UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21497

ALLIANCEBERNSTEIN CORPORATE SHARES

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: April 30, 2009

Date of reporting period: April 30, 2009

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

2

ANNUAL REPORT

AllianceBernstein

Corporate Income Shares

April 30, 2009

Annual Report

Investment Products Offered

| • | Are Not FDIC Insured |

| • | May Lose Value |

| • | Are Not Bank Guaranteed |

The investment return and principal value of an investment in the Fund will fluctuate as the prices of the individual securities in which it invests fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. You should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For a free copy of the Fund’s prospectus, which contains this and other information, visit our web site at www.alliancebernstein.com or call your financial advisor or AllianceBernstein® at (800) 227-4618. Please read the prospectus carefully before you invest.

You may obtain performance information current to the most recent month-end by visiting www.alliancebernstein.com.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AllianceBernstein’s web site at www.alliancebernstein.com, or go to the Securities and Exchange Commission’s (the “Commission”) web site at www.sec.gov, or call AllianceBernstein at (800) 227-4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s web site at www.sec.gov. The Fund’s Forms N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. AllianceBernstein publishes full portfolio holdings for the Fund monthly at www.alliancebernstein.com.

AllianceBernstein Investments, Inc. is an affiliate of AllianceBernstein L.P., the manager of the AllianceBernstein funds, and is a member of FINRA.

AllianceBernstein® and the AB Logo are registered trademarks and service marks used by permission of the owner, AllianceBernstein L.P.

June 15, 2009

Annual Report

This report provides management’s discussion of fund performance for AllianceBernstein Corporate Income Shares (the “Fund”) for the annual reporting period ended April 30, 2009. Please note that shares of this Fund are offered exclusively through registered investment advisers approved by the Adviser.

Investment Objective and Policies

The Fund’s investment objective is high current income. The Fund invests, under normal circumstances, at least 80% of its net assets in US corporate bonds. The Fund may also invest in US Government securities (other than US Government securities that are mortgage-backed or asset-backed securities), repurchase agreements and forward contracts relating to US Government securities. The Fund normally invests all of its assets in securities that are rated, at the time of purchase, at least BBB- or the equivalent. The Fund will not invest in unrated corporate debt securities. The Fund has the flexibility to invest in long- and short-term fixed-income securities. In making decisions about whether to buy or sell securities, the Fund will consider, among other things, the strength of certain sectors of the fixed-income market relative to others, interest rates and other general market conditions and the credit quality of individual issuers. The Fund also may invest in convertible debt securities; invest up to 10% of its assets in inflation-protected securities; invest up to 5% of its net assets in preferred stock; purchase and sell interest rate futures contracts and options; enter

into swap transactions; invest in zero coupon securities and payment-in-kind debentures; and make secured loans of portfolio securities.

Investment Results

The table on page 5 shows the Fund’s performance compared to its benchmark, the Barclays Capital US Credit Index, for the six and 12-month periods ended April 30, 2009.

The Corporate Income Shares Fund underperformed its benchmark for the six- and 12-month periods as the credit crisis intensified and spreads continued to widen across non-government sectors of the fixed-income markets. Corporate security selection, particularly an overweight to financials which underperformed, detracted from performance for both periods. The Fund’s overweight in BBB-rated issues and underweight in the non-corporate portion of the credit index detracted for the 12-month period but helped for the six-month period, as credit markets rallied strongly in April. Lastly, the Fund’s underweight in long-maturity corporates and an allocation to Treasuries hurt during the six-month period and helped for the 12-month period ended April 30, 2009.

Market Review and Investment Strategy

Extreme risk aversion that seized the markets following the bankruptcy of Lehman Brothers in mid-September accelerated into the fourth quarter of 2008 as massive global deleveraging continued. Tumult in the financial markets bled into the real economy, in

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 1 |

the US and across the globe. Economic data for virtually every country experienced a significant downturn. Investors flocked to the safety of governments and credit markets experienced an extreme sell-off. The yield on US Treasury bills reached near zero, showing that investors were willing to forgo a return on their investment in exchange for a safe place to park their cash. While global government bond yields hit or neared record lows, yield spreads on investment-grade corporate bonds shot to peaks unseen since the 1930s.

In an effort to restart borrowing, central banks around the world aggressively slashed interest rates. Official rates in the US, Switzerland and Japan are now near zero. Monetary authorities also unveiled an array of unorthodox measures including directly purchasing assets such as mortgages and long-term Treasuries. Additionally, governments in both developed and developing countries have pledged a record dose of fiscal stimulus including a mix of tax cuts and infrastructure spending to help cushion the impact of the downturn.

Challenges continued into the first quarter of 2009 as asset prices in many markets continued to fall and policymakers scrambled to combat the severe global economic slowdown. Volatility remained high, although below the peaks of late 2008. Late in the quarter and into April, however, signs emerged that the deepest recession since the great depression was beginning to bottom. Optimism prevailed in April with reports of

increased consumer confidence, modest growth in consumer spending and a slower pace of job losses. Credit sensitive sectors rallied strongly in April, with corporates posting their strongest monthly excess returns versus Treasuries on record for the month.

For the annual reporting period, credit markets posted a return of -3.15% with non-corporates at -0.03% outperforming corporates at -4.26%. By industry, corporate returns were mixed for the period. Outperforming industries included consumer non-cyclicals at 5.90%, aerospace/defense at 5.26% and consumer products at 4.46%. Underperforming industries included building materials at -13.08%, financial institutions at -12.45% and metals & mining at -7.13%. Intermediate credit at -1.69% outperformed long credit at -7.49% as longer-maturity securities were negatively impacted more by extraordinary market volatility. By quality, less risk averse higher rated quality tiers generally outperformed with AAA-rated debt returning 1.97%, followed by AA at -1.50%, BBB at -3.65% and finally A-rated debt at -5.88%.

The global economy and financial markets continue to face real challenges. The timing of recovery remains unclear and uncertainty still surrounds government actions and their impact on the economy. However, the Fund’s Corporate Income Shares Investment Team (the “Team”) believes that powerful forces for a recovery are gathering. Across the capital markets, strong recoveries typically follow very

| 2 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

weak periods. These market upturns tend to come swiftly, often before there is solid evidence of an economic turnaround (i.e. April/May 2009’s strong rebound in equity and credit sensitive markets).

The Team believes the recent turmoil has created opportunities not seen in generations. While Fund performance tracked the indices lower as the credit crisis deepened, the Team believes the Fund is well positioned for recovery.

The recent turmoil has created compelling valuations in fixed-income markets and wide yield spreads are compensating investors generously as they wait for a recovery. Risk premiums over governments are near historic highs in many industries. The Team believes more than at any time in recent history, investors are likely to be well rewarded for sticking to a disciplined, long-term approach to asset allocation.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 3 |

HISTORICAL PERFORMANCE

An Important Note About the Value of Historical Performance

The performance on the following pages represents past performance and does not guarantee future results. The Fund is relatively new and has been in existence for less than three years. The returns reflected may not be illustrative of long-term performance. Current performance may be lower or higher than the performance information shown. All fees and expenses related to the operation of the Fund have been deducted. Performance assumes reinvestment of distributions and does not account for taxes.

Benchmark Disclosure

The unmanaged Barclays Capital US Credit Index does not reflect fees and expenses associated with the active management of a fund portfolio. The Index comprises the Barclays Capital US Corporate Index and the Barclays Capital US Non-Corporate Credit Index (the non-native currency subcomponent of the Barclays Capital US Government-Related Index). An investor cannot invest directly in an index, and its results are not indicative of the performance for any specific investment, including the Fund.

A Word About Risk

Price fluctuation in the Fund’s securities may be caused by changes in the general level of interest rates or changes in bond credit quality ratings. Please note, as interest rates rise, existing bond prices fall and can cause the value of an investment in the Fund to decline. Changes in interest rates have a greater effect on bonds with longer maturities than those with shorter maturities. Similar to direct bond ownership, bond funds have the same interest rate, inflation and credit risks that are associated with the underlying bonds owned by the Fund. The Fund can utilize leverage as an investment strategy. When a fund borrows money or otherwise leverages its portfolio, it may be volatile because leverage tends to exaggerate the effect of any increase or decrease in the value of a Fund’s investments. The Fund may create leverage through the use of derivatives. High yield bonds, otherwise known as “junk bonds,” involve a greater risk of default and price volatility than other bonds. Investing in below-investment grade securities presents special risks, including credit risk. Investments in the Fund are not guaranteed because of fluctuation in the net asset value of the underlying fixed-income related investments. The Fund is subject to liquidity risk because derivatives and securities involving substantial interest rate and credit risk tend to involve greater liquidity risk. While the Fund invests principally in bonds and other fixed-income securities, in order to achieve its investment objective, the Fund may at times use certain types of investment derivatives, such as options, futures, forwards and swaps. These instruments involve risks different from, and in certain cases, greater than, the risks presented by more traditional investments. These risks are fully discussed in the Fund’s prospectus.

(Historical Performance continued on next page)

| 4 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

| THE FUND VS. ITS BENCHMARK PERIODS ENDED APRIL 30, 2009 | Returns | |||||

| 6 Months | 12 Months | |||||

AllianceBernstein Corporate Income Shares | 9.79% | -7.76% | ||||

Barclays Capital* US Credit Index | 11.47% | -3.15% | ||||

* Formerly Lehman Brothers. | ||||||

GROWTH OF A $10,000 INVESTMENT IN THE FUND 12/11/06* TO 4/30/09

*Since the Portfolio’s Inception on 12/11/06.

This chart illustrates the total value of an assumed $10,000 investment in AllianceBernstein Corporate Income Shares (from 12/11/06 to 4/30/09) as compared to the performance of the Fund’s benchmark.

See Historical Performance and Benchmark disclosures on previous page.

(Historical Performance continued on next page)

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 5 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

| AVERAGE ANNUAL RETURNS AS OF APRIL 30, 2009 | |||

Returns | |||

1 Year | -7.76 | % | |

Since Inception* | -1.96 | % | |

| SEC AVERAGE ANNUAL RETURNS (WITH ANY APPLICABLE SALES CHARGES) AS OF THE MOST RECENT CALENDAR QUARTER-END (MARCH 31, 2009) | |||

| Returns | |||

1 Year | -10.11 | % | |

Since Inception* | -3.36 | % | |

The Fund’s current prospectus fee table shows the Fund’s total operating expense ratio as 0.35% and the Fund’s net expense ratio as 0.00%, reflecting the fact that the Adviser is absorbing all expenses of operating the Fund, except extraordinary expenses, and is waiving any fees from the Fund. The Fund is an integral part of “wrap fee” programs sponsored by investment advisers unaffiliated with the Fund or the Adviser. Typically, participants in these programs pay a “wrap” fee to their investment adviser for all costs and expenses of the wrap-fee program, including investment advice and portfolio execution. The Fund’s total operating expense ratio reflects the estimated portion of the wrap fee attributable to the management of the Fund. Absent reimbursements or waivers, performance would have been lower.

| * | Inception Date: 12/11/06. |

See Historical Performance disclosures on page 4.

| 6 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Historical Performance

FUND EXPENSES

(unaudited)

As a shareholder of a mutual fund, you may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the hypothetical example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value November 1, 2008 | Ending Account Value April 30, 2009 | Expenses Paid During Period* | ||||||||||||||||

| Actual | Hypothetical | Actual | Hypothetical** | Actual | Hypothetical | |||||||||||||

| Class A | $ | 1,000 | $ | 1,000 | $ | 1,097.90 | $ | 1,024.79 | $ | 0.00 | $ | 0.00 | ||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 0.00%. The Fund’s expenses are borne by the Adviser or it affiliates. |

| ** | Assumes 5% return before expenses. |

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 7 |

Fund Expenses

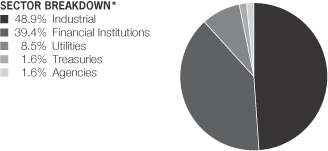

PORTFOLIO SUMMARY

April 30, 2009 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $57.0

| * | All data are as of April 30, 2009. The Fund’s sector breakdown is expressed as a percentage of total investments and may vary over time. |

Please Note: The issuer classifications presented herein are based on the Barclays Capital Fixed Income Indices developed by Barclays Capital. The fund components are divided either into duration, country, bond ratings or corporate sectors as classified by Barclays Capital. These sector classifications are broadly defined. The “Portfolio of Investments” section of the report reflects more specific industry information and is consistent with the investment restrictions discussed in the fund’s prospectus.

| 8 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio Summary

PORTFOLIO OF INVESTMENTS

April 30, 2009

| Principal Amount (000) | U.S. $ Value | |||||

CORPORATES - INVESTMENT | ||||||

Industrial – 44.0% | ||||||

Basic – 4.3% | ||||||

Commercial Metals Co. | $ | 400 | $ | 286,520 | ||

The Dow Chemical Co. | 430 | 305,405 | ||||

Eastman Chemical Co. | 305 | 261,461 | ||||

Freeport-McMoRan Copper & Gold, Inc. | 490 | 482,650 | ||||

International Paper Co. | 400 | 347,981 | ||||

The Mosaic Co. | 225 | 226,125 | ||||

PPG Industries, Inc. | 170 | 173,005 | ||||

6.65%, 3/15/18 | 85 | 81,264 | ||||

Weyerhaeuser Co. | 360 | 272,671 | ||||

| 2,437,082 | ||||||

Capital Goods – 3.9% | ||||||

Boeing Co. | 140 | 147,220 | ||||

Caterpillar, Inc. | 445 | 400,191 | ||||

CRH America, Inc. | 695 | 584,639 | ||||

Dover Corp. | 350 | 354,390 | ||||

General Electric Co. | 520 | 492,076 | ||||

Vulcan Materials Co. | 295 | 256,444 | ||||

| 2,234,960 | ||||||

Communications - Media – 5.1% | ||||||

CBS Corp. | 220 | 211,441 | ||||

7.875%, 7/30/30 | 85 | 59,871 | ||||

Comcast Cable Communications Holdings, Inc. | 175 | 196,251 | ||||

9.455%, 11/15/22 | 455 | 528,755 | ||||

News America Holdings, Inc. | 415 | 394,871 | ||||

RR Donnelley & Sons Co. | 675 | 516,830 | ||||

5.50%, 5/15/15 | 210 | 158,331 | ||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 9 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

TCI Communications, Inc. | $ | 150 | $ | 143,600 | ||

Time Warner Entertainment Co. LP | 350 | 377,860 | ||||

10.15%, 5/01/12 | 270 | 304,241 | ||||

| 2,892,051 | ||||||

Communications - Telecommunications – 5.6% | ||||||

Ameritech Capital Funding Corp. | 605 | 588,996 | ||||

6.55%, 1/15/28 | 760 | 634,509 | ||||

Bellsouth Capital Funding Corp. | 565 | 454,401 | ||||

Embarq Corp. | 150 | 144,750 | ||||

Qwest Corp. | 185 | 175,287 | ||||

8.875%, 3/15/12 | 100 | 101,500 | ||||

US Cellular Corp. | 135 | 106,613 | ||||

Valor Telecommunications Enterprises | 55 | 54,175 | ||||

Verizon New York, Inc. | 595 | 547,317 | ||||

Verizon Virginia, Inc. | 375 | 368,279 | ||||

| 3,175,827 | ||||||

Consumer Cyclical - Automotive – 1.5% | ||||||

Daimler Finance North America LLC | 310 | 313,582 | ||||

Johnson Controls, Inc. | 635 | 552,536 | ||||

| 866,118 | ||||||

Consumer Cyclical - Entertainment – 1.0% | ||||||

Historic TW, Inc. | 80 | 85,327 | ||||

Time Warner Cos, Inc. | 120 | 110,395 | ||||

Turner Broadcasting System, Inc. | 350 | 362,706 | ||||

| 558,428 | ||||||

Consumer Cyclical - Other – 1.3% | ||||||

Marriott International, Inc. | 250 | 234,191 | ||||

| 10 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

Toll Brothers Finance Corp. | $ | 620 | $ | 504,610 | ||

| 738,801 | ||||||

Consumer Cyclical - Retailers – 1.2% | ||||||

Home Depot, Inc. | 315 | 302,567 | ||||

Kohls Corp. | 255 | 246,431 | ||||

Nordstrom, Inc. | 160 | 124,475 | ||||

| 673,473 | ||||||

Consumer Non-Cyclical – 11.6% | ||||||

Abbott Laboratories | 305 | 313,871 | ||||

Allergan, Inc. | 520 | 498,302 | ||||

AmerisourceBergen Corp. | 305 | 292,710 | ||||

Amgen, Inc. | 320 | 328,756 | ||||

Anheuser-Busch Cos, Inc. | 210 | 198,594 | ||||

6.50%, 2/01/43 | 250 | 195,801 | ||||

Archer-Daniels-Midland Co. | 245 | 290,645 | ||||

Avon Products, Inc. | 145 | 148,470 | ||||

Bristol-Myers Squibb Co. | 275 | 258,269 | ||||

Bunge Ltd. Finance Corp. | 705 | 630,859 | ||||

ConAgra Foods, Inc. | 300 | 358,284 | ||||

Fisher Scientific International, Inc. | 140 | 139,300 | ||||

Fortune Brands, Inc. | 100 | 87,316 | ||||

The Kroger Co. | 435 | 474,638 | ||||

Merck & Co., Inc. | 325 | 337,986 | ||||

Pepsi Bottling Group, Inc. | 127 | 138,487 | ||||

Pfizer, Inc. | 135 | 145,123 | ||||

Quest Diagnostics, Inc. | 370 | 345,018 | ||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 11 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

Reynolds American, Inc. | $ | 165 | $ | 150,464 | ||

Safeway, Inc. | 570 | 612,369 | ||||

Sara Lee Corp. | 340 | 325,716 | ||||

Schering-Plough Corp. | 315 | 333,978 | ||||

| 6,604,956 | ||||||

Energy – 2.8% | ||||||

Amerada Hess Corp. | 154 | 146,151 | ||||

ConocoPhillips | 390 | 412,754 | ||||

Duke Capital LLC | 155 | 153,473 | ||||

Halliburton Co. | 240 | 232,916 | ||||

Nabors Industries, Inc. | 150 | 141,574 | ||||

Noble Energy, Inc. | 143 | 155,837 | ||||

The Premcor Refining Group, Inc. | 366 | 363,924 | ||||

| 1,606,629 | ||||||

Services – 0.8% | ||||||

The Western Union Co. | 515 | 492,015 | ||||

Technology – 3.2% | ||||||

Cisco Systems, Inc. | 132 | 140,341 | ||||

Electronic Data Systems Corp. | 305 | 326,214 | ||||

International Business Machines Corp. | 445 | 440,339 | ||||

Motorola, Inc. | 560 | 411,700 | ||||

Oracle Corp. | 135 | 143,025 | ||||

Xerox Corp. | 325 | 266,500 | ||||

7.625%, 6/15/13 | 100 | 92,000 | ||||

| 1,820,119 | ||||||

Transportation - Airlines – 0.9% | ||||||

Southwest Airlines Co. | 550 | 507,490 | ||||

| 12 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

Transportation - Railroads – 0.8% | ||||||

CSX Corp. | $ | 460 | $ | 484,428 | ||

| 25,092,377 | ||||||

Financial Institutions – 36.1% | ||||||

Banking – 22.9% | ||||||

Bank of America Corp. | 500 | 352,276 | ||||

The Bear Stearns Co., Inc. | 575 | 511,445 | ||||

Capital One Financial Corp. | 168 | 101,502 | ||||

Citigroup, Inc. | 570 | 369,050 | ||||

5.00%, 9/15/14 | 565 | 387,001 | ||||

5.50%, 2/15/17 | 320 | 220,636 | ||||

5.85%, 7/02/13 | 365 | 326,682 | ||||

6.125%, 8/25/36 | 115 | 68,014 | ||||

Comerica Bank | 560 | 414,594 | ||||

Countrywide Financial Corp. | 318 | 236,594 | ||||

Credit Suisse USA, Inc. | 550 | 535,092 | ||||

Fifth Third Bancorp | 520 | 482,248 | ||||

Fifth Third Bank | 395 | 287,186 | ||||

First Union Institutional Capital I | 360 | 236,690 | ||||

FleetBoston Financial Corp. | 180 | 110,862 | ||||

The Goldman Sachs Group, Inc. | 250 | 236,902 | ||||

5.625%, 1/15/17 | 530 | 454,046 | ||||

6.125%, 2/15/33 | 815 | 710,027 | ||||

HSBC Bank USA | 475 | 461,605 | ||||

JP Morgan Chase & Co. | 345 | 342,773 | ||||

5.375%, 1/15/14 | 515 | 524,307 | ||||

6.125%, 6/27/17 | 255 | 238,002 | ||||

JP Morgan Chase Capital XXV | 300 | 219,636 | ||||

Manufacturers & Traders Trust Co. | 270 | 169,835 | ||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 13 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

Marshall & Ilsley Bank | $ | 300 | $ | 199,925 | ||

Merrill Lynch & Co., Inc. | 190 | 124,563 | ||||

6.11%, 1/29/37 | 440 | 257,042 | ||||

6.15%, 4/25/13 | 520 | 478,088 | ||||

Morgan Stanley | 535 | 532,160 | ||||

5.30%, 3/01/13 | 160 | 155,709 | ||||

6.00%, 4/28/15 | 100 | 94,461 | ||||

7.25%, 4/01/32 | 130 | 119,820 | ||||

National City Bank | 395 | 350,308 | ||||

PNC Bank NA | 250 | 209,150 | ||||

SouthTrust Corp. | 500 | 437,593 | ||||

Sovereign Bank | 335 | 273,171 | ||||

State Street Corp. | 95 | 84,289 | ||||

Union Bank of California | 555 | 425,711 | ||||

Union Planters Corp. | 341 | 326,246 | ||||

Wachovia Corp. | 200 | 174,973 | ||||

5.25%, 8/01/14 | 360 | 319,954 | ||||

Wells Fargo & Co. | 410 | 394,641 | ||||

4.625%, 4/15/14 | 100 | 87,967 | ||||

| 13,042,776 | ||||||

Brokerage – 0.5% | ||||||

Ameriprise Financial, Inc. | 200 | 173,517 | ||||

Schwab Capital Trust I | 145 | 100,568 | ||||

| 274,085 | ||||||

Finance – 3.2% | ||||||

General Electric Capital Corp. | 90 | 84,031 | ||||

5.40%, 2/15/17 | 520 | 453,315 | ||||

6.375%, 11/15/67(c) | 520 | 298,476 | ||||

HSBC Finance Capital Trust IX | 570 | 259,025 | ||||

International Lease Finance Corp. | 530 | 298,632 | ||||

Series MTN | 106 | 61,863 | ||||

| 14 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

SLM Corp. | $ | 385 | $ | 221,799 | ||

5.45%, 4/25/11 | 180 | 147,644 | ||||

| 1,824,785 | ||||||

Insurance – 6.1% | ||||||

Ace INA Holdings, Inc. | 225 | 223,553 | ||||

Aetna, Inc. | 360 | 346,078 | ||||

The Allstate Corp. | 165 | 163,352 | ||||

Assurant, Inc. | 110 | 87,715 | ||||

Fund American Cos, Inc. | 635 | 494,434 | ||||

GE Global Insur | 290 | 226,768 | ||||

Genworth Financial, Inc. | 510 | 149,603 | ||||

Series MTN | 180 | 57,119 | ||||

Hartford Financial Services Group, Inc. | 330 | 172,913 | ||||

Humana, Inc. | 215 | 179,846 | ||||

Marsh & McLennan Cos, Inc. | 295 | 290,984 | ||||

5.375%, 7/15/14 | 165 | 143,770 | ||||

Prudential Financial, Inc. | 130 | 105,541 | ||||

Series MTNB | 285 | 231,869 | ||||

The Travelers Cos, Inc. | 230 | 232,047 | ||||

UnitedHealth Group, Inc. | 140 | 131,017 | ||||

WellPoint, Inc. | 250 | 253,562 | ||||

| 3,490,171 | ||||||

REITS – 3.4% | ||||||

ERP Operating LP | 560 | 482,953 | ||||

Health Care Property Investors, Inc. | 585 | 510,985 | ||||

Health Care REIT, Inc. | 585 | 460,296 | ||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 15 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

Simon Property Group LP | $ | 575 | $ | 497,415 | ||

| 1,951,649 | ||||||

| 20,583,466 | ||||||

Utility – 8.2% | ||||||

Electric – 5.6% | ||||||

Allegheny Energy Supply Co. LLC | 295 | 303,534 | ||||

8.25%, 4/15/12(a) | 95 | 95,947 | ||||

Consolidated Edison Co. of New York, Inc. | 115 | 115,316 | ||||

Constellation Energy Group, Inc. | 140 | 113,908 | ||||

Consumers Energy Co. | 165 | 167,533 | ||||

Dominion Resources, Inc. | 370 | 233,100 | ||||

Series 06-B | 315 | 179,550 | ||||

Series C | 80 | 77,626 | ||||

FirstEnergy Corp. | 167 | 142,373 | ||||

MidAmerican Energy Co. | 285 | 291,259 | ||||

Nisource Finance Corp. | 710 | 614,251 | ||||

6.15%, 3/01/13 | 130 | 120,384 | ||||

Pacific Gas & Electric Co. | 195 | 200,554 | ||||

PPL Capital Funding, Inc. | 370 | 214,600 | ||||

PSEG Power LLC | 105 | 107,486 | ||||

Public Service Company of Colorado | 170 | 188,536 | ||||

| 3,165,957 | ||||||

Natural Gas – 2.6% | ||||||

CenterPoint Energy Resources Corp. | 115 | 120,604 | ||||

Colorado Interstate Gas Co. | 115 | 114,258 | ||||

| 16 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

Energy Transfer Partners LP | $ | 535 | $ | 491,368 | ||

Enterprise Products Operating LP | 360 | 370,006 | ||||

Kinder Morgan Energy Partners LP | 95 | 83,664 | ||||

Southern Union Co. | 60 | 48,214 | ||||

Williams Co., Inc. | 285 | 280,725 | ||||

| 1,508,839 | ||||||

| 4,674,796 | ||||||

Total Corporates – Investment Grades | 50,350,639 | |||||

CORPORATES - NON-INVESTMENT GRADES – 4.8% | ||||||

Industrial – 3.0% | ||||||

Basic – 0.6% | ||||||

United States Steel Corp. | 550 | 378,183 | ||||

Capital Goods – 1.9% | ||||||

Masco Corp. | 680 | 496,601 | ||||

Mohawk Industries, Inc. | 525 | 445,045 | ||||

Textron Financial Corp. | 170 | 124,993 | ||||

| 1,066,639 | ||||||

Consumer Cyclical - Other – 0.5% | ||||||

Sheraton Holding Corp. | 360 | 292,500 | ||||

| 1,737,322 | ||||||

Financial Institutions – 1.8% | ||||||

Banking – 1.0% | ||||||

BankAmerica Capital II | 237 | 141,949 | ||||

RBS Capital Trust I | 340 | 122,400 | ||||

RBS Capital Trust III | 500 | 185,000 | ||||

Zions Banc Corp. | 155 | 80,882 | ||||

5.65%, 5/15/14 | 75 | 35,028 | ||||

| 565,259 | ||||||

Finance – 0.6% | ||||||

CIT Group, Inc. | 605 | 318,175 | ||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 17 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||

Insurance – 0.2% | ||||||

American International Group, Inc. | $ | 495 | $ | 61,875 | ||

Genworth Financial, Inc. | 575 | 80,301 | ||||

| 142,176 | ||||||

| 1,025,610 | ||||||

Total Corporates – Non-Investment Grades | 2,762,932 | |||||

GOVERNMENTS - TREASURIES – 1.6% | ||||||

Treasuries – 1.6% | ||||||

United States – 1.6% | ||||||

U.S. Treasury Bonds | 770 | 888,869 | ||||

AGENCIES – 1.5% | ||||||

Agency Debentures – 1.5% | ||||||

Bank of America Corp. – FDIC Insured | 280 | 281,779 | ||||

JPMorgan Chase & Co. – FDIC Insured | 280 | 280,624 | ||||

Wells Fargo & Co. – FDIC Insured | 280 | 281,934 | ||||

Total Agencies | 844,337 | |||||

Total Investments – 96.2% | 54,846,777 | |||||

Other assets less liabilities – 3.8% | 2,147,399 | |||||

Net Assets – 100.0% | $ | 56,994,176 | ||||

| (a) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. These securities are considered liquid and may be resold in transactions exempt from registration, normally to qualified institutional buyers. At April 30, 2009, the aggregate market value of these securities amounted to $696,562 or 1.2% of net assets. |

| (b) | Coupon rate adjusts periodically based upon a predetermined schedule. Stated interest rate in effect at April 30, 2009. |

| (c) | Variable rate coupon, rate shown as of April 30, 2009. |

| Glossary: |

FDIC – Federal Deposit Insurance Corporation

MTN – Medium Term Note

REIT – Real Estate Investment Trust

See notes to financial statements.

| 18 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

STATEMENT OF ASSETS & LIABILITIES

April 30, 2009

| Assets | ||||

Investments in securities, at value (cost $65,316,291) | $ | 54,846,777 | ||

Cash | 841,282 | |||

Interest receivable | 1,051,427 | |||

Receivable for investment securities sold | 454,195 | |||

Receivable for shares of beneficial interest sold | 52,881 | |||

Total assets | 57,246,562 | |||

| Liabilities | ||||

Payable for shares of beneficial interest redeemed | 138,788 | |||

Dividends payable | 113,598 | |||

Total liabilities | 252,386 | |||

Net Assets | $ | 56,994,176 | ||

| Composition of Net Assets | ||||

Shares of beneficial interest, at par | $ | 69 | ||

Additional paid-in capital | 71,732,841 | |||

Undistributed net investment income | 73,418 | |||

Accumulated net realized loss on investment transactions | (4,342,638 | ) | ||

Net unrealized depreciation on investments | (10,469,514) | |||

| $ | 56,994,176 | |||

Net Asset Value Per Share—unlimited shares of beneficial interest authorized, $.00001 par value (based on 6,907,056 common shares outstanding) | $ | 8.25 | ||

See notes to financial statements.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 19 |

Statement of Assets & Liabilities

STATEMENT OF OPERATIONS

Year Ended April 30, 2009

| Investment Income | ||||

Interest | $ | 4,656,797 | ||

| Realized and Unrealized Loss on Investment Transactions | ||||

Net realized loss on investment transactions | (3,348,583 | ) | ||

Net change in unrealized appreciation/depreciation of investments | (8,031,893 | ) | ||

Net loss on investment transactions | (11,380,476) | |||

Net Decrease in Net Assets from Operations | $ | (6,723,679 | ) | |

See notes to financial statements.

| 20 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Statement of Operations

STATEMENT OF CHANGES IN NET ASSETS

| Year Ended April 30, 2009 | Year Ended April 30, 2008 | |||||||

| Increase (Decrease) in Net Assets from Operations | ||||||||

Net investment income | $ | 4,656,797 | $ | 5,040,453 | ||||

Net realized loss on investment transactions | (3,348,583 | ) | (930,338 | ) | ||||

Net change in unrealized appreciation/depreciation of investments | (8,031,893 | ) | (2,081,113 | ) | ||||

Contributions from Adviser (see Note B) | – 0 | – | 15,585 | |||||

Net increase (decrease) in net assets from operations | (6,723,679 | ) | 2,044,587 | |||||

| Dividends to Shareholders from | ||||||||

Net investment income | (4,656,797 | ) | (5,040,453 | ) | ||||

| Transactions in Shares of Beneficial Interest | ||||||||

Net increase (decrease) | (18,455,698) | 699,311 | ||||||

Total decrease | (29,836,174 | ) | (2,296,555 | ) | ||||

| Net Assets | ||||||||

Beginning of period | 86,830,350 | 89,126,905 | ||||||

End of period (including undistributed net investment income of $73,418 and $70,667, respectively) | $ | 56,994,176 | $ | 86,830,350 | ||||

See notes to financial statements.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 21 |

Statement of Changes in Net Assets

NOTES TO FINANCIAL STATEMENTS

April 30, 2009

NOTE A

Significant Accounting Policies

AllianceBernstein Corporate Shares (the “Trust”) was organized as a Massachusetts business trust under the laws of The Commonwealth of Massachusetts by an Agreement and Declaration of Trust (“Declaration of Trust”) dated January 26, 2004. The Trust is registered under the Investment Company Act of 1940, as an open-end, diversified management investment company. The Trust operates as a “series” company currently having one separate portfolio: AllianceBernstein Corporate Income Shares (the “Portfolio”). AllianceBernstein Corporate Income Shares is considered to be a separate entity for financial reporting and tax purposes. The Portfolio commenced investment operations on December 11, 2006. Prior to the commencement of investment operations on December 11, 2006, the Portfolio had no operations other than the sale to the Adviser of 10,000 Portfolio shares for $10 each for the aggregate amount of $100,000 on May 17, 2006.

