As filed with the Securities and Exchange Commission on March 14, 2017.

Registration No. 333-________

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

[ ] Pre-Effective Amendment No. ___

[ ] Post-Effective Amendment No. ____

PRINCIPAL VARIABLE CONTRACTS FUNDS, INC.

(Exact name of Registrant as specified in charter)

711 High Street, Des Moines, Iowa 50392

(Address of Registrant's Principal Executive Offices)

515-235-9328

(Registrant's Telephone Number, Including Area Code)

Adam U. Shaikh

Assistant Counsel, Principal Variable Contracts Funds, Inc.

The Principal Financial Group

Des Moines, Iowa 50392

(Name and Address of Agent for Service)

|

| |

| Copies of all communications to: |

| | |

| | JOSHUA B. DERINGER |

| | Drinker Biddle & Reath, LLP |

| | One Logan Square, Ste 2000 |

| | Philadelphia, PA 19103-6996 |

| | 215-988-2959 |

Approximate date of proposed public offering: As soon as practicable after this Registration Statement becomes effective.

Title of Securities Being Registered: Class 1 Shares, par value $.01 per share.

No filing fee is due because an indefinite number of shares have been registered in reliance on Section 24(f) under the Investment Company Act of 1940, as amended.

PRINCIPAL VARIABLE CONTRACTS FUNDS, INC.

711 High Street

Des Moines, Iowa 50392

800-222-5852

_________, 2017

Dear Contract Owner:

A Special Meeting of Shareholders of Principal Variable Contracts Funds, Inc. (“PVC”) will be held at 711 High Street, Des Moines, Iowa 50392, on May 25, 2017 at 10:30 a.m., Central Time.

At the meeting, shareholders of the Balanced Account (the “Acquired Fund”) will be asked to consider and approve a Plan of Acquisition (the “Plan”) providing for the reorganization of the Acquired Fund into the Diversified Balanced Account (the “Acquiring Fund”) (together, the "Funds"). Each of these Funds is a separate series or fund of PVC.

As an investor through a variable annuity contract or variable life insurance policy issued through an insurance company, you can instruct your insurance company as to how to vote on the proposed reorganization. At the special meeting of shareholders, your insurance company will vote on as instructed by you and other investors holding contracts or policies through your insurance company.

Under the Plan: (i) the Acquiring Fund will acquire all the assets, subject to all the liabilities, of the Acquired Fund in exchange for shares of the Acquiring Fund; and (ii) the Acquiring Fund shares will be distributed to the shareholders of the Acquired Fund in complete liquidation and termination of the Acquired Fund (the “Reorganization”). As a result of the Reorganization, each shareholder of the Acquired Fund will become a shareholder of the Acquiring Fund. The total value of all shares of the Acquiring Fund issued in the Reorganization will equal the total value of the net assets of the Acquired Fund. The number of full and fractional shares of the Acquiring Fund received by a shareholder of the Acquired Fund will be equal in value to the value of that shareholder’s shares of the Acquired Fund as of the close of regularly scheduled trading on the New York Stock Exchange (“NYSE”) on the closing date of the Reorganization. Shareholders of the Acquired Fund, which issues only Class 1 shares, will receive Class 1 shares of the Acquiring Fund. The Reorganization is expected to occur on or about the close of regularly scheduled trading on the NYSE on May 26, 2017.

*****

Enclosed you will find a Notice of Special Meeting of Shareholders, a Proxy Statement/Prospectus, and a voting instruction card for the shares of the Acquired Fund attributable to your variable contract or policy as of April 5, 2017, the record date for the Meeting. The Proxy Statement/Prospectus provides background information and describes in detail the matters to be voted on at the Meeting.

The Board of Directors of PVC has unanimously voted in favor of the proposed Reorganization and recommends that you vote FOR the Proposal.

In order for shares to be voted at the Meeting, we urge you to read the Proxy Statement/Prospectus and then complete and mail your voting instruction card(s) in the enclosed postage-paid envelope, allowing sufficient time for receipt by us by May 24, 2017. As a convenience, we offer three options by which to vote your shares:

By Internet: Follow the instructions located on your voting instruction card.

By Phone: The phone number is located on your voting instruction card. Be sure you have your control number, as printed on your voting instruction card, available at the time you call.

By Mail: Sign your voting instruction card and enclose it in the postage-paid envelope provided in this proxy package.

We appreciate your taking the time to respond to this important matter. Your vote is important. If you have any questions regarding the Reorganization, please call our shareholder services department toll free at 1-800-222-5852.

Sincerely,

Michael J. Beer

President and CEO

PRINCIPAL VARIABLE CONTRACTS FUNDS, INC.

711 High Street

Des Moines, Iowa 50392

800-222-5852

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To the Contract Owners of the Balanced Account:

Notice is hereby given that a Special Meeting of Shareholders (the “Meeting”) of the Balanced Account (the “Acquired Fund”), a series of Principal Variable Contracts Funds, Inc. (“PVC”), will be held at 711 High Street, Des Moines, Iowa 50392, on May 25, 2017 at 10:30 a.m., Central Time. A Proxy Statement/Prospectus providing information about the following proposal to be voted on at the Meeting is included with this notice. The Meeting is being held to consider and vote on such proposal as well as any other business that may properly come before the Meeting or any adjournment thereof.

| |

| Proposal: | Approval of a Plan of Acquisition providing for the reorganization of the Balanced Account into the Diversified Balanced Portfolio. |

The Board of Directors of PVC recommends that shareholders of the Acquired Fund vote FOR the Proposal.

Approval of the Proposal will require the affirmative vote of the holders of at least a “Majority of the Outstanding Voting Securities” (as defined in the accompanying Proxy Statement/Prospectus) of the Acquired Fund.

Each shareholder of record at the close of business on April 5, 2017 is entitled to receive notice of and to vote at the Meeting. Please read the attached Proxy Statement/Prospectus.

By order of the Board of Directors

Michael J. Beer

President and CEO

____________, 2017

Des Moines, Iowa

PRINCIPAL VARIABLE CONTRACTS FUNDS, INC.

711 High Street

Des Moines, Iowa 50392

800-222-5852

---------------------------------

PROXY STATEMENT/PROSPECTUS

SPECIAL MEETING OF SHAREHOLDERS

TO BE HELD MAY 25, 2017

RELATING TO THE REORGANIZATION OF THE BALANCED ACCOUNT INTO THE DIVERSIFIED BALANCED ACCOUNT

This Proxy Statement/Prospectus is furnished in connection with the solicitation by the Board of Directors (the “Board” or “Directors”) of Principal Variable Contracts Funds, Inc. (“PVC”) of proxies to be used at a Special Meeting of Shareholders of PVC to be held at 711 High Street, Des Moines, Iowa 50392, on May 25, 2017, at 10:30 a.m., Central Time (the “Meeting”).

At the Meeting, the shareholders of the Balanced Account (the “Acquired Fund”) will be asked to consider and approve the Plan of Acquisition (the “Plan”) providing for its reorganization into the Diversified Balanced Account (the “Acquiring Fund”) (with the Acquired Fund, the "Funds").

All shares of the Acquired Fund are owned of record by sub-accounts of separate accounts ("Separate Accounts") of an insurance company established to fund benefits under variable annuity contracts and variable life insurance policies (each a "Contract") issued by an insurance company. Persons holding Contracts are referred to herein as "Contract Owners."

Under the Plan: (i) the Acquiring Fund will acquire all the assets, subject to all the liabilities, of the Acquired Fund in exchange for shares of the Acquiring Fund; and (ii) the Acquiring Fund shares will be distributed to the shareholders of the Acquired Fund in complete liquidation and termination of the Acquired Fund (the “Reorganization”). As a result of the Reorganization, each shareholder of the Acquired Fund will become a shareholder of the Acquiring Fund. The total value of all shares of the Acquiring Fund issued in the Reorganization will equal the total value of the net assets of the Acquired Fund. The number of full and fractional shares of the Acquiring Fund received by a shareholder of the Acquired Fund will be equal in value to the value of that shareholder’s shares of the Acquired Fund as of the close of regularly scheduled trading on the New York Stock Exchange (“NYSE”) on the closing date of the Reorganization. Shareholders of the Acquired Fund, which issues only Class 1 shares, will receive Class 1 shares of the Acquiring Fund. The Reorganization is expected to occur on or about the close of regularly scheduled trading on the NYSE on May 26, 2017. The terms and conditions of the Reorganization are more fully described below in this Proxy Statement/Prospectus and the Form of Plan of Acquisition which is attached hereto as Appendix A.

