Semiannual Report

Franklin Mutual Recovery Fund

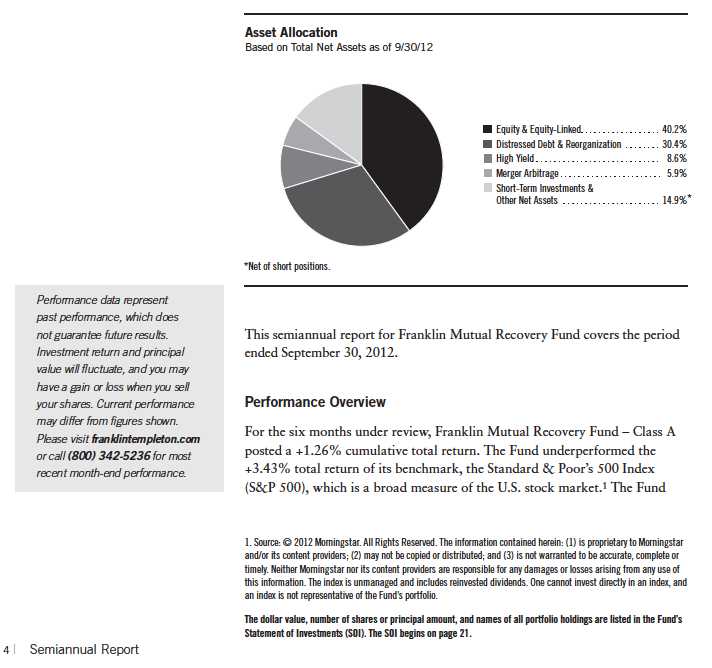

Your Fund s Goal and Main Investments: Franklin Mutual Recovery Fund s goal is capital appreciation. The Fund seeks to achieve superior risk-adjusted returns with a moderate correlation to U.S. equity markets by investing in distressed companies, merger arbitrage securities and special situation/undervalued securities. The Fund may take long and short positions, with the latter typically utilized in connection with the merger arbitrage strategy.

also underperformed the +1.94% total return of the Bloomberg/EFFAS U.S. Government 3-5 Years Total Return Index, which serves as a transparent benchmark for the U.S. government bond market.2

The performance of the Fund relative to the Bloomberg index is used as the basis for calculating the performance adjustment to the base management fee paid to the Fund s adviser. (Please refer to Notes 4a and 4f in the Notes to Financial Statements for additional information related to the performance adjustment and the base management fee.) You can find the Fund s long-term performance data in the Performance Summary beginning on page 12.

Economic and Market Overview

The U.S. economy, as measured by gross domestic product, grew at a modest rate during the six-month period ended September 30, 2012. Encouraging labor market and housing data as well as an expanding services sector helped offset a loss of momentum in the manufacturing sector, a major driver of the U.S. economy. The national unemployment rate declined from 8.2% at the beginning of the period to a 44-month low of 7.8% in September.3 Although prices of some key commodities increased during the period and contributed to higher producer prices, consumer price inflation remained fairly low.

The U.S. Federal Reserve Board (Fed) recognized significant headwinds to the pace of U.S. economic recovery, including the ongoing European fiscal and banking crisis and its potential spillover to U.S. financial markets and institutions, as well as signs of slowing global economic growth. In addition, the looming possibility that U.S. tax increases and government expenditure reductions would come into effect at the beginning of 2013 (the so-called fiscal cliff ) prompted many businesses to hold off on major investment and hiring decisions. Seeking to support a stronger economy, in September the Fed agreed to purchase additional mortgage-backed securities to provide further quantitative easing (QE3) and to continue extending the average maturity of its Treasury holdings (commonly called Operation Twist). The Fed also anticipated it would maintain historically low interest rates at least through mid-2015.

At the end of the reporting period, the U.S. presidential contest dominated headlines. Significant challenges to the U.S. economy remained, including an elevated although improved level of unemployment, lack of broad public and political agreement on how to achieve U.S. deficit reduction, and uncertainty surrounding deeply indebted European countries. Signs of China s economic

2. Source: Bloomberg LP.

3. Source: Bureau of Labor Statistics.

Semiannual Report | 5

growth slowdown further contributed to pessimism. Long-term resolution of European debt issues remained unclear, but in September the European Central Bank (ECB) and European leaders established the European Stability Mechanism that, once funded by eurozone members, was expected to provide relief to troubled eurozone countries and banks.

Global developed and emerging stock markets, as measured by the MSCI All Country World Index, reflected general risk aversion early in the period, and equities declined while bonds rose. In the latter half of the period, stocks rallied as investors welcomed positive corporate earnings reports and became generally more optimistic about the global economic recovery and progress by the ECB and European leaders in solving the region s sovereign debt crisis. Stocks generally made gains for the period overall. Not all investors favored stocks, however, and many sought perceived safe havens such as gold bullion, the Japanese yen, the U.S. dollar and U.S. Treasuries. By period-end, the nominal yield on the 10-year U.S. Treasury note declined to 1.65%.

During the six-month reporting period, global merger and acquisition (M&A) activity continued to be slow and fell significantly year-over-year as concerns about the health of the global economy likely led many companies to delay large investment decisions. Despite the presence of several potential catalysts to deal-making activity, such as record levels of cash on corporate balance sheets and difficulties achieving organic top-line growth, M&A activity will likely remain muted until more of the questions facing the global economy are answered.

Globally, U.S.-based companies were the most active in the second and third quarters. Western Europe s M&A activity dropped year-over-year in the second quarter, and aggregate global deal volume was the lowest in nearly three years. China was active in the third quarter, including CNOOC s announced takeover of Canada s Nexen. Global deal activity was particularly pronounced in the financials, energy and retail sectors.

In the distressed debt arena, the rate of corporate bankruptcies and the number of reorganization and restructuring situations remained low during the period. The Fed s actions to keep interest rates at record lows increased investor demand for higher yielding assets, leading spreads between high yield bonds and Treasuries to narrow to below 6%.4 The recent environment of low

4. Source: Credit Suisse.

6 | Semiannual Report

rates and yield scarcity made it easier for companies with poor fundamentals to obtain financing and may have reduced the prevalence of distressed investment opportunities. During the period, U.S. corporate default rates remained well below the 25-year average of 4.7%, suggesting the frequency of liquidations and restructurings was unlikely to increase in the near future.4 However, U.S. and global default rates for speculative-grade securities increased slightly late in the period, a trend we monitor closely.

Investment Strategy

We follow a distinctive investment approach and can seek investments in distressed companies, merger arbitrage and special situations/undervalued stocks. The availability of investments at attractive prices in each of these categories varies with market cycles. Therefore, the percentage of the Fund s assets invested in each of these areas will fluctuate as we attempt to take advantage of opportunities afforded by cyclical changes. We employ rigorous, fundamental analysis to find investment opportunities. In choosing investments, we look at the market price of an individual company s securities relative to our evaluation of its asset value based on such factors as book value, cash flow potential, long-term earnings and earnings multiples. We may invest in distressed companies if we believe the market overreacted to adverse developments or failed to appreciate positive changes.

Manager s Discussion

During the six months under review, several Fund holdings increased in value and contributed positively to performance. Among the top contributors were debt investments in real estate services company Realogy, multimedia firm Tribune and power company Texas Competitive Electric Holdings.

We held various debt obligations of Realogy. Realogy provides real estate and relocation services through its portfolio of brands, which includes Century 21, Coldwell Banker, ERA and Sotheby s International. In the spring of 2007, private equity firm Apollo Management acquired Realogy in an $8.5 billion leveraged buyout, significantly increasing the company s debt load. The transaction proved ill-timed as the housing crisis led to weaker home sales and a deteriorating operating environment. Cash flows worsened as the company struggled to make interest payments on the acquisition-related debt and by

Semiannual Report | 7

2009, the company had become cash flow negative. In 2010, Apollo and other stakeholders agreed to convert their holdings of senior notes and senior subordinated debt into new convertible notes in what was effectively a restructuring and potential catalyst with benefits the market largely ignored at the time. Since then, operational performance has improved as the stabilizing U.S. housing market has contributed to declining inventories and rising prices in many of Realogy s markets. Subsequent to period-end in early October, the company raised approximately $1 billion in an initial public offering (IPO), which garnered significant interest and traded above the IPO price. The IPO transformed Realogy s capital structure by reducing leverage. In our assessment, the reduction in interest expense arising from the IPO and from the conversion of the aforementioned notes will allow Realogy to once again become free cash flow positive.

