Exhibit 99.2

Telkom SA Limited

Group Annual Results

for the year ended March 31, 2008

for the year ended March 31, 2008

June 9, 2008

Changing the way we do business

Cautionary statement on forward looking statements

All of the statements included in this document, as well as oral statements that may be made by us or by officers, directors or employees acting on

behalf of us, that are not statements of historical facts, including but not limited to financial targets and prospects, constitute or are based on

forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995, specifically Section 27A of the US

Securities Act of 1933, as amended, and Section 21E of the US Securities Exchange Act of 1934, as amended. These forward-looking statements

involve a number of known and unknown risks, uncertainties and other factors that could cause our actual results and outcomes to be materially

different from historical results or from any future results expressed or implied by such forward-looking statements. Among the factors that could

cause our actual results or outcomes to differ materially from our expectations are those risks identified in Item 3. “Key Information-Risk Factors,” of

Telkom’s most recent Annual Report on Form 20-F filed with the US Securities and Exchange Commission (SEC) and its other filings and

submissions with the SEC which are available on Telkom’s website at www.telkom.co.za/ir, including, but not limited to, any changes to our mobile

strategy and Vodacom holdings and our ability to impact such strategy and organizational changes thereto, increased competition in the South

African fixed-line, mobile and data communications markets; our ability to implement our strategy of transforming from basic voice and data

connectivity to fully converged solutions, developments in the regulatory environment; continued mobile growth and reductions in Vodacom’s and

Telkom’s net interconnect margins; Telkom’s and Vodacom’s ability to expand their operations and make investments and acquisitions in other

African countries and the general economic, political, social and legal conditions in South Africa and in other countries where Telkom and Vodacom

invest; our ability to improve and maintain our management information and other systems; our ability to attract and retain key personnel and

partners; our inability to appoint a majority of Vodacom’s directors and the consensus approval rights at Vodacom may limit our flexibility and ability

to implement our preferred strategies; Vodacom’s continued payment of dividends or distributions to us; our negative working capital; changes in

technology and delays in the implementation of new technologies; our ability to reduce theft, vandalism, network and payphone fraud and lost

revenue to non-licensed operators; the amount of damages Telkom is ultimately required to pay to Telcordia Technologies Incorporated; the

outcome of regulatory, legal and arbitration proceedings, including tariff approvals, and the outcome of Telkom’s hearings before the Competition

Commission and others; any requirements that we unbundle the local loop, our ability to negotiate favorable terms, rates and conditions for the

provision of interconnection services and facilities leasing services or if ICASA finds that we or Vodacom have significant market power or otherwise

imposes unfavorable terms and conditions on us; our ability to implement and recover the substantial capital and operational costs associated with

carrier pre-selection, number portability and the monitoring, interception and customer registration requirements contained in the South African

Regulation of Interception of Communications and Provisions of Communication-Related Information Act and the impact of these requirements on

our business; Telkom’s ability to comply with the South African Public Finance Management Act and South African Public Audit Act and the impact

of the Municipal Property Rates Act; fluctuations in the value of the Rand and inflation rates; the impact of unemployment, poverty, crime, HIV

infection, labor laws and labor relations, exchange control restrictions, and power outages in South Africa; and other matters not yet known to us or

not currently considered material by us.

behalf of us, that are not statements of historical facts, including but not limited to financial targets and prospects, constitute or are based on

forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995, specifically Section 27A of the US

Securities Act of 1933, as amended, and Section 21E of the US Securities Exchange Act of 1934, as amended. These forward-looking statements

involve a number of known and unknown risks, uncertainties and other factors that could cause our actual results and outcomes to be materially

different from historical results or from any future results expressed or implied by such forward-looking statements. Among the factors that could

cause our actual results or outcomes to differ materially from our expectations are those risks identified in Item 3. “Key Information-Risk Factors,” of

Telkom’s most recent Annual Report on Form 20-F filed with the US Securities and Exchange Commission (SEC) and its other filings and

submissions with the SEC which are available on Telkom’s website at www.telkom.co.za/ir, including, but not limited to, any changes to our mobile

strategy and Vodacom holdings and our ability to impact such strategy and organizational changes thereto, increased competition in the South

African fixed-line, mobile and data communications markets; our ability to implement our strategy of transforming from basic voice and data

connectivity to fully converged solutions, developments in the regulatory environment; continued mobile growth and reductions in Vodacom’s and

Telkom’s net interconnect margins; Telkom’s and Vodacom’s ability to expand their operations and make investments and acquisitions in other

African countries and the general economic, political, social and legal conditions in South Africa and in other countries where Telkom and Vodacom

invest; our ability to improve and maintain our management information and other systems; our ability to attract and retain key personnel and

partners; our inability to appoint a majority of Vodacom’s directors and the consensus approval rights at Vodacom may limit our flexibility and ability

to implement our preferred strategies; Vodacom’s continued payment of dividends or distributions to us; our negative working capital; changes in

technology and delays in the implementation of new technologies; our ability to reduce theft, vandalism, network and payphone fraud and lost

revenue to non-licensed operators; the amount of damages Telkom is ultimately required to pay to Telcordia Technologies Incorporated; the

outcome of regulatory, legal and arbitration proceedings, including tariff approvals, and the outcome of Telkom’s hearings before the Competition

