UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21128

Legg Mason Partners Variable Equity Trust

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 47th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Marc A. De Oliveira.

Franklin Templeton

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: 877-6LM-FUND/656-3863

Date of fiscal year end: December 31

Date of reporting period: June 30, 2023

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

June 30, 2023

Semi-Annual Report

Franklin Templeton

Model Portfolio Funds

Franklin Templeton Aggressive Model Portfolio

Franklin Templeton Moderately Aggressive Model Portfolio

Franklin Templeton Moderate Model Portfolio

Franklin Templeton Moderately Conservative Model Portfolio

Franklin Templeton Conservative Model Portfolio

The Securities and Exchange Commission has adopted new regulations that will result in changes to the design and delivery of annual and semi-annual shareholder reports beginning in July 2024.

If you have previously elected to receive shareholder reports electronically, you will continue to do so and need not take any action.

Otherwise, paper copies of the Fund’s shareholder reports will be mailed to you beginning in July 2024. If you would like to receive shareholder reports and other communications from the Fund electronically instead of by mail, you may make that request at any time by contacting your insurance company or your financial intermediary (such as a broker-dealer or bank).

|

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Franklin Templeton Model Portfolio Funds

Franklin Templeton Model Portfolio Funds (“Model Portfolio Funds”) consists of separate investment Portfolios, each with its own investment objective and policies. Each Portfolio is a “fund of funds,” investing in other mutual funds, and is managed as an asset allocation program.

The Portfolios are separate investment series of Legg Mason Partners Variable Equity Trust, a Maryland statutory trust.

Letter from the president

Dear Shareholder,

We are pleased to provide the semi-annual report of Franklin Templeton Model Portfolio Funds for the six-month reporting period ended June 30, 2023. Please read on for each Portfolio’s performance information during the Portfolios’ reporting period.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.franklintempleton.com. Here you can gain immediate access to market and investment information, including:

| • | | Market insights and commentaries from our portfolio managers and |

| • | | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

President and Chief Executive Officer

July 31, 2023

| | |

II | | Franklin Templeton Model Portfolio Funds |

Portfolios overview

Each of the five Franklin Templeton Model Portfolio Funds is managed as an asset allocation program and allocates its assets among insurance-dedicated mutual funds that have been selected by New York Life Insurance and Annuity Corporation (“NYLIAC”) as investment options for use with their variable annuity and variable universal life insurance policies, noninsurance-dedicated mutual funds and exchange traded funds (the “underlying funds”). The underlying funds include funds managed by investment advisers that are not affiliated with the Portfolios’ manager and funds managed by affiliated investment advisers. When selecting investments to fulfill a desired asset class exposure, the portfolio managers expect to allocate primarily to underlying funds managed by unaffiliated investment advisers, but may also allocate to affiliated underlying funds. The underlying funds may change from time to time without prior notice to shareholders.

Franklin Templeton Aggressive Model Portfolio1

Franklin Templeton Aggressive Model Portfolio seeks capital appreciation. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 80% to 100% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 0% to 20% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 75% Russell 3000 Indexi, 15% MSCI World Ex U.S.A. Indexii, and 10% Bloomberg U.S. Aggregate Indexiii. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Performance review

For the six months ended June 30, 2023, Class I shares of Franklin Templeton Aggressive Model Portfolio returned 10.94%. The Portfolio’s unmanaged benchmarks, the Bloomberg U.S. Aggregate Index, the Russell 3000 Index, and the Aggressive Model Portfolio Composite Benchmarkiv, returned 2.09%, 16.17% and 14.00%, respectively, over the same time frame.

| | | | |

Performance Snapshot as of June 30, 2023

(unaudited) | |

| | | 6 months | |

| Franklin Templeton Aggressive Model Portfolio: | | | | |

Class I | | | 10.94 | % |

Class II | | | 10.79 | % |

| Bloomberg U.S. Aggregate Index | | | 2.09 | % |

| Russell 3000 Index | | | 16.17 | % |

| Aggressive Model Portfolio Composite Benchmark | | | 14.00 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Portfolio expenses. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

The portfolio managers periodically adjust the allocation of the Portfolio’s assets among the underlying funds depending upon the portfolio managers’ outlook for the equity and bond markets in general, particular sectors of such markets and the performance outlook for the underlying funds. In assessing the equity and bond markets, the portfolio managers consider a broad range of market and economic trends and quantitative factors.

|

| Total Annual Operating Expenses† (unaudited) |

As of the Portfolio’s current prospectus dated May 1, 2023, the gross total annual fund operating expense ratios for Class I and Class II were 0.65% and 0.90%, respectively.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Fund expense ratios are more likely to increase when markets are volatile.

| 1 | The Portfolio is an underlying investment option of various variable annuity and variable life insurance products. The Portfolio’s performance returns do not reflect the deduction of expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the performance of the Portfolio. Past performance is no guarantee of future results. |

| † | Includes expenses of the underlying funds in which the Portfolio invests. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | III |

Portfolios overview (cont’d)

Franklin Templeton Moderately Aggressive Model Portfolio1

Franklin Templeton Moderately Aggressive Model Portfolio seeks capital appreciation. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 60% to 70% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 30% to 40% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 60% Russell 3000 Index, 10% MSCI World Ex U.S.A. Index, and 30% Bloomberg U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Performance review

For the six months ended June 30, 2023, Class I shares of Franklin Templeton Moderately Aggressive Model Portfolio returned 9.25%. The Portfolio’s unmanaged benchmarks, the Bloomberg U.S. Aggregate Index, the Russell 3000 Index, and the Moderately Aggressive Model Portfolio Composite Benchmarkv, returned 2.09%, 16.17% and 11.36%, respectively, over the same time frame.

| | | | |

Performance Snapshot as of June 30, 2023

(unaudited) | |

| | | 6 months | |

| Franklin Templeton Moderately Aggressive Model Portfolio: | | | | |

Class I | | | 9.25 | % |

Class II | | | 9.08 | % |

| Bloomberg U.S. Aggregate Index | | | 2.09 | % |

| Russell 3000 Index | | | 16.17 | % |

| Moderately Aggressive Model Portfolio Composite Benchmark | | | 11.36 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Portfolio expenses. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

The portfolio managers periodically adjust the allocation of the Portfolio’s assets among the underlying funds depending upon the portfolio managers’ outlook for the equity and bond markets in general, particular sectors of such markets and the performance outlook for the underlying funds. In assessing the equity and bond markets, the portfolio managers consider a broad range of market and economic trends and quantitative factors.