Shares of the Portfolio are offered exclusively to holders of accounts established under wrap-fee programs sponsored and maintained by certain registered investment advisers approved by the Adviser. The Portfolio’s shares may be purchased at the relevant net asset value without a sales charge or other fee. The financial statements have been prepared in conformity with U.S. generally accepted accounting principles which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements and amounts of income and expenses during the reporting period. Actual results could differ from those estimates. The following is a summary of significant accounting policies followed by the Portfolio.

1. Security Valuation

Portfolio securities are valued at their current market value determined on the basis of market quotations or, if market quotations are not readily available or are deemed unreliable, at “fair value” as determined in accordance with procedures established by and under the general supervision of the Portfolio’s Board of Trustees.

In general, the market value of securities which are readily available and deemed reliable are determined as follows. Securities listed on a national securities exchange (other than securities listed on the NASDAQ Stock Market, Inc. (“NASDAQ”)) or on a foreign securities exchange are valued at the last sale price at the close of the exchange or foreign securities exchange. If there has been no sale on such day, the securities are valued at the mean of the closing bid and asked prices on such day. Securities listed on more than one exchange are valued by reference to the principal exchange on which the securities are traded; securities listed only on NASDAQ are valued in accordance with the NASDAQ Official Closing Price; listed put or call options are valued at the last sale price. If there has been no sale on that day, such securities will be valued at the closing bid prices on that day; open futures contracts and options thereon are valued

| 22 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

using the closing settlement price or, in the absence of such a price, the most recent quoted bid price. If there are no quotations available for the day of valuation, the last available closing settlement price is used; securities traded in the over-the-counter market (“OTC”) are valued at the mean of the current bid and asked prices as reported by the National Quotation Bureau or other comparable sources; U.S. government securities and other debt instruments having 60 days or less remaining until maturity are valued at amortized cost if their original maturity was 60 days or less; or by amortizing their fair value as of the 61st day prior to maturity if their original term to maturity exceeded 60 days; fixed-income securities, including mortgage backed and asset backed securities, may be valued on the basis of prices provided by a pricing service or at a price obtained from one or more of the major broker/dealers. In cases where broker/dealer quotes are obtained, AllianceBernstein L.P. (the “Adviser”) may establish procedures whereby changes in market yields or spreads are used to adjust, on a daily basis, a recently obtained quoted price on a security; and OTC and other derivatives are valued on the basis of a quoted bid price or spread from a major broker/dealer in such security. Investments in money market funds are valued at their net asset value each day.

Securities for which market quotations are not readily available (including restricted securities) or are deemed unreliable are valued at fair value. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, analysis of the issuer’s financial statements or other available documents. In addition, the Portfolio may use fair value pricing for securities primarily traded in non-U.S. markets because most foreign markets close well before the Portfolio values its securities at 4:00 p.m., Eastern Time. The earlier close of these foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred in the interim and may materially affect the value of those securities.

2. Fair Value Measurements

The Portfolio adopted Financial Accounting Standards Board (“FASB”) Statement of Financial Accounting Standards No. 157, “Fair Value Measurements” (“FAS 157”), effective May 1, 2008. In accordance with FAS 157, fair value is defined as the price that the Portfolio would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. FAS 157 also establishes a framework for measuring fair value, and a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability. Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Portfolio. Unobservable inputs reflect the Portfolio’s own assumptions about the assumptions that market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. Each investment is

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 23 |

Notes to Financial Statements

assigned a level based upon the observability of the inputs which are significant to the overall valuation. The three-tier hierarchy of inputs is summarized below.

| • | Level 1—quoted prices in active markets for identical investments |

| • | Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| • | Level 3—significant unobservable inputs (including the Portfolio’s own assumptions in determining the fair value of investments) |

The following table summarizes the valuation of the Portfolio’s investments by the above fair value hierarchy levels as of April 30, 2009:

Level | Investments in Securities | Other Financial Instruments* | ||||||

Level 1 | $ | – 0 | – | $ | – 0 | – | ||

Level 2 | 54,846,777 | – 0 | – | |||||

Level 3 | – 0 | – | – 0 | – | ||||

Total | $ | 54,846,777 | $ | – 0 | – | |||

| * | Other financial instruments are derivative instruments, such as futures, forwards and swap contracts, which are valued at the unrealized appreciation/depreciation on the instrument. |

3. Taxes

It is the Portfolio’s policy to meet the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its investment company taxable income and net realized gains, if any, to shareholders. Therefore, no provisions for federal income or excise taxes are required.

In accordance with FASB Interpretation No. 48, “Accounting for Uncertainties in Income Taxes” (“FIN 48”), management has analyzed the Portfolio’s tax positions taken on federal and state income tax returns for all open tax years (the current and the prior three tax years) and has concluded that no provision for income tax is required in the Portfolio’s financial statements.

4. Investment Income and Investment Transactions

Dividend income is recorded on the ex-dividend date or as soon as the Portfolio is informed of the dividend. Interest income is accrued daily. Investment transactions are accounted for on the date the securities are purchased or sold. Investment gains or losses are determined on the identified cost basis. The Portfolio amortizes premiums and accretes discounts as adjustments to interest income.

5. Dividends and Distributions

Dividends and distributions to shareholders, if any, are recorded on the ex-dividend date. Income dividends and capital gains distributions are determined in accordance with federal tax regulations and may differ from those determined in accordance with U.S. generally accepted accounting principles. To

| 24 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

the extent these differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax basis treatment; temporary differences do not require such reclassification.

NOTE B

Advisory Fee and Other Transactions with Affiliates

Under the terms of the Advisory Agreement, the Portfolio pays no advisory fee to the Adviser. The Adviser serves as investment manager and adviser of the Portfolio and continuously furnishes an investment program for the Portfolio and manages, supervises and conducts the affairs of the Portfolio, subject to the supervisions of the Portfolio’s Board of Trustees. The Advisory Agreement provides that the Adviser or an affiliate will furnish, or pay the expenses of the Portfolio for, office space, facilities and equipment, services of executive and other personnel of the Portfolio and certain administrative services.

During the year ended April 30, 2008, the Adviser reimbursed the Portfolio $15,585 for trading losses incurred due to a trade entry error.

The Portfolio has entered into a Distribution Agreement (the “Agreement”) with AllianceBernstein Investments, Inc., the Portfolio’s principal underwriter (the “Underwriter”), to permit the Underwriter to distribute the Portfolio’s shares, which are sold at their net asset value without any sales charge. The Underwriter receives no fee for this service. The Underwriter is a wholly owned subsidiary of the Adviser.

AllianceBernstein Investor Services, Inc. (“ABIS”), an indirect wholly-owned subsidiary of the Adviser, acts as the Portfolios’ registrar, transfer agent and dividend-disbursing agent. ABIS registers the transfer, issuance and redemption of Portfolio shares and disburses dividends and other distributions to Portfolio shareholders. ABIS receives no fee for this service.

