As filed with the Securities and Exchange Commission on March 7, 2008

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file Number: 811-4255

Dividend Capital Realty Income Allocation Fund

(Exact Name of the Registrant as Specified in Charter)

518 17th Street, Suite 1200, Denver, CO 80202

(Address of Principal Executive Offices—Zip Code)

Registrant’s Telephone Number, including area code: 303-228-2200

Derek Mullins

Secretary and Assistant Treasurer

518 17th Street, Suite 1200

Denver, CO 80202

(Names and Addresses of agents for service)

Date of fiscal year end: December 31*

Date of reporting period: December 31, 2007

* The fiscal year end of the Fund was recently changed from September 30 to December 31.

Item 1. Reports to Shareholders

The following is a copy of the report to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (the “Act”).

TABLEOF CONTENTS

The Investment Commentary included in this shareholder report contains certain forward-looking statements about the factors that may affect the performance of the Funds in the future. These statements are based on Fund management’s predictions and expectations concerning certain future events and their expected impact on the Funds, such as performance of the economy as a whole and of the real estate sector, changes in the level of interest rates, the impact of developing world events, and other factors that may influence the future performance of the Funds. Management believes these forward looking statements to be reasonable, although they are inherently uncertain and difficult to predict and there is no guarantee of their accuracy. Actual events may cause adjustments in portfolio management strategies from those currently expected to be employed.

1

INVESTMENT COMMENTARY

Dividend Capital Realty Income Allocation Fund

February 27, 2008

To our shareholders:

We submit to you Dividend Capital Realty Income Allocation Fund’s (“DCA” or “the Fund”) annual report for the three-months ended December 31, 2007. This short reporting period results from changing the Fund’s fiscal year-end from September to December. This change was made to better facilitate the Fund’s management by aligning its fiscal year-end with excise tax measurement periods.

The residential sub-prime mortgage-led credit crisis that began in mid-2007 has continued to deteriorate, resulting in significant turmoil in global financial markets. This credit crisis has been indiscriminate in its scope, impacting pricing and liquidity on a wide variety of debt and credit-sensitive instruments across industries and credit quality. Its ongoing expansion has led to broad based stock market declines, pronounced concerns of a U.S. recession and aggressive interest rate cuts by the Federal Reserve.

DCA’s investment mandate, which consists of allocating investments among common equity, preferred equity and debt securities of real estate companies, has not been immune from this market dislocation. As a result, the Fund’s net asset value (NAV) and market price experienced a significant decline.

As mentioned in our November 27, 2007 letter, we are disappointed with the Fund’s recent performance, but continue to focus our efforts on finding opportunities that we believe will preserve value and positioning the Fund to offer opportunity for attractive total returns as market conditions change and improve.

Performance Review

As displayed in the performance table that follows this letter, during the three months ended December 31, 2007, the Fund’s NAV total return was -20.62% while the market price total return was -25.08%. Since inception, the Fund’s NAV return has been -8.61% with a market price return of -11.50%. As reference points, the results can be compared to a return of -10.88% and -1.36% for the Wachovia Hybrid & Preferred REIT Securities Index, -13.17% and 11.38% for the MSCI U.S. REIT Index and -0.88% and 6.90% for the Lehman Brothers High Yield CMBS Index over the three-month and since inception periods, respectively.

2

INVESTMENT COMMENTARY (CONTINUED)

Dividend Capital Realty Income Allocation Fund (continued)

While we believe the benchmarks provide reference points for overall market conditions, the Fund’s performance may differ substantially from benchmark performance. These differences arise from a variety of factors, including investment allocation decisions among common stock, preferred stock and debt securities and the composition of the Fund’s investments, which may differ materially from benchmark composition. For example, the Fund invests in common stock of Canadian real estate companies, Commercial Mortgage REITs/Specialty Finance Companies, non-investment grade/unrated preferred securities and structured-finance debt securities, including Commercial Real Estate Collateralized Debt Obligations and Collateralized Loan Obligations, in proportions that are different from the representative benchmarks or may not be represented in the benchmarks. In addition, the Fund’s use of leverage has a material impact on performance. In executing the investment strategy, we construct the Fund’s portfolio in an effort to achieve the primary objective of high current income and secondary objective of capital appreciation rather, than strategic allocation decisions against representative benchmarks.

Over the fiscal time period, DCA’s NAV performance was driven by declines in the valuations of all asset classes in which we invest.

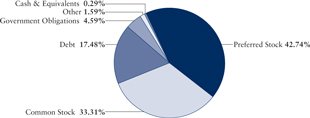

Within the preferred stock portfolio (42.75% of the Fund’s direct investments and indirect economic exposure as of 12/31/07), DCA experienced a decline in values driven by what we believe to be primarily technical rather than widespread fundamental issues. As liquidity dried up across a wide variety of credit and real estate sensitive securities, preferred stocks experienced a significant decline in trading volumes and market prices. DCA’s investments in below investment grade and non-rated preferred securities contributed to the underperformance. At this point, we believe underlying fundamentals on the majority of this portfolio remain good. In our opinion, we believe these investments represent the potential for an increase in long-term value as they are trading at attractive absolute and relative yields.

DCA’s overall debt portfolio (17.48% of the Fund’s direct investments and indirect economic exposure as of 12/31/07) experienced a significant decline in values based primarily on what we believe to be pronounced market concern over credit, real estate and structured finance related securities. DCA’s investments in structured finance debt instruments, including collateralized debt obligations and collateralized loan obligations, contributed to the underperformance. It is noteworthy that the current underlying fundamentals for the majority of the Fund’s debt positions continue to be in-line with initial underwriting expectations and therefore we believe these securities offer an attractive source of income and the potential for a recovery in value. Exceptions to this are securities issued by Taberna

3

INVESTMENT COMMENTARY (CONTINUED)

Dividend Capital Realty Income Allocation Fund (continued)

Preferred Funding III and V (combined these investments represent 0.16% of the Fund’s direct investments and indirect economic exposure as of 12/31/07), which are not currently paying their coupon and have experienced a significant and likely unrecoverable decline in value.

Finally, the financial market disruption has impacted the Fund’s common equity holdings (33.31% of the Fund’s direct investments and indirect economic exposure as of 12/31/07). The Fund experienced declines in the values of U.S. Equity REITs, Canadian real estate companies and significant declines in Commercial Mortgage REITs/Specialty Finance companies. In particular, U.S. Equity REITs have declined 26.51% from their February 7, 2007 peak and appear to be priced for a larger decline in commercial real estate values than has occurred thus far. Commercial Mortgage REITs/Specialty Finance companies have business models that contain a high degree of sensitivity to the real estate credit markets and therefore have been directly impacted by the credit crisis.

The broad based decline in all the real estate asset classes in which the Fund invests underscores the tremendous headwinds currently facing the markets.

Outlook

In our opinion, significant risks are prevalent in the U.S. economy and financial markets. The full impact of the credit crisis and ongoing declines in home prices on the U.S. economy, and therefore commercial real estate fundamentals, is uncertain. The persistence, duration and expansion of the credit crisis and de-leveraging of financial markets increase these risks. In reaction to these risks, we believe, there have been positive steps taken to address market issues. These include actions by the U.S. Federal Reserve to aggressively lower the Fed Funds Rate, the quick approval of an economic stimulus package and other measures taken by the U.S. Government.

Against this severe market disruption, we seek to take advantage of investment opportunities that are being created. In response to this, one step we intend on taking is to expand the Fund’s investment in foreign securities to include exposure outside of North America. This change was implemented to enhance investment flexibility by providing the opportunity to invest in a broader universe of real estate securities. We believe this increased investment flexibility enhances our ability to achieve the Fund’s objectives.

4

INVESTMENT COMMENTARY (CONTINUED)

Dividend Capital Realty Income Allocation Fund (continued)

In addition, in consultation with the Fund’s Board, we have eliminated the Fund’s policy that limits investment in illiquid securities. Historically, the Fund has limited investment in illiquid securities to 10% of managed assets, determined at time of purchase. As market conditions changed in 2007, we concluded that securities previously considered liquid became illiquid and have categorized them as such since June 2007. While this change did not result in violating the Fund’s limitation on illiquid securities, going forward we believe it is best to eliminate the limitation on illiquid securities to better reflect the liquidity profile of the Fund. While this has the potential to increase portfolio flexibility, we do not presently intend to increase investment in illiquid securities.

In closing, we continue to have conviction in DCA’s investment strategy, which we believe offers the potential for current income and the ability to realize NAV appreciation over time. Through our focus on execution of the Fund’s strategy and options offered by investments across the capital structure of real estate companies, we believe the Fund’s long-term investment objectives can be achieved. Thank you for your continued support.

| | |

| |  |

| David W. Agostine | | Charles Song |

| President | | Senior Portfolio Manager |

| |

| | |

| Jeffrey Taylor | | |

| Vice President and Treasurer | | |

5

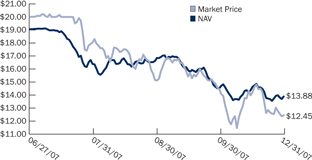

TOTAL RETURNSAND TRADING HISTORY

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

Average Annual Total Returns (1)

| | | | | | | | | |

| | | October 1, 2007 to

December 31, 2007 | | | Year Ended

September 30, 2007 | | | Since

Inception (7) | |

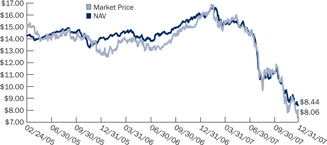

DCA at Market Price (“MP”) | | -25.08 | % | | -14.93 | % | | -11.50 | % |

DCA at Net Asset Value (“NAV”) (2) | | -20.62 | % | | -19.05 | % | | -8.61 | % |

Wachovia Hybrid & Preferred Securities REIT IndexSM (3) | | -10.88 | % | | -1.85 | % | | -1.36 | % |

