Exhibit 99.2

Fred Sutherland

ARAMARK

Executive Vice President and Chief Financial Officer

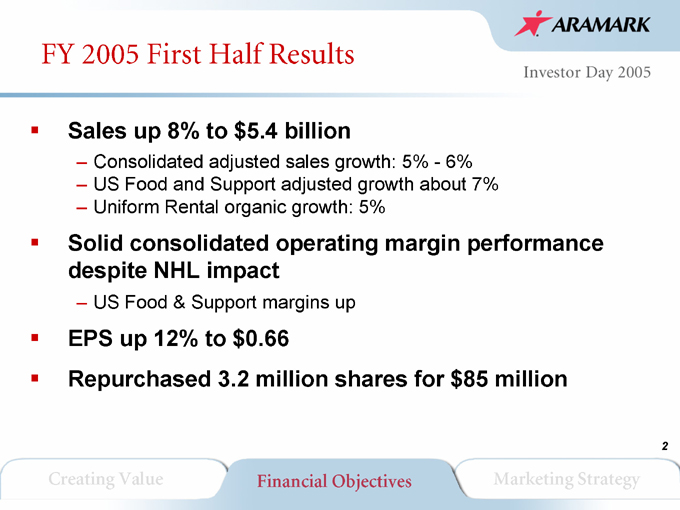

FY 2005 First Half Results

Sales up 8% to $5.4 billion

Consolidated adjusted sales growth: 5%—6%

US Food and Support adjusted growth about 7%

Uniform Rental organic growth: 5%

Solid consolidated operating margin performance despite NHL impact

US Food & Support margins up

EPS up 12% to $0.66

Repurchased 3.2 million shares for $85 million

Creating Value Financial Objectives Marketing Strategy

2

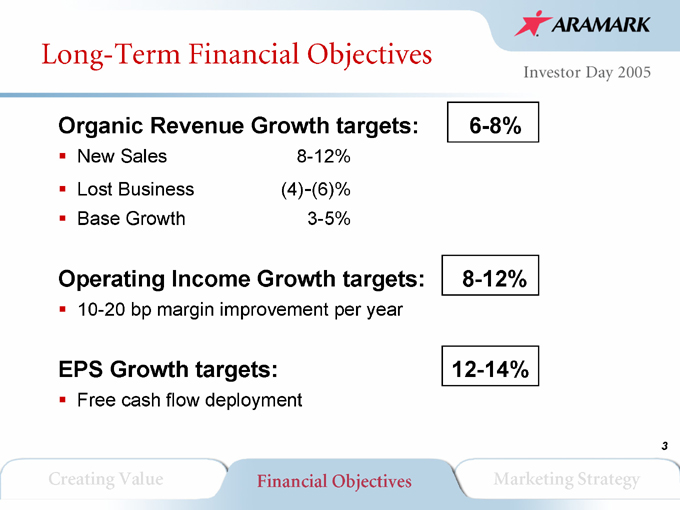

Long-Term Financial Objectives

Organic Revenue Growth targets:

New Sales Lost Business Base Growth

8-12% (4)-(6)% 3-5%

6-8%

Operating Income Growth targets:

10-20 bp margin improvement per year

8-12%

EPS Growth targets:

Free cash flow deployment

12-14%

Creating Value Financial Objectives Marketing Strategy

3

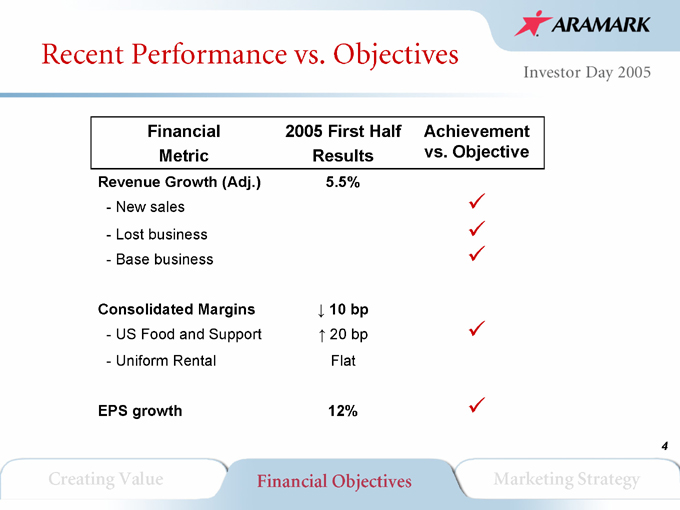

Recent Performance vs. Objectives

Financial Metric

2005 First Half Results

Achievement vs. Objective

Revenue Growth (Adj.) 5.5%

New sales

Lost business

Base business

Consolidated Margins ?10 bp

US Food and Support ?20 bp

Uniform Rental Flat

EPS growth 12%

Creating Value Financial Objectives Marketing Strategy

4

Growth Opportunities Exist in All Sectors

Outsourcing penetration rates vary

Many sectors are significantly self-operated

Base business growth opportunities exist across all sectors

Significant portion of spend not captured

Opportunity for add-on services

Creating Value Financial Objectives Marketing Strategy

5

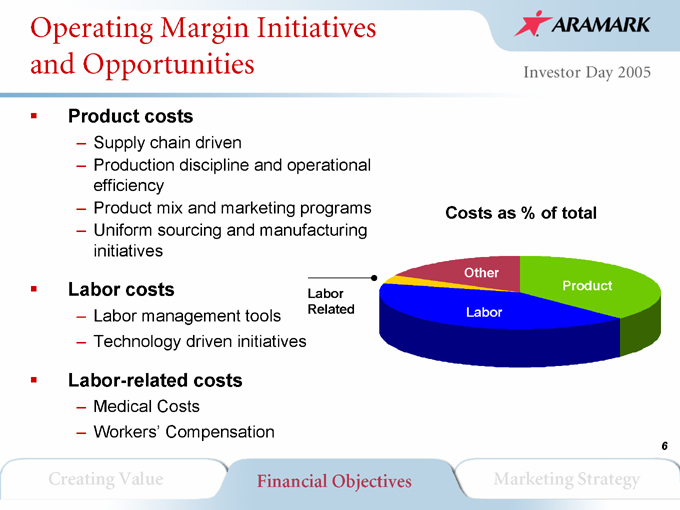

Operating Margin Initiatives and Opportunities

Product costs

Supply chain driven

Production discipline and operational efficiency

Product mix and marketing programs

Uniform sourcing and manufacturing initiatives

Labor costs

Labor management tools

Technology driven initiatives

Labor-related costs

Medical Costs

Workers’ Compensation

Labor Related

Costs as % of total

Other

Labor

Product

Creating Value Financial Objectives Marketing Strategy

6

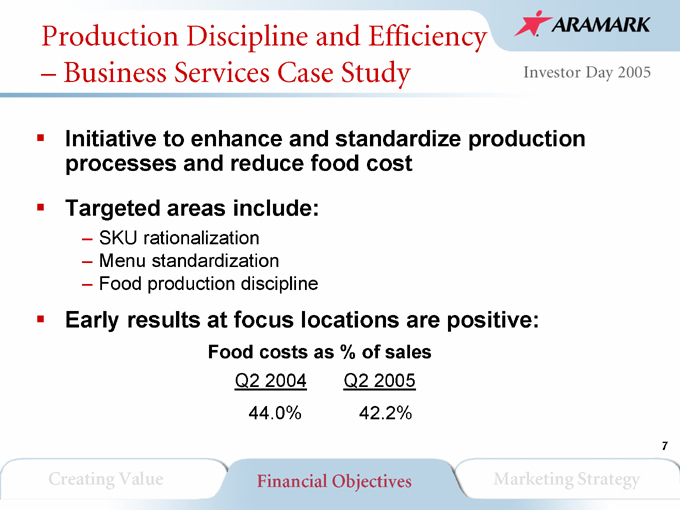

Production Discipline and Efficiency

Business Services Case Study

Initiative to enhance and standardize production processes and reduce food cost Targeted areas include:

SKU rationalization

Menu standardization

Food production discipline

Early results at focus locations are positive:

Food costs as % of sales

Q2 2004 Q2 2005 44.0% 42.2%

Creating Value Financial Objectives Marketing Strategy

7

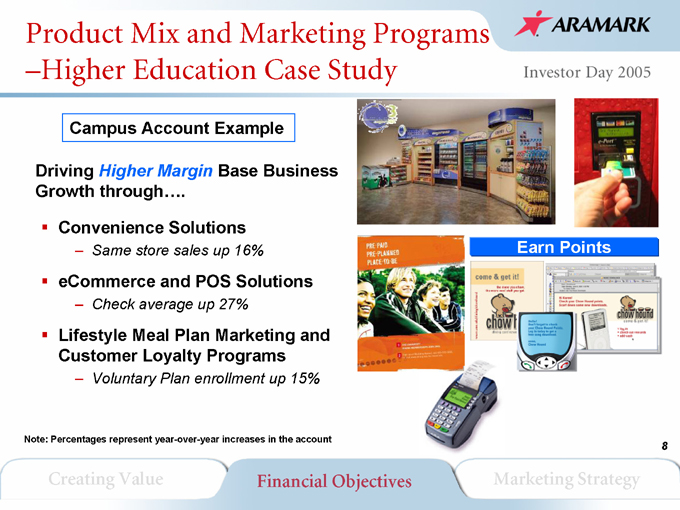

Product Mix and Marketing Programs –Higher Education Case Study

Campus Account Example

Driving Higher Margin Base Business Growth through….

Convenience Solutions

Same store sales up 16%

eCommerce and POS Solutions

Check average up 27%

Lifestyle Meal Plan Marketing and Customer Loyalty Programs

Voluntary Plan enrollment up 15%

Earn Points

Note: Percentages represent year-over-year increases in the account

Creating Value Financial Objectives Marketing Strategy

8

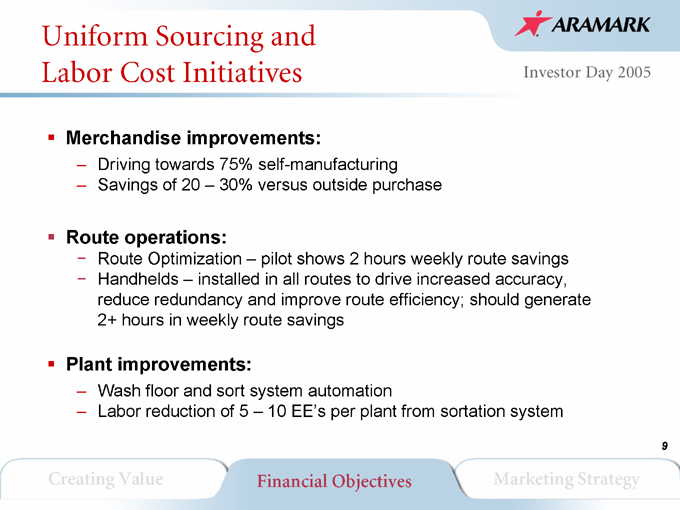

Uniform Sourcing and Labor Cost Initiatives

Merchandise improvements:

Driving towards 75% self-manufacturing

Savings of 20 – 30% versus outside purchase

Route operations:

Route Optimization – pilot shows 2 hours weekly route savings

Handhelds – installed in all routes to drive increased accuracy, reduce redundancy and improve route efficiency; should generate 2+ hours in weekly route savings

Plant improvements:

Wash floor and sort system automation

Labor reduction of 5 – 10 EE’s per plant from sortation system

Creating Value Financial Objectives Marketing Strategy

9

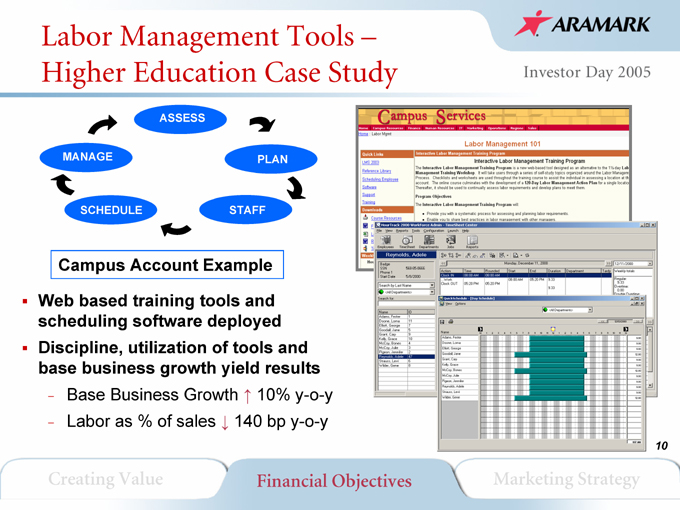

Labor Management Tools –Higher Education Case Study

ASSESS

PLAN

STAFF

SCHEDULE

MANAGE

Campus Account Example

Web based training tools and scheduling software deployed Discipline, utilization of tools and base business growth yield results

Base Business Growth 10% y-o-y

Labor as % of sales 140 bp y-o-y

Creating Value Financial Objectives Marketing Strategy

10

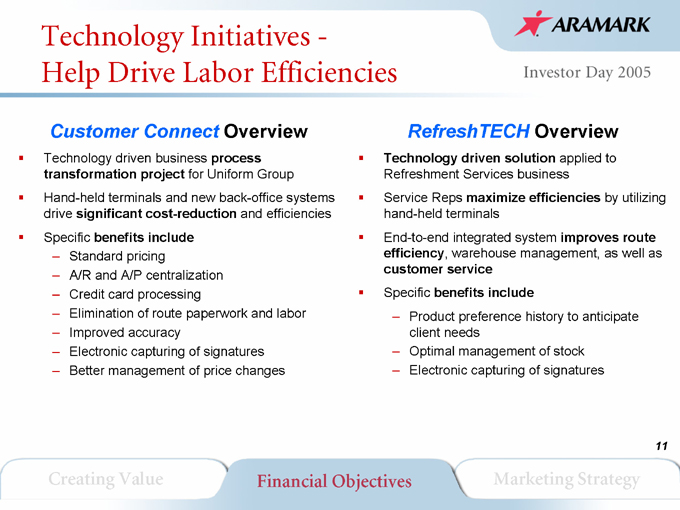

Technology Initiatives -Help Drive Labor Efficiencies

Customer Connect Overview

Technology driven business process transformation project for Uniform Group Hand-held terminals and new back-office systems drive significant cost-reduction and efficiencies Specific benefits include

Standard pricing

A/R and A/P centralization

Credit card processing

Elimination of route paperwork and labor

Improved accuracy

Electronic capturing of signatures

Better management of price changes

RefreshTECH Overview

Technology driven solution applied to Refreshment Services business

Service Reps maximize efficiencies by utilizing hand-held terminals End-to-end integrated system improves route efficiency, warehouse management, as well as customer service Specific benefits include

