UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED ANNUAL SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-21410

The Weitz Funds

(Exact name of registrant as specified in charter)

Suite 200

1125 South 103 Street

Omaha, NE 68124-1071

(Address of principal executive offices) (Zip code)

Wallace R. Weitz & Company

The Weitz Funds

Suite 200

1125 South 103 Street

Omaha, NE 68124-1071

(Name and address of agent for service)

Registrant’s telephone number, including area code: 402-391-1980

Date of fiscal year end: March 31

Date of reporting period: March 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Report to Stockholders.

WEITZ INVESTMENT PHILOSOPHY

Over the 25+ year history of Weitz Funds, we have seen many changes. Advancements in technology combined with economic, political and global events have continued to shape investors’ thoughts and actions.

Our mission has remained constant— we have an unwavering commitment to our shareholders and a focus on finding strong, well-managed companies priced significantly below their true business value.

We “eat our own cooking.”

We believe in putting our money where our mouth is. All of our employees and trustees have significant personal investments in our “family” of funds. This does not guarantee that the Funds will go up, but it does mean that we win or lose together and that shareholders definitely have our full attention.

We are patient, long-term investors.

When we analyze potential equity investments, we think about the business behind the stock. We buy shares only when we believe they are selling at a large discount to the company’s underlying business value. Ideally, the business value rises over time, and the stock price follows. This often allows us to hold the stock for many years.

Knowing what you don’t know is important in all aspects of life, but it is crucial in investing.

We think our odds of investment success are much higher when we invest in securities of companies we understand and where we may have an edge over other investors. As a result, our portfolios are not diversified among all the various sectors of the economy. Instead, we expect to have a deeper knowledge and understanding of the industries and companies in which we do invest. Our experienced research team has a broad “circle of competence,” and we believe in staying within it.

We worry about permanent loss of capital—not price volatility.

Our Funds are designed for long-term shareholders. We believe concentrating our portfolios in the most attractive investment ideas, although it may cause short-term price volatility, is the best way to earn consistent returns over the long term.

We believe in being flexible and using common sense.

We are often contrarian and do not pay attention to benchmarks when making investment decisions. We also believe that cash is sometimes the most attractive investment.

Our goal is to earn good absolute investment returns over long

periods of time without exposing our clients’ and our own

capital to undue risk.

2 Weitz Funds

TABLE OF CONTENTS

| | Performance Summary | 4 | |

| | | | |

| | Letter to Shareholders | 5 | |

| | | | |

| | Analyst Corner | 8 | |

| | | | |

| | Value Fund | 9 | |

| | | | |

| | Partners Value Fund | 13 | |

| | | | |

| | Partners III Opportunity Fund | 18 | |

| | | | |

| | Research Fund | 23 | |

| | | | |

| | Hickory Fund | 27 | |

| | | | |

| | Balanced Fund | 31 | |

| | | | |

| | Short-Intermediate Income Fund | 36 | |

| | | | |

| | Nebraska Tax-Free Income Fund | 44 | |

| | | | |

| | Government Money Market Fund | 50 | |

| | | | |

| | Financial Statements | 52 | |

| | | | |

| | Notes to Financial Statements | 63 | |

| | | | |

| | Report of Independent Registered Public Accounting Firm | 76 | |

| | | | |

| | Actual and Hypothetical Expenses for Comparison Purposes | 77 | |

| | | | |

| | Other Information | 78 | |

| | | | |

| | Information About the Trustees and Officers | 80 | |

| | | | |

| | Index Descriptions | 82 | |

| | Coming Soon – Redesigned weitzfunds.com We are pleased to announce that our website is currently undergoing a major redesign. We are updating our look and adding new functionality to enhance your online experience. Visit weitzfunds.com soon. |

| | | | |

| | The management of Weitz Funds has chosen paper for the 80 page body of this financial report from a paper manufacturer certified under the Sustainable Forestry Initiative standard. | | |

Portfolio composition is subject to change at any time and references to specific securities, industries, and sectors referenced in this report are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. See the Schedules of Investments included in this report for the percent of assets in each of the Funds invested in particular industries or sectors.

weitzfunds.com 3

PERFORMANCE SUMMARY

MARCH 31, 2012

| | | | | | | Total Returns | | | Average Annual Total Returns | |

| | | | Inception | | | | | | | | | | | | | | | | | | | | | | | | | | Since |

| Fund Name | | | Date | | 3 Mos. | | 1 Year | | 3 Year | | 5 Year | | 10 Year | | 15 Year | | 20 Year | | 25 Year | | Inception |

| Value | | | 5/09/86 | | | 9.5 | % | | 9.9 | % | | 25.2 | % | | -1.0 | % | | 3.3 | % | | 8.8 | % | | 10.3 | % | | 10.4 | % | | 10.4 | % |

| Russell 1000 | | | | | | | | | | | | 24.0 | | | 2.2 | | | 4.5 | | | | | | | | | | | | N/A | |

| Russell 1000 Value | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | N/A | |

Partners Value(a) | | | 6/01/83 | | | 10.5 | | | 5.4 | | | 25.5 | | | 1.3 | | | 4.4 | | | 9.7 | | | 11.3 | | | 11.0 | | | 12.4 | |

Partners III Opportunity(a) | | | 6/01/83 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 13.2 | |

Investor Class(b) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 13.2 | |

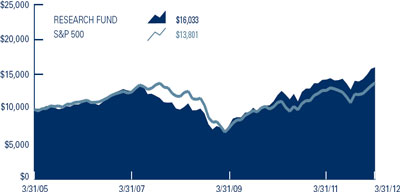

Research(a)(c) | | | 4/01/05 | | | 11.9 | | | 12.3 | | | 28.0 | | | 4.9 | | | — | | | — | | | — | | | — | | | 7.0 | |

| Russell 3000 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | — | |

| Russell 3000 Value | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | — | |

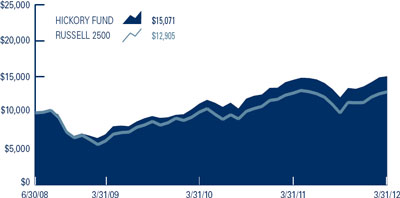

| Hickory | | | 4/01/93 | | | 10.3 | | | 3.4 | | | 29.2 | | | 1.6 | | | 5.1 | | | 8.4 | | | — | | | — | | | 10.2 | |

| Russell 2500 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 9.9 | |

| Russell 2500 Value | | | | | | | | | | | | | | | | | | | | | | | | — | | | | | | 10.5 | |

| S&P 500 | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | — | |

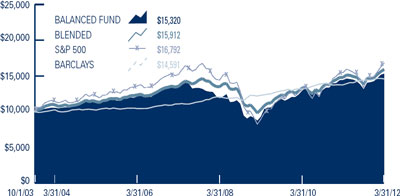

| Balanced | | | 10/01/03 | | | 7.5 | | | 6.2 | | | 18.2 | | | 2.5 | | | — | | | — | | | — | | | — | | | 5.1 | |

| Blended Index | | | | | | | | | | | | | | | | | | — | | | — | | | — | | | | | | 5.6 | |

| Short-Intermediate Income | | | 12/23/88 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 6.0 | |

Investor Class(b) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 6.0 | |

| Barclays Intermediate Credit | | | | | | 0.6 | | | | | | | | | | | | | | | | | | | | | | | | 6.7 | |

NebraskaTax-Free Income(a) | | | 10/01/85 | | | 0.5 | | | 6.1 | | | 4.3 | | | 3.9 | | | 4.1 | | | 4.4 | | | 4.8 | | | 5.0 | | | 5.4 | |

| Barclays 5-Year Muni. Bond | | | | | | | | | | | | | | | | | | | | | | | | | | | — | | | — | |

These performance numbers reflect the deduction of each Fund’s annual operating expenses. Annual operating expenses for each Fund, as stated in the most recent Prospectus, and expressed as a percentage of each Fund’s net assets, are: Value, 1.21%; Partners Value, 1.21%; Partners III Opportunity -Institutional Class, 1.53%; Partners III Opportunity - Investor Class, 1.74% (estimated gross); Research, 1.81% (estimated gross); Hickory, 1.28%; Balanced, 1.15%; Short-Intermediate Income - Institutional Class, 0.65%; Short-Intermediate Income - Investor Class, 0.84% (estimated gross); and Nebraska Tax-Free Income, 0.74%. The returns assume redemption at the end of each period and reinvestment of dividends. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses by the Adviser. This information represents past performance and past performance does not guarantee future results. The investment return and the principal value of an investment in any of the Funds will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance may be higher or lower than the performance data quoted above. Performance data current to the most recent month end may be obtained at www.weitzfunds.com/performance/monthly.asp.

