This page intentionally left blank.

Item 2. Code of Ethics.

(a) The Registrant has adopted a code of ethics that applies to its principal executive officers and principal financial and accounting officer.

(c) N/A

(d) N/A

(f) Pursuant to Item 12(a)(1), the Registrant is attaching as an exhibit a copy of its code of ethics that applies to its principal executive officers and principal financial and accounting officer.

Item 3. Audit Committee Financial Expert.

(a)(1) The Registrant has an audit committee financial expert serving on its audit committee.

(2) The audit committee financial expert is Ann Torre Bates and she is "independent" as defined under the relevant Securities and Exchange Commission Rules and Releases.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees

The aggregate fees paid to the principal accountant for professional services rendered by the principal accountant for the audit of the registrant’s annual financial statements or for services that are normally provided by the principal accountant in connection with statutory and regulatory filings or engagements were $73,560 for the fiscal year ended March 31, 2013 and $75,070 for the fiscal year ended March 31, 2012.

(b) Audit-Related Fees

There were no fees paid to the principal accountant for assurance and related services rendered by the principal accountant to the registrant that are reasonably related to the performance of the audit of the registrant's financial statements and are not reported under paragraph (a) of Item 4.

There were no fees paid to the principal accountant for assurance and related services rendered by the principal accountant to the registrant's investment adviser and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the registrant that are reasonably related to the performance of the audit of their financial statements.

(c) Tax Fees

The aggregate fees paid to the principal accountant for professional services rendered by the principal accountant to the registrant for tax compliance, tax advice and tax planning were $474 the fiscal year ended March 31, 2013 and $497 for the fiscal year ended March 31, 2012. The services for which these fees were paid include identifying passive foreign investment company to manage exposure to tax liabilities.

The aggregate fees paid to the principal accountant for professional services rendered by the principal accountant to the registrant’s investment adviser and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the registrant for tax compliance, tax advice and tax planning were $67,000 for the fiscal year ended March 31, 2013 and $0 for the fiscal year ended March 31, 2012. The services for which these fees were paid included web based application providing technical information related to withholding tax rates, treaties, procedures, and form/instructions for portfolio dividends and interest, and capital gains in foreign governments

(d) All Other Fees

There were no fees paid to the principal accountant for products and services rendered by the principal accountant to the registrant not reported in paragraphs (a)-(c) of Item 4.

There were no paid to the principal accountant for products and services rendered by the principal accountant to the registrant’s investment adviser and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the registrant other than services reported in paragraphs (a)-(c) of Item 4.

(e) (1) The registrant’s audit committee is directly responsible for approving the services to be provided by the auditors, including:

(i) pre-approval of all audit and audit related services;

(ii) pre-approval of all non-audit related services to be provided to the Fund by the auditors;

(iii) pre-approval of all non-audit related services to be provided to the registrant by the auditors to the registrant’s investment adviser or to any entity that controls, is controlled by or is under common control with the registrant’s investment adviser and that provides ongoing services to the registrant where the non-audit services relate directly to the operations or financial reporting of the registrant; and

(iv) establishment by the audit committee, if deemed necessary or appropriate, as an alternative to committee pre-approval of services to be provided by the auditors, as required by paragraphs (ii) and (iii) above, of policies and procedures to permit such services to be pre-approved by other means, such as through establishment of guidelines or by action of a designated member or members of the committee; provided the policies and procedures are detailed as to the particular service and the committee is informed of each service and such policies and procedures do not include delegation of audit committee responsibilities, as contemplated under the Securities Exchange Act of 1934, to management; subject, in the case of (ii) through (iv), to any waivers, exceptions or exemptions that may be available under applicable law or rules.

(e) (2) None of the services provided to the registrant described in paragraphs (b)-(d) of Item 4 were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of regulation S-X.

(f) No disclosures are required by this Item 4(f).

(g) The aggregate non-audit fees paid to the principal accountant for services rendered by the principal accountant to the registrant and the registrant’s investment adviser and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the registrant were $67,474 for the fiscal year ended March 31, 2013 and $497 for the fiscal year ended March 31, 2012.

(h) The registrant’s audit committee of the board has considered whether the provision of non-audit services that were rendered to the registrant’s investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the registrant that were not pre-approved pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X is compatible with maintaining the principal accountant’s independence.

Item 5. Audit Committee of Listed Registrants.

Members of the Audit Committee are: Edward I. Altman, Ann Torre Bates and Robert E. Wade.

