 32.20 meters of 0.33% zinc, 0.20% lead and 4.4 g/ton silver; 0.85 meter of 2.12% zinc, 4.29% lead, 0.27% copper and 62.5 g/ton silver and 11.65 meters of 0.19% vanadium (V2O5)

·

PR-07-27 intersected 43.50 meters 40.9 g/ton silver, 0.20% copper, 0.14% lead, and 0.15% zinc;15 meters of 0.24% copper as well as another 15 meters of 0.22% zinc; 1.5 meters of 1.80% copper and 24.3 g/ton silver and 1.5 meters of 1.65% copper and 24.3 g/ton silver.

31

The Echo Bay IOCG and Uranium target

The Echo Bay IOCG and uranium target drill program was designed to re-evaluate the economic potential of the former Eldorado-Echo Bay silver and uranium mines and its untested surrounding area. The Echo Bay silver-uranium target are is located on the Company’s property, on the north side of Echo Bay (figure 9).

The results of the first six holes of an eight hole 2007 program intersected multiple zones of altered and mineralized poly-metallic zones with disseminated and vein hosted high grade copper, silver, lead and zinc.

Highlights from significant mineralized down hole intervals from the first six of an eight hole 2007 program include:

·

EBM-07-06 intersected 7.50 meters of 0.18% copper and 0.12% zinc within that 1.50 meter 0.42% copper. Another zone of 0.58 meter of 0.43% lead was also intersected in this drill hole.

·

EBM-07-08 intersected 24.75 meters of 2.50% lead, 0.49% copper, 0.31% zinc and 26.50 g/ton silver, within that 4.50 meters of 8.38% lead, 0.50% copper, 0.68% zinc and 34.4 g/ton silver. Also several mineralized zones enriched in copper, lead or zinc were intersected in this drill hole.

·

EBM-07-09 intersected several zinc-bearing zones including 3.0 meters of 0.27% zinc, 2.9 meters of 0.38% zinc, 1.5 meters of 0.20% zinc and 6 meters of 0.22% zinc. Also 1.5 meters of 0.27% copper was intersected.

·

EBM-07-11 intersected several mineralized zones including 58.25 meters of 0.61% zinc, 0.20% lead, and 2.44 g/ton silver and within that 1.50 meters of 2.56% zinc, 0.43% lead and 6.63 g/ton silver and also 1.50 meters of 2.35% zinc, 0.79% lead and 3.90 g/ton silver was intersected in this drill hole.

·

EBM-07-12 intersected 15.50 meters of 0.54% zinc and 0.20% copper and 3.29 g/ton silver including 2 meters of 0.16% copper, 0.30% lead, 1.27% zinc and 3.33 g/ton silver. Other mineralized zones include 3 meters of 0.43% lead and 0.14% zinc and 4.0 meters of 0.1% copper, 0.56% lead, 0.19% zinc; 3 meters 0.16% lead and 0.39% zinc.

·

EBM-07-13 intersected 30.10 meters of 0.75% zinc, 0.28% lead. Another zone of 0.25 meter of 16.47% zinc, 0.64% copper, 0.46% lead and 403.0 g/ton silver. Also several mineralized zones enriched in copper, lead or zinc were intersected in this drill hole.

Eldorado Camelback IOCG and Uranium Target

The Company has intersected multiple zones of poly-metallic mineralization that is associated with zones of strong hydrothermal alteration and brecciation that are locally enriched in silver, copper, lead, zinc, cobalt, uranium and vanadium. Multiple zones of sulfide mineralization outcrop in semi-continuous gossanous zones for over 3.5 kilometers in length. The Camelback IOCG target is approximately 3.5 kilometers in length and 1 kilometer in width. This large IOCG target extends from north end of Glacier Lake to the eastern shore of Cameron Bay. The Camelback target is located 7.5 km east of the Port Radium (Eldorado uranium mine). This IOCG target is associated with a large recently discovered geophysical anomaly and this geological feature has the potential of hosting a bulk tonnage IOCG and uranium target within a regional alteration signature.

The results of the first seven of a sixteen hole 2007 program has confirmed additional widespread poly-metallic IOCG & uranium style mineralization

32

Highlights from significant mineralized down hole intervals from the first thirteen of a sixteen hole 2007 program include:

·

CB-07-4 intersected 6.0 meters of 0.37% zinc

·

CB-07-5 intersected 1.5 meters of 0.33% copper, 0.36% zinc and 3.9 g/ton silver

·

CB-07-6 intersected several mineralized zone including 2.0 meters of 0.40% copper, 3.09% zinc and 37.2 g/ton silver

·

CB-07-13a intersected 10.0 meters of 0.22% copper as well as 10.5 meters 0.13% copper and 0.25 meters of 0.12% U3O8

·

CB-07-14 intersected 52.0 meters of 0.30% copper as well as 31.55 meters of 0.34%

copper

·

CB-07-15 intersected 13.30 meters of 0.21% copper as well as 1.55 meter of 0.69% copper and 20.6 g/ton silver, 4.2 meters of 0.37% copper, 0.23% V2O5 and also 1.5 meters of 0.23% V2O5

·

CB-07-16 intersected 13.5 meters of 0.15% copper

33

Figure 9

34

3.

