UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21497

ALLIANCEBERNSTEIN CORPORATE SHARES

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: April 30, 2014

Date of reporting period: April 30, 2014

ITEM 1. REPORTS TO STOCKHOLDERS.

ANNUAL REPORT

AllianceBernstein

Corporate Income Shares

April 30, 2014

Annual Report

Investment Products Offered

| • | Are Not FDIC Insured |

| • | May Lose Value |

| • | Are Not Bank Guaranteed |

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.alliancebernstein.com or contact your AllianceBernstein Investments representative. Please read the prospectus and/or summary prospectus carefully before investing.

This shareholder report must be preceded or accompanied by the Fund’s prospectus for individuals who are not current shareholders of the Fund.

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AllianceBernstein’s website at www.alliancebernstein.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AllianceBernstein at (800) 227-4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov. The Fund’s Forms N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AllianceBernstein family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the manager of the funds.

AllianceBernstein® and the AB Logo are registered trademarks and service marks used by permission of the owner, AllianceBernstein L.P.

June 9, 2014

Annual Report

This report provides management’s discussion of fund performance for AllianceBernstein Corporate Income Shares (the “Fund”) for the annual reporting period ended April 30, 2014. Please note, shares of this Fund are offered exclusively through registered investment advisers approved by AllianceBernstein L.P. (the “Adviser”).

Investment Objective and Policies

The Fund’s investment objective is to earn high current income. The Fund invests, under normal circumstances, at least 80% of its net assets in U.S. corporate bonds. The Fund may also invest in U.S. Government securities (other than U.S. Government securities that are mortgage-backed or asset-backed securities), repurchase agreements and forward contracts relating to U.S. Government securities. The Fund normally invests all of its assets in securities that are rated, at the time of purchase, at least BBB- or the equivalent. The Fund will not invest in unrated corporate debt securities. The Fund has the flexibility to invest in long- and short-term fixed-income securities. In making decisions about whether to buy or sell securities, the Adviser will consider, among other things, the strength of certain sectors of the fixed-income market relative to others, interest rates and other general market conditions and the credit quality of individual issuers. The Fund also may invest in convertible debt securities; invest up to 10% of its assets in inflation-protected securities; invest up to 5% of its net assets in preferred stock; purchase and sell interest rate futures contracts and options; enter into swap

transactions; invest in zero-coupon securities and “payment-in-kind” debentures; make secured loans of portfolio securities; and invest in U.S. dollar-denominated fixed-income securities issued by non-U.S. companies.

Investment Results

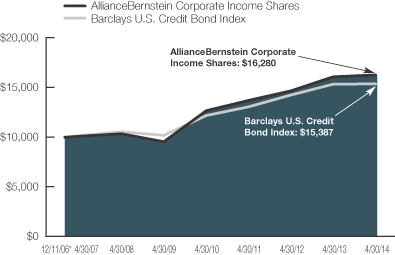

The table on page 5 shows the Fund’s performance compared to its benchmark, the Barclays U.S. Credit Bond Index, for the six- and 12-month periods ended April 30, 2014.

The Fund outperformed its benchmark for both periods. Corporate security selection, particularly in bank holdings where the Fund was overweight to subordinated debt, was a primary positive contributor. An underweight to the non-corporate part of the credit benchmark (sovereigns, supranationals, agencies and local governments) was also additive for both periods. Conversely, an allocation to U.S. Treasuries was a modest detractor. Overall yield curve positioning detracted for both periods; for the six-month period, an underweight in longer-maturity holdings detracted, while an overweight in seven- to 10-year maturities, where yields rose most, detracted for the 12-month period.

The Fund utilized derivatives in the form of interest rate swaps to manage overall duration and yield curve positioning during both periods.

Market Review and Investment Strategy

Global equity markets responded positively to economic improvement in key developed countries, and accommodative monetary policies of major central banks supported fixed-income markets during

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 1 |

the annual period ended April 30, 2014. The direction of U.S. federal policy also played a significant role in market activity. Fixed-income markets underperformed in the beginning of the period, as interest rates rose in response to signals by the U.S. Federal Reserve (the “Fed”) that it would consider reducing its bond-buying program, which then came to pass in December. At the end of the period, however, capital markets rebounded with almost all major fixed-income sectors outperforming, as Fed Chair Janet Yellen reaffirmed that tapering would continue unabated. Investors were encouraged to hear that the program is expected to be reduced in measured steps and that monetary stance should remain accommodative for the foreseeable future.

U.S. credit market returns were relatively soft, however, for the 12-month period, primarily due to the selloff early in the period as investors priced in higher rates. Within the credit space, U.S. corporates outperformed the non-corporate part of the credit market with financials, specifically subordinated banks, outperforming. During the period, spreads tightened and are close to fair value, in the view of the Corporate Income Shares Investment Team (the “Team”). With official rates in the U.S. unlikely to rise

much above zero for some time, the Team believes investor demand for income—and thus technical support for the corporate sector—should persist, which is likely to put a ceiling on significant widening. Companies in the industrial space continue to exhibit mid- to late-cycle behavior with rising industrial leverage. Within financials, fundamentals continue to be favorable as firms’ deleveraging continues and, in the Team’s view, remain a compelling opportunity.

Within the Fund’s positioning, it remains underweight the non-corporate part of the credit benchmark. Within the Fund’s industry allocation, it is overweight in the banking, real estate investment trusts, communication and insurance sectors, with an underweight in consumer non-cyclicals, electric and capital goods. The Fund’s bank positions remain focused on subordinated issues over senior debt where the Team continues to see more favorable valuation. The Fund is also positioned in intermediate maturities where the curve is steepest. In quality, the Fund continues to be overweight BBBs, where the Team sees value. Overall duration was slightly short of the benchmark at the end of the period.

| 2 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

DISCLOSURES AND RISKS

Benchmark Disclosure

The unmanaged Barclays U.S. Credit Bond Index does not reflect fees and expenses associated with the active management of a fund. The Barclays U.S. Credit Bond Index represents the performance of the U.S. credit securities within the U.S. fixed-income market. An investor cannot invest directly in an index, and its results are not indicative of the performance for any specific investment, including the Fund.

A Word About Risk

Market Risk: The value of the Fund’s assets will fluctuate as the stock or bond market fluctuates. The value of the Fund’s investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events that affect large portions of the market.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

Interest Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest rate risk is generally greater for fixed-income securities with longer maturities or durations.

Inflation Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the Fund’s distributions. This risk is significantly greater for fixed-income securities with longer maturities.

Foreign (Non-U.S.) Risk: Investments in securities of non-U.S. issuers may involve more risk than those of U.S. issuers. These securities may fluctuate more widely in price and may be less liquid due to adverse market, economic, political, regulatory or other factors.

Derivatives Risk: Investments in derivatives may be illiquid, difficult to price, and leveraged so that small changes may produce disproportionate losses for the Fund, and may be subject to counterparty risk to a greater degree than more traditional investments.

Management Risk: The Fund is subject to management risk because it is an actively-managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is no guarantee that its techniques will produce the intended results.

These risks are fully discussed in the Fund’s prospectus.

An Important Note About Historical Performance

The performance shown on the following pages represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. You may obtain performance information current to the most recent month-end by calling (800) 227-4618. The investment return and principal value of an investment in the Fund will fluctuate, so that your shares, when redeemed, may be worth more or less than their original cost. Performance assumes reinvestment of distributions and does not account for taxes.

(Disclosures, Risks and Note about Historical Performance continued on next page)

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 3 |

Disclosures and Risks

DISCLOSURES AND RISKS

(continued from previous page)

Investors should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. For copies of our prospectus and/or summary prospectus, which contain this and other information, visit us online at www.alliancebernstein.com or contact your AllianceBernstein Investments representative. Please read the prospectus and/or summary prospectus carefully before investing.

| 4 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Disclosures and Risks

HISTORICAL PERFORMANCE

THE FUND VS. ITS BENCHMARK PERIODS ENDED APRIL 30, 2014 (unaudited) | NAV Returns | |||||||||

| 6 Months | 12 Months | |||||||||

| AllianceBernstein Corporate Income Shares* | 4.48% | 1.31% | ||||||||

| ||||||||||

| Barclays U.S. Credit Bond Index | 3.60% | 0.41% | ||||||||

| ||||||||||

* Includes the impact of proceeds received and credited to the Fund resulting from class action settlements, which enhanced the performance of the Fund for the 12-month period ended April 30, 2014 by 0.05%. | ||||||||||

GROWTH OF A $10,000 INVESTMENT IN THE FUND

12/11/06* TO 4/30/14

This chart illustrates the total value of an assumed $10,000 investment in AllianceBernstein Corporate Income Shares (from 12/11/06 to 4/30/14) as compared to the performance of the Fund’s benchmark.

| * | Inception date: 12/11/2006. |

See Disclosures, Risks and Note about Historical Performance on pages 3-4.