This Proxy Statement/Prospectus contains information shareholders should know before voting on the Reorganization. Please read it carefully and retain it for future reference. The Annual and Semi-Annual Reports to Shareholders of PVC contain additional information about the investments of the Acquired and Acquiring Funds, and the Annual Report contains discussions of the market conditions and investment strategies that significantly affected these Funds during the fiscal year ended December 31, 2016. Copies of these reports may be obtained at no charge by calling our shareholder services department toll free at 1-800-222-5852.

A Statement of Additional Information dated ___________, 2017 (the “Statement of Additional Information”) relating to this Proxy Statement/Prospectus has been filed with the Securities and Exchange Commission (“SEC”) (File No. 02-35570) and is incorporated by reference into this Proxy Statement/Prospectus. PVC’s Prospectus, dated April 30, 2012 and as supplemented (“PVC Prospectus”), and the Statement of Additional Information for PVC, dated April 30, 2012 and as supplemented (“PVC SAI”), have been filed with the SEC (File No. 02-35570) and, insofar as they relate to the Acquired Fund, are incorporated by reference into this Proxy Statement/Prospectus. Copies of these documents may be obtained without charge by writing to PVC at the address noted above or by calling our shareholder services department toll free at 1-800-222-5852. You may also call our shareholder services department toll free at 1-800-222-5852 if you have any questions regarding the Reorganization.

PVC is subject to the informational requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940 (the “1940 Act”) and files reports, proxy materials and other information with the SEC. Such reports, proxy materials and other information may be inspected and copied at the Public Reference Room of the SEC at 100 F Street, N.E., Washington, D.C. 20549 (information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-202-551-8090). Such materials are also available on the SEC’s EDGAR Database on its Internet site at www.sec.gov, and copies may be obtained, after paying a duplicating fee, by email request addressed to publicinfo@sec.gov or by writing to the SEC’s Public Reference Room.

The SEC has not approved or disapproved these securities or passed upon the accuracy or adequacy of this Proxy Statement/Prospectus. Any representation to the contrary is a criminal offense.

The date of this Proxy Statement/Prospectus is ___________, 2017.

|

| | |

| TABLE OF CONTENTS |

| | |

| | Page |

|

| INTRODUCTION | 3 |

|

| THE REORGANIZATION | 3 |

|

| PROPOSAL: APPROVAL OF A PLAN OF ACQUISITION PROVIDING FOR THE REORGANIZATION OF THE BALANCED ACCOUNT INTO THE DIVERSIFIED BALANCED ACCOUNT | 4 |

|

| Comparison of Acquired and Acquiring Funds | 4 |

|

| Comparison of Investment Objectives and Strategies | 5 |

|

| Fees and Expenses of the Funds | 6 |

|

| Comparison of Principal Investment Risks | 7 |

|

| Performance | 9 |

|

| Board Consideration of the Reorganization | 10 |

|

| INFORMATION ABOUT THE REORGANIZATION | 11 |

|

| Plan of Acquisition | 11 |

|

| Description of the Securities to Be Issued | 12 |

|

| Federal Income Tax Consequences | 12 |

|

| CAPITALIZATION | 12 |

|

| ADDITIONAL INFORMATION ABOUT INVESTMENT STRATEGIES AND RISKS | 13 |

|

| ADDITIONAL INFORMATION ABOUT THE FUNDS | 21 |

|

| Multiple Classes of Shares | 21 |

|

| Intermediary Compensation | 21 |

|

| Dividends and Distributions | 21 |

|

| Pricing of Fund Shares | 21 |

|

| TAX INFORMATION | 22 |

|

| ADDITIONAL INFORMATION REGARDING INTERMEDIARY COMPENSATION | 22 |

|

| ONGOING FEES | 23 |

|

| Frequent Trading and Market Timing (Abusive Trading Practices) | 23 |

|

| Eligible Purchasers | 24 |

|

| Shareholder Rights | 24 |

|

| Purchase of Fund Shares | 25 |

|

| Sale of Fund Shares | 25 |

|

| Restricted Transfers | 26 |

|

| Financial Statements | 26 |

|

| Portfolio Holdings Information | 26 |

|

| VOTING INFORMATION | 26 |

|

| OUTSTANDING SHARES AND SHARE OWNERSHIP | 27 |

|

| FINANCIAL HIGHLIGHTS | 27 |

|

| FINANCIAL STATEMENTS | 30 |

|

| LEGAL MATTERS | 30 |

|

| OTHER INFORMATION | 30 |

|

| APPENDIX A Form of Plan of Acquisition | A-1 |

|

INTRODUCTION

This Proxy Statement/Prospectus is being furnished to shareholders of the Acquired Fund to provide information regarding the Plan and the Reorganization.

Principal Variable Contracts Funds, Inc. PVC is a Maryland corporation and an open-end management investment company registered with the SEC under the 1940 Act. PVC currently offers 38 separate series or funds (the “PVC Accounts”), including the Acquired and Acquiring Funds. The sponsor of PVC is Principal Life Insurance Company (“Principal Life”), and the investment advisor to the PVC Funds is Principal Management Corporation (“PMC”). Principal Funds Distributor, Inc. (the “Distributor” or “PFD”) is the distributor for all share classes. Principal Life, an insurance company organized in 1879 under the laws of Iowa, PMC and PFD are indirect, wholly-owned subsidiaries of Principal Financial Group, Inc. (“PFG”). Their address is the Principal Financial Group, 711 High Street, Des Moines, Iowa 50392.

Investment Management. Pursuant to an investment advisory agreement with PVC with respect to the Acquired and Acquiring Funds, PMC provides investment advisory services and is also responsible for, among other things, administering the business and affairs of each of the Acquired and Acquiring Funds and selecting, contracting with, compensating and monitoring the performance of any investment sub-advisor that manages the investment of the assets of the Funds pursuant to sub-advisory agreements. As permitted by the investment advisory agreement, PMC has entered into a sub-advisory agreement with respect to the Acquired Fund as follows:

|

| |

Balanced Account (Acquired Fund) | Diversified Balanced Account (Acquiring Fund) |

Investment Advisor: PMC | Investment Advisor: PMC |

Sub-Advisor: Principal Global Investors, LLC ("PGI") | Sub-Advisor: None |

PGI and PMC are registered with the SEC as investment advisors under the Investment Advisers Act of 1940.

PGI is located at 801 Grand Avenue, Des Moines, IA 50392. PGI is an indirect wholly owned subsidiary of Principal Life Insurance Company, an affiliate of PMC, and a member of the Principal Financial Group.

THE REORGANIZATION

At its meeting held on December 13, 2016, the Board of Directors of PVC (the “Board”), including all the Directors who are not “interested persons” (as defined in the 1940 Act) of PVC (the “Independent Directors”), approved the Reorganization pursuant to the Plan providing for the combination of the Acquired Fund into the Acquiring Fund. The Board concluded that the Reorganization is in the best interests of the Acquired Fund and Acquiring Fund and that the interests of existing shareholders of each Fund will not be diluted as a result of the Reorganization. The factors that the Board considered in deciding to approve the Reorganization are discussed below under “Board Consideration of the Reorganization.”

The Reorganization contemplates: (i) the transfer of all the assets, subject to all of the liabilities, of the Acquired Fund to the Acquiring Fund in exchange for shares of the Acquiring Fund; and (ii) the distribution to Acquired Fund shareholders of the Acquiring Fund shares in complete liquidation and termination of the Acquired Fund. As a result of the Reorganization, each shareholder of the Acquired Fund will become a shareholder of the Acquiring Fund. In the Reorganization, the Acquiring Fund will issue a number of shares with a total value equal to the total value of the net assets of the Acquired Fund, and each shareholder of the Acquired Fund will receive a number of full and fractional shares of the Acquiring Fund with a value equal to the value of that shareholder’s shares of the Acquired Fund, as of the close of regularly scheduled trading on the NYSE on the closing date of the Reorganization (the “Effective Time”). The closing date of the Reorganization is expected to be on or about May 26, 2017. Shareholders of the Acquired Fund, which issues Class 1 shares, will receive Class 1 shares of the Acquiring Fund. The terms and conditions of the Reorganization are more fully described below in this Proxy Statement/Prospectus and in the Form of Plan of Acquisition, which is attached hereto as Appendix A.

