UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21666

Hatteras Master Fund, L.P.

(Exact name of registrant as specified in charter)

8540 Colonnade Center Drive, Suite 401

Raleigh, North Carolina 27615

(Address of principal executive offices) (Zip code)

David B. Perkins

8540 Colonnade Center Drive, Suite 401

Raleigh, North Carolina 27615

(Name and address of agent for service)

Registrant’s telephone number, including area code: (919) 846-2324

Date of fiscal year end: March 31

Date of reporting period: March 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

The Report to Shareholders is attached herewith.

LETTERFROMTHE PRESIDENT

Robert L. Worthington, CFA

On behalf of Hatteras Funds, I would like to thank our investors for the confidence you place in us to help manage your investment dollars. We take our fiduciary responsibilities seriously and will continue to put forth our greatest efforts to meet the investment objectives outlined to you and your financial advisors.

This past fiscal year was one characterized by lower volatility and a lack of a true equity market correction like 2010 and 2011, together with a fairly unabated rise in the markets that started in the fourth quarter of 2012. The markets were heavily influenced in the first six months by political headlines from tightly contested pre-election polls, the reelection of President Obama and congressional negotiations over the self-created and looming “fiscal cliff.” Afterwards an improving US economy, together with the positive impact of European Central Bank President Draghi stating to do whatever is necessary to save the Euro contributed to the strong rise in equity and fixed income markets during the latter part of 2012 and first part of 2013. All this while many market indicators signaled a slow growth economy domestically, and a stagnant economy in Europe and much of the developed world. Regardless of these signals, international equities posted strong returns with the ECB’s support lessening European debt crisis worries, China’s GDP growth exceeding expectations and more quantitative easing in Japan. Fixed income markets produced positive returns as strong investor demand pushed corporate yields to near record lows.

The hedge fund industry produced modest returns during the year as many managers positioned portfolios conservatively due to global macro issues.

In the latter part of the year as global macro worries subsided a little, there was a pickup in corporate activity, including mergers and acquisitions, which helped Event Driven strategies produce some of the best returns among hedge fund strategies. Credit strategies and specifically corporate credit strategies were some of the best performers this past year as corporate spreads tightened throughout much of the year due to investors searching for higher yield. However, as a whole, hedged strategies continued to lag the returns of an exuberant S&P 500, which posted significant gains yet again. For alternative strategies, the silver lining of the strong rally in the markets we believe will be the exit opportunities for private equity investments. As companies, flush with cash, look to grow their revenues, purchasing established lines of business could be an easy answer, and therefore provide ample exit opportunity for private equity funds.

Even in these challenging times, ensuring that our portfolio and risk management efforts exceed your expectations is a commitment that never wavers. We appreciate the confidence you have placed in Hatteras and your investment in the Hatteras Core Alternatives Fund. In closing, we feel positive about the future of our organization and we will continue to strive to deliver the risk- adjusted returns outlined in our investment objectives. We thank you for your continued confidence and support.

Robert L. Worthington, CFA

President

MANAGERS DISCUSSIONOF FUND PERFORMANCE

Mark W. Yusko

The Hatteras Core Alternatives Institutional Fund, L.P. (the “Fund”) finished the fiscal year up 4.87%, outperforming its benchmark, the HFRX Global Hedge Fund Index, which finished with a 3.50% return over the same period. The outperformance over the benchmark was driven largely from the Fund’s private investment strategy which was up 11.50% for the year. We continue to believe that our single greatest opportunity today is our maturing Private Investment strategy finding exits in today’s capital markets where valuations have greatly increased and stifling amounts of cash are waiting to be deployed. We believe that in this low GDP growth environment companies will look to take away market share from competitors pushing cash rich companies into the private markets to grow their business through acquisitions and build for the future.

In the broader markets, concerns around Europe manifested during the year but significant injections

of liquidity from the central banks managed to keep equity market valuations elevated despite problems with Greece, Spain, Italy and most recently, Cypress during the year. Domestically, while the year passed without any fiscal cliff related economic blow-up, the underlying fundamental debt problems remain. Economic indicators continue to show growing signs of improvement, but we seem trapped in a global environment of relatively slow growth for the foreseeable future. While central banks helped equity markets across the globe produce mid-teen returns in 2012, a return to a more fundamental market seems inevitable, as the impact of government stimulation on stock prices continues to wane. All of this market intervention and liquidity will come at a price, and as such we are expecting a reflationary environment for commodities in the long-run but this may take time given the continuing “currency war” pressures that have forced recent dollar appreciation and corresponding commodity weakness.

STRATEGY COMMENTARY

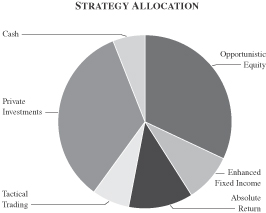

Private Investments

The Private Investment portfolio produced another double digit return for the year, and has an average annual return over 10% for the past three years, further demonstrating the overall maturity of the strategy. As previously mentioned the private investment strategy finished the fiscal year with a return of 11.50%, and a 34% weighting of the overall fund. The story for the year was definitely the robust performance of our Private Energy strategy that

posted significant gains and we are eagerly awaiting the potential for distributions from this sector in the very near future.

We recently conducted an exhaustive study through manager by manager conversations to determine upcoming liquidity events within the Private portfolio for the coming year. We were excited to see that we finished the year with distributions ($84.4M) slightly ahead of capital calls ($80.0M)* and based on our

| * | Distributions include cash distributions from private investment funds, secondary transactions and net transfers between investment strategies. |

ONE

manager conversations, we are anticipating realizations over the next six quarters that we believe may continue to outpace capital calls for the foreseeable future.

Illustrating where we are in our own life cycle is the percentage of capital that has been funded from our commitments. When the level is below 50%, a private equity program is in its “growth phase” and there is a significant distance from an active period for exits. In our experience, when greater than 65% is funded, you are entering a “mature phase” where distributions start to accelerate. Calls exceeding 80% of committed capital suggest a portfolio nearing the realization stage. The Core Alternatives Fund had a total funded ratio of 85.1% at the end of the fiscal year.

Our multi-vintage year program for private investments is entering a maturity phase at a time when capital markets appear increasingly receptive. We believe this confluence of events could be conducive for the Fund to achieve its investment objectives and also to help the Fund maintain its balance with our more liquid Hedge Fund strategy as Private Investment funds potentially exit underlying companies. Barring additional fiscal cliff concerns seizing the markets we believe much of the next year will be dominated by activity from this part of our portfolio. We are excited about the potential in the private portfolio as the private strategy continues to be the Fund’s differentiator in the market.

Hedge Fund Strategies

Our Hedge Fund Strategy was up +2.36% during the fiscal year. Enhanced Fixed Income and Absolute Return were our best performing strategies for the year while Tactical Trading was the biggest detractor.

A prominent focus over the past year was to improve the hedge fund lineup and we took significant steps to concentrate this area of the portfolio. During the

year, we allocated to 14 funds while redeeming 35. With this new emphasis on concentration, we plan to have a much heavier concentration of our managers with the biggest conviction. We hope to have 60% of the total fund assets invested in no more than 30 funds by the end of 2013. As of the fiscal year-end, the thirty largest funds represent 50.6% of the Fund’s assets.

Opportunistic Equity

Opportunistic Equity ended the year with a 34% weight and returned 0.31% for the year. Within the strategy, our best performing sub-strategy was the Financials category as global financials bounced back dramatically after a very difficult 2011. Overall, we had fairly mixed performance from our sector specialists as Healthcare and Financials had decent returns but performance from our Energy specialists significantly detracted due to losses from gold-mining

equity positions. Technology specialists also lagged as the market proved to be a challenging space for the smaller cap names that hedge funds typically specialize. In terms of our geographic focused managers, our Domestic Equity and Developed Asia managers were our best performing funds and averaged double digit returns. Global Long/Short and Emerging Market posted modest gains.

Enhanced Fixed Income

Enhanced Fixed Income finished the year at a 9% weight and posted solid gains for the year, +8.93%. We diversified away dramatically from Enhanced Fixed Income during the course of the year and cut our position nearly in half from the beginning of the year as we were concerned about a growing bond bubble and another credit crisis stemming from Europe and the US fiscal cliff. In retrospect, the dramatic reduction in our Enhanced Fixed Income allocation proved to be ill timed as credit strategies

proved to be some of the best performing of all hedge fund strategies during the year and accordingly, Structured Credit was our best performer within Enhanced Fixed Income. All of the other underlying sub-strategies posted strong gains for the year. We maintain a cautious approach to the space given the recent valuations but we are looking to increasingly concentrate our allocations within Enhanced Fixed Income, particularly with more idiosyncratic niche managers that take more of a relative value approach.

TWO

Absolute Return

Absolute Return was up 5.66% for the year and the allocation increased slightly during the year to a 13% weighting at year-end. Our Multi-Strategy managers delivered consistent positive returns throughout the quarter and the year. These managers are some of most reputable on Wall Street and they have done a

remarkable job utilizing leverage prudently to trade with a market neutral approach while consistently adding alpha. We added some new names to this strategy during the year but as we further concentrate the portfolio we expect to only have a handful of primary positions in this strategy going forward.