Commission and others; any requirements that we unbundle the local loop, our ability to negotiate favorable terms, rates and conditions for the

provision of interconnection services and facilities leasing services or if ICASA finds that we or Vodacom have significant market power or otherwise

imposes unfavorable terms and conditions on us; our ability to implement and recover the substantial capital and operational costs associated with

carrier pre-selection, number portability and the monitoring, interception and customer registration requirements contained in the South African

Regulation of Interception of Communications and Provisions of Communication-Related Information Act and the impact of these requirements on

our business; Telkom’s ability to comply with the South African Public Finance Management Act and South African Public Audit Act and the impact

of the Municipal Property Rates Act; fluctuations in the value of the Rand and inflation rates; the impact of unemployment, poverty, crime, HIV

infection, labor laws and labor relations, exchange control restrictions, and power outages in South Africa; and other matters not yet known to us or

not currently considered material by us.

We caution you not to place undue reliance on these forward-looking statements. All written and oral forward-looking statements attributable to us,

or persons acting on our behalf, are qualified in their entirety by these cautionary statements. Moreover, unless we are required by law to update

these statements, we will not necessarily update any of these statements after the date hereof, either to confirm them to actual results or to changes

in our expectation.

or persons acting on our behalf, are qualified in their entirety by these cautionary statements. Moreover, unless we are required by law to update

these statements, we will not necessarily update any of these statements after the date hereof, either to confirm them to actual results or to changes

in our expectation.