MSCI U.S. REIT Index (4) | | -13.17 | % | | 4.67 | % | | 11.38 | % |

CMBS Index (5) | | -0.88 | % | | -0.67 | % | | 6.90 | % |

Trading History(1)(6)

| | | | | |

| | Average Premium/Discount to NAV | |

| | 1-Month | | -4.41 | % |

| | 3-Month | | -2.80 | % |

| | 1-Year | | -0.49 | % |

| | Since Inception | | -2.21 | % |

| | 52-Week Price History Range | |

| | MP | | $7.37 - $16.88 | |

| | NAV | | $8.41 - $16.81 | |

(1) | Past performance is no guarantee of future results. Investors cannot invest directly into any index. This chart is for illustrative purposes only and does not relate to the future performance of the Fund. For current to the most recent month-end performance, visit dividend capital.com, or call 866.DCG.REIT (324.7348). Performance data quoted above is historical. Current performance may be higher or lower than the performance data quoted. Performance does not include transaction fees that may be charged by your financial advisor or brokerage firm. |

(2) | Total return assumes reinvestment of dividend and capital gain distributions. Investors cannot invest at NAV. |

(3) | The Wachovia Hybrid & Preferred Securities REIT IndexSM is a capitalization weighted unmanaged index of exchange listed perpetual REIT preferred stocks and depository shares. The index is compiled by Wachovia Capital Markets, LLC and calculated by the American Stock Exchange. The Fund expects to invest in securities not included in this index, such as debt securities which may have lower returns than preferred stock, and common stock and non-U.S. securities which may be riskier than U.S. preferred stock. This index also includes securities in which the Fund will not invest. |

(4) | The MSCI U.S. REIT Index (RMS) is an unmanaged index of REIT securities of reasonable size and liquidity, weighted by market capitalization and considered representative of U.S. equity REIT performance. The index is used in comparison to the Fund because the Fund invests in common stock of companies primarily engaged in real estate, including REITs. |

(5) | The Lehman Brothers High-Yield CMBS Index is an unmanaged index of non-investment-grade and unrated CMBS, weighted by market value and comprised of all new issue U.S. CMBS transactions that have a maturity greater than one year, an original transaction size in excess of $500 million, and aggregate outstanding transaction size of at least $300 million, and is considered representative of the high-yield CMBS market. The index is used in comparison to the Fund because the Fund invests in commercial mortgage-backed securities. |

(6) | Market price and NAV price history are since inception, based upon closing market price. |

(7) | Fund inception is 02/24/2005. |

6

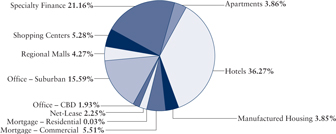

PORTFOLIO PROFILE

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

Portfolio Allocation (2)(3)

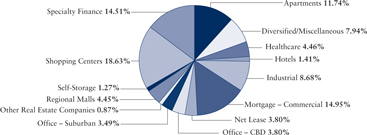

Common Stock Property Type Allocation(1)(3)(4)

Preferred Stock Property Type Allocation (1)(3)

(1) | Property-type allocation percentages are based on the market value of the Fund’s direct and indirect economic exposure to the preferred stock and common stock asset classes, respectively. |

(2) | Allocation percentages are based on the Fund’s direct investments and indirect economic exposure. Indirect economic exposure is generally obtained through the use of total return swaps and such exposure is calculated by using the investment’s notional value plus or minus related unrealized gains or losses. |

(3) | Holdings and composition of holdings are subject to change, and may not be representative of future investments. |

(4) | Some or all of the common stock exposure is derived through total return swaps. |

7

INVESTMENT COMMENTARY

Dividend Capital Strategic Global Realty Fund

February 27, 2008

To our shareholders:

We submit to you Dividend Capital Strategic Global Realty Fund’s (“DCW” or “the Fund”) annual report for the period June 27, 2007 through December 31, 2007. This period represents DCW’s first fiscal period of operations.

Triggered by concerns within the U.S. housing market, sub-prime mortgages and the impact to credit markets around the world, this reporting period has been characterized by significant turmoil in global financial markets. This credit crisis has been indiscriminate in its scope, impacting pricing and liquidity on a wide variety of debt and credit-sensitive instruments across industries and credit quality. Credit market conditions have continued to deteriorate and as the crisis has expanded it has contributed to broad based global stock market declines. It has also led to concerns of the impact to the global economy of a U.S. recession.

DCW’s investment mandate, which consists of allocating investments among common equity, preferred equity and debt securities of global real estate companies, has not been immune from this market dislocation. As a result, the Fund’s net asset value (NAV) and market price experienced a significant decline.

We are disappointed with the Fund’s recent performance, but continue to focus our efforts on finding opportunities that we believe will preserve value and positioning the Fund to offer the opportunity for attractive total returns as market conditions change and improve.

Performance Review

As displayed in the performance table that follows this letter, the Fund’s NAV total return during the reporting period was -23.20% while the market price total return was -34.36%. As reference points, this can be compared to a return of -6.48% for the FTSE EPRA/NAREIT Global Real Estate Index, -14.93% for the Wachovia Hybrid & Preferred REIT Securities Index, and 4.51% for the Lehman Brothers CMBS Index.

While we believe the benchmarks provide reference points for overall market conditions, the Fund’s performance may differ substantially from benchmark performance. These differences arise from a variety of factors, including investment allocation decisions among common stock, preferred stock and debt securities, overall country allocation decisions and the composition of the Fund’s investments, which may differ materially from benchmark composition. For example, the Fund invests in common stock of Commercial Mortgage REITs/

8

INVESTMENT COMMENTARY (CONTINUED)

Dividend Capital Strategic Global Realty Fund (continued)

Specialty Finance Companies, non-investment grade/unrated preferred securities and investment grade structured-finance debt securities, including Commercial Real Estate Collateralized Debt Obligations, in proportions that are different from the representative benchmarks or may not be represented in the benchmarks. In addition, the Fund’s use of leverage has a material impact on performance. In executing the investment strategy, we construct the Fund’s portfolio in an effort to achieve the primary objective of high current income and secondary objective of capital appreciation, rather than strategic allocation decisions against representative benchmarks.

Over the fiscal period, DCW’s NAV performance was driven by declines in the valuations of all asset classes in which we invest.

The financial market disruption impacted the Fund’s global common equity holdings (50.24% of the Fund’s direct investments and indirect economic exposure as of 12/31/07). The Fund experienced declines in the values of Japan, Canada, Singapore and U.S. Commercial Mortgage REITs/Specialty Finance Companies. Japan stock prices have also been impacted by political turmoil led by the Prime Minister’s resignation in September of 2007. Despite the declines, we believe longer-term fundamentals are positive for the markets and securities in which the Fund invests. Further, the ability to allocate investments across global markets helps to temper the impact of U.S. weakness and offers exposure to real estate securities with differing fundamental drivers.

Within the preferred stock portfolio (28.38% of the Fund’s direct investments and indirect economic exposure as of 12/31/07), DCW experienced a decline in values driven by what we believe to be primarily technical, rather than widespread fundamental issues. As liquidity dried up across a wide variety of credit and real estate sensitive securities, preferred stocks experienced a significant decline in trading volumes and market prices. DCW’s investments in below investment grade and non-rated preferred securities contributed to the underperformance. At this point, we believe underlying fundamentals on the majority of the Fund’s portfolio remain good and therefore we believe these investments represent the potential for an increase in long-term value as they are trading at attractive absolute and relative yields.

While relatively small, DCW’s debt portfolio (4.14% of the Fund’s direct investments and indirect economic exposure as of 12/31/07) experienced a significant decline in values based primarily on what we believe are market concerns over credit, real estate and structured finance related securities. DCW’s investments in structured finance debt instruments, including collateralized debt obligations, contributed to the underperformance. However, it is noteworthy that the underlying fundamentals for the Fund’s debt positions continue to be in-line with initial underwriting and we remain positive on the investment outlook for these securities.

9

INVESTMENT COMMENTARY (CONTINUED)

Dividend Capital Strategic Global Realty Fund (continued)

Outlook

In our opinion, significant risks are prevalent in the U.S. economy and global financial markets. The full impact of the credit crisis and ongoing declines in home prices on the U.S. economy, and therefore commercial real estate fundamentals, is uncertain. The persistence, duration and expansion of the credit crisis and deleveraging of financial markets increase these risks. In reaction to these risks, we believe, there have been positive steps taken to address market issues, including actions by the U.S. Federal Reserve to aggressively lower the Fed Funds Rate, the quick approval of an economic stimulus package and other measures taken by the U.S. Government. Global capital markets should benefit from a stabilization of U.S. capital markets. Finally, while the debate continues regarding de-coupling of global economies from the U.S., we believe real estate fundamentals in non-U.S. markets, particularly in Asia, remain strong.