Index performance is hypothetical and is shown for illustrative purposes only. See page 82 for a description of all indices.

| (a) | Performance of the Partners Value and Partners III Opportunity Funds is measured from June 1, 1983, the inception of Weitz Partners II Limited Partnership (“Partners II”) and Weitz Partners III Limited Partnership (“Partners III”), respectively. Performance of the Research Fund is measured from April 1, 2005, the inception of Weitz Research Fund, L.P. (“Research L.P.”). Performance of the Nebraska Tax-Free Income Fund is measured from October 1, 1985, the inception of Weitz Income Partners Limited Partnership (“Income Partners”). On the last business day of December 1993, 2005, 2006 and 2010, the Partners Value, Partners III Opportunity, Nebraska Tax-Free Income and Research Funds (the “Funds”) succeeded to substantially all of the assets of Partners II, Partners III, Income Partners and Research L.P. (the “Partnerships”), respectively. The investment objectives, policies and restrictions of the Funds are materially equivalent to those of the respective Partnerships and the Partnerships were managed at all times with full investment authority by Wallace R. Weitz & Company. The performance information includes performance for the period before the Funds became investment companies registered with the Securities and Exchange Commission. During these periods, none of the Partnerships were registered under the Investment Company Act of 1940 and therefore were not subject to certain investment or other restrictions or requirements imposed by the 1940 Act or the Internal Revenue Code. If any of the Partnerships had been registered under the 1940 Act during these periods, the respective Partnerships’ performance might have been adversely affected. |

| (b) | Investor Class shares first became available for sale on August 1, 2011. For performance prior to that date, this table includes the actual performance of the Fund’s Institutional Class (and uses the actual expenses of the Fund’s Institutional Class, for such period of time), without any adjustments. For any such period of time, the performance of the Fund’s Investor Class would have been substantially similar to, yet lower than, the performance of the Fund’s Institutional Class, because the shares of both classes are invested in the same portfolio of securities, but the classes bear different expenses. |

| (c) | Starting January 1, 2011, these performance numbers reflect the deduction of the Research Fund’s actual operating expenses. For periods of time prior to January 1, 2011, the performance numbers reflect the deduction of annual pro forma operating expenses of 1.50%. Annual operating expenses for the Research Fund, as stated in the Research Fund’s Prospectus, are 1.81% (estimated gross) and 0.91% (net) of the Fund’s net assets. The investment adviser has agreed, in writing, to limit the total annual fund operating expenses (excluding taxes, interest, brokerage commissions, and acquired fund fees and expenses) to 0.90% of the Fund’s average daily net assets through July 31, 2012. |

| N/A | Indicates information is not available. |

LETTER TO SHAREHOLDERS

APRIL 3, 2012

Dear Fellow Shareholder:

The first calendar quarter of 2012 was a very good one for the stock market. Our stock funds earned total returns ranging from +7.8% (Partners III) to +11.9% (Research). The market has rallied very strongly from its lows of last October, and we have become more cautious as the average price to value of the stocks in our portfolios has risen from roughly 60% to 75-80%.

When our stocks approach full value, we trim our positions. As we sold into rallies, our cash levels rose from 10-15% last October to 20-25% at quarter end. In a strong market, cash dampens returns, and we trailed our benchmarks in the quarter. We would prefer to beat all the market indexes all the time, but we are content to celebrate the good absolute returns and wait patiently for our chance to redeploy our cash reserves.

The short table below shows results for our stock funds for the past 3 months and 12 months. The table on the page opposite this letter gives more comprehensive information for each of the funds and their respective benchmarks. As usual, I would suggest that the longer-term results are more meaningful.

| | | | Period Ended 3/31/2012 |

| | | | Quarter | | Fiscal Year |

| Value | | | 9.5 | % | | 9.9 | % |

| Partners Value | | | 10.5 | | | 5.4 | |

| Partners III – | | | | | | | |

| Institutional Class | | | 7.8 | | | 4.9 | |

| Research | | | 11.9 | | | 12.3 | |

| Hickory | | | 10.3 | | | 3.4 | |

| S&P 500 | | | 12.6 | | | 8.5 | |

The Balanced Fund turned in excellent results for the quarter (+7.5%). The Balanced Fund invests in both stocks and bonds. A “neutral” allocation would be 60% stocks and 40% bonds. Brad has shifted Balanced to a more defensive posture and still generated a return that would be pretty good for a full year.

Our bond funds remain very defensive. Short-Intermediate has eschewed the “fear trade” in Treasuries and has kept quality high and duration short. Yet Tom managed a +1.5% return for the quarter for the Institutional Class. Going forward, as we have said every quarter for some time, the environment for bond investing is very negative. We will remain very cautious and while we believe we can deliver positive returns over time, bond investors should keep their expectations low.

As usual, there are several pages of detail on each Fund later in this report. We encourage shareholders to read these sections for each of the Funds they own.

“Uncertainty” is a Permanent Condition

The U.S. economy continues to recover slowly. The problems of excess housing supply and unserviceable mortgage debt are slowly being resolved. Companies have been slow to rehire during the recovery as they have found ways to increase productivity among their remaining workers. Depressed tax receipts have led to austerity measures at the state and local levels while highly stimulative national fiscal and monetary policies seem to be losing their effectiveness. Investors are impatient for growth but also concerned about future inflation.

Europe is struggling with similar issues of excess private and public sector debt and over-built real estate markets. Problems are distributed unevenly among European countries and the Euro Zone’s hybrid governance structure—a common currency but separate, and often conflicting, fiscal policies—makes it very difficult to devise good solutions.

Asian and Latin American “emerging markets” are generally growing much faster than U.S. and European markets. A number of our U.S. based companies are earning a growing share of their profits in emerging markets. Dynamic changes in these rapidly growing markets inspire both hope and anxiety among economists and investors.

Global economic cross-currents always make it difficult to make broad generalizations and sweeping predictions. Investors hate “uncertainty” and both individuals and professional investors are anxious for definitive answers. The financial press confuses the issue, as usual, with its cacophony of pronouncements based on isolated data points.

Uncertainty will always be part of investing. However, sensible and creative management teams are aware of the political and economic trends that affect their businesses. They can develop strategies to avoid serious disruptions and can sometimes take advantage of the situation. For example, Wells Fargo has made bulk purchases of European bank loans secured by U.S. assets at bargain prices. As conditions change, companies with global businesses make adjustments as to where they source raw materials and sell finished product. As citizens, we have serious concerns about the state of the country and the world, but as investors, we feel reasonably confident that we own companies that can generate good returns on our investments under most conditions.

A Short Look at History

Human nature leads investors to focus on the recent past when making current investment decisions. The mortgage crisis and severe bear market are fresh in investors’ minds. Many are fearful—especially if they had a similar bad experience with the technology stock

weitzfunds.com 5

bubble and 2000-2002 bear market. They observe that bonds performed better than stocks over the past 10-12 years and have shifted hundreds of billions of dollars from stock mutual funds to bond funds.

To put the current period in better perspective, it might be helpful to look at a much longer period of stock market history. Between 1932 and 2000, the S&P 500 index rose from about 5 to 1550. This period can be divided into four periods of 16-17 years each during which the S&P alternately (a) moved erratically sideways and (b) rose sharply in a major bull market. This period saw war and depression, deflation and inflation. We would assert, though, that GDP growth and the growth in corporate earning power generally rose over the entire period in a path that was much less volatile than the stock market.

There are many reasons for the differences between the “facts” of gradually increasing company earnings and the “opinions” that drive wildly volatile stock prices. We believe the most powerful single factor is investor psychology. Unfortunately for investors, they always seem to get more enthusiastic about buying stocks as prices move higher. Conversely, when prices fall, making good businesses cheaper to own, they tend to become fearful and sell more shares.

Each of the four periods provides a similar lesson, but we will focus on the most recent. As the S&P 500 index rose from about 100 in 1982 to 1550 in 2000 (+1450%), company earnings roughly tripled, but the price-earnings multiple (P/E) placed on S&P stocks more than quadrupled from a low of 7 times to a high of 31 times. In short, the companies’ values increased, but their stocks’ valuations increased even more.

This illustrates the core concept of our investment approach—stock prices fluctuate widely around a company’s business value. Ideally, we buy at a discount to business value, the business value grows, and we sell at or near business value. Easier said than done, but success depends on measuring value and being price-sensitive in our buying and selling—NOT on waiting for ideal macroeconomic conditions or an absence of “uncertainty.”

Back to the Future

So where are we now? The market peaked in March of 2000 (with the S&P 500 at about 1550) as tech stock valuations reached absurd levels. During the intervening twelve years, many of the growth favorites of the day, both tech-oriented and others, have experienced strong business growth while their stock prices have languished. Microsoft, Dell and Wal-Mart have each roughly tripled earnings per share, but their stock prices have nothing to show for it. Value rose, but valuation (the price people were willing to pay for those earnings) shrank.

Five years ago, the S&P 500 peaked again around 1550. This time the most extreme over-valuations were to be found in housing and mortgage finance. It turned out that we had over-built the housing stock—borrowing demand from future years—and over-borrowed to finance the houses. Demand for houses, construction materials and furnishings evaporated and triggered a serious recession. Liquidity issues in the financial sector triggered by the devaluation of mortgage-related assets compounded the problem.

The revaluation process for stocks in general that started in 2000 may have about run its course. The deleveraging of personal and bank balance sheets may have many more years to run (although we would guess that the worst is over). It would be too much of a coincidence to expect that the current sideways market which is twelve years old would end in exactly 4-5 years to conform to the 16-17 year pattern of the last eighty years, but it may very well continue for some time.

A few more years of subdued stock market behavior does not have to be a terrible thing for investors. It would be nice to enjoy the double-digit annual returns of the 1990’s—and from the right valuation base—that can happen again. In the meantime, over the past twelve years, while the S&P produced a total return of 1.4% per year, Value, Partners Value and Partners III have earned average annual total returns of 4.6%, 5.4%, and 10.6%, respectively. These are not sexy numbers, but thanks to compounding, they mean shareholder capital has grown by 71%, 87% and 234% in the Funds vs. 18% for the S&P 500.

An Improving Value Equation

In spite of the muted recovery and the various headwinds affecting global economic growth, we are still finding interesting investments for our Funds. Volatility of prices of existing positions allows us to buy extra shares on dips and earn trading profits when the shares rebound. This is not our primary focus, but it can add some incremental return in a sideways market. The more interesting additions are companies our analysts uncover and that appear to be cheap for temporary reasons.