Item 6. Schedule of Investments. N/A

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

The board of trustees of the Fund has delegated the authority to vote proxies related to the portfolio securities held by the Fund to the Fund’s investment manager Franklin Mutual Advisers LLC (FMAL) in accordance with the Proxy Voting Policies and Procedures (Policies) adopted by the investment manager.

The investment manager has delegated its administrative duties with respect to the voting of proxies to the Proxy Group within Franklin Templeton Companies, LLC (Proxy Group), an affiliate and wholly owned subsidiary of Franklin Resources, Inc. All proxies received by the Proxy Group will be voted based upon the investment manager’s instructions and/or policies. The investment manager votes proxies solely in the best interests of the Fund and its shareholders.

To assist it in analyzing proxies, the investment manager subscribes to Institutional Shareholder Services, Inc. (ISS), an unaffiliated third-party corporate governance research service that provides in-depth analyses of shareholder meeting agendas, vote recommendations, executing votes, ballot reconciliation, recordkeeping and vote disclosure services. In addition, the investment manager subscribes to Glass, Lewis & Co., LLC (Glass Lewis), an unaffiliated third-party analytical research firm, to receive analyses and vote recommendations on the shareholder meetings of publicly held U.S. companies, as well as a limited subscription to its international research. Although ISS’ and/or Glass Lewis’ analyses are thoroughly reviewed and considered in making a final voting decision, the investment manager does not consider recommendations from ISS, Glass Lewis or any other third party to be determinative of the investment manager’s ultimate decision. As a matter of

policy, the officers, directors/trustees and employees of the investment manager and the Proxy Group will not be influenced by outside sources whose interests conflict with the interests of the Fund and its shareholders. Efforts are made to resolve all conflicts in the best interests of the investment manager’s clients. Material conflicts of interest are identified by the Proxy Group based upon analyses of client, distributor, broker-dealer and vendor lists, information periodically gathered from directors and officers, and information derived from other sources, including public filings. In situations where a material conflict of interest is identified, the Proxy Group may defer to the voting recommendation of ISS, Glass Lewis or those of another independent third-party provider of proxy services; or send the proxy directly to the Fund's board or a committee of the board with the investment manager's recommendation regarding the vote for approval.

Where a material conflict of interest has been identified, but the items on which the investment manager’s vote recommendations differ from Glass Lewis, ISS, or another independent third-party provider of proxy services relate specifically to (1) shareholder proposals regarding social or environmental issues, (2) “Other Business” without describing the matters that might be considered, or (3) items the investment manager wishes to vote in opposition to the recommendations of an issuer’s management, the Proxy Group may defer to the vote recommendations of the investment manager rather than sending the proxy directly to the Fund's board or a board committee for approval.

To avoid certain potential conflicts of interest, the investment manager will employ echo voting, if possible, in the following instances: (1) when the Fund invests in an underlying fund in reliance on any one of Sections 12(d) (1) (E), (F), or (G) of the 1940 Act, the rules thereunder, or pursuant to a SEC exemptive order thereunder; (2) when the Fund invests uninvested cash in affiliated money market funds pursuant to the rules under the 1940 Act or any exemptive orders thereunder (“cash sweep arrangement”); or (3) when required pursuant to the Fund’s governing documents or applicable law. Echo voting means that the investment manager will vote the shares in the same proportion as the vote of all of the other holders of the Fund’s shares.

The recommendation of management on any issue is a factor that the investment manager considers in determining how proxies should be voted. However, the investment manager does not consider recommendations from management to be determinative of the investment manager’s ultimate decision. As a matter of practice, the votes with respect to most issues are cast in accordance with the position of the company's management. Each issue, however, is considered on its own merits, and the investment manager will not support the position of the company's management in any situation where it deems that the ratification of management’s position would adversely affect the investment merits of owning that company’s shares.

Investment manager’s proxy voting policies and principles The investment manager has adopted general proxy voting guidelines, which are summarized below. These guidelines are not an exhaustive list of all the issues that may arise and the investment manager cannot anticipate all future situations. In all cases, each proxy will be considered based on the relevant facts and circumstances.

Board of directors. The investment manager supports an independent board of directors, and prefers that key committees such as audit, nominating, and compensation committees be comprised of independent directors. The investment

manager will generally vote against management efforts to classify a board and will generally support proposals to declassify the board of directors. The investment manager will consider withholding votes from directors who have attended less than 75% of meetings without a valid reason. While generally in favor of separating Chairman and CEO positions, the investment manager will review this issue as well as proposals to restore or provide for cumulative voting on a case-by-case basis, taking into consideration factors such as the company’s corporate governance guidelines or provisions and performance. The investment manager generally will support non-binding shareholder proposals to require a majority vote standard for the election of directors; however, if these proposals are binding, the investment manager will give careful review on a case-by-case basis of the potential ramifications of such implementation.

