UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21457

Name of Fund: BlackRock Allocation Target Shares

Series C Portfolio

Series M Portfolio

Series P Portfolio

Series S Portfolio

Fund Address: 100 Bellevue Parkway, Wilmington, DE 19809

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Allocation Target Shares, 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 441-7762

Date of fiscal year end: 03/31/2014

Date of reporting period: 03/31/2014

Item 1 – Report to Stockholders

MARCH 31, 2014

BlackRock Allocation Target Shares

„ Series C Portfolio

„ Series M Portfolio

„ Series P Portfolio

„ Series S Portfolio

| | |

| Not FDIC Insured ¡ May Lose Value ¡ No Bank Guarantee | | |

| | | | | | |

| 2 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

Shareholder Letter

Dear Shareholder,

One year ago, U.S. financial markets were improving despite a sluggish global economy, as easy monetary policy provided investors with enough conviction to take on more risk in their portfolios. Slow but positive growth in the U.S. was sufficient to support corporate earnings, while uncomfortably high unemployment reinforced expectations that the Federal Reserve would continue to maintain its aggressive monetary stimulus programs.

Sentiment swiftly reversed in May when then-Fed Chairman Bernanke first mentioned the possibility of reducing (or “tapering”) the central bank’s asset purchase programs — comments that were widely misinterpreted as signaling an end to the Fed’s zero-interest-rate policy. U.S. Treasury yields rose sharply, triggering a steep sell-off across fixed income markets. (Bond prices move in the opposite direction of yields.) Global equities also suffered as investors feared the implications of a potential end to a program that had greatly supported the markets. Emerging markets, which are more sensitive to changes in global liquidity, were particularly hurt by the prospect of ebbing cash flows from the U.S. Markets rebounded in late June, however, when the Fed’s tone turned more dovish, and improving economic indicators and better corporate earnings helped extend gains through most of the summer.

Although the tone of economic and financial news was mixed during the autumn, it was a surprisingly positive period for most asset classes. Early on, the Fed defied market expectations with its decision to delay tapering, but higher volatility returned in late September when the U.S. Treasury Department warned that the national debt would soon breach its statutory maximum. The ensuing political brinksmanship led to a partial government shutdown, roiling global financial markets through the first half of October. Equities and other so-called “risk assets” managed to resume their rally when politicians engineered a compromise to reopen the government and extend the debt ceiling.

The remainder of 2013 was generally positive for stock markets in the developed world, although investors continued to grapple with uncertainty about when and how much the Fed would scale back on stimulus. When the Fed ultimately announced its tapering plans in mid-December, markets reacted positively, as this action signaled the Fed’s perception of real improvement in the economy, and investors were finally relieved from the anxiety that had gripped them for quite some time.

The start of the new year brought another turn in sentiment, as heightened risks in emerging markets and mixed U.S. economic data caused global equities to weaken in January while bond markets found renewed strength. Although these headwinds persisted, equities were back on the rise in Feb-ruary as investors were encouraged by a one-year extension of the U.S. debt ceiling and market-friendly comments from the Fed’s new Chairwoman, Janet Yellen. While U.S. economic data pointed to softer growth, investors viewed this trend as temporarily driven by poor winter weather and continued adding risk to their portfolios on the belief that growth would pick up in the coming months. In March, markets focused on decelerating growth in China and tensions between Russia and Ukraine over the disputed region of Crimea. Additionally, investors were caught off guard by a statement from Chairwoman Yellen indicating that the Fed may raise short-term interest rates earlier than the markets had previously forecasted. Bond markets came under pressure as the middle of the yield curve vaulted higher in response to the unexpected shift in forward guidance.

Against a backdrop of modest economic growth, investors over the past year remained highly attuned to potential changes in monetary policy. Despite the fact that markets were gearing up for a modest shift toward tighter conditions from the Fed, equity markets in the developed world generated strong returns for the six- and 12-month periods ended March 31, with stocks in the United States performing particularly well. In contrast, emerging markets were weighed down by concerns about reduced global liquidity, severe currency weakness, high levels of debt and uneven growth.

Interest rate uncertainty posed a headwind for fixed income assets, and higher-quality sectors of the market experienced heightened volatility and poor performance over the reporting period. High yield bonds, however, benefited from income-oriented investors’ search for yield in the overall low-rate environment. Short-term interest rates remained near zero, keeping yields on money market securities close to historic lows.

At BlackRock, we believe investors need to think globally, extend their scope across a broad array of asset classes and be prepared to move freely as market conditions change over time. We encourage you to talk with your financial advisor and visit www.blackrock.com for further insight about investing in today’s world.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

In a modest global growth environment, expectations around monetary policy changes continued to be a key theme in financial market performance.

Rob Kapito

President, BlackRock Advisors, LLC

| | | | | | | | |

| Total Returns as of March 31, 2014 | |

| | | 6-month | | | 12-month | |

U.S. large cap equities

(S&P 500® Index) | | | 12.51 | % | | | 21.86 | % |

U.S. small cap equities

(Russell 2000® Index) | | | 9.94 | | | | 24.90 | |

International equities

(MSCI Europe, Australasia, Far East Index) | | | 6.41 | | | | 17.56 | |

Emerging market equities

(MSCI Emerging Markets Index) | | | 1.39 | | | | (1.43 | ) |

3-month Treasury bill

(BofA Merrill Lynch

3-Month U.S. Treasury

Bill Index) | | | 0.03 | | | | 0.07 | |

U.S. Treasury securities

(BofA Merrill Lynch

10-Year U.S. Treasury

Index) | | | 0.85 | | | | (4.38 | ) |

U.S. investment grade

bonds (Barclays U.S.

Aggregate Bond Index) | | | 1.70 | | | | (0.10 | ) |

Tax-exempt municipal

bonds (S&P Municipal Bond Index) | | | 3.91 | | | | 0.31 | |

U.S. high yield bonds

(Barclays U.S. Corporate

High Yield 2% Issuer

Capped Index) | | | 6.66 | | | | 7.53 | |

|

| Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. | |

| | | | | | |

| | | THIS PAGE NOT PART OF YOUR FUND REPORT | | | | 3 |

| | | | |

| Fund Summary as of March 31, 2014 | | | Series C Portfolio | |

Series C Portfolio’s (the “Fund”) investment objective is to seek to maximize total return, consistent with income generation and prudent investment management.

|

| Portfolio Management Commentary |

How did the Fund perform?

| Ÿ | | For the 12-month period ended March 31, 2014, the Fund outperformed its benchmark, the Barclays U.S. Credit Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| Ÿ | | The Fund’s outperformance relative to the benchmark index was driven by security selection within industrials and financials. Maintaining an underweight to emerging market securities proved advantageous as well. An allocation to high yield contributed positively to results, as did the Fund’s duration (management of interest rate sensitivity) and yield curve positioning. As the investment advisor tactically changed duration positioning over the period, the Fund benefited from a short duration bias relative to the benchmark in the second quarter of 2013 and in December of 2013. |

| Ÿ | | The Fund held derivatives during the period as part of its investment strategy. Interest rate derivatives are used primarily as a means of managing the portfolio’s duration risk. The Fund may also use credit default swaps against individual securities or broad indices to manage credit risk in the portfolio. Credit default swaps against indices help to manage market risk as well. During the period, the use of derivatives had a positive impact on Fund returns. |

| Ÿ | | Conversely, an overweight to the utility sector was a modest detractor from performance as this group lagged over the period. |

Describe recent portfolio activity.

| Ÿ | | The Fund maintained an overweight exposure to financials throughout most of the 12-month period given attractive valuations and renewed capital requirements that the investment advisor viewed as beneficial for debt-holders. In industrials, the Fund continued to favor the communications sub-sector, while remaining cautious of industries where re-leveraging risk has been increasing. Within utilities, the Fund maintained a preference for the natural gas pipeline and electric industries given the dependable nature of their cash flows. In the non-corporate space, the Fund remained underweight emerging markets, given the challenges to global growth and China in particular. Throughout the period, the Fund continued to favor bonds on the short end of the yield curve as well as on the very long end of the curve; however, the Fund began to add exposure to the intermediate part of the curve toward the end of the period. From a quality standpoint, the Fund held tactical allocations to lower-rated investment grade bonds and crossover names (bonds that have the potential to be upgraded to investment grade), while also holding high-quality U.S. Treasury securities. |

Describe portfolio positioning at period end.

| Ÿ | | As of period end, the Fund was overweight relative to the Barclays U.S. Credit Index in the financials and utilities sectors, and underweight in industrials. The Fund’s weightings in emerging market debt and municipal bonds were essentially in line with that of the index. The Fund also held non-benchmark allocations to high yield credit and U.S. Treasury securities. The Fund ended the period with duration that was neutral relative to the benchmark index. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Long-Term

