UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT

COMPANIES

COMPANIES

| Investment Company Act file number: | 811-21335 |

| Exact name of registrant as specified in charter: | Optimum Fund Trust |

| Address of principal executive offices: | 2005 Market Street |

| Philadelphia, PA 19103 | |

| Name and address of agent for service: | David F. Connor, Esq. |

| 2005 Market Street | |

| Philadelphia, PA 19103 | |

| Registrant’s telephone number, including area code: | (800) 523-1918 |

| Date of fiscal year end: | March 31 |

| Date of reporting period: | March 31, 2010 |

Item 1. Reports to Stockholders

| | ||

| Optimum Fund Trust | ||

| May 28, 2010 | ||

This brochure accompanies an annual report for the information of Optimum Fund Trust shareholders, but it may be used with prospective investors when preceded or accompanied by a current prospectus for Optimum Fund Trust. You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The prospectus contains this and other important information about the Funds. Prospectuses for Optimum Fund Trust are available from your financial advisor, online at www.optimummutualfunds.com, or by phone at 800 914-0278. Please read the prospectus carefully before you invest or send money. The figures in the annual report for Optimum Fund Trust represent past results, which are not a guarantee of future results. The return and principal value of an investment in a Fund will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. | ||

| | |||

| Optimum Fixed Income Fund | |||

| Optimum International Fund | |||

| Optimum Large Cap Growth Fund | |||

| Optimum Large Cap Value Fund | |||

| Optimum Small-Mid Cap Growth Fund | |||

| Optimum Small-Mid Cap Value Fund | |||

| Annual Report | |||

| March 31, 2010 | |||

Table of contents

| > Portfolio management review | |

| Optimum Fixed Income Fund | 1 |

| Optimum International Fund | 4 |

| Optimum Large Cap Growth Fund | 7 |

| Optimum Large Cap Value Fund | 10 |

| Optimum Small-Mid Cap Growth Fund | 13 |

| Optimum Small-Mid Cap Value Fund | 15 |

| > Performance summary | |

| Optimum Fixed Income Fund | 18 |

| Optimum International Fund | 22 |

| Optimum Large Cap Growth Fund | 24 |

| Optimum Large Cap Value Fund | 26 |

| Optimum Small-Mid Cap Growth Fund | 28 |

| Optimum Small-Mid Cap Value Fund | 30 |

| > Disclosure of Fund expenses | 32 |

| > Sector/Country allocations | |

| and top 10 holdings | 34 |

| > Financial statements | |

| Statements of net assets | 38 |

| Statements of assets and liabilities | 80 |

| Statements of operations | 81 |

| Statements of changes in net assets | 82 |

| Financial highlights | 85 |

| Notes to financial statements | 109 |

| > Report of independent | |

| registered public accounting firm | 126 |

| > Other fund information | 127 |

| > Board of trustees and officers addendum | 130 |

| > About the organization | 132 |

On January 4, 2010, Delaware Management Holdings, Inc., and its subsidiaries (collectively known by the marketing name of Delaware Investments) were sold by a subsidiary of Lincoln National Corporation to Macquarie Group Limited, a global provider of banking, financial, advisory, investment and funds management services. Please see your Funds’ prospectus and any supplements thereto for more complete information.

Investments in Optimum Fixed Income Fund, Optimum International Fund, Optimum Large Cap Growth Fund, Optimum Large Cap Value Fund, Optimum Small-Mid Cap Growth Fund, and Optimum Small-Mid Cap Value Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies, and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Funds, the repayment of capital from the Funds, or any particular rate of return.

Unless otherwise noted, the views expressed in this report are as of March 31, 2010, and are subject to change at any time. Holdings are as of the date indicated and subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor.

© 2010 Delaware Distributors, L.P.

All third-party trademarks are the property of their respective owners.

Portfolio management review

Optimum Fixed Income Fund

April 6, 2010

| Performance review (for the year ended March 31, 2010) | |||

| Optimum Fixed Income Fund (Class A shares) | 1-year return | +28.24% | |

| Optimum Fixed Income Fund (Institutional Class shares) | 1-year return | +28.73% | |

| Barclays Capital U.S. Aggregate Index (benchmark) | 1-year return | +7.69% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Fixed Income Fund, please see the table on page 18.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisor

Pacific Investment Management Company LLC (PIMCO)

On April 1, 2010, PIMCO replaced TCW Investment Management (TCW) as a sub-adviser to the Fund. TCW was the Fund’s sub-advisor for the entire year ending March 31, 2010. Please see the Supplement to the Fund’s prospectuses, dated March 23, 2010, for more information.

On the heels of a historically difficult prior fiscal period, the stage was set for a strong “snapback” recovery. Such a recovery came to fruition for the fixed income market (as well as the equity market) early in the fiscal year and was the defining element of the period. For example, investors’ apparent risk aversion seemingly eased within weeks of the start of the period — slowly at first, and more quickly as the year progressed. The robust market performance was significantly aided by the U.S. federal government, which acted aggressively to replace the private capital lost in the preceding year with public capital intended to prop up asset prices.

This aggressive action by the government seemed most evident in the mortgage and asset-backed sectors, which were at the epicenter of the meltdown and saw a defection of investors as security prices plunged in 2008. Programs such as the Term Asset-backed Loan Facility (TALF) and Public-Private Investment Program (PPIP) were fully ramped up during this period, employing government-provided leverage in the consumer asset-backed securities (ABS) and nonagency mortgage-backed securities (MBS) markets, respectively. This was aimed at attracting new investors into these largely abandoned sectors. It generally worked as intended, with asset prices recovering some of the ground lost during the previous year.

The Federal Reserve and U.S. Treasury completed their $1.5 billion agency MBS repurchase program at the end of March 2010. The end of the program was well telegraphed and expected by the market, yet some yields (which move inversely to prices) rose modestly in the last few days of March as the prospective departure of the sector’s largest purchaser did have some effects. Nonetheless, the small increase in yields did little to blunt the overall effectiveness of the program.

Somewhat surprisingly, the market recovery that occurred during the year took place despite economic data that were mixed at best. Unemployment remained near 10% for the entire period. Economic growth turned positive, but was characterized by relatively unsustainable increases in inventories rather than final demand. Home prices were roughly stable through the period as well, with lower-priced homes reaching a floor (thanks in part to the home buyer tax credit enacted by the federal government) while higher-priced homes continued to show modest declines. Softness was also seen across a wide variety of other data including consumer confidence, manufacturing output, consumer spending, and capacity utilization. While there was certainly improvement from the lows of 2008, nothing in the data suggested the kind of rebound seen in fixed income, equities, and most other financial assets.

(continues) 1

Portfolio management review

Optimum Fixed Income Fund

DMC

The portion of Optimum Fixed Income Fund managed by DMC employs a diversified “core plus” investment strategy. This means that DMC seeks to invest the core of its assets under management in U.S. investment grade securities, and then strategically allocates other assets to additional fixed income markets. These additional sectors include U.S. high yield bonds as well as established and emerging international markets.