NOTE C

Investment Transactions

Purchases and sales of investment securities (excluding short-term investments) for the year ended April 30, 2009 were as follows:

| Purchases | Sales | |||||

Investment securities (excluding | $ | 16,349,888 | $ | 30,759,525 | ||

U.S. government securities | 1,636,231 | 6,118,557 | ||||

The cost of investments for federal income tax purposes, gross unrealized appreciation and unrealized depreciation are as follows:

Cost | $ | 65,366,562 | ||

Gross unrealized appreciation | $ | 244,822 | ||

Gross unrealized depreciation | (10,764,607 | ) | ||

Net unrealized depreciation | $ | (10,519,785 | ) | |

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 25 |

Notes to Financial Statements

NOTE D

Capital Stock

Transactions in shares of beneficial interest were as follows:

| Shares | Amount | |||||||||||||||||

| Year Ended April 30, 2009 | Year Ended April 30, 2008 | Year Ended April 30, 2009 | Year Ended April 30, 2008 | |||||||||||||||

| Class A | ||||||||||||||||||

Shares sold | 1,722,870 | 2,530,105 | $ | 14,602,971 | $ | 24,484,305 | ||||||||||||

Shares redeemed | (3,898,891 | ) | (2,456,360 | ) | (33,058,669 | ) | (23,784,994 | ) | ||||||||||

Net increase (decrease) | (2,176,021 | ) | 73,745 | $ | (18,455,698 | ) | $ | 699,311 | ||||||||||

NOTE E

Risks Involved in Investing in the Portfolio

Interest Rate Risk and Credit Risk—Interest rate risk is the risk that changes in interest rates will affect the value of an Underlying Portfolio’s investments in fixed-income debt securities such as bonds or notes. Increases in interest rates may cause the value of the Portfolio’s investments to decline. Credit risk is the risk that the issuer or guarantor of a debt security, or the counterparty to a derivative contract, will be unable or unwilling to make timely principal and/or interest payments, or to otherwise honor its obligations. The degree of risk for a particular security may be reflected in its credit risk rating. Credit risk is greater for medium quality and lower-rated securities. Lower-rated debt securities and similar unrated securities (commonly known as “junk bonds”) have speculative elements or are predominantly speculative risks.

Indemnification Risk—In the ordinary course of business, the Portfolio enters into contracts that contain a variety of indemnifications. The Portfolio’s maximum exposure under these arrangements is unknown. However, the Portfolio has not had prior claims or losses pursuant to these indemnification provisions and expects the risk of loss thereunder to be remote.

NOTE F

Distributions to Shareholders

The tax character of distributions paid during the fiscal years ended April 30, 2009 and April 30, 2008 were as follows:

| 2009 | 2008 | |||||

Distributions paid from: | ||||||

Ordinary income | $ | 4,656,797 | $ | 5,040,453 | ||

Total taxable distributions | 4,656,797 | 5,040,453 | ||||

Total distributions paid | $ | 4,656,797 | $ | 5,040,453 | ||

| 26 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

As of April 30, 2009, the components of accumulated earnings/(deficit) on a tax basis were as follows:

Undistributed ordinary income | $ | 187,016 | ||

Accumulated capital and other losses | (4,292,367 | )(a) | ||

Unrealized appreciation/(depreciation) | (10,519,785 | )(b) | ||

Total accumulated earnings/(deficit) | $ | (14,625,136 | )(c) | |

| (a) | On April 30, 2009, the Fund had capital loss carryforward of $2,784,306 of which $591,158 expires in 2016, and $2,193,148 expires in 2017. Net capital losses incurred after October 31, and within the taxable year are deemed to arise on the first business day of the Fund’s next taxable year. For the fiscal year ended April 30, 2009, the Fund deferred to May 1, 2009, post-October capital losses of $1,508,061. |

| (b) | The difference between book-basis and tax-basis unrealized appreciation/(depreciation) is attributable primarily to the tax deferral of losses on wash sales. |

| (c) | The difference between book-basis and tax-basis components of accumulated earnings/(deficit) is attributable primarily to dividends payable. |

During the current fiscal year, permanent differences due to consent fee reclassification, resulted in an increase to both undistributed net investment income and accumulated net realized loss on investment transactions. This reclassification had no effect on net assets.

NOTE G

Legal Proceedings

On October 2, 2003, a purported class action complaint entitled Hindo, et al. v. AllianceBernstein Growth & Income Fund, et al. (“Hindo Complaint”) was filed against the Adviser, Alliance Capital Management Holding L.P. (“Alliance Holding”), Alliance Capital Management Corporation, AXA Financial, Inc., the AllianceBernstein Funds, certain officers of the Adviser (“AllianceBernstein defendants”), and certain other unaffiliated defendants, as well as unnamed Doe defendants. The Hindo Complaint was filed in the United States District Court for the Southern District of New York by alleged shareholders of two of the AllianceBernstein Funds. The Hindo Complaint alleges that certain of the AllianceBernstein defendants failed to disclose that they improperly allowed certain hedge funds and other unidentified parties to engage in “late trading” and “market timing” of AllianceBernstein Fund securities, violating Sections 11 and 15 of the Securities Act, Sections 10(b) and 20(a) of the Exchange Act and Sections 206 and 215 of the Advisers Act. Plaintiffs seek an unspecified amount of compensatory damages and rescission of their contracts with the Adviser, including recovery of all fees paid to the Adviser pursuant to such contracts.

Following October 2, 2003, 43 additional lawsuits making factual allegations generally similar to those in the Hindo Complaint were filed in various federal and state courts against the Adviser and certain other defendants. On September 29, 2004, plaintiffs filed consolidated amended complaints with respect to four claim types: mutual fund shareholder claims; mutual fund derivative claims; derivative claims brought on behalf of Alliance Holding; and

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 27 |

Notes to Financial Statements

claims brought under ERISA by participants in the Profit Sharing Plan for Employees of the Adviser. All four complaints include substantially identical factual allegations, which appear to be based in large part on the Order of the SEC dated December 18, 2003 as amended and restated January 15, 2004 (“SEC Order”) and the New York State Attorney General Assurance of Discontinuance dated September 1, 2004 (“NYAG Order”).

On April 21, 2006, the Adviser and attorneys for the plaintiffs in the mutual fund shareholder claims, mutual fund derivative claims, and ERISA claims entered into a confidential memorandum of understanding containing their agreement to settle these claims. The agreement will be documented by a stipulation of settlement and will be submitted for court approval at a later date. The settlement amount ($30 million), which the Adviser previously accrued and disclosed, has been disbursed. The derivative claims brought on behalf of Alliance Holding, in which plaintiffs seek an unspecified amount of damages, remain pending.

It is possible that these matters and/or other developments resulting from these matters could result in increased redemptions of the AllianceBernstein Mutual Funds’ shares or other adverse consequences to the AllianceBernstein Mutual Funds. This may require the AllianceBernstein Mutual Funds to sell investments held by those funds to provide for sufficient liquidity and could also have an adverse effect on the investment performance of the AllianceBernstein Mutual Funds. However, the Adviser believes that these matters are not likely to have a material adverse effect on its ability to perform advisory services relating to the AllianceBernstein Mutual Funds.

NOTE H

Recent Accounting Pronouncement

On March 19, 2008, the FASB released Statement of Financial Accounting Standards No. 161, “Disclosures about Derivative Instruments and Hedging Activities” (“FAS 161”). FAS 161 requires qualitative disclosures about objectives and strategies for using derivatives, quantitative disclosures about fair value amounts of and gains and losses on derivative instruments, and disclosures about credit-risk-related contingent features in derivative agreements. The application of FAS 161 is required for fiscal years and interim periods beginning after November 15, 2008. At this time, management is evaluating the implications of FAS 161 and believes the adoption of FAS 161 will have no material impact on the Portfolio’s financial statements.

| 28 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

FINANCIAL HIGHLIGHTS

Selected Data For A Share Of Beneficial Interest Outstanding Throughout Each Period

| Year Ended April 30, | December 11, 2006(a) to | ||||||||

| 2009 | 2008 | ||||||||

Net asset value, beginning of period | $ 9.56 | $ 9.89 | $ 10.00 | ||||||

Income From Investment Operations | |||||||||

Net investment income(b) | .57 | .56 | .21 | ||||||

Net realized and unrealized loss on investment transactions | (1.31 | ) | (.33 | ) | (.11 | ) | |||

Net increase (decrease) in net asset value from operations | (.74 | ) | .23 | .10 | |||||

Less: Dividends | |||||||||

Dividends from net investment income | (.57 | ) | (.56 | ) | (.21 | ) | |||

Net asset value, end of period | $ 8.25 | $ 9.56 | $ 9.89 | ||||||

Total Return | |||||||||

Total investment return based on net asset value(c) | (7.76 | )% | 2.38 | % | 1.02 | % | |||

