UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-21148

Eaton Vance New York Municipal Bond Fund

(Exact Name of Registrant as Specified in Charter)

Two International Place, Boston, Massachusetts 02110

(Address of Principal Executive Offices)

Maureen A. Gemma

Two International Place, Boston, Massachusetts 02110

(Name and Address of Agent for Services)

(617) 482-8260

(Registrant’s Telephone Number)

September 30

Date of Fiscal Year End

September 30, 2017

Date of Reporting Period

Item 1. Reports to Stockholders

Eaton Vance

Municipal Bond Funds

Annual Report

September 30, 2017

Municipal (EIM) • California (EVM) • New York (ENX)

Commodity Futures Trading Commission Registration. Effective December 31, 2012, the Commodity Futures Trading Commission (“CFTC”) adopted certain regulatory changes that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. Each Fund has claimed an exclusion from the definition of the term “commodity pool operator” under the Commodity Exchange Act. Accordingly, neither the Funds nor the adviser with respect to the operation of the Funds is subject to CFTC regulation. Because of its management of other strategies, each Fund’s adviser is registered with the CFTC as a commodity pool operator and a commodity trading advisor.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

Annual Report September 30, 2017

Eaton Vance

Municipal Bond Funds

Table of Contents

| | | | |

Management’s Discussion of Fund Performance | | | 2 | |

| |

Performance and Fund Profile | | | | |

| |

| | | | |

Municipal Bond Fund | | | 4 | |

California Municipal Bond Fund | | | 5 | |

New York Municipal Bond Fund | | | 6 | |

| |

| | | | |

| |

Endnotes and Additional Disclosures | | | 7 | |

| |

Financial Statements | | | 8 | |

| |

Report of Independent Registered Public Accounting Firm | | | 36 | |

| |

Federal Tax Information | | | 37 | |

| |

Annual Meeting of Shareholders | | | 38 | |

| |

Dividend Reinvestment Plan | | | 39 | |

| |

Board of Trustees’ Contract Approval | | | 41 | |

| |

Management and Organization | | | 45 | |

| |

Important Notices | | | 48 | |

Eaton Vance

Municipal Bond Funds

September 30, 2017

Management’s Discussion of Fund Performance1

Economic and Market Conditions

The fiscal year that began on October 1, 2016 played out as a tale of two markets. For the first two months of the period, interest rates rose and municipal bond prices declined. But from December 2016 until nearly the end of the period on September 30, 2017, longer-term rates generally fell and municipals gained back some, but not all, of their previous losses.

As the period opened, municipal bonds had just come off of a rally fueled by mixed U.S. economic reports, ongoing Federal Reserve Board (the Fed) caution, and the United Kingdom’s June 2016 vote to leave the European Union. In early fall 2016, the rally had ended when remarks by the European Central Bank, the Bank of Japan and the Fed seemed to indicate that rates might begin to rise sooner than markets had anticipated. As a result, municipal rates crept upward in October of 2016.

In November 2016, Donald Trump’s surprise win in the U.S. presidential election precipitated one of the largest municipal market declines in at least two decades. Rates rose, the yield curve steepened and bond prices fell as markets anticipated that decreasing regulation and lower tax rates under a Trump administration could lead to higher economic growth and inflation.

In December 2016, however, interest rates began to reverse direction, despite a Fed rate hike that month and two subsequent hikes in 2017 that put upward pressure on short-term rates. Mixed U.S. economic data, along with loss of confidence that the Trump administration could accomplish health care or tax reform, put downward pressure on long-term rates that would increase as the period wore on. As a result, municipal bonds rallied modestly in December and continued to stabilize during January and February 2017. From March through July, long-term rates drifted downward and the yield curve flattened. In August and early September, increasing geopolitical tension between the U.S. and North Korea led to a “flight to quality” that drove investors toward the perceived safety of U.S. Treasurys. As a result, rates declined further as Treasury prices rallied, and the municipal market rallied along with Treasurys. But in the final weeks of the period, the rally ended as rates rose in response to Republican legislators’ release of their outline for tax reform, which was viewed as a potential driver of higher U.S. economic growth and inflation.

For the 12-month period, municipal market returns were relatively flat. The Bloomberg Barclays Municipal Bond Index,2 a broad measure of the asset class, returned 0.87%, as total return generated from coupon payments was largely canceled out by price declines early in the fiscal year.

For the one-year period as a whole, rates rose throughout the yield curve for municipal AAA-rated7 issues. The greatest increases occurred at the long end of the curve, causing the curve to steepen for the one year period and longer-term bonds to underperform shorter-term issues. Across the curve, municipal bonds with maturities of 10 years and less outperformed comparable U.S. Treasurys, while 30-year municipals performed in line with 30-year Treasurys.

Fund Performance

For the fiscal year ended September 30, 2017, Municipal Bond Fund, California Municipal Bond Fund and New York Municipal Bond Fund shares at net asset value (NAV) underperformed the 0.59% return of the Funds’ benchmark, the Bloomberg Barclays Long (22+) Year Municipal Bond Index (the Index).

The Funds’ overall strategy is to invest primarily in higher quality bonds (rated A or higher). In managing the Funds, management employs leverage through Residual Interest Bond (RIB) financing6 to seek to enhance the Funds’ tax-exempt income. The use of leverage has the effect of achieving additional exposure to the municipal market, and thus magnifying a fund’s exposure to its underlying investments in both up and down market environments. During this period of relatively flat performance by municipal bonds, the additional income generated by the use of leverage was a modest contributor to performance versus the Index — which does not employ leverage — for all three funds.

Management hedges to various degrees against the greater potential risk of volatility caused by the use of leverage and investing in bonds at the long end of the yield curve by using Treasury futures and/or interest-rate swaps. As a risk management tactic within the Funds’ overall strategy, interest rate hedging is intended to moderate performance on both the upside and the downside of the market. So in a period when municipal and Treasury bonds generally declined in price, the hedging strategy mitigated a portion of that decline — and was thus a contributor to relative performance versus the unhedged Index — for all three funds.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested and include management fees and other expenses. Fund performance at market price will differ from its results at NAV due to factors such as changing perceptions about the Fund, market conditions, fluctuations in supply and demand for Fund shares, or changes in Fund distributions. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Municipal Bond Funds

September 30, 2017

Management’s Discussion of Fund Performance — continued

Fund Specific Results

Eaton Vance Municipal Bond Fund shares at NAV returned -0.19% during the fiscal year ended September 30, 2017, underperforming the 0.59% return of the Index. The main detractors from performance versus the Index included security selection in local general obligation (GO) bonds, security selection in 3.00% to 4.50% coupon bonds, and security selection in long-maturity bonds with 22 years or more remaining to maturity. The chief contributors to performance relative to the Index were the Fund’s hedging strategy; security selection in zero-coupon bonds, which were the worst-performing coupon structure in the Index during the period; and bonds in the Fund’s portfolio that were prerefunded, or escrowed, during the period.

Eaton Vance California Municipal Bond Fund shares at NAV returned 0.27% during the fiscal year ended September 30, 2017, underperforming the 0.59% return of the Index. Security selection in the water and sewer sector; an underweight, relative to the Index, in A-rated bonds; an underweight in BBB-rated bonds, which were the best-performing ratings category in the Index during the period; and security selection in local GO bonds all detracted from performance versus the Index. In contrast, the Fund’s hedging strategy contributed to performance relative to the Index, as did security selection in zero-coupon bonds and holdings that were prerefunded during the period.

Eaton Vance New York Municipal Bond Fund shares at NAV returned 0.02% during the fiscal year ended September 30, 2017, underperforming the 0.59% return of the Index. Key detractors from performance versus the Index included security selection in AAA-rated bonds, security selection and an overweight in bonds with 22 years or more remaining to maturity, and security selection in the transportation sector. Primary contributors to performance relative to the Index included the Fund’s hedging strategy, security selection in zero-coupon bonds, and an overweight in the industrial development revenue (IDR) sector, which was the best-performing sector in the Index during the period.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested and include management fees and other expenses. Fund performance at market price will differ from its results at NAV due to factors such as changing perceptions about the Fund, market conditions, fluctuations in supply and demand for Fund shares, or changes in Fund distributions. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Municipal Bond Fund

September 30, 2017

Performance2,3

Portfolio Manager Cynthia J. Clemson

| | | | | | | | | | | | | | | | |

| % Average Annual Total Returns | | Inception Date | | | One Year | | | Five Years | | | Ten Years | |

Fund at NAV | | | 08/30/2002 | | | | –0.19 | % | | | 5.38 | % | | | 5.67 | % |

Fund at Market Price | | | — | | | | –2.08 | | | | 3.18 | | | | 4.68 | |

Bloomberg Barclays Long (22+) Year Municipal Bond Index | | | — | | | | 0.59 | % | | | 4.12 | % | | | 5.16 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| % Premium/Discount to NAV4 | | | | | | | | | | | | |

| | | | | | | | | | | | | | | –7.71 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| Distributions5 | | | | | | | | | | | | |

Total Distributions per share for the period | | | | | | | | | | | | | | $ | 0.641 | |

Distribution Rate at NAV | | | | | | | | | | | | | | | 4.55 | % |

Taxable-Equivalent Distribution Rate at NAV | | | | | | | | | | | | | | | 8.04 | % |

Distribution Rate at Market Price | | | | | | | | | | | | | | | 4.93 | % |

Taxable-Equivalent Distribution Rate at Market Price | | | | | | | | | | | | | | | 8.71 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| % Total Leverage6 | | | | | | | | | | | | |

Residual Interest Bond (RIB) Financing | | | | | | | | | | | | | | | 39.09 | % |

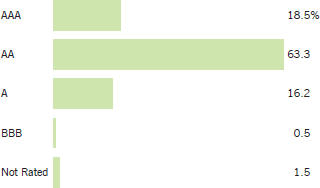

Fund Profile

Credit Quality (% of total investments)7, 8

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested and include management fees and other expenses. Fund performance at market price will differ from its results at NAV due to factors such as changing perceptions about the Fund, market conditions, fluctuations in supply and demand for Fund shares, or changes in Fund distributions. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

