ISSUER FREE WRITING PROSPECTUS NO. 1032AB Filed Pursuant to Rule 433 Registration Statement No. 333-162195 Dated December 3, 2010 |  |

$ · Deutsche Bank AG Optimization Securities with Contingent Return

Linked to the Russell 2000® Index due June 28, 2012

Investment Description

Optimization Securities with Contingent Return (the “Securities”) are senior unsecured obligations of Deutsche Bank AG, London Branch (the “Issuer”) with returns linked to the performance of the Russell 2000® Index (the “Index”). The amount you receive at maturity is based on the performance of the Russell 2000® Index and on whether the Final Index Level is below the specified Trigger Level, which is 75.00% of the Initial Index Level. If the Final Index Level is equal to or greater than the Trigger Level, at maturity you will receive your principal plus a return equal to the greater of (i) the Contingent Return of 8.00% and (ii) the Index Return, subject to the Maximum Gain of between 18.00% and 23.00% (to be determined on the Trade Date). If the Final Index Level is below the Trigger Level, you will receive your principal reduced by 1% (or a fraction thereof) for each 1% (or fraction thereof) that the Final Index Level is less than the Initial Index Level.Investing in the Securities is subject to significant risks, including potential loss of up to 100% of your initial investment, limited appreciation at maturity and Deutsche Bank AG’s credit risk.The contingent return feature, including the contingent protection it provides, applies only if you hold the Securities to maturity.Any payment on the Securities, including any contingent protection provided at maturity, is subject to the creditworthiness of the Issuer.

Features

| q | Tactical Investment Opportunity: At maturity, the Securities provide a minimum return of 8.00% as long as the Final Index Level is not less than the Trigger Level, and a Maximum Gain of 18.00% to 23.00% (to be determined on the Trade Date). In moderately bearish to moderately bullish market environments, this strategy may provide the opportunity to outperform direct investments in the Index or the stocks included in the index. |

| q | Contingent Return Feature: The Contingent Return feature also provides contingent protection. If you hold the Securities to maturity and the Final Index Level is equal to or greater than the Trigger Level, you will receive at least 100% of your principal, plus the Contingent Return of 8.00%, subject to the creditworthiness of the Issuer. If the Final Index Level is below the Trigger Level, you will lose the benefit of the Contingent Return feature, including any contingent protection, and you will be fully exposed to the negative Index Return. |

Key Dates 1

| Trade Date | December 22, 2010 | |

| Settlement Date | December 28, 2010 | |

| Final Valuation Date2 | June 22, 2012 | |

| Maturity Date3 | June 28, 2012 | |

| CUSIP | 25154P 73 3 | |

| ISIN | US25154P7336 |

| 1 | The Securities are expected to price on or about December 22, 2010 and settle on or about December 28, 2010. In the event that we make any changes to the expected Trade Date and Settlement Date, the Final Valuation Date and Maturity Date will be changed to ensure that the stated term of the Securities remains the same. |

| 2 | Subject to postponement as described under “Description of Securities—Adjustments to Valuation Dates and Payment Dates” in the accompanying product supplement. |

| 3 | In the event the Final Valuation Date is postponed, the Maturity Date will be the fourth business day after the Final Valuation Date as postponed. |

Security Offerings

We are offering Optimization Securities with Contingent Return linked to the performance of theRussell 2000® Index (the “Index”). The return of the Securities is subject to, and will in no event exceed, the predetermined Maximum Gain of between 18.00% and 23.00% (to be determined on the Trade Date). The Securities are offered at a minimum investment of $1,000 in denominations of $10 and integral multiples in excess thereof.

| Offering | Index | Contingent Return | Maximum Gain† | Initial Index Level† | Trigger Level† | CUSIP/ISIN | ||||||

Optimization Securities with Contingent Return | Russell 2000® Index (Ticker: RTY) | 8.00% | 18.00% to 23.00% per annum | 75.00% of the Initial Index Level | 25154P 73 3 / US25154P7336 |

| †The | Maximum Gain, Initial Index Level and Trigger Level will be set on the Trade Date. |

See “Additional Terms Specific to the Securities” in this free writing prospectus. The Securities will have the terms specified in underlying supplement No. 1 dated September 29, 2009, product supplement AB dated September 29, 2009, the prospectus supplement dated September 29, 2009 relating to our Series A global notes of which these Securities are a part and the prospectus dated September 29, 2009, as modified and supplemented by this free writing prospectus. See “Key Risks” on page 6 of this free writing prospectus and “Risk Factors” beginning on page 7 in the accompanying product supplement.

Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this free writing prospectus relates. Before you invest in the Securities offered hereby, you should read these documents and any other documents relating to this offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Our Central Index Key, or CIK, on the SEC website is 0001159508. Alternatively, Deutsche Bank AG, any agent or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement, underlying supplement and this free writing prospectus if you so request by calling toll-free 1-800-311-4409.

You may revoke your offer to purchase the Securities at any time prior to the time at which we accept such offer by notifying the applicable agent. We reserve the right to change the terms of, or reject any offer to purchase, the Securities prior to their issuance. We will notify you in the event of any changes to the terms of the Securities, and you will be asked to accept such changes in connection with your purchase of the Securities. You may also choose to reject such changes, in which case we may reject your offer to purchase the Securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Securities or passed upon the accuracy or the adequacy of this free writing prospectus, the underlying supplement the accompanying prospectus, the prospectus supplement and product supplement AB. Any representation to the contrary is a criminal offense. The Securities are not bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

| Offering of Securities | Price to Public | Discounts and Commissions | Proceeds to Us | |||

| Optimization Securities with Contingent Return linked to the Russell 2000® Index | ||||||

Per Security | $10.00 | $0.20 | $9.80 | |||

Total | ||||||

Deutsche Bank Securities Inc. (“DBSI”) is our affiliate. For more information see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus.

| UBS Financial Services Inc. | Deutsche Bank Securities |

Additional Terms Specific to the Securities

You should read this free writing prospectus, together with the underlying supplement No. 1 dated September 29, 2009, product supplement AB dated September 29, 2009, the prospectus supplement dated September 29, 2009 relating to our Series A global notes of which these Securities are a part and the prospectus dated September 29, 2009. You may access these documents on the SEC website atwww.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| ¨ | Underlying supplement No. 1 dated September 29, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312509200168/d424b21.pdf

| ¨ | Product supplement AB dated September 29, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312509200386/d424b21.pdf

| ¨ | Prospectus supplement dated September 29, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312509200021/d424b31.pdf

| ¨ | Prospectus dated September 29, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000095012309047023/f03158be424b2xpdfy.pdf

References to “Deutsche Bank AG,” “we,” “our” and “us” refer to Deutsche Bank AG, including, as the context requires, acting through one of its branches. In this free writing prospectus, “Securities” refers to the Optimization Securities with Contingent Return that are offered hereby, unless the context otherwise requires. This free writing prospectus, together with the documents listed above, contains the terms of the Securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Key Risks” in this free writing prospectus and “Risk Factors” in the accompanying product supplement, as the Securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before deciding to invest in the Securities.

Investor Suitability

The suitability considerations identified below are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review “Key Risks” on page 6 of this free writing prospectus and “Risk Factors” on page 7 of the accompanying product supplement.

The Securities may be suitable for you if:

| ¨ | You seek an investment whose return is linked to the performance of the Index. |

| ¨ | You believe that the level of the Index will increase moderately—meaning that the Index level will increase over the term of the Securities, although such an increase is unlikely to exceed the Maximum Gain indicated herein at maturity. |

| ¨ | You are willing to risk losing your principal if the Final Index Level is below the Trigger Level. |

| ¨ | You are willing to invest in the Securities based on the Contingent Return of 8.00% and the range indicated for the predetermined Maximum Gain of 18.00% to 23.00% (to be determined on the Trade Date). |

| ¨ | You are willing to forgo dividends or other distributions paid on the stocks included in the Index. |

| ¨ | You do not seek current income from this investment. |

| ¨ | You are willing and able to hold the Securities to maturity, a term of 18 months. |

| ¨ | You are willing to invest in Securities for which there may be little or no secondary market. |

| ¨ | You are comfortable with the creditworthiness of Deutsche Bank AG, as Issuer of the Securities. |