Against this severe market disruption, we seek to take advantage of investment opportunities that are being created. We continue to have conviction in DCW’s investment strategy, which we believe offers the potential for current income and the ability to realize NAV appreciation over time. Through our focus on execution of the Fund’s strategy and options offered by investments across the capital structure of real estate companies, we believe the Fund’s long-term investment objectives can be achieved. Thank you for your continued support.

| | |

| | |

| David W. Agostine | | Charles Song |

| President | | Senior Portfolio Manager |

| |

| | |

| Jeffrey Taylor | | |

| Vice President and Treasurer | | |

10

TOTAL RETURNSAND TRADING HISTORY

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

Average Annual Total Returns (1)

| | | |

| | | Since

Inception (7) | |

DCW at Market Price (“MP”) | | -34.36 | % |

DCW at Net Asset Value (“NAV”) (2) | | -23.20 | % |

FTSE EPRA/NAREIT Global Real Estate Index® (3) | | -6.48 | % |

Wachovia Hybrid & Preferred Securities REIT IndexSM (4) | | -14.93 | % |

Lehman Brothers Investment Grade CMBS Index™ (5) | | 4.51 | % |

Trading History (1)(6)

| | | | | |

| | Average Premium/Discount to NAV | |

| | 1-Month | | -5.06 | % |

| | 3-Month | | -4.24 | % |

| | 1-Year | | N/A | |

| | Since Inception | | 0.68 | % |

| | Since Inception Price History Range | |

| | MP | | $11.47 - $20.20 | |

| | NAV | | $13.56 - $19.11 | |

(1) | Past performance is no guarantee of future results. Investors cannot invest directly into any index. This chart is for illustrative purposes only and does not relate to the future performance of the Fund. For current to the most recent month-end performance, visit dividendcapital.com, or call 866.DCG.REIT (324.7348). Performance data quoted above is historical. Current performance may be higher or lower than the performance data quoted. Performance does not include transaction fees that may be charge our financial advisor or brokerage firm. |

(2) | Total return assumes reinvestment of dividend and capital gain distributions. Investors cannot invest at NAV. |

(3) | The FTSE EPRA/NAREIT Global Real Estate Index® is a market capitalization weighted index, based on the last trade price of shares of all eligible companies. The index is structured in such a way that it can be considered to represent general trends in all eligible real estate stocks worldwide. The index is designed to reflect the stock performance of companies engaged in specific aspects of the North American, European and Asian real estate markets as perceived by institutional investors. Relevant real estate activities are defined as the ownership, disposure and development of income-producing real estate. |

(4) | The Wachovia Hybrid & Preferred Securities REIT IndexSM is a capitalization weighted unmanaged index of exchange listed perpetual REIT preferred stocks and depository shares. The index is compiled by Wachovia Capital Markets, LLC and calculated by the American Stock Exchange. The Fund expects to invest in securities not included in this index, such as debt securities which may have lower returns than preferred stock, and common stock and non-U.S. securities which may be riskier than U.S. preferred stock. This index also includes securities in which the Fund will not invest. |

11

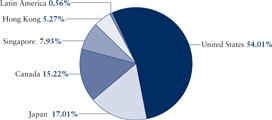

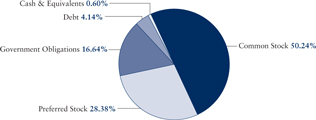

PORTFOLIO PROFILE

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

Country Allocation (8)(9)(11)

Security Type Allocation(8)(10)(11)

(5) | The Lehman Brothers Investment Grade CMBS Index™ is an unmanaged index of investment grade commercial mortgage backed securities (CMBS). This index is used because the fund may invest in debt securities of global real estate companies. The index only represents CMBS of U.S. real estate companies while the fund may invest in CMBS and other debt securities of global real estate companies. The fund expects to invest in securities not included in this index, such as common stock, preferred stock and non-U.S. securities which may be riskier than U.S. debt securities. This index also includes securities in which the fund will not invest. |

(6) | Market price and NAV price history are since inception, based upon closing market price. |

(7) | Fund inception is 06/27/2007. |

(8) | Allocation percentages are based on the fund’s direct investments and indirect economic exposure. Indirect economic exposure is generally obtained through the use of total return swaps and such exposure is calculated by using the investment’s notional value plus or minus related unrealized gains or losses. |

(9) | Country allocation percentages are based on the market value of the fund’s direct and indirect economic exposure exclusive of cash or U.S. government obligations. |

(10) | Security type allocation percentages are based on the market value of the fund’s direct and indirect economic exposure including cash and U.S. government obligations. |

(11) | Holdings and composition of holdings are subject to change, and may not be representative of future investments. |

12

STATEMENTOF INVESTMENTS

December 31, 2007

Dividend Capital Realty Income Allocation Fund

| | | | | |

| | | Shares | | Market

Value |

COMMON STOCK 32.10% | | | | | |

Apartments 0.49% | | | | | |

Essex Property Trust | | 5,900 | | $ | 575,191 |

| | |

Diversified/Miscellaneous 1.25% | | | | | |

Cousins Properties Inc. | | 9,300 | | | 205,530 |

Vornado Realty Trust | | 14,400 | | | 1,266,480 |

| | | | | |

| | | | | 1,472,010 |

| | | | | |

| | |

Health Care 0.84% | | | | | |

HCP Inc. | | 15,300 | | | 532,134 |

Ventas Inc. | | 10,200 | | | 461,550 |

| | | | | |

| | | | | 993,684 |

| | | | | |

| | |

Hotels 0.80% | | | | | |

Host Hotels & Resorts Inc. | | 20,000 | | | 340,800 |

LaSalle Hotel Properties | | 12,000 | | | 382,800 |

Starwood Hotels & Resorts Worldwide Inc. | | 5,100 | | | 224,553 |

| | | | | |

| | | | | 948,153 |

| | | | | |

| | |

Industrial 1.18% | | | | | |

AMB Property Corp. | | 13,200 | | | 759,792 |

ProLogis | | 9,900 | | | 627,462 |

| | | | | |

| | | | | 1,387,254 |

| | | | | |

| | |

Mortgage – Commercial 7.18% | | | | | |

Anthracite Capital Inc. | | 501,500 | | | 3,630,860 |

iStar Financial Inc. | | 37,300 | | | 971,665 |

Resource Capital Corp. | | 412,300 | | | 3,838,513 |

Resource Capital Corp.—Warrants* | | 55,000 | | | 38,399 |

| | | | | |

| | | | | 8,479,437 |

| | | | | |

| | |

Net Lease 2.17% | | | | | |

Entertainment Properties Trust | | 24,700 | | | 1,160,900 |

National Retail Properties Inc. | | 10,500 | | | 245,490 |

Realty Income Corp. | | 42,800 | | | 1,156,456 |

| | | | | |

| | | | | 2,562,846 |

| | | | | |

| | |

Office – Central Business District 2.17% | | | | | |

Boston Properties Inc. | | 16,700 | | | 1,533,227 |

SL Green Realty Corp. | | 11,000 | | | 1,028,060 |

| | | | | |

| | | | | 2,561,287 |

| | | | | |

Footnotes to DCA Statement of Investments on page 19.

13

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

| | | | | |

| | | Shares | | Market

Value |

COMMON STOCK (continued) | | | | | |

Office – Suburban 1.99% | | | | | |

Alexandria Real Estate Equities Inc. | | 7,000 | | $ | 711,690 |

Digital Realty Trust Inc. | | 14,400 | | | 552,528 |

Duke Realty Corp. | | 10,900 | | | 284,272 |

Highwoods Properties Inc. | | 27,300 | | | 802,074 |

| | | | | |

| | | | | 2,350,564 |

| | | | | |

| | |

Other Real Estate Companies 0.50% | | | | | |

Brookfield Properties Corp. | | 30,500 | | | 587,125 |

| | |

Regional Malls 2.54% | | | | | |

Pennsylvania Real Estate Investment Trust | | 7,000 | | | 207,760 |

Simon Property Group Inc. | | 24,900 | | | 2,162,814 |

Taubman Centers Inc. | | 12,800 | | | 629,632 |

| | | | | |

| | | | | 3,000,206 |

| | | | | |

| | |

Self Storage 0.73% | | | | | |

Public Storage Inc. | | 11,700 | | | 858,897 |

| | |

Shopping Centers 1.98% | | | | | |

Federal Realty Investment Trust | | 22,600 | | | 1,856,590 |

Kimco Realty Corp. | | 13,200 | | | 480,480 |

| | | | | |

| | | | | 2,337,070 |

| | | | | |

| | |

Speciality Finance 8.28% | | | | | |

Arbor Realty Trust Inc. | | 73,100 | | | 1,177,641 |

Deerfield Triarc Capital Corp. | | 261,800 | | | 2,094,400 |

Gramercy Capital Corp. | | 140,400 | | | 3,413,124 |

KKR Financial Holdings LLC. | | 37,234 | | | 523,138 |

NorthStar Realty Finance Corp. | | 288,500 | | | 2,573,420 |

| | | | | |

| | | | | 9,781,723 |

| | | | | |

TOTAL COMMON STOCK (Cost $48,144,513) | | | | | 37,895,447 |

| | | | | |

Footnotes to DCA Statement of Investments on page 19.

14

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

| | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Shares | | Market

Value |

PREFERRED STOCK 73.28% | | | | | | | |

Apartments 2.83% | | | | | | | |

Apartment Investment & Management Co.: | | | | | | | |

Series U, 7.750% (3) | | Ba3/B+ | | 44,200 | | $ | 924,664 |

Series V, 8.000% (3) | | Ba3/B+ | | 75,700 | | | 1,554,121 |

BRE Properties Inc.: | | | | | | | |

Series C, 6.750% | | Baa3/BBB- | | 15,000 | | | 290,100 |

Series D, 6.750% | | Baa3/BBB- | | 28,500 | | | 570,000 |

| | | | | | | |

| | | | | | | 3,338,885 |

| | | | | | | |

| | | |

Hotels 26.58% | | | | | | | |

Ashford Hospitality Trust: | | | | | | | |

Series A, 8.550% (3) | | NR/NR | | 93,300 | | | 1,749,375 |

AP AIMCAP Corp., Series A, 8.250% (2)(4)* | | NR/NR | | 212,600 | | | 4,230,549 |

FelCor Lodging Trust Inc., Series C, 8.000% (3) | | B2/B- | | 259,000 | | | 4,804,450 |

Hersha Hospitality Trust, Series A, 8.000%(3) | | NR/NR | | 75,300 | | | 1,611,420 |

Innkeepers USA Trust, Series C, 8.000% | | NR/NR | | 40,100 | | | 481,200 |

LaSalle Hotel Properties, Series G, 7.250%(3) | | NR/NR | | 434,000 | | | 7,490,840 |

Strategic Hotels & Resorts Inc.: | | | | | | | |

Series A, 8.500% (3) | | NR/NR | | 177,500 | | | 3,333,450 |

Series C, 8.250% (3) | | NR/NR | | 259,000 | | | 5,050,500 |

Sunstone Hotel Investors Inc., Series A, 8.000% (3) | | NR/NR | | 134,800 | | | 2,632,644 |

| | | | | | | |

| | | | | | | 31,384,428 |

| | | | | | | |

| | | |

Manufactured Housing 2.83% | | | | | | | |

Hilltop Holdings Inc., | | | | | | | |

Series A, 8.250% (3) | | NR/NR | | 150,400 | | | 3,335,120 |

| | | |

Mortgage – Commercial 4.04% | | | | | | | |

Anthracite Capital Inc., | | | | | | | |

Series D, 8.250% (3) | | NR/NR | | 140,000 | | | 2,212,000 |

Newcastle Investment Corp., | | | | | | | |

Series C, 8.050% (3) | | NR/NR | | 165,000 | | | 2,557,500 |

| | | | | | | |

| | | | | | | 4,769,500 |

| | | | | | | |

| | | |

Mortgage – Residential 0.02% | | | | | | | |

American Home Mortgage Investment Corp.: | | | | | | | |

Series A, 9.750% (9) | | NR/NR | | 266,950 | | | 21,356 |

Series B, 9.250% (9) | | NR/NR | | 29,700 | | | 1,485 |

| | | | | | | |

| | | | | | | 22,841 |

| | | | | | | |

Footnotes to DCA Statement of Investments on page 19.