Investments |

| | | | |

Corporate Bonds | | | 85 | % |

Capital Trusts | | | 4 | |

Taxable Municipal Bonds | | | 3 | |

Foreign Agency Obligations | | | 3 | |

Foreign Government Obligations | | | 3 | |

U.S. Treasury Obligations | | | 2 | |

| | |

| Credit Quality Allocation1 | | Percent of

Long-Term

Investments |

| | | | |

AAA/Aaa2 | | | 3 | % |

AA/Aa | | | 11 | |

A | | | 38 | |

BBB/Baa | | | 47 | |

BB/Ba | | | 1 | |

| 1 | Using the higher of Standard & Poor’s (“S&P’s”) or Moody’s Investors Service (“Moody’s”) ratings. |

| 2 | Includes U.S. Government Sponsored Agency Securities and U.S. Treasury Obli- gations, which are deemed AAA/Aaa by the investment advisor. |

| | | | | | |

| 4 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

|

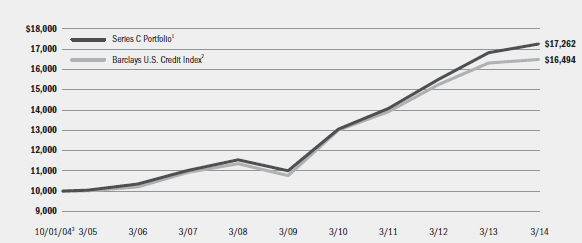

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund is non-diversified and will primarily invest its assets in investment grade fixed income securities, such as corporate bonds, notes and debentures, asset-backed securities, commercial and residential mortgage-backed securities, obligations of non-U.S. governments and supra- national organizations, which are chartered to promote economic development, collateralized mortgage obligations, U.S. Treasury and agency securities, cash equivalent investments, when-issued and delayed delivery securities, derivatives, repurchase agreements and reverse repurchase agreements. |

| | 2 | An unmanaged index that includes publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. |

| | 3 | Commencement of operations. |

| | | | | | | | | | | | | | | | |

| Performance Summary for the Period Ended March 31, 2014 | |

| | | | | | Average Annual Total Returns4 | |

| | | 6-Month

Total Returns | | | 1 Year | | | 5 Years | | | Since Inception5 | |

Series C Portfolio | | | 4.75 | % | | | 2.55 | % | | | 9.42 | % | | | 5.92 | % |

Barclays U.S. Credit Index | | | 3.86 | | | | 1.02 | | | | 8.90 | | | | 5.41 | |

| | 4 | See “About Fund Performance” on page 12 for a detailed description of performance related information. |

| | 5 | The Fund commenced operations on October 1, 2004. |

| | | Past performance is not indicative of future results. |

| | | | | | | | | | | | | | | | | | |

| Expense Example |

| | | Actual | | Hypothetical8 |

| | | | | | | Including

Interest Expense | | Excluding

Interest Expense | | | | Including Interest Expense | | Excluding Interest Expense |

| | | Beginning

Account Value

October 1, 2013 | | Ending Account Value

March 31, 2014 | | Expenses Paid

During the Period6 | | Expenses Paid

During the Period7 | | Beginning

Account Value

October 1, 2013 | | Ending Account Value

March 31, 2014 | | Expenses Paid

During the Period6 | | Ending Account Value

March 31, 2014 | | Expenses Paid

During the Period7 |

Series C Portfolio | | $1,000.00 | | $1,047.50 | | $0.10 | | $0.00 | | $1,000.00 | | $1,024.83 | | $0.10 | | $1,024.93 | | $0.00 |

| | 6 | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.02%, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 7 | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.00%, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 8 | Hypothetical 5% annual return before expenses is calculated by pro rating the number of days in the most recent fiscal half year divided by 365. |

| | | See “Disclosure of Expenses” on page 12 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | 5 |

| | | | |

| Fund Summary as of March 31, 2014 | | | Series M Portfolio | |

Series M Portfolio’s (the “Fund”) investment objective is to seek to maximize total return, consistent with income generation and prudent investment management.

|

| Portfolio Management Commentary |

How did the Fund perform?

| Ÿ | | For the 12-month period ended March 31, 2014, the Fund outperformed its benchmark, the Barclays MBS Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| Ÿ | | The largest contributor to performance was the Fund’s non-benchmark exposure to commercial mortgage-backed securities (“CMBS”), which were buoyed by continued investor demand for yield. Duration management (sensitivity to interest rate movements) and yield curve positioning also had a positive impact on returns. Within asset-backed securities (“ABS”), the Fund’s exposure to private student loans added to performance. |

| Ÿ | | The Fund held derivatives during the period as part of its investment strategy. Derivatives are used by the Fund primarily as a means to manage interest rate risk and yield curve positioning. During the period, the use of derivatives had a positive impact on performance. |

| Ÿ | | Detracting from relative returns was security selection within 30-year agency mortgage-backed securities (“MBS”). |

Describe recent portfolio activity.

| Ÿ | | During the 12-month period, the Fund traded exposure across agency MBS coupons in consideration of prepayment risk. In the beginning of |

| | | the period, this generally meant tactical trading within middle coupons while avoiding higher coupons given the anticipated impact of the Home Affordable Refinance Program 2.0. However, in the middle of the period, the Fund moved to an overweight in high coupon issues as prepayment risk was reduced due to rising long-term interest rates in the second quarter of 2013. In the final months of the period, as the U.S. Federal Reserve continued to gradually reduce its purchasing activity in the mortgage market and expectations for economic data continued to be positive, the Fund actively managed duration and scaled back on exposure to agency MBS, ending the period underweight duration. |

| Ÿ | | Throughout the period, the Fund increased exposure to CMBS as the sector exhibited a strong income profile and fair valuations. |

| Ÿ | | The Fund held cash that was committed for pending transactions. The cash balance did not have a material impact on performance. |

Describe portfolio positioning at period end.

| Ÿ | | Relative to the Barclays MBS Index, the Fund was overweight in middle-coupon agency MBS and underweight in select low and high coupons. The Fund was positioned for higher interest rates generally, predicated on expectations that U.S. economic data will continue to improve from the lackluster start to 2014. The Fund also continued to maintain non-benchmark exposure to higher-quality CMBS issues that exhibit attractive liquidity and high carry (income) characteristics. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Long-Term

Investments |

| | | | |

U.S. Government Sponsored Agency Securities | | | 89 | % |

Non-Agency Mortgage-Backed Securities | | | 8 | |

Asset-Backed Securities | | | 2 | |

U.S. Treasury Obligations | | | 1 | |

| | |

| Credit Quality Allocation1 | | Percent of

Long-Term

Investments |

| | 1 | Using the higher of S&P’s or Moody’s ratings. |

| | 2 | Includes U.S. Government Sponsored Agency Securities and U.S. Treasury Obligations, which are deemed AAA/Aaa by the investment advisor. |

| | | | | | |

| 6 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

|

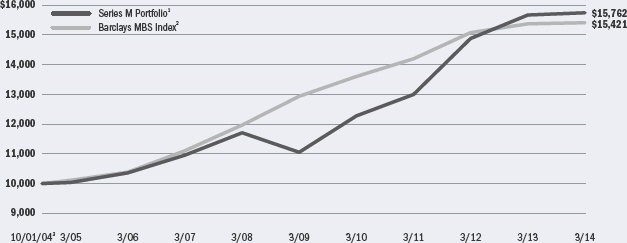

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund is non-diversified and will primarily invest its assets in investment grade commercial and residential mortgage-backed securities, asset- backed securities, collateralized mortgage obligations, U.S. Treasury and agency securities, cash equivalent instruments, when-issued and delayed delivery securities, derivatives and dollar rolls. |

| | 2 | An unmanaged index that includes the mortgage-backed pass-through securities of Ginnie Mae, Fannie Mae and Freddie Mac that meet the maturity and liquidity criteria. |

| | 3 | Commencement of operations. |

|

| Performance Summary for the Period Ended March 31, 2014 |

| | | | | | | | | | | | | | | | |

| | | | | | Average Annual Total Returns4 | |

| | | 6-Month

Total Returns | | | 1 Year | | | 5 Years | | | Since Inception5 | |

Series M Portfolio | | | 1.63 | % | | | 0.52 | % | | | 7.36 | % | | | 4.91 | % |

Barclays MBS Index | | | 1.16 | | | | 0.20 | | | | 3.57 | | | | 4.67 | |

| | 4 | See “About Fund Performance” on page 12 for a detailed description of performance related information. |

| | 5 | The Fund commenced operations on October 1, 2004. |

| | | Past performance is not indicative of future results. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Actual | | | Hypothetical7 | | | | |

| | | Beginning

Account Value

October 1, 2013 | | | Ending

Account Value

March 31, 2014 | | | Expenses Paid

During the Period6 | | | Beginning

Account Value

October 1, 2013 | | | Ending

Account Value

March 31, 2014 | | | Expenses Paid

During the Period6 | | | Annualized

Expense Ratio | |

Series M Portfolio | | $ | 1,000.00 | | | $ | 1,016.30 | | | $ | 0.05 | | | $ | 1,000.00 | | | $ | 1,024.88 | | | $ | 0.05 | | | | 0.01 | % |

| | 6 | For shares of the Fund, expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 7 | Hypothetical 5% annual return before expenses is calculated by pro rating the number of days in the most recent fiscal half year divided by 365. |

| | | See “Disclosure of Expenses” on page 12 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | 7 |

| | | | |

| Fund Summary as of March 31, 2014 | | | Series P Portfolio | |

Series P Portfolio’s (the “Fund”) investment objective is to seek to provide a duration that is the inverse of its benchmark.

|

| Portfolio Management Commentary |

How did the Fund perform?

| Ÿ | | For the 12-month period ended March 31, 2014, the Fund outperformed its benchmark, the Barclays U.S. Treasury 7-10 Year Bond Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| Ÿ | | The Fund’s allocation to BlackRock Allocation Target Shares: Series S Portfolio (“Series S Portfolio”) contributed positively to performance for the period. Series S Portfolio generated positive returns driven by non-benchmark exposures to asset-backed securities (“ABS”) and commercial mortgage-backed securities (“CMBS”). Series S Portfolio’s corporate credit allocation, where results were driven by positioning within industrials and financials, also had a positive impact. Detracting from performance in Series S Portfolio was a non-benchmark exposure to agency mortgage-backed securities (“MBS”). |

| Ÿ | | As part of its strategy, the Fund engages in the selling of U.S. Treasury futures and uses interest rate swaps to achieve negative duration (i.e., the inverse effect of the benchmark index duration). Cash is received and held by the Fund as collateral for these transactions. During the period, the use of derivatives had a negative impact on Fund returns. The use and costs of derivatives will result in a negative contribution to returns when interest rates fall; however, the Fund’s strategy is designed to offset |

| | | these costs by holding shares of Series S Portfolio, a short-term proprietary fund. The use of derivatives is necessary to achieve the Fund’s objective and should therefore be evaluated in a portfolio context and not as a stand-alone strategy. |

Describe recent portfolio activity.