Tribune is an American multimedia corporation with television, newspaper and radio interests. Although the company s reorganization plan was approved in bankruptcy court in July, the Federal Communications Commission (FCC) must grant regulatory approval before Tribune can exit Chapter 11. While the company awaits completion of the FCC s review, Tribune s operational results have been strong, surpassing guidance in its 2012 business plan due to strong performance in its publishing division. We continue to see value in the com-pany s various business interests, which we believe provide tax-efficient ways to sell assets or potentially spin off the publishing division. A particularly valuable asset is Tribune s 31% stake in television channel Food Network, which we believe could potentially be sold for over $2 billion to Scripps Networks Interactive, which holds the other 69%.

Our investment in Texas Competitive Electric Holdings debt appreciated as power market fundamentals and natural gas prices showed some signs of improvement in the latter part of the six months under review. The repayment of an inter-company loan by its parent company also helped drive performance.

8 | Semiannual Report

Despite broad-based strength in the U.S. equity market, several of our equity investments declined in value and detracted from performance during the period. These included equity positions in securities exchange operator NYSE Euronext, casino entertainment company Caesars Entertainment and Germany-based KHD Humboldt Wedag International, which provides equipment and services for the global cement and mining industries.

Declining trading volumes across several asset classes depressed NYSE Euronext shares. Given the high fixed costs associated with the exchange business, declining volumes compressed margins and weighed on earnings expectations. Despite the difficult short-term operating environment, management continued to do its part by reducing costs where possible and returning capital to shareholders through dividends and share buybacks. We believe such actions have the potential to support performance until volumes and revenues improve.

Caution among consumers and a competitive entertainment industry resulted in a difficult operating environment and weighed on investor sentiment, leading our equity stake in Caesars Entertainment to decline. Despite the short-term trends, we believe Caesars represents an attractive investment opportunity as the company continues to execute on its plans to grow revenues in its various operational regions.

Although KHD Humboldt Wedag International has remained profitable and maintained a healthy balance sheet through the recent downturn, declining demand for mining and cement equipment weighed on the company s shares during the period. At period-end, the stock s market price remained well below our assessment of its intrinsic value.

Semiannual Report | 9

Thank you for your interest and participation in Franklin Mutual Recovery Fund. We look forward to serving your future investment needs. We are Fund owners as well as the portfolio managers, and we remain steadfast in our commitment to deliver the kind of performance we all expect from the Fund.

Portfolio Management Team

Franklin Mutual Recovery Fund

CFA® is a trademark owned by CFA Institute.

The foregoing information reflects our analysis, opinions and portfolio holdings as of September 30, 2012, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

10 | Semiannual Report

Christian Correa has been a portfolio manager for Franklin Mutual Recovery Fund since 2004. He joined Mutual Series in 2003 and serves as Director of Research. Previously, he covered merger arbitrage and special situations at Lehman Brothers Holdings Inc.

Shawn Tumulty has been a portfolio manager for Franklin Mutual Recovery Fund since 2005. He is the head of Mutual Series distressed securities team. Prior to joining Mutual Series, Mr. Tumulty was an analyst and portfolio manager at Kidder Peabody, Bankers Trust and Hamilton Partners Limited, where he focused on distressed debt investing.

Keith Luh has been a portfolio manager for Franklin Mutual Recovery Fund since 2009. He is also a research analyst specializing in distressed securities, merger and capital structure arbitrage, and event-driven situations. Prior to joining Mutual Series in 2005, Mr. Luh was an analyst in global investment research at Putnam Investments, where he also helped manage a best-ideas research fund. Previously, he worked in the investment banking group at Volpe Brown Whelan and Co., LLC, and the derivative products trading group at BNP. Mr. Luh is also Adjunct Professor at the Gabelli School of Business, Fordham University.

Semiannual Report | 11

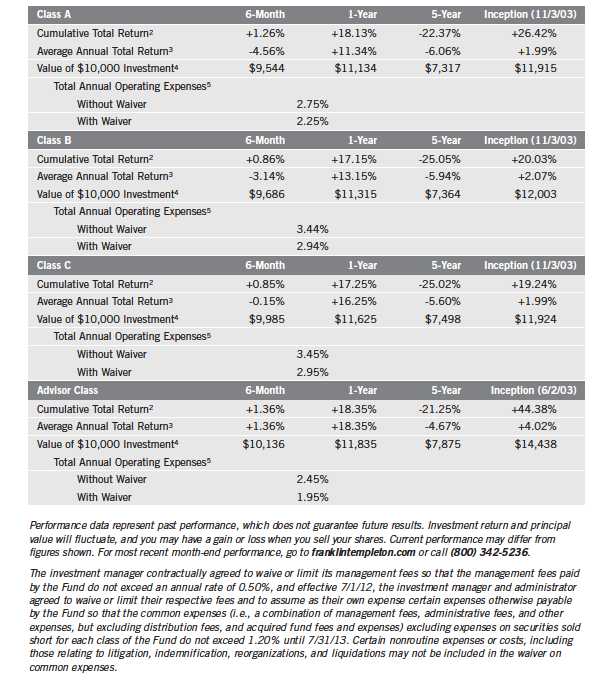

Performance Summary as of 9/30/12

Your dividend income will vary depending on dividends or interest paid by securities in the Fund s portfolio, adjusted for operating expenses of each class. Capital gain distributions are net profits realized from the sale of portfolio securities. The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund s dividends and capital gain distributions, if any, and any unrealized gains or losses.

12 | Semiannual Report

Performance Summary (continued)

Performance1

Cumulative total return excludes sales charges. Average annual total return and value of $10,000 investment include maximum sales charges. Class A: 5.75% maximum initial sales charge; Class B: contingent deferred sales charge (CDSC) declining from 4% to 1% over six years, and eliminated thereafter; Class C: 1% CDSC in first year only; Advisor Class: no sales charges.

Semiannual Report | 13

Performance Summary (continued)

Endnotes

All investments involve risks, including possible loss of principal. The Fund may invest in companies engaged in mergers, reorganizations or

liquidations, which involve special risks, as pending deals may not be completed on time or on favorable terms, as well as lower rated bonds,

which entail higher credit risk. The Fund is a nondiversified fund and may experience increased susceptibility to adverse economic or regula-

tory developments affecting similar issuers or securities. The Fund may invest in foreign securities whose risks include currency fluctuations,

and economic and political uncertainties. The Fund is actively managed but there is no guarantee that the manager s investment decisions will

produce the desired results. The Fund s prospectus also includes a description of the main investment risks.

| |

Class B: Class C: | These shares have higher annual fees and expenses than Class A shares. Prior to 1/1/04, these shares were offered with an initial sales charge; thus actual total returns would have differed. These shares have higher annual fees and expenses than Class A shares. |

Advisor Class: | Shares are available to certain eligible investors as described in the prospectus. |

1. Fund investment results reflect the expense reduction, without which the results would have been lower. 2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. Six-month return has not been annualized.

4. These figures represent the value of a hypothetical $10,000 investment in the Fund over the periods indicated.

5. Figures are as stated in the Fund s prospectus current as of the date of this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

14 | Semiannual Report

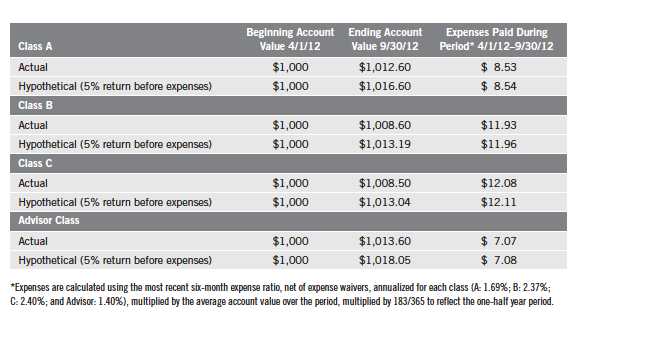

Your Fund s Expenses

As a Fund shareholder, you can incur two types of costs:

" Transaction costs, including sales charges (loads) on Fund purchases; and

" Ongoing Fund costs, including management fees, distribution and service (12b-1) fees, and other

Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses.

The following table shows ongoing costs of investing in the Fund and can help you understand

these costs and compare them with those of other mutual funds. The table assumes a $1,000

investment held for the six months indicated.

Actual Fund Expenses

The first line (Actual) for each share class listed in the table provides actual account values and

expenses. The Ending Account Value is derived from the Fund s actual return, which includes

the effect of Fund expenses.

You can estimate the expenses you paid during the period by following these steps. Of course,

your account value and expenses will differ from those in this illustration:

1. Divide your account value by $1,000.

If an account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6.