(Historical Performance continued on next page)

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 5 |

Historical Performance

HISTORICAL PERFORMANCE

(continued from previous page)

| AVERAGE ANNUAL RETURNS AS OF APRIL 30, 2014 (unaudited) | ||||

| NAV Returns | ||||

1 Year | 1.31 | % | ||

5 Years | 11.28 | % | ||

Since Inception* | 6.82 | % | ||

SEC AVERAGE ANNUAL RETURNS MARCH 31, 2014 (unaudited) | ||||

| SEC Returns | ||||

1 Year | 1.92 | % | ||

5 Years | 11.68 | % | ||

Since Inception* | 6.70 | % | ||

The prospectus fee table shows the fees and the total fund operating expenses of the Fund as 0.00% because the Adviser does not charge any fees or expenses and reimburses Fund operating expenses. Participants in a wrap fee program or other investment program eligible to invest in the Fund pay fees to the program sponsor and should review the program brochure or other literature provided by the sponsor for a discussion of fees and expenses charged.

| * | Inception date: 12/11/2006. |

See Disclosures, Risks and Note about Historical Performance on pages 3-4.

| 6 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Historical Performance

EXPENSE EXAMPLE

As a shareholder of the Fund, you may incur various ongoing non-operating and extraordinary costs. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or contingent deferred sales charges on redemptions. Therefore, the hypothetical example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value November 1, 2013 | Ending Account Value April 30, 2014 | Expenses Paid During Period* | Annualized Expense Ratio* | |||||||||||||

Actual | $ | 1,000 | $ | 1,044.80 | $ | – 0 | – | 0.00 | % | |||||||

Hypothetical** | $ | 1,000 | $ | 1,024.79 | $ | – 0 | – | 0.00 | % | |||||||

| * | Expenses are equal to the Fund’s annualized expense ratios multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). The Fund’s operating expenses are borne by the Adviser or its affiliates. |

| ** | Assumes 5% annual return before expenses. |

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 7 |

Expense Example

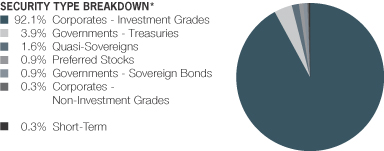

PORTFOLIO SUMMARY

April 30, 2014 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $46.0

| * | All data are as of April 30, 2014. The Fund’s security type breakdown is expressed as a percentage of total investments and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Portfolio of Investments” section of the report for additional details). |

| 8 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio Summary

PORTFOLIO OF INVESTMENTS

April 30, 2014

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

CORPORATES – INVESTMENT GRADES – 90.4% | ||||||||

Industrial – 41.0% | ||||||||

Basic – 5.3% | ||||||||

Alpek SA de CV | $ | 200 | $ | 200,500 | ||||

Barrick Gold Corp. | 215 | 209,354 | ||||||

CF Industries, Inc. | 50 | 60,254 | ||||||

Dow Chemical Co. (The) | 190 | 200,731 | ||||||

Freeport-McMoRan Copper & Gold, Inc. | 69 | 69,391 | ||||||

Georgia-Pacific LLC | 240 | 311,252 | ||||||

Glencore Funding LLC | 70 | 70,000 | ||||||

International Paper Co. | ||||||||

4.75%, 2/15/22 | 175 | 191,941 | ||||||

7.95%, 6/15/18 | 50 | 61,393 | ||||||

9.375%, 5/15/19 | 81 | 106,748 | ||||||

LyondellBasell Industries NV | 200 | 224,198 | ||||||

Mosaic Co. (The) | 120 | 124,207 | ||||||

Plains Exploration & Production Co. | 275 | 303,531 | ||||||

Rio Tinto Finance USA Ltd. | 95 | 101,069 | ||||||

Teck Resources Ltd. | 100 | 103,633 | ||||||

Xstrata Finance Canada Ltd. | 90 | 89,193 | ||||||

|

| |||||||

| 2,427,395 | ||||||||

|

| |||||||

Capital Goods – 1.4% | ||||||||

Boeing Co. (The) | 140 | 175,653 | ||||||

Embraer SA | 200 | 211,000 | ||||||

Owens Corning | 210 | 263,605 | ||||||

|

| |||||||

| 650,258 | ||||||||

|

| |||||||

Communications - Media – 4.6% | ||||||||

21st Century Fox America, Inc. | 110 | 106,993 | ||||||

7.43%, 10/01/26 | 55 | 69,301 | ||||||

8.875%, 4/26/23 | 125 | 167,455 | ||||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 9 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

CBS Corp. | $ | 169 | $ | 195,117 | ||||

Comcast Cable Communications Holdings, Inc. | 110 | 157,756 | ||||||

Cox Communications, Inc. | 135 | 150,070 | ||||||

DirecTV Holdings LLC/DirecTV Financing Co., Inc. | ||||||||

3.80%, 3/15/22 | 90 | 90,071 | ||||||

4.45%, 4/01/24 | 100 | 101,454 | ||||||

5.20%, 3/15/20 | 53 | 58,531 | ||||||

Discovery Communications LLC | 84 | 84,442 | ||||||

Omnicom Group, Inc. | 165 | 193,810 | ||||||

TCI Communications, Inc. | 150 | 199,668 | ||||||

Thomson Reuters Corp. | 375 | 376,443 | ||||||

Time Warner Cable, Inc. | ||||||||

4.50%, 9/15/42 | 65 | 62,866 | ||||||

5.50%, 9/01/41 | 25 | 27,603 | ||||||

5.875%, 11/15/40 | 30 | 34,607 | ||||||

6.55%, 5/01/37 | 39 | 47,813 | ||||||

|

| |||||||

| 2,124,000 | ||||||||

|

| |||||||

Communications - Telecommunications – 7.5% | ||||||||

America Movil SAB de CV | 130 | 144,481 | ||||||

American Tower Corp. | ||||||||

3.40%, 2/15/19 | 40 | 41,245 | ||||||

4.50%, 1/15/18 | 40 | 43,245 | ||||||

7.25%, 5/15/19 | 150 | 180,083 | ||||||

Ameritech Capital Funding Corp. | 130 | 145,430 | ||||||

AT&T, Inc. | ||||||||

3.00%, 2/15/22 | 420 | 413,455 | ||||||

3.875%, 8/15/21 | 230 | 240,796 | ||||||

BellSouth Corp. | 145 | 167,231 | ||||||

British Telecommunications PLC | 175 | 276,047 | ||||||

Deutsche Telekom International Finance BV | 190 | 195,101 | ||||||

Rogers Communications, Inc. | 50 | 51,665 | ||||||

Telefonica Emisiones SAU | 345 | 388,456 | ||||||

Verizon Communications, Inc. | 46 | 46,440 | ||||||

3.50%, 11/01/21 | 275 | 279,578 | ||||||

| 10 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

4.50%, 9/15/20 | $ | 50 | $ | 54,492 | ||||

5.15%, 9/15/23 | 397 | 437,627 | ||||||

6.55%, 9/15/43 | 104 | 128,283 | ||||||

Verizon New York, Inc. | 170 | 208,200 | ||||||

|

| |||||||

| 3,441,855 | ||||||||

|

| |||||||

Consumer Cyclical - Automotive – 2.5% | ||||||||

Ford Motor Co. | 225 | 261,460 | ||||||

Ford Motor Credit Co. LLC | 575 | 666,528 | ||||||

Johnson Controls, Inc. | 105 | 113,069 | ||||||

TRW Automotive, Inc. | 120 | 122,400 | ||||||

|

| |||||||

| 1,163,457 | ||||||||

|

| |||||||

Consumer Cyclical - Entertainment – 1.3% | ||||||||

Time Warner, Inc. | 210 | 211,513 | ||||||

4.70%, 1/15/21 | 60 | 65,808 | ||||||

6.25%, 3/29/41 | 130 | 155,613 | ||||||

Viacom, Inc. | 120 | 125,067 | ||||||

5.25%, 4/01/44 | 50 | 52,300 | ||||||

|

| |||||||

| 610,301 | ||||||||

|

| |||||||

Consumer Cyclical - Other – 1.2% | ||||||||

Carnival Corp. | 180 | 180,635 | ||||||

Host Hotels & Resorts LP | 91 | 89,450 | ||||||

Marriott International, Inc./DE | 151 | 154,831 | ||||||

Wyndham Worldwide Corp. | 115 | 116,022 | ||||||

|

| |||||||

| 540,938 | ||||||||

|

| |||||||

Consumer Cyclical - Restaurants – 0.1% | ||||||||

Yum! Brands, Inc. | 60 | 62,532 | ||||||

|

| |||||||

Consumer Cyclical - Retailers – 2.3% | ||||||||

Advance Auto Parts, Inc. | 115 | 120,463 | ||||||

CVS Caremark Corp. | 150 | 178,076 | ||||||

Dollar General Corp. | 105 | 99,143 | ||||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 11 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

