| | OMB APPROVAL |

| | OMB Number: | 3235-0570 |

| | Expires: | January 31, 2014 |

| UNITED STATES | Estimated average burden hours per response. . . . . . . . . . . . . . . . .20.6 |

| SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| | | | |

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21308 |

|

Alger China-U.S. Growth Fund |

(Exact name of registrant as specified in charter) |

|

360 Park Ave South New York, New York | | 10010 |

(Address of principal executive offices) | | (Zip code) |

|

Mr. Hal Liebes

Fred Alger Management, Inc.

360 Park Ave South

New York, New York 10010 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 212-806-8800 | |

|

Date of fiscal year end: | October 31 | |

|

Date of reporting period: | October 31, 2011 | |

| | | | | | | | |

ITEM 1. REPORTS TO STOCKHOLDERS.

Alger China-U.S. Growth Fund | |

| |

ANNUAL REPORT | |

October 31, 2011 | |

Table of Contents

ALGER CHINA-U.S. GROWTH FUND

Letter to Our Shareholders (Unaudited) | 1 |

| |

Fund Highlights (Unaudited) | 8 |

| |

Portfolio Summary (Unaudited) | 10 |

| |

Schedule of Investments | 11 |

| |

Statement of Assets and Liabilities | 18 |

| |

Statement of Operations | 19 |

| |

Statements of Changes in Net Assets | 20 |

| |

Financial Highlights | 21 |

| |

Notes to Financial Statements | 23 |

| |

Report of Independent Registered Public Accounting Firm | 33 |

| |

Additional Information (Unaudited) | 34 |

Go Paperless With Alger Electronic Delivery Service

Alger is pleased to provide you with the ability to access regulatory materials online. When documents such as prospectuses and annual and semi-annual reports are available, we’ll send you an e-mail notification with a convenient link that will take you directly to the fund information on our website. To sign up for this free service, simply enroll at www.icsdelivery.com/alger.

Dear Shareholders, | | December 1, 2011 |

A Challenging Year

Market volatility surged during the 12-month period ended October 31, 2011, as fears grew over the euro-zone sovereign debt crisis and U.S. deficit spending. As the year progressed, political paralysis on both sides of the Atlantic fueled pessimism over elected officials’ ability to resolve both of those issues. Investors also grew increasingly cautious as the global economic recovery appeared to lose steam. For the 12-month period, the S&P 500 Index generated an 8.09% return.

For Alger, challenging times are nothing new. Over the course of our more than 45-year history, we have honed our investment strategy during both up and down markets. In doing so, we have experienced Black Monday of 1987, the Asian Crisis of 1997, the dot com bubble burst of 2000, the terrorist attacks of 2001, and the subprime mortgage crisis of 2007 to 2010. Based on our review of past crises and our view of U.S. economic fundamentals, we maintain that equity markets—while still facing various challenges—have strong potential to rally once the euro-zone crisis is resolved. We also believe that investor pessimism—as measured by an equity risk premium that has reached a 55-year high and by high free-cash-flow yields—may be excessive, especially when viewed from a historical perspective.

Government Policies Drive Market Volatility

In some ways, markets performed in a predictable fashion during the reporting period. Markets advanced when investors perceived that progress was being made on the U.S. debt ceiling debate and on the euro-zone crisis. Conversely, markets declined when it appeared that those issues were worsening. For example, during the early portion of the third quarter of 2011, concerns grew that feuding parties in Congress would fail to raise the country’s $14.3 trillion debt ceiling, which could have prompted an unpopular government shutdown and a default on U.S. debt. The nations’ leaders finally agreed shortly before an August 2 deadline to raise the debt ceiling and to cut at least $2.1 trillion from the nation’s spending. In the process, however, many investors lost confidence in Washington’s ability to tackle tough problems, including structural budget issues that have contributed to deficit spending. Investors weren’t the only ones to express disappointment. Standard & Poor’s, which had been threatening for months to downgrade its U.S. debt rating, pulled the trigger shortly after the debt ceiling agreement was announced, signaling a lack of confidence in the nation’s ability to enact meaningful budget reform.

Broadly speaking, U.S. economic headline numbers also disappointed. The U.S. Department of Commerce lowered its early second quarter GDP growth estimate of 1.3% to 1% and the International Monetary Fund lowered its 2012 U.S. GDP forecast from 2.7% to 2%. Unemployment in July and August, meanwhile, lingered at a discouragingly high rate of 9.1%. The economic slowdown didn’t go unnoticed: the Conference Board’s Consumer Confidence Index for August tumbled from 59.2 to 44.5, its lowest level in more than two years.

1

In Europe, the sovereign debt problem lingered and at times appeared to worsen, with riots in Greece sparked by new austerity measures being implemented to fulfill requirements of debt relief programs. Debate over the nature, size, and conditions of relief programs continued among leaders of European nations and organizations such as the IMF, the European Financial Stability Facility and the European Central Bank (ECB), sparking fear among investors that the crisis may grind on and send Europe and possibly other regions into an economic slowdown. Concerns grew that troubled European countries would face a funding emergency as high interest rates made issuing debt difficult.

Euro-Zone Crisis in Perspective

Estimates of the range of potential euro-zone write-downs vary considerably, but losses could be as high as 600 billion euros, according to J.P. Morgan. That amount is comparable to losses from the 1997 Asian crisis on an inflation-adjusted basis, but it is dwarfed by the $2.7 trillion in losses resulting from the U.S. subprime mortgage crisis of 2007-2010. That crisis drove U.S. equity markets down more than 40%, until markets eventually rallied. We note that in the Asian Crisis, U.S. equity markets declined approximately 20% and then rallied 33% in the three months after the issue was resolved. We believe that once the fear of the euro crisis is alleviated, a market rally is likely. While it’s hard to say how and when the euro-zone issue will be resolved, elected officials and organizations such as the ECB and the IMF are under increasing pressure to take action. In the meantime, investors’ high level of fear is currently illustrated by an equity risk premium of 6.27%, according to J.P. Morgan. The 6.27% premium, in addition to exceeding the premium during the subprime mortgage crisis, is at a 55-year high, even though the potential scope of the euro-zone crisis is considerably smaller than the subprime debacle.

Reasons for Optimism with U.S. Economy

One reason that we believe a rally is possible once the euro-zone crisis is resolved is that in many ways, the U.S. economy, despite many gloomy headline developments, is stronger than during the subprime mortgage crisis. We believe that the U.S. economy has considerable potential for expanding. In the aftermath of the mortgage crisis, U.S. corporations have consistently expanded their earnings and exhibited strong discipline with spending, which has allowed them to reduce leverage and to accumulate record levels of cash. As of the second quarter, U.S. corporations held $2 trillion in cash, which is an all-time high. Corporate earnings have also been strong, with year-over year quarterly increases having occurred for every quarter since the third quarter of 2009. With strong balance sheets, many U.S. corporations are well prepared to weather moderating GDP growth and to continue to seek attractive opportunities in emerging markets and from large scale trends, such as the increasing use of Internet-connected devices. Deep corporate coffers, furthermore, are allowing businesses to buy back stock, implement or increase dividends, and engage in mergers and acquisitions, all of which support equity valuations and serve as economic stimuli.

2

Unemployment, of course, continues to be a hurdle for the U.S. economic recovery. It is important to realize, however, that the private sector is creating jobs, granted at a discouragingly slow pace, while public employers downsize their workforces. At the same time, however, we believe that GDP growth may eventually surprise on the upside as real estate markets and industrial activity improve. So far, the languishing housing market has been a considerable drag on GDP, with well-above average inventories of homes in many markets. With large volumes of foreclosure sales, real estate values are depressed and tight lending requirements are making it difficult for many Americans to qualify for mortgages. Yet, our proprietary research also shows some glimmer of improvement, with some markets experiencing increases in prices and transaction volumes. This is particularly true with high-end real estate, but other select high-quality markets are also seeing improvements. U.S. industry, particularly automobile manufacturing, may also support GDP growth. Auto manufacturing increased 5.2% in July after having declined for three straight months following supply chain disruptions associated with the Japan disasters. Supply chain improvements since then have clearly facilitated an increase in manufacturing levels, but other factors may be involved. Indeed, demand for new cars in the U.S. has been growing among frugal consumers who have refrained from buying big ticket items. According to estimates from Edmunds.com, Americans are expected to buy only 12.6 million vehicles in 2011, down from 12.9 as estimated previously by the firm. That is a considerable decline from the 16 million to 17 million cars typically sold each year. In delaying new car purchases, consumers have allowed their autos to age considerably, with the average car in the U.S. being 11 years old, according to R. L. Polk & Co., which tracks automobile data. That is a considerable increase from 1995, when the average car was only 8.4 years old. American consumers, of course, will eventually need to replace their aging automobiles. When they do, they will provide a strong growth opportunity for the automobile industry and a boost to U.S. GDP.

