The Bloomberg/EFFAS U.S. Government 3-5 Years Total Return Index, which serves as a transparent benchmark for the U.S. government bond market, had a six-month total return of -0.83%.2

The performance of the Fund relative to the Bloomberg index is used as the basis for calculating the performance adjustment to the base management fee paid to the Fund’s adviser. (Please refer to Notes 4a and 4f in the Notes to Financial Statements for additional information related to the performance adjustment, base management fee and related fee waivers or limits.) You can find the Fund’s long-term performance data in the Performance Summary beginning on page 12.

Economic and Market Overview

The U.S. economy, as measured by gross domestic product, grew modestly during the six-month period ended September 30, 2013, supported by business investment and consumer spending. Accelerating new and existing home sales accompanied historically low mortgage rates, rising but affordable housing prices, low inventories and the lowest level of U.S. foreclosures in nearly eight years. Manufacturing, a mainstay of economic productivity, expanded for most of the period, and the unemployment rate fell to 7.2% in September from 7.6% in March.3

Budgetary agreement between congressional parties on January 1, 2013, preserved lower income tax rates for most U.S. households, but Washington’s lack of consensus on proposed expenditure reductions resulted in further across-the-board federal spending cuts starting in March. After indicating in May that the Federal Reserve Board (Fed) might reduce monthly purchases of mortgage-backed securities and Treasuries, assuming ongoing U.S. recovery, Fed Chairman Ben Bernanke announced in September that any tapering of its purchases would be postponed until U.S. economic growth strengthened. At period-end, because of partisan disagreement about a new health care law, Congress did not authorize some routine federal funding, resulting in a temporary shutdown of non-essential U.S. government services beginning on October 1. Unless prolonged, the shutdown was not expected to hinder long-term economic growth, but the political impasse added to concerns about congressional ability to successfully navigate federal debt ceiling negotiations in October.

2. Source: Bloomberg LP. The index is unmanaged and includes reinvested income or distributions. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

3. Source: Bureau of Labor Statistics.

6 | Semiannual Report

Chairman Bernanke’s statements and the impending U.S. government shutdown sparked some market sell-offs. Rising corporate profits and generally favorable economic data bolstered investor confidence, however, and U.S. stocks generated healthy six-month returns as the S&P 500 and Dow Jones Industrial Average reached all-time highs during the period.

For the six months under review, global total mergers and acquisitions (M&A) deal count declined year-over-year. However, global dollar volumes increased as a number of megadeals were announced. Despite a decrease in the number of deals, a gradually improving outlook for the global economy appeared to give executives more confidence in moving forward with large-scale corporate actions.

North America and western Europe had the largest sequential increases in M&A volumes during the period. Although the number of deals declined slightly in the region, western Europe displayed the most notable increase in terms of total deal value, in large part because of an improved economic environment. Volumes also increased in emerging Asia, but developed Asia recorded the most notable decrease in total deal value during the period, despite a similar number of deals.

Telecommunications accounted for the largest volume of deals among the global industry groups as Verizon Communications announced that it would pay $130 billion for Vodafone Group’s 45% stake in Verizon Wireless. Compared to the prior year’s period, volumes increased notably in the banking, diversified financial services and real estate industries.

Opportunities in distressed debt investing remained limited. Highly leveraged institutions benefited from the low interest rate environment and the ease with which these companies were able to raise funds or refinance existing debt, and this trend contributed to a fairly low rate of corporate bankruptcies. In our view, the recent environment enabled companies with poor credit fundamentals to obtain financing, limiting the amount of distressed opportunities in the marketplace. As a result, the U.S. corporate default rate remained well below its historical average during the past six months. Although interest rates increased during the period, based on speculation that the Federal Reserve Board would begin to taper its bond buying program before the end of the year, spreads between high yield bonds and Treasuries remained narrow and below the historical average.

Despite the lack of reorganization opportunities, we managed to find a number of idiosyncratic investments in debt trading below par, select refinancing of leveraged companies and other situations where we identified value. Our

Semiannual Report | 7

ability to invest anywhere in the capital structure allows us to approach the space opportunistically, and we will continue to seek new opportunities that, in our opinion, provide favorable risk-reward profiles.

Investment Strategy

We follow a distinctive investment approach and can seek investments in distressed companies, merger arbitrage and special situations/undervalued stocks. The availability of investments at attractive prices in each of these categories varies with market cycles. Therefore, the percentage of the Fund’s assets invested in each of these areas will fluctuate as we attempt to take advantage of opportunities afforded by cyclical changes. We employ rigorous, fundamental analysis to find investment opportunities. In choosing investments, we look at the market price of an individual company’s securities relative to our evaluation of its asset value based on such factors as book value, cash flow potential, long-term earnings and earnings multiples. We may invest in distressed companies if we believe the market overreacted to adverse developments or failed to appreciate positive changes.

Manager’s Discussion

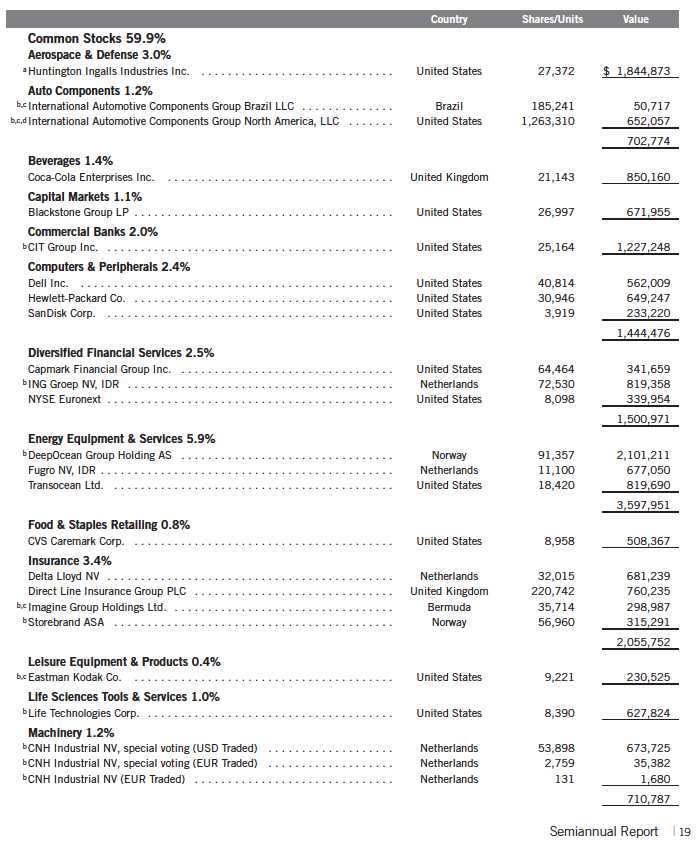

During the six months under review, top contributors to performance included investments in offshore engineering firm DeepOcean Group Holding, shipbuilder Huntington Ingalls Industries and energy exploration and production company WPX Energy.

Shares of DeepOcean appreciated during the period under review. The company operates in the offshore energy industry and provides seabed mapping and subsea services, including installation, inspection, maintenance, repair and decommissioning. The Fund originally invested in the secured debt of a legacy holding company and subsequently participated in a debt-for-equity exchange at the operating company that became the present DeepOcean. With a clean balance sheet, DeepOcean was able to execute on long-needed capital improvement projects while bringing working capital accounts back in line. The company’s stronger financial standing helped position DeepOcean to take advantage of increased business opportunities.

Huntington Ingalls builds nuclear submarines, aircraft carriers and amphibious assault ships for the U.S. Navy and also provides ship support services. The company continued to show signs that its turnaround was on track as earnings in the second quarter exceeded expectations. The Ingalls unit, where the company has focused its turnaround efforts, showed further benefits of restructuring with results exceeding our expectations. In addition, management expressed further confidence that the company would return to a normalized margin level by 2015.

8 | Semiannual Report

Shares of WPX Energy rose during the period following a hedge fund’s disclosure that it acquired a 6.39% stake in the company with the intent to discuss ways of increasing shareholder value with management. We believe substantial hidden value resides in the company’s asset base, which could potentially be unlocked in asset sales or by other means. We were also encouraged by company management’s recent ability to make progress in resolving operational challenges and continued to view the company’s solid balance sheet and attractive asset base favorably.

Several Fund holdings negatively affected performance during the period under review. Key detractors included investments in specialty telecommunications company Sorenson Communications, offshore drilling firm Transocean and gaming company Echo Entertainment Group.