PMC recommended the Reorganization to the Board and believes it will serve the interests of both the Acquired Fund and Acquiring Fund shareholders. PMC does not expect the Acquired Fund to gather significant new assets in the future. For that reason, the Reorganization is expected to result in economies of scale that will benefit shareholders of the Acquired Fund. The Funds have similar objectives in that the Acquired Fund seeks to generate a total return consisting of current income and capital appreciation while the Acquiring Fund seeks to provide as high a level of total return (consisting of reinvested income and capital appreciation) as is consistent with reasonable risk. The Funds also have similar investment strategies and risks in that both are asset allocation funds with broadly comparable asset allocation targets and ranges among equity and fixed income. The principal difference is that Acquiring Fund operates as a fund-of-funds investing primarily in index funds, Institutional Class shares of funds of Principal Funds, Inc., and of Class 1 shares of other PVC Funds, while the Acquired Fund directly purchases securities. Although past performance is no guarantee of future performance, the Acquiring Fund has a comparable performance history to the Acquired Fund. The Acquired Fund's assets are relatively small and PMC is expecting to see a continual decline in the Acquired Fund's assets. The Acquiring Fund's expense ratio is lower than the Acquired Fund's expense ratio (0.30% and 0.67%, respectively); accordingly, Acquired Fund shareholders are expected to enjoy cost savings as a result of the Reorganization (fully recumbent of Reorganization related costs to be borne by the Acquired Fund). Further, PMC believes the organization may be expected to afford shareholders of the Acquired Fund, on an ongoing basis, greater prospects for growth and efficient management due to lower fees.

In the opinion of legal counsel, the Reorganization will likely be considered a taxable transaction for federal income tax purposes and the Acquired Fund will recognize capital gains or losses on the Effective Date. Since the taxable impact of the transaction does not flow through to the Contract Owners of the insurance separate accounts that own the Acquired Fund shares, the reorganization is not expected to be a taxable event for federal income tax purposes for contract owners. See “Information About the Reorganization - Federal Income Tax Consequences.”

The Reorganization will not result in any material change in the purchase and redemption procedures followed with respect to the distribution of shares. See “Additional Information About the Funds - Purchases, Redemptions and Exchanges of Shares.”

The Acquired Fund will pay all expenses and out-of-pocket fees incurred in connection with the Reorganization, including printing, mailing, and legal fees which are estimated to be $17,000. The trading costs are estimated to be $55,000. It is expected that 100% of the portfolio securities of the Acquired Fund will be disposed of, a reduction in net asset value per share of approximately $0.03. The estimated taxable gain would be $2,896,000 on a U.S. GAAP basis. The Acquired Fund is considered a Regulated Investment Company (“RIC”) for tax purposes.

PROPOSAL:

APPROVAL OF A PLAN OF ACQUISITION PROVIDING FOR THE REORGANIZATION

OF THE BALANCED ACCOUNT INTO THE DIVERSIFIED BALANCED ACCOUNT

Shareholders of the Balanced Account (the “Acquired Fund”) are being asked to approve the reorganization of the Acquired Fund into the Diversified Balanced Account (the “Acquiring Fund”).

Comparison of Acquired and Acquiring Funds

The following table provides comparative information with respect to the Acquired and Acquiring Funds. As indicated in the table, the Funds have similar objectives in that the Acquired Fund seeks to generate a total investment return consistent with the preservation of capital while the Acquiring Fund seeks to provide as high a level of total return (consisting of reinvested income and capital appreciation) as is consistent with reasonable risk. The Funds also have similar investment strategies and risks in that both are asset allocation funds with broadly comparable asset allocation targets and ranges among fixed income securities and equity securities. The principal difference between the Funds, however, is that the Acquired Fund invests directly in securities while the Acquiring Fund operates as a fund-of-funds investing primarily in Institutional Class shares of funds of Principal Funds, Inc., and Class 1 shares of other PVC Funds. Further, as a fund-of-funds, a majority of the fees and expenses the Acquiring Fund pays are fees and expenses of the underlying funds in which it invests.

|

| |

Balanced Account (Acquired Fund) | Diversified Balanced Account (Acquiring Fund) |

| Approximate Net Assets as of December 31, 2016: | |

| $41,813,000 | $1,099,647,000 |

| | |

| Investment Advisor: | |

| PMC |

| | |

| Sub-Advisor: | |

| PGI | None |

| | |

| Portfolio Managers: | |

Matthew D. Annenberg (since 2014) has been with PGI since 2012. Prior to PGI, he was Managing Director at K2 Advisors from 2009 to 2012. He earned a bachelor's degree in Finance from Harvard College. Mr. Annenberg has earned the right to use the Chartered Financial Analyst designation. Scott Smith (since 2014) has been with PGI since 1999. He earned a bachelor’s degree in Finance from Iowa State University.

| James W. Fennessey (since 2009) joined the Principal Financial Group in 2000. Mr. Fennessey earned a B.S. in Business Administration, with an emphasis in Finance, and a minor in Economics from Truman State University. He has earned the right to use the Chartered Financial Analyst designation. Randy L. Welch (since 2009) joined the Principal Financial Group in 1989. Mr. Welch is an affiliate member of the Chartered Financial Analysts (CFA) Institute. Mr. Welch earned a B.A. in Business/Finance from Grand View College and an M.B.A. from Drake University. |

| | |

| | |

| | |

| | |

|

| |

Balanced Account (Acquired Fund) | Diversified Balanced Account (Acquiring Fund) |

| Comparison of Investment Objectives and Strategies |

| Investment Objectives: | |

| The Acquired Fund seeks to generate a total return consisting of current income and capital appreciation. | The Acquiring Fund seeks to provide as high a level of total return (consisting of reinvested income and capital appreciation) as is consistent with reasonable risk. |

| Principal Investment Strategies: | |

The Acquired Fund invests primarily in a diversified portfolio of equity securities and bonds. Though the percentages in each category are not fixed, equity securities generally represent 50% to 70% of the Acquired Fund's assets. The remainder of the Acquired Fund's assets is invested in bonds and cash. The Acquired Fund utilizes an asset allocation approach that primarily focuses on asset class allocation (equity versus fixed income) and secondarily for its equity investments, on growth versus value, domestic versus foreign, and market capitalization size. The Acquired Fund invests in equity securities of small, medium, and large market capitalization companies. The Acquired Fund actively trades portfolio securities. Under normal circumstances, the Acquired Fund invests in intermediate maturity fixed-income securities, which are rated, at the time of purchase, BBB- or higher by S&P Global Ratings ("S&P Global") or Baa3 or higher by Moody's Investors Service, Inc. ("Moody's"). The fixed-income securities in which the Acquired Fund invests include securities issued or guaranteed by the U.S. government or its agencies or instrumentalities (including collateralized mortgage obligations), asset-backed securities and mortgage backed securities representing an interest in a pool of mortgage loans or other assets (securitized products); corporate bonds; and securities issued by or guaranteed by foreign governments payable in U.S. dollars. The Acquired Fund also invests in foreign securities and up to 20% of its assets in below investment grade bonds (sometimes called “high yield bonds” or "junk bonds") which are rated at the time of purchase Ba1 or lower by Moody's and BB+ or lower by S&P Global (if the bond has been rated by only one of those agencies, that rating will determine whether the bond is below investment grade; if the bond has not been rated by either of those agencies the Sub-Advisor will determine whether the bond is of a quality comparable to those rated below investment grade). Under normal circumstances, the Acquired Fund maintains an average portfolio duration that is within + 25% of the duration of the Bloomberg Barclays U.S. Aggregate Bond Index, which as of December 31, 2016, the average portfolio duration of the fixed-income portion of the Acquired Fund was 5.89 years. During the fiscal year ended December 31, 2016, the average ratings of the Acquired Fund's fixed-income assets, based on market value at each month-end, were as follows (all ratings are by Moody's): 54.39% in securities rated Aaa; 3.90% in securities rated Aa; 13.49% in securities rated A; 18.93% in securities rated Baa; 4.79% in securities rated Ba; 2.66% in securities rated B; 1.04% in securities rated Caa; 0.04% in securities rated Ca; and 0.76% in securities not rated.