|

| Total Annual Operating Expenses† (unaudited) |

As of the Portfolio’s current prospectus dated May 1, 2023, the gross total annual fund operating expense ratios for Class I and Class II were 0.62% and 0.87%, respectively.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Portfolio expense ratios are more likely to increase when markets are volatile.

| 1 | The Portfolio is an underlying investment option of various variable annuity and variable life insurance products. The Portfolio’s performance returns do not reflect the deduction of expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the performance of the Portfolio. Past performance is no guarantee of future results. |

| † | Includes expenses of the underlying funds in which the Portfolio invests. |

| | |

IV | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Franklin Templeton Moderate Model Portfolio1

Franklin Templeton Moderate Model Portfolio seeks capital appreciation. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 45% to 65% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 35% to 55% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 45% Russell 3000 Index, 10% MSCI World Ex U.S.A. Index, and 45% Bloomberg U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Performance review

For the six months ended June 30, 2023, Class I shares of Franklin Templeton Moderate Model Portfolio returned 7.46%. The Portfolio’s unmanaged benchmarks, the Bloomberg U.S. Aggregate Index, the Russell 3000 Index, and the Moderate Model Portfolio Composite Benchmarkvi, returned 2.09%, 16.17% and 9.23%, respectively, over the same time frame.

| | | | |

Performance Snapshot as of June 30, 2023

(unaudited) | |

| | | 6 months | |

| Franklin Templeton Moderate Model Portfolio: | | | | |

Class I | | | 7.46 | % |

Class II | | | 7.39 | % |

| Bloomberg U.S. Aggregate Index | | | 2.09 | % |

| Russell 3000 Index | | | 16.17 | % |

| Moderate Model Portfolio Composite Benchmark | | | 9.23 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Portfolio expenses. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

The portfolio managers periodically adjust the allocation of the Portfolio’s assets among underlying funds depending upon the portfolio managers’ outlook for the equity and bond markets in general, particular sectors of such markets and the performance outlook for the underlying funds. In assessing the equity and bond markets, the portfolio managers consider a broad range of market and economic trends and quantitative factors.

|

| Total Annual Operating Expenses† (unaudited) |

As of the Portfolio’s current prospectus dated May 1, 2023, the gross total annual fund operating expense ratios for Class I and Class II were 0.59% and 0.84%, respectively.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Portfolio expense ratios are more likely to increase when markets are volatile.

| 1 | The Portfolio is an underlying investment option of various variable annuity and variable life insurance products. The Portfolio’s performance returns do not reflect the deduction of expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the performance of the Portfolio. Past performance is no guarantee of future results. |

| † | Includes expenses of the underlying funds in which the Portfolio invests. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | V |

Portfolios overview (cont’d)

Franklin Templeton Moderately Conservative Model Portfolio1

Franklin Templeton Moderately Conservative Model Portfolio seeks a balance of capital appreciation and income. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 30% to 50% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 50% to 70% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 35% Russell 3000 Index, 5% MSCI World Ex U.S.A. Index, and 60% Bloomberg U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Performance review

For the six months ended June 30, 2023, Class I shares of Franklin Templeton Moderately Conservative Model Portfolio returned 5.37%. The Portfolio’s unmanaged benchmarks, the Bloomberg U.S. Aggregate Index, the Russell 3000 Index, and the Moderately Conservative Model Portfolio Composite Benchmarkvii, returned 2.09%, 16.17% and 7.36%, respectively, over the same time frame.

| | | | |

Performance Snapshot as of June 30, 2023

(unaudited) | |

| | | 6 months | |

| Franklin Templeton Moderately Conservative Model Portfolio: | | | | |

Class I | | | 5.37 | % |

Class II | | | 5.28 | % |

| Bloomberg U.S. Aggregate Index | | | 2.09 | % |

| Russell 3000 Index | | | 16.17 | % |

| Moderately Conservative Model Portfolio Composite Benchmark | | | 7.36 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Portfolio expenses. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

The portfolio managers periodically adjust the allocation of the Portfolio’s assets among underlying funds depending upon the portfolio managers’ outlook for the equity and bond markets in general, particular sectors of such markets and the performance outlook for the underlying funds. In assessing the equity and bond markets, the portfolio managers consider a broad range of market and economic trends and quantitative factors.

|

| Total Annual Operating Expenses† (unaudited) |

As of the Portfolio’s current prospectus dated May 1, 2023, the gross total annual fund operating expense ratios for Class I and Class II were 0.61% and 0.85%, respectively.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Fund expense ratios are more likely to increase when markets are volatile.

| 1 | The Portfolio is an underlying investment option of various variable annuity and variable life insurance products. The Portfolio’s performance returns do not reflect the deduction of expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the performance of the Portfolio. Past performance is no guarantee of future results. |

| † | Includes expenses of the underlying funds in which the Portfolio invests. |

| | |

VI | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Franklin Templeton Conservative Model Portfolio1

Franklin Templeton Conservative Model Portfolio seeks a balance of capital appreciation and income. The Portfolio organizes its investments in underlying funds into two main asset classes: the equity class (equity securities of all types) and the fixed income class (fixed income securities of all types). The portfolio managers may invest across all asset classes and strategies. Under ordinary circumstances, the portfolio managers expect to allocate between 10% to 30% of the Portfolio’s assets among underlying funds that invest in equity and equity-like strategies and between 70% to 90% of the Portfolio’s assets among underlying funds that invest in fixed income strategies. The Portfolio’s allocation to each class will be measured at the time of purchase and may vary thereafter as a result of market movement. The Portfolio compares its performance to a composite benchmark, consisting of 20% Russell 3000 Index and 80% Bloomberg U.S. Aggregate Index. The portfolio managers will seek to maintain a level of risk in the Portfolio similar to that of this composite benchmark.

