UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21279

The Merger Fund VL

(Exact name of registrant as specified in charter)

100 Summit Lake Drive

Valhalla, New York 10595

(Address of principal executive offices) (Zip code)

Roy Behren and Michael T. Shannon

100 Summit Lake Drive

Valhalla, New York 10595

(Name and address of agent for service)

1-800-343-8959

Registrant's telephone number, including area code

Date of fiscal year end: December 31, 2018

Date of reporting period: December 31, 2018

Item 1. Reports to Stockholders.

December 31, 2018

Annual Report

THE MERGER FUND VL

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, at the election of your insurance company, paper copies of the Fund’s shareholder reports may no longer be sent by mail, unless you specifically request paper copies of the reports from your insurance company. Instead, the reports will be made available free of charge on a website, and if you have not previously elected electronic delivery of your shareholder reports, you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from your insurance company electronically by contacting your insurance company. You may elect to receive all future reports in paper free of charge. You can inform your insurance company that you wish to continue receiving paper copies of your shareholder reports by contacting your insurance company. Your election to receive reports in paper will apply to all funds held in your account with your insurance company.

| STANDARDIZED | Mutual Fund Assets: | |

| PERFORMANCE SUMMARY | Merger Arbitrage1 | $3.0 billion |

| As of December 31, 2018 | Opportunistic Credit | $3.8 million |

| | Multi-Event2 | $381.3 million |

| | |

| | Average Annual Total Return (%) |

| Merger Arbitrage | QTD | YTD | 1 YR | 5 YR | 10 YR | Life |

| The Merger Fund | | | | | | |

| (Institutional) | 1.98 | 7.98 | 7.98 | 2.91 | n/a | 3.10 |

| The Merger Fund | | | | | | |

| (Investor) | 1.92 | 7.68 | 7.68 | 2.62 | 3.38 | 6.10 |

| Insurance | | | | | | |

Dedicated Funds5 | | | | | | |

| The Merger Fund VL | 1.73 | 7.09 | 7.09 | 2.48 | 3.64 | 4.70 |

Opportunistic Credit5 | | | | | | |

| Credit Event Fund | | | | | | |

| (Institutional) | -3.12 | -2.93 | -2.93 | n/a | n/a | -2.92 |

| Credit Event Fund | | | | | | |

| (Investor) | -3.23 | -3.23 | -3.23 | n/a | n/a | -3.22 |

Multi Event5 | | | | | | |

| Event-Driven Fund | | | | | | |

| (Institutional) | -0.41 | 5.27 | 5.27 | n/a | n/a | 2.89 |

| Event-Driven Fund | | | | | | |

| (Investor) | -0.44 | 4.95 | 4.95 | n/a | n/a | 4.92 |

| | Annual Operating Expense Ratio (%)3 |

| | | | Net Expenses | | |

| | Gross | Net | excluding | | |

| | Expense | Expense | Investment- | Performance | |

| Merger Arbitrage | Ratio | Ratio3 | Related Expenses4,5 | Inception | Ticker |

| The Merger Fund | | | | | |

| (Institutional) | 1.60% | 1.59% | 1.17% | 08/01/2013 | MERIX |

| The Merger Fund | | | | | |

| (Investor) | 1.92% | 1.91% | 1.49% | 01/31/1989 | MERFX |

| Insurance | | | | | |

Dedicated Funds5 | | | | | |

| The Merger Fund VL | 2.57% | 1.84% | 1.40% | 05/26/2004 | MERVX |

Opportunistic Credit5 | | | | | |

| Credit Event Fund | | | | | |

| (Institutional) | 2.30% | 1.88% | 1.64% | 12/29/2017 | WCFIX |

| Credit Event Fund | | | | | |

| (Investor) | 2.55% | 2.13% | 1.89% | 12/29/2017 | WCFRX |

Multi Event5 | | | | | |

| Event-Driven Fund | | | | | |

| (Institutional) | 2.32% | 2.32% | 1.74% | 01/02/2014 | WCEIX |

| Event-Driven Fund | | | | | |

| (Investor) | 2.57% | 2.57% | 1.99% | 03/22/2017 | WCERX |

QTD and YTD performance is not annualized. Performance data quoted represent past performance; past performance does not guarantee future results. The performance results portrayed herein reflect the reinvestment of all interest, dividends and distributions. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data included herein for periods prior to 2011 reflect that of Westchester Capital Management, Inc., the Funds’ prior investment advisor. Messrs. Behren and Shannon, the Funds’ current portfolio managers, have served as co-portfolio managers of the Funds since 2007. Performance data current to the most recent month-end may be obtained by calling (800) 343-8959 or by visiting www.westchestercapitalfunds.com.

1Includes USD 147 million in a sub-advised fund. 2Includes USD 237 million in sub-advised funds. 3Net expense ratios are as of a fund’s most recent prospectus and were applicable to investors. 4Investment related expenses include expenses related to short sales and interest on any borrowing and acquired fund fees and expenses. 5The Adviser has contractually agreed to waive a portion of its investment advisory fee through April 30, 2019 for The Merger Fund® and WCM Alternatives: Event-Driven Fund, and through December 31, 2019 for The Merger Fund VL. The Adviser has contractually agreed to waive a portion of its investment advisory fee and to reimburse other ordinary operating expenses through April 30, 2019 for the WCM Alternatives: Credit Event Fund.

Trailing Returns

As of Date: 12/31/2018

| | QTD | YTD | 1 Year | 5 Years | 10 Years |

| US Fund Market Neutral | -0.45% | -0.63% | -0.63% | 0.82% | 0.33% |

| US Fund Multialternative | -4.51% | -4.61% | -4.61% | 0.08% | 2.40% |

| US Fund Long-Short Credit | -2.74% | -2.16% | -2.16% | 0.86% | 5.13% |

| Wilshire Liq Alt Event Driven | -1.65% | 0.27% | 0.27% | 0.26% | 2.73% |

| S&P 500 | -13.52% | -4.39% | -4.39% | 8.50% | 13.12% |

| BBgBarc US Agg Bond | 1.64% | 0.01% | 0.01% | 2.52% | 3.48% |

| BofAML US 3M Trsy Bill | 0.56% | 1.88% | 1.88% | 0.63% | 0.38% |

Fellow Shareholders,

The Merger Fund® advanced by 1.98% (MERIX) and 1.92% (MERFX) during the 4th quarter, posting a 7.98% and 7.68% YTD return, respectively. The Merger Fund VL, our insurance dedicated vehicle, was up 1.73% for the quarter and 7.09% year-to-date. The WCM Alternatives: Event-Driven Fund (WCEIX) Institutional and (WCERX) Investor share classes, ended the year on a positive note as well, up 5.27% and 4.95%, respectively. 2018 performance was at the high end of our targeted returns and we significantly outperformed most comparable vehicles.

2018: Few Places to Hide

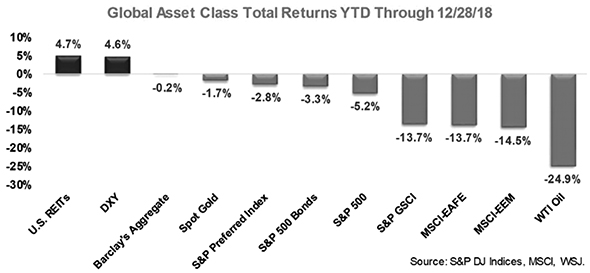

The fourth quarter’s market swoon pulled down a variety of strategies’ performance, including some of those thought to be market-neutral. A confluence of events boosted volatility and dragged down major markets, to finish their worst year since 2008. For the year, the Dow Jones Industrial Average was down 5.6%, the S&P 500 off 4.4% and the NASDAQ down 3.9%. Our relative and absolute performance in this environment illustrates the use case for uncorrelated and volatility-dampening products such as those that we manage.1

As William Watts wrote in Marketwatch in January, almost every asset class suffered declines for the year leaving investors “nowhere to hide.” Quoting a note from Sam Stovall, Chief Investment Strategist at CFRA, Watts added: “No matter the investment, investors likely experienced declines in annual returns. Indeed, even though U.S. REITs and the dollar recorded total returns in excess of 4.5%, declines were seen in bonds, gold, oil, preferred stocks and U.S. equities, along with developed international and emerging market indices.”2

__________

1 | U.S. Indexes Close with worst yearly losses since 2008, The Wall Street Journal, 1/1/19 |

2 | Here’s how ugly 2018 was for stocks and other assets, Marketwatch, 1/1/19 |

Of note, bond funds struggled, influenced by rising rates and credit quality concerns. The Bloomberg Barclays Aggregate Bond Index finished in negative territory and the average intermediate-term bond fund, a popular retail product, also lost 0.5 percent. According to the Seattle Times, funds that focus on corporate debt fared even worse as worries rose that a possible recession could lead to defaults and downgrades. The average corporate bond fund lost 2.5 percent, and the average high-yield bond fund dropped 2.6 percent in 2018.

Merger Arbitrage

The year 2018 was exceptional for mergers and acquisitions, characterized by large successful transactions in many industrial sectors, as companies aimed to create both cost-savings and earnings growth through transactions. Seeking to expand the top line, bottom line and also product lines, the buy vs. build decision was decided in favor of corporate acquisitions. This pursuit of scale drove a surge in deal activity – mostly via strategic transactions within the same industries, including telecommunications, energy, consumer goods and services, and healthcare. Transactions larger than USD10 billion rose by 120% to reach the second highest figure in the last 15 years, while the number of deals above USD5 billion were at decade-long highs.