Ratios/Supplemental Data | |||||||||

Net assets, end of period (000’s omitted) | $56,994 | $86,830 | $89,127 | ||||||

Ratio to average net assets of: | |||||||||

Net investment income | 6.56 | % | 5.73 | % | 5.58 | %(d) | |||

Portfolio turnover rate | 26 | % | 58 | % | 33 | % | |||

| (a) | Commencement of operations. |

| (b) | Based on average shares outstanding. |

| (c) | Total investment return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, and redemption on the last day of the period. Initial sales charges or contingent deferred sales charges are not reflected in the calculation of total investment return. Total return does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Total investment return calculated for a period of less than one year is not annualized. |

| (d) | Annualized. |

See notes to financial statements.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 29 |

Financial Highlights

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

The Trustees and Shareholders

AllianceBernstein Corporate Income Shares

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of AllianceBernstein Corporate Income Shares (the Portfolio) as of April 30, 2009, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the two-year period then ended and for the period from December 11, 2006 (commencement of operations) to April 30, 2007. These financial statements and financial highlights are the responsibility of the Portfolio’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of April 30, 2009, by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of AllianceBernstein Corporate Income Shares as of April 30, 2009, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the two-year period then ended and for the period from December 11, 2006 to April 30, 2007, in conformity with U.S. generally accepted accounting principles.

New York, New York

June 24, 2009

| 30 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Report of Independent Registered Public Accounting Firm

TAX INFORMATION

(unaudited)

For foreign shareholders, the Fund designates 99.94% of its ordinary dividends as interest related dividends.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 31 |

Tax Information

BOARD OF TRUSTEES

| William H. Foulk, Jr.(1), Chairman | Nancy P. Jacklin(1) | |

John H. Dobkin(1) | Marshall C. Turner, Jr.(1) Earl D. Weiner(1) | |

| Michael J. Downey(1) | ||

| D. James Guzy(1) |

OFFICERS

Robert M. Keith, President and Chief Executive Officer Philip L. Kirstein, Senior Vice President and Independent Compliance Officer Douglas J. Peebles, Senior Vice President Lawrence J. Shaw(2), Senior Vice President | Shawn E. Keegan(2), Vice President Joel J. McKoan(2), Vice President Emilie D. Wrapp, Secretary Joseph J. Mantineo, Treasurer and Chief Financial Officer Phyllis J. Clarke, Controller |

Custodian and Accounting Agent State Street Bank and Trust Company

Principal Underwriter AllianceBernstein Investments, Inc.

Transfer Agent AllianceBernstein Investor Services, Inc. | Legal Counsel Seward & Kissel LLP One Battery Park Plaza New York, NY 10004

Independent Registered Public Accounting Firm KPMG LLP 345 Park Avenue New York, NY 10154 |

| (1) | Member of the Audit Committee, the Governance and Nominating Committee and the Independent Directors Committee. Mr. Foulk is the sole member of the Fair Value Pricing Committee. |

| (2) | The day-to-day management of, and investment decisions for, the Fund’s portfolio are made by the Corporate Income Shares Investment Team. Messrs. Shawn E. Keegan, Joel J. McKoan and Lawrence J. Shaw are the investment professionals primarily responsible for the day-to-day management of the Fund’s portfolio. |

| 32 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Board of Trustees

TRUSTEES AND OFFICERS INFORMATION

Board of Trustees Information

The business and affairs of the Fund are managed under the direction of the Board of Trustees. Certain information concerning the Fund’s Trustees is set forth below.

| NAME, ADDRESS*, AGE, (YEAR ELECTED**) | PRINCIPAL OCCUPATION(S) DURING PAST 5 YEARS | PORTFOLIOS IN FUND COMPLEX OVERSEEN BY TRUSTEE | OTHER DIRECTORSHIPS HELD BY TRUSTEE | |||

| DISINTERESTED TRUSTEES | ||||||

Chairman of the Board (2004) | Investment Adviser and an Independent Consultant. Previously, he was Senior Manager of Barrett Associates, Inc., a registered investment adviser, with which he had been associated since prior to 2004. He was formerly Deputy Comptroller and Chief Investment Officer of the State of New York and, prior thereto, Chief Investment Officer of the New York Bank for Savings. | 91 | None | |||

John H. Dobkin, # (2004) | Consultant. Formerly, President of Save Venice, Inc. (preservation organization) from 2001-2002, Senior Advisor from June 1999-June 2000 and President of Historic Hudson Valley (historic preservation) from December 1989-May 1999. Previously, Director of the National Academy of Design. | 89 | None | |||

Michael J. Downey, # (2005) | Private Investor since January 2004. Formerly, managing partner of Lexington Capital, LLC (investment advisory firm) from December 1997 until December 2003. From 1987 until 1993, Chairman and CEO of Prudential Mutual Fund Management. | 89 | Asia Pacific Fund, Inc., The Merger Fund and Prospect Acquisition Corp. (financial services) | |||

D. James Guzy, # (2005) | Chairman of the Board of PLX Technology (semi-conductors) and of SRC Computers Inc., with which he has been associated since prior to 2004. He was formerly a director of the Intel Corporation (semi- conductors) until May 2008. | 89 | Cirrus Logic Corporation (semi- conductors) | |||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 33 |

Trustees and Officers Information

| NAME, ADDRESS*, AGE, (YEAR ELECTED**) | PRINCIPAL OCCUPATION(S) DURING PAST 5 YEARS | PORTFOLIOS IN FUND COMPLEX OVERSEEN BY TRUSTEE | OTHER DIRECTORSHIPS HELD BY TRUSTEE | |||

DISINTERESTED TRUSTEES (continued) | ||||||

Nancy P. Jacklin, # (2006) | Professorial Lecturer at the Johns Hopkins School of Advanced International Studies and Adjunct Professor at Georgetown University Law Center in the 2008-2009 academic year. She was formerly, U.S. Executive Director of the International Monetary Fund (December 2002-May 2006); Partner, Clifford Chance (1992-2002); Sector Counsel, International Banking and Finance, and Associate General Counsel, Citicorp (1985-1992); Assistant General Counsel (International), Federal Reserve Board of Governors (1982-1985); and Attorney Advisor, U.S. Department of the Treasury (1973-1982). Member of the Bar of the District of Columbia and of New York; and member of the Council on Foreign Relations. | 89 | None | |||

Marshall C. Turner, Jr., # (2005) | He was Interim CEO of MEMC Electronic Materials, Inc. (semi-conductor and solar cell substrates) since November 2008 until March 2, 2009. He was Chairman and CEO of Dupont Photomasks, Inc. (components of semi-conductor manufacturing), 2003-2005, and President and CEO, 2005-2006, after the company was renamed Toppan Photomasks, Inc. | 89 | Xilinx, Inc. (programmable logic semi-conductors) and MEMC Electronic Materials, Inc. | |||

| 34 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Trustees and Officers Information

| NAME, ADDRESS*, AGE, (YEAR ELECTED**) | PRINCIPAL OCCUPATION(S) DURING PAST 5 YEARS | PORTFOLIOS IN FUND COMPLEX OVERSEEN BY TRUSTEE | OTHER DIRECTORSHIPS HELD BY TRUSTEE | |||

DISINTERESTED TRUSTEES (continued) | ||||||

Earl D. Weiner, # 69 (2007) | Of Counsel, and Partner prior to January 2007, of the law firm Sullivan & Cromwell LLP; member of ABA Federal Regulation of Securities Committee Task Force on Fund Director’s Guidebook, and member of the Advisory Board of Sustainable Forestry Management Limited. | 89 | None | |||

| * | The address for each of the Fund’s disinterested Trustees is c/o AllianceBernstein L.P., Attn: Philip L. Kirstein, 1345 Avenue of the Americas, New York, NY 10105. |

| ** | There is no stated term of office for the Fund’s Trustees. |

| # | Member of the Audit Committee, the Governance and Nominating Committee and the Independent Directors Committee. |

| + | Member of the Fair Value Pricing Committee. |

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 35 |

Trustees and Officers Information

Officer Information

Certain information concerning the Fund’s officers is set forth below.

