UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21682 | |||||||

| ||||||||

BB&T Variable Insurance Funds | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

434 Fayetteville Street, 5th Floor, Raleigh, NC |

| 27626-0575 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

BISYS Fund Services, 3435 Stelzer Road, Columbus, OH 43219 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | (800) 228-1872 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2005 |

| ||||||

Item 1. Reports to Stockholders.

BB&T Variable Insurance Funds

Table of Contents

Fund Summary

| Large Cap Value VIF | 1 | ||||||

| Mid Cap Growth VIF | 2 | ||||||

| Large Company Growth VIF | 3 | ||||||

| Capital Manager Equity VIF | 4 | ||||||

| Special Opportunities Equity VIF | 5 | ||||||

| Total Return Bond VIF | 7 | ||||||

| Summary of Portfolio Holdings | 9 | ||||||

| Expense Example | 10 | ||||||

Schedule of Portfolio Investments

| Large Cap Value VIF | 11 | ||||||

| Mid Cap Growth VIF | 12 | ||||||

| Large Company Growth VIF | 13 | ||||||

| Capital Manager Equity VIF | 14 | ||||||

| Special Opportunities Equity VIF | 15 | ||||||

| Total Return Bond VIF | 16 | ||||||

| Financial Statements | 20 | ||||||

| Notes to Financial Statements | 26 | ||||||

| Report of Independent Registered Public Accounting Firm | 31 | ||||||

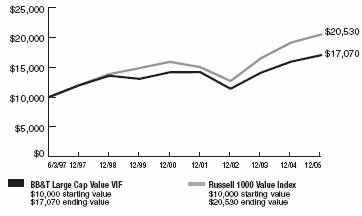

BB&T Large Cap Value VIF

Performance Overview 6/3/1997 - 12/31/2005

Growth of a $10,000 investment

Portfolio Manager

Rick B. Jones, CFA

Senior Vice President – Director, Value Equities

BB&T Asset Management, Inc.

Average Annual Returns (Inception 6/3/1997)

|

| 1 Year |

| 5 Year |

| Since Inception |

|

BB&T Large Cap Value VIF |

| 6.90 | % | 3.78 | % | 6.43 | % |

Russell 1000 Value Index |

| 7.05 | % | 5.28 | % | 8.74 | % |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of dividends and capital gains. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes. Common stocks, and funds investing in common stocks, generally provide greater return potential when compared with other types of investments. Value-based investments are subject to the risk that the broad market may not recognize their intrinsic value.

The Fund’s 6.90% total return comfortably outpaced the S&P 500 Index which returned 4.91% for the one-year period, but slightly trailed its primary benchmark, the Russell 1000® Value Index(1), which rose 7.05%.

Overall the Fund’s returns were solid as traditionally value oriented sectors of the stock market, like Energy and Utilities, continued to do well.

The portfolio carried a full weighting in energy throughout the period and not surprisingly our two top contributors to performance were energy stocks: ConocoPhillips and Anadarko Corp. A significant contribution was also made by Hewlett Packard Co., which underwent a management change.

Because we have had difficulty finding reasonably valued utility stocks, the portfolio was underweighted in a sector that did very well in 2005. Our consumer stock sector selection was also challenged. Specifically, the Albertson’s Inc. stock position performed poorly, as the company rejected a buy-out bid late in the period (has since accepted a sweetened offer) and its Sara Lee holding had a bumpy start to a dramatic reshaping program, registering disappointing performance.

As of December 31, 2005, the top five equity holdings in the Fund were Bank of America Corp. (3.1% of the portfolio’s net assets), ConocoPhillips (2.7%), Citigroup, Inc. (2.7%), J.P. Morgan Chase & Co. (2.6%) and ChevronTexaco Corp. (25%)(2).

We continue to be disciplined in applying our diversified value investment approach. We are steadfastly focused on maintaining diversified portfolio of financially strong companies that we believe are currently trading at reasonable valuation levels given our assessment of their prospects. The portfolio enters the new-year being overweighted healthcare and technology stocks while being most underweighted in financial and utility stocks.

(1) The Fund is measured against the Russell 1000 Value Index an unmanaged index which consists of 1,000 of the largest capitalized U.S. domiciled companies. Companies in this index generally have low price-to-book and price-to-earnings ratios, higher dividend yields and lower forecasted growth values. The index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

(2) Portfolio composition is as of December 31, 2005, and is subject to change.

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the period would have been lower.