2. Multiply the result by the number under the heading Expenses Paid During Period.

If Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50.

In this illustration, the estimated expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Information in the second line (Hypothetical) for each class in the table can help you compare

ongoing costs of investing in the Fund with those of other mutual funds. This information may not

be used to estimate the actual ending account balance or expenses you paid during the period. The

hypothetical Ending Account Value is based on the actual expense ratio for each class and an

assumed 5% annual rate of return before expenses, which does not represent the Fund s actual

return. The figure under the heading Expenses Paid During Period shows the hypothetical

expenses your account would have incurred under this scenario. You can compare this figure with

the 5% hypothetical examples that appear in shareholder reports of other funds.

Semiannual Report | 15

Your Fund s Expenses (continued)

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transaction costs, such as sales charges. Therefore, the second line for each class is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transaction costs were included, your total costs would have been higher. Please refer to the Fund prospectus for additional information on operating expenses.

16 | Semiannual Report

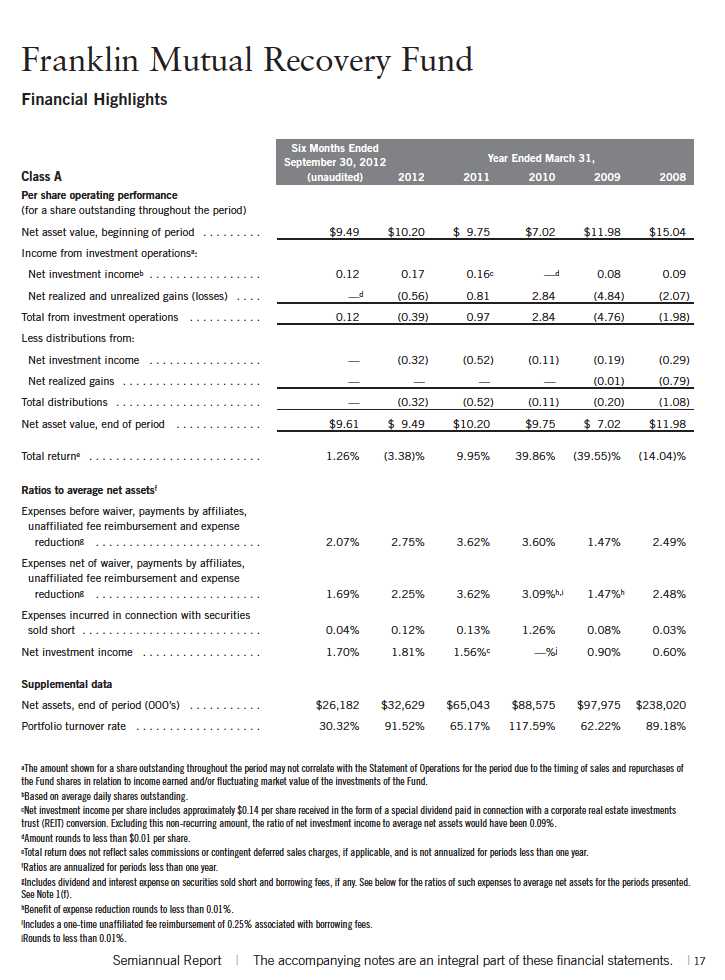

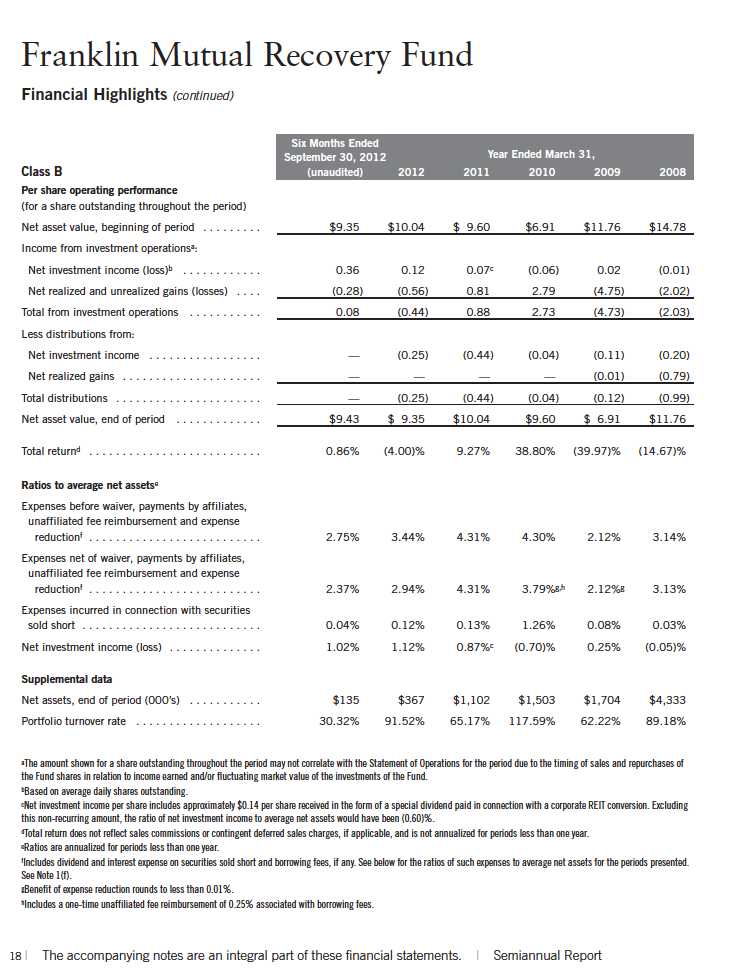

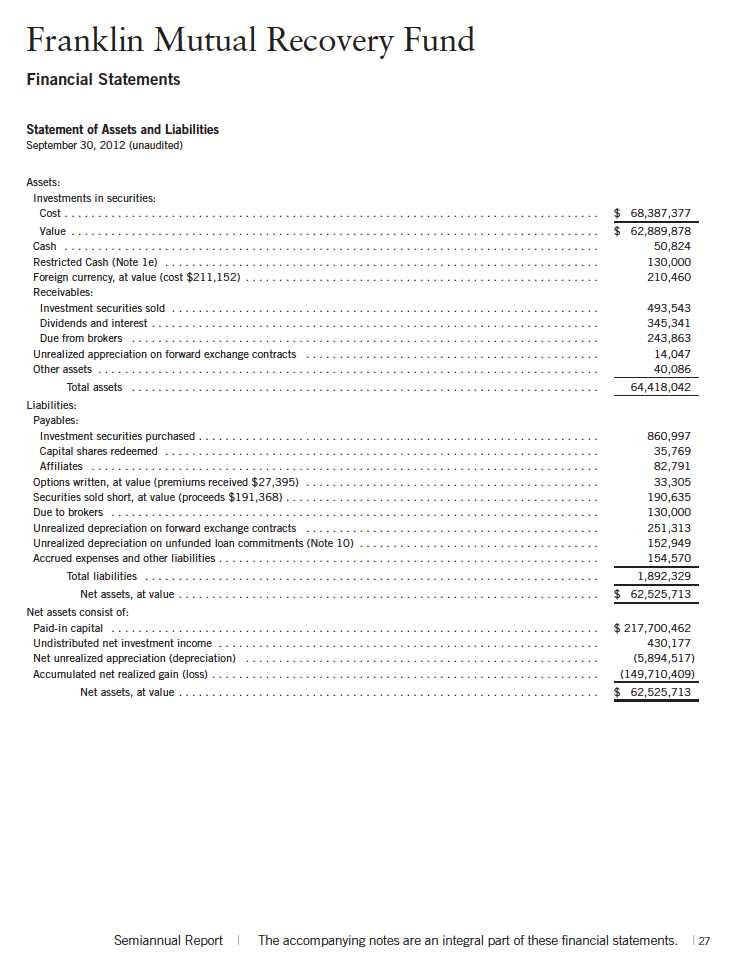

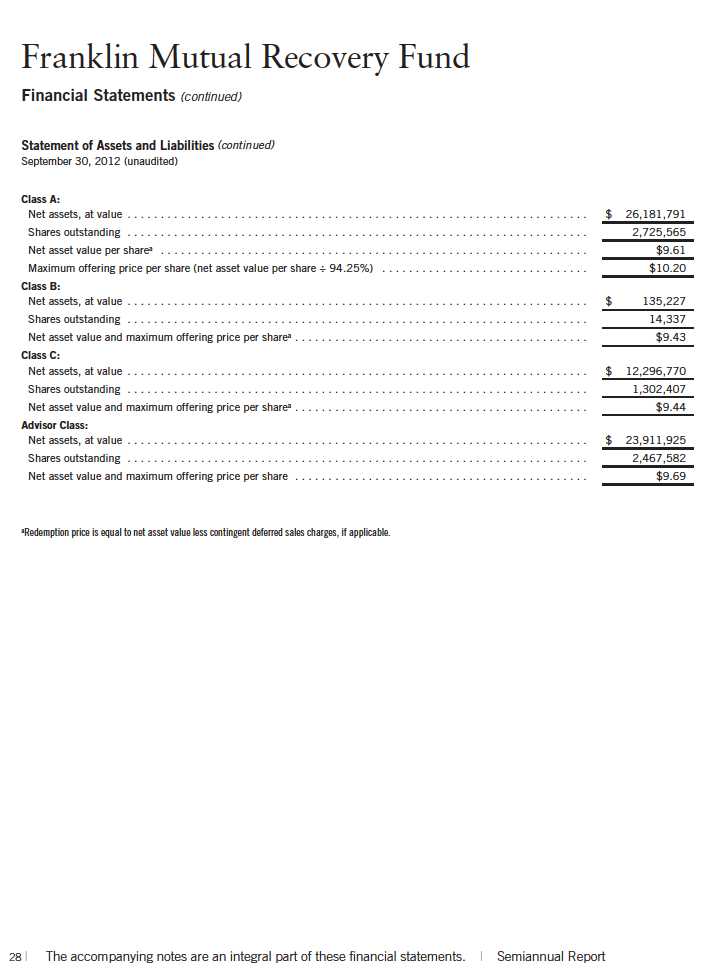

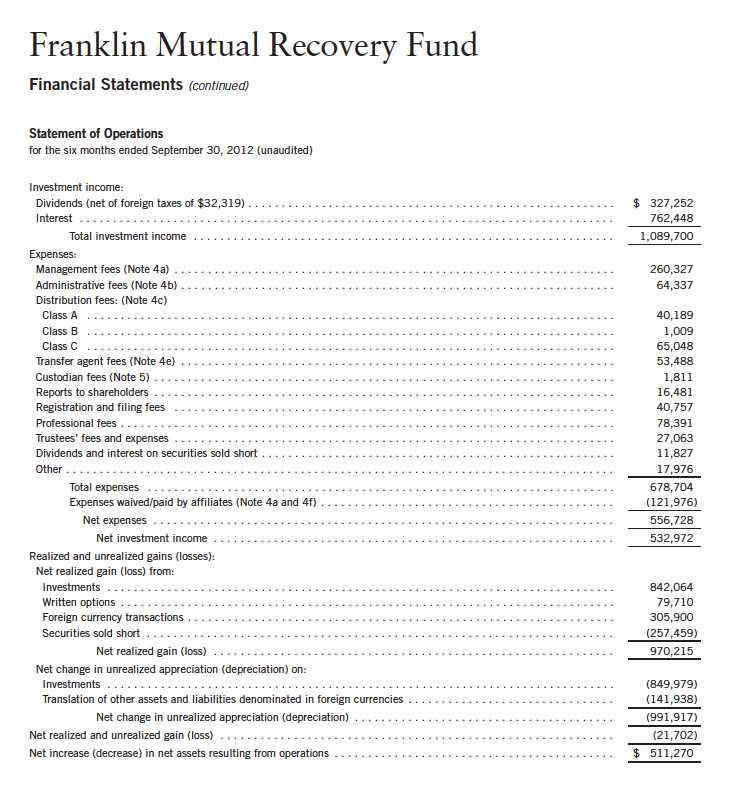

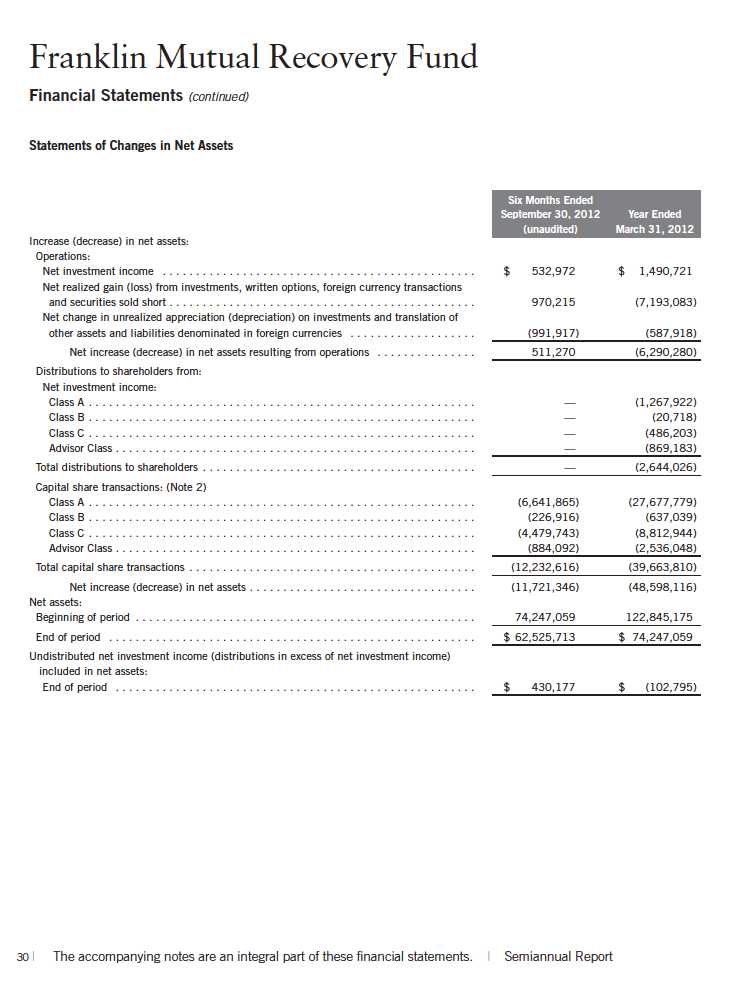

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 29

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

The Franklin Mutual Recovery Fund (Fund) is registered under the Investment Company Act of

1940, as amended, (1940 Act) as a closed-end, continuously offered investment company. The

Fund offers four classes of shares: Class A, Class B, Class C, and Advisor Class. Each class of

shares differs by its initial sales load, contingent deferred sales charges, distribution fees, voting

rights on matters affecting a single class and its exchange privilege.

The following summarizes the Fund s significant accounting policies.

a. Financial Instrument Valuation

The Fund s investments in financial instruments are carried at fair value daily. Fair value is the

price that would be received to sell an asset or paid to transfer a liability in an orderly transaction

between market participants on the measurement date. Under procedures approved by the Fund s