| The Acquiring Fund operates as a fund of funds and invests in underlying funds, each of which tracks an index. In pursuing its investment objective, the Acquiring Fund typically allocates its assets, within predetermined percentage ranges, among the “underlying funds”: Funds of Principal Funds, Inc. ("PFI") (Institutional Class shares) - the International Equity Index, MidCap S&P 400 Index, and SmallCap S&P 600 Index Funds - and Accounts of Principal Variable Contracts Funds, Inc. ("PVC") (Class 1 shares) - the Bond Market Index and LargeCap S&P 500 Index Accounts. The Acquiring Fund generally allocates approximately 50% of its assets to the equity index funds to gain broad market capitalization exposure to both U.S. and non-U.S investments and approximately 50% to the Bond Market Index Account for intermediate duration fixed-income exposure. The percentages reflect the extent to which the Acquiring Fund normally invests in the particular market segment represented by the underlying funds, and the asset allocation strategy influences the potential investment risk and reward of the Acquiring Fund. Without shareholder approval, Principal Management Corporation ("PMC"), the manager for PVC and PFI, may alter the percentage ranges and/or substitute or remove underlying funds (including investing in other investment companies) when it deems appropriate in order to achieve the Acquiring Fund’s investment objective. The assets of the Acquiring Fund are allocated among underlying funds in accordance with its investment objective, while considering PMC's outlook for the economy, the financial markets, and the relative market valuations of the underlying funds. In selecting underlying funds and their target weights, PMC considers, among other things, quantitative measures, such as past performance, expected levels of risk and returns, expense levels, diversification of existing funds, and style consistency. The Acquiring Fund is re-balanced monthly. The net asset value of the Acquiring Fund's shares is affected by changes in the value of the shares of the underlying funds it owns. The Acquiring Fund's investments are invested in the underlying funds and, as a result, the Acquiring Fund's performance is directly related to their performance. The Acquiring Fund's ability to meet its investment objective depends on the ability of the underlying funds to achieve their investment objectives. The Acquiring Fund’s underlying funds utilize derivative strategies. A derivative is a financial arrangement, the value of which is derived from, or based on, a traditional security, asset, or market index. Specifically, the underlying funds invest in equity index futures and exchange-traded funds (ETFs) to manage the equity exposure.

|

Temporary Defensive Investing:

For temporary defensive purposes in times of unusual or adverse market, economic, or political conditions, each Fund may invest up to 100% of its assets in cash and cash equivalents. In taking such defensive measures, either Fund may fail to achieve its investment objective.

Fundamental Investment Restrictions:

The Funds are subject to identical fundamental investment restrictions. These fundamental restrictions deal with such matters as the issuance of senior securities, purchasing or selling real estate or commodities, borrowing money, making loans, underwriting securities of other issuers, diversification or concentration of investments, and short sales of securities. The fundamental investment restrictions of the Funds are described in the Statement of Additional Information.

The investment objective of each Fund may be changed by the Board without shareholder approval.

Additional information about the investment strategies and the types of securities in which the Funds may invest is discussed below under “Certain Investment Strategies and Related Risks of the Funds” as well as in the Statement of Additional Information.

The Statement of Additional Information provides further information about the portfolio manager(s) for each Fund, including information about compensation, other accounts managed and ownership of Fund shares.

Fees and Expenses of the Funds

Fees and Expenses as a % of average daily net assets

The following table shows: (a) the ratios of expenses to average net assets of the Acquired Fund for the fiscal year ended December 31, 2016; (b) the ratios of expenses to average net assets of the Acquiring Fund for the fiscal year ended December 31, 2016; and (c) the pro forma expense ratios of the Acquiring Fund for the fiscal year ended December 31, 2016 assuming that the Reorganization had taken place at the commencement of the fiscal year ended December 31, 2016.

These fees and expenses do not include the effect of any sales charge, separate account expenses or other contract level expenses which may be applied at the variable life insurance or variable annuity product level. If such charges or fees were included, overall expenses would be higher and would lower the Acquired and Acquiring Funds’ performance.

Annual Fund Operating Expenses

(Expenses that you pay each year as a percentage of the value of your investment)

|

| | | | | |

| | Management Fees | Other Expenses | Acquired Fund Fees and Expenses | Total Annual Account Operating Expenses |

| (a) Balanced Account (Acquired Fund) |

| Class 1 | 0.60% | 0.07% | 0.00% | 0.67% |

| |

| (b) Diversified Balanced Account (Acquiring Fund) |

| Class 1 | 0.05% | 0.00% | 0.25% | 0.30% |

| |

| (c) Diversified Balanced Account (Acquiring Fund) (Pro forma assuming Reorganization) |

| Class 1 | 0.05% | 0.00% | 0.25% | 0.30% |

Examples: The following examples are intended to help you compare the costs of investing in shares of the Acquired and Acquiring Funds. The examples assume that fund expenses continue at the rates shown in the table above, that you invest $10,000 in the particular fund for the time periods indicated and that all dividends and distributions are reinvested. The examples also assume that your investment has a 5% return each year. The examples also take into account the relevant contractual expense limit until the date of expiration. The examples should not be considered a representation of future expense of the Acquired or Acquiring Fund. Actual expense may be greater or less than those shown.

|

| | | | | |

| | 1 Year | 3 Years | 5 Years | 10 Years |

| Balanced Account (Acquired Fund) | Class 1 | $68 | $214 | $373 | $835 |

| Diversified Balanced Account (Acquiring Fund) | Class 1 | 31 | 97 | 169 | 381 |

Diversified Balanced Account (Acquiring Fund) (Pro forma assuming Reorganization) | Class 1 | 31 | 97 | 169 | 381 |

Portfolio Turnover

Each Fund (the Acquired Fund directly and the Acquiring Fund, as a fund of funds, indirectly through the underlying funds) pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction fees. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the portfolio turnover rate for the Acquired Fund was 107.7% of the average value of its portfolio while the portfolio turnover rate for the Acquiring Fund was 14.1%.

Investment Management Fees/Sub-Advisory Arrangements

The Funds each pay their investment advisor, PMC, an advisory fee which for each Fund is calculated as a percentage of the Fund’s average daily net assets pursuant to the following fee schedule: |

| | | |

Balanced Account (Acquired Fund) | Diversified Balanced Account (Acquiring Fund) |

| First $100 Million | 0.60% | Overall Fee | 0.05% |

| Next $100 Million | 0.55% | | |

| Next $100 Million | 0.50% | | |

| Next $100 Million | 0.45% | | |

| Thereafter | 0.40% | | |

As sub-advisor to the Acquired Fund, PGI is paid sub-advisory fees for its services. These sub-advisory fees are paid by PMC, not by the Acquired Funds.

A discussion of the basis of the Board’s approval of the advisory and sub-advisory agreements with respect to the Acquired and Acquiring Funds is available in PVC’s Annual Report to Shareholders for the fiscal year ended December 31, 2016.

Comparison of Principal Investment Risks

In deciding whether to approve the Reorganization, shareholders should consider the amount and character of investment risk involved in the respective investment objectives and strategies of the Acquired and Acquiring Funds.

Risks Applicable to both Funds:

Asset Allocation Risk. A fund's selection and weighting of asset classes may cause it to underperform other funds with a similar investment objective.

Equity Securities Risk. The value of equity securities could decline if the issuer's financial condition declines or in response to overall market and economic conditions. A fund's principal market segment(s) (such as market capitalization or style), may underperform other market segments or the equity markets as a whole.

| |

| • | Growth Stock Risk. If growth companies do not increase their earnings at a rate expected by investors, the market price of the stock may decline significantly, even if earnings show an absolute increase. Growth company stocks also typically lack the dividend yield that can lessen price declines in market downturns. |

| |

| • | Small and Medium Market Capitalization Companies. Investments in small and medium sized companies may involve greater risk and price volatility than investments in larger, more mature companies. |

| |

| • | Value Stock Risk. Value stocks may continue to be undervalued by the market for extended periods, including the entire period during which the stock is held by the fund, or the events that the portfolio manager believed would cause the stock price to increase may not occur as anticipated or at all. Moreover, a stock judged to be undervalued actually may be appropriately priced at a low level and therefore would not be profitable for the fund. |

Fixed-Income Securities Risk. Fixed-income securities are subject to interest rate risk and credit quality risk. The market value of fixed-income securities generally declines when interest rates rise, and an issuer of fixed-income securities could default on its payment obligations.