California Municipal Bond Fund

September 30, 2017

Performance2,3

Portfolio Manager Craig R. Brandon, CFA

| | | | | | | | | | | | | | | | |

| % Average Annual Total Returns | | Inception Date | | | One Year | | | Five Years | | | Ten Years | |

Fund at NAV | | | 08/30/2002 | | | | 0.27 | % | | | 4.82 | % | | | 4.49 | % |

Fund at Market Price | | | — | | | | –6.67 | | | | 4.65 | | | | 4.34 | |

Bloomberg Barclays Long (22+) Year Municipal Bond Index | | | — | | | | 0.59 | % | | | 4.12 | % | | | 5.16 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| % Premium/Discount to NAV4 | | | | | | | | | | | | |

| | | | | | | | | | | | | | | –3.29 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| Distributions5 | | | | | | | | | | | | |

Total Distributions per share for the period | | | | | | | | | | | | | | $ | 0.584 | |

Distribution Rate at NAV | | | | | | | | | | | | | | | 4.69 | % |

Taxable-Equivalent Distribution Rate at NAV | | | | | | | | | | | | | | | 9.56 | % |

Distribution Rate at Market Price | | | | | | | | | | | | | | | 4.85 | % |

Taxable-Equivalent Distribution Rate at Market Price | | | | | | | | | | | | | | | 9.88 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| % Total Leverage6 | | | | | | | | | | | | |

RIB Financing | | | | | | | | | | | | | | | 41.96 | % |

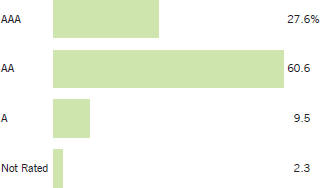

Fund Profile

Credit Quality (% of total investments)7, 8

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested and include management fees and other expenses. Fund performance at market price will differ from its results at NAV due to factors such as changing perceptions about the Fund, market conditions, fluctuations in supply and demand for Fund shares, or changes in Fund distributions. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

New York Municipal Bond Fund

September 30, 2017

Performance2,3

Portfolio Manager Craig R. Brandon, CFA

| | | | | | | | | | | | | | | | |

| % Average Annual Total Returns | | Inception Date | | | One Year | | | Five Years | | | Ten Years | |

Fund at NAV | | | 08/30/2002 | | | | 0.02 | % | | | 4.22 | % | | | 4.93 | % |

Fund at Market Price | | | — | | | | –5.18 | | | | 2.88 | | | | 4.61 | |

Bloomberg Barclays Long (22+) Year Municipal Bond Index | | | — | | | | 0.59 | % | | | 4.12 | % | | | 5.16 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| % Premium/Discount to NAV4 | | | | | | | | | | | | |

| | | | | | | | | | | | | | | –5.00 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| Distributions5 | | | | | | | | | | | | |

Total Distributions per share for the period | | | | | | | | | | | | | | $ | 0.618 | |

Distribution Rate at NAV | | | | | | | | | | | | | | | 4.54 | % |

Taxable-Equivalent Distribution Rate at NAV | | | | | | | | | | | | | | | 8.80 | % |

Distribution Rate at Market Price | | | | | | | | | | | | | | | 4.78 | % |

Taxable-Equivalent Distribution Rate at Market Price | | | | | | | | | | | | | | | 9.26 | % |

| | | | |

| | | | | | | | | | | | | | | | |

| % Total Leverage6 | | | | | | | | | | | | |

RIB Financing | | | | | | | | | | | | | | | 40.53 | % |

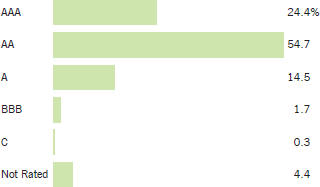

Fund Profile

Credit Quality (% of total investments)7, 8

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested and include management fees and other expenses. Fund performance at market price will differ from its results at NAV due to factors such as changing perceptions about the Fund, market conditions, fluctuations in supply and demand for Fund shares, or changes in Fund distributions. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Municipal Bond Funds

September 30, 2017

Endnotes and Additional Disclosures

| 1 | The views expressed in this report are those of the portfolio manager(s) and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance and the Fund(s) disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This commentary may contain statements that are not historical facts, referred to as “forward looking statements”. The Fund’s actual future results may differ significantly from those stated in any forward looking statement, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission. |

| 2 | Bloomberg Barclays Municipal Bond Index is an unmanaged index of municipal bonds traded in the U.S. Bloomberg Barclays Long (22+) Year Municipal Bond Index is an unmanaged index of municipal bonds traded in the U.S. with maturities of 22 years or more. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 3 | Performance results reflect the effects of leverage. Performance since inception for an index, if presented, is the performance since the Fund’s or oldest share class’ inception, as applicable. |

| 4 | The shares of the Fund often trade at a discount or premium from their net asset value. The discount or premium of the Fund may vary over time and may be higher or lower than what is quoted in this report. For up-to-date premium/discount information, please refer to http://eatonvance.com/closedend. |

| 5 | The Distribution Rate is based on the Fund’s last regular distribution per share in the period (annualized) divided by the Fund’s NAV or market price at the end of the period. The Fund’s distributions may be comprised of amounts characterized for federal income tax purposes as tax-exempt income, qualified and non-qualified ordinary dividends, capital gains and nondividend distributions, also known as return of capital. The Fund will determine the federal income tax character of distributions paid to a shareholder after the end of the calendar year. This is reported on the IRS form 1099-DIV and provided to the shareholder shortly after each year-end. For information about the tax character of distributions made in prior calendar years, please refer to Performance-Tax Character of Distributions on the Fund’s webpage available at eatonvance.com. |

| | The Fund’s distributions are determined by the investment adviser based on its current assessment of the Fund’s long-term return potential. Fund distributions may be affected by numerous factors including changes in Fund performance, the cost of financing for Funds that employ leverage, portfolio holdings, realized and projected returns, and other factors. As portfolio and market conditions change, the rate of distributions paid by the Fund could change. Taxable-equivalent performance is based on the highest combined federal and state income tax rates, where applicable. Lower tax rates would result in lower tax-equivalent performance. Actual tax rates will vary depending on your income, exemptions and deductions. Rates do not include local taxes. |

| 6 | Fund employs RIB financing. The leverage created by RIB investments provides an opportunity for increased income but, at the same time, creates special risks (including the likelihood of greater price volatility). The cost of leverage rises and falls with changes in short-term interest rates. See “Floating Rate Notes Issued in Conjunction with Securities Held” in the notes to the financial statements for more information about RIB financing. RIB leverage represents the amount of Floating Rate Notes outstanding at period end as a percentage of Fund net assets plus Floating Rate Notes. |

| 7 | Ratings are based on Moody’s, S&P or Fitch, as applicable. If securities are rated differently by the ratings agencies, the higher rating is applied. Ratings, which are subject to change, apply to the creditworthiness of the issuers of the underlying securities and not to the Fund or its shares. Credit ratings measure the quality of a bond based on the issuer’s creditworthiness, with ratings ranging from AAA, being the highest, to D, being the lowest based on S&P’s measures. Ratings of BBB or higher by S&P or Fitch (Baa or higher by Moody’s) are considered to be investment-grade quality. Credit ratings are based largely on the ratings agency’s analysis at the time of rating. The rating assigned to any particular security is not necessarily a reflection of the issuer’s current financial condition and does not necessarily reflect its assessment of the volatility of a security’s market value or of the liquidity of an investment in the security. Holdings designated as “Not Rated” are not rated by the national ratings agencies stated above. |

| 8 | The chart includes the municipal bonds held by a trust that issues residual interest bonds, consistent with the Portfolio of Investments. |

| | Fund profile subject to change due to active management. |

Important Notice to Shareholders

| | Effective September 30, 2017, the Funds’ benchmark was changed to the Bloomberg Barclays Municipal Bond Index. |

Eaton Vance

Municipal Bond Fund

September 30, 2017

Portfolio of Investments

| | | | | | | | |

| Tax-Exempt Investments — 162.6% | |

| | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Education — 12.2% | |

Connecticut Health and Educational Facilities Authority, (Fairfield University), 5.00%, 7/1/46 | | $ | 3,250 | | | $ | 3,645,980 | |

Houston Higher Education Finance Corp., TX, (St. John’s School), 5.25%, 9/1/33 | | | 3,985 | | | | 4,411,594 | |

Houston Higher Education Finance Corp., TX, (William Marsh Rice University), 5.00%, 5/15/35(1) | | | 15,000 | | | | 16,401,600 | |

Massachusetts Health and Educational Facilities Authority, (Boston College), 5.50%, 6/1/27 | | | 5,710 | | | | 7,336,836 | |

Massachusetts Health and Educational Facilities Authority, (Boston College), 5.50%, 6/1/30 | | | 8,325 | | | | 10,786,286 | |

New York Dormitory Authority, (Rockefeller University), 5.00%, 7/1/40(1) | | | 15,300 | | | | 16,294,347 | |

North Carolina Capital Facilities Finance Agency, (Duke University), 5.00%, 10/1/41(1) | | | 10,000 | | | | 11,591,300 | |

University of California, Prerefunded to 5/15/19, 5.25%, 5/15/39 | | | 720 | | | | 770,494 | |

University of California, Prerefunded to 5/15/19, 5.25%, 5/15/39 | | | 2,460 | | | | 2,632,520 | |

University of Cincinnati, OH, 5.00%, 6/1/45(1) | | | 6,000 | | | | 6,902,820 | |

University of Massachusetts Building Authority, 5.00%, 11/1/39(1) | | | 14,175 | | | | 16,153,688 | |

University of Michigan, 5.00%, 4/1/40(1) | | | 15,000 | | | | 17,506,950 | |

| | | | | | | | | |

| | | $ | 114,434,415 | |

| | | | | | | | | |

|

Electric Utilities — 3.0% | |

Energy Northwest, WA, (Columbia Generating Station), 5.00%, 7/1/40 | | $ | 2,320 | | | $ | 2,664,381 | |

Nebraska Public Power District, 5.00%, 1/1/34 | | | 5,000 | | | | 5,837,650 | |

Pima County Industrial Development Authority, AZ, (Tucson Electric Power Co.), 5.25%, 10/1/40 | | | 10,000 | | | | 10,726,300 | |

Unified Government of Wyandotte County/Kansas City Board of Public Utilities, KS, 5.00%, 9/1/36 | | | 3,425 | | | | 3,808,394 | |

Utility Debt Securitization Authority, NY, 5.00%, 12/15/35 | | | 4,500 | | | | 5,264,640 | |

| | | | | | | | | |

| | | $ | 28,301,365 | |

| | | | | | | | | |

|

Escrowed / Prerefunded — 18.9% | |

California Department of Water Resources, Prerefunded to 12/1/20, 5.25%, 12/1/35(1) | | $ | 9,715 | | | $ | 11,008,548 | |

California Educational Facilities Authority, (University of Southern California), Prerefunded to 10/1/18, 5.25%, 10/1/38(1) | | | 9,750 | | | | 10,180,170 | |

California Health Facilities Financing Authority, (Cedars-Sinai Medical Center), Prerefunded to 8/15/19, 5.00%, 8/15/39 | | | 11,570 | | | | 12,445,039 | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Escrowed / Prerefunded (continued) | |

Charleston, SC, Waterworks and Sewer Revenue, Prerefunded to 1/1/21, 5.00%, 1/1/35 | | $ | 2,735 | | | $ | 3,076,082 | |

Connecticut Health and Educational Facilities Authority, (Wesleyan University), Prerefunded to 7/1/20, 5.00%, 7/1/39(1) | | | 14,700 | | | | 16,260,111 | |

Honolulu City and County, HI, Wastewater System, Prerefunded to 7/1/21, 5.25%, 7/1/36(1) | | | 9,750 | | | | 11,199,532 | |

King County, WA, Sewer Revenue, Prerefunded to 1/1/21, 5.00%, 1/1/34(1) | | | 6,000 | | | | 6,731,880 | |

Marco Island, FL, Utility System, Prerefunded to 10/1/20, 5.00%, 10/1/34 | | | 1,445 | | | | 1,612,302 | |

Marco Island, FL, Utility System, Prerefunded to 10/1/20, 5.00%, 10/1/40 | | | 6,325 | | | | 7,057,309 | |

Maryland Health and Higher Educational Facilities Authority, (Charlestown Community, Inc.), Prerefunded to 1/1/21, 6.125%, 1/1/30 | | | 1,175 | | | | 1,359,193 | |

Mississippi, Prerefunded to 10/1/21, 5.00%, 10/1/30(1) | | | 10,000 | | | | 11,477,500 | |

Mississippi, Prerefunded to 10/1/21, 5.00%, 10/1/36(1) | | | 12,075 | | | | 13,859,081 | |

North Carolina Capital Facilities Finance Agency, (Duke University), Prerefunded to 4/1/19, 5.00%, 10/1/38(1) | | | 13,500 | | | | 14,308,110 | |

North Carolina, Limited Obligation Bonds, Prerefunded to 5/1/21, 5.00%, 5/1/30(1) | | | 10,000 | | | | 11,357,300 | |

Oregon, Prerefunded to 8/2/21, 5.00%, 8/1/36 | | | 1,140 | | | | 1,303,214 | |

Oregon State Department of Administrative Services, Lottery Revenue, Prerefunded to 4/1/21, 5.25%, 4/1/30 | | | 6,425 | | | | 7,329,961 | |

Pennsylvania Turnpike Commission, Prerefunded to 12/1/20, 6.00%, 12/1/34 | | | 720 | | | | 830,203 | |

Pennsylvania Turnpike Commission, Prerefunded to 12/1/20, 6.00%, 12/1/34 | | | 760 | | | | 876,326 | |

Pennsylvania Turnpike Commission, Prerefunded to 12/1/20, 6.00%, 12/1/34 | | | 3,520 | | | | 4,055,216 | |

South Carolina Public Service Authority, Prerefunded to 1/1/19, 5.50%, 1/1/38 | | | 565 | | | | 597,369 | |

Tarrant County Cultural Education Facilities Finance Corp., TX, (Scott & White Healthcare), Prerefunded to 8/15/20, 5.25%, 8/15/40 | | | 450 | | | | 502,853 | |

Tarrant County Cultural Education Facilities Finance Corp., TX, (Scott & White Healthcare), Prerefunded to 8/15/20, 5.25%, 8/15/40 | | | 5,655 | | | | 6,319,180 | |

Tennessee School Bond Authority, Prerefunded to 5/1/18, 5.50%, 5/1/38 | | | 5,000 | | | | 5,135,850 | |

Triborough Bridge and Tunnel Authority, NY, Prerefunded to 5/15/18, 5.00%, 11/15/33 | | | 5,000 | | | | 5,129,850 | |

University of California, Prerefunded to 5/15/19, 5.25%, 5/15/39 | | | 1,270 | | | | 1,359,065 | |

| | | | |

| | 8 | | See Notes to Financial Statements. |

Eaton Vance

Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Escrowed / Prerefunded (continued) | |

University of Colorado, (University Enterprise Revenue), Prerefunded to 6/1/21, 5.25%, 6/1/36(1) | | $ | 10,000 | | | $ | 11,458,300 | |

| | | | | | | | | |

| | | $ | 176,829,544 | |

| | | | | | | | | |

|

General Obligations — 13.8% | |

California, 5.00%, 10/1/33(1) | | $ | 18,800 | | | $ | 22,267,284 | |

California, 5.00%, 8/1/46(1) | | | 15,000 | | | | 17,376,600 | |

Chicago Park District, IL, (Harbor Facilities), 5.25%, 1/1/37(1) | | | 8,320 | | | | 8,939,174 | |

Delaware Valley Regional Finance Authority, PA, 5.75%, 7/1/32 | | | 3,000 | | | | 3,828,630 | |

Klein Independent School District, TX, (PSF Guaranteed), 5.00%, 2/1/36(1) | | | 2,000 | | | | 2,226,500 | |

New York, NY, 5.00%, 10/1/32 | | | 10,000 | | | | 11,611,000 | |

Ocean City, NJ, 1.00%, 11/15/28 | | | 2,500 | | | | 2,076,325 | |

Oregon, 5.00%, 8/1/35(1) | | | 6,750 | | | | 7,658,213 | |

Oregon, 5.00%, 8/1/36 | | | 860 | | | | 972,952 | |

Port of Houston Authority of Harris County, TX, 5.00%, 10/1/35 | | | 7,500 | | | | 8,309,475 | |

Tacoma School District No. 10, WA, 5.00%, 12/1/39(1) | | | 10,000 | | | | 11,620,500 | |

Washington, 4.00%, 7/1/28(1) | | | 10,000 | | | | 10,909,900 | |

Washington, 5.00%, 2/1/35(1) | | | 18,250 | | | | 21,269,280 | |

| | | | | | | | | |

| | | $ | 129,065,833 | |

| | | | | | | | | |

|

Hospital — 9.6% | |

California Health Facilities Financing Authority, (Catholic Healthcare West), 5.25%, 3/1/27 | | $ | 1,000 | | | $ | 1,125,530 | |

California Health Facilities Financing Authority, (Catholic Healthcare West), 5.25%, 3/1/28 | | | 1,770 | | | | 1,970,523 | |

Hawaii Department of Budget and Finance, (Hawaii Pacific Health), 5.50%, 7/1/38 | | | 2,790 | | | | 3,171,839 | |

Massachusetts Development Finance Agency, (Partners HealthCare System), 5.00%, 7/1/41(1) | | | 10,000 | | | | 11,380,900 | |

New Jersey Health Care Facilities Financing Authority, (Robert Wood Johnson University Hospital), 5.25%, 7/1/35 | | | 4,385 | | | | 5,009,819 | |

Ohio Higher Educational Facility Commission, (Cleveland Clinic Health System), 5.00%, 1/1/32 | | | 10,950 | | | | 12,422,228 | |

Tampa, FL, (BayCare Health System), 5.00%, 11/15/46(1) | | | 12,000 | | | | 13,549,200 | |

Vermont Educational and Health Buildings Financing Agency, (University of Vermont Medical Center), 4.00%, 12/1/42 | | | 3,000 | | | | 3,093,120 | |

Vermont Educational and Health Buildings Financing Agency, (University of Vermont Medical Center), 5.00%, 12/1/33 | | | 1,600 | | | | 1,821,728 | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Hospital (continued) | |

West Virginia Hospital Finance Authority, (West Virginia United Health System Obligated Group), 5.375%, 6/1/38 | | $ | 7,605 | | | $ | 8,552,963 | |

Wisconsin Health and Educational Facilities Authority, (Ascension Health Alliance Senior Credit Group), 5.00%, 11/15/41(1) | | | 11,500 | | | | 12,658,510 | |

Wisconsin Health and Educational Facilities Authority, (Ascension Senior Credit Group), 4.50%, 11/15/39 | | | 14,180 | | | | 15,492,643 | |

| | | | | | | | | |

| | | $ | 90,249,003 | |

| | | | | | | | | |

|

Industrial Development Revenue — 0.5% | |

Maricopa County Pollution Control Corp., AZ, (El Paso Electric Co.), 4.50%, 8/1/42 | | $ | 4,245 | | | $ | 4,386,401 | |

| | | | | | | | | |

| | | $ | 4,386,401 | |

| | | | | | | | | |

|

Insured – Education — 2.2% | |

Massachusetts Development Finance Agency, (College of the Holy Cross), (AMBAC), 5.25%, 9/1/32 | | $ | 15,900 | | | $ | 20,288,241 | |

| | | | | | | | | |

| | | $ | 20,288,241 | |

| | | | | | | | | |

|

Insured – Electric Utilities — 0.6% | |

Louisiana Energy and Power Authority, (AGM), 5.25%, 6/1/38 | | $ | 4,905 | | | $ | 5,619,610 | |

| | | | | | | | | |

| | | $ | 5,619,610 | |

| | | | | | | | | |

|

Insured – Escrowed / Prerefunded — 16.2% | |

American Municipal Power-Ohio, Inc., OH, (Prairie State Energy Campus), (AGC), Prerefunded to 2/15/19, 5.75%, 2/15/39 | | $ | 5,000 | | | $ | 5,326,950 | |