| Ÿ | | During the 12-month period, the Fund actively managed interest rate risk on the 7- to 10-year part of the yield curve by using derivatives as described above. The Fund maintained its allocation to Series S Portfolio in order to offset the cost of the derivatives. |

| Ÿ | | Series S Portfolio decreased exposure to CMBS while increasing exposure to ABS, specifically adding to sub-prime auto loans and credit cards. Series S Portfolio also increased the allocation to agency MBS, particularly in 30-year pass-through securities. In corporate credit, Series S Portfolio slightly increased exposure to high yield, while reducing exposure to investment grade credit in the context of relatively unattractive valuations, embedded duration risk and potential leveraged buyout event risks. |

Describe portfolio positioning at period end.

| Ÿ | | At period end, the Fund held positions in U.S. Treasury futures and interest rate swaps, Series S Portfolio and the Bank of New York Cash Reserve Money Market Fund. Through its investment in Series S Portfolio, the Fund held exposures to investment grade credit, high yield credit, agency MBS, CMBS, ABS and government sectors, including U.S. Treasuries and U.S. agency debentures. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | |

Percent of

Net Assets |

| | | | |

Fixed Income Funds | | | 24 | % |

Other Assets Less Liabilities1 | | | 76 | |

| | 1 | Includes derivative instruments and cash held for such derivative instruments. |

| | |

| Portfolio Holdings | | Percent of

Affiliated

Investment

Companies |

| | | | |

BlackRock Allocation Target Shares: Series S Portfolio | | | 100 | % |

| | | | | | |

| 8 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

|

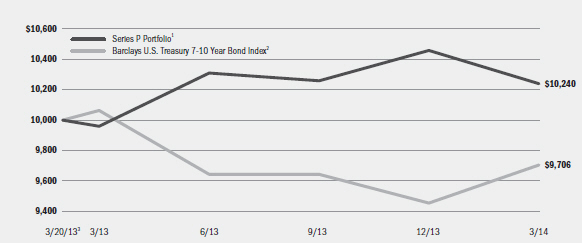

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund is non-diversified and may invest in a portfolio of securities and other financial instruments, including derivative instruments, in an attempt to provide returns that are the inverse of its benchmark index. |

| | 2 | An unmanaged index that includes all publicly issued, U.S. Treasury securities that have a remaining maturity of between 7 and 10 years, are non- convertible, are denominated in U.S. dollars, are rated Baa3 (or better) by Moody’s or BBB- (or better) by S&P, are fixed rate, and have more than $250 million par outstanding. |

| | 3 | Commencement of operations. |

|

| Performance Summary for the Period Ended March 31, 2014 |

| | | | | | | | | | | | |

| | | | | | Average Annual Total Returns4 | |

| | | 6-Month Total Returns | | | 1 Year | | | Since Inception5 | |

Series P Portfolio | | | (0.20 | )% | | | 2.81 | % | | | 2.33 | % |

Barclays U.S. Treasury 7-10 Year Bond Index | | | 0.65 | | | | (3.56 | ) | | | (2.86 | ) |

| | 4 | See “About Fund Performance” on page 12 for a detailed description of performance related information. |

| | 5 | The Fund commenced operations on March 20, 2013. |

| | | Past performance is not indicative of future results. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Actual | | | Hypothetical7 | | | | |

| | | Beginning

Account Value

October 1, 2013 | | | Ending

Account Value

March 31, 2014 | | | Expenses Paid

During the Period6 | | | Beginning

Account Value

October 1, 2013 | | | Ending

Account Value

March 31, 2014 | | | Expenses Paid

During the Period6 | | | Annualized

Expense Ratio | |

Series P Portfolio | | $ | 1,000.00 | | | $ | 998.00 | | | $ | 0.00 | | | $ | 1,000.00 | | | $ | 1,024.93 | | | $ | 0.00 | | | | 0.00 | % |

| | 6 | For shares of the Fund, expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period shown). The fees and expenses of the underlying funds in which the Fund invests are not included in the Fund’s annualized expense ratio. BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 7 | Hypothetical 5% annual return before expenses is calculated by pro rating the number of days in the most recent fiscal half year divided by 365. |

| | | See “Disclosure of Expenses” on page 12 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | 9 |

| | | | |

| Fund Summary as of March 31, 2014 | | | Series S Portfolio | |

Series S Portfolio’s (the “Fund”) investment objective is to seek to maximize total return, consistent with income generation and prudent investment management.

|

| Portfolio Management Commentary |

How did the Fund perform?

| Ÿ | | For the 12-month period ended March 31, 2014, the Fund outperformed its benchmark, the BofA Merrill Lynch 1-3 Year Treasury Index. Shares of the Fund can be purchased or held only by or on behalf of certain separately managed account clients. Comparisons of the Fund’s performance versus its benchmark index will differ from comparisons of the benchmark against the performance of the separately managed accounts. |

What factors influenced performance?

| Ÿ | | Contributing positively to performance were the Fund’s non-benchmark exposures to asset-backed securities (“ABS”) and commercial mortgage-backed securities (“CMBS”). The Fund’s corporate credit allocation, where results were driven by positioning within industrials and financials, also had a positive impact. |

| Ÿ | | The Fund held derivatives during the period as part of its investment strategy. Interest rate derivatives are used primarily as a means of managing the portfolio’s duration risk (sensitivity to interest rate movements). The Fund may also use credit default swaps against individual securities or broad indices to manage credit risk in the portfolio. Credit default swaps against indices help to manage market risk as well. In addition, the Fund may trade foreign currency exchange contracts or use foreign currency derivatives to manage currency risk in the portfolio. During the period, the use of derivatives had a positive impact on Fund returns. |

| Ÿ | | Conversely, the Fund’s non-benchmark exposure to agency mortgage-backed securities (“MBS”) detracted from relative performance for the period. |

Describe recent portfolio activity.

| Ÿ | | During the 12-month period, in the securitized asset sectors, the Fund decreased exposure to CMBS while increasing exposure to ABS. Within ABS, the Fund added to sub-prime auto loans and credit cards. The Fund also increased the allocation to agency MBS, particularly in 30-year pass-through securities. In corporate credit, the Fund slightly increased exposure to high yield, while reducing exposure to investment grade credit in the context of relatively unattractive valuations, embedded duration risk and potential leveraged buyout event risks. |

Describe portfolio positioning at period end.

| Ÿ | | At period end, the Fund held non-benchmark allocations in investment grade credit, high yield credit, agency MBS, CMBS, ABS and U.S. agency debentures. Relative to the BofA Merrill Lynch 1-3 Year Treasury Index, the Fund was underweight in U.S. Treasuries and maintained a longer duration profile. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | |

| Portfolio Composition | | Percent of

Long-Term

Investments |

| | | | |

Corporate Bonds | | | 36 | % |

Non-Agency Mortgage-Backed Securities | | | 21 | |

U.S. Treasury Obligations | | | 17 | |

Asset-Backed Securities | | | 13 | |

U.S. Government Sponsored Agency Securities | | | 11 | |

Foreign Agency Obligations | | | 1 | |

Foreign Government Obligations | | | 1 | |

| | |

| Credit Quality Allocation1 | | Percent of

Long-Term

Investments |

| | | | |

AAA/Aaa2 | | | 52 | % |

AA/Aa | | | 5 | |

A | | | 17 | |

BBB/Baa | | | 25 | |

BB/Ba | | | 1 | |

| | 1 | Using the higher of S&P’s or Moody’s ratings. |

| | 2 | Includes U.S. Government Sponsored Agency Securities and U.S. Treasury Obligations, which are deemed AAA/Aaa by the investment advisor. |

| | | | | | |

| 10 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

|

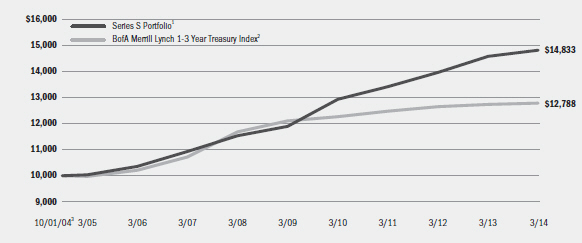

| Total Return Based on a $10,000 Investment |

| | 1 | The Fund is non-diversified and will primarily invest its assets in investment grade fixed income securities, such as commercial and residential mortgage-backed securities, obligations of non-U.S. governments and supra-national organizations, which are chartered to promote economic development, obligations of domestic and non-U.S. corporations, asset-backed securities, collateralized mortgage obligations, U.S. Treasury and agency securities, cash equivalent investments, when-issued and delayed delivery securities, repurchase agreements, reverse repurchase agreements and dollar rolls. |

| | 2 | An unmanaged index comprised of Treasury securities with maturities from 1 to 2.99 years. |

| | 3 | Commencement of operations. |

| | | | | | | | | | | | | | | | |

| Performance Summary for the Period Ended March 31, 2014 | |

| | | | | | Average Annual Total Returns4 | |

| | | 6 Months Total Returns | | | 1 Year | | | 5 Years | | | Since Inception5 | |

Series S Portfolio | | | 1.56 | % | | | 1.66 | % | | | 4.51 | % | | | 4.24 | % |

BofA Merrill Lynch 1-3 Year Treasury Index | | | 0.20 | | | | 0.38 | | | | 1.10 | | | | 2.62 | |

| | 4 | See “About Fund Performance” on page 12 for a detailed description of performance related information. |

| | 5 | The Fund commenced operations on October 1, 2004. |

| | | Past performance is not indicative of future results. |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Expense Example | |

| | | Actual | | | Hypothetical8 | |

| | | | | | | | | Including

Interest Expense | | | Excluding

Interest Expense | | | | | | Including

Interest Expense | | | Excluding

Interest Expense | |

| | | Beginning

Account Value

October 1, 2013 | | | Ending

Account Value

March 31, 2014 | | | Expenses Paid

During the Period6 | | | Expenses Paid

During the Period7 | | | Beginning

Account Value

October 1, 2013 | | | Ending

Account Value

March 31, 2014 | | | Expenses Paid

During the Period6 | | | Ending

Account Value

March 31, 2014 | | | Expenses Paid

During the Period7 | |

Series S Portfolio | | $ | 1,000.00 | | | $ | 1,015.60 | | | $ | 0.20 | | | $ | 0.00 | | | $ | 1,000.00 | | | $ | 1,024.73 | | | $ | 0.20 | | | $ | 1,024.93 | | | $ | 0.00 | |

| | 6 | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.04%, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 7 | For shares of the Fund, expenses are equal to the annualized expense ratio of 0.00%, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period shown). BlackRock has contractually agreed to waive all fees and pay or reimburse all direct expenses, except extraordinary expenses and interest expense, incurred by the Fund. This agreement has no fixed term. |

| | 8 | Hypothetical 5% annual return before expenses is calculated by pro rating the number of days in the most recent fiscal half year divided by 365. |

| | | See “Disclosure of Expenses” on page 12 for further information on how expenses were calculated. |

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | 11 |

Performance information reflects past performance and does not guarantee future results. Current performance may be lower or higher than the performance data quoted. Performance results do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Figures shown in each of the performance tables on the previous pages assume reinvestment of all dividends and distributions, if any, at net asset value (“NAV”) on the ex-dividend/payable date. Investment return and principal value of shares will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The performance information also reflects fee waivers and reimbursements that subsidize and reduce the total operating expenses of each Fund. The Funds’ returns would have been lower if there were no such waivers and reimbursements.

