Table of Contents

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Act of 1934

For the month of December, 2002

of Chile, Bank

(Translation of Registrant’s name into English)

Chile

(Jurisdiction of incorporation or organization)

Ahumada 251

Santiago, Chile

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F x Form 40-F ¨

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g-3-2(b) under the Securities Exchange Act of 1934.

Yes ¨ No x

(If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82- .)

Table of Contents

BANCO DE CHILE

REPORT ON FORM 6-K

Attached are (i) a free translation from it’s original in Spanish, of a letter filed by Banco de Chile (the “Bank”) with the Superintendency of Banks and Financial Institutions, dated December 19, 2002, informing the admission of Banco de Chile’s ADRs to the Official List by the United Kingdom Listing Authority (UKLA) and the admission of such ADRs to trading on the market for listed securities of the London Stock Exchange and (ii) copy of the Listing Particulars stamped by the UKLA, together with Annexes C, F and H.

2

Table of Contents

FREE TRANSLATION

Santiago, December 19, 2002

Mr. Enrique Marshall Rivera

Superintendent of Banks

and Financial Institutions

Mr. Superintendent:

According to articles 9° and 10° of the Securities Law Nº 18.045 and Chapter 18-10 of the Regulations of the Superintendency of Banks and Financial Institutions (the “Superintendency”), I inform as an essential fact, the admission of Banco de Chile’s ADRs to the Official List by the United Kingdom Listing Authority (UKLA) and the admission of such ADRs to trading on the market for listed securities of the London Stock Exchange. The commencing of trading is expected for December 20, 2002.

Each ADR represents 600 Banco de Chile shares. JP Morgan Chase Bank will continue to act as depositary.

NM Rothschild & Sons Limited acted as Authorized Adviser in the preparation of the listing particulars for the admission of the ADRs.

Likewise, Deutshe Bank A.G. London, will act as “Member Firm” for the ADRs in the London Stock Exchange, providing a market to the ADRs, according to local regulations.

Please find enclosed copy of the Listing Particulars presented to the UKLA. A Spanish translation will be sent shortly.

Sincerely yours,

Julio Guzman H.

Acting General Manager

3

Table of Contents

LISTING PARTICULARS

4

Table of Contents

A copy of this document which, including its Annexes, comprises listing particulars relating to Banco de Chile (together, where appropriate, with its subsidiaries, the “Bank”) in accordance with the Listing Rules made under section 74 of the Financial Services and Markets Act 2000 (the “Act”), has been delivered to the Registrar of Companies in accordance with section 83 of the Act.

Applications have been made to the UK Listing Authority (the “UKLA”) for American Depositary Receipts (“ADRs”) evidencing American Depositary Shares (“ADSs”) to be admitted to the Official List and to the London Stock Exchange for those ADRs to be admitted to trading on its market for Depositary Receipts. Each ADR represents 600 shares of the Bank’s common stock. The ADRs do not have a par value. It is expected that admission to the Official List will become effective, and that dealings in the ADRs will commence, on 20 December 2002. The current expected aggregate market value of the ADRs on admission is £395 million.

For a discussion of certain risks that should be considered prior to an investment in the ADRs, see “Risk Factors” commencing on page 5 of Annex B. The ADRs are specialist securities and should normally only be bought and traded by investors who are particularly knowledgeable in investment matters.

BANCO DE CHILE

(Incorporated in the Republic of Chile)

Admission to the Official List and

to trading on the London Stock Exchange

of 38,578,544 American Depositary Receipts

Authorised Adviser

NM Rothschild & Sons Limited

This document does not constitute an offer to sell, or an invitation by or on behalf of the Bank, the Authorised Adviser or any other person to subscribe for or purchase any of the ADRs. The distribution of this document in certain jurisdictions is restricted by law. Persons into whose possession this document may come are required by the Bank and the Authorised Adviser to inform themselves about and to observe such restrictions. This document may not be used for or in connection with any offer to, or solicitation by, anyone in any jurisdiction.

The Bank’s common stock is traded on the Santiago Stock Exchange, the Valparaiso Stock Exchange, the Chilean Electronic Stock Exchange and the Madrid Stock Exchange. The Bank also has ADRs trading on the New York Stock Exchange (“NYSE”) under the symbol “BCH”. No new shares or ADRs are being issued, and no new money is being raised, at this time. For a description of the ADRs see “American Depositary Receipts” in this document.

Banco de Chile, whose address is Ahumada 251, Santiago, Chile, accepts responsibility for the information contained in this document. To the best of the knowledge and belief of Banco de Chile (which has taken all reasonable care to ensure that such is the case) the information contained in this document is in accordance with the facts and does not omit anything likely to affect the import of such information.

5

Table of Contents

Any reference in this document to listing particulars means this document (including all Annexes) excluding all information incorporated by reference. The Bank has confirmed that any information incorporated by reference, including any such information to which readers of this document are expressly referred, has not been and does not need to be included in the listing particulars to satisfy the requirements of the Act or the Listing Rules. The Bank believes that none of the information incorporated herein by reference conflicts in any material respect with the information included in the listing particulars.

References in this document to “Ch$” are to Chilean Pesos and to “UF” are to “Unidades de Fomento”, an inflation-indexed, peso-denominated monetary unit. Unless otherwise stated, financial information is presented in millions of constant Chilean Pesos as at 30 September 2002 and is based on the conversion rates on 30 September 2002 of £1 = Ch$1,166.70 and US$1 = Ch$747.62. On 16 December 2002 such rates were £1 = Ch$1,103.55 and US$1 = Ch$695.57.

Banco de Chile’s consolidated, unaudited accounts as at and for the quarter ended 30 September 2002 are included as Annex A to this document. Annex A, in particular pages 20 to 24 thereof, contains proforma financial information which has been prepared as if the merger between the Bank and Banco de A. Edwards had occurred prior to 1 January 2002. Annex H contains a reconciliation of the actual financial information of the Bank and Banco de A. Edwards with the proforma financial information. The proforma financial information represents the aggregation of the actual balances for Banco de Chile and Banco de A. Edwards plus an adjustment to uplift balances to take account of inflation for the relevant period, pursuant to the requirements of Chilean GAAP. The inflation uplift is approximately 1.3% for the period from 31 December 2001 to 30 September 2002, approximately 2.2% for the period from 30 September 2001 to 30 September 2002 and approximately 4.4% for the period from 31 December 2000 to 30 September 2002. No other adjustments to the proforma financial information have been made. The proforma financial information is included for illustrative purposes only and, because of its nature, it may not give a true picture of the Bank’s actual financial position or results.

No person is authorised to give any information or to make any representation not contained in this document and, if given or made, such information or representation must not be relied upon as having been authorised by the Bank or the Authorised Adviser. No representation or warranty, express or implied, is made by the Authorised Adviser or any of its affiliates or advisers as to the accuracy or completeness of any information contained in this document and nothing contained in this document is, or shall be relied upon as, a promise or representation by the Authorised Adviser as to the past or the future. Any reproduction or distribution of this document, in whole or in part, and any disclosure of its contents or use of any information herein for any purpose other than considering an investment in the ADRs is prohibited, except to the extent that such information is otherwise publicly available. Neither the delivery of this document nor any sale made of ADRs shall, under any circumstances, create any implication that there has been no change in the affairs of the Bank since the date of this document or that the information contained herein is correct at any time subsequent to its date.

17 December 2002

6

Table of Contents

Page | ||

| 9 | ||

| 9 | ||

| 10 | ||

| 41 | ||

| 42 | ||

| 45 | ||

| 47 | ||

| 58 | ||

| 58 | ||

| 61 | ||

| Annexes: |

| A. | Banco de Chile’s consolidated, unaudited accounts as at and for the quarter ended 30 September 2002. |

| B. | Banco de Chile’s Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 (Form 20-F) for the year ended 31 December 2001. |

| C | Banco de Chile’s consolidated, unaudited balance sheet and income statement as at and for the nine months ended 30 September 2001. |

| D. | Banco de Chile’s audited consolidated financial statements as at and for each of the years ended 31 December 1999 and 31 December 2000. |

| E | Banco de A. Edwards’ Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 (Form 20-F) for the year ended 31 December 2001. |

| F. | Banco de A. Edwards’ consolidated, unaudited balance sheet and income statement as at and for the nine months ended 30 September 2001. |

| G. | Banco de A. Edwards’ audited consolidated financial statements as at and for each of the years ended 31 December 1999 and 31 December 2000. |

| H. | Proforma financial information. |

Annexes A to H referred to above (each an “Annex” and together, the “Annexes”) form a part of this document. The publication of this document should not be taken to imply that any such Annex is accurate at any time subsequent to the date indicated in it. To the extent that the information in the Annexes conflicts with any information presented in other parts of this document the more recent information shall prevail.