1

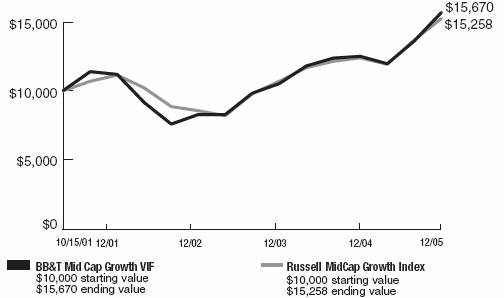

BB&T Mid Cap Growth VIF

Performance Overview 10/15/2001 - 12/31/2005

Growth of a $10,000 investment

Portfolio Manager

David P. Nolan

Senior Vice President and Portfolio Manager

BB&T Asset Management, Inc.

Average Annual Returns (Inception 10/15/2001)

|

| 1 Year |

| Since Inception |

|

BB&T Mid Cap Growth VIF |

| 14.38 | % | 11.26 | % |

Russell MidCap Growth Index |

| 12.10 | % | 10.55 | % |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of dividends and capital gains. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Mid-capitalization funds typically carry additional risks since smaller companies generally have a higher risk of failure, and historically, their stocks have experienced a greater degree of market volatility than stocks on average

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes. Common stocks, and funds investing in common stocks, generally provide greater return potential when compared with other types of investments. Value-based investments are subject to the risk that the broad market may not recognize their intrinsic value.

The Fund produced robust performance of 14.38% during the last 12 months, nearly tripling the 2005 return of 4.91% for the S&P 500 Index and notably outpacing the Russell MidCap® Growth Index(1) return of 12.10%.

Our investments in the energy sector, such as Peabody Energy Corp. (1.7% of the portfolio’s net assets), were especially productive, as we were overweight in energy for much of the period. At one point, the Fund’s allocation to energy was roughly 50% higher than the allocation of our benchmark, and we reaped the benefits of energy stocks’ steady climb. Another positive factor in our performance was our decision to underweight the consumer discretionary and consumer staples sectors in the second half of the year as concerns grew over the consumer’s allocation of discretionary income in the face of rising fuel prices. Technology holdings such as Apple Computer (sold) and Marvell Technology Group, Ltd. (2.0%) were strong performers for the period. Other standouts were Celgene Corp. (2.0%) and the Chicago Mercantile Exchange Holdings, Inc. (1.8%).

The mid cap arena has been on a roll for quite some time, outperforming large and small cap stocks for much of the last decade. To some extent, our strong gains reflected a continuation of this long-term trend.

The greatest detractors from performance during the period were found in the technology sector. Negative returns were experienced in F5 Networks (sold), and in semiconductor companies Cree, Inc. (sold) and Tessera Technologies (sold).

As of December 31, 2005, the top five individual equity holdings in the Fund were American Tower Corp. – Class A (3.0%), Cognizant Technology Solutions Corp. – Class A (2.3%), Comverse Technology, Inc. (2.2%), UTI Worldwide (2.1%), and Celgene Corp. (2.0%)(2).

We think energy will continue to play a key role in the market going forward, and we hope to see a further upward revision of earnings estimates. Energy stocks will swing, sometimes dramatically, on short-term movements in the prices of crude oil and natural gas. But we believe energy prices are not going to retreat significantly and that positive earning “surprises” will continue. The energy sector is expected by analysts to lead the mid cap area in 2006 earnings per share growth.

For now, as long as higher energy prices and the Fed’s tightening bias do not contribute to a recessionary environment and the economy keeps growing at a three percent-or-better pace, then we believe that mid cap growth stocks in general should continue to provide competitive returns. In that environment, we believe that investment opportunities will be found in numerous sectors in addition to energy. Among these would be technology, health care, industrial and select financial stocks which should all show strong year-over-year earnings gains.

(1) The Fund is measured against the Russell MidCap Growth Index, an unmanaged index which measures the performance of those securities in the Russell 1000 Index with higher price-to-book ratios and lower forecasted growth values. The index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

(2) Portfolio composition is as of December 31, 2005, and is subject to change.

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the period would have been lower.

2

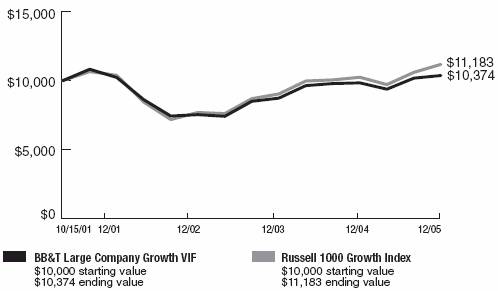

BB&T Large Company Growth VIF

Performance Overview 10/15/2001 - 12/31/2005

Growth of a $10,000 investment

Portfolio Manager

Jeffery J. Schappe, CFA

Senior Vice President and Chief Investment Officer

BB&T Asset Management, Inc.