Shareholders of the Funds may incur the following charges: (a) transactional expenses and (b) operating expenses, including administration fees and other Fund expenses. The expense examples on the previous pages (which are based on a hypothetical investment of $1,000 invested on October 1, 2013 and held through March 31, 2014) are intended to assist shareholders both in calculating expenses based on an investment in each Fund and in comparing these expenses with similar costs of investing in other mutual funds.

The expense examples provide information about actual account values and actual expenses. In order to estimate the expenses a shareholder paid during the period covered by this report, shareholders can divide their account value by $1,000 and then multiply the result by the number corresponding to their Fund under the headings entitled “Expenses Paid During the Period.”

The expense examples also provide information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses. In order to assist shareholders in comparing the ongoing expenses of investing in these Funds and other funds, compare the 5% hypothetical example with the 5% hypothetical examples that appear in other funds’ shareholder reports.

The expenses shown in the expense examples are intended to highlight shareholders’ ongoing costs only and do not reflect any transactional expenses, if any. Therefore, the hypothetical examples are useful in comparing ongoing expenses only, and will not help shareholders determine the relative total expenses of owning different funds. If these transactional expenses were included, shareholder expenses would have been higher.

| | | | | | |

| 12 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

| | |

| The Benefits and Risks of Leveraging | | |

The Funds may utilize leverage to seek to enhance their yields and NAVs. However, these objectives cannot be achieved in all interest rate environments.

The Funds may utilize leverage by entering into reverse repurchase agreements. In general, the concept of leveraging is based on the premise that the financing cost of assets to be obtained from leverage, which will be based on short-term interest rates, will normally be lower than the income earned by each Fund on its longer-term portfolio investments. To the extent that the total assets of each Fund (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, each Fund’s shareholders will benefit from the incremental net income.

The interest earned on securities purchased with the proceeds from leverage is paid to shareholders in the form of dividends, and the value of these portfolio holdings is reflected in the per share NAV. However, in order to benefit shareholders, the yield curve must be positively sloped; that is, short-term interest rates must be lower than long-term interest rates. If the yield curve becomes negatively sloped, meaning short-term interest rates exceed long-term interest rates, income to shareholders will be lower than if the Funds had not used leverage.

If short-term interest rates rise, narrowing the differential between short-term and long-term interest rates, the incremental net income pickup will be reduced or eliminated completely. Furthermore, if prevailing short-term interest rates rise above long-term interest rates, the yield curve will have a negative slope. In this case, the Funds pay higher short-term interest rates whereas the Funds’ total portfolio earns income based on lower long-term interest rates.

Furthermore, the value of the Funds’ portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can influence the value of portfolio investments. As a result, changes in interest rates can influence the Funds’ NAVs positively or negatively in addition to the impact on Fund performance from leverage.

The use of leverage may enhance opportunities for increased income to the Funds, but as described above, it also creates risks as short- or long-term interest rates fluctuate. Leverage also will generally cause greater changes in the Funds’ NAVs, market prices and dividend rates than comparable portfolios without leverage. If the income derived from securities purchased with assets received from leverage exceeds the cost of leverage, the Funds’ net income will be greater than if leverage had not been used. Conversely, if the income from the securities purchased is not sufficient to cover the cost of leverage, each Fund’s net income will be less than if leverage had not been used, and therefore the amount available for distribution to shareholders will be reduced. Each Fund may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause a Fund to incur losses. The use of leverage may limit each Fund’s ability to invest in certain types of securities or use certain types of hedging strategies. Each Fund will incur expenses in connection with the use of leverage, all of which are borne by Fund shareholders and may reduce income.

| | |

| Derivative Financial Instruments | | |

The Funds may invest in various derivative financial instruments, including financial futures contracts, options and swaps, as specified in Note 4 of the Notes to Financial Statements, which may constitute forms of economic leverage. Such derivative financial instruments are used to obtain exposure to a security, index and/or market without owning or taking physical custody of securities or to hedge market, credit and/or interest rate risks. Derivative financial instruments involve risks, including the imperfect correlation between the value of a derivative financial instrument and the underlying asset, possible default of the counterparty to the transaction or illiquidity of the derivative financial instrument. The

Funds’ ability to use a derivative financial instrument successfully depends on the investment advisor’s ability to predict pertinent market movements accurately, which cannot be assured. The use of derivative financial instruments may result in losses greater than if they had not been used, may require a Fund to sell or purchase portfolio investments at inopportune times or for distressed values, may limit the amount of appreciation a Fund can realize on an investment, may result in lower dividends paid to shareholders and/or may cause a Fund to hold an investment that it might otherwise sell. The Funds’ investments in these instruments are discussed in detail in the Notes to Financial Statements.

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | 13 |

| | | | |

| Schedule of Investments March 31, 2014 | | | Series C Portfolio | |

| | | (Percentages shown are based on Net Assets) | |

| | | | | | | | |

| Capital Trusts | | Par

(000) | | | Value | |

Banks — 0.0% | | | | | | | | |

Wachovia Capital Trust III, 5.57% (a)(b) | | $ | 225 | | | $ | 216,281 | |

Capital Markets — 0.3% | | | | | | | | |

State Street Capital Trust IV, 1.23%, 6/01/77 (a) | | | 1,075 | | | | 881,500 | |

Diversified Financial Services — 1.4% | | | | | | | | |

General Electric Capital Corp., 5.25%, (a)(b) | | | 900 | | | | 875,430 | |

JPMorgan Chase & Co.: | | | | | | | | |

6.00% (a)(b) | | | 1,325 | | | | 1,305,125 | |

7.90% (a)(b) | | | 1,500 | | | | 1,695,000 | |

ZFS Finance USA Trust V, 6.50%, 5/09/67 (a)(c) | | | 500 | | | | 536,250 | |

| | | | | | | | |

| | | | | | | | 4,411,805 | |

Insurance — 1.9% | | | | | | | | |

The Allstate Corp.: | | | | | | | | |

5.75%, 8/15/53 (a) | | | 740 | | | | 777,000 | |

6.50%, 5/15/67 (a) | | | 150 | | | | 159,165 | |

American International Group, Inc., 8.18%, 5/15/68 (a) | | | 760 | | | | 998,450 | |

Lincoln National Corp., 7.00%, 5/17/66 (a) | | | 875 | | | | 896,875 | |

MetLife Capital Trust IV, 7.88%, 12/15/67 (c) | | | 420 | | | | 495,600 | |

New York Life Insurance Co., 6.75%, 11/15/39 (c) | | | 600 | | | | 781,398 | |

Pacific Life Insurance Co., 9.25%, 6/15/39 (c) | | | 605 | | | | 886,407 | |

Prudential Financial, Inc., 8.88%, 6/15/68 (a) | | | 850 | | | | 1,041,250 | |

| | | | | | | | |

| | | | | | | | 6,036,145 | |

Media — 0.6% | | | | | | | | |

NBCUniversal Enterprise, Inc., 5.25% (b)(c) | | | 1,800 | | | | 1,818,000 | |

Oil, Gas & Consumable Fuels — 0.4% | | | | | | | | |

Enterprise Products Operating LLC, 7.03%, 1/15/68 (a) | | | 1,090 | | | | 1,234,425 | |

Total Capital Trusts — 4.6% | | | | | | | 14,598,156 | |

| | | | | | | | |

| Corporate Bonds | | | | | | |

Aerospace & Defense — 1.1% | | | | | | | | |

Northrop Grumman Systems Corp., 7.88%, 3/01/26 | | | 1,000 | | | | 1,329,973 | |

United Technologies Corp.: | | | | | | | | |

1.80%, 6/01/17 | | | 820 | | | | 833,704 | |

6.05%, 6/01/36 | | | 450 | | | | 554,684 | |

4.50%, 6/01/42 | | | 740 | | | | 753,521 | |

| | | | | | | | |

| | | | | | | | 3,471,882 | |

Air Freight & Logistics — 0.2% | | | | | | | | |

Federal Express Corp. Pass-Through Trust, Series 2012, 2.63%, 1/15/18 (c) | | | 721 | | | | 729,214 | |

| | | | | | | | |

| Corporate Bonds | | Par

(000) | | | Value | |

Airlines — 0.7% | | | | | | | | |

Doric Nimrod Air Alpha Pass-Through Trust, Series 2013-1, 5.25%, 5/30/25 (c) | | $ | 1,025 | | | $ | 1,076,250 | |

U.S. Airways Pass-Through Trust, Series 2013-1, Class A, 3.95%, 5/15/27 | | | 925 | | | | 931,937 | |