Arizona Health Facilities Authority, (Banner Health), (BHAC), Prerefunded to 1/1/18, 5.375%, 1/1/32 | | | 8,250 | | | | 8,345,370 | |

Bossier City, LA, Utilities Revenue, (BHAC), Prerefunded to 10/1/18, 5.25%, 10/1/26 | | | 3,185 | | | | 3,321,891 | |

Bossier City, LA, Utilities Revenue, (BHAC), Prerefunded to 10/1/18, 5.25%, 10/1/27 | | | 1,985 | | | | 2,070,315 | |

Bossier City, LA, Utilities Revenue, (BHAC), Prerefunded to 10/1/18, 5.50%, 10/1/38 | | | 3,170 | | | | 3,314,172 | |

California Statewide Communities Development Authority, (Sutter Health), (AGM), Prerefunded to 8/15/18, 5.05%, 8/15/38(1) | | | 11,000 | | | | 11,407,990 | |

Chicago, IL, (O’Hare International Airport), (AGM), Prerefunded to 1/1/18, 4.75%, 1/1/34(1) | | | 21,640 | | | | 21,853,586 | |

Chicago, IL, Wastewater Transmission Revenue, (BHAC), Prerefunded to 1/1/18, 5.50%, 1/1/38 | | | 2,060 | | | | 2,084,143 | |

| | | | |

| | 9 | | See Notes to Financial Statements. |

Eaton Vance

Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Insured – Escrowed / Prerefunded (continued) | |

Colorado Health Facilities Authority, (Catholic Health), (AGM), Prerefunded to 4/29/18, 5.10%, 10/1/41(1) | | $ | 11,500 | | | $ | 11,782,095 | |

District of Columbia Water and Sewer Authority, (AGC), Prerefunded to 10/1/18, 5.00%, 10/1/34(1) | | | 8,500 | | | | 8,848,925 | |

Iowa Finance Authority, Health Facilities, (Iowa Health System), (AGC), Prerefunded to 8/15/19, 5.625%, 8/15/37 | | | 2,625 | | | | 2,849,621 | |

Kane, Cook and DuPage Counties School District No. 46, IL, (AMBAC), Escrowed to Maturity, 0.00%, 1/1/22 | | | 13,145 | | | | 12,241,676 | |

New Jersey Economic Development Authority, (School Facilities Construction), (AGC), Prerefunded to 12/15/18, 5.50%, 12/15/34 | | | 1,015 | | | | 1,071,343 | |

New Jersey Economic Development Authority, (School Facilities Construction), (AGC), Prerefunded to 12/15/18, 5.50%, 12/15/34 | | | 1,875 | | | | 1,980,488 | |

North Carolina Turnpike Authority, (Triangle Expressway System), (AGC), Prerefunded to 1/1/19, 5.50%, 1/1/29 | | | 1,015 | | | | 1,071,830 | |

North Carolina Turnpike Authority, (Triangle Expressway System), (AGC), Prerefunded to 1/1/19, 5.75%, 1/1/39 | | | 1,160 | | | | 1,228,556 | |

Paducah Electric Plant Board, KY, (AGC), Prerefunded to 4/1/19, 5.25%, 10/1/35 | | | 2,735 | | | | 2,906,977 | |

Palm Beach County Solid Waste Authority, FL, (BHAC), Prerefunded to 10/1/19, 5.00%, 10/1/24 | | | 1,985 | | | | 2,142,887 | |

Palm Beach County Solid Waste Authority, FL, (BHAC), Prerefunded to 10/1/19, 5.00%, 10/1/26 | | | 1,575 | | | | 1,700,591 | |

Palm Springs Unified School District, CA, (AGC), Prerefunded to 8/1/19, 5.00%, 8/1/32 | | | 8,955 | | | | 9,620,446 | |

San Diego County Water Authority, CA, Certificates of Participation, (AGM), Prerefunded to 5/1/18, 5.00%, 5/1/38(1) | | | 24,000 | | | | 24,592,320 | |

South Carolina Public Service Authority, (BHAC), Prerefunded to 1/1/19, 5.50%, 1/1/38 | | | 625 | | | | 660,806 | |

Texas Transportation Commission, (Central Texas Turnpike System), (AMBAC), Escrowed to Maturity, 0.00%, 8/15/20 | | | 5,570 | | | | 5,344,693 | |

Washington Health Care Facilities Authority, (MultiCare Health System), (AGC), Prerefunded to 8/15/19, 6.00%, 8/15/39 | | | 5,795 | | | | 6,324,373 | |

| | | | | | | | | |

| | | $ | 152,092,044 | |

| | | | | | | | | |

|

Insured – General Obligations — 6.9% | |

Chicago Park District, IL, (Limited Tax Park), (BAM), 5.00%, 1/1/39 | | $ | 35 | | | $ | 38,109 | |

Chicago Park District, IL, (Limited Tax Park), (BAM), 5.00%, 1/1/39(1) | | | 13,600 | | | | 14,808,224 | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Insured – General Obligations (continued) | |

Cincinnati City School District, OH, (AGM), (FGIC), 5.25%, 12/1/30 | | $ | 3,750 | | | $ | 4,796,288 | |

Clark County, NV, (AMBAC), 2.50%, 11/1/36 | | | 11,845 | | | | 10,387,354 | |

Frisco Independent School District, TX, (PSF Guaranteed), (AGM), 2.75%, 8/15/39 | | | 9,530 | | | | 8,787,899 | |

Kane, Cook and DuPage Counties School District No. 46, IL, (AMBAC), 0.00%, 1/1/22 | | | 16,605 | | | | 15,218,150 | |

Port Arthur Independent School District, TX, (AGC), Prerefunded to 2/15/18, 4.75%, 2/15/38(1) | | | 10,950 | | | | 11,109,980 | |

| | | | | | | | | |

| | | $ | 65,146,004 | |

| | | | | | | | | |

|

Insured – Hospital — 6.4% | |

Illinois Finance Authority, (Children’s Memorial Hospital), (AGC), 5.25%, 8/15/47(1) | | $ | 15,000 | | | $ | 15,461,400 | |

Maryland Health and Higher Educational Facilities Authority, (AGC), 4.75%, 7/1/47(1) | | | 8,635 | | | | 8,651,577 | |

New Jersey Health Care Facilities Financing Authority, (Virtua Health), (AGC), 5.50%, 7/1/38 | | | 13,115 | | | | 14,032,132 | |

Washington Health Care Facilities Authority, (Providence Health Care), Series C, (AGM), 5.25%, 10/1/33(1) | | | 8,700 | | | | 9,032,688 | |

Washington Health Care Facilities Authority, (Providence Health Care), Series D, (AGM), 5.25%, 10/1/33(1) | | | 12,605 | | | | 13,104,409 | |

| | | | | | | | | |

| | | $ | 60,282,206 | |

| | | | | | | | | |

|

Insured – Industrial Development Revenue — 1.0% | |

Pennsylvania Economic Development Financing Authority, (Aqua Pennsylvania, Inc.), (BHAC), 5.00%, 10/1/39(1) | | $ | 9,000 | | | $ | 9,611,280 | |

| | | | | | | | | |

| | | $ | 9,611,280 | |

| | | | | | | | | |

|

Insured – Other Revenue — 1.7% | |

Harris County-Houston Sports Authority, TX, (AGM), (NPFG), 0.00%, 11/15/34 | | $ | 16,795 | | | $ | 8,260,957 | |

New York City Industrial Development Agency, NY, (Yankee Stadium), (AGC), 7.00%, 3/1/49 | | | 6,750 | | | | 7,311,262 | |

| | | | | | | | | |

| | | $ | 15,572,219 | |

| | | | | | | | | |

|

Insured – Special Tax Revenue — 5.9% | |

Alabama Public School and College Authority, (AGM), 2.50%, 12/1/27 | | $ | 15,975 | | | $ | 15,979,633 | |

Houston, TX, Hotel Occupancy Tax, (AMBAC), 0.00%, 9/1/24 | | | 18,035 | | | | 15,067,882 | |

Miami-Dade County, FL, Professional Sports Franchise Facilities, (AGC), 7.00%, (0.00% until 10/1/19), 10/1/39 | | | 15,000 | | | | 18,093,450 | |

| | | | |

| | 10 | | See Notes to Financial Statements. |

Eaton Vance

Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Insured – Special Tax Revenue (continued) | |

Puerto Rico Sales Tax Financing Corp., (NPFG), 0.00%, 8/1/45 | | $ | 28,945 | | | $ | 6,088,870 | |

| | | | | | | | | |

| | | $ | 55,229,835 | |

| | | | | | | | | |

|

Insured – Student Loan — 0.5% | |

Maine Educational Loan Authority, (AGC), 5.625%, 12/1/27 | | $ | 4,465 | | | $ | 4,730,712 | |

| | | | | | | | | |

| | | $ | 4,730,712 | |

| | | | | | | | | |

|

Insured – Transportation — 10.7% | |

Chicago, IL, (O’Hare International Airport), (AGM), 5.00%, 1/1/28 | | $ | 2,500 | | | $ | 2,868,275 | |

Chicago, IL, (O’Hare International Airport), (AGM), 5.00%, 1/1/29 | | | 1,000 | | | | 1,146,240 | |

Chicago, IL, (O’Hare International Airport), (AGM), 5.125%, 1/1/30 | | | 1,800 | | | | 2,042,190 | |

Chicago, IL, (O’Hare International Airport), (AGM), 5.125%, 1/1/31 | | | 1,570 | | | | 1,775,858 | |