Average Annual Returns (Inception 10/15/2001)

|

| 1 Year |

| Since Inception |

|

BB&T Large Company Growth VIF |

| 1.88 | % | 0.88 | % |

Russell 1000 Growth Index |

| 5.26 | % | 2.69 | % |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of dividends and capital gains. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes. Common stocks, and funds investing in common stocks, generally provide greater return potential when compared with other types of investments. Value-based investments are subject to the risk that the broad market may not recognize their intrinsic value.

We were not completely satisfied with the Fund’s performance during the last 12 months. Although we posted a positive total return of 1.88%, we trailed our primary benchmark, the Russell 1000® Growth Index(1) by 3.38%.

The Fund underperformed its benchmark due to security selection but also because we have focused on higher quality names, which have lagged for much of the year. We believe, however, that a continued bias towards quality companies boosts return potential over the long run. Lagging behind the broader market was a group of historically strong growth stocks, such as General Electric Co. (4.2% of the portfolio’s net assets), Microsoft Corp. (4.2%), Cisco Systems, Inc. (2.2%), Dell, Inc. (1.0%), and Home Depot, Inc. (1.0%); all of these stocks produced returns for the period that were below the benchmark’s performance.

We did, however, enjoy strong returns in a number of traditional growth sectors. In health care, such stalwarts as UnitedHealth Group, Inc. (+41% total return), WellPoint, Inc. (+32%), and Gilead Sciences, Inc. (+50%) delivered results that ranged from robust to outstanding. Technology stocks such as Motorola, Inc. (+32%) and Texas Instruments, Inc. (31%) enhanced fund returns.

As of December 31, 2005, the top five equity holdings in the Fund were General Electric Co. (4.2% of the portfolio’s net assets), Microsoft Corp. (4.2%), Intel Corp. (3.3%), Johnson & Johnson (3.0%), and Wal Mart Stores, Inc. (2.4%)(2).

Looking out over the next six to 12 months, we believe conditions point to a relatively constructive environment for the type of high-quality growth stocks we favor.

Respectable economic growth, low inflation, and the Fed adopting a neutral bias should provide a favorable backdrop for equities, in general. Because growth stocks have trailed value equities the past several years, we hope that a more normal valuation relationship between growth and value will emerge this year.

As is our practice, we continue to invest in the stocks of financially strong companies with reasonable earnings growth prospects. We feel this approach should serve our shareholders well through our next fiscal year.

(1) The Fund is measured against the Russell 1000 Growth Index an unmanaged index which is comprised of 1,000 of the largest capitalized U.S. domiciled companies with higher price-to-book ratios and higher forecasted growth values whose common stock is traded in the United States on the New York Stock Exchange, American Stock Exchange and NASDAQ. The index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

(2) Portfolio composition is as of December 31, 2005, and is subject to change.

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the period would have been lower.

3

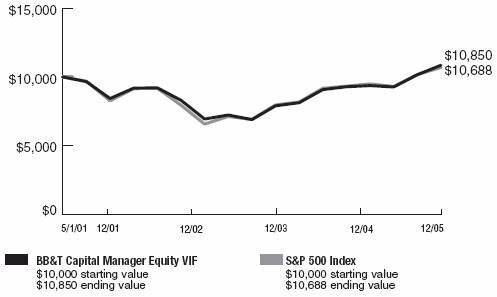

BB&T Capital Manager Equity VIF

Performance Overview 5/1/2001 - 12/31/2005

Growth of a $10,000 investment

Portfolio Management Team

Managed by the BB&T Balanced Portfolio Management Team

Average Annual Returns (Inception 5/1/2001)

|

| 1 Year |

| Since Inception |

|

BB&T Capital Manager Equity VIF |

| 6.77 | % | 1.76 | % |

S&P 500 Index |

| 4.91 | % | 1.44 | % |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of dividends and capital gains. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes. Common stocks, and funds investing in common stocks, generally provide greater return potential when compared with other types of investments. Value-based investments are subject to the risk that the broad market may not recognize their intrinsic value.

For the twelve-month period ended December 31, 2005, the BB&T Capital Manager Equity VIF provided a total return of 6.77%. In comparison, the S&P 500 Index returned 4.91% for the same period.

The Fund invests in a diversified selection of underlying portfolios from the BB&T family of mutual funds. As such, our allocation decisions play a big role in the Fund’s performance.

In 2005, we benefited from strong, absolute returns from the shares we owned in the BB&T Large Company Value Fund and BB&T International Equity Fund. We have a long-term strategic overweight in the value arena, which did well versus growth. Also, our strategic overweights in mid-cap and small-cap significantly contributed to our outperformance in 2005.