As the reporting period began, investors’ previously deep level of pessimism shifted to a more optimistic outlook, as many investors rediscovered their appetite for risk. The bond market appeared to anticipate better times ahead as prices rose dramatically on virtually all assets across the risk spectrum. We believe the portion of the Fund managed by DMC was well positioned for the shift in investor sentiment, which contributed to the Fund’s overall outperformance of the benchmark.

Specifically, our overweight allocation to investment grade corporate bonds had relatively positive effects on results. Corporate bonds were among the asset classes previously most affected by the credit crisis, as yields on these securities soared to levels rarely seen before (source: Bloomberg). As credit conditions eased, however, investment grade corporate bonds experienced a massive and sustained rally. Within DMC’s portion of the Fund, security selection was a significant positive across many industries, including banking, basic industry, communications, consumer (both cyclicals and noncyclicals), and technology.

Our exposure to high yield and emerging-market debt, which are not included in the benchmark index, also helped the Fund’s relative performance for the year, as these sectors of the market outperformed. Our emphasis on higher-quality credits within the high yield asset class moderated the relative gains, as market returns were progressively stronger within the lower-quality credit categories.

Though we maintained a limited exposure to the sector, emerging-market bonds generally provided another source of strength for the Fund. Our emerging-market focus during the period was on countries that we believed had good fiscal policies in place prior to the downturn, less-distressed economies, or sufficiently flexible economic stimulus programs. These countries tended to experience more-vigorous economic recoveries. Examples include Indonesia, Brazil, and India, among others.

TCW

The portion of Optimum Fixed Income Fund previously managed by TCW was predominantly invested in a combination of agency and nonagency MBS, both of which posted strong results for the period. Given the extraordinarily difficult conditions that the fixed income markets experienced during the previous fiscal year, we were able to purchase many of these assets at attractive valuations.

Nonagency prime and alt-A (or just above subprime) MBS were the largest contributors to relative returns during the period. These assets were purchased at substantial discounts to par, and often enjoyed significant price appreciation. Further, our allocation to agency MBS also contributed to performance, as prices rose at least in part due to the large government purchase program.

Our overall strategy remained consistent over the course of the period, with an emphasis on nonagency MBS. However, we did implement some minor adjustments as market conditions developed. At the beginning of the period, our nonagency holdings were focused primarily in bonds backed by prime and higher-quality alt-A collateral. As was expected, those sectors were among the first to recover. As prices rose toward the end of 2009 and into 2010, we began to move our portion of the Fund out of those sectors and into lower-priced alt-A and subprime collateral that we believed offered better risk-return characteristics at that time.

2

While there were brief periods within the year that individual sectors underperformed, those periods tended to be short, and bond prices moved overwhelmingly higher across all sectors over the course of the year. Our specific holdings within each sector mattered less than simply investing in each sector and letting the proverbial rising tide lift the boat.

(continues) 3

Portfolio management review

Optimum International Fund

April 6, 2010

| Performance review (for the year ended March 31, 2010) | |||

| Optimum International Fund (Class A shares) | 1-year return | +50.29% | |

| Optimum International Fund (Institutional Class shares) | 1-year return | +50.88% | |

| MSCI EAFE Index (benchmark) (gross) | 1-year return | +55.20% | |

| MSCI EAFE Index (benchmark) (net) | 1-year return | +54.44% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum International Fund, please see the table on page 22.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

BlackRock Advisors, LLC (BlackRock)

Mondrian Investments Partners Limited (Mondrian)

For the fiscal period, the Fund’s benchmark, the MSCI EAFE (Europe, Australasia, Far East) Index, advanced +54.44% (net) — an impressive gain on an absolute basis.

Every EAFE region rose by double digits during the Fund’s fiscal year. The United Kingdom rose by 59.5% as most economic indicators showed improvement in 2009. France rose by 50.8%, underperforming the benchmark, as did Germany and Switzerland, returning 51.4% and 54.0%, respectively.

Australia was up 86.7%, benefiting from strength in its financials and materials sectors, together with the strength of its currency. Singapore advanced impressively, driven by improvements in the external environment along with strength in its well-capitalized banking sector and price increases in its property market.

Japan had the worst performance among Asian countries, advancing by 37.9%. Greece experienced sharp underperformance (up just 24.2%) as the government’s near-term liquidity and longer-term solvency issues led to sovereign debt–related concerns that weighed heavily on the market.

Within broader equity markets, and in much more general terms, markets rose substantially during the period as investors began anticipating a recovery from a recession and financial crisis that have affected economies around the world. After bottoming in early March 2009, stocks experienced a significant rebound as risk appetite recovered from extremely pessimistic levels.

The recovery slowed as the year progressed, as investors began questioning the effects of eventual withdrawals of monetary and fiscal stimulus policies. At the same time, fears grew about the headwinds that massive budget deficits across the developed world could cause going forward.

As often happens after recessions and financial crises, stocks that suffered the most during the downturn dramatically outperformed when markets began to recover. Stocks in the financials and materials sectors were among the strongest examples. Once the financial world appeared to have been saved from implosion and an economic recovery seemed probable, the sector rallied. Materials advanced strongly as well driven by Asian demand. Weaker sectors included the more traditionally defensive sectors such as healthcare, telecommunications, and utilities.

BlackRock

For the Fund’s fiscal year, the Fund’s BlackRock sleeve outperformed the Fund’s benchmark, the MSCI EAFE Index. Stock selection was generally strong during the period, with the most significant contributions coming from holdings in the consumer discretionary and energy sectors. Some of our energy holdings (especially those related to the exploration and production of oil and gas) meaningfully outpaced their industry peers, as the demand outlook improved and capacity cuts helped

4

limit conditions of oversupply. Within the consumer discretionary space, we benefited from positions within consumer services, media, and retailing industries that saw strong returns as economic conditions improved.

From a sector point of view, our positioning was generally positive, especially from an overweight in the materials sector, which benefited from rising commodity prices. Underweights in the more defensive healthcare and utilities sectors also had positive effects. In contrast, our cash position (while small) detracted somewhat from total returns, and our overweight in the energy sector also hurt performance compared to that of the index.

Regionally, performance as measured against the benchmark index was positively influenced by our out-of-benchmark exposures to emerging markets and Canada, which outperformed most developed-market constituents of the MSCI EAFE Index. Our underweight in Japan for most of the period also had a positive effect on relative performance.

Turns in the market typically pose significant difficulties for fundamental managers and lead to wide disparities in relative returns immediately before and immediately after the market’s trough. One of the reasons we were able to navigate this environment more effectively than many of our peers was our recognition of oversold conditions and record-high valuation spreads, even as credit markets had already begun to heal. That meant carefully looking back to cyclical industries and stocks that seemed most severely punished in the downturn. This was based on the notion that such holdings were likely to lead the market recovery while offering the most compelling risk-reward opportunities.

