| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | August 31, 2011 |

| UNITED STATES | Estimated average burden hours per response: . . . . . . . . . . . . . . .18.9 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21308 |

|

Alger China-U.S. Growth Fund |

(Exact name of registrant as specified in charter) |

|

111 Fifth Avenue New York, New York | | 10003 |

(Address of principal executive offices) | | (Zip code) |

|

Mr. Hal Liebes Fred Alger Management, Inc. 111 Fifth Avenue New York, New York 10003 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 212-806-8800 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | April 30, 2009 | |

| | | | | | | |

ITEM 1. REPORT(S) TO STOCKHOLDERS.

Alger China-U.S. Growth Fund

SEMI-ANNUAL REPORT

April 30, 2009

(Unaudited) | |

|

Table of Contents | |

| |

ALGER CHINA-U.S. GROWTH FUND | |

| |

Letter to Our Shareholders | 1 |

| |

Fund Highlights | 8 |

| |

Portfolio Summary | 9 |

| |

Schedule of Investments | 10 |

| |

Statement of Assets and Liabilities | 16 |

| |

Statement of Operations | 17 |

| |

Statements of Changes in Net Assets | 18 |

| |

Financial Highlights | 20 |

| |

Notes to Financial Statements | 22 |

| |

Additional Information | 30 |

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online. When documents such as prospectuses and annual and semi-annual reports are available, we’ll send you an e-mail notification with a convenient link that will take you directly to the fund information on our website. To sign up for this free service, simply enroll at www.icsdelivery.com/alger.

Dear Shareholders, | | May 25, 2009 |

We can look at the last six months as the melting away of an illusion; as a time when reality has come painfully back into play. Many philosophers built vast realms of study on the idea that misguided reason can twist reality into something that perhaps suits us in the moment but ultimately only serves to keep us in an illusory state—and, in our current case, wreak havoc on our economy and our confidence.

The housing and credit crises and ensuing financial breakdown began with an illusion based on flawed ideas held by many financial lenders and insurers: the latent belief that growth in the housing market would continue unhampered on its upward trajectory. Underlying the assumption of unimpeded growth was the idea that financial derivatives could not only provide the increase in debt necessary to support the financial system but also manage the associated risk. In the mid-2000s, the illusion grew as more and more lenders extended more and more credit to “subprime” borrowers who, if their circumstances declined, were less and less likely to be able to pay the loans back. Although the practice was based on a belief that growth would continue, experience has shown again and again that the upward trend of growth over time is much more jagged than we like to recall.

When the illusion disintegrated, not only did the borrowers suffer from foreclosures, but the resulting housing crisis created a massive ripple effect that crippled the U.S.’s major financial firms. Along with the weakening of the financial sector, so went credit availability, consumer spending, jobs, and, ultimately, consumer confidence. By the fourth quarter of 2008, the scale of the crisis had ceased to be solely “subprime”—it had gone global. Into the first quarter of 2009, the volatility continued with the Dow Jones Industrial Average(i) climbing as high as 9,034 points and falling as low as 6,547 points.

Toward the end of the first quarter and into the second quarter of the calendar year, economic indicators were struggling to recover. Retail sales fell 1.3% in March and a further 0.4% in April—a larger dip than expected. The Consumer Price Index declined 0.7% on an annual basis in April, only the second year-over-year decline in nearly 54 years following March’s 0.4% drop(ii). Industrial production decreased 0.5% in April after having fallen 1.7% in March(iii). And GDP for the first quarter of 2009 decreased 6.1% compared to the fourth quarter of 2008, which experienced a decline of 6.3%.

Europe did not fare much better. GDP fell 2.5% in the first quarter of 2009 versus the last quarter of 2008, which experienced a decline of 1.5%—the figures were for both the 16-country euro currency zone and the broader 27-country European Union bloc(iv). China is anticipated to fare less poorly, and although its export growth is expected to slow, the country is taking measures to focus on innovation rather than outright cost-efficiency.

Emerging from the Darkness

Plato famously dealt with illusion in what came to be called Plato’s Cave. He described people in a cave whose notion of reality was entirely comprised of shadows projected on a wall. Similarly, one could say that we were in such a cave, deceived by

1

the shadows of easy credit, with no real idea of the hows or whys of what we were seeing.

Now, however, we are beginning to see clearly where things unraveled. Actions are being taken by the Obama administration as well as the housing, financial, and automotive industries to stave off a repetition of the disaster; whether or not those actions will succeed remains to be seen.

What we do know is that, as of the date of this writing, some light has begun to shine in growth investing. In the first quarter, growth funds beat their value rivals by the largest margin in nine years. As of April 28, mid-cap growth funds were up 4.3%, small-cap growth funds were up 0.8%, and large-cap growth funds were up 2.6%, according to investment researcher Morningstar Inc.—a sign that investors are beginning to shed their aversion to risk and test the market.

Then and Now

Much has been made of the similarities between the current downturn and the Great Depression. During the “Roaring Twenties,” people were busy buying automobiles and appliances on credit and eagerly speculating in the stock market, feeding the illusion that the good times would continue to roll.

Then, like now, thought—in terms of easy credit and unimpeded growth—was divorced from reality. Back then, however, government policy either declined to intervene or, worse, intervened in ways that exacerbated rather than alleviated the financial crisis, thus allowing the devastation to spread across the U.S. economy. Things today move much more quickly. The current economy has turned downward faster in a shorter period of time than in any prior period, including the Depression. Fortunately, our government has responded with alacrity and, in a broad sense, moved in the right direction both by injecting massive amounts of liquidity into the financial system and by proactively assuring consumers of the safety of their savings and deposit accounts. As a result, we are likely to emerge faster from this crisis, and certainly much faster than in the 1930s. Government cannot be the only driver of recovery. Today, the depth and breadth of investors in markets across the globe is much stronger than ever before, and their actions will likely speed and strengthen the shape of recovery in both equity and debt markets.

As we have noted in our Alger Market Commentaries (see www.alger.com), companies were quick to respond to the downturn in the second half of 2008 by moving rapidly to cut expenses. At the end of the first quarter of 2009, as we tracked the corporate earnings results of the companies we follow, we discovered a pattern: Despite the rapidity of the economic downturn, we saw companies reporting free cash flow of both absolute strength and relative resilience. We expect the continued stabilization of the U.S. economy and company fundamentals to support the market’s rally from March lows.

We are already seeing signs of a bottoming in the housing market in the earliest-hit and hardest-hit areas of the U.S. where declines in foreclosures and short sales have begun to occur. Looking at Orange County, California, home prices increased 2.5% in March from February; sales jumped 27.5% in March from February and 47.4% from last year, according to the California Association of Realtors. The county had about four months of inventory as of May, a level not seen since April 2006. Inventory was at eight months a year ago and peaked at 11 months in 2007.

2

As a lagging indicator, the unemployment rate won’t yield for a while as companies are expected to be slow to add new jobs, but the market can rebound long before the level of employment does. The unemployment rate hit a 25-year high in April, but there were signs of hope as the monthly job loss total for April fell to 539,000, down from 699,000 jobs lost in March and the lowest level in six months—since October, when the economy shed 380,000 jobs.

The Institute for Supply Management’s manufacturing index, a key measure of manufacturing activity, rose for the fourth straight month in April, suggesting the sector may be stabilizing even though the indicator has been at the contraction level for 15 months in a row. And the Consumer Confidence Index, which had posted a slight increase in March, improved considerably in April. The Index now stands at 39.2 (1985=100), up from 26.9 in March.

Apart from the Crowd

Looking forward, we are grounded in a more complete picture of reality—for the overall economy and our firm. Danish philosopher Søren Kierkegaard, too, examined illusion in a way, writing that crowds limit and stifle the unique individual. Like any economic bubble, we can, of course, now say in hindsight that the adjoining crises were a result of exactly this kind of crowd mentality. The resulting economic disaster, while painful, has effectively broken up the crowd, razing the illusion and once again opening the investing field up to new and creative opportunities. There is, after all, a stunning amount of cash on the sidelines. The savings rate is up to 5%, meaning that there is about $500 billion currently being held in cash. As consumer confidence repairs itself, the sidelined cash will be invested. While we believe that the economy will technically be in recession for most of 2009, negative GDP figures will gradually become less severe.

The stock market, however, is a discounting mechanism; investors look forward toward the potential range of economic, sector, and company-specific outcomes in terms of revenues, margins, profits, and growth to assess the value of equity. At Alger, our investment process includes valuation analysis that considers outcomes that are both highly pessimistic and optimistic. Most of the time, we observe stocks selling within ranges that reflect varying but ultimately balanced views between the divergent possibilities.