Performance review

For the six months ended June 30, 2023, Class I shares of Franklin Templeton Conservative Model Portfolio returned 3.83%. The Portfolio’s unmanaged benchmarks, the Bloomberg U.S. Aggregate Index, the Russell 3000 Index, and the Conservative Model Portfolio Composite Benchmarkviii, returned 2.09%, 16.17% and 4.82%, respectively, over the same time frame.

| | | | |

Performance Snapshot as of June 30, 2023

(unaudited) | |

| | | 6 months | |

| Franklin Templeton Conservative Model Portfolio: | | | | |

Class I | | | 3.83 | % |

Class II | | | 3.72 | % |

| Bloomberg U.S. Aggregate Index | | | 2.09 | % |

| Russell 3000 Index | | | 16.17 | % |

| Conservative Model Portfolio Composite Benchmark | | | 4.82 | % |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value and investment returns will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost.

All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Portfolio expenses. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

The portfolio managers periodically adjust the allocation of the Portfolio’s assets among underlying funds depending upon the portfolio managers’ outlook for the equity and bond markets in general, particular sectors of such markets and the performance outlook for the underlying funds. In assessing the equity and bond markets, the portfolio managers consider a broad range of market and economic trends and quantitative factors.

|

| Total Annual Operating Expenses† (unaudited) |

As of the Portfolio’s current prospectus dated May 1, 2023, the gross total annual fund operating expense ratios for Class I and Class II were 0.64% and 0.89%, respectively.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Fund expense ratios are more likely to increase when markets are volatile.

| 1 | The Portfolio is an underlying investment option of various variable annuity and variable life insurance products. The Portfolio’s performance returns do not reflect the deduction of expenses imposed in connection with investing in variable annuity or variable life insurance contracts, such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the performance of the Portfolio. Past performance is no guarantee of future results. |

| † | Includes expenses of the underlying funds in which the Portfolio invests. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | VII |

Portfolios overview (cont’d)

As always, thank you for your confidence in our stewardship of your assets.

Sincerely,

Jane Trust, CFA

President and Chief Executive Officer

July 31, 2023

RISKS: Equity securities are subject to price fluctuation and possible loss of principal. Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks. International investments are subject to special risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Emerging market countries tend to have economic, political, and legal systems that are less developed and are less stable than those of more developed countries. Fixed income securities involve interest rate, credit, inflation, and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. High yield bonds are subject to greater price volatility, illiquidity, and possibility of default.

Each Portfolio is a fund of funds and is subject to the risks of the underlying funds in which it invests. In addition to the Portfolios’ operating expenses, you will indirectly bear the operating expenses of the underlying funds. The investment strategies employed by the underlying funds and the securities in which they invest may change without the knowledge of the Portfolios’ portfolio managers. The portfolio managers may invest each Portfolio’s assets in underlying funds that have a limited performance history. Each underlying fund may engage in active and frequent trading, resulting in higher portfolio turnover and transaction costs. The underlying funds in which each Portfolio invests may be either diversified or non-diversified. Certain of the underlying funds may engage in short selling, which is a speculative strategy that involves special risks. Unlike the possible loss on a security that is purchased, there is no limit on the amount of loss on an appreciating security that is sold short.

The model used to manage each Portfolio’s assets provides no assurance that the recommended allocation will either maximize returns or minimize risks. There is no assurance that a recommended allocation will prove the ideal allocation in all circumstances. Derivatives, such as options and futures, can be illiquid, may disproportionately increase losses, and have a potentially large impact on each Portfolio’s performance. The market values of securities or other assets will fluctuate, sometimes sharply and unpredictably, due to changes in general market conditions, overall economic trends or events, governmental actions or intervention, actions taken by the U.S. Federal Reserve or foreign central banks, market disruptions caused by trade disputes or other factors, political developments, armed conflicts, economic sanctions and countermeasures in response to sanctions, major cybersecurity events, investor sentiment, the global and domestic effects of a pandemic, and other factors that may or may not be related to the issuer of the security or other asset. Please see the Portfolios’ prospectus for a more complete discussion of these and other risks and each Portfolio’s investment strategies.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

IMPORTANT INFORMATION: The Portfolios are available only to insurance company separate accounts established by New York Life Insurance and Annuity Corporation that fund certain variable annuity and variable life insurance contracts. These Portfolios may not be available in all states and may only be offered in certain variable products. Please refer to the prospectuses. Variable annuities are long-term, tax-deferred investment vehicles designed for retirement purposes. Gains from tax-deferred investments are taxable as ordinary income upon withdrawal. Withdrawals made prior to age 59 1/2 are subject to a 10% IRS penalty charge and/or surrender charges. Investments in a variable annuity are subject to market risks, including loss of principal. Guarantees are based on the claims-paying ability of the insurer.

| i | The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the U.S. equity market. |

| ii | MSCI World Ex U.S.A. Index captures large-, mid- and small-cap representation across 22 of 23 Developed Markets (DM) countries — excluding the United States. The MSCI World Ex U.S.A. Index calculates performance utilizing local currencies taking out the effect of converting to the U.S. dollar. |

| iii | The Bloomberg U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| iv | The Aggressive Model Portfolio Composite Benchmark is a hypothetical representation of the performance of the Portfolio’s major asset classes. It consists of consists of 75% Russell 3000 Index, 15% MSCI World Ex U.S.A. Index, and 10% Bloomberg U.S. Aggregate Index. |

| v | The Moderately Aggressive Model Portfolio Composite Benchmark is a hypothetical representation of the performance of the Portfolio’s major asset classes. It consists of consists of 60% Russell 3000 Index, 10% MSCI World Ex U.S.A. Index, and 30% Bloomberg U.S. Aggregate Index. |

| vi | The Moderate Model Portfolio Composite Benchmark is a hypothetical representation of the performance of the Portfolio’s major asset classes. It consists of 45% Russell 3000 Index, 10% MSCI World Ex U.S.A. Index, and 45% Bloomberg U.S. Aggregate Index. |

| vii | The Moderately Conservative Model Portfolio Composite Benchmark is a hypothetical representation of the performance of the Portfolio’s major asset classes. It consists of consists of 35% Russell 3000 Index, 5% MSCI World Ex U.S.A. Index, and 60% Bloomberg U.S. Aggregate Index. |

| viii | The Conservative Model Portfolio Composite Benchmark is a hypothetical representation of the performance of the Portfolio’s major asset classes. It consists of 20% Russell 3000 Index and 80% Bloomberg U.S. Aggregate Index. |

| | |

VIII | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Portfolios at a glance (unaudited)