Board of Trustees (the Board), the Fund s administrator, investment manager and other affiliates

have formed the Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides

administration and oversight of the Fund s valuation policies and procedures, which are approved

annually by the Board. Among other things, these procedures allow the Fund to utilize independ-

ent pricing services, quotations from securities and financial instrument dealers, and other market

sources to determine fair value.

Equity securities and derivative financial instruments (derivatives) listed on an exchange or on the

NASDAQ National Market System are valued at the last quoted sale price or the official closing

price of the day, respectively. Foreign equity securities are valued as of the close of trading on the

foreign stock exchange on which the security is primarily traded, or the NYSE, whichever is earlier.

The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the

close of the NYSE on the day that the value of the security is determined. Over-the-counter (OTC)

securities are valued within the range of the most recent quoted bid and ask prices. Securities that

trade in multiple markets or on multiple exchanges are valued according to the broadest and most

representative market. Certain equity securities are valued based upon fundamental characteristics

or relationships to similar securities.

Debt securities generally trade in the OTC market rather than on a securities exchange. The

Fund s pricing services use multiple valuation techniques to determine fair value. In instances

where sufficient market activity exists, the pricing services may utilize a market-based approach

through which quotes from market makers are used to determine fair value. In instances where

sufficient market activity may not exist or is limited, the pricing services also utilize proprietary

valuation models which may consider market characteristics such as benchmark yield curves,

credit spreads, estimated default rates, anticipated market interest rate volatility, coupon rates,

anticipated timing of principal repayments, underlying collateral, and other unique security fea-

tures in order to estimate the relevant cash flows, which are then discounted to calculate the fair

Semiannual Report | 31

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| a. | Financial Instrument Valuation (continued) |

value. Securities denominated in a foreign currency are converted into their U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the date that the values of the foreign debt securities are determined.