FLIR Systems (FLIR—$25) makes infrared and thermal imaging equipment for military and commercial use. It is a leader in a secularly expanding industry and earns high returns on capital. It has a history of thoughtful capital deployment and sells at a 35% discount to our current estimate of its business value ($39). Fears of cutbacks in defense spending (which we think are over-stated for FLIR’s products) and underestimation of the prospects for FLIR’s commercial business caused the stock to decline sharply last summer and to tread water ever since. The combination of future earnings per share growth (which we expect to average at least 15% per year) and a higher

6 Weitz Funds

valuation for those earnings could make FLIR an excellent long-term holding for several of our Funds.

Range Resources (RRC—$58) is a domestic natural gas exploration and production company. Its “crown jewel” is in the Southwest Pennsylvania portion of the Marcellus field. New techniques for producing oil and gas from shale have led to a several-fold increase in the U.S.’s estimated gas reserves and a temporary glut in available gas across the country. As a result, gas prices have plunged to 10+ year lows and gas producers’ stocks are out of favor. Range has a very low cost of production, is increasing its natural gas liquids and oil production, and can continue to reinvest at attractive returns, even at today’s very low gas prices. For a variety of both supply-and demand-related reasons, we would expect gas prices to rise from today’s depressed $2.15 per mcf in future years. Change happens slowly for both producers and consumers of energy, but over the next 5-10 years, we believe Range can produce very good returns for us. (We also own Southwestern Energy (SWN—$31), a stock with a similar investment thesis.)

Americans and American businesses are pretty resilient. We think there are reasons to be hopeful that the current period of consolidation and revaluation in the stock market in general will give way to a more positive market environment.

| (1) | Housing starts in the U.S. fell by 73% from 2005 (2.073 million) to 2009 (0.553 million) and were only 0.611 million in 2011. Starts had been greater than one million each year for the past 50 years, until 2008. But, household formation continues, some of the housing stock needs to be replaced each year, and personal interest in home ownership is alive and well. Eventually, the number of homes being built (and furnished) will rise significantly. Aside from the direct impact on the economy and employment, stabilizing of home prices should have a positive impact on consumer confidence; |

| | |

| (2) | A stronger economy should revive tax receipts at all levels. State and local governments should be able to relax the austerity measures that have been a drag on the economy. At the Federal level, higher tax receipts and lower demands on safety net programs should decrease the quantity of new government bonds that must be sold (leaving more capital for investment in stocks). We could hope that Congress addresses the longer-term issues of funding Medicare and Medicaid, but that would be an unexpected bonus; |

| | |

| (3) | Some years ago, the price of natural gas fluctuated wildly as supplies were just slightly too big in a warm winter and just slightly too small in a cold one. Many industry observers believed that the supply of gas was in secular decline in the U.S. Now, thanks to new (albeit controversial) technology, gas is being produced from sources previously considered inaccessible. Some think we now have a 100-year supply of natural gas and that it could bring the U.S. a measure of energy independence. There are problems of production, distribution and conversion of facilities to use gas, but most individuals and thousands of companies will be direct beneficiaries of this cheap and abundant fuel; |

| | |

| (4) | Finally, as investors’ memories of recession and collapsing home prices fade, we may find that some of the hundreds of billions (trillions?) of dollars that had been “hiding” in U.S. Treasuries and other “safe” assets may find their way back into the stock market. The incremental demand could make a significant difference in stock valuations. |

Great! But When?

We are optimistic about the long-term outlook for our stock portfolios. Human nature does not seem to change over time and the reasons that assets are sometimes mis-priced are rooted in human behavior. We still need to do our part in analyzing and measuring value and in exercising the patience and discipline to take advantage of investment opportunities—that is, keeping our own “human natures” under control.

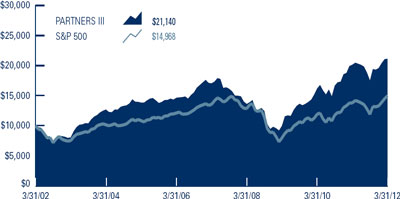

The 28+ year history of our Firm has spanned most of the 1982-2000 bull market and all of the 2000-March 2012 period of consolidation. The two Funds which (including their predecessor partnerships) span our entire history, Partners Value and Partners III, have returned 12.4% and 13.2% per year, respectively, on an annualized basis (after deducting fees and expenses) vs. 10.5% for the S&P 500. These 2% and 3% margins sound insignificant, but on a cumulative basis they make a big difference. Ten thousand dollars invested on June 1, 1983 would have grown to $178,496 in the S&P 500, $295,119 if invested in Partners Value, and $361,967 if invested in Partners III-Institutional Class.

We live in an uncertain world, but having learned some lessons and having added several bright young people to our investment team over the years, we are hopeful that we can build on this record.

Sincerely,

| | | |

| | |

| Wallace R. Weitz | | Bradley P. Hinton |

| wally@weitzfunds.com | | brad@weitzfunds.com |

weitzfunds.com 7

ANALYST CORNER

A PERSPECTIVE ON AON

By Barton Hooper, CFA

Aon is one of the world’s largest commercial insurance and reinsurance brokers (60% of revenue) as well as a leader in human resources consulting (40% of revenue). The company has added significant scale in recent years with the acquisition of reinsurance brokerage Benfield in 2008 and Hewitt Associates in 2010. We believe both industries in which Aon competes have attractive structural characteristics. The placement of insurance is a necessity for any business and is very complicated; this circumstance allows insurance brokers to act as a toll booth for this vital product. An insurance brokerage requires little capital and involves no underwriting risk. Aon is one of only three brokers who can place risk on a global basis.

Businesses, both large and small, need expert advice in designing and implementing comprehensive HR programs. The human resources consulting industry addresses the many complexities businesses face in setting benefit, retirement and incentive compensation policies. Multinational companies have additional challenges in setting policies and programs that adhere to the varying legal and regulatory requirements of different countries. Similar to its insurance brokerage operation, Aon is one of the few global-scale industry participants.

Several Catalysts

Since the arrival of CEO Greg Case in 2005, Aon has substantially improved its operating profit margin as it shed unprofitable businesses, cut costs and improved productivity. However, there is still room for Aon’s margins to improve as it has publicly stated that its insurance brokerage unit can deliver margins of 25% (22% in 2011) and achieve margins of 22% (18%) in the HR consulting business. While we count on more conservative margins in our estimate of business value, we are confident that Aon has the capability to deliver on its goals. The company has provided several examples of margin enhancing programs such as the Global Risk Insight Platform (GRIP) in brokerage and the Aon Hewitt integration plan in the human resources segment.

In addition, Aon and other insurance brokers will benefit if short-term interest rates rise above today’s minuscule levels. The company collects fiduciary interest income on client funds held prior to remittance to insurers for in force policies. While Aon does not hold these funds very long, there is a significant volume of this “float” that is material at reasonable interest levels.

Aon recently moved its place of incorporation to the United Kingdom from the United States which will provide its senior management team more direct access to the globally important London insurance placement market. The move should also result in a lower corporate tax rate and greater capital flexibility with respect to cash generated from its overseas operations. Aon estimates that the move immediately freed up $300 million of capital held internationally that it can deploy for buybacks, dividends or acquisitions.

Valuation and Margin of Safety

Aon generates significant cash flow but the company’s per share earnings are optically obscured due to significant non-cash intangible amortization expenses generated from the Benfield and Hewitt acquisitions. We do not believe this accounting amortization reflects a charge for future reinvestment and therefore Aon’s cash generating capabilities are undervalued. With a price of just over $49, Aon trades for approximately 11x our estimate of 2012 cash earnings. Our estimate of intrinsic value is above $70 and as such we believe the company’s shares represent an attractive investment for our shareholders.

| |

| Barton Hooper, CFA, joined Weitz in 2007. He graduated from the University of Missouri and previously spent four years as a research analyst at Oak Value Capital Management and Trilogy Capital Management. Barton has been a CFA charterholder since 1999. |

| |

8 Weitz Funds

VALUE FUND

PORTFOLIO MANAGERS’ DISCUSSION & ANALYSIS

Co-Portfolio Managers:

Wallace R. Weitz, CFA; Bradley P. Hinton, CFA; & David A. Perkins, CFA

The Value Fund returned +9.5% in the first calendar quarter, compared to a +12.6% gain for the S&P 500 and a +12.9% gain for the Russell 1000. Wells Fargo, Microsoft and Comcast were the three largest positive contributors to performance during the quarter, each generating total returns of approximately 25%. Wells benefitted from improving investor sentiment around the U.S. economy, a relatively clean bill of health from the Federal Reserve’s so called “stress test,” and the beginning of a much-anticipated boost in capital returns to shareholders. Long-time holding Microsoft continued to see relatively strong business adoption of its Windows 7 platform, along with anticipation of a strong 2012 product line (including the upcoming launch of Windows 8). Comcast announced very strong fourth quarter results in mid-February. Positive trends in basic video subscriber losses continued with the company reporting its lowest rate of attrition in 5 years, while broadband, phone and advertising continued to show good growth. Management also meaningfully boosted the company’s dividend and announced a new $6.5 billion share repurchase authorization. The two largest detractors from first quarter performance were two of our newest holdings – Hewlett-Packard and Range Resources (which we discuss in more detail below).

For the fiscal year ended March 31, 2012, the Fund increased +9.9% compared to an +8.5% gain for the S&P 500 and a +7.9% return for the Russell 1000. Microsoft, Valeant Pharmaceuticals, Wells Fargo and Tyco International were key full year performance drivers, each chipping in roughly a full percentage point to solid fiscal 2012 returns. We are pleased Microsoft’s stock is beginning to receive some past-due credit for the operating results it has generated over the past couple of years. While most of the company’s $52B cash hoard is held outside the United States (and thus taxable if brought back to the U.S.), we would happily cheer any move to unlock this value on behalf of shareholders. Valeant rebounded nicely following an unwarranted selloff last August. We continue to believe its shares are undervalued and anticipate further value creation via future acquisitions and thoughtful capital deployment. Finally, Tyco International closed our fiscal year on a high note proposing a value-enhancing combination of its Flow Control segment with similarly focused industrial Pentair.