Virgin Australia Trust, 5.00%, 10/23/25 (c) | | | 325 | | | | 342,875 | |

| | | | | | | | |

| | | | | | | | 2,351,062 | |

Auto Components — 0.4% | | | | | | | | |

Icahn Enterprises LP/Icahn Enterprises Finance Corp.: | | | | | | | | |

3.50%, 3/15/17 (c) | | | 225 | | | | 227,250 | |

4.88%, 3/15/19 (c) | | | 501 | | | | 509,767 | |

5.88%, 2/01/22 (c) | | | 600 | | | | 609,000 | |

| | | | | | | | |

| | | | | | | | 1,346,017 | |

Automobiles — 1.5% | | | | | | | | |

Daimler Finance North America LLC: | | | | | | | | |

2.30%, 1/09/15 (c) | | | 800 | | | | 810,074 | |

1.25%, 1/11/16 (c) | | | 2,300 | | | | 2,312,896 | |

Ford Motor Co., 7.45%, 7/16/31 | | | 669 | | | | 858,408 | |

Volkswagen International Finance NV, 1.63%, 3/22/15 (c) | | | 850 | | | | 859,659 | |

| | | | | | | | |

| | | | | | | | 4,841,037 | |

Banks — 5.7% | | | | | | | | |

Associated Banc-Corp., 5.13%, 3/28/16 | | | 1,490 | | | | 1,592,415 | |

Cooperatieve Centrale Raiffeisen- Boerenleenbank BA: | | | | | | | | |

3.95%, 11/09/22 | | | 1,050 | | | | 1,042,827 | |

4.63%, 12/01/23 | | | 625 | | | | 643,159 | |

Fifth Third Bancorp, 4.30%, 1/16/24 | | | 600 | | | | 608,289 | |

HSBC Bank USA, N.A., 4.63%, 4/01/14 | | | 5,500 | | | | 5,500,000 | |

HSBC Holdings PLC: | | | | | | | | |

4.25%, 3/14/24 | | | 550 | | | | 550,677 | |

6.80%, 6/01/38 | | | 755 | | | | 927,695 | |

ING Bank NV: | | | | | | | | |

2.38%, 6/09/14 (c) | | | 850 | | | | 853,244 | |

3.00%, 9/01/15 (c) | | | 1,625 | | | | 1,671,605 | |

Intesa Sanpaolo SpA, 3.13%, 1/15/16 | | | 630 | | | | 645,000 | |

Regions Financial Corp., 5.75%, 6/15/15 | | | 550 | | | | 580,053 | |

Royal Bank of Scotland Group PLC, 6.00%, 12/19/23 | | | 775 | | | | 793,564 | |

Wells Fargo & Co.: | | | | | | | | |

3.68%, 6/15/16 (d) | | | 300 | | | | 318,103 | |

3.50%, 3/08/22 | | | 1,500 | | | | 1,530,811 | |

3.45%, 2/13/23 | | | 405 | | | | 393,087 | |

4.13%, 8/15/23 | | | 350 | | | | 354,075 | |

| | | | | | | | |

| | | | | | | | 18,004,604 | |

Beverages — 0.5% | | | | | | | | |

Anheuser-Busch InBev Worldwide, Inc., 2.50%, 7/15/22 | | | 1,800 | | | | 1,699,540 | |

| | | | |

| Portfolio Abbreviations |

GO General Obligation Bonds | | RB Revenue Bonds | | |

LIBOR London Interbank Offered Rate | | TBA To-be-announced | | |

OTC Over-the-counter | | | | |

See Notes to Financial Statements.

| | | | | | |

| 14 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

| | | | |

| Schedule of Investments (continued) | | | Series C Portfolio | |

| | | (Percentages shown are based on Net Assets) | |

| | | | | | | | |

| Corporate Bonds | | Par

(000) | | | Value | |

Biotechnology — 0.8% | | | | | | | | |

Amgen, Inc.: | | | | | | | | |

1.88%, 11/15/14 (e) | | $ | 1,975 | | | $ | 1,990,470 | |

5.38%, 5/15/43 | | | 520 | | | | 555,588 | |

| | | | | | | | |

| | | | | | | | 2,546,058 | |

Capital Markets — 3.6% | | | | | | | | |

Credit Suisse AG, 6.50%, 8/08/23 (c) | | | 1,000 | | | | 1,097,500 | |

The Goldman Sachs Group, Inc.: | | | | | | | | |

6.25%, 9/01/17 | | | 635 | | | | 725,152 | |

6.15%, 4/01/18 | | | 850 | | | | 971,713 | |

2.63%, 1/31/19 | | | 1,000 | | | | 997,438 | |

5.75%, 1/24/22 | | | 165 | | | | 187,097 | |

4.00%, 3/03/24 | | | 400 | | | | 398,227 | |

6.25%, 2/01/41 | | | 725 | | | | 860,898 | |

Morgan Stanley: | | | | | | | | |

0.72%, 10/15/15 (a) | | | 2,050 | | | | 2,050,970 | |

6.25%, 8/28/17 | | | 885 | | | | 1,012,864 | |

7.30%, 5/13/19 | | | 1,625 | | | | 1,970,789 | |

5.63%, 9/23/19 | | | 265 | | | | 301,417 | |

5.50%, 7/28/21 | | | 10 | | | | 11,299 | |

5.00%, 11/24/25 | | | 800 | | | | 823,136 | |

| | | | | | | | |

| | | | | | | | 11,408,500 | |

Chemicals — 0.4% | | | | | | | | |

CF Industries, Inc., 5.38%, 3/15/44 | | | 350 | | | | 364,899 | |

LyondellBasell Industries NV, 5.00%, 4/15/19 | | | 825 | | | | 918,604 | |

| | | | | | | | |

| | | | | | | | 1,283,503 | |

Commercial Services & Supplies — 0.7% | | | | | | | | |

The ADT Corp., 2.25%, 7/15/17 | | | 400 | | | | 395,256 | |

Aviation Capital Group Corp., 6.75%, 4/06/21 (c) | | | 1,575 | | | | 1,737,620 | |

| | | | | | | | |

| | | | | | | | 2,132,876 | |

Communications Equipment — 0.3% | | | | | | | | |

Brocade Communications Systems, Inc., 6.88%, 1/15/20 | | | 725 | | | | 774,844 | |

Consumer Finance — 2.0% | | | | | | | | |

Capital One Financial Corp.: | | | | | | | | |

2.15%, 3/23/15 | | | 2,900 | | | | 2,943,622 | |

1.00%, 11/06/15 | | | 475 | | | | 475,673 | |

Discover Bank, 4.20%, 8/08/23 | | | 500 | | | | 512,644 | |

Discover Financial Services, 3.85%, 11/21/22 | | | 650 | | | | 638,056 | |

SLM Corp., 3.88%, 9/10/15 | | | 1,700 | | | | 1,751,000 | |

| | | | | | | | |

| | | | | | | | 6,320,995 | |

Diversified Financial Services — 10.5% | | | | | | | | |

Bank of America Corp.: | | | | | | | | |

6.50%, 8/01/16 (e) | | | 3,330 | | | | 3,729,780 | |

5.63%, 10/14/16 | | | 325 | | | | 359,106 | |

5.75%, 12/01/17 | | | 1,755 | | | | 1,986,909 | |

5.70%, 1/24/22 | | | 2,125 | | | | 2,438,066 | |

4.00%, 4/01/24 | | | 1,250 | | | | 1,248,529 | |

4.88%, 4/01/44 | | | 500 | | | | 502,275 | |

BP Capital Markets PLC, 3.13%, 10/01/15 (e) | | | 2,875 | | | | 2,983,275 | |

Citigroup, Inc.: | | | | | | | | |

5.50%, 10/15/14 | | | 1,800 | | | | 1,847,437 | |

4.75%, 5/19/15 | | | 371 | | | | 387,373 | |

5.30%, 1/07/16 | | | 768 | | | | 825,073 | |

2.50%, 9/26/18 | | | 1,125 | | | | 1,131,108 | |

6.00%, 10/31/33 | | | 100 | | | | 107,999 | |

CME Group Index Services LLC, 4.40%, 3/15/18 (c) | | | 1,700 | | | | 1,840,634 | |

Ford Motor Credit Co. LLC: | | | | | | | | |

2.75%, 5/15/15 | | | 2,350 | | | | 2,397,917 | |

| | | | | | | | |

| Corporate Bonds | | Par

(000) | | | Value | |

Diversified Financial Services (concluded) | | | | | | | | |

1.70%, 5/09/16 | | $ | 700 | | | $ | 707,816 | |

8.13%, 1/15/20 | | | 1,400 | | | | 1,765,393 | |

General Electric Capital Corp.: | | | | | | | | |

6.75%, 3/15/32 | | | 1,075 | | | | 1,382,162 | |

6.15%, 8/07/37 (e) | | | 715 | | | | 867,180 | |

HSBC Finance Corp., 6.68%, 1/15/21 | | | 1,100 | | | | 1,283,635 | |

Iberdrola Finance Ireland Ltd., 3.80%, 9/11/14 (c) | | | 750 | | | | 759,810 | |

ING US, Inc., 2.90%, 2/15/18 | | | 775 | | | | 794,078 | |

JPMorgan Chase & Co.: | | | | | | | | |

3.20%, 1/25/23 | | | 1,275 | | | | 1,236,329 | |

3.88%, 2/01/24 | | | 700 | | | | 706,280 | |

Merrill Lynch & Co., Inc., 6.05%, 5/16/16 | | | 1,350 | | | | 1,475,559 | |

SteelRiver Transmission Co. LLC, 4.71%, 6/30/17 (c) | | | 568 | | | | 598,622 | |

| | | | | | | | |

| | | | | | | | 33,362,345 | |

Diversified Telecommunication Services — 4.5% | | | | | | | | |

AT&T Inc., 6.50%, 9/01/37 | | | 877 | | | | 1,020,281 | |

Deutsche Telekom International Finance BV, 3.13%, 4/11/16 (c) | | | 950 | | | | 990,311 | |

Qwest Corp., 7.50%, 10/01/14 | | | 1,075 | | | | 1,109,902 | |

Telefonica Moviles Chile SA, 2.88%, 11/09/15 (c) | | | 1,375 | | | | 1,398,849 | |