Sorenson Communications is the largest U.S. company providing videophones, applications and video relay services to the hearing impaired. The company’s systems allow users to place and receive calls through a professional American Sign Language interpreter, providing deaf and hard-of-hearing individuals the functional equivalent of a voice telephone. Our investment in Sorenson debt declined following the Federal Communications Commission’s July announcement that it would cut reimbursement rates for telecommunications relay services.

Transocean owns the world’s largest offshore drilling fleet and has been dogged by planned and unplanned out-of-service time that negatively affected profitability. In response, the company took numerous steps to rein in costs including a $300 million restructuring program to rationalize the company’s shore-based expenses. However, in the reporting period, operational inefficiencies outweighed the cost-cutting program and impacted Transocean’s share price. At period-end, we believed that Transocean shares traded at a discount to its net asset value and that shareholders could potentially benefit from recently announced initiatives, including further cost reductions and an enhanced dividend.

The Fund purchased shares in Echo Entertainment, an Australian gaming company, when competitors Crown Limited and Genting Group acquired material stakes in the company and filed for regulatory approval to acquire additional shares. We believed that a competitive bidding war for Echo was likely as both potential bidders had logical reasons for acquiring Echo. However, the situation changed abruptly, and Crown chose instead to pursue a development project enabling it to compete with Echo in the core Sydney market. Genting continues to be a material shareholder, but has shown no interest in obtaining control of Echo. We liquidated our position in Echo shares by period-end.

Semiannual Report | 9

10 | Semiannual Report

Semiannual Report | 11

12 | Semiannual Report

Semiannual Report | 13

14 | Semiannual Report

Semiannual Report | 15

Franklin Mutual Recovery Fund

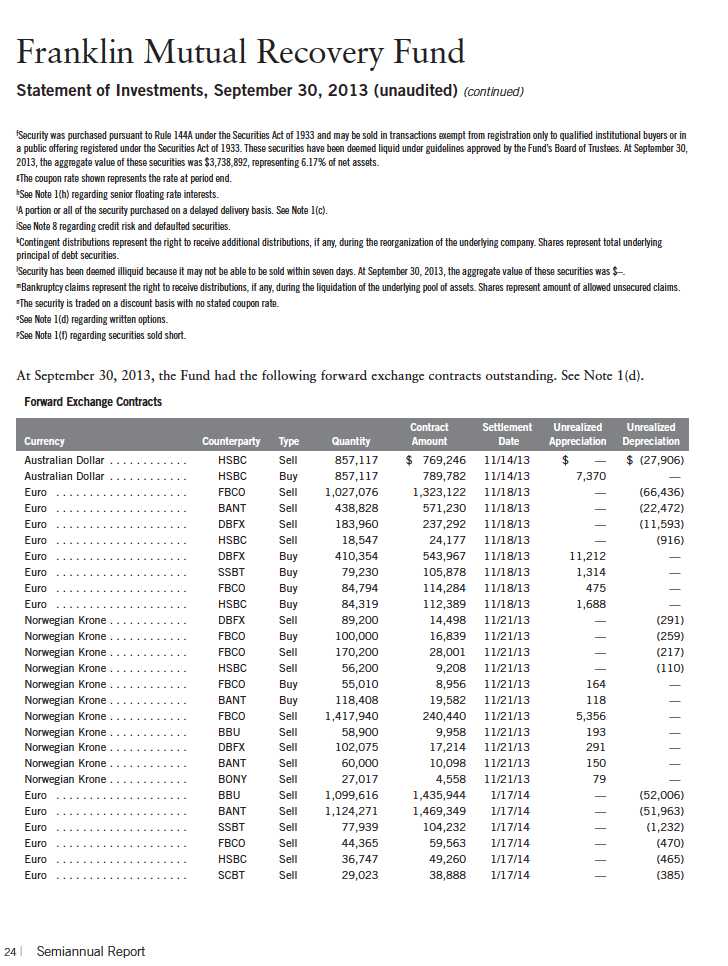

Statement of Investments, September 30, 2013 (unaudited)

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 25

26 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 27

28 | The accompanying notes are an integral part of these financial statements. | Semiannual Report

Semiannual Report | The accompanying notes are an integral part of these financial statements. | 29

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES

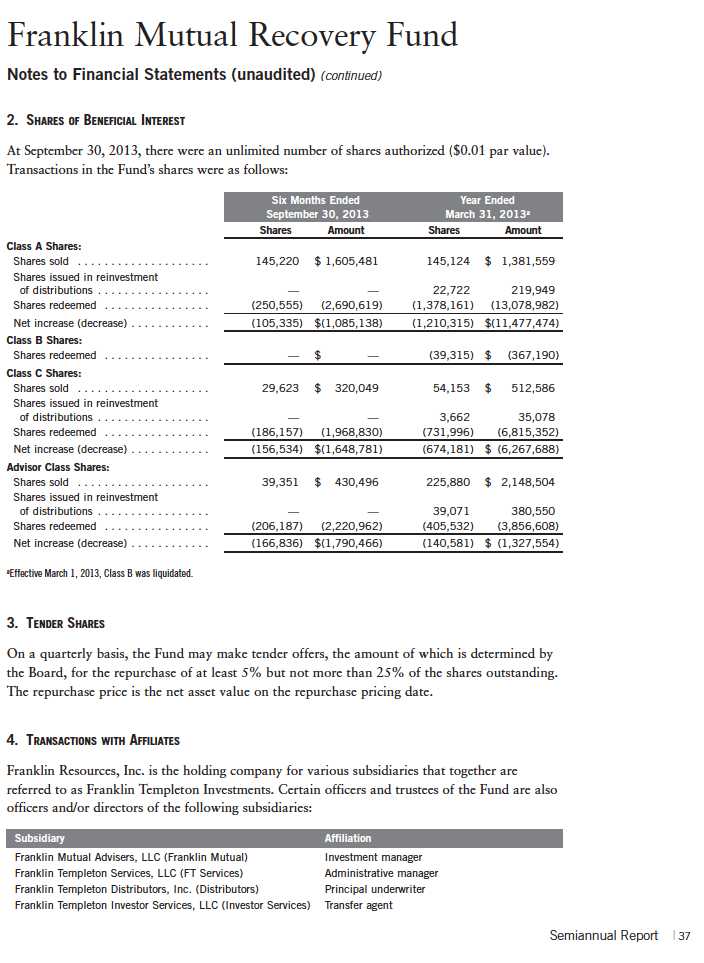

The Franklin Mutual Recovery Fund (Fund) is registered under the Investment Company Act of 1940, as amended, (1940 Act) as a closed-end, continuously offered investment company. The Fund offers three classes of shares: Class A, Class C, and Advisor Class. Each class of shares differs by its initial sales load, contingent deferred sales charges, voting rights on matters affecting a single class, its exchange privilege and fees primarily due to differing arrangements for distribution and transfer agent fees.

The following summarizes the Fund’s significant accounting policies.

a. Financial Instrument Valuation

The Fund’s investments in financial instruments are carried at fair value daily. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants on the measurement date. Under procedures approved by the Fund’s Board of Trustees (the Board), the Fund’s administrator, investment manager and other affiliates have formed the Valuation and Liquidity Oversight Committee (VLOC). The VLOC provides administration and oversight of the Fund’s valuation policies and procedures, which are approved annually by the Board. Among other things, these procedures allow the Fund to utilize independent pricing services, quotations from securities and financial instrument dealers, and other market sources to determine fair value.

Equity securities and derivative financial instruments (derivatives) listed on an exchange or on the NASDAQ National Market System are valued at the last quoted sale price or the official closing price of the day, respectively. Foreign equity securities are valued as of the close of trading on the foreign stock exchange on which the security is primarily traded, or the NYSE, whichever is earlier. The value is then converted into its U.S. dollar equivalent at the foreign exchange rate in effect at the close of the NYSE on the day that the value of the security is determined. Over-the-counter (OTC) securities are valued within the range of the most recent quoted bid and ask prices. Securities that trade in multiple markets or on multiple exchanges are valued according to the broadest and most representative market. Certain equity securities are valued based upon fundamental characteristics or relationships to similar securities.

Debt securities generally trade in the OTC market rather than on a securities exchange. The Fund’s pricing services use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the pricing services may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the pricing services also utilize proprietary valuation models which may consider market characteristics such as benchmark yield curves, credit spreads, estimated default rates, anticipated market interest rate volatility, coupon rates, anticipated timing of principal repayments, underlying collateral, and other unique security features in order to estimate the relevant cash flows, which are then discounted to calculate the fair value. Securities denominated in a foreign currency are converted into their U.S. dollar

30 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| b. | Foreign Currency Translation |

Portfolio securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollars based on the exchange rate of such currencies against U.S. dollars on the date of valuation. The Fund may enter into foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of securities, income and expense items denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date. Portfolio securities and assets and liabilities denominated in foreign currencies contain risks that those currencies will decline in value relative to the U.S. dollar. Occasionally, events may impact the availability or reliability of foreign exchange rates used to convert the U.S. dollar equivalent value. If such an event occurs, the foreign exchange rate will be valued at fair value using procedures established and approved by the Board.