Our substantial weighting in the BB&T International Equity Fund demonstrated the potential value of diversifying outside the U.S., as the MSCI EAFE Index(1), which tracks international stocks, gained over twice as much as the S&P 500 Index(2), our domestic equity benchmark.

As of December 31, 2005, the portfolio’s five largest allocations in underlying BB&T portfolios were the Large Company Value Fund (30.3% of portfolio’s net assets), the Large Company Growth Fund (20.3%), the International Equity Fund (14.6%), the Equity Index Fund (12.6%), and the Mid Cap Value Fund (7.0%)(3).

These five funds are the same, and in the same order, as the allocations we had one year earlier. This similarity reflects our practice of rebalancing the Fund’s assets back to our strategic weightings on a regular basis.

While still providing positive returns, our investment in the BB&T Large Company Growth Fund underperformed the other asset classes for the year.

Looking ahead to the next twelve months, we have positive expectations for stocks, and we expect stocks to outperform bonds.

Steady economic growth, relatively contained inflation, low long-term interest rates, and reasonable valuation levels all contribute to a favorable backdrop for stocks.

One of the risks to this view is that corporate profit margins, currently near record levels, are being pressured by higher short-term interest rates and higher commodity prices. Although decelerating, earnings growth continues and remains healthy in a number of sectors. Other risks to our view include lower housing affordability and a peaking housing market. However, we believe capital management activity will increase. Cash on corporate balance sheets is high, which should support continued solid merger and acquisition activity, as well as potential dividend increases and share repurchases.

(1) The MSCI EAFE Index is an unmanaged index which is generally representative of the performance of stock markets in that region. The index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

(2) The Fund is measured against the S&P 500 Index, an unmanaged index generally representative of the U.S. stock market as a whole. The Index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

(3) Portfolio composition is as of December 31, 2005, and is subject to change.

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the period would have been lower.

4

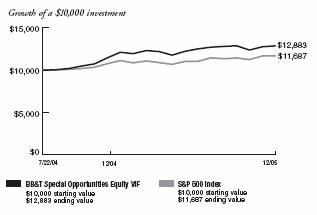

BB&T Special Opportunities Equity VIF

Performance Overview 7/22/04 - 12/31/05

Portfolio Manager

George F. Shipp, CFA

Chief Investment Officer

Scott & Stringfellow, Inc.

Average Annual Returns (Inception 7/22/04)

|

| 1 Year |

| Since Inception |

|

BB&T Special Opportunities Equity VIF |

| 6.29 | % | 19.18 | % |

S&P 500 Index |

| 4.91 | % | 11.40 | % |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of dividends and capital gains. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance doe not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of this Fund will fluctuate as the value of the securities in the portfolio changes. A concentrated portfolio may add a measure of volatility to performance, as major fluctuations in any one holding will likely affect the Fund more than a fund with greater diversification.

For the full year 2005, the BB&T Special Opportunities Equity VIF produced a 6.29% gain, outpacing both the 4.91% total return of the S&P 500 Index(1) and the 6.1% result of the Russell 3000 Index. This was also only slightly ahead of the Lipper Multi-Cap Value group, which posted a 6.2% gain for the year.

We manage a concentrated portfolio and were fortunate to have a few more big winners than losers. We entered October with a decent performance advantage against the market, but Hurricanes Katrina and Rita knocked a few of our companies off track. We became mesmerized by the associated spike in energy quotes and determined to hold our Apache Corp. and Pioneer Natural Resources Co. positions, even though we were well aware their Gulf of Mexico operations had been hard hit. Oil and gas quotes soon topped out due to the “demand destruction” caused by refinery and chemical outages in tandem with $3/gallon gasoline, causing the energy group to under-perform the S&P 500 by 9% in the 4th quarter. In the short term both of these stocks lagged land-focused exploration and production companies (such as Burlington, EOG, or XTO). Another fund holding, MedCath Corp. had a cardiovascular-focused hospital in Hurricane Katrina’s path. Although it managed to keep its doors open throughout the disaster, that facility in a New Orleans suburb contributed to a reduced outlook. MedCath Corp. shares fell 22% during the quarter and the year. At the end of the year, though, our admiration of energy had served our clients well, as Apache Corp., Pioneer Natural Resources Co. and Weatherford International, Ltd. (a driller for energy) all posted gains exceeding 35% over the period.

Late in 2005 we waved good-bye to our biggest gainer of the year, managed healthcare leader Coventry Health Care, Inc. Coventry shares were up over 50% from our original purchase price towards the end of 2005, on top of 23% gains in 2004 and a 122% rebound in 2003. That adds up to a cumulative +357%, whereas earnings have advanced 170% over those three years. The resultant doubling in P/E valuation raises risks, while at the same time logic would say that margin gains will become increasingly difficult. Healthcare risk underwriting used to be a cyclical business, so despite our strong admiration for the company’s management, we decided to move on.