Chicago, IL, (O’Hare International Airport), (AGM), 5.25%, 1/1/32 | | | 1,015 | | | | 1,152,167 | |

Chicago, IL, (O’Hare International Airport), (AGM), 5.25%, 1/1/33 | | | 1,150 | | | | 1,301,167 | |

Clark County, NV, (Las Vegas-McCarran International Airport), (AGM), 5.25%, 7/1/39 | | | 8,080 | | | | 8,756,862 | |

E-470 Public Highway Authority, CO, (NPFG), 0.00%, 9/1/21 | | | 10,200 | | | | 9,532,206 | |

E-470 Public Highway Authority, CO, (NPFG), 0.00%, 9/1/39 | | | 25,000 | | | | 9,226,750 | |

Harris County, TX, Toll Road Revenue, (BHAC), (NPFG), 5.00%, 8/15/33(1) | | | 7,800 | | | | 7,825,428 | |

Manchester, NH, (Manchester-Boston Regional Airport), (AGM), 5.125%, 1/1/30 | | | 6,710 | | | | 6,909,690 | |

Metropolitan Washington Airports Authority, D.C., (BHAC), 5.00%, 10/1/29 | | | 1,785 | | | | 1,916,519 | |

New Jersey Transportation Trust Fund Authority, (AGC), 5.50%, 12/15/38 | | | 11,700 | | | | 12,180,402 | |

Port Palm Beach District, FL, (XLCA), 0.00%, 9/1/24 | | | 1,605 | | | | 1,170,735 | |

Port Palm Beach District, FL, (XLCA), 0.00%, 9/1/25 | | | 1,950 | | | | 1,351,662 | |

Port Palm Beach District, FL, (XLCA), 0.00%, 9/1/26 | | | 1,000 | | | | 660,680 | |

San Joaquin Hills Transportation Corridor Agency, CA, (Toll Road Bonds), (NPFG), 0.00%, 1/15/25 | | | 26,215 | | | | 20,978,816 | |

Texas Transportation Commission, (Central Texas Turnpike System), (AMBAC), 0.00%, 8/15/20 | | | 10,275 | | | | 9,827,832 | |

| | | | | | | | | |

| | | $ | 100,623,479 | |

| | | | | | | | | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Insured – Water and Sewer — 5.1% | |

Chicago, IL, Wastewater Transmission Revenue, (NPFG), 0.00%, 1/1/23 | | $ | 13,670 | | | $ | 11,817,578 | |

DeKalb County, GA, Water and Sewerage Revenue, (AGM), 5.25%, 10/1/32(1) | | | 10,000 | | | | 12,304,900 | |

Massachusetts Water Resources Authority, (AGM), 5.25%, 8/1/32 | | | 5,540 | | | | 7,273,521 | |

Massachusetts Water Resources Authority, (AGM), 5.25%, 8/1/38 | | | 1,070 | | | | 1,425,090 | |

Michigan Finance Authority, (Detroit Water and Sewerage Department), (AGM), 5.00%, 7/1/32 | | | 2,615 | | | | 2,970,195 | |

Michigan Finance Authority, (Detroit Water and Sewerage Department), (AGM), 5.00%, 7/1/33 | | | 2,240 | | | | 2,532,477 | |

Michigan Finance Authority, (Detroit Water and Sewerage Department), (AGM), 5.00%, 7/1/35 | | | 2,730 | | | | 3,070,404 | |

Michigan Finance Authority, (Detroit Water and Sewerage Department), (AGM), 5.00%, 7/1/37 | | | 2,240 | | | | 2,506,202 | |

San Luis Obispo County, CA, (Nacimiento Water Project), (NPFG), 4.50%, 9/1/40 | | | 3,535 | | | | 3,544,085 | |

| | | | | | | | | |

| | | $ | 47,444,452 | |

| | | | | | | | | |

|

Lease Revenue / Certificates of Participation — 2.3% | |

Hudson Yards Infrastructure Corp., NY, 5.75%, 2/15/47 | | $ | 790 | | | $ | 904,882 | |

Hudson Yards Infrastructure Corp., NY, Prerefunded to 2/15/21, 5.75%, 2/15/47 | | | 1,190 | | | | 1,370,618 | |

North Carolina, Limited Obligation Bonds, 5.00%, 5/1/26 | | | 10 | | | | 11,996 | |

North Carolina, Limited Obligation Bonds, 5.00%, 5/1/26(1) | | | 16,000 | | | | 19,193,440 | |

| | | | | | | | | |

| | | $ | 21,480,936 | |

| | | | | | | | | |

|

Other Revenue — 1.6% | |

New York City Transitional Finance Authority, NY, (Building Aid), 5.00%, 7/15/36(1) | | $ | 10,750 | | | $ | 12,017,102 | |

Oregon State Department of Administrative Services, Lottery Revenue, 5.25%, 4/1/30 | | | 1,275 | | | | 1,445,876 | |

Texas Municipal Gas Acquisition and Supply Corp. III, Gas Supply Revenue, 5.00%, 12/15/30 | | | 1,700 | | | | 1,897,574 | |

| | | | | | | | | |

| | | $ | 15,360,552 | |

| | | | | | | | | |

|

Special Tax Revenue — 16.2% | |

Central Puget Sound Regional Transit Authority, WA, Sales and Use Tax Revenue, 5.00%, 11/1/30(1) | | $ | 12,575 | | | $ | 15,206,948 | |

Central Puget Sound Regional Transit Authority, WA, Sales and Use Tax Revenue, 5.00%, 11/1/41(1) | | | 10,000 | | | | 11,667,000 | |

Connecticut, Special Tax Obligation, (Transportation Infrastructure), 5.00%, 1/1/31(1) | | | 20,000 | | | | 22,270,200 | |

| | | | |

| | 11 | | See Notes to Financial Statements. |

Eaton Vance

Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Special Tax Revenue (continued) | |

Los Angeles County Metropolitan Transportation Authority, CA, Sales Tax Revenue, 5.00%, 7/1/38 | | $ | 5,000 | | | $ | 5,961,400 | |

Massachusetts School Building Authority, Dedicated Sales Tax Revenue, 5.00%, 8/15/37(1) | | | 20,200 | | | | 23,538,858 | |

Metropolitan Transportation Authority, NY, Dedicated Tax Revenue, Green Bonds, 5.25%, 11/15/33 | | | 5,000 | | | | 6,193,100 | |

New York City Transitional Finance Authority, NY, Future Tax Revenue, 5.00%, 2/1/37(1) | | | 20,000 | | | | 22,552,200 | |

New York Convention Center Development Corp., Hotel Occupancy Tax, 5.00%, 11/15/45(1) | | | 13,000 | | | | 14,862,510 | |

New York Dormitory Authority, Personal Income Tax Revenue, 5.00%, 6/15/31 | | | 10,000 | | | | 11,720,500 | |

New York Dormitory Authority, Sales Tax Revenue, 5.00%, 3/15/34 | | | 3,285 | | | | 3,761,292 | |

New York Dormitory Authority, Sales Tax Revenue, 5.00%, 3/15/35 | | | 12,040 | | | | 13,712,476 | |

| | | | | | | | | |

| | | $ | 151,446,484 | |

| | | | | | | | | |

|

Transportation — 15.3% | |

Chicago, IL, (O’Hare International Airport), 5.00%, 1/1/36 | | $ | 6,000 | | | $ | 6,890,400 | |

Chicago, IL, (O’Hare International Airport), 5.00%, 1/1/38 | | | 2,105 | | | | 2,405,783 | |

Dallas and Fort Worth, TX, (Dallas/Fort Worth International Airport), 5.25%, 11/1/30 | | | 3,205 | | | | 3,802,957 | |

Dallas and Fort Worth, TX, (Dallas/Fort Worth International Airport), 5.25%, 11/1/31 | | | 4,950 | | | | 5,867,829 | |

Delaware River Port Authority of Pennsylvania and New Jersey, 5.00%, 1/1/35 | | | 8,275 | | | | 8,909,030 | |

Illinois Toll Highway Authority, 5.00%, 12/1/32(1) | | | 10,425 | | | | 12,104,572 | |

Illinois Toll Highway Authority, 5.00%, 1/1/37(1) | | | 10,000 | | | | 11,405,400 | |

Kansas Department of Transportation, 5.00%, 9/1/35(1) | | | 10,000 | | | | 11,778,600 | |

Los Angeles Department of Airports, CA, (Los Angeles International Airport), 5.25%, 5/15/28 | | | 3,285 | | | | 3,629,925 | |

Metropolitan Transportation Authority, NY, 5.25%, 11/15/32 | | | 4,380 | | | | 5,199,586 | |

Metropolitan Transportation Authority, NY, 5.25%, 11/15/38 | | | 4,640 | | | | 5,300,365 | |

Metropolitan Transportation Authority, NY, 5.25%, 11/15/40 | | | 4,735 | | | | 5,263,568 | |

Miami-Dade County, FL, (Miami International Airport), 5.00%, 10/1/41 | | | 10,825 | | | | 11,689,484 | |

Miami-Dade County, FL, Aviation Revenue, 5.00%, 10/1/37 | | | 4,615 | | | | 5,342,601 | |

New Jersey Transportation Trust Fund Authority, (Transportation System), 5.00%, 12/15/24 | | | 10,000 | | | | 11,312,800 | |

New Jersey Turnpike Authority, 5.00%, 1/1/34 | | | 3,200 | | | | 3,801,696 | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Transportation (continued) | |

Orlando-Orange County Expressway Authority, FL, 5.00%, 7/1/35 | | $ | 610 | | | $ | 666,370 | |

Orlando-Orange County Expressway Authority, FL, 5.00%, 7/1/40 | | | 1,580 | | | | 1,719,751 | |

Orlando-Orange County Expressway Authority, FL, Prerefunded to 7/1/20, 5.00%, 7/1/35 | | | 2,305 | | | | 2,546,979 | |

Orlando-Orange County Expressway Authority, FL, Prerefunded to 7/1/20, 5.00%, 7/1/40 | | | 1,010 | | | | 1,116,030 | |