In the event of a contested election, the investment manager will review a number of factors in making a decision including management’s track record, the company’s financial performance, qualifications of candidates on both slates, and the strategic plan of the dissidents.

Ratification of auditors of portfolio companies. The investment manager will closely scrutinize the independence, role and performance of auditors. On a case-by-case basis, the investment manager will examine proposals relating to non-audit relationships and non-audit fees. The investment manager will also consider, on a case-by-case basis, proposals to rotate auditors, and will vote against the ratification of auditors when there is clear and compelling evidence of a lack of independence, accounting irregularities or negligence. The investment manager may also consider whether the ratification of auditors has been approved by an appropriate audit committee that meets applicable composition and independence requirements.

Management and director compensation. A company’s equity-based compensation plan should be in alignment with the shareholders’ long-term interests. The investment manager believes that executive compensation should be directly linked to the performance of the company. The investment manager evaluates plans on a case-by-case basis by considering several factors to determine whether the plan is fair and reasonable, including the ISS quantitative model utilized to assess such plans and/or the Glass Lewis evaluation of the plans. The investment manager will generally oppose plans that have the potential to be excessively dilutive, and will almost always oppose plans that are structured to allow the repricing of underwater options, or plans that have an automatic share replenishment “evergreen” feature. The investment manager will generally support employee stock option plans in which the purchase price is at least 85% of fair market value, and when potential dilution is 10% or less.

Severance compensation arrangements will be reviewed on a case-by-case basis, although the investment manager will generally oppose “golden parachutes” that are considered to be excessive. The investment manager will normally support proposals that require a percentage of directors’ compensation to be in the form of common stock, as it aligns their interests with those of shareholders.

The investment manager will review non-binding say-on-pay proposals on a case-by-case basis, and will generally vote in favor of such proposals unless compensation is misaligned with performance and/or shareholders’ interests,

the company has not provided reasonably clear disclosure regarding its compensation practices, or there are concerns with the company’s remuneration practices.

Anti-takeover mechanisms and related issues. The investment manager generally opposes anti-takeover measures since they tend to reduce shareholder rights. However, as with all proxy issues, the investment manager conducts an independent review of each anti-takeover proposal. On occasion, the investment manager may vote with management when the research analyst has concluded that the proposal is not onerous and would not harm the Fund or its shareholders’ interests. The investment manager generally supports proposals that require shareholder rights’ plans (“poison pills”) to be subject to a shareholder vote and will closely evaluate such plans on a case-by-case basis to determine whether or not they warrant support. In addition, the investment manager will generally vote against any proposal to issue stock that has unequal or subordinate voting rights. The investment manager generally opposes any supermajority voting requirements as well as the payment of “greenmail.” The investment manager generally supports “fair price” provisions and confidential voting. The investment manager will review a company’s proposal to reincorporate to a different state or country on a case-by-case basis taking into consideration financial benefits such as tax treatment as well as comparing corporate governance provisions and general business laws that may result from the change in domicile.

Changes to capital structure. The investment manager realizes that a company's financing decisions have a significant impact on its shareholders, particularly when they involve the issuance of additional shares of common or preferred stock or the assumption of additional debt. The investment manager will review, on a case-by-case basis, proposals by companies to increase authorized shares and the purpose for the increase. The investment manager will generally not vote in favor of dual-class capital structures to increase the number of authorized shares where that class of stock would have superior voting rights. The investment manager will generally vote in favor of the issuance of preferred stock in cases where the company specifies the voting, dividend, conversion and other rights of such stock and the terms of the preferred stock issuance are deemed reasonable. The investment manager will review proposals seeking preemptive rights on a case-by-case basis.

Mergers and corporate restructuring. Mergers and acquisitions will be subject to careful review by the research analyst to determine whether they would be beneficial to shareholders. The investment manager will analyze various economic and strategic factors in making the final decision on a merger or acquisition. Corporate restructuring proposals are also subject to a thorough examination on a case-by-case basis.