First quarter portfolio activity was relatively light. We closed a successful multi-year investment in ConocoPhillips near our estimate of intrinsic value and redeployed the proceeds into independent natural gas producer Range Resources (ticker: RRC). We have admired Range and its culture for some time. Abnormally mild winter weather across much of the U.S. pushed natural gas prices – and investor sentiment – to fresh lows during the first quarter, giving us an opportunity to pick up shares of the company at a significant discount. We believe Range is worth in excess of $90 per share assuming domestic natural gas prices eventually return to $4/mcf and oil prices remain above $70 per barrel (and oil prices are at $100+ today). For context, many industry experts believe the marginal cost of supply for natural gas is significantly higher than $4. We are not banking on it given continued advancements in technology and the proclivity of producers to operate at or below cash costs. Regardless, Range’s core assets in the Marcellus shale and Mississippi Lime formation generate attractive returns on investment even at today’s depressed gas prices. As a result, management can grow the company’s net asset value with internally generated cash flows in an environment when most domestic gas producers are forced to retrench.

As of quarter end, residual cash stood at 21% of Fund net assets, relatively unchanged versus three months ago. As we have written in the past, our cash position is simply a reflection of our perception of the present opportunity set -the fewer the bargains, the higher our reserves, and vice versa. While our fully-researched “on deck” list includes a significant number of larger company ideas, our valuation discipline has more recently kept us on the sidelines awaiting greater margins of safety. Borderline investments in the name of activity are the kinds of opportunity cost we seek to avoid. Our goal, as always, is to remain patient, fair-minded, and focused in our pursuit of above-average long-term returns.

The Value Fund invests in our best larger company ideas. The Fund’s weighted average market cap is approximately $60 billion, reflecting its mix of large-cap and mega-cap stocks. The Fund remains relatively concentrated with its top twenty holdings representing approximately two-thirds of net assets.

| | New and Eliminated Securities for Quarter Ended March 31, 2012 | |

| New Purchases ($mil) | | | | | Eliminations ($mil) | | | | |

| Range Resources | | | $ | 22.0 | | ConocoPhillips | | | $ | 14.9 | |

weitzfunds.com 9

VALUE FUND

PERFORMANCE • (UNAUDITED)

| | | | Total Returns | | | | | | Average Annual Total Returns | |

| | | | 3 Mos. | | 1 Year | | 3 Year | | 5 Year | | 10 Year | | 15 Year | | 20 Year | | 25 Year |

| Value | | | 9.5 | % | | 9.9 | % | | 25.2 | % | | -1.0 | % | | 3.3 | % | | 8.8 | % | | 10.3 | % | | 10.4 | % |

| S&P 500 | | | 12.6 | | | 8.5 | | | 23.4 | | | 2.0 | | | 4.1 | | | 6.1 | | | 8.6 | | | 8.9 | |

| Russell 1000 | | | 12.9 | | | 7.9 | | | 24.0 | | | 2.2 | | | 4.5 | | | 6.4 | | | 8.8 | | | 9.1 | |

| Russell 1000 Value | | | 11.1 | | | 4.8 | | | 22.8 | | | -0.8 | | | 4.6 | | | 6.8 | | | 9.4 | | | 9.3 | |

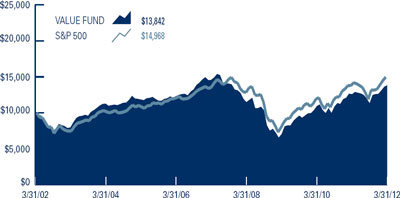

Growth of $10,000

This chart depicts the change in the value of a $10,000 investment in the Value Fund for the period March 31 2002 through March 31, 2012, as compared with the growth of the Standard & Poor’s 500 Index during the same period. Index performance is hypothetical and is shown for illustrative purposes only.

| | | | Value | | | S&P 500 | | | Relative | |

| Year | | | (1) | | | (2) | | | Results (1)-(2) | |

| 1986 (5/9/86) | | | 3.5 | % | | 4.1 | % | | -0.6 | % |

| 1987 | | | -0.5 | | | 5.1 | | | -5.6 | |

| 1988 | | | 16.4 | | | 16.6 | | | -0.2 | |

| 1989 | | | 22.1 | | | 31.7 | | | -9.6 | |

| 1990 | | | -5.2 | | | -3.1 | | | -2.1 | |

| 1991 | | | 27.6 | | | 30.5 | | | -2.9 | |

| 1992 | | | 13.6 | | | 7.6 | | | 6.0 | |

| 1993 | | | 20.0 | | | 10.1 | | | 9.9 | |

| 1994 | | | -9.8 | | | 1.3 | | | -11.1 | |

| 1995 | | | 38.4 | | | 37.6 | | | 0.8 | |

| 1996 | | | 18.7 | | | 23.0 | | | -4.3 | |

| 1997 | | | 38.9 | | | 33.4 | | | 5.5 | |

| 1998 | | | 28.9 | | | 28.6 | | | 0.3 | |

| 1999 | | | 21.0 | | | 21.0 | | | 0.0 | |

| 2000 | | | 19.6 | | | -9.1 | | | 28.7 | |

| 2001 | | | 0.2 | | | -11.9 | | | 12.1 | |

| 2002 | | | -17.1 | | | -22.1 | | | 5.0 | |

| 2003 | | | 28.7 | | | 28.7 | | | 0.0 | |

| 2004 | | | 15.7 | | | 10.9 | | | 4.8 | |

| 2005 | | | -2.8 | | | 4.9 | | | -7.7 | |

| 2006 | | | 21.8 | | | 15.8 | | | 6.0 | |

| 2007 | | | -10.3 | | | 5.5 | | | -15.8 | |

| 2008 | | | -40.7 | | | -37.0 | | | -3.7 | |

| 2009 | | | 27.6 | | | 26.5 | | | 1.1 | |

| 2010 | | | 19.9 | | | 15.1 | | | 4.8 | |

| 2011 | | | 6.1 | | | 2.1 | | | 4.0 | |

| 2012 (3/31/12) | | | 9.5 | | | 12.6 | | | -3.1 | |

| Since Inception: | | | | | | | | | | |

| Cumulative Return | | | 1,183.6 | | | 974.8 | | | 208.8 | |

| Avg. Annual Return | | | 10.4 | | | 9.6 | | | 0.8 | |

These performance numbers reflect the deduction of the Fund’s annual operating expenses which as stated in its most recent Prospectus are 1.21% of the Fund’s net assets. The returns assume redemption at the end of each period and reinvestment of dividends. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses by the Adviser. This information represents past performance and past performance does not guarantee future results. The investment return and the principal value of an investment in this Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data quoted. Performance data current to the most recent month-end may be obtained at www.weitzfunds.com/performance/monthly.asp.

See page 4 for additional performance disclosures. See page 82 for a description of all indices.

Performance information does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

10 Weitz Funds

VALUE FUND

PORTFOLIO PROFILE • (UNAUDITED)

| Top Ten Stocks | |

| Berkshire Hathaway, Inc. - CL B | | | 4.7 | % |

| Wells Fargo & Co. | | | 4.3 | |

| Aon Corp. | | | 4.1 | |

| Google, Inc. - CL A | | | 4.1 | |

| Valeant Pharmaceuticals International, Inc. | | | 4.0 | |

| Tyco International Ltd. | | | 3.7 | |

| Comcast Corp. - CL A Special | | | 3.5 | |

| Texas Instruments, Inc. | | | 3.5 | |

| United Parcel Service, Inc. - CL B | | | 3.2 | |

| Hewlett-Packard Co. | | | 3.2 | |

| % of Net Assets | | | 38.3 | % |

| Industry Sectors |

| Information Technology | | | 17.7 | % |

| Consumer Discretionary | | | 17.0 | |

| Financials | | | 13.1 | |

| Consumer Staples | | | 8.9 | |

| Industrials | | | 8.4 | |

| Materials | | | 5.2 | |

| Energy | | | 4.9 | |

| Health Care | | | 4.0 | |

| Short-Term Securities/Other | | | 20.8 | |

| Net Assets | | | 100.0 | % |

| Top Performers for Quarter Ended March 31, 2012 |

| | | | QTD Return | | Average Weight | | Contribution to |

| Security Name | | | of Security | | in Portfolio | | Fund Performance |

| Wells Fargo & Co. | | | 24.7 | % | | 4.4 | % | | 1.01 | % |

| Microsoft Corp. | | | 25.1 | | | 3.8 | | | 0.97 | |

| Comcast Corp. - CL A Special | | | 25.3 | | | 3.2 | | | 0.74 | |

| Tyco International Ltd. | | | 20.9 | | | 3.4 | | | 0.68 | |

| Liberty Global, Inc. - Series C | | | 21.2 | | | 3.1 | | | 0.66 | |

Contributions to Fund performance are based on actual daily holdings. Securities may have been bought or sold during the quarter.