15

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

| | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Shares | | Market

Value |

PREFERRED STOCK (continued) | | | | | | | |

Net Lease 1.64% | | | | | | | |

Entertainment Properties Trust, | | | | | | | |

Series B, 7.750% (3) | | NR/NR | | 93,400 | | $ | 1,942,720 |

Office – Central Business District 1.42% | | | | | | | |

Maguire Properties Inc., | | | | | | | |

Series A, 7.625% (3) | | NR/NR | | 120,000 | | | 1,672,800 |

Office – Suburban 11.42% | | | | | | | |

BioMed Realty Trust Inc., Series A, 7.375%(3) | | NR/NR | | 365,000 | | | 7,464,250 |

Brandywine Realty Trust: | | | | | | | |

Series C, 7.500% | | NR/NR | | 38,831 | | | 793,706 |

Series D, 7.375% (3) | | NR/NR | | 47,000 | | | 930,600 |

Digital Realty Trust Inc.: | | | | | | | |

Series A, 8.500% (3) | | NR/NR | | 174,300 | | | 3,923,493 |

Series B, 7.875% | | NR/NR | | 16,800 | | | 372,120 |

| | | | | | | |

| | | | | | | 13,484,169 |

| | | | | | | |

Regional Malls 3.13% | | | | | | | |

CBL & Associates Properties Inc., | | NR/NR | | 41,000 | | | 803,600 |

Series D, 7.375% (3) | | | | | | | |

Glimcher Realty Trust, Series G, 8.125% (3) | | B1/B | | 60,000 | | | 1,146,000 |

Taubman Centers Inc.: | | | | | | | |

Series G, 8.000% (3) | | B1/NR | | 67,000 | | | 1,584,550 |

Series H, 7.625% | | B1/NR | | 6,600 | | | 157,080 |

| | | | | | | |

| | | | | | | 3,691,230 |

| | | | | | | |

Shopping Centers 3.87% | | | | | | | |

Kimco Realty Corp., Series G, 7.75% | | Baa2/BBB+ | | 200,000 | | | 4,572,000 |

| | | |

Speciality Finance 15.50% | | | | | | | |

CapLease Inc., Series A, 8.125% (3) | | NR/NR | | 156,700 | | | 3,018,042 |

Gramercy Capital Corp., Series A, 8.125% (3) | | NR/NR | | 280,000 | | | 5,516,000 |

NorthStar Realty Finance Corp.: | | | | | | | |

Series A, 8.750% (3) | | NR/NR | | 353,600 | | | 5,852,080 |

Series B, 8.250% (3) | | NR/NR | | 246,400 | | | 3,920,224 |

| | | | | | | |

| | | | | | | 18,306,346 |

| | | | | | | |

TOTAL PREFERRED STOCK (Cost $120,587,932) | | | | | | | 86,520,039 |

| | | | | | | |

Footnotes to DCA Statement of Investments on page 19.

16

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

| | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Shares/Principal

Amount | | Market

Value |

COMMERCIAL REAL ESTATE | | | | | | | |

COLLATERALIZED DEBT OBLIGATIONS 14.02% | | | | | | | |

CW Capital Cobalt II, Ltd.: | | | | | | | |

Series K, 8.203%, 04/26/2016 (1)(2)(4)(6)(8) | | Ba2/BB | | 4,000,000 | | $ | 3,121,612 |

Class P.S., 16.586%, 04/26/2016 (1)(2)(4)(6)(7) | | NR/NR | | 3,500,000 | | | 1,697,045 |

Lenox Street, Series 2007-1, 15.173%, | | | | | | | |

06/04/2017 (1)(2)(4)(6)(7) | | NR/NR | | 1,000,000 | | | 542,061 |

Sorin Real Estate CDO II Ltd., Series 2005 2A, | | | | | | | |

Class H, 8.703%, 01/04/2016 (1)(2)(4)(6)(8) | | Ba3/BB | | 7,500,000 | | | 4,791,488 |

Taberna Preferred Funding III Ltd., Class E, | | | | | | | |

9.203%, 11/05/2015 (1)(2)(4)(6)(8)(9) | | NR/B+ | | 2,000,000 | | | 256,820 |

Taberna Preferred Funding V Ltd. | | | | | | | |

Class B-IL, 7.453%, 02/05/2016 (1)(2)(4)(6)(8)(9) | | NR/B | | 3,000,000 | | | 34,929 |

Class B-2L, 9.453%, 02/05/2016 (1)(2)(4)(6)(8)(9) | | NR/CCC- | | 3,000,000 | | | 31,485 |

Vertical CRE CDO 2006-I, Ltd.: | | | | | | | |

Class G, 8.703%, 04/22/2013 (1)(2)(4)(6)(8) | | NR/BB+ | | 6,500,000 | | | 4,853,940 |

Class P.S., 15.508%, 04/22/2013 (1)(2)(4)(6)(7) | | NR/NR | | 1,800,000 | | | 1,224,000 |

TOTAL COMMERCIAL REAL ESTATE COLLATERALIZED DEBT OBLIGATIONS (Cost $32,263,574) | | | | | | | 16,553,380 |

| | | | | | | |

| | | |

COLLATERALIZED LOAN OBLIGATIONS 11.20% | | | | | | | |

Babson CLO 2005-III, Ltd., | | | | | | | |

20.810%, 11/11/2019 (1)(2)(4)(6)(7) | | NR/NR | | 13,000,000 | | | 10,930,946 |

Fraser Sullivan CLO I Ltd., | | | | | | | |

8.177%, 03/15/2017 (1)(2)(4)(6)(7) | | NR/NR | | 3,400,000 | | | 2,291,233 |

TOTAL COLLATERALIZED LOAN OBLIGATIONS (Cost $16,400,000) | | | | | | | 13,222,179 |

| | | | | | | |

| | | |

COMMERCIAL MORTGAGE-BACKED SECURITIES 0.95% | | | | | | | |

JP Morgan Chase, Series 2005-LDP2, | | | | | | | |

Class M, 5.806%, 06/15/2016 (1)(2)(4)(6)(8) | | Ba3/BB | | 1,597,000 | | | 977,667 |

Wachovia Bank, | | | | | | | |

Series 2005 C18, 7.028%, 05/19/2015 (1)(4)(6) | | B1/B+ | | 248,100 | | | 145,998 |

TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES (Cost $1,434,067) | | | | | | | 1,123,665 |

| | | | | | | |

| | | |

LOAN PARTICIPATIONS 3.79% | | | | | | | |

Mervyn’s Junior Syndication Mezzanine, | | | | | | | |

8.100%, 01/01/2008 (2)(4)(8) | | NR/NR | | 4,476,028 | | | 4,476,028 |

TOTAL LOAN PARTICIPATIONS (Cost $4,476,028) | | | | | | | 4,476,028 |

| | | | | | | |

Footnotes to DCA Statement of Investments on page 19.

17

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

| | | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Shares/Principal

Amount | | Market

Value | |

U.S. GOVERNMENT OBLIGATIONS 7.87% | | | | | | | | |

U.S. Treasury Notes, 4.125%, 08/15/2008 (5) | | | | 8,525,000 | | $ | 8,563,635 | |

U.S. Treasury Bills, 01/24/2008 (5) * | | | | 730,000 | | | 728,834 | |

TOTAL U.S. GOVERNMENT OBLIGATIONS (Cost $9,233,388) | | | | | | | 9,292,469 | |

| | | | | | | | |

| | | |

NON-REGISTERED INVESTMENT COMPANIES 2.68% | | | | | | | | |

INVESCO Navigator Fund, 8.665% (1)(2)(4) | | NR/NR | | 3,946 | | | 3,171,195 | |

TOTAL NON-REGISTERED INVESTMENT COMPANIES (Cost $3,946,000) | | | | | | | 3,171,195 | |

| | | | | | | | |

| | | |

REPURCHASE AGREEMENTS 0.49% | | | | | | | | |

State Street Bank & Trust Co., dated 12/31/2007, 2.75%, due 01/02/2008, proceeds of $577,609 collateralized by Fannie Mae, 6.000%, 05/15/2008, valued at $578,233 including accrued interest | | NR/NR | | 577,609 | | | 577,609 | |

TOTAL REPURCHASE AGREEMENTS (Cost $577,609) | | | | | | | 577,609 | |

| | | | | | | | |

TOTAL INVESTMENTS 146.39% (Cost $237,063,111) | | | | | | $ | 172,832,011 | |

Liabilities in Excess of Other Assets (46.39%) | | | | | | | (54,770,359 | ) |

| | | | | | | | |

NET ASSETS 100.00% | | | | | | $ | 118,061,652 | |

| | | | | | | | |

Footnotes to DCA Statement of Investments:

| * | Non-income producing security. |

(1) | This security was purchased pursuant to the terms of a private placement memorandum and is exempt from registration under the Securities Act of 1933, as amended (the “Securities Act”), pursuant to Rule 144A of the Securities Act. This security may only be sold in transactions exempt from registration under the Securities Act, which most commonly involves a sale to “qualified institutional buyers” under Rule 144A. As of December 31,2007 the value of these securities amounted to $34,070,419 or 19.71% of total investments. |

(2) | This security has been valued at its fair value determined in good faith by or under the direction of the Board of Trustees. |

(3) | All or a portion of the shares held in this security are pledged as collateral for the borrowings under the Revolving Credit and Security Agreement (Note 6). |

(4) | This security is considered illiquid by the Adviser. |

(5) | All or a portion of the entire principal amount of this security is pledged as collateral for total return swap agreements. |

(6) | The expected maturity date listed herein differs from the legal maturity date due to the expected schedule of principal payments. |

(7) | This security represents a junior tranche whereby the holder is entitled to all residual interest, if any, which can vary. The rate listed is the Adviser’s estimated rate of residual interest as of the reporting date. |

(8) | The coupon rate shown on floating or adjustable rate securities represents the current effective rate at each period. |

See accompanying Notes to Financial Statements.

18

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Realty Income Allocation Fund (continued)

Open Interest Rate Swap Contracts as of December 31, 2007

| | | | | | | | | | | | | | | | | | | |

Counterparty | | Termination

Date | | Underlying

Notional | | Fixed Rate Paid

by the Fund at

12/31/07 | | | Floating Rate

Received by

the Fund at

12/31/07 | | | Net Interest

Receivable | | | Unrealized

Depreciation | |

JPMorgan Chase | | 06/14/2012 | | $ | 27,000,000 | | 4.090 | % | | 5.103 | %* | | $ | 13,669 | | | $ | (469,086 | ) |

JPMorgan Chase | | 06/14/2010 | | | 27,000,000 | | 3.890 | % | | 5.103 | %* | | | 16,369 | | | | (230,099 | ) |

Royal Bank of Canada | | 08/30/2012 | | | 32,000,000 | | 4.845 | % | | 4.839 | %** | | | (183 | ) | | | (568,130 | ) |

| | | | | | | | | | | | | | | | | | | |

Total | | | | | | | | | | | | | $ | 29,855 | | | $ | (1,267,315 | ) |

| | | | | | | | | | | | | | | | | | | |

| * | Based on one-month LIBOR (London Interbank Offered Rate). |

| ** | Based on three-month CDOR (Canadian Interbank Offered Rate). |

Open Total Return Swap Contracts (“TRS”) *** as of December 31, 2007

Counterparty: Royal Bank of Canada

| | | | | | | | | | | |

Contract Type | | Termination

Date | | Notional

Shares | | Underlying

Notional

($CAD) | | Unrealized

Appreciation

(Depreciation)

($USD) | |

Artis Real Estate Investment Trust TRS | | 09/27/2012 | | 100,000 | | $ | 1,760,720 | | $ | (258,088 | ) |

Calloway Real Estate Investment Trust TRS | | 11/30/2009 | | 145,000 | | | 3,233,500 | | | 321,748 | |

Canadian Apartment Properties Real Estate Investment Trust TRS | | 03/13/2009 | | 190,000 | | | 4,057,241 | | | (1,024,917 | ) |

Chartwell Senior Housing Real Estate Investment Trust TRS | | 08/2/2013 | | 175,000 | | | 2,450,000 | | | (469,882 | ) |

Dundee Real Estate Investment Trust TRS | | 10/18/2012 | | 113,593 | | | 4,327,893 | | | (504,116 | ) |

Firm Capital Mortgage Investment Funds TRS | | 08/2/2013 | | 160,000 | | | 1,728,000 | | | (110,239 | ) |

H&R Real Estate Investment Trust TRS | | 10/18/2012 | | 222,200 | | | 5,103,934 | | | (704,682 | ) |

Northern Property Real Estate Investment Trust TRS | | 10/18/2012 | | 188,000 | | | 4,248,800 | | | (47,621 | ) |

Primaris Retail Real Estate Investment Trust TRS | | 10/18/2012 | | 275,000 | | | 5,255,250 | | | (225,695 | ) |

| | | | | | | | | | | |

Total | | | | 1,568,793 | | $ | 32,165,338 | | $ | (3,023,492 | ) |

| | | | | | | | | | | |

| *** | For each total return swap contract, the Fund receives the total return and dividend income on the underlying security and pays a floating rate based on three-month CDOR (Canadian Interbank Offered Rate) plus a spread of 0.50%. |

19

STATEMENTOF INVESTMENTS

December 31, 2007

Dividend Capital Strategic Global Realty Fund

| | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Shares | | Market

Value |

COMMON STOCK 23.53% | | | | | | | |

Building - Heavy Construction 0.82% | | | | | | | |

Socovesa S.A. - Chile (1)* | | | | 80,000 | | $ | 863,200 |

Healthcare 2.00% | | | | | | | |

Medical Properties Trust, Inc. | | | | 205,000 | | | 2,088,950 |

Hotels 1.55% | | | | | | | |

Ashford Hospitality Trust, Inc. | | | | 225,000 | | | 1,617,750 |

Mortgage - Commercial 3.66% | | | | | | | |

iStar Financial, Inc. | | | | 146,600 | | | 3,818,930 |

Real Estate Operators & Developers 1.15% | | | | | | | |

Franshion Properties China Ltd. - Hong Kong* | | | | 1,835,000 | | | 986,053 |

Sino-Ocean Land Holdings Ltd. - Hong Kong* | | | | 173,000 | | | 214,325 |

| | | | | | | |

| | | | | | | 1,200,378 |

| | | | | | | |

Specialty Finance 14.35% | | | | | | | |

Arbor Realty Trust Inc. | | | | 88,000 | | | 1,417,680 |

Gramercy Capital Corp. | | | | 236,000 | | | 5,737,160 |

JER Investors Trust Inc. | | | | 295,000 | | | 3,177,150 |

NorthStar Realty Finance Corp. | | | | 522,000 | | | 4,656,240 |

| | | | | | | |

| | | | | | | 14,988,230 |

| | | | | | | |

TOTAL COMMON STOCK | | | | | | | |

(Cost $ 32,913,316) | | | | | | | 24,577,438 |

| | | | | | | |

PREFERRED STOCK 50.22% | | | | | | | |

Apartments 1.89% | | | | | | | |

BRE Properties, Inc.: | | | | | | | |

Series C, 6.750% | | Baa3/BBB- | | 85,000 | | | 1,643,900 |

Series D, 6.750% | | Baa3/BBB- | | 16,600 | | | 332,000 |

| | | | | | | |

| | | | | | | 1,975,900 |

| | | | | | | |

Diversified/Miscellaneous 2.36% | | | | | | | |

Vornado Realty Trust: | | | | | | | |

Series F, 6.750% | | Baa3/BBB- | | 109,000 | | | 2,247,580 |

Series I/L, 6.625% | | Baa3/BBB- | | 11,000 | | | 217,470 |

| | | | | | | |

| | | | | | | 2,465,050 |

| | | | | | | |

Footnotes to DCW Statement of Investments on page 25.

20

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

| | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Shares | | Market

Value |

PREFERRED STOCK (continued) | | | | | | | |

Hotels 10.72% | | | | | | | |

Ashford Hospitality Trust, Inc., | | | | | | | |

Series D, 8.450% | | NR/NR | | 264,000 | | $ | 5,016,000 |

Hospitality Properties Trust, | | | | | | | |

Series C, 7.000% | | Baa3/BB+ | | 34,447 | | | 620,046 |

LaSalle Hotel Properties: | | | | | | | |

Series D, 7.500% | | NR/NR | | 76,400 | | | 1,398,120 |

Series E, 8.000% | | NR/NR | | 10,000 | | | 191,000 |

Series G, 7.250% | | NR/NR | | 27,500 | | | 474,650 |

Strategic Hotels & Resorts Inc.: | | | | | | | |

Series B, 8.250% | | NR/NR | | 74,530 | | | 1,434,703 |

Series C, 8.250% | | NR/NR | | 54,000 | | | 1,053,000 |

Sunstone Hotel Investors Inc., | | | | | | | |

Series A, 8.000% | | NR/NR | | 51,400 | | | 1,003,842 |

| | | | | | | |

| | | | | | | 11,191,361 |

| | | | | | | |

Industrial 0.47% | | | | | | | |

AMB Property Corp., Series M, 6.750% | | Baa2/BBB- | | 23,500 | | | 495,850 |

Mortgage – Commercial 5.37% | | | | | | | |

iStar Financial, Inc.: | | | | | | | |

Series F, 7.800% | | Ba1/BB+ | | 80,000 | | | 1,540,000 |

Series I, 7.500% | | Ba1/BB+ | | 62,000 | | | 1,140,800 |

Newcastle Investment Corp., | | | | | | | |

Series D, 8.375% | | NR/NR | | 200,000 | | | 2,924,000 |

| | | | | | | |

| | | | | | | 5,604,800 |

| | | | | | | |

Net Lease 2.55% | | | | | | | |

Entertainment Properties Trust, | | | | | | | |

Series B, 7.750% | | NR/NR | | 40,000 | | | 832,000 |

Lexington Realty Trust, | | | | | | | |

Series D, 7.550% | | NR/NR | | 12,800 | | | 244,480 |

Realty Income Corp., | | | | | | | |

Series E, 6.750% | | Baa2/BBB- | | 75,000 | | | 1,587,000 |

| | | | | | | |

| | | | | | | 2,663,480 |

| | | | | | | |

Office – Central Business District 2.90% | | | | | | | |

SL Green Realty Corp., | | | | | | | |

Series C, 7.625% | | NR/NR | | 133,200 | | | 3,028,968 |

Footnotes to DCW Statement of Investments on page 25.