Product preference history to anticipate client needs

Optimal management of stock

Electronic capturing of signatures

Creating Value Financial Objectives Marketing Strategy

11

Medical Cost and Workers’ Compensation Initiatives

Medical Costs

Enrollment changes

Enhanced utilization of health provider networks

Expanded mail-order pharmacy participation

Care/Disease Management Program

Targets specific, high cost chronic illnesses

2005 growth reduced to single digits

Workers’ Compensation

Key changes implemented

Safety/Loss Control

Centralized and expanded

Claims Management

Centralized and expanded

Reporting/Financial

Unit level accountability

First half 2005 results

Overall cost reduced 9%

Loss per $1K payroll down 11%

Creating Value Financial Objectives Marketing Strategy

12

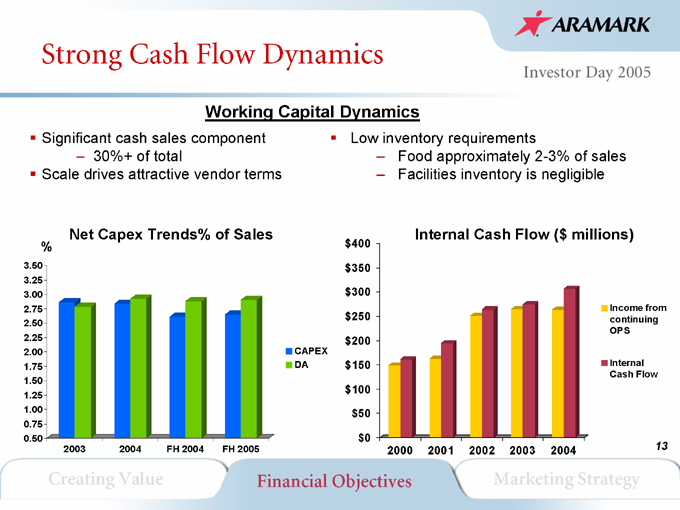

Strong Cash Flow Dynamics

Working Capital Dynamics

Significant cash sales component

30%+ of total

Scale drives attractive vendor terms

Low inventory requirements

Food approximately 2-3% of sales

Facilities inventory is negligible

Net Capex Trends% of Sales

%

3.50 3.25 3.00 2.75 2.50 2.25 2.00 1.75 1.50 1.25 1.00 0.75 0.50

2003 2004 FH 2004 FH 2005

CAPEX DA

Internal Cash Flow ($ millions) $400 $350 $300 $250 $200 $150 $100 $50 $0

2000 2001 2002 2003 2004

Income from continuing OPS

Internal Cash Flow

Creating Value Financial Objectives Marketing Strategy

13

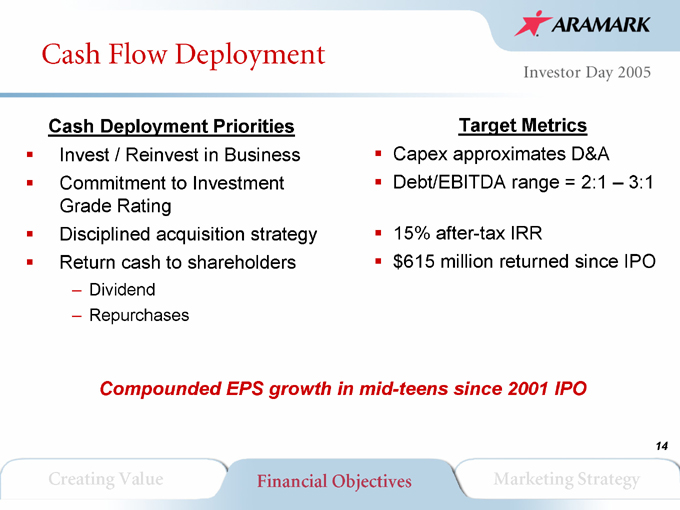

Cash Flow Deployment

Cash Deployment Priorities

Invest / Reinvest in Business Commitment to Investment Grade Rating Disciplined acquisition strategy Return cash to shareholders