Source: FactSet Portfolio Analytics

| Bottom Performers for Quarter Ended March 31, 2012 | |

| | | | QTD Return | | Average Weight | | Contribution to |

| Security Name | | | of Security | | in Portfolio | | Fund Performance |

| Hewlett-Packard Co. | | | (7.0 | )% | | 3.3 | % | | (0.25 | )% |

| Range Resources Corp. | | | (6.1 | ) | | 0.6 | | | (0.16 | ) |

| Google, Inc. - CL A | | | (0.7 | ) | | 4.0 | | | (0.07 | ) |

| Southwestern Energy Co. | | | (4.2 | ) | | 2.1 | | | (0.04 | ) |

Contributions to Fund performance are based on actual daily holdings. Securities may have been bought or sold during the quarter.

Source: FactSet Portfolio Analytics

weitzfunds.com 11

VALUE FUND

SCHEDULE OF INVESTMENTS • MARCH 31, 2012

| COMMON STOCKS — 79.2% | | | Shares | | Value | |

| Information Technology — 17.7% | | | | | | | |

| Computers & Peripherals — 6.0% | | | | | | | |

| Hewlett-Packard Co. | | | 1,350,000 | | $ | 32,170,500 | |

| Dell, Inc.* | | | 1,700,000 | | | 28,220,000 | |

| | | | | | | 60,390,500 | |

| Internet Software & Services — 4.1% | | | | | | | |

| Google, Inc. - CL A* | | | 65,000 | | | 41,680,600 | |

| Semiconductors — 3.5% | | | | | | | |

| Texas Instruments, Inc. | | | 1,050,000 | | | 35,290,500 | |

| Software — 2.8% | | | | | | | |

| Microsoft Corp. | | | 900,000 | | | 29,025,000 | |

| IT Services — 1.3% | | | | | | | |

| Accenture plc - CL A | | | 200,000 | | | 12,900,000 | |

| | | | | | | 179,286,600 | |

| Consumer Discretionary — 17.0% | | | | | | | |

| Cable & Satellite — 6.3% | | | | | | | |

| Comcast Corp. - CL A Special | | | 1,200,000 | | | 35,412,000 | |

| Liberty Global, Inc. - Series C* | | | 600,000 | | | 28,734,000 | |

| | | | | | | 64,146,000 | |

| Multiline Retail — 3.1% | | | | | | | |

| Target Corp. | | | 530,000 | | | 30,883,100 | |

| Internet & Catalog Retail — 3.0% | | | | | | | |

| Liberty Interactive Corp. - Series A* | | | 1,600,000 | | | 30,544,000 | |

| Advertising — 2.9% | | | | | | | |

| Omnicom Group, Inc. | | | 575,000 | | | 29,123,750 | |

| Movies and Entertainment — 1.7% | | | | | | | |

| The Walt Disney Co. | | | 400,000 | | | 17,512,000 | |

| | | | | | | 172,208,850 | |

| Financials — 13.1% | | | | | | | |

| Property & Casualty Insurance — 4.7% | | | | | | | |

| Berkshire Hathaway, Inc. - CL B* | | | 590,000 | | | 47,878,500 | |

| Commercial Banks — 4.3% | | | | | | | |

| Wells Fargo & Co. | | | 1,275,000 | | | 43,528,500 | |

| Insurance Brokers — 4.1% | | | | | | | |

| Aon Corp. | | | 850,000 | | | 41,701,000 | |

| | | | | | | 133,108,000 | |

| Consumer Staples — 8.9% | | | | | | | |

| Beverages — 4.5% | | | | | | | |

| Anheuser-Busch InBev SA/NV - | | | | | | | |

| Sponsored ADR | | | 400,000 | | | 29,088,000 | |

| Diageo plc - Sponsored ADR | | | 175,000 | | | 16,887,500 | |

| | | | | | | 45,975,500 | |

| Food & Staples Retailing — 4.4% | | | | | | | |

| CVS Caremark Corp. | | | 580,000 | | | 25,984,000 | |

| Wal-Mart Stores, Inc. | | | 300,000 | | | 18,360,000 | |

| | | | | | | 44,344,000 | |

| | | | | | | 90,319,500 | |

| | | | Principal | | | |

| | | | amount | | | |

| | | | or shares | | Value | |

| Industrials — 8.4% | | | | | | | |

| Industrial Conglomerates — 3.7% | | | | | | | |

| Tyco International Ltd. | | | 660,000 | | $ | 37,078,800 | |

| Air Freight & Logistics — 3.2% | | | | | | | |

| United Parcel Service, Inc. - CL B | | | 402,500 | | | 32,489,800 | |

| Aerospace & Defense — 1.5% | | | | | | | |

| Lockheed Martin Corp. | | | 170,000 | | | 15,276,200 | |

| | | | | | | 84,844,800 | |

| Materials — 5.2% | | | | | | | |

| Construction Materials — 3.1% | | | | | | | |

| Martin Marietta Materials, Inc. | | | 360,000 | | | 30,826,800 | |

| Industrial Gases — 1.4% | | | | | | | |

| Praxair, Inc. | | | 125,000 | | | 14,330,000 | |

| Fertilizers & Agricultural Chemicals — 0.7% | | | | | | | |

| The Mosaic Co. | | | 125,000 | | | 6,911,250 | |

| | | | | | | 52,068,050 | |

| Energy — 4.9% | | | | | | | |

| Oil & Gas Exploration & Production — 4.9% | | | | | | | |

| Southwestern Energy Co.* | | | 675,000 | | | 20,655,000 | |

| Range Resources Corp. | | | 350,000 | | | 20,349,000 | |

| Apache Corp. | | | 80,000 | | | 8,035,200 | |

| | | | | | | 49,039,200 | |

| Health Care — 4.0% | | | | | | | |

| Pharmaceuticals — 4.0% | | | | | | | |

| Valeant Pharmaceuticals International, Inc.* | | | 750,000 | | | 40,267,500 | |

| Other — 0.0% | | | | | | | |

| Adelphia Recovery Trust, | | | | | | | |

Series ACC-7* # | | | 3,535,000 | | | — | |

| Total Common Stocks | | | | | | | |

| (Cost $603,351,202) | | | | | | 801,142,500 | |

| SHORT-TERM SECURITIES — 21.3% | | | | | | | |

| Wells Fargo Advantage Government Money Market Fund - | | | | | | | |

Institutional Class 0.01%(a) | | | 5,432,596 | | | 5,432,596 | |

| U.S. Treasury Bills, 0.01% to 0.09%, | | | | | | | |

4/19/12 to 5/31/12(b) | | $ | 210,000,000 | | | 209,990,530 | |

| Total Short-Term Securities | | | | | | | |

| (Cost $215,425,736) | | | | | | 215,423,126 | |

| Total Investments in Securities | | | | | | | |

| (Cost $818,776,938) | | | | | | 1,016,565,626 | |

| Other Liabilities in Excess of Other Assets — (0.5%) | | | | | | (4,894,202 | ) |

| Net Assets — 100.0% | | | | | $ | 1,011,671,424 | |

| Net Asset Value Per Share | | | | | $ | 32.98 | |

| * | Non-income producing |

| # | Illiquid and/or restricted security that has been fair valued. |

| (a) | Rate presented represents the annualized 7-day yield at March 31, 2012. |

| (b) | Interest rates presented represent the yield to maturity at the date of purchase. |

| | The accompanying notes form an integral part of these financial statements. |

12 Weitz Funds

PARTNERS VALUE FUND

PORTFOLIO MANAGERS’ DISCUSSION & ANALYSIS

Co-Portfolio Managers:

Wallace R. Weitz, CFA & Bradley P. Hinton, CFA

The Partners Value Fund returned +10.5% in the first calendar quarter, compared to a +12.6% return for the S&P 500 and a +12.9% return for the Russell 3000. Stock gains were broad based in the quarter, and our companies on the whole have been doing well. Our cable providers (Comcast +25%, Liberty Global +21%), material producers (Eagle Materials +35%, Martin Marietta Materials +14%) and retailers (Liberty Interactive +18%, Target +14%) paced the Fund’s returns in the quarter. Other notable contributors included Wells Fargo (+25%), Microsoft (+25%) and Tyco (+21%). New holding Hewlett-Packard detracted from near-term results as we built our position on the stock’s weakness.

For the fiscal year ended March 31, 2012, the Fund gained 5.4% compared to an 8.5% gain for the S&P 500 and a 7.2% gain for the Russell 3000. Several large-cap companies delivered exceptional returns. Microsoft (+30%), Comcast (+30%), and Tyco (+28%) posted solid earnings growth while executing on their strategic plans. New additions Wells Fargo and Valeant Pharmaceuticals were also among the Fund’s largest contributors. Both remain core holdings with sound long-term prospects.

Smaller company results were more mixed for the fiscal year. Omnicare (+19%) made significant progress under John Figueroa’s refreshing leadership, and Grand Canyon Education (+22%) rebounded from depressed levels. On the other hand, SandRidge Energy (-39%) and Redwood Trust (-22%) detracted materially from the Fund’s results. SandRidge made several bold strategic moves that upgraded the company’s asset base, helped fund its ambitious drilling program, and improved its financial flexibility. While the stock is volatile, we think the company is taking the right steps to increase its ultimate potential value. Redwood is well positioned to play a large role when the government inevitably reduces its massive support of the residential mortgage market. The company trades for less than book value, is building a franchise for the long haul, and pays a healthy dividend while we wait for conditions to improve.

We bought one new stock during the quarter as Hewlett-Packard again pulled back into our buying range. HP faces near-term challenges as management reformulates its strategy and integrates the Autonomy acquisition. More importantly, it will take time for Meg Whitman and her team to rebuild customer (and investor) trust after a series of missteps under prior leadership. Still, we think HP’s portfolio includes a number of attractive and entrenched businesses that are not going away, and that are worth far more than six times earnings to owners with a long enough investing horizon.

