UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21629

SPECIAL VALUE EXPANSION FUND, LLC

(Exact Name of Registrant as Specified in Charter)

2951 28TH STREET, SUITE 1000

SANTA MONICA, CALIFORNIA 90405

(Address of Principal Executive Offices) (Zip Code)

ELIZABETH GREENWOOD, SECRETARY

SPECIAL VALUE EXPANSION FUND, LLC

2951 28TH STREET, SUITE 1000

SANTA MONICA, CALIFORNIA 90405

(Name and Address of Agent for Service)

Registrant's telephone number, including area code: (310) 566-1000

Copies to:

RICHARD T. PRINS, ESQ.

SKADDEN, ARPS, SLATE, MEAGHER & FLOM LLP

FOUR TIMES SQUARE

NEW YORK, NEW YORK 10036

Date of fiscal year end: SEPTEMBER 30, 2008

Date of reporting period: SEPTEMBER 30, 2008

ITEM 1. REPORTS TO STOCKHOLDERS.

Annual Shareholder Report

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

September 30, 2008

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Annual Shareholder Report

September 30, 2008

Contents

| Performance Summary | | 2 |

| Portfolio Asset Allocation | | 3 |

| | | |

| Financial Statements | | |

| | | |

| Report of Independent Registered Public Accounting Firm | | 4 |

| Statement of Assets and Liabilities | | 5 |

| Statement of Investments | | 6 |

| Statement of Operations | | 12 |

| Statements of Changes in Net Assets | | 13 |

| Statement of Cash Flows | | 14 |

| Notes to Financial Statements | | 15 |

| Schedule of Changes in Investments in Affiliates | | 30 |

| | | |

| Supplemental Information (Unaudited) | | |

| | | |

| Directors and Officers | | 31 |

| Approval of Investment Management Agreement | | 36 |

Special Value Expansion Fund, LLC (the “Company”) files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Company’s Forms N-Q are available on the SEC’s website at http://www.sec.gov. The Company’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A free copy of the Company’s proxy voting guidelines and information regarding how the Company voted proxies relating to portfolio securities during the most recent 12-month period may be obtained without charge on the SEC’s website at http://www.sec.gov or by calling the Company’s advisor, Tennenbaum Capital Partners, LLC, at (310) 566-1000. Collect calls for this purpose are accepted.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

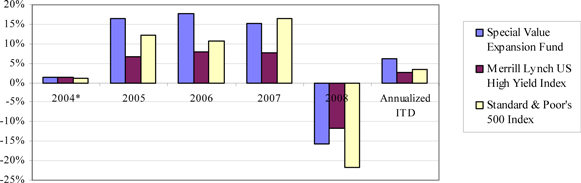

Performance Summary

Inception (September 1, 2004) through September 30, 2008

Fund Returns v. Merrill Lynch US High Yield and S&P 500 Indices

| | | Return on Equity (1) | | IRR (2) | |

| | | 2004* | | 2005 | | 2006 | | 2007 | | 2008 | | Inception-to-Date | |

| Special Value Expansion Fund | | | 1.5 | % | | 16.4 | % | | 17.7 | % | | 15.1 | % | | -15.7 | % | | 6.2 | % |

| Merrill Lynch US High Yield Index | | | 1.4 | % | | 6.7 | % | | 7.9 | % | | 7.7 | % | | -11.6 | % | | 2.6 | % |

| Standard & Poor's 500 Index | | | 1.1 | % | | 12.3 | % | | 10.8 | % | | 16.4 | % | | -21.8 | % | | 3.3 | % |

* Period from inception (September 1, 2004) through September 30, 2004

Past performance of Special Value Expansion Fund, LLC (the "Company") is not a guarantee of future performance. Company returns are net of dividends to preferred shareholders and Company expenses, including financing costs and management and performance fees.

(1) Return on equity (net of dividends to preferred shareholders and Company expenses, including financing costs and management and performance fees) calculated on a monthly geometrically linked, time-weighted basis. Returns are reduced in earlier periods because organizational costs and other expenses are high relative to assets.

(2) Internal rate of return ("IRR") is the imputed annual return over an investment period and, mathematically, is the rate of return at which the discounted cash flows equal the initial outlays. The IRR presented assumes a liquidation of the Company at net asset value as of the period end date.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

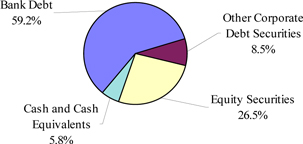

Portfolio Asset Allocation

September 30, 2008

Portfolio Holdings by Investment Type (% of Cash and Investments)

Portfolio Holdings by Industry (% of Cash and Investments)

| Communications Equipment Manufacturing | | | 15.8 | % |

| Telecom Wireline | | | 13.9 | % |

| Data Processing, Hosting, and Related Services | | | 8.5 | % |

| Plastics Product Manufacturing | | | 7.8 | % |

| Motor Vehicle Parts Manufacturing | | | 7.0 | % |

| Activities Related to Credit Intermediation | | | 6.5 | % |

| Satellite Telecommunications | | | 5.8 | % |

| Cable Service Carriers | | | 4.8 | % |

| Alumina and Aluminum Production and Processing | | | 4.3 | % |

| Semiconductor and Other Electronic Component Manufacturing | | | 4.1 | % |

| Scheduled Air Transportation | | | 3.9 | % |

| Offices of Real Estate Agents and Brokers | | | 2.4 | % |

| Clothing Stores | | | 1.5 | % |

| Industrial Machinery Manufacturing | | | 1.2 | % |

| Gambling Industries | | | 1.2 | % |

| Other Amusement and Recreation Industries | | | 1.2 | % |

| Computer and Peripheral Equipment Manufacturing | | | 1.2 | % |

| Depository Credit Intermediation | | | 1.0 | % |

| Electric Power Generation, Transmission and Distribution | | | 0.8 | % |

| Management, Scientific, and Technical Consulting Services | | | 0.7 | % |

| Sporting Goods, Hobby, and Musical Instrument Stores | | | 0.2 | % |

| Home Furnishings Stores | | | 0.2 | % |

| Radio and Television Broadcasting | | | 0.1 | % |

| Basic Chemical Manufacturing | | | 0.1 | % |

| Cash and Cash Equivalents | | | 5.8 | % |

| | | | | |

| Total | | | 100.0 | % |

Report of Independent Registered Public Accounting Firm

The Shareholders and Board of Directors of

Special Value Expansion Fund, LLC

We have audited the accompanying statement of assets and liabilities of Special Value Expansion Fund, LLC (a Delaware Limited Liability Company) (the “Company”), including the statement of investments, as of September 30, 2008, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein. These financial statements and financial highlights are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Company’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included verification by examination of securities held by the custodian as of September 30, 2008, and confirmation of securities not held by the custodian by correspondence with others or by other appropriate auditing procedures where replies from others were not received. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Special Value Expansion Fund, LLC at September 30, 2008, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the periods indicated therein, in conformity with U.S. generally accepted accounting principles.

/s/ Ernst & Young LLP

Los Angeles, California

November 24, 2008

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Assets and Liabilities

September 30, 2008

| Assets | | | | |

| Investments, at fair value: | | | | |

| Unaffiliated issuers (cost $336,803,168) | | $ | 285,269,290 | |

| Affiliates (cost $125,660,206) | | | 128,549,322 | |

| Total investments (cost $462,463,374) | | | 413,818,612 | |

| | | | | |

| Cash and cash equivalents | | | 25,209,904 | |

| Accrued interest income: | | | | |

| Unaffiliated issuers | | | 5,533,088 | |

| Affiliates | | | 67,547 | |

| Receivable for investment securities sold | | | 5,142,945 | |

| Deferred debt issuance costs | | | 1,225,702 | |

| Other receivables | | | 673,868 | |

| Prepaid expenses and other assets | | | 47,794 | |

| Total assets | | | 451,719,460 | |

| | | | | |

| Liabilities | | | | |

| Credit facility payable | | | 113,000,000 | |

| Unrealized depreciation on swaps and forward contracts | | | 3,604,167 | |

| Payable for investment securities purchased | | | 506,687 | |

| Management and advisory fees payable | | | 300,000 | |

| Payable to affiliate | | | 49,428 | |

| Interest payable | | | 37,729 | |

| Accrued expenses and other liabilities | | | 983,865 | |

| Total liabilities | | | 118,481,876 | |

| | | | | |

| Preferred stock | | | | |

| Auction-rate preferred shares (Series A and B); $50,000/share liquidation preference; unlimited shares authorized, 2,000 shares issued and outstanding | | | 100,000,000 | |

| Accumulated dividends on auction-rate preferred shares | | | 260,553 | |

| Series S, $1,000/share liquidation preference; 1 share authorized, no shares issued and outstanding | | | - | |

| Series Z, $500/share liquidation preference; 500 shares authorized, 312 shares issued and outstanding | | | 156,000 | |

| Accumulated dividends on Series Z preferred shares | | | 12,514 | |

| Total preferred stock | | | 100,429,067 | |

| | | | | |

| Net assets applicable to common shareholders | | $ | 232,808,517 | |

| | | | | |

| Composition of net assets applicable to common shareholders | | | | |

| Common stock, $0.001 par value; unlimited shares authorized; 546,750.239 shares issued and outstanding | | $ | 547 | |

| Paid-in capital in excess of par | | | 295,354,714 | |

| Accumulated net investment income | | | 1,908,443 | |

| Accumulated net realized loss | | | (11,942,244 | ) |

| Accumulated net unrealized depreciation | | | (52,239,876 | ) |

| Accumulated dividends to preferred shareholders | | | (273,067 | ) |

| Net assets applicable to common shareholders | | $ | 232,808,517 | |

| | | | | |

| Common stock, NAV per share | | $ | 425.80 | |

See accompanying notes.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Investments

September 30, 2008

Showing Percentage of Total Cash and Investments of the Company

| | | | | | | Percent of | |

| | | Principal | | Fair | | Cash and | |

Security | | Amount | | Value | | Investments | |

Debt Securities (67.73%) | | | | | | | | | | |

Bank Debt (59.22%) (1) | | | | | | | | | | |

Alumina and Aluminum Production and Processing (4.30%) | | | | | | | | | | |

| Revere Industries, LLC, 2nd Lien Term Loan, LIBOR + 12.5%, due 6/14/11 | | | | | | | | | | |

| (Acquired 12/14/05, Amortized Cost $20,734,331) | | $ | 20,734,331 | | $ | 18,868,241 | | | 4.30 | % |

| | | | | | | | | | | |

Basic Chemical Manufacturing (0.06%) | | | | | | | | | | |

| Hawkeye Renewables, LLC, 2nd Lien Term Loan, LIBOR + 7.25%, due 6/30/13 | | | | | | | | | | |

| (Acquired 7/18/06, Amortized Cost $1,157,270) | | $ | 1,186,944 | | | 262,611 | | | 0.06 | % |

| | | | | | | | | | | |

Cable Service Carriers (4.82%) | | | | | | | | | | |

| Casema, Mezzanine Term Loan, EURIBOR + 4.5% Cash + 4.75% PIK, due 9/12/16 | | | | | | | | | | |

(Acquired 10/3/06, Amortized Cost $20,635,755) - (Netherlands) (8) | | € | 16,008,319 | | | 21,160,270 | | | 4.82 | % |

| | | | | | | | | | | |

Communications Equipment Manufacturing (11.24%) | | | | | | | | | | |

| Dialogic Corporation, Senior Secured Notes, LIBOR + 10%, due 9/30/10 | | | | | | | | | | |

| (Acquired 9/28/06, Amortized Cost $7,418,398) | | $ | 7,418,398 | | | 7,603,858 | | | 1.73 | % |

| Dialogic Corporation, Senior Secured Notes, LIBOR + 8%, due 10/6/12 | | | | | | | | | | |

| (Acquired 10/5/07, Amortized Cost $2,937,686) | | $ | 2,967,359 | | | 3,026,706 | | | 0.69 | % |

| Enterasys Networks Distribution Limited, 2nd Lien Term Loan, | | | | | | | | | | |

| LIBOR + 9.25%, due 2/22/11 | | | | | | | | | | |

(Acquired 3/1/06, Amortized Cost $2,700,297) - (Ireland)(2), (3) | | $ | 2,755,405 | | | 2,727,851 | | | 0.62 | % |

| Enterasys Networks, Inc., 2nd Lien Term Loan, LIBOR + 9%, due 2/22/11 | | | | | | | | | | |

(Acquired 3/1/06, Amortized Cost $11,839,763) (2), (3) | | $ | 12,081,390 | | | 11,960,576 | | | 2.72 | % |

| Enterasys Networks, Inc., Mezzanine Term Loan, LIBOR + 9.166%, due 2/22/11 | | | | | | | | | | |

(Acquired 3/1/06, Amortized Cost $10,240,323) (2), (3) | | $ | 11,661,721 | | | 11,282,715 | | | 2.57 | % |

| Mitel Networks Corporation, 1st Lien Term Loan, LIBOR + 3.25%, due 8/10/14 | | | | | | | | | | |

| (Acquired 12/13/07, Amortized Cost $13,518,790) | | $ | 14,381,692 | | | 12,770,942 | | | 2.91 | % |

Total Communications Equipment Manufacturing | | | | | | 49,372,648 | | | | |

| | | | | | | | | | | |

Computer and Peripheral Equipment Manufacturing (1.15%) | | | | | | | | | | |

| Palm, Inc., Tranche B Term Loan, LIBOR + 3.5%, due 4/24/14 | | | | | | | | | | |

| (Acquired 11/1/07, Amortized Cost $7,394,602) | | $ | 8,216,224 | | | 5,052,978 | | | 1.15 | % |

| | | | | | | | | | | |

Data Processing, Hosting, and Related Services (8.19%) | | | | | | | | | | |

| GXS Worldwide, Inc., 1st Lien Term Loan, LIBOR + 4%, due 3/31/13 | | | | | | | | | | |

(Acquired 10/12/07, Amortized Cost $6,556,547) (2) | | $ | 6,690,354 | | | 6,322,385 | | | 1.44 | % |

| GXS Worldwide, Inc., 2nd Lien Term Loan, LIBOR + 7.5%, due 9/30/13 | | | | | | | | | | |

(Acquired 10/12/07, Amortized Cost $16,115,893)(2) | | $ | 16,361,312 | | | 15,706,860 | | | 3.58 | % |

| Terremark Worldwide, Inc., 1st Lien Term Loan, LIBOR + 3.75%, due 7/31/12 | | | | | | | | | | |

| (Acquired 8/1/07, Amortized Cost $4,097,738) | | $ | 4,097,738 | | | 3,913,340 | | | 0.89 | % |

| Terremark Worldwide, Inc., 2nd Lien Term Loan, | | | | | | | | | | |

| LIBOR + 3.25% Cash + 4.5% PIK, due 1/31/13 | | | | | | | | | | |

| (Acquired 8/1/07, Amortized Cost $10,486,964) | | $ | 10,546,244 | | | 10,005,749 | | | 2.28 | % |

Total Data Processing, Hosting, and Related Services | | | | | | 35,948,334 | | | | |

| | | | | | | | | | | |

Electric Power Generation, Transmission and Distribution (0.07%) | | | | | | |

| La Paloma Generating Company, Residual Bank Debt | | | | | | | | | | |

(Acquired 2/2/05, 3/18/05, and 5/6/05, Amortized Cost $1,227,816) (4) | | $ | 13,943,926 | | | 328,891 | | | 0.07 | % |

| | | | | | | | | | | |

Management, Scientific, and Technical Consulting Services (0.68%) | | | | | | |

| Booz Allen Hamilton Mezzanine Loan, 11% Cash + 2% PIK, due 7/31/16 | | | | | | | | | | |

| (Acquired 8/1/08, Amortized cost $3,051,740) | | $ | 3,082,566 | | | 2,997,796 | | | 0.68 | % |

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Investments (Continued)

September 30, 2008

Showing Percentage of Total Cash and Investments of the Company

| | | | | | | Percent of | |

| | | Principal | | Fair | | Cash and | |

Security | | Amount | | Value | | Investments | |

| | | | | | | | |

Debt Securities (continued) | | | | | | | | | | |

Motor Vehicle Parts Manufacturing (0.98%) | | | | | | | | | | |

| EaglePicher Corporation, 1st Lien Tranche B Term Loan, | | | | | | | | | | |

| LIBOR + 4.5%, due 12/31/12 | | | | | | | | | | |

(Acquired 12/31/07, Amortized Cost $2,352,393)(2), (3) | | $ | 2,352,393 | | $ | 2,269,275 | | | 0.52 | % |

| EaglePicher Corporation, 2nd Lien Term Loan, LIBOR + 7.5%, due 12/31/13 | | | | | | | | | | |

(Acquired 12/31/07, Amortized Cost $2,077,151)(2), (3) | | $ | 2,077,151 | | | 2,033,184 | | | 0.46 | % |

Total Motor Vehicle Parts Manufacturing | | | | | | 4,302,459 | | | | |

| | | | | | | | | | | |

Offices of Real Estate Agents and Brokers (1.87%) | | | | | | | | | | |

| Realogy Corporation, Revolver, LIBOR + 2.25%, due 4/10/13 | | | | | | | | | | |

| (Acquired 6/28/07 and 7/13/07, Cost $3,213,333) | | $ | 10,000,000 | | | 1,303,333 | | | 0.30 | % |

| Realogy Corporation, Delayed Draw Term Loan, LIBOR + 3%, due 10/10/13 | | | | | | | | | | |

(Acquired 10/9/07, Amortized Cost $4,668,300) (5) | | $ | 4,940,000 | | | 3,689,562 | | | 0.84 | % |

| Realogy Corporation, Term Loan B, LIBOR + 3%, due 10/10/13 | | | | | | | | | | |

| (Acquired 7/17/07, 7/18/07, 7/19/07, 8/15/07, 8/16/07, | | | | | | | | | | |

10/26/07, and 1/11/08, Amortized Cost $3,925,844)(6) | | $ | 4,263,196 | | | 3,184,074 | | | 0.73 | % |

Total Offices of Real Estate Agents and Brokers | | | | | | 8,176,969 | | | | |

| | | | | | | | | | | |

Plastics Product Manufacturing (2.18%) | | | | | | | | | | |

| TR Acquisition Holdings, LLC, 10% PIK, due 5/31/10 | | | | | | | | | | |

(Acquired 12/27/07 and 1/3/08, Amortized Cost $7,601,957)(2), (3) | | $ | 7,602,196 | | | 6,537,889 | | | 1.49 | % |

| WinCup Inc., Term Loan C-2, LIBOR + 14.5% PIK, due 5/29/10 | | | | | | | | | | |

(Acquired 9/18/08, Amortized Cost $2,967,359)(2), (3), (11) | | $ | 2,967,359 | | | 3,011,870 | | | 0.69 | % |

Total Plastics Product Manufacturing | | | | | | 9,549,759 | | | | |

| | | | | | | | | | | |

Radio and Television Broadcasting (0.13%) | | | | | | | | | | |

| High Plains Broadcasting Operating Company, Term Loan, LIBOR + 5%, due 9/14/16 | | | | | | | | | | |

| (Acquired 9/15/08, Amortized Cost $130,589) | | $ | 143,505 | | | 121,979 | | | 0.03 | % |

| Newport Television LLC, Term Loan B, LIBOR + 5%, due 9/14/16 | | | | | | | | | | |

| (Acquired 5/1/08 and 5/29/08, Amortized Cost $493,608) | | $ | 542,426 | | | 461,062 | | | 0.10 | % |

Total Radio and Television Broadcasting | | | | | | 583,041 | | | | |

| | | | | | | | | | | |

Satellite Telecommunications (5.22%) | | | | | | | | | | |

| WildBlue Communications, Inc., 1st Lien Delayed Draw Term Loan, | | | | | | | | | | |

| LIBOR + 4% Cash + 2.5% PIK, due 12/31/09 | | | | | | | | | | |

(Acquired 6/6/06, Amortized Cost $11,500,013) (2) | | $ | 11,518,965 | | | 10,796,726 | | | 2.46 | % |

| WildBlue Communications, Inc., 2nd Lien Delayed Draw Term Loan, | | | | | | | | | | |

| LIBOR + 8.5% Cash + 7.25% PIK, due 8/15/11 | | | | | | | | | | |

(Acquired 8/16/06, Amortized Cost $12,636,652)(2) | | $ | 13,025,511 | | | 12,123,494 | | | 2.76 | % |

Total Satellite Telecommunications | | | | | | 22,920,220 | | | | |

| | | | | | | | | | | |

Scheduled Air Transportation (3.90%) | | | | | | | | | | |

| Northwest Airlines, Inc., 1st Preferred Mortgage Loan, N645NW, 9.85%, due 10/15/12 | | | | | | | | | | |

| (Restated and Amended 1/18/06, Amortized Cost $4,774,254) | | $ | 4,804,182 | | | 4,812,589 | | | 1.10 | % |

| Northwest Airlines, Inc., 1st Preferred Mortgage Loan, N646NW, 9.85%, due 10/15/12 | | | | | | | | | | |

| (Restated and Amended 1/18/06, Amortized Cost $4,774,254) | | $ | 4,804,182 | | | 4,812,589 | | | 1.10 | % |

| Northwest Airlines, Inc., 1st Preferred Mortgage Loan, N632NW, 9.85%, due 7/15/13 | | | | | | | | | | |

| (Restated and Amended 1/18/06, Amortized Cost $5,325,735) | | $ | 5,359,056 | | | 5,360,396 | | | 1.22 | % |

| Northwest Airlines, Inc., 1st Preferred Mortgage Loan, N631NW, 9.85%, due 12/15/13 | | | | | | | | | | |

| (Restated and Amended 1/18/06, Amortized Cost $2,131,436) | | $ | 2,144,772 | | | 2,138,337 | | | 0.48 | % |

Total Scheduled Air Transportation | | | | | | 17,123,911 | | | | |

| | | | | | | | | | | |

Semiconductor and Other Electronic Component Manufacturing (3.64%) | | | | | | | | | | |

| Isola USA Corporation, 1st Lien Term Loan, LIBOR + 6.75%, due 12/18/12 | | | | | | | | | | |

| (Acquired 7/12/07 and 11/19/07, Amortized Cost $2,885,859) | | $ | 3,021,104 | | | 2,794,521 | | | 0.64 | % |

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Investments (Continued)

September 30, 2008

Showing Percentage of Total Cash and Investments of the Company

| | | | | | | Percent of | |

| | | Principal | | Fair | | Cash and | |

Security | | Amount | | Value | | Investments | |

| | | | | | | | |

Debt Securities (continued) | | | | | | | | | | |

| Isola USA Corporation, 2nd Lien Term Loan, LIBOR + 11%, due 12/18/13 | | | | | | | | | | |

| (Acquired 12/21/06, 4/16/07 and 5/22/07, Amortized Cost $14,661,398) | | $ | 15,133,531 | | $ | 13,166,172 | | | 3.00 | % |

Total Semiconductor and Other Electronic Component Manufacturing | | | | | | 15,960,693 | | | | |

| | | | | | | | | | | |

Telecom Wireline (10.79%) | | | | | | | | | | |

| Cavalier Telephone Corporation, Senior Secured 1st Lien Term Loan, | | | | | | | | | | |

| LIBOR + 6.25% Cash + 1% PIK, due 12/31/12 | | | | | | | | | | |

| (Acquired 4/24/08, Amortized Cost $508,857) | | $ | 651,648 | | | 390,989 | | | 0.09 | % |

| Global Crossing Limited, Tranche B Term Loan, LIBOR + 6.25%, due 5/9/12 | | | | | | | | | | |

| (Acquired 6/4/07, Amortized Cost $6,129,791) | | $ | 6,129,791 | | | 5,670,057 | | | 1.29 | % |

| Hawaiian Telcom Communications, Inc., Revolver, LIBOR + 2.25%, due 4/30/12 | | | | | | | | | | |

| (Acquired 5/9/08 and 5/16/08, Cost $(446,439)) | | $ | 2,198,498 | | | (593,594 | ) | | (0.14 | )% |

| Integra Telecom, Inc., 2nd Lien Term Loan, LIBOR + 7%, due 2/28/14 | | | | | | | | | | |

(Acquired 7/31/06, Amortized Cost $12,595,236) (2) | | $ | 13,120,038 | | | 11,676,834 | | | 2.66 | % |

| Integra Telecom, Inc., Term Loan, LIBOR + 10% PIK, due 8/31/14 | | | | | | | | | | |

(Acquired 9/05/07, Amortized Cost $17,247,348) (2) | | $ | 17,247,348 | | | 13,625,405 | | | 3.10 | % |

| Interstate Fibernet, Inc., 1st Lien Term Loan, LIBOR + 4%, due 7/31/13 | | | | | | | | | | |

| (Acquired 8/01/07, Amortized Cost $8,010,455) | | $ | 8,236,972 | | | 6,919,056 | | | 1.58 | % |

| Interstate Fibernet, Inc., 2nd Lien Term Loan, LIBOR + 7.5%, due 7/31/14 | | | | | | | | | | |

| (Acquired 7/31/07, Amortized Cost $8,892,017) | | $ | 8,892,017 | | | 8,260,684 | | | 1.88 | % |

| NEF Telecom Company BV, 2nd Lien Tranche D Term Loan, EURIBOR + 5.5%, | | | | | | | | | | |

| due 2/16/17 | | | | | | | | | | |

(Acquired 8/29/07, Amortized Cost $1,529,010) - (Netherlands) (8) | | € | 1,113,961 | | | 1,440,285 | | | 0.33 | % |

Total Telecom Wireline | | | | | | 47,389,716 | | | | |

| | | | | | | | | | | |

Total Bank Debt (Cost $280,700,323) | | | | | | 259,998,537 | | | | |

| | | | | | | | | | | |

Other Corporate Debt Securities (8.51%) | | | | | | | | | | |

Gambling Industries (1.20%) | | | | | | | | | | |

| Harrah's Operating Company Inc., Senior Notes, 10.75%, due 2/1/16 | | $ | 9,250,000 | | | 4,810,000 | | | 1.09 | % |

| Harrah's Operating Company Inc., Senior Notes, 5.375%, due 12/15/13 | | $ | 1,418,000 | | | 476,561 | | | 0.11 | % |

Total Gambling Industries | | | | | | 5,286,561 | | | | |

| | | | | | | | | | | |

Home Furnishings Stores (0.18%) | | | | | | | | | | |

Linens 'n Things, Inc., Senior Secured Notes, LIBOR + 5.625%, due 1/15/14 (4) | | $ | 2,782,000 | | | 775,649 | | | 0.18 | % |

| | | | | | | | | | | |

Industrial Machinery Manufacturing (1.06%) | | | | | | | | | | |

| GSI Group Corporation, Senior Notes, 11%, due 8/20/13 | | | | | | | | | | |

(Acquired 8/20/08, Amortized Cost $4,822,396) (9) | | $ | 5,632,000 | | | 4,663,296 | | | 1.06 | % |

| | | | | | | | | | | |

Offices of Real Estate Agents and Brokers (0.49%) | | | | | | | | | | |

| Realogy Corporation, Senior Subordinated Notes, 12.375%, due 4/15/15 | | $ | 3,556,000 | | | 1,359,637 | | | 0.31 | % |

| Realogy Corporation, Senior Notes, 10.5%, due 4/15/14 | | $ | 1,707,000 | | | 772,418 | | | 0.18 | % |

Total Offices of Real Estate Agents and Brokers | | | | | | 2,132,055 | | | | |

| | | | | | | | | | | |

Other Amusement and Recreation Industries (1.18%) | | | | | | | | | | |

| Bally Total Fitness Holdings, Inc., Senior Subordinated Notes, | | | | | | | | | | |

| 14% Cash or 15.625% PIK, due 10/1/13 | | | | | | | | | | |

(Acquired 10/1/07, Amortized Cost $13,275,383)(9) | | $ | 12,989,333 | | | 5,195,733 | | | 1.18 | % |

| | | | | | | | | | | |

Plastics Product Manufacturing (1.42%) | | | | | | | | | | |

| Pliant Corporation, Senior Secured 2nd Lien Notes, 11.125%, due 9/1/09 | | $ | 7,424,000 | | | 5,339,638 | | | 1.22 | % |

| Radnor Holdings, Senior Secured Tranche C Notes, LIBOR + 7.25%, due 9/15/09 | | | | | | | | | | |

(Acquired 4/4/06, Amortized Cost $6,811,237)(4), (9) | | $ | 6,973,000 | | | 890,173 | | | 0.20 | % |

Total Plastics Product Manufacturing | | | | | | 6,229,811 | | | | |

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Investments (Continued)

September 30, 2008

Showing Percentage of Total Cash and Investments of the Company

| | | | | | | Percent of | |

| | | Principal Amount | | Fair | | Cash and | |

Security | | or Shares | | Value | | Investments | |

| | | | | | | | |

Other Corporate Debt Securities (continued) | | | | | | | | | | |

Sporting Goods, Hobby, and Musical Instrument Stores (0.24%) | | | | | | | | | | |

| Michaels Stores, Inc., Senior Unsecured Notes, 10%, due 11/1/14 | | $ | 1,703,000 | | $ | 1,072,890 | | | 0.24 | % |

| | | | | | | | | | | |

Telecom Wireline (2.74%) | | | | | | | | | | |

| NEF Telecom Company BV, Mezzanine Term Loan, EURIBOR + 10% PIK, due 8/16/17 | | | | | | | | | | |

(Acquired 8/29/07, Amortized Cost $14,162,432) - (Netherlands) (8) | | € | 10,188,993 | | | 12,014,331 | | | 2.74 | % |

| | | | | | | | | | | |

Total Other Corporate Debt Securities (Cost $62,040,918) | | | | | | 37,370,326 | | | | |

| | | | | | | | | | | |

Total Debt Securities (Cost $342,741,241) | | | | | | 297,368,863 | | | | |

| | | | | | | | | | | |

Equity Securities (26.53%) | | | | | | | | | | |

Activities Related to Credit Intermediation (6.46%) | | | | | | | | | | |

| Online Resources Corporation, Series A-1 Convertible Preferred Stock | | | | | | | | | | |

(Acquired 7/3/06, Cost $22,255,193) (2), (3), (4), (9), (11) | | | 22,255,193 | | | 24,091,246 | | | 5.49 | % |

Online Resources Corporation, Common Stock(3), (4), (7), (11) | | | 549,555 | | | 4,270,042 | | | 0.97 | % |

Total Activities Related to Credit Intermediation | | | | | | 28,361,288 | | | | |

| | | | | | | | | | | |

Basic Chemical Manufacturing (0.07%) | | | | | | | | | | |

| THL Hawkeye Equity Investors, LP Interest | | | | | | | | | | |

(Acquired 7/25/06, Cost $2,255,196) (4), (9) | | | 2,373,887 | | | 287,834 | | | 0.07 | % |

| | | | | | | | | | | |

Clothing Stores (1.54%) | | | | | | | | | | |

| Stage Stores Inc., Common Stock | | | 494,746 | | | 6,758,230 | | | 1.54 | % |

| | | | | | | | | | | |

Communications Equipment Manufacturing (4.59%) | | | | | | | | | | |

| Dialogic Corporation, Class A Convertible Preferred Stock | | | | | | | | | | |

(Acquired 9/28/06, Cost $2,967,357) (4), (9) | | | 3,037,033 | | | 3,143,329 | | | 0.71 | % |

| Enterasys Networks, Inc., Series A Convertible Preferred Stock | | | | | | | | | | |

(Acquired 3/1/06 and 11/9/06, Cost $10,385,327) (2), (3), (4), (9), (11) | | | 10,385.327 | | | 15,526,064 | | | 3.54 | % |

| Enterasys Networks, Inc., Series B Convertible Preferred Stock | | | | | | | | | | |

(Acquired 3/1/06, Cost $1,188,164) (2), (3), (4), (9), (11) | | | 1,843.827 | | | 1,484,281 | | | 0.34 | % |

Total Communications Equipment Manufacturing | | | | | | 20,153,674 | | | | |

| | | | | | | | | | | |

Data Processing, Hosting, and Related Services (0.30%) | | | | | | | | | | |

| GXS Holdings, Inc., Common Stock | | | | | | | | | | |

(Acquired 3/28/08, Cost $681,620) (4), (9), (10) | | | 708,885 | | | 1,268,904 | | | 0.29 | % |

| GXS Holdings, Inc., Series A Preferred Stock | | | | | | | | | | |

(Acquired 3/28/08, Cost $27,265) (4), (9), (10) | | | 28,335 | | | 50,756 | | | 0.01 | % |

Total Data Processing, Hosting, and Related Services | | | | | | 1,319,660 | | | | |

| | | | | | | | | | | |

Depository Credit Intermediation (1.02%) | | | | | | | | | | |

| Doral Holdings, LP Interest | | | | | | | | | | |

(Acquired 7/12/07, Cost $4,151,971) (4), (9) | | | 4,151,971 | | | 4,480,000 | | | 1.02 | % |

| | | | | | | | | | | |

Electric Power Generation, Transmission and Distribution (0.75%) | | | | | | |

| Mach Gen, LLC, Common Units | | | | | | | | | | |

(Acquired 8/17/05, 11/9/05, 12/14/05 and 12/19/05, Cost $795,120) (4), (9) | | | 4,542 | | | 2,876,449 | | | 0.66 | % |

| Mach Gen, LLC, Warrants to purchase Warrant Units | | | | | | | | | | |

(Acquired 8/17/05, 11/9/05, 12/14/05 and 12/19/05, Cost $336,895) (4), (9) | | | 1,831 | | | 411,975 | | | 0.09 | % |

Total Electric Power Generation, Transmission and Distribution | | | | | | 3,288,424 | | | | |

| | | | | | | | | | | |

Industrial Machinery Manufacturing (0.13%) | | | | | | | | | | |

| GSI Group, Inc., Warrant to purchase Common Shares | | | | | | | | | | |

(Acquired 8/20/08, Cost $822,739) (4), (9) | | | 157,764 | | | 555,329 | | | 0.13 | % |

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Investments (Continued)

September 30, 2008

Showing Percentage of Total Cash and Investments of the Company

| | | | | | | Percent of | |

| | | Principal Amount | | Fair | | Cash and | |

Security | | or Shares | | Value | | Investments | |

| | | | | | | | |

Equity Securities (continued) | | | | | | | | | | |

Motor Vehicle Parts Manufacturing (6.05%) | | | | | | | | | | |

| EaglePicher Holdings, Inc., Common Stock | | | | | | | | | | |

(Acquired 3/9/05, Cost $16,009,993) (2), (3), (4), (9), (11), (12) | | | 854,400 | | $ | 26,559,024 | | | 6.05 | % |

| | | | | | | | | | | |

Plastics Product Manufacturing (4.15%) | | | | | | | | | | |

| Pliant Corporation, Common Stock | | | | | | | | | | |

(Acquired 07/19/06, Cost $91) (4), (9), (13) | | | 217 | | | 217 | | | - | |

| Pliant Corporation, 13% PIK, Preferred Stock | | | 3,535 | | | 1,437,137 | | | 0.32 | % |

| Radnor Holdings, Series A Convertible Preferred Stock | | | | | | | | | | |

(Acquired 10/27/05, Cost $7,163,929) (4), (9) | | | 7,874,163 | | | - | | | - | |

| Radnor Holdings, Common Stock | | | | | | | | | | |

(Acquired 7/31/06, Cost $60,966) (4), (9) | | | 30 | | | - | | | - | |

| Radnor Holdings, Non-Voting Common Stock | | | | | | | | | | |

(Acquired 7/31/06, Cost $628,814) (4), (9) | | | 305 | | | - | | | - | |

| Radnor Holdings, Warrants for Common Stock | | | | | | | | | | |

(Acquired 10/27/05, Cost $594) (4), (9) | | | 1 | | | - | | | - | |

| Radnor Holdings, Warrants for Non-Voting Common Stock | | | | | | | | | | |

(Acquired 10/27/05, Cost $594) (4), (9) | | | 1 | | | - | | | - | |

| WinCup, Inc., Common Stock | | | | | | | | | | |

(Acquired 11/29/06, Cost $31,020,365)(2), (3), (4), (9), (11) | | | 31,020,365 | | | 16,795,305 | | | 3.83 | % |

Total Plastics Product Manufacturing | | | | | | 18,232,659 | | | | |

| | | | | | | | | | | |

Satellite Telecommunications (0.61%) | | | | | | | | | | |

| WildBlue Communications, Inc., Warrants to Purchase Common Stock | | | | | | | | | | |

(Acquired 8/16/08, Cost $508,737) (2), (4), (9) | | | 39,225 | | | 2,670,046 | | | 0.61 | % |

| | | | | | | | | | | |

Semiconductor and Other Electronic Component Manufacturing (0.49%) | | | | | | | | | | |

| TPG Hattrick Holdco, LLC, Common Units | | | | | | | | | | |

(Acquired 4/21/06, Cost $1,630,062) (4), (9) | | | 969,092 | | | 2,170,766 | | | 0.49 | % |

| | | | | | | | | | | |

Telecom Wireline (0.37%) | | | | | | | | | | |

| NEF Kamchia Co-Investment Fund, LP Interest | | | | | | | | | | |

(Acquired 7/30/07, Cost $2,439,543) - (Cayman Islands) (4), (8), (9) | | | 1,779,000 | | | 1,612,815 | | | 0.37 | % |

| | | | | | | | | | | |

Total Equity Securities (Cost $119,722,133) | | | | | | 116,449,749 | | | | |

| | | | | | | | | | | |

Total Investments (Cost $462,463,374) (14) | | | | | | 413,818,612 | | | | |

| | | | | | | | | | | |

Cash and Cash Equivalents (5.74%) | | | | | | | | | | |

| Toyota Motor Credit Corporation, Commercial Paper, 2%, due 10/8/08 | | $ | 4,000,000 | | | 3,995,000 | | | 0.91 | % |

| Toyota Motor Credit Corporation, Commercial Paper, 2%, due 10/1/08 | | $ | 1,000,000 | | | 1,000,000 | | | 0.23 | % |

| General Electric Credit Corporation, Commercial Paper, 2.25%, due 10/7/08 | | $ | 8,000,000 | | | 7,997,000 | | | 1.82 | % |

| Wells Fargo, Overnight Repurchase Agreement, 0.55%, | | | | | | | | | | |

| Collateralized by FHLB Discount Notes | | $ | 3,355,885 | | | 3,355,885 | | | 0.76 | % |

| Cash Denominated in Foreign Currencies (Cost $255,413) | | € | 187,670 | | | 264,465 | | | 0.06 | % |

| Cash Held on Account at Various Institutions | | $ | 8,597,554 | | | 8,597,554 | | | 1.96 | % |

Total Cash and Cash Equivalents (15) | | | | | | 25,209,904 | | | | |

| | | | | | | | | | | |

Total Cash and Investments | | | | | $ | 439,028,516 | | | 100.00 | % |

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Investments (Continued)

September 30, 2008

Notes to Statement of Investments

| (1) | Investments in bank debt generally are bought and sold among institutional investors in transactions not subject to registration under the Securities Act of 1933. Such transactions are generally subject to contractual restrictions, such as approval of the agent or borrower. |

| (2) | Priced by an independent third party pricing service. |

| (3) | Affiliated issuer - as defined under the Investment Company Act of 1940 (ownership of 5% or more of the outstanding voting securities of this issuer). |

| (4) | Non-income producing security. |

| (5) | On 10/9/07, the Company held Realogy Corporation Senior Subordinated Notes, 12.375%, due 4/15/15, priced at 77.598. |

| (6) | On 10/26/07 and 1/11/08, the Company held Realogy Corporation Senior Subordinated Notes, 12.375%, due 4/15/15, priced at 73 and 58.227, respectively. |

| (7) | Priced at NASDAQ closing price. |

| (8) | Principal amount denominated in euros. Amortized cost and fair value converted from euros to U.S. dollars. |

| (10) | Priced by the investment manager. |

| (11) | Investment is not a controlling position. |

| (12) | The Company's advisor may demand registration at any time more than 180 days following the first initial public offering of common equity by the issuer. |

| (13) | The Company may demand registration of the shares as part of a majority (by interest) of the registrable shares of the issuer, or in connection with an initial public offering by the issuer. |

| (14) | Includes investments with an aggregate fair value of $12,044,792 that have been segregated to collateralize certain unfunded commitments. |

| (15) | Includes $7.2 million pledged as collateral for certain derivative contracts. |

Aggregate purchases and aggregate sales of securities, other than Government securities, totaled $173,283,012 and $162,904,465 respectively. Aggregate purchases include securities received as payment in kind. Aggregate sales include principal paydowns on debt securities.

The total value of restricted securities and bank debt as of September 30, 2008 was $374,732,079 or 85.35% of total cash and investments of the Company.

Swaps and forward contracts at September 30, 2008 were as follows:

| | | Number of | | | |

| | | Contracts or | | Fair | |

| Instrument | | Notional Amount | | Value | |

| | | | | | |

| Forward Contracts | | | | | | | |

| Euro/US Dollar Forward Currency Contract, Expires 9/15/09 | | $ | 463,148 | | $ | (34,141 | ) |

| Euro/US Dollar Forward Currency Contract, Expires 2/1/10 | | $ | 772,997 | | | (42,751 | ) |

| Total Forwards Contracts | | | | | | (76,892 | ) |

| | | | | | | | |

| Swaps | | | | | | | |

| Euro/US Dollar Cross Currency Basis Swap, Pay Euros / Receive USD, Expires 9/13/16 | | $ | 20,393,859 | | | (2,789,306 | ) |

| Euro/US Dollar Cross Currency Basis Swap, Pay Euros / Receive USD, Expires 5/17/12 | | $ | 13,121,097 | | | (737,969 | ) |

| Total Swaps | | | | | | (3,527,275 | ) |

| | | | | | | | |

| Total Swaps and Forward Contracts | | | | | $ | (3,604,167 | ) |

See accompanying notes.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Operations

Year Ended September 30, 2008

| Investment income | | | | |

| Interest income: | | | | |

| Unaffiliated issuers | | $ | 48,250,896 | |

| Affiliates | | | 4,483,672 | |

| Dividend income - unaffiliated issuers | | | 475,529 | |

| Other income - affiliates | | | 780,998 | |

| Total investment income | | | 53,991,095 | |

| | | | | |

| Operating expenses | | | | |

| Performance fee adjustment (Notes 3 and 7) | | | (2,328,293 | ) |

| Interest expense | | | 5,332,772 | |

| Management and advisory fees | | | 3,600,000 | |

| Credit enhancement fees | | | 635,542 | |

| Commitment fees | | | 537,708 | |

| Legal fees, professional fees and due diligence expenses | | | 298,935 | |

| Amortization of deferred debt issuance costs | | | 297,484 | |

| Preferred shares brokerage fees | | | 246,876 | |

| Director fees | | | 176,000 | |

| Custody fees | | | 100,000 | |

| Insurance expense | | | 88,249 | |

| Other operating expenses | | | 385,262 | |

| Total expenses | | | 9,370,535 | |

| | | | | |

| Net investment income | | | 44,620,560 | |

| | | | | |

| Net realized and unrealized loss | | | | |

| Net realized loss from: | | | | |

| Investments in unaffiliated issuers | | | (11,942,244 | ) |

| Foreign currency transactions | | | (128,044 | ) |

| Net realized loss | | | (12,070,288 | ) |

| | | | | |

| Net change in net unrealized appreciation (depreciation) on: | | | | |

| Investments | | | (73,781,717 | ) |

| Foreign currency | | | 1,127 | |

| Net change in unrealized appreciation (depreciation) | | | (73,780,590 | ) |

| | | | | |

| Net realized and unrealized loss | | | (85,850,878 | ) |

| | | | | |

| Distributions to preferred shareholders | | | (6,318,235 | ) |

| Net change in reserve for distributions to preferred shareholders | | | 227,867 | |

| | | | | |

| Net decrease in net assets applicable to common shareholders resulting from operations | | $ | (47,320,686 | ) |

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statements of Changes in Net Assets

| | | Year Ended | | Year Ended | |

| | | September 30, 2008 | | September 30, 2007 | |

| | | | | | |

| Total common shareholder committed capital | | $ | 300,000,000 | | $ | 300,000,000 | |

| | | | | | | | |

| Net assets applicable to common shareholders, beginning of year | | $ | 313,129,203 | | $ | 314,270,127 | |

| | | | | | | | |

| Net investment income | | | 44,620,560 | | | 23,421,580 | |

| Net realized gain (loss) on investments | | | (12,070,288 | ) | | 32,610,387 | |

| Net change in unrealized appreciation (depreciation) on investments and foreign currency | | | (73,780,590 | ) | | (4,732,297 | ) |

| Distributions to preferred shareholders from net investment income | | | (6,318,235 | ) | | (1,782,075 | ) |

| Distributions to preferred shareholders from net realized gains on investments | | | - | | | (3,492,349 | ) |

| Net change in reserve for distributions to preferred shareholders | | | 227,867 | | | (283,003 | ) |

| Net increase (decrease) in net assets applicable to common shareholders | | | | | | | |

| resulting from operations | | | (47,320,686 | ) | | 45,742,243 | |

| | | | | | | | |

| Distributions to common shareholders from: | | | | | | | |

| Net investment income | | | (33,000,000 | ) | | (14,858,351 | ) |

| Net realized gains | | | - | | | (29,118,038 | ) |

| Returns of capital | | | - | | | (2,906,778 | ) |

| Total distributions to common shareholders | | | (33,000,000 | ) | | (46,883,167 | ) |

| | | | | | | | |

| Net assets applicable to common shareholders, end of year (including accumulated net investment income of $1,908,443 and distributions in excess of net investment income of $3,265,838, respectively) | | $ | 232,808,517 | | $ | 313,129,203 | |

See accompanying notes.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Statement of Cash Flows

Year Ended September 30, 2008

| Operating activities | | | | |

| Net decrease in net assets applicable to common shareholders resulting from operations | | $ | (47,320,686 | ) |

Adjustments to reconcile net decrease in net assets applicable to common

shareholders resulting from operations to net cash provided by operating activities: | | | | |

| Net realized loss on investments | | | 12,070,288 | |

| Net change in unrealized appreciation (depreciation) on investments | | | 73,781,717 | |

| Distributions paid to preferred shareholders | | | 6,318,235 | |

| Decrease in reserve for distributions to preferred shareholders | | | (227,867 | ) |

| Accretion of original issue discount | | | (963,399 | ) |

| Net accretion of market discount/premium | | | (3,511,430 | ) |

| Income from paid in-kind capitalization | | | (11,456,746 | ) |

| Amortization of deferred debt issuance costs | | | 297,484 | |

| Changes in assets and liabilities: | | | | |

| Purchases of investment securities | | | (161,826,266 | ) |

| Proceeds from sales, maturities and paydowns of investment securities | | | 162,904,465 | |

| Decrease in accrued interest income - unaffiliated issuers | | | 99,816 | |

| Decrease in accrued interest income - affiliates | | | 956,863 | |

| Decrease in prepaid expenses and other assets | | | 108,744 | |

| Increase in receivable for investment securities sold | | | (4,059,745 | ) |

| Decrease in other receivables | | | 1,466,434 | |

| Decrease in payable for investment securities purchased | | | (5,317,517 | ) |

| Decrease in performance fee payable | | | (3,455,016 | ) |

| Decrease in interest payable | | | (102,955 | ) |

| Decrease in payable to affiliate | | | (29,930 | ) |

| Decrease in accrued expenses and other liabilities | | | (546,241 | ) |

| Net cash provided by operating activities | | | 19,186,248 | |

| | | | | |

| Financing activities | | | | |

| Proceeds from draws on credit facility | | | 92,500,000 | |

| Principal repayment on credit facility | | | (129,500,000 | ) |

| Distributions paid to common shareholders | | | (33,000,000 | ) |

| Distributions paid to preferred shareholders | | | (6,318,235 | ) |

| Net cash used in financing activities | | | (76,318,235 | ) |

| | | | | |

| Net decrease in cash and cash equivalents | | | (57,131,987 | ) |

| Cash and cash equivalents at beginning of year | | | 82,341,891 | |

| Cash and cash equivalents at end of year | | $ | 25,209,904 | |

| | | | | |

| Supplemental cash flow information | | | | |

| Interest payments | | $ | 5,435,727 | |

See accompanying notes.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements

September 30, 2008

1. Organization and Nature of Operations

Special Value Expansion Fund, LLC (the “Company”), a Delaware Limited Liability Company, is registered as a nondiversified, closed-end management investment company under the Investment Company Act of 1940 (the “1940 Act”). The Company has elected to be treated as a regulated investment company (“RIC”) for U.S. federal income tax purposes. The Company will not be taxed on its income to the extent that it distributes such income each year and satisfies other applicable income tax requirements.

The Certificate of Formation of the Company was filed with the Delaware Secretary of State on August 12, 2004. Investment operations commenced and initial funding was received on September 1, 2004. The Company was formed to acquire a portfolio of investments consisting primarily of bank loans, distressed debt, stressed high yield debt, mezzanine investments and public equities. The stated objective of the Company is to generate current income as well as long-term capital appreciation using a leveraged capital structure. GMAM Investment Funds Trust II (“GMAM”) owns 99.5% of the Company’s common shares.

Tennenbaum Capital Partners, LLC (“TCP”) serves as the Investment Manager of the Company. The Company, TCP and their members and affiliates may be considered related parties.

Company management consists of the Investment Manager and the Board of Directors. The Investment Manager directs and executes the day-to-day operations of the Company, subject to oversight from the Board of Directors, which sets the broad policies for the Company. The Board of Directors consists of three persons, two of whom are independent. If the Company has preferred shares outstanding, as it currently does, the holders of the preferred shares voting separately as a class will be entitled to elect two of the Company’s Directors. The remaining Director of the Company will be subject to election by holders of common shares and preferred shares voting together as a single class.

Company Structure

Total maximum capitalization of the Company is $600 million, consisting of $300 million of common equity, $100 million of auction-rate preferred shares (“APS”), $200 million under a senior secured revolving credit facility (the “Senior Facility”), $156,000 of Series Z Preferred Stock and $1,000 of Series S Preferred Stock (see Note 7). The contributed investor capital, APS and the amount drawn under the Senior Facility are to be used to purchase Company investments and to pay certain fees and expenses of the Company. Most of these investments are included in the collateral for the Senior Facility.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

1. Organization and Nature of Operations (continued)

Credit enhancement with respect to the APS and Senior Facility is provided by a monoline insurer (the “Insurer”) through surety policies issued pursuant to an insurance and indemnity agreement between the Company and the Insurer. Under the surety policies, the Insurer will guarantee payment of the liquidation preference and unpaid dividends on the APS and amounts drawn under the Senior Facility. The cost of the surety polices is 0.11% for unutilized portions of the APS and the Senior Facility and 0.24% for the outstanding portions of those sources of capital.

The Company will liquidate and distribute its assets and will be dissolved at September 1, 2014, subject to up to two one-year extensions if requested by the Investment Manager and approved by a majority of the Company’s equity interests. However, the Company’s operating agreement prohibits the liquidation of the Company prior to September 1, 2014 if the APS are not redeemed in full prior to such liquidation.

Auction-Rate Preferred Capital

At September 30, 2008, the Company had 2,000 shares of APS issued and outstanding with a liquidation preference of $50,000 per share (plus an amount equal to accumulated but unpaid dividends upon liquidation). The APS are redeemable at the option of the Company, subject to certain limitations. Additionally, under certain conditions, the Company may be required to either redeem certain of the APS or repay indebtedness, at the Company’s option. Such conditions would include a failure by the Company to maintain adequate collateral as required by its credit facility agreement or by the Statement of Preferences of the APS, or a failure by the Company to maintain sufficient asset coverage as required by the 1940 Act. As of September 30, 2008, the Company was in full compliance with such requirements.

2. Summary of Significant Accounting Policies

Basis of Presentation

The financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). In the opinion of the Investment Manager, the financial results of the Company included herein contain all adjustments necessary to present fairly the financial position of the Company as of September 30, 2008, the results of its operations and cash flows for the year then ended, and the changes in net assets for each of the two years in the period then ended. The following is a summary of the significant accounting policies of the Company.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

2. Summary of Significant Accounting Policies (continued)

Investment Valuation

Management values investments held by the Company at fair value based upon the principles and methods of valuation set forth in policies adopted by the Company’s Board of Directors and in conformity with procedures set forth in the Senior Facility and Statement of Preferences for the APS. Investments listed on a recognized exchange or market quotation system, whether U.S. or foreign, are valued for financial reporting purposes as of the last business day of the reporting period using the closing price on the date of valuation.

Liquid investments not listed on a recognized exchange or market quotation system are valued by an approved nationally recognized pricing service or by using either the average of the bid prices on the date of valuation, as supplied by three approved broker-dealers, or the lower of two quotes from approved broker-dealers. At September 30, 2008, all but 2.8% of the investments of the Company were valued based on prices from a recognized exchange or market quotation system, a nationally recognized pricing service or an approved third-party appraisal.

Investments not listed on a recognized exchange or market quotation system nor priced by broker-dealers or a pricing service (“Unquoted Investments”) are valued by a third-party valuation service or, for investments aggregating less than 5% of the total capitalization of the Company, by the Investment Manager.

Investments for which market quotations are not readily available or are determined to be unreliable are valued at fair value under guidelines adopted by the Board of Directors, with such fair valuations subject to their approval. Fair value is generally defined as the amount for which an investment could be sold in an orderly disposition over a reasonable time. Generally, to increase objectivity in valuing the Company’s investments, the Investment Manager will utilize external measures of value, such as public markets or third-party transactions, whenever possible.

The Investment Manager’s valuation is not based on long-term work-out value, immediate liquidation value, nor incremental value for potential changes that may take place in the future. The values assigned to investments that are valued by the Investment Manager are based on available information and do not necessarily represent amounts that might ultimately be realized, as these amounts depend on future circumstances and cannot reasonably be determined until the individual investments are actually liquidated. The Investment Manager generally uses three methods to fair value investments:

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

2. Summary of Significant Accounting Policies (continued)

(i) Cost Method. The cost method is based on the original cost of the investments to the Company. This method is generally used in the early stages of a portfolio company’s development until significant positive or negative events occur subsequent to the date of the original investment by the Company in such company that dictate a change to another valuation method.

(ii) Private Market Method. The private market method uses actual, executed, historical transactions in a portfolio company’s securities by responsible third parties as a basis for valuation. In connection with utilizing the private market method, the Investment Manager may also use, where applicable, unconditional firm offers by responsible third parties as a basis for valuation.

(iii) Analytic Method. The analytical method is generally used by the Investment Manager to value an investment position when there is no established public or private market in the portfolio company’s securities or when the factual information available to the Investment Manager dictates that an investment should no longer be valued under either the cost or private market method. This valuation method is based on the judgment of the Investment Manager, using data available for the applicable portfolio investments.

Because of the inherent uncertainty of valuations, these estimated values may differ significantly from the values that would have been used had a ready market for such investments existed, and the differences could be material.

Investment Transactions

The Company records investment transactions on the trade date, except for private transactions that have conditions to closing, which are recorded on the closing date. The cost of investments purchased is based upon the purchase price plus those professional fees which are specifically identifiable to the investment transaction. Realized gains and losses on investments are recorded based on the specific identification method, which typically allocates the highest cost inventory to the basis of the investments sold.

Cash and Cash Equivalents

Cash consists of amounts held in accounts with brokerage firms and the custodian bank. Cash equivalents consist of highly liquid investments with an original maturity of three months or less. For purposes of reporting cash flows, cash consists of the cash held with brokerage firms and the custodian bank and cash equivalents maturing within 90 days.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

2. Summary of Significant Accounting Policies (continued)

Repurchase Agreements

In connection with transactions in repurchase agreements, it is the Company’s policy that its custodian take possession of the underlying collateral, the fair value of which is required to exceed the principal amount of the repurchase transaction, including accrued interest, at all times. If the seller defaults, and the fair value of the collateral declines, realization of the collateral by the Company may be delayed or limited.

Restricted Investments

The Company may invest in instruments that are subject to legal or contractual restrictions on resale. These investments generally may be resold to institutional investors in transactions exempt from registration or to the public if the securities are registered. Disposal of these investments may involve time-consuming negotiations and additional expense, and prompt sale at an acceptable price may be difficult. Information regarding restricted investments is included at the end of the Statement of Investments. Restricted investments, including any restricted investments in affiliates, are valued in accordance with the investment valuation policies discussed above.

Foreign Investments

The Company may invest in instruments traded in foreign countries and denominated in foreign currencies. At September 30, 2008, the Company had foreign currency denominated investments with an aggregate market value of approximately 8.8% of the Company’s total investments. Such positions were converted at the closing rate in effect at September 30, 2008 and reported in U.S. dollars. Purchases and sales of investments and income and expense items denominated in foreign currencies, when they occur, are translated into U.S. dollars on the respective dates of such transactions. As such, foreign investment positions and transactions are susceptible to foreign currency as well as overall market risk. Accordingly, potential unrealized gains and losses from foreign investment transactions may be affected by fluctuations in foreign exchange rates. Such fluctuations are included in the net realized and unrealized gain or loss from investments. Net unrealized foreign currency losses of $588,086 were included in net unrealized depreciation on investments at September 30, 2008.

Securities and bank debt of foreign companies and foreign governments may involve special risks and considerations not typically associated with investing in U.S. companies and securities of the U.S. government. These risks include, among other things, revaluation of currencies, less reliable information about issuers, different transactions clearance and settlement practices, and potential future adverse political and economic developments. Moreover, securities and bank debt of some foreign companies and foreign governments and their markets may be less liquid and their prices more volatile than those of comparable U.S. companies and the U.S. government.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

2. Summary of Significant Accounting Policies (continued)

Derivatives

In order to mitigate certain currency exchange and interest rate risks associated with foreign currency denominated investments, the Company has entered into several swaps and currency forward transactions. The Company recognizes all derivatives as either assets or liabilities in the Statement of Assets and Liabilities. The transactions entered into are accounted for using the mark-to-market method with the resulting change in fair value recognized in earnings for the current year.

Debt Issuance Costs

Costs of $2.4 million were incurred in connection with placing the Company’s Senior Facility. These costs were deferred and were being amortized on a straight-line basis over eight years, the estimated life of the Senior Facility. The impact of utilizing the straight-line amortization method versus the effective-interest method was not material to the Company’s operations. On October 1, 2008, in accordance with the Company’s adoption of FASB Statement No. 159, The Fair Value Option for Financial Assets and Financial Liabilities, all remaining debt issuance costs were written off.

Purchase Discounts

The majority of the Company’s high yield and distressed debt investments are purchased at a considerable discount to par as a result of the underlying credit risks and financial results of the issuer and by general market factors that influence the financial markets as a whole. GAAP require that discounts on corporate (investment grade) bonds, municipal bonds and treasury bonds be amortized using the effective-interest or constant-yield method. The process of accreting the purchase discount of a debt investment to par over the holding period results in accounting entries that increase the cost basis of the investment and record a noncash income accrual to the statement of operations. The Company considers it prudent to follow GAAP guidance that requires the Investment Manager to consider the collectibility of interest when making accruals. AICPA Statement of Position 93-1 discusses financial accounting and reporting for high yield debt investments and notes for which, because of the credit risks associated with high yield and distressed debt investments, income recognition must be carefully considered and constantly evaluated for collectibility.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

2. Summary of Significant Accounting Policies (continued)

Accordingly, when accounting for purchase discounts, management recognizes discount accretion income when it is probable that such amounts will be collected and when such amounts can be estimated. A reclassification entry is recorded upon disposition to reflect purchase discounts on all realized investments. For income tax purposes, the economic gain resulting from the sale of debt investments purchased at a discount is allocated between interest income and realized gains.

Distributions to Common Shareholders

Distributions to common shareholders are recorded on the ex-dividend date. The amount to be paid out as a distribution is determined by the Board of Directors, which has provided the Investment Manager with criteria for such distributions, and is generally based upon estimated taxable earnings. Net realized capital gains are distributed at least annually. As of September 30, 2008, the Company had distributed $115,960,000 since inception.

Income Taxes

The Company intends to comply with the applicable provisions of the Internal Revenue Code of 1986, as amended, pertaining to regulated investment companies and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes. Accordingly, no provision for income taxes is required in the financial statements. As of September 30, 2008, all tax years beginning October 1, 2004 remain subject to examination by federal and state tax authorities. No such examinations are currently pending.

Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from accounting principles generally accepted in the United States. Capital accounts within the financial statements are adjusted at year end for any permanent book and tax differences. These adjustments have no impact on net assets or the results of operations. Temporary differences are attributable to differing book and tax treatments for the timing of the recognition of gains and losses on certain investment transactions and the timing of the deductibility of certain expenses, and will reverse in subsequent periods.

Cost and unrealized appreciation (depreciation) for U.S. federal income tax purposes of the investments of the Company at September 30, 2008 were as follows:

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

2. Summary of Significant Accounting Policies (continued)

| Unrealized appreciation | | $ | 26,598,289 | |

| Unrealized depreciation | | | (78,847,218 | ) |

| Net unrealized depreciation | | $ | (52,248,929 | ) |

| | | | | |

| Cost | | $ | 462,463,374 | |

The tax character of distributions paid during the years ended September 30, 2008 and 2007 was as follows:

| | | 2008 | | 2007 | |

| Common distributions: | | | | | | | |

| Ordinary income | | $ | 33,000,000 | | $ | 22,247,602 | |

| Long-term capital gains | | | - | | | 21,728,787 | |

| Returns of capital | | | - | | | 2,906,778 | |

| Total common distributions | | $ | 33,000,000 | | $ | 46,883,167 | |

| | | | | | | | |

| Preferred distributions: | | | | | | | |

| Ordinary income | | $ | 6,318,235 | | $ | 2,668,326 | |

| Long-term capital gains | | | - | | | 2,606,098 | |

| Total preferred distributions | | $ | 6,318,235 | | $ | 5,274,424 | |

Undistributed ordinary income and capital gains as of September 30, 2008 were $309,362 and $1,475,648, respectively. Post-October capital losses of $13,417,884 have been deferred to the following tax year.