7

Table of Contents

References in the Annexes to “we”, “us” and “our” refer to Banco de Chile or (in Annexes E and G) to Banco de A. Edwards.

References to net income for the period to 30 September 2002 are to the net unaudited income for the financial period from 1 January 2002 to that date. Financial information provided in this document as at 30 September 2002 and for the nine month period ended 30 September 2002 is provided on an unaudited basis.

8

Table of Contents

Founded in 1893, the Bank has for much of its recent history been among the largest and most profitable Chilean banks in terms of returns on assets and shareholders’ equity. On 1 January 2002, the Bank merged with Banco de A. Edwards (“Edwards”); the banks were, respectively, the second and fourth largest private sector banks in terms of loans and the third and fifth in terms of equity. The merger created what was at the time the largest Chilean bank in terms of loans and equity.

The financial information for both the Bank and Edwards for each of the years ended 31 December 2001, 2000 and 1999 (Annexes B to G) provide information on the financial position of each of the relevant banks prior to the merger. The principal developments in the Bank’s financial position following the merger are described in Annex A (the Bank’s consolidated, unaudited accounts for the quarter ended and as at 30 September 2002).

The most significant development in 2002 to date has been the merger with Edwards and the subsequent integration of the business and operations of the two banks. Edwards was a Chilean bank with total assets of Ch$2,896,470 million as at 31 December 2001. Edwards merged into the Bank and the Bank acquired all the assets and assumed all the liabilities of Edwards, and incorporated all of the equity and shareholders of that bank.

The Bank has chosen to maintain almost all of the full range of products offered by both institutions and to integrate the market segmentation of the two banks, which in any event had similar divisional structures reflecting this segmentation. In adopting this approach, the Bank has aimed to maximise the focus on customers and to continue to provide the products and services already familiar to them.

The Bank has a multi-brand strategy and has maintained both main brands: “Banco de Chile” and “Banco Edwards”. Twenty of Edwards’ full-service branches have kept the Edwards brand, with a focus on the high-income retail market.

In respect of technology, the Bank has retained Banco de Chile’s operational platform and implemented a two-step integration process. In January 2002, basic interconnection was achieved to facilitate communication between the different platforms. The second stage, involving full integration onto one common platform, was completed in October 2002. The Bank believes this should facilitate completion of the consolidation of a final branch network and related personnel changes on schedule. The Bank has already reduced the initial total of 281 branches by 48, out of the total expected reduction of 51.

The Bank has designed a full programme of activities to foster the integration of the personnel of each institution and to create a common culture within the Bank.

The global mission, strategy and specific goals of the Bank have been articulated and disseminated within the Bank. The Bank has also redefined the functions and responsibilities of its core management group.

9

Table of Contents

The following section describes the business of the Bank following the merger.

Business

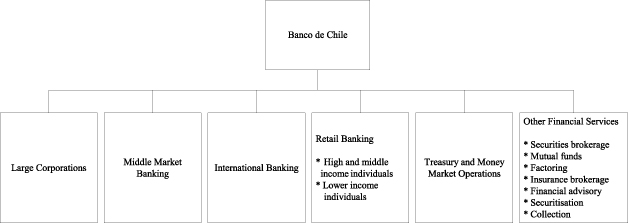

The Bank is engaged principally in commercial banking in Chile, providing general banking services to a diverse customer base that includes large corporations, small and mid-sized businesses and individuals. The Bank is a full-service financial institution providing, directly and indirectly through its subsidiaries and affiliates, a wide variety of credit and non-credit products and services to all segments of the Chilean financial market. The operations of the Bank are organised in five principal business areas:

· | large corporations; |

· | middle market banking; |

· | retail banking; |

· | international banking; and |

· | treasury and money market operations, |

as well as eight non-banking financial services subsidiaries. The Bank’s corporate banking services include commercial loans, working capital facilities and trade finance, foreign exchange, capital market services, cash management and non-credit services such as payroll and payment services. The Bank also provides a wide range of treasury and risk management products to its corporate customers, and provides its individual customers with credit cards, residential mortgages, auto and consumer loans as well as traditional deposit services such as cheque and savings accounts and time deposits.

The Bank offers international banking services through its branch in New York, its agency in Miami, representative offices in Buenos Aires, São Paulo and Mexico City and a worldwide network of approximately 1,000 correspondent banks. In addition to its commercial banking operations, the Bank through its subsidiaries, offers a variety of non-banking financial services including securities brokerage, mutual fund management, financial advisory services, factoring, insurance brokerage, securitisation, collection and sales services.

As at 30 September 2002, the Bank had:

· | total assets of Ch$9,237,750 million (US$12,356 million); |

· | loans outstanding of Ch$6,216,954 million (US$8,316 million); |

· | deposits of Ch$5,410,368 million (US$7,237 million); and |

· | shareholders’ equity of Ch$598,104 million (US$800 million). |

As at 30 September 2002, the Bank was the second largest private bank in Chile, in terms of total loans (excluding interbank loans), reaching a market share of 18.9% at

10

Table of Contents

that date, according to the Superintendency of Banks and Financial Institutions in Chile (the“Chilean Superintendency of Banks”).

The Bank is headquartered in Santiago and, as at 30 September 2002, had 8,978 employees and delivered financial products and services through a nationwide network of 233 branches, 745 automated teller machines (“ATMs”) and other electronic distribution channels.

Business Strategy

The Bank’s long-term strategy is to maintain its position as a leading bank in Chile, providing a broad range of financial products and services to large corporations, small and mid-sized companies and individuals nationwide. As part of this strategy, the Bank operates under a multi-brand approach in order to target the different market segments taking advantage of its well positioned brand names: “Banco de Chile”, “Banco Edwards”, “Banchile”, “Credichile” and “Leasing Andino”.

The Bank’s strategy is focused on:

· | delivering superior service that responds to the specific needs of its customers in each market segment; |

· | enhancing profitability by increasing revenues from fee-based services through development of new services and active cross-selling of such services to its customers; |

· | continuing to focus on measures that control costs and otherwise enhance productivity to improve its existing efficiency standards; and |

· | further developing the international products and services that it offers to its customers. |

The key components of the Bank’s strategy are described below.

· | Deliver Superior Customer Service |

The Bank’s banking strategy is focused on developing long-term relationships with its customers by emphasising customer service and providing a broad range of financial products and services. As the Chilean economy recovers, the Bank expects its corporate and individual customers to continue to require more comprehensive credit and non-credit financial services than in the past. In the large corporate segment, the Bank is focused on increasing offerings of specialised lending products, treasury and cash management services. In the middle market segment, the Bank intends to increase its lending activities and offerings of fee-based services such as electronic banking, import-export financial services, financial advisory services and cash management services. To expand the Bank’s high and middle-income individual customer base, the Bank intends to market actively its broad range of products and services to this segment, to cross-sell products and services, such as mutual funds, lease financing, factoring and securities brokerage services, and to develop new services targeted to the specific needs of these customers.

11

Table of Contents

· | Expand Fee-Based Services |

In recent years, the Bank’s margins from traditional lending activities have declined significantly and, as a result, it has increasingly shifted its focus to developing other sources of revenue such as fee-based products and services. The Bank’s consolidated income from fees and other services has continued to grow over the last three years and was Ch$62,902 million in the first nine months of 2002. The Bank seeks to continue to grow fee revenue by developing new services and by cross-selling these services to its existing customer base. In the Bank’s corporate business, it intends to market actively fee-based services such as electronic banking, receivables collection, payroll services, supplier payments, investment advisory services and cash management. In the Bank’s retail banking business, it seeks to increase revenues from fee-based services such as telephone and PC banking, ATMs, general cheque services, credit cards, mutual funds, securities brokerage and insurance brokerage.