The Securities may not be suitable for you if:

| ¨ | You do not seek an investment with exposure to the performance of the Index. |

| ¨ | You believe the level of the Index will decrease below the Trigger Level or you believe the level of the Index will increase more than moderately over the term of the Securities—meaning that such an increase is likely to exceed the Maximum Gain indicated herein at maturity. |

| ¨ | You seek an investment that is fully principal protected and you are not willing to make an investment that is exposed to the full downside performance of the Index if the Final Index Level is below the Trigger Level. |

| ¨ | You seek an investment that is exposed to the full potential appreciation of the Index, without a cap on participation. |

| ¨ | You prefer to receive the dividends or other distributions paid on any stocks included in the Index. |

| ¨ | You seek current income from this investment. |

| ¨ | You are unable or unwilling to hold the Securities to maturity, a term of 18 months. |

| ¨ | You seek an investment for which there will be an active secondary market. |

| ¨ | You are not willing or are unable to assume the credit risk associated with Deutsche Bank AG, as Issuer of the Securities. |

2

Indicative Terms

Issuer | Deutsche Bank AG, London Branch | |||

Issue Price | $10.00 per Security | |||

Term | 18 months | |||

Index | Russell 2000® Index (Ticker: RTY) | |||

Contingent Return | 8.00% | |||

Maximum Gain | 18.00% to 23.00%. The actual Maximum Gain will be determined on the Trade Date. | |||

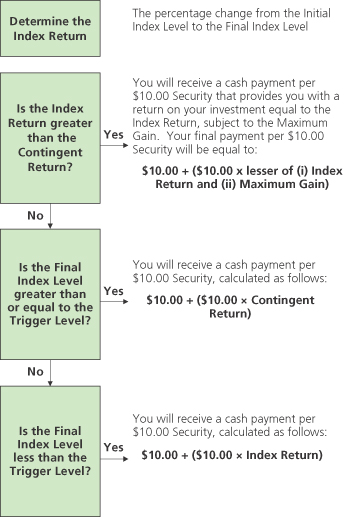

Payment at Maturity (per $10.00 Security) | If the Index Return is greater than the Contingent Return,you will receive a cash payment per $10.00 Security, which will be calculated as follows:

$10.00 + ($10.00 × the lesser of (i) Index Return and (ii) Maximum Gain)

If the Index Return is equal to or less than the Contingent Return and the Final Index Level is greater than or equal to the Trigger Level,you will receive a cash payment per $10.00 Security, which will be calculated as follows:

$10.00 + ($10.00 × Contingent Return)

If the Final Index Level is less than the Trigger Level , you will receive a cash payment per $10.00 Security, which will be calculated as follows:

$10.00 + ($10.00 × Index Return)

In this scenario, you will lose a significant portion, and possibly all, of your initial investment.

Any payment on the Securities, including any contingent protection provided by the contingent return feature, is subject to the creditworthiness of the Issuer. | |||

Index Return | Final Index Level – Initial Index Level Initial Index Level | |||

Initial Index Level | The closing level of the Index on the Trade Date. | |||

Final Index Level | The closing level of the Index on the Final Valuation Date. | |||

Trigger Level | 75.00% of the Initial Index Level | |||

The performance of the Securities will depend on the performance of the Index.

Determining Payment at Maturity Per $10.00 Security

In this scenario, you will lose a significant portion, and possibly all, of your initial investment.

Any payment on the Securities, including any contingent protection provided by the contingent return feature, is subject to the creditworthiness of the Issuer.

3

What Are the Tax Consequences of an Investment in the Securities?

You should review carefully the section of the accompanying product supplement entitled “U.S. Federal Income Tax Consequences.” Although the tax consequences of an investment in the Securities are uncertain, we believe the Securities should be treated as prepaid financial contracts for U.S. federal income tax purposes. Under this treatment, you should not recognize taxable income or loss prior to the maturity of your Securities, other than pursuant to a sale or exchange. Your gain or loss on the Securities should be capital gain or loss and should be long-term capital gain or loss if you have held the Securities for more than one year. If, however, the Internal Revenue Service (the “IRS”) were successful in asserting an alternative treatment for the Securities, the tax consequences of ownership and disposition of the Securities might be affected materially and adversely. We do not plan to request a ruling from the IRS, and the IRS or a court might not agree with the tax treatment described in this free writing prospectus and the accompanying product supplement.