Digital Insight, Inc. was another of our original purchases for the Fund, after shares fell on some negative short-term news just before our inception date, giving us a chance to enter around $14. Since then, we have trimmed the position on a few occasions to manage risk (wish we hadn’t but hindsight is always 20/20). As much as we like the company and its prospects, today we find ourselves uncomfortable initiating positions at current levels around $33 (up 30% in 2005 alone), so we sold out of our position and took our profits. Digital Insight, Inc. sees non-GAAPEPS in a $1.04-1.06 range in 2006 (+21%), which puts the stock’s P/E valuation at a “full” 35x forecasts.

5

There was bad with the good, as there will likely always be. Mistakes will be made, learned from, and actions taken. We can forgive ourselves for riding out the energy storm, but not for the red ink we spilled in printer maker Lexmark International, Inc., which reported two major reductions in its earnings outlook in 2005 on the way to seeing its value nearly cut in half. We should have taken the hint the first time, i.e. “fool me twice, shame on us.” That second miss (October 3) cost us about 30% on our Lexmark position in the quarter as investors (including us) lost faith in the “razor and blade” thesis that had carried the company for about nine years. A 23% quarterly decline in security and storage software leader Symantec Corp. and 12% drop in cable operator Comcast Corp. – Class A were a little more frustrating, only because we did not see material news (“increasing competition” often is cited for both) to fully explain the serious depreciation.

Ours is not a dividend-oriented portfolio, but 15 of our 28 year-end equity holdings raised their payouts in 2005, by an average 35% (median +17%). If fourth quarter earnings estimates generally are accurate, our companies’ profits grew by an average 17% in 2005, superior to the still-impressive +13% expectation for the S&P 500.We believe that should be encouraging for our portfolio’s 2006 prospects.

As of December 31, 2005, the top five equity holdings in the Fund were Smithfield Foods, Inc. (4.2% of the portfolio’s net assets), CONSOL Energy, Inc. (4.1%), Weatherford International, Ltd. (3.9%), PACCAR, Inc. (3.8%), and Comcast Corp.- Class A (3.8%)(2).

(1) The Fund is measured against the S&P 500 Index, an unmanaged index generally representative of the U.S. stock market as a whole. The Index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

(2) Portfolio composition is as of December 31, 2005, and is subject to change.

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the period would have been lower.

6

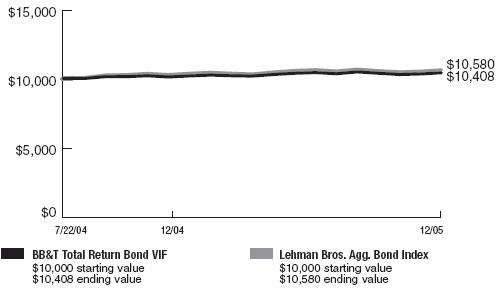

BB&T Total Return Bond VIF

Performance Overview 7/22/04 - 12/31/05

Growth of a $10,000 investment

Portfolio Manager

David M Ralston, CFA

Managing Director and Chief Investment Officer

Sterling Capital Management, LLC

Average Annual Returns (Inception 7/22/04)

|

| 1 Year |

| Since Inception |

|

|

|

|

|

|

|

BB&T Total Return Bond VIF |

| 2.29 | % | 2.81 | % |

Lehman Bros. Agg. Bond Index |

| 2.43 | % | 3.98 | % |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of dividends and capital gains. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Bonds offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss. Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return.

The Fund is subject to the risk that principal value reacts in opposition to the movement of interest rates and that a rising interest rate environment increases the risk of loss of principal.

For the twelve-month period ended December 31, 2005, the BB&I Total Return Bond VIF produced a total return of 2.29%, compared to 2.43% for the Lehman Brothers Aggregate Bond Index(1).

Effective July 18, 2005, Sterling Capital Management LLC began serving as subadviser to the Fund*.

2005 will be remembered as the year of an active Federal Reserve, a flatter yield curve and a benevolent foreign investor. Throughout the year the Fed continued on its “measured” path of removing prior years of monetary accommodation. The Fed raised the overnight borrowing rate a total of eight times in 2005 to 4.25%.

As the Fed removed monetary accommodation from an economy exhibiting amazing resilience, yields on Treasury securities from 3 months to approximately 15 years rose. The rather benign increase in core inflation along with a continued inflow of foreign capital provided a consistent bid for the long end of the Treasury curve. In fact, when looking at total returns for the year (coupon and price appreciation), long Treasury securities had the best relative returns, up approximately 9% for the year. Due to the flattening of the curve, the distant second place segment of the yield curve was the return on 6 month Treasury bills which returned 3.1% for the same time period.