2

Reuben September

Overview

Financial summary

• Group operating revenue increased by 9.0% to

R56.3 billion

R56.3 billion

• Group EBITDA increased by 4.2% to R20.6 billion

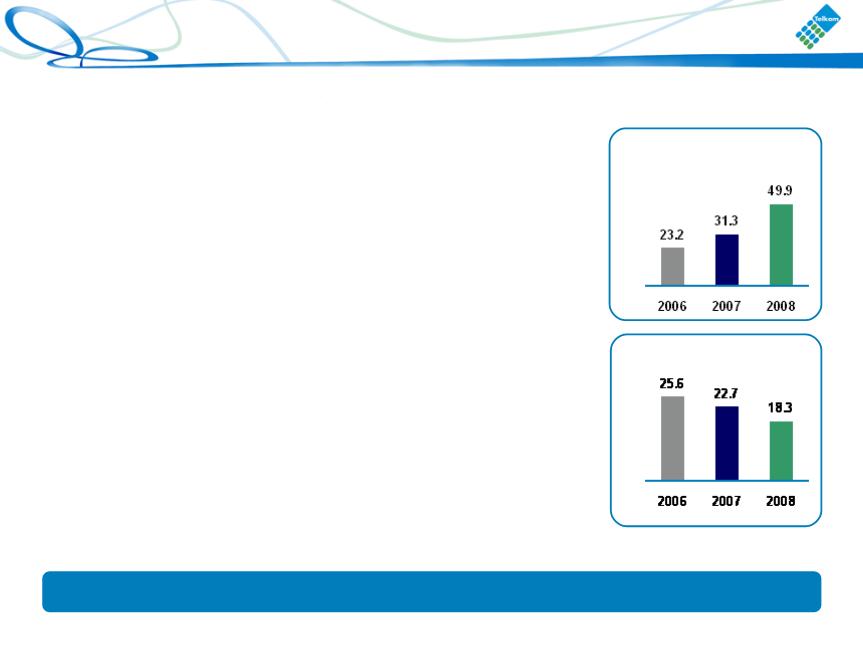

• Net debt to equity increased to 49.9% from 31.3%

at March 31, 2007

at March 31, 2007

• Cash generated from operations increased by

3.6% to R21.1 billion

3.6% to R21.1 billion

• HEPS decreased by 4.0% to 1634.5 cents

per share

per share

• Ordinary dividend increased by 10.0% to

660 cents per share payable on July 7, 2008

660 cents per share payable on July 7, 2008

• No special dividend declared - investing in

South African and African operations

South African and African operations

4

Strategy overview - defend and grow

Changing the way we do business

Fixed Mobile

Geographic

Data

• Core strategy remains defend

and grow

and grow

• Telkom continues to move up

the value added data services

chain

the value added data services

chain

• We continue to pursue

acquisition opportunities in fast

growing emerging markets

acquisition opportunities in fast

growing emerging markets

• We aim to establish Telkom as a

regional ICT player

regional ICT player

• Leveraging our core strengths to

be a full play service provider

be a full play service provider

5

Traditional voice

• Annuity revenue increased 14.1% to R6.9 billion

• Telkom Closer packages increased 63.3% to 471,742

• Supreme call packages increased 121.4% to 12,777

• Term & Volume discount plans of R3.4 billion signed in FY2008

Defensive strategies are successful

• Continue converting revenue streams to

annuity revenues

annuity revenues

• Bundling call minutes with access line rental

in attractive subscription based value

propositions

in attractive subscription based value

propositions

6

*

Pricing initiatives

• Offering value-based calling plans

• Rebalancing tariffs to reduce arbitrage opportunities

• Driving the penetration of bundles to increase annuity based revenues

Offering value to remain competitive

7

Data

• Data revenues climbed 10.9% to R8.3 billion

• Focus on innovative products such as VPN Lite

• Ethos of innovation and speed to market being fostered

Data connectivity | Rbn4.5 | 4.5% |

Mobile leased lines | Rbn1.9 | 11.1% |

Internet access | Rbn1.2 | 29.1% |

Managed network services | Rm728.5 | 36.2% |

VPN services | Rm500.0 | 46.6% |

Data continues to grow in importance

8

Data centre business

• Increase Telkom’s share of the ICT revenue pie

• Stimulate use of bandwidth over our network

• Towards one-stop solutions as IT and

telecommunications converge

telecommunications converge

• Regulators insisting that data is properly protected

• Improving efficiencies through shared resources

• Telkom is pursuing the acquisition of a data centre

business outside South Africa

business outside South Africa

Moving up the value added services data chain

9

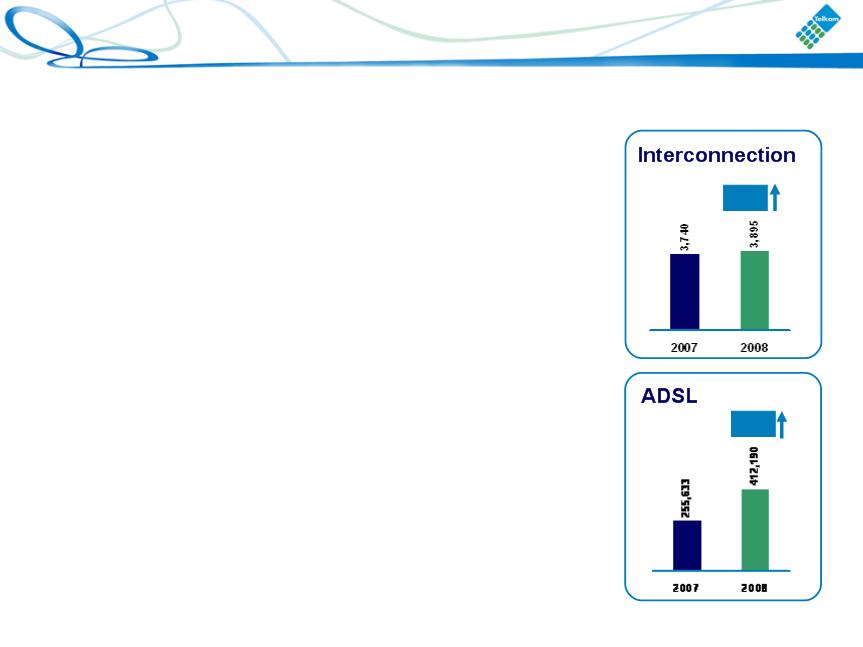

Broadband and converged services

• ADSL footprint now covering 92% of the network

• Coverage in township areas - 69%

• ADSL subscribers grown 61.2% to 412,190

• Do Broadband packages increased by 245.6% to

119,288

119,288

• Wholesale ADSL services have grown to 18,740 from

2,545 at September 2007

2,545 at September 2007

• ATTI has improved to 19 days from 23 days at

March 31, 2007

March 31, 2007

• 57% of all ADSL installation done through self-install

option

option

• Targeting 592,000 ADSL subscribers for FY 2009

Targeting ADSL penetration of 15% - 20% of fixed-access lines

by FY 2010/11

by FY 2010/11

10

Results to March 31, 2008

• Revenue of R845.4 million

• Profit after tax - R49.0 million

• ARPU for 11 months ended March 31, 2008 - $32

• Subscribers at March 31, 2008 - 813,392

• Subscribers at May 31, 2008 - 1,000,251

Strong operational performance

11

Fast becoming a serious competitor in Nigeria

12

•Ability to deliver complex data products to corporates growing

• Planned capex expenditure

– Further Metro Ethernet rings to be build in

Abuja, Lagos, Kano, Kaduna and Delta

Abuja, Lagos, Kano, Kaduna and Delta

– Six NGN nodes to be built during FY 2009

• Aggressively pursuing opportunities in the

growing markets of Nigeria

growing markets of Nigeria

13

• Targeted EBITDA margin range 17% - 22% at March 31, 2009

• Targeted base station growth 2009 - 1,150

• Targeted fibre deployment 2009 - 2,000km

• Targeted customer growth 2009 - 3.5 million

Multi-Links will be substantial contributor to Telkom

14

Ghana

Namibia

Swaziland

Zimbabwe

Uganda

Tanzania

Cote D’Ivoire

Kenya

Small company with big opportunities

15

Telkom Management Services Company

• Opportunities in sub-Saharan Africa for reputable

operator to provide management services

operator to provide management services

• Target market - -

– State owned incumbent operators

– Numerous new entrants in ICT industry