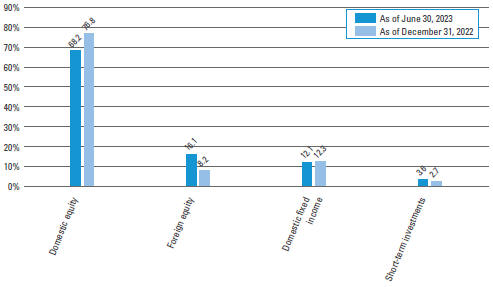

Franklin Templeton Aggressive Model Portfolio Investment Breakdown† (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of June 30, 2023 and December 31, 2022. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 1 |

Portfolios at a glance (unaudited) (cont’d)

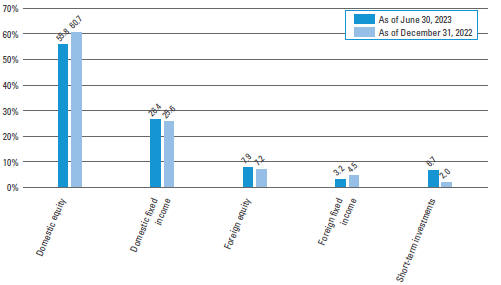

Franklin Templeton Moderately Aggressive Model Portfolio Investment Breakdown† (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of June 30, 2023 and December 31, 2022. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| | |

2 | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

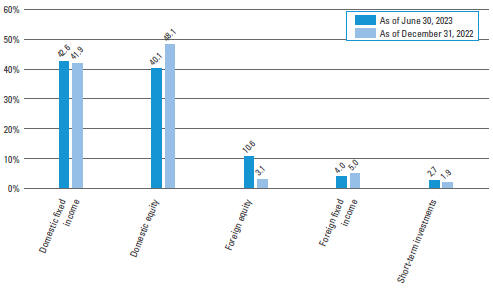

Franklin Templeton Moderate Model Portfolio Investment Breakdown† (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of June 30, 2023 and December 31, 2022. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 3 |

Portfolios at a glance (unaudited) (cont’d)

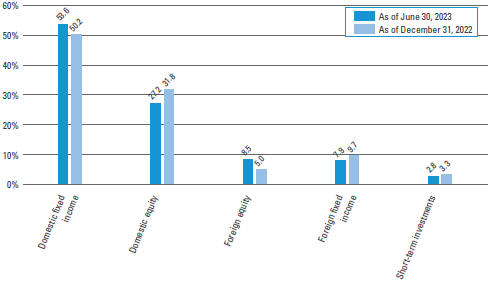

Franklin Templeton Moderately Conservative Model Portfolio Investment Breakdown† (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of June 30, 2023 and December 31, 2022. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| | |

4 | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

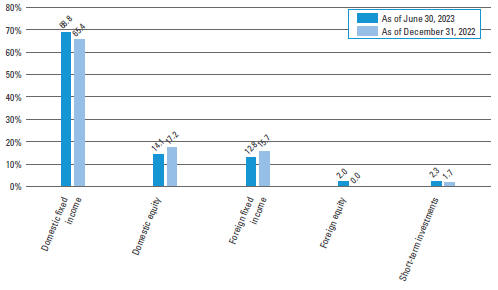

Franklin Templeton Conservative Model Portfolio Investment Breakdown† (%) as a percent of total investments

| † | The bar graph above represents the composition of the Portfolio’s investments as of June 30, 2023 and December 31, 2022. The Portfolio is actively managed. As a result, the composition of the Portfolio’s investments is subject to change at any time. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 5 |

Portfolios expenses (unaudited)

Example

As a shareholder of the Portfolio, you may incur two types of costs: (1) transaction costs and (2)ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2023 and held for the six months ended June 30, 2023.

Actual expenses

The table below titled “Based on actual total return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on hypothetical total return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Based on actual total return1 | | | | | | Based on hypothetical total return1 | |

Franklin

Templeton

Aggressive

Model

Portfolio | | Actual

Total Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Franklin

Templeton

Aggressive

Model

Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | |

| Class I | | | 10.94 | % | | $ | 1,000.00 | | | $ | 1,109.40 | | | | 0.13 | % | | $ | 0.68 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,024.15 | | | | 0.13 | % | | $ | 0.65 | |

| Class II | | | 10.79 | | | | 1,000.00 | | | | 1,107.90 | | | | 0.38 | | | | 1.99 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.91 | | | | 0.38 | | | | 1.91 | |

| 1 | For the six months ended June 30, 2023. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181), then divided by 365. |

| | |

6 | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Example

As a shareholder of the Portfolio, you may incur two types of costs:(1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2023 and held for the six months ended June 30, 2023.

Actual expenses

The table below titled “Based on actual total return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on hypothetical total return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| Based on actual total return1 | | | | | | | | | Based on hypothetical total return1 | |

Franklin

Templeton

Moderately

Aggressive

Model

Portfolio | | Actual

Total Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Franklin

Templeton

Moderately

Aggressive

Model

Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | |

| Class I | | | 9.25 | % | | $ | 1,000.00 | | | $ | 1,092.50 | | | | 0.12 | % | | $ | 0.62 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,024.20 | | | | 0.12 | % | | $ | 0.60 | |

| Class II | | | 9.08 | | | | 1,000.00 | | | | 1,090.80 | | | | 0.37 | | | | 1.92 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.96 | | | | 0.37 | | | | 1.86 | |

| 1 | For the six months ended June 30, 2023. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181), then divided by 365. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 7 |

Portfolios expenses (unaudited) (cont’d)

Example

As a shareholder of the Portfolio, you may incur two types of costs:(1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2023 and held for the six months ended June 30, 2023.

Actual expenses

The table below titled “Based on actual total return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on hypothetical total return” providesinformationabouthypotheticalaccountvaluesandhypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Based on actual total return1 | | | | | | Based on hypothetical total return1 | |

Franklin

Templeton

Moderate

Model

Portfolio | | Actual

Total Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Franklin

Templeton

Moderate

Model

Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | |

| Class I | | | 7.46 | % | | $ | 1,000.00 | | | $ | 1,074.60 | | | | 0.12 | % | | $ | 0.62 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,024.20 | | | | 0.12 | % | | $ | 0.60 | |

| Class II | | | 7.39 | | | | 1,000.00 | | | | 1,073.90 | | | | 0.37 | | | | 1.90 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.96 | | | | 0.37 | | | | 1.86 | |

| 1 | For the six months ended June 30, 2023. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181), then divided by 365. |

| | |

8 | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Example

As a shareholder of the Portfolio, you may incur two types of costs:(1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2023 and held for the six months ended June 30, 2023.