Foreign Currency Risk. Risks of investing in securities denominated, or that trade, in foreign (non-U.S.) currencies include changes in foreign exchange rates and foreign exchange restrictions.

Foreign Securities Risk. The risks of foreign securities include loss of value as a result of: political or economic instability; nationalization, expropriation or confiscatory taxation; settlement delays; and limited government regulation (including less stringent reporting, accounting, and disclosure standards than are required of U.S. companies).

High Yield Securities Risk. High yield fixed-income securities (commonly referred to as "junk bonds") are subject to greater credit quality risk than higher rated fixed-income securities and should be considered speculative.

Portfolio Duration Risk. Portfolio duration is a measure of the expected life of a fixed-income security and its sensitivity to changes in interest rates. The longer a fund's average portfolio duration, the more sensitive the fund will be to changes in interest rates.

Portfolio Turnover (Active Trading) Risk. A fund that has a portfolio turnover rate over 100% is considered actively traded. Actively trading portfolio securities may accelerate realization of taxable gains and losses, lower fund performance and may result in high portfolio turnover rates and increased brokerage costs.

Real Estate Securities Risk. Investing in real estate securities subjects the fund to the risks associated with the real estate market (which are similar to the risks associated with direct ownership in real estate), including declines in real estate values, loss due to casualty or condemnation, property taxes, interest rate changes, increased expenses, cash flow of underlying real estate assets, regulatory changes (including zoning, land use and rents), and environmental problems, as well as to the risks related to the management skill and creditworthiness of the issuer.

Securitized Products Risk. Investments in securitized products are subject to risks similar to traditional fixed income securities, such as credit, interest rate, liquidity, prepayment, extension, and default risk, as well as additional risks associated with the nature of the assets and the servicing of those assets. Unscheduled prepayments on securitized products may have to be reinvested at lower rates. A reduction in prepayments may increase the effective maturities of these securities, exposing them to the risk of decline in market value over time (extension risk).

U.S. Government Securities Risk. Yields available from U.S. government securities are generally lower than yields from many other fixed-income securities.

U.S. Government-Sponsored Securities Risk. Securities issued by U.S. government-sponsored or -chartered enterprises such as the Federal Home Loan Mortgage Corporation, the Federal National Mortgage Association, and the Federal Home Loan Banks are not issued or guaranteed by the U.S. Treasury.

Principal Risks of Investing in the Acquiring Fund:

The principal risks of investing in the Acquiring Fund that are inherent in the fund of funds, in alphabetical order, are:

Asset Allocation Risk. A fund's selection and weighting of asset classes may cause it to underperform other funds with a similar investment objective.

Conflict of Interest Risk. The Advisor and its affiliates earn different fees from different underlying funds and may have an incentive to allocate more fund-of-fund assets to underlying funds from which they receive higher fees.

Derivatives Risk. Derivatives may not move in the direction anticipated by the portfolio manager. Transactions in derivatives may increase volatility, cause the liquidation of portfolio positions when not advantageous to do so, and result in disproportionate losses that may be substantially greater than a fund's initial investment.

| |

| • | Futures. Futures involve specific risks, including: the imperfect correlation between the change in market value of the instruments held by the fund and the price of the future,; possible lack of a liquid secondary market for a future and the resulting inability to close a future when desired; counterparty risk; and if the fund has insufficient cash, it may have to sell securities from its portfolio to meet daily variation margin requirements. |

Equity Securities Risk. The value of equity securities could decline if the issuer's financial condition declines or in response to overall market and economic conditions. A fund's principal market segment(s) (such as market capitalization or style), may underperform other market segments or the equity markets as a whole.

| |

| • | Growth Stock Risk. If growth companies do not increase their earnings at a rate expected by investors, the market price of the stock may decline significantly, even if earnings show an absolute increase. Growth company stocks also typically lack the dividend yield that can lessen price declines in market downturns. |

| |

| • | Small and Medium Market Capitalization Companies. Investments in small and medium sized companies may involve greater risk and price volatility than investments in larger, more mature companies. |

| |

| • | Value Stock Risk. Value stocks may continue to be undervalued by the market for extended periods, including the entire period during which the stock is held by the fund, or the events that the portfolio manager believed would cause the stock price to increase may not occur as anticipated or at all. Moreover, a stock judged to be undervalued actually may be appropriately priced at a low level and therefore would not be profitable for the fund. |

Exchange-Traded Funds ("ETFs") Risk. An ETF is subject to the risks associated with direct ownership of the securities in which the ETF invests or that comprise the index on which the ETF is based. Fund shareholders indirectly bear their proportionate share of the expenses of the ETFs in which the fund invests.

Fixed-Income Securities Risk. Fixed-income securities are subject to interest rate risk and credit quality risk. The market value of fixed-income securities generally declines when interest rates rise, and an issuer of fixed-income securities could default on its payment obligations.

Fund of Funds Risk. The performance and risks of a fund of funds directly correspond to the performance and risks of the underlying funds in which the fund invests. Fund shareholders bear indirectly their proportionate share of the expenses of other investment companies in which the fund invests.

Index Fund Risk. More likely than not, an index fund will underperform the index due to cash flows and the fees and expenses of the fund. The correlation between fund performance and index performance may also be affected by changes in securities markets, changes in the composition of the index and the timing of purchases and sales of fund shares.

Investment Company Securities Risk. Fund shareholders bear indirectly their proportionate share of the expenses of other investment companies in which the fund invests.

Portfolio Duration Risk. Portfolio duration is a measure of the expected life of a fixed-income security and its sensitivity to changes in interest rates. The longer a fund's average portfolio duration, the more sensitive the fund will be to changes in interest rates.

Real Estate Securities Risk. Investing in real estate securities subjects the fund to the risks associated with the real estate market (which are similar to the risks associated with direct ownership in real estate), including declines in real estate values, loss due to casualty or condemnation, property taxes, interest rate changes, increased expenses, cash flow of underlying real estate assets, regulatory changes (including zoning, land use and rents), and environmental problems, as well as to the risks related to the management skill and creditworthiness of the issuer.

Redemption Risk. A fund that serves as an underlying fund for a fund of funds is subject to certain risks. When a fund of funds reallocates or rebalances its investments, an underlying fund may experience relatively large redemptions or investments. These transactions may cause the underlying fund to sell portfolio securities to meet such redemptions, or to invest cash from such investments, at times it would not otherwise do so, and may as a result increase transaction costs and adversely affect underlying fund performance.

Securitized Products Risk. Investments in securitized products are subject to risks similar to traditional fixed income securities, such as credit, interest rate, liquidity, prepayment, extension, and default risk, as well as additional risks associated with the nature of the assets and the servicing of those assets. Unscheduled prepayments on securitized products may have to be reinvested at lower rates. A reduction in prepayments may increase the effective maturities of these securities, exposing them to the risk of decline in market value over time (extension risk).

U.S. Government Securities Risk. Yields available from U.S. government securities are generally lower than yields from many other fixed-income securities.

U.S. Government-Sponsored Securities Risk. Securities issued by U.S. government-sponsored or -chartered enterprises such as the Federal Home Loan Mortgage Corporation, the Federal National Mortgage Association, and the Federal Home Loan Banks are not issued or guaranteed by the U.S. Treasury.

Performance

The following information provides some indication of the risks of investing in the Acquiring and Acquired Funds by showing their performance from year to year and by showing how the Acquiring and Acquired Fund’s average annual returns for 1, 5, and 10 years compare with those of one or more broad measures of market performance. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis. The indices included in the performance tables are as follows: (1) Bloomberg Barclays U.S. Aggregate Bond Index is used to show performance of domestic, taxable fixed-income securities performance. (2) S&P 500 Index is used to show large cap U.S. equity market performance. (3) MSCI EAFE Index NDTR D is used to show international stock performance. (4) S&P Midcap 400 Index is used to show mid cap U.S. equity market performance. (5) S&P Smallcap 600 Index is used to show small cap U.S. equity market performance. (6) Diversified Balanced Custom Index is used to show the performance of the various asset classes used by the Account, and the Average Annual Total Returns table shows performance of the components of the custom index. The weightings for the custom index are 50% Bloomberg Barclays U.S. Aggregate Bond Index, 35% S&P 500 Index, 7% MSCI EAFE Index NDTR D, 4% S&P Midcap 400 Index, and 4% S&P Smallcap 600 Index.