Going Forward

Slowing economic growth, the euro-zone crisis, and the debt ceiling debate have clearly damaged investor sentiment. With that in mind, forecasting the timing and the scope of a possible equity rally is fraught with potential pitfalls, including uncertainty over how the U.S. will address deficit spending and the timeframe for a resolution of the euro-zone issue. We note, however, that equity valuations point to stocks being highly attractive. As of October 31, the S&P 500 price-to-earnings ratio was only 14.26 based on 2011 earnings of 87.92 per share, according to Standard & Poor’s. In comparison, the 50-year historical average P/E for the S&P 500 at the end of the third quarter was 19.11, according to Standard & Poor’s.

We remind readers that our bottom up stock selection is not based on making broad market judgments. Rather, we conduct careful analysis of companies and industry sectors. We believe our focus on companies that are best suited to respond to constant changes occurring among consumers and industries can provide our clients with attractive investment performance. We remain committed to our highly-disciplined, research-driven investment strategy that we believe helps us find the most compelling opportunities for our clients.

3

Portfolio Matters

The Alger China-U.S. Growth Fund returned -9.63% for the 12-month period ended October 31, 2011, compared to the -13.51% return of the MSCI Zhong Hua Index and the 8.09% return of the S&P 500 Index.

As of October 1, 2011, Fred Alger Management, Inc. replaced Martin Currie, Inc., which had served as sub-advisor to the Fund. Fred Alger Management Chief Executive Officer and Chief Investment Officer Dan Chung, CFA, and Alger Senior Vice President and Portfolio Manager Deborah Vélez Medenica, CFA, are now responsible for the day-to-day management of the Fund.

During the one-year period, the largest sector weightings in the Alger China-U.S. Growth Fund were in the Information Technology and Industrials sectors. The largest sector overweight for the period was in Information Technology and the largest sector underweight for the period was in Health Care. Relative outperformance in the Utilities and Materials sectors was the most important contributor to performance, while Financials and Industrials detracted from results.

Among the most important relative contributors were Dongyue Group; Spreadtrum Communications, Inc.; Sina Corp.; Westport Innovations, Inc.; and Baidu, Inc. Shanghai-based Spreadtrum designs, develops, and markets semiconductor products for wireless communications. During the reporting period, its 2G solution continued to sell well and the company’s gross margin guidance exceeded that of its Taiwanese competitor, Mediatek.

Conversely, detracting from overall results on a relative basis were Exxon Mobil Corp.; Noah Holdings Ltd.; VanceInfo Technologies Inc.; China Life Insurance Co. Ltd.; and O-Net Communications Ltd. VanceInfo Technologies is a China-based offshore IT service provider that serves U.S. and European multinationals domiciled in China. Its stock performance was weak in the second quarter after it announced results that were modestly above consensus expectations, but nevertheless disappointed investors who are accustomed to the company substantially exceeding expectations.

As always, we strive to deliver consistently superior investment results for you, our shareholders, and we thank you for your business and your continued confidence in Alger.

Respectfully submitted, | |

| |

| |

| |

Daniel C. Chung, CFA | |

Chief Investment Officer | |

Investors cannot invest directly in an index. Index performance does not reflect the deduction for fees, expenses, or taxes.

4

This report and the financial statements contained herein are submitted for the general information of shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless proceeded or accompanied by an effective prospectus for the Fund. Fund performance returns represent the fiscal 12-month period return of Class A shares prior to the deduction of any sales charges and include the reinvestment of any dividends or distributions.

The performance data quoted represents past performance, which is not an indication or guarantee of future results.

Standardized performance results can be found on the following pages. The investment return and principal value of an investment in a Fund will fluctuate so that an investor’s shares when redeemed may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, visit us at www.alger.com, or call us at (800) 992-3863.

The views and opinions of the Fund’s management in this report are as of the date of the Shareholders letter and are subject to change at any time subsequent to this date. There is no guarantee that any of the assumptions that formed the basis for the opinions stated herein are accurate or that they will materialize. Moreover, the information forming the basis for such assumptions is from sources believed to be reliable, however, there is no guarantee that such information is accurate. Any securities mentioned, whether owned in a Fund or otherwise, are considered in the context of the construction of an overall portfolio of securities and therefore reference to them should not be construed as a recommendation or offer to purchase or sell any such security. Inclusion of such securities in a Fund and transactions in such securities, if any, may be for a variety of reasons, including without limitation, in response to cash flows, inclusion in a benchmark, and risk control. The reference to a specific security should also be understood in such context and not viewed as a statement that the security is a significant holding in a Fund. Please refer to the Schedule of Investments for the Fund which is included in this report for a complete list of Fund holdings as of October 31, 2011.

A Word about Risk

Growth stocks tend to be more volatile than other stocks as the price of growth stocks tends to be higher in relation to their companies’ earnings and may be more sensitive to market, political, and economic developments. Investing in the stock market involves gains and losses and may not be suitable for all investors. Stocks of small- and mid-sized companies are subject to greater risk than stocks of larger, more established companies owing to such factors as limited liquidity, inexperienced management, and limited financial resources. Investing in foreign securities involves additional risk (including currency risk, risks related to political, social, or economic conditions, and risks associated with the Chinese markets, such as increased volatility, limited liquidity, less stringent regulatory and legal system, and lack of industry and country diversification), and may not be suitable for all investors. Funds that participate in leveraging, such as the Alger China-U.S. Growth Fund, are

5

subject to the risk that borrowing money to leverage will exceed the returns for securities purchased or that the securities purchased may actually go down in value; thus, the Fund’s net asset value can decrease more quickly than if the Fund had not borrowed. For a more detailed discussion of the risks associated with the Fund, please see the Fund’s Prospectus.

Before investing, carefully consider a Fund’s investment objective, risks, charges, and expenses. For a prospectus or a summary prospectus containing this and other information about the Fund call us at (800) 992-3863 or visit us at www.alger.com. Read it carefully before investing.

Fred Alger & Company, Incorporated, Distributor. Member NYSE Euronext, SIPC.

NOT FDIC INSURED. NOT BANK GUARANTEED. MAY LOSE VALUE.

6

Definitions:

· Standard & Poor’s is a credit rating agency and provider of financial data.

· Edmunds.com provides research and publications covering the automobile industry.

· Standard & Poor’s 500 Index (S&P 500 Index) is an index of 500 leading companies in leading industries in the United States.

· The MSCI Zhong Hua Index is an aggregate of the MSCI Hong Kong Index (a capitalization-weighted index that monitors the performance of stocks from Hong Kong) and the MSCI China Free Index (an unmanaged market capitalization-weighted index of Chinese companies available to non-domestic investors).

FUND PERFORMANCE AS OF 9/30/11 (Unaudited) †

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | Since

11/3/2003 | |

Alger China-U.S. Growth Class A (Inception 11/3/03) | | -21.10 | | 1.20 | | 7.47 | |

Alger China-U.S. Growth Class C (Inception 3/3/08)* | | -18.16 | | 1.62 | | 7.45 | |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains.

† | Returns reflect maximum sales charges on Class A shares and applicable contingent deferred sales charges on Class C shares. |

| |

* | Performance figures prior to 3/3/08, inception of Class C shares, are those of the Fund’s Class A shares. Performance has been adjusted to remove the front-end sales charge imposed by Class A shares. Class C shares do not impose a front-end sales charge but do impose a contingent deferred sales charge of 1% on shares redeemed. If Class A sales charges were reflected, annual returns for the Class C shares would be lower. The performance figures prior to 3/3/08 have also been adjusted to reflect the higher operating expenses and applicable contingent deferred sales charge of Class C shares. |

7

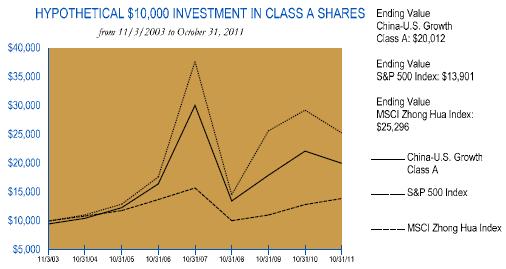

ALGER CHINA-U.S. GROWTH FUND

Fund Highlights Through October 31, 2011 (Unaudited)

The chart above illustrates the growth in value of a hypothetical $10,000 investment made in the Alger China-U.S. Growth Fund Class A shares, with an initial maximum sales charge of 5.25%, and the S&P 500 Index and the MSCI Zhong Hau Index (unmanaged indices of common stocks) from November 3, 2003, the inception date of the Alger China-U.S. Growth Fund Class A shares, through October 31, 2011. The figures for the Alger China-U.S. Growth Fund Class A shares, the S&P 500 Index, and the MSCI Zhong Hau Index include reinvestment of dividends. Performance for the Alger China-U.S. Growth Fund Class C shares will vary from the results shown above due to differences in expenses and sales charges that class bears.

Investors cannot invest directly in any index. Index performance does not reflect deduction for fees, expenses, or taxes.