Actual expenses

The table below titled “Based on actual total return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on hypothetical total return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Based on actual total return1 | | | | | | Based on hypothetical total return1 | |

Franklin

Templeton

Moderately

Conservative

Model

Portfolio | | Actual

Total Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Franklin

Templeton

Moderately

Conservative

Model

Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | |

| Class I | | | 5.37 | % | | $ | 1,000.00 | | | $ | 1,053.70 | | | | 0.14 | % | | $ | 0.71 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,024.10 | | | | 0.14 | % | | $ | 0.70 | |

| Class II | | | 5.28 | | | | 1,000.00 | | | | 1,052.80 | | | | 0.38 | | | | 1.93 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.91 | | | | 0.38 | | | | 1.91 | |

| 1 | For the six months ended June 30, 2023. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181), then divided by 365. |

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 9 |

Portfolios expenses (unaudited) (cont’d)

Example

As a shareholder of the Portfolio, you may incur two types of costs:(1) transaction costs and (2) ongoing costs, including management fees; service and/or distribution (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other funds.

This example is based on an investment of $1,000 invested on January 1, 2023 and held for the six months ended June 30, 2023.

Actual expenses

The table below titled “Based on actual total return” provides information about actual account values and actual expenses. You may use the information provided in this table, together with the amount you invested, to estimate the expenses that you paid over the period. To estimate the expenses you paid on your account, divide your ending account value by $1,000 (for example, an $8,600 ending account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled “Expenses Paid During the Period”.

Hypothetical example for comparison purposes

The table below titled “Based on hypothetical total return” provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5.00% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use the information provided in this table to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare the 5.00% hypothetical example relating to the Portfolio with the 5.00% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table below are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Based on actual total return1 | | | | | | Based on hypothetical total return1 | |

Franklin

Templeton

Conservative

Model

Portfolio | | Actual

Total Return2 | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | | | | | | Franklin

Templeton

Conservative

Model

Portfolio | | Hypothetical

Annualized

Total Return | | | Beginning

Account

Value | | | Ending

Account

Value | | | Annualized

Expense

Ratio3 | | | Expenses

Paid

During

the

Period4 | |

| Class I | | | 3.83 | % | | $ | 1,000.00 | | | $ | 1,038.30 | | | | 0.17 | % | | $ | 0.86 | | | | | | | Class I | | | 5.00 | % | | $ | 1,000.00 | | | $ | 1,023.95 | | | | 0.17 | % | | $ | 0.85 | |

| Class II | | | 3.72 | | | | 1,000.00 | | | | 1,037.20 | | | | 0.42 | | | | 2.12 | | | | | | | Class II | | | 5.00 | | | | 1,000.00 | | | | 1,022.71 | | | | 0.42 | | | | 2.11 | |

| 1 | For the six months ended June 30, 2023. |

| 2 | Assumes the reinvestment of all distributions, including returns of capital, if any, at net asset value. Total return is not annualized, as it may not be representative of the total return for the year. Total returns do not reflect expenses associated with separate accounts such as administrative fees, account charges and surrender charges, which, if reflected, would reduce the total returns. Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| 3 | Does not include fees and expenses of the Underlying Funds in which the Portfolio invests. |

| 4 | Expenses (net of compensating balance arrangements, fee waivers and/or expense reimbursements) are equal to each class’ respective annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181), then divided by 365. |

| | |

10 | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Schedules of investments (unaudited)

June 30, 2023

Franklin Templeton Aggressive Model Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | | | | | | | | | | | | |

| Description | | | | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 98.2% | | | | | | | | | | | | | | | | |

| Domestic Equity — 69.5% | | | | | | | | | | | | | | | | |

American Funds Insurance Series — Growth Fund, Class 1A | | | | | | | | | | | 440,220 | | | $ | 39,166,422 | |

BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | | | | | | | | | | 832,416 | | | | 20,294,301 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | | | | | 536,025 | | | | 19,146,820 | |

Fidelity Concord Street Trust — Fidelity® 500 Index Fund, Institutional Premium Shares | | | | | | | | | | | 227,451 | | | | 35,257,123 | |

Legg Mason Partners Variable Equity Trust — ClearBridge Variable Appreciation Portfolio, Class I Shares | | | | | | | | | | | 517,304 | | | | 29,191,469 | (a) |

MainStay VP Funds Trust: | | | | | | | | | | | | | | | | |

MainStay VP Epoch U.S. Equity Yield Portfolio, Initial Class | | | | | | | | | | | 1,688,640 | | | | 29,111,647 | |

MainStay VP Fidelity Institutional AM® Utilities Portfolio, Initial Class | | | | | | | | | | | 1,142,514 | | | | 14,577,223 | (b) |

MainStay VP Small Cap Growth Portfolio, Initial Class | | | | | | | | | | | 1,394,168 | | | | 14,573,519 | |

MainStay VP Wellington U.S. Equity Portfolio, Initial Class | | | | | | | | | | | 1,587,031 | | | | 38,894,486 | |

MFS Variable Insurance Portfolios: | | | | | | | | | | | | | | | | |

MFS® Investors Trust Series, Initial Class | | | | | | | | | | | 671,616 | | | | 24,137,863 | |

MFS® Research Series, Initial Class | | | | | | | | | | | 615,757 | | | | 19,297,823 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | | | | | 1,287,155 | | | | 31,509,545 | |

Variable Insurance Products Fund III — VIP Growth Opportunities Portfolio, Initial Class | | | | | | | | | | | 444,904 | | | | 23,757,898 | |

Total Domestic Equity | | | | | | | | | | | | | | | 338,916,139 | |

| Foreign Equity — 16.4% | | | | | | | | | | | | | | | | |

Fidelity Concord Street Trust — Fidelity® International Index Fund, Institutional Premium Shares | | | | | | | | | | | 368,464 | | | | 17,008,294 | |

Invesco Variable Insurance Funds — Invesco V.I. International Growth Fund, Class I Shares | | | | | | | | | | | 664,917 | | | | 21,802,617 | |

MainStay VP Funds Trust — MainStay VP MacKay International Equity Portfolio, Initial Class | | | | | | | | | | | 1,567,441 | | | | 17,039,025 | |

Variable Insurance Products Fund — VIP Emerging Markets Portfolio, Initial Class | | | | | | | | | | | 2,316,703 | | | | 24,140,048 | |