Dividend

Repurchases

Target Metrics

Capex approximates D&A Debt/EBITDA range = 2:1 – 3:1

15% after-tax IRR $615 million returned since IPO

Compounded EPS growth in mid-teens since 2001 IPO

Creating Value Financial Objectives Marketing Strategy

14

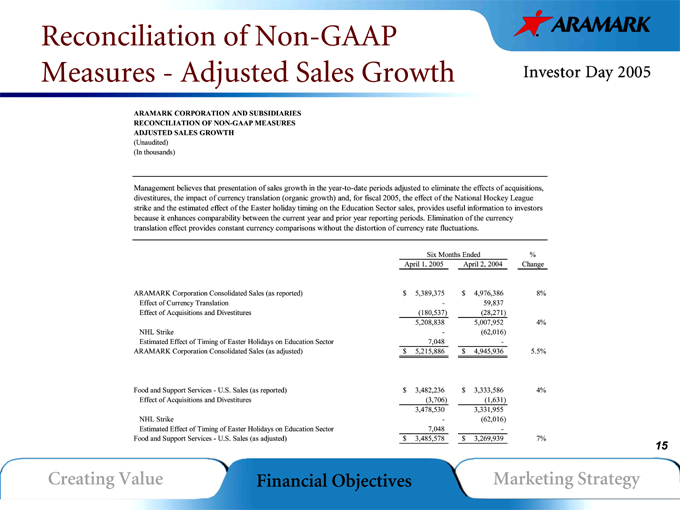

Reconciliation of Non-GAAP Measures—Adjusted Sales Growth

ARAMARK CORPORATION AND SUBSIDIARIES RECONCILIATION OF NON-GAAP MEASURES ADJUSTED SALES GROWTH

(Unaudited) (In thousands)

Management believes that presentation of sales growth in the year-to-date periods adjusted to eliminate the effects of acquisitions, divestitures, the impact of currency translation (organic growth) and, for fiscal 2005, the effect of the National Hockey League strike and the estimated effect of the Easter holiday timing on the Education Sector sales, provides useful information to investors because it enhances comparability between the current year and prior year reporting periods. Elimination of the currency translation effect provides constant currency comparisons without the distortion of currency rate fluctuations.

Six Months Ended %

April 1, 2005 April 2, 2004 Change

ARAMARK Corporation Consolidated Sales (as reported) $ 5,389,375 $ 4,976,386 8%

Effect of Currency Translation - 59,837

Effect of Acquisitions and Divestitures (180,537) (28,271)

5,208,838 5,007,952 4%

NHL Strike - (62,016)

Estimated Effect of Timing of Easter Holidays on Education Sector 7,048 -

ARAMARK Corporation Consolidated Sales (as adjusted) $ 5,215,886 $ 4,945,936 5.5%

Food and Support Services—U.S. Sales (as reported) $ 3,482,236 $ 3,333,586 4%

Effect of Acquisitions and Divestitures (3,706) (1,631)

3,478,530 3,331,955

NHL Strike - (62,016)

Estimated Effect of Timing of Easter Holidays on Education Sector 7,048 -

Food and Support Services—U.S. Sales (as adjusted) $ 3,485,578 $ 3,269,939 7%

Creating Value Financial Objectives Marketing Strategy

15

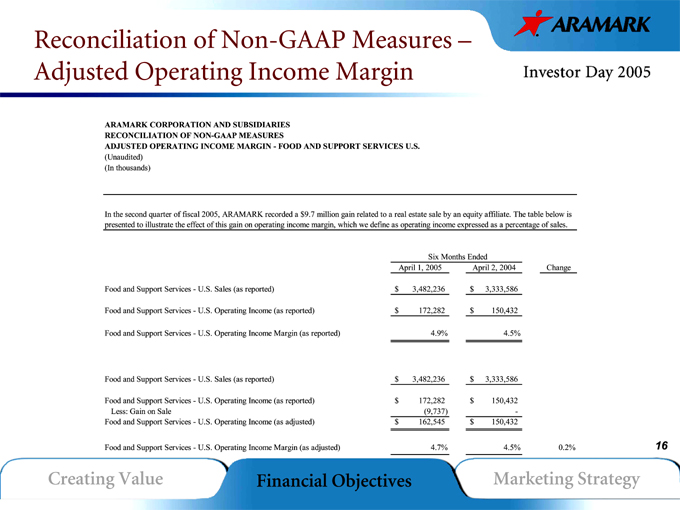

Reconciliation of Non-GAAP Measures –Adjusted Operating Income Margin

ARAMARK CORPORATION AND SUBSIDIARIES RECONCILIATION OF NON-GAAP MEASURES

ADJUSTED OPERATING INCOME MARGIN—FOOD AND SUPPORT SERVICES U.S.