As noted, The Merger Fund® advanced by 1.92% (MERFX) and 1.98% (MERIX) during the 4th quarter, its 94th gain in the 120 quarters since its inception 30 years ago, posting 7.68% and 7.98% YTD returns, respectively. The Merger Fund VL, our insurance dedicated vehicle, was up 1.73% for the quarter and 7.09% year-to-date. As is typical, the volatility of our returns was a fraction of that of the broad market, with the S&P 500’s 3-year standard deviation at 15.65% versus The Merger Fund’s roughly 2.90%. Speaking of 3 year track records, we are pleased to point out that The Merger Fund® Institutional share class (MERIX) was awarded a five-star Morningstar rating as of January 2019 for its most recent 3 year performance.

The biggest contributor to performance, Twenty-First Century Fox/Walt Disney Co., added 0.46% to the portfolio. We expect this deal to close by the end of next month. Our biggest detractor, DowDuPont Inc., which is in the process of splitting into 3 separately traded public entities, cost the fund 0.15% after the company lowered its earnings guidance in concert with weakness in the materials sector. The transaction appears to provide an attractive risk/reward profile, and we will keep you posted as the situation plays out further. Winners outnumbered the losers by more than 2 to 1 during the period, and no single position contributed to performance by more than 50 basis points. We added 32 new positions, ending with 89 positions in a broad variety of industries, and were 75%

invested as a number of deals closed at or near year end. Despite the relatively large temporary cash position, The Merger Fund® is off to a good start to 2019, ahead by 0.67% and 0.74% for the Investor and Institutional share class, respectively, through the end of January.

| NOTABLE WINNERS | NOTABLE LOSERS |

| Deal | Attribution | Deal | Attribution |

| Twenty-First Century | 0.46% | DowDupont Inc. | -0.15% |

| Fox/Walt Disney | | | |

| Dell Technologies | 0.35% | Newfield Exploration | -0.08% |

| Inc./VMware Inc. | | Co./Encana Corp. | |

| Macro Portfolio Hedge | 0.33% | Huntsman Corporation | -0.08% |

| Shire PLC/Takeda | 0.26% | Time Warner Inc./ | -0.08% |

| Pharmaceutical | | AT&T Inc. | |

| Aetna Inc./CVS | 0.25% | NXP Semiconductors | -0.07% |

| Health Corporation | | NV | |

| Rockwell Collins/ | 0.18% | Altaba Inc./Alibaba | -0.05% |

| United Technologies | | Group Holding Ltd. | |

Event-Driven

| Strategy | Allocations | | Strategy allocations result from our bottom-up process; our investment decisions are based on each opportunity’s unique characteristics. Every investment is based on public information rather than speculation, has a defined timeline and calculable expected return. The strategy is designed to “go where the events are.” We do not weight the portfolio according to pre-determined allocations to macro-factors such as strategy, sector or geography. |

| Arbitrage | 61.48% | |

| Special Situations | 10.48% | |

| Credit-Catalyst | 12.87% | |

| Corporate Restructuring | 15.17% | |

| Total | 100.00% | |

| | | |

The WCM Alternatives: Event-Driven Fund lost 0.41% and 0.44% in the Institutional (WCEIX) and Investor (WCERX) share classes respectively, during the quarter, reaching 5.27% and 4.95% returns for the year. Although lower than The Merger Fund®, it’s performance still comfortably beat most of its peers, as the event-driven space tends to have a larger market correlation than pure merger arbitrage vehicles. In fact, our event-driven fund has a sufficient long-term track record for Morningstar to include it in its overall category rankings, and we are proud to say that we have just been awarded the maximum 5 stars overall as of January 2019! During the quarter, we were invested in 135 events; 69 positions posted gains versus 66 with negative marks-to-market and 16 events were completed. Additionally, we entered 22 new positions and the fund was fully invested at quarter-end due to its broad investment mandate.

Many of the top performers and detractors for WCEIX included transactions invested in by The Merger Fund due to several attractive merger arbitrage opportunities; however, there were 28 non-merger arbitrage investments which added value during the quarter.

The largest contributor was Dell Technologies tracking stock, which gained as a result of Michael Dell increasing his offer to buy in the shares in order to merge them and their embedded holdings of VMware stock with the “parent company” (+0.49%). The largest detractor was Tenneco Inc. (-0.46%), which completed the acquisition of Federal-Mogul for a total consideration of $5.4 billion in October, and intends to separate the combined businesses into two independent, publicly traded companies through a tax-free spin-off to shareholders sometime in late 2019. Although we had some company-specific option hedges in place, we retained a partial delta to the underlying stock, and the position declined along with market and auto sector weakness.

SPACs (Special Purpose Acquisition Company) continue to provide attractive opportunities to deploy our cash balances in relatively low return but extremely low risk investments, which also offer potential upside optionality from the rights or warrants that accompany the purchase of IPO units.

Credit Event

The WCM Alternatives: Credit Event Fund was fully invested at quarter-end. The Institutional and Investor share classes lost 3.12% and 3.23% during the quarter, ending the year down 2.93% and 3.23% respectively. Seasonal factors and distortions stemming from the significant stock market correction and Federal Reserve policy confusion were the primary causes of the fund’s draw down. The good news is that we deployed a significant amount of capital in December and the fund bounced strongly in January, gaining 3.56%, recouping more than the negative marks-to-market from the fourth quarter.

There was no single biggest contributor to performance. SPAC investments generated a 30 basis points positive contribution. The largest single name detractor of performance was Colony Capital preferred stock that cost the fund 38 bps.

Thematically speaking, the biggest Q4 detractor was the group of closed end fund3 investments which as a whole lost 143 bps. We acquired a diversified basket of closed end funds that invest in leveraged loans. The investment thesis was that a) such corporate borrowings would perform well in a rising-rate environment due to the floating rate nature of the instruments; and b) what made them more attractive was that we could buy these loans at a discount of 7-12% through certain closed end funds. The discounts at which we purchased the closed end funds were abnormally wide by several standard deviations, exacerbated by year-end tax-related selling.

Unfortunately, throughout the second half of 2018, and especially in late November and December, the closed end funds declined in price because: a) discounts to net asset value (NAV) widened even more, to the mid-to-high teens, and b) the price of the loans themselves declined. The leveraged loan index as whole declined around 5 points as the fixed income market “dislocated” towards the end of the year.

Thus far, our belief that the dislocation was temporary has been partly vindicated. In January, the leveraged loan index recovered by several points. Additionally, closed end fund discounts to NAV have also narrowed back to the low teens and we have continued receiving dividend payments while awaiting such reversion. Overall, we remain constructive on our credit portfolio, and we believe we are positioned to generate an attractive risk-adjusted return by maintaining a short duration and low credit risk while retaining upside to certain opportunistic events and price reversions.

Outlook

We have yet to see signs of a downturn in transaction activity, and opportunities remain plentiful in the event space. We are monitoring many types of events such as product litigation, GSE (government sponsored entities such as Fannie Mae [FNMA] and Freddie Mac [FHLMC]) reform, and corporate restructurings such as spin-offs, subsidiary buy-ins, significant asset sales and late-stage bankruptcy emergences. Although there may be reason to be directionally nervous, due to political and regulatory uncertainty and possible early indicators of an economic

__________

3 | A closed end fund is a fund that is raises “permanent capital” within a fund structure (by managers such as Pimco, Nuveen, etc.) to invest using a particular strategy. Investors in a closed end fund, unlike in an open end fund, do not purchase or redeem shares directly from the fund. Instead, once a fixed amount of money has been raised, the shares trade in public markets similar to that of a normal individual stock. The end-of-day net asset value (NAV) of a typical mutual fund, called an “open end fund” will be the price that an investor transacts at. A key difference with a closed end fund, is that the price per share of a closed end fund may, and often does, trade at a discount or a premium to the NAV. Closed end funds have different investment strategies and may employ equities, preferred securities, leveraged loans or other fixed income securities, or a combination of the above. |

downturn, we try to insulate our investments from directional exposure and market or interest rate correlation. Our investments, both in merger arbitrage as well as the broader equity and credit event space, are primarily predicated opportunistically on the successful completion of announced catalysts rather than speculative valuation movements. Nonetheless, we believe the key drivers of many deals in 2018 –record access to investment capital, strong cash-rich and under-levered corporate balance, and persistently low borrowing costs along with ready access to financing – continue to provide significant support for transaction activity in the year ahead.