NAME, ADDRESS,* AND AGE | POSITION(S) HELD WITH FUND | PRINCIPAL OCCUPATION DURING PAST 5 YEARS | ||

Robert M. Keith 49 | President and Chief Executive Officer | Executive Vice President of AllianceBernstein L.P. (the “Adviser”)** since July 2008; Executive Managing Director AllianceBernstein Investments, Inc. (“ABI”)** since 2006 and the head of ABI since July 2008. Prior to joining ABI in 2006, Executive Managing Director of Bernstein Global Wealth Management, and prior thereto, Senior Managing Director and Global Head of Client Service and Sales of AllianceBernstein’s institutional investment management business since 2004. Prior thereto, he was a Managing Director and Head of North American Client Service and Sales in AllianceBernstein’s institutional investment management business, with which he had been associated since prior to 2004. | ||

| Philip L. Kirstein, 64 | Senior Vice President and Independent Compliance Officer | Senior Vice President and Independent Compliance Officer of the AllianceBernstein Funds, with which he has been associated since October 2004. Prior thereto, he was Of Counsel to Kirkpatrick & Lockhart, LLP from October 2003 to October 2004, and General Counsel of Merrill Lynch Investment Managers, L.P. since prior to 2004. | ||

| Douglas J. Peebles, 43 | Senior Vice President | Executive Vice President of the Adviser,** with which he has been associated since prior to 2004. | ||

| Lawrence J. Shaw, 58 | Senior Vice President | Senior Vice President of the Adviser,** with which he has been associated since prior to 2004. | ||

| Shawn E. Keegan, 37 | Vice President | Vice President of the Adviser,** with which he has been associated since prior to 2004. | ||

Joel J. McKoan 51 | Vice President | Senior Vice President of the Adviser,** with which he has been associated since prior to 2004. | ||

| Emilie D. Wrapp, 53 | Secretary | Senior Vice President, Assistant General Counsel and Assistant Secretary of ABI,** with which she has been associated since prior to 2004. | ||

| Joseph J. Mantineo, 50 | Treasurer and Chief Financial Officer | Senior Vice President of AllianceBernstein Investor Services, Inc. (“ABIS”),** with which he has been associated since prior to 2004. |

| 36 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Trustees and Officers Information

NAME, ADDRESS,* AND AGE | POSITION(S) HELD WITH FUND | PRINCIPAL OCCUPATION DURING PAST 5 YEARS | ||

Phyllis J. Clarke, 48 | Controller | Assistant Vice President of ABIS,** with which she has been associated since prior to 2004. |

| * | The address for each of the Fund’s Officers is 1345 Avenue of the Americas, New York, NY 10105. |

| ** | The Adviser, ABI and ABIS are affiliates of the Fund. |

| The Fund’s Statement of Additional Information (“SAI”) has additional information about the Fund’s Trustees and Officers and is available without charge upon request. Contact your financial representative or AllianceBernstein at 1-800-227-4618 for a free prospectus or SAI. |

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 37 |

Trustees and Officers Information

Information Regarding the Review and Approval of the Fund’s Advisory Agreement

The disinterested trustees (the “trustees”) of AllianceBernstein Corporate Shares (the “Fund”) unanimously approved the continuance of the Advisory Agreement with the Adviser at a meeting held on November 4-6, 2008. AllianceBernstein Corporate Income Shares is the Fund’s sole portfolio or series and is referred to as the “Fund”.

Prior to approval of the continuance of the Advisory Agreement in respect of the Fund, the trustees had requested from the Adviser, and received and evaluated, extensive materials. They reviewed the proposed continuance of the Advisory Agreement with the Adviser and with experienced counsel who are independent of the Adviser, who advised on the relevant legal standards. The trustees also reviewed an independent evaluation prepared by the Fund’s Senior Officer (who is also the Fund’s Independent Compliance Officer) of the reasonableness of the advisory fee in the Advisory Agreement wherein the Senior Officer concluded that the contractual fee (zero) for the Fund was reasonable. The trustees also discussed the proposed continuance in private sessions with counsel and the Fund’s Senior Officer.

The trustees noted that the Fund is designed as a vehicle for the wrap fee account market (where investors pay fees to a wrap fee sponsor which pays investment fees and expenses from such fee). The trustees also noted that no advisory fee is payable by the Fund, that the Advisory Agreement does not include the reimbursement provision for certain administrative expenses included in the advisory agreements of most of the open-end AllianceBernstein Funds, and that the Adviser is responsible for payment of the Fund’s ordinary expenses. The trustees noted that the Fund acknowledges in the Advisory Agreement that the Adviser and its affiliates expect to receive compensation from third parties in connection with services provided under the Advisory Agreement. The trustees further noted that the Adviser receives payments from the wrap fee program sponsors (the “Sponsors”) that use the Fund as an investment vehicle for their clients.

The trustees considered their knowledge of the nature and quality of the services provided by the Adviser to the Fund gained from their experience as trustees or directors of most of the registered investment companies advised by the Adviser, their overall confidence in the Adviser’s integrity and competence they have gained from that experience, the Adviser’s initiative in identifying and raising potential issues with the trustees and its responsiveness, frankness and attention to concerns raised by the trustees in the past, including the Adviser’s willingness to consider and implement organizational and operational changes designed to improve investment results and the services provided to the AllianceBernstein Funds. The trustees noted that they have four regular meetings each year, at each of which they receive presentations from the Adviser on the investment results of the Fund and review extensive materials and information presented by the Adviser.

| 38 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

The trustees also considered all other factors they believed relevant, including the specific matters discussed below. In their deliberations, the trustees did not identify any particular information that was all-important or controlling, and different trustees may have attributed different weights to the various factors. The trustees determined that the selection of the Adviser to manage the Fund, and the overall arrangements between the Fund and the Adviser as provided in the Advisory Agreement, including the advisory fee, were fair and reasonable in light of the services performed, expenses incurred and such other matters as the trustees considered relevant in the exercise of their business judgment. The material factors and conclusions that formed the basis for the trustees’ determination included the following:

Nature, Extent and Quality of Services Provided

The trustees considered the scope and quality of services provided by the Adviser under the Advisory Agreement, including the quality of the investment research capabilities of the Adviser and the other resources it has dedicated to performing services for the Fund. They also noted the professional experience and qualifications of the Fund’s portfolio management team and other senior personnel of the Adviser. The quality of administrative and other services, including the Adviser’s role in coordinating the activities of the Fund’s other service providers, also were considered. The trustees concluded that, overall, they were satisfied with the nature, extent and quality of services provided to the Fund under the Advisory Agreement.

Costs of Services Provided and Profitability

The trustees reviewed a schedule of the revenues, expenses and related notes indicating the profitability of the Fund to the Adviser for calendar year 2007 that had been prepared with an expense allocation methodology arrived at in consultation with an independent consultant retained by the Fund’s Senior Officer. The trustees considered that while the Adviser does not receive any advisory fee from the Fund or expense reimbursement, it does receive fees paid by the Sponsors. They also noted that the Adviser bears certain costs in providing services to the Fund and in paying its ordinary expenses. The trustees reviewed the assumptions and methods of allocation used by the Adviser in preparing fund-specific profitability data and noted that there are a number of potentially acceptable allocation methodologies for information of this type. The trustees noted that the profitability information reflected all revenues and expenses of the Adviser’s relationship with the Fund. The trustees recognized that it is difficult to make comparisons of profitability between fund advisory contracts because comparative information is not generally publicly available and is affected by numerous factors, including in the case of the Fund, the fact that it does not pay an advisory fee. The trustees focused on the profitability of the Adviser’s relationship with the Fund before taxes and distribution expenses. The trustees concluded that they were satisfied that the Adviser’s level of profitability from its relationship with the Fund was not unreasonable.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 39 |

Fall-Out Benefits

The trustees considered the benefits to the Adviser and its affiliates from their relationships with the Fund other than the fees payable to it by the Sponsors whose clients invest in the Fund. The trustees noted that since the Fund does not engage in brokerage transactions, the Adviser does not receive soft dollar benefits in respect of portfolio transactions of the Fund. The trustees understood that the Adviser also might derive reputational and other benefits from its association with the Fund.

Investment Results