The Fund does not separately report the effect of changes in foreign exchange rates from changes in market prices on securities held. Such changes are included in net realized and unrealized gain or loss from investments on the Statement of Operations.

Realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions and the difference between the recorded amounts of dividends, interest, and foreign withholding taxes and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in foreign exchange rates on foreign denominated assets and liabilities other than investments in securities held at the end of the reporting period.

c. Securities Purchased on a Delayed Delivery Basis

The Fund purchases securities on a delayed delivery basis, with payment and delivery scheduled for a future date. These transactions are subject to market fluctuations and are subject to the risk that the value at delivery may be more or less than the trade date purchase price. Although the Fund will generally purchase these securities with the intention of holding the securities, it may sell the securities before the settlement date. Sufficient assets have been segregated for these securities.

d. Derivative Financial Instruments

The Fund invested in derivatives in order to manage risk or gain exposure to various other investments or markets. Derivatives are financial contracts based on an underlying or notional amount, require no initial investment or an initial net investment that is smaller than would normally be required to have a similar response to changes in market factors, and require or permit net settlement. Derivatives contain various risks including the potential inability of the counterparty to fulfill their obligations under the terms of the contract, the potential for an illiquid secondary market, and/or the potential for market movements which expose the Fund to gains or losses in excess of the amounts shown on the Statement of Assets and Liabilities. Realized gain and loss and unrealized appreciation and depreciation on these contracts for the period are included in the Statement of Operations.

32 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| d. | Derivative Financial Instruments (continued) |

Derivative counterparty credit risk is managed through a formal evaluation of the creditworthiness of all potential counterparties. The Fund attempts to reduce its exposure to counterparty credit risk on OTC derivatives, whenever possible, by entering into International Swaps and Derivatives Association (ISDA) master agreements with certain counterparties. These agreements contain various provisions, including but not limited to collateral requirements, events of default, or early termination. Termination events applicable to the counterparty include certain deteriorations in the credit quality of the counterparty. Termination events applicable to the Fund include failure of the Fund to maintain certain net asset levels and/or limit the decline in net assets over various periods of time. In the event of default or early termination, the ISDA master agreement gives the non-defaulting party the right to net and close-out all transactions traded, whether or not arising under the ISDA agreement, to one net amount payable by one counterparty to the other. However, absent an event of default or early termination, OTC derivative assets and liabilities are presented gross and not offset in the Statement of Assets and Liabilities. Early termination by the counter-party may result in an immediate payment by the Fund of any net liability owed to that counter-party under the ISDA agreement.

Collateral requirements differ by type of derivative. Collateral or initial margin requirements are set by the broker or exchange clearing house for exchange traded and centrally cleared derivatives. Initial margin deposited is held at the exchange and can be in the form of cash and/or securities. For OTC derivatives traded under an ISDA master agreement, posting of collateral is required by either the Fund or the applicable counterparty if the total net exposure of all OTC derivatives with the applicable counterparty exceeds the minimum transfer amount, which typically ranges from $100,000 to $250,000, and can vary depending on the counter-party and the type of the agreement. Generally, collateral is determined at the close of fund business each day and any additional collateral required due to changes in derivative values may be delivered by the Fund or the counterparty within a few business days. Collateral pledged and/or received by the Fund for OTC derivatives, if any, is held in segregated accounts with the Fund’s custodian/counterparty broker and can be in the form of cash and/or securities. Unrestricted cash may be invested according to the Fund’s investment objectives.

The Fund entered into OTC forward exchange contracts primarily to manage exposure to certain foreign currencies. A forward exchange contract is an agreement between the Fund and a counter-party to buy or sell a foreign currency at a specific exchange rate on a future date.

The Fund purchased or wrote exchange traded and/or OTC option contracts primarily to manage and/or gain exposure to equity price, interest rate and foreign exchange rate risk. An option is a contract entitling the holder to purchase or sell a specific amount of shares or units of an asset or notional amount of a swap (swaption), at a specified price. Options purchased are recorded as an asset while options written are recorded as a liability. Upon exercise of an option, the acquisition cost or sales proceeds of the underlying investment is adjusted by any premium received or paid.

Semiannual Report | 33

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| d. | Derivative Financial Instruments (continued) |

Upon expiration of an option, any premium received or paid is recorded as a realized gain or loss. Upon closing an option other than through expiration or exercise, the difference between the premium and the cost to close the position is recorded as a realized gain or loss.

See Notes 7 and 10 regarding investment transactions and other derivative information, respectively.

e. Restricted Cash

At September 30, 2013, the Fund received restricted cash in connection with investments in certain derivative securities. Restricted cash is held in a segregated account with the Fund’s custodian/counterparty broker and is reflected in the Statement of Assets and Liabilities.

f. Securities Sold Short

The Fund is engaged in selling securities short, which obligates the Fund to replace a borrowed security with the same security at current market value. The Fund incurs a loss if the price of the security increases between the date of the short sale and the date on which the Fund replaces the borrowed security. The Fund realizes a gain if the price of the security declines between those dates. Gains are limited to the price at which the Fund sold the security short, while losses are potentially unlimited in size.

The Fund is required to establish a margin account with the broker lending the security sold short. While the short sale is outstanding, the broker retains the proceeds of the short sale and the Fund must maintain a deposit with the broker consisting of cash and/or securities having a value equal to a specified percentage of the value of the securities sold short. The Fund is obligated to pay fees for borrowing the securities sold short and is required to pay the counterparty any dividends or interest due on securities sold short. Such dividends or interest and any security borrowing fees are recorded as an expense to the Fund.

g. Securities Lending

The Fund participates in an agency based securities lending program. The Fund receives cash collateral against the loaned securities in an amount equal to at least 102% of the market value of the loaned securities. Collateral is maintained over the life of the loan in an amount not less than 100% of the market value of loaned securities, as determined at the close of fund business each day; any additional collateral required due to changes in security values is delivered to the Fund on the next business day. The collateral is invested in a non-registered money fund. The Fund receives income from the investment of cash collateral, in addition to lending fees and rebates paid by the borrower. The Fund bears the market risk with respect to the collateral investment, securities loaned, and the risk that the agent may default on its obligations to the Fund. The securities lending agent has agreed to indemnify the Fund in the event of default by a third party borrower. At September 30, 2013, the Fund had no securities on loan.

34 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| h. | Senior Floating Rate Interests |

The Fund invests in senior secured corporate loans that pay interest at rates which are periodically reset by reference to a base lending rate plus a spread. These base lending rates are generally the prime rate offered by a designated U.S. bank or the London InterBank Offered Rate (LIBOR). Senior secured corporate loans often require prepayment of principal from excess cash flows or at the discretion of the borrower. As a result, actual maturity may be substantially less than the stated maturity.

Senior secured corporate loans in which the Fund invests are generally readily marketable, but may be subject to certain restrictions on resale.

i. Income and Deferred Taxes

It is the Fund’s policy to qualify as a regulated investment company under the Internal Revenue Code. The Fund intends to distribute to shareholders substantially all of its taxable income and net realized gains to relieve it from federal income and excise taxes. As a result, no provision for U.S. federal income taxes is required.

The Fund may be subject to foreign taxation related to income received, capital gains on the sale of securities and certain foreign currency transactions in the foreign jurisdictions in which it invests. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in the foreign markets in which the Fund invests. When a capital gain tax is determined to apply the Fund records an estimated deferred tax liability in an amount that would be payable if the securities were disposed of on the valuation date.

The Fund recognizes the tax benefits of uncertain tax positions only when the position is “more likely than not” to be sustained upon examination by the tax authorities based on the technical merits of the tax position. As of September 30, 2013, and for all open tax years, the Fund has determined that no liability for unrecognized tax benefits is required in the Fund’s financial statements related to uncertain tax positions taken on a tax return (or expected to be taken on future tax returns). Open tax years are those that remain subject to examination and are based on each tax jurisdiction statute of limitation.

j. Security Transactions, Investment Income, Expenses and Distributions

Security transactions are accounted for on trade date. Realized gains and losses on security transactions are determined on a specific identification basis. Interest income and estimated expenses are accrued daily. Amortization of premium and accretion of discount on debt securities are included in interest income. Dividend income and dividends declared on securities sold short are recorded on the ex-dividend date except that certain dividends from foreign securities are recognized as soon as the Fund is notified of the ex-dividend date. Distributions to shareholders are recorded on the ex-dividend date and are determined according to income

Semiannual Report | 35

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES (continued) |

| j. | Security Transactions, Investment Income, Expenses and Distributions (continued) |

tax regulations (tax basis). Distributable earnings determined on a tax basis may differ from earnings recorded in accordance with accounting principles generally accepted in the United States of America. These differences may be permanent or temporary. Permanent differences are reclassified among capital accounts to reflect their tax character. These reclassifications have no impact on net assets or the results of operations. Temporary differences are not reclassified, as they may reverse in subsequent periods.