Mondrian

The Fund’s Mondrian sleeve lagged the MSCI EAFE Index for the fiscal year. Being defensive value managers, we would not expect to outperform during such an unusually strong fiscal period.

While the effects of our currency holdings were positive, the effects of market selection and stock selection were negative. Our overweight position in the outperforming Singaporean market had a positive effect on performance relative to the index, as were the zero weightings in Greece and Ireland — two countries that underperformed the broader index. Our overweight position in the underperforming telecommunications services sector was unhelpful, as was the underweight position in the relatively strongly performing materials and financials sectors. The effects of stock selection in the financial sector were, however, supportive to our sleeve’s overall returns.

For the fiscal year, the strongest stocks were in Australia and Asia. They included the Australian conglomerate Wesfarmers (up by slightly more than 130%) and the Hong Kong ports and property company Wharf Holdings (gaining 131.1%).

Wesfarmers is a conglomerate with interests in coal, insurance, fertilizers, and chemicals. It also has the largest do-it-yourself chain in Australia. In 2007, it was transformed by its acquisition of the Coles Group in a deal that was finalized at the end of that year. In 2008, there were concerns that the company would not be able to roll over some of its debt refinancing. This was resolved with an equity issue that left its balance sheet in a very strong position. The share price recovered strongly in 2009, helped by commodity prices that helped the earnings of its coal division. There have also been positive signs of improvement in the Coles businesses, with improved sales and encouraging results from the new supermarkets Coles is rolling out. The company has also announced an expansion of its production of “coking coal,” which is used in the manufacture of other substances such as steel and iron.

Wharf Holdings’ principal activities involve the development and management of investment properties and the operation of container terminals. The steady cash flow from its property and ports businesses has allowed the group to increase the scale of its investments in China, particularly in property development. This is expected to become a significant portion of earnings over the next decade.

(continues) 5

Portfolio management review

Optimum International Fund

Stocks that lagged the benchmark during the Fund’s fiscal year included a number of Japanese stocks such as retailer Seven & I Holdings (up 13.3%), insurance company Tokio Marine Holdings (up 18.7%), and the telecommunications company KDDI (gaining 13.5%). Other relatively underperforming names included Chunghwa Telecom in Taiwan (+11.6%) and France Telecom in France (+13.6%). Hongkong Electric Holdings, another underperformer, rose by just 4.5% during the 12 months ending March 31, 2010.

Chunghwa Telecom is a dominant telecommunications operator in Taiwan and is primarily government owned. It has the largest fixed-line business and is the number one mobile operator in that country. It has a strong balance sheet and strong cash flows that support dividend payments. Despite anemic growth prospects, we believe the strong cash flow, high dividend payout, and low risk profile make the stock attractive, though it has underperformed due to the defensive nature of the company and the broader communications sector.

Seven & I Holdings is the fifth-largest retailer globally with more than 30,000 stores. It is the holding company for a comprehensive retail operation including Ito-Yokado (superstores), 7-Eleven Japan, and 7-Eleven Inc. (which also serves the United States). In common with other Japanese retail operators, the company has suffered under the deflationary environment in Japan, coupled with high levels of competition. With the exception of 7-Eleven Japan, the various businesses have generally achieved low profitability. However, we believe the company can translate the success of 7-Eleven across its other stores.

Going forward, we seek to continue managing our portion of the Fund according to the same style we always have: an active, value-oriented defensive style. We plan to seek out securities that show strong potential for long-term income flows. Dividend yield and future real growth will continue playing a central role in our investment decisions, and we believe the dividend component may likely be a meaningful portion of expected total return over time.

6

Optimum Large Cap Growth Fund

April 6, 2010

| Performance review (for the year ended March 31, 2010) | |||

| Optimum Large Cap Growth Fund (Class A shares) | 1-year return | +52.22% | |

| Optimum Large Cap Growth Fund (Institutional Class shares) | 1-year return | +52.87% | |

| Russell 1000® Growth Index (benchmark) | 1-year return | +49.75% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Large Cap Growth Fund, please see the table on page 24.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Fred Alger Management, Inc. (Alger)

T. Rowe Price Associates, Inc. (T. Rowe Price)

Marsico Capital Management, LLC (Marsico)

Early during the fiscal year, the equity markets began to emerge from the deep losses experienced during calendar year 2008 and in the beginning of 2009. From March 2009 through March 2010, equity performance worldwide was remarkable, amid stronger-than-expected corporate earnings and signs of economic stabilization across the globe. While we believe the recession in the United States largely ended in the third quarter of 2009, a full economic recovery in the U.S. is far from complete. Risks remain, however, including a still notably weak housing market, the possibility of higher interest rates in 2010, and the lingering effects of the recession that continue to engender caution among individual investors and companies.

The Russell 1000 Growth Index gained nearly 50% for the 12-month period ending March 31, 2010, with the more cyclical sectors outperforming traditionally defensive sectors in the improving economy. Financials was by far the top-performing sector within the benchmark index, followed by the industrials, business services, and consumer discretionary sectors. The utilities sector was the worst performer, despite posting double-digit returns, followed by the healthcare and consumer staples sectors. Based on returns by Russell’s capitalization-size and investment-style indices, large-cap value stocks outperformed large-cap growth during the period, and among growth stocks, small-caps outperformed large-caps.

Alger

It was a strong year for stocks. In many cases, our analysts were able to identify companies undergoing “positive dynamic change,” where our fundamental outlook for their revenues, earnings, and cash flow exceeded consensus estimates.

Among the most important absolute contributors to our annual performance were Apple and BE Aerospace. Conversely, detracting from overall results were Cephalon and ITT Educational Services.

Apple was the leading absolute contributor to our portion of the Fund’s performance. The company continued to grow impressive revenues and margins during the period. Sales of Mac computers and iPhones primarily drove revenue growth, and we believe the introduction of the new iPad portable tablet computer should be a catalyst for future growth.

BE Aerospace is the leading manufacturer of commercial aircraft and business jet cabin interior products worldwide. The company’s shares declined sharply in 2008, but as the commercial airline business began to recover in 2009, the company received new orders to refurbish and upgrade the first-class and business-class sections of commercial wide-body aircraft. As a result, the shares were unusually strong performers during the past 12 months ending March 31, 2010, more than tripling in price.

Cephalon is a biopharmaceutical company that engages in the discovery, development, and commercialization of products for central nervous system, inflammatory disease, pain, and oncology therapeutic areas. The shares performed poorly as investors became more concerned

(continues) 7

Portfolio management review

Optimum Large Cap Growth Fund

about the success of the Nuvigil launch (follow-on product to Provigil) because of the likely onset of generic competition. As a result of this prospect, we exited the position.

ITT Educational Services provides accredited, technology-oriented undergraduate and graduate degree programs through its ITT Technical Institutes and Daniel Webster College. The negative impact of the ongoing recession and the continuing uncertainty surrounding government support programs (Pell Grants) caused the shares to underperform and detracted from Fund performance. We continued to hold the stock because we believe that enrollment metrics suggest continued strong demand for the company’s programs.