Use of Estimates

The preparation of the financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements as well as the reported amounts of revenues and expenses during the reporting period. Although management believes these estimates and assumptions to be reasonable and accurate, actual results could differ from those estimates.

Recently Issued Accounting Pronouncements

In September 2006, the FASB issued SFAS No. 157, Fair Value Measurements, which defines fair value, establishes a framework for measuring fair value in generally accepted accounting principles and expands disclosures about fair value measurements. SFAS No. 157 does not require any new fair value measurements, but provides guidance on how to measure fair value by providing a fair value hierarchy used to classify the source of the information. This statement became effective for the Company on October 1, 2008. The adoption of SFAS No. 157 did not have a significant impact on the Company’s financial statements.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

2. Summary of Significant Accounting Policies (continued)

In February 2007, the FASB issued SFAS No. 159, The Fair Value Option for Financial Assets and Financial Liabilities, which permits entities to choose to measure many financial instruments and certain other items at fair value. The FASB’s stated objective of the statement is to improve financial reporting by providing entities with the opportunity to mitigate volatility in reported earnings caused by measuring related assets and liabilities differently without having to apply complex hedge accounting provisions. The Company elected to adopt SFAS No. 159 with regards to its credit facility effective October 1, 2008. The adoption resulted in a recognition on October 1, 2008 of approximately $17 million in unrealized gains on the Company’s credit facility, offset in part by the simultaneous write-off of the Company’s remaining deferred debt issuance costs of approximately $1.2 million. This net gain will be reflected in the financial statements for periods that include that date, as adjusted for subsequent changes during the respective period.

3. Distributions and Performance Fees

As a performance fee, the Investment Manager receives an amount equal to 20% of distributions of net income and gain (gross of performance fees) after cumulative distributions to common shareholders in an amount equal to a 12% annual weighted-average return on common shareholders’ undistributed contributed equity, and a subsequent catch-up payment to the Investment Manager until cumulative performance fee payments equal 20% of cumulative income and gain distributions (gross of performance fees).

The timing of distributions is determined by the Board of Directors, which has provided the Investment Manager with certain criteria for such distributions. Performance fees payable to the Investment Manager are accrued in accordance with the manner used to determine distributions as specified above. During the year ended September 30, 2008, the Company paid $1,126,724 in performance fees to the Investment Manager, and accrued performance fees were reduced by an additional $2,328,293 adjustment as reflected in the Statement of Operations.

The APS dividend rates were determined by auction at periodic intervals until regular auctions ceased in September of 2008. Following the cessation of regular auctions, rates are determined as specified under such circumstances in the Statement of Preferences for the APS. APS rates averaged 6.09% during the year ended September 30, 2008.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

3. Distributions and Performance Fees (continued)

The Series Z share dividend rate is fixed at 8% per annum.

4. Management Fees and Other Expenses

The Company incurs an annual management and advisory fee, payable to the Investment Manager monthly in arrears, equal to 0.60% of the sum of the total common shareholder commitments and the APS and debt potentially issuable in respect of such common commitments, subject to reduction by the amount of the debt when no facility is outstanding and the amount of the APS when less than $1 million in liquidation value of preferred stock is outstanding. For purposes of computing the management fee, total committed capital during the year ended September 30, 2008 was $600 million, consisting of $300 million of capital committed by investors to purchase the Company’s common shares, $100 million of APS and $200 million of debt. In addition, the Investment Manager is entitled to a performance fee as discussed in Note 3, above.

The Company pays all expenses incurred in connection with the business of the Company, including fees and expenses of outside contracted services, such as custodian, trustee, administrative, legal, audit and tax preparation fees, costs of valuing investments, insurance costs, brokers’ and finders’ fees relating to investments and any other transaction costs associated with the purchase and sale of investments of the Company.

5. Senior Secured Revolving Credit Facility

The Company has entered into a credit agreement with certain lenders, which provides for a senior secured revolving credit facility (“Senior Facility”). The Senior Facility is a revolving extendible credit facility pursuant to which amounts may be drawn up to $200 million. The Senior Facility matures November 17, 2012, subject to extension by the lenders at the request of the Company for one 12-month period.

Advances under the Senior Facility bear interest at either (i) the Eurodollar Rate or Commercial Paper Rate plus 0.43% per annum; or (ii) the higher of (x) the “Prime Rate” plus 0.43% per annum and (y) the “Federal Funds Effective Rate,” plus 0.50% per annum. Additionally, advances under the swingline facility bear interest at either the Eurodollar Rate or Commercial Paper Rate plus 0.43% per annum.

In addition to amounts due on outstanding debt, the Senior Facility accrues commitment fees of 0.30% per annum on the Senior Facility, or $2,208 per day when the outstanding borrowings are less than $150,000,000, subject to certain ramp-up provisions.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

6. Commitments, Concentration of Credit Risk and Off-Balance Sheet Risk

The Company conducts business with brokers and dealers that are primarily headquartered in New York and Los Angeles and are members of the major securities exchanges. Banking activities are conducted with a firm headquartered in the New York area.

In the normal course of business, the Company’s investment activities involve executions, settlement and financing of various investment transactions resulting in receivables from, and payables to, brokers, dealers, and the Company’s custodian. These activities may expose the Company to risk in the event such parties are unable to fulfill contractual obligations. Management does not anticipate any material losses from counterparties with whom it conducts business.

The Statement of Investments may include certain unfunded or partially funded loan commitments. These commitments are reflected at fair value and may be drawn up to the principal amount shown.

Consistent with standard business practice, the Company enters into contracts that contain a variety of indemnifications. The Company’s maximum exposure under these arrangements is unknown. However, the Company expects the risk of loss to be remote.

7. Preferred Capital

In addition to the APS capital described in Note 1, the Company had one Series S preferred share authorized but unissued and 312 Series Z preferred shares authorized, issued and outstanding as of September 30, 2008.

Series S Preferred Share

The Company had issued, at inception, one share of its Series S preferred shares to SVOF/MM, LLC, having a liquidation preference of $1,000 plus accumulated but unpaid dividends. SVOF/MM, LLC is controlled by the Investment Manager and owned substantially entirely by the Investment Manager and certain affiliates. On May 9, 2005, the Series S preferred share was retired and assumed the status of an authorized but unissued share. Prior to retirement, the Series S preferred shareholder was entitled to receive, as dividends, the amount of the performance allocation pursuant to Note 3, above, which is now payable to the Investment Manager as a performance fee which reduces operating income as reflected in the Statement of Operations. The retirement of the Series S preferred share had no impact on any shareholder other than the Series S preferred shareholder.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

7. Preferred Capital (continued)

Series Z Preferred Shares

The Company issued 312 shares of its Series Z preferred shares, having a liquidation preference of $500 per share plus accumulated but unpaid dividends and paying dividends at an annual rate equal to 8% of liquidation preference. The Series Z preferred shares rank on par with the APS with respect to the payment of dividends and distribution of amounts on liquidation and vote with the APS as a single class. The Series Z preferred shares are redeemable at any time at the option of the Company and may only be transferred with the consent of the Company.

Special Value Expansion Fund, LLC

(A Delaware Limited Liability Company)

Notes to Financial Statements (Continued)

September 30, 2008

8. Financial Highlights

| | | | | | Period from | |

| | | | | | September 1 to | |

| | | Year Ended September 30, | | | September 30, | |

| | | 2008 | | | 2007 | | | 2006 | | | 2005 | | | 2004 | |

| | | | | | | | | | | | | | | | |

Per Common Share(1) | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | | $ | 572.71 | | | $ | 574.80 | | | $ | 550.96 | | | $ | 509.44 | | | $ | 499.43 | |

| | | | | | | | | | | | | | | | | | | | | |

| Investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | | 81.61 | | | | 42.84 | | | | 50.20 | | | | 8.43 | | | | (2.65 | ) |

| Net realized and unrealized gain (loss) | | | (157.02 | ) | | | 50.99 | | | | 54.11 | | | | 79.06 | | | | 14.52 | |

| Distributions to preferred shareholders from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (11.56 | ) | | | (3.26 | ) | | | (7.23 | ) | | | (2.92 | ) | | | - | |

| Realized gains | | | - | | | | (6.39 | ) | | | (1.71 | ) | | | (1.34 | ) | | | - | |

| Net change in reserve for distributions to preferred shareholders | | | 0.42 | | | | (0.52 | ) | | | (0.56 | ) | | | (1.16 | ) | | | (1.86 | ) |

| Total from investment operations | | | (86.55 | ) | | | 83.66 | | | | 94.81 | | | | 82.07 | | | | 10.01 | |

| | | | | | | | | | | | | | | | | | | | | |

| Distributions to common shareholders from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | (60.36 | ) | | | (27.17 | ) | | | (55.75 | ) | | | (22.71 | ) | | | - | |

| Net realized gains on investments | | | - | | | | (53.26 | ) | | | (15.22 | ) | | | (10.41 | ) | | | - | |

| Returns of capital | | | - | | | | (5.32 | ) | | | - | | | | - | | | | - | |

| Total distributions to common shareholders | | | (60.36 | ) | | | (85.75 | ) | | | (70.97 | ) | | | (33.12 | ) | | | - | |