Occasionally, however, the crowd mentality of the market overwhelms such rational behavior and investors see something entirely different: equities of companies, even the strongest, suddenly priced to fail. We believe the S&P 500 Index(v) lows in March reflected such an event and, thus, we are increasingly confident that those lows will mark the bottom. Because we do not expect the economy—and, in particular, investor sentiment about economic recovery and future growth—to recover in a straight line, we think continued market volatility is likely. The inevitable sell-offs in the stock market that will accompany such uncertain economic progress will offer excellent buying opportunities for patient, long-term investors.

During the last six months, we had limited exposure to the hardest-hit areas of the financial sector, and our performance was largely a result of the market’s broad and indiscriminate decline. Even in the best of times investing is a challenge; however, it is during bad times that an investment firm proves its capability to manage through crisis, focus on improving performance, and not only endure but

3

also improve upon its strengths. Alger investment professionals have remained focused and disciplined in executing upon our consistent investment philosophy and process. Now in 2009, our 45th year in the business of investing, we have successfully passed through many shadowy times and found new opportunities amidst economic and generational change.

Kierkegaard once wrote, “The task must be made difficult, for only the difficult inspires the noble-hearted.” We have perhaps encountered the most difficult task our generation will see, and our firm has come out of it more inspired than ever to deliver exceptional investment results for an exceptional group of individuals and institutions: our clients.

Portfolio Matters

For the six-month period ending April 30, 2009, the Alger China-U.S. Growth Fund returned 5.98% . During the same period the S&P 500 Index returned -8.49%, and the MSCI Zhong Hua Indexvi returned 26.46% .

During the period, compared to the S&P 500 Index, the largest portfolio weightings in the Alger China-U.S. Growth Fund were in the Information Technology and Financials sectors. The largest sector overweight for the period was in Information Technology. The largest sector underweight for the period was in Health Care. Relative outperformance in the Financials and Materials sectors were the most important contributors to performance. Sectors that detracted from the portfolio included Information Technology and Telecommunications Services.

During the period, compared to the MSCI Zhong Hua Index, the largest portfolio weightings in the Alger China-U.S. Growth Fund were in the Information Technology and Financials sectors. The largest sector overweight for the period was in Information Technology. The largest sector underweight for the period was in Financials. Relative outperformance in the Materials and Information Technology sectors were the most important contributors to performance. Sectors that detracted from the portfolio included Financials and Energy.

Among the most important relative contributors to the portfolio during the six months ended April 30, 2009, were Companhia Vale do Rio Doce (ADS), China National Building Material Co. Ltd., China High Speed Transmission Equipment Group Co. Ltd., China Life Insurance Co. Ltd. (China), and ZTE CORP H. Conversely, detracting from overall results were Autodesk Inc., JA Solar Holdings Co. Ltd. (ADS), China Insurance International Holdings Co. Ltd., SINA Corp., and Agile Property Holdings Ltd.

Respectfully submitted, | |

| |

Daniel C. Chung | |

Chief Investment Officer | |

4

(i) The Dow Jones Industrial Average is an index of common stocks comprised of major industrial companies and assumes reinvestment of dividends. It is frequently used as a general measure of stock market performance.

(ii) Labor Department

(iii) Federal Reserve

(iv) EU statistics office

(v) Standard & Poor’s 500 Index is an index of the 500 largest and most profitable companies in the United States.

(vi) The MSCI Zhong Hua Index is an aggregate of the MSCI Hong Kong Index (a capitalization-weighted index that monitors the performance of stocks from Hong Kong) and the MSCI China Free Index (an unmanaged market capitalization-weighted index of Chinese companies available to non-domestic investors).

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses or taxes.

This report and the financial statements contained herein are submitted for the general information of shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless proceeded or accompanied by an effective prospectus for the Fund. Fund returns represent the fiscal six month period return of Class A shares prior to the deduction of any sales charges. The performance data quoted represents past performance, which is not an indication or guarantee of future results.

Standardized performance results can be found on the following pages. The investment return and principal value of an investment in a fund will fluctuate so that an investor’s shares when redeemed may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the Fund’s management in this report are as of the date of the Shareholders letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable, however, there is no guarantee that such information is accurate. Any securities mentioned, whether owned in a fund or otherwise, are considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a fund and transactions in such securities, if any, may be for a variety of reasons, including without limitation, in response to cash flows, inclusion in a benchmark, and risk control. The reference to a specific security should also be understood in such context and not viewed as a statement that the security is a significant holding in a portfolio. Please refer to the Schedule of Investments for each fund which is included in this report for a complete list of fund holdings as of April 30, 2009. Securities mentioned in the Shareholders letter, if not found in the Schedule of Investments, may have been held by the Fund during the six-month fiscal period.

A Word About Risk

Growth stocks tend to be more volatile than other stocks as the price of growth stocks tends to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Investing in the stock market involves gains and losses and may not be suitable for all investors. Stocks of small- and

5

mid-sized companies are subject to greater risk than stocks of larger, more established companies owing to such factors as limited liquidity, inexperienced management, and limited financial resources. Investing in foreign securities involves additional risk (including currency risk, risks related to political, social, or economic conditions, and risks associated with the Chinese markets, such as increased volatility, limited liquidity, less stringent regulatory and legal system, and lack of industry and country diversification), and may not be suitable for all investors. Funds that participate in leveraging, such as the Alger China-U.S. Growth Fund, are subject to the risk that borrowing money to leverage will exceed the returns for securities purchased or that the securities purchased may actually go down in value; thus, the funds’ net asset value can decrease more quickly than if the fund had not borrowed. For a more detailed discussion of the risks associated with the Fund, please see the Fund’s Prospectus.

Before investing, carefully consider a fund’s investment objective, risks, charges, and expenses. For a prospectus containing this and other information about The Alger Funds call us at (800) 992-3863 or visit us at www.alger.com. Read it carefully before investing. Fred Alger & Company, Incorporated, Distributor. Member NYSE Euronext, SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

6

FUND PERFORMANCE AS OF 3/31/09 (Unaudited) †

AVERAGE ANNUAL TOTAL RETURNS

| | 1 | | 5 | | 10 | | SINCE | |

| | YEAR | | YEARS | | YEARS | | INCEPTION | |

Alger China-U.S. Growth Class A | | | | | | | | | |

(Inception 11/3/03) | | (48.29 | )% | 1.93 | % | n/a | | 4.26 | % |

Alger China-U.S. Growth Class C* | | | | | | | | | |

(Inception 3/3/08) | | (46.32 | )% | 2.45 | % | n/a | | 4.69 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on fund distributions or on the redemption of fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

† Returns reflect maximum sales charges on Class A shares and applicable contingent deferred sales charges on Class C shares.

* Performance figures prior to 3/3/08, inception of Class C shares, are those of the Fund’s Class A shares. Performance has been adjusted to remove the front-end sales charge imposed by Class A shares. Class C shares do not impose a front-end sales charge but do impose a contingent deferred sales charge of 1% on shares redeemed. If Class A sales charges were reflected, annual returns for the Class C shares would be lower. The performance figures prior to 3/3/08 have also been adjusted to reflect the higher operating expenses and applicable contingent sales charge of Class C Shares.

7

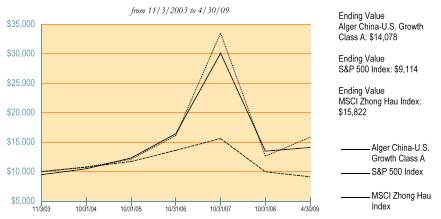

ALGER CHINA-U.S. GROWTH FUND

Fund Highlights Through April 30, 2009 (Unaudited)

HYPOTHETICAL $10,000 INVESTMENT IN CLASS A SHARES

The chart above illustrates the growth in value of a hypothetical $10,000 investment made in the Alger China-U.S. Growth Fund Class A shares, with an initial maximum sales charge of 5.25%, and the S&P 500 Index and the MSCI Zhong Hau Index (unmanaged indices of common stocks) on November 3, 2003, the inception date of the Alger China-U.S. Growth Fund Class A, through April 30, 2009. The figures for the Alger China-U.S. Growth Fund Class A shares, the S&P 500 Index, and the MSCI Zhong Hau Index include reinvestment of dividends.

Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

PERFORMANCE COMPARISON AS OF 4/30/09 †

AVERAGE ANNUAL TOTAL RETURNS

| | | | | | | | SINCE | |

| | 1 YEAR | | 5 YEARS | | 10 YEARS | | INCEPTION | |

Class A (Inception 11/3/03) | | (46.35 | )% | 6.39 | % | n/a | | 6.42 | % |

S&P 500 Index | | (35.31 | )% | (2.70 | )% | n/a | | (1.67 | )% |

MSCI Zhong Hau Index | | (38.49 | )% | 9.82 | % | n/a | | 8.71 | % |

| | | | | | | | | |

Class C (Inception 3/3/08)* | | (44.35 | )% | 6.94 | % | n/a | | 6.86 | % |

S&P 500 Index | | (35.31 | )% | (2.70 | )% | n/a | | (1.67 | )% |

MSCI Zhong Hau Index | | (38.49 | )% | 9.82 | % | n/a | | 8.71 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on fund distributions or on the redemption of fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

† Returns reflect maximum sales charges on Class A shares and applicable contingent deferred sales charges on Class C shares.

* Performance figures prior to 3/3/08, inception of Class C shares, are those of the Fund’s Class A shares. Performance has been adjusted to remove the front-end sales charge imposed by Class A shares. Class C shares do not impose a front-end sales charge but do impose a contingent deferred sales charge of 1% on shares redeemed. If Class A sales charges were reflected, annual returns for the Class C shares would be lower. The performance figures prior to 3/3/08 have also been adjusted to reflect the higher operating expenses and applicable contingent sales charge of Class C Shares.

8

PORTFOLIO SUMMARY†

April 30, 2009 (Unaudited)

| | CHINA-U.S. | |

COUNTRY | | GROWTH | |

AUSTRALIA | | 2.6 | % |

BRAZIL | | 2.1 | |

CANADA | | 1.5 | |

CAYMAN ISLANDS | | 0.8 | |

CHINA | | 24.9 | |

HONG KONG | | 19.1 | |

JAPAN | | 1.5 | |

SWITZERLAND | | 1.0 | |

TAIWAN | | 11.9 | |

UNITED STATES | | 30.4 | |

Cash and Net Other Assets | | 4.2 | |

| | 100.0 | % |

† Based on net assets.

9

ALGER CHINA-U.S. GROWTH FUND

Schedule of Investments (Unaudited) April 30, 2009

| | SHARES | | VALUE | |

COMMON STOCKS—95.6% | | | | | |

AUSTRALIA—2.6% | | | | | |

OIL & GAS EXPLORATION & PRODUCTION—2.6% | | | | | |

Linc Energy Ltd.*

(Cost $840,246) | | 736,600 | | $ | 1,358,362 | |

| | | | | |

BRAZIL—2.1% | | | | | |

DIVERSIFIED METALS & MINING—2.1% | | | | | |

Cia Vale do Rio Doce#

(Cost $763,634) | | 67,950 | | 1,121,855 | |

| | | | | |

CANADA—1.5% | | | | | |

COMMUNICATIONS EQUIPMENT—0.8% | | | | | |

Research In Motion Ltd.* | | 6,350 | | 441,325 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.5% | | | | | |

Potash Corporation of Saskatchewan Inc. | | 2,750 | | 237,848 | |

| | | | | |

GOLD—0.2% | | | | | |

Goldcorp Inc. | | 750 | | 20,640 | |

Yamana Gold Inc. | | 13,200 | | 104,412 | |

| | | | 125,052 | |

TOTAL CANADA

(Cost $709,924) | | | | 804,225 | |

| | | | | |

CAYMAN ISLANDS—0.8% | | | | | |

APPLICATION SOFTWARE—0.3% | | | | | |

VanceInfo Technologies Inc.#* | | 18,750 | | 149,250 | |

| | | | | |

EDUCATION SERVICES—0.2% | | | | | |

New Oriental Education & Technology Group#* | | 2,400 | | 127,152 | |

| | | | | |

INTERNET SOFTWARE & SERVICES—0.3% | | | | | |

Netease.com#* | | 4,450 | | 134,301 | |

| | | | | |

TOTAL CAYMAN ISLANDS

(Cost $289,620) | | | | 410,703 | |

| | | | | |

CHINA—24.9% | | | | | |

AUTOMOBILE MANUFACTURERS—0.7% | | | | | |

Great Wall Motor Co., Ltd.* | | 705,500 | | 376,866 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—0.7% | | | | | |

ZTE Corp. | | 111,748 | | 379,215 | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—1.8% | | | | | |

China High Speed Transmission Equipment Group Co., Ltd. | | 297,000 | | 536,506 | |

China National Materials Co., Ltd. | | 533,000 | | 409,886 | |

| | | | 946,392 | |

CONSTRUCTION MATERIALS—1.6% | | | | | |

China National Building Material Co., Ltd. | | 392,000 | | 833,554 | |

| | | | | |

DIVERSIFIED BANKS—2.6% | | | | | |

Bank of Communications Co., Ltd. | | 338,000 | | 275,628 | |

China Construction Bank Corp. | | 872,000 | | 509,688 | |

Industrial & Commercial Bank of China | | 1,019,000 | | 589,036 | |

| | | | 1,374,352 | |

| | | | | | |

10

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

CHINA—(CONT.) | | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—2.7% | | | | | |

Byd Co., Ltd. * | | 77,500 | | $ | 203,496 | |

JA Solar Holdings Co., Ltd. #* | | 111,750 | | 392,243 | |

Suntech Power Holdings Co., Ltd. #* | | 38,200 | | 570,325 | |

Yingli Green Energy Holding Co., Ltd. #* | | 34,600 | | 241,508 | |

| | | | 1,407,572 | |

ELECTRONIC COMPONENTS—0.5% | | | | | |

AAC Acoustic Technologies Holdings Inc. | | 482,000 | | 264,318 | |

| | | | | |

HEALTH CARE EQUIPMENT—1.0% | | | | | |

China Medical Technologies Inc.# | | 28,650 | | 559,821 | |

| | | | | |

INTEGRATED OIL & GAS—2.0% | | | | | |

China Petroleum & Chemical Corp. | | 1,062,000 | | 833,140 | |

PetroChina Co Ltd., CL. H | | 272,000 | | 240,408 | |

| | | | 1,073,548 | |

INTERNET SOFTWARE & SERVICES—2.4% | | | | | |

Baidu Inc. #* | | 2,700 | | 628,830 | |

Tencent Holdings Ltd. | | 70,000 | | 629,988 | |

| | | | 1,258,818 | |

LEISURE PRODUCTS—0.6% | | | | | |

Anta Sports Products Ltd. | | 350,000 | | 299,865 | |

| | | | | |

LIFE & HEALTH INSURANCE—4.3% | | | | | |

China Life Insurance Co., Ltd. | | 427,000 | | 1,515,132 | |

Ping An Insurance Group Co., of China Ltd. | | 117,000 | | 730,670 | |

| | | | 2,245,802 | |

PACKAGED FOODS & MEATS—1.0% | | | | | |

China Yurun Food Group Ltd. | | 228,000 | | 271,534 | |

Want Want China Holdings Ltd. | | 478,000 | | 239,921 | |

| | | | 511,455 | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—1.5% | | | | | |

Guangzhou R&F Properties Co., Ltd. | | 115,400 | | 188,508 | |

Sino-Ocean Land Holdings Ltd. | | 780,000 | | 582,724 | |

| | | | 771,232 | |

REAL ESTATE SERVICES—1.0% | | | | | |

E-House China Holdings Ltd.#* | | 45,850 | | 568,082 | |

| | | | | |

STEEL—0.5% | | | | | |

Maanshan Iron & Steel* | | 623,123 | | 254,872 | |

| | | | | |

TOTAL CHINA

(Cost $11,605,470) | | | | 13,125,764 | |

| | | | | |

HONG KONG—19.1% | | | | | |

ELECTRONIC MANUFACTURING SERVICES—0.6% | | | | | |

Ju Teng International Holdings Ltd.* | | 710,000 | | 311,478 | |

| | | | | |

EXCHANGE TRADED FUNDS—1.6% | | | | | |

iShares Asia Trust - iShares FTSE/Xinhua A50 China Tracker | | 592,300 | | 846,782 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.5% | | | | | |

China BlueChemical Ltd. | | 449,000 | | 239,848 | |

| | | | | | |

11

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HONG KONG—(CONT.) | | | | | |