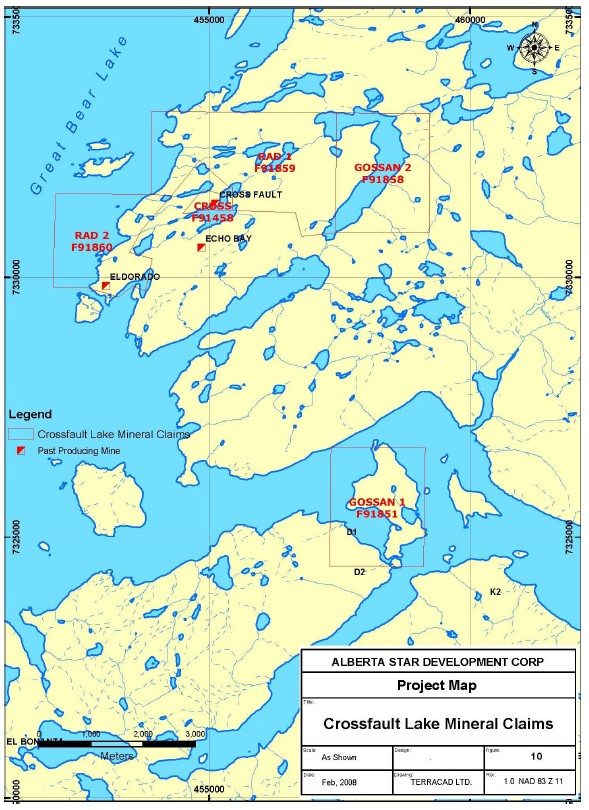

Port Radium – Crossfault Lake Mineral Claims, Northwest Territories

During the year ended November 30, 2005, we acquired a 100% undivided right, title and interest, subject to a 2% NSR, in five mineral claims totalling 1,447.26 ha (3,574.73 acres) (the “Port Radium – Crossfault Lake Mineral Claims”) located north of Port Radium on Great Bear Lake, NT, for cash payments of $60,000 (paid) and 450,000 common shares (issued and valued at $297,000) of the Company. We may purchase one-half of the NSR for a one-time payment of $1,000,000 (figure 10).

The Crossfault Lake claim block includes over 40 different metallic minerals, as identified by past geologists. The Port Radium uranium belt was formally one of Canada’s principal producers of Pitchblende uranium in the 1930s and 1940s.

A summary of our claims can be found below:

| Name | Tag Number | Size (ha) |

| GOSSAN 1 | F91851 | 418.04 |

| GOSSAN 2 | F91858 | 418.04 |

| CROSS | F91458 | 33.44 |

| RAD 1 | F91859 | 253.76 |

| RAD 2 | F91860 | 323.98 |

| |

| | | 1,447.26 |

Total expenditures related to the Port Radium – Crossfault Lake Mineral Claims consist of acquisition costs of $357,000, made during the year ended November 30, 2005.

35

Figure 10

36

4.

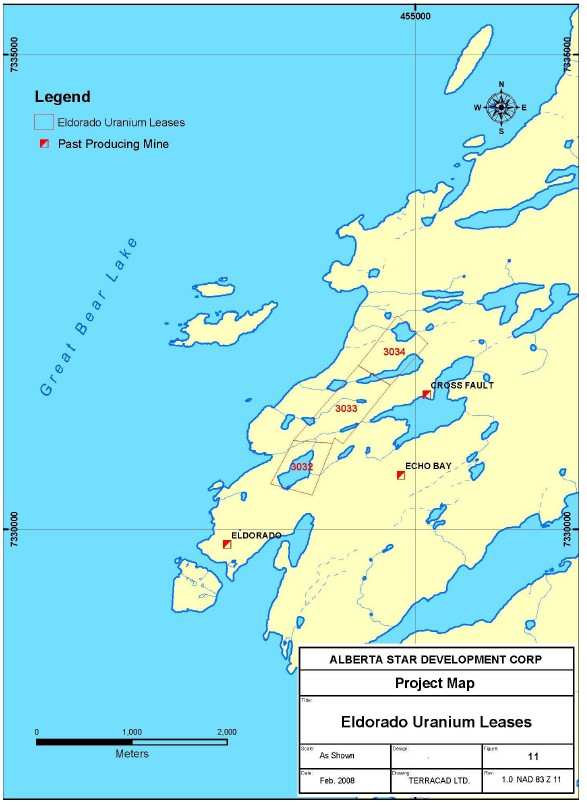

Eldorado Uranium Mineral Claims, Northwest Territories

During the year ended November 30, 2005, we entered into a lease agreement with South Malartic Exploration Inc. to purchase a 50% undivided interest, title and right in three mineral claims, totalling 106.53 ha (263.13 acres) (the “Eldorado Uranium Mineral Claims”)located at Port Radium on Great Bear Lake, NT, for a cash payment of $20,000 (paid) (figure 11).