Tactical Trading

Tactical Trading, which incorporates managed futures, Commodity Trading Advisors (“CTAs”), global macro and tail risk managers, had the lowest allocation amongst our strategies at 6% and was the worst performing strategy for the Fund during year finishing down -6.15%. Tactical Trading remains a key liquid diversifier for the rest of the Fund’s portfolio while the strategy proved its worth during the market dislocation in May of 2012, the corresponding Central Bank interventions caused significant losses in the credit default swap (CDS) positions within our Tail Risk managers. Our global macro managers did post sizable gains during the year that helped offset some of the pain suffered from Tail Risk positions and the net short discretionary commodity CTAs. While robust risk-on periods drive returns elsewhere in the portfolio, we believe that the potential benefits of negative correlation that Tactical Trading adds will prove to be a prudent allocation if volatility spikes reappear.

In addition to concentrating the overall hedge fund portfolio, we have been looking for better ways to implement our short term views and themes in the Tactical Trading strategy and we will be looking to add more liquid solutions going forward.

As always, we appreciate the confidence you have placed in Hatteras and your investment in the Hatteras Core Alternatives Fund. Thank you again, and if you have any questions please do not hesitate to contact us.

Mark W. Yusko

THREE

PERFORMANCE SUMMARY1 (UNAUDITED)

HATTERAS CORE ALTERNATIVES FUND, L.P. (INCEPTIONDATE: APRIL 1, 2005)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year | | Jan | | Feb | | Mar | | Apr | | May | | Jun | | Jul | | Aug | | Sep | | Oct | | Nov | | Dec | | Year2 |

2013 | | 1.16% | | -0.03% | | 0.54% | | | | | | | | | | | | | | | | | | | | 1.68% |

2012 | | 1.96% | | 0.89% | | -0.18% | | 0.07% | | -0.58% | | 0.01% | | 0.50% | | 0.74% | | 0.64% | | -0.04% | | 0.08% | | 0.94% | | 5.10% |

2011 | | 0.41% | | 1.09% | | 0.69% | | 0.83% | | -0.22% | | -0.79% | | 0.19% | | -2.37% | | -3.27% | | 1.02% | | -0.96% | | -0.56% | | -3.97% |

2010 | | -0.30% | | 0.06% | | 1.72% | | 0.94% | | -2.63% | | -1.13% | | 0.34% | | -0.11% | | 2.29% | | 1.30% | | 0.28% | | 2.31% | | 5.06% |

2009 | | 0.17% | | -0.43% | | -0.50% | | 0.49% | | 3.69% | | 0.79% | | 2.20% | | 1.20% | | 2.39% | | 0.11% | | 0.85% | | 0.95% | | 12.50% |

2008 | | -2.89% | | 1.86% | | -2.88% | | 1.57% | | 2.10% | | -0.48% | | -2.84% | | -1.53% | | -8.28% | | -7.54% | | -4.29% | | -1.01% | | -23.79% |

2007 | | 0.97% | | 0.67% | | 1.60% | | 1.86% | | 2.01% | | 0.78% | | -0.05% | | -1.85% | | 1.93% | | 2.71% | | -1.72% | | 0.92% | | 10.16% |

2006 | | 2.80% | | -0.20% | | 1.74% | | 1.10% | | -1.97% | | -0.75% | | 0.37% | | 0.76% | | 0.26% | | 1.60% | | 2.09% | | 0.93% | | 8.98% |

2005 | | | | | | | | -1.54% | | 0.26% | | 1.46% | | 2.16% | | 0.48% | | 1.39% | | -1.46% | | 1.35% | | 1.85% | | 6.04% |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Returns | | Fund | | | S&P 5003 | | | HFRXGL3 | | | | | Historical Data

(since inception) | | Fund | | | S&P 5003 | | | HFRXGL3 | |

Year-to-date | | | 1.68 | % | | | 10.61 | % | | | 3.13 | % | | | | Cumulative Return | | | 17.67 | % | | | 57.31 | % | | | 5.28 | % |

1-Year | | | 4.09 | % | | | 13.96 | % | | | 3.50 | % | | | | Standard Deviation4 | | | 6.52 | % | | | 15.82 | % | | | 6.53 | % |

3-Year (annualized) | | | 2.04 | % | | | 12.67 | % | | | 0.23 | % | | | | Largest Drawdown5 | | | -24.98 | % | | | -50.95 | % | | | -25.21 | % |

5-Year (annualized) | | | -0.77 | % | | | 5.81 | % | | | -1.74 | % | | | | Drawdown — # of months6 | | | 17 | | | | 16 | | | | 14 | |

Annualized Since Inception | | | 2.06 | % | | | 5.83 | % | | | 0.65 | % | | | | | | | | | | | | | | | | |

HATTERAS CORE ALTERNATIVES TEI FUND, L.P. (INCEPTIONDATE: APRIL 1, 2005)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year | | Jan | | Feb | | Mar | | Apr | | May | | Jun | | Jul | | Aug | | Sep | | Oct | | Nov | | Dec | | Year2 |

2013 | | 1.15% | | -0.04% | | 0.48% | | | | | | | | | | | | | | | | | | | | 1.60% |

2012 | | 1.94% | | 0.88% | | -0.20% | | 0.06% | | -0.59% | | 0.00% | | 0.49% | | 0.73% | | 0.63% | | -0.05% | | 0.08% | | 0.93% | | 4.99% |

2011 | | 0.41% | | 1.09% | | 0.68% | | 0.83% | | -0.22% | | -0.79% | | 0.19% | | -2.37% | | -3.28% | | 1.01% | | -0.96% | | -0.59% | | -4.02% |

2010 | | -0.34% | | 0.06% | | 1.72% | | 0.94% | | -2.63% | | -1.12% | | 0.35% | | -0.12% | | 2.27% | | 1.28% | | 0.26% | | 2.29% | | 4.95% |

2009 | | 0.16% | | -0.44% | | -0.50% | | 0.47% | | 3.71% | | 0.79% | | 2.19% | | 1.20% | | 2.39% | | 0.11% | | 0.85% | | 0.95% | | 12.48% |

2008 | | -2.95% | | 1.82% | | -2.92% | | 1.53% | | 2.08% | | -0.52% | | -2.88% | | -1.57% | | -8.33% | | -7.56% | | -4.31% | | -0.86% | | -23.98% |

2007 | | 0.94% | | 0.64% | | 1.58% | | 1.83% | | 1.99% | | 0.75% | | -0.07% | | -1.88% | | 1.89% | | 2.68% | | -1.74% | | 0.87% | | 9.79% |

2006 | | 2.77% | | -0.20% | | 1.72% | | 1.09% | | -1.98% | | -0.75% | | 0.37% | | 0.72% | | 0.23% | | 1.57% | | 2.05% | | 0.90% | | 8.73% |

2005 | | | | | | | | -1.54% | | 0.26% | | 1.46% | | 2.16% | | 0.48% | | 1.39% | | -1.46% | | 1.32% | | 1.82% | | 5.97% |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Returns | | Fund | | | S&P 5003 | | | HFRXGL3 | | | | | Historical Data

(since inception) | | Fund | | | S&P 5003 | | | HFRXGL3 | |

Year-to-date | | | 1.60% | | | | 10.61% | | | | 3.13% | | | | | Cumulative Return | | | 16.22% | | | | 57.31% | | | | 5.28% | |

1-Year | | | 3.93% | | | | 13.96% | | | | 3.50% | | | | | Standard Deviation4 | | | 6.53% | | | | 15.82% | | | | 6.53% | |

3-Year (annualized) | | | 1.94% | | | | 12.67% | | | | 0.23% | | | | | Largest Drawdown5 | | | -25.23% | | | | -50.95% | | | | -25.21% | |

5-Year (annualized) | | | -0.86% | | | | 5.81% | | | | -1.74% | | | | | Drawdown — # of months6 | | | 17 | | | | 16 | | | | 14 | |

Annualized Since Inception | | | 1.90% | | | | 5.83% | | | | 0.65% | | | | | | | | | | | | | | | | | |

| 1. | Performance results and calculations after the Funds’ most recent fiscal year are unaudited. The principal value of the Funds will fluctuate so that an investor’s units, when redeemed, may be worth more or less than the original cost. Returns are net of all expenses of the Funds, including the management fee and incentive allocations, and reflect reinvestment of all distributions, if applicable. Returns do not reflect payment of the 2% redemption fee or up-front placement fees, which could be up to 2%, which would reduce returns shown above. Past performance does not guarantee future results and current performance may be lower or higher than the figures shown. The net expense ratio and total expense ratio for the Hatteras Core Alternatives Fund, L.P. are 2.30% and 7.69%, respectively. The next expense ratio and total expense ratio for the Hatteras Core Alternatives TEI Fund, L.P. are 2.38% and 7.79%, respectively. The total expense ratio for both funds includes Acquired Fund Fees and Expenses of 5.36%. The Investment Manager has contractually agreed to waive fees and/or reimburse certain expenses through July 31, 2013 so that the total annual expenses will not exceed 2.35%. Please see the current Prospectus for detailed information regarding the expenses of the Funds. |

| 2. | Cumulative Return. Returns are net of all expenses of the Funds, including the management fee and incentive allocations, and reflect reinvestment of all distributions, if applicable. Returns do not reflect payment of placement fees, if applicable, which would reduce returns noted above. |

| 3. | S&P 500 Index and HFRX Global Hedge Fund Index (HFRXGL) data are sourced from Bloomberg. The indices are unmanaged portfolios of securities. Their performance results do not reflect the deduction of management fees, incentive compensation, commissions or other expenses. An investor cannot invest directly in an index. The S&P 500 Index consists of 500 stocks chosen for market size, liquidity and industry group representation. It is a market value weighted index, with each stock’s weight in the Index proportionate to its market value. HFRXGL is designed to be representative of the overall composition of the hedge fund universe. It is comprised of eight strategies: convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry. |

| 4. | Measurement of the investment’s volatility. |

| 5. | The peak to trough decline of an investment. |

| 6. | Number of months of a peak to trough decline of an investment. |

FOUR

PERFORMANCE SUMMARY1 (UNAUDITED)