Gap, Inc. (The) | $ | 100 | $ | 113,797 | ||||

Home Depot, Inc. (The) | 130 | 149,697 | ||||||

5.875%, 12/16/36 | 30 | 36,785 | ||||||

Kohl’s Corp. | 85 | 98,283 | ||||||

Macy’s Retail Holdings, Inc. | 250 | 259,624 | ||||||

|

| |||||||

| 1,055,868 | ||||||||

|

| |||||||

Consumer Non-Cyclical – 4.1% | ||||||||

Actavis, Inc. | 130 | 131,121 | ||||||

Altria Group, Inc. | 370 | 405,282 | ||||||

Amgen, Inc. | 120 | 126,683 | ||||||

Bristol-Myers Squibb Co. | 52 | 63,309 | ||||||

Grupo Bimbo SAB de CV | 200 | 206,972 | ||||||

Kroger Co. (The) | 35 | 34,908 | ||||||

3.85%, 8/01/23 | 50 | 50,769 | ||||||

McKesson Corp. | 105 | 129,134 | ||||||

Mylan, Inc./PA | 120 | 120,380 | ||||||

Procter & Gamble Co. (The) | 55 | 67,781 | ||||||

Reynolds American, Inc. | 61 | 58,210 | ||||||

Teva Pharmaceutical Finance Co. BV | 135 | 138,052 | ||||||

Tyson Foods, Inc. | 110 | 116,435 | ||||||

Whirlpool Corp. | 120 | 120,375 | ||||||

Wyeth LLC | 100 | 123,538 | ||||||

|

| |||||||

| 1,892,949 | ||||||||

|

| |||||||

Energy – 5.8% | ||||||||

Anadarko Petroleum Corp. | 265 | 306,207 | ||||||

Apache Corp. | 215 | 206,888 | ||||||

| 12 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

ConocoPhillips Holding Co. | $ | 166 | $ | 222,752 | ||||

Hess Corp. | 40 | 45,312 | ||||||

7.875%, 10/01/29 | 144 | 193,565 | ||||||

Nabors Industries, Inc. | 170 | 173,719 | ||||||

5.10%, 9/15/23(a) | 195 | 206,943 | ||||||

Noble Energy, Inc. | 65 | 69,377 | ||||||

Noble Holding International Ltd. | 90 | 97,051 | ||||||

Phillips 66 | 54 | 57,738 | ||||||

Talisman Energy, Inc. | 64 | 64,461 | ||||||

7.75%, 6/01/19 | 96 | 117,301 | ||||||

Transocean, Inc. | 195 | 220,373 | ||||||

6.50%, 11/15/20 | 85 | 96,057 | ||||||

Valero Energy Corp. | 70 | 82,173 | ||||||

6.625%, 6/15/37 | 67 | 82,125 | ||||||

7.50%, 4/15/32 | 46 | 59,512 | ||||||

Weatherford International Ltd./Bermuda | 205 | 216,212 | ||||||

5.125%, 9/15/20 | 85 | 93,983 | ||||||

9.625%, 3/01/19 | 45 | 59,045 | ||||||

|

| |||||||

| 2,670,794 | ||||||||

|

| |||||||

Other Industrial – 0.5% | ||||||||

Fresnillo PLC | 200 | 204,000 | ||||||

|

| |||||||

Technology – 2.2% | ||||||||

Hewlett-Packard Co. | 51 | 51,831 | ||||||

3.75%, 12/01/20 | 51 | 52,465 | ||||||

4.30%, 6/01/21 | 80 | 84,194 | ||||||

4.65%, 12/09/21 | 29 | 31,271 | ||||||

Motorola Solutions, Inc. | 220 | 219,428 | ||||||

Seagate HDD Cayman | 140 | 140,175 | ||||||

Telefonaktiebolaget LM Ericsson | 120 | 123,700 | ||||||

Total System Services, Inc. | 105 | 104,049 | ||||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 13 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

Xerox Corp. | $ | 100 | $ | 113,900 | ||||

6.40%, 3/15/16 | 100 | 109,895 | ||||||

|

| |||||||

| 1,030,908 | ||||||||

|

| |||||||

Transportation - Airlines – 0.3% | ||||||||

Southwest Airlines Co. | 130 | 143,923 | ||||||

|

| |||||||

Transportation - Railroads – 1.0% | ||||||||

CSX Corp. | 180 | 176,225 | ||||||

Norfolk Southern Corp. | 230 | 232,733 | ||||||

Union Pacific Corp. | 40 | 43,189 | ||||||

|

| |||||||

| 452,147 | ||||||||

|

| |||||||

Transportation - Services – 0.9% | ||||||||

FedEx Corp. | 40 | 50,027 | ||||||

Penske Truck Leasing Co. LP/PTL Finance Corp. | 120 | 127,811 | ||||||

Ryder System, Inc. | 185 | 188,110 | ||||||

5.85%, 11/01/16 | 28 | 30,951 | ||||||

|

| |||||||

| 396,899 | ||||||||

|

| |||||||

| 18,868,224 | ||||||||

|

| |||||||

Financial Institutions – 39.8% | ||||||||

Banking – 22.3% | ||||||||

ABN AMRO Bank NV | 255 | 281,826 | ||||||

Bank of America Corp. | 425 | 434,230 | ||||||

5.00%, 5/13/21 | 235 | 258,963 | ||||||

5.70%, 1/24/22 | 140 | 160,285 | ||||||

5.875%, 2/07/42 | 110 | 128,762 | ||||||

Series 1 | ||||||||

3.75%, 7/12/16 | 175 | 184,761 | ||||||

Bank of New York Mellon Corp. (The) | 110 | 100,842 | ||||||

Bank One Michigan | 440 | 587,360 | ||||||

Barclays Bank PLC | 225 | 242,337 | ||||||

BB&T Corp. | 275 | 311,291 | ||||||

BPCE SA | 200 | 203,358 | ||||||

| 14 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

Capital One Bank USA NA | $ | 550 | $ | 543,277 | ||||

Citigroup, Inc. | 350 | 333,832 | ||||||

6.625%, 1/15/28 | 405 | 488,638 | ||||||

Countrywide Financial Corp. | 253 | 277,028 | ||||||

Fifth Third Bancorp | 31 | 31,427 | ||||||

5.45%, 1/15/17 | 105 | 115,899 | ||||||

Goldman Sachs Capital I | 115 | 121,598 | ||||||

Goldman Sachs Group, Inc. (The) | 130 | 131,498 | ||||||

5.75%, 1/24/22 | 435 | 496,331 | ||||||

Series D | ||||||||

6.00%, 6/15/20 | 320 | 369,929 | ||||||

Series G | ||||||||

7.50%, 2/15/19 | 75 | 91,066 | ||||||

JPMorgan Chase & Co. | 220 | 246,134 | ||||||

Morgan Stanley | 280 | 319,255 | ||||||

Series G | ||||||||

5.50%, 7/24/20 | 700 | 794,306 | ||||||

6.625%, 4/01/18 | 100 | 116,673 | ||||||

People’s United Financial, Inc. | 175 | 173,243 | ||||||

PNC Bank NA | 650 | 717,826 | ||||||

Rabobank Capital Funding Trust III | 100 | 105,500 | ||||||

Regions Financial Corp. | 300 | 296,548 | ||||||

Royal Bank of Scotland PLC (The) | 340 | 397,800 | ||||||

Santander Holdings USA, Inc./PA | 130 | 135,770 | ||||||

State Street Corp. | 240 | 262,665 | ||||||

SunTrust Bank/Atlanta GA | 145 | 170,044 | ||||||

Turkiye Garanti Bankasi AS | 200 | 200,512 | ||||||

UBS AG/Stamford CT | 100 | 124,965 | ||||||

UniCredit Luxembourg Finance SA | 100 | 109,500 | ||||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 15 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