GOLD—0.5% | | | | | |

Zhaojin Mining Industry Co Ltd. | | 199,000 | | $ | 257,796 | |

| | | | | |

INDUSTRIAL CONGLOMERATES—0.8% | | | | | |

Hutchison Whampoa Ltd. | | 69,000 | | 407,760 | |

| | | | | |

MARINE—0.4% | | | | | |

Orient Overseas International Ltd. | | 76,000 | | 220,641 | |

| | | | | |

MULTI-LINE INSURANCE—0.7% | | | | | |

China Insurance International Holdings Co., Ltd.* | | 204,000 | | 342,187 | |

| | | | | |

OIL & GAS EXPLORATION & PRODUCTION—1.6% | | | | | |

CNOOC Ltd. | | 739,000 | | 827,664 | |

| | | | | |

PAPER PRODUCTS—0.3% | | | | | |

Nine Dragons Paper Holdings Ltd. | | 353,685 | | 162,007 | |

| | | | | |

RAILROADS—0.4% | | | | | |

MTR Corp.* | | 91,203 | | 232,063 | |

| | | | | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—5.4% | | | | | |

Cheung Kong Holdings Ltd. | | 75,000 | | 787,726 | |

Cheung Kong Infrastructure Holdings Ltd. | | 47,728 | | 185,058 | |

China Resources Land Ltd. | | 184,705 | | 334,607 | |

New World Development Ltd. | | 443,000 | | 587,606 | |

Shimao Property Holdings Ltd. | | 258,500 | | 291,516 | |

Sino Land Co. | | 308,000 | | 397,412 | |

Sun Hung Kai Properties Ltd. | | 26,000 | | 270,563 | |

| | | | 2,854,488 | |

SPECIALIZED FINANCE—3.5% | | | | | |

Hong Kong Exchanges and Clearing Ltd. | | 160,550 | | 1,871,666 | |

| | | | | |

WIRELESS TELECOMMUNICATION SERVICES—2.8% | | | | | |

China Mobile Ltd. | | 167,000 | | 1,456,643 | |

| | | | | |

TOTAL HONG KONG

(Cost $8,514,855) | | | | 10,031,023 | |

| | | | | |

JAPAN—1.5% | | | | | |

HOME ENTERTAINMENT SOFTWARE—1.5% | | | | | |

Nintendo Co., Ltd.#

(Cost $820,902) | | 22,600 | | 760,490 | |

| | | | | |

SWITZERLAND—1.0% | | | | | |

OIL & GAS DRILLING—1.0% | | | | | |

Transocean Ltd.*

(Cost $353,425) | | 7,950 | | 536,466 | |

| | | | | |

TAIWAN—11.9% | | | | | |

COMPUTER HARDWARE—1.0% | | | | | |

Acer Inc. * | | 148,495 | | 284,207 | |

HTC Corp. * | | 21,000 | | 284,457 | |

| | | | 568,664 | |

COMPUTER STORAGE & PERIPHERALS—0.6% | | | | | |

InnoLux Display Corp.* | | 261,000 | | 288,435 | |

| | | | | | |

12

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

TAIWAN—(CONT.) | | | | | |

CONSTRUCTION MATERIALS—0.9% | | | | | |

Taiwan Cement Corp. | | 476,000 | | $ | 454,793 | |

| | | | | |

DISTRIBUTORS—0.8% | | | | | |

WPG Holdings Co., Ltd.* | | 505,000 | | 419,135 | |

| | | | | |

DIVERSIFIED BANKS—1.2% | | | | | |

Chinatrust Financial Holding Co., Ltd. * | | 663,000 | | 303,701 | |

First Financial Holding Co., Ltd. * | | 625,000 | | 330,703 | |

| | | | 634,404 | |

ELECTRICAL COMPONENTS & EQUIPMENT—1.3% | | | | | |

Cheng Uei Precision Industry Co., Ltd. * | | 281,000 | | 392,526 | |

Simplo Technology Co., Ltd. * | | 76,480 | | 292,522 | |

| | | | 685,048 | |

ELECTRONIC COMPONENTS—0.5% | | | | | |

Wintek Corp.* | | 563,000 | | 260,447 | |

| | | | | |

ELECTRONIC MANUFACTURING SERVICES—1.3% | | | | | |

HON HAI Precision Industry Co., Ltd. * | | 141,000 | | 407,565 | |

Young Fast Optoelectronics Co Ltd. | | 29,000 | | 256,036 | |

| | | | 663,601 | |

HEALTH CARE EQUIPMENT—0.5% | | | | | |

Apex Biotechnology Corp.* | | 144,000 | | 247,304 | |

| | | | | |

OTHER DIVERSIFIED FINANCIAL SERVICES—0.6% | | | | | |

Fubon Financial Holding Co., Ltd.* | | 390,000 | | 303,052 | |

| | | | | |

PACKAGED FOODS & MEATS—0.5% | | | | | |

Uni-President Enterprises Corp.* | | 263,000 | | 264,404 | |

| | | | | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—0.7% | | | | | |

Sinyi Realty Co.* | | 276,000 | | 349,658 | |

| | | | | |

SEMICONDUCTORS—2.0% | | | | | |

Advanced Semiconductor Engineering Inc. * | | 393,000 | | 211,511 | |

MediaTek Inc. * | | 31,000 | | 322,902 | |

Pixart Imaging Inc. * | | 40,000 | | 243,095 | |

Taiwan Semiconductor Manufacturing Co., Ltd. # | | 24,600 | | 260,022 | |

| | | | 1,037,530 | |

TOTAL TAIWAN

(Cost $5,230,689) | | | | 6,176,475 | |

| | | | | |

UNITED STATES—30.2% | | | | | |

AEROSPACE & DEFENSE—1.9% | | | | | |

BE Aerospace Inc.* | | 93,800 | | 1,012,102 | |

| | | | | |

AIR FREIGHT & LOGISTICS—2.0% | | | | | |

United Parcel Service Inc., Cl. B | | 20,100 | | 1,052,034 | |

| | | | | |

BIOTECHNOLOGY—0.7% | | | | | |

Alexion Pharmaceuticals Inc. * | | 4,900 | | 163,758 | |

Celgene Corp. * | | 4,600 | | 196,512 | |

| | | | 360,270 | |

CASINOS & GAMING—1.3% | | | | | |

Las Vegas Sands Corp.* | | 83,850 | | 655,707 | |

| | | | | | |

13

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

UNITED STATES—(CONT.) | | | | | |

COMMERCIAL PRINTING—0.3% | | | | | |

Warnaco Group Inc., /The* | | 4,550 | | $ | 131,222 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—4.1% | | | | | |

Cisco Systems Inc. * | | 57,800 | | 1,116,695 | |

Qualcomm Inc. | | 24,600 | | 1,041,072 | |

| | | | 2,157,767 | |

COMPUTER & ELECTRONICS RETAIL—0.2% | | | | | |

Best Buy Co., Inc. | | 3,200 | | 122,816 | |

| | | | | |

COMPUTER HARDWARE—0.6% | | | | | |

Apple Inc.* | | 2,300 | | 289,410 | |

| | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—1.9% | | | | | |

Cummins Inc. | | 9,700 | | 329,800 | |

Deere & Co. | | 15,450 | | 637,467 | |

| | | | 967,267 | |

DATA PROCESSING & OUTSOURCED SERVICES—0.5% | | | | | |

Mastercard Inc. | | 1,550 | | 284,348 | |

| | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—0.6% | | | | | |

First Solar Inc.* | | 1,700 | | 318,393 | |

| | | | | |

EXCHANGE TRADED FUNDS—1.1% | | | | | |

iShares MSCI Taiwan Index Fund | | 53,864 | | 550,490 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.5% | | | | | |