T. Rowe Price

In keeping with our investment strategy, we sought companies during the period that we thought had an above-average rate of earnings growth and the potential ability to pay increasing dividends through strong cash flow.

Stock selection contributed to our relative performance, while sector weightings generally detracted. The financials, industrials and business services, and telecommunication services sectors were our major detractors relative to the benchmark. The information technology, healthcare, and consumer staples sectors were our leading contributors.

Performance among our holdings in the financial sector, the top-performing sector in the benchmark, was the primary detractor from our relative performance. Shares of Northern Trust declined amid weakness in its wealth management, securities lending, and foreign exchange trading businesses. We like the company’s long-term growth outlook, which we believe should benefit when interest rates rise.

Moody’s, the second-largest credit rating agency, saw its stock decline under the weight of regulatory and legal risks. A low interest rate environment has resulted in increased bond issuances and refinancing, but rising costs have slowed earnings growth at the company. As a result, we exited the position during the period.

The industrials and business services sectors were significant detractors within our portion of the Fund, with results largely driven by Danaher, a manufacturer of tools for various professional, medical, industrial, and consumer markets. Danaher did not fully participate in the recent rally, as the company’s diversified end markets left it less leveraged to economic conditions. The fact that we believe the stock is less sensitive to cyclical conditions is the primary reason we continue to hold it in our portfolio.

Tencent Holdings was a leading contributor to performance within our portion of the Fund. The company, China’s largest internet provider, benefited from growing trends in online gaming and instant-messaging markets. Rapid growth of mobile users has also driven company growth. Shares of Baidu, China’s leading internet search provider with more than 60% of the market, increased significantly after Google announced it was leaving the market. Google refused to censor search results and sustained a cyber attack in January that was traced to China.

Pharmacy benefits manager Express Scripts was also a notable contributor within our portion of the Fund. The company benefited from an increasing demand for generic drugs. We believe that the trend toward mail-order prescriptions as a cost-cutting measure in the healthcare sector should further benefit the company.

Contributor to performance Intuitive Surgical, a maker of robotic surgery systems, has consistently met market expectations in a challenging capital equipment environment. A new system launch and a well-executed commercial strategy led to outstanding results for the firm in 2009.

Marsico

As market conditions improved during the Fund’s fiscal period, we continued to rigorously apply our investment strategy — analyzing the competitive landscape using a

8

top-down macroeconomic perspective while employing fundamental research to identify what we believe are high-quality companies with compelling potential for long-term capital appreciation.

We increased our exposure to the financial sector while decreasing our position in the healthcare sector. Stock selection in the diversified financials and banks industries contributed to our portion of the Fund’s performance during the period. JPMorgan Chase was among our largest individual contributors during the year, as it benefited from a consolidation in the investment banking space and less competition, a trend we believe should continue.

Additionally, stock choices in the materials sector were a source of outperformance. In particular, positions in Dow Chemical and BHP Billiton were notable contributors. Dow Chemical realized significant benefit in the period from its restructuring efforts, while BHP Billiton capitalized on emerging-market demand for natural resources.

Stocks in the healthcare sector were a source of underperformance. Positions in Roche Holding and Schering-Plough, both sold during the period, were the largest individual detractors within our portion of the Fund during the period. Both companies declined apparently due to investor concerns about the strength of their product pipelines.

Throughout the year, our portion of the Fund maintained an overweight position in the materials sector, which hampered performance as this turned out to be one of the weakest performing sectors in the benchmark index.

(continues) 9

Portfolio management review

Optimum Large Cap Value Fund

April 6, 2010

| Performance review (for the year ended March 31, 2010) | |||

| Optimum Large Cap Value Fund (Class A shares) | 1-year return | +49.92% | |

| Optimum Large Cap Value Fund (Institutional Class shares) | 1-year return | +50.47% | |

| Russell 1000® Value Index (benchmark) | 1-year return | +53.56% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Large Cap Value Fund please see the table on page 26.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

TCW Investment Management Company (TCW)

Massachusetts Financial Services Company (MFS)

The massive monetary and fiscal stimulus that mobilized in the fourth quarter of 2008, while much debated, eventually achieved the desired effect of stabilizing the U.S. and global monetary panic. The U.S. economy troughed in the first half of 2009, with gross domestic product declining more than 6% in the first quarter and receding 0.7% in the second quarter (source: U.S. Commerce Department).

While job recovery has been slow, the Bureau of Labor Statistics (BLS) just reported a gain of 162,000 jobs in March. Unemployment has stabilized at 9.7% and the BLS has reported a continuation of strong temporary employment activity with positive statistics since September (temporary employment has traditionally been a harbinger for an employment recovery). The equity markets have thus far sustained China’s credit tightening and the economic travails in Greece. Oil has remained stable with crude prices hovering around $80 a barrel, which has kept energy and gas prices relatively low.

The equity markets experienced one of the best bull markets in history, which began in early March 2009, just shy of the Fund’s fiscal year start. With the exception of October 2009 and January 2010, every month in the fiscal period had positive returns (source: Bloomberg). Both the Russell 1000 Value Index and the S&P 500 Index advanced approximately 50%. In general, lower-quality, lower-market-cap, and higher-beta (high risk) stocks outperformed during this period, as the market rose from multiyear lows.

Improved retail sales data was supported largely by the cash-for-clunkers program for much of summer 2009. However, the latter part of 2009 brought improvements without such overt government support. Several major retailers from across the price spectrum, including Target, TJX (parent company to TJ Maxx, Marshalls, and other discount stores), and luxury retailer Saks Fifth Avenue posted improved sales figures during the fourth quarter. In all, retail sales figures came in above Wall Street expectations in both October and November of 2009. (Source: Dow Jones.)

Additionally, the U.S. manufacturing sector further separated itself from previous lows, posting its seventh consecutive month of growth through February 2010 (as indicated by the Institute for Supply Management).

The first quarter of 2010 began on the heels of a nearly year-long “risk rally” during which both the equity and fixed income markets recovered much of the losses they experienced in 2008. The end of the Fund’s fiscal period demonstrated that investors could potentially achieve solid total returns despite their worries that the rally might fizzle in the new year.

TCW

The portion of the Fund managed by TCW benefited from all sector allocations, with the exception of our overweight in telecommunications, which was the worst-performing sector over the fiscal year. Security selection also contributed to outperformance, with large strides achieved in: materials, including United States Steel, MeadWestvaco, Packaging Corporation

10

of America, and E.I. du Pont de Nemours (DuPont); telecommunications, including Qwest Communications International; and information technology, including Tyco Electronics, KLA-Tencor, and LSI.