Verizon Communications, Inc.: | | | | | | | | |

3.65%, 9/14/18 | | | 3,500 | | | | 3,725,862 | |

5.15%, 9/15/23 | | | 725 | | | | 793,381 | |

6.40%, 9/15/33 | | | 1,375 | | | | 1,632,465 | |

6.25%, 4/01/37 | | | 850 | | | | 988,322 | |

3.85%, 11/01/42 | | | 425 | | | | 355,829 | |

6.55%, 9/15/43 | | | 1,050 | | | | 1,277,782 | |

Verizon Global Funding Corp., 7.75%, 12/01/30 | | | 750 | | | | 991,824 | |

| | | | | | | | |

| | | | | | | | 14,284,808 | |

Electric Utilities — 6.7% | | | | | | | | |

American Transmission Systems, Inc., 5.25%, 1/15/22 (c) | | | 400 | | | | 431,071 | |

Carolina Power & Light Co., 6.30%, 4/01/38 | | | 750 | | | | 964,357 | |

Duke Energy Carolinas LLC, 5.25%, 1/15/18 | | | 450 | | | | 506,320 | |

Duke Energy Corp., 3.35%, 4/01/15 | | | 1,700 | | | | 1,745,441 | |

E.ON International Finance BV, 5.80%, 4/30/18 (c) | | | 1,100 | | | | 1,248,962 | |

Entergy Arkansas, Inc., 3.70%, 6/01/24 | | | 825 | | | | 837,304 | |

Florida Power & Light Co., 5.95%, 2/01/38 | | | 1,075 | | | | 1,303,837 | |

Great Plains Energy, Inc., 5.29%, 6/15/22 (d) | | | 745 | | | | 826,274 | |

Jersey Central Power & Light Co., 5.65%, 6/01/17 | | | 1,710 | | | | 1,889,208 | |

Kentucky Utilities Co., 5.13%, 11/01/40 | | | 375 | | | | 420,125 | |

MidAmerican Energy Holdings Co.: | | | | | | | | |

5.30%, 3/15/18 | | | 2,170 | | | | 2,451,095 | |

5.75%, 4/01/18 | | | 1,475 | | | | 1,678,939 | |

Mississippi Power Co., 4.25%, 3/15/42 | | | 400 | | | | 368,871 | |

Northern States Power Co., 6.20%, 7/01/37 | | | 725 | | | | 910,483 | |

Ohio Power Co., 6.60%, 3/01/33 | | | 675 | | | | 833,900 | |

Oncor Electric Delivery Co. LLC: | | | | | | | | |

4.10%, 6/01/22 | | | 650 | | | | 681,013 | |

5.30%, 6/01/42 | | | 700 | | | | 778,536 | |

PacifiCorp, 6.00%, 1/15/39 | | | 450 | | | | 556,696 | |

Progress Energy, Inc.: | | | | | | | | |

4.88%, 12/01/19 | | | 1,075 | | | | 1,192,683 | |

3.15%, 4/01/22 | | | 775 | | | | 761,302 | |

Southern California Edison Co., 5.35%, 7/15/35 | | | 825 | | | | 937,955 | |

| | | | | | | | |

| | | | | | | | 21,324,372 | |

See Notes to Financial Statements.

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | 15 |

| | | | |

| Schedule of Investments (continued) | | | Series C Portfolio | |

| | | (Percentages shown are based on Net Assets) | |

| | | | | | | | |

| Corporate Bonds | | Par

(000) | | | Value | |

Energy Equipment & Services — 1.8% | | | | | | | | |

Ensco PLC, 3.25%, 3/15/16 | | $ | 1,600 | | | $ | 1,668,390 | |

Transocean, Inc.: | | | | | | | | |

5.05%, 12/15/16 | | | 1,775 | | | | 1,930,636 | |

6.50%, 11/15/20 | | | 686 | | | | 770,328 | |

6.38%, 12/15/21 | | | 889 | | | | 999,195 | |

Weatherford International Ltd.: | | | | | | | | |

4.50%, 4/15/22 | | | 150 | | | | 157,079 | |

5.95%, 4/15/42 | | | 200 | | | | 215,487 | |

| | | | | | | | |

| | | | | | | | 5,741,115 | |

Food & Staples Retailing — 1.1% | | | | | | | | |

Tesco PLC, 5.50%, 11/15/17 (c) | | | 1,840 | | | | 2,051,374 | |

Wal-Mart Stores, Inc.: | | | | | | | | |

5.25%, 9/01/35 | | | 675 | | | | 761,477 | |

6.50%, 8/15/37 | | | 385 | | | | 498,511 | |

6.20%, 4/15/38 | | | 230 | | | | 289,194 | |

| | | | | | | | |

| | | | | | | | 3,600,556 | |

Food Products — 0.3% | | | | | | | | |

Kraft Foods Group, Inc.: | | | | | | | | |

6.88%, 1/26/39 | | | 368 | | | | 473,812 | |

5.00%, 6/04/42 | | | 495 | | | | 518,341 | |

| | | | | | | | |

| | | | | | | | 992,153 | |

Gas Utilities — 0.3% | | | | | | | | |

Atmos Energy Corp., 8.50%, 3/15/19 | | | 800 | | | | 1,020,815 | |

Health Care Equipment & Supplies — 1.2% | | | | | | | | |

Covidien International Finance SA: | | | | | | | | |

1.35%, 5/29/15 | | | 800 | | | | 806,434 | |

6.00%, 10/15/17 | | | 2,300 | | | | 2,641,260 | |

2.95%, 6/15/23 | | | 525 | | | | 497,494 | |

| | | | | | | | |

| | | | | | | | 3,945,188 | |

Health Care Providers & Services — 0.7% | | | | | | | | |

Coventry Health Care, Inc., 5.45%, 6/15/21 | | | 850 | | | | 974,761 | |

WellPoint, Inc., 4.35%, 8/15/20 | | | 1,275 | | | | 1,354,918 | |

| | | | | | | | |

| | | | | | | | 2,329,679 | |

Independent Power and Renewable Electricity Producers — 0.3% | |

IPALCO Enterprises, Inc., 5.00%, 5/01/18 | | | 925 | | | | 978,187 | |

Industrial Conglomerates — 0.9% | | | | | | | | |

Eaton Corp.: | | | | | | | | |

2.75%, 11/02/22 | | | 975 | | | | 922,967 | |

4.15%, 11/02/42 | | | 375 | | | | 350,222 | |

Hutchison Whampoa International Ltd., 4.63%, 9/11/15 (c) | | | 1,000 | | | | 1,051,946 | |

Tyco Electronics Group SA, 3.50%, 2/03/22 | | | 600 | | | | 594,929 | |

| | | | | | | | |

| | | | | | | | 2,920,064 | |

Insurance — 5.9% | | | | | | | | |

ACE INA Holdings, Inc., 2.60%, 11/23/15 | | | 625 | | | | 643,691 | |

Allied World Assurance Co. Holdings Ltd., 5.50%, 11/15/20 | | | 825 | | | | 917,473 | |

American International Group, Inc.: | | | | | | | | |

4.88%, 9/15/16 | | | 500 | | | | 545,499 | |

3.80%, 3/22/17 | | | 900 | | | | 962,910 | |

5.45%, 5/18/17 | | | 725 | | | | 809,058 | |

5.85%, 1/16/18 (e) | | | 1,530 | | | | 1,748,424 | |

3.38%, 8/15/20 | | | 1,000 | | | | 1,020,892 | |

6.40%, 12/15/20 | | | 485 | | | | 577,849 | |

Genworth Holdings, Inc.: | | | | | | | | |

6.52%, 5/22/18 | | | 200 | | | | 230,666 | |

7.63%, 9/24/21 | | | 330 | | | | 406,523 | |

4.80%, 2/15/24 | | | 450 | | | | 468,121 | |

Manulife Financial Corp., 4.90%, 9/17/20 | | | 750 | | | | 815,089 | |

Massachusetts Mutual Life Insurance Co., 8.88%, 6/01/39 (c) | | | 575 | | | | 874,454 | |

| | | | | | | | |

| Corporate Bonds | | Par

(000) | | | Value | |

Insurance (concluded) | | | | | | | | |

MetLife Institutional Funding II, 1.63%, 4/02/15 (c)(e) | | $ | 6,000 | | | $ | 6,071,574 | |

Prudential Financial, Inc.: | | | | | | | | |

5.40%, 6/13/35 | | | 1,000 | | | | 1,085,322 | |

5.70%, 12/14/36 | | | 175 | | | | 198,294 | |

Teachers Insurance & Annuity Association of America, 6.85%, 12/16/39 (c) | | | 1,050 | | | | 1,377,846 | |

| | | | | | | | |

| | | | | | | | 18,753,685 | |

IT Services — 0.2% | | | | | | | | |

Fidelity National Information Services, Inc., 3.50%, 4/15/23 | | | 625 | | | | 593,996 | |