• Telkom has first hand experience of privatisation

• Leveraging experience with technology innovation,

equipment manufacturers, operator support

systems, business planning, support services and

IT solutions

equipment manufacturers, operator support

systems, business planning, support services and

IT solutions

TMSC will provide total management solutions

16

Potential corporate action announced on June 2, 2008

Binding proposals subject to requisite shareholder approval

• Proposal received from Vodafone:

– Vodafone would acquire a portion of Telkom’s stake in Vodacom; and

– Telkom would unbundle its remaining shareholding in Vodacom to Telkom

shareholders

shareholders

• Letter received from consortium lead by Mvelaphanda Holdings

– Consortium is considering making an offer for the entire issued share capital

of Telkom;

of Telkom;

– Offer will only be made if a number of pre-conditions are met;

– Proposal contemplates that Telkom will unbundle or sell its entire 50% stake

in Vodacom;

in Vodacom;

– In effect, the Consortium would acquire Telkom’s fixed line business

– Vodafone discussions are independent from the approach from the Consortium

• Telkom aims to continuously and expeditiously seek ways to unlock value

• To this end:

– Board and management evaluating the above proposals;

– Discussions are being held and clarifications are being obtained;

– Further announcement will be made when appropriate

17

Fixed mobile and mobile data network

Getting ready to compete aggressively

• W-CDMA, capable of full mobility, to be deployed

in selective areas

in selective areas

• Huawei approved as exclusive vendor - scale

benefits with Multi-Links

benefits with Multi-Links

• Alleviate losses and service impacts of theft,

breakages and incidences

breakages and incidences

• Replacing high cost of copper in vulnerable areas

• Business case - R1.7 billion over 3 years with IRR

in excess of 20%

in excess of 20%

• First customers to be connected in September

2008

2008

18

Key NGN and capacity achievements

• 84 Metro Ethernet nodes deployed

• Dense Wave Division Multiplexing System deployed between Gauteng and

Durban - - significant increase in transport bandwidth capability

Durban - - significant increase in transport bandwidth capability

• Automatic self-healing rerouting of bandwidth has commenced

• National and local bandwidth increased by 1.2 Tbit/s - 21% increase

• International bandwidth increased to 4.5 Gbit/s - 88% increase

• 41% increase in bandwidth on ATM network

• National IP network bandwidth increased to 32.2 Gbit/s - 11% increase

• Diginet and Diginet Plus has increased to 27 Gbit/s - 20% increase

• 237 WiFi hotspots deployed

• WiMax - 56 base stations now installed

Telkom fulfilling commitment to dramatically increase bandwidth

19

Capability management

No need to own resources in order to use them

• Redesign of Telkom’s operations model to address rapidly changing technology,

speed of technology deployment and fluctuating demand in the most cost

efficient manner

speed of technology deployment and fluctuating demand in the most cost

efficient manner

• Includes outsourcing, out-tasking, consolidation and in-tasking

• Aim is to:

– Increase focus on customer service

– Deliver new differentiated services to the market faster

– Facilitate smoother and more rapid technology transition

– Facilitate risk and benefit sharing model

– Complete roll-out over two years

• Sustained employability and wellbeing of Telkom staff is of paramount importance

20

Capability management (cont.)

Moving towards a nimble, efficient organisation

• Capability management is in progress

– Commenced with issuing closed request for proposals for the

provisioning of professional services

provisioning of professional services

– Information sharing with unions started in July 2007, consultation

in April 2008

in April 2008

– Joint union and management team conducted benchmark studies

in Germany, Australia, New Zealand and Brazil

in Germany, Australia, New Zealand and Brazil

• Reducing number of contractors providing similar services currently

– Commenced with service provider consolidation process

21

Customer service quality improvement initiatives

Call Centre Operations - improving customer service

• Restructured all call centres under one structure

• Active traffic load distribution among call centres

• Selected single supplier of temporary staff

– Standardised remuneration

– Created temporary staff development path

• Automated credit note on theft affected services

• Enhanced alternate fault reporting via web

Vital to enhance customer service

22

Customer service quality improvement initiatives

Customer centricity starting to bear fruit

Focus on improving customer service

• Various initiatives in the Call Centres and Field

Operations resulted in:

Operations resulted in:

– Faults dropped from peak in February by 47%

– Reduction of theft by 15% from January

– Customer Fault Handling capacity improved

by 22%

by 22%

– ADSL call handling capacity improved by 37%

over last 3 months

over last 3 months

– Corporate fault management improved by 8%

– Corporate calls answered in 20 seconds

improved from 54% to 74%

improved from 54% to 74%

23

• On March 31, 2008 Telkom announced its intention to substantially

reduce its shareholding in Telkom Media

reduce its shareholding in Telkom Media

• A potential investor has been identified

• A definite proposal is expected to be received end June 2008

• Expansion of content rich services is crucial

• Content acts as a revenue driver and product differentiator in crowded

broadband market

broadband market

• Content can be sourced from other operators

Fast resolution of Telkom Media issue

24

Financial overview

Deon Fredericks

Group income statement

ZAR million | 2007 | 2008 | % | |

Operating revenue | 51,619 | 56,285 | 9.0 | |

Other income | 384 | 534 | 39.1 | |

Operating expenses | (37,533) | (42,337) | 12.8 | |

Operating profit | 14,470 | 14,482 | 0.1 | |

Investment income | 235 | 197 | 16.2 | |

EBITDA | 19,786 | 20,612 | 4.2 | |

Finance charges | (1,125) | (1,803) | 60.3 | |