Cosmetic company Estée Lauder Companies and semiconductor company KLA-Tencor were completely sold, both realizing approximate gains of 50% from cost. ConocoPhillips was sold from our portion of the Fund, as it met our downside sell discipline and Mattel was sold on the upside as it outperformed relative to the market.

We acted on the attractive prices found in the battered financials sector by adding insurer MBIA and financial services company Morgan Stanley; however, stock selection in financials detracted from the Fund’s performance.

Additionally, as commodity prices fell, there were individual opportunities presented in the energy sector, including exploration and production company Devon Energy, oil service company Baker Hughes, and offshore contract drilling company, Ensco International. Additional initiations included CA and Textron in the information technology and industrials sectors, respectively.

Our underweight in the healthcare and consumer discretionary sectors contributed to our portion of the Fund’s performance. Our overweight in the poorly performing telecommunications sector detracted from performance as did our underweight in the outperforming industrials sector.

The two leading contributors to our section of the Fund’s performance over the fiscal year were Tyco Electronics in the technology sector and hospital company Tenet Healthcare, both of which posted impressive returns. Tyco Electronics outperformed its peers due to better execution and exposure to the rebuilding automotive sector. Tenet Healthcare benefited from a multiyear program meant to increase the quality of care while reducing costs and paying down debt.

The two worst-performing stocks affecting performance were integrated energy company Chevron, which is the second-largest energy company, and Regal Entertainment Group. Chevron’s return lagged the peer group and although it outperformed its largest competitor, Exxon Mobil, it could not keep pace with its smaller competitors. The cash-flow-rich movie theater owner and operator Regal Entertainment, typically a defensive play, lagged the more cyclically tied consumer discretionary stocks.

MFS

During the fiscal period, security selection and, to a lesser extent, an underweighted position in the financial services sector, dampened returns versus the Russell 1000 Value Index within our portion of the Fund. Our positioning in Bank of America detracted from relative performance. We added this stock to the Fund in late 2009, as our confidence in its balance sheet, normalized earnings, and future credit trends had improved from earlier in the year. Bank of America is a large holding within the benchmark index and while we’ve continued to increase our exposure, we remain underweighted.

An overweight position in Bank of New York Mellon, which underperformed the benchmark during the reporting period, hindered relative performance. We believe that shares in Bank of New York Mellon struggled — improvements in its revenue growth profile and its exposure to an improving credit environment was not as significant as other areas of financials, which attracted the interest of investors and performed better. In our opinion, the low interest rate environment is putting pressure on the company’s revenue growth, leading to below-normal earnings in the current period. However, we believe the company has an attractive mix of businesses, generates very good returns over time, has a good balance sheet, and trades for an attractive valuation; therefore, we continue to hold the stock.

Stock selection in the industrial goods and services sector also detracted from relative performance within our portion of the Fund, particularly our position in global security company Lockheed Martin. Lockheed Martin has a sustainable, durable business, a strong balance

(continues) 11

Portfolio management review

Optimum Large Cap Value Fund

sheet, and generates significant free cash flow. Its underperformance last year did not change our positive long-term view of the company and we continue to hold the name as our largest position, given our view of its high-quality characteristics and attractive valuation.

Our cash position was another detractor from relative performance within our portion of the Fund. The Fund holds cash to buy new holdings and provide liquidity. In a period when equity markets rose, as measured by the Fund’s benchmark index, holding cash hurt performance when compared against the benchmark, which had no cash position.

A combination of stock selection and an underweight position in the energy sector aided relative performance. Our underweight position in Exxon Mobil helped as this stock underperformed the benchmark during the fiscal period. Exxon Mobil, as well as integrated oil stocks as a group, underperformed the market significantly during the period as investors appeared to have rotated into less-defensive areas.

An underweighted position in the utilities and communications sector was another contributor, including our positioning in Verizon Communications, which bolstered relative performance. We sold Verizon during the quarter — its shares lagged the benchmark as we believe investors gravitated toward lower-quality, more-leveraged businesses, due in part to a growing optimism about the potential U.S. economic recovery.

MetLife was also a contributor to our portion of the Fund. A dramatic recovery in the credit markets in the spring of 2009 led to substantial upward revisions in the valuations for a number of MetLife’s investments. With a valuation below book value, the company’s share price reacted positively to these developments.

During the reporting period, our currency exposure was also a contributor to relative performance. All MFS investment decisions are driven by the fundamentals of each individual opportunity, and as such, it is common for us to have different currency exposure than that of the benchmark.

12

Optimum Small-Mid Cap Growth Fund

April 6, 2010

| Performance review (for the year ended March 31, 2010) | |||

| Optimum Small-Mid Cap Growth Fund (Class A shares) | 1-year return | +64.94% | |

| Optimum Small-Mid Cap Growth Fund (Institutional Class shares) | 1-year return | +65.36% | |

| Russell 2500™ Growth Index (benchmark) | 1-year return | +63.92% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Small-Mid Cap Growth Fund, please see the table on page 28.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

For complete, annualized performance for Optimum Small-Mid Cap Growth Fund, please see the table on page 28.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Wellington Management Company, LLP (Wellington)

Columbia Wanger Asset Management, L.P. (Columbia WAM)

After continuing their nosedive early in 2009, stocks bounced off their lows in March 2009 and managed one of the most impressive rallies in history. U.S. equities across all styles and capitalizations extended the remarkable rally as credit market conditions improved, corporate earnings were generally better than expected, and the economy showed signs that it was emerging from the longest and deepest recession since the Great Depression.

Substantial efforts to stimulate global economies over the fiscal year helped to avert a worst-case scenario. Among the most prominent measures in the United States was the Federal Reserve’s continued purchases of mortgage-backed securities issued by Fannie Mae, Freddie Mac, and Ginnie Mae. This helped keep mortgage rates near multidecade lows. The prospects for continuing low rates and healthier corporate earnings seemed to stimulate investors’ appetites for riskier assets, including stocks.

Government intervention — together with easy year-on-year comparisons, lean inventories and staffing, and muted expectations — led companies to post better-than-anticipated earnings. But the attendant seismic shift in sentiment from the extreme anxiety that ushered stocks to multiyear lows in March 2009, to the ebullience that propelled equities to close the fiscal year decisively higher, proved a significant navigational challenge.

While it was a remarkable period for U.S. equities, concerns remain that an extended period of extraordinary monetary and fiscal stimulus may have very severe implications for future inflation as the economy recovers.

Wellington

We adhered to our investment approach, even as company fundamentals seemingly took a back seat to macroeconomic forces in driving stock performance during much of this period. We kept our research resources focused on identifying companies able to sustain superior revenue and earnings growth by virtue of their advantaged market position. We also remained conservative in the assumptions we used to estimate companies’ future earnings and cash flows, as well as in the valuation metrics we employed to set target prices. Against this backdrop, our portion of the Fund experienced positive absolute and relative returns.