Past performance is not necessarily an indication of how the Funds will perform in the future. Performance figures for the Funds do not include any separate account expenses, cost of insurance, or other contract-level expenses; total returns for the Funds would be lower if such expenses were included.

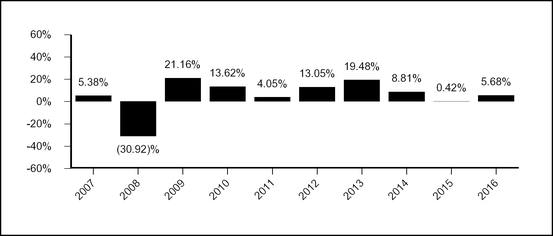

Calendar Year Total Return (%) as of 12/31 Each Year (Class 1 Shares)

Balanced Account (Acquired Fund)

|

| | |

| Highest return for a quarter during the period of the bar chart above: | Q3 ‘09 | 12.74% |

| Lowest return for a quarter during the period of the bar chart above: | Q4 '08 | (17.87)% |

|

| | | |

| Average Annual Total Returns |

| For the periods ended December 31, 2016 | 1 Year | 5 Years | 10 Years |

| Balanced Account - Class 1 | 5.68% | 9.30% | 4.98% |

| S&P 500 Index (reflects no deduction for fees, expenses, or taxes) | 11.96% | 14.66% | 6.95% |

| Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees, expenses, or taxes) | 2.65% | 2.23% | 4.34% |

| 60% S&P 500 Index/40% Bloomberg Barclays Aggregate Bond Index (reflects no deduction for fees, expenses, or taxes) | 8.31% | 9.69% | 6.21% |

For periods prior to the inception date of Class 1 Shares (May 1, 2017), the performance shown in the bar chart and table for Class 1 shares is based on the performance of the Account's Class 2 shares, adjusted to reflect the fees and expenses of the Class 1 shares. These adjustments for Class 1 shares result in performance for such periods that is no higher than the historical performance of the Class 2 shares, which were first sold on December 30, 2009.

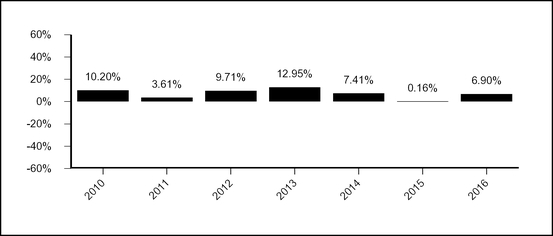

Calendar Year Total Return (%) as of 12/31 Each Year (Class 1 Shares)

Diversified Balanced Account (Acquiring Fund)

|

| | |

| Highest return for a quarter during the period of the bar chart above: | Q3 ‘10 | 6.79% |

| Lowest return for a quarter during the period of the bar chart above: | Q3 ‘11 | (6.34)% |

|

| | | |

| Average Annual Total Returns |

| For the periods ended December 31, 2016 | 1 Year | 5 Years | Life of Account |

| Diversified Balanced Account - Class 1 | 6.90% | 7.34% | 7.20% |

| Bloomberg Barclays U.S. Aggregate Bond Index (reflects no deduction for fees, expenses, or taxes) | 2.65% | 2.23% | 3.60% |

| S&P 500 Index (reflects no deduction for fees, expenses, or taxes) | 11.96% | 14.66% | 12.66% |

| MSCI EAFE Index NR (reflects no deduction for fees, expenses, or taxes) | 1.00% | 6.53% | 3.88% |

| S&P Midcap 400 Index (reflects no deduction for fees, expenses, or taxes) | 20.74% | 15.33% | 14.02% |

| S&P Smallcap 600 Index (reflects no deduction for fees, expenses, or taxes) | 26.56% | 16.62% | 15.32% |

| Diversified Balanced Custom Index (reflects no deduction for fees, expenses, or taxes) | 7.52% | 8.03% | 7.88% |

Board Consideration of the Reorganization

The Board, including the Independent Directors, considered the Reorganization pursuant to the Plan at its meeting on December 13, 2016. The Board considered information presented by PMC, and the Independent Directors were assisted by independent legal counsel. The Board requested and evaluated such information as it deemed necessary to consider the Reorganization. At the meeting, the Board unanimously approved the Reorganization after concluding that participation in the Reorganization is in the best interests of the Acquired Fund and the Acquiring Fund and that the interests of existing shareholders and contract owners of the Funds will not be diluted as a result of the Reorganization.

In determining whether to approve the Reorganization, the Board made inquiry into a number of matters and considered, among others, the following factors, in no order of priority:

| |

| (1) | the similar investment objectives, similar principal investment strategies, and identical fundamental investment restrictions of the Funds; |

| |

| (2) | the expense ratios and available information regarding the fees and expenses of the Funds; |

| |

| (3) | the comparative investment performance of the Funds for the periods the Board reviewed and other information pertaining to the Funds; |

| |

| (4) | the prospects for growth of and for achieving economies of scale by the Acquired Fund in combination with the Acquiring Fund; |

| |

| (5) | the estimated trading costs associated with disposing of any portfolio securities of the Acquired Fund and reinvesting the proceeds in connection with the Reorganization; |

| |

| (6) | the absence of any material differences in the rights of shareholders of the Funds; |

| |

| (7) | the financial strength, investment experience and resources of PMC, which currently serves as investment advisor to both funds; |

| |

| (8) | any direct or indirect benefits expected to be derived by PMC and its affiliates from the Reorganization; |

| |

| (9) | the direct or indirect federal income tax consequences of the Reorganization, including the expected taxable nature of the Reorganization and the impact of any federal income tax loss carry forwards and the estimated capital gain or loss expected to be incurred in connection with disposing of any portfolio securities that would not be compatible with the investment objectives and strategies of the Acquiring Fund; and managements representation that the taxable impact of the Reorganization would not flow through to the Contract Owners of the insurance separate accounts that own the Acquired Fund shares; |

| |

| (10) | PMC’s representation that the Reorganization will not result in any dilution of Acquired or Acquiring Fund shareholder interests; |

| |

| (11) | the terms and conditions of the Plan; and |

| |

| (12) | possible alternatives to the Reorganization. |

The Board’s decision to recommend approval of the Reorganization was based on a number of factors, including the following:

| |

| (1) | it should be reasonable for shareholders of the Acquired Fund to have similar investment expectations after the Reorganization because the Funds have similar investment objectives; |

| |

| (2) | PMC; as Investment Advisor of the Acquiring Fund, may be expected to provide high quality investment advisory services and personnel for the foreseeable future; |

| |

| (3) | the Acquiring Fund has a lower advisory fee rate and expense ratio than the Acquired Fund |

| |

| (4) | Acquired Fund shareholders are expected to benefit from a lower expense ratio after taking into account the Reorganization related costs to be borne by the Acquired Fund; and |

| |

| (5) | the Reorganization may be expected to afford shareholders of the Acquired Fund on an ongoing basis greater prospect for growth and efficient management. |

INFORMATION ABOUT THE REORGANIZATION

Plan of Acquisition

The terms of the Plan are summarized below. The summary is qualified in its entirety by reference to the Form of the Plan which is attached as Appendix A to this Proxy Statement/Prospectus.

Under the Plan, the Acquiring Fund will acquire all the assets and assume all the liabilities of the Acquired Fund. We expect that the closing date will be May 26, 2017, or such earlier or later date as PMC may determine, and that the Effective Time of the Reorganization will be as of the close of regularly scheduled trading on the NYSE (normally 3:00 p.m., Central Time) on that date. Each Fund will determine its net asset values as of the close of trading on the NYSE using the procedures described in its then current prospectus (the procedures applicable to the Acquired Fund and Acquiring Fund are identical). The Acquiring Fund will issue to the Acquired Fund a number of shares with a total value equal to the total value of the net assets of the corresponding share class of the Acquired Fund outstanding at the Effective Time.