OUR COMPANY

WCM manages a total of six SEC-registered mutual funds. Our other vehicles span the spectrum from lower-return, lower-volatility expectations to additional volatility with potentially higher return expectations:

| Account | Vehicle | Strategy | Inception |

The Merger Fund® | SEC ‘40-Act Fund | Merger Arbitrage | 1989 |

| Investor Share | | | |

| Class (MERFX) | | | 1989 |

| Institutional Share | | | |

| Class (MERIX) | | | 2013 |

| The Merger | | | |

| Fund VL (MERVX) | Variable Insurance Trust | Merger Arbitrage | 2004 |

| WCM Alternatives: | | | |

| Credit Event | | | |

Fund New | SEC ‘40-Act Fund | Opportunistic Credit | 2017 |

| Investor Share | | | |

| Class (WCFRX) | | | 2017 |

| Institutional Share | | | |

| Class (WCFIX) | | | 2017 |

| WCM Alternatives: | | | |

| Event-Driven Fund | SEC ‘40-Act Fund | Event-Driven | 2014 |

| Investor Share | | | |

| Class (WCERX) | | | 2017 |

| Institutional Share | | | |

| Class (WCEIX) | | | 2014 |

| JNL/Westchester | | | |

| Capital Event | Sub-advised | | |

| Driven Fund | SEC ‘40-Act Fund | Event-Driven | 2015 |

| Westchester Merger | | | |

| Arbitrage Strategy | | | |

| of the JNL | | | |

| Multi-Manager | Sub-advised | | |

| Alternative Fund | SEC ‘40-Act Fund | Merger Arbitrage | 2016 |

As usual, quarterly statistical summaries for all of our vehicles are provided within two weeks of the end of the quarter- typically one month prior to the release of the quarterly letter. They are available electronically on our website, and we would be happy to provide a scheduled email as soon as the data becomes available. For convenience, investors can arrange for e-alerts of important Fund communications. Through our website at www.westchestercapitalfunds.com, you can check direct account balances, make purchases and sales, and sign up for notification of trade confirmations, statements, and shareholder communications via e-mail.

Please contact us with any questions or comments. We are always available and we enjoy speaking with our investors.

|  |

| Roy Behren | Mike Shannon |

IMPORTANT DISCLOSURES

Before investing in The Merger Fund®, WCM Alternatives: Event-Driven Fund, and/or WCM Alternatives: Credit Event Fund, carefully consider the investment objectives, risks, charges, and expenses. For a prospectus or summary prospectus containing this and other information, please call (800) 343-8959. Please read the prospectus carefully before investing. The Merger Fund VL is available through variable products offered by third-party insurance companies. For a prospectus containing information for any variable annuity or variable life product that invests in The Merger Fund VL, contact your financial advisor or the offering insurance company for a contract prospectus and prospectus for the underlying funds. Please read it carefully before investing. Shares of JNL/Westchester Capital Event Driven Fund are offered to separate accounts of participating life insurance companies for the purpose of funding variable annuity contracts and variable life insurance policies. Shares of the fund are not offered directly to the public. For a prospectus containing information for any variable annuity or variable life product that invests in the Fund, contact your financial advisor or the offering insurance company for a contract prospectus and prospectus for the underlying funds. Please read it carefully before investing. Variable annuities are long-term, tax-deferred investments designed for retirement, involve investment risks and may lose value. Earnings are taxable as ordinary income when distributed and may be subject to a 10% federal tax penalty if withdrawn before age 59½. Optional benefit costs are added to the ongoing fees and expenses of the variable annuity.

Variable annuities (VA650, VA660) are issued by Jackson National Life Insurance Company® (Home Office: Lansing, Michigan) and in New York (VA650NY, VA660NY) by Jackson National Life Insurance Company of New York® (Home Office: Purchase, New York). Variable annuities are distributed by Jackson National Life Distributors LLC, member FINRA. May not be available in all states and state variations may apply. These products have limitations and restrictions, including withdrawal charges, recapture charges and excess interest adjustments (interest rate adjustments in New York) where applicable. Jackson® issues other annuities with similar features, benefits, limitations, and charges. Contact Jackson for more information. Jackson is the marketing name for Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. The Ten Largest Positions as a Percent of Net Assets for The Merger Fund® as of December 31, 2018 were: Altaba Inc. (10.39%), Twenty-First Century Fox, Inc. Cl. B (7.14%), Red Hat, Inc. (5.74%), Shire PLC (4.38%), ARRIS International plc (2.85%), Aspen Insurance Holdings Limited (2.56%), Dominion Energy Midstream Partners, LP (2.53%), Columbia Pipeline Group, Inc. (2.16%), Valero Energy Partners LP (1.99%), Esterline Technologies Corporation (1.98%). The Ten Largest Positions as a Percent of Net Assets for The Merger Fund VL as of December 31, 2018 were: Altaba Inc. (9.13%), Twenty-First Century Fox, Inc. Cl. B (6.91%), Red Hat, Inc. (5.42%), Randgold Resources Limited (4.14%), Shire PLC (3.92%), ARRIS International plc (2.64%), Aspen Insurance Holdings Limited (2.41%), Dominion Energy Midstream Partners, LP (2.38%), Valero Energy Partners LP (1.85%), Esterline Technologies Corporation (1.85%). The Ten Largest Positions as a Percent of Net Assets for WCM Alternatives: Event-Driven Fund as of December 31, 2018 were: Altaba Inc. (9.92%), Twenty-First Century Fox, Inc. Cl. B (8.66%), Red Hat, Inc. (5.93%), Shire PLC (5.10%), ARRIS International plc (3.14%), Aspen Insurance Holdings Limited (2.90%), Dominion Energy Midstream Partners, LP (2.81%), Nielsen Finance LLC (2.66%), Esterline Technologies Corporation (2.49%), United Technologies Corporation (2.15%). The Ten Largest Positions as a Percent of Net Assets for WCM Alternatives: Credit Event Fund as of December 31, 2018 were: CM Seven Star Acquisition Corp. (6.30%), Univar USA Inc. (6.08%), Spectrum Brands Holdings, Inc. (5.98%), Ardagh Packaging Finance PLC (5.96%), Momentive Performance (5.23%), Alberton Acquisition Corporation (5.18%), EIG INVESTORS CORP (5.17%), Nielsen Finance LLC (5.15%), DJO FIN LLC/DJO FIN CORP (4.97%), Tribune Media (4.96%).

Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Mutual fund investing involves risk. Principal loss is possible. Merger-arbitrage and event-driven investing involve the risk that the adviser’s evaluation of the outcome of a proposed event, whether it be a merger, reorganization, regulatory issue or other events, will prove incorrect and that the Funds’ return on the investment will be negative. Investments in foreign companies may entail political, cultural, regulatory, legal, and tax risks different from those associated with comparable transactions in the United States. The frequency of the Fund’s transactions will vary from year to year, though merger arbitrage portfolios typically have higher turnover rates than portfolios of typical long-only funds. Increased portfolio turnover may result in higher brokerage commissions, dealer mark‐ups, and other transaction costs. The higher costs associated with increased portfolio turnover may offset gains in the Fund’s performance. The Funds’ may enter into short sale transactions for, among other reasons, purposes of protecting against a decline in the market value of the acquiring company’s shares prior to the acquisition completion. If the price of a security sold short increases between the time of the short sale and the time the Fund covers its short position, the Fund will incur a loss. The amount of a potential loss on an uncovered short sale transaction is theoretically unlimited. Debt securities may fluctuate in value due to, among other things, changes in interest rates, general economic conditions, industry fundamentals, market sentiment and the financial condition of the issuer, including the issuer’s credit rating or financial performance. Derivatives may create leverage which will amplify the effect of the performance of those instruments on the Funds’ and may produce significant losses. The Funds’ hedging strategy will be subject to the Funds’ investment adviser’s ability to assess correctly the degree of correlation between the performance of the instruments used in the hedging strategy and the performance of the investments in the portfolio being hedged. Investments in lower rated and non-rated securities present a great risk of loss to principal and interest than higher-rated securities. The WCM Alternatives: Credit Event Fund is non-diversified and therefore has a greater potential to realize losses upon the occurrence of adverse events affecting an issuer in its portfolio.

Any tax or legal information provided is merely a summary of our understanding and interpretation of some of the current income tax regulations and is not exhaustive. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation. Neither the Funds’ nor any of their representatives may give legal or tax advice.

The views expressed are as of January 31, 2019 and are a general guide to the views of Westchester Capital Management, are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security. Distributions are not guaranteed. This document does not replace portfolio and fund-specific materials.

The Morningstar Rating™ for funds, or “star rating”, is calculated for managed products (including mutual funds, variable annuity, and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product’s monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, and the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receives 1 star. The Overall Morningstar Rating™ for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating™ metrics.

The weights are 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns and 50% 10-year rating/30%

five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods. As of December 31, 2018, The Merger Fund® was rated against the following numbers of U.S.-domiciled Market Neutral funds over the following time periods: 122 funds in the last three years, 98 funds in the last five years, and 31 funds in the last ten years. With respect to these Market Neutral funds, The Merger Fund® – Investor share class (MERFX) received a Morningstar Rating of 4 stars, 4 stars and 4 stars for the three-, five- and ten-year periods, respectively. The Merger Fund® – Institutional share class (MERIX) received a Morningstar rating of 5 stars, 4 stars and 4 stars for the three-, five- and ten-year periods, respectively. Ten-year ratings are Extended Performance Ratings computed by Morningstar using historical adjusted returns prior to the 8/1/2013 inception date of MERIX and reflect the historical performance of MERFX, (inception date 1/31/1989), adjusted to reflect the fees and expenses of the Institutional shares. As of December 31, 2018, WCM Alternatives: Event-Driven Fund was rated against the following numbers of U.S.-domiciled Multi Alternative funds over the following time periods: 290 funds in the last three years. With respect to these Multi Alternative funds, WCM Alternatives: Event-Driven Fund – Institutional share class (WCEIX) received a Morningstar Rating of 4 stars for the three-year period. WCM Alternatives: Event-Driven Fund – Investor share class (WCERX) received a Morningstar Rating of 4 stars for the three-year period. As of January 31, 2019, WCM Alternatives: Event-Driven Fund was rated against the following numbers of U.S.-domiciled Multi Alternative funds over the following time periods: 278 funds in the last three years and 177 funds in the last five years. With respect to these Multi Alternative funds, WCM Alternatives: Event-Driven Fund – Institutional share class (WCEIX) received a Morningstar Rating of 4 stars for the three-year period and 5 stars for the five-year period. 3-year and 5-year ratings are Extended Performance Ratings computed by Morningstar using historical adjusted returns prior to the 3/22/2017 inception date of WCERX and reflect the historical performance of WCEIX, (inception date 1/2/2014), adjusted to reflect the fees and expenses of the Investor shares. © 2018 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Absolute return strategies are not intended to outperform stocks and bonds during strong market rallies. An absolute return fund may not achieve its goals and may underperform during periods of strong positive market performance.