Top individual contributors for the period included technology hardware companies Seagate Technology and Jabil Circuit. Seagate, a manufacturer and distributor of disk drives, fixed a weak balance sheet earlier in the period. This removed significant risk to the company’s viability and allowed investors to focus on strong disk drive unit demand and the company’s significant cost-saving initiatives. Jabil Circuit, one of the largest electronic manufacturing services providers, benefited from improving conditions in several key end markets and a healthy relationship with Research In Motion.

Relative detractors included Corinthian Colleges and Advance Auto Parts. Corinthian Colleges is a postsecondary education services company with

(continues) 13

Portfolio management review

Optimum Small-Mid Cap Growth Fund

operations in the U.S. and Canada. Concerns about higher default rates among student borrowers and regulatory pressures weighed on the stock. As a result, we eliminated the position. Auto parts retailer Advance Auto Parts experienced sluggish sales growth, which caused the stock to lag the market. Concerns that spending on growth initiatives would create headwinds for the firm’s turnaround plans led us to sell the stock near the end of the period.

Columbia WAM

We believe the smallest and riskiest stocks tend to jump the most off a deep market bottom as many of these companies are hit the hardest during a bear market. With this in mind, we increased our investment in several of these types of stocks because we believed the potential gains were well worth the additional risk. We believe this approach was the primary driver of outperformance versus the benchmark in our portion of the Fund.

Energy stocks were strong performers during the period, particularly those of oil services providers. Stocks of these companies surged as oil prices rebounded sharply. Underwater well head manufacturer FMC Technologies and offshore drilling contractor Atwood Oceanics were both strong contributors to performance. Both companies are in long-lead-time businesses with large backlogs. The prior sag in oil prices didn’t hurt these stocks very much, and with oil prices rising, offshore drilling is likely to remain strong.

Telecom services stocks were also strong performers for the year. Crown Castle International, an owner of communications towers, was a key contributor to overall return within our portion of the Fund. We believe Crown Castle’s share price was overly depressed due to leverage on the balance sheet. The company was able to raise capital at reasonable rates to repair its balance sheet and therefore have solid revenue growth.

ITT Educational Services was a primary detractor from performance within our portion of the Fund. We have some concerns about the headwinds facing private education companies, which have been caused by regulatory issues. That being said, ITT’s education business has been particularly strong, with fourth-quarter revenues up 34% from the prior year and new student enrollment up 31%. We believe ITT’s private education business model is a strong one.

ESCO Technologies, a maker of electronic meter readers, was down on weaker-than-expected sales. Although the company lagged during the period, we believe its long-term outlook remains bright due to the growing interest in its meter-reading products from several international electric utilities. Additionally, we believe the potential for new U.S. contracts remains strong.

Myriad Genetics, a biotech company involved in genetic diagnostic testing, declined as the sluggish economy caused a sharp deceleration in its revenue growth. We sold our position because we were concerned that its core breast cancer diagnostic market was becoming saturated.

14

Optimum Small-Mid Cap Value Fund

April 6, 2010

| Performance review (for the year ended March 31, 2010) | |||

| Optimum Small-Mid Cap Value Fund (Class A shares) | 1-year return | +76.98% | |

| Optimum Small-Mid Cap Value Fund (Institutional Class shares) | 1-year return | +77.56% | |

| Russell 2500™ Value Index (benchmark) | 1-year return | +67.17% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Small-Mid Cap Value Fund please see the table on page 30.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

For complete, annualized performance for Optimum Small-Mid Cap Value Fund please see the table on page 30.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

The Delafield Group, a division of Tocqueville Asset Management L.P. (Tocqueville)

The Killen Group, Inc. (Killen)

Westwood Management Corp. (Westwood)

The market made an astonishing recovery during the Fund’s fiscal year. Early in the reporting period, investors responded favorably to efforts by governments world-wide to stimulate the global economy, and as fears of a systemic failure of the world banking system dissipated and liquidity slowly improved, attention turned toward signs of recovery.

The rally began in March 2009 (just shy of the Fund’s fiscal year start) and carried into the spring and summer of 2009, producing impressive double-digit gains that were led by lower-quality, high-beta (high-risk) stocks. As the year progressed, continuing signs of economic recovery, better-than-expected corporate earnings growth, and improved balance sheets buoyed investor optimism, which led to a solid gain for the equity markets in the fourth quarter of 2009.

By this time, however, many investors seemed to lose their appetite for risk, as they began to price in the potential for less liquidity and higher interest rates in 2010. Specifically, investors began to rotate out of lower-quality, smaller-cap securities into higher-quality, larger-cap securities with sustainable earnings growth potential.

January 2010 began with a selloff in the broad market, as investors digested gains from 2009 and seemed to view sovereign debt problems in Europe and potentially slower economic growth in China as reasons for caution. In February, however, investor sentiment turned as global economic data continued to be supportive of a broad-based global recovery, and the Federal Reserve looked to maintain an accommodative interest rate policy — from zero to 0.25% — for an extended period. In addition, the U.S. Congress passed a healthcare reform bill in March 2010 that did not include a “public option” for healthcare coverage, removing uncertainty about the effect the bill could have on the market.

As of this writing, investors seem to continue to anticipate a smooth recovery, though unemployment in the United States continues to hover just below 10% and is only expected to improve at a modest pace, according to consensus estimates.

Tocqueville

Until Sept. 28, 2009, the Delafield Asset Management, a division of Reich & Tang Asset Management, LLC served as a sub-adviser to Optimum Small-Mid Cap Value Fund. On Sept. 28, 2009, the portfolio management team and certain support staff of Delafield joined Tocqueville Asset Management, L.P. Please see the supplement to the Fund’s prospectuses, dated Sept. 25, 2009, for more information.

We have constructed our portion of the Fund using a bottom-up approach; that is, we focus intently on valuation and analyze cash flows of individual companies in an attempt to invest at prices that we believe undervalue the underlying franchise. This is the strategy that we consistently employ — it also helped drive performance during the Fund’s fiscal year.

(continues) 15

Portfolio management review

Optimum Small-Mid Cap Value Fund

While we generally do not set sector or industry allocation targets for our portion of the Fund, we found several attractive investment opportunities in the materials sector and our relative overweight in that area benefited performance. We were also heavily weighted toward the industrials sector, which rebounded after being among the hardest-hit sectors in the previous fiscal year. We continued to avoid the energy and financial sectors, which hurt performance relative to the benchmark index because these sectors realized dramatic gains during the reporting period.

Flextronics International and Ashland were the leading contributors to performance in our portion of the Fund. Flextronics, with nearly $31 billion in 2009 revenue, is a leading provider of electronic manufacturing services. The company’s shares rebounded strongly during the year as substantial cost reductions contributed to improved performance, and liquidity fears eased. Ashland is a diversified company with specialty chemical, motor oil (Valvoline brand), and material distribution businesses. Its shares rose sharply as profitability strengthened and balance sheet worries diminished.