Realized and unrealized gains and losses and net investment income, not including class specific expenses, are allocated daily to each class of shares based upon the relative proportion of net assets of each class. Differences in per share distributions, by class, are generally due to differences in class specific expenses.

Distributions received by the Fund from certain securities may be a return of capital (ROC). Such distributions reduce the cost basis of the securities, and any distributions in excess of the cost basis are recognized as capital gains.

k. Accounting Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

l. Guarantees and Indemnifications

Under the Fund’s organizational documents, its officers and trustees are indemnified by the Fund against certain liabilities arising out of the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts with service providers that contain general indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. Currently, the Fund expects the risk of loss to be remote.

36 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

| 4. | TRANSACTIONS WITH AFFILIATES (continued) |

| a. | Management Fees |

The Fund pays Franklin Mutual an investment management fee comprised of a “base fee” and a “performance adjustment”. The base fee is calculated at the beginning of each month using an annual rate of 1.50% of the prior month’s average daily net assets. The performance adjustment is calculated at the beginning of each month based on how much the Fund’s total return exceeded or lagged its performance fee index, the Bloomberg/EFFAS U.S. Government 3-5 Years Total Return Index (Fund performance differential), over the preceding twelve-month period (performance period). A performance adjustment is applicable if the Fund performance differential exceeds 1.00%, either upwards (an increase to the base fee) or downwards (a decrease to the base fee). The performance adjustment rate is equal to 0.01% for each additional 0.05% that the Fund performance differential exceeds 1.00%. The performance adjustment amount is determined by multiplying the performance adjustment rate by the average daily net assets of the performance period. The performance adjustment rate may not exceed 1.00% annualized, either upwards or downwards. At the end of each month, an annualized investment management fee ratio is calculated (total investment management fees divided by fiscal year to date average daily net assets). In accordance with the Investment Management Agreement, the investment management fee ratio may not exceed 2.50% or fall below 0.50% for the fiscal year. For the period, the total annualized management fee rate, including the performance adjustment, and prior to any expense waiver, was 2.49% of the average daily net assets of the Fund.

Franklin Mutual has contractually agreed to waive or limit its fees so that the management fees paid by the Fund do not exceed an annual rate of 0.50% of the Fund’s average daily net assets through July 31, 2014.

b. Administrative Fees

The Fund pays administrative fees to FT Services of 0.20% per year of the average daily net assets of the Fund.

c. Distribution Fees

The Board has adopted distribution plans for each share class, with the exception of Advisor Class shares, pursuant to Rule 12b-1 under the 1940 Act. Distribution fees are not charged on shares held by affiliates. Under the Fund’s Class A reimbursement distribution plan, the Fund reimburses Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate. Under the Class A reimbursement distribution plan, costs exceeding the maximum for the current plan year cannot be reimbursed in subsequent periods. In addition, under the Fund’s Class C compensation distribution plan, the Fund pays Distributors for costs incurred in connection with the servicing, sale and distribution of the Fund’s shares up to the maximum annual plan rate. The plan year, for purposes of monitoring compliance with the maximum annual plan rates, is February 1 through January 31.

38 | Semiannual Report

Semiannual Report | 39

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

5. EXPENSE OFFSET ARRANGEMENT

The Fund has entered into an arrangement with its custodian whereby credits realized as a result of uninvested cash balances are used to reduce a portion of the Fund’s custodian expenses. During the period ended September 30, 2013, there were no credits earned.

6. INCOME TAXES

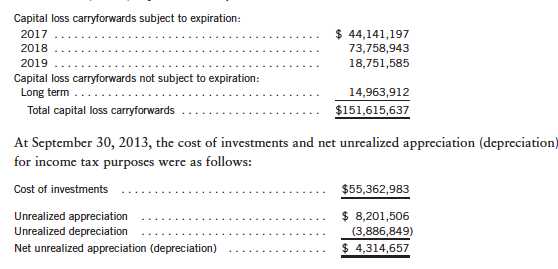

For tax purposes, capital losses may be carried over to offset future capital gains. Capital loss carryforwards with no expiration, if any, must be fully utilized before those losses with expiration dates.

At March 31, 2013, capital loss carryforwards were as follows:

Differences between income and/or capital gains as determined on a book basis and a tax basis are primarily due to differing treatments of defaulted securities, foreign currency transactions, passive foreign investment company shares, pass-through entity income, bond discounts and premiums and corporate actions.

7. INVESTMENT TRANSACTIONS

Purchases and sales of investments (excluding short term securities and securities sold short) for the period ended September 30, 2013, aggregated $16,635,699 and $15,091,832, respectively.

40 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

7. INVESTMENT TRANSACTIONS (continued)

Transactions in options written during the period ended September 30, 2013, were as follows:

See Notes 1(d) and 10 regarding derivative financial instruments and other derivative information, respectively.

8. CREDIT RISK AND DEFAULTED SECURITIES

The Fund may purchase the pre-default or defaulted debt of distressed companies. Distressed companies are financially troubled and are about to be or are already involved in financial restructuring or bankruptcy. Risks associated with purchasing these securities include the possibility that the bankruptcy or other restructuring process takes longer than expected, or that distributions in restructuring are less than anticipated, either or both of which may result in unfavorable consequences to the Fund. If it becomes probable that the income on debt securities, including those of distressed companies, will not be collected, the Fund discontinues accruing income and recognizes an adjustment for uncollectible interest.

At September 30, 2013, the aggregate value of distressed company securities for which interest recognition has been discontinued was $4,830,880, representing 7.97% of the Fund’s net assets. For information as to specific securities, see the accompanying Statement of Investments.

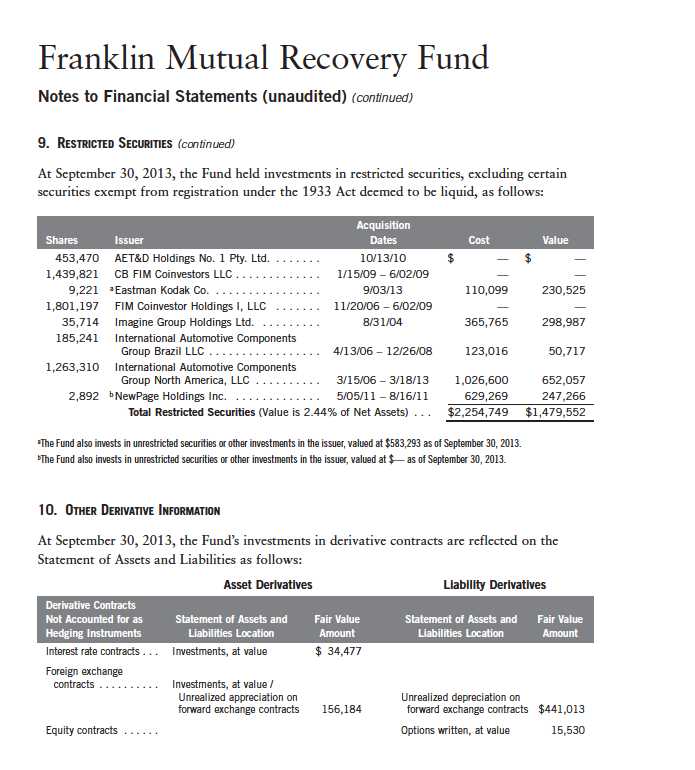

9. RESTRICTED SECURITIES

The Fund invests in securities that are restricted under the Securities Act of 1933 (1933 Act) or which are subject to legal, contractual, or other agreed upon restrictions on resale. Restricted securities are often purchased in private placement transactions, and cannot be sold without prior registration unless the sale is pursuant to an exemption under the 1933 Act. Disposal of these securities may require greater effort and expense, and prompt sale at an acceptable price may be difficult. The Fund may have registration rights for restricted securities. The issuer generally incurs all registration costs.