Definitions: The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general; The Bloomberg Barclays Aggregate Bond Index is an intermediate-term index comprised of investment grade bonds. The Bloomberg Barclays US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P are Ba1/BB+/BB+ or below. The Morningstar Category: US Fund Market Neutral is comprised of a universe of funds with similar investment objectives. The Morningstar Category: The US Fund MultiAlternative encompasses funds that have a majority of their assets exposed to alternative strategies and include both funds with static allocations to alternative strategies and funds tactically allocating among alternative strategies and asset classes. The ICE BofA Merrill Lynch US 3-Month Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Indices are unavailable for direct investment. The Dow Jones Industrial Average, or simply the Dow, is a stock market index that shows how 30 large, publicly owned companies based in the United States have traded during a standard trading session in the stock market. Nasdaq is a global electronic marketplace for buying and selling securities, as well as the benchmark index for U.S. technology stocks. Indices are unavailable for direct investment. The Wilshire Liquid Alternative Event Driven IndexSM measures the performance of the event-driven strategy component of The Wilshire

Liquid Alternative IndexSM. Event-driven strategies predominantly invest in companies involved in corporate transactions such as mergers, restructuring, distressed, buy-backs, or other capital structure changes. The Wilshire Liquid Alternative Event Driven Index (WLIQAED) is designed to provide a broad measure of the liquid alternative event-driven market. HFRX Event Driven Index is comprised of investment Managers who maintain positions in companies currently or prospectively involved in corporate transactions of a wide variety including but not limited to mergers, restructurings, financial distress, tender offers, shareholder buybacks, debt exchanges, security issuance or other capital structure adjustments. DOJ or The United States Department of Justice Antitrust Division is a law enforcement agency responsible for enforcing the antitrust laws of the United States. Standard Deviation is the degree to which returns vary relative to the average return: The higher the standard deviation, the greater the variability of the investment. Beta is a measure of the fund’s sensitivity to market movements. A portfolio with a beta greater than 1 is more volatile than the market and a portfolio with a beta less than 1 is less volatile than the market; Correlation is calculated using R-Squared; which is a measure that represents the percentage of a fund’s movements that can be explained by movements in a benchmark index. A fund with low R-squared doesn’t act much like the index; A special purpose acquisition company (SPAC) is a corporation formed by private individuals to facilitate investment through an initial public offering (IPO). The proceeds are used to buy one or more existing companies. A put option is an option contract giving the owner the right, but not the obligation, to sell a specified amount of an underlying security at a specified price within a specified time frame. This is the opposite of a call option, which gives the holder the right to buy an underlying security at a specified price before the option expires. The returns shown are based on net asset values calculated for shareholder transactions and may differ from the returns shown in the financial highlights of the annual report, which reflects adjustments made to the net asset values in accordance with accounting principles generally accepted in the United States of America.

The Merger Fund®, WCM Alternatives: Event-Driven Fund and WCM Alternatives: Credit Event Fund are distributed by Compass Distributors, LLC. The Merger VL is available through variable products offered by third-party insurance companies and is not affiliated with Compass Distributors, LLC.

DEAL COMPOSITION

The Merger Fund VL (Unaudited)

| Type of Buyer | | | | Deal Terms* | | |

| Strategic | 95.7% | | | Cash | 52.5% | |

| Financial | 4.3% | | | Stock and Stub(1) | 23.6% | |

| | | | | Stock with Fixed Exchange Ratio | 14.8% | |

| By Deal Type | | | | Cash & Stock | 9.1% | |

| Friendly | 100.0% | | | Stock with Flexible | | |

| Hostile | —% | | | Exchange Ratio (Collar) | —% | ** |

| | | | | Undetermined(2) | —% | |

| * | | Data expressed as a percentage of long common stock, corporate bonds and swap contract positions as of December 31, 2018. |

| ** | | Less than 0.05%. |

(1) | | “Stub” includes assets other than cash and stock (e.g., escrow notes). |

(2) | | The compensation is undetermined because the compensation to be received (e.g., stock, cash, escrow notes, other) will be determined at a later date, potentially at the option of the Fund’s investment adviser. |

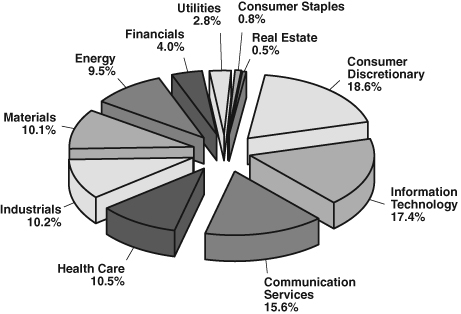

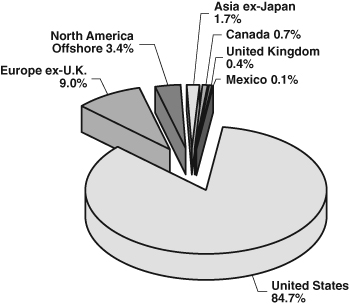

PORTFOLIO COMPOSITION*

The Merger Fund VL (Unaudited)

By Sector

By Region

| * | Data expressed as a percentage of long common stock, closed-end funds, preferred stocks, contingent value rights, rights, warrants, bank loans, corporate bonds and swap contract positions as of December 31, 2018. Data expressed excludes special purpose acquisition companies, short-term investments, short investments, written options, forward currency exchange contracts and short total return swap contracts. Please refer to the Schedule of Investments for more details on the Fund’s individual holdings. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services (”Fund Services”).

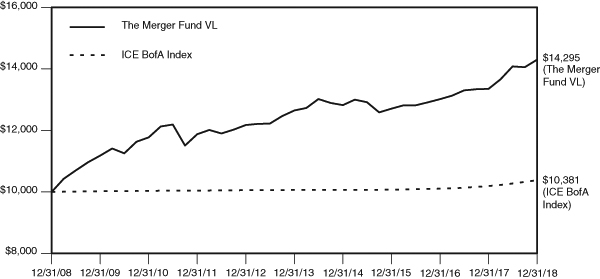

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT

IN THE MERGER FUND VL AND THE ICE BofA MERRILL LYNCH

3-MONTH U.S. TREASURY BILL INDEX (Unaudited)

THE MERGER FUND VL

AVERAGE ANNUAL TOTAL RETURN

as of December 31, 2018

| | 1 Year | 3 Year | 5 Year | 10 Year |

| The Merger Fund VL | 7.09% | 4.01% | 2.48% | 3.64% |

| ICE BofA Index | 1.87% | 1.02% | 0.63% | 0.37% |

This chart assumes an initial gross investment of $10,000 made on December 31, 2008. Returns shown include the reinvestment of all dividends. Past performance is not predictive of future performance. The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or upon redemption of fund shares. Investment return and principal value will fluctuate, so that your shares, when redeemed, may be worth more or less than the original cost.

The ICE BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (“ICE BofA Index”) is comprised of a single issue purchased at the beginning of the month and held for a full month. At the end of the month that issue is sold and rolled into a newly selected issue. The issue selected at each month-end rebalancing is the outstanding U.S. Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date. To qualify for selection, an issue must have settled on or before the month-end rebalancing date. The index is unmanaged and does not include any expenses, fees or sales charges. It is not possible to invest directly in an index.

The Merger Fund VL

EXPENSE EXAMPLE

December 31, 2018 (Unaudited)

As a shareholder of The Merger Fund VL (the “Fund”), you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees, and other Fund specific expenses. The expense example is intended to help a shareholder understand ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the most recent six-month period.

The Actual Expenses comparison provides information about actual account values and actual expenses. A shareholder may use the information in this line, together with the amount invested, to estimate the expenses paid over the period. A shareholder may divide his/her account value by $1,000 (e.g., an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses paid on his/her account during this period. The example below includes, among other fees, management fees, fund accounting, custody and transfer agent fees. However, the example does not include portfolio trading commissions and related expenses or extraordinary expenses. In addition, charges and expenses at the insurance company separate account level are not reflected.

The Hypothetical Example for Comparison Purposes provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses paid for the period. A shareholder may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, a shareholder would compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

The expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemptions fees, or exchange fees. Therefore, the Hypothetical Example for Comparison Purposes is useful in comparing ongoing costs only, and will not help to determine the relevant total costs of owning different funds. In addition, if these transactional costs were included, shareholder costs would have been higher.