PERFORMANCE COMPARISON AS OF 10/31/11 †

AVERAGE ANNUAL TOTAL RETURNS

| | 1 YEAR | | 5 YEARS | | Since

11/3/2003 | |

Class A (Inception 11/3/03) | | (14.39 | )% | 2.90 | % | 9.07 | % |

Class C (Inception 3/3/08)* | | (11.21 | )% | 3.34 | % | 9.04 | % |

S&P 500 Index | | 8.09 | % | 0.25 | % | 4.21 | % |

MSCI Zhong Hua Index | | (13.51 | )% | 7.45 | % | 12.31 | % |

The performance data quoted represents past performance, which is not an indication or a guarantee of future results. The Fund’s average annual total returns include changes in share price and reinvestment of dividends and capital gains. The chart and table above do not reflect the deduction of taxes that a shareholder would have paid on Fund distributions or on the redemption of Fund shares. Investment return and principal will fluctuate and the Fund’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance current to the most recent month end, visit us at www.alger.com or call us at (800) 992-3863.

† | Returns reflect maximum sales charges on Class A shares and applicable contingent deferred sales charges on Class C shares. |

8

* | Performance figures prior to 3/3/08, inception of Class C shares, are those of the Fund’s Class A shares. Performance has been adjusted to remove the front-end sales charge imposed by Class A shares. Class C shares do not impose a front-end sales charge but do impose a contingent deferred sales charge of 1% on shares redeemed. If Class A sales charges were reflected, annual returns for the Class C shares would be lower. The performance figures prior to 3/3/08 have also been adjusted to reflect the higher operating expenses and applicable contingent deferred sales charge of Class C shares. |

9

PORTFOLIO SUMMARY†

October 31, 2011 (Unaudited)

COUNTRY | | Alger China-

U.S. Growth

Fund | |

Australia | | 0.4 | % |

Bermuda | | 0.6 | |

Brazil | | 1.7 | |

Canada | | 3.3 | |

Cayman Islands | | 4.2 | |

China | | 20.7 | |

Hong Kong | | 18.3 | |

Italy | | 1.5 | |

Japan | | 0.8 | |

Mongolia | | 0.5 | |

Netherlands | | 0.9 | |

Taiwan | | 7.8 | |

United States | | 36.7 | |

Cash and Net Other Assets | | 2.6 | |

| | 100.0 | % |

† Based on net assets.

10

ALGER CHINA-U.S. GROWTH FUND

Schedule of Investments‡ October 31, 2011

| | SHARES | | VALUE | |

COMMON STOCKS—96.4% | | | | | |

AUSTRALIA—0.4% | | | | | |

COAL & CONSUMABLE FUELS—0.4% | | | | | |

Linc Energy Ltd.*,(L2)

(Cost $104,156) | | 116,000 | | $ | 248,996 | |

| | | | | |

BERMUDA—0.6% | | | | | |

OIL & GAS DRILLING—0.6% | | | | | |

Nabors Industries Ltd.*

(Cost $434,619) | | 19,700 | | 361,101 | |

| | | | | |

BRAZIL—0.7% | | | | | |

DIVERSIFIED METALS & MINING—0.7% | | | | | |

Vale SA#

(Cost $157,366) | | 15,650 | | 397,667 | |

| | | | | |

CANADA—3.3% | | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—1.1% | | | | | |

Westport Innovations, Inc.* | | 19,750 | | 597,438 | |

| | | | | |

DIVERSIFIED METALS & MINING—0.7% | | | | | |

Ivanhoe Mines Ltd.* | | 19,550 | | 400,971 | |

| | | | | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.6% | | | | | |

Potash Corporation of Saskatchewan, Inc. | | 7,150 | | 338,410 | |

| | | | | |

GOLD—0.9% | | | | | |

Yamana Gold, Inc. | | 35,500 | | 531,435 | |

| | | | | |

TOTAL CANADA

(Cost $1,360,332) | | | | 1,868,254 | |

| | | | | |

CAYMAN ISLANDS—4.2% | | | | | |

APPLICATION SOFTWARE—0.6% | | | | | |

Kingdee International Software Group Co., Ltd.(L2) | | 914,000 | | 366,780 | |

| | | | | |

COMPUTER STORAGE & PERIPHERALS—0.3% | | | | | |

Seagate Technology PLC | | 12,150 | | 196,223 | |

| | | | | |

INTERNET SOFTWARE & SERVICES—1.7% | | | | | |

Sina Corp. * | | 3,400 | | 276,386 | |

Tencent Holdings Ltd. (L2) | | 29,650 | | 682,362 | |

| | | | 958,748 | |

SEMICONDUCTORS—1.6% | | | | | |

Spreadtrum Communications, Inc.# | | 34,200 | | 908,694 | |

| | | | | |

TOTAL CAYMAN ISLANDS

(Cost $1,764,768) | | | | 2,430,445 | |

| | | | | |

CHINA—20.7% | | | | | |

ADVERTISING—0.5% | | | | | |

Focus Media Holding Ltd.#* | | 11,400 | | 309,852 | |

| | | | | |

APPAREL RETAIL—0.6% | | | | | |

Belle International Holdings Ltd.(L2) | | 189,000 | | 367,791 | |

| | | | | | |

11

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

CHINA—(CONT.) | | | | | |

ASSET MANAGEMENT & CUSTODY BANKS—0.4% | | | | | |

Noah Holdings Ltd.#* | | 25,921 | | $ | 226,031 | |

| | | | | |

COAL & CONSUMABLE FUELS—0.7% | | | | | |

Yanzhou Coal Mining Co., Ltd.(L2) | | 164,000 | | 405,948 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—0.6% | | | | | |

ZTE Corp.(L2) | | 113,400 | | 321,897 | |

| | | | | |

COMPUTER & ELECTRONICS RETAIL—0.5% | | | | | |

GOME Electrical Appliances Holdings Ltd.(L2) | | 890,000 | | 273,998 | |

| | | | | |

CONSTRUCTION & ENGINEERING—0.7% | | | | | |

China Singyes Solar Technologies Holdings Ltd.(L2) | | 728,000 | | 396,210 | |

| | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—0.6% | | | | | |

Sany Heavy Equipment International Holdings Co., Ltd.(L2) | | 387,500 | | 341,387 | |

| | | | | |

CONSTRUCTION MATERIALS—1.4% | | | | | |

Anhui Conch Cement Co., Ltd. (L2) | | 90,050 | | 324,046 | |

China National Building Material Co., Ltd. (L2) | | 386,000 | | 494,430 | |

| | | | 818,476 | |

DIVERSIFIED BANKS—3.6% | | | | | |

Bank of China Ltd. (L2) | | 1,362,900 | | 485,068 | |

China Construction Bank Corp. (L2) | | 1,313,700 | | 965,222 | |

Industrial & Commercial Bank of China (L2) | | 939,455 | | 585,467 | |

| | | | 2,035,757 | |

DIVERSIFIED METALS & MINING—1.5% | | | | | |

Jiangxi Copper Co. (L2) | | 149,000 | | 358,664 | |

Tiangong International Co., Ltd. (L2) | | 2,753,000 | | 487,666 | |

| | | | 846,330 | |

INDEPENDENT POWER PRODUCERS & ENERGY TRADERS—0.7% | | | | | |

GCL Poly Energy Holdings Ltd.(L2) | | 1,212,000 | | 391,229 | |

| | | | | |

INDUSTRIAL MACHINERY—0.7% | | | | | |

Airtac International Group(L2) | | 73,000 | | 408,586 | |

| | | | | |

INTEGRATED OIL & GAS—2.9% | | | | | |

China Petroleum & Chemical Corp. (L2) | | 766,000 | | 723,456 | |

PetroChina Co., Ltd. (L2) | | 686,000 | | 890,560 | |

| | | | 1,614,016 | |

INTEGRATED TELECOMMUNICATION SERVICES—1.2% | | | | | |

China Telecom Corp., Ltd.(L2) | | 1,030,000 | | 634,627 | |

| | | | | |

INTERNET SOFTWARE & SERVICES—1.8% | | | | | |

Baidu, Inc. #* | | 3,350 | | 469,603 | |

Netease.com #* | | 12,450 | | 589,757 | |

| | | | 1,059,360 | |

OIL & GAS EXPLORATION & PRODUCTION—0.9% | | | | | |

CNOOC Ltd.(L2) | | 301,000 | | 568,998 | |

| | | | | | |

12

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

CHINA—(CONT.) | | | | | |

SPECIALTY CHEMICALS—1.4% | | | | | |

Dongyue Group(L2) | | 1,084,000 | | $ | 829,860 | |

| | | | | |

TOTAL CHINA

(Cost $10,670,444) | | | | 11,850,353 | |

| | | | | |

HONG KONG—18.3% | | | | | |

AGRICULTURAL PRODUCTS—0.5% | | | | | |

Global Bio-Chem Technology Group Co., Ltd.(L2) | | 1,356,000 | | 310,328 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—0.5% | | | | | |