Certain derivatives trade in the OTC market. The Fund s pricing services use various techniques including industry standard option pricing models and proprietary discounted cash flow models to determine the fair value of those instruments. The Fund s net benefit or obligation under the derivative contract, as measured by the fair market value of the contract, is included in net assets.

The Fund has procedures to determine the fair value of financial instruments for which market prices are not reliable or readily available. Under these procedures, the VLOC convenes on a regular basis to review such financial instruments and considers a number of factors, including significant unobservable valuation inputs, when arriving at fair value. The VLOC primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information for the investment to determine the fair value of the investment. An income-based valuation approach may also be used in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed. The VLOC employs various methods for calibrating these valuation approaches including a regular review of key inputs and assumptions, transactional back-testing or disposition analysis, and reviews of any related market activity.

Trading in securities on foreign securities stock exchanges and OTC markets may be completed before the daily close of business on the NYSE. Occasionally, events occur between the time at which trading in a foreign security is completed and the close of the NYSE that might call into question the reliability of the value of a portfolio security held by the Fund. As a result, differences may arise between the value of the Fund s portfolio securities as determined at the foreign market close and the latest indications of value at the close of the NYSE. In order to minimize the potential for these differences, the VLOC monitors price movements following the close of trading in foreign stock markets through a series of country specific market proxies (such as baskets of American Depositary Receipts, futures contracts and exchange traded funds). These price movements are measured against established trigger thresholds for each specific market proxy to assist in determining if an event has occurred that may call into question the reliability of the values of the foreign securities held by the Fund. If such an event occurs, the securities may be valued using fair value procedures, which may include the use of independent pricing services.

32 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| b. | Foreign Currency Translation |

Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. The Fund may enter into foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of securities, income and expense items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date. Portfolio securities and assets and liabilities denominated in foreign currencies contain risks that those currencies will decline in value relative to the U.S. dollar. Occasionally, events may impact the availability or reliability of foreign exchange rates used to convert the U.S. dollar equivalent value. If such an event occurs, the foreign exchange rate will be valued at fair value using procedures established and approved by the Board.

The Fund does not separately report the effect of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized and unrealized gain or loss from investments on the Statement of Operations.

Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period.

c. Securities Purchased on a Delayed Delivery Basis

The Fund purchases securities on a delayed delivery basis, with payment and delivery scheduled for a future date. These transactions are subject to market fluctuations and are subject to the risk that the value at delivery may be more or less than the trade date purchase price. Although the Fund will generally purchase these securities with the intention of holding the securities, it may sell the securities before the settlement date. Sufficient assets have been segregated for these securities.

d. Derivative Financial Instruments

The Fund invested in derivatives in order to manage risk or gain exposure to various other investments or markets. Derivatives are financial contracts based on an underlying or notional amount, require no initial investment or an initial net investment that is smaller than would normally be required to have a similar response to changes in market factors, and require or permit net settlement. Derivatives contain various risks including the potential inability of the counterparty to fulfill their obligations under the terms of the contract, the potential for an illiquid secondary market, and/or the potential for market movements which expose the Fund to gains or losses in excess of the amounts shown on the Statement of Assets and Liabilities. Realized gain and loss and unrealized appreciation and depreciation on these contracts for the period are included in the Statement of Operations.

Semiannual Report | 33

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| d. | Derivative Financial Instruments (continued) |

The Fund s investments in OTC derivatives are subject to the terms of International Swaps and Derivatives Association Master Agreements and other related agreements between the Fund and certain derivative counterparties. These agreements contain various provisions, including but not limited to collateral requirements, events of default, requirements for the Fund to maintain certain net asset levels and/or limit the decline in net assets over various periods of time. Should the Fund fail to meet any of these provisions, the derivative counterparty has the right to terminate the derivative contract and require immediate payment by the Fund for those OTC derivatives with that particular counterparty that are in a net unrealized loss position. At September 30, 2012, the Fund had OTC derivatives in a net unrealized loss position for such contracts of $238,443.

The Fund entered into OTC forward exchange contracts primarily to manage exposure to certain foreign currencies. A forward exchange contract is an agreement between the Fund and a coun-terparty to buy or sell a foreign currency for a specific exchange rate on a future date. Pursuant to the terms of the forward exchange contracts, cash or securities may be required to be deposited as collateral. Unrestricted cash may be invested according to the Fund s investment objectives.

The Fund purchased or wrote exchange traded and/or OTC option contracts primarily to manage and/or gain exposure to equity price, interest rate and foreign exchange rate risk. An option is a contract entitling the holder to purchase or sell a specific amount of shares or units of an asset or notional amount of a swap (swaption), at a specified price. Options purchased are recorded as an asset while options written are recorded as a liability. Upon exercise of an option, the acquisition cost or sales proceeds of the underlying investment is adjusted by any premium received or paid. Upon expiration of an option, any premium received or paid is recorded as a realized gain or loss. Upon closing an option other than through expiration or exercise, the difference between the premium and the cost to close the position is recorded as a realized gain or loss. Pursuant to the terms of the written option contract, cash or securities may be required to be deposited as collateral.

See Notes 7 and 11 regarding investment transactions and other derivative information, respectively.

e. Restricted Cash

At September 30, 2012, the Fund held restricted cash in connection with investments in certain derivative securities. Restricted cash is held in a segregated account with the Fund s custodian/counterparty broker and is reflected in the Statement of Assets and Liabilities.

f. Securities Sold Short

The Fund is engaged in selling securities short, which obligates the Fund to replace a borrowed security with the same security at current market value. The Fund incurs a loss if the price of the security increases between the date of the short sale and the date on which the Fund replaces the

34 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| f. | Securities Sold Short (continued) |

borrowed security. The Fund realizes a gain if the price of the security declines between those dates. Gains are limited to the price at which the Fund sold the security short, while losses are potentially unlimited in size.

The Fund is required to establish a margin account with the broker lending the security sold short. While the short sale is outstanding, the broker retains the proceeds of the short sale and the Fund must maintain a deposit with the broker consisting of cash and/or securities having a value equal to a specified percentage of the value of the securities sold short. The Fund is obligated to pay fees for borrowing the securities sold short and is required to pay the counterparty any dividends or interest due on securities sold short. Such dividends or interest and any security borrowing fees are recorded as an expense to the Fund.

g. Securities Lending

The Fund participates in an agency based securities lending program. The Fund receives cash collateral against the loaned securities in an amount equal to at least 102% of the market value of the loaned securities. Collateral is maintained over the life of the loan in an amount not less than 100% of the market value of loaned securities, as determined at the close of fund business each day; any additional collateral required due to changes in security values is delivered to the Fund on the next business day. The collateral is invested in a non-registered money fund. The Fund receives income from the investment of cash collateral, in addition to lending fees and rebates paid by the borrower. The Fund bears the market risk with respect to the collateral investment, securities loaned, and the risk that the agent may default on its obligations to the Fund. The securities lending agent has agreed to indemnify the Fund in the event of default by a third party borrower. At September 30, 2012, the Fund had no securities on loan.

h. Senior Floating Rate Interests

The Fund invests in senior secured corporate loans that pay interest at rates which are periodically reset by reference to a base lending rate plus a spread. These base lending rates are generally the prime rate offered by a designated U.S. bank or the London InterBank Offered Rate (LIBOR). Senior secured corporate loans often require prepayment of principal from excess cash flows or at the discretion of the borrower. As a result, actual maturity may be substantially less than the stated maturity.

Senior secured corporate loans in which the Fund invests are generally readily marketable, but may be subject to some restrictions on resale.

i. Income and Deferred Taxes

It is the Fund s policy to qualify as a regulated investment company under the Internal Revenue Code. The Fund intends to distribute to shareholders substantially all of its taxable income and

Semiannual Report | 35

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued)

i. Income and Deferred Taxes (continued)

net realized gains to relieve it from federal income and excise taxes. As a result, no provision for

U.S. federal income taxes is required.

The Fund may be subject to foreign taxation related to income received, capital gains on the sale

of securities and certain foreign currency transactions in the foreign jurisdictions in which it

invests. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in

the foreign markets in which the Fund invests. When a capital gain tax is determined to apply

the Fund records an estimated deferred tax liability in an amount that would be payable if the

securities were disposed of on the valuation date.