Mosaic Co., /The | | 7,750 | | 313,487 | |

| | | | | |

GENERAL MERCHANDISE STORES—0.6% | | | | | |

Target Corp. | | 7,850 | | 323,891 | |

| | | | | |

HYPERMARKETS & SUPER CENTERS—1.7% | | | | | |

Wal-Mart Stores Inc. | | 18,150 | | 914,760 | |

| | | | | |

INDUSTRIAL MACHINERY—0.9% | | | | | |

SPX Corp. | | 9,900 | | 457,083 | |

| | | | | |

INTERNET RETAIL—0.5% | | | | | |

Amazon.com Inc.* | | 3,150 | | 253,638 | |

| | | | | |

INTERNET SOFTWARE & SERVICES—1.5% | | | | | |

Yahoo! Inc.* | | 55,200 | | 788,807 | |

| | | | | |

OIL & GAS EQUIPMENT & SERVICES—1.0% | | | | | |

Smith International Inc. | | 19,800 | | 511,830 | |

| | | | | |

OTHER DIVERSIFIED FINANCIAL SERVICES—0.2% | | | | | |

Bank of America Corp. | | 11,600 | | 103,588 | |

| | | | | |

PHARMACEUTICALS—1.8% | | | | | |

Johnson & Johnson | | 18,000 | | 942,480 | |

| | | | | |

REAL ESTATE SERVICES—0.1% | | | | | |

Mack-Cali Realty Corp. | | 1,150 | | 30,889 | |

| | | | | |

RESTAURANTS—1.7% | | | | | |

Burger King Holdings Inc. | | 18,400 | | 300,656 | |

Yum! Brands Inc. | | 16,700 | | 556,945 | |

| | | | 857,601 | |

| | | | | | |

14

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

UNITED STATES—(CONT.) | | | | | |

SEMICONDUCTORS—2.1% | | | | | |

Altera Corp. | | 25,700 | | $ | 419,167 | |

Atheros Communications Inc. * | | 15,250 | | 262,605 | |

Intel Corp. | | 30,950 | | 488,390 | |

| | | | 1,170,162 | |

SPECIALIZED FINANCE—0.8% | | | | | |

CME Group Inc. | | 1,800 | | 398,430 | |

| | | | | |

SPECIALIZED REITS—0.1% | | | | | |

Host Hotels & Resorts Inc. | | 4,100 | | 31,529 | |

| | | | | |

SYSTEMS SOFTWARE—1.5% | | | | | |

Microsoft Corp. | | 38,150 | | 772,919 | |

| | | | | |

TOTAL UNITED STATES

(Cost $16,843,797) | | | | 15,772,920 | |

| | | | | |

TOTAL COMMON STOCKS

(Cost $45,972,562) | | | | 50,098,283 | |

| | | | | | |

| | PRINCIPAL | | | |

| | AMOUNT | | | |

CORPORATE BONDS—0.2% | | | | | |

UNITED STATES—0.2% | | | | | |

CASINOS & GAMING—0.2% | | | | | |

Wynn Las Vegas LLC / Wynn Las Vegas Capital Corp, 6.25%, 12/1/14

(Cost $82,215) | | 100,000 | | 85,000 | |

| | | | | |

SHORT-TERM INVESTMENTS—5.7% | | | | | |

TIME DEPOSITS—5.7% | | | | | |

Citibank London, 0.03%, 5/01/09

(Cost $2,994,409) | | 2,994,409 | | 2,994,409 | |

| | | | | |

Total Investments

(Cost $49,049,186)(a) | | 101.5 | % | 53,177,692 | |

Liabilities in Excess of Other Assets | | (1.5 | ) | (793,514 | ) |

NET ASSETS | | 100.0 | % | $ | 52,384,178 | |

| | | | | | |

* | | Non-income producing security. |

# | | American Depositary Receipts. |

(a) | | At April 30, 2009, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $51,942,537 amounted to $1,235,155 which consisted of aggregate gross unrealized appreciation of $6,832,068 and aggregate gross unrealized depreciation of $5,596,913. |

See Notes to Financial Statements.

15

ALGER CHINA-U.S. GROWTH FUND

Statement of Assets and Liabilities (Unaudited) April 30, 2009

ASSETS: | | | |

Investments in securities, at value (Identified cost)* | | | |

see accompanying schedules of investments | | $ | 53,177,692 | |

Foreign Cash** | | 5,508 | |

Receivable for investment securities sold | | 629,295 | |

Receivable for shares of beneficial interest sold | | 137,717 | |

Dividends and interest receivable | | 137,890 | |

Prepaid Expenses | | 34,925 | |

Total Assets | | 54,123,027 | |

LIABILITIES: | | | |

Payable for investment securities purchased | | 1,339,360 | |

Payable foreign currency contracts | | 16 | |

Payable for shares of beneficial interest redeemed | | 221,314 | |

Accrued investment advisory fees | | 49,891 | |

Accrued transfer agent fees | | 41,022 | |

Accrued distribution fees | | 10,586 | |

Accrued administrative fees | | 1,135 | |

Accrued other expenses | | 75,525 | |

Total Liabilities | | 1,738,849 | |

NET ASSETS | | $ | 52,384,178 | |

Net Assets Consist of: | | | |

Paid in capital | | 90,384,305 | |

Undistributed net investment income (accumulated loss) | | (260,960 | ) |

Undistributed net realized gain (accumulated loss) | | (41,867,762 | ) |

Net unrealized appreciation on investments | | 4,128,595 | |

NET ASSETS | | $ | 52,384,178 | |

SHARES OF BENEFICIAL INTEREST OUTSTANDING—NOTE 6 | | | |

Class A | | 4,873,011 | |

Class C | | 45,565 | |

Net Asset Value Per Share | | | |

Class A | | $ | 10.65 | |

Class C | | $ | 10.59 | |

Offering Price Per Share | | | |

Class A | | $ | 11.24 | |

Class C | | $ | 10.59 | |

*Identified Cost | | $ | 49,049,186 | |

**Cost Foreign Cash | | $ | 5,430 | |

See Notes to Financial Statements.

16

ALGER CHINA-U.S. GROWTH FUND

Statement of Operations (Unaudited)

For the six months ended April 30, 2009

INCOME: | | | |

Dividends (net of foreign withholding taxes*) | | $ | 360,112 | |

Interest (net of foreign withholding taxes*) | | 27 | |

Total Income | | 360,139 | |

EXPENSES | | | |

Advisory fees—Note 3(a) | | 292,980 | |

Distribution fees—Note 3(f): | | | |

Class A | | 60,635 | |

Class C | | 1,608 | |

Administrative fees—Note 3(a) | | 6,714 | |

Custodian fees | | 49,608 | |

Interest expenses | | 1,903 | |

Transfer agent fees and expenses—Note 3(b) | | 83,835 | |

Prepaid expenses | | 30,195 | |

Printing fees | | 21,575 | |

Professional fees | | 51,521 | |

Registration fees | | 6,696 | |

Trustee fees-Note 3(e) | | 6,447 | |

Miscellaneous | | 7,382 | |

Total Expenses | | 621,099 | |

NET INVESTMENT LOSS | | (260,960 | ) |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY TRANSACTIONS: | | | |

Net realized loss on investments | | (26,611,135 | ) |

Net realized loss on foreign currency transactions | | (3,286 | ) |

Net change in unrealized appreciation (depreciation) on investments and foreign currency translations | | 27,118,700 | |

Net realized and unrealized gain on investments, options and foreign currency | | 504,279 | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 243,319 | |

*Foreign withholding taxes | | $ | 7,382 | |

See Notes to Financial Statements.

17

ALGER CHINA-U.S. GROWTH FUND

Statements of Changes in Net Assets

| | For the | | | |

| | Six Months Ended | | For the | |

| | April 30, 2009 | | Year Ended | |

| | (Unaudited) | | October 31, 2008 | |

Net investment loss | | $ | (260,960 | ) | $ | (636,163 | ) |

Net realized loss on investments and foreign currency transactions | | (26,614,421 | ) | (15,006,368 | ) |

Net change in unrealized appreciation (depreciation) on investments, options and foreign currency translations | | 27,118,700 | | (86,405,116 | ) |

Net increase (decrease) in net assets resulting from operations | | 243,319 | | (102,047,647 | ) |

Distributions to shareholders from: | | | | | |

Net realized gains | | | | | |

Class A | | — | | (17,061,054 | ) |

Total distributions to shareholders | | — | | (17,061,054 | ) |

Increase (decrease) from shares of beneficial interest transactions: | | | | | |

Class A | | (13,183,452 | ) | (17,917,679 | ) |

Class C | | 120,694 | | 606,622 | |

Net decrease from shares of beneficial interest transactions—Note 6 | | (13,062,758 | ) | (17,311,057 | ) |

Total decrease | | (12,819,439 | ) | (136,419,758 | ) |

Net Assets: | | | | | |

Beginning of period | | 65,203,617 | | 201,623,375 | |

END OF PERIOD | | $ | 52,384,178 | | $ | 65,203,617 | |

Undistributed net investment income (accumulated loss) | | $ | (260,960 | ) | $ | — | |

See Notes to Financial Statements.