· | Maintain Focus on Operating Efficiencies |

During the year ended 31 December 2001, the Bank’s consolidated operating expenses represented approximately 54.4% of its operating revenue. This ratio increased to 59.8% in the first nine months of 2002 mainly as a result of non-recurring expenses related to the merger. As the Chilean banking sector continues to grow, the Bank believes that a low-cost structure will become increasingly important to compete profitably.

The Bank has invested in technology during recent years and plans to continue to focus on technology in the future to achieve further improvements in customer service and operating efficiency.

· | Provide Competitive International Products and Services |

The Bank intends to provide to its primarily Chilean customer base the complete array of international products locally offered at competitive prices. The Bank’s primary focus in this respect will be on trade financing of customer related operations, one of its traditional areas of international activity. To implement this strategy, the Bank intends to take advantage of its New York branch and Miami agency to strengthen its relationships with Chilean businesses engaged in international trade.

History

The Bank was established in 1893 as a result of a merger of Banco Nacional de Chile, Banco Agricola and Banco de Valparaiso which created the largest privately held bank in Chile. To the best of the Bank’s knowledge, it retained this status until the mid-1990s. Throughout the 20th century, the Bank developed a well-recognised name in Chile and expanded its operations in foreign markets where it developed an extensive network of correspondent banks. In 1906, the Bank established a representative office in London which it maintained until 1985, when the Bank’s foreign operations were centralised at the New York branch.

Beginning in the early 1970s, the Chilean government assumed control of a majority of Chilean banks then in operation and all but one of the foreign banks operating at the time closed their branches and offices in Chile. Throughout this era, the Bank remained

12

Table of Contents

privately owned, with the Chilean government owning participating shares which it sold to private investors in 1975.

· The 1982-1983 Economic Crisis and the Central Bank Subordinated Debt

During the 1982-1983 economic crisis, the Chilean banking system experienced significant instability due to, among other things, a recession in most of the world’s major economies accompanied by high international interest rates, an overvalued peso, a lack of stringent banking regulation and ineffective credit policies at most Chilean banking organisations. The financial crisis required that the Central Bank and the Chilean government provide assistance to most Chilean private-sector banks (including the Bank).

During this period, the Bank experienced significant financial difficulties, as a result of which the Chilean government assumed administrative control over it. In 1985 and 1986, the Bank increased its capital and sold shares representing 88% of its capital to more than 30,000 new shareholders. As a result, no single shareholder held a controlling stake in the Bank. In 1987, the Chilean Superintendency of Banks returned control and administration of the Bank to its shareholders.

Subsequent to the 1982-1983 economic crisis, like most major Chilean banks, the Bank sold certain of its non-performing loans to the Central Bank at face value on terms that included a repurchase obligation. The repurchase obligation was later exchanged for subordinated debt of each participating bank issued in favour of the Central Bank. In 1989, pursuant to Law No. 18,818, banks were permitted to repurchase the portfolio of non-performing loans previously sold to the Central Bank for a price equal to the economic value of such loans, provided the bank assumed a subordinated obligation equal to the difference between the face value of the loans and the economic value paid (the “Central Bank Subordinated Debt”). In November 1989, the Bank repurchased its portfolio of non-performing loans from the Central Bank and assumed the Central Bank Subordinated Debt.

The repayment terms of the Central Bank Subordinated Debt, which at 30 June 1989 equalled approximately US$1.75 billion, required that a certain percentage of the Bank’s income before provisions for the Central Bank Subordinated Debt be applied to repay this obligation. The Central Bank Subordinated Debt did not have a fixed maturity, and payments were made only to the extent that the Bank earned income before provisions for the Central Bank Subordinated Debt. In 1993, 1994 and 1995, the Bank applied 72.9%, 67.6% and 65.8%, respectively, of its income before provisions for the Central Bank Subordinated Debt to the repayment of such debt.

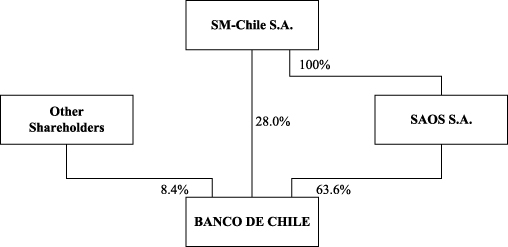

In November 1996, pursuant to Law No. 19,396, the Bank’s shareholders approved a reorganisation by which Banco de Chile was converted into a holding company named SM-Chile S.A. In turn, SM-Chile S.A. organised a new wholly-owned banking subsidiary named Banco de Chile to which it contributed all of its assets and liabilities other than the Central Bank Subordinated Debt. SM-Chile S.A. then created SAOS S.A., a second wholly-owned subsidiary that, pursuant to a prior agreement with the Central Bank, assumed a new repayment obligation (the “Central Bank Indebtedness”) in favour of the Central Bank which replaced the Central Bank Subordinated Debt in its entirety.

13

Table of Contents

This Central Bank Indebtedness, for which SAOS S.A. is solely responsible and for which there is no recourse to the Bank or SM-Chile S.A., was equal to the unpaid principal of the Central Bank Subordinated Debt that it replaced but had terms that differed in certain respects, the most important of which included a rescheduling of the debt for a term of 40 years providing for equal annual instalments and a pledge of the Bank’s shares as collateral for such debt. The Central Bank Indebtedness bears interest at a rate of 5.0% per year and is denominated in Unidades de Fomento.

In exchange for assuming the Central Bank Indebtedness, SAOS S.A. received from SM-Chile S.A. 63.6% of the Bank’s shares, which serve as collateral for the Central Bank Indebtedness. As a result of the Bank’s merger with Edwards, the percentage of the Bank’s shares held by SAOS S.A. decreased to 42.0%. Dividends received from the Bank are the sole source of SAOS S.A.’s revenue, which it must apply to repay the Central Bank Indebtedness. However, under SAOS S.A.’s agreement with the Central Bank regarding this indebtedness, the Bank has no obligation to distribute dividends to its shareholders. To the extent that distributed dividends are not sufficient to pay the amount due on the Central Bank Indebtedness, SAOS S.A. is permitted to maintain a cumulative deficit balance with the Central Bank that SAOS S.A. commits to pay with future dividends. If the cumulative deficit balance exceeds an amount equal to 20% of the Bank’s capital and reserves, the Central Bank may require SAOS S.A. to sell a sufficient number of shares of the Bank’s stock owned by SAOS S.A. to pay the entire deficit amount accumulated. The shareholders of SM-Chile S.A. have a right of first refusal with respect to that sale. As at 30 September 2002, SAOS S.A. maintained a deficit balance with the Central Bank of Ch$5,678 million, equivalent to 1.02% of the Bank’s capital and reserves. As at the same date, 20.0% of the Bank’s capital and reserves would have amounted to Ch$110,843 million. This deficit is expected to increase at the year end as a result of dividends based on the net income for the full year being less than the amount needed to pay amounts due on the Central Bank Indebtedness. See “Risk Factors” commencing on page 5 of Annex B.

If from time to time in the future the Bank’s shareholders decide to retain and capitalise all or part of the Bank’s annual net income in order to finance the Bank’s future growth, and to distribute stock dividends among its shareholders, the Central Bank may require the Bank to pay the portion of the net income corresponding to shares owned by SAOS S.A. in cash to SAOS S.A. If the Bank distributes stock dividends and the Central Bank does not require it to pay that portion in cash, the shares received by SAOS S.A. must be sold by SAOS S.A. within the following 12 months. The shareholders of SM-Chile S.A. will have a right of first refusal with respect to that sale.