Immediately after the Effective Time, the Acquired Fund will distribute to its shareholders Acquiring Fund shares of the same class as the Acquired Fund shares each shareholder owns in exchange for all Acquired Fund shares of that class. Acquired Fund shareholders will receive a number of full and fractional shares of the Acquiring Fund that are equal in value to the value of the shares of the Acquired Fund that are surrendered in the exchange. In connection with the exchange, the Acquiring Fund will credit on its books an appropriate number of its shares to the account of the Acquired Fund shareholder, and the Acquired Fund will cancel on its books all its shares registered to the account of that shareholder. After the Effective Time, the Acquired Fund will be terminated in accordance with applicable law.

The Plan may be amended, but no amendment may be made which in the opinion of the Board would materially adversely affect the interests of the shareholders of the Acquired Fund. The Board may abandon and terminate the Plan at any time before the Effective Time if it believes that consummation of the transactions contemplated by the Plan would not be in the best interests of the shareholders of either of the Funds.

Under the Plan, the Acquired Fund will pay all proxy expenses and out-of-pocket fees incurred in connection with the Reorganization. The Acquired Fund will also pay the trading costs associated with the Reorganization.

If the Plan is not consummated for any reason, the Board will consider other possible courses of action.

Description of the Securities to Be Issued

PVC is a Maryland corporation that is authorized to issue its shares of common stock in separate series and separate classes of series. The Acquired and Acquiring Funds are each a separate series of PVC, and the Class 1 shares of common stock of the Acquiring Fund to be issued in connection with the Reorganization represent interests in the assets belonging to that series and have identical dividend, liquidation and other rights, except that expenses allocated to a particular series or class are borne solely by that series or class and may cause differences in rights as described herein. The Acquiring Fund also issues Class 2 shares of common stock. Expenses related to the distribution of, and other identified expenses properly allocated to, the shares of a particular series or class are charged to, and borne solely by, that series or class, and the bearing of expenses by a particular series or class may be appropriately reflected in the net asset value attributable to, and the dividend and liquidation rights of, that series or class.

All shares of PVC have equal voting rights and are voted in the aggregate and not by separate series or class of shares except that shares are voted by series or class: (i) when expressly required by Maryland law or the 1940 Act and (ii) on any matter submitted to shareholders which the Board has determined affects the interests of only a particular series or class.

The share classes of the Acquired Fund have the same rights with respect to the Acquired Fund that the share classes of the Acquiring Fund have with respect to the Acquiring Fund.

Shares of both Funds, when issued, have no cumulative voting rights, are fully paid and non-assessable, have no preemptive or conversion rights and are freely transferable. Each fractional share has proportionately the same rights as are provided for a full share.

Federal Income Tax Consequences

To be considered a tax-free “reorganization” under Section 368 of the Internal Revenue Code of 1986, as amended (the “Code”), a reorganization must exhibit a continuity of business enterprise. Because of the differences in strategies between the Acquiring Fund and Acquiring Fund, the reorganization will likely be considered a taxable reorganization under applicable provisions of the Code.

The principal federal income tax considerations that are expected to result from the Reorganization include the following; the Acquired Fund will recognize gain or loss on the sale immediately before the Effective Time of all, or substantially all, of its assets for cash; the Acquired Fund more likely than not will recognize gain or loss on the transfer of its assets to the Acquiring Fund; each shareholder of the Acquired Fund more likely than not will recognize a taxable gain or loss equal to the difference between its tax basis in its Acquired Fund shares and the fair market value of the shares of the Acquiring Fund it receives; the Acquiring Fund will recognize no gain or loss as a result of the Reorganization; the aggregate tax basis of the shares of the Acquiring Fund to be received by a shareholder of the Acquired Fund to be received by a shareholder of the Acquired Fund more likely than not will be equal to the fair market value of such Acquiring Fund shares on the date of distribution; and the holding period of the shares of the Acquiring Fund received by a shareholder of the Acquired Fund more likely than not will begin on the day following the date of receipt of the Acquiring Fund shares.

The foregoing is only a summary of the principal federal income tax consequences of the Reorganization and should not be considered to be tax advice. There can be no assurance that the Internal Revenue Service will concur on all or any of the issues discussed above. You may wish to consult with your own tax advisors regarding the federal, state, and local tax consequences with respect to the foregoing matters and any other considerations which may apply in your particular circumstances.

CAPITALIZATION

The following tables show as of December 31, 2016: (i) the capitalization of the Acquired Fund; (ii) the capitalization of the Acquiring Fund; and (iii) the pro forma combined capitalization of the Acquiring Fund, adjusted to reflect the estimated expenses of the Reorganization, as if the Reorganization had occurred as of that date. As of December 31, 2016, the Acquired Fund had outstanding Class 1 shares and the Acquiring Fund had outstanding Class 2 shares.

The Acquired Fund will pay all expenses and out-of-pocket fees incurred in connection with the Reorganization. The expenses and fees Balanced Account will pay are expected to total $17,000. The Acquired Fund will pay any trading costs associated with disposing of any portfolio securities. These trading costs are estimated to be $55,000. The estimated gain (net of trading costs) would be approximately $2,841,000 ($1.18 per share) on a U.S. GAAP basis.

|

| | | | |

| | Net Assets (000s) | Net Asset Value Per Share | Shares Outstanding (000s) |

| Balanced Account (Acquired Fund) | Class 1 | $41,813 | $17.32 | 2,414 |

| | | $41,813 | | 2,414 |

| | | | | |

| Diversified Balanced Account (Acquiring Fund) | Class 2 | 1,099,647 | 14.76 | 74,510 |

| | | $1,099,647 | | 74,510 |

| | | | | |

| Reduction in net assets and decrease in net asset values per share of the Acquired Fund to reflect the estimated expenses of the trading costs associated with disposing of portfolio securities | Class 1 | $(72) | $(0.03) | (4) |

| | Class 2 | | | |

| | | | | |

| Increase in shares outstanding of the Acquired Fund to reflect the exchange for shares of the Acquiring Fund | Class 1 | | | 418 |

| | Class 2 | | | — |

| | | | | |

| Diversified Balanced Account (Acquiring Fund) | Class 1 | $41,741 | $14.76 | 2,828 |

| (pro forma assuming Reorganization) | Class 2 | 1,099,647 | 14.76 | 74,510 |

| | | $1,141,388 | | 77,338 |

ADDITIONAL INFORMATION ABOUT INVESTMENT STRATEGIES AND RISKS

The investment strategies identified in this section provide specific information about the Acquired and Acquiring Funds, but there are some general principles PMC and/or the sub-advisors apply in making investment decisions. When making decisions about whether to buy or sell equity securities, PMC and/or the sub-advisors may consider, among other things, a company's strength in fundamentals, its potential for earnings growth over time, its ability to navigate certain macroeconomic environments, and the current price of its securities relative to their perceived worth and relative to others in its industry. When making decisions about whether to buy or sell fixed-income investments, PMC and/or the sub-advisors may consider, among other things, the strength of certain sectors of the fixed- income market relative to others, interest rates, the macroeconomic backdrop, the balance between supply and demand for certain asset classes, other general market conditions, and the credit quality of individual issuers.

The Funds are designed to be a portion of an investor's portfolio. No Fund is intended to be a complete investment program. Investors should consider the risks of the Fund before making an investment and be prepared to maintain the investment during periods of adverse market conditions. It is possible to lose money by investing in the Funds.