Port Authority of New York and New Jersey, 5.00%, 12/1/34(1) | | | 14,360 | | | | 16,659,323 | |

Port Authority of New York and New Jersey, 5.00%, 7/15/39 | | | 5,000 | | | | 5,483,750 | |

| | | | | | | | | |

| | | $ | 142,896,799 | |

| | | | | | | | | |

|

Water and Sewer — 12.0% | |

Charleston, SC, Waterworks and Sewer Revenue, 5.00%, 1/1/45(1) | | $ | 25,000 | | | $ | 28,818,000 | |

Dallas, TX, Waterworks and Sewer System Revenue, 5.00%, 10/1/41 | | | 15,000 | | | | 17,455,050 | |

Detroit, MI, Sewage Disposal System, 5.00%, 7/1/32 | | | 1,070 | | | | 1,176,593 | |

Detroit, MI, Sewage Disposal System, 5.25%, 7/1/39 | | | 1,965 | | | | 2,170,500 | |

Detroit, MI, Water Supply System, 5.25%, 7/1/41 | | | 2,910 | | | | 3,153,713 | |

King County, WA, Sewer Revenue, 5.00%, 1/1/34(1) | | | 4,000 | | | | 4,439,080 | |

Metropolitan St. Louis Sewer District, MO, 5.00%, 5/1/35(1) | | | 8,750 | | | | 10,227,000 | |

Metropolitan St. Louis Sewer District, MO, 5.00%, 5/1/36(1) | | | 7,925 | | | | 9,244,909 | |

New York City Municipal Water Finance Authority, NY, 5.00%, 6/15/31 | | | 10,000 | | | | 11,497,500 | |

Portland, OR, Water System, 5.00%, 5/1/36 | | | 5,385 | | | | 5,978,642 | |

Texas Water Development Board, 5.00%, 10/15/40(1) | | | 15,500 | | | | 18,037,815 | |

| | | | | | | | | |

| | | $ | 112,198,802 | |

| | | | | | | | | |

| |

Total Tax-Exempt Investments — 162.6%

(identified cost $1,413,995,928) | | | $ | 1,523,290,216 | |

| | | | | | | | | |

| |

Other Assets, Less Liabilities — (62.6)% | | | $ | (586,638,141 | ) |

| | | | | | | | | |

| |

Net Assets — 100.0% | | | $ | 936,652,075 | |

| | | | | | | | | |

The percentage shown for each investment category in the Portfolio of Investments is based on net assets.

| | | | |

| | 12 | | See Notes to Financial Statements. |

Eaton Vance

Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

At September 30, 2017, the concentration of the Fund’s investments in the various states and territories, determined as a percentage of total investments, is as follows:

| | | | |

| New York | | | 11.9% | |

| California | | | 10.6% | |

| Others, representing less than 10% individually | | | 77.5% | |

The Fund invests primarily in debt securities issued by municipalities. The ability of the issuers of the debt securities to meet their obligations may be

affected by economic developments in a specific industry or municipality. In order to reduce the risk associated with such economic developments, at September 30, 2017, 35.2% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution or financial guaranty assurance agency ranged from 0.2% to 12.7% of total investments.

| (1) | Security represents the municipal bond held by a trust that issues residual interest bonds (see Note 1G). |

| | | | | | | | | | | | | | | | | | | | |

| Futures Contracts | |

| Description | | Number of

Contracts | | | Position | | | Expiration

Month/Year | | | Notional

Amount | | | Value/Net

Unrealized

Appreciation | |

| | | | | |

Interest Rate Futures | | | | | | | | | | | | | | | | | | | | |

| U.S. Long Treasury Bond | | | 229 | | | | Short | | | | Dec-17 | | | $ | (34,994,063 | ) | | $ | 573,858 | |

| | | | | |

| | | | | | | | | | | | | | | | | | | $ | 573,858 | |

Abbreviations:

| | | | |

| AGC | | – | | Assured Guaranty Corp. |

| AGM | | – | | Assured Guaranty Municipal Corp. |

| AMBAC | | – | | AMBAC Financial Group, Inc. |

| BAM | | – | | Build America Mutual Assurance Co. |

| BHAC | | – | | Berkshire Hathaway Assurance Corp. |

| | | | |

| FGIC | | – | | Financial Guaranty Insurance Company |

| NPFG | | – | | National Public Finance Guaranty Corp. |

| PSF | | – | | Permanent School Fund |

| XLCA | | – | | XL Capital Assurance, Inc. |

| | | | |

| | 13 | | See Notes to Financial Statements. |

Eaton Vance

California Municipal Bond Fund

September 30, 2017

Portfolio of Investments

| | | | | | | | |

| Tax-Exempt Investments — 170.6% | |

| | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Education — 12.6% | |

California Educational Facilities Authority, (Claremont McKenna College), 5.00%, 1/1/27 | | $ | 770 | | | $ | 777,723 | |

California Educational Facilities Authority, (Harvey Mudd College), 5.25%, 12/1/31 | | | 550 | | | | 635,954 | |

California Educational Facilities Authority, (Harvey Mudd College), 5.25%, 12/1/36 | | | 940 | | | | 1,073,762 | |

California Educational Facilities Authority, (Loyola Marymount University), 5.00%, 10/1/30 | | | 1,375 | | | | 1,470,081 | |

California Educational Facilities Authority, (Pepperdine University), 5.00%, 10/1/46(1) | | | 6,600 | | | | 7,686,756 | |

California Educational Facilities Authority, (University of San Francisco), 6.125%, 10/1/36 | | | 650 | | | | 774,969 | |

California Educational Facilities Authority, (University of the Pacific), 5.00%, 11/1/30 | | | 1,790 | | | | 2,012,282 | |

California Municipal Finance Authority, (University of San Diego), 5.00%, 10/1/31 | | | 1,175 | | | | 1,335,529 | |

California Municipal Finance Authority, (University of San Diego), 5.00%, 10/1/35 | | | 800 | | | | 906,288 | |

California Municipal Finance Authority, (University of San Diego), 5.25%, 10/1/26 | | | 2,270 | | | | 2,609,978 | |

California Municipal Finance Authority, (University of San Diego), 5.25%, 10/1/27 | | | 2,395 | | | | 2,749,652 | |

California Municipal Finance Authority, (University of San Diego), 5.25%, 10/1/28 | | | 2,520 | | | | 2,888,928 | |

California State University, 5.00%, 11/1/41(1) | | | 7,550 | | | | 8,785,029 | |

| | | | | | | | | |

| | | $ | 33,706,931 | |

| | | | | | | | | |

|

Electric Utilities — 1.2% | |

Southern California Public Power Authority, (Tieton Hydropower), 5.00%, 7/1/35 | | $ | 1,890 | | | $ | 2,068,945 | |

Vernon, Electric System Revenue, 5.125%, 8/1/21 | | | 1,165 | | | | 1,245,618 | |

| | | | | | | | | |

| | | $ | 3,314,563 | |

| | | | | | | | | |

|

Escrowed / Prerefunded — 15.4% | |

California Educational Facilities Authority, (California Institute of Technology), Prerefunded to 11/1/19, 5.00%, 11/1/39(1) | | $ | 10,000 | | | $ | 10,842,100 | |

California Educational Facilities Authority, (Claremont McKenna College), Prerefunded to 1/1/18, 5.00%, 1/1/27 | | | 1,910 | | | | 1,930,609 | |

California Educational Facilities Authority, (Santa Clara University), Prerefunded to 2/1/20, 5.00%, 2/1/29 | | | 285 | | | | 311,494 | |

California Educational Facilities Authority, (University of Southern California), Prerefunded to 10/1/18, 5.25%, 10/1/39 | | | 6,200 | | | | 6,473,544 | |

California Health Facilities Financing Authority, (Cedars-Sinai Medical Center), Prerefunded to 8/15/19, 5.00%, 8/15/39 | | | 4,505 | | | | 4,845,713 | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Escrowed / Prerefunded (continued) | |

Foothill-De Anza Community College District, Prerefunded to 8/1/21, 5.00%, 8/1/36(1) | | $ | 10,000 | | | $ | 11,476,100 | |

San Diego Community College District, (Election of 2002), Prerefunded to 8/1/21, 5.00%, 8/1/32 | | | 1,375 | | | | 1,577,964 | |

San Diego Community College District, (Election of 2006), Prerefunded to 8/1/21, 5.00%, 8/1/31 | | | 2,545 | | | | 2,920,667 | |

Vernon, Electric System Revenue, Prerefunded to 8/1/19, 5.125%, 8/1/21 | | | 500 | | | | 529,670 | |

| | | | | | | | | |

| | | $ | 40,907,861 | |

| | | | | | | | | |

|

General Obligations — 48.7% | |

Berryessa Union School District, (Election of 2014), 5.00%, 8/1/40(1) | | $ | 7,450 | | | $ | 8,701,749 | |

Burbank Unified School District, (Election of 2013), 4.00%, 8/1/31(1) | | | 6,900 | | | | 7,429,368 | |

California, 5.50%, 11/1/35 | | | 4,600 | | | | 5,200,438 | |

Castro Valley Unified School District, (Election of 2016), 5.00%, 8/1/41 | | | 2,500 | | | | 2,936,475 | |

Contra Costa Community College District, (Election of 2006), 5.00%, 8/1/38(1) | | | 9,750 | | | | 11,275,095 | |

Desert Community College District, 5.00%, 8/1/36(1) | | | 7,500 | | | | 8,792,250 | |

Mountain View Whisman School District, (Election of 2012), 4.00%, 9/1/42(1) | | | 10,000 | | | | 10,552,800 | |

Napa Valley Unified School District, 5.00%, 8/1/41 | | | 2,885 | | | | 3,388,692 | |

Palo Alto, (Election of 2008), 5.00%, 8/1/40(1) | | | 7,020 | | | | 7,721,158 | |

Palomar Community College District, 5.00%, 8/1/44(1) | | | 10,000 | | | | 11,538,400 | |

San Bernardino Community College District, 4.00%, 8/1/27(1) | | | 5,775 | | | | 6,414,292 | |