None of the stocks in our portion of the Fund turned in negative performance for the year. However, our investments in Dun & Bradstreet and Pharmaceutical Product Development generated below-market returns for the year and contributed only modestly to performance. We continue to maintain our Dun & Bradstreet position; however, we exited our Pharmaceutical Product Development position toward the end of the fiscal year because the turnaround we had envisioned did not occur.

Killen

Our contrarian style led us to become more aggressive heading into 2009, and while this did not help performance in the Fund’s previous fiscal year, it contributed to strong gains in this year’s sharp rebound. Our bottom-up philosophy prevented us from becoming overly defensive during the stock market’s weakness, and we were able to purchase solid companies at what we viewed as attractive prices. This enabled us to record attractive absolute and relative returns for the reporting period.

Our investment approach remains the same during both weak and strong markets: We emphasize companies that we believe exhibit a sound long-term operating strategy, strong management, and a solid financial structure, and that are selling at a deep discount to what we believe to be the true value of their business.

Given the broad market strength for the fiscal year, virtually every sector contributed to performance in our sleeve of the Fund. Areas of particular strength included information technology and energy. Both sectors struggled as the economic backdrop weakened in 2008 and early 2009, but when results proved not as bad as previously feared (and in some cases were actually quite healthy on an absolute basis), most of our stocks in these sectors experienced healthy gains.

The weakest sectors during the period were financials and utilities. Financials lagged while still being additive on an absolute basis. Despite low market valuations, the results of most companies in the sector have been strong and should support higher prices in the longer term. Utilities, a small piece of our portion of the Fund, lagged on an absolute basis as demand remained constrained due to economic weakness.

Two stocks that contributed to the Fund’s performance during the fiscal year were Dress Barn and Rudolph Technologies.

We purchased shares of retailer Dress Barn during the economic downturn in the fall of 2008. Dress Barn’s business held up quite well during the recession and the company had the financial ability to complete an attractive acquisition (Tween Brands) during the reporting period. As the economy rebounded, the combined entity performed above expectations and the stock responded in kind. Based on stock price, we began selling our Dress Barn position in the third quarter of the fiscal year. By the end of the fiscal year, we had eliminated the position from our portion of the Fund.

Rudolph Technologies is a semiconductor capital equipment provider. Its business dropped precipitously as the economy weakened and capital expenditures were

16

slashed. We owned the stock prior to the downturn and purchased additional shares as it fell. Our patience was validated as the demand for the company’s products rebounded, as did its stock price. We continue to hold a full position.

Two examples of stocks that underperformed were LaBranche and Granite Construction.

LaBranche is one of the largest specialist market-maker firms on the New York Stock Exchange. The company has been adjusting its business model for several years, trying to adapt to the new era dominated by electronic trading. Ultimately, the transition was unsuccessful as the company was unable to consistently generate profits. We sold the position during the year.

Granite Construction, a civil engineering contractor, has had to contend with state-budget shortfalls and increased competition from smaller contractors. We continue to believe the company should do well in the longer term despite the stock’s underperformance during the period. We maintained the position.

Westwood

With the rescue and stimulus packages instituted by the Fed and U.S. government in late 2008 and early 2009, investor sentiment quickly turned, and the worst-performing stocks of the 12 months prior to the reporting period became the best-performing stocks over the ensuing six months.

The portion of the Fund we manage produced strong absolute performance over the period but lagged the performance of the benchmark Russell 2500 Value Index, primarily because of the rally of high-beta, low-quality stocks that began in March 2009.

Because we do not change our investment approach, our portion of the Fund may underperform in environments in which growth-oriented strategies are in favor, or when high-risk investments perform strongly. However, we focus on high-quality companies with strong fundamental characteristics and visible earnings prospects. The low-quality bias during the period was most pronounced in the consumer discretionary, technology, and real estate investment trust (REIT) sectors.

With regard to specific sectors and holdings, performance relative to the benchmark was aided by our underweight in the relatively poor-performing utilities sector and by our security selection in the materials and processing sector. Utilities generally underperformed because investors sought out more economically sensitive securities. Our holdings in the materials and processing sector benefited from leverage to global commodity demand.

Relative performance was hindered by security selection in the technology sector and by security selection and an underweight in the consumer discretionary sector. These sectors were among the most negatively affected by the low-quality, high-beta rally. Subsequently, they had a large effect on the relative performance of our portion of the Fund because of our focus on high-quality stocks.

Among the best-performing securities in our portion of the Fund for the period were consumer products firm Tupperware Brands, which reported strong sales in Asian markets, and commodity and specialty chemical producer Eastman Chemical, which posted multiple quarterly earnings surprises and benefited from the global recovery.

Our worst-performing securities included computer hardware firm Novell, whose management disappointed investors with an unplanned acquisition. Part of our investment thesis was that the company would return cash to shareholders; however, when the acquisition was announced it became clear management had other ideas for deploying cash. We exited the position during the period.

Regional bank People’s United Financial was another poor performer. The stock declined due to growing concerns about potential losses in the company’s bank loan portfolios. In our opinion, the company has one of the best capitalization levels of all the regional banks in our universe, and we believe investor concerns about credit quality are inappropriate. We continue to hold the stock.

17

Performance summary

Optimum Fixed Income Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.

You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The Optimum Fixed Income Fund prospectus contains this and other important information about the investment company. Please request a prospectus through your financial advisor or by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Read the prospectus carefully before you invest or send money.

| Fund performance | ||||

| Average annual total returns | ||||

| Through March 31, 2010 | 1 year | 3 years | 5 years | Lifetime |

| Class A (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | +28.24% | +7.05% | +5.98% | +5.90% |

| Including sales charge | +22.39% | +5.41% | +5.01% | +5.17% |

| Class B (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | +27.51% | +6.34% | +5.29% | +5.22% |

| Including sales charge | +23.51% | +5.68% | +5.04% | +5.22% |

| Class C (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | +27.34% | +6.34% | +5.29% | +5.22% |

| Including sales charge | +26.34% | +6.34% | +5.29% | +5.22% |

| Institutional Class (Est. Aug. 1, 2003) | +28.73% | +7.40% | +6.34% | +6.26% |

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted in the following paragraphs.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Expense limitations were in effect for all classes during the periods shown in the Fund performance chart and in the “Performance of a $10,000 Investment” chart. Note that all charts and graphs referred to in the “Performance summary” section of this report are found on pages 18 through 19. Performance would have been lower had the expense limitation not been in effect.

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 4.50%, and have an annual distribution and service fee of up to 0.35% of average daily net assets.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges. Please see the most recent prospectus for additional information on Class B purchases and sales charges. As described in the prospectus, Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held.

Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Institutional Class shares are sold without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund performance” table and the “Performance of a $10,000 Investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has voluntarily agreed to reimburse certain expenses and/or waive investment advisory fees in order to prevent total annual fund operating expenses from exceeding 1.00% of the Fund’s average daily net assets from Aug. 1, 2009 until the voluntary cap is discontinued. Please see the most recent prospectus for additional information on these fee waivers and/or reimbursements.