Environment, social and governance issues. The investment manager will generally give management discretion with regard to social, environmental and ethical issues, although the investment manager may vote in favor of those that are believed to have significant economic benefits or implications for the Fund and its shareholders. The investment manager generally supports the right of shareholders to call special meetings and act by written consent. However, the investment manager will review such shareholder proposals on a case-by-case basis in an effort to ensure that such proposals do not disrupt the course of business or waste company resources for the benefit of a small minority of shareholders. The investment manager will consider supporting a shareholder proposal seeking disclosure and greater board oversight of

lobbying and corporate political contributions if the investment manager believes that there is evidence of inadequate oversight by the company’s board, if the company’s current disclosure is significantly deficient, or if the disclosure is notably lacking in comparison to the company’s peers. The investment manager will consider on a case-by-case basis any well-drafted and reasonable proposals for proxy access considering such factors as the size of the company, ownership thresholds and holding periods, responsiveness of management, intentions of the shareholder proponent, company performance, and shareholder base.

Global corporate governance. Many of the tenets discussed above are applied to the investment manager's proxy voting decisions for international investments. However, the investment manager must be flexible in these worldwide markets. Principles of good corporate governance may vary by country, given the constraints of a country’s laws and acceptable practices in the markets. As a result, it is on occasion difficult to apply a consistent set of governance practices to all issuers. As experienced money managers, the investment manager's analysts are skilled in understanding the complexities of the regions in which they specialize and are trained to analyze proxy issues germane to their regions.

The investment manager will generally attempt to process every proxy it receives for all domestic and foreign securities. However, there may be situations in which the investment manager may be unable to vote a proxy, or may choose not to vote a proxy, such as where: (i) the proxy ballot was not received from the custodian bank; (ii) a meeting notice was received too late; (iii) there are fees imposed upon the exercise of a vote and it is determined that such fees outweigh the benefit of voting; (iv) there are legal encumbrances to voting, including blocking restrictions in certain markets that preclude the ability to dispose of a security if the investment manager votes a proxy or where the investment manager is prohibited from voting by applicable law or other regulatory or market requirements, including but not limited to, effective Powers of Attorney; (v) the investment manager held shares on the record date but has sold them prior to the meeting date; (vi) proxy voting service is not offered by the custodian in the market; (vii) the investment manager believes it is not in the best interest of the Fund or its shareholders to vote the proxy for any other reason not enumerated herein; or (viii) a security is subject to a securities lending or similar program that has transferred legal title to the security to another person. The investment manager or its affiliates may, on behalf of one or more of the proprietary registered investment companies advised by the investment manager or its affiliates, determine to use its best efforts to recall any security on loan where the investment manager or its affiliates (a) learn of a vote on a material event that may affect a security on loan and (b) determine that it is in the best interests of such proprietary registered investment companies to recall the security for voting purposes.

Shareholders may view the complete Policies online at franklintempleton.com. Alternatively, shareholders may request copies of the Policies free of charge by calling the Proxy Group collect at (954) 527-7678 or by sending a written request to: Franklin Templeton Companies, LLC, 300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923, Attention: Proxy Group. Copies of the Fund’s proxy voting records are available online at franklintempleton.com and posted on the SEC website at www.sec.gov. The proxy voting records are updated each year by August 31 to reflect the most recent 12-month period ended June 30.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

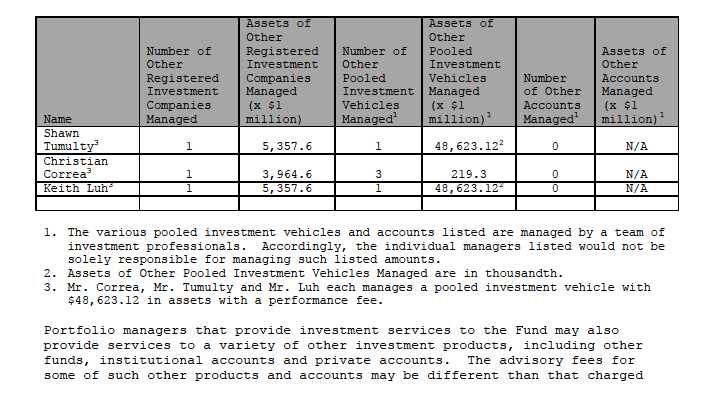

(a)(1) As of May 24, 2013, the portfolio managers of the Fund are as follows:

SHAWN TUMULTY, Vice President of FMAL.

Mr. Tumulty has been a manager of the Fund since 2005. He joined Franklin Templeton Investments in 2000.

CHRISTIAN CORREA, Portfolio Manager of FMAL

Mr. Correa has been manager of the Fund since 2004. He joined Franklin Templeton Investments in 2003.