The Merger Fund VL

EXPENSE EXAMPLE (continued)

December 31, 2018 (Unaudited)

| | Annualized | Beginning | Ending | Expenses Paid |

| | Net Expense | Account | Account | During Period |

| | Ratio | Value | Value | 7/1/18 — |

| | 12/31/18 | 7/1/18 | 12/31/18 | 12/31/18(1) |

Actual Expenses(2)(3) | 1.79% | $1,000.00 | $1,015.50 | $9.09 |

| Hypothetical Example | | | | |

| for Comparison Purposes | | | | |

| (5% return before | | | | |

expenses)(3) | 1.79% | $1,000.00 | $1,016.18 | $9.10 |

| (1) | Expenses are equal to the Fund’s annualized net expense ratio, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| (2) | Based on the actual returns of 1.55% for the six-month period ended December 31, 2018. |

| (3) | Excluding dividends on short positions and borrowing expenses on securities sold short, your actual cost of investment in and your hypothetical cost of investment in the Fund would have been $7.11 and $7.12, respectively. |

The Merger Fund VL

SCHEDULE OF INVESTMENTS

December 31, 2018

| | | Shares | | | Value | |

| LONG INVESTMENTS — 98.32% | | | | | | |

| COMMON STOCKS — 42.64% | | | | | | |

| AEROSPACE & DEFENSE — 2.72% | | | | | | |

| Esterline Technologies Corporation (a) | | | 6,338 | | | $ | 769,750 | |

| L3 Technologies, Inc. | | | 2,098 | | | | 364,339 | |

| | | | | | | | 1,134,089 | |

| APPLICATION SOFTWARE — 0.10% | | | | | | | | |

| SendGrid, Inc. (a) | | | 980 | | | | 42,307 | |

| BIOTECHNOLOGY — 0.77% | | | | | | | | |

| Shire plc — ADR | | | 1,848 | | | | 321,626 | |

| BROADCASTING — 0.16% | | | | | | | | |

| Discovery Communications, Inc. Class C (a) | | | 2,937 | | | | 67,786 | |

| BUILDING PRODUCTS — 1.38% | | | | | | | | |

| USG Corporation | | | 13,461 | | | | 574,246 | |

| COMMUNICATIONS EQUIPMENT — 2.64% | | | | | | | | |

| ARRIS International plc (a)(b) | | | 35,976 | | | | 1,099,786 | |

| COPPER — 0.16% | | | | | | | | |

| Nevsun Resources Ltd. (b)(f) | | | 15,344 | | | | 67,324 | |

| DATA PROCESSING & | | | | | | | | |

| OUTSOURCED SERVICES — 0.15% | | | | | | | | |

| Travelport Worldwide Ltd. (b) | | | 3,988 | | | | 62,293 | |

| DIVERSIFIED CHEMICALS — 1.00% | | | | | | | | |

| DowDuPont, Inc. (e)(k) | | | 7,800 | | | | 417,144 | |

| ELECTRONIC EQUIPMENT | | | | | | | | |

| & INSTRUMENTS — 1.06% | | | | | | | | |

| Orbotech Ltd. (a)(b) | | | 7,796 | | | | 440,786 | |

| GOLD — 4.14% | | | | | | | | |

| Randgold Resources Ltd. — ADR (f) | | | 20,136 | | | | 1,724,510 | |

| HEALTH CARE EQUIPMENT | | | | | | | | |

| & SUPPLIES — 1.70% | | | | | | | | |

| NxStage Medical, Inc. (a) | | | 24,717 | | | | 707,401 | |

| HEALTH CARE TECHNOLOGY — 0.48% | | | | | | | | |

| athenahealth, Inc. (a) | | | 1,528 | | | | 201,589 | |

| INTEGRATED TELECOMMUNICATION | | | | | | | | |

| SERVICES — 0.48% | | | | | | | | |

| AT&T, Inc. (e)(k) | | | 7,062 | | | | 201,549 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

| | | Shares | | | Value | |

| LIFE & HEALTH INSURANCE — 0.05% | | | | | | |

| Genworth Financial, Inc. Class A (a) | | | 4,159 | | | $ | 19,381 | |

| MOVIES & ENTERTAINMENT — 8.35% | | | | | | | | |

| Pandora Media, Inc. (a) | | | 68,946 | | | | 557,773 | |

| Twenty-First Century Fox, Inc. Class A | | | 902 | | | | 43,404 | |

| Twenty-First Century Fox, Inc. Class B (e) | | | 60,237 | | | | 2,878,124 | |

| | | | | | | | 3,479,301 | |

| MULTI-UTILITIES — 1.20% | | | | | | | | |

| SCANA Corporation | | | 10,415 | | | | 497,629 | |

| OIL & GAS EXPLORATION | | | | | | | | |

| & PRODUCTION — 0.69% | | | | | | | | |

| Encana Corporation (b) | | | 23,327 | | | | 134,830 | |

| Newfield Exploration Company (a) | | | 10,318 | | | | 151,262 | |

| | | | | | | | 286,092 | |

| OIL & GAS REFINING & MARKETING — 0.03% | | | | | | | | |

| EnLink Midstream Partners LP | | | 987 | | | | 10,867 | |

| OIL & GAS STORAGE | | | | | | | | |

| & TRANSPORTATION — 5.30% | | | | | | | | |

| Columbia Pipeline Group, Inc. (a)(d)(g)(i) | | | 16,892 | | | | 443,558 | |

| Dominion Energy Midstream Partners LP | | | 54,930 | | | | 990,937 | |

| Valero Energy Partners LP | | | 18,301 | | | | 771,753 | |

| | | | | | | | 2,206,248 | |

| PROPERTY & CASUALTY INSURANCE — 2.41% | | | | | | | | |

| Aspen Insurance Holdings Ltd. (b) | | | 23,923 | | | | 1,004,527 | |

| REITs — 0.33% | | | | | | | | |

| Brookfield Property REIT, Inc. Class A | | | 8,413 | | | | 135,449 | |

| RESEARCH & CONSULTING SERVICES — 1.21% | | | | | | | | |

| The Dun & Bradstreet Corporation | | | 3,525 | | | | 503,158 | |

| SYSTEMS SOFTWARE — 5.42% | | | | | | | | |

| Red Hat, Inc. (a)(e) | | | 12,855 | | | | 2,257,852 | |

| TECHNOLOGY HARDWARE, | | | | | | | | |

| STORAGE & PERIPHERALS — 0.71% | | | | | | | | |

| Dell Technologies, Inc. Class C (a) | | | 6,019 | | | | 294,134 | |

| TOTAL COMMON STOCKS (Cost $17,710,560) | | | | | | | 17,757,074 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

| | | Shares | | | Value | |

| SPECIAL PURPOSE | | | | | | |

| ACQUISITION COMPANIES — 7.44% (a) | | | | | | |

| Black Ridge Acquisition Corporation | | | 3,305 | | | $ | 33,182 | |

| CF Finance Acquisition Corporation | | | 5,187 | | | | 51,870 | |

| ChaSerg Technology Acquisition Corporation | | | 5,904 | | | | 58,981 | |

| Collier Creek Holdings Class A (b)(f) | | | 11,400 | | | | 114,456 | |

| Constellation Alpha Capital Corporation (b) | | | 34,369 | | | | 350,907 | |

| Federal Street Acquisition Corporation Class A | | | 5,016 | | | | 51,314 | |

| Forum Merger II Corporation Class A | | | 3,446 | | | | 33,254 | |

| Gordon Pointe Acquisition Corporation (f) | | | 17,028 | | | | 170,706 | |

| Graf Industrial Corporation (f) | | | 51,254 | | | | 513,053 | |

| Legacy Acquisition Corporation Class A | | | 949 | | | | 9,319 | |

| Leisure Acquisition Corporation | | | 6,820 | | | | 66,972 | |

| Megalith Financial Acquisition | | | | | | | | |

| Corporation Class A | | | 3,536 | | | | 34,299 | |

| Modern Media Acquisition Corporation | | | 18,790 | | | | 191,658 | |

| Mudrick Capital Acquisition | | | | | | | | |

| Corporation Class A (f) | | | 5,919 | | | | 58,480 | |

| Opes Acquisition Corporation | | | 4,080 | | | | 40,514 | |

| Pensare Acquisition Corporation | | | 11,440 | | | | 115,887 | |

| Pure Acquisition Corporation | | | 9,128 | | | | 89,820 | |

| Thunder Bridge Acquisition Ltd. (b)(f) | | | 10,600 | | | | 107,908 | |

| Thunder Bridge Acquisition Ltd. Class A (b) | | | 45,274 | | | | 448,213 | |

| Tiberius Acquisition Corporation | | | 4,193 | | | | 41,091 | |

| TKK Symphony Acquisition Corporation (b) | | | 5,669 | | | | 54,706 | |

| Trident Acquisitions Corporation | | | 13,674 | | | | 136,330 | |

| Trinity Merger Corporation Class A | | | 3,140 | | | | 31,369 | |

| Twelve Seas Investment Company (b) | | | 7,333 | | | | 72,010 | |

| VectoIQ Acquisition Corporation | | | 22,805 | | | | 221,208 | |

| TOTAL SPECIAL PURPOSE | | | | | | | | |

| ACQUISITION COMPANIES (Cost $3,046,201) | | | | | | | 3,097,507 | |

| | | | | | | | | |

| CLOSED-END FUNDS — 9.13% (a)(e) | | | | | | | | |

| Altaba, Inc. | | | 65,636 | | | | 3,802,950 | |

| TOTAL CLOSED-END FUNDS (Cost $4,235,383) | | | | | | | 3,802,950 | |

| | | | | | | | | |

| PREFERRED STOCKS — 0.17% | | | | | | | | |

| Colony Capital, Inc., 8.750%, Series E | | | 284 | | | | 6,572 | |

| NuStar Logistics LP, 9.170% | | | | | | | | |

| (3 Month LIBOR + 6.734%), 1/15/2043 (e)(j) | | | 2,732 | | | | 65,131 | |

| TOTAL PREFERRED STOCKS (Cost $76,013) | | | | | | | 71,703 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