Zions Bancorporation | $ | 175 | $ | 175,672 | ||||

|

| |||||||

| 10,240,951 | ||||||||

|

| |||||||

Finance – 2.1% | ||||||||

GE Capital Trust I | 345 | 382,088 | ||||||

General Electric Capital Corp. | 200 | 226,914 | ||||||

5.875%, 1/14/38 | 140 | 167,616 | ||||||

HSBC Finance Capital Trust IX | 170 | 176,375 | ||||||

|

| |||||||

| 952,993 | ||||||||

|

| |||||||

Insurance – 8.3% | ||||||||

American International Group, Inc. | 285 | 344,023 | ||||||

8.175%, 5/15/58 | 65 | 86,938 | ||||||

Assurant, Inc. | 105 | 105,111 | ||||||

Chubb Corp. (The) | 190 | 218,388 | ||||||

Cigna Corp. | 175 | 183,967 | ||||||

7.875%, 5/15/27 | 65 | 83,841 | ||||||

Guardian Life Insurance Co. of America | 42 | 57,385 | ||||||

Hartford Financial Services Group, Inc. (The) | 190 | 210,126 | ||||||

5.50%, 3/30/20 | 100 | 114,239 | ||||||

6.10%, 10/01/41 | 45 | 55,043 | ||||||

Lincoln National Corp. | 100 | 110,464 | ||||||

8.75%, 7/01/19 | 82 | 106,546 | ||||||

Markel Corp. | 59 | 71,160 | ||||||

MetLife Capital Trust IV | 150 | 182,250 | ||||||

Metropolitan Life Global Funding I | 250 | 247,509 | ||||||

Nationwide Mutual Insurance Co. | 90 | 138,142 | ||||||

Principal Financial Group, Inc. | 170 | 170,733 | ||||||

Progressive Corp. (The) | 62 | 68,696 | ||||||

Prudential Financial, Inc. | 225 | 234,535 | ||||||

4.50%, 11/15/20 | 39 | 42,685 | ||||||

5.625%, 6/15/43 | 200 | 206,500 | ||||||

| 16 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

Series B | ||||||||

5.75%, 7/15/33 | $ | 135 | $ | 155,004 | ||||

Reliance Standard Life Global Funding II | 140 | 138,141 | ||||||

Swiss Re Solutions Holding Corp. | 90 | 111,155 | ||||||

UnitedHealth Group, Inc. | 170 | 173,054 | ||||||

WellPoint, Inc. | 105 | 125,466 | ||||||

XLIT Ltd. | 75 | 87,849 | ||||||

|

| |||||||

| 3,828,950 | ||||||||

|

| |||||||

REITS – 7.1% | ||||||||

Alexandria Real Estate Equities, Inc. | 100 | 98,282 | ||||||

Boston Properties LP | 200 | 192,101 | ||||||

DDR Corp. | 105 | 120,980 | ||||||

Duke Realty LP | 55 | 64,775 | ||||||

EPR Properties | 175 | 180,441 | ||||||

Essex Portfolio LP | 56 | 53,682 | ||||||

3.375%, 1/15/23(a) | 225 | 216,227 | ||||||

HCP, Inc. | 150 | 153,711 | ||||||

6.70%, 1/30/18 | 160 | 186,743 | ||||||

Health Care REIT, Inc. | 107 | 108,264 | ||||||

5.25%, 1/15/22 | 140 | 155,619 | ||||||

Healthcare Trust of America Holdings LP | 140 | 135,150 | ||||||

Hospitality Properties Trust | 210 | 220,784 | ||||||

Kimco Realty Corp. | 70 | 83,940 | ||||||

Realty Income Corp. | 210 | 238,633 | ||||||

Senior Housing Properties Trust | 115 | 115,855 | ||||||

Trust F/1401 | 230 | 232,587 | ||||||

Ventas Realty LP/Ventas Capital Corp. | 216 | 216,915 | ||||||

4.25%, 3/01/22 | 129 | 135,406 | ||||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 17 |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