Comba Telecom Systems Holdings Ltd.(L2) | | 332,000 | | 279,907 | |

| | | | | |

CONSTRUCTION & ENGINEERING—0.7% | | | | | |

China State Construction International Holdings Ltd.(L2) | | 496,800 | | 382,629 | |

| | | | | |

DISTRIBUTORS—0.3% | | | | | |

Li & Fung Ltd.(L2) | | 84,000 | | 161,884 | |

| | | | | |

DIVERSIFIED BANKS—0.6% | | | | | |

BOC Hong Kong Holdings Ltd.(L2) | | 144,000 | | 340,239 | |

| | | | | |

DIVERSIFIED CAPITAL MARKETS—0.9% | | | | | |

Digital China Holdings Ltd.(L2) | | 327,000 | | 518,465 | |

| | | | | |

DIVERSIFIED CONSUMER SERVICES—0.8% | | | | | |

China Resources Enterprise Ltd.(L2) | | 129,200 | | 471,845 | |

| | | | | |

ELECTRIC UTILITIES—2.0% | | | | | |

Power Assets Holdings Ltd.(L2) | | 150,500 | | 1,139,767 | |

| | | | | |

INDUSTRIAL CONGLOMERATES—1.2% | | | | | |

Hutchison Whampoa Ltd.(L2) | | 72,000 | | 658,088 | |

| | | | | |

INTEGRATED TELECOMMUNICATION SERVICES—0.4% | | | | | |

China Unicom Hong Kong Ltd.(L2) | | 122,000 | | 245,295 | |

| | | | | |

LIFE & HEALTH INSURANCE—1.9% | | | | | |

AIA Group Ltd.(L2) | | 350,800 | | 1,072,655 | |

| | | | | |

PACKAGED FOODS & MEATS—0.7% | | | | | |

China Mengniu Dairy Co., Ltd.(L2) | | 127,000 | | 403,066 | |

| | | | | |

RAILROADS—0.9% | | | | | |

MTR Corp.(L2) | | 163,921 | | 530,179 | |

| | | | | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—3.2% | | | | | |

Cheung Kong Holdings Ltd. (L2) | | 57,000 | | 704,401 | |

Sun Hung Kai Properties Ltd. (L2) | | 58,000 | | 796,379 | |

Wharf Holdings Ltd. (L2) | | 61,000 | | 324,474 | |

| | | | 1,825,254 | |

RETAIL REITS—1.2% | | | | | |

Link REIT, /The(L2) | | 192,000 | | 659,374 | |

| | | | | |

SPECIALIZED FINANCE—1.3% | | | | | |

Hong Kong Exchanges and Clearing Ltd.(L2) | | 44,500 | | 752,672 | |

| | | | | | |

13

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

HONG KONG—(CONT.) | | | | | |

WIRELESS TELECOMMUNICATION SERVICES—1.2% | | | | | |

China Mobile Ltd.(L2) | | 73,000 | | $ | 693,817 | |

| | | | | |

TOTAL HONG KONG

(Cost $10,140,749) | | | | 10,445,464 | |

| | | | | |

ITALY—1.5% | | | | | |

APPAREL RETAIL—0.8% | | | | | |

Prada SpA* | | 91,600 | | 459,250 | |

| | | | | |

FOOTWEAR—0.7% | | | | | |

Salvatore Ferragamo Italia SpA* | | 26,100 | | 422,886 | |

| | | | | |

TOTAL ITALY

(Cost $915,860) | | | | 882,136 | |

| | | | | |

JAPAN—0.8% | | | | | |

APPAREL RETAIL—0.8% | | | | | |

Fast Retailing Co., Ltd.(L2)

(Cost $346,255) | | 2,650 | | 476,033 | |

| | | | | |

MONGOLIA—0.5% | | | | | |

DIVERSIFIED METALS & MINING—0.5% | | | | | |

Mongolian Mining Corp.*,(L2)