| | | Shares | | | Value | |

| CONTINGENT VALUE RIGHTS — 0.00% (a)(e)(g) | | | | | | |

| Media General, Inc. | | | 8,397 | | | $ | 252 | |

| TOTAL CONTINGENT VALUE RIGHTS (Cost $0) | | | | | | | 252 | |

| | | | | | | | | |

| RIGHTS — 0.01% (a) | | | | | | | | |

| Black Ridge Acquisition Corporation | | | 3,305 | | | | 991 | |

| Modern Media Acquisition Corporation | | | 5,284 | | | | 1,321 | |

| Pensare Acquisition Corporation | | | 7,938 | | | | 2,302 | |

| TOTAL RIGHTS (Cost $6,600) | | | | | | | 4,614 | |

| | | | | | | | | |

| WARRANTS — 0.03% (a) | | | | | | | | |

| Black Ridge Acquisition Corporation | | | 3,305 | | | | 1,058 | |

| ConvergeOne Holdings, Inc. (f) | | | 1,547 | | | | 1,524 | |

| Federal Street Acquisition | | | | | | | | |

| Corporation Class A (f) | | | 724 | | | | 543 | |

| Modern Media Acquisition Corporation | | | 2,642 | | | | 711 | |

| Mudrick Capital Acquisition | | | | | | | | |

| Corporation Class A | | | 5,919 | | | | 2,663 | |

| Pensare Acquisition Corporation | | | 3,969 | | | | 794 | |

| Pure Acquisition Corporation | | | 4,543 | | | | 5,179 | |

| Tiberius Acquisition Corporation | | | 4,193 | | | | 1,635 | |

| TOTAL WARRANTS (Cost $17,096) | | | | | | | 14,107 | |

| | | | | | | | | |

| | | Principal | | | | | |

| | | Amount | | | | | |

| BANK LOANS — 1.67% (f)(j) | | | | | | | | |

| Tribune Media Company | | | | | | | | |

| 5.520% (1 Month | | | | | | | | |

| LIBOR + 3.000%), 1/27/2024 | | $ | 393,000 | | | | 388,087 | |

| Zayo Group LLC | | | | | | | | |

| 4.477% (1 Month | | | | | | | | |

| LIBOR + 2.000%), 1/19/2021 | | | 313,721 | | | | 305,878 | |

| TOTAL BANK LOANS (Cost $703,659) | | | | | | | 693,965 | |

| | | | | | | | | |

| CORPORATE BONDS — 6.88% (f) | | | | | | | | |

| Ardagh Packaging Finance plc / | | | | | | | | |

| Ardagh Holdings USA, Inc. | | | | | | | | |

| 7.250%, 5/15/2024 (b)(h) | | | 338,000 | | | | 338,422 | |

| DJO Finance LLC / DJO Finance Corporation | | | | | | | | |

| 8.125%, 6/15/2021 (h) | | | 290,000 | | | | 299,425 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

| | | Principal | | | | | | |

| | | Amount | | | | | Value | |

| Vistra Energy Corporation | | | | | | | | |

| 5.875%, 6/1/2023 | | $ | 198,000 | | | | | $ | 198,990 | |

| EIG Investors Corporation | | | | | | | | | | |

| 10.875%, 2/1/2024 | | | 225,000 | | | | | | 241,875 | |

| Momentive Performance Materials, Inc. | | | | | | | | | | |

| 3.880%, 10/24/2021 | | | 189,000 | | | | | | 201,049 | |

| Nationstar Mortgage LLC / | | | | | | | | | | |

| Nationstar Capital Corporation | | | | | | | | | | |

| 6.500%, 7/1/2021 | | | 40,000 | | | | | | 39,100 | |

| 6.500%, 6/1/2022 | | | 27,000 | | | | | | 26,511 | |

| Nielsen Finance LLC / | | | | | | | | | | |

| Nielsen Finance Company | | | | | | | | | | |

| 5.000%, 4/15/2022 (h) | | | 163,000 | | | | | | 156,480 | |

| Rent-A-Center, Inc. | | | | | | | | | | |

| 6.625%, 11/15/2020 | | | 119,000 | | | | | | 116,025 | |

| 4.750%, 5/1/2021 (e) | | | 200,000 | | | | | | 192,000 | |

| Spectrum Brands Holdings, Inc. | | | | | | | | | | |

| 7.750%, 1/15/2022 | | | 228,000 | | | | | | 231,420 | |

| T-Mobile USA, Inc. | | | | | | | | | | |

| 6.500%, 1/15/2024 | | | 145,000 | | | | | | 149,376 | |

| Unitymedia GmbH | | | | | | | | | | |

| 6.125%, 1/15/2025 (b)(h) | | | 231,000 | | | | | | 233,287 | |

| Unitymedia Hessen GmbH & Company | | | | | | | | | | |

| KG / Unitymedia NRW GmbH | | | | | | | | | | |

| 5.000%, 1/15/2025 (b)(h) | | | 113,000 | | | | | | 110,966 | |

| Univar USA, Inc. | | | | | | | | | | |

| 6.750%, 7/15/2023 (h) | | | 333,000 | | | | | | 330,086 | |

| TOTAL CORPORATE BONDS (Cost $2,928,460) | | | | | | | | | 2,865,012 | |

| | | | | | | | | | | |

| | | Contracts | | | | | | | |

| | | (100 shares | | | Notional | | | | |

| | | per contract) | | | Amount | | | | |

| PURCHASED PUT OPTIONS — 0.42% (a) | | | | | | | | | | |

| DowDuPont, Inc. | | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | | |

| Exercise Price: $55.00 | | | 4 | | $ | 21,392 | | | 972 | |

| Expiration: February 2019, | | | | | | | | | | |

| Exercise Price: $45.00 | | | 74 | | | 395,752 | | | 3,589 | |

| First Trust Natural Gas ETF Trust | | | | | | | | | | |

| Expiration: March 2019, | | | | | | | | | | |

| Exercise Price: $22.00 | | | 54 | | | 79,380 | | | 39,960 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

| | | Contracts | | | | | | | |

| | | (100 shares | | | Notional | | | | |

| | | per contract) | | | Amount | | | Value | |

| SPDR S&P 500 ETF Trust | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | |

| Exercise Price: $247.00 | | | 31 | | | $ | 774,752 | | | $ | 12,400 | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $255.00 | | | 12 | | | | 299,904 | | | | 9,156 | |

| SPDR S&P Oil & Gas Exploration | | | | | | | | | | | | |

| & Production ETF Trust | | | | | | | | | | | | |

| Expiration: February 2019, | | | | | | | | | | | | |

| Exercise Price: $32.00 | | | 83 | | | | 220,199 | | | | 46,480 | |

| Technology Select Sector SPDR Fund | | | | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $70.00 | | | 45 | | | | 278,910 | | | | 36,090 | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $71.00 | | | 29 | | | | 179,742 | | | | 26,158 | |

| The Walt Disney Company | | | | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $95.00 | | | 83 | | | | 910,095 | | | | 1,328 | |

| TOTAL PURCHASED OPTIONS (Cost $151,974) | | | | | | | | | | | 176,133 | |

| | | | | | | | | | | | | |

| | | Principal | | | | | | | | | |

| | | Amount | | | | | | | | | |

| ESCROW NOTES — 0.03% (a)(d)(g) | | | | | | | | | | | | |

| AMR Corporation | | $ | 7,668 | | | | | | | | 11,885 | |

| T-Mobile USA, Inc. | | | 108,000 | | | | | | | | — | |

| TOTAL ESCROW NOTES (Cost $4,196) | | | | | | | | | | | 11,885 | |

| | | | | | | | | | | | | |

| | | Shares | | | | | | | | | |

| SHORT-TERM INVESTMENTS — 29.90% | | | | | | | | | | | | |

| MONEY MARKET FUNDS — 29.04% (c) | | | | | | | | | | | | |

| First American Government Obligations Fund, | | | | | | | | | | | | |

| Institutional Share Class, 2.32% | | | 1,931,000 | | | | | | | | 1,931,000 | |

| Goldman Sachs Financial Square | | | | | | | | | | | | |

| Funds — Government Fund, | | | | | | | | | | | | |

| Institutional Share Class, 2.34% | | | 1,931,000 | | | | | | | | 1,931,000 | |

| The Government & Agency Portfolio, | | | | | | | | | | | | |

| Institutional Share Class, 2.30% | | | 1,931,000 | | | | | | | | 1,931,000 | |

| JPMorgan Prime Money Market Fund, | | | | | | | | | | | | |

| Institutional Share Class, 2.53% (e) | | | 507,672 | | | | | | | | 507,720 | |

| JPMorgan U.S. Government Money Market | | | | | | | | | | | | |

| Fund, Institutional Share Class, 2.33% (e) | | | 1,931,000 | | | | | | | | 1,931,000 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