Vornado Realty LP | $ | 215 | $ | 231,947 | ||||

Washington Real Estate Investment Trust | 140 | 150,302 | ||||||

|

| |||||||

| 3,292,344 | ||||||||

|

| |||||||

| 18,315,238 | ||||||||

|

| |||||||

Utility – 8.5% | ||||||||

Electric – 2.6% | ||||||||

Berkshire Hathaway Energy Co. | 150 | 183,231 | ||||||

CMS Energy Corp. | 165 | 194,683 | ||||||

Consolidated Edison Co. of New York, Inc. | 100 | 109,026 | ||||||

Series 07-A | ||||||||

6.30%, 8/15/37 | 30 | 38,608 | ||||||

Empresa Nacional de Electricidad SA/Chile | 33 | 33,059 | ||||||

Exelon Corp. | 220 | 229,710 | ||||||

Pacific Gas & Electric Co. | 50 | 49,369 | ||||||

PacifiCorp | 70 | 87,858 | ||||||

Potomac Electric Power Co. | 65 | 86,258 | ||||||

PPL Capital Funding, Inc. | 109 | 108,616 | ||||||

System Energy Resources, Inc. | 97 | 99,564 | ||||||

|

| |||||||

| 1,219,982 | ||||||||

|

| |||||||

Natural Gas – 5.9% | ||||||||

AGL Capital Corp. | 105 | 118,301 | ||||||

DCP Midstream LLC | 90 | 114,795 | ||||||

Enbridge Energy Partners LP | 100 | 104,519 | ||||||

Energy Transfer Partners LP | 75 | 78,350 | ||||||

4.65%, 6/01/21 | 150 | 159,968 | ||||||

5.20%, 2/01/22 | 170 | 185,873 | ||||||

Enterprise Products Operating LLC | 350 | 396,708 | ||||||

Kinder Morgan Energy Partners LP | 175 | 175,989 | ||||||

7.40%, 3/15/31 | 145 | 177,906 | ||||||

| 18 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

| Principal Amount (000) | U.S. $ Value | |||||||

| ||||||||

NiSource Finance Corp. | $ | 100 | $ | 119,025 | ||||

ONEOK Partners LP | 240 | 234,782 | ||||||

Spectra Energy Capital LLC | 70 | 86,630 | ||||||

Spectra Energy Partners LP | 77 | 79,198 | ||||||

4.60%, 6/15/21 | 75 | 81,144 | ||||||

Sunoco Logistics Partners Operations LP | 54 | 55,059 | ||||||

5.30%, 4/01/44 | 60 | 62,276 | ||||||

Williams Partners LP | 300 | 333,285 | ||||||

Williams Partners LP/Williams Partners Finance Corp. | 115 | 132,027 | ||||||

|

| |||||||

| 2,695,835 | ||||||||

|

| |||||||

| 3,915,817 | ||||||||

|

| |||||||

Non-Corporate Sectors – 1.1% | ||||||||

Agencies - Not Government Guaranteed – 1.1% | ||||||||

CNOOC Finance 2013 Ltd. | 295 | 270,594 | ||||||

Ecopetrol SA | 77 | 84,219 | ||||||

Petrobras International Finance Co. | 130 | 133,136 | ||||||

|

| |||||||

| 487,949 | ||||||||

|

| |||||||

Total Corporates – Investment Grades | 41,587,228 | |||||||

|

| |||||||

GOVERNMENTS – TREASURIES – 3.8% | ||||||||

United States – 3.8% | ||||||||

U.S. Treasury Bonds | 660 | 623,906 | ||||||

3.625%, 8/15/43-2/15/44 | 850 | 876,438 | ||||||

4.625%, 2/15/40 | 195 | 237,717 | ||||||

|

| |||||||

Total Governments – Treasuries | 1,738,061 | |||||||

|

| |||||||

QUASI-SOVEREIGNS – 1.6% | ||||||||

Quasi-Sovereign Bonds – 1.6% | ||||||||

Mexico – 1.6% | ||||||||

Comision Federal de Electricidad | 200 | 198,750 | ||||||

Petroleos Mexicanos | 455 | 445,313 | ||||||

6.625%, 6/15/35 | 70 | 78,400 | ||||||

|

| |||||||

Total Quasi-Sovereigns | 722,463 | |||||||

|

| |||||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 19 |

Portfolio of Investments

| Company |

Shares | U.S. $ Value | ||||||

| ||||||||

PREFERRED STOCKS – 0.9% | ||||||||

Financial Institutions – 0.9% | ||||||||

Banking – 0.5% | ||||||||

US Bancorp/MN | 9,000 | $ | 249,300 | |||||

|

| |||||||

Insurance – 0.4% | ||||||||

Allstate Corp. (The) | 6,950 | 174,584 | ||||||

|

| |||||||

Total Preferred Stocks | 423,884 | |||||||

|

| |||||||

| Principal Amount (000) | ||||||||

GOVERNMENTS – SOVEREIGN | ||||||||

Poland – 0.9% | ||||||||

Poland Government International Bond | $ | 410 | 413,485 | |||||

|

| |||||||

CORPORATES – NON-INVESTMENT | ||||||||

Industrial – 0.2% | ||||||||

Basic – 0.2% | ||||||||

Commercial Metals Co. | 80 | 90,900 | ||||||

|

| |||||||

Financial Institutions – 0.1% | ||||||||

Finance – 0.1% | ||||||||

SLM Corp. | 46 | 47,323 | ||||||

|

| |||||||

Total Corporates – Non-Investment Grades | 138,223 | |||||||

|

| |||||||

SHORT-TERM INVESTMENTS – 0.3% | ||||||||

Time Deposit – 0.3% | ||||||||

State Street Time Deposit | 119 | 119,132 | ||||||

|

| |||||||

Total Investments – 98.2% | 45,142,476 | |||||||

Other assets less liabilities – 1.8% | 846,842 | |||||||

|

| |||||||

Net Assets – 100.0% | $ | 45,989,318 | ||||||

|

| |||||||

| 20 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Portfolio of Investments

CENTRALLY CLEARED INTEREST RATE SWAPS (see Note C)

| Rate Type | ||||||||||||||||

| Clearing Broker / (Exchange) | Notional Amount (000) | Termination Date | Payments made by the Fund | Payments received by the Fund | Unrealized Appreciation/ (Depreciation) | |||||||||||

Citigroup Global Markets Inc./(CME Group) | $ | 510 | 5/02/24 | 2.790% | 3 Month LIBOR | $ | – 0 | – | ||||||||

Citigroup Global Markets Inc./(CME Group) | 320 | 5/02/34 | 3 Month LIBOR | 3.363% | – 0 | – | ||||||||||

Morgan Stanley & Co., LLC/(CME Group) | 770 | 11/29/23 | 2.793% | 3 Month LIBOR | (15,253 | ) | ||||||||||

Morgan Stanley & Co., LLC/(CME Group) | 510 | 1/28/24 | 2.861% | 3 Month LIBOR | (10,236 | ) | ||||||||||

Morgan Stanley & Co., LLC/(CME Group) | 250 | 1/29/24 | 2.880% | 3 Month LIBOR | (5,451 | ) | ||||||||||

|

| |||||||||||||||

| $ | (30,940 | ) | ||||||||||||||

|

| |||||||||||||||

INTEREST RATE SWAPS (see Note C)

| Rate Type | ||||||||||||||||

| Swap Counterparty | Notional Amount (000) | Termination Date | Payments made by the Fund | Payments received by the Fund | Unrealized Appreciation/ (Depreciation) | |||||||||||

Barclays Bank PLC | $ | 470 | 6/10/23 | 2.264% | 3 Month LIBOR | $ | 10,603 | |||||||||

Deutsche Bank AG | 600 | 6/10/43 | 3 Month LIBOR | 3.191% | (22,154 | ) | ||||||||||

JPMorgan Chase Bank, NA | 520 | 6/10/23 | 2.293% | 3 Month LIBOR | 10,410 | |||||||||||

JPMorgan Chase Bank, NA | 350 | 6/10/33 | 3 Month LIBOR | 3.027% | (10,876 | ) | ||||||||||

|

| |||||||||||||||

| $ | (12,017 | ) | ||||||||||||||

|

| |||||||||||||||

| (a) | Security is exempt from registration under Rule 144A of the Securities Act of 1933. These securities are considered liquid and may be resold in transactions exempt from registration, normally to qualified institutional buyers. At April 30, 2014, the aggregate market value of these securities amounted to $4,711,166 or 10.2% of net assets. |

| (b) | Variable rate coupon, rate shown as of April 30, 2014. |

Glossary:

CME – Chicago Mercantile Exchange

LIBOR – London Interbank Offered Rates

REIT – Real Estate Investment Trust

See notes to financial statements.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 21 |

Portfolio of Investments

STATEMENT OF ASSETS & LIABILITIES

April 30, 2014

| Assets | ||||

Investments in securities, at value (cost $43,760,008) | $ | 45,142,476 | ||

Due from broker | 42,070 | (a) | ||

Interest receivable | 543,711 | |||

Receivable for investment securities sold | 416,664 | |||

Receivable for shares of beneficial interest sold | 45,889 | |||

Unrealized appreciation on interest rate swaps | 21,013 | |||

|

| |||

Total assets | 46,211,823 | |||

|

| |||

| Liabilities | ||||

Dividends payable | 141,547 | |||

Payable for shares of beneficial interest redeemed | 38,900 | |||

Unrealized depreciation on interest rate swaps | 33,030 | |||

Payable for variation margin on centrally cleared interest rate swaps | 5,880 | |||

Payable for investment securities purchased | 3,148 | |||

|

| |||

Total liabilities | 222,505 | |||

|

| |||

Net Assets | $ | 45,989,318 | ||

|

| |||

| Composition of Net Assets | ||||

Shares of beneficial interest, at par | $ | 41 | ||

Additional paid-in capital | 45,761,089 | |||

Undistributed net investment income | 81,883 | |||

Accumulated net realized loss on investment transactions | (1,193,206 | ) | ||

Net unrealized appreciation on investments | 1,339,511 | |||

|

| |||

| $ | 45,989,318 | |||

|

| |||

Net Asset Value Per Share—unlimited shares of beneficial interest authorized, $.00001 par value (based on 4,133,235 common shares outstanding) | $ | 11.13 | ||

|

|

| (a) | Represents amount on deposit at the broker as collateral for open derivative contracts. |

See notes to financial statements.

| 22 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Statement of Assets & Liabilities

STATEMENT OF OPERATIONS

Year Ended April 30, 2014

| Investment Income | ||||||||

Interest | $ | 1,735,130 | ||||||

Dividends | 22,361 | |||||||

|

| |||||||

Total investment income | $ | 1,757,491 | ||||||

|

| |||||||

| Realized and Unrealized Gain (Loss) on Investment Transactions | ||||||||

Net realized gain (loss) on: | ||||||||

Investment transactions | (2,418 | ) | ||||||

Swaps | 4,576 | |||||||

Net change in unrealized appreciation/depreciation of: | ||||||||

Investments | (940,348 | ) | ||||||

Swaps | (42,957 | ) | ||||||

|

| |||||||

Net loss on investment transactions | (981,147 | ) | ||||||

|

| |||||||

Net Increase in Net Assets from Operations | $ | 776,344 | ||||||

|

|

See notes to financial statements.

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 23 |

Statement of Operations

STATEMENT OF CHANGES IN NET ASSETS

| Year Ended April 30, 2014 | Year Ended April 30, 2013 | |||||||

| Increase (Decrease) in Net Assets from Operations | ||||||||

Net investment income | $ | 1,757,491 | $ | 1,774,202 | ||||

Net realized gain on investment transactions | 2,158 | 1,890,585 | ||||||

Net change in unrealized appreciation/depreciation of investments | (983,305 | ) | 393,090 | |||||

|

|

|

| |||||

Net increase in net assets from operations | 776,344 | 4,057,877 | ||||||

| Dividends to Shareholders from | ||||||||

Net investment income | (1,755,639 | ) | (1,776,601 | ) | ||||

| Transactions in Shares of Beneficial Interest | ||||||||

Net increase (decrease) | 4,169,590 | (6,330,460 | ) | |||||

|

|

|

| |||||

Total increase (decrease) | 3,190,295 | (4,049,184 | ) | |||||

| Net Assets | ||||||||

Beginning of period | 42,799,023 | 46,848,207 | ||||||

|

|

|

| |||||

End of period (including undistributed net investment income of $81,883 and $75,455, respectively) | $ | 45,989,318 | $ | 42,799,023 | ||||

|

|

|

| |||||

See notes to financial statements.

| 24 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Statement of Changes in Net Assets

NOTES TO FINANCIAL STATEMENTS

April 30, 2014

NOTE A

Significant Accounting Policies

AllianceBernstein Corporate Shares (the “Trust”) was organized as a Massachusetts business trust under the laws of The Commonwealth of Massachusetts by an Agreement and Declaration of Trust dated January 26, 2004. The Trust is registered under the Investment Company Act of 1940, as an open-end, diversified management investment company. The Trust operates as a “series” company and currently offers three separate portfolios: AllianceBernstein Corporate Income Shares (the “Portfolio”), AllianceBernstein Municipal Income Shares and AllianceBernstein Taxable Multi-Sector Income Shares. Each Portfolio is considered to be a separate entity for financial reporting and tax purposes. This report relates only to AllianceBernstein Corporate Income Shares.