The Fund recognizes the tax benefits of uncertain tax positions only when the position is more

likely than not to be sustained upon examination by the tax authorities based on the technical

merits of the tax position. As of September 30, 2012, and for all open tax years, the Fund has

determined that no liability for unrecognized tax benefits is required in the Fund s financial

statements related to uncertain tax positions taken on a tax return (or expected to be taken on

future tax returns). Open tax years are those that remain subject to examination and are based

on each tax jurisdiction statute of limitation.

j. Security Transactions, Investment Income, Expenses and Distributions

Security transactions are accounted for on trade date. Realized gains and losses on security

transactions are determined on a specific identification basis. Interest income and estimated

expenses are accrued daily. Amortization of premium and accretion of discount on debt secu-

rities are included in interest income. Dividend income and dividends declared on securities

sold short are recorded on the ex-dividend date except that certain dividends from foreign

securities are recognized as soon as the Fund is notified of the ex-dividend date. Distributions

to shareholders are recorded on the ex-dividend date and are determined according to income

tax regulations (tax basis). Distributable earnings determined on a tax basis may differ from

earnings recorded in accordance with accounting principles generally accepted in the United

States of America. These differences may be permanent or temporary. Permanent differences

are reclassified among capital accounts to reflect their tax character. These reclassifications

have no impact on net assets or the results of operations. Temporary differences are not

reclassified, as they may reverse in subsequent periods.

Realized and unrealized gains and losses and net investment income, not including class specific

expenses, are allocated daily to each class of shares based upon the relative proportion of net

assets of each class. Differences in per share distributions, by class, are generally due to differ-

ences in class specific expenses.

Distributions received by the Fund from certain securities may be a return of capital (ROC).

Such distributions reduce the cost basis of the securities, and any distributions in excess of the

cost basis are recognized as capital gains.

36 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued)

k. Accounting Estimates

The preparation of financial statements in accordance with accounting principles generally

accepted in the United States of America requires management to make estimates and assump-

tions that affect the reported amounts of assets and liabilities at the date of the financial

statements and the amounts of income and expenses during the reporting period. Actual

results could differ from those estimates.

l. Guarantees and Indemnifications

Under the Fund s organizational documents, its officers and trustees are indemnified by the Fund

against certain liabilities arising out of the performance of their duties to the Fund. Additionally,

in the normal course of business, the Fund enters into contracts with service providers that con-

tain general indemnification clauses. The Fund s maximum exposure under these arrangements is

unknown as this would involve future claims that may be made against the Fund that have not

yet occurred. Currently, the Fund expects the risk of loss to be remote.

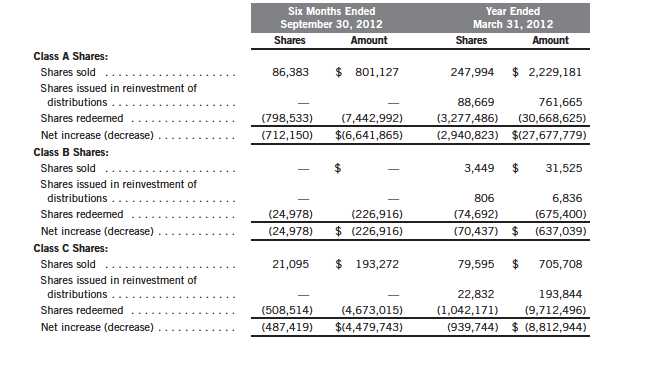

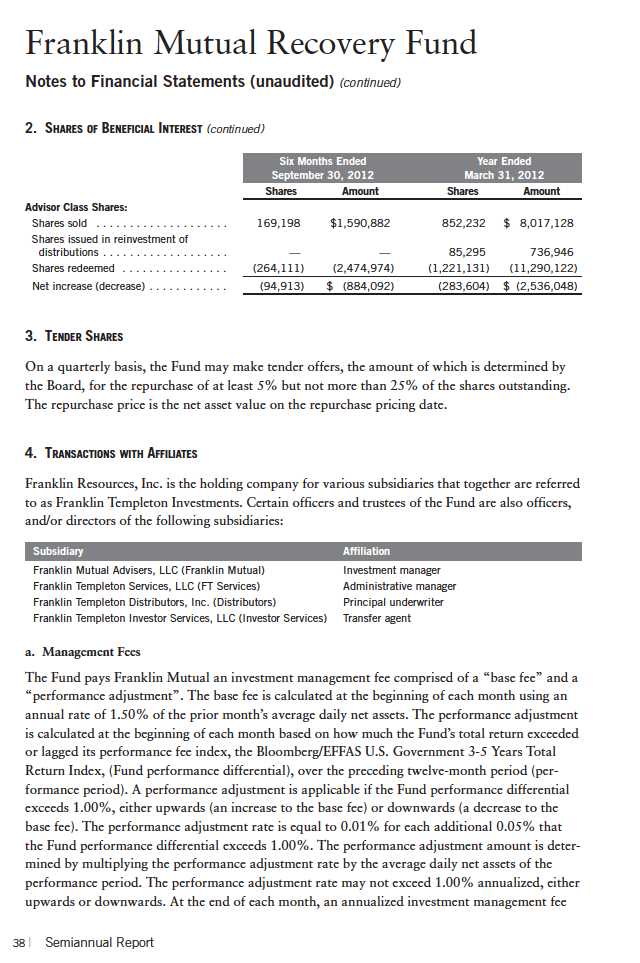

2. SHARES OF BENEFICIAL INTEREST

At September 30, 2012, there were an unlimited number of shares authorized ($0.01 par

value). Transactions in the Fund s shares were as follows:

Semiannual Report | 37

Semiannual Report | 39

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

8. CREDIT RISK AND DEFAULTED SECURITIES (continued)

At September 30, 2012, the aggregate value of distressed company securities for which interest

recognition has been discontinued was $6,811,585, representing 10.89% of the Fund s net assets.

For information as to specific securities, see the accompanying Statement of Investments.

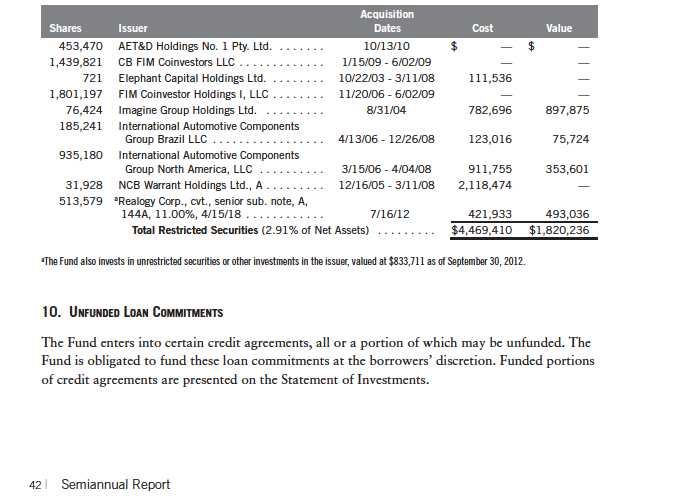

9. RESTRICTED SECURITIES

The Fund invests in securities that are restricted under the Securities Act of 1933 (1933 Act) or

which are subject to legal, contractual, or other agreed upon restrictions on resale. Restricted

securities are often purchased in private placement transactions, and cannot be sold without

prior registration unless the sale is pursuant to an exemption under the 1933 Act. Disposal of

these securities may require greater effort and expense, and prompt sale at an acceptable price

may be difficult. The Fund may have registration rights for restricted securities. The issuer gen-

erally incurs all registration costs.

At September 30, 2012, the Fund held investments in restricted securities, excluding certain

securities exempt from registration under the 1933 Act deemed to be liquid, as follows:

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

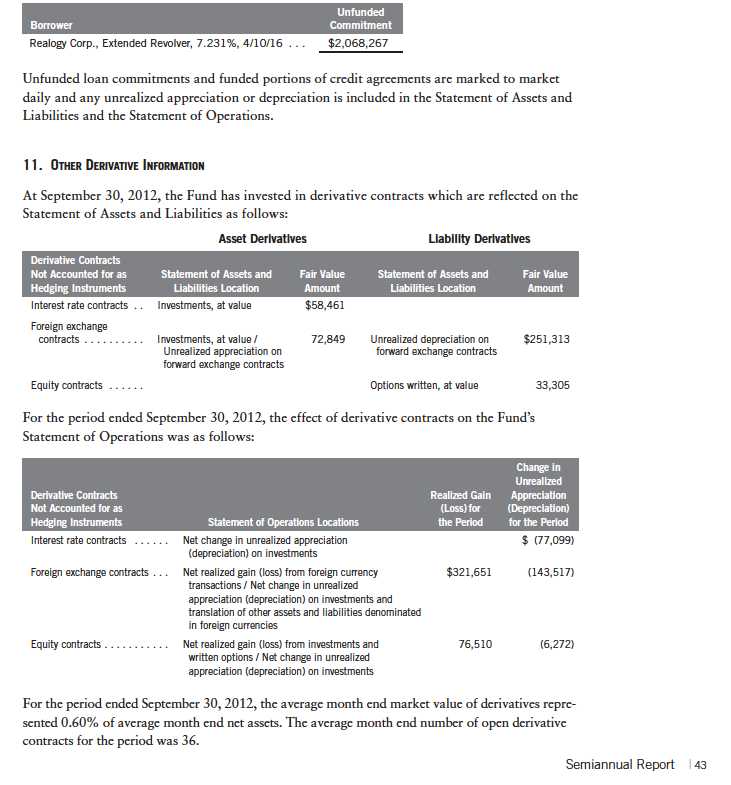

10. UNFUNDED LOAN COMMITMENTS (continued)

At September 30, 2012, unfunded commitments were as follows:

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

11. OTHER DERIVATIVE INFORMATION (continued)

See Notes 1(d) and 7 regarding derivative financial instruments and investment transactions, respectively.

12. CREDIT FACILITY

The Fund participates in a $10 million senior unsecured revolving credit facility to fund shareholder redemptions or meet unfunded loan commitments. Under the terms of the current credit facility, which expires on May 24, 2013, and may or may not be extended for subsequent periods on the same or different terms, the Fund shall, in addition to interest charged on any borrowings made by the Fund, pay an annual commitment fee based upon the unused portion of the credit facility. During the period, the Fund incurred commitment fees of $10,026, which is reflected in other expenses on the Statement of Operations. During the period ended September 30, 2012, the Fund did not use the credit facility.

13. FAIR VALUE MEASUREMENTS

The Fund follows a fair value hierarchy that distinguishes between market data obtained from independent sources (observable inputs) and the Fund s own market assumptions (unobservable inputs). These inputs are used in determining the value of the Fund s financial instruments and are summarized in the following fair value hierarchy:

- Level 1 quoted prices in active markets for identical financial instruments

- Level 2 other significant observable inputs (including quoted prices for similar financial instruments, interest rates, prepayment speed, credit risk, etc.)

- Level 3 significant unobservable inputs (including the Fund s own assumptions in determining the fair value of financial instruments)

The inputs or methodology used for valuing financial instruments are not an indication of the risk associated with investing in those financial instruments.

For movements between the levels within the fair value hierarchy, the Fund has adopted a policy of recognizing the transfers as of the date of the underlying event which caused the movement.

44 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

13. FAIR VALUE MEASUREMENTS (continued)

A summary of inputs used as of September 30, 2012, in valuing the Fund s assets and liabilities carried at fair value, is as follows:

Semiannual Report | 45

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

13. FAIR VALUE MEASUREMENTS (continued)

A reconciliation of assets in which Level 3 inputs are used in determining fair value is presented when there are significant Level 3 investments at the end of the period. At September 30, 2012, the reconciliation of assets, is as follows:

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

13. FAIR VALUE MEASUREMENTS (continued)

company. A significant and reasonable increase or decrease in the valuations of the underlying

assets would result in a significant increase or decrease in the fair value measurement. A signifi-

cant and reasonable increase or decrease in the assumed net debt would result in a significant

decrease or increase in the fair value measurement.

The significant unobservable inputs used in the fair value measurement of the Fund s investment

in insurance companies are the price to book multiple and a discount for lack of marketability.

A significant and reasonable increase or decrease in the price to book multiple would not result

in a significant increase or decrease in the fair value measurement. A significant and reasonable

increase or decrease in the discount for lack of marketability would result in a significant

decrease or increase in the fair value measurement.

14. NEW ACCOUNTING PRONOUNCEMENTS

In December 2011, the Financial Accounting Standards Board issued Accounting Standards

Update (ASU) No. 2011-11, Balance Sheet (Topic 210): Disclosures about Offsetting Assets

and Liabilities. The amendments in the ASU enhance disclosures about offsetting of financial

assets and liabilities to enable investors to understand the effect of these arrangements on a

fund s financial position. The ASU is effective for interim and annual reporting periods begin-

ning on or after January 1, 2013. The Fund believes the adoption of this ASU will not have a

material impact on its financial statements.

15. SUBSEQUENT EVENTS

The Fund has evaluated subsequent events through the issuance of the financial statements and

determined that no events have occurred that require disclosure.

Semiannual Report | 47

Franklin Mutual Recovery Fund

Shareholder Information

Board Review of Investment Management Agreements

The Board of Trustees (Board), including the independent trustees, at a Board meeting held on May 21, 2012, unanimously approved renewal of the Fund s investment management agreement, as well as the Fund s administrative services agreement, after negotiating with management the continuation of the existing cap to the investment management fee and the institution of an additional fee cap on total expenses, each as more fully discussed below. Prior to a meeting of all of the trustees for the purpose of considering such renewals, the independent trustees held three meetings dedicated to the renewal process (those trustees unable to attend in person were present by telephonic conference means). Throughout the process, the independent trustees received assistance and advice from and met separately with independent counsel. The independent trustees met with and interviewed officers of the investment manager (including portfolio managers), the transfer agent and shareholder services group and the distributor. In approving the renewal of the investment management agreement and the administrative services agreement for the Fund, the Board, including the independent trustees, determined that, taking into account the caps on the investment management fee and total expenses, the investment management fee structure was fair and reasonable and that continuance of the agreements was in the best interests of the Fund and its shareholders.

In reaching their decision on the investment management agreement (as well as the administrative services agreement), the trustees took into account information furnished throughout the year at regular Board meetings, as well as information specifically requested and furnished for the renewal process, which culminated in the meetings referred to above for the specific purpose of considering such agreements. Information furnished throughout the year included, among others, reports on the Fund s investment performance, expenses, portfolio composition, portfolio brokerage execution, client commission arrangements, derivatives, securities lending, portfolio turnover, Rule 12b-l plans, distribution, shareholder servicing, legal and compliance matters, pricing of securities and sales and redemptions, along with related financial statements and other information about the scope and quality of services provided by the investment manager and its affiliates and enhancements to such services over the past year. In addition, the trustees received periodic reports throughout the year and during the renewal process relating to compliance with the Fund s investment policies and restrictions. During the renewal process, the independent trustees considered the investment man-ager s methods of operation within the Franklin Templeton group and its activities on behalf of other clients.

In addition, the trustees received a Profitability Study (Profitability Study) prepared by management discussing the profitability to Franklin Templeton Investments from its overall U.S. fund operations, as well as on an individual fund-by-fund basis.

Over the past year, the Board and counsel to the independent trustees continued to receive reports on management s handling of recent regulatory actions and pending legal actions against the investment manager and its affiliates. The independent trustees were satisfied with the actions taken to date by management in response to such regulatory and legal proceedings.

48 | Semiannual Report

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

Particular attention was given to management s diligent risk management procedures, including continuous monitoring of counterparty credit risk and attention given to derivatives and other complex instruments. The Board also took into account, among other things, the strong financial position of the investment manager s parent company and its commitment to the mutual fund business. In addition, the Board received updates from management on the Securities and Exchange Commission s (SEC) progress in implementing the rule making requirements established by the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was enacted July 21, 2010, and the investment manager s compliance with rules and regulations already promulgated by the SEC under such act.

In addition to the above and other matters considered by the trustees throughout the course of the year, the following discussion relates to certain primary factors relevant to the Board s decision. This discussion of the information and factors considered by the Board (as well as the discussion above) is not intended to be exhaustive, but rather summarizes certain factors considered by the Board. In view of the wide variety of factors considered, the Board did not, unless otherwise noted, find it practicable to quantify or otherwise assign relative weights to the foregoing factors. In addition, individual trustees may have assigned different weights to various factors.

NATURE, EXTENT AND QUALITY OF SERVICES. The trustees reviewed the nature, extent and quality of the services provided by the investment manager. In this regard, they reviewed the Fund s investment approach and concluded that, in their view, it continues to differentiate the Fund from typical core investment products in the mutual fund field. The trustees cited the investment manager s ability to implement the Fund s disciplined value investment approach and its long-term relationship with the Fund since the Fund s inception eight and one half years ago as reasons that shareholders choose to invest, and remain invested, in the Fund. The trustees reviewed the Fund s portfolio management team, including its performance, staffing, skills and compensation program. With respect to portfolio manager compensation, management assured the trustees that the Fund s longer-term performance is a significant component of incentive-based compensation and noted that a portion of a portfolio manager s incentive-based compensation is paid in shares of predesignated funds from the portfolio manager s fund management area. The trustees noted that the portfolio manager compensation program aligned the interests of the portfolio managers with that of Fund shareholders. The trustees discussed with management various other products, portfolios and entities that are advised by the investment manager and the allocation of assets and expenses among and within them, as well as their relative fees and reasons for differences with respect thereto and any potential conflicts. During regular Board meetings and the aforementioned meetings of the independent trustees, the trustees received reports and presentations on the investment manager s best execution trading policies. The trustees considered periodic reports provided to them showing that the investment manager complied with the investment policies and restrictions of the Fund as well as other reports periodically furnished to the Board covering matters such as the compliance of portfolio managers and other management personnel with the code of ethics covering the investment management personnel, the adherence to fair value pricing procedures established by the Board and the accuracy of net asset value calculations. The Board noted the extent of the benefits provided to

Semiannual Report | 49

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

Fund shareholders from being part of the Franklin Templeton group, including the right to exchange investments between funds (same class) without a sales charge, the ability to reinvest Fund dividends into other funds and the right to combine holdings of other funds to obtain reduced sales charges. The trustees considered the investment manager s significant efforts in developing and implementing compliance procedures established in accordance with SEC requirements. The trustees also reviewed the nature, extent and quality of the Fund s other service agreements to determine that, on an overall basis, Fund shareholders were well served. In this connection, the Board also took into account administrative and transfer agent and shareholder services provided to Fund shareholders by an affiliate of the investment manager, noting continuing expenditures by management to increase and improve the scope of such services and favorable periodic reports on shareholder services conducted by independent third parties. While such considerations directly affected the trustees decision in renewing the Fund s administrative services and transfer agent and shareholder services agreement, the Board also considered these commitments as incidental benefits to Fund shareholders deriving from the investment management relationship.

Based on their review, the trustees were satisfied with the nature and quality of the overall services provided by the investment manager and its affiliates to the Fund and its shareholders and were confident in the abilities of the management team to continue the disciplined value investment approach of the Fund and to provide quality services to the Fund and its shareholders.

INVESTMENT PERFORMANCE. The trustees reviewed and placed significant emphasis on the investment performance of the Fund. In this context, the trustees believed that it is difficult to find open or closed-end funds that are truly comparable to the Fund due, in part, to the unique nature of the Fund as a closed-end interval fund investing in the categories of bankruptcy and distressed companies, merger arbitrage and undervalued stocks and debt instruments. They considered the performance of the Fund over the past eight and one half years since formation of the Fund relative to various benchmarks. As part of their review, they inquired of management regarding benchmarks (including the benchmark on which the Fund s performance adjustment fee is based), style drift and restrictions on permitted investments. Consideration was also given to performance in the context of available levels of cash during the periods.

The trustees had meetings during the year, including the meetings referred to above held in connection with the renewal process, with the Fund s portfolio managers to discuss performance. The Board reviewed the Fund s annualized total returns (Class A shares) for the one-, three-, and five-year periods ended December 31, 2011, and discussed with the investment manager the reasons for the Fund s underperformance relative to various benchmarks over certain of these periods. After discussing the Fund s performance and after considering various options and other factors, including, but, not limited to, the Fund s expense ratios, the Board negotiated, as more fully discussed below, to retain the existing cap on the Fund s investment management fee and to institute a total expense cap.

50 | Semiannual Report

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

COMPARATIVE EXPENSES AND MANAGEMENT PROFITABILITY. The trustees considered the cost of the services provided and to be provided and the profits realized by the investment manager and its affiliates from their respective relationships with the Fund. As part of the approval process, they explored with management the trends in expense ratios over the past three fiscal years and the reasons for any increase in the Fund s expenses ratios (both including and excluding the performance adjustment fee). The trustees also compared the Fund s fees to the fees charged to other accounts managed by the manager.

The trustees noted that the Fund s investment management fee is comprised of two components, a base fee and a performance adjustment to the base fee. The adjustment is based on the Fund s performance relative to the Bloomberg/EFFAS U.S. Government 3-5 Years Total Return Index (Index) over a rolling 12-month period ending with the most recently completed month (Performance Period). The first component of the fee is a base fee equal to an annual rate of 1.50% of the Fund s average daily net assets during the month that ends on the last day of the Performance Period. The second component is a performance adjustment that either increases or decreases the base fee, depending on how the Fund has performed relative to the Index over the Performance Period. The maximum annual investment management fee is 2.50% of average daily net assets over each fiscal year of the Fund and the minimum annual investment management fee is 0.50% of average daily net assets over each fiscal year of the Fund.

In the context of, among other factors, the performance of the Fund, including performance relative to various benchmarks, the trustees decided to negotiate with the investment manager to lower the Fund s expenses. Accordingly, the trustees negotiated with management both the retention of the existing investment management fee cap of 0.50% of the Fund s average daily net assets and the addition of a fee cap on total expenses of 1.20% of the Fund s average daily net assets (excluding Rule 12b-1 fees charged to the Fund and dividends and interest for securities sold short and other related expenses in connection with securities sold short). Each cap is effective for the period commencing on July 1, 2012, and ending on July 31, 2013.

The trustees also reviewed the Profitability Study addressing profitability of Franklin Resources, Inc., from its overall U.S. fund business, as well as profitability to the Fund s investment manager and its affiliates, from providing investment management and other services to the Fund during the 12-month period ended September 30, 2011, the then most recent fiscal year-end of Franklin Resources, Inc. The trustees reviewed the basis on which such reports are prepared and the cost allocation methodology utilized in the Profitability Study, it being recognized that allocation methodologies may each be reasonable while producing different results. In this respect, the Board noted that the reasonableness of the cost allocation methodologies was reviewed by independent accountants on an every other year basis.

The independent trustees met with management to discuss the Profitability Study. This included, among other things, a comparison of investment management income with investment management expenses of the Fund; comparison of underwriting revenues and expenses; the relative relationship

Semiannual Report | 51

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

of investment management and underwriting expenses; shareholder servicing profitability (losses); economies of scale; and the relative contribution of the Fund to the profitability of the investment manager and its parent. In discussing the Profitability Study with the Board, the investment manager stated its belief that the costs incurred in establishing the infrastructure necessary to operate the type of mutual fund operations conducted by it and its affiliates may not be fully reflected in the expenses allocated to the Fund in determining its profitability.

The trustees considered a study by Lipper, Inc., an independent third-party analyst, analyzing the profitability of the parent of the investment manager as compared to other publicly held investment managers, which also aided the trustees in considering profitability excluding distribution costs. The Board also took into account management s expenditures in improving shareholder services provided to the Fund as well as the need to meet additional regulatory and compliance requirements resulting from the Sarbanes-Oxley Act and recent SEC and other regulatory requirements. The trustees also considered the extent to which the investment manager may derive ancillary benefits from Fund operations, including those derived from economies of scale, discussed below, the allocation of Fund brokerage and the use of commission dollars to pay for research and other similar services.

Based upon their consideration of all these factors, including, but not limited to, continuing the existing cap on the Fund s investment management fee and instituting a new cap on total expenses, the trustees determined that the level of profits realized by the manager and its affiliates in providing services to the Fund was not excessive in view of the nature, quality and extent of services provided.

ECONOMIES OF SCALE. The trustees considered that economies of scale may be realized by the manager and its affiliates as the Fund grows larger and the extent to which they are shared with Fund shareholders, as for example, in the level of the investment management fee charged, in the quality and efficiency of services rendered and in increased capital commitments benefiting the Fund directly or indirectly. Since the amount of assets under management of the Fund remains relatively small, the trustees concluded that economies of scale were difficult to consider at that time.

Proxy Voting Policies and Procedures

The Fund s investment manager has established Proxy Voting Policies and Procedures (Policies) that the Fund uses to determine how to vote proxies relating to portfolio securities. Shareholders may view the Fund s complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 300 S.E. 2nd Street, Fort Lauderdale, FL 33301, Attention: Proxy Group. Copies of the Fund s proxy voting records are also made available online at franklintempleton.com and posted on the U.S. Securities and Exchange Commission s website at sec.gov and reflect the most recent 12-month period ended June 30.

52 | Semiannual Report

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Quarterly Statement of Investments

The Fund files a complete statement of investments with the U.S. Securities and Exchange Commission for the first and third quarters for each fiscal year on Form N-Q. Shareholders may view the filed Form N-Q by visiting the Commission s website at sec.gov. The filed form may also be viewed and copied at the Commission s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling (800) SEC-0330.

Semiannual Report | 53

This page intentionally left blank.

This page intentionally left blank.

This page intentionally left blank.