In 2005 the U.S. became increasingly more dependent upon the foreign investor. Spending to finance the Iraq war and the rebuilding cost associated with hurricanes in the gulf coast led to a further deterioration of the budget deficit. Increased reliance on foreign oil and Americans’ preferences for imported goods led to a ballooning of the trade deficit. The inflow of foreign funds has had an increasing degree of importance in helping fund our internal shortfall. It is estimated that in 2005 70% of all new Treasuries issued were bought by foreign investors. This support has been critically important in maintaining low long-term interest rates, but the magnitude of these flows is worrisome and is a significant risk looking forward.

Another important influence on rates during 2005 was the energy price spike due to the dislocation of oil and refinery capacity. The Iraq war and the unprecedented back to back hurricanes hitting the refinery rich gulf coast had a severe impact on prices and consumer confidence. However, the economy weathered these storms and appears to be once again expanding at a healthy pace.

As we look forward to the year ahead the economy continues to expand at a pace that is expected to be above trend. While consensus expectations are for a slight slowing of domestic growth, the global economy is solidly gaining momentum. In 2006 corporate spending and manufacturing are expected to have a more prominent leadership role in the economy. The improved health of Corporate America that is flush with liquidity is expected to facilitate the generation of new jobs in the coming year. It is our belief that the strength of the production side of the economy will continue to create new jobs in 2006. During the last few years many of these new jobs have been created by the housing sector. While we acknowledge that there are pockets of excessive residential price appreciation, we do not believe we have a bubble in home values that is getting ready to burst. Yet we do expect the economic contribution of housing to be weaker in 2006 than in 2005. However, nearly every measure of the sector is stronger that where it was a year ago.

7

Continued new job creation is critical to our positive outlook on the economy moving forward. With lower rates and increased refinancing, consumers extracted a great deal of equity from their homes over the last several years. As rates rise, this stimulus of personal consumption will decline. Another source of optimism for us toward economic expansion is the continued growth of federal spending. Support for reconstruction of the Gulf states region is expected to go on for years. Spending for defense is expected to remain at elevated levels.

On top of robust growth, we are anticipating a higher level of core inflation over the next twelve months. We feel several factors will contribute to an increase in prices. First, we believe the Chinese will eventually capitulate to political pressure from Congress and allow a second more realistic revaluation of their currency. This will reduce the downward pressure we have seen on import prices over the last several years. Second, we believe that the economy is approaching full employment and the pressure on wages will continue to rise.

In addition, the “output gap”, or the slack in the economy, is narrowing as the production side of the economy accelerates. History has shown that with capacity utilization above 80%, producers will be able to raise prices.

Our belief that the economy is healthy and advancing combined with our expectations of higher inflation leads us to a cynical view of the current level of interest rates. Simply stated, we do not believe an investor is being sufficiently paid to have exposure to current yield levels. We view the interest rate market as range-bound with current prices at the high end and yields at the low end of the range for the next several months. Therefore, we are currently short duration in our core portfolios.

From a yield curve perspective, we have shifted our positioning over the last two months. After being barbelled for most of 2005 we have moved to more of a bullet approach.

Since we expect the Fed to continue to raise short rates we remain overweight in floating rate securities to participate in the anticipated upward adjustment that accompanies Fed rate increases. Security selection in the treasury, agency and taxable muni sectors detracted about 5 basis points relative to the benchmark, and sector allocations to the taxable muni sector cost us another 2 basis points of excess return. Convexity choice across all sectors was also a small detractor from performance.

From a sector perspective, we remain convinced that having a portfolio that is of higher quality and higher yield is the proper strategy. We still believe that the restructuring risk in the market due to the emerging importance of private equity funds favors equity investors over bondholders. As such we are underweight credit and expect to remain so over the next few months.

Due to our range-bound view towards interest rates and our concern about credit, we are overweight mortgages and structure product. We believe the high quality and superior yields offered by direct issue mortgages, commercial mortgage-backed securities and AAA rated home equity Asset Backed Securities will provide superior return opportunities over time.

As of December 31, 2005, the Fund’s effective duration was 4.30 years2. Approximately 40.1% of the portfolio was invested in corporate obligations, 32.7% in U.S. Treasury and agency securities, 24.8% in collateralized mortgage-backed securities, 7.5% in cash and cash equivalents and 2.2% in municipal bonds. The Fund’s average credit quality was Aa1 (as rated by Moody’s)(3)(4).

We expect a challenging market environment for bonds in the first half of 2006. We feel our conservative posturing of the portfolio will provide us extension opportunities in the months ahead. We believe the Fed will raise rates a few more times and pause when the Fed funds rate reaches 4.75% to 5%. At this point we believe the yield curve will once again steepen and we expect to more heavily invest in Treasury securities in the intermediate part of the curve.