Shares of the Portfolio are offered exclusively to holders of accounts established under wrap-fee programs sponsored and maintained by certain registered investment advisers approved by AllianceBernstein L.P. (the “Adviser”). The Portfolio’s shares may be purchased at the relevant net asset value without a sales charge or other fee. The financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements and amounts of income and expenses during the reporting period. Actual results could differ from those estimates. The following is a summary of significant accounting policies followed by the Portfolio.

1. Security Valuation

Portfolio securities are valued at their current market value determined on the basis of market quotations or, if market quotations are not readily available or are deemed unreliable, at “fair value” as determined in accordance with procedures established by and under the general supervision of the Trust’s Board of Trustees (the “Board”).

In general, the market values of securities which are readily available and deemed reliable are determined as follows: securities listed on a national securities exchange (other than securities listed on the NASDAQ Stock Market, Inc. (“NASDAQ”)) or on a foreign securities exchange are valued at the last sale price at the close of the exchange or foreign securities exchange. If there has been no sale on such day, the securities are valued at the last traded price from the previous day. Securities listed on more than one exchange are valued by reference to the principal exchange on which the securities are traded; securities listed only on NASDAQ are valued in accordance with the NASDAQ Official Closing Price; listed or over the counter (“OTC”) market put or call options are valued at the mid level between the current bid and ask prices. If either a current bid or current ask price is unavailable, the Adviser will have discretion to determine the best valuation (e.g. last trade price in the case of listed options);

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 25 |

Notes to Financial Statements

open futures are valued using the closing settlement price or, in the absence of such a price, the most recent quoted bid price. If there are no quotations available for the day of valuation, the last available closing settlement price is used; U.S. government securities and other debt instruments having 60 days or less remaining until maturity are valued at amortized cost if their original maturity was 60 days or less. If the original term to maturity exceeded 60 days, the securities are valued by a pricing service, if a market price is available. If a market price is not available, the securities are valued by using amortized cost as of the 61st day prior to maturity. Fixed-income securities, including mortgage-backed and asset-backed securities, may be valued on the basis of prices provided by a pricing service or at a price obtained from one or more of the major broker-dealers. In cases where broker-dealer quotes are obtained, the Adviser may establish procedures whereby changes in market yields or spreads are used to adjust, on a daily basis, a recently obtained quoted price on a security. Swaps and other derivatives are valued daily, primarily using independent pricing services, independent pricing models using market inputs, as well as third party broker-dealers or counterparties. Investment companies are valued at their net asset value each day.

Securities for which market quotations are not readily available (including restricted securities) or are deemed unreliable are valued at fair value. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, analysis of the issuer’s financial statements or other available documents. In addition, the Portfolio may use fair value pricing for securities primarily traded in non-U.S. markets because most foreign markets close well before the Portfolio values its securities at 4:00 p.m., Eastern Time. The earlier close of these foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred in the interim and may materially affect the value of those securities.

2. Fair Value Measurements

In accordance with U.S. GAAP regarding fair value measurements, fair value is defined as the price that the Portfolio would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. U.S. GAAP establishes a framework for measuring fair value, and a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability (including those valued based on their market values as described in Note A.1 above). Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Portfolio. Unobservable inputs reflect the Portfolio’s own assumptions about the assumptions that market participants would use in pricing the asset or liability based on the best information available in the circumstances. Each investment is assigned a

| 26 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

level based upon the observability of the inputs which are significant to the overall valuation. The three-tier hierarchy of inputs is summarized below.

| • | Level 1—quoted prices in active markets for identical investments |

| • | Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| • | Level 3—significant unobservable inputs (including the Portfolio’s own assumptions in determining the fair value of investments) |

The fair value of debt instruments, such as bonds, and over-the-counter derivatives is generally based on market price quotations, recently executed market transactions (where observable) or industry recognized modeling techniques and are generally classified as Level 2. Pricing vendor inputs to Level 2 valuations may include quoted prices for similar investments in active markets, interest rate curves, coupon rates, currency rates, yield curves, option adjusted spreads, default rates, credit spreads and other unique security features in order to estimate the relevant cash flows which are then discounted to calculate fair values. If these inputs are unobservable and significant to the fair value, these investments will be classified as Level 3. In addition, non-agency rated investments are classified as Level 3.

Other fixed income investments, including non-U.S. government and corporate debt, are generally valued using quoted market prices, if available, which are typically impacted by current interest rates, maturity dates and any perceived credit risk of the issuer. Additionally, in the absence of quoted market prices, these inputs are used by pricing vendors to derive a valuation based upon industry or proprietary models which incorporate issuer specific data with relevant yield/spread comparisons with more widely quoted bonds with similar key characteristics. Those investments for which there are observable inputs are classified as Level 2. Where the inputs are not observable, the investments are classified as Level 3.

The following table summarizes the valuation of the Portfolio’s investments by the above fair value hierarchy levels as of April 30, 2014:

Investments in Securities: | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Assets: | ||||||||||||||||

Corporates – Investment Grades | $ | – 0 | – | $ | 41,587,228 | $ | – 0 | – | $ | 41,587,228 | ||||||

Governments – Treasuries | – 0 | – | 1,738,061 | – 0 | – | 1,738,061 | ||||||||||

Quasi-Sovereigns | – 0 | – | 722,463 | – 0 | – | 722,463 | ||||||||||

Preferred Stocks | 423,884 | – 0 | – | – 0 | – | 423,884 | ||||||||||

Governments – Sovereign Bonds | – 0 | – | 413,485 | – 0 | – | 413,485 | ||||||||||

Corporates – Non-Investment Grades | – 0 | – | 138,223 | – 0 | – | 138,223 | ||||||||||

Short-Term Investments | – 0 | – | 119,132 | – 0 | – | 119,132 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Investments in Securities | 423,884 | 44,718,592 | – 0 | – | 45,142,476 | |||||||||||

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 27 |

Notes to Financial Statements

Investments in Securities: | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Other Financial Instruments*: | ||||||||||||||||

Assets: | ||||||||||||||||

Interest Rate Swaps | $ | – 0 | – | $ | 21,013 | $ | – 0 | – | $ | 21,013 | ||||||

Liabilities: | ||||||||||||||||

Centrally Cleared Interest Rate Swaps | – 0 | – | (30,940 | ) | – 0 | – | (30,940 | )# | ||||||||

Interest Rate Swaps | – 0 | – | (33,030 | ) | – 0 | – | (33,030 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total^ | $ | 423,884 | $ | 44,675,635 | $ | – 0 | – | $ | 45,099,519 | |||||||

|

|

|

|

|

|

|

| |||||||||

| * | Other financial instruments are derivative instruments, such as futures, forwards and swaps, which are valued at the unrealized appreciation/depreciation on the instrument. |

| # | Only variation margin receivable/payable at period end is reported within the statement of assets and liabilities. This amount reflects cumulative appreciation/(depreciation) of exchange traded derivatives in the portfolio of investments. |

| ^ | There were no transfers between any levels during the reporting period. |

The Portfolio recognizes all transfers between levels of the fair value hierarchy assuming the financial instruments were transferred at the beginning of the reporting period.

The Adviser has established a Valuation Committee (the “Committee”) which is responsible for overseeing the pricing and valuation of all securities held in the Portfolio. The Committee operates under pricing and valuation policies and procedures established by the Adviser and approved by the Board, including pricing policies which set forth the mechanisms and processes to be employed on a daily basis to implement these policies and procedures. In particular, the pricing policies describe how to determine market quotations for securities and other instruments. The Committee’s responsibilities include: 1) fair value and liquidity determinations (and oversight of any third parties to whom any responsibility for fair value and liquidity determinations is delegated), and 2) regular monitoring of the Adviser’s pricing and valuation policies and procedures and modification or enhancement of these policies and procedures (or recommendation of the modification of these policies and procedures) as the Committee believes appropriate.