On balance we were net sellers into the continuing rally. We sold Mohawk Industries as investors bid up housing-related stocks in anticipation of the long-awaited recovery. While we like Mohawk’s business outlook as housing conditions improve, the stock had already priced in much of the potential good news well in advance. We also eliminated ConocoPhillips at healthy gains while increasing our investment in out-of-favor natural gas producer Southwestern Energy. Finally, we trimmed a long list of positions as stocks continued to march higher and discounts to value on average narrowed. As a result, the Fund’s residual cash position rose from 16% in December to 21% at quarter end.

Partners Value is a flexible, multi-cap fund that invests in companies of all sizes. The portfolio remains tilted to larger companies with strong competitive positions, relatively stable cash flows, able managements and sturdy balance sheets. Roughly 60% of the Fund’s equity holdings are in large-cap companies (market capitalization greater than $10B), with the other 40% split between medium-sized and smaller businesses.

| New and Eliminated Securities for Quarter Ended March 31, 2012 | |

| New Purchases ($mil) | | Eliminations ($mil) | |

| Hewlett-Packard | | $ | 15.7 | | Mohawk Industries | | $ | 12.6 | |

| | | | | | ConocoPhillips | | | 7.3 | |

weitzfunds.com 13

PARTNERS VALUE FUND

PERFORMANCE • (UNAUDITED)

| | | | Total Returns | | | Average Annual Total Returns | |

| | | | 3 Mos. | | 1 Year | | 3 Year | | 5 Year | | 10 Year | | 15 Year | | 20 Year | | 25 Year |

| Partners Value | | | 10.5 | % | | 5.4 | % | | 25.5 | % | | 1.3 | % | | 4.4 | % | | 9.7 | % | | 11.3 | % | | 11.0 | % |

| S&P 500 | | | 12.6 | | | 8.5 | | | 23.4 | | | 2.0 | | | 4.1 | | | 6.1 | | | 8.6 | | | 8.9 | |

| Russell 3000 | | | 12.9 | | | 7.2 | | | 24.3 | | | 2.2 | | | 4.7 | | | 6.5 | | | 8.7 | | | 9.0 | |

| Russell 3000 Value | | | 11.2 | | | 4.3 | | | 23.0 | | | -0.8 | | | 4.7 | | | 6.9 | | | 9.5 | | | 9.4 | |

Growth of $10,000

This chart depicts the change in the value of a $10,000 investment in the Partners Value Fund for the period March 31, 2002 through March 31, 2012, as compared with the growth of the Standard & Poor’s 500 Index during the same period. Index performance is hypothetical and is shown for illustrative purposes only.

| | | | Partners | | | | | Relative |

| | | | Value | | S&P 500 | | Results |

| Year | | | (1) | | (2) | | (1)-(2) |

| 1983 (6/1/83) | | | 9.9 | % | | 4.2 | % | | 5.7 | % |

| 1984 | | | 14.5 | | | 6.1 | | | 8.4 | |

| 1985 | | | 40.7 | | | 31.6 | | | 9.1 | |

| 1986 | | | 11.1 | | | 18.6 | | | -7.5 | |

| 1987 | | | 4.3 | | | 5.1 | | | -0.8 | |

| 1988 | | | 14.9 | | | 16.6 | | | -1.7 | |

| 1989 | | | 20.3 | | | 31.7 | | | -11.4 | |

| 1990 | | | -6.3 | | | -3.1 | | | -3.2 | |

| 1991 | | | 28.1 | | | 30.5 | | | -2.4 | |

| 1992 | | | 15.1 | | | 7.6 | | | 7.5 | |

| 1993 | | | 23.0 | | | 10.1 | | | 12.9 | |

| 1994 | | | -9.0 | | | 1.3 | | | -10.3 | |

| 1995 | | | 38.7 | | | 37.6 | | | 1.1 | |

| 1996 | | | 19.1 | | | 23.0 | | | -3.9 | |

| 1997 | | | 40.6 | | | 33.4 | | | 7.2 | |

| 1998 | | | 29.1 | | | 28.6 | | | 0.5 | |

| 1999 | | | 22.1 | | | 21.0 | | | 1.1 | |

| 2000 | | | 21.1 | | | -9.1 | | | 30.2 | |

| 2001 | | | -0.9 | | | -11.9 | | | 11.0 | |

| 2002 | | | -17.0 | | | -22.1 | | | 5.1 | |

| 2003 | | | 25.4 | | | 28.7 | | | -3.3 | |

| 2004 | | | 15.0 | | | 10.9 | | | 4.1 | |

| 2005 | | | -2.4 | | | 4.9 | | | -7.3 | |

| 2006 | | | 22.5 | | | 15.8 | | | 6.7 | |

| 2007 | | | -8.5 | | | 5.5 | | | -14.0 | |

| 2008 | | | -38.1 | | | -37.0 | | | -1.1 | |

| 2009 | | | 31.3 | | | 26.5 | | | 4.8 | |

| 2010 | | | 27.5 | | | 15.1 | | | 12.4 | |

| 2011 | | | 2.2 | | | 2.1 | | | 0.1 | |

| 2012 (3/31/12) | | | 10.5 | | | 12.6 | | | -2.1 | |

| Since Inception: | | | | | | | | | | |

| Cumulative | | | | | | | | | | |

| Return | | | 2,851.2 | | | | | | 1,166.2 | |

| Avg. Annual | | | | | | | | | | |

| Return | | | 12.4 | | | 10.5 | | | 1.9 | |

These performance numbers reflect the deduction of the Fund’s annual operating expenses which as stated in its most recent Prospectus are 1.21% of the Fund’s net assets. The returns assume redemption at the end of each period and reinvestment of dividends. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses by the Adviser. This information represents past performance and past performance does not guarantee future results. The investment return and the principal value of an investment in this Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data quoted. Performance data current to the most recent month-end may be obtained at www.weitzfunds.com/performance/monthly.asp.

See page 4 for additional performance disclosures. See page 82 for a description of all indices.

Performance information does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

14 Weitz Funds

PARTNERS VALUE FUND

PORTFOLIO PROFILE • (UNAUDITED)

| Top Ten Stocks |

| Wells Fargo & Co. | | | 4.2 | % |

| Berkshire Hathaway, Inc. - CL B | | | 3.9 | |

| Aon Corp. | | | 3.8 | |

| Liberty Interactive Corp. - Series A | | | 3.5 | |

| Texas Instruments, Inc. | | | 3.4 | |

| Tyco International Ltd. | | | 3.2 | |

| Google, Inc. - CL A | | | 3.2 | |

| Redwood Trust, Inc. | | | 3.1 | |

| Liberty Global, Inc. - Series C | | | 3.0 | |

| SandRidge Energy, Inc. | | | 2.9 | |

| % of Net Assets | | | 34.2 | % |

| Industry Sectors |

| Consumer Discretionary | | | 23.0 | % |

| Information Technology | | | 17.3 | |

| Financials | | | 15.0 | |

| Health Care | | | 8.3 | |

| Energy | | | 5.4 | |

| Materials | | | 5.0 | |

| Industrials | | | 3.2 | |

| Consumer Staples | | | 1.9 | |

| Short-Term Securities/Other | | | 20.9 | |

| Net Assets | | | 100.0 | % |

| Top Performers for Quarter Ended March 31, 2012 |

| Security Name | | | QTD Return of Security | | Average Weight in Portfolio | | Contribution to Fund Performance |

| Wells Fargo & Co. | | | 24.7 | % | | 4.2 | % | | 0.96 | % |

| Microsoft Corp. | | | 25.1 | | | 3.7 | | | 0.93 | |

| Eagle Materials, Inc. | | | 35.4 | | | 2.0 | | | 0.73 | |

| Liberty Interactive Corp. - Series A | | | 17.8 | | | 4.0 | | | 0.72 | |

| Liberty Global, Inc. - Series C | | | 21.2 | | | 3.2 | | | 0.68 | |

Contributions to Fund performance are based on actual daily holdings. Securities may have been bought or sold during the quarter.

Source: FactSet Portfolio Analytics

| Bottom Performers for Quarter Ended March 31, 2012 | |

| | | | QTD Return | | Average Weight | | Contribution to |

| Security Name | | | of Security | | in Portfolio | | Fund Performance |

| Hewlett-Packard Co. | | | (7.0 | )% | | 1.1 | % | | (0.18 | )% |

| SandRidge Energy, Inc. | | | (4.0 | ) | | 3.1 | | | (0.12 | ) |

| Google, Inc. - CL A | | | (0.7 | ) | | 3.1 | | | (0.05 | ) |

| Southwestern Energy Co. | | | (4.2 | ) | | 2.0 | | | (0.02 | ) |

Contributions to Fund performance are based on actual daily holdings. Securities may have been bought or sold during the quarter.