18

| Fund expense ratios | Class A | Class B | Class C | Institutional Class | |||

| Total annual operating expenses | |||||||

| (without fee waivers) | 1.47% | 2.12% | 2.12% | 1.12% | |||

| Net expenses | |||||||

| (including fee waivers, if any) | 1.35% | 2.00% | 2.00% | 1.00% | |||

| Type of waiver | Voluntary | Voluntary | Voluntary | Voluntary |

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds.

If and when we invest in forward foreign currency contracts or use other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

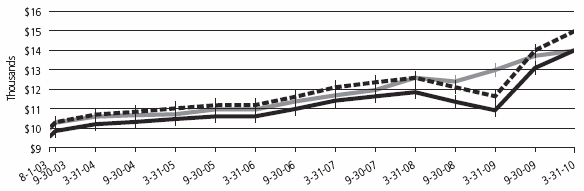

Performance of a $10,000 Investment

Aug. 1, 2003 (Fund’s inception), through March 31, 2010

Aug. 1, 2003 (Fund’s inception), through March 31, 2010

| Starting value (Aug. 1, 2003) | Ending value (Mar. 31, 2010) | |||||

| Optimum Fixed Income Fund — Institutional Class shares | $10,000 | $14,991 | ||||

| Barclays Capital U.S. Aggregate Index | $10,000 | $14,028 | ||||

| Optimum Fixed Income Fund — Class A shares | $9,550 | $13,995 | ||||

The chart assumes $10,000 invested in the Fund on Aug. 1, 2003, and includes the effect of a 4.50% front-end sales charge for Class A shares and the reinvestment of all distributions. Please note additional details on these fees in the “Performance summary” section of this report, which includes pages 18 through 19.

The chart also assumes $10,000 invested in the Barclays Capital U.S. Aggregate Index as of Aug. 1, 2003. The Barclays Capital U.S. Aggregate Index is a broad composite of more than 8,500 securities that tracks the investment grade domestic bond market.

(continues) 19

Performance summary

Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Stock symbols and CUSIP numbers | ||

| Nasdaq symbols | CUSIPs | |

| Class A | OAFIX | 246118681 |

| Class B | OBFIX | 246118673 |

| Class C | OCFIX | 246118665 |

| Institutional Class | OIFIX | 246118657 |

20

Performance summary

Optimum International Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.

You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The Optimum International Fund prospectus contains this and other important information about the investment company. Please request a prospectus through your financial advisor or by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Read the prospectus carefully before you invest or send money.

| Fund performance | ||||

| Average annual total returns | ||||

| Through March 31, 2010 | 1 year | 3 years | 5 years | Lifetime |

| Class A (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | +50.29% | -8.33% | +2.90% | +7.34% |

| Including sales charge | +41.60% | -10.14% | +1.69% | +6.38% |

| Class B (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | +49.42% | -8.93% | +2.24% | +6.64% |

| Including sales charge | +45.42% | -9.67% | +1.82% | +6.64% |

| Class C (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | +49.20% | -8.95% | +2.22% | +6.64% |

| Including sales charge | +48.20% | -8.95% | +2.22% | +6.64% |

| Institutional Class (Est. Aug. 1, 2003) | +50.88% | -8.01% | +3.25% | +7.71% |

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted in the following paragraphs.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Expense limitations were in effect for all classes during the periods shown in the Fund performance chart and in the “Performance of a $10,000 Investment” chart. Note that all charts and graphs referred to in the “Performance summary” section of this report are found on pages 22 through 23. Performance would have been lower had the expense limitation not been in effect.

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 5.75%, and have an annual distribution and service fee of up to 0.35% of average daily net assets.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges. Please see the most recent prospectus for additional information on Class B purchases and sales charges. As described in the prospectus, Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held.

Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Institutional Class shares are sold without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund performance” table and the “Performance of a $10,000 Investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has voluntarily agreed to reimburse certain expenses and/or waive investment advisory fees in order to prevent total annual fund operating expenses from exceeding 1.40% of the Fund’s average daily net assets from Aug. 1, 2009 until the voluntary cap is discontinued. Please see the most recent prospectus for additional information on these fee waivers and/or reimbursements.

22

| Fund expense ratios | Class A | Class B | Class C | Institutional Class | |||

| Total annual operating expenses | |||||||

| (without fee waivers) | 1.86% | 2.51% | 2.51% | 1.51% | |||

| Net expenses | |||||||

| (including fee waivers, if any) | 1.75% | 2.40% | 2.40% | 1.40% | |||

| Type of waiver | Voluntary | Voluntary | Voluntary | Voluntary |

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

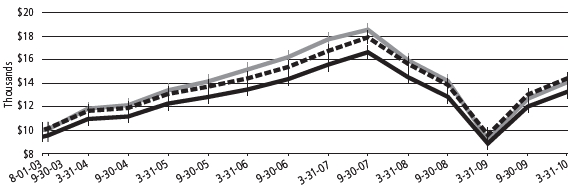

Performance of a $10,000 Investment

Aug. 1, 2003 (Fund’s inception), through March 31, 2010

Aug. 1, 2003 (Fund’s inception), through March 31, 2010

| Starting value (Aug. 1, 2003) | Ending value (Mar. 31, 2010) | |||||

| MSCI EAFE Index (gross) | $10,000 | $18,349 | ||||

| MSCI EAFE Index (net) | $10,000 | $17,834 | ||||

| Optimum International Fund — Institutional Class shares | $10,000 | $16,404 | ||||

| Optimum International Fund — Class A shares | $9,425 | $15,111 | ||||

The chart assumes $10,000 invested in the Fund on Aug. 1, 2003, and includes the effect of a 5.75% front-end sales charge for Class A share and the reinvestment of all distributions. Please note additional details on these fees in the “Performance summary” section of this report, which includes pages 22 through 23.

The chart also assumes $10,000 invested in the MSCI EAFE Index as of Aug. 1, 2003. The MSCI EAFE Index measures equity market performance across developed market countries in Europe, Australasia, and the Far East. Index “net” return approximates the minimum possible dividend reinvestment, after deduction of withholding tax at the highest possible rate. Index “gross” return reflects the maximum possible dividend reinvestment.

Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Stock symbols and CUSIP numbers | ||

| Nasdaq symbols | CUSIPs | |

| Class A | OAIEX | 246118731 |

| Class B | OBIEX | 246118723 |

| Class C | OCIEX | 246118715 |

| Institutional Class | OIIEX | 246118699 |

(continues) 23

Performance summary

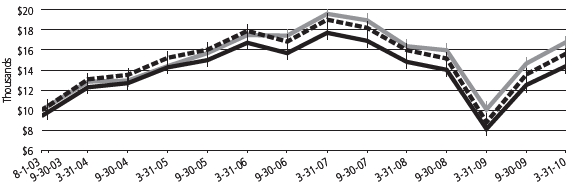

Optimum Large Cap Growth Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.