KEITH LUH, Assistant Portfolio Manager of FMAL

Mr. Luh has been a portfolio manager of the Fund since 2009, providing research and advice on purchases and sales of individual securities, and portfolio risk assessment. He joined Franklin Templeton Investments in 2005.

Shawn Tumulty and Christian Correa are jointly responsible for the day-to-day management of the Fund. The co-portfolio managers have equal authority over all aspects of the Fund's investment portfolio, including but not limited to, purchases and sales of individual securities, portfolio risk assessment, and the management of daily cash balances in accordance with anticipated management requirements. The degree to which each manager may perform these functions, and the nature of these functions, may change from time to time.

(a)(2) This section reflects information about the portfolio managers as of the fiscal year ended March 31, 2013.

The following table shows the number of other accounts managed by each portfolio manager and the total assets in the accounts managed within each category

to the Fund and may include performance based compensation. This may result in fees that are higher (or lower) than the advisory fees paid by the Fund. As a matter of policy, each fund or account is managed solely for the benefit of the beneficial owners thereof. As discussed below, the separation of the trading execution function from the portfolio management function and the application of objectively based trade allocation procedures helps to mitigate potential conflicts of interest that may arise as a result of the portfolio managers managing accounts with different advisory fees.

Conflicts. The management of multiple funds, including the Fund, and accounts may also give rise to potential conflicts of interest if the funds and other accounts have different objectives, benchmarks, time horizons, and fees as the portfolio manager must allocate his or her time and investment ideas across multiple funds and accounts. The investment manager seeks to manage such competing interests for the time and attention of portfolio managers by having portfolio managers focus on a particular investment discipline. Most other accounts managed by a portfolio manager are managed using the same investment strategies that are used in connection with the management of the Fund. Accordingly, portfolio holdings, position sizes, and industry and sector exposures tend to be similar across similar portfolios, which may minimize the potential for conflicts of interest. As noted above, the separate management of the trade execution and valuation functions from the portfolio management process also helps to reduce potential conflicts of interest. However, securities selected for funds or accounts other than the Fund may outperform the securities selected for the Fund. Moreover, if a portfolio manager identifies a limited investment opportunity that may be suitable for more than one fund or other account, the Fund may not be able to take full advantage of that opportunity due to an allocation of that opportunity across all eligible funds and other accounts. The investment manager seeks to manage such potential conflicts by using procedures intended to provide a fair allocation of buy and sell opportunities among funds and other accounts.

The structure of a portfolio manager’s compensation may give rise to potential conflicts of interest. A portfolio manager’s base pay and bonus tend to increase with additional and more complex responsibilities that include increased assets under management. As such, there may be an indirect relationship between a portfolio manager’s marketing or sales efforts and his or her bonus.

Finally, the management of personal accounts by a portfolio manager may give rise to potential conflicts of interest. While the funds and the investment manager have adopted a code of ethics which they believe contains provisions reasonably necessary to prevent a wide range of prohibited activities by portfolio managers and others with respect to their personal trading activities, there can be no assurance that the code of ethics addresses all individual conduct that could result in conflicts of interest.

The investment manager and the Fund have adopted certain compliance procedures that are designed to address these, and other, types of conflicts. However, there is no guarantee that such procedures will detect each and every situation where a conflict arises.

Compensation. The investment manager seeks to maintain a compensation program that is competitively positioned to attract, retain and motivate top-quality investment professionals. Portfolio managers receive a base salary, a cash incentive bonus opportunity, an equity compensation opportunity, and a

benefits package. Portfolio manager compensation is reviewed annually and the level of compensation is based on individual performance, the salary range for a portfolio manager’s level of responsibility and Franklin Templeton guidelines. Portfolio managers are provided no financial incentive to favor one fund or account over another. Each portfolio manager’s compensation consists of the following three elements:

Base salary Each portfolio manager is paid a base salary.

Annual bonus Annual bonuses are structured to align the interests of the portfolio manager with those of the Fund’s shareholders. Each portfolio manager is eligible to receive an annual bonus. Bonuses generally are split between cash (50% to 65%) and restricted shares of Resources stock (17.5% to 25%) and mutual fund shares (17.5% to 25%). The deferred equity-based compensation is intended to build a vested interest of the portfolio manager in the financial performance of both Resources and mutual funds advised by the investment manager. The bonus plan is intended to provide a competitive level of annual bonus compensation that is tied to the portfolio manager achieving consistently strong investment performance, which aligns the financial incentives of the portfolio manager and Fund shareholders. The Chief Investment Officer of the investment manager and/or other officers of the investment manager, with responsibility for the Fund, have discretion in the granting of annual bonuses to portfolio managers in accordance with Franklin Templeton guidelines. The following factors are generally used in determining bonuses under the plan:

- Investment performance. Primary consideration is given to the historic investment performance over the 1, 3 and 5 preceding years of all accounts managed by the portfolio manager. The pre-tax performance of each fund managed is measured relative to a relevant peer group and/or applicable benchmark as appropriate.