18

(This page has been intentionally left blank)

ALGER CHINA-U.S. GROWTH FUND

Financial Highlights for a share outstanding throughout the period

| | Class A | |

| | | | | | | | | | | | From | |

| | | | | | | | | | | | 11/3/2003 | |

| | | | | | | | | | | | (commencement | |

| | Six months | | | | | | | | | | of | |

| | ended | | Year ended | | Year ended | | Year ended | | Year ended | | operations) to | |

| | 4/30/2009(i) | | 10/31/2008 | | 10/31/2007 | | 10/31/2006 | | 10/31/2005 | | 10/31/2004(ii) | |

INCOME FROM INVESTMENT OPERATIONS | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 10.18 | | $ | 25.09 | | $ | 15.57 | | $ | 12.99 | | $ | 11.05 | | $ | 10.00 | |

Net investment loss(iii) | | (0.05 | ) | (0.08 | ) | (0.13 | ) | (0.04 | ) | (0.07 | ) | (0.08 | ) |

Net realized and unrealized gain (loss) on investments | | 0.52 | | (12.79 | ) | 11.67 | | 4.03 | | 2.01 | | 1.13 | |

Total from investment operations | | 0.47 | | (12.87 | ) | 11.54 | | 3.99 | | 1.94 | | 1.05 | |

Distributions from net realized gains | | — | | (2.04 | ) | (2.02 | ) | (1.41 | ) | — | | — | |

Net asset value, end of period | | $ | 10.65 | | $ | 10.18 | | $ | 25.09 | | $ | 15.57 | | $ | 12.99 | | $ | 11.05 | |

Total return | | 4.5 | % | (55.2 | )% | 83.0 | % | 33.5 | % | 17.6 | % | 10.5 | % |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 51,902 | | $ | 64,865 | | $ | 201,623 | | $ | 73,147 | | $ | 36,630 | | $ | 26,290 | |

Ratio of gross expenses to average net assets | | 2.55 | % | 2.15 | % | 2.17 | % | 2.36 | % | 2.77 | % | 2.87 | % |

Ratio of expense reimbursements to average net assets | | 0.00 | % | (0.25 | )% | (0.25 | )% | (0.16 | )% | (0.51 | )% | (0.43 | )% |

Ratio of net expenses to average net assets | | 2.55 | % | 1.90 | % | 1.92 | % | 2.20 | % | 2.26 | % | 2.44 | % |

Ratio of net investment income to average net assets | | (1.04 | )% | (0.43 | )% | (0.71 | )% | (0.30 | )% | (0.56 | )% | (0.81 | )% |

Portfolio turnover rate | | 111.47 | % | 190.60 | % | 107.57 | % | 192.21 | % | 288.53 | % | 267.42 | % |

(i) Unaudited. Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(ii) Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(iii) Amount was computed based on average shares outstanding during the period.

20

| | Class C | |

| | | | From | |

| | | | 3/3/2008 | |

| | | | (commencement | |

| | Six months | | of | |

| | ended | | operations) to | |

| | 4/30/2009(i) | | 10/31/2008(ii) | |

INCOME FROM INVESTMENT OPERATIONS | | | | | |

Net asset value, beginning of period | | $ | 10.16 | | $ | 18.20 | |

Net investment loss(iii) | | (0.09 | ) | (0.05 | ) |

Net realized and unrealized gain (loss) on investments | | 0.52 | | 7.99 | |

Total from investment operations | | 0.43 | | 8.04 | |

Net asset value, end of period | | $ | 10.59 | | $ | 10.16 | |

Total return | | 4.1 | % | (44.2 | )% |

RATIOS/SUPPLEMENTAL DATA: | | | | | |

Net assets, end of period (000’s omitted) | | $ | 482 | | $ | 339 | |

Ratio of gross expenses to average net assets | | 3.54 | % | 3.02 | % |

Ratio of expense reimbursements to average net assets | | 0.00 | % | (0.21 | )% |

Ratio of net expenses to average net assets | | 3.54 | % | 2.81 | % |

Ratio of net investment income to average net assets | | (1.99 | )% | (0.52 | )% |

Portfolio turnover rate | | 111.47 | % | 190.60 | % |

(i) Unaudited. Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(ii) Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(iii) Amount was computed based on average shares outstanding during the period.

21

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited)

NOTE 1 — General:

The Alger China-U.S. Growth Fund (formerly The China-U.S. Growth Fund) (the “Fund”) is a diversified open-end registered investment company organized as a business trust under the laws of the Commonwealth of Massachusetts. The Fund’s investment objective is long-term capital appreciation. It seeks to achieve its objective by normally investing in equity securities which are publicly traded in the United States, China, Hong Kong and Taiwan markets. The Fund commenced operations on November 3, 2003 with the issuance of 10,000 shares at $10.00 per share to Fred Alger Management, Inc. (“Alger Management”), the Fund’s investment manager. The Fund’s single share class was redesignated as Class A shares effective January 24, 2005, and are generally subject to an initial sales charge. Class C shares were first offered March 3, 2008, and are generally subject to a deferred sales charge.

NOTE 2 — Significant Accounting Policies:

(a) Investment Valuation: Investments of the Fund are valued on each day the New York Stock Exchange (the “NYSE”) is open as of the close of the NYSE (normally 4:00 p.m. Eastern time). Securities for which such information is readily available are valued at the last reported sales price or official closing price as reported by an independent pricing service on the primary market or exchange on which they are traded. In the absence of reported sales, securities are valued at a price within the bid and asked price or, in the absence of a recent bid or asked price, the equivalent as obtained from one or more of the major market makers for the securities to be valued.

Securities for which market quotations are not readily available are valued at fair value, as determined in good faith pursuant to procedures established by the Board of Trustees.

Securities in which the Fund invests may be traded in markets that close before the close of the NYSE. Developments that occur between the close of the foreign markets and the close of the NYSE (normally 4:00 p.m. Eastern time) may result in adjustments to the closing prices to reflect what the investment adviser, pursuant to policies established by the Board of Trustees, believes to be the fair value of these securities as of the close of the NYSE. The Fund may also fair value securities in other situations, for example, when a particular foreign market is closed but the Fund is open.

Short-term securities having a remaining maturity of sixty days or less are valued at amortized cost which approximates market value. Shares of mutual funds are valued at the net asset value of the underlying mutual fund.

Effective November 1, 2008, the Fund adopted Financial Accounting Standards Board Statement of Financial Accounting Standards No. 157, Fair Value Measurements (FAS 157). In accordance with FAS 157, fair value is defined as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. FAS 157 established a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for

22

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability and may be observable or unobservable. Observable inputs are based on market data obtained from sources independent of the Fund. Unobservable inputs are inputs that reflect the Fund’s own assumptions based on the best information available in the circumstances. The three-tier hierarchy of inputs is summarized in the three broad levels listed below:

· Level 1 – quoted prices in active markets for identical securities

· Level 2 – significant other observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

· Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, money market securities are valued using amortized cost, in accordance with rules under the Investment Company Act of 1940 (the “1940 Act”). Generally, amortized cost approximates the current fair value of a security, but since the value is not obtained from a quoted price in an active market, such securities are reflected as level 2.

The Fund’s valuation techniques are consistent with the market approach whereby process and other relevant information generated by market transactions involving identical or comparable assets are used to measure fair value.

The following is a summary of the inputs used as of April 30, 2009 in valuing the Fund’s investments carried at fair value:

DESCRIPTION | | TOTAL FUND | | LEVEL 1 | | LEVEL 2 | | LEVEL 3 | |

Alger China-U.S. Growth Fund | | | | | | | | | |

Investments in securities | | $ | 53,177,692 | | $ | 53,092,692 | | $ | 85,000 | | $ | — | |

Total | | $ | 53,177,692 | | $ | 53,092,692 | | $ | 85,000 | | $ | — | |

(b) Securities Transactions and Investment Income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the basis of identified cost. Dividend income is recognized on the ex-dividend date and interest income is recognized on the accrual basis. Occasionally, dividends are recorded as soon after the ex-dividend date as the Fund, using reasonable diligence, becomes aware of such dividends.

(c) Foreign Currency Translations: The books and records of the Fund are maintained in U.S. dollars. Foreign currencies, investments and other assets and liabilities are translated into U.S. dollars at the prevailing rates of exchange on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the prevailing exchange rates on the respective dates of such transactions.

Net realized gains and losses on foreign currency transactions represent net gains and losses from the disposition of foreign currencies, currency gains and losses realized between the trade dates and settlement dates of security transactions, and the difference

23

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

between the amount of net investment income accrued and the U.S. dollar amount actually received. The effects of changes in foreign currency exchange rates on investments in securities are included in realized and unrealized gain or loss on investments in the Statement of Operations.

(d) Dividends to Shareholders: Dividends and distributions payable to shareholders are recorded by the Fund on the ex-dividend date. Dividends from net investment income and distributions from net realized gains are declared and paid annually after the end of the fiscal year in which earned.