Total Foreign Equity | | | | | | | | | | | | | | | 79,989,984 | |

| Domestic Fixed Income — 12.3% | | | | | | | | | | | | | | | | |

Fidelity Salem Street Trust — Fidelity® U.S. Bond Index Fund, Institutional Premium Shares | | | | | | | | | | | 5,884,700 | | | | 60,377,021 | |

Total Investments in Underlying Funds before Short-Term Investments (Cost — $481,765,010) | | | | | | | | 479,283,144 | |

| | | | |

| | | Rate | | | | | | | | | | |

| Short-Term Investments — 3.7% | | | | | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $17,893,378) | | | 5.024 | % | | | | | | | 17,893,378 | | | | 17,893,378 | (c) |

Total Investments — 101.9% (Cost — $499,658,388) | | | | | | | | | | | | | | | 497,176,522 | |

Liabilities in Excess of Other Assets — (1.9)% | | | | | | | | | | | | | | | (9,438,305 | ) |

Total Net Assets — 100.0% | | | | | | | | | | | | | | $ | 487,738,217 | |

| (a) | Underlying Fund is affiliated with Franklin Resources, Inc. and more information about the Underlying Fund is available at www.franklintempleton.com (Note 8). |

| (b) | Fidelity Institutional AM is a registered service mark of FMR LLC. |

| (c) | Rate shown is one-day yield as of the end of the reporting period. |

See Notes to Financial Statements.

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 11 |

Schedules of investments (unaudited) (cont’d)

June 30, 2023

Franklin Templeton Moderately Aggressive Model Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | | | | | | | | | | | | |

| Description | | | | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 99.5% | | | | | | | | | | | | | | | | |

| Domestic Equity — 56.3% | | | | | | | | | | | | | | | | |

American Funds Insurance Series — Growth Fund, Class 1A | | | | | | | | | | | 1,077,559 | | | $ | 95,870,372 | |

BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | | | | | | | | | | 1,273,415 | | | | 31,045,847 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | | | | | 940,854 | | | | 33,607,318 | |

Fidelity Concord Street Trust — Fidelity® 500 Index Fund, Institutional Premium Shares | | | | | | | | | | | 937,579 | | | | 145,334,173 | |

Legg Mason Partners Variable Equity Trust — ClearBridge Variable Appreciation Portfolio, Class I Shares | | | | | | | | | | | 1,483,425 | | | | 83,709,677 | (a) |

MainStay VP Funds Trust: | | | | | | | | | | | | | | | | |

MainStay VP Epoch U.S. Equity Yield Portfolio, Initial Class | | | | | | | | | | | 3,436,287 | | | | 59,240,562 | |

MainStay VP Fidelity Institutional AM® Utilities Portfolio, Initial Class | | | | | | | | | | | 3,410,698 | | | | 43,516,752 | (b) |

MainStay VP Small Cap Growth Portfolio, Initial Class | | | | | | | | | | | 2,821,568 | | | | 29,494,410 | |

MainStay VP Wellington U.S. Equity Portfolio, Initial Class | | | | | | | | | | | 3,000,805 | | | | 73,542,835 | |

MFS Variable Insurance Portfolios: | | | | | | | | | | | | | | | | |

MFS® Investors Trust Series, Initial Class | | | | | | | | | | | 1,618,920 | | | | 58,183,996 | |

MFS® Research Series, Initial Class | | | | | | | | | | | 1,649,277 | | | | 51,688,339 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | | | | | 2,871,349 | | | | 70,290,623 | |

Variable Insurance Products Fund III — VIP Growth Opportunities Portfolio, Initial Class | | | | | | | | | | | 1,173,673 | | | | 62,674,140 | |

Total Domestic Equity | | | | | | | | | | | | | | | 838,199,044 | |

| Domestic Fixed Income — 26.6% | | | | | | | | | | | | | | | | |

American Funds Insurance Series — The Bond Fund of America, Class 1A | | | | | | | | | | | 4,633,448 | | | | 43,693,414 | |

BlackRock Variable Series Funds II, Inc. — BlackRock High Yield V.I. Fund, Class I Shares | | | | | | | | | | | 3,350,593 | | | | 22,113,913 | |

Fidelity Salem Street Trust — Fidelity® U.S. Bond Index Fund, Institutional Premium Shares | | | | | | | | | | | 14,424,014 | | | | 147,990,383 | |

Legg Mason Partners Variable Income Trust — Western Asset Core Plus VIT Portfolio, Class I Shares | | | | | | | | | | | 10,309,379 | | | | 51,237,614 | (a) |

MainStay VP Funds Trust: | | | | | | | | | | | | | | | | |

MainStay VP Bond Portfolio, Initial Class | | | | | | | | | | | 2,957,820 | | | | 36,474,065 | |

MainStay VP PIMCO Real Return Portfolio, Initial Class | | | | | | | | | | | 3,491,360 | | | | 29,140,288 | |

PIMCO Variable Insurance Trust — PIMCO Total Return Portfolio, Institutional Class | | | | | | | | | | | 7,298,493 | | | | 65,686,439 | |

Total Domestic Fixed Income | | | | | | | | | | | | | | | 396,336,116 | |

| Foreign Equity — 13.3% | | | | | | | | | | | | | | | | |

Fidelity Concord Street Trust — Fidelity® International Index Fund, Institutional Premium Shares | | | | | | | | | | | 1,607,661 | | | | 74,209,633 | |

Invesco Variable Insurance Funds — Invesco V.I. International Growth Fund, Class I Shares | | | | | | | | | | | 1,578,687 | | | | 51,765,131 | |

MainStay VP Funds Trust — MainStay VP MacKay International Equity Portfolio, Initial Class | | | | | | | | | | | 2,569,442 | | | | 27,931,375 | |

Variable Insurance Products Fund — VIP Emerging Markets Portfolio, Initial Class | | | | | | | | | | | 4,242,798 | | | | 44,209,959 | |

Total Foreign Equity | | | | | | | | | | | | | | | 198,116,098 | |

| Foreign Fixed Income — 3.3% | | | | | | | | | | | | | | | | |

Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class 1 | | | | | | | | | | | 2,470,988 | | | | 18,680,671 | |

PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar- Hedged), Institutional Class | | | | | | | | | | | 3,124,596 | | | | 29,464,938 | |