(Cost $359,095) | | 290,450 | | 258,791 | |

| | | | | |

NETHERLANDS—0.9% | | | | | |

INTEGRATED OIL & GAS—0.9% | | | | | |

Royal Dutch Shell PLC#

(Cost $498,991) | | 7,000 | | 496,370 | |

| | | | | |

TAIWAN—7.8% | | | | | |

COMMUNICATIONS EQUIPMENT—1.2% | | | | | |

Wistron NeWeb Corp.(L2) | | 279,549 | | 659,843 | |

| | | | | |

COMPUTER HARDWARE—0.3% | | | | | |

Foxconn Technology Co., Ltd.(L2) | | 52,000 | | 181,239 | |

| | | | | |

COMPUTER STORAGE & PERIPHERALS—1.2% | | | | | |

Catcher Technology Co., Ltd.(L2) | | 115,700 | | 644,622 | |

| | | | | |

ELECTRICAL COMPONENTS & EQUIPMENT—1.3% | | | | | |

Cheng Uei Precision Industry Co., Ltd. (L2) | | 112,128 | | 251,942 | |

Simplo Technology Co., Ltd. (L2) | | 87,794 | | 516,594 | |

| | | | 768,536 | |

ELECTRONIC EQUIPMENT MANUFACTURERS—0.5% | | | | | |

TXC Corp.(L2) | | 234,599 | | 276,154 | |

| | | | | |

FOOD RETAIL—1.5% | | | | | |

President Chain Store Corp.(L2) | | 159,000 | | 884,156 | |

| | | | | |

PACKAGED FOODS & MEATS—0.8% | | | | | |

Uni-President Enterprises Corp.(L2) | | 320,150 | | 440,258 | |

| | | | | | |

14

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

TAIWAN—(CONT.) | | | | | |

SEMICONDUCTORS—1.0% | | | | | |

MediaTek, Inc.(L2) | | 54,000 | | $ | 566,690 | |

| | | | | |

TOTAL TAIWAN

(Cost $3,485,668) | | | | 4,421,498 | |

| | | | | |

UNITED STATES—36.7% | | | | | |

AEROSPACE & DEFENSE—1.8% | | | | | |

Goodrich Corp. | | 5,250 | | 643,808 | |

Spirit Aerosystems Holdings, Inc., Cl. A * | | 23,300 | | 397,731 | |

| | | | 1,041,539 | |

AIR FREIGHT & LOGISTICS—1.4% | | | | | |

United Parcel Service, Inc., Cl. B | | 11,550 | | 811,272 | |

| | | | | |

APPAREL ACCESSORIES & LUXURY GOODS—0.8% | | | | | |

Coach, Inc. | | 3,950 | | 257,027 | |

PVH Corp. | | 2,400 | | 178,584 | |

| | | | 435,611 | |

ASSET MANAGEMENT & CUSTODY BANKS—1.9% | | | | | |

Blackstone Group LP | | 40,600 | | 597,226 | |

KKR & Co., LP | | 34,700 | | 467,756 | |

| | | | 1,064,982 | |

CASINOS & GAMING—0.9% | | | | | |

Las Vegas Sands Corp.* | | 11,400 | | 535,230 | |

| | | | | |

COAL & CONSUMABLE FUELS—0.7% | | | | | |

Peabody Energy Corp. | | 9,000 | | 390,330 | |

| | | | | |

COMMUNICATIONS EQUIPMENT—2.9% | | | | | |

Acme Packet, Inc. * | | 3,200 | | 115,872 | |

Cisco Systems, Inc. | | 42,900 | | 794,937 | |

QUALCOMM, Inc. | | 14,500 | | 748,200 | |

| | | | 1,659,009 | |

COMPUTER HARDWARE—3.0% | | | | | |

Apple, Inc.* | | 4,150 | | 1,679,837 | |

| | | | | |

COMPUTER STORAGE & PERIPHERALS—1.3% | | | | | |

NetApp, Inc. * | | 4,300 | | 176,128 | |

SanDisk Corp. * | | 11,450 | | 580,172 | |

| | | | 756,300 | |

CONSTRUCTION & ENGINEERING—0.8% | | | | | |

Aecom Technology Corp.* | | 21,550 | | 450,825 | |

| | | | | |

CONSTRUCTION & FARM MACHINERY & HEAVY TRUCKS—0.9% | | | | | |

Cummins, Inc. | | 1,800 | | 178,974 | |

Joy Global, Inc. | | 3,750 | | 327,000 | |

| | | | 505,974 | |

DATA PROCESSING & OUTSOURCED SERVICES—1.2% | | | | | |

Mastercard, Inc. | | 1,900 | | 659,756 | |

| | | | | | |

15

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

UNITED STATES—(CONT.) | | | | | |

DIVERSIFIED METALS & MINING—2.8% | | | | | |

Cliffs Natural Resources, Inc. | | 7,750 | | $ | 528,704 | |

Freeport-McMoRan Copper & Gold, Inc. | | 7,050 | | 283,833 | |

Molycorp, Inc. * | | 9,500 | | 363,565 | |

Walter Energy, Inc. | | 5,350 | | 404,728 | |

| | | | 1,580,830 | |

FERTILIZERS & AGRICULTURAL CHEMICALS—0.7% | | | | | |

Mosaic Co., /The | | 6,600 | | 386,496 | |

| | | | | |

FOOTWEAR—1.0% | | | | | |

NIKE, Inc., Cl. B | | 5,750 | | 554,013 | |

| | | | | |

HOUSEHOLD PRODUCTS—0.6% | | | | | |

Procter & Gamble Co., /The | | 5,250 | | 335,948 | |

| | | | | |

INDUSTRIAL MACHINERY—1.5% | | | | | |

Flowserve Corp. | | 1,350 | | 125,132 | |

SPX Corp. | | 13,150 | | 718,121 | |

| | | | 843,253 | |

INTEGRATED OIL & GAS—1.1% | | | | | |

Exxon Mobil Corp. | | 8,300 | | 648,147 | |

| | | | | |

INTERNET RETAIL—1.0% | | | | | |

Amazon.com, Inc.* | | 2,550 | | 544,451 | |

| | | | | |

OIL & GAS EQUIPMENT & SERVICES—0.6% | | | | | |

National Oilwell Varco, Inc. | | 4,600 | | 328,118 | |

| | | | | |

OIL & GAS EXPLORATION & PRODUCTION—1.2% | | | | | |

Brigham Exploration Co. * | | 10,550 | | 384,178 | |

Devon Energy Corp. | | 4,050 | | 263,048 | |

| | | | 647,226 | |

PHARMACEUTICALS—1.2% | | | | | |

Johnson & Johnson | | 9,850 | | 634,241 | |

Mylan, Inc. * | | 3,650 | | 71,431 | |

| | | | 705,672 | |

REAL ESTATE SERVICES—0.6% | | | | | |

CBRE Group, Inc.* | | 19,950 | | 354,711 | |

| | | | | |

RESEARCH & CONSULTING SERVICES—0.3% | | | | | |

IHS, Inc., Cl. A* | | 2,250 | | 188,978 | |

| | | | | |

RESTAURANTS—2.2% | | | | | |

McDonald’s Corp. | | 3,400 | | 315,690 | |

Starbucks Corp. | | 9,650 | | 408,581 | |

Yum! Brands, Inc. | | 9,650 | | 516,950 | |

| | | | 1,241,221 | |

SEMICONDUCTORS—1.8% | | | | | |

Altera Corp. | | 10,450 | | 396,264 | |

Inphi Corp. * | | 18,000 | | 198,720 | |

Skyworks Solutions, Inc. * | | 22,850 | | 452,659 | |

| | | | 1,047,643 | |

| | | | | | |

16

| | SHARES | | VALUE | |

COMMON STOCKS—(CONT.) | | | | | |

UNITED STATES—(CONT.) | | | | | |

SOFT DRINKS—1.4% | | | | | |

Coca-Cola Co., /The | | 3,800 | | $ | 259,616 | |

PepsiCo, Inc. | | 8,200 | | 516,190 | |

| | | | 775,806 | |

SPECIALIZED FINANCE—0.6% | | | | | |

CME Group, Inc. | | 600 | | 165,336 | |

IntercontinentalExchange, Inc. * | | 1,300 | | 168,844 | |

| | | | 334,180 | |

SPECIALTY CHEMICALS—0.5% | | | | | |

Rockwood Holdings, Inc.* | | 5,800 | | 267,032 | |

| | | | | |

TOTAL UNITED STATES

(Cost $18,221,871) | | | | 20,774,390 | |

| | | | | |

TOTAL COMMON STOCKS

(Cost $48,460,174) | | | | 54,911,498 | |

| | | | | |

CONVERTIBLE PREFERRED STOCK—1.0% | | | | | |

BRAZIL—1.0% | | | | | |

DIVERSIFIED METALS & MINING—1.0% | | | | | |

Vale Capital II, 6.75%, 6/15/2012

(Cost $448,597) | | 7,630 | | 582,932 | |

| | | | | |

Total Investments

(Cost $48,908,771)(a) | | 97.4 | % | 55,494,430 | |

Other Assets in Excess of Liabilities | | 2.6 | | 1,494,596 | |

NET ASSETS | | 100.0 | % | $ | 56,989,026 | |

‡ | Securities classified as Level 1 for ASC 820 disclosure purposes based on valuation inputs unless otherwise noted. |

* | Non-income producing security. |

# | American Depository Receipts. |

(a) | At October 31, 2011, the net unrealized appreciation on investments, based on cost for federal income tax purposes of $50,099,194, amounted to $5,395,236 which consisted of aggregate gross unrealized appreciation of $10,700,269 and aggregate gross unrealized depreciation of $5,305,033. |

L2 | Security classified as Level 2 for ASC 820 disclosure purposes based on valuation inputs. |

Industry classifications are unaudited.

See Notes to Financial Statements.

17

ALGER CHINA-U.S. GROWTH FUND

Statement of Assets and Liabilities October 31, 2011

ASSETS: | | | |

Investments in securities, at value (identified cost)*

see accompanying schedules of investments | | $ | 55,494,430 | |

Cash and cash equivalents | | 782,625 | |

Foreign cash** | | 265,502 | |

Receivable for investment securities sold | | 633,885 | |

Receivable for shares of beneficial interest sold | | 47,793 | |

Dividends and interest receivable | | 40,134 | |

Prepaid expenses | | 33,987 | |

Total Assets | | 57,298,356 | |

LIABILITIES: | | | |

Payable for investment securities purchased | | 51,040 | |

Payable for shares of beneficial interest redeemed | | 63,224 | |

Accrued investment advisory fees | | 55,454 | |

Accrued transfer agent fees | | 28,980 | |

Accrued distribution fees | | 13,795 | |

Accrued administrative fees | | 1,271 | |

Accrued shareholder servicing fees | | 762 | |

Accrued other expenses | | 94,804 | |

Total Liabilities | | 309,330 | |

NET ASSETS | | $ | 56,989,026 | |

Net Assets Consist of: | | | |

Paid in capital (par value of $.001 per share) | | 71,398,771 | |

Undistributed net investment income (accumulated loss) | | (467,084 | ) |

Undistributed net realized gain (accumulated realized loss) | | (20,530,497 | ) |

Net unrealized appreciation on investments | | 6,587,836 | |

NET ASSETS | | $ | 56,989,026 | |

Net Assets By Class | | | |

Class A | | $ | 53,310,911 | |

Class C | | $ | 3,678,115 | |

Shares Of Beneficial Interest Outstanding—Note 6 | | | |

Class A | | 3,527,371 | |

Class C | | 248,654 | |

Net Asset Value Per Share | | | |

Class A | | $ | 15.11 | |

Class C | | $ | 14.79 | |

Offering Price Per Share(a) | | | |

Class A | | $ | 15.95 | |

Class C | | $ | 14.79 | |

*Identified cost | | $ | 48,908,771 | |

**Cost of foreign cash | | $ | 263,282 | |

(a) Class A Offering Price includes a 5.25% sales charge.

See Notes to Financial Statements.

18

ALGER CHINA-U.S. GROWTH FUND

Statement of Operations

For the year ended October 31, 2011

INCOME | | | |

Dividends (net of foreign withholding taxes*) | | $ | 1,206,571 | |

Interest | | 1,951 | |

Total Income | | 1,208,522 | |

EXPENSES | | | |

Advisory fees—Note 3(a) | | 871,653 | |

Distribution fees—Note 3(f): | | | |

Class A | | 171,101 | |

Class C | | 41,976 | |

Administrative fees—Note 3(a) | | 19,975 | |

Custodian fees | | 117,902 | |

Interest expenses | | 1,129 | |

Transfer agent fees and expenses—Note 3(b) | | 133,550 | |

Printing fees | | 44,125 | |

Professional fees | | 85,969 | |

Registration fees | | 52,383 | |

Trustee fees—Note 3(e) | | 19,898 | |

Miscellaneous | | 36,763 | |

Total Expenses | | 1,596,424 | |

NET INVESTMENT LOSS | | (387,902 | ) |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY | | | |

Net realized gain on investments | | 6,983,067 | |

Net realized gain on foreign currency transactions | | 19,909 | |

Net change in unrealized appreciation (depreciation) on investments and foreign currency | | (13,015,405 | ) |

Net realized and unrealized loss on investments and foreign currency | | (6,012,429 | ) |

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (6,400,331 | ) |

*Foreign withholding taxes | | $ | 74,978 | |

See Notes to Financial Statements.