The following table identifies whether the strategies and risks discussed in this section (listed in alphabetical order) are principal, non-principal, or not applicable to each Fund. The risks described below for the Acquiring Fund are risks at both the underlying funds level and the fund of funds level. The Acquiring Fund is also subject to the risks of the Underlying Funds in which it invest. The Statement of Additional Information ("SAI") contains additional information about investment strategies and their related risks.

|

| | |

| INVESTMENT STRATEGIES AND RISKS | BALANCED | DIVERSIFIED BALANCED |

| Bank Loans (also known as Senior Floating Rate Interests) | Non-Principal | Not Applicable |

| Convertible Securities | Non-Principal | Non-Principal |

| Derivatives | Non-Principal | Principal |

| Emerging Markets | Non-Principal | Non-Principal |

| Equity Securities | Principal | Principal |

| Exchange Traded Funds ("ETFs") | Non-Principal | Principal |

| Fixed-Income Securities | Principal | Principal |

| Foreign Securities | Principal | Non-Principal |

| Fund of Funds | Not Applicable | Principal |

| Hedging | Non-Principal | Non-Principal |

| High Yield Securities | Principal | Not Applicable |

| Leverage | Non-Principal | Non-Principal |

| Municipal Obligations and AMT-Subject Bonds | Non-Principal | Non-Principal |

| Portfolio Turnover (Active Trading) | Principal | Non-Principal |

| Preferred Securities | Non-Principal | Not Applicable |

| Real Estate Investment Trusts ("REITS") | Non-Principal | Non-Principal |

| Real Estate Securities | Principal | Principal |

| Securitized Products | Principal | Principal |

Bank Loans (also known as Senior Floating Rate Interests)

Bank loans typically hold the most senior position in the capital structure of a business entity (the "Borrower"), are secured by specific collateral, and have a claim on the Borrower's assets and/or stock that is senior to that held by the Borrower's unsecured subordinated debtholders and stockholders. The proceeds of bank loans primarily are used to finance leveraged buyouts, recapitalizations, mergers, acquisitions, stock repurchases, dividends, and, to a lesser extent, to finance internal growth and for other corporate purposes. Bank loans are typically structured and administered by a financial institution that acts as the agent of the lenders participating in the bank loan. Most bank loans that will be purchased by a fund are rated below-investment-grade (sometimes called “junk”) or will be comparable if unrated, which means they are more likely to default than investment-grade loans. A default could lead to non-payment of income which would result in a reduction of income to the fund, and there can be no assurance that the liquidation of any collateral would satisfy the Borrower's obligation in the event of non-payment of scheduled interest or principal payments, or that such collateral could be readily liquidated. Most bank loans are not traded on any national securities exchange. Bank loans generally have less liquidity than investment-grade bonds and there may be less public information available about them. Bank loan interests may not be considered “securities,” and purchasers therefore may not be entitled to rely on the anti-fraud protections of the federal securities laws.

The primary and secondary market for bank loans may be subject to irregular trading activity, wide bid/ask spreads and extended trade settlement periods, which may cause a fund to be unable to realize full value and thus cause a material decline in a fund's net asset value. Because transactions in bank loans may be subject to extended settlement periods, a fund may not receive proceeds from the sale of a bank loan for a period of time after the sale. As a result, sale proceeds may not be available to make additional investments or to meet a fund’s redemption obligations for a period of time after the sale of the bank loans, which could lead to a fund having to sell other investments, borrow to meet obligations, or borrow to remain fully invested while awaiting settlement.

Bank loans pay interest at rates which are periodically reset by reference to a base lending rate plus a spread. These base lending rates are generally the prime rate offered by a designated U.S. bank or the London Interbank Offered Rate (LIBOR) or the prime rate offered by one or more major U.S. banks.

Bank loans generally are subject to mandatory and/or optional prepayment. Because of these prepayment conditions and because there may be significant economic incentives for the borrower to repay, prepayments may occur.

Convertible Securities

Convertible securities are usually fixed-income securities that a fund has the right to exchange for equity securities at a specified conversion price. Convertible securities could also include corporate bonds, notes, or preferred stocks of U.S. or foreign issuers. Convertible securities allow a fund to realize additional returns if the market price of the equity securities exceeds the conversion price. For example, a fund may hold fixed-income securities that are convertible into shares of common stock at a conversion price of $10 per share. If the market value of the shares of common stock reached $12, the fund could realize an additional $2 per share by converting its fixed-income securities.

Convertible securities have lower yields than comparable fixed-income securities. In addition, at the time a convertible security is issued the conversion price exceeds the market value of the underlying equity securities. Thus, convertible securities may provide lower returns than non-convertible fixed-income securities or equity securities depending upon changes in the price of the underlying equity securities. However, convertible securities permit a fund to realize some of the potential appreciation of the underlying equity securities with less risk of losing its initial investment.

Depending on the features of the convertible security, a fund will treat a convertible security as a fixed-income security, equity security, or preferred security for purposes of investment policies and limitations because of the unique characteristics of convertible securities. Funds that invest in convertible securities may invest in convertible securities that are below investment grade. Many convertible securities are relatively illiquid.

Derivatives

Generally, a derivative is a financial arrangement, the value of which is derived from, or based on, a traditional security, asset, or market index. A fund may invest in certain derivative strategies to earn income, manage or adjust the risk profile of the fund, replace more direct investments, or obtain exposure to certain markets. A fund may enter into forward commitment agreements, which call for the fund to purchase or sell a security on a future date at a fixed price. A fund may also enter into contracts to sell its investments either on demand or at a specific interval.

The risks associated with derivative investments include:

| |

| • | increased volatility of a fund; |

| |

| • | the inability of those managing investments of the fund to predict correctly the direction of securities prices, interest rates, currency exchange rates, asset values, and other economic factors; |

| |

| • | losses caused by unanticipated market movements, which may be substantially greater than a fund's initial investment and are potentially unlimited; |

| |

| • | the possibility that there may be no liquid secondary market, which may make it difficult or impossible to close out a position when desired; |

| |

| • | the possibility that the counterparty may fail to perform its obligations; and |

| |

| • | the inability to close out certain hedged positions to avoid adverse tax consequences. |

There are many different types of derivatives and many different ways to use them.

| |

| • | Commodity Index-Linked Notes are derivative debt instruments issued by U.S. and foreign banks, brokerage firms, insurance companies and other corporations with principal and/or coupon payments linked to the performance of commodity indices. These notes expose a fund to movements in commodity prices. They are also subject to credit, counterparty, and interest rate risk. Commodity index-linked notes are often leveraged, increasing the volatility of each note's market value relative to changes in the underlying commodity index. At the maturity of the note, a fund may receive more or less principal than it originally invested. A fund may also receive interest payments on the note that are less than the stated coupon interest payments. |

| |

| • | Credit Default Swap Agreements may be entered into by a fund as a "buyer" or "seller" of credit protection. Credit default swap agreements involve special risks because they may be difficult to value, are highly susceptible to liquidity and credit risk, and generally pay a return to the party that has paid the premium only in the event of an actual default by the issuer of the underlying obligation (as opposed to a credit downgrade or other indication of financial difficulty). Credit default swaps can increase credit risk because a fund has exposure to both the issuer of the referenced obligation and the counterparty to the credit default swap. |

| |

| • | Foreign Currency Contracts (such as foreign currency options and foreign currency forward and swap agreements) may be used by funds to increase exposure to a foreign currency or to shift exposure to foreign currency fluctuations from one country to another. A forward currency contract involves a privately negotiated obligation to purchase or sell a specific currency at a future date at a price set in the contract. For currency contracts, there is also a risk of government action through exchange controls that would restrict the ability of a fund to deliver or receive currency. |

| |

| • | Forwards, futures contracts and options thereon (including commodities futures); options (including put or call options); and swap agreements and over-the-counter swap agreements (e.g., interest rate swaps, total return swaps and credit default swaps) may be used by funds for hedging purposes in an effort to protect a fund from loss due to changing interest rates, securities prices, asset values, currency exchange rates, and other market conditions; non-hedging purposes to seek to increase the fund’s income or otherwise enhance return; and as a low-cost method of gaining exposure to a particular market without investing directly in those securities or assets. These derivative investments are subject to special risk considerations, particularly the imperfect correlation between the change in market value of the instruments held by a fund and the price of the derivative instrument. If a fund has insufficient cash, it may have to sell securities from its portfolio to meet daily variation margin requirements, even when it may be disadvantageous to do so. Options and Swap Agreements also involve counterparty risk. With respect to options, there may be difference in trading hours for the options markets and the markets for the underlying securities (rate movements can take place in the underlying markets that cannot be reflected in the options markets) and an insufficient liquid secondary market for particular options. |

| |

| • | Index/structured securities. Certain derivative securities are described more accurately as index/structured securities, which are derivative securities whose value or performance is linked to other equity securities (such as depositary receipts), currencies, interest rates, indices, or other financial indicators (reference indices). |

Emerging Markets

Emerging market securities are defined as those issued by:

| |

| • | companies with their principal place of business or principal office in emerging market countries or |

| |

| • | companies whose principal securities trading market is an emerging market country. |