Source: FactSet Portfolio Analytics

weitzfunds.com 15

PARTNERS VALUE FUND

SCHEDULE OF INVESTMENTS • MARCH 31, 2012

| COMMON STOCKS — 79.1% | | | Shares | | | Value | |

| Consumer Discretionary — 23.0% | | | | | | | |

| Cable & Satellite — 5.8% | | | | | | | |

| Liberty Global, Inc. - Series C* | | | 449,800 | | $ | 21,540,922 | |

| Comcast Corp. - CL A Special | | | 650,000 | | | 19,181,500 | |

| | | | | | | 40,722,422 | |

| Internet & Catalog Retail — 3.5% | | | | | | | |

| Liberty Interactive Corp. - Series A* | | | 1,300,000 | | | 24,817,000 | |

| Multiline Retail — 2.9% | | | | | | | |

| Target Corp. | | | 350,000 | | | 20,394,500 | |

| Hotels, Restaurants & Leisure — 2.6% | | | | | | | |

| Interval Leisure Group, Inc. | | | 1,050,000 | | | 18,270,000 | |

| Broadcasting — 2.6% | | | | | | | |

| Liberty Media Corp. - | | | | | | | |

| Liberty Capital - Series A* | | | 205,000 | | | 18,070,750 | |

| Movies & Entertainment — 2.0% | | | | | | | |

| Live Nation Entertainment, Inc.* | | | 1,525,100 | | | 14,335,940 | |

| Textiles, Apparel & Luxury Goods — 1.8% | | | | | | | |

| Iconix Brand Group, Inc.* | | | 750,000 | | | 13,035,000 | |

| Education Services — 0.9% | | | | | | | |

| Grand Canyon Education, Inc.* | | | 367,979 | | | 6,535,307 | |

| Specialized Consumer Services — 0.9% | | | | | | | |

Coinstar, Inc.* (c) | | | 100,000 | | | 6,355,000 | |

| | | | | | | 162,535,919 | |

| Information Technology — 17.3% | | | | | | | |

| Internet Software & Services — 4.5% | | | | | | | |

| Google, Inc. - CL A* | | | 34,800 | | | 22,315,152 | |

| XO Group, Inc.* | | | 1,000,000 | | | 9,390,000 | |

| | | | | | | 31,705,152 | |

| Computers & Peripherals — 4.4% | | | | | | | |

| Dell, Inc.* | | | 1,000,000 | | | 16,600,000 | |

| Hewlett-Packard Co. | | | 600,000 | | | 14,298,000 | |

| | | | | | | 30,898,000 | |

| Semiconductors — 3.4% | | | | | | | |

| Texas Instruments, Inc. | | | 725,000 | | | 24,367,250 | |

| Software — 2.9% | | | | | | | |

| Microsoft Corp. | | | 630,000 | | | 20,317,500 | |

| Electronic Equipment & Instruments — 2.1% | | | | | | | |

| FLIR Systems, Inc. | | | 600,000 | | | 15,186,000 | |

| | | | | | | 122,473,902 | |

| Financials — 15.0% | | | | | | | |

| Commercial Banks — 4.2% | | | | | | | |

| Wells Fargo & Co. | | | 860,000 | | | 29,360,400 | |

| Property & Casualty Insurance — 3.9% | | | | | | | |

| Berkshire Hathaway, Inc. - CL B* | | | 340,000 | | | 27,591,000 | |

| Insurance Brokers — 3.8% | | | | | | | |

| Aon Corp. | | | 550,000 | | | 26,983,000 | |

| Mortgage REIT’s — 3.1% | | | | | | | |

| Redwood Trust, Inc. | | | 1,950,000 | | | 21,840,000 | |

| | | | | | | 105,774,400 | |

| | | | Principal | | | | |

| | | | amount | | | | |

| | | | or shares | | | Value | |

| Health Care — 8.3% | | | | | | | |

| Health Care Services — 5.4% | | | | | | | |

| Laboratory Corp. of America Holdings* | | | 210,000 | | $ | 19,223,400 | |

| Omnicare, Inc. | | | 540,000 | | | 19,207,800 | |

| | | | | | | 38,431,200 | |

| Pharmaceuticals — 2.9% | | | | | | | |

| Valeant Pharmaceuticals International, Inc.* | | | 375,000 | | | 20,133,750 | |

| | | | | | | 58,564,950 | |

| Energy — 5.4% | | | | | | | |

| Oil & Gas Exploration & Production — 5.4% | | | | | | | |

| SandRidge Energy, Inc.* | | | 2,612,000 | | | 20,451,960 | |

| Southwestern Energy Co.* | | | 460,000 | | | 14,076,000 | |

| Apache Corp. | | | 40,000 | | | 4,017,600 | |

| | | | | | | 38,545,560 | |

| Materials — 5.0% | | | | | | | |

| Construction Materials — 5.0% | | | | | | | |

| Martin Marietta Materials, Inc. | | | 172,500 | | | 14,771,175 | |

| Eagle Materials, Inc. | | | 350,000 | | | 12,162,500 | |

| Texas Industries, Inc. | | | 250,000 | | | 8,752,500 | |

| | | | | | | 35,686,175 | |

| Industrials — 3.2% | | | | | | | |

| Industrial Conglomerates — 3.2% | | | | | | | |

| Tyco International Ltd. | | | 400,000 | | | 22,472,000 | |

| Consumer Staples — 1.9% | | | | | | | |

| Food & Staples Retailing — 1.9% | | | | | | | |

| CVS Caremark Corp. | | | 300,000 | | | 13,440,000 | |

| Other — 0.0% | | | | | | | |

| Adelphia Recovery Trust, | | | | | | | |

Series ACC-7* # | | | 2,310,000 | | | — | |

| Total Common Stocks | | | | | | | |

| (Cost $436,845,066) | | | | | | 559,492,906 | |

| | | | | | | | |

| SHORT-TERM SECURITIES — 21.5% | | | | | | | |

| Wells Fargo Advantage Government Money Market Fund - | | | | | | | |

Institutional Class 0.01%(a) | | | 3,798,678 | | | 3,798,678 | |

| U.S. Treasury Bills, 0.01% to 0.11%, | | | | | | | |

4/05/12 to 5/31/12(b) | | $ | 148,000,000 | | | 147,993,732 | |

| Total Short-Term Securities | | | | | | | |

| (Cost $151,792,345) | | | | | | 151,792,410 | |

| | | | | | | | |

| Total Investments in Securities | | | | | | | |

| (Cost $588,637,411) | | | | | | 711,285,316 | |

| Options Written — 0.0% | | | | | | (96,000 | ) |

| Other Liabilities in Excess of Other Assets — (0.6%) | | | | | | (4,014,999 | ) |

| Net Assets — 100.0% | | | | | $ | 707,174,317 | |

| Net Asset Value Per Share | | | | | $ | 23.25 | |

| 16 Weitz Funds | The accompanying notes form an integral part of these financial statements. |

| | | | Expiration | | | Shares | | | | |

| | | | date/ | | | subject | | | | |

| OPTIONS WRITTEN* | | | Strike price | | | to option | | | Value | |

| Covered Call Options | | | | | | | | | | |

| Coinstar, Inc. | | | April 2012 / $62.50 | | | 15,000 | | $ | (37,500 | ) |

| Coinstar, Inc. | | | July 2012 / $62.50 | | | 10,000 | | | (58,500 | ) |

| | | | | | | | | | | |

| Total Options Written | | | | | | | | | | |

| (premiums received $101,873) | | | | | | | | $ | (96,000 | ) |

| * | Non-income producing |

| # | Illiquid and/or restricted security that has been fair valued. |

| (a) | Rate presented represents the annualized 7-day yield at March 31, 2012. |

| (b) | Interest rates presented represent the yield to maturity at the date of purchase. |

| (c) | Fully or partially pledged on outstanding written options. |

| The accompanying notes form an integral part of these financial statements. | weitzfunds.com 17 |

PARTNERS III OPPORTUNITY FUND

PORTFOLIO MANAGER’S DISCUSSION & ANALYSIS

Portfolio Manager: Wallace R. Weitz, CFA

The Partners III Opportunity Fund-Institutional Class returned +7.8% in the first calendar quarter, compared to a +12.6% return for the S&P 500 and a +12.9% return for the Russell 3000. Stock gains were broad-based in the quarter, and our companies on the whole have been doing well. Notable contributors included Wells Fargo (+25%), Microsoft (+25%), and a slew of consumer discretionary companies such as Liberty Global (+21%), Interval Leisure (+29%) and National CineMedia (+25%). As expected in a strongly rising market, the Fund’s short positions posted negative returns. While Ascent Capital (-7%), Intelligent Systems (-9%) and a few other stocks declined, our conservative positioning was the primary reason that the Fund lagged the market during the quarter.

For the fiscal year ended March 31, 2012, the Fund’s Institutional Class gained 4.9% compared to an 8.5% gain for the S&P 500 and a 7.2% gain for the Russell 3000. A trio of stocks (Liberty Interactive +19%, Liberty Media +20%, Liberty Global +20%) chaired by one of our favorite partners, John Malone, helped drive the Fund’s positive absolute returns. New additions Wells Fargo and Valeant Pharmaceuticals were also among the Fund’s largest contributors. Long-time holding Microsoft (+30%) kept churning out cash flow, and investors finally started to take note. Finally, Omnicare (+19%) made significant strategic progress under John Figueroa’s refreshing leadership.

While most of our stocks rose, the Fund trailed the broader indices for the fiscal year. The Fund’s energy and financial holdings (other than Wells Fargo) detracted materially from results. SandRidge Energy (-39%) made several bold strategic moves that upgraded the company’s asset base, helped fund its ambitious drilling program, and improved its financial flexibility. While the stock is volatile, we think the company is taking the right steps to increase its ultimate potential value. Southwestern Energy (-29%) fell as prices for U.S. natural gas collapsed throughout the year. The near-term environment is challenging, yet we think this low-cost producer has a strong multi-year outlook.

Redwood Trust (-22%) is well positioned to play a large role when the government inevitably reduces its massive support of the residential mortgage market. Redwood trades for less than book value, is building a franchise for the long haul, and pays a healthy dividend while we wait for conditions to improve. Aon (-6%) continues to make slow but steady forward progress. The company should benefit over time from global economic growth and healthier insurance market pricing.

Range Resources was our only new purchase in the first quarter. Range is a domestic natural gas exploration and production company, with “crown jewel” acreage in the Southwest Pennsylvania portion of the Marcellus field. We also added significantly to our holdings of FLIR Systems. FLIR designs and manufactures infrared and thermal imaging equipment for commercial and military customers. Please see the Letter to Shareholders at the beginning of this report for more details on both Range and FLIR. Other notable position size increases included Target, Iconix Brand Group and Valeant Pharmaceuticals.