19

ALGER CHINA-U.S. GROWTH FUND

Statements of Changes in Net Assets

| | For the

Year Ended

October 31, 2011 | | For the

Year Ended

October 31, 2010 | |

Net investment loss | | $ | (387,902 | ) | $ | (424,338 | ) |

Net realized gain on investments and foreign currency | | 7,002,976 | | 9,724,972 | |

Net change in unrealized appreciation (depreciation) on investments and foreign currency | | (13,015,405 | ) | 5,835,765 | |

Net increase (decrease) in net assets resulting from operations | | (6,400,331 | ) | 15,136,399 | |

Dividends and distributions to shareholders from: | | | | | |

Net investment income | | | | | |

Class A | | — | | (109,702 | ) |

Total dividends and distributions to shareholders | | — | | (109,702 | ) |

Increase (decrease) from shares of beneficial interest transactions: | | | | | |

Class A | | (12,562,021 | ) | (10,601,919 | ) |

Class C | | (92,087 | ) | 2,034,569 | |

Net decrease from shares of beneficial interest transactions—Note 6 | | (12,654,108 | ) | (8,567,350 | ) |

Total increase (decrease) | | (19,054,439 | ) | 6,459,347 | |

Net Assets: | | | | | |

Beginning of period | | 76,043,465 | | 69,584,118 | |

END OF PERIOD | | $ | 56,989,026 | | $ | 76,043,465 | |

Undistributed net investment income (accumulated loss) | | $ | (467,084 | ) | $ | (342,431 | ) |

See Notes to Financial Statements.

20

ALGER CHINA-U.S. GROWTH FUND

Financial Highlights for a share outstanding throughout the period

| | Class A | |

| | Year ended

10/31/2011 | | Year ended

10/31/2010 | | Year ended

10/31/2009 | | Year ended

10/31/2008 | | Year ended

10/31/2007 | |

Net asset value, beginning of period | | $ | 16.74 | | $ | 13.55 | | $ | 10.18 | | $ | 25.09 | | $ | 15.57 | |

INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | | | |

Net investment loss (i) | | (0.08 | ) | (0.08 | ) | (0.05 | ) | (0.08 | ) | (0.13 | ) |

Net realized and unrealized gain (loss) on investments | | (1.55 | ) | 3.29 | | 3.42 | | (12.79 | ) | 11.67 | |

Total from investment operations | | (1.63 | ) | 3.21 | | 3.37 | | (12.87 | ) | 11.54 | |

Dividends from net investment income | | — | | (0.02 | ) | — | | — | | — | |

Distributions from net realized gains | | — | | — | | — | | (2.04 | ) | (2.02 | ) |

Net asset value, end of period | | $ | 15.11 | | $ | 16.74 | | $ | 13.55 | | $ | 10.18 | | $ | 25.09 | |

Total return (ii) | | (9.6 | )% | 23.5 | % | 33.1 | % | (55.2 | )% | 83.0 | % |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 53,311 | | $ | 71,835 | | $ | 67,989 | | $ | 64,865 | | $ | 201,623 | |

Ratio of gross expenses to average net assets | | 2.15 | % | 2.12 | % | 2.31 | % | 2.15 | % | 2.17 | % |

Ratio of expense reimbursements to average net assets | | 0.00 | % | 0.00 | % | 0.00 | % | (0.25 | )% | (0.25 | )% |

Ratio of net expenses to average net assets | | 2.15 | % | 2.12 | % | 2.31 | % | 1.90 | % | 1.92 | % |

Ratio of net investment income (loss) to average net assets | | (0.49 | )% | (0.56 | )% | (0.48 | )% | (0.43 | )% | (0.71 | )% |

Portfolio turnover rate | | 82.13 | % | 89.15 | % | 149.17 | % | 190.60 | % | 107.57 | % |

See Notes to Financial Statements.

(i) Amount was computed based on average shares outstanding during the period.

(ii) Does not reflect the effect of sales charges, if applicable.

21

ALGER CHINA-U.S. GROWTH FUND

Financial Highlights for a share outstanding throughout the period

| | Class C | |

| | Year ended

10/31/2011 | | Year ended

10/31/2010 | | Year ended

10/31/2009 | | From

3/3/2008

(commencement

of

operations) to

10/31/2008(i) | |

Net asset value, beginning of period | | $ | 16.50 | | $ | 13.43 | | $ | 10.16 | | $ | 18.20 | |

INCOME FROM INVESTMENT OPERATIONS: | | | | | | | | | |

Net investment loss (ii) | | (0.21 | ) | (0.18 | ) | (0.14 | ) | (0.05 | ) |

Net realized and unrealized gain (loss) on investments | | (1.50 | ) | 3.25 | | 3.41 | | (7.99 | ) |

Total from investment operations | | (1.71 | ) | 3.07 | | 3.27 | | (8.04 | ) |

Net asset value, end of period | | $ | 14.79 | | $ | 16.50 | | $ | 13.43 | | $ | 10.16 | |

Total return (iii) | | (10.3 | )% | 22.7 | % | 32.2 | % | (44.2 | )% |

RATIOS/SUPPLEMENTAL DATA: | | | | | | | | | |

Net assets, end of period (000’s omitted) | | $ | 3,678 | | $ | 4,208 | | $ | 1,595 | | $ | 339 | |

Ratio of gross expenses to average net assets | | 2.95 | % | 2.91 | % | 3.03 | % | 3.02 | % |

Ratio of expense reimbursements to average net assets | | 0.00 | % | 0.00 | % | 0.00 | % | (0.21 | )% |

Ratio of net expenses to average net assets | | 2.95 | % | 2.91 | % | 3.03 | % | 2.81 | % |

Ratio of net investment income (loss) to average net assets | | (1.26 | )% | (1.25 | )% | 1.19 | % | (0.52 | )% |

Portfolio turnover rate | | 82.13 | % | 89.15 | % | 149.17 | % | 190.60 | % |

See Notes to Financial Statements.

(i) Ratios have been annualized; total return and portfolio turnover rate have not been annualized.

(ii) Amount was computed based on average shares outstanding during the period.

(iii) Does not reflect the effect of sales charges, if applicable.

See Notes to Financial Statements.

22

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS

NOTE 1 — General:

The Alger China-U.S. Growth Fund (the “Fund”) is a diversified, open-end registered investment company organized as a business trust under the laws of the Commonwealth of Massachusetts. The Fund’s investment objective is long-term capital appreciation. It seeks to achieve its objective by investing in equity securities that are economically tied to China (including Hong Kong and Taiwan) or the United States. The Fund offers Class A shares and Class C shares. Class A shares are generally subject to an initial sales charge while Class C shares are generally subject to a deferred sales charge. Each class has identical rights to assets and earnings except that each share class bears the cost of its plan of distribution and transfer agency and sub-transfer agency services.

NOTE 2 — Significant Accounting Policies:

(a) Investment Valuation: The Fund values its financial instruments at fair value using independent dealers or pricing services under policies approved by the Board. Investments are valued on each day the New York Stock Exchange (the “NYSE”) is open, as of the close of the NYSE (normally 4:00 p.m. Eastern time).

Equity securities for which valuation information is readily available are valued at the last reported sales price or official closing price as reported by an independent pricing service on the primary market or exchange on which they are traded. In the absence of reported sales, such securities are valued at a price within the bid and ask price or, in the absence of a recent bid or ask price, the equivalent as obtained from one or more of the major market makers for the securities to be valued.

Securities for which market quotations are not readily available are valued at fair value, as determined in good faith pursuant to procedures established by the Board of Trustees.

Securities in which the Fund invests may be traded in foreign markets that close before the close of the NYSE. Developments that occur between the close of the foreign markets and the close of the NYSE may result in adjustments to the closing prices to reflect what the investment adviser, pursuant to policies established by the Board of Trustees, believes to be the fair value of these securities as of the close of the NYSE. The Fund may also fair value securities in other situations, for example, when a particular foreign market is closed but the Fund is open.

Financial Accounting Standards Board Accounting Standards Codification 820 — Fair Value Measurements and Disclosures (“ASC 820”) defines fair value as the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. ASC 820 established a three-tier hierarchy to maximize the use of observable market

23

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability and may be observable or unobservable. Observable inputs are based on market data obtained from sources independent of the Fund. Unobservable inputs are inputs that reflect the Fund’s own assumptions based on the best information available in the circumstances. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below.

· Level 1 — quoted prices in active markets for identical investments

· Level 2 — significant other observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

· Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

The Fund’s valuation techniques are consistent with the market approach whereby prices and other relevant information generated by market transactions involving identical or comparable assets are used to measure fair value. Inputs for Level 1 include exchange listed prices and broker quotes in an active market. Inputs for Level 2 include the last trade price in the case of a halted security, a broker quote in an inactive market, an exchange listed price which has been adjusted for fair value factors, and prices of closely related securities. Additional Level 2 inputs include an evaluated price which is based upon a compilation of observable market information such as spreads for fixed income and preferred securities. Inputs for Level 3 include derived prices from unobservable market information which can include cash flows and other information obtained from a company’s financial statements, or from market indicators such as benchmarks and indices.

(b) Cash and Cash Equivalents: Cash and cash equivalents include U.S. dollars and overnight time deposits.