21

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

| | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Shares | | Market

Value |

PREFERRED STOCK (continued) | | | | | | | |

Office - Suburban 7.99% | | | | | | | |

BioMed Realty Trust Inc., | | | | | | | |

Series A, 7.375% | | NR/NR | | 225,000 | | $ | 4,601,250 |

Digital Realty Trust Inc., | | | | | | | |

Series B, 7.875% | | NR/NR | | 50,000 | | | 1,107,500 |

Kilroy Realty Corp., | | | | | | | |

Series F, 7.500% | | NR/NR | | 120,000 | | | 2,640,000 |

| | | | | | | |

| | | | | | | 8,348,750 |

| | | | | | | |

Regional Malls 2.29% | | | | | | | |

CBL & Associates Properties Inc., | | | | | | | |

Series C, 7.750% | | NR/NR | | 30,000 | | | 660,000 |

Glimcher Realty Trust, | | | | | | | |

Series G, 8.125% | | B1/B | | 90,400 | | | 1,726,640 |

| | | | | | | |

| | | | | | | 2,386,640 |

| | | | | | | |

Shopping Centers 9.19% | | | | | | | |

Kimco Realty Corp., | | | | | | | |

Series G, 7.750% | | Baa2/BBB+ | | 400,000 | | | 9,144,000 |

Regency Centers Corp., | | | | | | | |

Series C, 7.450% | | Baa3/BBB | | 20,500 | | | 452,025 |

| | | | | | | |

| | | | | | | 9,596,025 |

| | | | | | | |

Storage 2.05% | | | | | | | |

Public Storage, Inc.: | | | | | | | |

Series E, 6.750% | | Baa1/BBB+ | | 16,900 | | | 331,409 |

Series M, 6.625% | | Baa1/BBB+ | | 95,000 | | | 1,805,000 |

| | | | | | | |

| | | | | | | 2,136,409 |

| | | | | | | |

Speciality Finance 2.44% | | | | | | | |

Gramercy Capital Corp., | | | | | | | |

Series A, 8.125% | | NR/NR | | 80,000 | | | 1,576,000 |

NorthStar Realty Finance Corp.: | | | | | | | |

Series A, 8.750% | | NR/NR | | 39,500 | | | 653,725 |

Series B, 8.250% | | NR/NR | | 20,000 | | | 318,200 |

| | | | | | | |

| | | | | | | 2,547,925 |

| | | | | | | |

TOTAL PREFERRED STOCK | | | | | | | |

(Cost $64,039,063) | | | | | | | 52,441,158 |

| | | | | | | |

Footnotes to DCW Statement of Investments on page 25.

22

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

| | | | | | | | | |

| | | Bond Rating

Moody’s/S&P

(Unaudited) | | Principal

Amount | | Market

Value | |

COMMERCIAL REAL ESTATE | | | | | | | | | |

COLLATERALIZED DEBT OBLIGATIONS 7.32% | | | | | | | | | |

Gramercy Real Estate, Series 2007-1A: | | | | | | | | | |

Class GFX, 6.000%, 08/15/2016 (1)(2)(3)(4) | | NR/BBB | | $ | 2,000,000 | | $ | 1,286,260 | |

Class HFX, 6.000%, 08/15/2016 (1)(2)(3)(4) | | NR/BBB- | | | 5,150,000 | | | 2,985,713 | |

Morgan Stanley Capital I, 2007-SRR4, | | | | | | | | | |

Series G, 7.240%, 06/20/2016 (1)(2)(3)(4) | | NR/NR | | | 5,750,000 | | | 3,370,650 | |

| | | |

TOTAL COMMERCIAL REAL ESTATE | | | | | | | | | |

COLLATERALIZED DEBT OBLIGATIONS | | | | | | | | | |

(Cost $11,649,504) | | | | | | | | 7,642,623 | |

| | | | | | | | | |

| | | |

U.S. GOVERNMENT OBLIGATIONS 29.45% | | | | | | | | | |

U.S. Treasury Bills: | | | | | | | | | |

2.260%, 01/24/2008 (5) | | | | | 1,300,000 | | | 1,298,107 | |

2.280%, 01/24/2008 (5) | | | | | 29,500,000 | | | 29,457,044 | |

TOTAL U.S. GOVERNMENT OBLIGATIONS | | | | | | | | | |

(Cost $30,755,151) | | | | | | | | 30,755,151 | |

| | | | | | | | | |

| | | |

REPURCHASE AGREEMENTS 1.05% | | | | | | | | | |

State Street Bank & Trust Co. , dated 12/31/2007, 2.75%, due 01/02/2008, proceeds of $1,087,000 collateralized by Fannie Mae, 6.00%, 05/15/2008, valued at $ 1,100,769 including accrued interest. | | | | | 1,100,305 | | | 1,100,305 | |

| | | |

TOTAL REPURCHASE AGREEMENTS | | | | | | | | | |

(Cost $1,100,305) | | | | | | | | 1,100,305 | |

| | | | | | | | | |

| | | |

TOTAL INVESTMENTS 111.57% | | | | | | | $ | 116,516,675 | |

(Cost $140,457,339) | | | | | | | | | |

Liabilities in Excess of Other Assets (11.57%) | | | | | | | | (12,084,020 | ) |

| | | | | | | | | |

NET ASSETS 100.00% | | | | | | | $ | 104,432,655 | |

| | | | | | | | | |

Footnotes to DCW Statement of Investments on page 25.

23

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

Footnotes to DCW Statement of Investments:

| * | Non-incoming producing security. |

(1) | This security was purchased pursuant to the terms of a private placement memorandum and is exempt from registration under the Securities Act of 1933, as amended (the “Securities Act”), pursuant to Rule 144A of the Securities Act. This security may only be sold in transactions exempt from registration under the Securities Act, which most commonly involves a sale to “qualified institutional buyers” under Rule 144A. As of December 31,2007 the value of these securities amounted to $8,505,823 or 7.30% of total investments. |

(2) | This security has been valued at fair values determined in good faith by or under the direction of the Board of Trustees. |

(3) | The expected maturity date of this security listed herein is earlier than/later than the legal maturity date of the security due to the expected acceleration/deceleration of the schedule of principal payments by the issuer. |

(4) | This security is considered illiquid by the Adviser. |

(5) | All or a portion of the principal amount of this security is pledged as collateral for total return swap agreements. See accompanying Notes to Financial Statements. |

Open Interest Rate Swap Contracts as of December 31, 2007

| | | | | | | | | | | | | | | | | | |

Counter Party | | Termination

Date | | Underlying Notional

(local currency) | | Fixed Rate Paid

by the Fund at

12/31/07 | | | Floating Rate

Received by

the Fund at

12/31/07 | | | Net Interest

Receivable | | | Unrealized

Depreciation

($USD) | |

Royal Bank of Canada | | 08/30/2012 | | 26,000,000 CAD | | 4.85 | % | | 4.84 | % * | | $ | (149 | ) | | $ | (471,738 | ) |

Deutsche Bank | | 10/4/2012 | | 3,604,314,133 JPY | | 1.45 | % | | 1.00 | % ** | | | (49,515 | ) | | | (412,954 | ) |

| | 10/4/2012 | | 21,500,000 SGD | | 3.02 | % | | 1.90 | % *** | | | (20,316 | ) | | | (37,366 | ) |

| | | | | | | | | | | | | | | | | | |

Total | | | | | | | | | | | | | | | | $ | (922,058 | ) |

| | | | | | | | | | | | | | | | | | |

| * | Based on three-month CDOR (Canadian Interbank Offered Rate). |

| ** | Based on one-month TIBOR (Tokyo Interbank Domestic Yen Offered Rate). |

| *** | Based on one-month fixing SGD swap. |

24

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

Open Total Return Swap Contracts (“TRS”)^ as of December 31, 2007

| | | | | | | | | | |

Counter Party Contract Type | | Termination

Date | | Notional

Shares | | Underlying

Notional

(local currency) | | Unrealized

Appreciation

/(Depreciation)

($USD) | |

Deutsche Bank | | | | | | | | | | |

Ascendas Real Estate Investment Trust TRS | | 07/27/2010 | | 2,517,000 | | 7,851,339 SGD | | $ | (1,152,884 | ) |

Ascott Residence Trust TRS | | 07/27/2010 | | 1,668,000 | | 3,356,795 SGD | | | (686,536 | ) |

CapitaMall Trust TRS | | 07/27/2010 | | 820,000 | | 3,326,078 SGD | | | (339,628 | ) |

CDL Hospitality Trusts TRS | | 07/27/2010 | | 1,351,000 | | 3,487,952 SGD | | | (217,515 | ) |

Champion Real Estate Investment Trust TRS | | 07/26/2010 | | 5,934,000 | | 28,087,402 HKD | | | (124,265 | ) |

DA Office Investment Corporation TRS | | 08/02/2010 | | 520 | | 409,943,676 JPY | | | (299,545 | ) |

Frasers Centrepoint Trust TRS | | 08/02/2010 | | 1,977,000 | | 3,477,893 SGD | | | (410,902 | ) |

Japan Hotel and Resort, Inc. TRS | | 08/02/2010 | | 811 | | 515,659,773 JPY | | | (1,574,102 | ) |

Japan Logistics Fund, Inc. TRS | | 08/02/2010 | | 230 | | 276,140,038 JPY | | | (808,307 | ) |

Japan Real Estate Investment Corporation TRS | | 08/02/2010 | | 373 | | 542,304,671 JPY | | | (179,964 | ) |

Japan Retail Fund Investment Corporation TRS | | 08/02/2010 | | 380 | | 417,200,211 JPY | | | (1,023,499 | ) |

Kenedix Realty Investment Corporation TRS | | 08/02/2010 | | 460 | | 411,595,068 JPY | | | (612,586 | ) |

Nippon Building Fund, Inc. TRS | | 08/02/2010 | | 320 | | 557,724,060 JPY | | | (495,225 | ) |

Nippon Residential Investment Corporation TRS | | 08/02/2010 | | 660 | | 466,258,344 JPY | | | (1,196,064 | ) |

Sunlight Real Estate Investment Trust TRS | | 07/26/2010 | | 11,250,000 | | 25,628,965 HKD | | | 89,265 | |

| ^ | For each total return swap contract, the Fund receives the total return on dividend income on the underlying security and pays a floating rate based on local interest rates plus a spread of 0.30% to 0.50%. |