Taxation | (4,731) | (4,704) | 0.6 | |

Net profit | 8,849 | 8,172 | (7.7) | |

Basic earnings per share (cents) | 1,681.0 | 1,565.0 | (6.9) | |

Dividend per share | 900.0 | 1,100 | 22.2 |

EBITDA margin

%

HEPS

Cents

Business environment changing - margin pressure continues

26

Group balance sheet

ZAR million | 2007 | 2008 | % | |

Non-current assets | 48,770 | 57,763 | 18.4 | |

Current assets | 10,376 | 12,609 | 21.5 | |

Total assets | 59,146 | 70,372 | 19.0 | |

Capital & reserves | 32,008 | 33,337 | 4.2 | |

Non-current liabilities | 8,554 | 15,104 | 76.6 | |

Current liabilities | 18,584 | 21,931 | 18.0 | |

Total equity & liabilities | 59,146 | 70,372 | 19.0 | |

Net debt | 10,026 | 16,617 | 65.7 |

50% net debt to equity

%

Balance sheet remains strong

18% return on assets

%

27

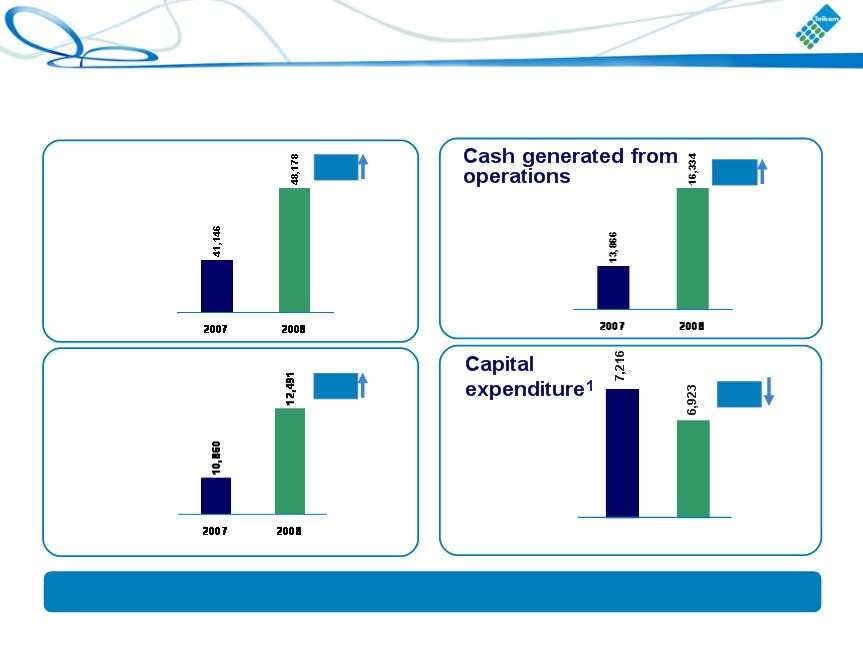

Group cash flow

ZAR millions | 2007 | 2008 | % |

Cash generated from operations | 20,520 | 21,256 | 3.6 |

Dividend paid | (4,784) | (5,732) | 19.8 |

Cash generated from operating activities | 9,356 | 10,603 | 13.3 |

Investing activities | 10,412 | (14,106) | 35.5 |

Financing activities | (2,920) | 2,943 | (200.8) |

Net increase/(decrease) in cash | (3,976) | (560) | (85.9) |

Cash at the end of the year | 308 | (208) | (167.5) |