Life Sciences Tools & Services — 0.7% | | | | | | | | |

Life Technologies Corp.: | | | | | | | | |

3.50%, 1/15/16 | | | 1,295 | | | | 1,349,251 | |

6.00%, 3/01/20 | | | 820 | | | | 943,618 | |

| | | | | | | | |

| | | | | | | | 2,292,869 | |

Machinery — 0.3% | | | | | | | | |

AGCO Corp., 5.88%, 12/01/21 | | | 775 | | | | 842,820 | |

Media — 4.6% | | | | | | | | |

Comcast Corp.: | | | | | | | | |

4.25%, 1/15/33 | | | 650 | | | | 637,095 | |

6.50%, 11/15/35 | | | 550 | | | | 682,056 | |

6.55%, 7/01/39 | | | 500 | | | | 624,119 | |

4.50%, 1/15/43 | | | 225 | | | | 219,449 | |

COX Communications, Inc.: | | | | | | | | |

2.95%, 6/30/23 (c) | | | 475 | | | | 433,505 | |

8.38%, 3/01/39 (c) | | | 625 | | | | 819,949 | |

DIRECTV Holdings LLC/DIRECTV Financing Co., Inc.: | | | | | | | | |

5.20%, 3/15/20 | | | 800 | | | | 875,994 | |

6.38%, 3/01/41 | | | 229 | | | | 248,925 | |

Discovery Communications LLC, 3.70%, 6/01/15 | | | 1,175 | | | | 1,215,683 | |

Grupo Televisa SAB, 6.63%, 1/15/40 | | | 900 | | | | 1,030,906 | |

News America, Inc., 6.40%, 12/15/35 | | | 781 | | | | 933,328 | |

Omnicom Group, Inc., 4.45%, 8/15/20 | | | 328 | | | | 349,848 | |

TCM Sub LLC, 3.55%, 1/15/15 (c) | | | 1,750 | | | | 1,788,463 | |

Time Warner Cable, Inc.: | | | | | | | | |

7.50%, 4/01/14 | | | 1,425 | | | | 1,425,000 | |

8.25%, 4/01/19 | | | 695 | | | | 865,939 | |

6.55%, 5/01/37 | | | 625 | | | | 725,894 | |

Time Warner, Inc., 6.25%, 3/29/41 | | | 682 | | | | 798,950 | |

Virgin Media Secured Finance PLC, 6.50%, 1/15/18 | | | 820 | | | | 849,725 | |

| | | | | | | | |

| | | | | | | | 14,524,828 | |

Metals & Mining — 1.9% | | | | | | | | |

Barrick Gold Corp., 4.10%, 5/01/23 | | | 475 | | | | 450,602 | |

BHP Billiton Finance USA Ltd., 3.85%, 9/30/23 | | | 1,175 | | | | 1,203,726 | |

Freeport-McMoRan Copper & Gold, Inc.: | | | | | | | | |

3.10%, 3/15/20 | | | 550 | | | | 535,051 | |

3.55%, 3/01/22 | | | 1,530 | | | | 1,461,179 | |

3.88%, 3/15/23 | | | 600 | | | | 573,704 | |

Rio Tinto Finance USA Ltd., 7.13%, 7/15/28 | | | 550 | | | | 699,226 | |

Southern Copper Corp., 6.75%, 4/16/40 | | | 450 | | | | 457,984 | |

Teck Resources Ltd., 6.25%, 7/15/41 | | | 557 | | | | 575,059 | |

| | | | | | | | |

| | | | | | | | 5,956,531 | |

Multiline Retail — 0.4% | | | | | | | | |

Dollar General Corp., 3.25%, 4/15/23 | | | 1,300 | | | | 1,227,207 | |

Multi-Utilities — 1.7% | | | | | | | | |

CenterPoint Energy, Inc., 6.50%, 5/01/18 | | | 850 | | | | 985,611 | |

CMS Energy Corp., 5.05%, 3/15/22 | | | 1,644 | | | | 1,828,595 | |

See Notes to Financial Statements.

| | | | | | |

| 16 | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | |

| | | | |

| Schedule of Investments (continued) | | | Series C Portfolio | |

| | | (Percentages shown are based on Net Assets) | |

| | | | | | | | | | |

| Corporate Bonds | | | | Par

(000) | | | Value | |

Multi-Utilities (concluded) | | | | | | | | | | |

NiSource Finance Corp., 5.25%, 2/15/43 | | | | $ | 440 | | | $ | 449,408 | |

Pacific Gas & Electric Co., 3.85%, 11/15/23 | | | | | 575 | | | | 579,847 | |

PSEG Power LLC, 4.30%, 11/15/23 | | | | | 580 | | | | 593,084 | |

Virginia Electric & Power Co., 6.00%, 1/15/36 | | | | | 900 | | | | 1,102,396 | |

| | | | | | | | | | |

| | | | | | | | | | 5,538,941 | |

Oil, Gas & Consumable Fuels — 8.0% | | | | | | | | | | |

Anadarko Petroleum Corp.: | | | | | | | | | | |

5.75%, 6/15/14 | | | | | 900 | | | | 909,167 | |

6.38%, 9/15/17 | | | | | 1,545 | | | | 1,768,739 | |

Canadian Natural Resources Ltd., 5.90%, 2/01/18 | | | | | 1,700 | | | | 1,934,903 | |

Continental Resources, Inc.: | | | | | | | | | | |

7.13%, 4/01/21 | | | | | 460 | | | | 520,375 | |

5.00%, 9/15/22 | | | | | 790 | | | | 829,500 | |

DCP Midstream LLC: | | | | | | | | | | |

5.35%, 3/15/20 (c) | | | | | 260 | | | | 279,392 | |

4.75%, 9/30/21 (c) | | | | | 161 | | | | 165,552 | |

El Paso Natural Gas Co. LLC, 8.63%, 1/15/22 | | | | | 485 | | | | 627,889 | |

El Paso Pipeline Partners Operating Co. LLC,

6.50%, 4/01/20 | | | | | 390 | | | | 446,390 | |

Energy Transfer Partners LP: | | | | | | | | | | |

5.20%, 2/01/22 | | | | | 1,130 | | | | 1,219,844 | |

6.50%, 2/01/42 | | | | | 560 | | | | 634,666 | |

Enterprise Products Operating LLC: | | | | | | | | | | |

3.70%, 6/01/15 | | | | | 500 | | | | 516,543 | |

6.45%, 9/01/40 | | | | | 800 | | | | 972,220 | |

5.70%, 2/15/42 | | | | | 490 | | | | 543,927 | |

Kerr-McGee Corp.: | | | | | | | | | | |

6.95%, 7/01/24 | | | | | 720 | | | | 873,065 | |

7.88%, 9/15/31 | | | | | 450 | | | | 584,136 | |

Kinder Morgan Energy Partners LP,

7.30%, 8/15/33 | | | | | 1,400 | | | | 1,717,701 | |

Noble Holding International Ltd., 3.95%, 3/15/22 | | | | | 480 | | | | 475,971 | |

Pioneer Natural Resources Co.: | | | | | | | | | | |

6.88%, 5/01/18 | | | | | 880 | | | | 1,029,042 | |

7.50%, 1/15/20 | | | | | 120 | | | | 146,496 | |

Plains Exploration & Production Co.,

6.50%, 11/15/20 | | | | | 400 | | | | 440,500 | |

Schlumberger Norge AS, 4.20%, 1/15/21 (c) | | | | | 975 | | | | 1,054,105 | |

Shell International Finance BV, 6.38%, 12/15/38 | | | | | 800 | | | | 1,031,299 | |

Texas Eastern Transmission LP, 2.80%, 10/15/22 (c) | | | | | 1,400 | | | | 1,296,406 | |

TransCanada PipeLines Ltd., 3.75%, 10/16/23 | | | | | 850 | | | | 856,484 | |

Valero Energy Corp., 6.63%, 6/15/37 | | | | | 426 | | | | 512,685 | |

Western Gas Partners LP, 5.38%, 6/01/21 | | | | | 1,025 | | | | 1,123,814 | |

The Williams Cos., Inc.: | | | | | | | | | | |

3.70%, 1/15/23 | | | | | 1,200 | | | | 1,088,981 | |

7.75%, 6/15/31 | | | | | 186 | | | | 208,677 | |

8.75%, 3/15/32 | | | | | 155 | | | | 186,856 | |

Williams Partners LP: | | | | | | | | | | |

4.50%, 11/15/23 | | | | | 1,300 | | | | 1,330,087 | |

6.30%, 4/15/40 | | | | | 225 | | | | 255,667 | |

| | | | | | | | | | |

| | | | | | | | | | 25,581,079 | |

Paper & Forest Products — 0.4% | | | | | | | | | | |

International Paper Co., 7.95%, 6/15/18 | | | | | 1,150 | | | | 1,406,505 | |

Pharmaceuticals — 4.8% | | | | | | | | | | |

AbbVie, Inc.: | | | | | | | | | | |

1.75%, 11/06/17 | | | | | 2,220 | | | | 2,227,015 | |

2.90%, 11/06/22 | | | | | 1,805 | | | | 1,737,641 | |

Allergan, Inc., 5.75%, 4/01/16 | | | | | 550 | | | | 603,991 | |

Express Scripts Holding Co., 2.10%, 2/12/15 | | | | | 775 | | | | 784,875 | |

Hospira, Inc., 5.20%, 8/12/20 | | | | | 900 | | | | 961,544 | |

Merck & Co., Inc., 6.55%, 9/15/37 | | | | | 250 | | | | 324,372 | |

| | | | | | | | | | |

| Corporate Bonds | | | | Par

(000) | | | Value | |

Pharmaceuticals (concluded) | | | | | | | | | | |

Mylan, Inc.: | | | | | | | | | | |

2.60%, 6/24/18 | | | | $ | 968 | | | $ | 975,269 | |

6.00%, 11/15/18 (c) | | | | | 1,780 | | | | 1,879,199 | |

Perrigo Co. PLC, 4.00%, 11/15/23 (c) | | | | | 750 | | | | 749,710 | |

Pfizer, Inc., 3.00%, 6/15/23 | | | | | 950 | | | | 921,309 | |

Roche Holding, Inc., 6.00%, 3/01/19 (c) | | | | | 824 | | | | 968,085 | |

Teva Pharmaceutical Finance Co. LLC,

6.15%, 2/01/36 | | | | | 400 | | | | 454,539 | |

Teva Pharmaceutical Finance IV BV,

3.65%, 11/10/21 | | | | | 1,140 | | | | 1,141,895 | |

Teva Pharmaceutical Finance IV LLC,

2.25%, 3/18/20 | | | | | 425 | | | | 405,895 | |

Wyeth LLC, 5.95%, 4/01/37 | | | | | 800 | | | | 968,240 | |

| | | | | | | | | | |

| | | | | | | | | | 15,103,579 | |

Professional Services — 0.6% | | | | | | | | | | |

The Dun & Bradstreet Corp., 3.25%, 12/01/17 | | | | | 1,300 | | | | 1,344,079 | |