SGD – Singapore Dollar

HKD – Hong Kong Dollar

JPY – Japanese Yen

25

STATEMENTOF INVESTMENTS (CONTINUED)

December 31, 2007

Dividend Capital Strategic Global Realty Fund (continued)

Open Total Return Swap Contracts (“TRS”)^ as of December 31, 2007

(continued)

| | | | | | | | | | |

Counter Party Contract Type | | Termination

Date | | Notional

Shares | | Underlying

Notional

(local currency)

(CAD$) | | Unrealized

Appreciation

/(Depreciation)

($ USD) | |

Royal Bank of Canada | | | | | | | | | | |

Allied Properties Real Estate Investment Trust TRS | | 07/16/2012 | | 131,000 | | 2,812,989 | | $ | (97,319 | ) |

Artis Real Estate Investment Trust TRS | | 07/16/2012 | | 151,000 | | 2,619,790 | | | (350,301 | ) |

Artis Real Estate Investment Trust TRS | | 07/16/2012 | | 49,000 | | 833,015 | | | (96,332 | ) |

Calloway Real Estate Investment Trust TRS | | 07/16/2012 | | 88,300 | | 2,311,429 | | | (150,932 | ) |

Canadian Apartment Properties Real Estate Investment Trust TRS | | 07/16/2012 | | 180,000 | | 3,523,662 | | | (646,702 | ) |

Chartwell Senior Housing Real Estate Investment Trust TRS | | 07/16/2012 | | 148,000 | | 2,319,944 | | | (648,609 | ) |

H&R Real Estate Investment Trust TRS | | 07/16/2012 | | 127,000 | | 3,044,787 | | | (532,050 | ) |

Northern Property Real Estate Investment Trust TRS | | 07/16/2012 | | 117,000 | | 2,707,790 | | | (94,067 | ) |

Primaris Retail Real Estate Investment Trust TRS | | 07/16/2012 | | 115,000 | | 2,279,036 | | | (176,843 | ) |

RioCan Real Estate Investment Trust TRS | | 07/16/2012 | | 150,000 | | 3,766,455 | | | (499,980 | ) |

Total | | | | 26,777,054 | | | | $ | (12,324,892 | ) |

| ^ | For each total return swap contract, the Fund receives the total return on dividend income on the underlying security and pays a floating rate based on local interest rates plus a spread of 0.30% to 0.50% CAD- Canadian Dollar. |

26

STATEMENTSOF ASSETS & LIABILITIES

December 31, 2007

| | | | | | | | |

| | | Dividend Capital

Realty Income

Allocation Fund | | | Dividend Capital

Strategic Global

Realty Fund | |

ASSETS: | | | | | | | | |

Investments at market value | | $ | 172,832,011 | | | $ | 116,516,675 | |

Cash | | | — | | | | 1,100,305 | |

Receivable for securities sold | | | 2,385,348 | | | | — | |

Dividends and interest receivable | | | 3,068,772 | | | | 1,990,723 | |

Swap interest receivable | | | 149,959 | | | | 681,800 | |

Unrealized appreciation on swap agreements | | | 321,748 | | | | 89,265 | |

| | | | | | | | |

TOTAL ASSETS | | $ | 178,757,838 | | | $ | 120,378,768 | |

| | |

LIABILITIES: | | | | | | | | |

Line of credit payable to bank | | $ | 53,872,000 | | | $ | — | |

Distributions payable | | | 1,538,813 | | | | 496,544 | |

Payable for line of credit fees | | | 276,743 | | | | — | |

Payable for securities purchased | | | — | | | | 1,100,305 | |

Unrealized depreciation on swap agreements | | | 4,612,555 | | | | 13,336,215 | |

Swap interest payable | | | 5,581 | | | | 829,269 | |

Payable for investment advisory fees | | | 129,390 | | | | 87,195 | |

Payable for administrative fees | | | 15,223 | | | | 8,720 | |

Payable for trustees’ fee | | | 19,931 | | | | 9,828 | |

Payable for excise tax | | | 95,926 | | | | 21,434 | |

Other liabilities | | | 130,024 | | | | 56,603 | |

| | | | | | | | |

TOTAL LIABILITIES | | $ | 60,696,186 | | | $ | 15,946,113 | |

| | | | | | | | |

NET ASSETS | | $ | 118,061,652 | | | $ | 104,432,655 | |

| | | | | | | | |

| | |

COMPOSITION OF NET ASSETS: | | | | | | | | |

Common stock, $0.001 par value (unlimited number of shares authorized) | | $ | 13,989 | | | $ | 7,523 | |

Paid-in capital | | | 197,255,006 | | | | 143,365,588 | |

(Over)/undistributed net investment income | | | 3,249,478 | | | | (484,331 | ) |

Accumulated net realized loss on investments, swap contracts and foreign currency transactions | | | (13,934,914 | ) | | | (1,091,893 | ) |

Net unrealized depreciation of investments, swap contracts and translation of assets and liabilities denominated in foreign currencies | | | (68,521,907 | ) | | | (37,364,232 | ) |

| | | | | | | | |

NET ASSETS | | $ | 118,061,652 | | | $ | 104,432,655 | |

| | | | | | | | |

| | |

COST OF INVESTMENTS | | $ | 237,063,111 | | | $ | 140,457,339 | |

| | | | | | | | |

| | |

SHARES OUTSTANDING AND NET ASSET VALUE PER SHARE: | | | | | | | | |

Common shares outstanding, $0.001 par value (unlimited number of shares authorized) | | | 13,989,197 | | | | 7,522,785 | |

Net asset value per share | | $ | 8.44 | | | $ | 13.88 | |

See accompanying Notes to Financial Statements.

27

STATEMENTSOF OPERATIONS

December 31, 2007

| | | | | | | | | | | | |

| | | Dividend Capital Realty Income

Allocation Fund | | | Dividend Capital

Strategic Global

Realty Fund

Period Ended

December 31,

2007 (2) | |

| | Period Ended

December 31,

2007 (1) | | | Year Ended

September 30,

2007 | | |

INVESTMENT INCOME: | | | | | | | | | | | | |

Dividends (net of withholding taxes of $640, $4,353 and $0, respectively) | | $ | 398,568 | | | $ | 15,994,962 | | | $ | 3,791,833 | |

Interest | | | 1,371,245 | | | | 6,475,525 | | | | 1,464,057 | |

| | | | | | | | | | | | |

Total Investment Income | | | 1,769,813 | | | | 22,470,487 | | | | 5,255,890 | |

| | | |

EXPENSES: | | | | | | | | | | | | |

Line of credit interest and fees (Note 6) | | $ | 948,013 | | | | 4,874,287 | | | | — | |

Investment Advisory fees (Note 5) | | | 421,719 | | | | 2,427,190 | | | | 626,879 | |

Administrative fees (Note 5) | | | 49,614 | | | | 285,552 | | | | 62,688 | |

Trustee fees and expenses (Note 5) | | | 43,184 | | | | 118,397 | | | | 31,008 | |

Excise taxes | | | 95,926 | | | | — | | | | 21,434 | |

Custodian fees and expenses | | | 5,644 | | | | 17,707 | | | | 4,961 | |

Audit and tax fees | | | 74,104 | | | | 75,854 | | | | 55,725 | |

Transfer agent fees and expenses | | | 10,212 | | | | 30,135 | | | | 10,500 | |

Legal expenses | | | 51,368 | | | | 120,251 | | | | 22,040 | |

Debt issuance expense | | | 50,324 | | | | 170,827 | | | | — | |

Shareholder reports expenses | | | 13,476 | | | | 82,220 | | | | 18,308 | |

Other expenses | | | 6,848 | | | | 121,635 | | | | 40,464 | |

| | | | | | | | | | | | |

| | | |

Total Expenses | | | 1,770,432 | | | | 8,324,055 | | | | 894,007 | |

| | | | | | | | | | | | |

NET INVESTMENT INCOME/(LOSS) | | $ | (619 | ) | | $ | 14,146,432 | | | $ | 4,361,883 | |

| | | | | | | | | | | | |

| | | |

REALIZED AND UNREALIZED GAIN/(LOSS): | | | | | | | | | | | | |

Net realized gain/(loss) from: | | | | | | | | | | | | |

Investments | | | (8,889,049 | ) | | | (51,123 | ) | | | (894,751 | ) |

Swap contracts | | | (377,881 | ) | | | 8,847,040 | | | | 877,274 | |

Foreign currency transactions | | | 8,556 | | | | 5,346 | | | | (1,694 | ) |

Increase from payment by affiliate | | | — | | | | — | | | | 51,302 | |

| | | | | | | | | | | | |

Net realized gain/(loss) | | | (9,258,374 | ) | | | 8,801,263 | | | | 32,131 | |

| | | | | | | | | | | | |

Net change in unrealized appreciation/(depreciation) on: | | | | | | | | | | | | |

Investments | | | (16,292,098 | ) | | | (54,684,572 | ) | | | (23,940,664 | ) |

Swap contracts | | | (6,046,539 | ) | | | (4,447,087 | ) | | | (13,419,906 | ) |

Translation of assets and liabilities denominated in foreign currencies | | | 5,888 | | | | (4,447 | ) | | | (3,662 | ) |

| | | | | | | | | | | | |

Net change | | | (22,332,749 | ) | | | (59,136,106 | ) | | | (37,364,232 | ) |

| | | |

DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | (31,591,742 | ) | | $ | (36,188,411 | ) | | $ | (32,970,218 | ) |

| | | | | | | | | | | | |

(1) | The Dividend Capital Realty Income Allocation Fund changed its fiscal year from September 30th to December 31st. Amounts shown are for the period from October 1, 2007 to December 31, 2007. |

(2) | For the period from June 27, 2007 (inception date of the Fund’s initial public offering) through December 31, 2007. |

See accompanying Notes to Financial Statements.