(c) Securities Transactions and Investment Income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income is recognized on the accrual basis.

(d) Foreign Currency Translations: The books and records of the Fund are maintained in U.S. dollars. Foreign currencies, investments and other assets and liabilities are translated into U.S. dollars at the prevailing rates of exchange on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the prevailing exchange rates on the respective dates of such transactions.

24

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Net realized gains and losses on foreign currency transactions represent net gains and losses from the disposition of foreign currencies, currency gains and losses realized between the trade dates and settlement dates of security transactions, and the difference between the amount of net investment income accrued and the U.S. dollar amount actually received. The effects of changes in foreign currency exchange rates on investments in securities are included in realized and unrealized gain or loss on investments in the Statement of Operations.

(e) Dividends to Shareholders: Dividends and distributions payable to shareholders are recorded by the Fund on the ex-dividend date. Dividends from net investment income and distributions from net realized gains are declared and paid annually after the end of the fiscal year in which earned.

Each class is treated separately in determining the amounts of dividends from net investment income payable to holders of its shares.

The characterization of distributions to shareholders for financial reporting purposes is determined in accordance with federal income tax rules. Therefore, the source of the Fund’s distributions may be shown in the accompanying financial statements as either from, or in excess of net investment income, net realized gain on investment transactions or return of capital, depending on the type of book/tax differences that may exist. Capital accounts within the financial statements are adjusted for permanent book/tax differences. Reclassifications result primarily from the difference in tax treatment of net operating losses, passive foreign investment companies, and foreign currency transactions. The reclassifications are done annually at fiscal year end and have no impact on the net asset value of the Fund and are designed to present the Fund’s capital accounts on a tax basis.

(f) Federal Income Taxes: It is the Fund’s policy to comply with the requirements of the Internal Revenue Code Subchapter M applicable to regulated investment companies and to distribute all of its taxable income to its shareholders. Provided that the Fund maintains such compliance, no federal income tax provision is required.

Financial Accounting Standards Board Accounting Standards Codification 740 — Income Taxes (“ASC 740”) requires the Fund to measure and recognize in its financial statements the benefit of a tax position taken (or expected to be taken) on an income tax return if such position will more likely than not be sustained upon examination based on the technical merits of the position. No tax years are currently under investigation. The Fund files income tax returns in the U.S. Federal jurisdiction, as well as the New York State and New York City jurisdictions. The statute of limitations on the Fund’s tax returns remains open for the tax years 2008-2011. Management does not believe there are any uncertain tax positions that require recognition of a tax liability.

25

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

(g) Estimates: These financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America, which require using estimates and assumptions that affect the reported amounts therein. Actual results may differ from those estimates.

NOTE 3 — Investment Advisory Fees and Other Transactions with Affiliates:

(a) Investment Advisory and Administration Fees: Fees incurred by the Fund, pursuant to the provisions of its Investment Advisory Agreement and its Administration Agreement with Fred Alger Management, Inc. (Alger Management or the Manager), are payable monthly and computed based on the value of the average daily net assets of the Fund, at the following rates:

Advisory

Fee | | Administration

Fee | |

1.20 | % | 0.0275 | % |

Martin Currie Inc., a registered investment adviser, acted as sub-advisor to the Fund under a written sub-advisory agreement with Alger Management from September 20, 2006 to September 30, 2011.

(b) Shareholder Administrative Fees: The Fund has entered into a shareholder administrative services agreement with Alger Management to compensate Alger Management for its liaison and administrative oversight of Boston Financial Data Services, Inc. the transfer agent, and other related services. The Fund compensates Alger Management at the annual rate of 0.0165% of the average daily net assets for these services. For the year ended October 31, 2011, the Fund incurred fees of $11,985 for these services provided by Alger Management, which are included in the transfer agent fees and expenses in the Statement of Operations.

Alger Management makes payments to intermediaries that provide sub-accounting services to omnibus accounts, held by the Fund. Fees paid by Alger Management to intermediaries that provide sub-accounting services are charged back to the Fund, subject to certain limitations, as approved by the Fund’s Board of Trustees. For the year ended October 31, 2011, Alger Management charged back $16,729 to the Fund for these services, which are included in the transfer agent fees and expenses in the Statement of Operations.

(c) Sales Charges: Purchases of shares of the Fund may be subject to initial sales charges or contingent deferred sales charges. For the year ended October 31, 2011, the initial sales charges and contingent deferred sales charges imposed, all of which were retained by Fred Alger & Company, Incorporated, the Fund’s distributor (the “Distributor” or “Alger Inc.”), were approximately $2,475 and $2,201 respectively. The contingent deferred sales charges are used by Alger Inc. to offset distribution expenses previously incurred. Sales charges do not represent expenses of the Fund.

26

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

(d) Brokerage Commissions: During the year ended October 31, 2011, the Fund paid Alger Inc. $17,398 in connection with securities transactions.

(e) Trustees’ Fees: The Fund pays each trustee who is not affiliated with Alger Management or its affiliates $750 for each meeting attended, to a maximum of $3,000 per annum, plus travel expenses incurred for attending the meeting. The chairman of the Board of Trustees receives an additional annual fee of $15,000 which is paid, pro rata, by all funds managed by Alger Management. Additionally, each member of the audit committee receives an additional $75 for each audit committee meeting attended, to a maximum of $300 per annum.

(f) Distribution/Shareholder Servicing Fees: The Fund has adopted a distribution plan pursuant to which the Fund pays Alger Inc. a fee at the annual rate of 0.25% of the average daily net assets of the Class A shares and 1.00% of the average daily net assets of the Class C shares to compensate Alger Inc. for its activities and expenses incurred in distributing the Fund’s shares and shareholder servicing. Fees charged may be more or less than the expenses incurred by Alger Inc.

(g) Interfund Loans: The Fund, along with other funds advised by Alger Management, may borrow money from and lend money to each other for temporary or emergency purposes. To the extent permitted under its investment restrictions, each fund may lend uninvested cash in an amount up to 15% of its net assets to other funds. If a fund has borrowed from other funds and has aggregate borrowings from all sources that exceed 10% of the fund’s total assets, such fund will secure all of its loans from other funds. The interest rate charged on interfund loans is equal to the average of the overnight time deposit rate and bank loan rate available to the funds. There were no interfund loans outstanding for the year ended October 31, 2011.

(h) Other Transactions with Affiliates: Certain officers of the Fund are directors and officers of Alger Management and the Alger Inc.

NOTE 4 — Securities Transactions:

The following summarizes the securities transactions by the Fund, other than U.S. Government and short-term securities, for the year ended October 31, 2011:

| | PURCHASES | | SALES | |

Alger China-U.S. Growth Fund | | $ | 57,722,918 | | $ | 94,678,431 | |

| | | | | | | |

Transactions in foreign securities may involve certain considerations and risks not typically associated with those of U.S. companies because of, among other factors, the level of governmental supervision and regulation of foreign security markets, and the possibility of political or economic instability.

27

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

NOTE 5 — Borrowings:

The Fund may borrow from its custodian on an uncommitted basis. The Fund pays the custodian a market rate of interest, generally based upon the London Inter-Bank Offer Rate. The Fund may also borrow from other funds advised by Alger Management, as discussed in Note 3(g). For the year ended October 31, 2011, the Fund had the following borrowings:

| | AVERAGE DAILY

BORROWING | | WEIGHTED AVERAGE

INTEREST RATE | |

Alger China-U.S. Growth Fund | | $ | 56,612 | | 2.23 | % |

| | | | | | |

The highest amount borrowed during the year ended October 31, 2011 was $1,036,656.

NOTE 6 — Share Capital:

(a) The Fund has an unlimited number of authorized shares of beneficial interest of $.001 par value. Transactions of shares of beneficial interest were as follows:

| | FOR THE YEAR ENDED

OCTOBER 31, 2011 | | FOR THE YEAR ENDED

OCTOBER 31, 2010 | |

| | SHARES | | AMOUNT | | SHARES | | AMOUNT | |

Alger China-U.S. Growth Fund | | | | | | | | | |

Class A: | | | | | | | | | |

Shares sold | | 455,227 | | $ | 7,814,836 | | 846,924 | | $ | 12,476,955 | |

Dividends reinvested | | — | | — | | 6,130 | | 88,830 | |

Shares redeemed | | (1,219,701 | ) | (20,376,857 | ) | (1,578,296 | ) | (23,167,704 | ) |

Net decrease | | (764,474 | ) | $ | (12,562,021 | ) | (725,242 | ) | $ | (10,601,919 | ) |

Class C: | | | | | | | | | |

Shares sold | | 87,116 | | $ | 1,471,616 | | 178,520 | | $ | 2,656,503 | |

Shares redeemed | | (93,440 | ) | (1,563,703 | ) | (42,293 | ) | (621,934 | ) |

Net increase (decrease) | | (6,324 | ) | $ | (92,087 | ) | 136,227 | | $ | 2,034,569 | |