The characterization of distributions to shareholders for financial statement purposes is determined in accordance with federal income tax rules. Therefore, the source of the Fund’s distributions may be shown in the accompanying financial statements as either from, or in excess of net investment income, net realized gain on investment transactions or return of capital, depending on the type of book/tax differences that may exist. Capital accounts within the financial statements are adjusted for permanent book/tax differences. Reclassifications result primarily from the differences in tax treatment of net operating losses and foreign currency transactions. The reclassifications have no impact on the net asset value of the Fund and are designed to present the Fund’s capital accounts on a tax basis.

(e) Federal Income Taxes: It is the Fund’s policy to comply with the requirements of the Internal Revenue Code Subchapter M applicable to regulated investment companies and to distribute all of its investment company taxable income to its shareholders. Provided the Fund maintains such compliance, no federal income tax provision is required.

The Fund has adopted Financial Accounting Standards Board Interpretation No. 48 “Accounting for Uncertainty in Income Taxes” (‘FIN 48”). FIN 48 requires the Fund to measure and recognize in its financial statements the benefit of a tax position taken (or expected to be taken) on an income tax return if such position will more likely than not be sustained upon examination based on the technical merits of the position. The Fund files income tax returns in the US Federal jurisdiction, as well as the New York State and New York City jurisdictions. Based upon its review of tax positions for the Fund’s open tax years of 2005-2008 in these jurisdictions, the Fund has determined that FIN 48 did not have a material impact on the Fund’s financial statements for the six months ended April 30, 2009.

(f) Indemnification: The Fund enters into contracts that contain a variety of indemnification provisions. The Fund’s maximum exposure under these arrangements is unknown. The Fund does not anticipate recognizing any loss related to these arrangements.

(g) Estimates: These financial statements have been prepared in accordance with U.S. generally accepted accounting principles, which require using estimates and assumptions that affect the reported amounts therein. Actual results may differ from those estimates. These unaudited interim financial statements reflect all adjustments which are, in the opinion of management, necessary to a fair statement of results for the interim period presented. All such adjustments are of a normal recurring nature.

24

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

NOTE 3 — Investment Advisory Fees and Other Transactions with Affiliates:

(a) Investment Advisory and Administration Fees: Fees incurred by the Fund, pursuant to the provisions of its Investment Advisory Agreement and its Administration Agreement with Fred Alger Management, Inc. (Alger Management), are payable monthly and computed based on the value of the average daily net assets of the Fund, at the following rates:

Advisory | | Administration | |

Fee | | Fee | |

1.20 | % | 0.0275 | % |

Martin Currie, Inc., a registered investment advisor, acts as sub-advisor to the Fund under a written sub-advisory agreement with Alger Management.

(b) Shareholder Administrative Fees: : The Fund has entered into a shareholder administrative services agreement with Alger Management to compensate Alger Management on a per account basis for its liaison and administrative oversight of Boston Financial Data Services, Inc., the transfer agent for the Fund (“BFDS”) and other related services. During the six months ended April 30, 2009, the Fund incurred fees of $10,943 for these services provided by Alger Management.

(c) Sales Charges: Purchases of shares of the Fund may be subject to initial sales charges or contingent deferred sales charges. For the six months ended April 30, 2009, the initial sales charges and contingent deferred sales charges retained by Fred Alger & Company (the “Distributor”), were approximately $1,736 and $0, respectively. The contingent deferred sales charges are used by the Distributor to offset distribution expenses previously incurred. Sales charges do not represent expenses of the Fund.

(d) Brokerage Commissions: During the six months ended April 30, 2009, the Fund paid Fred Alger & Company, Incorporated (“Alger Inc.”), an affiliate of Alger Management, $34,501 in connection with securities transactions.

(e) Trustees’ Fees: The Fund pays each trustee who is not affiliated with Alger Management or its affiliates $500 for each meeting attended, to a maximum of $2,000 per annum. The chairman of the Board of Trustees receives an additional annual fee of $10,000 which is paid, pro rata, by all funds managed by Alger Management. Additionally, each member of the audit committee receives an additional $50 for each audit committee meeting attended, to a maximum of $200 per annum.

(f) Distribution/Shareholder Servicing Fees: The Fund has adopted a distribution plan pursuant to which the Fund pays Alger Inc. a fee at the annual rate of .25% of the average daily net assets of the Class A shares and 1.00% of the daily net assets of the Class C shares to compensate Alger Inc. for its activities and expenses incurred in distributing the Fund’s shares and shareholder servicing. Fees charged may be more or less than the expenses incurred by Alger Inc.

(g) Other Transactions with Affiliates: Certain trustees and officers of the Fund are directors and officers of Alger Management, the Distributor and Alger Services.

25

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

NOTE 4 — Securities Transactions:

The following summarizes the securities transactions by the Fund, other than short-term securities, for the six months ended April 30, 2009:

| | PURCHASES | | SALES | |

China-U.S. Growth Fund | | $ | 45,767,708 | | $ | 61,196,080 | |

| | | | | | | |

Transactions in foreign securities may involve certain considerations and risks not typically associated with those of U.S. companies because of, among other factors, the level of governmental supervision and regulation of foreign security markets, and the possibility of political or economic instability.

NOTE 5 — Borrowings:

The Fund may borrow from its custodian on an uncommitted basis. For the six months ended April 30, 2009, the Fund had the following borrowings:

| | AVERAGE | | WEIGHTED AVERAGE | |

| | BORROWING | | INTEREST RATE | |

China-U.S. Growth Fund | | $ | 169,834 | | 3.24 | % |

| | | | | | |

NOTE 6 — Share Capital:

(a) The Fund has an unlimited number of authorized shares of beneficial interest of $.001 par value. Transactions of shares of beneficial interest were as follows:

| | FOR THE SIX MONTHS ENDED | | FOR THE YEAR ENDED | |

| | APRIL 30, 2009 | | OCTOBER 31, 2008 | |

| | SHARES | | AMOUNT | | SHARES | | AMOUNT | |

ALGER CHINA-U.S. GROWTH FUND | | | | | | | | | |

Class A: | | | | | | | | | |

Shares sold | | 328,899 | | $ | 3,131,615 | | 2,119,855 | | $ | 41,320,905 | |

Dividends reinvested | | — | | — | | 692,401 | | 13,695,683 | |

Shares redeemed | | (1,825,031 | ) | (16,315,067 | ) | (4,480,405 | ) | (72,934,267 | ) |

Net decrease | | (1,496,132 | ) | $ | (13,183,452 | ) | (1,668,149 | ) | $ | (17,917,679 | ) |

Class C: | | | | | | | | | |

Shares sold | | 20,416 | | $ | 195,010 | | 38,183 | | $ | 662,404 | |

Shares redeemed | | (8,169 | ) | (74,316 | ) | (4,865 | ) | (55,782 | ) |

Net increase | | 12,247 | | $ | 120,694 | | 33,318 | | $ | 606,622 | |

(b) Redemption Fee: The Fund may impose a 2.00% redemption fee on Fund shares redeemed (including shares redeemed by exchange) less than 30 days after such shares were acquired. The fees retained by the Fund are included as paid-in capital on the Statement of Assets and Liabilities and were as follows:

26

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

For the Six | | For the | |

Months Ended | | Year Ended | |

April 30, 2009 | | October 31, 2008 | |

$ | 22,950 | | $ | 443,981 | |

| | | | | |

NOTE 7 — Tax Character of Distributions to Shareholders:

The tax character of distributions paid during the six months ended April 30, 2009 and the year ended October 31, 2008 was as follows:

| | SIX MONTHS ENDED | | YEAR ENDED | |

| | April 30, 2009 | | October 31, 2008 | |

Distributions paid from: | | | | | |

Ordinary Income | | — | | $ | 13,376,314 | |

Long-term capital gain | | — | | 3,684,739 | |

Total distributions paid | | — | | $ | 17,061,053 | |

As of October 31, 2008, the components of distributable earnings on a tax basis were as follows:

CHINA-U.S. GROWTH FUND | | | |

Undistributed ordinary income | | $ | — | |

Undistributed long-term gain | | — | |

Unrealized appreciation | | $ | (25,883,456 | ) |

The difference between book basis and tax basis unrealized appreciation is determined annually and is attributable primarily to the tax deferral of losses on wash sales.

At October 31, 2008, the Fund, for federal income tax purposes, had capital loss carryforward of $12,021,793 which expires in 2016. This amount may be applied against future net realized gains until the earlier of their utilization or expiration.