Semiannual Report | 41

42 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

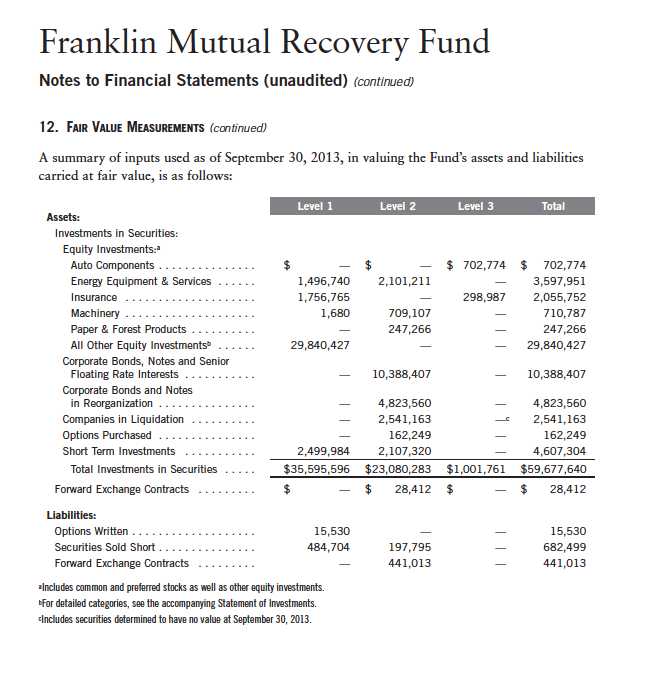

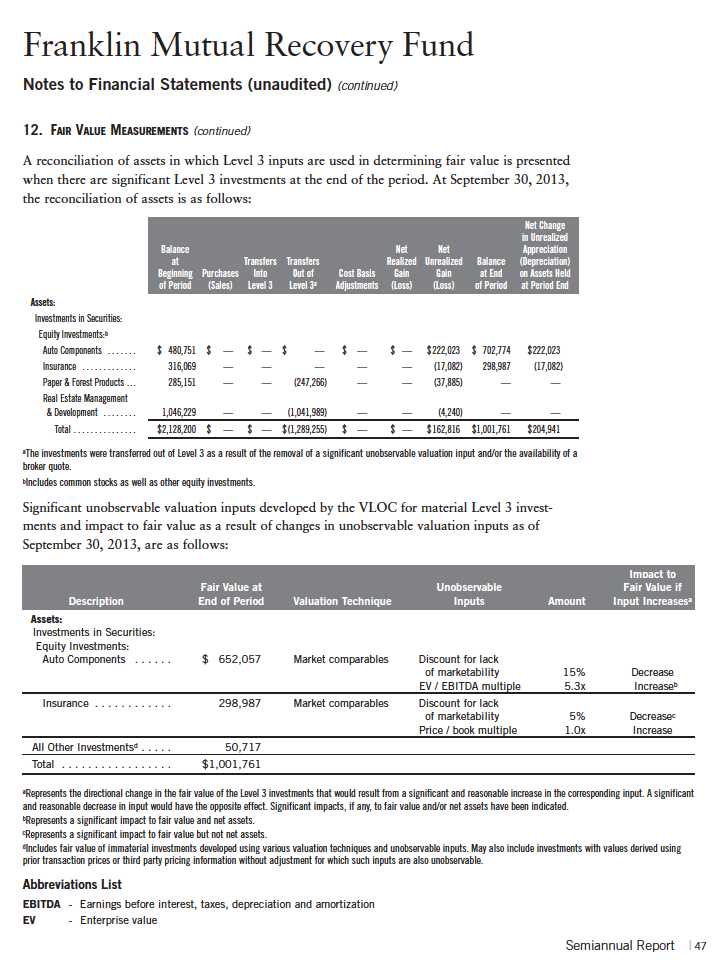

10. OTHER DERIVATIVE INFORMATION (continued)

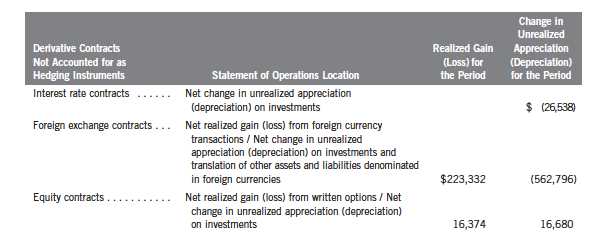

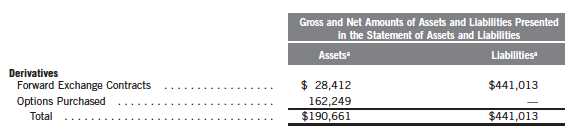

For the period ended September 30, 2013, the effect of derivative contracts on the Fund’s Statement of Operations was as follows:

For the period ended September 30, 2013, the average month end fair value of derivatives represented 0.86% of average month end net assets. The average month end number of open derivative contracts for the period was 77.

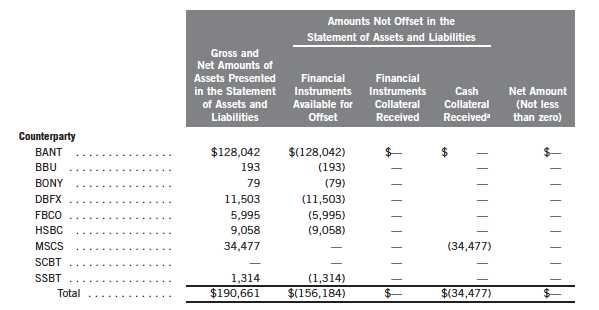

At September 30, 2013, the Fund’s OTC derivative assets and liabilities are as follows:

aAbsent an event of default or early termination, OTC derivative assets and liabilities are presented gross and not offset in the Statement of Assets and Liabilities.

Semiannual Report | 43

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

10. OTHER DERIVATIVE INFORMATION (continued)

At September 30, 2013, the Fund’s OTC derivative assets which may be offset against the Fund’s derivative liabilities, and collateral received from the counterparty, is as follows:

aIn some instances, the collateral amount disclosed in the table above was adjusted due to the requirement to limit the collateral amount to avoid the effect of overcollateralization. Actual collateral received and/or pledged may be more than the amount disclosed herein.

At September 30, 2013, the Fund’s OTC derivative liabilities which may be offset against the Fund’s derivative assets, and collateral pledged to the counterparty, is as follows:

44 | Semiannual Report

Semiannual Report | 45

46 | Semiannual Report

Franklin Mutual Recovery Fund

Notes to Financial Statements (unaudited) (continued)

13. NEW ACCOUNTING PRONOUNCEMENTS

In June 2013, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2013-08, Investment Companies (Topic 946): Amendments to the Scope, Measurement, and Disclosure Requirements. The ASU modifies the criteria used in defining an investment company under U.S. Generally Accepted Accounting Principles and also sets forth certain measurement and disclosure requirements. Under the ASU, an entity that is registered under the 1940 Act automatically qualifies as an investment company. The ASU is effective for interim and annual reporting periods beginning after December 15, 2013. The Fund is currently reviewing the requirements and believes the adoption of this ASU will not have a material impact on its financial statements.

14. SUBSEQUENT EVENTS

The Fund evaluated subsequent events through the issuance of the financial statements and determined that no events have occurred that require disclosure.

48 | Semiannual Report

Franklin Mutual Recovery Fund

Shareholder Information

Board Review of Investment Management Agreements

The Board of Trustees (Board), including the independent trustees, at a Board meeting held on May 21, 2013, unanimously approved renewal of the Fund’s investment management agreement, as well as the Fund’s administrative services agreement, after negotiating with management the continuation of the existing cap on the investment management fee and on total expenses, each as more fully discussed below. Prior to a meeting of all of the trustees for the purpose of considering such renewals, the independent trustees held two meetings dedicated to the renewal process (those trustees unable to attend in person were present by telephonic conference means). Throughout the process, the independent trustees received assistance and advice from and met separately with independent counsel. The independent trustees met with and interviewed officers of the investment manager (including portfolio managers), the transfer agent and shareholder services group and the distributor. In approving the renewal of the investment management agreement and the administrative services agreement for the Fund, the Board, including the independent trustees, determined that, taking into account the caps on the investment management fee and total expenses, the investment management fee structure was fair and reasonable and that continuance of the agreements was in the best interests of the Fund and its shareholders.