San Jose Unified School District, 5.00%, 8/1/32(1) | | | 7,500 | | | | 8,879,700 | |

San Jose-Evergreen Community College District, (Election of 2010), 5.00%, 8/1/37(1) | | | 4,975 | | | | 5,680,157 | |

Santa Monica Community College District, (Election of 2008), 5.00%, 8/1/44(1) | | | 7,500 | | | | 8,697,225 | |

Santa Rosa High School District, (Election of 2014), 5.00%, 8/1/41 | | | 3,495 | | | | 4,105,192 | |

Torrance Unified School District, (Election of 2008), 5.00%, 8/1/35 | | | 7,500 | | | | 8,742,900 | |

Ventura County Community College District, 5.00%, 8/1/30(1) | | | 8,000 | | | | 9,548,960 | |

| | | | | | | | | |

| | | $ | 129,604,851 | |

| | | | | | | | | |

|

Hospital — 7.8% | |

California Health Facilities Financing Authority, (Catholic Healthcare West), 5.25%, 3/1/27 | | $ | 1,750 | | | $ | 1,969,677 | |

California Health Facilities Financing Authority, (Catholic Healthcare West), 5.25%, 3/1/28 | | | 550 | | | | 612,310 | |

California Health Facilities Financing Authority, (City of Hope), 5.00%, 11/15/32 | | | 1,795 | | | | 2,039,282 | |

| | | | |

| | 14 | | See Notes to Financial Statements. |

Eaton Vance

California Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Hospital (continued) | |

California Health Facilities Financing Authority, (City of Hope), 5.00%, 11/15/35 | | $ | 2,565 | | | $ | 2,910,069 | |

California Health Facilities Financing Authority, (St. Joseph Health System), 5.00%, 7/1/33 | | | 4,480 | | | | 5,105,094 | |

California Health Facilities Financing Authority, (St. Joseph Health System), 5.00%, 7/1/37 | | | 2,100 | | | | 2,371,320 | |

California Health Facilities Financing Authority, (Sutter Health), 5.25%, 8/15/31(1) | | | 5,000 | | | | 5,722,000 | |

| | | | | | | | | |

| | | $ | 20,729,752 | |

| | | | | | | | | |

|

Insured – Electric Utilities — 4.3% | |

Northern California Power Agency, (Hydroelectric), (AGC), 5.00%, 7/1/24 | | $ | 2,000 | | | $ | 2,058,720 | |

Puerto Rico Electric Power Authority, (NPFG), 5.25%, 7/1/34 | | | 3,840 | | | | 4,091,943 | |

Sacramento Municipal Utility District, (AGM), 5.00%, 8/15/27 | | | 615 | | | | 636,820 | |

Sacramento Municipal Utility District, (AMBAC), (BHAC), 5.25%, 7/1/24 | | | 4,000 | | | | 4,755,880 | |

| | | | | | | | | |

| | | $ | 11,543,363 | |

| | | | | | | | | |

|

Insured – Escrowed / Prerefunded — 6.7% | |

Glendale, Electric System Revenue, (AGC), Prerefunded to 2/1/18, 5.00%, 2/1/31 | | $ | 2,240 | | | $ | 2,272,010 | |

Palm Springs Unified School District, (Election of 2008), (AGC), Prerefunded to 8/1/19, 5.00%, 8/1/33 | | | 4,500 | | | | 4,834,395 | |

Sacramento Municipal Utility District, (AGM), Prerefunded to 8/15/18, 5.00%, 8/15/27 | | | 385 | | | | 399,183 | |

San Diego County Water Authority, Certificates of Participation, (AGM), Prerefunded to 5/1/18, 5.00%, 5/1/38(1) | | | 10,000 | | | | 10,246,800 | |

| | | | | | | | | |

| | | $ | 17,752,388 | |

| | | | | | | | | |

|

Insured – General Obligations — 12.2% | |

Burbank Unified School District, (Election of 1997), (NPFG), 0.00%, 8/1/21 | | $ | 4,135 | | | $ | 3,903,936 | |

San Diego Unified School District, (NPFG), 0.00%, 7/1/22 | | | 2,300 | | | | 2,120,646 | |

San Diego Unified School District, (NPFG), 0.00%, 7/1/23 | | | 5,000 | | | | 4,489,550 | |

San Juan Unified School District, (AGM), 0.00%, 8/1/21 | | | 5,630 | | | | 5,317,423 | |

San Mateo County Community College District, (NPFG), 0.00%, 9/1/22 | | | 4,840 | | | | 4,463,884 | |

San Mateo County Community College District, (NPFG), 0.00%, 9/1/23 | | | 4,365 | | | | 3,920,861 | |

San Mateo County Community College District, (NPFG), 0.00%, 9/1/25 | | | 3,955 | | | | 3,337,743 | |

San Mateo Union High School District, (NPFG), 0.00%, 9/1/21 | | | 5,240 | | | | 4,944,202 | |

| | | | | | | | | |

| | | $ | 32,498,245 | |

| | | | | | | | | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Insured – Special Tax Revenue — 6.4% | |

Hesperia Public Financing Authority, (Redevelopment and Housing Projects), (XLCA), 5.00%, 9/1/31 | | $ | 595 | | | $ | 595,964 | |

Hesperia Public Financing Authority, (Redevelopment and Housing Projects), (XLCA), 5.00%, 9/1/37 | | | 7,240 | | | | 7,249,122 | |

Pomona Public Financing Authority, (NPFG), 5.00%, 2/1/33 | | | 5,940 | | | | 5,959,424 | |

Puerto Rico Sales Tax Financing Corp., (NPFG), 0.00%, 8/1/45 | | | 15,020 | | | | 3,159,607 | |

| | | | | | | | | |

| | | $ | 16,964,117 | |

| | | | | | | | | |

|

Insured – Water and Sewer — 1.7% | |

Riverside, Water System Revenue, (AGM), 5.00%, 10/1/38 | | $ | 1,595 | | | $ | 1,658,800 | |

San Luis Obispo County, (Nacimiento Water Project), (BHAC), (NPFG), 5.00%, 9/1/38 | | | 250 | | | | 250,813 | |

San Luis Obispo County, (Nacimiento Water Project), (NPFG), 4.50%, 9/1/40 | | | 2,750 | | | | 2,757,067 | |

| | | | | | | | | |

| | | $ | 4,666,680 | |

| | | | | | | | | |

|

Lease Revenue / Certificates of Participation — 1.1% | |

California Public Works Board, 5.00%, 11/1/38 | | $ | 2,565 | | | $ | 2,950,058 | |

| | | | | | | | | |

| | | $ | 2,950,058 | |

| | | | | | | | | |

|

Special Tax Revenue — 17.3% | |

Jurupa Public Financing Authority, 5.00%, 9/1/30 | | $ | 625 | | | $ | 721,875 | |

Jurupa Public Financing Authority, 5.00%, 9/1/32 | | | 625 | | | | 715,619 | |

Los Angeles County Metropolitan Transportation Authority, Sales Tax Revenue, 5.00%, 7/1/42 | | | 3,185 | | | | 3,779,416 | |

Riverside County Transportation Commission, Sales Tax Revenue, 5.25%, 6/1/39(1) | | | 6,285 | | | | 7,386,064 | |

San Bernardino County Transportation Authority, 5.25%, 3/1/40(1) | | | 10,375 | | | | 12,246,754 | |

San Diego County Regional Transportation Commission, Sales Tax Revenue, 5.00%, 4/1/41 | | | 8,150 | | | | 9,566,062 | |

San Francisco Bay Area Rapid Transportation District, Sales Tax Revenue, 5.00%, 7/1/36(1) | | | 6,250 | | | | 7,200,687 | |

Successor Agency to San Diego Redevelopment Agency, 5.00%, 9/1/32 | | | 3,720 | | | | 4,443,131 | |

| | | | | | | | | |

| | | $ | 46,059,608 | |

| | | | | | | | | |

|

Transportation — 11.4% | |

Bay Area Toll Authority, Toll Bridge Revenue, (San Francisco Bay Area), Prerefunded to 4/1/19, 5.25%, 4/1/29(1) | | $ | 6,500 | | | $ | 6,922,890 | |

Long Beach, Harbor Revenue, 5.00%, 5/15/27 | | | 1,960 | | | | 2,155,843 | |

Long Beach, Harbor Revenue, 5.00%, 5/15/42(1) | | | 7,500 | | | | 8,670,525 | |

Los Angeles Department of Airports, (Los Angeles International Airport), 5.00%, 5/15/35(1) | | | 7,500 | | | | 8,217,150 | |

| | | | |

| | 15 | | See Notes to Financial Statements. |

Eaton Vance

California Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Transportation (continued) | |

San Francisco City and County Airport Commission, (San Francisco International Airport), 5.00%, 5/1/35 | | $ | 2,190 | | | $ | 2,378,471 | |

San Jose, Airport Revenue, 5.00%, 3/1/31 | | | 1,750 | | | | 1,930,968 | |

| | | | | | | | | |

| | | $ | 30,275,847 | |

| | | | | | | | | |

|

Water and Sewer — 23.8% | |

Beverly Hills Public Financing Authority, Water Revenue, 5.00%, 6/1/37(1) | | $ | 5,725 | | | $ | 6,583,464 | |

East Bay Municipal Utility District, 5.00%, 6/1/36 | | | 5,725 | | | | 6,898,567 | |

Eastern Municipal Water District Financing Authority, 5.25%, 7/1/42(1) | | | 9,000 | | | | 10,939,140 | |

Los Angeles Department of Water and Power, Water System Revenue, 5.00%, 7/1/39(1) | | | 10,000 | | | | 11,646,100 | |

Los Angeles, Wastewater System Revenue, 5.00%, 6/1/43(1) | | | 7,500 | | | | 8,609,550 | |

Orange County Sanitation District, Wastewater Revenue, 5.00%, 2/1/35(1) | | | 10,000 | | | | 11,733,800 | |

Rancho California Water District Financing Authority, 5.00%, 8/1/46(1) | | | 6,000 | | | | 7,021,920 | |

| | | | | | | | | |

| | | $ | 63,432,541 | |

| | | | | | | | | |

| |

Total Tax-Exempt Investments — 170.6%

(identified cost $428,321,770) | | | $ | 454,406,805 | |

| | | | | | | | | |

| |

Other Assets, Less Liabilities — (70.6)% | | | $ | (188,060,676 | ) |

| | | | | | | | | |

| |

Net Assets — 100.0% | | | $ | 266,346,129 | |

| | | | | | | | | |

The percentage shown for each investment category in the Portfolio of Investments is based on net assets.