Free cash flow | 3,728 | 2,150 | (42.3) |

Investing for future revenue growth

28

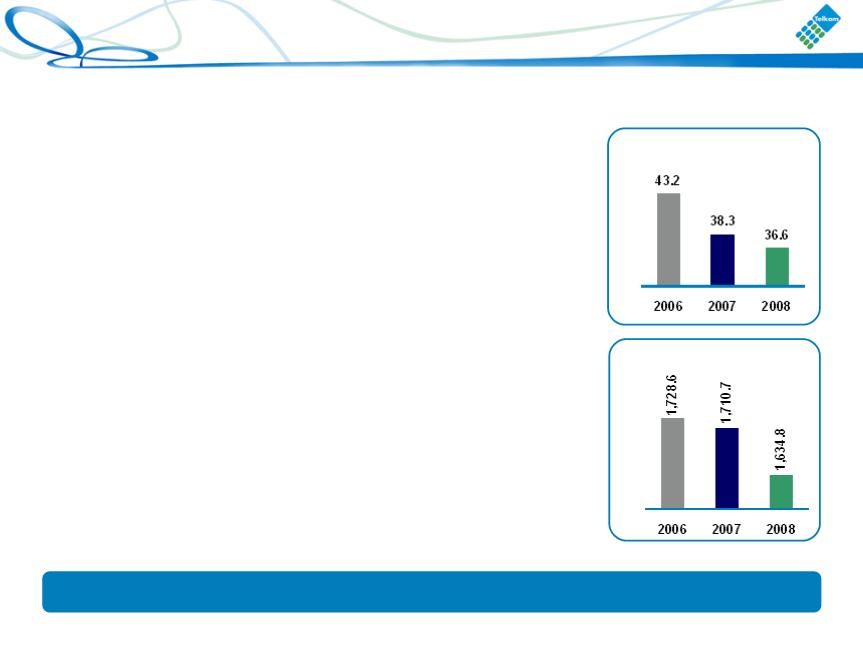

Segmental contribution

after inter-segmental eliminations

Operating revenue

Operating profit

EBITDA

Fixed line remains the major contributor

Mobile

Fixed-Line

Other

1%

38%

3%

56%

40%

3%

36%

29

Fixed-line income statement

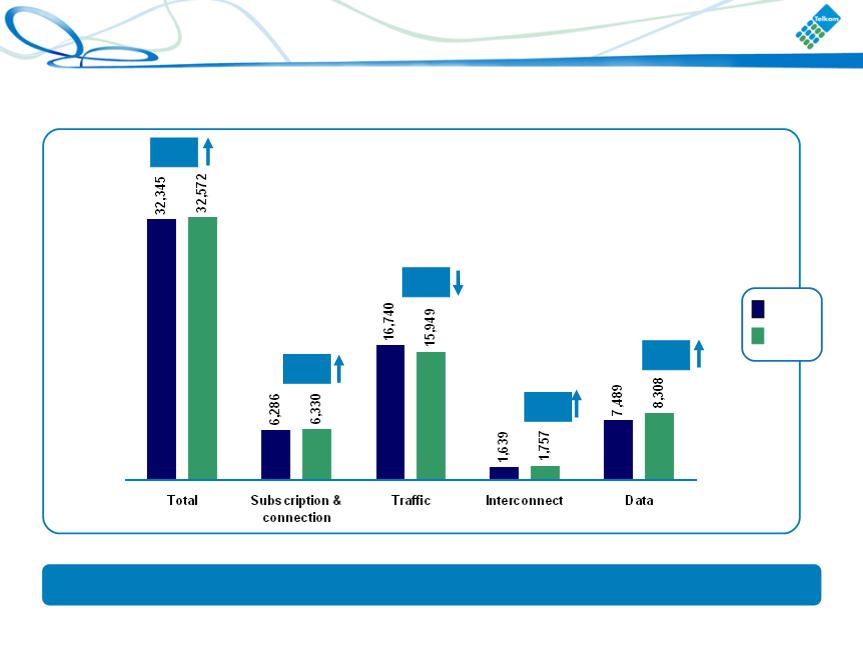

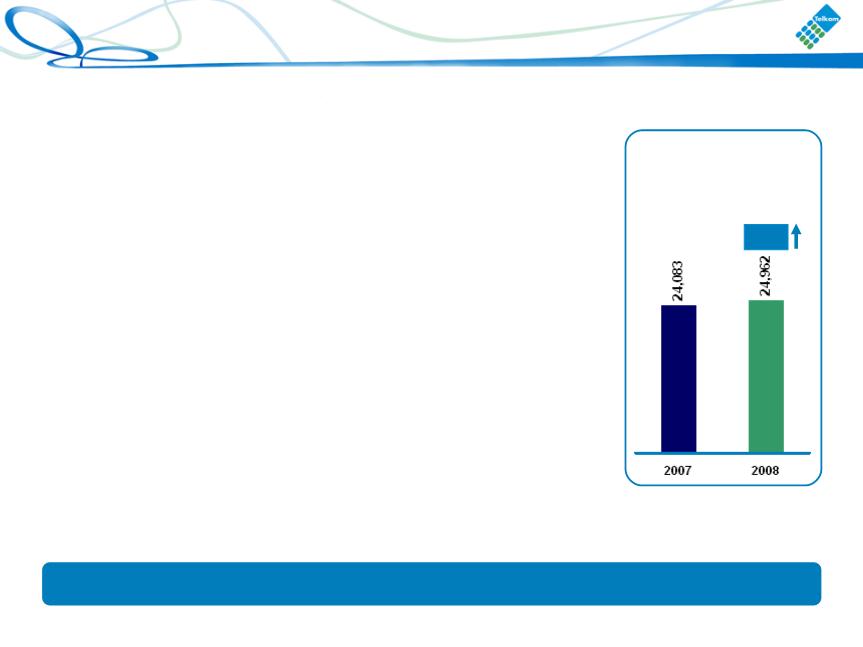

ZAR million | 2007 | 2008 | % | |

Operating revenue | 32,346 | 32,572 | 0.7 | |

Other income | 334 | 497 | 48.8 | |

Operating expenses | (24,083) | (24,962) | 3.6 | |

Operating profit | 8,597 | 8,107 | (5.7) | |

Investment income | 3,041 | 3,975 | 30.7 | |

EBITDA | 12,179 | 12,058 | (1.0) | |

Finance charges | (856) | (1,277) | 49.2 | |

Taxation | (2,652) | (2,630) | (0.8) | |

Net profit | 8,130 | 8,175 | 0.6 |

EBITDA margin

%

EBIT margin

%

Excluding Telkom Media provision - EBITDA margin 37%

30

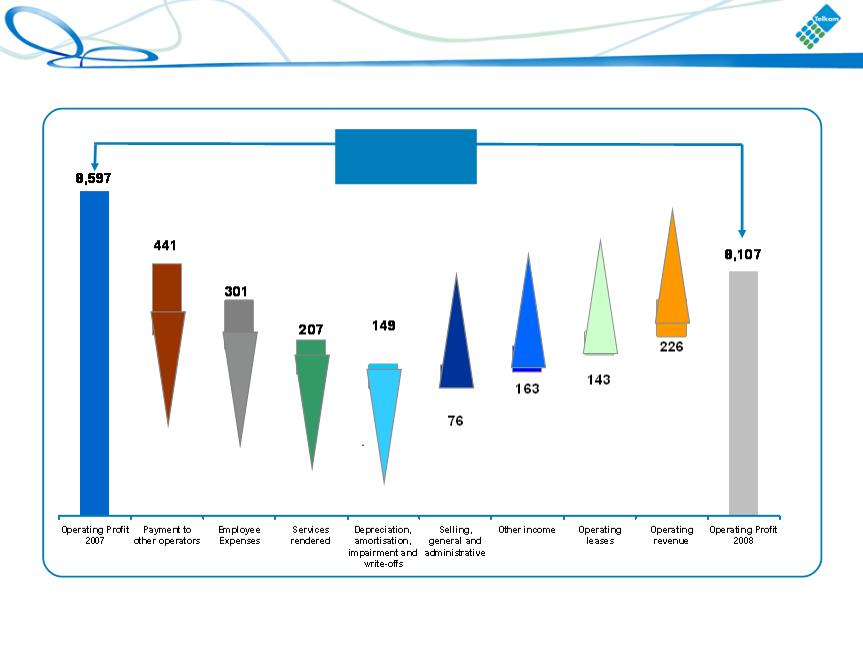

Fixed-line operating profit drivers

(R490 million)

ZAR million

31

Fixed-line revenue

ZAR million

7.2%

(4.7%)

0.7%

0.7%

10.9%

Strong data revenue growth

2007

2008

32

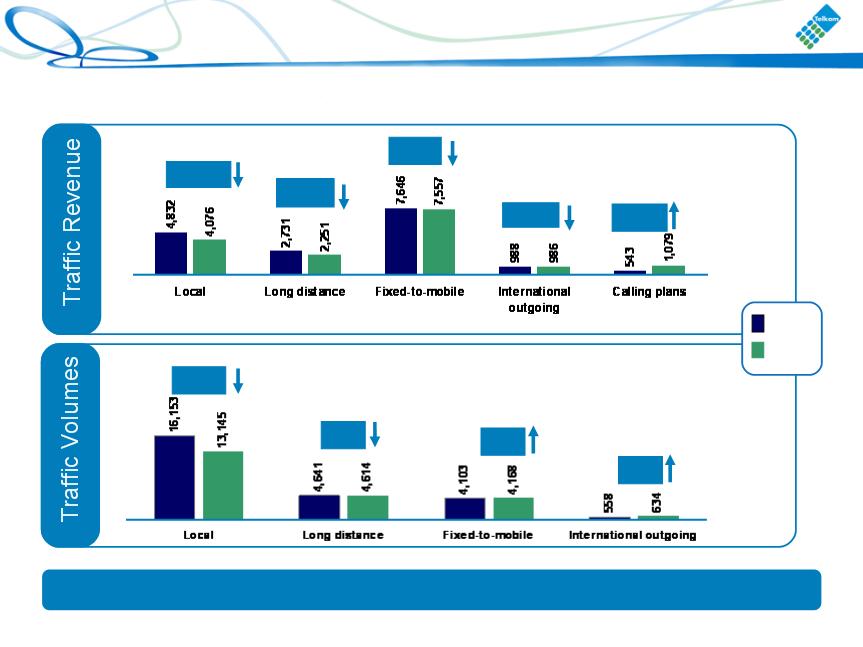

Fixed-line traffic

ZAR millions

Millions of minutes

(1.2%)