HATTERAS CORE ALTERNATIVES INSTITUTIONAL FUND, L.P. (INCEPTIONDATE: JANUARY 1, 2007)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year | | Jan | | Feb | | Mar | | Apr | | May | | Jun | | Jul | | Aug | | Sep | | Oct | | Nov | | Dec | | Year2 |

2013 | | 1.23% | | 0.03% | | 0.59% | | | | | | | | | | | | | | | | | | | | 1.85% |

2012 | | 2.03% | | 0.96% | | -0.12% | | 0.13% | | -0.52% | | 0.07% | | 0.56% | | 0.80% | | 0.70% | | 0.02% | | 0.15% | | 1.00% | | 5.92% |

2011 | | 0.47% | | 1.15% | | 0.75% | | 0.89% | | -0.16% | | -0.72% | | 0.25% | | -2.31% | | -3.20% | | 1.09% | | -0.89% | | -0.50% | | -3.23% |

2010 | | -0.24% | | 0.12% | | 1.78% | | 1.01% | | -2.57% | | -1.06% | | 0.41% | | -0.04% | | 2.36% | | 1.36% | | 0.34% | | 2.37% | | 5.89% |

2009 | | 0.24% | | -0.36% | | -0.45% | | 0.55% | | 3.75% | | 0.86% | | 2.27% | | 1.27% | | 2.46% | | 0.17% | | 0.91% | | 1.01% | | 13.35% |

2008 | | -2.85% | | 1.91% | | -2.81% | | 1.63% | | 2.14% | | -0.42% | | -2.78% | | -1.47% | | -8.22% | | -7.50% | | -4.23% | | -0.94% | | -23.27% |

2007 | | 1.12% | | 0.73% | | 1.65% | | 1.89% | | 2.06% | | 0.82% | | 0.00% | | -1.89% | | 2.00% | | 2.75% | | -1.71% | | 0.97% | | 10.76% |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Returns | | Fund | | | S&P 5003 | | | HFRXGL3 | | | | | Historical Data

(since inception) | | Fund | | | S&P 5003 | | | HFRXGL3 | |

Year-to-date | | | 1.85% | | | | 10.61% | | | | 3.13% | | | | | Cumulative Return | | | 6.50% | | | | 26.71% | | | | -7.17% | |

1-Year | | | 4.87% | | | | 13.96% | | | | 3.50% | | | | | Standard Deviation4 | | | 6.94% | | | | 17.57% | | | | 6.98% | |

3-Year (annualized) | | | 2.83% | | | | 12.67% | | | | 0.23% | | | | | Largest Drawdown5 | | | -24.29% | | | | -50.95% | | | | -25.21% | |

5-Year (annualized) | | | -0.01% | | | | 5.81% | | | | -1.74% | | | | | Drawdown — # of months6 | | | 17 | | | | 16 | | | | 14 | |

Annualized Since Inception | | | 1.01% | | | | 3.86% | | | | -1.18% | | | | | | | | | | | | | | | | | |

HATTERAS CORE ALTERNATIVES TEI INSTITUTIONAL FUND, L.P. (INCEPTIONDATE: FEBRUARY 1, 2007)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year | | Jan | | Feb | | Mar | | Apr | | May | | Jun | | Jul | | Aug | | Sep | | Oct | | Nov | | Dec | | Year2 |

2013 | | 1.10% | | 0.03% | | 0.47% | | | | | | | | | | | | | | | | | | | | 1.60% |

2012 | | 2.01% | | 0.94% | | -0.13% | | 0.13% | | -0.52% | | 0.07% | | 0.56% | | 0.80% | | 0.70% | | 0.02% | | 0.14% | | 1.00% | | 5.85% |

2011 | | 0.48% | | 1.16% | | 0.69% | | 0.81% | | -0.14% | | -0.65% | | 0.23% | | -2.24% | | -3.21% | | 1.07% | | -0.91% | | -0.51% | | -3.26% |

2010 | | -0.23% | | 0.13% | | 1.79% | | 1.01% | | -2.56% | | -1.06% | | 0.42% | | -0.05% | | 2.34% | | 1.35% | | 0.33% | | 2.36% | | 5.88% |

2009 | | 0.24% | | -0.36% | | -0.43% | | 0.54% | | 3.74% | | 0.85% | | 2.26% | | 1.27% | | 2.46% | | 0.18% | | 0.92% | | 1.02% | | 13.37% |

2008 | | -2.87% | | 1.87% | | -2.83% | | 1.59% | | 2.09% | | -0.44% | | -2.82% | | -1.50% | | -8.26% | | -7.51% | | -4.24% | | -0.91% | | -23.48% |

2007 | | | | 0.71% | | 1.62% | | 1.87% | | 2.03% | | 0.80% | | -0.04% | | -1.95% | | 2.01% | | 2.72% | | -1.76% | | 0.96% | | 9.23% |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Returns | | Fund | | | S&P 5003 | | | HFRXGL3 | | | | | Historical Data

(since inception) | | Fund | | | S&P 5003 | | | HFRXGL3 | |

Year-to-date | | | 1.60% | | | | 10.61% | | | | 3.13% | | | | | Cumulative Return | | | 4.38% | | | | 24.82% | | | | -8.54% | |

1-Year | | | 4.58% | | | | 13.96% | | | | 3.50% | | | | | Standard Deviation4 | | | 6.97% | | | | 17.68% | | | | 6.99% | |

3-Year (annualized) | | | 2.70% | | | | 12.67% | | | | 0.23% | | | | | Largest Drawdown5 | | | -24.53% | | | | -50.95% | | | | -25.21% | |

5-Year (annualized) | | | -0.12% | | | | 5.81% | | | | -1.74% | | | | | Drawdown — # of months6 | | | 17 | | | | 16 | | | | 14 | |

Annualized Since Inception | | | 0.70% | | | | 3.66% | | | | -1.44% | | | | | | | | | | | | | | | | | |

| 1. | Performance results and calculations after the Funds’ most recent fiscal year are unaudited. The principal value of the Funds will fluctuate so that an investor’s units, when redeemed, may be worth more or less than the original cost. Returns are net of all expenses of the Funds, including the management fee and incentive allocations, and reflect reinvestment of all distributions, if applicable. Returns do not reflect payment of the 2% redemption fee or up-front placement fees, which could be up to 2%, which would reduce returns shown above. Past performance does not guarantee future results and current performance may be lower or higher than the figures shown. The net expense ratio and total expense ratio for the Hatteras Core Alternatives Institutional Fund, L.P. are 1.54% and 6.91%, respectively. The next expense ratio and total expense ratio for the Hatteras Core Alternatives TEI Institutional Fund, L.P. are 1.74% and 6.98%, respectively. The total expense ratio for both funds includes Acquired Fund Fees and Expenses of 5.36%. The Investment Manager has contractually agreed to waive fees and/or reimburse certain expenses through July 31, 2013 so that total annual expenses will not exceed 1.75%. Please see the current Prospectus for detailed information regarding the expenses of the Funds. |

| 2. | Cumulative Return. Returns are net of all expenses of the Funds, including the management fee and incentive allocations, and reflect reinvestment of all distributions, if applicable. Returns do not reflect payment of placement fees, if applicable, which would reduce returns noted above. |

| 3. | S&P 500 Index and HFRX Global Hedge Fund Index (HFRXGL) data are sourced from Bloomberg. The indices are unmanaged portfolios of securities. Their performance results do not reflect the deduction of management fees, incentive compensation, commissions or other expenses. An investor cannot invest directly in an index. The S&P 500 Index consists of 500 stocks chosen for market size, liquidity and industry group representation. It is a market value weighted index, with each stock’s weight in the Index proportionate to its market value. HFRXGL is designed to be representative of the overall composition of the hedge fund universe. It is comprised of eight strategies: convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry. |

| 4. | Measurement of the investment’s volatility. |

| 5. | The peak to trough decline of an investment. |

| 6. | Number of months of a peak to trough decline of an investment. |

| 7. | Number of months to recover from a drawdown. |

FIVE

PERFORMANCE SUMMARY (UNAUDITED)