| | | Shares | | | Value | |

| Morgan Stanley Institutional Liquidity | | | | | | |

| Fund — Government Portfolio, | | | | | | |

| Institutional Share Class, 2.32% | | | 1,931,000 | | | $ | 1,931,000 | |

| Morgan Stanley Institutional Liquidity | | | | | | | | |

| Fund — Treasury Portfolio, | | | | | | | | |

| Institutional Share Class, 2.33% | | | 1,931,000 | | | | 1,931,000 | |

| | | | | | | | 12,093,720 | |

| | | | | | | | | |

| | | Principal | | | | | |

| | | Amount | | | | | |

| U.S. TREASURY BILLS — 0.86% (e)(f) | | | | | | | | |

| United States Treasury Bills | | | | | | | | |

| 2.19%, 2/28/2019 | | $ | 58,000 | | | | 57,778 | |

| 2.38%, 4/25/2019 | | | 305,000 | | | | 302,651 | |

| | | | | | | | 360,429 | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | | | | |

| (Cost $12,454,243) | | | | | | | 12,454,149 | |

| TOTAL LONG INVESTMENTS | | | | | | | | |

| (Cost $41,334,385) — 98.32% | | | | | | | 40,949,351 | |

| | | | | | | | | |

| | | Shares | | | | | |

| SHORT INVESTMENTS — (19.65)% | | | | | | | | |

| COMMON STOCKS — (18.95)% | | | | | | | | |

| AEROSPACE & DEFENSE — (0.88)% | | | | | | | | |

| Harris Corporation | | | (2,728 | ) | | | (367,325 | ) |

| AIRLINES — (0.03)% | | | | | | | | |

| American Airlines Group, Inc. | | | (402 | ) | | | (12,908 | ) |

| BROADCASTING — (0.17)% | | | | | | | | |

| Discovery Communications, Inc. Class A | | | (2,937 | ) | | | (72,661 | ) |

| CABLE & SATELLITE — (1.36)% | | | | | | | | |

| Sirius XM Holdings, Inc. | | | (98,861 | ) | | | (564,496 | ) |

| GOLD — (4.01)% | | | | | | | | |

| Barrick Gold Corporation (b) | | | (123,393 | ) | | | (1,670,741 | ) |

| INTERNET & DIRECT | | | | | | | | |

| MARKETING RETAIL — (7.56)% | | | | | | | | |

| Alibaba Group Holding Ltd. — ADR | | | (22,975 | ) | | | (3,149,183 | ) |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

| | | Shares | | | Value | |

| INTERNET SERVICES | | | | | | |

| & INFRASTRUCTURE — (0.10)% | | | | | | |

| Twilio, Inc. Class A | | | (478 | ) | | $ | (42,686 | ) |

| MANAGED HEALTH CARE — (0.00)% | | | | | | | | |

| Cigna Corporation | | | (1 | ) | | | (190 | ) |

| MOVIES & ENTERTAINMENT — (0.35)% | | | | | | | | |

| The Walt Disney Company | | | (1,324 | ) | | | (145,177 | ) |

| MULTI-UTILITIES — (3.54)% | | | | | | | | |

| Dominion Energy, Inc. | | | (20,656 | ) | | | (1,476,078 | ) |

| OIL & GAS STORAGE | | | | | | | | |

| & TRANSPORTATION — (0.05)% | | | | | | | | |

| Enbridge, Inc. (b) | | | (278 | ) | | | (8,640 | ) |

| EnLink Midstream LLC | | | (1,135 | ) | | | (10,771 | ) |

| | | | | | | | (19,411 | ) |

| PHARMACEUTICALS — (0.21)% | | | | | | | | |

| Takeda Pharmaceutical Company Ltd. (b)(f) | | | (325 | ) | | | (10,933 | ) |

| Takeda Pharmaceutical Company Ltd. — ADR | | | (4,544 | ) | | | (76,430 | ) |

| | | | | | | | (87,363 | ) |

| REITs — (0.27)% | | | | | | | | |

| Brookfield Property Partners LP (b) | | | (6,863 | ) | | | (110,632 | ) |

| SEMICONDUCTORS — (0.42)% | | | | | | | | |

| KLA-Tenor Corporation | | | (1,949 | ) | | | (174,416 | ) |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Proceeds $7,934,684) | | | | | | | (7,893,267 | ) |

| | | | | | | | | |

| PRIVATE PLACEMENTS — (0.70)% (f) | | | | | | | | |

| Twenty-First Century Fox, Inc. Class A | | | (9,072 | ) | | | (290,871 | ) |

| TOTAL PRIVATE PLACEMENTS | | | | | | | | |

| (Proceeds $302,355) | | | | | | | (290,871 | ) |

| TOTAL SHORT INVESTMENTS | | | | | | | | |

| (Proceeds $8,237,039) — (19.65)% | | | | | | | (8,184,138 | ) |

| TOTAL NET INVESTMENTS | | | | | | | | |

| (Cost $33,097,346) — 78.67% | | | | | | | 32,765,213 | |

| OTHER ASSETS IN EXCESS | | | | | | | | |

| OF LIABILITIES — 21.33% | | | | | | | 8,882,947 | |

| TOTAL NET ASSETS — 100.00% | | | | | | $ | 41,648,160 | |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

December 31, 2018

ADR – American Depository Receipt

ETF – Exchange-Traded Fund

LIBOR – London Interbank Offered Rate

plc – Public Limited Company

REITs – Real Estate Investment Trusts

| (a) | Non-income producing security. |

| (b) | Foreign security. |

| (c) | The rate quoted is the annualized seven-day yield as of December 31, 2018. |

| (d) | Security fair valued by the Valuation Group in good faith in accordance with the policies adopted by the Board of Trustees. |

| (e) | All or a portion of the shares have been committed as collateral for open securities sold short, written option contracts, swap contracts, and forward currency exchange contracts. |

| (f) | Level 2 Security. Please see Note 2 in the Notes to the Financial Statements for more information. |

| (g) | Level 3 Security. Please see Note 2 in the Notes to the Financial Statements for more information. |

| (h) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration normally to qualified institutional buyers. As of December 31, 2018, these securities represent 3.53% of total net assets. |

| (i) | Restricted security. The Fund may own investment securities that have other legal or contractual limitations, and thus are restricted as to resale. These securities are valued by the Valuation Group under the supervision of the Board of Trustees. As of December 31, 2018, this common stock had a cost of $428,231 and its market value represented 1.07% of total net assets. The Fund’s adviser perfected its appraisal rights over this security as of 6/20/2016. Please see Note 2 in the Notes to the Financial Statements for more information. |

| (j) | The coupon rate shown on variable rate securities represents the rate as of December 31, 2018. |

| (k) | This security is held in connection with a written option contract. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by Fund Services.

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

Open Written Options

December 31, 2018

| | | Contracts | | | | | | | |

| | | (100 shares | | | Notional | | | | |

| | | per contract) | | | Amount | | | Value | |

| WRITTEN CALL OPTIONS | | | | | | | | | |

| AT&T, Inc. | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | |

| Exercise Price: $31.00 | | | (14 | ) | | $ | (39,956 | ) | | $ | (56 | ) |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $32.00 | | | (14 | ) | | | (39,956 | ) | | | (42 | ) |

| DowDuPont, Inc. | | | | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $60.00 | | | (4 | ) | | | (21,392 | ) | | | (24 | ) |

| Expiration: February 2019, | | | | | | | | | | | | |

| Exercise Price: $50.00 | | | (74 | ) | | | (395,752 | ) | | | (36,630 | ) |

| SPDR S&P 500 ETF Trust | | | | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $260.00 | | | (18 | ) | | | (449,856 | ) | | | (2,430 | ) |

| The Walt Disney Company | | | | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $115.00 | | | (77 | ) | | | (844,305 | ) | | | (4,389 | ) |

| | | | | | | | | | | | (43,571 | ) |

| WRITTEN PUT OPTIONS | | | | | | | | | | | | |

| SPDR S&P 500 ETF Trust | | | | | | | | | | | | |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $230.00 | | | (17 | ) | | | (424,864 | ) | | | (1,513 | ) |

| Expiration: January 2019, | | | | | | | | | | | | |

| Exercise Price: $240.00 | | | (6 | ) | | | (149,952 | ) | | | (1,302 | ) |

| | | | | | | | | | | | (2,815 | ) |

| TOTAL WRITTEN OPTIONS | | | | | | | | | | | | |

| (Premiums received $69,854) | | | | | | | | | | $ | (46,386 | ) |

ETF – Exchange-Traded Fund

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

Forward Currency Exchange Contracts

December 31, 2018

| | | | | | | | | USD Value at | | | | | | | USD Value at | | | Unrealized | |

| Settlement | | | | Currency to | | December 31, | | | Currency to | | December 31, | | | Appreciation | |

| Date | | Counterparty | | be Delivered | | 2018 | | | be Received | | 2018 | | | (Depreciation)* | |

| 1/16/19 | | JPM | | | 85,099 | | CAD | | $ | 62,362 | | | | 65,718 | | USD | | $ | 65,718 | | | $ | 3,356 | |

| 1/3/19 | | JPM | | | 499,652 | | EUR | | | 572,616 | | | | 577,163 | | USD | | | 577,163 | | | | 4,547 | |

| 1/3/19 | | JPM | | | 33,711 | | USD | | | 33,711 | | | | 29,274 | | EUR | | | 33,549 | | | | (162 | ) |

| 2/20/19 | | JPM | | | 63,745 | | EUR | | | 73,351 | | | | 73,244 | | USD | | | 73,244 | | | | (107 | ) |

| 3/21/19 | | JPM | | | 268,899 | | EUR | | | 310,191 | | | | 319,524 | | USD | | | 319,524 | | | | 9,333 | |

| 3/21/19 | | JPM | | | 256,303 | | USD | | | 256,303 | | | | 217,435 | | EUR | | | 250,824 | | | | (5,479 | ) |

| | | | | | | | | | $ | 1,308,534 | | | | | | | | $ | 1,320,022 | | | $ | 11,488 | |

CAD – Canadian Dollar

EUR – Euro

JPM – JPMorgan Chase & Co., Inc.