In reaching their decision on the investment management agreement (as well as the administrative services agreement), the trustees took into account information furnished throughout the year at regular Board meetings, as well as information specifically requested and furnished for the renewal process, which culminated in the meetings referred to above for the specific purpose of considering such agreements. Information furnished throughout the year included, among others, reports on the Fund’s investment performance, expenses, portfolio composition, portfolio brokerage execution, client commission arrangements, derivatives, securities lending, portfolio turnover, Rule 12b-1 plans, distribution, shareholder servicing, legal and compliance matters, pricing of securities and sales and redemptions, as well as a third-party survey of transfer agent fees charged to funds within the Franklin Templeton Investments complex in comparison with those charged to other fund complexes deemed comparable. Also, related financial statements and other information about the scope and quality of services provided by the investment manager and its affiliates and enhancements to such services over the past year were provided. In addition, the trustees received periodic reports throughout the year and during the renewal process relating to compliance with the Fund’s investment policies and restrictions. During the renewal process, the independent trustees considered the investment manager’s methods of operation within the Franklin Templeton group and its activities on behalf of other clients.

In addition, the trustees received a Profitability Study (Profitability Study) prepared by management discussing the profitability to Franklin Templeton Investments from its overall U.S. fund operations, as well as on an individual fund-by-fund basis.

Over the past year, the Board and counsel to the independent trustees continued to receive reports on management’s handling of recent regulatory inquiries and pending legal actions against the investment manager and its affiliates. The independent trustees were satisfied with the actions taken to date by management in response to such regulatory and legal proceedings.

Semiannual Report | 49

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

Particular attention was given to management’s diligent risk management procedures, including continuous monitoring of counterparty credit risk and attention given to derivatives and other complex instruments. The Board also took into account, among other things, the strong financial position of the investment manager’s parent company and its commitment to the mutual fund business. In addition, the Board received updates from management on the Securities and Exchange Commission’s (SEC) progress in implementing the rule making requirements established by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act), which was enacted July 21, 2010, and the investment manager’s compliance with rules and regulations already promulgated by the SEC under such act.

In addition to the above and other matters considered by the trustees throughout the course of the year, the following discussion relates to certain primary factors relevant to the Board’s decision. This discussion of the information and factors considered by the Board (as well as the discussion above) is not intended to be exhaustive, but rather summarizes certain factors considered by the Board. In view of the wide variety of factors considered, the Board did not, unless otherwise noted, find it practicable to quantify or otherwise assign relative weights to the foregoing factors. In addition, individual trustees may have assigned different weights to various factors.

NATURE, EXTENT AND QUALITY OF SERVICES. The trustees reviewed the nature, extent and quality of the services provided by the investment manager. In this regard, they reviewed the Fund’s investment approach and concluded that, in their view, it continues to differentiate the Fund from typical core investment products in the mutual fund field. The trustees cited the investment manager’s ability to implement the Fund’s disciplined value investment approach and its long-term relationship with the Fund since the Fund’s inception nine and one-half years ago as reasons that shareholders choose to invest, and remain invested, in the Fund. The trustees reviewed the Fund’s portfolio management team, including its performance, staffing, skills and compensation program. With respect to portfolio manager compensation, management assured the trustees that the Fund’s longer term performance is a significant component of incentive-based compensation and noted that a portion of a portfolio manager’s incentive-based compensation is paid in shares of predesignated funds from the portfolio manager’s fund management area. The trustees noted that the portfolio manager compensation program aligned the interests of the portfolio managers with that of Fund shareholders. The trustees discussed with management various other products, portfolios and entities that are advised by the investment manager and the allocation of assets and expenses among and within them, as well as their relative fees and reasons for differences with respect thereto and any potential conflicts. During regular Board meetings and the aforementioned meetings of the independent trustees, the trustees received reports and presentations on the investment manager’s best execution trading policies. The trustees considered periodic reports provided to them showing that the investment manager complied with the investment policies and restrictions of the Fund as well as other reports periodically furnished to the Board covering matters such as the compliance of portfolio managers and other management personnel with the code of ethics covering the investment management personnel, the adherence

50 | Semiannual Report

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

to fair value pricing procedures established by the Board and the accuracy of net asset value calculations. The Board noted the extent of the benefits provided to Fund shareholders from being part of the Franklin Templeton group, including the right to exchange investments between funds (same class) without a sales charge, the ability to reinvest Fund dividends into other funds and the right to combine holdings of other funds to obtain reduced sales charges. The trustees considered the investment manager’s substantial efforts in developing and implementing compliance procedures established in accordance with SEC and other requirements. The trustees also reviewed the nature, extent and quality of the Fund’s other service agreements to determine that, on an overall basis, Fund shareholders were well served. In this connection, the Board also took into account administrative and transfer agent and shareholder services provided to Fund shareholders by an affiliate of the investment manager, noting continuing expenditures by management to increase and improve the scope of such services and favorable periodic reports on shareholder services conducted by independent third parties. While such considerations directly affected the trustees’ decision in renewing the Fund’s administrative services and transfer agent and shareholder services agreement, the Board also considered these commitments as incidental benefits to Fund shareholders deriving from the investment management relationship.

Based on their review, the trustees were satisfied with the nature and quality of the overall services provided by the investment manager and its affiliates to the Fund and its shareholders and were confident in the abilities of the management team to continue the disciplined value investment approach of the Fund and to provide quality services to the Fund and its shareholders.

INVESTMENT PERFORMANCE. The trustees reviewed and placed significant emphasis on the investment performance of the Fund. In this context, the trustees believed that it is difficult to find open- or closed-end funds that are truly comparable to the Fund due, in part, to the unique nature of the Fund as a closed-end interval fund investing in the categories of bankruptcy and distressed companies, merger arbitrage and undervalued stocks and debt instruments. They considered the performance of the Fund over the past nine and one-half years since formation of the Fund relative to various benchmarks. As part of their review, they inquired of management regarding benchmarks (including the benchmark on which the Fund’s performance adjustment fee is based), style drift and restrictions on permitted investments. Consideration was also given to performance in the context of available levels of cash during the periods.

The trustees had meetings during the year, including the meetings referred to above held in connection with the renewal process, with the Fund’s portfolio managers to discuss performance. The Board reviewed the Fund’s annualized total returns (Class A shares) for the one-, three- and five-year periods ended December 31, 2012, and discussed with the investment manager the reasons for the Fund’s underperformance relative to various benchmarks over certain of these periods. After discussing the Fund’s performance and after considering various options and other factors, including, but, not limited to, the Fund’s expense ratios, the Board negotiated, as more fully discussed below, to retain the existing caps on the Fund’s investment management fee and on the Fund’s total expenses.

Semiannual Report | 51

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

COMPARATIVE EXPENSES AND MANAGEMENT PROFITABILITY. The trustees considered the cost of the services provided and to be provided and the profits realized by the investment manager and its affiliates from their respective relationships with the Fund. As part of the approval process, they explored with management the trends in expense ratios over the past three fiscal years and the reasons for any increase in the Fund’s expenses ratios (both including and excluding the performance adjustment fee). The trustees also compared the Fund’s fees to the fees charged to other accounts managed by the investment manager.

The trustees noted that the Fund’s investment management fee is comprised of two components, a base fee and a performance adjustment to the base fee. The adjustment is based on the Fund’s performance relative to the Bloomberg/EFFAS U.S. Government 3-5 Years Total Return Index (Index) over a rolling 12-month period ending with the most recently completed month (Performance Period). The first component of the fee is a base fee equal to an annual rate of 1.50% of the Fund’s average daily net assets during the month that ends on the last day of the Performance Period. The second component is a performance adjustment that either increases or decreases the base fee, depending on how the Fund has performed relative to the Index over the Performance Period. The maximum annual investment management fee is 2.50% of average daily net assets over each fiscal year of the Fund, and the minimum annual investment management fee is 0.50% of average daily net assets over each fiscal year of the Fund.

As noted above, the trustees negotiated with management both the retention of the existing investment management fee cap of 0.50% of the Fund’s average daily net assets and the existing total expense ratio cap of 1.20% of the Fund’s average daily net assets (excluding Rule 12b-1 fees charged to the Fund and dividends and interest for securities sold short and other related expenses in connection with securities sold short). Each cap will remain in effect through July 31, 2014.

The trustees also reviewed the Profitability Study addressing profitability of Franklin Resources, Inc., from its overall U.S. fund business, as well as profitability to the Fund’s investment manager and its affiliates, from providing investment management and other services to the Fund during the 12-month period ended September 30, 2012, the then most recent fiscal year-end of Franklin Resources, Inc. The trustees reviewed the basis on which such reports are prepared and the cost allocation methodology utilized in the Profitability Study, it being recognized that allocation methodologies may each be reasonable while producing different results. In this respect, the Board noted that the reasonableness of the cost allocation methodologies was reviewed by independent accountants on an every other year basis.