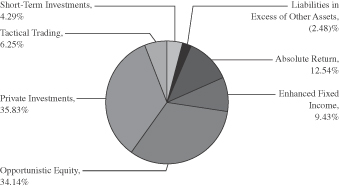

ALLOCATION

| | | | | | | | | | | | |

| Strategies | | Target

Allocation | | | Allocation

Actual* | | | # of Funds | |

Opportunistic Equity (OE) | | | 30 | % | | | 34 | % | | | 30 | |

Enhanced Fixed Income (EFI) | | | 20 | % | | | 9 | % | | | 16 | |

Absolute Return (AR) | | | 15 | % | | | 13 | % | | | 17 | |

Tactical Trading (TT) | | | 10 | % | | | 6 | % | | | 11 | |

Private Investments (PI) | | | 25 | % | | | 34 | % | | | 106 | |

Cash | | | 0 | % | | | 4 | % | | | 0 | |

Total | | | 100 | % | | | 100 | % | | | 180 | |

| | Portfolio composition will change due to ongoing management of the Fund. |

| * | Percentages are based on portfolio composition as of March 31, 2013 prior to net investor cash flows effective April 1, 2013. |

SIX

PERFORMANCE SUMMARY (UNAUDITED)

CONTRIBUTION

HATTERAS CORE ALTERNATIVES FUND, L.P. (INCEPTIONDATE: APRIL 1, 2005)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Strategy Performance1 | | Month% | | | YTD% | | | ITD%3 | | | | | Strategy Contribution2 | | Month% | | | YTD% | | | ITD%3 | |

Opportunistic Equity | | | 1.20 | | | | 2.03 | | | | 14.56 | | | | | Opportunistic Equity | | | 0.42 | | | | 0.68 | | | | 10.53 | |

Enhanced Fixed Income | | | 1.43 | | | | 3.89 | | | | 9.81 | | | | | Enhanced Fixed Income | | | 0.14 | | | | 0.38 | | | | 4.07 | |

Absolute Return | | | 0.10 | | | | 1.12 | | | | 11.55 | | | | | Absolute Return | | | 0.01 | | | | 0.14 | | | | 3.12 | |

Tactical Trading | | | 1.39 | | | | -1.10 | | | | 6.05 | | | | | Tactical Trading | | | 0.09 | | | | -0.09 | | | | -0.19 | |

Private Investments | | | -0.32 | | | | 1.64 | | | | 2.55 | | | | | Private Investments | | | -0.11 | | | | 0.56 | | | | 0.14 | |

HATTERAS CORE ALTERNATIVES TEI FUND, L.P. (INCEPTIONDATE: APRIL 1, 2005)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Strategy Performance1 | | Month% | | | YTD% | | | ITD%3 | | | | | Strategy Contribution2 | | Month% | | | YTD% | | | ITD%3 | |

Opportunistic Equity | | | 1.13 | | | | 1.95 | | | | 13.14 | | | | | Opportunistic Equity | | | 0.39 | | | | 0.65 | | | | 10.03 | |

Enhanced Fixed Income | | | 1.36 | | | | 3.81 | | | | 8.46 | | | | | Enhanced Fixed Income | | | 0.13 | | | | 0.38 | | | | 3.93 | |

Absolute Return | | | 0.03 | | | | 1.03 | | | | 10.18 | | | | | Absolute Return | | | 0.00 | | | | 0.13 | | | | 2.92 | |

Tactical Trading | | | 1.32 | | | | -1.18 | | | | 4.75 | | | | | Tactical Trading | | | 0.08 | | | | -0.10 | | | | -0.28 | |

Private Investments | | | -0.38 | | | | 1.56 | | | | 1.29 | | | | | Private Investments | | | -0.14 | | | | 0.53 | | | | -0.38 | |

HATTERAS CORE ALTERNATIVES INSTITUTIONAL FUND, L.P. (INCEPTIONDATE: JANUARY 1, 2007)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Strategy Performance1 | | Month% | | | YTD% | | | ITD%3 | | | | | Strategy Contribution2 | | Month% | | | YTD% | | | ITD%3 | |

Opportunistic Equity | | | 1.25 | | | | 2.21 | | | | -3.98 | | | | | Opportunistic Equity | | | 0.43 | | | | 0.74 | | | | -1.41 | |

Enhanced Fixed Income | | | 1.48 | | | | 4.08 | | | | 2.89 | | | | | Enhanced Fixed Income | | | 0.14 | | | | 0.40 | | | | 1.51 | |

Absolute Return | | | 0.15 | | | | 1.30 | | | | 8.96 | | | | | Absolute Return | | | 0.02 | | | | 0.17 | | | | 2.00 | |

Tactical Trading | | | 1.44 | | | | -0.92 | | | | 9.31 | | | | | Tactical Trading | | | 0.09 | | | | -0.08 | | | | 0.04 | |

Private Investments | | | -0.27 | | | | 1.83 | | | | 27.52 | | | | | Private Investments | | | -0.10 | | | | 0.63 | | | | 4.37 | |

HATTERAS CORE ALTERNATIVES TEI INSTITUTIONAL FUND, L.P. (INCEPTIONDATE: FEBRUARY 1, 2007)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

| Strategy Performance1 | | Month% | | | YTD% | | | ITD%3 | | | | | Strategy Contribution2 | | Month% | | | YTD% | | | ITD%3 | |

Opportunistic Equity | | | 1.12 | | | | 1.95 | | | | -5.53 | | | | | Opportunistic Equity | | | 0.39 | | | | 0.65 | | | | -2.12 | |

Enhanced Fixed Income | | | 1.36 | | | | 3.82 | | | | 0.69 | | | | | Enhanced Fixed Income | | | 0.13 | | | | 0.38 | | | | 1.18 | |

Absolute Return | | | 0.02 | | | | 1.04 | | | | 5.76 | | | | | Absolute Return | | | 0.00 | | | | 0.13 | | | | 1.42 | |

Tactical Trading | | | 1.32 | | | | -1.18 | | | | 7.43 | | | | | Tactical Trading | | | 0.08 | | | | -0.09 | | | | -0.08 | |

Private Investments | | | -0.39 | | | | 1.56 | | | | 25.28 | | | | | Private Investments | | | -0.14 | | | | 0.53 | | | | 3.98 | |

| 1. | Strategy Performance: The above illustration offers historical performance for each individual strategy as a composite of the actual underlying advisory funds. The historical performance shown indicates how each strategy (composite) performed on a stand-alone basis, net of all fees. However, none of the (composite) strategies shown above are offered as stand-alone investments. This is not meant to predict or project results into the future, nor is it intended to portray performance of the Fund. |

| 2. | Strategy Contribution: The above illustration attempts to break down the pro rata contribution of the six strategies of the Fund (in other words, their contribution to the Fund’s overall return) by strategy, and is intended to allocate the portion of the (past) performance that is attributable to the particular strategy. It is not meant to predict or project results into the future, nor is it intended to portray performance of the Fund. |

| 3. | ITD = Inception to date. |

SEVEN

TOP 10 HOLDINGS (UNAUDITED)

| | | | | | | | |

| | |

| | | Capital Balance,

March 31, 2013 | | | Percent of

Partners’ Capital | |

| | |

Citadel Wellington Partners LLC (Class A) | | $ | 32,002,386.30 | | | | 2.58 | % |

| | |

Bay Pond Partners, LP | | | 30,081,649.26 | | | | 2.42 | % |

| | |

Hound Partners, LP | | | 29,884,685.00 | | | | 2.41 | % |

| | |

Ashoka Fund, L.P. | | | 28,375,753.18 | | | | 2.29 | % |

| | |

Providence MBS Fund, LP | | | 28,361,189.45 | | | | 2.29 | % |

| | |

Glade Brook Global Domestic Fund, L.P. | | | 27,788,938.43 | | | | 2.24 | % |

| | |

Value Partners Hedge Fund, LLC | | | 27,278,752.21 | | | | 2.20 | % |

| | |

Tybourne Equity (US) Fund | | | 27,242,854.00 | | | | 2.20 | % |

| | |

Millennium USA LP | | | 26,734,845.33 | | | | 2.15 | % |

| | |

Broadfin Healthcare Fund, LP | | | 26,666,226.00 | | | | 2.15 | % |

Portfolio composition will change due to ongoing management of the Fund.

EIGHT

DEFINITIONS

The HFRX Global Hedge Fund Index is index data, sourced from Hedge Funds Research, Inc., is designed to be representative of the overall composition of the hedge fund universe. It is comprised of all eligible hedge fund strategies; including but not limited to convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage, and relative value arbitrage. The strategies are asset weighted based on the distribution of assets in the hedge fund industry.

Standard & Poor’s (S&P) 500 Index is an index of 500 stocks chosen for market size, liquidity, and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. Companies included in the index are selected by the S&P Index Committee, a team of analysts and economists at Standard & Poor’s. The S&P 500 is a market value weighted index — each stock’s weight in the index is proportionate to its market value.

NINE

SAFE HARBORAND FORWARD-LOOKING STATEMENTS DISCLOSURE

Safe Harbor Statement: This presentation shall not constitute an offer to sell or a solicitation of an offer to buy, nor shall there be any sale of, the securities in any state or jurisdiction in which such offer or solicitation or sale would be unlawful prior to registration or qualification under the laws of such state or jurisdiction. Forward-Looking Statements: This presentation contains certain statements that may include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements, other than statements of historical fact, included herein are “forward-looking statements.” Included among “forward-looking statements” are, among other things, statements about our future outlook on opportunities based upon current market conditions. Although the company believes that the expectations reflected in these forward-looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. Actual results could differ materially from those anticipated in these forward-looking statements as a result of a variety of factors. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this discussion. Other than as required by law, the company does not assume a duty to update these forward-looking statements. Past performance is no guarantee of future results. The illustrations are not intended to predict the performance of any specific investment or security. The past performance figures do not represent performance of any Hatteras security and there can be no assurance that any Hatteras security will achieve the past returns of the illustrative examples. This is not an offering to subscribe for units in any fund and is intended for informational purposes only. An offering can only be made by delivery of the Prospectus to “qualified clients” within the meaning of U.S. securities laws.