USD – U.S. Dollar

| * | Net unrealized appreciation (depreciation) is a receivable (payable). |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

SCHEDULE OF INVESTMENTS (continued)

Open Swap Contracts

December 31, 2018

| | | | | | | Pay/Receive | | | | | | | | | | | | | |

| | | | | | | on | | | | | | | | | | | | Unrealized | |

| Counter- | | | | Termination | | Financing | | | | Payment | | | | | Notional | | | Appreciation | |

| party | | Security | | Date | | Rate | | Financing Rate | | Frequency | | Shares | | | Amount | | | (Depreciation)* | |

| LONG TOTAL RETURN SWAP CONTRACTS | | | | | | | | | | | | | | | |

| JPM | | Ci:z Holdings Company Ltd. | | 12/28/19 | | Pay | | 0.400% +3 Month LIBOR | | Quarterly | | 10 | | | $ | 527 | | | $ | 10 | |

| BAML | | Gemalto NV | | 5/31/19 | | Pay | | 0.350% +1 Month LIBOR | | Monthly | | 9,220 | | | | 538,171 | | | | (3,520 | ) |

| JPM | | Innogy SE | | 7/18/19 | | Pay | | 0.400% +3 Month LIBOR | | Quarterly | | 1,350 | | | | 57,650 | | | | 5,274 | |

| JPM | | Man SE | | 11/8/19 | | Pay | | 0.400% +3 Month LIBOR | | Quarterly | | 706 | | | | 72,589 | | | | 237 | |

| BAML | | Shire plc | | 6/29/19 | | Pay | | 0.800% +1 Month LIBOR | | Monthly | | 14,448 | | | | 832,433 | | | | 4,218 | |

| JPM | | Shire plc | | 9/28/19 | | Pay | | 0.300% +3 Month LIBOR | | Quarterly | | 286 | | | | 17,410 | | | | (858 | ) |

| GS | | Shire plc | | 12/7/19 | | Pay | | 0.500% +1 Month LIBOR | | Monthly | | 7,904 | | | | 457,683 | | | | (351 | ) |

| | | | | | | | | | | | | | | | | | | | | | |

| SHORT TOTAL RETURN SWAP CONTRACTS | | | | | | | | | | | | | | | | | |

| BAML | | Brookfield Property | | | | | | | | | | | | | | | | | | | |

| | | Partners LP | | 3/28/19 | | Pay | | (4.500)% +1 Month LIBOR | | Monthly | | (1,550 | ) | | | (28,935 | ) | | | 3,934 | |

| JPM | | Takeda Pharmaceutical | | | | | | | | | | | | | | | | | | | |

| | | Company Ltd. | | 8/17/19 | | Pay | | (5.250)% +3 Month LIBOR | | Quarterly | | (1,815 | ) | | | (75,869 | ) | | | 14,747 | |

| BAML | | Takeda Pharmaceutical | | | | | | | | | | | | | | | | | | | |

| | | Company Ltd. | | 12/7/19 | | Pay | | (4.500)% +1 Month LIBOR | | Monthly | | (12,924 | ) | | | (540,001 | ) | | | 104,850 | |

| GS | | Takeda Pharmaceutical | | | | | | | | | | | | | | | | | | | |

| | | Company Ltd. | | 12/7/19 | | Pay | | (5.000)% +1 Month LIBOR | | Monthly | | (6,308 | ) | | | (213,573 | ) | | | 747 | |

| | | | | | | | | | | | | | | | | | | | $ | 129,288 | |

BAML – Bank of America Merrill Lynch & Co., Inc.

GS – Goldman, Sachs & Co.

JPM – JPMorgan Chase & Co., Inc.

LIBOR – London Interbank Offered Rate

plc – Public Limited Company

| * | Based on the net swap value held at each counterparty, unrealized appreciation (depreciation) is a receivable (payable). |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

STATEMENT OF ASSETS AND LIABILITIES

December 31, 2018

| ASSETS: | | | | | | |

| Investments, at value (Cost $41,334,385) | | | | | $ | 40,949,351 | |

| Deposits at brokers for securities sold short | | | | | | 8,237,039 | |

| Deposits at brokers for other investments | | | | | | 1,121,112 | |

| Receivable for forward currency exchange contracts | | | | | | 11,488 | |

| Receivable for swap contracts | | | | | | 129,288 | |

| Receivable for investments sold | | | | | | 696,557 | |

| Dividends and interest receivable | | | | | | 96,492 | |

| Receivable for fund shares issued | | | | | | 73,675 | |

| Prepaid expenses and other receivables | | | | | | 258 | |

| Total Assets | | | | | | 51,315,260 | |

| LIABILITIES: | | | | | | | |

| Securities sold short, at value (Proceeds of $8,237,039) | | $ | 8,184,138 | | | | | |

| Written option contracts, at value | | | | | | | | |

| (Premiums received $69,854) | | | 46,386 | | | | | |

| Payable for investments purchased | | | 1,353,974 | | | | | |

| Payable to the investment adviser | | | 17,268 | | | | | |

| Payable for fund shares redeemed | | | 1,767 | | | | | |

| Dividends payable | | | 1,609 | | | | | |

| Accrued expenses and other liabilities | | | 61,958 | | | | | |

| Total Liabilities | | | | | | | 9,667,100 | |

| NET ASSETS | | | | | | $ | 41,648,160 | |

| NET ASSETS CONSISTS OF: | | | | | | | | |

| Paid-in capital | | | | | | $ | 39,835,684 | |

| Distributable earnings | | | | | | | 1,812,476 | |

| Total Net Assets | | | | | | $ | 41,648,160 | |

| | | | | | | | | |

| NET ASSET VALUE and offering price per share* | | | | | | | | |

| ($41,648,160 / 3,666,774 shares of | | | | | | | | |

| beneficial interest outstanding) | | | | | | $ | 11.36 | |

| * | The redemption price per share may vary based on the length of time a shareholder holds Fund shares. |

The accompanying notes are an integral part of these financial statements.

The Merger Fund VL

STATEMENT OF OPERATIONS

For the Year Ended December 31, 2018

| INVESTMENT INCOME: | | | | | | |

| Interest | | | | | $ | 377,799 | |

| Dividend income on long positions | | | | | | | |

| (net of foreign withholding taxes of $483) | | | | | | 680,499 | |

| Total investment income | | | | | | 1,058,298 | |

| EXPENSES: | | | | | | | |

| Investment advisory fees | | $ | 434,792 | | | | | |

| Transfer agent and shareholder servicing agent fees | | | 91,221 | | | | | |

| Professional fees | | | 90,900 | | | | | |

| Fund accounting expenses | | | 43,381 | | | | | |

| Administration fees | | | 38,918 | | | | | |

| Reports to shareholders | | | 13,255 | | | | | |

| Trustees’ fees and expenses | | | 13,157 | | | | | |

| Custody fees | | | 10,823 | | | | | |

| Compliance fees | | | 2,607 | | | | | |

| Miscellaneous expenses | | | 2,589 | | | | | |

| Federal and state registration fees | | | 802 | | | | | |

| Borrowing expenses on securities sold short | | | 58,895 | | | | | |

| Dividends on securities sold short | | | 93,789 | | | | | |

| Total expenses before expense reimbursement by adviser | | | | | | | 895,129 | |

| Expense reimbursed by adviser (Note 3) | | | | | | | (255,478 | ) |

| Net expenses | | | | | | | 639,651 | |

| NET INVESTMENT INCOME | | | | | | | 418,647 | |

| REALIZED AND CHANGE IN UNREALIZED | | | | | | | | |

| GAIN (LOSS) ON INVESTMENTS: | | | | | | | | |

| Realized gain (loss) on: | | | | | | | | |

| Investments | | | 786,770 | | | | | |

| Securities sold short | | | (13,422 | ) | | | | |

| Written option contracts expired or closed | | | 117,637 | | | | | |

| Forward currency exchange contracts | | | 115,718 | | | | | |

| Swap contracts | | | 1,159,697 | | | | | |

| Foreign currency transactions | | | (6,289 | ) | | | | |

| Net realized gain | | | | | | | 2,160,111 | |

| Change in unrealized appreciation (depreciation) on: | | | | | | | | |

| Investments | | | (1,508,617 | ) | | | | |

| Securities sold short | | | 1,353,334 | | | | | |

| Written option contracts | | | 89,729 | | | | | |

| Forward currency exchange contracts | | | 59,670 | | | | | |

| Swap contracts | | | (123,866 | ) | | | | |

| Foreign currency translation | | | (2 | ) | | | | |

| Net change in unrealized depreciation | | | | | | | (129,752 | ) |

| NET REALIZED AND CHANGE IN UNREALIZED | | | | | | | | |

| GAIN ON INVESTMENTS | | | | | | | 2,030,359 | |

| NET INCREASE IN NET ASSETS | | | | | | | | |

| RESULTING FROM OPERATIONS | | | | | | $ | 2,449,006 | |