In 2007, Treasury and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments, such as the Securities. The notice focuses in particular on whether to require holders of these instruments to accrue income over the term of their investment. It also asks for comments on a number of related topics, including the character of income or loss with respect to these instruments; the relevance of factors such as the nature of the underlying property to which the instruments are linked; the degree, if any, to which income (including any mandated accruals) realized by non-U.S. persons should be subject to withholding tax; and whether these instruments are or should be subject to the “constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income and impose an interest charge. While the notice requests comments on appropriate transition rules and effective dates, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the Securities, possibly with retroactive effect.

Recently enacted legislation requires certain individuals who hold “debt or equity interests” in any “foreign financial institution” that are not “regularly traded on an established securities market” to report information about such holdings on their U.S. federal income tax returns, generally for tax years beginning in 2011, unless a regulatory exemption is provided. Individuals who purchase the Securities should consult their tax advisers regarding this legislation.

Under current law, the United Kingdom will not impose withholding tax on payments made with respect to the Securities.

For a discussion of certain German tax considerations relating to the Securities, you should refer to the section in the accompanying prospectus supplement entitled “Taxation by Germany of Non-Resident Holders.”

Neither we nor UBS Financial Services Inc. provides any advice on tax matters. Prospective investors should consult their tax advisers regarding the U.S. federal tax consequences of an investment in the Securities (including possible alternative treatments and the issues presented by the 2007 notice), as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

4

Scenario Analysis and Examples at Maturity

The following table and hypothetical examples below illustrate the Payment at Maturity per $10.00 Security for a hypothetical range of performance for the Index from -100.00% to +100.00% and assume a Maximum Gain of 20.50%, an Initial Index Level of 740.00 and a Trigger Level of 555.00 (75.00% of the Initial Index Level). The actual Maximum Gain, Initial Index Level and Trigger Level will be set on the Trade Date. The hypothetical Payment at Maturity examples set forth below are for illustrative purposes only and may not be the actual returns applicable to a purchaser of the Securities. The actual Payment at Maturity will be determined based on the Final Index Level on the Final Valuation Date. You should consider carefully whether the Securities are suitable to your investment goals. The numbers appearing in the table below have been rounded for ease of analysis.

| Final Index Level | Index Return (%) | Payment at Maturity ($) | Return at Maturity (%) | |||

| $1,480.00 | 100.00% | $12.05 | 20.50% | |||

| $1,406.00 | 90.00% | $12.05 | 20.50% | |||

| $1,332.00 | 80.00% | $12.05 | 20.50% | |||

| $1,258.00 | 70.00% | $12.05 | 20.50% | |||

| $1,184.00 | 60.00% | $12.05 | 20.50% | |||

| $1,110.00 | 50.00% | $12.05 | 20.50% | |||

| $1,036.00 | 40.00% | $12.05 | 20.50% | |||

| $962.00 | 30.00% | $12.05 | 20.50% | |||

| $891.70 | 20.50% | $12.05 | 20.50% | |||

| $888.00 | 20.00% | $12.00 | 20.00% | |||

| $851.00 | 15.00% | $11.50 | 15.00% | |||

| $814.00 | 10.00% | $11.00 | 10.00% | |||

| $799.20 | 8.00% | $10.80 | 8.00% | |||

| $777.00 | 5.00% | $10.80 | 8.00% | |||

| $740.00 | 0.00% | $10.80 | 8.00% | |||

| $703.00 | -5.00% | $10.80 | 8.00% | |||

| $666.00 | -10.00% | $10.80 | 8.00% | |||

| $592.00 | -20.00% | $10.80 | 8.00% | |||

| $555.00 | -25.00% | $10.80 | 8.00% | |||

| $518.00 | -30.00% | $7.00 | -30.00% | |||

| $444.00 | -40.00% | $6.00 | -40.00% | |||

| $370.00 | -50.00% | $5.00 | -50.00% | |||

| $296.00 | -60.00% | $4.00 | -60.00% | |||

| $222.00 | -70.00% | $3.00 | -70.00% | |||

| $148.00 | -80.00% | $2.00 | -80.00% | |||

| $74.00 | -90.00% | $1.00 | -90.00% | |||

| $0.00 | -100.00% | $0.00 | -100.00% |

Example 1 — The level of the Index increases by 30.00% from the Initial Index Level of 740.00 to the Final Index Level of 962.00.Because the Index Return of 30.00% is greater than the Maximum Gain of 20.50%, you will receive the Maximum Gain of 20.50%, resulting in a Payment at Maturity of $12.05 per $10.00 Security, calculated as follows:

$10.00 + ($10.00 × Maximum Gain)

$10.00 + ($10.00 × 20.50%) = $12.05

Example 2 — The level of the Index increases by 15.00% from the Initial Index Level of 740.00 to the Final Index Level of 851.00.Because the Index Return of 15.00% is less than the Maximum Gain of 20.50%, you will receive a cash payment of $11.50 per $10.00 Security, calculated as follows:

$10.00 + ($10.00 × Index Return)

$10.00 + ($10.00 × 15.00%) = $11.50

Example 3 – The level of the Index increases by 5.00% from the Initial Index Level of 740.00 to the Final Index Level of 777.00.Because the Index Return of 5.00% is less than the Contingent Return, and the Final Index Level of 777.00 is greater than the Trigger Level of 555.00, you will receive the Contingent Return of 8.00%, resulting in a Payment at Maturity of $10.80 per $10.00 Security, calculated as follows:

$10.00 + ($10.00 × Contingent Return)

$10.00 + ($10.00 × 8.00%) = $10.80

Example 4 — The level of the Index decreases by 30.00% from the Initial Index Level of 740.00 to the Final Index Level of 518.00.Because the Final Index Level of 518.00 is less than the Trigger Level of 555.00, the contingent return feature is lost and you will receive a cash payment of $7.00 per $10.00 Security, calculated as follows:

$10.00 + ($10.00 × Index Return)

$10.00 + ($10.00 × -30.00%) = $7.00

If the Final Index Level is less than the Trigger Level, you will be fully exposed to any decline of the Final Index Level as compared to the Initial Index Level, and you will lose a significant portion, and could lose all, of your initial investment. Any payment on the Securities, including any contingent protection provided by the contingent return feature, is subject to the creditworthiness of the Issuer.

5

Key Risks

An investment in the Securities involves significant risks. Some of the risks that apply to an investment in the Securities offered hereby are summarized below, but we urge you to read the more detailed explanation of risks relating to the Securities generally in the “Risk Factors” section of the accompanying product supplement AB. We also urge you to consult your investment, legal, tax, accounting and other advisers before you invest in the Securities offered hereby.

| ¨ | Your Investment in the Securities May Result in a Loss of Your Initial Investment — The Securities do not guarantee any return of your initial investment. The return on the Securities at maturity is linked to the performance of the Index and will depend on whether, and to the extent which, the Index Return is positive or negative and if the Index Return is negative, whether the Final Index Level is less than the Trigger Level. If the Final Index Level is less than the Trigger Level, you will lose 1% (or a fraction thereof) of your investment for each 1% (or fraction thereof) that the Final Index Level is less than the Initial Index Level.Accordingly, you may lose a significant portion, and could lose all, of your initial investment if the Final Index Level is less than the Trigger Level. |

| ¨ | Capped Appreciation Potential — If the Index Return is positive, you will be entitled to receive at maturity only your initial investment plus an amount equal to the greater of (i) the Contingent Return of 8.00% and (ii) the Index Return, up to the Maximum Gain of between 18.00% and 23.00% (to be determined on the Trade Date). Your return on the Securities will not exceed the Maximum Gain, regardless of any further increase in the level of the Index, which may be significant. Accordingly, the maximum Payment at Maturity will be between $11.80 and $12.30 per $10.00 Security (to be determined on the Trade Date). |

| ¨ | Any Payment on the Securities Is Subject to the Credit of the Issuer — The Securities are senior unsecured debt obligations of the Issuer, Deutsche Bank AG, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Securities, including any contingent protection provided by the Contingent Return feature at maturity, depends on the ability of Deutsche Bank AG to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of Deutsche Bank AG will affect the value of the Securities, and in the event Deutsche Bank AG were to default on its obligations, you may not receive the contingent protection or any amount owed to you under the terms of the Securities. |

| ¨ | Trading and Other Transactions By Us or Our Affiliates, or UBS AG or Its Affiliates, in the Equity and Equity Derivative Markets May Impair the Value of the Securities — We or one or more of our affiliates may hedge our exposure from the Securities by entering into equity and equity derivative transactions, such as over-the-counter options or exchange-traded instruments. Such trading and hedging activities may affect the Index and make it less likely that you will receive a return on your investment in the Securities. It is possible that we or our affiliates could receive substantial returns from these hedging activities while the value of the Securities declines. We or our affiliates, or UBS AG or its affiliates, may also engage in trading in instruments linked to the Index on a regular basis as part of our general broker-dealer and other businesses, for proprietary accounts, for other accounts under management or to facilitate transactions for customers, including block transactions. We or our affiliates, or UBS AG or its affiliates, may also issue or underwrite other securities or financial or derivative instruments with returns linked or related to the Index. By introducing competing products into the marketplace in this manner, we or our affiliates, or UBS AG or its affiliates, could adversely affect the value of the Securities. Any of the foregoing activities described in this paragraph may reflect trading strategies that differ from, or are in direct opposition to, the trading strategy of investors in the Securities. |

| ¨ | Contingent Return Feature, Including Any Contingent Protection, Applies Only if You Hold the Securities to Maturity — You should be willing to hold your Securities to maturity. If you sell your Securities prior to maturity in the secondary market, you may have to sell them at a discount and none of your initial investment will be protected. |

| ¨ | No Coupon or Dividend Payments or Voting Rights — As a holder of the Securities, you will not receive coupon payments, and you will not have voting rights or rights to receive cash dividends or other distributions or other rights that holders of component stocks underlying the Index would have. |

| ¨ | Investing in the Securities Is Not the Same as Investing In the Index — The return on your Securities may not reflect the return you would realize if you invested directly in the Index or the stocks composing the Index, or a security linked directly to the uncapped performance of the Index. |

| ¨ | There May Be Little or No Secondary Market for the Securities — The Securities will not be listed on any securities exchange. Deutsche Bank AG or its affiliates may offer to purchase the Securities in the secondary market but are not required to do so and may cease such market-making activities at any time. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell your Securities easily. Because other dealers are not likely to make a secondary market for the Securities, the price at which you may be able to trade your Securities is likely to depend on the price, if any, at which Deutsche Bank AG or its affiliates are willing to buy the Securities. |

| ¨ | Price Prior to Maturity Is Affected by Many Factors — The market price for the Securities will be affected by many unpredictable and interrelated factors, including the level of the Index; the volatility of the Index; the composition of the Index; the dividend rate on the stocks composing the Index and changes that affect those stocks and their issuers; the time remaining to the maturity of the Securities; interest rates in the markets; geopolitical conditions and economic, financial, political and regulatory or judicial events; and the creditworthiness of Deutsche Bank AG. |

| ¨ | The Securities Have Certain Built-In Costs — While the Payment at Maturity described in this free writing prospectus is based on your entire initial investment, the original Issue Price of the Securities includes the agents’ commission and the estimated cost of hedging our obligations under the Securities through one or more of our affiliates. Such cost includes our or our affiliates’ expected cost of providing such hedge, as well as the profit we or our affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. As a result, the price, if any, at which Deutsche Bank AG or its affiliates would be willing to purchase Securities from you prior to maturity in secondary market transactions, if at all, will likely be lower than the original Issue Price, and any sale prior to the maturity date could result in a substantial loss to you. The Securities are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Securities to maturity. |