*Sterling Capital Management LLC is a majority owned, non-bank subsidiary of BB&T Corporation, and is an affiliate of BB&T Asset Management, Inc.

(1) The Fund is measured against Lehman Brothers Aggregate Bond Index which is a market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of at least one year. The index is unmanaged and does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities.

(2) Duration is a measure of a bond’s or a bond fund’s price risk that is adjusted for any optionality.

(3) Portfolio composition is as of December 31, 2005 and is subject to change.

(4) Moody’s Fund Ratings represent an opinion only, not a recommendation to buy or sell.

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the period would have been lower.

8

BB&T Variable Insurance Funds

Summary of Portfolio Holdings (Unaudited)

December 31, 2005

The BB&T Variable Insurance Funds portfolio composition was as follows at December 31, 2005:

| BB&T Large Cap Value VIF | Percentage of net assets | ||||||

| Consumer Discretionary | 7.8 | % | |||||

| Consumer Staples | 6.1 | ||||||

| Energy | 13.0 | ||||||

| Financials | 30.5 | ||||||

| Health Care | 9.0 | ||||||

| Industrials | 7.4 | ||||||

| Information Technology | 8.3 | ||||||

| Materials | 4.9 | ||||||

| Repurchase Agreement | 2.7 | ||||||

| Telecommunication Services | 5.0 | ||||||

| Utilities | 5.3 | ||||||

| 100.0 | % | ||||||

BB&T Mid Cap Growth VIF

| Consumer Discretionary | 12.6 | % | |||||

| Energy | 13.1 | ||||||

| Exchange Traded Funds | 4.3 | ||||||

| Financials | 8.3 | ||||||

| Health Care | 16.1 | ||||||

| Industrials | 13.2 | ||||||

| Information Technology | 21.9 | ||||||

| Materials | 2.5 | ||||||

| Repurchase Agreement | 3.6 | ||||||

| Telecommunication Services | 4.8 | ||||||

| 100.4 | % | ||||||

BB&T Large Company Growth VIF

| Consumer Discretionary | 9.2 | % | |||||

| Consumer Staples | 8.8 | ||||||

| Energy | 5.6 | ||||||

| Financials | 4.8 | ||||||

| Health Care | 20.2 | ||||||

| Industrials | 17.3 | ||||||

| Information Technology | 28.8 | ||||||

| Repurchase Agreement | 4.4 | ||||||

| Telecommunication Services | 0.9 | ||||||

| 100.0 | % | ||||||

BB&T Capital Manager Equity VIF

| Equity Index | 12.6 | % | |||||

| International Equity | 14.7 | ||||||

| Large Company Equity | 50.6 | ||||||

| Mid Cap Equity | 11.6 | ||||||

| Money Market | 3.0 | ||||||

| Small Cap | 7.4 | ||||||

| 99.9 | % | ||||||

BB&T Special Opportunities Equity VIF

| Commercial Services | 6.8 | % | |||||

| Consumer Discretionary | 20.4 | ||||||

| Energy | 15.0 | ||||||

| Financials | 8.2 | ||||||

| Health Care | 13.2 | ||||||

| Industrials | 7.6 | ||||||

| Information Technology | 18.5 | ||||||

| Repurchase Agreement | 10.7 | ||||||

| 100.4 | % | ||||||

BB&T Total Return Bond VIF

| Corporate Bonds | 40.1 | % | |||||

| Federal Home Loan Bank | 4.4 | ||||||

| Federal Home Loan Mortgage Corporation—Mortgage Backed Securities | 7.6 | ||||||

| Federal Home Loan Mortgage Corporation—U.S. Government Agencies | 3.2 | ||||||

| Federal National Mortgage Association—Mortgage Backed Securities | 17.2 | ||||||

| Federal National Mortgage Association—U.S. Government Agencies | 4.7 | ||||||

| Government National Mortgage Association | 8.4 | ||||||

| Municipal Bonds | 2.2 | ||||||

| Repurchase Agreement | 7.5 | ||||||

| Student Loan Marketing Association | 1.6 | ||||||

| U.S. Treasury Bonds | 9.5 | ||||||

| U.S. Treasury Notes | 0.9 | ||||||

| 107.3 | % | ||||||

9

BB&T Variable Insurance Funds

Expense Example (Unaudited)

December 31, 2005

As a shareholder of the BB&T Variable Insurance Funds, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees; and other Fund expenses.

These examples are intended to help you understand your ongoing costs (in dollars) of investing in the BB&T Variable Insurance Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

These examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2005 through December 31, 2005.