- Non-investment performance. The more qualitative contributions of the portfolio manager to the investment manager’s business and the investment management team, including business knowledge, contribution to team efforts, mentoring of junior staff, and contribution to the marketing of the Funds, are evaluated in determining the amount of any bonus award.

- Research. Where the portfolio management team also has research responsibilities, each portfolio manager is evaluated on the number and performance of recommendations over time.Responsibilities. The characteristics and complexity of funds managed by the portfolio manager are factored in the investment manager’s appraisal.

Additional long-term equity-based compensation Portfolio managers may also be awarded restricted shares or units of Resources stock or restricted shares or units of one or more mutual funds. Awards of such deferred equity-based compensation typically vest over time, so as to create incentives to retain key talent.

Portfolio managers also participate in benefit plans and programs available generally to all employees of the manager.

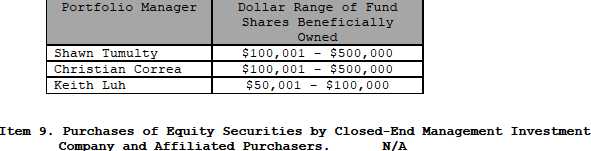

Ownership of Fund shares. The investment manager has a policy of encouraging portfolio managers to invest in the funds they manage. Exceptions arise when,

for example, a fund is closed to new investors or when tax considerations or jurisdictional constraints cause such an investment to be inappropriate for the portfolio manager. The following is the dollar range of Fund shares beneficially owned by each portfolio manager (such amounts may change from time to time):

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no changes to the procedures by which shareholders may recommend nominees to the Registrant's Board of Trustees that would require disclosure herein.

Item 11. Controls and Procedures.

(a) Evaluation of Disclosure Controls and Procedures. The Registrant maintains disclosure controls and procedures that are designed to ensure that information required to be disclosed in the Registrant’s filings under the Securities Exchange Act of 1934 and the Investment Company Act of 1940 is recorded, processed, summarized and reported within the periods specified in the rules and forms of the Securities and Exchange Commission. Such information is accumulated and communicated to the Registrant’s management, including its principal executive officer and principal financial officer, as appropriate, to allow timely decisions regarding required disclosure. The Registrant’s management, including the principal executive officer and the principal financial officer, recognizes that any set of controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving the desired control objectives.

Within 90 days prior to the filing date of this Shareholder Report on Form N-CSR, the Registrant had carried out an evaluation, under the supervision and with the participation of the Registrant’s management, including the Registrant’s principal executive officer and the Registrant’s principal financial officer, of the effectiveness of the design and operation of the Registrant’s disclosure controls and procedures. Based on such evaluation, the Registrant’s principal executive officer and principal financial officer concluded that the Registrant’s disclosure controls and procedures are effective.

(b) Changes in Internal Controls. There have been no changes in the Registrant’s internal controls or in other factors that could materially affect the internal controls over financial reporting subsequent to the date of their evaluation in connection with the preparation of this Shareholder Report on Form N-CSR.

Item 12. Exhibits.

(a) (1) Code of Ethics

(a) (2) Certifications pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 of Laura F. Fergerson, Chief Executive Officer - Finance and Administration, and Robert G. Kubilis, Chief Financial Officer and Chief Accounting Officer

(b) Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 of Laura F. Fergerson, Chief Executive Officer - Finance and Administration, and Robert G. Kubilis, Chief Financial Officer and Chief Accounting Officer

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

FRANKLIN MUTUAL RECOVERY FUND

By /s/ Laura F. Fergerson

Laura F. Fergerson

Chief Executive Officer - Finance and

Administration

Date June 5, 2013

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By /s/ Laura F. Fergerson

Laura F. Fergerson

Chief Executive Officer - Finance and

Administration

Date June 5, 2013

By /s/ Robert G. Kubilis

Robert G. Kubilis

Chief Financial Officer and

Chief Accounting Officer

Date June 5, 2013