Total Foreign Fixed Income | | | | | | | | | | | | | | | 48,145,609 | |

Total Investments in Underlying Funds before Short-Term Investments

(Cost — $1,515,120,847) | | | | | | | | 1,480,796,867 | |

See Notes to Financial Statements.

| | |

12 | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Franklin Templeton Moderately Aggressive Model Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | | | | | | | | | | | | |

| Description | | Rate | | | | | | Shares | | | Value | |

| Short-Term Investments — 1.5% | | | | | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $21,733,915) | | | 5.024 | % | | | | | | | 21,733,915 | | | $ | 21,733,915 | (c) |

Total Investments — 101.0% (Cost — $1,536,854,762) | | | | | | | | | | | | | | | 1,502,530,782 | |

Liabilities in Excess of Other Assets — (1.0)% | | | | | | | | | | | | | | | (14,495,719 | ) |

Total Net Assets — 100.0% | | | | | | | | | | | | | | $ | 1,488,035,063 | |

| (a) | Underlying Fund is affiliated with Franklin Resources, Inc. and more information about the Underlying Fund is available at www.franklintempleton.com (Note 8). |

| (b) | Fidelity Institutional AM is a registered service mark of FMR LLC. |

| (c) | Rate shown is one-day yield as of the end of the reporting period. |

See Notes to Financial Statements.

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 13 |

Schedules of investments (unaudited) (cont’d)

June 30, 2023

Franklin Templeton Moderate Model Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | | | | | | | | | | | | |

| Description | | | | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 98.1% | | | | | | | | | | | | | | | | |

| Domestic Fixed Income — 43.0% | | | | | | | | | | | | | | | | |

American Funds Insurance Series — The Bond Fund of America, Class 1A | | | | | | | | | | | 12,265,967 | | | $ | 115,668,069 | |

BlackRock Variable Series Funds II, Inc. — BlackRock High Yield V.I. Fund, Class I Shares | | | | | | | | | | | 3,619,017 | | | | 23,885,515 | |

Fidelity Salem Street Trust — Fidelity® U.S. Bond Index Fund, Institutional Premium Shares | | | | | | | | | | | 14,604,776 | | | | 149,844,997 | |

Legg Mason Partners Variable Income Trust — Western Asset Core Plus VIT Portfolio, Class I Shares | | | | | | | | | | | 13,223,457 | | | | 65,720,584 | (a) |

MainStay VP Funds Trust: | | | | | | | | | | | | | | | | |

MainStay VP Bond Portfolio, Initial Class | | | | | | | | | | | 2,856,190 | | | | 35,220,819 | |

MainStay VP MacKay Convertible Portfolio, Initial Class | | | | | | | | | | | 1,648,801 | | | | 23,975,044 | |

MainStay VP PIMCO Real Return Portfolio, Initial Class | | | | | | | | | | | 3,514,150 | | | | 29,330,498 | |

PIMCO Variable Insurance Trust — PIMCO Total Return Portfolio, Institutional Class | | | | | | | | | | | 8,263,223 | | | | 74,369,010 | |

Total Domestic Fixed Income | | | | | | | | | | | | | | | 518,014,536 | |

| Domestic Equity — 40.4% | | | | | | | | | | | | | | | | |

American Funds Insurance Series — Growth Fund, Class 1A | | | | | | | | | | | 565,174 | | | | 50,283,500 | |

BNY Mellon Investment Portfolios — Technology Growth Portfolio, Initial Shares | | | | | | | | | | | 1,062,026 | | | | 25,892,183 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | | | | | 518,114 | | | | 18,507,046 | |

Fidelity Concord Street Trust — Fidelity® 500 Index Fund, Institutional Premium Shares | | | | | | | | | | | 573,055 | | | | 88,829,274 | |

Legg Mason Partners Variable Equity Trust — ClearBridge Variable Appreciation Portfolio, Class I Shares | | | | | | | | | | | 967,964 | | | | 54,622,219 | (a) |

MainStay VP Funds Trust: | | | | | | | | | | | | | | | | |

MainStay VP Epoch U.S. Equity Yield Portfolio, Initial Class | | | | | | | | | | | 1,366,589 | | | | 23,559,592 | |

MainStay VP Fidelity Institutional AM® Utilities Portfolio, Initial Class | | | | | | | | | | | 2,702,996 | | | | 34,487,261 | (b) |

MainStay VP Small Cap Growth Portfolio, Initial Class | | | | | | | | | | | 1,748,528 | | | | 18,277,713 | |

MainStay VP Wellington U.S. Equity Portfolio, Initial Class | | | | | | | | | | | 1,982,431 | | | | 48,584,816 | |

MFS Variable Insurance Portfolios: | | | | | | | | | | | | | | | | |

MFS® Investors Trust Series, Initial Class | | | | | | | | | | | 1,002,479 | | | | 36,029,089 | |

MFS® Research Series, Initial Class | | | | | | | | | | | 972,482 | | | | 30,477,600 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | | | | | 1,296,136 | | | | 31,729,398 | |

Variable Insurance Products Fund III — VIP Growth Opportunities Portfolio, Initial Class | | | | | | | | | | | 484,819 | | | | 25,889,363 | |

Total Domestic Equity | | | | | | | | | | | | | | | 487,169,054 | |

| Foreign Equity — 10.7% | | | | | | | | | | | | | | | | |

Fidelity Concord Street Trust — Fidelity® International Index Fund, Institutional Premium Shares | | | | | | | | | | | 892,021 | | | | 41,175,694 | |

Invesco Variable Insurance Funds — Invesco V.I. International Growth Fund, Class I Shares | | | | | | | | | | | 1,070,982 | | | | 35,117,495 | |

MainStay VP Funds Trust — MainStay VP MacKay International Equity Portfolio, Initial Class | | | | | | | | | | | 2,122,764 | | | | 23,075,722 | |

Variable Insurance Products Fund — VIP Emerging Markets Portfolio, Initial Class | | | | | | | | | | | 2,811,823 | | | | 29,299,192 | |

Total Foreign Equity | | | | | | | | 128,668,103 | |

| Foreign Fixed Income — 4.0% | | | | | | | | | | | | | | | | |

Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class 1 | | | | | | | | | | | 2,402,514 | | | | 18,163,005 | |

PIMCO Variable Insurance Trust — PIMCO International Bond Portfolio (U.S. Dollar- Hedged), Institutional Class | | | | | | | | | | | 3,200,389 | | | | 30,179,671 | |