(Unaudited) (In thousands)

In the second quarter of fiscal 2005, ARAMARK recorded a $9.7 million gain related to a real estate sale by an equity affiliate. The table below is presented to illustrate the effect of this gain on operating income margin, which we define as operating income expressed as a percentage of sales.

Six Months Ended

April 1, 2005 April 2, 2004 Change

Food and Support Services—U.S. Sales (as reported) $ 3,482,236 $ 3,333,586

Food and Support Services—U.S. Operating Income (as reported) $ 172,282 $ 150,432

Food and Support Services—U.S. Operating Income Margin (as reported) 4.9% 4.5%

Food and Support Services—U.S. Sales (as reported) $ 3,482,236 $ 3,333,586

Food and Support Services—U.S. Operating Income (as reported) $ 172,282 $ 150,432

Less: Gain on Sale (9,737) -

Food and Support Services—U.S. Operating Income (as adjusted) $ 162,545 $ 150,432

Food and Support Services—U.S. Operating Income Margin (as adjusted) 4.7% 4.5% 0.2%

Creating Value Financial Objectives Marketing Strategy

16

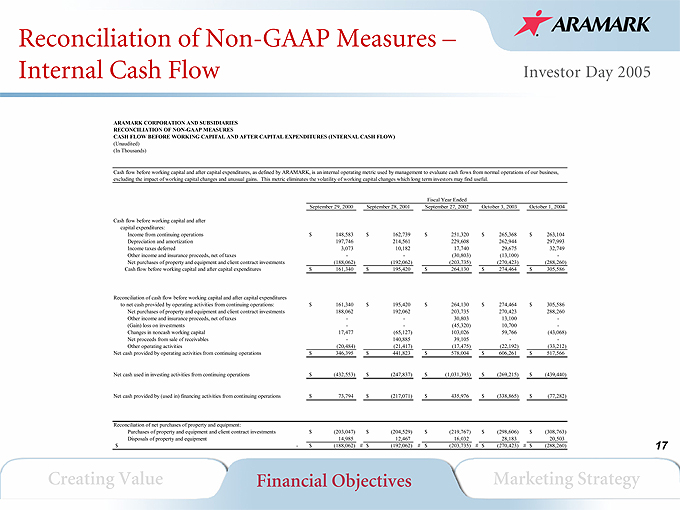

Reconciliation of Non-GAAP Measures –Internal Cash Flow

ARAMARK CORPORATION AND SUBSIDIARIES RECONCILIATION OF NON-GAAP MEASURES

CASH FLOW BEFORE WORKING CAPITAL AND AFTER CAPITAL EXPENDITURES (INTERNAL CASH FLOW)

(Unaudited) (In Thousands)

Cash flow before working capital and after capital expenditures, as defined by ARAMARK, is an internal operating metric used by management to evaluate cash flows from normal operations of our business, excluding the impact of working capital changes and unusual gains. This metric eliminates the volatility of working capital changes which long term investors may find useful.

Fiscal Year Ended

September 29, 2000 September 28, 2001 September 27, 2002 October 3, 2003 October 1, 2004

Cash flow before working capital and after

capital expenditures:

Income from continuing operations $ 148,583 $ 162,739 $ 251,320 $ 265,368 $ 263,104

Depreciation and amortization 197,746 214,561 229,608 262,944 297,993

Income taxes deferred 3,073 10,182 17,740 29,675 32,749

Other income and insurance proceeds, net of taxes - - (30,803) (13,100) -

Net purchases of property and equipment and client contract investments (188,062) (192,062) (203,735) (270,423) (288,260)

Cash flow before working capital and after capital expenditures $ 161,340 $ 195,420 $ 264,130 $ 274,464 $ 305,586