Please carefully consider the investment objectives, risks, and charges and expenses of the Funds before investing. Please read the Prospectus carefully before investing as it contains important information on the investment objectives, composition, fees, charges and expenses, risks, suitability, and tax obligations of investing in the Funds. Copies of the Prospectus and performance data current to the most recent month-end may be obtained online at hatterasfunds.com or by contacting Hatteras at 866.388.6292. Past performance does not guarantee future results.

The Hatteras Core Alternatives Fund, L.P.; the Hatteras Core Alternatives TEI Fund, L.P; the Hatteras Core Alternatives Institutional Fund, L.P.; and the Hatteras Core Alternatives TEI Institutional Fund, L.P. (collectively referred to herein as the “Hatteras Core Alternatives Fund” or the “Fund”) are Delaware limited partnerships that are registered under the Investment Company Act of 1940 (the “1940 Act”), as amended, as non-diversified, closed-end management investment companies whose units are registered under the Securities Act of 1933, as amended. The Hatteras Core Alternatives Fund is a fund of alternative investments. As such, the Fund invests in private hedge funds and private equity investments. Hedge funds are speculative investments and are not suitable for all investors, nor do they represent a complete investment program. A hedge fund can be described generally as a private and unregistered investment pool that accepts investors’ money and employs hedging and arbitrage techniques using long and short positions, leverage and derivatives, and investments in many markets.

Key Risk Factors: The Fund, through an investment in the Master Fund, will invest substantially all of its assets in underlying funds that are generally not registered as investment companies under the 1940 Act and, therefore, the Fund will not have the benefit of various protections provided under the 1940 Act with respect to an investment in those underlying funds. The Fund can be highly volatile, carry substantial fees, and involve complex tax structures. Investments in the Fund involve a high degree of risk, including loss of entire capital. The underlying funds may engage in speculative investment strategies and practices, such as the use of leverage, short sales, and derivatives transactions, which can increase the risk of investment loss. The Fund provides limited liquidity, and units in the Fund are not transferable. Liquidity will be provided only through repurchase offers made by the Fund from time to time, generally on a quarterly basis upon prior written notice. The success of the Fund is highly dependent on the financial and managerial expertise of its principals and key personnel of the Fund’s investment manager. Although the investment manager for the Fund expects to receive detailed information from each underlying fund on a regular basis regarding its valuation, investment performance, and strategy, in most cases the investment managers have little or no means of independently verifying this information. The underlying funds are not required to provide

TEN

transparency with respect to their respective investments. By investing in the underlying funds indirectly through the Fund, investors will be subject to a dual layer of fees, both at the Fund and underlying fund levels. Certain underlying funds will not provide final Schedule K-1s for any fiscal year before April 15th of the following year. Those funds, however, will endeavor to provide estimates of taxable income or losses with respect to their investments. Please see the Prospectus for a detailed

discussion of the specific risks disclosed here and other important risks and considerations.

Securities offered through Hatteras Capital Distributors, LLC, member FINRA /SIPC. Hatteras Capital Distributors, LLC is affiliated with Hatteras Investment Partners, LLC by virtue of common control/ownership. This document is not an offering to subscribe for units of any fund and is intended for informational purposes only.

ELEVEN

HATTERAS FUNDS

Hatteras Core Alternatives Fund, L.P. (a Delaware Limited Partnership)

Hatteras Core Alternatives TEI Fund, L.P. (a Delaware Limited Partnership)

Hatteras Core Alternatives Institutional Fund, L.P. (a Delaware Limited Partnership)

Hatteras Core Alternatives TEI Institutional Fund, L.P. (a Delaware Limited Partnership)

Financial Statements

As of and for the year ended March 31, 2013

with Report of Independent Registered Public Accounting Firm

HATTERAS FUNDS

As of and for the year ended March 31, 2013

Hatteras Core Alternatives Fund, L.P. (a Delaware Limited Partnership)

Hatteras Core Alternatives TEI Fund, L.P. (a Delaware Limited Partnership)

Hatteras Core Alternatives Institutional Fund, L.P. (a Delaware Limited Partnership)

Hatteras Core Alternatives TEI Institutional Fund, L.P. (a Delaware Limited Partnership)

Table of Contents

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To each Board of Directors and Partners of Hatteras Core Alternatives Fund, L.P., Hatteras Core Alternatives TEI Fund, L.P., Hatteras Core Alternatives Institutional Fund, L.P., and Hatteras Core Alternatives TEI Institutional Fund, L.P.:

We have audited the accompanying statements of assets, liabilities, and partners’ capital of Hatteras Core Alternatives Fund, L.P, Hatteras Core Alternatives TEI Fund, L.P., Hatteras Core Alternatives Institutional Fund, L.P., and Hatteras Core Alternatives TEI Institutional Fund, L.P. (each a Delaware Limited Partnership) (collectively the “Feeder Funds”) as of March 31, 2013, and the related statements of operations and cash flows for the year then ended, and the statements of changes in partners’ capital for each of the two years in the period then ended. These financial statements are the responsibility of the Feeder Funds’ management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Feeder Funds are not required to have, nor were we engaged to perform, audits of their internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Feeder Funds’ internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such financial statements referred to above present fairly, in all material respects, the financial position of each of the Feeder Funds as of March 31, 2013, the results of their operations and their cash flows for the year then ended, and the changes in their partners’ capital for each of the two years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

As discussed in Note 2 to the Hatteras Master Fund, L.P. financial statements, which are attached herein and should be read in conjunction with this report, the financial statements include investments valued at $1,110,504,519 (88.96% of total assets) as of March 31, 2013, whose fair value have been estimated by management in the absence of readily determinable fair values. Management’s estimates are based on information provided by the underlying fund advisers.

DELOITTE & TOUCHE LLP

Philadelphia, Pennsylvania

May 30, 2013

ONE

HATTERAS FUNDS

(each a Delaware Limited Partnership)

STATEMENTSOF ASSETS, LIABILITIESAND PARTNERS’ CAPITAL

March 31, 2013

| | | | | | | | | | | | | | | | |

| | | Hatteras

Core Alternatives

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Fund, L.P.* | | | Hatteras

Core Alternatives

Institutional

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Institutional

Fund, L.P.* | |

Assets | | | | | | | | | | | | | | | | |

Investment in Hatteras Master Fund, L.P., at fair value (cost $173,813,008; $235,350,872; $197,227,809 and $501,121,436, respectively) | | $ | 184,990,210 | | | $ | 246,124,934 | | | $ | 197,557,979 | | | $ | 531,471,798 | |

Cash | | | 350,000 | | | | 405,000 | | | | 200,000 | | | | 305,000 | |

Receivable for withdrawal from Hatteras Master Fund, L.P. | | | 9,734,007 | | | | 12,947,528 | | | | 10,400,149 | | | | 27,977,343 | |

Investment in Hatteras Master Fund, L.P. paid in advance | | | 163,401 | | | | 102,229 | | | | 486,857 | | | | 439,525 | |

Prepaid assets | | | 4,397 | | | | 5,849 | | | | 4,445 | | | | 11,727 | |

Total assets | | $ | 195,242,015 | | | $ | 259,585,540 | | | $ | 208,649,430 | | | $ | 560,205,393 | |

Liabilities and partners’ capital | | | | | | | | | | | | | | | | |

Withdrawals payable | | $ | 9,734,094 | | | $ | 12,947,528 | | | $ | 10,400,149 | | | $ | 27,977,343 | |

Contributions received in advance | | | 345,000 | | | | 339,000 | | | | 555,200 | | | | 552,190 | |

Servicing fee payable | | | 137,996 | | | | 183,550 | | | | 17,335 | | | | 46,631 | |

Professional fees payable | | | 43,652 | | | | 25,667 | | | | 44,220 | | | | 14,510 | |

Accounting and administration fees payable | | | 11,567 | | | | 16,082 | | | | 9,539 | | | | 16,148 | |

Printing fees payable | | | 10,000 | | | | 15,000 | | | | 5,000 | | | | 27,599 | |

Custodian fees payable | | | 800 | | | | 1,400 | | | | 800 | | | | 1,400 | |

Other accrued expenses | | | 5,000 | | | | 8,045 | | | | 5,000 | | | | 14,671 | |

Total liabilities | | | 10,288,109 | | | | 13,536,272 | | | | 11,037,243 | | | | 28,650,492 | |

Partners’ capital | | | 184,953,906 | | | | 246,049,268 | | | | 197,612,187 | | | | 531,554,901 | |

Total liabilities and partners’ capital | | $ | 195,242,015 | | | $ | 259,585,540 | | | $ | 208,649,430 | | | $ | 560,205,393 | |

Components of partners’ capital | | | | | | | | | | | | | | | | |

Capital contributions (net) | | $ | 189,224,280 | | | $ | 256,952,363 | | | $ | 200,780,774 | | | $ | 510,333,097 | |

Accumulated net investment loss | | | (17,310,145 | ) | | | (23,209,570 | ) | | | (3,094,849 | ) | | | (5,394,315 | ) |

Accumulated net realized gain (loss) | | | (5,146,344 | ) | | | (4,833,016 | ) | | | (5,251,753 | ) | | | 977,293 | |

Accumulated net unrealized appreciation on investments | | | 18,186,115 | | | | 17,139,491 | | | | 5,178,015 | | | | 25,638,826 | |

Partners’ capital | | $ | 184,953,906 | | | $ | 246,049,268 | | | $ | 197,612,187 | | | $ | 531,554,901 | |

Net asset value per unit | | $ | 93.23 | | | $ | 92.88 | | | $ | 96.68 | | | $ | 96.26 | |

Maximum offering price per unit** | | $ | 95.09 | | | $ | 94.74 | | | $ | 96.68 | | | $ | 96.26 | |

Number of authorized units | | | 7,500,000.00 | | | | 7,500,000.00 | | | | 7,500,000.00 | | | | 10,000,000.00 | |

Number of outstanding units | | | 1,983,779.66 | | | | 2,648,968.08 | | | | 2,043,885.22 | | | | 5,522,226.42 | |

| * | Consolidated Statement. See note 1. |

| ** | The maximum sales load for the Hatteras Core Alternatives Fund, L.P. and the Hatteras Core Alternatives TEI Fund, L.P. is 2.00%. The remaining funds are not subject to a sales load. |

See notes to financial statements.