We sold a handful of small positions during the quarter. Mohawk Industries rose as investors bid up housing-related stocks in anticipation of the long-awaited recovery. While we like Mohawk’s business outlook as housing conditions improve, the stock had priced in much of the potential good news well in advance. We eliminated Energizer Holdings at a moderate gain as the stock approached our value estimate, and we exited Grand Canyon Education as education stocks rallied early in the quarter. Finally, we sold several exchange-traded funds (ETF’s), one that invested in home builders, one that invested in banks and one that shorted long Treasury bonds.

Partners III Opportunity has the broadest toolkit of our equity funds. The Fund invests in companies of all sizes, and typically maintains short positions to help manage risk. Partners III is approximately 73% “net long” at quarter end, relatively unchanged from December. Our long positions edged up to 91% of net assets, while we also increased our effective short positions to 18% of net assets. The Fund’s shorts include small-, mid- and large-cap stock ETF’s.

| New and Eliminated Securities for Quarter Ended March 31, 2012 | |

| New ($mil) | | Eliminations ($mil) | |

| Range Resources | | $ | 9.5 | | SPDR S&P Bank ETF | | $ | 4.3 | |

| | | | | | Grand Canyon Education | | | 4.1 | |

| | | | | | ProShares Short 20+ Year Treasury Fund | | | 3.8 | |

| | | | | | Energizer Holdings | | | 3.2 | |

| | | | | | Mohawk Industries | | | 1.7 | |

| | | | | | Ishares Dow Jones U.S. Home Construction Index Fund | | | 0.5 | |

18 Weitz Funds

PARTNERS III OPPORTUNITY FUND

PERFORMANCE • (UNAUDITED)

| | | | Total Returns | | | Average Annual Total Returns | |

| | | | 3 Mos. | | 1 Year | | 3 Year | | 5 Year | | 10 Year | 15 Year | | 20 Year | | 25 Year |

| Partners III – Institutional Class | | | 7.8 | % | | 4.9 | % | | 28.4 | % | | 4.4 | % | | 7.8 | % | | 11.3 | % | | 13.0 | % | | 12.2 | % |

| S&P 500 | | | 12.6 | | | 8.5 | | | 23.4 | | | 2.0 | | | 4.1 | | | 6.1 | | | 8.6 | | | 8.9 | |

| Russell 3000 | | | 12.9 | | | 7.2 | | | 24.3 | | | 2.2 | | | 4.7 | | | 6.5 | | | 8.7 | | | 9.0 | |

| Russell 3000 Value | | | 11.2 | | | 4.3 | | | 23.0 | | | -0.8 | | | 4.7 | | | 6.9 | | | 9.5 | | | 9.4 | |

Growth of $10,000

This chart depicts the change in the value of a $10,000 investment in Partners III – Institutional Class for the period March 31, 2002 through March 31, 2012, as compared with the growth of the Standard & Poor’s 500 Index during the same period. Index performance is hypothetical and is shown for illustrative purposes only.

| | | | Partners III | | S&P 500 | | Relative |

| Year | | | (1) | | (2) | | Results (1)-(2) |

| 1983 (6/1/83) | | | 8.6 | % | | 4.2 | % | | 4.4 | % |

| 1984 | | | 11.2 | | | 6.1 | | | 5.1 | |

| 1985 | | | 38.6 | | | 31.6 | | | 7.0 | |

| 1986 | | | 8.5 | | | 18.6 | | | -10.1 | |

| 1987 | | | -1.4 | | | 5.1 | | | -6.5 | |

| 1988 | | | 19.5 | | | 16.6 | | | 2.9 | |

| 1989 | | | 19.4 | | | 31.7 | | | -12.3 | |

| 1990 | | | -5.5 | | | -3.1 | | | -2.4 | |

| 1991 | | | 23.2 | | | 30.5 | | | -7.3 | |

| 1992 | | | 13.5 | | | 7.6 | | | 5.9 | |

| 1993 | | | 32.3 | | | 10.1 | | | 22.2 | |

| 1994 | | | -11.1 | | | 1.3 | | | -12.4 | |

| 1995 | | | 43.3 | | | 37.6 | | | 5.7 | |

| 1996 | | | 25.0 | | | 23.0 | | | 2.0 | |

| 1997 | | | 37.1 | | | 33.4 | | | 3.7 | |

| 1998 | | | 10.9 | | | 28.6 | | | -17.7 | |

| 1999 | | | 10.6 | | | 21.0 | | | -10.4 | |

| 2000 | | | 32.4 | | | -9.1 | | | 41.5 | |

| 2001 | | | 6.6 | | | -11.9 | | | 18.5 | |

| 2002 | | | -16.1 | | | -22.1 | | | 6.0 | |

| 2003 | | | 42.6 | | | 28.7 | | | 13.9 | |

| 2004 | | | 22.1 | | | 10.9 | | | 11.2 | |

| 2005 | | | -0.7 | | | 4.9 | | | -5.6 | |

| 2006 | | | 20.4 | | | 15.8 | | | 4.6 | |

| 2007 | | | -12.9 | | | 5.5 | | | -18.4 | |

| 2008 | | | -34.4 | | | -37.0 | | | 2.6 | |

| 2009 | | | 42.0 | | | 26.5 | | | 15.5 | |

| 2010 | | | 33.0 | | | 15.1 | | | 17.9 | |

| 2011 | | | 5.6 | | | 2.1 | | | 3.5 | |

| 2012 (3/31/12) | | | 7.8 | | | 12.6 | | | -4.8 | |

| Since Inception: | | | | | | | | | | |

| Cumulative | | | | | | | | | | |

| | | 3,519.7 | | | 1,685.0 | | | 1,834.7 | |

| Avg. Annual | | | | | | | | | | |

| Return | | | 13.2 | | | 10.5 | | | 2.7 | |

These performance numbers reflect the deduction of the Fund’s Institutional Class annual operating expenses which as stated in its most recent Prospectus are 1.53% of the Fund’s net assets. The returns assume redemption at the end of each period and reinvestment of dividends. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses by the Adviser. This information represents past performance and past performance does not guarantee future results. The investment return and the principal value of an investment in this Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data quoted. Performance data current to the most recent month-end may be obtained at www.weitzfunds.com/performance/monthly.asp.

See page 4 for additional performance disclosures. See page 82 for a description of all indices.

Performance information does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

weitzfunds.com 19

PARTNERS III OPPORTUNITY FUND

PORTFOLIO PROFILE • (UNAUDITED)

| Top Ten Stocks |

| Wells Fargo & Co. | | | 6.3 | % |

| SandRidge Energy, Inc. | | | 4.3 | |

| Liberty Media Corp. - Liberty Capital - Series A | | | 4.1 | |

| Redwood Trust, Inc. | | | 4.0 | |

| Berkshire Hathaway, Inc. - CL B | | | 3.9 | |

| Valeant Pharmaceuticals International, Inc. | | | 3.9 | |

| Liberty Interactive Corp. - Series A | | | 3.8 | |

| Live Nation Entertainment, Inc. | | | 3.7 | |

| Liberty Global, Inc. - Series C | | | 3.7 | |

| Texas Instruments, Inc. | | | 3.6 | |

| % of Net Assets | | | 41.3 | % |

| Industry Sectors |

| Consumer Discretionary | | | 27.0 | % |

| Financials | | | 19.0 | |

| Information Technology | | | 15.9 | |

| Health Care | | | 10.1 | |

| Energy | | | 8.8 | |

| Industrials | | | 5.2 | |

| Materials | | | 3.9 | |

| Consumer Staples | | | 0.4 | |

| Telecommunication Services | | | 0.1 | |

| Securities Sold Short | | | (11.7 | ) |

| Short Proceeds/Other | | | 21.3 | |

| Net Assets | | | 100.0 | % |

| Top Performers for Quarter Ended March 31, 2012 |

| | | | QTD Return | | Average Weight | | Contribution to |

| Security Name | | | of Security | | in Portfolio | | Fund Performance |

| Wells Fargo & Co. | | | 24.7 | % | | 5.8 | % | | 1.32 | % |

| Microsoft Corp. | | | 25.1 | | | 3.3 | | | 0.79 | |

| Liberty Global, Inc. - Series C | | | 21.2 | | | 3.7 | | | 0.74 | |

| Liberty Interactive Corp. - Series A | | | 17.8 | | | 4.1 | | | 0.70 | |

| Live Nation Entertainment, Inc. | | | 13.1 | | | 4.1 | | | 0.60 | |

Contributions to Fund performance are based on actual daily holdings. Securities may have been bought or sold during the quarter.

Source: FactSet Portfolio Analytics

| Bottom Performers for Quarter Ended March 31, 2012 |

| | | | QTD Return | | Average Weight | | Contribution to |

| Security Name | | | of Security | | in Portfolio | | Fund Performance |

| Ishares Russell 2000 Fund (short) | | | 12.8 | % | | (4.2 | )% | | (0.53 | )% |

| SPDR S&P 500 ETF Trust (short) | | | 12.6 | | | (3.2 | ) | | (0.41 | ) |

| Ishares Russell Midcap Fund (short) | | | 12.9 | | | (3.1 | ) | | (0.39 | ) |

| Ascent Capital Group, Inc. - CL A | | | (6.8 | ) | | 2.8 | | | (0.18 | ) |

| Ishares Russell 2000 Value Fund (short) | | | 11.6 | | | (1.5 | ) | | (0.17 | ) |