52 | Semiannual Report

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Board Review of Investment Management Agreements (continued)

The independent trustees met with management to discuss the Profitability Study. This included, among other things, a comparison of investment management income with investment management expenses of the Fund; comparison of underwriting revenues and expenses; the relative relationship of investment management and underwriting expenses; shareholder servicing profitability (losses); economies of scale; and the relative contribution of the Fund to the profitability of the investment manager and its parent. In discussing the Profitability Study with the Board, the investment manager stated its belief that the costs incurred in establishing the infrastructure necessary to operate the type of mutual fund operations conducted by it and its affiliates may not be fully reflected in the expenses allocated to the Fund in determining its profitability.

The trustees considered a study by Lipper, Inc., an independent third-party analyst, analyzing the profitability of the parent of the investment manager as compared to other publicly held investment managers, which also aided the trustees in considering profitability excluding distribution costs. The Board also took into account management’s expenditures in improving shareholder services provided to the Fund, as well as the need to meet additional regulatory and compliance requirements resulting from the Sarbanes-Oxley Act, the Dodd-Frank Act and recent SEC and other regulatory requirements. The trustees also considered the extent to which the investment manager may derive ancillary benefits from Fund operations, including those derived from economies of scale, discussed below, the allocation of Fund brokerage and the use of commission dollars to pay for research and other similar services.

Based upon their consideration of all these factors, including, but not limited to, continuing the existing cap on the Fund’s investment management fee and cap on total expenses, the trustees determined that the level of profits realized by the investment manager and its affiliates in providing services to the Fund was not excessive in view of the nature, quality and extent of services provided.

ECONOMIES OF SCALE. The trustees considered that economies of scale may be realized by the investment manager and its affiliates as the Fund grows larger and the extent to which they are shared with Fund shareholders, as for example, in the level of the investment management fee charged, in the quality and efficiency of services rendered and in increased capital commitments benefiting the Fund directly or indirectly. Since the amount of assets under management of the Fund remains relatively small, the trustees concluded that economies of scale were difficult to consider at that time.

Semiannual Report | 53

Franklin Mutual Recovery Fund

Shareholder Information (continued)

Proxy Voting Policies and Procedures

The Fund’s investment manager has established Proxy Voting Policies and Procedures (Policies) that the Fund uses to determine how to vote proxies relating to portfolio securities. Shareholders may view the Fund’s complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 300 S.E. 2nd Street, Fort Lauderdale, FL 33301, Attention: Proxy Group. Copies of the Fund’s proxy voting records are also made available online at franklintempleton.com and posted on the U.S. Securities and Exchange Commission’s website at sec.gov and reflect the most recent 12-month period ended June 30.

Quarterly Statement of Investments

The Fund files a complete statement of investments with the U.S. Securities and Exchange Commission for the first and third quarters for each fiscal year on Form N-Q. Shareholders may view the filed Form N-Q by visiting the Commission’s website at sec.gov. The filed form may also be viewed and copied at the Commission’s Public Reference Room in Washington, DC. Information regarding the operations of the Public Reference Room may be obtained by calling (800) SEC-0330.

54 | Semiannual Report

This page intentionally left blank.

This page intentionally left blank.

Item 2. Code of Ethics.

(a) The Registrant has adopted a code of ethics that applies to its principal executive officers and principal financial and accounting officer.

| (c) | N/A |

| (d) | N/A |

| (f) | Pursuant to Item 12(a)(1), the Registrant is attaching as an exhibit a |

copy of its code of ethics that applies to its principal executive officers and principal financial and accounting officer.

Item 3. Audit Committee Financial Expert.

(a)(1) The Registrant has an audit committee financial expert serving on its audit committee.

(2) The audit committee financial expert is Ann Torre Bates and she is "independent" as defined under the relevant Securities and Exchange Commission Rules and Releases.

Item 4. Principal Accountant Fees and Services. N/A

Item 5. Audit Committee of Listed Registrants.

Members of the Audit Committee are: Edward I. Altman, Ann Torre Bates and Robert E. Wade.

Item 6. Schedule of Investments.

N/A

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

The board of trustees of the Fund has delegated the authority to vote proxies related to the portfolio securities held by the Fund to the Fund’s investment manager Franklin Mutual Advisers, LLC in accordance with the Proxy Voting Policies and Procedures (Policies) adopted by the investment manager.

The investment manager has delegated its administrative duties with respect to the voting of proxies to the Proxy Group within Franklin Templeton Companies, LLC (Proxy Group), an affiliate and wholly owned subsidiary of Franklin Resources, Inc. All proxies received by the Proxy Group will be voted based upon the investment manager’s instructions and/or policies. The investment manager votes proxies solely in the best interests of the Fund and its shareholders.

To assist it in analyzing proxies, the investment manager subscribes to Institutional Shareholder Services, Inc. (ISS), an unaffiliated third-party corporate governance research service that provides in-depth analyses of shareholder meeting agendas, vote recommendations, vote execution services, ballot reconciliation services, recordkeeping and vote disclosure services. In addition, the investment manager subscribes to Glass, Lewis & Co., LLC

(Glass Lewis), an unaffiliated third-party analytical research firm, to receive analyses and vote recommendations on the shareholder meetings of publicly held U.S. companies, as well as a limited subscription to its international research. Although ISS’ and/or Glass Lewis’ analyses are thoroughly reviewed and considered in making a final voting decision, the investment manager does not consider recommendations from ISS, Glass Lewis or any other third party to be determinative of the investment manager’s ultimate decision. As a matter of policy, the officers, directors/trustees and employees of the investment manager and the Proxy Group will not be influenced by outside sources whose interests conflict with the interests of the Fund and its shareholders. Efforts are made to resolve all conflicts in the best interests of the investment manager’s clients. Material conflicts of interest are identified by the Proxy Group based upon analyses of client, distributor, broker-dealer and vendor lists, information periodically gathered from directors and officers, and information derived from other sources, including public filings. In situations where a material conflict of interest is identified, the Proxy Group may defer to the voting recommendation of ISS, Glass Lewis or those of another independent third-party provider of proxy services; or send the proxy directly to the Fund's board or a committee of the board with the investment manager's recommendation regarding the vote for approval.

Where a material conflict of interest has been identified, but the items on which the investment manager’s vote recommendations differ from Glass Lewis, ISS, or another independent third-party provider of proxy services relate specifically to (1) shareholder proposals regarding social or environmental issues, (2) “Other Business” without describing the matters that might be considered, or (3) items the investment manager wishes to vote in opposition to the recommendations of an issuer’s management, the Proxy Group may defer to the vote recommendations of the investment manager rather than sending the proxy directly to the Fund's board or a board committee for approval.

To avoid certain potential conflicts of interest, the investment manager will employ echo voting, if possible, in the following instances: (1) when the Fund invests in an underlying fund in reliance on any one of Sections 12(d) (1) (E), (F), or (G) of the 1940 Act, the rules thereunder, or pursuant to a SEC exemptive order thereunder; (2) when the Fund invests uninvested cash in affiliated money market funds pursuant to the rules under the 1940 Act or any exemptive orders thereunder (“cash sweep arrangement”); or (3) when required pursuant to the Fund’s governing documents or applicable law. Echo voting means that the investment manager will vote the shares in the same proportion as the vote of all of the other holders of the Fund’s shares.

The recommendation of management on any issue is a factor that the investment manager considers in determining how proxies should be voted. However, the investment manager does not consider recommendations from management to be determinative of the investment manager’s ultimate decision. As a matter of practice, the votes with respect to most issues are cast in accordance with the position of the company's management. Each issue, however, is considered on its own merits, and the investment manager will not support the position of the company's management in any situation where it deems that the ratification of management’s position would adversely affect the investment merits of owning that company’s shares.

Investment manager’s proxy voting policies and principles The investment manager has adopted general proxy voting guidelines, which are summarized

below. These guidelines are not an exhaustive list of all the issues that may arise and the investment manager cannot anticipate all future situations. In all cases, each proxy will be considered based on the relevant facts and circumstances.

Board of directors. The investment manager supports an independent board of directors, and prefers that key committees such as audit, nominating, and compensation committees be comprised of independent directors. The investment manager will generally vote against management efforts to classify a board and will generally support proposals to declassify the board of directors. The investment manager will consider withholding votes from directors who have attended less than 75% of meetings without a valid reason. While generally in favor of separating Chairman and CEO positions, the investment manager will review this issue as well as proposals to restore or provide for cumulative voting on a case-by-case basis, taking into consideration factors such as the company’s corporate governance guidelines or provisions and performance. The investment manager generally will support non-binding shareholder proposals to require a majority vote standard for the election of directors; however, if these proposals are binding, the investment manager will give careful review on a case-by-case basis of the potential ramifications of such implementation.