The Fund invests primarily in debt securities issued by California municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. In order to reduce the risk associated with such economic developments, at September 30, 2017, 18.4% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution or financial guaranty assurance agency ranged from 1.0% to 9.6% of total investments.

| (1) | Security represents the municipal bond held by a trust that issues residual interest bonds (see Note 1G). |

Abbreviations:

| | | | |

| AGC | | – | | Assured Guaranty Corp. |

| AGM | | – | | Assured Guaranty Municipal Corp. |

| AMBAC | | – | | AMBAC Financial Group, Inc. |

| BHAC | | – | | Berkshire Hathaway Assurance Corp. |

| NPFG | | – | | National Public Finance Guaranty Corp. |

| XLCA | | – | | XL Capital Assurance, Inc. |

| | | | |

| | 16 | | See Notes to Financial Statements. |

Eaton Vance

New York Municipal Bond Fund

September 30, 2017

Portfolio of Investments

| | | | | | | | |

| Tax-Exempt Investments — 167.4% | |

| | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Bond Bank — 9.1% | |

New York Environmental Facilities Corp., 5.00%, 10/15/39 | | $ | 3,360 | | | $ | 3,650,842 | |

New York Environmental Facilities Corp., Clean Water and Drinking Water, 4.00%, 6/15/46(1) | | | 15,000 | | | | 15,800,400 | |

| | | | | | | | | |

| | | $ | 19,451,242 | |

| | | | | | | | | |

|

Education — 30.0% | |

Geneva Development Corp., (Hobart and William Smith Colleges), 5.00%, 9/1/30 | | $ | 200 | | | $ | 233,552 | |

Geneva Development Corp., (Hobart and William Smith Colleges), 5.00%, 9/1/33 | | | 105 | | | | 121,176 | |

Geneva Development Corp., (Hobart and William Smith Colleges), 5.00%, 9/1/34 | | | 200 | | | | 230,094 | |

Geneva Development Corp., (Hobart and William Smith Colleges), Series 2012, 5.00%, 9/1/32 | | | 1,330 | | | | 1,515,468 | |

Geneva Development Corp., (Hobart and William Smith Colleges), Series 2014, 5.00%, 9/1/32 | | | 200 | | | | 231,774 | |

Hempstead Local Development Corp., (Adelphi University), 5.00%, 6/1/21 | | | 950 | | | | 1,067,677 | |

Hempstead Local Development Corp., (Adelphi University), 5.00%, 6/1/31 | | | 800 | | | | 896,264 | |

Hempstead Local Development Corp., (Adelphi University), 5.00%, 6/1/32 | | | 300 | | | | 335,415 | |

New York City Cultural Resource Trust, (The Juilliard School), 5.00%, 1/1/39 | | | 240 | | | | 251,388 | |

New York City Cultural Resource Trust, (The Juilliard School), 5.00%, 1/1/39(1) | | | 10,000 | | | | 10,474,500 | |

New York Dormitory Authority, (Columbia University), 5.00%, 10/1/41(1) | | | 10,000 | | | | 11,214,700 | |

New York Dormitory Authority, (Cornell University), 5.00%, 7/1/37(1) | | | 5,700 | | | | 6,273,819 | |

New York Dormitory Authority, (New York University), 4.00%, 7/1/35 | | | 1,500 | | | | 1,622,040 | |

New York Dormitory Authority, (New York University), Prerefunded to 7/1/19, 5.00%, 7/1/39(1) | | | 10,000 | | | | 10,703,300 | |

New York Dormitory Authority, (Rochester Institute of Technology), 5.00%, 7/1/40 | | | 2,000 | | | | 2,182,560 | |

New York Dormitory Authority, (Rockefeller University), 5.00%, 7/1/40 | | | 500 | | | | 532,495 | |

New York Dormitory Authority, (Rockefeller University), 5.00%, 7/1/40(1) | | | 2,700 | | | | 2,875,473 | |

New York Dormitory Authority, (Skidmore College), 5.00%, 7/1/26 | | | 1,175 | | | | 1,332,896 | |

New York Dormitory Authority, (Skidmore College), 5.25%, 7/1/30 | | | 250 | | | | 284,895 | |

New York Dormitory Authority, (The New School), 5.00%, 7/1/46 | | | 1,660 | | | | 1,889,097 | |

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Education (continued) | |

New York Dormitory Authority, (The New School), Prerefunded to 7/1/20, 5.50%, 7/1/40 | | $ | 5,250 | | | $ | 5,875,170 | |

Onondaga County Cultural Resources Trust, (Syracuse University), 5.00%, 12/1/38 | | | 3,305 | | | | 3,819,754 | |

| | | | | | | | | |

| | | $ | 63,963,507 | |

| | | | | | | | | |

|

Electric Utilities — 1.6% | |

Utility Debt Securitization Authority, 5.00%, 12/15/33 | | $ | 2,895 | | | $ | 3,414,652 | |

| | | | | | | | | |

| | | $ | 3,414,652 | |

| | | | | | | | | |

|

Escrowed / Prerefunded — 3.4% | |

Peekskill, Prerefunded to 6/1/18, 5.00%, 6/1/35 | | $ | 465 | | | $ | 477,927 | |

Peekskill, Prerefunded to 6/1/18, 5.00%, 6/1/36 | | | 490 | | | | 503,622 | |

Triborough Bridge and Tunnel Authority, Prerefunded to 11/15/18, 5.00%, 11/15/38(1) | | | 5,955 | | | | 6,232,090 | |

| | | | | | | | | |

| | | $ | 7,213,639 | |

| | | | | | | | | |

|

General Obligations — 11.7% | |

Long Beach City School District, 4.50%, 5/1/26 | | $ | 3,715 | | | $ | 4,027,209 | |

New York, 4.00%, 10/1/41(2) | | | 2,500 | | | | 2,667,725 | |

New York, 5.00%, 2/15/34(1) | | | 7,250 | | | | 8,148,347 | |

New York City, 5.00%, 8/1/34(1) | | | 8,650 | | | | 10,042,044 | |

| | | | | | | | | |

| | | $ | 24,885,325 | |

| | | | | | | | | |

|

Hospital — 9.5% | |

New York Dormitory Authority, (Highland Hospital of Rochester), 5.00%, 7/1/26 | | $ | 620 | | | $ | 669,612 | |

New York Dormitory Authority, (Highland Hospital of Rochester), 5.20%, 7/1/32 | | | 820 | | | | 881,156 | |

New York Dormitory Authority, (Memorial Sloan-Kettering Cancer Center), 4.375%, 7/1/34(1) | | | 9,325 | | | | 9,873,496 | |

New York Dormitory Authority, (North Shore-Long Island Jewish Obligated Group), Escrowed to Maturity, 5.00%, 5/1/20 | | | 1,065 | | | | 1,171,479 | |

Suffolk County Economic Development Corp., (Catholic Health Services of Long Island Obligated Group), 5.00%, 7/1/28 | | | 5,890 | | | | 6,453,320 | |

Suffolk County Economic Development Corp., (Catholic Health Services of Long Island Obligated Group), Prerefunded to 7/1/21, 5.00%, 7/1/28 | | | 1,010 | | | | 1,152,511 | |

| | | | | | | | | |

| | | $ | 20,201,574 | |

| | | | | | | | | |

|

Housing — 6.1% | |

New York City Housing Development Corp., 3.55%, 11/1/42 | | $ | 1,640 | | | $ | 1,623,272 | |

New York City Housing Development Corp., 3.80%, 11/1/37 | | | 885 | | | | 905,833 | |

| | | | |

| | 17 | | See Notes to Financial Statements. |

Eaton Vance

New York Municipal Bond Fund

September 30, 2017

Portfolio of Investments — continued

| | | | | | | | |

| Security | | Principal

Amount

(000’s omitted) | | | Value | |

| | | | | | | | |

|

Housing (continued) | |

New York City Housing Development Corp., 4.05%, 11/1/41 | | $ | 2,030 | | | $ | 2,105,110 | |

New York City Housing Development Corp., 4.95%, 11/1/39 | | | 2,500 | | | | 2,560,150 | |

New York Housing Finance Agency, (FHLMC), (FNMA), (GNMA), 3.20%, 11/1/46 | | | 3,385 | | | | 3,303,354 | |

New York Housing Finance Agency, (FHLMC), (FNMA), (GNMA), 4.00%, 11/1/42 | | | 500 | | | | 518,020 | |

New York Housing Finance Agency, (FNMA), 3.95%, 11/1/37 | | | 1,000 | | | | 1,038,530 | |

New York Mortgage Agency, 3.55%, 10/1/33 | | | 995 | | | | 1,010,621 | |

| | | | | | | | | |

| | | $ | 13,064,890 | |

| | | | | | | | | |

|

Industrial Development Revenue — 1.3% | |

New York Liberty Development Corp., (Goldman Sachs Group, Inc.), 5.25%, 10/1/35 | | $ | 640 | | | $ | 820,550 | |

New York Liberty Development Corp., (Goldman Sachs Group, Inc.), 5.50%, 10/1/37 | | | 1,440 | | | | 1,906,258 | |

| | | | | | | | | |

| | | $ | 2,726,808 | |

| | | | | | | | | |

|

Insured – Education — 3.6% | |

New York Dormitory Authority, (City University), (AMBAC), 5.50%, 7/1/35 | | $ | 1,025 | | | $ | 1,342,391 | |