Acquisition of the 50% ownership in the property entitled the Company to full access and possession to a detailed technical library, exploration reports and historical data in South Malartic’s possession. Also, included in the data acquisition were reports, maps, historical uranium production records, drill logs and uranium assay reports.

The property is located on Labine Point at Port Radium, NT. Starting in 1933, the mine produced 15 million pounds of high grade uranium and 8 million ounces of silver, plus copper, nickel, radium, lead and polonium. The mine currently has about 40 km of existing underground workings on 14 levels.

A summary of our claims can be found below:

| Name | Tag Number | Size (ha) |

| ELDORADO | Lease 3032 | 30.32 |

| ELDORADO | Lease 3033 | 44.81 |

| ELDORADO | Lease 3034 | 31.40 |

| |

| | | 106.53 |

Our expenditures related to the Eldorado Uranium Mineral Claims can be summarized as follows:

| | Cumulative | | | |

| | amounts from | For the year | For the year | For the year |

| | inception to | ended 30 | ended 30 | ended 30 |

| | 30 November | November | November | November |

| | 2007 | 2007 | 2006 | 2005 |

| | $ | $ | $ | $ |

| |

| Exploration operating expense | | | | |

| Claim maintenance and permitting | 526 | 526 | - | - |

| Acquisition of mineral propertyinterests | 20,000 | - | 20,000 | - |

| |

| | 20,526 | 526 | 20,000 | - |

J. Fingler, P.Geo., of Vancouver, British Columbia completed a National Instrument 43-101 compliant technical report dated August 21, 2006 (“Technical Report”) on the Eldorado-Port Radium Property. The Technical Report provides a comprehensive description of the Eldorado-Port Radium Property including previous work, geology and mineralization and also makes recommendations for further work on the Property.

37

Figure 11

38

5.

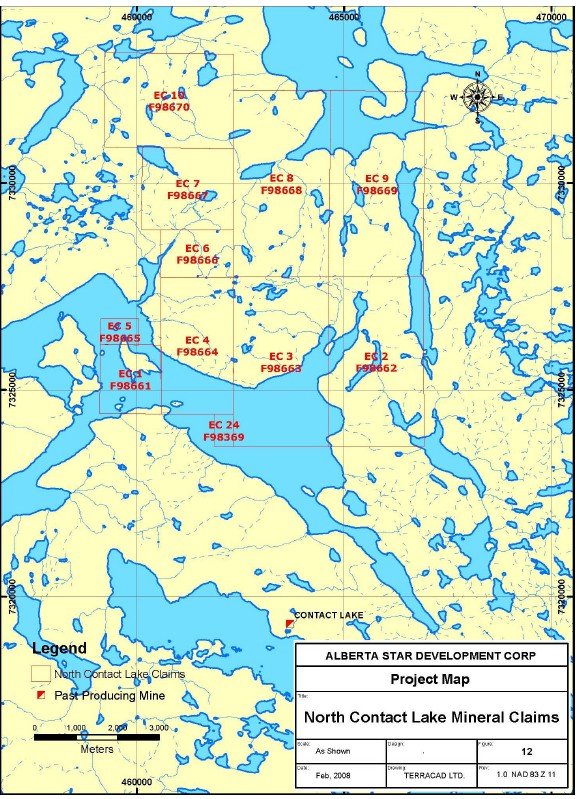

North Contact Lake Mineral Claims, Northwest Territories

During the year ended November 30, 2006, we acquired a 100% right, interest and title, subject to a 2% NSR, in eleven mineral claims (the “North Contact Lake Mineral Claims”), for cash payments of $75,000 and the issue of 250,000 common shares of the Company valued at $182,500. We may purchase one-half of the NSR for a one-time payment of $1,000,000. The North Contact Lake Mineral Claims are situated north of Contact Lake on Great Bear Lake approximately 680 km (423 miles) north of Yellowknife, NT, totalling 5,867.23 ha (14,492.06 acres) (figure 12).

The property is the northern extension of the Contact Lake Project and includes the Contact Lake – Echo Bay Stato-volcanic complex, having hundreds of known or recorded copper, gold, silver, nickel, cobalt, REE and high grade uranium occurrences identified in Proterozoic rocks.

A summary of our claims can be found below:

| Name | Tag Number | Size (ha) |

| EC 1 | F98661 | 250.82 |

| EC 2 | F98662 | 731.57 |

| EC 3 | F98663 | 836.08 |

| EC 4 | F98664 | 587.35 |

| EC 5 | F98665 | 55.60 |

| EC 6 | F98666 | 192.30 |

| EC 7 | F98667 | 477.82 |

| EC 8 | F98668 | 1,045.10 |

| EC 9 | F98669 | 1,045.10 |

| EC 10 | F98670 | 627.06 |

| EC 24 | F98369 | 18.43 |

| |

| | | 5,867.23 |

Total expenditures related to the North Contact Lake Mineral Claims consist of acquisition costs of $257,500 made during the year ended November 30, 2006.

39

Figure 12

40

6.

South Eldorado Uranium Project, Northwest Territories