In the event of a contested election, the investment manager will review a number of factors in making a decision including management’s track record, the company’s financial performance, qualifications of candidates on both slates, and the strategic plan of the dissidents.

Ratification of auditors of portfolio companies. The investment manager will closely scrutinize the independence, role and performance of auditors. On a case-by-case basis, the investment manager will examine proposals relating to non-audit relationships and non-audit fees. The investment manager will also consider, on a case-by-case basis, proposals to rotate auditors, and will vote against the ratification of auditors when there is clear and compelling evidence of a lack of independence, accounting irregularities or negligence. The investment manager may also consider whether the ratification of auditors has been approved by an appropriate audit committee that meets applicable composition and independence requirements.

Management and director compensation. A company’s equity-based compensation plan should be in alignment with the shareholders’ long-term interests. The investment manager believes that executive compensation should be directly linked to the performance of the company. The investment manager evaluates plans on a case-by-case basis by considering several factors to determine whether the plan is fair and reasonable, including the ISS quantitative model utilized to assess such plans and/or the Glass Lewis evaluation of the plans. The investment manager will generally oppose plans that have the potential to be excessively dilutive, and will almost always oppose plans that are structured to allow the repricing of underwater options, or plans that have an automatic share replenishment “evergreen” feature. The investment manager will generally support employee stock option plans in which the purchase price is at least 85% of fair market value, and when potential dilution is 10% or less.

Severance compensation arrangements will be reviewed on a case-by-case basis, although the investment manager will generally oppose “golden parachutes”

that are considered to be excessive. The investment manager will normally support proposals that require a percentage of directors’ compensation to be in the form of common stock, as it aligns their interests with those of shareholders.

The investment manager will review non-binding say-on-pay proposals on a case-by-case basis, and will generally vote in favor of such proposals unless compensation is misaligned with performance and/or shareholders’ interests, the company has not provided reasonably clear disclosure regarding its compensation practices, or there are concerns with the company’s remuneration practices.

Anti-takeover mechanisms and related issues. The investment manager generally opposes anti-takeover measures since they tend to reduce shareholder rights. However, as with all proxy issues, the investment manager conducts an independent review of each anti-takeover proposal. On occasion, the investment manager may vote with management when the research analyst has concluded that the proposal is not onerous and would not harm the Fund or its shareholders’ interests. The investment manager generally supports proposals that require shareholder rights’ plans (“poison pills”) to be subject to a shareholder vote and will closely evaluate such plans on a case-by-case basis to determine whether or not they warrant support. In addition, the investment manager will generally vote against any proposal to issue stock that has unequal or subordinate voting rights. The investment manager generally opposes any supermajority voting requirements as well as the payment of “greenmail.” The investment manager generally supports “fair price” provisions and confidential voting. The investment manager will review a company’s proposal to reincorporate to a different state or country on a case-by-case basis taking into consideration financial benefits such as tax treatment as well as comparing corporate governance provisions and general business laws that may result from the change in domicile.

Changes to capital structure. The investment manager realizes that a company's financing decisions have a significant impact on its shareholders, particularly when they involve the issuance of additional shares of common or preferred stock or the assumption of additional debt. The investment manager will review, on a case-by-case basis, proposals by companies to increase authorized shares and the purpose for the increase. The investment manager will generally not vote in favor of dual-class capital structures to increase the number of authorized shares where that class of stock would have superior voting rights. The investment manager will generally vote in favor of the issuance of preferred stock in cases where the company specifies the voting, dividend, conversion and other rights of such stock and the terms of the preferred stock issuance are deemed reasonable. The investment manager will review proposals seeking preemptive rights on a case-by-case basis.

Mergers and corporate restructuring. Mergers and acquisitions will be subject to careful review by the research analyst to determine whether they would be beneficial to shareholders. The investment manager will analyze various economic and strategic factors in making the final decision on a merger or acquisition. Corporate restructuring proposals are also subject to a thorough examination on a case-by-case basis.

Environment, social and governance issues. The investment manager will generally give management discretion with regard to social, environmental and ethical issues, although the investment manager may vote in favor of those

that are believed to have significant economic benefits or implications for the Fund and its shareholders. The investment manager generally supports the right of shareholders to call special meetings and act by written consent. However, the investment manager will review such shareholder proposals on a case-by-case basis in an effort to ensure that such proposals do not disrupt the course of business or waste company resources for the benefit of a small minority of shareholders. The investment manager will consider supporting a shareholder proposal seeking disclosure and greater board oversight of lobbying and corporate political contributions if the investment manager believes that there is evidence of inadequate oversight by the company’s board, if the company’s current disclosure is significantly deficient, or if the disclosure is notably lacking in comparison to the company’s peers. The investment manager will consider on a case-by-case basis any well-drafted and reasonable proposals for proxy access considering such factors as the size of the company, ownership thresholds and holding periods, responsiveness of management, intentions of the shareholder proponent, company performance, and shareholder base.

Global corporate governance. Many of the tenets discussed above are applied to the investment manager's proxy voting decisions for international investments. However, the investment manager must be flexible in these worldwide markets. Principles of good corporate governance may vary by country, given the constraints of a country’s laws and acceptable practices in the markets. As a result, it is on occasion difficult to apply a consistent set of governance practices to all issuers. As experienced money managers, the investment manager's analysts are skilled in understanding the complexities of the regions in which they specialize and are trained to analyze proxy issues germane to their regions.

The investment manager will generally attempt to process every proxy it receives for all domestic and foreign securities. However, there may be situations in which the investment manager may be unable to vote a proxy, or may choose not to vote a proxy, such as where: (i) the proxy ballot was not received from the custodian bank; (ii) a meeting notice was received too late; (iii) there are fees imposed upon the exercise of a vote and it is determined that such fees outweigh the benefit of voting; (iv) there are legal encumbrances to voting, including blocking restrictions in certain markets that preclude the ability to dispose of a security if the investment manager votes a proxy or where the investment manager is prohibited from voting by applicable law or other regulatory or market requirements, including but not limited to, effective Powers of Attorney; (v) the investment manager held shares on the record date but has sold them prior to the meeting date; (vi) proxy voting service is not offered by the custodian in the market; (vii) the investment manager believes it is not in the best interest of the Fund or its shareholders to vote the proxy for any other reason not enumerated herein; or (viii) a security is subject to a securities lending or similar program that has transferred legal title to the security to another person. The investment manager or its affiliates may, on behalf of one or more of the proprietary registered investment companies advised by the investment manager or its affiliates, determine to use its best efforts to recall any security on loan where the investment manager or its affiliates (a) learn of a vote on a material event that may affect a security on loan and (b) determine that it is in the best interests of such proprietary registered investment companies to recall the security for voting purposes.

Shareholders may view the complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923, Attention: Proxy Group. Copies of the Fund’s proxy voting records are available online at franklintempleton.com and posted on the SEC website at www.sec.gov. The proxy voting records are updated each year by August 31 to reflect the most recent 12-month period ended June 30.

Item 8. Portfolio Managers of Closed-End Management Investment Companies. N/A

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers. N/A

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no changes to the procedures by which shareholders may recommend nominees to the Registrant's Board of Trustees that would require disclosure herein.

Item 11. Controls and Procedures.

(a) Evaluation of Disclosure Controls and Procedures. The Registrant maintains disclosure controls and procedures that are designed to ensure that information required to be disclosed in the Registrant’s filings under the Securities Exchange Act of 1934 and the Investment Company Act of 1940 is recorded, processed, summarized and reported within the periods specified in the rules and forms of the Securities and Exchange Commission. Such information is accumulated and communicated to the Registrant’s management, including its principal executive officer and principal financial officer, as appropriate, to allow timely decisions regarding required disclosure. The Registrant’s management, including the principal executive officer and the principal financial officer, recognizes that any set of controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving the desired control objectives.

Within 90 days prior to the filing date of this Shareholder Report on Form N-CSR, the Registrant had carried out an evaluation, under the supervision and with the participation of the Registrant’s management, including the Registrant’s principal executive officer and the Registrant’s principal financial officer, of the effectiveness of the design and operation of the Registrant’s disclosure controls and procedures. Based on such evaluation, the Registrant’s principal executive officer and principal financial officer concluded that the Registrant’s disclosure controls and procedures are effective.

(b) Changes in Internal Controls. There have been no changes in the Registrant’s internal controls or in other factors that could materially affect the internal controls over financial reporting subsequent to the date of their evaluation in connection with the preparation of this Shareholder Report on Form N-CSR.

Item 12. Exhibits.

(a)(1) Code of Ethics