Total Foreign Fixed Income | | | | | | | | | | | | | | | 48,342,676 | |

Total Investments in Underlying Funds before Short-Term Investments

(Cost — $1,224,683,120) | | | | | | | | | | | | | | | 1,182,194,369 | |

See Notes to Financial Statements.

| | |

14 | | Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report |

Franklin Templeton Moderate Model Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | | | | | | | | | | | | |

| Description | | Rate | | | | | | Shares | | | Value | |

| Short-Term Investments — 2.7% | | | | | | | | | | | | | | | | |

Blackrock Liquidity Funds — Treasury Trust Fund, Institutional Shares

(Cost — $32,647,480) | | | 5.024 | % | | | | | | | 32,647,480 | | | $ | 32,647,480 | (c) |

Total Investments — 100.8% (Cost — $1,257,330,600) | | | | | | | | | | | | | | | 1,214,841,849 | |

Liabilities in Excess of Other Assets — (0.8)% | | | | | | | | | | | | | | | (9,803,124 | ) |

Total Net Assets — 100.0% | | | | | | | | | | | | | | $ | 1,205,038,725 | |

| (a) | Underlying Fund is affiliated with Franklin Resources, Inc. and more information about the Underlying Fund is available at www.franklintempleton.com (Note 8). |

| (b) | Fidelity Institutional AM is a registered service mark of FMR LLC. |

| (c) | Rate shown is one-day yield as of the end of the reporting period. |

See Notes to Financial Statements.

| | |

| Franklin Templeton Model Portfolio Funds 2023 Semi-Annual Report | | 15 |

Schedules of investments (unaudited) (cont’d)

June 30, 2023

Franklin Templeton Moderately Conservative Model Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | | | | | | | | | | | | |

| Description | | | | | | | | Shares | | | Value | |

| Investments in Underlying Funds — 98.0% | | | | | | | | | | | | | | | | |

| Domestic Fixed Income — 54.0% | | | | | | | | | | | | | | | | |

American Funds Insurance Series — The Bond Fund of America, Class 1A | | | | | | | | | | | 4,798,903 | | | $ | 45,253,658 | |

BlackRock Variable Series Funds II, Inc. — BlackRock High Yield V.I. Fund, Class I Shares | | | | | | | | | | | 1,855,241 | | | | 12,244,587 | |

Fidelity Salem Street Trust — Fidelity® U.S. Bond Index Fund, Institutional Premium Shares | | | | | | | | | | | 5,064,007 | | | | 51,956,717 | |

Legg Mason Partners Variable Income Trust — Western Asset Core Plus VIT Portfolio, Class I Shares | | | | | | | | | | | 5,835,234 | | | | 29,001,112 | (a) |

MainStay VP Funds Trust: | | | | | | | | | | | | | | | | |

MainStay VP Bond Portfolio, Initial Class | | | | | | | | | | | 2,354,502 | | | | 29,034,309 | |

MainStay VP MacKay Convertible Portfolio, Initial Class | | | | | | | | | | | 589,085 | | | | 8,565,825 | |

MainStay VP PIMCO Real Return Portfolio, Initial Class | | | | | | | | | | | 2,486,231 | | | | 20,751,075 | |

PIMCO Variable Insurance Trust — PIMCO Total Return Portfolio, Institutional Class | | | | | | | | | | | 3,209,219 | | | | 28,882,972 | |

Total Domestic Fixed Income | | | | | | | | | | | | | | | 225,690,255 | |

| Domestic Equity — 27.5% | | | | | | | | | | | | | | | | |

American Funds Insurance Series — Growth Fund, Class 1A | | | | | | | | | | | 94,141 | | | | 8,375,711 | |

Delaware VIP Trust — Delaware VIP Small Cap Value Series, Standard Class | | | | | | | | | | | 155,199 | | | | 5,543,700 | |

Fidelity Concord Street Trust — Fidelity® 500 Index Fund, Institutional Premium Shares | | | | | | | | | | | 162,112 | | | | 25,128,975 | |

Legg Mason Partners Variable Equity Trust — ClearBridge Variable Appreciation Portfolio, Class I Shares | | | | | | | | | | | 241,272 | | | | 13,614,970 | (a) |

MainStay VP Funds Trust: | | | | | | | | | | | | | | | | |

MainStay VP Epoch U.S. Equity Yield Portfolio, Initial Class | | | | | | | | | | | 485,796 | | | | 8,374,982 | |

MainStay VP Fidelity Institutional AM® Utilities Portfolio, Initial Class | | | | | | | | | | | 935,702 | | | | 11,938,530 | (b) |

MainStay VP Small Cap Growth Portfolio, Initial Class | | | | | | | | | | | 517,825 | | | | 5,412,929 | |

MainStay VP Wellington U.S. Equity Portfolio, Initial Class | | | | | | | | | | | 352,461 | | | | 8,638,010 | |

MFS Variable Insurance Portfolios: | | | | | | | | | | | | | | | | |

MFS® Investors Trust Series, Initial Class | | | | | | | | | | | 266,882 | | | | 9,591,745 | |

MFS® Research Series, Initial Class | | | | | | | | | | | 276,548 | | | | 8,667,020 | |

Variable Insurance Products Fund — VIP Equity-Income Portfolio, Initial Class | | | | | | | | | | | 380,286 | | | | 9,309,400 | |

Total Domestic Equity | | | | | | | | | | | | | | | 114,595,972 | |

| Foreign Equity — 8.6% | | | | | | | | | | | | | | | | |

Fidelity Concord Street Trust — Fidelity® International Index Fund, Institutional Premium Shares | | | | | | | | | | | 417,551 | | | | 19,274,168 | |

Invesco Variable Insurance Funds — Invesco V.I. International Growth Fund, Class I Shares | | | | | | | | | | | 253,909 | | | | 8,325,666 | |

Variable Insurance Products Fund — VIP Emerging Markets Portfolio, Initial Class | | | | | | | | | | | 800,000 | | | | 8,336,000 | |

Total Foreign Equity | | | | | | | | 35,935,834 | |

| Foreign Fixed Income — 7.9% | | | | | | | | | | | | | | | | |

Columbia Funds Variable Series Trust II — Columbia Variable Portfolio — Emerging Markets Bond Fund, Class 1 | | | | | | | | | | | 1,090,194 | | | | 8,241,864 | |