28

STATEMENTSOF CHANGESIN NET ASSETS

December 31, 2007

| | | | | | | | | | | | |

| | | Dividend Capital Realty Income Allocation Fund | |

| | | For the

Period Ended

December 31,

2007 (1) | | | For the

Year Ended

September 30,

2007 | | | For the

Year Ended

September 30,

2006 | |

Operations: | | | | | | | | | | | | |

Net investment income/(loss) | | $ | (619 | ) | | $ | 14,146,432 | | | $ | 13,525,045 | |

Net realized gain/(loss) on investments, swap transactions and foreign currency transactions | | | (9,258,374 | ) | | | 8,801,263 | | | | 1,227,850 | |

Change in net unrealized appreciation/(depreciation) on investments, swap transactions and foreign currency transactions | | | (22,332,749 | ) | | | (59,136,106 | ) | | | 12,175,374 | |

| | | | | | | | | | | | |

Increase/(decrease) in net assets resulting from operations | | | (31,591,742 | ) | | | (36,188,411 | ) | | | 26,928,269 | |

| | | | | | | | | | | | |

| | | |

Distributions to Shareholders: | | | | | | | | | | | | |

From net investment income | | | (4,613,247 | ) | | | (19,005,710 | ) | | | (17,980,293 | ) |

From net realized gain on investments | | | — | | | | (1,104,803 | ) | | | — | |

| | | | | | | | | | | | |

Net decrease in net assets from distributions to shareholders | | | (4,613,247 | ) | | | (20,110,513 | ) | | | (17,980,293 | ) |

| | | | | | | | | | | | |

| | | |

Capital Share Transactions: | | | | | | | | | | | | |

Net asset value of common shares issued to shareholders from reinvested dividends | | | 296,369 | | | | 3,321,306 | | | | 524,724 | |

Common share offering cost adjustment | | | — | | | | — | | | | 41,695 | |

| | | | | | | | | | | | |

Increase in net assets from capital share transactions | | | 296,369 | | | | 3,321,306 | | | | 566,419 | |

| | | | | | | | | | | | |

Net Increase (Decrease) in Net Assets | | | (35,908,620 | ) | | | (52,977,618 | ) | | | 9,514,395 | |

| | | |

NET ASSETS: | | | | | | | | | | | | |

Beginning of period | | | 153,970,272 | | | | 206,947,890 | | | | 197,433,495 | |

End of period (2) | | $ | 118,061,652 | | | $ | 153,970,272 | | | $ | 206,947,890 | |

| | | | | | | | | | | | |

(1) | The Dividend Capital Realty Income Allocation Fund changed its fiscal year from September 30th to December 31st. Amounts shown are for the period from October 1, 2007 to December 31, 2007. |

(2) | Includes (over)/undistributed net investment income of $3,249,478, $1,281,619 and ($2,128,983) respectively. |

See accompanying Notes to Financial Statements.

29

STATEMENTSOF CHANGESIN NET ASSETS (CONTINUED)

December 31, 2007

| | | | |

| | | Dividend Capital

Strategic Global

Realty Fund | |

| | | For the

Period Ended

December 31,

2007 (1) | |

Operations: | | | | |

Net investment income | | $ | 4,361,883 | |

Net realized gain on investments, swap transactions, foreign currency transactions and payments from affiliates | | | 32,131 | |

Change in net unrealized depreciation on investments, swap transactions and foreign currency transactions | | | (37,364,232 | ) |

| | | | |

Decrease in net assets resulting from operations | | | (32,970,218 | ) |

| | | | |

| |

Distributions to Shareholders: | | | | |

From net investment income | | | (5,940,370 | ) |

| | | | |

Net decrease in net assets from distributions to shareholders | | | (5,940,370 | ) |

| | | | |

| |

Capital Share Transactions: | | | | |

Proceeds from sales of common shares, net of offering costs | | | 142,950,000 | |

Net asset value of common shares issued to shareholders from reinvested dividends | | | 293,235 | |

| | | | |

Increase in net assets from capital share transactions | | | 143,243,235 | |

| | | | |

Net Increase in Net Assets | | | 104,332,647 | |

| |

NET ASSETS: | | | | |

Beginning of period | | | 100,008 | (2) |

End of period (2) | | $ | 104,432,655 | |

| | | | |

(1) | For the period June 27, 2007 (inception date of the Fund’s initial public offering) through December 31, 2007. |

(3) | Includes overdistributed net investment income of ($484,331). |

See accompanying Notes to Financial Statements.

30

STATEMENTSOF CASH FLOWS

December 31, 2007

| | | | | | | | |

| | | Dividend Capital Realty

Income Allocation Fund | |

| | | For the Period Ended

December 31, 2007(1) | | | For the Year Ended

September 30, 2007 | |

Cash Flows from Operating Activities: | | | | | | | | |

Net decrease in net assets from operations | | $ | (31,591,742 | ) | | $ | (36,188,411 | ) |

Adjustments to reconcile net increase in net assets from operations to net cash used in operating activities: | | | | | | | | |

Purchase of investment securities | | | (14,230,789 | ) | | | (130,812,042 | ) |

Proceeds from disposition of investment securities | | | 30,272,388 | | | | 135,511,809 | |

Net sale of short-term investments | | | 4,400,768 | | | | 16,115,646 | |

Net realized gain/(loss) from investments, swap transactions and foreign currency transactions | | | 9,258,374 | | | | (8,801,263 | ) |

Net change in unrealized appreciation on investments, swap transactions and foreign currency transactions | | | 22,332,749 | | | | 59,136,106 | |

Increase/decrease in dividends and interest receivable | | | (346,849 | ) | | | 135,751 | |

Decrease in net swap interest receivable | | | 13,953 | | | | 30,528 | |

Increase/decrease in receivable for securities sold | | | (2,385,348 | ) | | | 310,401 | |

Decrease in payable for securities purchased | | | 0 | | | | (2,223,768 | ) |

Decrease in prepaid expenses and other assets | | | 151,701 | | | | 105,113 | |

Increase in accrued expenses and other payables | | | (75,543 | ) | | | (27,083 | ) |

Increase/decrease in distributions payable | | | 1,538,813 | | | | (444,893 | ) |

Accretion/amortization of discounts/premium on investment securities | | | (21,597 | ) | | | 59,360 | |

| | | | | | | | |

Net Cash Provided by Operating Activities | | $ | 19,316,878 | | | $ | 32,907,254 | |

| | |

Cash Flows from Financing Activities: | | | | | | | | |

Proceeds from bank borrowing | | $ | 3,000,000 | | | $ | 7,500,000 | |

Payment on outstanding debt | | | (18,000,000 | ) | | | (23,628,000 | ) |

Cash distributions paid | | | (4,316,878 | ) | | | (16,789,207 | ) |

| | | | | | | | |

Net Cash Provided by Financing Activities | | $ | (19,316,878 | ) | | $ | (32,917,207 | ) |

| | | | | | | | |

| | |

Cash | | | | | | | | |

Beginning Balance | | $ | 0 | | | $ | 9,953 | |

Ending Balance | | $ | 0 | | | $ | 0 | |

| | |

Supplemental Disclosure of Cash Flow Information: | | | | | | | | |

Cash paid for interest and fees on bank borrowing | | $ | 1,024,168 | | | $ | 4,920,783 | |

Non-cash financing activities not included herein consist of reinvestment of dividends and distributions of $296,369 and $3,321,306, respectively.

(1) | The Dividend Capital Realty Income Allocation Fund changed its fiscal year from September 30th to December 31st. |

See accompanying Notes to Financial Statements.

31

FINANCIAL HIGHLIGHTS

Dividend Capital Realty Income Allocation Fund

| | | | |

| | | For the Period Ended

December 31, 2007 (10) | |

PER SHARE OPERATING DATA: | | | | |

Net Asset Value, Beginning of Period | | $ | 11.03 | |

Income from investment operations: | | | | |

Net investment income/(loss) (7) | | | (0.00 | ) (9) |

Net gains/(losses) on securities, realized and unrealized | | | (2.26 | ) |

| | | | |

Total From Investment Operations | | | (2.26 | ) |

Dividends and/or Distributions to Shareholders: | | | | |

Dividends from net investment income | | | (0.33 | ) |

Dividends from net realized gain on investments | | | 0.00 | |

| | | | |

Total Distributions | | | (0.33 | ) |

| | | | |

Offering Costs Charged to Paid-in Capital | | | 0.00 | |

Offering Cost Adjustment | | | 0.00 | |

Net Asset Value, End of Period | | $ | 8.44 | |

| | | | |

Market Price, End of Period | | $ | 8.06 | |

| | | | |

Total Return, Net Asset Value (3) | | | -20.62 | % |

| | | | |

Total Return, Market Value (3) | | | -25.08 | % |

Net Assets, End of Period (000’s) | | $ | 118,062 | |

Ratio of Total Expenses to Average Net Assets | | | 5.20 | % (4) |

Ratio of Total Expenses to Average Net Assets after reduction to custodian expenses | | | 5.20 | % (4) |

Ratio of Operating Expenses to Average Net Assets (6) | | | 2.42 | % (4) |

Ratio of Operating Expenses to Average Net Assets after reduction to custodian expenses (6) | | | 2.42 | % (4) |

Ratio of Net Investment Income/(Loss) to Average Net Assets | | | (0.00 | )% (9) |

Portfolio Turnover Rate (5) | | | 7.27 | % |

Bank Borrowings: | | | | |

Supplemental Data: | | | | |

Loan Outstanding, End of Period (000’s) | | $ | 53,872 | |

Asset Coverage for Loan Outstanding | | | 305 | % |

(1) | For the period from February 24, 2005 (inception of offering) to September 30, 2005. |

(2) | Net of sales load of $0.675 on initial shares issued. |

(3) | Total investment return is calculated assuming a purchase of common shares of the opening of the first day and sale on the closing of the last day of each period reported. Dividends and distributions are assumed, for purposes of this calculation, to be reinvested at prices obtained under the Fund’s reinvestment plan. Total investment return is not annualized for periods of less than one year. Brokerage commissions are not reflected. |

(4) | Ratio annualized for the period of less than one year. |

32

| | | | | | | | | | |

For the Year Ended