TWO

HATTERAS FUNDS

(each a Delaware Limited Partnership)

STATEMENTSOF OPERATIONS

For the year ended March 31, 2013

| | | | | | | | | | | | | | | | |

| | | Hatteras

Core Alternatives

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Fund, L.P.* | | | Hatteras

Core Alternatives

Institutional

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Institutional

Fund, L.P.* | |

Net investment income allocated from Hatteras Master Fund, L.P. | | | | | | | | | | | | | | | | |

Investment income | | $ | 4,639,378 | | | $ | 6,095,425 | | | $ | 4,783,945 | | | $ | 12,709,470 | |

Operating expenses | | | (2,768,691 | ) | | | (3,633,647 | ) | | | (2,844,337 | ) | | | (7,560,808 | ) |

Performance allocation | | | — | | | | — | | | | — | | | | (965,799 | ) |

Net investment income allocated from Hatteras Master Fund, L.P. | | | 1,870,687 | | | | 2,461,778 | | | | 1,939,608 | | | | 4,182,863 | |

Feeder Fund investment income | | | | | | | | | | | | | | | | |

Interest | | | 144 | | | | 158 | | | | 137 | | | | 274 | |

Total fund investment income | | | 144 | | | | 158 | | | | 137 | | | | 274 | |

Feeder Fund expenses | | | | | | | | | | | | | | | | |

Servicing fee | | | 1,844,133 | | | | 2,421,160 | | | | 222,847 | | | | 592,430 | |

Accounting and administration fees | | | 140,044 | | | | 200,876 | | | | 120,232 | | | | 209,751 | |

Professional fees | | | 57,631 | | | | 20,400 | | | | 70,632 | | | | 29,326 | |

Insurance fees | | | 52,815 | | | | 70,122 | | | | 52,901 | | | | 139,955 | |

Directors’ fees | | | 37,500 | | | | 37,500 | | | | 37,500 | | | | 37,500 | |

Printing fees | | | 20,499 | | | | 26,230 | | | | 20,938 | | | | 40,000 | |

Custodian fees | | | 5,242 | | | | 8,574 | | | | 6,485 | | | | 9,045 | |

Withholding tax | | | — | | | | 333,262 | | | | — | | | | 659,468 | |

Other expenses | | | 80,752 | | | | 61,301 | | | | 68,627 | | | | 83,333 | |

Total Feeder Fund expenses | | | 2,238,616 | | | | 3,179,425 | | | | 600,162 | | | | 1,800,808 | |

Net investment income/(loss) | | | (367,785 | ) | | | (717,489 | ) | | | 1,339,583 | | | | 2,382,329 | |

Net realized gain and change in unrealized appreciation on investments allocated from Hatteras Master Fund, L.P. | | | | | | | | | | | | | | | | |

Net realized gain from investments in Adviser Funds, securities and foreign exchange transactions | | | 5,481,387 | | | | 7,330,608 | | | | 5,841,578 | | | | 15,628,270 | |

Net change in unrealized appreciation on investments in Adviser Funds, securities and foreign exchange transactions | | | 2,989,143 | | | | 3,660,794 | | | | 2,892,592 | | | | 7,728,454 | |

Net realized gain and change in unrealized appreciation on investments allocated from Hatteras Master Fund, L.P. | | | 8,470,530 | | | | 10,991,402 | | | | 8,734,170 | | | | 23,356,724 | |

Net increase in partners’ capital resulting from operations | | $ | 8,102,745 | | | $ | 10,273,913 | | | $ | 10,073,753 | | | $ | 25,739,053 | |

| * | Consolidated Statement. See note 1. |

See notes to financial statements.

THREE

HATTERAS FUNDS

(each a Delaware Limited Partnership)

STATEMENTSOF CHANGESIN PARTNERS’ CAPITAL

For the year ended March 31, 2012 and the year ended March 31, 2013

| | | | | | | | | | | | | | | | |

| | | Hatteras

Core Alternatives

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Fund, L.P.* | | | Hatteras

Core Alternatives

Institutional

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Institutional

Fund, L.P.* | |

| | | Limited

Partners | | | Limited

Partners | | | Limited

Partners | | | Limited

Partners | |

Partners’ Capital, at March 31, 2011 | | $ | 248,882,108 | | | $ | 325,745,330 | | | $ | 238,674,737 | | | $ | 659,549,379 | |

Capital contributions | | | 37,627,191 | | | | 45,202,873 | | | | 52,807,746 | | | | 55,960,615 | |

Capital withdrawals | | | (42,007,165 | ) | | | (45,915,793 | ) | | | (47,422,023 | ) | | | (71,636,476 | ) |

Repurchase fees | | | 57,277 | | | | 5,418 | | | | 36,440 | | | | 16,501 | |

Net investment income/(loss) | | | (724,905 | ) | | | (1,262,773 | ) | | | 1,231,020 | | | | 3,013,883 | |

Net realized gain from investments in Adviser Funds, securities and foreign exchange transactions | | | 3,080,313 | | | | 3,877,391 | | | | 2,883,089 | | | | 7,796,071 | |

Net change in unrealized appreciation on investments in Adviser Funds, securities and foreign exchange contracts | | | (12,034,318 | ) | | | (15,448,686 | ) | | | (11,319,447 | ) | | | (30,153,048 | ) |

Partners’ Capital, at March 31, 2012** | | $ | 234,880,501 | | | $ | 312,203,760 | | | $ | 236,891,562 | | | $ | 624,546,925 | |

Capital contributions | | | 8,346,000 | | | | 10,697,277 | | | | 12,778,549 | | | | 26,609,863 | |

Capital withdrawals | | | (66,564,692 | ) | | | (87,225,548 | ) | | | (62,321,857 | ) | | | (145,459,748 | ) |

Repurchase fees | | | 189,352 | | | | 99,866 | | | | 190,180 | | | | 118,808 | |

Net investment income/(loss) | | | (367,785 | ) | | | (717,489 | ) | | | 1,339,583 | | | | 2,382,329 | |

Net realized gain from investments in Adviser Funds, securities and foreign exchange transactions | | | 5,481,387 | | | | 7,330,608 | | | | 5,841,578 | | | | 15,628,270 | |

Net change in unrealized appreciation on investments in Adviser Funds, securities and foreign exchange contracts | | | 2,989,143 | | | | 3,660,794 | | | | 2,892,592 | | | | 7,728,454 | |

Partners’ Capital, at March 31, 2013*** | | $ | 184,953,906 | | | $ | 246,049,268 | | | $ | 197,612,187 | | | $ | 531,554,901 | |

| * | Consolidated Statement. See note 1. |

| ** | Including accumulated net investment loss of $16,942,360; $22,492,081; $4,434,432; and $7,776,644, respectively. |

| *** | Including accumulated net investment loss of $17,310,145; $23,209,570; $3,094,849; and $5,394,315, respectively. |

See notes to financial statements.

FOUR

HATTERAS FUNDS

(each a Delaware Limited Partnership)

STATEMENTSOF CASHFLOWS

For the year ended March 31, 2013

| | | | | | | | | | | | | | | | |

| | | Hatteras

Core Alternatives

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Fund, L.P.* | | | Hatteras

Core Alternatives

Institutional

Fund, L.P. | | | Hatteras

Core Alternatives

TEI

Institutional

Fund, L.P.* | |

Cash flows from operating activities: | | | | | | | | | | | | | | | | |

Net increase in partners’ capital resulting from operations | | $ | 8,102,745 | | | $ | 10,273,913 | | | $ | 10,073,753 | | | $ | 25,739,053 | |

Adjustments to reconcile net increase in partners’ capital resulting from operations to net cash provided by operating activities: | | | | | | | | | | | | | | | | |

Purchase of interests in Hatteras Master Fund, L.P. | | | (6,067,031 | ) | | | (7,775,372 | ) | | | (12,262,630 | ) | | | (25,518,283 | ) |

Proceeds from withdrawals from Hatteras Master Fund, L.P. | | | 66,601,470 | | | | 87,595,350 | | | | 62,359,356 | | | | 146,172,438 | |

Net investment income allocated from Hatteras Master Fund, L.P. | | | (1,870,687 | ) | | | (2,461,778 | ) | | | (1,939,608 | ) | | | (4,182,863 | ) |

Net realized gain from investments in Adviser Funds, securities and foreign exchange transactions allocated from Hatteras Master Fund, L.P. | | | (5,481,387 | ) | | | (7,330,608 | ) | | | (5,841,578 | ) | | | (15,628,270 | ) |

Net change in unrealized appreciation on investments in Adviser Funds, securities and foreign exchange transactions allocated from Hatteras Master Fund, L.P. | | | (2,989,143 | ) | | | (3,660,794 | ) | | | (2,892,592 | ) | | | (7,728,454 | ) |

(Increase)/Decrease in receivable for withdrawals from Hatteras Master Fund, L.P. | | | 3,293,348 | | | | (1,361,906 | ) | | | 3,529,984 | | | | (8,824,387 | ) |

(Increase)/Decrease in investment in Hatteras Master Fund, L.P. paid in advance | | | (163,401 | ) | | | (102,229 | ) | | | (486,857 | ) | | | (439,525 | ) |

(Increase)/Decrease in prepaid assets | | | 150 | | | | 105 | | | | (112 | ) | | | (162 | ) |

Increase/(Decrease) in servicing fee payable | | | (37,724 | ) | | | (45,927 | ) | | | (3,568 | ) | | | (7,015 | ) |

Increase/(Decrease) in accounting and administration fees payable | | | (1,345 | ) | | | (1,326 | ) | | | (1,046 | ) | | | (2,843 | ) |

Increase/(Decrease) in professional fees payable | | | (5,248 | ) | | | (10,830 | ) | | | 8,590 | | | | (2,844 | ) |

Increase/(Decrease) in custodian fees payable | | | (838 | ) | | | — | | | | (100 | ) | | | (30 | ) |

Increase/(Decrease) in printing fees payable | | | (31 | ) | | | 1,829 | | | | 3,149 | | | | (4,097 | ) |

Increase/(Decrease) in other accrued expenses | | | 1,620 | | | | (4,034 | ) | | | 51 | | | | 5,704 | |

Net cash provided by operating activities | | | 61,382,498 | | | | 75,116,393 | | | | 52,546,792 | | | | 109,578,422 | |

Cash flows from financing activities: | | | | | | | | | | | | | | | | |

Capital contributions | | | 8,691,000 | | | | 11,036,277 | | | | 13,333,749 | | | | 27,162,053 | |

Capital withdrawals, net of repurchase fees | | | (69,847,153 | ) | | | (85,862,995 | ) | | | (65,822,099 | ) | | | (136,629,535 | ) |

Net cash used in financing activities | | | (61,156,153 | ) | | | (74,826,718 | ) | | | (52,488,350 | ) | | | (109,467,482 | ) |

Net change in cash | | | 226,345 | | | | 289,675 | | | | 58,442 | | | | 110,940 | |

Cash at beginning of year | | | 123,655 | | | | 115,325 | | | | 141,558 | | | | 194,060 | |

Cash at end of year | | $ | 350,000 | | | $ | 405,000 | | | $ | 200,000 | | | $ | 305,000 | |

| * | Consolidated Statement. See note 1. |

See notes to financial statements.

FIVE

HATTERAS FUNDS

(each a Delaware Limited Partnership)

NOTESTO FINANCIAL STATEMENTS

As of and for the year ended March 31, 2013

1. ORGANIZATION

The Hatteras Funds, each a “Feeder Fund” and collectively the “Feeder Funds” are:

Hatteras Core Alternatives Fund, L.P.

Hatteras Core Alternatives TEI Fund, L.P.

Hatteras Core Alternatives Institutional Fund, L.P.

Hatteras Core Alternatives TEI Institutional Fund, L.P.

The Hatteras Core Alternatives TEI Fund, L.P. and the Hatteras Core Alternatives TEI Institutional Fund, L.P. each invest substantially all of their assets in the Hatteras Core Alternatives Offshore Fund, LDC and Hatteras Core Alternatives Offshore Institutional Fund, LDC, (collectively the “Blocker Funds”), respectively. The Blocker Funds are Cayman Islands limited duration companies with the same investment objective as the Feeder Funds. The Blocker Funds serve solely as intermediate entities through which the Hatteras Core Alternatives TEI Fund, L.P. and the Hatteras Core Alternatives TEI Institutional Fund, L.P. invest in Hatteras Master Fund, L.P. (the “Master Fund” and together with the Feeder Funds, the “Funds”). The Blocker Funds enable tax-exempt Limited Partners (as defined below) to invest without receiving certain income in a form that would otherwise be taxable to such tax-exempt Limited Partners regardless of their tax-exempt status. The Hatteras Core Alternatives TEI Fund, L.P. owns 100% of the participating beneficial interests of the Hatteras Core Alternatives Offshore Fund, LDC and the Hatteras Core Alternatives TEI Institutional Fund, L.P. owns 100% of the participating beneficial interests of the Hatteras Core Alternatives Offshore Institutional Fund, LDC. Where these Notes to Financial Statements discuss the Feeder Funds’ investment in the Master Fund, for Hatteras Core Alternatives TEI Fund, L.P. and Hatteras Core Alternatives TEI Institutional Fund, L.P., it means their investment in the Master Fund through the applicable Blocker Fund.

The Feeder Funds are organized as Delaware limited partnerships, and are registered under the Securities Act of 1933, as amended, and the Investment Company Act of 1940, as amended, (the “1940 Act”) as closed-end, diversified, management investment companies. The primary investment objective of the Feeder Funds is to provide capital appreciation consistent with the return characteristic of the alternative investment portfolios of larger endowments. The Feeder Funds’ secondary objective is to provide capital appreciation with less volatility than that of the equity markets. To achieve their objectives, the Feeder Funds provide their investors with access to a broad range of investment strategies, asset categories and trading advisers (“Advisers”) and by providing overall asset allocation services typically available on a collective basis to larger institutions, through an investment of substantially all of their assets into the Master Fund, which is registered under the 1940 Act. The Feeder Funds are co-managed by Hatteras Investment Partners, LLC (“HIP”), a Delaware limited liability company registered as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”), and Morgan Creek Capital Management, LLC (“MCCM,” together with HIP, the “Investment Managers”), a North Carolina limited liability company registered as an investment adviser under the Advisers Act. Investors who acquire units of limited partnership interest in the Feeder Funds (“Units”) are the limited partners (each, a “Limited Partner” and together, the “Limited Partners”) of the Feeder Funds.

The financial statements of the Master Fund, including the schedule of investments, are included elsewhere in this report and should be read with the Feeder Funds’ financial statements. The percentage of the Master Fund’s beneficial limited partnership interests owned by the Feeder Funds at March 31, 2013 were:

| | | | |

Hatteras Core Alternatives Fund, L.P. | | | 15.67 | % |

Hatteras Core Alternatives TEI Fund, L.P. | | | 20.84 | % |

Hatteras Core Alternatives Institutional Fund, L.P. | | | 16.73 | % |

Hatteras Core Alternatives TEI Institutional Fund, L.P. | | | 45.02 | % |

Hatteras Investment Management, LLC, a Delaware limited liability company, serves as the General Partner of each of the Feeder Funds and the Master Fund (the “General Partner”). The General Partner is an affiliate of HIP. The General Partner has appointed a Board of Directors for each Feeder Fund (collectively the “Boards”) and, to the fullest extent permitted by applicable law, has irrevocably delegated to the Boards its rights and powers to

SIX

HATTERAS FUNDS

(each a Delaware Limited Partnership)

NOTESTO FINANCIAL STATEMENTS

As of and for the year ended March 31, 2013 (continued)

1. ORGANIZATION (CONTINUED)

monitor and oversee the business affairs of the Feeder Funds, including the complete and exclusive authority to oversee and establish policies regarding the management, conduct and operation of the Feeder Funds’ business.

2. SIGNIFICANT ACCOUNTING POLICIES

These financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) and are expressed in United States dollars. The following is a summary of significant accounting and reporting policies used in preparing the financial statements.

a. Investment Valuation

The Feeder Funds do not make direct investments in securities or financial instruments, and invest substantially all of their assets in the Master Fund. The Feeder Funds record their investment in the Master Fund at fair value. Because the full amount of investment cannot be redeemed at least quarterly, each Feeder Fund’s investment in the Master Fund would be considered level 3 under Accounting Standards Codification 820 — Fair Value, as described in the notes to the Master Fund’s financial statements included elsewhere in this report. Valuation of securities held by the Master Fund, including the Master Fund’s disclosure of investments under the three-tier hierarchy, is also discussed in the notes to the Master Fund’s financial statements.

b. Allocations from the Master Fund

The Feeder Funds record their allocated portion of income, expense, realized gains and losses and unrealized appreciation and depreciation from the Master Fund.

c. Feeder Fund Level Income and Expenses

Interest income on any cash or cash equivalents held by the Feeder Funds will be recognized on an accrual basis. Expenses that are specifically attributed to the Feeder Funds are charged to each Feeder Fund. Because the Feeder Funds bear their proportionate share of the management fee of the Master Fund, the Feeder Funds pay no direct management fee to the Investment Managers. The Feeder Funds’ specific expenses are recorded on an accrual basis.

d. Tax Basis Reporting

Because the Master Fund invests primarily in investment funds that are treated as partnerships for U.S. Federal tax purposes, the tax character of each of the Feeder Fund’s allocated earnings is established dependent upon the tax filings of the investment vehicles operated by the Advisers (“Adviser Funds”). Accordingly, the tax basis of these allocated earnings and the related balances are not available as of the reporting date.

e. Income Taxes

For U.S. Federal income tax purposes, the Feeder Funds are treated as partnerships, and each Limited Partner in each respective Feeder Fund is treated as the owner of its proportionate share of the net assets, income, expenses, and the realized and unrealized gains (losses) of such Feeder Fund. Accordingly, no federal, state or local income taxes have been provided on profits of the Feeder Funds since the Limited Partners are individually liable for the taxes on their share of the Feeder Funds.