NOTE 8 — Litigation:

The Manager has responded to inquiries, document requests and/or subpoenas from various regulatory authorities in connection with their investigations of practices in the mutual fund industry identified as “market timing” and “late trading.” On October 11, 2006, the Manager, the Distributor and Alger Shareholder Services, Inc. executed an Assurance of Discontinuance with the Office of the New York State Attorney General (“NYAG”). On January 18, 2007, the Securities and Exchange Commission (the “SEC”) approved a settlement with the Manager and the Distributor. As part of the settlements with the NYAG and the SEC, without admitting or denying liability, the firms consented to the payment of $30 million to reimburse fund shareholders; a fine of $10 million; and certain other remedial measures including a reduction in management fees of $1 million

27

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

per year for five years. The $40 million was paid into an SEC Fair Fund for distribution to investors.

On August 31, 2005, the West Virginia Securities Commissioner (the “WVSC”), in an ex parte Summary Order to Cease and Desist and Notice of Right to Hearing, concluded that the Manager and the Distributor had violated the West Virginia Uniform Securities Act (the “WVUSA”), and ordered the Manager and the Distributor to cease and desist from further violations of the WVUSA by engaging in the market-timing-related conduct described in the order. The ex parte order provided notice of their right to a hearing with respect to the violations of law asserted by the WVSC. Other firms unaffiliated with the Manager were served with similar orders. The Manager and the Distributor intend to request a hearing for the purpose of seeking to vacate or modify the order.

In addition, in 2003 and 2004 several purported class actions and shareholder derivative suits were filed against various parties in the mutual fund industry, including the Manager, certain mutual funds managed by the Manager (the “Alger Mutual Funds”), and certain current and former Alger Mutual Fund trustees and officers, alleging wrongful conduct related to market-timing and late-trading by mutual fund shareholders. These cases were transferred to the U.S. District Court of Maryland by the Judicial Panel on Multidistrict Litigation for consolidated pre-trial proceedings under the caption number 1:04-MD-15863 (JFM). After a number of the claims were dismissed by the court, the class and derivative suits were settled in principle, but such settlement remains subject to court approval.

NOTE 9 — Recent Accounting Pronouncements:

In March 2008, the Financial Accounting Standards Board issued the Statement of Financial Accounting Standards No. 161, Disclosures about Derivative Instruments and Hedging Activities (“FAS 161”). FAS 161 is effective for fiscal years and interim periods beginning after November 15, 2008. FAS 161 requires enhanced disclosures about the Fund’s derivative and hedging activities, including how such activities are accounted for and their effect on the Fund’s financial position, performance and cash flows. Management is currently evaluating the impact the adoption of FAS 161 will have on the Fund’s financial statements and related disclosures.

In April 2009, FASB issued a new Staff Position FSP FAS 157-4 which amends FASB Statement No. 157, Fair Value Measurements, and is effective for interim and annual periods ending after June 15, 2009. FSP FAS 157-4 provides additional guidance when the volume and level of activity for the asset or liability measured at fair value has significantly decreased. Additionally, FSP FAS 157-4 expands disclosure by reporting entities with respect to categories of assets and liabilities carried at fair value. Management is currently evaluating the impact the adoption of FSP FAS 157-4 will have on the Funds’ financial statements and related disclosures.

In May 2009, FASB issued Statement of Financial Accounting Standards No. 165, Subsequent Events (“FAS 165”), which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued or are available to be issued. Although there is new terminology, the standard is based on

28

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Unaudited) (Continued)

the same principles as those that currently exist in the auditing standards. The standard, which includes a new required disclosure of the date through which an entity has evaluated subsequent events, is effective for interim or annual periods ending after June 15, 2009. Management is currently evaluating the impact the adoption of FAS 165 will have on the Funds’ financial statements and related disclosures.

29

ALGER CHINA-U.S. GROWTH FUND

ADDITIONAL INFORMATION (Unaudited)

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: transaction costs, if applicable, including sales charges (loads) and redemption fees; and ongoing costs, including management fees, distribution (12b-1) fees, if applicable, and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example below is based on an investment of $1,000 invested at the beginning of the six-month period starting November 1, 2008 and ending April 30, 2009.

Actual Expenses

The first line for each class of shares in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you would have paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each class of shares in the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios for each class of shares and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as sales charges (loads) and redemption fees. Therefore, the second line under each class of shares in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

30

| | | | | | | | Ratio of | |

| | | | | | | | Expenses to | |

| | | | | | | | Average | |

| | | | | | Expenses | | Net Assets | |

| | Beginning | | Ending | | Paid During | | For the | |

| | Account | | Account | | the Six Months | | Six Months | |

| | Value | | Value | | Ended | | Ended | |

| | November 1, 2008 | | April 30, 2009 | | April 30, 2009(a) | | April 30, 2009(b) | |

ALGER CHINA-U.S. GROWTH FUND | | | | | | | | | |

Class A | Actual | | $ | 1,000.00 | | $ | 1,045.10 | | $ | 12.93 | | 2.55 | % |

| Hypothetical(c) | | 1,000.00 | | 1,012.15 | | 12.72 | | 2.55 | |

Class C | Actual | | 1,000.00 | | 1,041.30 | | 17.92 | | 3.54 | |

| Hypothetical(c) | | 1,000.00 | | 1,007.24 | | 17.62 | | 3.54 | |

| | | | | | | | | | | | | |

(a) | Expenses are equal to the annualized expense ratio of the respective share class, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

(b) | Annualized |

(c) | 5% annual return before expenses. |

31

Proxy Voting Policies

A description of the policies and procedures the Trust uses to determine how to vote proxies relating to portfolio securities and the proxy voting record is available, without charge, by calling (800) 992-3863 or online on the Funds’ website at http://www.alger.com or on the SEC’s website at http://www.sec.gov.

Fund Holdings

The Funds’ most recent month end portfolio holdings are available approximately sixty days after month end on the Funds’ website at www.alger.com. The Funds also file their complete schedule of portfolio holdings with the SEC for the first and third quarter of each fiscal year on Form N-Q. The Funds’ Forms N-Q is available online on the SEC’s website at http://www.sec.gov or may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information regarding the operation of the SEC’s Public Reference Room may be obtained by calling 1-800-SEC-0330. A copy of the most recent quarterly holdings may also be obtained from the Funds by calling (800) 992-3863.

Change in Independent Registered Public Accounting Firm

On May 12, 2009, Deloitte & Touche LLP was selected as the Fund’s independent registered public accounting firm for the 2009 fiscal year. A majority of the Fund’s Board of Trustees, including a majority of the Independent Trustees, approved the appointment of Deloitte & Touche LLP. The predecessor independent registered public accounting firm’s report on the Fund’s financial statements for the year ended October 31, 2008 and the year ended October 31, 2007 contained no adverse opinion or disclaimer of opinion and were not qualified or modified as to uncertainty, audit scope or accounting principles. During such fiscal periods and through May 12, 2009, there were no disagreements between the Fund and the predecessor independent registered public accounting firm on any matter of accounting principles or practices, financial statement disclosure, or audit scope or procedures, which such disagreements, if not resolved to the satisfaction of the predecessor independent registered public accounting firm, would have caused them to make reference to the subject matter of the disagreement in connection with their reports on the financial statements for such fiscal periods.

32

(This page has been intentionally left blank.)

(This page has been intentionally left blank.)

(This page has been intentionally left blank.)

(This page has been intentionally left blank.)

ALGER CHINA-U.S. GROWTH FUND

111 Fifth Avenue

New York, NY 10003

(800) 992-3362

www.alger.com

Investment Manager

Fred Alger Management, Inc.

111 Fifth Avenue

New York, NY 10003

Distributor

Fred Alger & Company, Incorporated

111 Fifth Avenue

New York, NY 10003

Transfer Agent and Dividend Disbursing Agent

Boston Financial Data Services, Inc.

P.O. Box 8480

Boston, MA 02266

This report is submitted for the general information of the shareholders of The Alger Funds. It is not authorized for distribution to prospective investors unless accompanied by an effective Prospectus for the Trust, which contains information concerning the Trust’s investment policies, fees and expenses as well as other pertinent information.

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online. When documents such as prospectuses and annual and semi-annual reports are available, we’ll send you an e-mail notification with a convenient link that will take you directly to the fund information on our website. To sign up for this free service, simply enroll at www.icsdelivery.com/alger.

SAC 043009

ITEM 2. CODE OF ETHICS.

Not applicable.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT.

Not applicable.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES.

Not applicable.

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANTS.

Not applicable.

ITEM 6. INVESTMENTS.

Not applicable.

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED END MANAGEMENT INVESTMENT COMPANIES.

Not applicable.

ITEM 8. PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

Not applicable.

ITEM 9. PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS.

Not applicable.