(15.6%)

(17.6%)

(0.2%)

(18.6)%

13.6%

(0.6%)

Traditional traffic declines, calling plans show strong growth

2007

2008

98.7%

1.6%

33

Fixed-line annuity revenue

ZAR millions | 2007 | 2008 | % |

Line rental | 4,503 | 4,731 | 5.1 |

Calling plans/packages | 543 | 1,079 | 98.7 |

CPE rental | 682 | 755 | 10.7 |

Value added services | 315 | 330 | 4.8 |

International other | 20 | 22 | 10.0 |

Total | 6,063 | 6,917 | 14.1 |

Recurring revenue continues to grow

• Annuity revenue includes all subscription revenue. It does not include usage or traffic related

revenue from calling plans/bundles, line installations, reconnection fees and CPE sales

revenue from calling plans/bundles, line installations, reconnection fees and CPE sales

34

Fixed-line revenue (continued)

ZAR millions | 2007 | 2008 | % |

Mobile | 816 | 838 | 2.7 |

Fixed domestic | 28 | - | |

International | 823 | 891 | 8.3 |

Interconnection revenue | 1,639 | 1,757 | 7.2 |

ZAR millions | 2007 | 2008 | % |

Leased lines | 5,825 | 6,460 | 10.9 |

Mobile leased facilities | 1,664 | 1,848 | 11.1 |

Data revenue | 7,489 | 8,308 | 10.9 |

Interconnection

Data

4.1%

61.2%

Millions of minutes

Subscribers

35

Fixed-line operating expenses

3.6%

ZAR millions | 2007 | 2008 | % |

Employee expenses | 7,096 | 7,397 | 4.2 |

Payments to other operators | 6,461 | 6,902 | 6.8 |

SG&A | 3,975 | 3,899 | (1.9) |

Services rendered | 2,206 | 2,413 | 9.4 |

Operating leases | 762 | 619 | (18.8) |

Depreciation, amortisation, impairment and write-offs | 3,583 | 3,732 | 4.2 |

Total

(Rm)

Operating expenses well contained in high inflationary environment

36

Fixed-line capex

ZAR millions | 2007 | 2008 | % |

Baseline expansion | 4,352 | 5,188 | 19.2 |

Sustainment | 416 | 277 | (33.4) |

Efficiencies & improvements | 1,141 | 841 | (26.3) |

Support | 501 | 451 | (10.0) |

Regulatory | 188 | 37 | (79.9) |

Total | 6,598 | 6,794 | 3.0 |

Telkom continues to build for the future

37

• Capex Plan of R30bn over 5 years from FY 2006 - FY 2010

• As at the end of the 2007/08 financial year R18,4bn (61%) of the R30bn

has been invested

has been invested

• An additional R2bn is planned for the last 2 years of the program

• The main drivers of the additional R2bn investment:

– FIFA 2010 requirements

– Fixed Wireless deployment

– International cable expansion

– Acceleration of a portion of the master plan

Investment in support of the strategy

Unpacking the R30bn 5 year capital expenditure program

38

Mobile financial highlights

Operating revenue

Operating profit

ZAR million

ZAR million

ZAR million

ZAR million

17.1%

17.8%

(4.0)%

15.0%

100% Vodacom (50% consolidated)

1. Including intangibles

Strong revenue growth

2007

2008

39

Leading the South African mobile market

Customers

ARPU1

Churn

Thousands

Thousands

ZAR

%

7.9%

10.9%

25.2%

1. Blended ARPU

ARPU remains stable

40

Performance in other African countries

ARPU1

ZAR

28%

30%

30%

25%

42%

1. Blended ARPU

Strong subscriber growth in African countries

2007

2008

41

Guidance for the next 3 financial years

Fixed-line and other

Constant revenue growth: CAGR to range between 5% - 10%

Capex to range between 23% and 27% of revenue over the

next 2 years and between 18% and 22% of revenue in the

2011 financial year

next 2 years and between 18% and 22% of revenue in the

2011 financial year

EBITDA margin to range between 32% and 36% - expect to see

improvement within the range towards the end of the 2011

financial year

improvement within the range towards the end of the 2011

financial year

Targeting net debt to EBITDA 1.3x

42

Thank you

Investor Relations

Nicola White

Tel: +27 12 311 5720

Fax: +27 12 311 5721

E-mail: whitenh@telkom.co.za

Telkom SA Limited

43