Reconciliation of cash flow before working capital and after capital expenditures

to net cash provided by operating activities from continuing operations: $ 161,340 $ 195,420 $ 264,130 $ 274,464 $ 305,586

Net purchases of property and equipment and client contract investments 188,062 192,062 203,735 270,423 288,260

Other income and insurance proceeds, net of taxes - - 30,803 13,100 -

(Gain) loss on investments - - (45,320) 10,700 -

Changes in noncash working capital 17,477 (65,127) 103,026 59,766 (43,068)

Net proceeds from sale of receivables - 140,885 39,105 - -

Other operating activities (20,484) (21,417) (17,475) (22,192) (33,212)

Net cash provided by operating activities from continuing operations $ 346,395 $ 441,823 $ 578,004 $ 606,261 $ 517,566

Net cash used in investing activities from continuing operations $ (432,553) $ (247,837) $ (1,031,393) $ (269,215) $ (439,440)

Net cash provided by (used in) financing activities from continuing operations $ 73,794 $ (217,071) $ 435,976 $ (338,865) $ (77,282)

Reconciliation of net purchases of property and equipment:

Purchases of property and equipment and client contract investments $ (203,047) $ (204,529) $ (219,767) $ (298,606) $ (308,763)

Disposals of property and equipment 14,985 12,467 16,032 28,183 20,503

- $$(188,062) $ (192,062) # $ (203,735) # $ (270,423) # $ (288,260)

Creating Value Financial Objectives Marketing Strategy

17

17

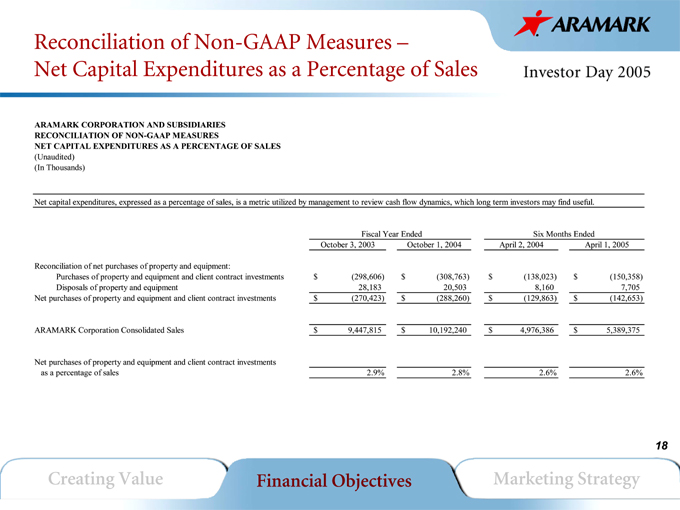

Reconciliation of Non-GAAP Measures –Net Capital Expenditures as a Percentage of Sales

ARAMARK CORPORATION AND SUBSIDIARIES RECONCILIATION OF NON-GAAP MEASURES

NET CAPITAL EXPENDITURES AS A PERCENTAGE OF SALES

(Unaudited) (In Thousands)

Net capital expenditures, expressed as a percentage of sales, is a metric utilized by management to review cash flow dynamics, which long term investors may find useful.

Fiscal Year Ended Six Months Ended

October 3, 2003 October 1, 2004 April 2, 2004 April 1, 2005

Reconciliation of net purchases of property and equipment:

Purchases of property and equipment and client contract investments $ (298,606) $ (308,763) $ (138,023) $ (150,358)

Disposals of property and equipment 28,183 20,503 8,160 7,705

Net purchases of property and equipment and client contract investments $ (270,423) $ (288,260) $ (129,863) $ (142,653)

ARAMARK Corporation Consolidated Sales $ 9,447,815 $ 10,192,240 $ 4,976,386 $ 5,389,375

Net purchases of property and equipment and client contract investments

as a percentage of sales 2.9% 2.8% 2.6% 2.6%

Creating Value Financial Objectives Marketing Strategy

18