Experian Finance PLC, 2.38%, 6/15/17 (c) | | | | | 600 | | | | 610,132 | |

| | | | | | | | | | |

| | | | | | | | | | 1,954,211 | |

Real Estate Investment Trusts (REITs) — 3.0% | | | | | | | | | | |

American Tower Corp.: | | | | | | | | | | |

4.63%, 4/01/15 | | | | | 1,000 | | | | 1,035,983 | |

4.70%, 3/15/22 | | | | | 575 | | | | 600,797 | |

3.50%, 1/31/23 | | | | | 525 | | | | 496,461 | |

5.00%, 2/15/24 | | | | | 568 | | | | 591,574 | |

AvalonBay Communities, Inc., 4.20%, 12/15/23 | | | | | 1,000 | | | | 1,028,743 | |

DDR Corp.: | | | | | | | | | | |

4.75%, 4/15/18 | | | | | 280 | | | | 303,561 | |

7.88%, 9/01/20 | | | | | 350 | | | | 434,704 | |

HCP, Inc., 3.75%, 2/01/16 | | | | | 525 | | | | 552,648 | |

Host Hotels & Resorts LP, 6.00%, 10/01/21 | | | | | 725 | | | | 819,131 | |

Plum Creek Timberlands LP, 4.70%, 3/15/21 | | | | | 875 | | | | 919,504 | |

Simon Property Group LP: | | | | | | | | | | |

1.50%, 2/01/18 (c) | | | | | 725 | | | | 714,825 | |

10.35%, 4/01/19 | | | | | 280 | | | | 378,955 | |

Ventas Realty LP/Ventas Capital Corp.: | | | | | | | | | | |

2.70%, 4/01/20 | | | | | 600 | | | | 584,025 | |

4.75%, 6/01/21 | | | | | 845 | | | | 910,718 | |

| | | | | | | | | | |

| | | | | | | | | | 9,371,629 | |

Road & Rail — 1.6% | | | | | | | | | | |

Burlington Northern Santa Fe LLC, 5.75%, 5/01/40 | | | | | 500 | | | | 572,979 | |

Canadian National Railway Co., 6.25%, 8/01/34 | | | | | 1,100 | | | | 1,370,451 | |

Canadian Pacific Railway Co., 7.25%, 5/15/19 | | | | | 500 | | | | 604,789 | |

Kansas City Southern de Mexico SA de CV,

2.35%, 5/15/20 | | | | | 370 | | | | 349,028 | |

Penske Truck Leasing Co. LP/PTL Finance Corp.: | | | | | | | | | | |

2.50%, 7/11/14 (c) | | | | | 475 | | | | 477,279 | |

3.13%, 5/11/15 (c) | | | | | 1,500 | | | | 1,536,959 | |

| | | | | | | | | | |

| | | | | | | | | | 4,911,485 | |

Software — 0.4% | | | | | | | | | | |

Autodesk, Inc., 1.95%, 12/15/17 | | | | | 550 | | | | 551,582 | |

Oracle Corp., 3.63%, 7/15/23 | | | | | 800 | | | | 810,095 | |

| | | | | | | | | | |

| | | | | | | | | | 1,361,677 | |

Specialty Retail — 0.9% | | | | | | | | | | |

QVC, Inc.: | | | | | | | | | | |

7.50%, 10/01/19 (c) | | | | | 865 | | | | 920,402 | |

7.38%, 10/15/20 (c) | | | | | 310 | | | | 334,308 | |

4.38%, 3/15/23 | | | | | 1,700 | | | | 1,675,296 | |

| | | | | | | | | | |

| | | | | | | | | | 2,930,006 | |

See Notes to Financial Statements.

| | | | | | |

| | | BLACKROCK ALLOCATION TARGET SHARES | | MARCH 31, 2014 | | 17 |

| | | | |

| Schedule of Investments (continued) | | | Series C Portfolio | |

| | | (Percentages shown are based on Net Assets) | |

| | | | | | | | | | |

| Corporate Bonds | | Par (000) | | | Value | |

Technology Hardware, Storage & Peripherals — 0.2% | | | | | |

Hewlett-Packard Co., 2.63%, 12/09/14 | | | | $ | 545 | | | $ | 552,324 | |

Tobacco — 1.5% | | | | | | | | | | |

Altria Group, Inc.: | | | | | | | | | | |

9.95%, 11/10/38 | | | | | 46 | | | | 73,806 | |

10.20%, 2/06/39 | | | | | 221 | | | | 362,668 | |

5.38%, 1/31/44 | | | | | 550 | | | | 574,967 | |

BAT International Finance PLC, 1.40%, 6/05/15 (c) | | | | | 1,200 | | | | 1,209,364 | |

Imperial Tobacco Finance PLC, 2.05%, 2/11/18 (c) | | | | | 950 | | | | 942,391 | |

Lorillard Tobacco Co., 7.00%, 8/04/41 | | | | | 350 | | | | 401,584 | |

Philip Morris International, Inc., 3.60%, 11/15/23 | | | | | 1,075 | | | | 1,071,126 | |

| | | | | | | | | | |

| | | | | | | | | | 4,635,906 | |

Wireless Telecommunication Services — 2.7% | | | | | | | | | | |

Alltel Corp., 7.88%, 7/01/32 | | | | | 470 | | | | 633,443 | |

America Movil SAB de CV: | | | | | | | | | | |

2.38%, 9/08/16 | | | | | 3,140 | | | | 3,231,060 | |

3.13%, 7/16/22 | | | | | 650 | | | | 620,181 | |

CC Holdings GS V LLC/Crown Castle GS III Corp., 2.38%, 12/15/17 | | | | | 300 | | | | 300,017 | |

Crown Castle Towers LLC, 6.11%, 1/15/40 (c) | | | | | 1,450 | | | | 1,662,148 | |

Rogers Communications, Inc., 7.50%, 3/15/15 | | | | | 2,125 | | | | 2,264,462 | |

| | | | | | | | | | |

| | | | | | | | | | 8,711,311 | |

Total Corporate Bonds — 86.0% | | | | 273,660,003 | |

| | | | | | | | | | |

| Foreign Agency Obligations | | | | | | | | |

CNOOC Finance 2013 Ltd., 3.00%, 5/09/23 | | | | | 800 | | | | 723,782 | |

Export-Import Bank of Korea, 0.99%, 1/14/17 (a) | | | | | 1,307 | | | | 1,314,186 | |

Nakilat, Inc., 6.07%, 12/31/33 (c) | | | | | 25 | | | | 26,143 | |

Petrobras International Finance Co.: | | | | | | | | | | |

2.88%, 2/06/15 | | | | | 775 | | | | 785,075 | |

3.88%, 1/27/16 | | | | | 700 | | | | 718,857 | |

5.88%, 3/01/18 | | | | | 2,350 | | | | 2,506,966 | |

Petroleos Mexicanos: | | | | | | | | | | |

3.50%, 7/18/18 | | | | | 1,700 | | | | 1,763,750 | |

3.50%, 1/30/23 | | | | | 650 | | | | 611,650 | |

6.38%, 1/23/45 (c) | | | | | 475 | | | | 512,406 | |

Total Foreign Agency Obligations — 2.8% | | | | 8,962,815 | |

| | | | | | | | | | |

| Foreign Government Obligations | | | | | | | | |

Brazil — 0.1% | | | | | | | | | | |

Federative Republic of Brazil, 5.63%, 1/07/41 | | | | | 328 | | | | 332,264 | |

Colombia — 0.4% | | | | | | | | | | |

Republic of Colombia: | | | | | | | | | | |

2.63%, 3/15/23 | | | | | 1,200 | | | | 1,080,000 | |

5.63%, 2/26/44 | | | | | 225 | | | | 234,900 | |

| | | | | | | | | | |

| | | | | | | | | | 1,314,900 | |

| | | | | | | | | | |

| Foreign Government Obligations | | Par (000) | | | Value | |

Indonesia — 0.3% | | | | | | | | | | |

Republic of Indonesia: | | | | | | | | | | |

4.88%, 5/05/21 | | | | $ | 500 | | | $ | 512,500 | |

5.88%, 1/15/24 | | | | | 400 | | | | 429,500 | |

| | | | | | | | | | |

| | | | | | | | | | 942,000 | |

Mexico — 1.4% | | | | | | | | | | |

United Mexican States: | | | | | | | | | | |

4.00%, 10/02/23 | | | | | 1,100 | | | | 1,111,000 | |

4.75%, 3/08/44 | | | | | 2,525 | | | | 2,398,750 | |

5.55%, 1/21/45 | | | | | 800 | | | | 850,000 | |

| | | | | | | | | | |

| | | | | | | | | | 4,359,750 | |

Philippines — 0.0% | | | | | | | | | | |

Republic of Philippine, 4.20%, 1/21/24 | | | | | 203 | | | | 209,598 | |

Turkey — 0.4% | | | | | | | | | | |

Republic of Turkey, 6.63%, 2/17/45 | | | | | 1,175 | | | | 1,238,156 | |

Total Foreign Government Obligations — 2.6% | | | | 8,396,668 | |

| | | | | | | | | | |

| Taxable Municipal Bonds | | | | | | | | |

Chicago O’Hare International Airport RB,

6.40%, 1/01/40 | | | | | 1,000 | | | | 1,200,680 | |

Los Angeles Department of Water & Power RB, 6.57%, 7/01/45 | | | | | 1,075 | | | | 1,424,848 | |

Metropolitan Transportation Authority, New York RB, 7.34%, 11/15/39 | | | | | 1,125 | | | | 1,579,883 | |

Municipal Electric Authority of Georgia RB,

6.64%, 4/01/57 | | | | | 1,200 | | | | 1,368,000 | |

Port Authority of New York & New Jersey RB, 4.46%, 10/01/62 | | | | | 1,300 | | | | 1,217,567 | |

State of California GO: | | | | | | | | | | |

7.30%, 10/01/39 | | | | | 510 | | | | 685,272 | |