14

Table of Contents

The following diagram presents in summary form the Bank’s ownership structure as at 31 December 2001, which resulted from the November 1996 reorganisation:

The following diagram shows the Bank’s new post-merger ownership structure:

15

Table of Contents

Principal Business Activities of Banco de Chile

The Bank is a full-service financial institution providing, directly and indirectly through its subsidiaries and affiliates, a wide variety of credit and non-credit products and services to all segments of the Chilean financial markets. The following diagram illustrates, in summary form, its principal business areas, which operate through the Bank or, in the case of “Other Financial Services,” through its subsidiaries:

The following table provides information on the composition of the Bank’s loans as at 30 September 2002, allocated among the Bank’s principal business areas:

As at 30 September 2002 | |||||||

(in millions of Ch$, except for percentages) | |||||||

| Large corporations | Ch$ | 2,754,954 | 44.3 | % | |||

| Middle market companies | 1,409,876 | 22.7 | |||||

| International banking | 372,142 | 6.0 | |||||

| Retail banking | 1,607,036 | 25.8 | |||||

| Treasury and money market operations | 29,276 | 0.5 | |||||

| Other financial services (subsidiaries) | 43,670 | 0.7 | |||||

Total loans(1) | 6,216,954 | 100.0 | % | ||||

| Allowances for loan losses | (210,252 | ) | — | ||||

| Total loans net of allowances | Ch$ | 6,006,702 | — | ||||

| (1) | Past due loans were Ch$155,910 million as at 30 September 2002, representing 2.5% of total loans. |

· | Large Corporations |

In general, the Bank’s large corporation business area services domestic companies with annual sales in excess of Ch$12,000 million (approximately US$16 million), multinational corporations, financial institutions, governmental entities and companies affiliated with Chile’s largest conglomerates (regardless of size). This area offers these companies a broad range of products and services tailored to their specific needs. These services include deposit-taking and lending in both pesos and foreign currency, trade and project financing and various non-credit services, such as collection, supplier payments and payroll management. In addition, the Bank’s large corporations area offers a broad range of banking products and services including working capital financing, lines of credit, commercial loans, leasing, corporate financial services,

16

Table of Contents

foreign trade financing, letters of credit in domestic and foreign currencies, mortgage loans, payment and asset management services, cheque accounts and time deposits, and, through its subsidiaries, brokerage, mutual funds and investment fund management services. All of the Bank’s branches (except the Credichile branches) provide services to its large corporation area customers directly and indirectly.

The Bank’s large corporate customers are engaged in a wide spectrum of industry sectors, including, among others: heavy industry, financial institutions, trade and commerce, real estate and construction, and agriculture.

As at 30 September 2002, the Bank had 2,981 large corporate debtors. Loans to large corporations totalled Ch$2,754,954 million as at 30 September 2002, representing 44.3% of the Bank’s total loans at that date.

The following table sets forth the composition of the Bank’s portfolio of loans to large corporations as at 30 September 2002:

As at 30 September 2002 | ||||||

(in millions of Ch$, except for percentages) | ||||||

| Commercial loans | Ch$ | 1,674,045 | 60.8 | % | ||

| Foreign trade loans | 427,705 | 15.5 | ||||

| Contingent loans | 225,803 | 8.2 | ||||

| Leasing contracts | 147,259 | 5.4 | ||||

| Mortgage loans | 113,884 | 4.1 | ||||

| Other loans | 166,258 | 6.0 | ||||

| Total | Ch$ | 2,754,954 | 100.0 | % | ||

The Bank’s large corporation area’s loan portfolio consists principally of unsecured loans with maturities between one and six months and of medium and long-term loans to finance fixed assets, investment projects and infrastructure projects. In addition, its large corporation business area issues contingent credit obligations in the form of letters of credit, bank guarantees and similar obligations in support of the operations of the Bank’s large corporate customers.

The market for loans to large corporations in Chile in recent years has been characterised by reduced profit margins, due in part to the greater direct access of such customers to domestic and international capital markets and other sources of funds. As a result, the Bank has been increasingly focused on fee-generating services, such as payroll processing, dividend payments and billing services as well as computer banking services. This strategy has enabled the Bank to maintain profitable relationships with its large corporate customers while preserving the ability to extend credit when appropriate opportunities arise.

The Bank was party to approximately 3,150 payment service contracts and approximately 730 collection service contracts with large corporate customers as at 30 September 2002. Under these payment contracts, the Bank provides large corporate customers with a system to manage their accounts and make payments to suppliers, pension funds and employees, thereby reducing administrative costs. The Bank believes that cash management and payment service contracts provide a source of low-cost deposits and the opportunity to cross-market its products and fees to payees, many of whom maintain accounts with it. Under the Bank’s collection contracts, the Bank

17

Table of Contents

acts as a collection agent for its large corporate customers, providing centralised collection services for their accounts receivable and other similar payments.

· | Middle Market Banking |

The Bank serves the financing needs of small and medium-size companies through its middle market banking business area. The Bank generally defines medium-size companies as those with annual sales of between Ch$300 million (approximately US$400,000) and Ch$12 billion (approximately US$16 million) and small or emerging companies as those with annual sales of between Ch$45 million (approximately US$60,000) and Ch$300 million. As at 30 September 2002, the Bank’s middle market banking area had approximately 66,500 cheque account holders, of which approximately 70% are small or emerging companies, although 64.2% of the business area’s total loan portfolio are loans to medium-size companies.

The Bank’s middle market banking business area offers its customers a broad range of financial products, including project financing, working capital financing, mortgage loans and debt rescheduling, as well as other alternatives such as leasing and factoring (through its Banchile Factoring subsidiary). The Bank also offers clients full advisory services aimed at facilitating foreign trade, as well as comprehensive financing and service alternatives.

The Bank has developed a set of services designed to facilitate and optimise the operational and financial management of small and medium size companies. These services include payment services (such as employee compensation, taxes and employee benefits), payments to suppliers and automated bill payments. It provides most of these services through remote service channels, such as the internet, to approximately 29,000 customers as at 30 September 2002. It also provides account receipts and instrument collection services through electronic means. All of these products and services are available through the Bank’s nationwide branch network.

Through the Bank’s subsidiaries, the middle market banking area offers customers a range of financial advisory, stock brokerage, mutual fund management and general and life insurance brokerage services.

18

Table of Contents

The following table sets forth the composition of the Bank’s portfolio of loans to middle market companies as at 30 September 2002:

As at 30 September 2002 | ||||||

(in millions of Ch$, except for percentages) | ||||||

| Commercial loans | Ch$ | 634,458 | 45.0 | % | ||

Consumer loans(1) | 14,295 | 1.0 | ||||

| Foreign trade loans | 124,239 | 8.8 | ||||

| Contingent loans | 82,883 | 5.9 | ||||

| Mortgage loans | 347,963 | 24.7 | ||||

| Leasing contracts | 91,261 | 6.5 | ||||

| Other loans | 114,777 | 8.1 | ||||

| Total | Ch$ | 1,409,876 | 100.0 | % | ||

| (1) | Certain commercial loans are classified as consumer loans. |

The Bank’s middle market banking area’s loan portfolio consists primarily of short and long-term commercial loans and mortgage loans. As at 30 September 2002, this area had made loans to customers in trade and commerce, industry, agriculture and construction.

As at 30 September 2002, the Bank had Ch$1,410 billion of outstanding loans to small and medium-size companies, representing 22.7% of its total loan portfolio as at that date.

Commercial Loans. The Bank’s middle market banking business area’s commercial loans, which mainly consist of project financing and working capital loans, are denominated in pesos, UF or U.S. dollars. Commercial loans may have fixed or variable rates of interest and generally mature between one and three months from the date of the loan. As at 30 September 2002, the Bank’s middle market banking area had outstanding commercial loans of Ch$634,458 million, representing 45.0% of the business area’s total loans and 10.2% of its total loans as at that date.

Mortgage Loans. The Bank’s middle market banking business area’s commercial mortgage loans are denominated in UF and generally have maturities of between five and 30 years. As at 30 September 2002, this area had granted mortgage loans outstanding of approximately Ch$347,963 million, representing 24.7% of the business area’s total loans and 5.6% of the Bank’s total loans as at that date.

| • | International Banking |

Through its international banking business area, the Bank offers a range of international services, principally import and export financing, letters of credit, guarantees and other forms of credit support, deposits through its US-based branch and agency as well as currency swaps, banking services and treasury services for corporate clients in Chile and abroad.

The Bank’s international banking business area has two main lines of business: foreign currency products and management of the Bank’s international network. This area deals with all banking products that involve foreign currency, including those related to foreign trade. The Bank’s international banking area designs foreign currency products, educates its account officer sales force throughout the Bank about the Bank’s foreign

19

Table of Contents

currency products, monitors its market share participation and promotes the use of the Bank’s foreign currency products.

As at 30 September 2002, the Bank had approximately Ch$696,322 million in foreign trade loans, representing 11.2% of its loan portfolio, and Ch$109,277 million in letters of credit and other contingent obligations related to foreign trade operations, representing 1.8% of the Bank’s loan portfolio.

The Bank’s international banking business area also manages its international network. This network is made up of a branch in New York and an agency in Miami, three representative offices (located in Mexico City, São Paulo and Buenos Aires) and approximately 1,000 correspondent banks (of which the Bank has established credit relations with approximately 90 correspondent banks and an account relationship with more than 40 correspondent banks). The Bank has reduced its exposure in Argentina and Brazil during the course of 2002.

The Bank uses its international network in order to:

| • | obtain all its foreign currency funding for either trade or general purposes (short or medium-term) for its Santiago head office and its foreign branches; |

| • | supply additional savings alternatives to its predominantly Chilean customers; |

| • | provide banking services to its corporate customers who operate outside of Chile; |

| • | provide treasury and cash management services and lending alternatives to its corporate customers on an international basis; |

| • | diversify its loan and investment portfolio by identifying, mainly through its representative offices, opportunities in dealing with selected customers in pre-approved countries; and |

| • | obtain commercial information on foreign companies that do business in Chile and business opportunities for its Chilean customers seeking to expand to new markets abroad. |

The following table sets forth the composition of the Bank’s portfolio of loans originated through the New York branch and Miami agency, in each case as at 30 September 2002:

As at 30 September 2002 | ||||||

New York Branch | Miami Agency | |||||

(in millions of Ch$ ) | ||||||

| Commercial loans | Ch$ | 63,317 | Ch$ | 51,325 | ||

| Foreign trade loans | 82,549 | 18,923 | ||||

| Interbank loans | 27,819 | 3,762 | ||||

| Contingent loans | 13,852 | 14,216 | ||||

| Other loans | 5,026 | 320 | ||||

| Total | Ch$ | 192,563 | Ch$ | 88,546 | ||

20

Table of Contents

The following table sets forth, as at 30 September 2002, the sources of funding for the New York branch and for the Miami agency:

As at 30 September 2002 | ||||||||||||

New York Branch | Miami Agency | |||||||||||

(in millions of Ch$, except for percentages) | ||||||||||||

| Demand deposits | Ch$ | 95,440 | 17.2 | % | Ch$ | 15,936 | 9.1 | % | ||||

| Certificates of deposit and time deposits | 234,256 | 42.4 | 125,666 | 71.9 | ||||||||

| Other demand deposits | 66,723 | 12.1 | 15,844 | 9.1 | ||||||||

| Contingent liabilities | 13,852 | 2.5 | 14,216 | 8.2 | ||||||||

| Foreign borrowings | 134,775 | 24.4 | 1,959 | 1.1 | ||||||||

| Other liabilities | 7,873 | 1.4 | 1,083 | 0.6 | ||||||||

| Total | Ch$ | 552,919 | 100.0 | % | Ch$ | 174,704 | 100.0 | % | ||||

New York Branch. The Bank’s wholly-owned New York branch was established in 1982 and provides a range of general banking services, including deposit-taking, mainly to non-residents of the United States. As at 30 September 2002, the New York branch had total assets of Ch$574,794 million, including a loan portfolio of Ch$192,563 million, representing 3.1% of the Bank’s total loan portfolio. Of the New York branch’s loans, Ch$63,317 million were commercial loans, mostly to large private corporations in Chile and in other Latin American countries. The remaining Ch$129,246 million were principally foreign trade loans, amounting to Ch$82,549 million, and contingent loans (letters of credit and stand-by letters of credit), amounting to Ch$13,852 million. Investments in bonds and foreign securities were Ch$189,474 million, most of which consisted of private sector bonds.

Funding sources for the New York branch include demand deposits, money market accounts and deposits for less than 30 days of Ch$254,735 million, time deposits of Ch$141,683 million and foreign borrowings of Ch$134,775 million, which is also the outstanding balance of the branch’s long-term syndicated bank loans. As at 30 September 2002, the New York branch’s unaudited financial statements showed shareholders’ equity of Ch$29,840 million (including a net loss for the nine-month period to 30 September 2002 of Ch$7,964 million).

As at 30 September 2002, the New York branch had Ch$2,369 million in past due loans. The New York branch’s allowances for loan losses totalled Ch$1,790 million, which represented 0.9% of the branch’s loan portfolio as at 30 September 2002. In addition, the New York branch had Ch$697 million in country risk allowances. Although the New York branch manages its assets and liabilities locally, it follows the same credit processes as those followed in Santiago, and all credit decisions are made in Santiago.

Miami Agency. The Miami agency was opened in 1995, and provides a range of traditional commercial banking services, mainly to non-residents of the United States, including deposit-taking, providing credit to finance foreign trade and making loans to individuals or Chilean companies involved in foreign trade. Additionally, the Miami agency provides correspondent banking services to financial institutions, including working capital loans, letters of credit and bankers’ acceptances. As at 30 September 2002, the Miami agency had total assets of Ch$180,836 million, a loan portfolio of Ch$88,546 million, representing 1.4% of the Bank’s total portfolio, and an investment portfolio of Ch$42,913 million. The Miami agency’s loan portfolio as at 30 September

21

Table of Contents

2002, consisted primarily of Ch$51,325 million of commercial loans to Latin American private sector companies, including Chilean companies with operations in other Latin American countries, and Ch$18,923 million of foreign trade loans. The agency’s funding sources include current accounts, demand deposits, money market accounts and deposits for less than 30 days (Ch$72,476 million), time deposits (Ch$84,969 million) and contingent liabilities (Ch$14,217 million). The unaudited shareholders’ equity of the Miami agency as at 30 September 2002 was Ch$6,132 million, including a net loss for the nine month period to 30 September 2002 of Ch$320 million. The Bank has a 100% ownership interest in the Miami agency.

As at 30 September 2002, the Miami agency did not have any loans in the past due category. Allowances for loan losses amounted to Ch$656 million, not including the Ch$842 million in country risk allowances. Although the Miami agency manages its assets and liabilities locally, it follows the same credit processes as those followed in Santiago, and all credit decisions are made in Santiago.

With regard to its international deposit-taking from individuals, the Bank applies money-laundering procedures consistent with Chilean and international practice and generally accepts deposits only from customers who have been accepted under the Bank’s customer approval procedures.

· | Retail Banking |

The Bank’s retail banking business area serves the needs of retail customers from high-income to lower-middle income individuals, with service being segmented according to the client’s income. As at 30 September 2002 the bank had Ch$1,607 billion loans made to retail customers outstanding representing 25.8% of the Bank’s total loan portfolio as at that date. The following table sets forth information on the composition of the Bank’s portfolio in loans of its retail banking business area as at 30 September 2002:

As at 30 September 2002 | |||||

(in millions of Ch$, except for percentages) | |||||

| Commercial loans | Ch$ 98,423 | 6.1 | % | ||

| Consumer loans | 374,949 | 23.4 | |||

| Foreign trade loans | 1,086 | 0.1 | |||

| Contingent loans | 1,824 | 0.1 | |||

| Mortgage loans | 741,323 | 46.1 | |||

| Leasing contracts | 4,991 | 0.3 | |||

| Other loans | 384,440 | 23.9 | |||

| Total | Ch$1,607,036 | 100.0 | % | ||

22

Table of Contents

High and Middle-Income Individuals

Through the retail banking area, the Bank serves the needs of high and middle income individuals in Chile. The Bank defines high and middle income individuals as those with annual income in excess of Ch$5.2 million (approximately US$7,000).

The Bank’s high and middle income individuals business area offers its customers a broad range of retail banking products, including residential mortgage loans, lines of credit and other consumer loans, credit cards, cheque accounts, savings accounts and time deposits. It also offers mutual funds and brokerage services to individuals as described under “Operations Through Subsidiaries” below. As at 30 September 2002, the Bank had outstanding extensions of credit to approximately 251,850 high and middle income individuals, including approximately 35,140 residential loans, 218,370 lines of credit, 91,860 other consumer loans and 234,690 credit card accounts. As at the same date, the high and middle income individuals business area maintained 287,480 cheque accounts, 117,180 savings accounts and 71,108 time deposits.

The Bank provides service to high and middle income individual customers through a network of 190 branches, 17 specialised transaction centres, seven specialised “Private Banking” centres, 2,737 ATMs (of which 745 are owned by the Bank) located throughout Chile that form part of a network operated by Redbanc S.A., a company owned by the Bank and 14 other private sector financial institutions. Since 1994, the Bank has offered a nationwide phone-banking, or “Fonobank,” service that permits its customers to receive balances and other account-related information, transfer funds between accounts and effect a wide variety of credit transactions. In 1997, the Bank launched a full 24-hour banking service under the brand “TodaHora” and its homepage on the internet to better serve these customers.

Mortgage Loans

As at 30 September 2002, there were outstanding mortgage loans of Ch$684,646 million, representing 42.6% of the high and middle income business area’s total loans to individuals and 11.0% of the Bank’s total loans. A feature of the Bank’s mortgage loans to individuals is that mortgaged property typically secures all of a mortgagor’s credit with the Bank, including credit card and other loans.

The Bank’s residential mortgage loans generally have maturities of between five and 30 years and are denominated in UF. To reduce the Bank’s exposure to interest rate fluctuations and inflation with respect to its residential loan portfolio, a majority of these residential loans are currently funded through the issuance of mortgage finance bonds, which are recourse obligations with payment terms that are matched to the residential loans and which bear a real market interest rate plus a fixed spread over the rate of change in the UF. Chilean banking regulations limit the amount of a residential mortgage loan that may be financed with a mortgage finance bond to the lesser of 75% of the purchase price of the property securing the loan or the appraised value of such property. In addition, the Bank generally requires that the monthly payments on a residential mortgage loan not exceed 25% of the borrower’s monthly household after-tax income.

The Bank has promoted the expansion of a mortgage-lending product which the Bank calls “Mutuos Hipotecarios” as an alternative form to traditional financing of mortgage

23

Table of Contents

loans with mortgage bonds. Whereas the Bank’s traditional mortgage loans are financed by means of mortgage finance bonds, Mutuos Hipotecarios are financed with the Bank’s general funds, especially long-term subordinated bonds. Mutuos Hipotecarios is a product that is tradable among banks and investment funds. Mutuos Hipotecarios offer the opportunity to finance 80% of the lower of the purchase price or the appraised value of the property, as opposed to the 75% that a standard mortgage would allow.

As at 30 September 2002, the Bank was Chile’s second largest private sector bank in terms of mortgage loans and, based on information prepared by the Chilean Superintendency of Banks, accounted for approximately 19.5% of the residential mortgage loans in the Chilean banking system and approximately 25.4% of such loans made by Chilean private-sector banks.

Credit Cards

The Bank issues both Visa and MasterCard credit cards, and its product portfolio includes both personal and corporate cards. In addition to traditional cards, its credit card portfolio also includes co-branded cards (Travel Club, United Airlines, Global Pass andClub de Beneficios) and 28 affinity card groups.

As at 30 September 2002, the Bank had 258,719 valid accounts, with 390,489 cards. Total charges on the Bank’s cards during the nine month period ended September 2002 amounted to Ch$238,172 million, with Ch$211,855 million corresponding to purchases and service payments in Chile and abroad and Ch$26,317 million corresponding to cash advances (both within Chile and abroad).

As at 30 September 2002, the Bank’s credit card loans amounted to Ch$49,022 million and represented 13.1% of loans in the high and middle income business area.

Merchant acquisition and credit card processing services are provided to the Bank by two related Chilean companies, Transbank S.A. and Nexus S.A. As at 30 June 2002, Transbank had nineteen shareholders and Nexus had seven shareholders, all of which are banks. As at 30 September 2002, the Bank’s equity ownership in Transbank was 17.4% and its equity interest in Nexus was 25.8%.

The Bank believes that the Chilean market for credit cards has a high potential for growth, especially among consumers in the middle-income segment, and that average merchant fees will continue to decline and encourage stores which do not currently accept credit cards to do so. The Bank believes that, in addition to the other banks that operate in Chile, its main competitors in card issuance are department stores and other non-banking businesses.

Debit Cards

The Bank has different types of cards with debit options. Depending on their specifications, the cards can be used for banking transactions on the ATMs that operate on the local network, Redbanc, the Visa International PLUS network, the local network of merchants participating in the local Recompra debit program or the international network of merchants associated with the Electron program. The Bank has given these debit cards different names (Chilecard Normal,Chilecard Plus,Chilecard Electron, Chilecard Empresas, Banjoven and Cheque Electronico) based on their specific

24

Table of Contents

functions and the relevant target market to which they are oriented. The Bank has attained a 28.1% market share of debit card transactions as at 30 September 2002, with approximately 678,000 transactions performed in September 2002.

Instalment Loans

The Bank’s consumer instalment loans to individuals are made within a pre-approved credit limit to finance the cost of goods or services, such as cars, travel and household furnishings. Consumer loans are denominated in pesos or UF, bear interest at fixed or variable rates of interest and are generally repayable in up to 36 monthly instalments.

As at 30 September 2002, the Bank had Ch$228,544 million in instalment loans outstanding, which accounted for 61.0% of the high and middle income business area’s consumer loans. The majority of instalment loans are denominated in pesos and are payable monthly. Auto loans have maturities of between 12 and 60 months at fixed or floating rates of interest. The Bank’s auto loans generate interest income and, in addition, fee income attributable to auto insurance policies.

Lines of Credit

As at 30 September 2002, the Bank had 218,370 approved lines of credit to customers in its high and middle income individuals business area and advances outstanding to 160,000 individuals.

The Bank’s individual lines of credit are generally available on a revolving basis, up to an approved credit limit, and may be used for any purpose. Advances under lines of credit are denominated in pesos and bear interest at a rate that is set monthly. At the customer’s option, such loans may be renewed and re-priced for successive monthly periods, in each case subject to minimum monthly payments.

Deposit Products

The Bank seeks to increase its deposit-taking activities as a means of diversifying its sources of funding. The Bank believes that the deposits of its individual customers provide it with a relatively low-cost, stable funding source, as well as the opportunity to cross-market the Bank’s other products and services. The Bank offers a broad range of cheque accounts, time deposits and savings accounts to its individual customers. Cheque accounts are peso-denominated and non-interest bearing, and savings accounts are denominated in UF and bear interest at a fixed rate of interest. Time deposits are denominated in pesos, UF or U.S. dollars and most bear interest at a fixed rate with a term of 30 to 360 days. Whilst historically demand has been mainly for UF-denominated deposits during times of high inflation, the advent of lower and more stable inflation rates in Chile has increased demand for deposits denominated in pesos.

As at 30 September 2002, the high and middle income business area administered 287,480 cheque accounts for approximately 276,000 customers. As at such date, the Bank’s cheque account balances totalled approximately Ch$1,010,395 million, representing 11.7% of its total liabilities.

25

Table of Contents

Lower-income Individuals: Credichile

The Bank offers products and services to the lower-middle to middle income segments of the Chilean population through Credichile. Credichile represents a distinct delivery channel for the Bank’s products and services in this market segment, maintaining a separate brand and network of 43 Credichile branches and 13 other credit centres.

Improved economic conditions in Chile over the last decade and the growth of the Chilean middle class has resulted in increased demand for consumer credit by lower-middle income individuals, whom the Bank classifies as persons with annual income between Ch$1.2 million (approximately US$2,000) and Ch$5.2 million (approximately US$7,000). Many of these individuals have not had prior exposure to banking products or services. The Bank estimates that this segment consists of approximately two million households. To respond to the unique credit needs of lower-middle income customers, the Bank established Credichile in 1995. Credichile focuses on developing and marketing innovative segment-oriented products to satisfy the needs of individuals in this segment while introducing them to the banking system, and complements the services offered in the Bank’s other business areas, especially its large corporations area, by offering services to employers such as direct deposit capabilities.

Credichile offers the Bank’s customers a range of products, including consumer loans, credit cards, auto loans and residential mortgage loans and a special demand deposit account (see “Bancuenta” below) targeted at low-income customers. As at 30 September 2002, Credichile had 172,408 debtors and total loans outstanding of Ch$162,680 million, representing 2.6% of the Bank’s total loan portfolio as at that date.

The Chilean Superintendency of Banks requires a greater allowance for loan losses with lower credit classifications, such as those of Credichile. Credichile employs its own credit scoring system and other criteria to evaluate and monitor credit risk. Credichile seeks to ensure the quality of the Bank’s loan portfolio through adherence to its loan origination procedures, particularly the use of its credit scoring system and credit management policies including the use of credit bureaus and the services of the Chilean Superintendency of Banks. Credichile also has rigorous procedures for collection of past due loans. Socofin S.A., the Bank’s specialised collection subsidiary whose procedures the Bank oversees, provides collection services. The Bank believes that it has the necessary procedures and infrastructure in place to manage the exposure to the higher degree of credit risk that Credichile presents. These procedures allow the Bank to take advantage of the higher growth and earnings potential of the lower middle income segment while helping to manage the higher risk.

Consumer Lending

Credichile provides short to medium-term consumer loans and credit card services. As at 30 September 2002, Credichile had approximately 159,230 consumer loans that totalled Ch$91,479 million. As at the same date, Credichile customers had 28,890 valid credit card accounts, with loans of Ch$5,900 million.

Bancuenta

Credichile introduced Bancuenta as a basic deposit product that provides consumers with flexibility and ease of use, while at the same time allowing the Bank to tap a segment of the consumer market that previously did not have access to the banking

26

Table of Contents

system. The Bancuenta account is a non-interest bearing demand deposit account without cheque privileges, targeted at customers who want a secure and convenient means of managing and accessing their money. Customers may use the ATM card linked to the Bancuenta account (which may include a revolving line of credit) to make deposits or automatic payments to other Credichile accounts through a network of ATMs available through the Redbanc system.

As at 30 September 2002, Credichile had 655,188 Bancuenta accounts, under which the account holder pays an annual fee, a fee each time the account holder draws on the Bancuenta line of credit and interest on any outstanding balance under the line of credit. All fees and interest due on a Bancuenta account are withdrawn automatically on a monthly basis from funds available in the account. Bancuenta allows the Bank to offer its large corporate customers the ability to pay their employees by direct deposit of funds into the individual employee’s account at Credichile. The Bank believes this product can lead to stronger long-term relationships with its large and middle market corporate customers and with the employees of such customers.

· | Treasury and Money Market Operations |

The Bank’s treasury and money market business area offers a wide range of financial services to its customers. Among these financial services are currency intermediation, instruments developed for currency and interest rate risk hedging, transactions under repurchase agreements and investment products based on bonds, mortgage notes and deposits. Also available through its delivery channels are investments in mutual funds and stock brokerage services.

In addition to providing services, the Bank’s treasury and money market business area is focused on managing currency, interest rate and maturity gaps, ensuring adequate liquidity levels and managing its investment portfolio. This area also performs the intermediation of fixed-income instruments, currencies and derivatives. Interest rate gap management is aimed at generating an adequate funding structure, prioritising the Bank’s capitalisation and asset and liability structure and funding source diversification.

The treasury and money market business area is also in charge of monitoring compliance with regulatory deposit limits, technical reserves and maturity and rate matches. This area monitors the Bank’s adherence to the security margins defined by regulatory limits, as well as risk limits for rate, currency and investment gaps. The treasury and money market business area continually monitors the funding costs of the local financial system, comparing them with the Bank’s costs.

The Bank’s investment portfolio as at 30 September 2002, amounted to Ch$1,872,968 million, of which 61.4% corresponded to instruments issued by the Central Bank, 17.5% corresponded to securities from foreign issuers and 10.8% corresponded to mortgage notes issued by the Bank. The Bank’s investment strategy is designed with a view to supplementing its expected profitability, risks and economic variable projections. The Bank’s investment strategy is kept within regulatory limits as well as internal limits defined by the Bank’s financial committee and its Asset and Liability Management Committee, or ALCO.

27

Table of Contents

· | Operations through Subsidiaries |

The Bank has made several strategic long-term investments in financial services companies, which are engaged in activities complementary to its commercial banking activities. The Bank’s principal goal in making these investments is to develop a full service financial services group capable of meeting the diverse financial needs of the Bank’s current and potential clients.

Chile’s General Banking Law, which took effect in 1981, restricted the ability of Chilean banks to provide non-banking financial services, although prior to 1981 the Bank had established a leasing subsidiary in 1977 and a mutual fund subsidiary in 1980. In 1987, the law was amended and banks were permitted to offer, through subsidiaries, certain services considered complementary to commercial banking activities. During the period from 1987 to 1989, the Bank established two additional subsidiaries to provide the full range of financial products and services that could be offered indirectly by Chilean banks under Chilean law. These products and services include financial leasing, financial advisory services, mutual funds and securities brokerage services. The General Banking Law was further amended in 1997 to extend the scope of permissible activities of banks and their subsidiaries to include factoring, securitisation and insurance brokerage, all of which have been incorporated by the Bank as new activities.

On 23 April 1999, the Bank increased its 65% interest in Leasing Andino S.A. by acquiring, together with Banchile Asesoria Financiera S.A., all of the shares of Leasing Andino S.A. owned by Orix Corporation. On 1 July 1999, the Bank acquired the remaining 6,380 shares outstanding in Leasing Andino S.A. and, consequently, held 100% of this company’s share capital. Leasing Andino S.A. was then dissolved and the Bank assumed all of its rights and obligations. The Bank is continuing the financing lease activities developed by Leasing Andino S.A., and has maintained the Leasing Andino brand and trademark.

On 27 June 2002, the Bank, jointly with Banchile Asesoría Financiera S.A., acquired 100% of the shares of Promarket S.A. and Socofin S.A., respectively. These two new subsidiaries are closed corporations (Sociedad Anónima Cerrada).

28

Table of Contents

The following table sets forth information with respect to the Bank’s financial services subsidiaries for the nine months ending and as at 30 September 2002:

As at 30 September 2002 | ||||||||||

Assets | Capital | Net Income | ||||||||

(in millions of Ch$) | ||||||||||

(unaudited) | ||||||||||

| Banchile Corredores de Bolsa S.A. | Ch$ | 177,080 | Ch$ | 16,968 | Ch$ | 4,335 | ||||

| Banchile Administradora General de Fondos S.A. | 10,565 | 5,301 | 1,256 | |||||||

| Banchile Factoring S.A. | 35,560 | 3,721 | 1,004 | |||||||

| Banchile Asesoria Financiera S.A. | 1,144 | 416 | 515 | |||||||

| Banchile Corredores de Seguros Ltda. | 3,207 | 1,681 | 655 | |||||||

| Banchile Securitizadora S.A. | 1,771 | 443 | (61 | ) | ||||||

| Promarket S.A. | 743 | 286 | 78 | |||||||

| Socofin S.A. | Ch$ | 3,865 | Ch$ | 583 | Ch$ | (314 | ) | |||

Each of these subsidiaries is incorporated under the laws of Chile.

The capital and reserves, net income and total shareholders’ equity of Socofin S.A. and Promarket S.A. are included in the table below:

As at 30 September 2002 | |||||||

Socofin S.A. | Promarket S.A. | ||||||

(in millions of Ch$) | |||||||

(unaudited) | |||||||

| Capital and reserves | Ch$ | 583 | Ch$ | 286 | |||

| Net income | (314 | ) | 78 | ||||

| Total shareholders’ equity | 269 | 364 | |||||

Transactions with Banco de Chile | |||||||

| Accounts receivable against Banco de Chile | 1,191 | 508 | |||||

| Obligations with Banco de Chile | 500 | 0 | |||||

| Net income for 2001 (in millions of constant Ch$) | Ch$ | 258 | Ch$ | 0 | |||

| Amount paid by Banco de Chile for percentage acquired (in millions of Ch$ as of June 2002) | Ch$ | 306 | Ch$ | 279 | |||

29

Table of Contents

The following tables show the names and addresses of all subsidiaries and investments of the Bank as at 17 December 2002:

Subsidiaries | % Holding | Business | Address | |||

| Banchile Factoring S.A. | 99.99 | Factoring | Huérfanos 740, piso 5°, Santiago | |||

| Banchile Administradora General de Fondos S.A. | 99.98 | Funds Administration | Agustinas 975, piso 2°, Santiago | |||

| Banchile Corredores de Bolsa S.A. | 99.98 | Stock Broker | Agustinas 975, piso 2°, Santiago | |||

| Banchile Corredores de Seguros Ltda. | 99.75 | Insurance | Huérfanos 740, piso 5°, Santiago | |||

| Banchile Asesoría Financiera S.A. | 99.52 | Financial Advisory | Agustinas 733, piso 1°, Santiago | |||

| Banchile Securitizadora S.A. | 99.00 | Securitisation | Huérfanos 740, piso 7°, Santiago | |||

| Promarket S.A. | 99.00 | Sale of Financial Products | Tenderini N° 157, Santiago | |||

| Socofin S.A. | 99.00 | Collections | Santo Domingo N° 1088, Santiago |

Investment in other Companies | % Holding | Business | Address | |||

| Artikos Chile | 50.00 | e business | Miraflores 178, piso 18, Stgo. | |||

| Servipag Ltda | 50.00 | Collection of payments for services | Hernando de Aguirre 128, piso 2, Stgo. | |||

| Redbanc S.A. | 25.42 | Funds transfers (ATM) | Huérfanos 770, piso 12, Stgo. | |||

| Soc. Operadora Tarjetas de Crédito Nexus S.A. | 25.81 | Credit card operator | Mc Iver 440, piso 2, Stgo | |||

| Transbank S.A. | 17.44 | Credit card administrator | Huérfanos 770, piso 10, Stgo. | |||

| Bolsa de Valores de Chile (Stock Exchange) | 5.00 | Stock exchange | Huérfanos 770, piso 14, Stgo. | |||

| Centro de Compensación Automatizado S.A. | 33.331 | Banking payment clearing | Huérfanos 770, piso 16, Stgo. | |||

| Sociedad Interbancaria de Depósitos de Valores S.A. | 17.60 | Securities Depositary | Ahumada 179, piso 12, Stgo. | |||

| Empresas de Tarjetas Inteligentes S.A. | 26.67 | Smart card supplier | Mc Iver 440, piso 15, Stgo. | |||

| Bolsa de Comercio de Santiago (Stock Exchange) | 4.17 | Stock exchange | La Bolsa 64, Stgo |

Securities Brokerage Services

The Bank operates securities brokerage services through Banchile Corredores de Bolsa S.A. (“Banchile Corredores”), which is registered with theSuperintendencia de Valores y Seguros, (the “SVS”), the regulator of Chilean open-stock corporations, as a securities broker and is a member of the Santiago Stock Exchange and the Chilean Electronic Stock Exchange. Since it was founded in 1989, Banchile Corredores has provided stock brokerage services, fixed income investments and foreign exchange products to individuals and businesses through the Bank’s branch network. As at 30 September 2002, Banchile Corredores had an aggregate trading volume on the Santiago

30

Table of Contents

Stock Exchange and the Chilean Electronic Stock Exchange of approximately Ch$1,019,738 million. As at 30 September 2002, Banchile Corredores had an unaudited net worth of Ch$21,303 million including a net income of Ch$4,335 million for the nine-month period ended 30 September 2002, which represented 9.9% of the Bank’s consolidated net income for such period.

Mutual and Investment Fund Management

Since 1980, the Bank has provided mutual fund management services through Administradora Banchile de Fondos Mutuos, a subsidiary that on 1 July 2002 changed its name to Banchile Administradora General de Fondos, after the merger between Banchile Mutual Fund and Banchile Investment Fund. As at 30 September 2002 it was the largest mutual fund manager in Chile, managing 27.0% of all Chilean mutual fund assets. As at 30 September 2002, Banchile Administradora General de Fondos operated 32 mutual funds and managed Ch$1,354,556 million in assets on behalf of 83,463 corporate and individual customers.

As at 30 September 2002, Banchile Administradora General de Fondos, a subsidiary of the Bank, had unaudited net worth of Ch$6,557 million, including unaudited net income for the nine months ended 30 September 2002 of Ch$1,256 million, representing 2.9% of the Bank’s consolidated net income for such period.

Factoring Services

This subsidiary, incorporated in May 1999, provides factoring services to the Bank’s customers. Through this service, the Bank purchases its customers’ outstanding debt portfolios, such as bills, notes, promissory notes or contracts, advancing them the cash flows involved and performing the collection of the related instruments. As at June 2002 (the latest practical date for the availability of this data) this subsidiary had an 11.95% market share in Chile’s factoring industry. Banchile Factoring S.A. had unaudited net income of Ch$1,004 million for the nine month period ended 30 September 2002.

Financial Advisory Services

The Bank provides financial advisory and other investment banking services to its customers through Banchile Asesoria Financiera. The services offered by Banchile Asesoria Financiera are directed primarily to the Bank’s corporate customers and include advisory services regarding mergers and acquisitions, restructuring, project financing and strategic alliances. As at 30 September 2002, Banchile Asesoria Financiera had unaudited net worth of Ch$931 million, and unaudited net income of Ch$515 million for the nine month period ended 30 September 2002.

Insurance Brokerage Services

The Bank provides insurance brokerage services to its customers through Banchile Corredores de Seguros Ltda. At the beginning of 2000 it began to offer life insurance policies associated with consumer loans and non-credit related insurance to its individual clients and the general public. Banchile Corredores de Seguros had unaudited net income of Ch$655 million for the nine month period ended 30 September 2002.

31

Table of Contents

Securitisation Services

Through Banchile Securitisation S.A. the Bank offers new investment products to meet the demands of institutional investors such as private pension funds and insurance companies. This subsidiary securitises financial assets, which involves the issuance of a debt instrument, with a credit rating, that can be traded in the Chilean marketplace, backed by a bundle of revenue-producing assets of the client company. As at 30 September 2002, Banchile Securitisation had unaudited net worth of Ch$382 million, including a net loss of Ch$61 million for the nine month period ended 30 September 2002.

Sales services

Promarket S.A. manages a direct sales force selling and promoting the Bank’s products and services (such as cheque accounts, consumer loans and credit cards), together with those of the Bank’s subsidiaries, and researches information about potential customers. As at 30 September 2002, Promarket S.A. had 1,229 employees. As at 30 September 2002, Promarket S.A. had unaudited net worth of Ch$364 million including net income of Ch$78 million for the nine month period ended 30 September 2002.

Collection Services

Through Socofin S.A., the Bank offers judicial and extrajudicial collection services of loans on behalf of the Bank or third parties. As at 30 September 2002, Socofin had unaudited net worth of Ch$269 million, including a net loss of Ch$314 million for the nine month period ended 30 September 2002.

· Distribution Channels and Electronic Banking

The Bank’s distribution network provides integrated financial services and products to its customers through a wide range of channels. This network includes branches, ATMs and home-banking and phone-banking. The Bank owns and operates 745 ATMs, and is connected to the nationwide Redbanc ATM network of approximately 2,737 ATMs. These ATMs allow customers to conduct self-service banking transactions during banking and non-banking hours.

As at 30 September 2002, the Bank had a network of 233 retail branches throughout Chile. The branch system serves as a distribution network for all of the products and services offered to its customers. The Bank’s full-service branches accept deposits, disburse cash, offer the full range of the Bank’s retail banking products such as consumer loans, automobile financing, credit cards and cheque accounts, lend to small and medium-size companies and provide information to current and potential customers.

The Bank offers electronic banking services to its customers 24 hours a day through its internet website, which has homepages that are segmented by market. The Bank’s retail homepage offers a wide variety of services, including the payment of bills, electronic fund transfers, stop payment and non-charge orders, as well as a wide variety of account inquiries. The Bank’s middle market banking homepage offers services including its office banking service,Banconexión, which enables its middle market

32

Table of Contents