The Committee is also responsible for monitoring the implementation of the pricing policies by the Adviser’s Pricing Group (the “Pricing Group”) and a third party which performs certain pricing functions in accordance with the pricing policies. The Pricing Group is responsible for the oversight of the third party on a day-to-day basis. The Committee and the Pricing Group perform a series of activities to provide reasonable assurance of the accuracy of prices including: 1) periodic vendor due diligence meetings, review of methodologies, new developments and processes at vendors, 2) daily comparison of security valuation versus prior day for all securities that exceeded established thresholds, and 3) daily review of unpriced, stale, and variance reports with exceptions reviewed by senior management and the Committee.

| 28 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

In addition, several processes outside of the pricing process are used to monitor valuation issues including: 1) performance and performance attribution reports are monitored for anomalous impacts based upon benchmark performance, and 2) portfolio managers review all portfolios for performance and analytics (which are generated using the Adviser’s prices).

3. Taxes

It is the Portfolio’s policy to meet the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its investment company taxable income and net realized gains, if any, to shareholders. Therefore, no provisions for federal income or excise taxes are required.

In accordance with U.S. GAAP requirements regarding accounting for uncertainties in income taxes, management has analyzed the Portfolio’s tax positions taken or expected to be taken on federal and state income tax returns for all open tax years (the current and the prior three tax years) and has concluded that no provision for income tax is required in the Portfolio’s financial statements.

4. Investment Income and Investment Transactions

Dividend income is recorded on the ex-dividend date or as soon as the Portfolio is informed of the dividend. Interest income is accrued daily. Investment transactions are accounted for on the date the securities are purchased or sold. Investment gains or losses are determined on the identified cost basis. The Portfolio amortizes premiums and accretes discounts as adjustments to interest income.

5. Dividends and Distributions

Dividends and distributions to shareholders, if any, are recorded on the ex-dividend date. Income dividends and capital gains distributions are determined in accordance with federal tax regulations and may differ from those determined in accordance with U.S. GAAP. To the extent these differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax basis treatment; temporary differences do not require such reclassification.

NOTE B

Advisory Fee and Other Transactions with Affiliates

Under the terms of the Advisory Agreement, the Portfolio pays no advisory fee to the Adviser and the Adviser reimburses or pays for the Portfolio’s operating expenses. The Portfolio is an integral part of separately managed accounts in wrap-fee programs and other investment programs. Typically, participants in these programs pay a fee to their investment adviser for all costs and expenses of the separately managed account, including costs and expenses associated with the Portfolio, and a fee is paid by their investment adviser to the Adviser. The Adviser serves as investment manager and adviser of the Portfolio and continuously furnishes an investment program for the Portfolio and manages, supervises and conducts the affairs of the Portfolio, subject to the supervisions of

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 29 |

Notes to Financial Statements

the Portfolio’s Board. The Advisory Agreement provides that the Adviser or an affiliate will furnish, or pay the expenses of the Portfolio for, office space, facilities and equipment, services of executive and other personnel of the Portfolio and certain administrative services.

The Portfolio has entered into a Distribution Agreement with AllianceBernstein Investments, Inc., the Portfolio’s principal underwriter (the “Underwriter”), to permit the Underwriter to distribute the Portfolio’s shares, which are sold at their net asset value without any sales charge. The Portfolio does not pay a fee for this service. The Underwriter is a wholly owned subsidiary of the Adviser.

AllianceBernstein Investor Services, Inc. (“ABIS”), a wholly-owned subsidiary of the Adviser, acts as the Portfolio’s registrar, transfer agent and dividend-disbursing agent. ABIS registers the transfer, issuance and redemption of Portfolio shares and disburses dividends and other distributions to Portfolio shareholders. The Portfolio does not pay a fee for this service.

NOTE C

Investment Transactions

Purchases and sales of investment securities (excluding short-term investments) for the year ended April 30, 2014 were as follows:

| Purchases | Sales | |||||||

Investment securities (excluding | $ | 23,469,205 | $ | 19,861,040 | ||||

U.S. government securities | 7,767,261 | 7,174,326 | ||||||

The cost of investments for federal income tax purposes, gross unrealized appreciation and unrealized depreciation are as follows:

Cost | $ | 43,790,616 | ||

|

| |||

Gross unrealized appreciation | $ | 1,571,043 | ||

Gross unrealized depreciation | (219,183 | ) | ||

|

| |||

Net unrealized appreciation | $ | 1,351,860 | ||

|

|

1. Derivative Financial Instruments

The Portfolio may use derivatives in an effort to earn income and enhance returns, to replace more traditional direct investments, to obtain exposure to otherwise inaccessible markets (collectively, “investment purposes”), or to hedge or adjust the risk profile of its portfolio.

The principal type of derivatives utilized by the Portfolio, as well as the methods in which they may be used are:

| • | Swaps |

The Portfolio may enter into swaps to hedge its exposure to interest rates, credit risk, or currencies. The Portfolio may also enter into swaps for non-hedging purposes as a means of gaining market exposures, including by

| 30 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

making direct investments in foreign currencies. A swap is an agreement that obligates two parties to exchange a series of cash flows at specified intervals based upon or calculated by reference to changes in specified prices or rates for a specified amount of an underlying asset. The payment flows are usually netted against each other, with the difference being paid by one party to the other. In addition, collateral may be pledged or received by the Portfolio in accordance with the terms of the respective swaps to provide value and recourse to the Portfolio or its counterparties in the event of default, bankruptcy or insolvency by one of the parties to the swap.

Risks may arise as a result of the failure of the counterparty to the swap to comply with the terms of the swap. The loss incurred by the failure of a counterparty is generally limited to the net interim payment to be received by the Portfolio, and/or the termination value at the end of the contract. Therefore, the Portfolio considers the creditworthiness of each counterparty to a swap in evaluating potential counterparty risk. This risk is mitigated by having a netting arrangement between the Portfolio and the counterparty and by the posting of collateral by the counterparty to the Portfolio to cover the Portfolio exposure to the counterparty. Additionally, risks may arise from unanticipated movements in interest rates or in the value of the underlying securities. The Portfolio accrues for the interim payments on swaps on a daily basis, with the net amount recorded within unrealized appreciation/depreciation of swaps on the statement of assets and liabilities, where applicable. Once the interim payments are settled in cash, the net amount is recorded as realized gain/(loss) on swaps on the statement of operations, in addition to any realized gain/(loss) recorded upon the termination of swaps. Fluctuations in the value of swaps are recorded as a component of net change in unrealized appreciation/depreciation of swaps on the statement of operations.

Certain standardized swaps, including certain interest rate swaps and credit default swaps, are (or soon will be) subject to mandatory central clearing. Cleared swaps are transacted through futures commission merchants (“FCMs”) that are members of central clearinghouses, with the clearinghouse serving as central counterparty, similar to transactions in futures contracts. Centralized clearing will be required for additional categories of swaps on a phased-in basis based on requirements published by the Securities and Exchange Commission and Commodity Futures Trading Commission.

At the time the Portfolio enters into a centrally cleared swap, the Portfolio deposits and maintains as collateral an initial margin with the broker, as required by the exchange on which the transaction is effected. Such amount is shown as due from broker on the statement of assets and liabilities. Pursuant to the contract, the Portfolio agrees to receive from or

pay to the broker an amount of cash equal to the daily fluctuation in the

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 31 |

Notes to Financial Statements

value of the contract. Such receipts or payments are known as variation margin and are recorded by the Portfolio as unrealized gains or losses. Risks may arise from the potential of a counterparty to meet the terms of the contract. The credit/counterparty risk for exchange-traded swaps is generally less than privately negotiated swaps, since the clearinghouse, which is the issuer or counterparty to each exchange-traded swap, has robust risk mitigation standards, including the requirement to provide initial and variation margin. When the contract is closed, the Portfolio records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the time it was closed.

Interest Rate Swaps:

The Portfolio is subject to interest rate risk exposure in the normal course of pursuing its investment objectives. Because the Portfolio holds fixed rate bonds, the value of these bonds may decrease if interest rates rise. To help hedge against this risk and to maintain its ability to generate income at prevailing market rates, the Portfolio may enter into interest rate swaps. Interest rate swaps are agreements between two parties to exchange cash flows based on a notional amount. The Portfolio may elect to pay a fixed rate and receive a floating rate, or, receive a fixed rate and pay a floating rate on a notional amount.

In addition, a Portfolio may also enter into interest rate swap transactions to preserve a return or spread on a particular investment or portion of its portfolio, or protecting against an increase in the price of securities the Portfolio anticipates purchasing at a later date. Interest rate swaps involve the exchange by the Portfolio with another party of their respective commitments to pay or receive interest (e.g., an exchange of floating rate payments for fixed rate payments) computed based on a contractually-based principal (or “notional”) amount. Interest rate swaps are entered into on a net basis (i.e., the two payment streams are netted out, with the Portfolio receiving or paying, as the case may be, only the net amount of the two payments).

During the year ended April 30, 2014, the Portfolio held interest rate swaps for hedging and non-hedging purposes.

The Portfolio typically enters into International Swaps and Derivatives Association, Inc. Master Agreements (“ISDA Master Agreement”) or similar master agreements (collectively, “Master Agreements”) with its OTC derivative contract counterparties in order to, among other things, reduce its credit risk to counterparties. ISDA Master Agreements include provisions for general obligations, representations, collateral and events of default or termination. Under an ISDA Master Agreement, the Portfolio typically may offset with the counterparty certain derivative financial instrument’s payables and/or receivables with collateral held and/or posted and create one single net payment (close-out netting) in the event of default or termination.

| 32 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

Various Master Agreements govern the terms of certain transactions with counterparties, including transactions such as exchange-traded derivative transactions, repurchase and reverse repurchase agreements. These Master Agreements typically attempt to reduce the counterparty risk associated with such transactions by specifying credit protection mechanisms and providing standardization that improves legal certainty. Cross-termination provisions under Master Agreements typically provide that a default in connection with one transaction between the Portfolio and a counterparty gives the non-defaulting party the right to terminate any other transactions in place with the defaulting party to create one single net payment due to/due from the defaulting party. In the event of a default by a Master Agreements counterparty, the return of collateral with market value in excess of the Portfolio’s net liability, held by the defaulting party, may be delayed or denied.

The Portfolio’s Master Agreements may contain provisions for early termination of OTC derivative transactions in the event the net assets of the Portfolio decline below specific levels (“net asset contingent features”). If these levels are triggered, the Portfolio’s counterparty has the right to terminate such transaction and require the Portfolio to pay or receive a settlement amount in connection with the terminated transaction. As of April 30, 2014, the Portfolio had OTC derivatives with contingent features in net liability positions in the amount of $22,620. If a trigger event had occurred at April 30, 2014, for those derivatives in a net liability position, an amount of $22,620 would be required to be posted by the Portfolio.

At April 30, 2014, the Portfolio had entered into the following derivatives:

Asset Derivatives | Liability Derivatives | |||||||||||

Derivative Type | Statement of | Fair Value | Statement of | Fair Value | ||||||||

Interest rate contracts |

Unrealized appreciation on interest rate swaps | $ | 21,013 |

|

Unrealized depreciation on interest rate swaps | $ | 33,030 |

| ||||

Interest rate contracts |

Receivable/Payable for variation margin on centrally cleared interest rate swaps |

| 30,940 | * | ||||||||

|

|

|

| |||||||||

Total | $ | 21,013 | $ | 63,970 | ||||||||

|

|

|

| |||||||||

| * | Only variation margin receivable/payable at period end is reported within the statement of assets and liabilities. This amount reflects cumulative appreciation/(depreciation) of exchange-traded derivatives as reported in the portfolio of investments. |

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 33 |

Notes to Financial Statements

The effect of derivative instruments on the statement of operations for the year ended April 30, 2014:

Derivative Type | Location of Gain | Realized Gain or (Loss) on Derivatives | Change in Unrealized Appreciation or (Depreciation) | |||||||

Interest rate contracts | Net realized gain (loss) on swaps; Net change in unrealized appreciation/depreciation of swaps | $ | 4,576 | $ | (42,957 | ) | ||||

|

|

|

| |||||||

Total | $ | 4,576 | $ | (42,957 | ) | |||||

|

|

|

| |||||||

The following table represents the volume of the Portfolio’s derivative transactions during the year ended April 30, 2014:

Interest Rate Swaps: | ||||

Average notional amount | $ | 1,940,000 | (a) | |

Centrally Cleared Interest Rate Swaps: | ||||

Average notional amount | $ | 1,415,000 | (b) |

| (a) | Positions were open for eleven months during the year. |

| (b) | Positions were open for six months during the year. |

For financial reporting purposes, the Portfolio does not offset derivative assets and derivative liabilities that are subject to netting arrangements in the statement of assets and liabilities.

All derivatives held at period end were subject to netting arrangements. The following table presents the Portfolio’s derivative assets and liabilities by counterparty net of amounts available for offset under Master Agreements (“MA”) and net of the related collateral received/ pledged by the Portfolio as of April 30, 2014:

Counterparty | Derivative Assets Subject to MA | Derivative Available for Offset | Cash Collateral Received | Securities Collateral Received | Net Amount of Derivatives Assets | |||||||||||||||

Barclays Bank PLC | $ | 10,603 | $ | – 0 | – | $ | – 0 | – | $ | – 0 | – | $ | 10,603 | |||||||

JPMorgan Chase Bank, NA | 10,410 | (10,410 | ) | – 0 | – | – 0 | – | – 0 | – | |||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total | $ | 21,013 | $ | (10,410 | ) | $ | – 0 | – | $ | – 0 | – | $ | 10,603 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| 34 | • ALLIANCEBERNSTEIN CORPORATE INCOME SHARES |

Notes to Financial Statements

Counterparty | Derivative Liabilities Subject to a MA | Derivatives Available for Offset | Cash Collateral Pledged | Securities Collateral Pledged | Net Amount of Derivatives Liabilities | |||||||||||||||

Deutsche Bank AG | $ | 22,154 | $ | – 0 | – | $ | – 0 | – | $ | – 0 | – | $ | 22,154 | |||||||

Exchange-Traded Morgan Stanley & Co., LLC* | 5,880 | – 0 | – | (5,880 | )** | – 0 | – | – 0 | – | |||||||||||

JPMorgan Chase Bank, NA | 10,876 | (10,410 | ) | – 0 | – | – 0 | – | 466 | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total | $ | 38,910 | $ | (10,410 | ) | $ | (5,880 | ) | $ | – 0 | – | $ | 22,620 | |||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| * | Cash has been posted for initial margin requirements for exchange-traded derivatives outstanding at April 30, 2014. |

| ** | The actual collateral received/pledged is more than the amount reported due to overcollateralization. |

NOTE D

Shares of Beneficial Interest

Transactions in shares of beneficial interest were as follows:

| Shares | Amount | |||||||||||||||||||

| Year Ended April 30, 2014 | Year Ended April 30, 2013 | Year Ended April 30, 2014 | Year Ended April 30, 2013 | |||||||||||||||||

|

| |||||||||||||||||||

| Class A | ||||||||||||||||||||

Shares sold | 1,360,531 | 1,477,058 | $ | 14,748,542 | $ | 16,643,111 | ||||||||||||||

| ||||||||||||||||||||

Shares redeemed | (976,510 | ) | (2,054,764 | ) | (10,578,952 | ) | (22,973,571 | ) | ||||||||||||

| ||||||||||||||||||||

Net increase (decrease) | 384,021 | (577,706 | ) | $ | 4,169,590 | $ | (6,330,460 | ) | ||||||||||||

| ||||||||||||||||||||

NOTE E

Risks Involved in Investing in the Portfolio

Interest Rate Risk and Credit Risk—Interest rate risk is the risk that changes in interest rates will affect the value of the Portfolio’s investments in fixed-income debt securities such as bonds or notes. Increases in interest rates may cause the value of the Portfolio’s investments to decline. Credit risk is the risk that the issuer or guarantor of a debt security, or the counterparty to a derivative contract, will be unable or unwilling to make timely principal and/or interest payments, or to otherwise honor its obligations. The degree of risk for a particular security may be reflected in its credit rating. Credit risk is greater for medium quality and lower-rated securities. Lower-rated debt securities and similar unrated securities (commonly known as “junk bonds”) have speculative elements or are predominantly speculative risks.

Indemnification Risk—In the ordinary course of business, the Portfolio enters into contracts that contain a variety of indemnifications. The Portfolio’s maximum

| ALLIANCEBERNSTEIN CORPORATE INCOME SHARES • | 35 |

Notes to Financial Statements

exposure under these arrangements is unknown. However, the Portfolio has not had prior claims or losses pursuant to these indemnification provisions and expects the risk of loss thereunder to be remote. Therefore, the Portfolio has not accrued any liability in connection with these indemnification provisions.

NOTE F

Distributions to Shareholders

The tax character of distributions paid during the fiscal years ended April 30, 2014 and April 30, 2013 were as follows:

| 2014 | 2013 | |||||||

Distributions paid from: | ||||||||