6

| ¨ | Potential Deutsche Bank AG Impact on Price — Trading or transactions by Deutsche Bank AG or its affiliates in the stocks comprising the Index, or in futures, options, exchange-traded funds or other derivative products on the stocks comprising the Index, may adversely affect the market value of the stocks composing the Index, the level of the Index, and, therefore, the value of the Securities. |

| ¨ | Potential Conflict of Interest — Deutsche Bank AG and its affiliates may engage in business with the issuers of the stocks composing the Index, which may present a conflict between the obligations of Deutsche Bank AG and you, as a holder of the Securities. The calculation agent, an affiliate of Deutsche Bank AG, will determine the Index Return and Payment at Maturity based on observed levels of the Index in the market. The calculation agent can postpone the determination of the Index Return or the Maturity Date if a market disruption event occurs on the Final Valuation Date. |

| ¨ | We and Our Affiliates or UBS AG and Its Affiliates, May Publish Research, Express Opinions or Provide Recommendations That Are Inconsistent With Investing in or Holding The Securities. Any Such Research, Opinions or Recommendations Could Affect the Index Return to Which the Securities Are Linked to and the Value of the Securities — We, our affiliates and agents, and UBS AG and its affiliates, publish research from time to time on financial markets and other matters that may influence the value of the Securities, or express opinions or provide recommendations that may be inconsistent with purchasing or holding the Securities. Any research, opinions or recommendations expressed by us, our affiliates or agents, or UBS AG or its affiliates, may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the Securities and the Index to which the Securities are linked. |

| ¨ | The U.S. Federal Income Tax Consequences of an Investment in the Securities Are Unclear— There is no direct legal authority regarding the proper U.S. federal income tax treatment of the Securities, and we do not plan to request a ruling from the IRS. Consequently, significant aspects of the tax treatment of the Securities are uncertain, and the IRS or a court might not agree with the treatment of the Securities as prepaid financial contracts. If the IRS were successful in asserting an alternative treatment for the Securities, the tax consequences of ownership and disposition of the Securities might be affected materially and adversely. As described above under “What Are the Tax Consequences of an Investment in the Securities?”, in 2007 Treasury and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments, such as the Securities. Any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the Securities, possibly with retroactive effect. Prospective investors should review carefully the section of the accompanying product supplement entitled “U.S. Federal Income Tax Consequences,” and consult their tax advisers regarding the U.S. federal income tax consequences of an investment in the Securities (including possible alternative treatments and the issues presented by the 2007 notice), as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

7

The Russell 2000® Index

The Russell 2000® Index is designed to track the performance of the small capitalization segment of the U.S. equity market. The Russell 2000® Index measures the composite price performance of stocks of approximately 2,000 companies domiciled in the U.S. and its territories and consists of the smallest 2,000 companies included in the Russell 3000® Index. The Russell 2000® Index represents approximately 10% of the total market capitalization of the Russell 3000® Index.This is just a summary of the Russell 2000® Index. For more information on the Russell 2000® Index, including information concerning its composition, calculation methodology and adjustment policy, please see the section entitled “The Russell Indices – Russell 2000® Index” in the accompanying underlying supplement No. 1 dated September 29, 2009.

The graph below illustrates the performance of the Russell 2000® Index from December 1, 2005 to December 1, 2010. The historical levels of the Russell 2000® Index should not be taken as an indication of future performance and no assurance can be given as to the Final Index Level or any future closing level of the Index.We cannot give you assurance that the performance of the Index will result in the return of any of your initial investment.

Source: Bloomberg

The Russell 2000® Index closing level on December 1, 2010 was 743.14.

Supplemental Plan of Distribution (Conflicts of Interest)

UBS Financial Services Inc. and its affiliates, and Deutsche Bank Securities Inc., acting as agents for Deutsche Bank AG, will receive or allow as a concession or reallowance to other dealers discounts and commissions of $0.20 per $10.00 Security. We will agree that UBS Financial Services Inc. may sell all or part of the Securities that it purchases from us to its affiliates at the price to the public indicated on the cover of the pricing supplement, the document that will be filed pursuant to Rule 424(b)(2) containing the final pricing terms of the Securities, minus a concession not to exceed the discounts and commissions indicated on the cover. DBSI, one of the agents for this offering, is our affiliate. In accordance with NASD Rule 2720, DBSI may not make sales in this offering to any discretionary account without the prior written approval of the customer. See “Underwriting (Conflicts of Interest)” in the accompanying product supplement.

8