(b) Redemption Fee: The Fund may impose a 2.00% redemption fee on Fund shares redeemed (including shares redeemed by exchange) less than 30 days after such shares were acquired. The fees retained by the Fund are included as paid-in capital on the Statement of Assets and Liabilities and were as follows:

28

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

FOR THE YEAR ENDED

OCTOBER 31, 2011 | | FOR THE YEAR ENDED

OCTOBER 31, 2010 | |

$ | 13,737 | | $ | 3,572 | |

| | | | | |

NOTE 7 — Income Tax Information:

The tax character of distributions paid during the year ended October 31, 2011 and the year ended October 31, 2010 was as follows:

| | FOR THE YEAR ENDED

OCTOBER 31, 2011 | | FOR THE YEAR ENDED

OCTOBER 31, 2010 | |

| | | | | |

Distributions paid from: | | | | | |

Ordinary Income | | — | | $ | 109,702 | |

Long-term capital gain | | — | | — | |

Total distributions paid | | — | | $ | 109,702 | |

As of October 31, 2011, the components of accumulated gains (losses) on a tax basis were as follows:

Alger China-U.S. Growth Fund | | | |

Undistributed ordinary income | | — | |

Undistributed long-term gains | | — | |

Net accumulated earnings | | — | |

Capital loss carryforwards | | $ | (19,807,158 | ) |

Net unrealized appreciation | | 5,397,413 | |

Total accumulated losses | | $ | (14,409,745 | ) |

At October 31, 2011, the Fund, for federal income tax purposes, had a capital loss carryforward of $19,807,158 which expires in 2017. The amounts may be applied against future net realized gains until the earlier of their utilization or expiration.

Under the recently enacted Regulated Investment Company Modernization Act of 2010, capital losses incurred by the Fund after October 31, 2011 will not be subject to expiration. In addition, losses incurred after October 31, 2011 must be utilized prior to the utilization of capital loss carryforwards above.

The difference between book-basis and tax-basis unrealized appreciation (depreciation) is determined annually and is attributable primarily to the tax deferral of losses on wash sales, the realization of unrealized appreciation of Passive Foreign Investment Companies, and partnership basis adjustments.

Permanent differences, primarily from net operating losses and real estate investment trusts and partnership investments sold by the Fund, resulted in the

29

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

following reclassifications among the Funds’s components of net assets at October 31, 2011:

Alger China-U.S. Growth Fund | | | |

Accumulated Undistributed Net Investment Income | | $ | 263,249 | |

Accumulated Net Realized Loss | | $ | (159,699 | ) |

Paid-in Capital | | $ | (103,550 | ) |

NOTE 8 — Fair Value Measurements:

The major categories of securities and their respective fair value inputs are detailed in the Fund’s Schedule of Investments. The following is a summary of the inputs used as of October 31, 2011 in valuing the Fund’s investments carried at fair value:

Alger China-U.S. Growth Fund | | TOTAL FUND | | LEVEL 1 | | LEVEL 2 | | LEVEL 3 | |

COMMON STOCKS | | | | | | | | | |

Consumer Discretionary | | $ | 5,782,220 | | $ | 4,502,514 | | $ | 1,279,706 | | — | |

Consumer Staples | | 3,149,562 | | 1,111,754 | | 2,037,808 | | — | |

Energy | | 5,709,250 | | 2,871,292 | | 2,837,958 | | — | |

Financials | | 9,656,165 | | 1,979,904 | | 7,676,261 | | — | |

Health Care | | 705,672 | | 705,672 | | — | | — | |

Industrials | | 7,924,894 | | 4,439,279 | | 3,485,615 | | — | |

Information Technology | | 12,222,702 | | 8,243,208 | | 3,979,494 | | — | |

Materials | | 6,656,298 | | 3,902,841 | | 2,753,457 | | — | |

Telecommunication Services | | 1,573,739 | | — | | 1,573,739 | | — | |

Utilities | | 1,530,996 | | — | | 1,530,996 | | — | |

TOTAL COMMON STOCKS | | $ | 54,911,498 | | $ | 27,756,464 | | $ | 27,155,034 | | — | |

CONVERTIBLE PREFERRED STOCK | | | | | | | | | |

Materials | | $ | 582,932 | | $ | 582,932 | | — | | — | |

TOTAL INVESTMENTS IN SECURITIES | | $ | 55,494,430 | | $ | 28,339,396 | | $ | 27,155,034 | | — | |

For the year ended October 31, 2011, the Fund transferred securities totaling $13,499,828 from Level 1 to Level 2, utilizing fair value adjusted prices rather than exchange listed prices.

NOTE 9 — Derivatives:

Financial Accounting Standards Board Accounting Standards Codification 815 — Derivatives and Hedging (“ASC 815”) requires qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts of and gains and losses on derivative instruments, and disclosures about credit-risk-related contingent features in derivative agreements.

Forward currency contracts—In connection with portfolio purchases and sales of securities denominated in foreign currencies, the Fund may enter into forward currency contracts. Additionally, the Fund may enter into such contracts to economically hedge certain other foreign currency denominated investments. These contracts are valued at the current cost of covering or offsetting such contracts, and

30

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

the related realized and unrealized foreign exchange gains and losses are included in the statement of operations. In the event that counterparties fail to settle these currency contracts or the related foreign security trades, the Fund could be exposed to foreign currency fluctuations.

Options—The Fund seeks to capture the majority of the returns associated with equity market investments. To meet this investment goal, the Fund invests in a broadly diversified portfolio of common stocks, while also buying and selling call and put options on equities and equity indices. The Fund purchases call options to increase its exposure to stock market risk and also provide diversification of risk. The Fund purchases put options in order to protect from significant market declines that may occur over a short period of time. The Fund can write covered call and cash secured put options to generate cash flows while reducing the volatility of the Fund’s portfolio. The cash flows may be an important source of the Fund’s return, although written call options may reduce the Fund’s ability to profit from increases in the value of the underlying security or equity portfolio. The value of a call option generally increases as the price of the underlying stock increases and decreases as the stock decreases in price. Conversely, the value of a put option generally increases as the price of the underlying stock decreases and decreases as the stock increases in price. The combination of the diversified stock portfolio and the purchase and sale of options is intended to provide the Fund with the majority of the returns associated with equity market investments but with reduced volatility and returns that are augmented with the cash flows from the sale of options.

There were no derivative transactions for the year ended October 31, 2011.

NOTE 10 — Litigation:

On August 31, 2005, the West Virginia Securities Commissioner (the “WVSC”), in an ex parte Summary Order to Cease and Desist and Notice of Right to Hearing, concluded that the Manager and the Distributor had violated the West Virginia Uniform Securities Act (the “WVUSA”), and ordered the Manager and the Distributor to cease and desist from further violations of the WVUSA by engaging in the market-timing-related conduct described in the order. The ex parte order provided notice of their right to a hearing with respect to the violations of law asserted by the WVSC. Other firms unaffiliated with the Manager were served with similar orders. The Manager and the Distributor intend to request a hearing for the purpose of seeking to vacate or modify the order.

NOTE 11 — Recent Accounting Pronouncements:

The Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2011-04, Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs (International Financial Reporting Standards). The ASU converges fair value measurement and disclosure

31

ALGER CHINA-U.S. GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

guidance in U.S. GAAP with the guidance in the International Accounting Standards Board’s concurrently issued IFRS 13, Fair Value Measurement. These amendments do not modify the requirements for when fair value measurements apply; rather, they generally represent clarifications on how to measure and disclose fair value under ASC 820, Fair Value Measurement. The application of ASU 2011-04 is required for fiscal years and interim periods beginning after December 15, 2011. At this time, management is evaluating the implications of ASU 2011-04.

NOTE 12 — Subsequent Events:

Management of the Fund has evaluated events that have occurred subsequent to October 31, 2011. No such events have been identified which require recognition and disclosure.

32

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Trustees of

The Alger China-U.S. Growth Fund:

We have audited the accompanying statement of assets and liabilities of Alger China — U.S. Growth Fund (the “Fund”), including the schedule of investments as of October 31, 2011, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the three years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits. The Funds’ financial highlights for the respective periods ended October 31, 2008 were audited by other auditors, whose report dated December 16, 2008, expressed an unqualified opinion on such financial highlights.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of their internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2011, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above, present fairly, in all material respects, the financial position of Alger China — U.S. Growth Fund as of October 31, 2011, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the three years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Deloitte & Touche LLP | |

New York, New York | |

December 23, 2011 | |

33

ALGER CHINA-U.S. GROWTH FUND

ADDITIONAL INFORMATION (Unaudited) (Continued)

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: transaction costs, if applicable, including sales charges (loads) and redemption fees; and ongoing costs, including management fees, distribution (12b-1) fees, if applicable, and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example below is based on an investment of $1,000 invested at the beginning of the six-month period starting May 1, 2011 and ending October 31, 2011.

Actual Expenses

The first line for each class of shares in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you would have paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes