UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21503

The FBR Funds

(Exact name of registrant as specified in charter)

1001 Nineteenth Street North

Arlington, VA 22209

(Address of principal executive offices) (Zip code)

Registrant’s telephone number, including area code: 703.469.1040

William Ginivan

General Counsel

FBR & Co.

Potomac Tower

1001 Nineteenth Street North

Arlington, VA 22209

(Name and address of agent for service)

Date of fiscal year end: October 31, 2011

Date of reporting period: October 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1. REPORT TO SHAREHOLDERS.

The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17CRF 270.30e-1).

|

| |

| |

| THE FBR FUNDS |

| |

| FBR Large Cap Fund |

| FBR Mid Cap Fund |

| FBR Small Cap Fund |

| FBR Focus Fund |

| FBR Large Cap Financial Fund |

| FBR Small Cap Financial Fund |

| FBR Technology Fund |

| FBR Gas Utility Index Fund |

| FBR Balanced Fund |

| FBR Core Bond Fund |

| |

Annual Report

October 31, 2011 |

[THIS PAGE INTENTIONALLY LEFT BLANK]

Annual Letter to Shareholders

Dear Shareholder:

We are pleased to present The FBR Funds’ Annual Report for the twelve-month period ended October 31, 2011. U.S. equity markets performed reasonably well during the twelve-month period. The Dow Jones Industrial Average rose 10.39%. The S&P 500 gained 8.09%, and the small capitalization Russell 2000 Index rose 6.71%. The best performing industry groups during the period were energy, real estate investment trusts and utilities. The worst performing industry groups during the period were industrials, basic materials and financial services. Finally, the S&P 500 remains 25% off its high reached on October 2007, before the financial crisis hit.

The last twelve months have been much the same as the previous twelve months before them. The investment roller coaster that began in 2007, when the financial bubble burst, continues. We believe that the economy remains over-leveraged and the growth headwinds of deleveraging will continue into 2012. The big, but not surprising, development in the last twelve months is that Europe has debt troubles too. Europe appears more over-leveraged than the U.S. and has, adding to concerns, a tenuous economic union among its common market members. Finally, it appears the new revelation in 2012 will be that China is over-leveraged as well.

After many years of borrowing prosperity, we are now in a worldwide effort to cut leverage and expenses to service the debt that produced the prosperity. Both strategies were brought about by central banks and politicians across the world. With governments over-leveraged, the outlook for growth will be muted as governments implement austerity programs. How long this period persists will depend on many things. Continued volatility is expected.

While our outlook is for difficult investment conditions, we believe our investment process is well suited to weather the storm(s). We believe our focus on well-constructed balance sheets and businesses with stable and longer term earnings potential will protect the downside and give our investors the best chance for positive returns. We remain buyers of companies, not traders of stocks.

As in prior years, what follows is a commentary from each portfolio manager or team regarding fund performance and their outlook. We believe this commentary is an important part of our semi-annual communication to you. We encourage you to read their comments to gain a better understanding of their current thinking.

All of us at The FBR Funds want to thank you for your continued support, and we look forward to serving your investment needs in the years ahead. As always, we welcome your questions and comments. You can reach us via e-mail at fbrfundsinfo@fbr.com or toll free at 888.888.0025. If you would like more timely updates, www.fbrfunds.com provides quarterly performance data as well as other important information.

Sincerely,

David H. Ellison

President, Chief Investment Officer and Trustee

The FBR Funds

2

Past performance is no guarantee of future results. The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption fees. If reflected, the redemption fee would reduce the performance quoted. To obtain performance data current to the most recent month-end please call 888.200.4710.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. This and other important information can be found in the Funds’ prospectus. To obtain a free prospectus, please call 888.200.4710 or visit www.fbrfunds.com. Please read the prospectus carefully before investing.

The FBR Funds are distributed by FBR Investment Services, Inc., member FINRA/SIPC.

3

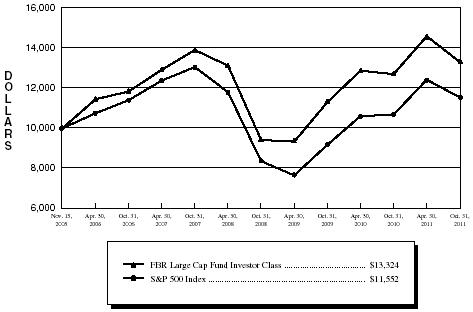

FBR Large Cap Fund

Management Overview

Portfolio Managers: Robert Barringer, CFA® and Ryan Kelley, CFA®

Over the previous 12 months, how did the Fund perform and what factors contributed to this performance?

For the twelve-month period ended October 31, 2011, the Investor Class Shares of the FBR Large Cap Fund returned 4.80%. This compares to the S&P 500 Index and the Morningstar Large Blend Category Average which over the same time period returned 8.09% and 5.33%, respectively.

During our fiscal year, the S&P 500 Index’s total return of 8.09% was a strong continuation of the positive momentum which began after the stock market bottom in March 2009. However, while the S&P 500 Index’s return of over 16% in the first half of the fiscal year was impressive, every major sector (except utilities) of the domestic equity market declined or was flat in the second half, and the S&P 500 Index had a total return of negative 7%. Among the issues that caused this erosion of investor confidence were: the continued European crisis; the unprecedented downgrade of the U.S. credit rating by Standard & Poor’s; and the continued weakness in the U.S. economy, including the struggling housing market and weak employment trends.

For the year, the Fund lagged both its benchmark index and Morningstar category, although it lagged its category by a small amount. While we are disappointed by our relative performance, we are encouraged that we outperformed the category during the weak second half of the year by approximately 38 basis points. One of the goals of the Fund is to outperform during weak markets, as we believe that strong returns are achieved over the long term by losing less value when the market is in decline.

During the fiscal year, technology, industrial, consumer, and energy related stocks performed exceptionally well and contributed the majority of our positive returns. Conversely, the Fund continued to suffer from its exposure to financial services companies, which was the only sector that showed negative returns for the fiscal year in both the Fund and the S&P 500 Index.

On a relative basis, industrial and technology investments performed best compared to our benchmark. Additionally, both in the industrial and consumer cyclical space, our stock selection drove the relative outperformance, as we were invested in stocks that performed significantly better on average than the general index. Conversely, our relative performance was most negatively affected by our investments in energy and financials.

Portfolio Managers’ comments on the Fund and the related investment outlook.

The Fund generally performs better than its benchmark in difficult environments but may lag as stocks rise rapidly, due to our portfolio management philosophy and style. We focus on high quality companies with strong balance sheets and consistent, high profitability, which means we may not be invested in some of the more volatile, cyclical stocks that soar during economic recoveries. We continue to position the portfolio in such a way as to seek

4

FBR Large Cap Fund

Management Overview (continued)

to outperform in difficult times while striving to keep pace during market upswings. We are disappointed by our relative performance for the entire fiscal year, despite beating our category for the second half.

We strive to invest in companies trading at attractive valuations that exhibit strong returns on equity with low volatility, low financial leverage and debt levels, good management teams, and compelling prospects of continued strong profitability. As of October 31, 2011, we are currently close to fully invested, and, of the major sectors, the Fund is slightly overweight technology and energy and underweight the consumer sector.

The stock market continues to be negatively impacted by both global issues as well as domestic economic and political problems. These issues are persistent, and we believe it will take some time for conditions to improve, despite unprecedented efforts on a global scale among many countries’ governments and monetary policy makers to find solutions for many of our economic problems. During this time of continued economic difficulties, we have positioned the Fund in a diverse array of companies that exhibit strong balance sheets, strong profitability, and less cyclicality.

The opinions expressed in this commentary reflect those of the Portfolio Managers as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

5

FBR Large Cap Fund

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. S&P 500 Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2011(4) | |

| | | | | | | Annualized | |

| | | | | Annualized | | Since | |

| | | One Year | | Five Year | | Inception(5) | |

| | |

| |

| |

| |

| FBR Large Cap Fund Investor Class(1)(2) | | 4.80% | | 2.38% | | 4.93% | |

| FBR Large Cap Fund Institutional Class(2)(6) | | 5.08% | | 2.51% | | 5.05% | |

| S&P 500 Index(1)(3) | | 8.09% | | 0.25% | | 2.45% | |

| |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. The Fund charges a redemption fee of 1.00% on shares redeemed or exchanged within 90 days; if reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710.

| |

|

| (1) | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | The S&P 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to represent the broad domestic economy through changes in aggregate market value of 500 stocks representing all major industries. |

| (4) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | For the period November 15, 2005 (commencement of operations) through October 31, 2011. |

| (6) | Represents the performance of the Institutional Class shares after May 30, 2008 (inception of the share class) and Investor Class for periods prior to that date. |

6

FBR Large Cap Fund

Portfolio Summary

October 31, 2011

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | % of Total Investments |

|

|

| Technology | | 18.2 | % |

| Consumer, Non-Cyclical | | 18.1 | % |

| Financial | | 13.4 | % |

| Energy | | 12.6 | % |

| Consumer, Cyclical | | 10.6 | % |

| Industrial | | 10.1 | % |

| Communications | | 6.6 | % |

| Basic Materials | | 4.4 | % |

| Utilities | | 1.9 | % |

| | | | |

| Cash | | 4.1 | % |

7

FBR Large Cap Fund

Portfolio of Investments

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | COMMON STOCKS — 95.9% | | | | |

| | | Basic Materials — 4.4% | | | | |

| 6,000 | | E.I. du Pont de Nemours and Co. | | $ | 288,420 | |

| 13,500 | | Freeport-McMoRan Copper & Gold, Inc. | | | 543,510 | |

| 3,000 | | Monsanto Co. | | | 218,250 | |

| 7,000 | | Newmont Mining Corp. | | | 467,810 | |

| 10,600 | | Ternium S.A. ADR | | | 260,124 | |

| | | | |

| |

| | | | | | 1,778,114 | |

| | | | |

| |

| | | Communications — 6.6% | | | | |

| 1,000 | | Amazon.com, Inc.* | | | 213,510 | |

| 33,600 | | Cisco Systems, Inc. | | | 622,608 | |

| 1,600 | | Google, Inc., Class A* | | | 948,224 | |

| 900 | | LinkedIn Corp., Class A* | | | 80,910 | |

| 6,500 | | Rackspace Hosting, Inc.* | | | 269,035 | |

| 30,800 | | Yahoo, Inc.* | | | 481,712 | |

| | | | |

| |

| | | | | | 2,615,999 | |

| | | | |

| |

| | | Consumer, Cyclical — 10.6% | | | | |

| 8,900 | | Bed Bath & Beyond, Inc.* | | | 550,376 | |

| 2,970 | | C.R. Bard, Inc. | | | 255,271 | |

| 9,400 | | Coach, Inc. | | | 611,658 | |

| 3,500 | | Deckers Outdoor Corp.* | | | 403,340 | |

| 11,700 | | Genuine Parts Co. | | | 671,931 | |

| 11,700 | | Kohl’s Corp. | | | 620,217 | |

| 2,000 | | Panera Bread Co., Class A* | | | 267,380 | |

| 7,500 | | Tiffany & Co. | | | 597,975 | |

| 1,400 | | W.W. Grainger, Inc. | | | 239,834 | |

| | | | |

| |

| | | | | | 4,217,982 | |

| | | | |

| |

| | | Consumer, Non-Cyclical — 18.1% | | | | |

| 8,640 | | Abbott Laboratories | | | 465,437 | |

| 7,000 | | Automatic Data Processing, Inc. | | | 366,310 | |

| 8,475 | | Baxter International, Inc. | | | 465,956 | |

| 9,400 | | Forest Laboratories, Inc.* | | | 294,220 | |

| 6,700 | | Gilead Sciences, Inc.* | | | 279,122 | |

| 14,900 | | Hormel Foods Corp. | | | 439,103 | |

| 14,400 | | Merck & Company, Inc. | | | 496,800 | |

| 12,000 | | Paychex, Inc. | | | 349,680 | |

8

FBR Large Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | Consumer, Non-Cyclical — 18.1% (continued) | | | | |

| 6,800 | | PepsiCo, Inc. | | $ | 428,060 | |

| 8,500 | | ResMed, Inc.* | | | 240,550 | |

| 10,700 | | Stryker Corp. | | | 512,637 | |

| 26,500 | | Sysco Corp. | | | 734,580 | |

| 9,200 | | The Coca-Cola Co. | | | 628,544 | |

| 4,800 | | The Estee Lauder Companies, Inc., Class A | | | 472,560 | |

| 22,450 | | Unilever PLC ADR | | | 755,443 | |

| 5,800 | | United Therapeutics Corp.* | | | 253,634 | |

| | | | |

| |

| | | | | | 7,182,636 | |

| | | | |

| |

| | | Energy — 12.6% | | | | |

| 4,202 | | Apache Corp. | | | 418,645 | |

| 10,000 | | Ensco PLC ADR | | | 496,600 | |

| 11,000 | | Halliburton Co. | | | 410,960 | |

| 9,000 | | Hess Corp. | | | 563,040 | |

| 14,700 | | Marathon Oil Corp. | | | 382,641 | |

| 7,350 | | Marathon Petroleum Corp. | | | 263,865 | |

| 10,400 | | Murphy Oil Corp. | | | 575,848 | |

| 30,800 | | Nexen, Inc. | | | 522,984 | |

| 18,000 | | Petroleo Brasileiro S.A. ADR | | | 486,180 | |

| 8,000 | | Range Resources Corp. | | | 550,720 | |

| 9,000 | | Rowan Companies, Inc.* | | | 310,410 | |

| | | | |

| |

| | | | | | 4,981,893 | |

| | | | |

| |

| | | Financial — 13.4% | | | | |

| 2,900 | | BlackRock, Inc. | | | 457,591 | |

| 10,000 | | Capital One Financial Corp. | | | 456,600 | |

| 14,600 | | Citigroup, Inc. | | | 461,214 | |

| 18,000 | | Discover Financial Services | | | 424,080 | |

| 3,575 | | Franklin Resources, Inc. | | | 381,202 | |

| 16,725 | | JPMorgan Chase & Co. | | | 581,361 | |

| 13,000 | | Morgan Stanley | | | 229,320 | |

| 8,100 | | Prudential Financial, Inc. | | | 439,020 | |

| 10,575 | | T. Rowe Price Group, Inc. | | | 558,783 | |

| 27,000 | | U.S. Bancorp | | | 690,930 | |

| 24,000 | | Wells Fargo & Co. | | | 621,840 | |

| | | | |

| |

| | | | | | 5,301,941 | |

| | | | |

| |

9

FBR Large Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | Industrial — 10.1% | | | | |

| 15,615 | | 3M Co. | | $ | 1,233,897 | |

| 7,100 | | Cummins, Inc. | | | 705,953 | |

| 14,800 | | Norfolk Southern Corp. | | | 1,095,052 | |

| 13,700 | | PerkinElmer, Inc. | | | 283,179 | |

| 6,950 | | Union Pacific Corp. | | | 692,012 | |

| | | | |

| |

| | | | | | 4,010,093 | |

| | | | |

| |

| | | Technology — 18.2% | | | | |

| 4,000 | | Apple, Inc.* | | | 1,619,120 | |

| 11,000 | | Cerner Corp.* | | | 697,730 | |

| 7,000 | | Check Point Software Technologies Ltd.* | | | 403,410 | |

| 3,600 | | Citrix Systems, Inc.* | | | 262,188 | |

| 27,000 | | Intel Corp. | | | 662,580 | |

| 3,000 | | International Business Machines Corp. | | | 553,890 | |

| 10,000 | | MICROS Systems, Inc.* | | | 492,200 | |

| 18,350 | | Microsoft Corp. | | | 488,660 | |

| 14,000 | | NetApp, Inc.* | | | 573,440 | |

| 25,500 | | Oracle Corp. | | | 835,635 | |

| 1,800 | | salesforce.com, Inc.* | | | 239,706 | |

| 3,000 | | SAP AG ADR | | | 181,080 | |

| 8,100 | | Western Digital Corp.* | | | 215,784 | |

| | | | |

| |

| | | | | | 7,225,423 | |

| | | | |

| |

| | | Utilities — 1.9% | | | | |

| 9,000 | | Exelon Corp. | | | 399,510 | |

| 8,500 | | PG&E Corp. | | | 364,650 | |

| | | | |

| |

| | | | | | 764,160 | |

| | | | |

| |

| | | | | | | |

| | | Total Common Stocks (Cost $36,040,585) | | | 38,078,241 | |

| | | | |

| |

10

FBR Large Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | SHORT-TERM INVESTMENT — 4.2% | | | | |

| 1,681,837 | | Fidelity Institutional Money Market Government Portfolio, Class I, 0.01%^ (Cost $1,681,837) | | $ | 1,681,837 | |

| | | | |

| |

| | | | | | | |

| | | Total Investments — 100.1% (Cost $37,722,422) | | | 39,760,078 | |

| | | | | | | |

| | | Liabilities Less Other Assets — (0.1)% | | | (52,056 | ) |

| | | | |

| |

| | | | | | | |

| | | Net Assets — 100.0% | | $ | 39,708,022 | |

| | | | |

| |

|

| * | Non-income producing security |

| ADR | American Depositary Receipts |

| PLC | Public Liability Company |

| ^ | 7-day yield as of October 31, 2011 |

| Note: | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

11

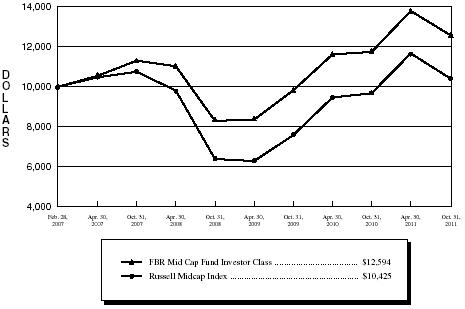

FBR Mid Cap Fund

Management Overview

Portfolio Manager: Ryan Kelley, CFA®

Over the previous 12 months, how did the Fund perform and what factors contributed to this performance?

For the twelve-month period ended October 31, 2011, the Investor Class of the FBR Mid Cap Fund returned 7.30%. This compares to the Russell Midcap Index and the Morningstar Mid Cap Blend Category Average which over the same time period returned 7.85% and 5.61%, respectively.

During our fiscal year, the Russell Midcap Index’s total return of 7.85% was a strong continuation of the positive momentum which began after the stock market bottom in March 2009. In the first half of the fiscal year, the index performed exceptionally well with a total return of 21%, but in the second half of the year the index fell close to 11% on a total return basis as every sector, excluding utilities, showed negative returns. Among the issues that caused this erosion of investor confidence were: the continued European crisis; the unprecedented downgrade of the U.S. credit rating by Standard & Poor’s; and the continued weakness in the U.S. economy including the struggling housing market and weak employment trends.

The Fund beat its Morningstar category average by 169 basis points for the year, despite slightly lagging its benchmark index. During the second half of the fiscal year as the markets dropped precipitously, the Fund outperformed the index by approximately 191 basis points and its Morningstar category by approximately 403 basis points. One of the goals of the Fund is to outperform during weak markets, as we believe that strong returns are achieved over the long term by losing less value when the market is in decline.

During the fiscal year, consumer, energy, and utilities stocks performed exceptionally well and contributed the majority of our positive returns. Conversely, the Fund continued to suffer from its exposure to financial services companies, which was one of two sectors that showed negative returns for the fiscal year in both the Fund and the Russell Midcap Index.

On a relative basis, consumer, industrial and technology investments performed best compared to the Fund’s benchmark. In all three of these sectors, our stock selection drove the relative outperformance, as we were invested in stocks that performed significantly better on average than the general index. Conversely, our relative performance was most negatively affected by our investments in energy and financials.

Portfolio Manager comments on the Fund and the related investment outlook.

Our goal is to provide better than average risk-adjusted returns over a complete market cycle. We strive to participate in the upside while protecting against the downside. We focus on high quality companies with strong balance sheets and consistent, high

12

FBR Mid Cap Fund

Management Overview (continued)

profitability, which means we may not be invested in some of the more volatile, cyclical stocks that outperform during economic recoveries. Certainly this year, we lagged during the first half as stocks soared yet outperformed in the second half as stocks dropped, and we ended the year significantly ahead of our Morningstar category.

The stock market continues to be negatively impacted by both global issues as well as domestic economic and political problems. These issues are persistent, and we believe it will take some time for conditions to improve, despite unprecedented efforts on a global scale among many countries’ governments and monetary policy makers to find solutions for many of our economic problems. During this time of continued economic difficulties, we currently have slightly higher than normal cash levels as we are looking for opportunities in this weak market. Additionally, we are slightly overweight technology, energy and consumer discretionary stocks while underweight financials and materials. Our goal is to remain invested in a diverse array of companies that exhibit strong balance sheets, strong profitability, and less cyclicality.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

13

FBR Mid Cap Fund

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. Russell Midcap Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2011(4) | |

| | | | | Annualized | |

| | | | | Since | |

| | | One Year | | Inception(5) | |

| | |

| |

| |

| FBR Mid Cap Fund Investor Class(1)(2) | | 7.30% | | 5.06% | |

| FBR Mid Cap Fund Institutional Class(2)(6) | | 7.43% | | 5.15% | |

| Russell Midcap Index(1)(3) | | 7.85% | | 0.90% | |

| |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. The Fund charges a redemption fee of 1.00% on shares redeemed or exchanged within 90 days; if reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710.

|

| (1) | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index, which represents approximately 31% of the total market capitalization of the Russell 1000 Index. |

| (4) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | For the period February 28, 2007 (commencement of operations) through October 31, 2011. |

| (6) | Represents the performance of the Institutional Class shares after May 30, 2008 (inception of the share class) and Investor Class for periods prior to that date. |

14

FBR Mid Cap Fund

Portfolio Summary

October 31, 2011

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | % of Total Investments |

|

|

| Consumer, Cyclical | | 19.3 | % |

| Consumer, Non-Cyclical | | 17.1 | % |

| Financial | | 14.5 | % |

| Industrial | | 10.8 | % |

| Technology | | 10.7 | % |

| Energy | | 8.2 | % |

| Utilities | | 4.5 | % |

| Communications | | 3.3 | % |

| Basic Materials | | 3.1 | % |

| | | | |

| Cash | | 8.5 | % |

15

FBR Mid Cap Fund

Portfolio of Investments

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | COMMON STOCKS — 91.5% | | | | |

| | | Basic Materials — 3.1% | | | | |

| 8,000 | | Gold Fields Ltd. ADR | | $ | 139,440 | |

| 3,984 | | Sigma-Aldrich Corp. | | | 260,872 | |

| 11,800 | | Yamana Gold, Inc. | | | 176,646 | |

| | | | |

| |

| | | | | | 576,958 | |

| | | | |

| |

| | | Communications — 3.3% | | | | |

| 3,797 | | FactSet Research Systems, Inc. | | | 377,498 | |

| 10,450 | | Telephone & Data Systems, Inc. | | | 242,231 | |

| | | | |

| |

| | | | | | 619,729 | |

| | | | |

| |

| | | Consumer, Cyclical — 19.3% | | | | |

| 4,515 | | Abercrombie & Fitch Co., Class A | | | 335,916 | |

| 3,900 | | Bed Bath & Beyond, Inc.* | | | 241,176 | |

| 9,080 | | Big Lots, Inc.* | | | 342,225 | |

| 9,485 | | Copart, Inc.* | | | 413,072 | |

| 1,600 | | Deckers Outdoor Corp.* | | | 184,384 | |

| 3,400 | | Genuine Parts Co. | | | 195,262 | |

| 2,700 | | Guess?, Inc. | | | 89,073 | |

| 8,130 | | Magna International, Inc. | | | 310,159 | |

| 12,824 | | Mattel, Inc. | | | 362,150 | |

| 2,800 | | MSC Industrial Direct Company, Inc., Class A | | | 190,428 | |

| 6,535 | | Tiffany & Co. | | | 521,036 | |

| 2,229 | | V.F. Corp. | | | 308,092 | |

| 3,700 | | Williams-Sonoma, Inc. | | | 138,898 | |

| | | | |

| |

| | | | | | 3,631,871 | |

| | | | |

| |

| | | Consumer, Non-Cyclical — 17.1% | | | | |

| 2,122 | | Bunge Ltd. | | | 131,076 | |

| 2,446 | | C.R. Bard, Inc. | | | 210,234 | |

| 2,600 | | Covance, Inc.* | | | 131,898 | |

| 9,050 | | Endo Pharmaceuticals Holdings, Inc.* | | | 292,406 | |

| 6,438 | | Forest Laboratories, Inc.* | | | 201,509 | |

| 5,750 | | Hansen Natural Corp.* | | | 512,267 | |

| 2,100 | | Humana, Inc. | | | 178,269 | |

| 6,995 | | Lincare Holdings, Inc. | | | 164,732 | |

| 9,575 | | Paychex, Inc. | | | 279,015 | |

16

FBR Mid Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | Consumer, Non-Cyclical — 17.1% (continued) | | | | |

| 16,850 | | SEI Investments Co. | | $ | 272,801 | |

| 3,385 | | Techne Corp. | | | 232,888 | |

| 1,650 | | Tupperware Brands Corp. | | | 93,291 | |

| 13,275 | | Tyson Foods, Inc., Class A | | | 256,208 | |

| 4,444 | | Varian Medical Systems, Inc.* | | | 260,952 | |

| | | | |

| |

| | | | | | 3,217,546 | |

| | | | |

| |

| | | Energy — 8.2% | | | | |

| 4,677 | | Energen Corp. | | | 229,454 | |

| 3,285 | | Ensco PLC ADR | | | 163,133 | |

| 1,200 | | First Solar, Inc.* | | | 59,724 | |

| 2,640 | | Helmerich & Payne, Inc. | | | 140,395 | |

| 7,800 | | Nabors Industries Ltd.* | | | 142,974 | |

| 2,925 | | Newfield Exploration Co.* | | | 117,760 | |

| 3,825 | | Pioneer Natural Resources Co. | | | 320,918 | |

| 5,800 | | Plains Exploration & Production Co.* | | | 182,700 | |

| 5,550 | | Rowan Companies, Inc.* | | | 191,420 | |

| | | | |

| |

| | | | | | 1,548,478 | |

| | | | |

| |

| | | Financial — 14.5% | | | | |

| 9,495 | | Capitol Federal Financial | | | 105,300 | |

| 6,375 | | Comerica, Inc. | | | 162,881 | |

| 17,900 | | Fifth Third Bancorp | | | 214,979 | |

| 25,225 | | Hudson City Bancorp, Inc. | | | 157,656 | |

| 26,950 | | KeyCorp | | | 190,267 | |

| 2,546 | | M&T Bank Corp. | | | 193,776 | |

| 8,185 | | New York Community Bancorp, Inc. | | | 108,942 | |

| 10,250 | | People’s United Financial, Inc. | | | 130,688 | |

| 8,700 | | Raymond James Financial, Inc. | | | 264,219 | |

| 33,600 | | Regions Financial Corp. | | | 132,048 | |

| 4,500 | | Reinsurance Group of America, Inc. | | | 235,035 | |

| 6,821 | | T. Rowe Price Group, Inc. | | | 360,422 | |

| 8,900 | | W. R. Berkley Corp. | | | 309,809 | |

| 9,600 | | Zions Bancorp | | | 166,656 | |

| | | | |

| |

| | | | | | 2,732,678 | |

| | | | |

| |

17

FBR Mid Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | Industrial — 10.8% | | | | |

| 6,625 | | Dolby Laboratories, Inc., Class A* | | $ | 193,715 | |

| 6,075 | | FLIR Systems, Inc. | | | 159,772 | |

| 6,200 | | Kansas City Southern | | | 391,654 | |

| 3,700 | | Kirby Corp.* | | | 227,698 | |

| 7,295 | | Pall Corp. | | | 373,285 | |

| 4,692 | | Roper Industries, Inc. | | | 380,521 | |

| 7,500 | | Spirit AeroSystems Holdings, Inc., Class A* | | | 128,025 | |

| 3,500 | | Tidewater, Inc. | | | 172,305 | |

| | | | |

| |

| | | | | | 2,026,975 | |

| | | | |

| |

| | | Technology — 10.7% | | | | |

| 32,168 | | Activision Blizzard, Inc. | | | 430,730 | |

| 8,403 | | Check Point Software Technologies Ltd.* | | | 484,265 | |

| 4,900 | | Microchip Technology, Inc. | | | 177,184 | |

| 3,400 | | SanDisk Corp.* | | | 172,278 | |

| 15,500 | | Seagate Technology PLC | | | 250,325 | |

| 30,900 | | Siliconware Precision Industries Co. Ltd. ADR | | | 160,680 | |

| 4,900 | | Western Digital Corp.* | | | 130,536 | |

| 6,200 | | Xilinx, Inc. | | | 207,452 | |

| | | | |

| |

| | | | | | 2,013,450 | |

| | | | |

| |

| | | Utilities — 4.5% | | | | |

| 8,800 | | Ameren Corp. | | | 280,544 | |

| 13,100 | | NRG Energy, Inc.* | | | 280,602 | |

| 10,650 | | Westar Energy, Inc. | | | 290,319 | |

| | | | |

| |

| | | | | | 851,465 | |

| | | | |

| |

| | | | | | | |

| | | Total Common Stocks (Cost $15,605,555) | | | 17,219,150 | |

| | | | |

| |

18

FBR Mid Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | SHORT-TERM INVESTMENT — 8.5% | | | | |

| 1,592,751 | | Fidelity Institutional Money Market Government Portfolio, Class I, 0.01%^ (Cost $1,592,751) | | $ | 1,592,751 | |

| | | | |

| |

| | | | | | | |

| | | Total Investments — 100.0% (Cost $17,198,306) | | | 18,811,901 | |

| | | | | | | |

| | | Other Assets Less Liabilities — 0.0% | | | 8,782 | |

| | | | |

| |

| | | | | | | |

| | | Net Assets — 100.0% | | $ | 18,820,683 | |

| | | | |

| |

|

| * | Non-income producing security |

| ADR | American Depositary Receipts |

| PLC | Public Liability Company |

| ^ | 7-day yield as of October 31, 2011 |

| Note: | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

19

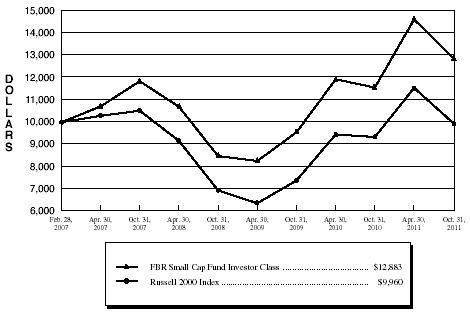

FBR Small Cap Fund

Management Overview

Portfolio Manager: Robert Barringer, CFA®

Over the previous 12 months, how did the Fund perform and what factors contributed to this performance?

For the twelve-month period ended October 31, 2011, the Investor Class of the FBR Small Cap Fund returned 11.40%. This compares to the Russell 2000 Index and the Morningstar Small Growth Category, which returned 6.71% and 8.84% for the same period, respectively.

The industry groups that helped the most were energy, healthcare and basic materials with the technology group being the main detractor from performance. A fair number of takeovers happened with respect to companies held by the Fund and this helped to boost performance as well. The performance was characterized once again by outperformance being generated by specific stock selections within the sectors and not from over or underweighting particular sectors. We believe this type of outperformance is indicative that our process can identify good investments within sectors and believe that it can provide for more consistent performance versus trying to outperform through large sector bets.

Portfolio Manager comments on the Fund and the related investment outlook.

The past year has been characterized by continued volatility in the markets amid uncertainty about the speed and durability of the recovery in the U.S. economy as well as the trouble that emerged in a number of the weaker European countries. In early December 2011, it is unclear as to a solution to the European financial problems and that solution’s related impact on the future economies in Europe, the United States and the other parts of the world. However, there are a number of attributes that our approach to investing possesses that should allow us to navigate this uncertain time with more confidence.

As we have previously stated, our investment approach tends to select those companies with low or below average debt, a company characteristic which allows much greater flexibility and stability in uncertain times. While the companies selected are small cap by nature, our approach emphasizes companies that have economic moats, with strong competitive positions and above average margins. As the past year has shown, these companies can succeed in more difficult times and are some of those most sought after for acquisition by larger companies and private equity.

We believe that the future will be a relatively volatile one as well, as Europe addresses its problems and deals with implementing a plan which will involve austerity and deleveraging. In addition, there are some lingering questions about Chinese economic growth as well. In this environment, we believe the U.S. will provide a relatively safe haven for investing as we are further along in addressing our problems. And while companies in small cap can be more volatile and perceived to be more risky, small cap has

20

FBR Small Cap Fund

Management Overview (continued)

the characteristic, unlike large cap, of being mainly concentrated in the relatively safer economy, the United States. As always, we will try to use any large volatility to our advantage in buying attractive companies for less and paring companies that have become extended in valuation.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

21

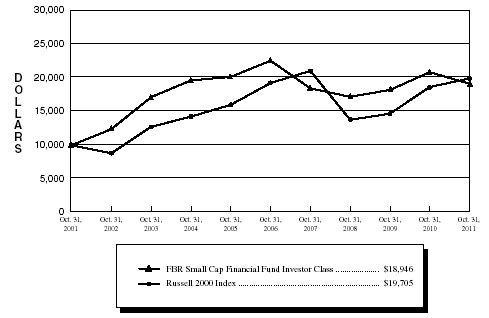

FBR Small Cap Fund

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. Russell 2000 Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2011(4) | |

| | | | | Annualized | |

| | | | | Since | |

| | | One Year | | Inception(5) | |

| | |

| |

| |

| FBR Small Cap Fund Investor Class(1)(2) | | 11.40% | | 5.57 | % | |

| FBR Small Cap Fund Institutional Class(2)(6) | | 11.82% | | 5.72 | % | |

| Russell 2000 Index(1)(3) | | 6.71% | | (0.09 | )% | |

| |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. The Fund charges a redemption fee of 1.00% on shares redeemed or exchanged within 90 days; if reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710.

|

| (1) | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | The Russell 2000 Index is comprised of the smallest of the 2000 companies of the Russell 3000 Index, representing approximately 8% of the Russell 3000’s total market capitalization. |

| (4) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | For the period February 28, 2007 (commencement of operations) through October 31, 2011. |

| (6) | Represents the performance of the Institutional Class shares after May 30, 2008 (inception of the share class) and Investor Class for periods prior to that date. |

22

FBR Small Cap Fund

Portfolio Summary

October 31, 2011

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | % of Total Investments |

|

|

| Financial | | 21.1 | % |

| Technology | | 17.8 | % |

| Consumer, Cyclical | | 16.8 | % |

| Industrial | | 13.9 | % |

| Consumer, Non-Cyclical | | 10.9 | % |

| Energy | | 8.4 | % |

| Basic Materials | | 5.2 | % |

| Communications | | 1.6 | % |

| Utilities | | 1.1 | % |

| Real Estate Investment Trust | | 0.6 | % |

| | | | |

| Cash | | 2.6 | % |

23

FBR Small Cap Fund

Portfolio of Investments

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | COMMON STOCKS — 97.4% | | | | |

| | | Basic Materials — 5.2% | | | | |

| 34,000 | | Hecla Mining Co.* | | $ | 213,180 | |

| 10,000 | | Innospec, Inc.* | | | 302,000 | |

| 8,000 | | Kraton Performance Polymers, Inc.* | | | 157,440 | |

| 1,500 | | NewMarket Corp. | | | 291,210 | |

| 20,000 | | PolyOne Corp. | | | 223,800 | |

| 5,000 | | Schnitzer Steel Industries, Inc., Class A | | | 234,000 | |

| 14,000 | | W.R. Grace & Co.* | | | 585,060 | |

| | | | |

| |

| | | | | | 2,006,690 | |

| | | | |

| |

| | | Communications — 1.6% | | | | |

| 2,000 | | Acme Packet, Inc.* | | | 72,420 | |

| 3,500 | | ADTRAN, Inc. | | | 117,600 | |

| 6,500 | | Aruba Networks, Inc.* | | | 153,985 | |

| 7,600 | | Sourcefire, Inc.* | | | 209,380 | |

| 3,600 | | Vocus, Inc.* | | | 73,368 | |

| | | | |

| |

| | | | | | 626,753 | |

| | | | |

| |

| | | Consumer, Cyclical — 16.8% | | | | |

| 44,000 | | American Axle & Manufacturing Holdings, Inc.* | | | 426,360 | |

| 13,000 | | Ascena Retail Group, Inc.* | | | 375,700 | |

| 9,500 | | Bally Technologies, Inc.* | | | 344,565 | |

| 19,000 | | Big Lots, Inc.* | | | 716,110 | |

| 13,000 | | Chico’s FAS, Inc. | | | 160,680 | |

| 7,000 | | Columbia Sportswear Co. | | | 376,180 | |

| 10,700 | | Crocs, Inc.* | | | 189,069 | |

| 70,000 | | JetBlue Airways Corp.* | | | 313,600 | |

| 15,000 | | Meritor, Inc.* | | | 142,800 | |

| 20,300 | | Modine Manufacturing Co.* | | | 214,571 | |

| 9,754 | | Owens & Minor, Inc. | | | 291,840 | |

| 20,200 | | Penn National Gaming, Inc.* | | | 727,200 | |

| 27,000 | | Pier 1 Imports, Inc.* | | | 337,770 | |

| 6,000 | | Steven Madden Ltd.* | | | 221,400 | |

| 5,600 | | The Buckle, Inc. | | | 249,536 | |

| 4,500 | | The Children’s Place Retail Stores, Inc.* | | | 211,275 | |

| 6,300 | | The Toro Co. | | | 340,452 | |

| 24,000 | | US Airways Group, Inc.* | | | 138,480 | |

24

FBR Small Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | Consumer, Cyclical — 16.8% (continued) | | | | |

| 8,000 | | Westport Innovations, Inc.* | | $ | 242,000 | |

| 14,500 | | Wolverine World Wide, Inc. | | | 549,985 | |

| | | | |

| |

| | | | | | 6,569,573 | |

| | | | |

| |

| | | Consumer, Non-Cyclical — 10.9% | | | | |

| 8,000 | | ImmunoGen, Inc.* | | | 108,640 | |

| 9,000 | | Impax Laboratories, Inc.* | | | 170,190 | |

| 10,000 | | InterMune, Inc.* | | | 255,000 | |

| 3,000 | | Jazz Pharmaceuticals, Inc.* | | | 116,880 | |

| 8,000 | | Optimer Pharmaceuticals, Inc.* | | | 114,160 | |

| 10,000 | | Par Pharmaceutical Companies, Inc.* | | | 306,000 | |

| 21,000 | | RSC Holdings, Inc.* | | | 204,960 | |

| 4,500 | | Seattle Genetics, Inc.* | | | 99,000 | |

| 47,000 | | SEI Investments Co. | | | 760,930 | |

| 15,150 | | Sirona Dental Systems, Inc.* | | | 725,685 | |

| 4,800 | | Sotheby’s | | | 169,056 | |

| 5,400 | | SuccessFactors, Inc.* | | | 144,180 | |

| 7,000 | | ViroPharma, Inc.* | | | 141,680 | |

| 20,110 | | Wright Express Corp.* | | | 942,757 | |

| | | | |

| |

| | | | | | 4,259,118 | |

| | | | |

| |

| | | Energy — 8.4% | | | | |

| 8,612 | | Atwood Oceanics, Inc.* | | | 368,077 | |

| 10,000 | | Brigham Exploration Co.* | | | 364,150 | |

| 16,500 | | Complete Production Services, Inc.* | | | 541,200 | |

| 12,000 | | Energy XXI (Bermuda) Ltd.* | | | 352,440 | |

| 22,200 | | Key Energy Services, Inc.* | | | 287,046 | |

| 92,000 | | Kodiak Oil & Gas Corp.* | | | 635,720 | |

| 15,000 | | Oasis Petroleum, Inc.* | | | 440,100 | |

| 6,000 | | Rosetta Resources, Inc.* | | | 266,040 | |

| | | | |

| |

| | | | | | 3,254,773 | |

| | | | |

| |

| | | Financial — 21.1% | | | | |

| 30,000 | | Associated Banc-Corp. | | | 334,500 | |

| 22,500 | | Astoria Financial Corp. | | | 186,750 | |

| 2,700 | | Bancorp Rhode Island, Inc. | | | 117,720 | |

| 10,000 | | Berkshire Hills Bancorp, Inc. | | | 200,200 | |

| 53,700 | | Brookline Bancorp, Inc. | | | 448,932 | |

25

FBR Small Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | Financial — 21.1% (continued) | | | | |

| 20,000 | | Brown & Brown, Inc. | | $ | 441,600 | |

| 29,454 | | Capitol Federal Financial | | | 326,645 | |

| 18,660 | | Chicopee Bancorp, Inc.* | | | 259,561 | |

| 28,500 | | CNO Financial Group, Inc.* | | | 178,125 | |

| 8,000 | | Encore Capital Group, Inc.* | | | 216,720 | |

| 28,253 | | First Horizon National Corp. | | | 197,488 | |

| 32,200 | | Fulton Financial Corp. | | | 303,968 | |

| 2,300 | | Hingham Institution for Savings | | | 110,308 | |

| 65,000 | | Horace Mann Educators Corp. | | | 874,250 | |

| 16,000 | | Independent Bank Corp. | | | 414,720 | |

| 3,407 | | Investors Title Co. | | | 123,231 | |

| 6,000 | | Newport Bancorp, Inc.* | | | 74,460 | |

| 9,000 | | Peoples Federal Bancshares, Inc.* | | | 117,900 | |

| 7,300 | | SI Financial Group, Inc. | | | 64,605 | |

| 40,800 | | Susquehanna Bancshares, Inc. | | | 296,208 | |

| 14,000 | | Tower Group, Inc. | | | 332,220 | |

| 34,550 | | United Financial Bancorp, Inc. | | | 557,637 | |

| 27,000 | | Waddell & Reed Financial, Inc. | | | 748,710 | |

| 11,400 | | Washington Federal, Inc. | | | 155,610 | |

| 2,700 | | White Mountainns Insurance Group Ltd. | | | 1,134,000 | |

| | | | |

| |

| | | | | | 8,216,068 | |

| | | | |

| |

| | | Industrial — 13.9% | | | | |

| 20,337 | | A.O. Smith Corp. | | | 755,723 | |

| 7,100 | | Armstrong World Industries, Inc. | | | 302,389 | |

| 8,000 | | Atlas Air Worldwide Holdings, Inc.* | | | 308,160 | |

| 3,000 | | Cymer, Inc.* | | | 130,350 | |

| 12,800 | | Genesee & Wyoming, Inc., Class A* | | | 757,888 | |

| 15,000 | | GrafTech International Ltd.* | | | 235,650 | |

| 12,100 | | Heartland Express, Inc. | | | 162,261 | |

| 9,000 | | Lennox International, Inc. | | | 289,710 | |

| 8,200 | | PerkinElmer, Inc. | | | 169,494 | |

| 8,000 | | Roadrunner Transportation Systems, Inc.* | | | 133,520 | |

| 25,860 | | Sauer-Danfoss, Inc.* | | | 1,001,299 | |

| 10,000 | | Simpson Manufacturing Company, Inc. | | | 306,600 | |

| 6,915 | | Sun Hydraulics Corp. | | | 198,875 | |

26

FBR Small Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | VALUE |

| SHARES | | | | (NOTE 2) |

|

| | | Industrial — 13.9% (continued) | | | | |

| 7,000 | | Twin Disc, Inc. | | $ | 272,300 | |

| 17,250 | | Werner Enterprises, Inc. | | | 408,825 | |

| | | | |

| |

| | | | | | 5,433,044 | |

| | | | |

| |

| | | Real Estate Investment Trust — 0.6% | | | | |

| 34,800 | | Sunstone Hotel Investors, Inc.* | | | 241,860 | |

| | | | |

| |

| | | | | | | |

| | | Technology — 17.8% | | | | |

| 16,000 | | Allscripts Healthcare Solutions, Inc.* | | | 306,400 | |

| 45,100 | | Brocade Communications Systems, Inc.* | | | 197,538 | |

| 11,000 | | Cirrus Logic, Inc.* | | | 183,040 | |

| 8,000 | | CommVault Systems, Inc.* | | | 340,640 | |

| 22,000 | | Compuware Corp.* | | | 185,900 | |

| 3,000 | | Concur Technologies, Inc.* | | | 139,560 | |

| 20,000 | | Emulex Corp.* | | | 167,600 | |

| 24,777 | | Jack Henry & Associates, Inc. | | | 803,023 | |

| 18,000 | | MedAssets, Inc.* | | | 191,880 | |

| 35,000 | | Medidata Solutions, Inc.* | | | 629,300 | |

| 10,500 | | Mellanox Technologies Ltd.* | | | 339,780 | |

| 5,000 | | MicroStrategy, Inc., Class A* | | | 658,850 | |

| 8,000 | | NetSuite, Inc.* | | | 304,320 | |

| 8,175 | | Open Text Corp.* | | | 498,838 | |

| 10,000 | | QLogic Corp.* | | | 139,700 | |

| 5,000 | | Quest Software, Inc.* | | | 87,950 | |

| 23,400 | | Radware Ltd.* | | | 618,696 | |

| 8,400 | | RightNow Technologies, Inc.* | | | 361,284 | |

| 8,000 | | Synchronoss Technologies, Inc.* | | | 240,480 | |

| 6,400 | | Taleo Corp., Class A* | | | 207,360 | |

| 1,800 | | The Ultimate Software Group, Inc.* | | | 108,324 | |

| 27,000 | | TriQuint Semiconductor, Inc.* | | | 143,640 | |

| 3,000 | | Veeco Instruments, Inc.* | | | 80,070 | |

| | | | |

| |

| | | | | | 6,934,173 | |

| | | | |

| |

| | | Utilities — 1.1% | | | | |

| 17,400 | | Portland General Electric Co. | | | 426,996 | |

| | | | |

| |

| | | | | | | |

| | | Total Common Stocks (Cost $38,797,992) | | | 37,969,048 | |

| | | | |

| |

27

FBR Small Cap Fund

Portfolio of Investments (continued)

October 31, 2011

|

| NO. OF | | | | | VALUE | |

| RIGHTS | | | | | (NOTE 2) | |

|

| | | RIGHTS — 0.0% | | | | |

| 5,500 | | Forest Laboraties, Inc., Contingent Value Rights* | | $ | 5,225 | |

| | | | |

| |

|

| SHARES | | | | | | |

|

| | | SHORT-TERM INVESTMENT — 2.6% | | | | |

| 1,030,168 | | Fidelity Institutional Money Market Government Portfolio, Class I, 0.01%^ (Cost $1,030,168) | | | 1,030,168 | |

| | | | |

| |

| | | | | | | |

| | | Total Investments — 100.0% (Cost $39,828,160) | | | 39,004,441 | |

| | | | | | | |

| | | Other Assets Less Liabilities — 0.0% | | | (125 | ) |

| | | | |

| |

| | | | | | | |

| | | Net Assets — 100.0% | | $ | 39,004,316 | |

| | | | |

| |

|

| * | Non-income producing security |

| ^ | 7-day yield as of October 31, 2011 |

| Note: | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

28

FBR Focus Fund

Management Overview

Portfolio Managers: David Rainey, CFA®, Brian Macauley, CFA® and Ira Rothberg, CFA®

Over the previous 12 months, how did the Fund perform and what factors contributed to this performance?

For the twelve-month period ended October 31, 2011, the Investor Class of the FBR Focus Fund returned 8.35% compared to 6.71% for the Russell 2000 Index, 8.09% for the S&P 500 Index, and 7.65% for the Morningstar Mid Cap Growth Category.

On average, the Fund’s portfolio companies produced growing earnings and improving earnings power over the period, with stable valuations. While economic conditions remain difficult and the recovery gradual, there was sufficient stability to allow the portfolio companies to invest in their businesses and increase their intrinsic value.

There were two major contributors to performance during the year- O’Reilly Automotive and 99 Cents Only Stores:

| | • | | O’Reilly Automotive completed a three year integration of its CSK Auto acquisition while continuing to extract value by growing commercial parts programs at those acquired stores. The company also struck new financing arrangements enabling it to improve its working capital efficiency and implement an aggressive share repurchase program. |

| | • | | 99 Cents Only Stores received a buyout offer organized by its founding family. We considered the $19.09 per share offer that was made on March 13, 2011 to be inadequate so we lobbied actively for a robust auction process and higher price (our letters to the board and special committee are a matter of public record available at www.sec.gov). Our demands were met, and on October 11, 2011 the company announced the acceptance of a more equitable buyout deal at $22.00 per share. |

The only major detractor from performance was Lamar Advertising. Demand for billboard advertising from Lamar’s core mid-market customers has lagged the broader advertising recovery seen over the last year. Lamar stock significantly underperformed during the year as this divergence in performance became apparent.

Capital gains tax distributions of $5.24 per share this year were somewhat high in relation to the Fund’s Investor Class ending share NAV on October 31, 2011 of $49.80. In general, the Fund’s investment approach has been, and should continue to be relatively tax efficient since capital gains tend to be realized at lower long-term tax rates rather than higher short-term rates (note that 100% of this year’s capital gain was characterized as long-term). However, the Fund’s investment approach can also lead to lumpiness in the timing of capital gains distributions – such as was the case this year – as gains are realized irregularly and often in large size when we exit a long term position.

We invest with a long-term time horizon and encourage Fund shareholders to do the same. Despite the discussion of one-year results referenced above, we encourage our shareholders to evaluate the Fund’s performance over three-, five-, and ten-year periods

29

FBR Focus Fund

Management Overview (continued)

since shorter time frames can be influenced by many transitory issues unrelated to the intrinsic worth of the Fund’s holdings. Long-term performance metrics for the Fund can be found in the table below.

Portfolio Manager comments on the Fund and the related investment outlook.

Over the past year, and particularly in the past six months, the financial headlines have been dominated by stories about macroeconomic risks and uncertainty. The European sovereign debt crisis, slowing GDP growth, lingering housing market distress, political rancor, and the U.S. credit downgrade have made for a very unsettled stock market.

While today’s problems do seem troubling, the reality is that the world is always an uncertain place. There are routinely macroeconomic or geopolitical concerns that flare up causing significant investor angst. Consider today’s concerns compared to those following the collapse of Lehman Brothers in 2008, after the attacks on September 11, 2001, during the emerging markets crisis in 1997/98, the “Japanese invasion”in the 1980s, a 20% prime rate in 1980, stagflation in the 1970s, or the 1973 oil embargo.

As investors, we are faced with the challenge of how to react to these various macroeconomic concerns. Most often these concerns prove inconsequential with the passage of time, but occasionally they manifest in damage to the real economy and corporate profits. Our general viewpoint is that it is extraordinarily difficult to make money by placing bets on macroeconomic events. Just observe the terrible track record of the full-time Wall Street economists in forecasting important turning points in the economy. The world is too complicated with too many moving parts to have this be a consistently profitable exercise. Experience has taught us that we are most effective when building the portfolio one security at a time.

As long-term investors, we fully expect that our portfolio will face turbulent economic times at various points during our investment horizon. So we prepare for this eventuality, not by selling all our stocks at the first signs of trouble, nor by rotating our portfolio into more conservative sectors, but rather by owning durable companies with a wide “margin of safety”. By this we mean companies with the business model and balance sheet to survive and thrive in many economic environments, owned at attractive prices so that our long-term investment is well protected against unfavorable company specific and macroeconomic developments.

Today, we think the Fund’s portfolio is composed of durable companies with a good margin of safety. In fact, we think that many of the Fund’s largest holdings are well positioned to grow cash earnings per share at a double digit clip over the next several years regardless of the rate of economic recovery. These companies have their own profit drivers that are largely independent of the overall economy, i.e. American Tower (9.3% of assets*) is driven by the adoption of data intensive smart phones, O’Reilly (11.0% of assets*) is driven by its ability to further improve acquired CSK stores, and Markel (8.0% of assets*)

* As of October 31, 2011.

30

FBR Focus Fund

Management Overview (continued)

is driven by the insurance pricing cycle and success of insurance and non insurance acquisitions.

We attempt to use stock market swoons to our advantage by purchasing shares in companies that we admire at discount prices. Over the last twelve months, we added six new holdings to the portfolio and increased the size of several other positions. Most of these changes took place during the market turmoil over the summer and fall. This is a lot of activity for us considering that the Fund has 22 total positions and a history of low turnover. However, this is also consistent with our historical pattern of long periods of portfolio inactivity when we believe that bargains are few, interspersed by a flurry of portfolio activity during periods when we believe that bargains are plentiful. While we often find ourselves in extended periods of portfolio inactivity, it is during these periods that we build and refine our list of investment prospects so that we are prepared for market opportunity when it arrives.

Whenever we add a new position to the portfolio, we carefully weigh its merit against the positions that we already have in the portfolio. We only add a new position if we believe that it is as good as, or better than what we already own. This comparison methodology helps us maintain a high standard for new purchases, and avoid complacency with existing positions. We are encouraged by these recent portfolio additions since they took the place of less favorable investment allocations in the Fund. Further, several of these new investments are in industries that did not have representation in the portfolio (i.e. health care, energy, and transportation) adding an increased level of overall diversification. Through this process of gradually, and sometimes not so gradually, layering new investment ideas into the portfolio, we achieve a process of continuous portfolio improvement. While in the short term the Fund may rise and fall with the overall market, over a period of years we think that the Fund’s carefully selected portfolio of companies should produce quite satisfactory overall investment results.

We thank you for entrusting your capital to us. We take this responsibility very seriously, and we will do our best to protect and grow your investment.

The opinions expressed in this commentary reflect those of the Portfolio Managers as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

31

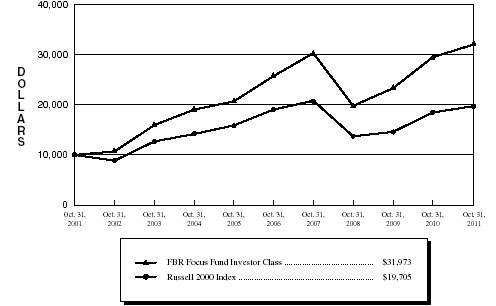

FBR Focus Fund

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. Russell 2000 Index(1)(3)

| Total Returns—For the Periods Ended October 31, 2011(4) | |

| | | | | Annualized | | Annualized | |

| | | One Year | | Five Year | | Ten Year |

| | |

| |

| |

|

FBR Focus Fund Investor Class(1)(2) | | 8.35% | | 4.42% | | 12.33% |

FBR Focus Fund Institutional Class(2)(5) | | 8.53% | | 4.67% | | 12.46% |

Russell 2000 Index(1)(3) | | 6.71% | | 0.68% | | 7.02% |

| |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. The Fund charges a redemption fee of 1.00% on shares redeemed or exchanged within 90 days; if reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710.

|

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |

| (2) | | FBR Fund Advisers, Inc. waived a portion of its advisory fees and agreed to contractually reimburse a portion of the Fund’s operating expenses, as necessary, to maintain existing expense limitations, as set forth in the notes to the financial statements. Total returns shown include fee waivers and expense reimbursements, if any; total returns would have been lower had there been no waiver of fees and/or reimbursement of expenses in excess of expense limitations. |

| (3) | | The Russell 2000 Index is comprised of the smallest of the 2000 companies of the Russell 3000 Index, representing approximately 8% of the Russell 3000’s total market capitalization. |

| (4) | | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. |

| (5) | | Represents the performance of the Institutional Class shares after May 30, 2008 (inception of share class) and Investor Class for periods prior to that date. |

32

FBR Focus Fund

Portfolio Summary

October 31, 2011

The following provides a breakdown of the Fund by industry sectors. The underlying securities represent a percentage of the portfolio investments.

| Industry Sector | | % of Total Investments |

| |

|

| Retail | | 32.1 | % |

| Entertainment | | 14.0 | % |

| Insurance | | 13.7 | % |

| Telecommunications | | 9.3 | % |

| Diversified Financial Services | | 7.1 | % |

| Internet | | 4.3 | % |

| Building Materials | | 3.8 | % |

| Media | | 3.4 | % |

| Advertising | | 2.1 | % |

| Home Furnishings | | 1.8 | % |

| Transportation | | 1.3 | % |

| Healthcare Products | | 1.0 | % |

| | | | |

| Cash | | 6.1 | % |

33

FBR Focus Fund

Portfolio of Investments

October 31, 2011

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | COMMON STOCKS — 93.9% | | | | |

| | | | Advertising — 2.1% | | | | |

| | 630,000 | | Lamar Advertising Co., Class A* | | $ | 14,168,700 | |

| | | | | |

| |

| | | | Building Materials — 3.8% | | | | |

| | 825,000 | | Simpson Manufacturing Company, Inc. | | | 25,294,500 | |

| | | | | |

| |

| | | | Diversified Financial Services — 7.1% | | | | |

| | 94,910 | | Diamond Hill Investment Group, Inc. | | | 7,144,825 | |

| | 503,756 | | Encore Capital Group, Inc.* | | | 13,646,750 | |

| | 401,508 | | Marlin Business Services Corp.* | | | 4,733,779 | |

| | 125,000 | | T. Rowe Price Group, Inc. | | | 6,605,000 | |

| | 912,000 | | The Charles Schwab Corp. | | | 11,199,360 | |

| | 173,137 | | White River Capital, Inc. | | | 3,331,156 | |

| | | | | |

| |

| | | | | | | 46,660,870 | |

| | | | | |

| |

| | | | Entertainment — 14.0% | | | | |

| | 1,169,000 | | Bally Technologies, Inc.* | | | 42,399,630 | |

| | 1,393,670 | | Penn National Gaming, Inc.* | | | 50,172,120 | |

| | | | | |

| |

| | | | | | | 92,571,750 | |

| | | | | |

| |

| | | | Healthcare Products — 1.0% | | | | |

| | 98,733 | | Henry Schein, Inc.* | | | 6,844,172 | |

| | | | | |

| |

| | | | Home Furnishings — 1.8% | | | | |

| | 680,160 | | American Woodmark Corp. | | | 11,569,522 | |

| | | | | |

| |

| | | | Insurance — 13.7% | | | | |

| | 805,750 | | Aon Corp. | | | 37,564,065 | |

| | 136,640 | | Markel Corp.* | | | 52,811,360 | |

| | | | | |

| |

| | | | | | | 90,375,425 | |

| | | | | |

| |

| | | | Internet — 4.3% | | | | |

| | 47,800 | | Google, Inc., Class A* | | | 28,328,192 | |

| | | | | |

| |

| | | | Media — 3.4% | | | | |

| | 1,303,000 | | News Corp., Class A | | | 22,828,560 | |

| | | | | |

| |

34

FBR Focus Fund

Portfolio of Investments (continued)

October 31, 2011

|

| | | | | | VALUE |

| | SHARES | | | | (NOTE 2) |

|

| | | | Retail — 32.1% | | | | |

| | 3,527,235 | | 99¢ Only Stores*† | | $ | 76,893,723 | |

| | 1,840,088 | | CarMax, Inc.* | | | 55,313,045 | |

| | 954,843 | | O’Reilly Automotive, Inc.* | | | 72,615,810 | |

| | 185,000 | | World Fuel Services Corp. | | | 7,372,250 | |

| | | | | |

| |

| | | | | | | 212,194,828 | |

| | | | | |

| |

| | | | Telecommunications — 9.3% | | | | |

| | 1,110,595 | | American Tower Corp., Class A* | | | 61,193,784 | |

| | | | | |

| |

| | | | Transportation — 1.3% | | | | |

| | 504,200 | | Roadrunner Transportation Systems, Inc.* | | | 8,415,098 | |

| | | | | |

| |

| | | | | | | | |

| | | | Total Common Stocks (Cost $327,154,110) | | | 620,445,401 | |

| | | | | |

| |

| | | | | | | | |

| | | | SHORT-TERM INVESTMENT — 6.1% | | | | |

| | 40,057,250 | | Fidelity Institutional Money Market Government Portfolio, Class I, 0.01%^ (Cost $40,057,250) | | | 40,057,250 | |

| | | | | |

| |

| | | | | | | | |

| | | | Total Investments — 100.0% (Cost $367,211,360) | | | 660,502,651 | |

| | | | | | | | |

| | | | Liabilities Less Other Assets — 0.0% | | | (160,006 | ) |

| | | | | |

| |

| | | | | | | | |

| | | | Net Assets — 100.0% | | $ | 660,342,645 | |

| | | | | |

| |

|

| * | | Non-income producing security |

| † | | Affiliated issuer as defined in the Investment Company Acto fo 1940 (ownership of at least 5% of the outstanding voting securities of the issuer) |

| ^ | | 7-day yield as of October 31, 2011 |

| | | |

| Note: | | For presentation purposes, the Fund has grouped some of the industry categories. For purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, the Fund uses more specific industry classifications. |

The accompanying notes are an integral part of the financial statements.

35

FBR Large Cap Financial Fund

Management Overview

Portfolio Manager: David Ellison

Over the previous 12 months, how did the Fund perform and what factors contributed to this performance?

For the twelve-month period ended October 31, 2011, the Investor Class of the FBR Large Cap Financial Fund returned -7.53%. This compares to the KBW Bank Index, the S&P 500 Index and the Morningstar Financial Category Average, which returned -10.39%, 8.09% and -6.80% for the same period, respectively.

The Fund performed in line with the Morningstar Financial Category during the period. Positions in the largest banks hurt performance during the period. Investments in credit card and insurance companies helped performance during the period. Large banks continue to fight the headwinds of weak labor and housing markets. Also, recent concerns with European debt and the impacts on world growth have provided additional headwinds for the big diversified banks. Credit card and insurance companies have seen improved delinquency rates and modest growth and are doing better in the current environment.

The Fund continues to be concentrated in the largest domestic commercial banks. We believe they offer the best upside when the U.S. economy improves. Also, these financials are not exposed to the debt troubles in Europe and related economic slowdown that appears to be developing.

Portfolio Manager comments on the Fund and the related investment outlook.

The industry continues to battle many earnings headwinds. Employment and housing remain weak. Investment banking activity is slow. Stock and bond trading volumes are light. Nonperforming assets have declined but recent declines have slowed. Loan demand is weak and some have seen their loan books decline. Low interest rates are helping borrowers somewhat, but are hurting lending spreads. European debt troubles and related economic weakness in Europe is hurting growth prospects in that region. Finally, public opinion of banks is right up there with Congress, i.e. not helping investor sentiment.

These negative operating conditions have been with the industry for over three years now. Investors in this space are weary and tired. As a result, there is little investor interest. Reduced investor interest is being reflected in low historical valuations as measured by earnings per share multiples and price to book ratios.

The good news, yes we have some, is that while macro conditions are difficult, the industry is working very hard to improve on a micro level. We are seeing improved capital ratios, loan loss reserves, liquidity levels, realistic loan write-downs, cost containment and reduction programs, regulatory compliance, internal loan review, credit risk controls and generally a much improved attention to detail. They are, in sum, getting back to the basic principles of sound banking abandoned some years ago.

36

FBR Large Cap Financial Fund

Management Overview (continued)

We believe the industry is “on the mend” and will gradually show improved earnings that will be more stable and predictable than what we have experienced the last five years. This improved earnings quality should lead to higher valuations as measured by earnings multiples and price to book ratios.

Investing in financial service stocks remains a challenge. We are doing our best to avoid the downside and having to rethink our positions, at times, almost daily. Finally, we remain mindful that investing is never ALWAYS about making the most, but is ALWAYS about preserving the MOST over the long run.

The opinions expressed in this commentary reflect those of the Portfolio Manager as of the date written. Any such opinions are subject to change based on market or other conditions. These opinions may not be relied upon as investment advice. Investment decisions for The FBR Funds are based on several factors, and may not be relied upon as an indication of trading intent on behalf of any FBR Fund. Security positions can and do change.

37

FBR Large Cap Financial Fund

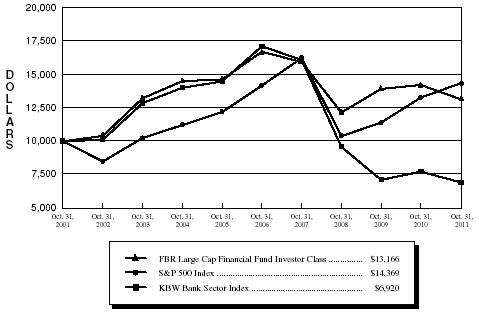

Comparison of Changes in Value of $10,000 Investment in

Investor Class Shares(1)(2) vs. Various Indices(1)(3)

| Total Returns—For the Periods Ended October 31, 2011(4) | |

| | | | | | | Annualized | | Annualized | |

| | | | One Year | | Five Year | | Ten Year | |

| | | |

| |

| |

| |

FBR Large Cap Financial Fund Investor Class(1)(2) | | | (7.53)% | | (4.68)% | | 2.79% | |

S&P 500 Index(1)(3) | | | 8.09% | | 0.25% | | 3.69% | |

KBW Bank Sector Index(1)(3) | | | (10.39)% | | (16.60)% | | (3.61)% | |

| |

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS.

The performance data quoted represents past performance and the current performance may be lower or higher than the performance data quoted. The investment return and principal will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The performance data does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption fees. The Fund charges a redemption fee of 1.00% on shares redeemed or exchanged within 90 days; if reflected, the redemption fee would reduce the performance data quoted. To obtain performance data current to the most recent month-end, please call 888.200.4710.

| (1) | | The graph assumes a hypothetical $10,000 initial investment in the Fund and reflects the reinvestment of dividends and all Fund expenses. Investors should note that the Fund is a professionally managed mutual fund while the index is unmanaged, does not incur expenses and is not available for investment. The performance of the index includes reinvested dividends, and does not reflect sales charges or expenses. |