The Feeder Funds file tax returns as prescribed by the tax laws of the jurisdictions in which they operate. In the normal course of business, the Feeder Funds are subject to examination by federal, state, local and foreign jurisdictions, where applicable. For returns filed for the years ended December 31, 2009 through December 31, 2012, the Feeder Funds remain subject to examination by the major tax jurisdictions under the statute of limitations.

The Feeder Funds have reviewed any potential tax positions as of March 31, 2013 and have determined that they do not have a liability for any unrecognized tax benefits or expense. The Feeder Funds recognize interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year ended March 31, 2013, the Feeder Funds did not incur any material interest or penalties.

SEVEN

HATTERAS FUNDS

(each a Delaware Limited Partnership)

NOTESTO FINANCIAL STATEMENTS

As of and for the year ended March 31, 2013 (continued)

2. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

f. Cash

Cash includes amounts held in interest bearing demand deposit accounts. Such cash, at times, may exceed federally insured limits. The Feeder Funds have not experienced any losses in such accounts and do not believe they are exposed to any significant credit risk on such accounts.

g. Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of increases and decreases in Limited Partners’ capital from operations during the reporting period. Actual results could differ from those estimates.

h. Consolidated Financial Statements

The asset, liability, and equity accounts of the Hatteras Core Alternatives TEI Fund, L.P. and the Hatteras Core Alternatives TEI Institutional Fund, L.P. are consolidated with their respective Blocker Funds as presented in the Statements of Assets, Liabilities, and Partners’ Capital, Statements of Operations, Statements of Changes in Partners’ Capital, and Statements of Cash Flows. All significant intercompany accounts and transactions have been eliminated in consolidation.

3. ALLOCATIONOF LIMITED PARTNERS’ CAPITAL

Net profits or net losses of the Feeder Funds for each allocation period (“Allocation Period”) will be allocated among and credited to or debited against the capital accounts of the Limited Partners. Net profits or net losses will be measured as the net change in the value of the Limited Partners’ capital of the Feeder Funds, including any net change in unrealized appreciation or depreciation of investments and realized income and gains or losses and expenses during an Allocation Period, adjusted to exclude any items to be allocated among the capital accounts of the Limited Partners in accordance with the Limited Partners’ respective investment percentages.

Allocation Periods generally begin on the first calendar day of each month and end at the close of business on the last day of each month.

The Feeder Funds maintain a separate capital account (“Capital Account”) on their books for each Limited Partner. Each Limited Partner’s Capital Account will have an opening balance equal to the Limited Partner’s initial purchase of the Feeder Fund (i.e., the amount of the investment less any applicable sales load of up to 2 percent of the purchased amount), and thereafter, will be (i) increased by the amount of any additional purchases by such Limited Partner; (ii) decreased for any payments upon repurchase or sale of such Limited Partner’s interest or any distributions in respect of such Limited Partner; and (iii) increased or decreased as of the close of each Allocation Period by such Limited Partner’s allocable share of the net profits or net losses of the Feeder Fund.

| | | | | | | | | | | | | | | | |

| | | Hatteras Core Alternatives Fund, L.P. | | | Hatteras Core Alternatives TEI

Fund, L.P. | | | Hatteras Core Alternatives

Institutional

Fund, L.P. | | | Hatteras Core Alternatives

TEI Institutional

Fund, L.P. | |

Beginning Units, April 1, 2011 | | | 2,680,763.77 | | | | 3,513,215.38 | | | | 2,517,400.45 | | | | 6,965,196.16 | |

Purchases | | | 410,349.15 | | | | 494,338.34 | | | | 566,263.72 | | | | 595,845.64 | |

Sales | | | (468,946.82 | ) | | | (514,360.89 | ) | | | (514,144.55 | ) | | | (775,804.70 | ) |

Beginning Units, April 1, 2012 | | | 2,622,166.10 | | | | 3,493,192.83 | | | | 2,569,519.62 | | | | 6,785,237.10 | |

Purchases | | | 92,593.95 | | | | 119,103.07 | | | | 137,183.02 | | | | 288,692 | |

Sales | | | (730,980.39 | ) | | | (963,327.82 | ) | | | (662,817.42 | ) | | | (1,551,702.68 | ) |

Ending units, March 31, 2013 | | | 1,983,779.66 | | | | 2,648,968.08 | | | | 2,043,885.22 | | | | 5,522,226.42 | |

EIGHT

HATTERAS FUNDS

(each a Delaware Limited Partnership)

NOTESTO FINANCIAL STATEMENTS

As of and for the year ended March 31, 2013 (continued)

4. RELATED PARTY TRANSACTIONSAND OTHER

In consideration for fund services, Hatteras Core Alternatives Fund, L.P., Hatteras Core Alternatives TEI Fund, L.P., Hatteras Core Alternatives Institutional Fund, L.P. and Hatteras Core Alternatives TEI Institutional Fund, L.P. will pay HIP (in such capacity, the “Servicing Agent”) a fund servicing fee at the annual rate of 0.85%, 0.85%, 0.10% and 0.10%, respectively, of the month-end partner’s capital of the applicable Feeder Fund. The respective Feeder Fund servicing fees payable to the Servicing Agent will be borne by all Limited Partners of the respective Feeder Fund on a pro-rata basis before giving effect to any repurchase of interests in the Master Fund effective as of that date, and will decrease the net profits or increase the net losses of the Master Fund that are credited to its interest holders, including each Feeder Fund.

The Servicing Agent may waive (to all investors on a pro-rata basis) or pay to third parties all or a portion of any such fees in its sole discretion. The Servicing Agent did not waive any of the servicing fees for the year ended March 31, 2013. HIP has contractually agreed to reimburse certain expenses through July 31, 2013, so that the total annual expenses (excluding taxes, interest, brokerage commissions, other transaction-related expenses, any extraordinary expenses of the Feeder Funds, any acquired fund fees and expenses, as well as any performance allocation payable by the Feeder Funds or the Master Fund) for this period will not exceed 2.35% for the Hatteras Core Alternatives Fund, L.P. and Hatteras Core Alternatives TEI Fund, L.P. and 1.75% for the Hatteras Core Alternatives Institutional Fund, L.P. and Hatteras Core Alternatives TEI Institutional Fund, L.P. (the “Expense Limitation”). The agreement automatically renews for a one-year term after the initial period until terminated by HIP or the applicable Feeder Fund. The Feeder Funds will carry forward, for a period not to exceed (3) three years from the date on which a reimbursement is made by HIP, any expenses in excess of the Expense Limitation and repay HIP such amounts, provided the Feeder Fund is able to effect such reimbursement and remain in compliance with the Expense Limitation disclosed in the applicable Feeder Fund’s then effective prospectus. There were no reimbursements from HIP, nor previous reimbursements repaid to HIP, nor expenses available for reimbursement as of and for the year ended March 31, 2013.

The performance allocation is calculated at the Master Fund level, and allocated to the Feeder Funds based on each Feeder Fund’s ownership interest in the Master Fund. The General Partner is allocated a performance allocation payable annually equal to 10% of the amount by which net new profits of the limited partner interests of the Master Fund exceed the non-cumulative “hurdle amount”, which is calculated as of the last day of the preceding calendar year of the Master Fund at a rate equal to the yield-to-maturity of the 90 day U.S. Treasury Bill as reported by the Wall Street Journal for the last business day of the preceding calendar year (the “Performance Allocation”). The Performance Allocation is made on a “peak to peak,” or “high watermark” basis, which means that the Performance Allocation is made only with respect to new net profits. If the Master Fund has a net loss in any period followed by a net profit, no Performance Allocation will be made with respect to such subsequent appreciation until such net loss has been recovered. MCCM is a non-voting member (“Member”) of HIP. HIP, MCCM and the General Partner have entered into a membership agreement (the “Member Agreement”). Pursuant to the Member Agreement, the General Partner makes distributions to MCCM equal to a percentage of the Performance Allocation the General Partner receives from the Master Fund. For the year ended March 31, 2013, the General Partner of the Master Fund accrued a Performance Allocation which was allocated to the Hatteras Core Alternatives TEI Institutional Fund, L.P. in the amount of $965,799, which is disclosed in the Statement of Operations.

Hatteras Capital Distributors LLC (“HCD”), an affiliate of HIP, serves as the Feeder Funds’ distributor. HCD receives a distribution fee from HIP equal to 0.10% on an annualized basis of the net assets of the Master Fund as of the last day of the month (before giving effect to any repurchase of interests in the Master Fund).