Actual Example

The table below provides information about actual account values and actual expenses. You may use the information below, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

| Beginning Account Value 7/1/05 | Ending Account Value 12/31/05 | Expenses Paid During Period* 7/1/05 – 12/31/05 | Expense Ratio During Period 7/1/05 – 12/31/05 | ||||||||||||||||

| BB&T Large Cap Value VIF | $ | 1,000.00 | $ | 1,054.40 | $ | 4.09 | 0.79 | % | |||||||||||

| BB&T Mid Cap Growth VIF | 1,000.00 | 1,129.00 | 4.19 | 0.78 | % | ||||||||||||||

| BB&T Large Company Growth VIF | 1,000.00 | 1,031.30 | 3.94 | 0.77 | % | ||||||||||||||

| BB&T Capital Manager Equity VIF | 1,000.00 | 1,062.50 | 0.99 | 0.19 | % | ||||||||||||||

| BB&T Special Opportunities Equity VIF | 1,000.00 | 1,029.00 | 6.03 | 1.18 | % | ||||||||||||||

| BB&T Total Return Bond VIF | 1,000.00 | 998.80 | 4.43 | 0.88 | % | ||||||||||||||

* Expenses are equal to the average account value times the Fund's annualized expense ratio multiplied by the number of days in the most recent fiscal half-year divided by the number of days in the fiscal year.

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on each BB&T Variable Insurance Funds' actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 7/1/05 | Ending Account Value 12/31/05 | Expenses Paid During Period* 7/1/05 – 12/31/05 | Expense Ratio During Period 7/1/05 – 12/31/05 | ||||||||||||||||

| BB&T Large Cap Value VIF | $ | 1,000.00 | $ | 1,021.22 | $ | 4.02 | 0.79 | % | |||||||||||

| BB&T Mid Cap Growth VIF | 1,000.00 | 1,021.27 | 3.97 | 0.78 | % | ||||||||||||||

| BB&T Large Company Growth VIF | 1,000.00 | 1,021.32 | 3.92 | 0.77 | % | ||||||||||||||

| BB&T Capital Manager Equity VIF | 1,000.00 | 1,024.25 | 0.97 | 0.19 | % | ||||||||||||||

| BB&T Special Opportunities Equity VIF | 1,000.00 | 1,019.26 | 6.01 | 1.18 | % | ||||||||||||||

| BB&T Total Return Bond VIF | 1,000.00 | 1,020.77 | 4.48 | 0.88 | % | ||||||||||||||

* Expenses are equal to the average account value times the Fund's annualized expense ratio multiplied by the number of days in the most recent fiscal half-year divided by the number of days in the fiscal year.

10

BB&T Large Cap Value VIF

Schedule of Portfolio Investments

December 31, 2005

| Shares | Fair Value | ||||||||||

| COMMON STOCKS (97.3%) | |||||||||||

| Consumer Discretionary (7.8%) | |||||||||||

| 8,223 | Federated Department Stores, Inc. | $ | 545,432 | ||||||||

| 45,000 | Gannett Co., Inc. | 2,725,649 | |||||||||

| 70,000 | Mattel, Inc. | 1,107,400 | |||||||||

| 17,475 | V.F. Corp. | 967,067 | |||||||||

| 99,000 | Walt Disney Co. (The) | 2,373,030 | |||||||||

| 13,100 | Whirlpool Corp. | 1,097,256 | |||||||||

| 8,815,834 | |||||||||||

| Consumer Staples (6.1%) | |||||||||||

| 55,400 | Albertson's, Inc. | 1,182,790 | |||||||||

| 24,000 | Altria Group, Inc. | 1,793,280 | |||||||||

| 38,000 | Kimberly-Clark Corp. | 2,266,700 | |||||||||

| 90,452 | Sara Lee Corp. | 1,709,543 | |||||||||

| 6,952,313 | |||||||||||

| Energy (13.0%) | |||||||||||

| 19,000 | Anadarko Petroleum Corp. | 1,800,250 | |||||||||

| 9,000 | Burlington Resources, Inc. | 775,800 | |||||||||

| 50,800 | ChevronTexaco Corp. | 2,883,916 | |||||||||

| 53,400 | ConocoPhillips | 3,106,812 | |||||||||

| 47,632 | Exxon Mobil Corp. | 2,675,489 | |||||||||

| 38,500 | Royal Dutch Shell PLC, A Shares, ADR | 2,367,365 | |||||||||

| 12,000 | Schlumberger, Ltd. | 1,165,800 | |||||||||

| 14,775,432 | |||||||||||

| Financials (30.5%) | |||||||||||

| 6,000 | Ambac Financial Group, Inc. | 462,360 | |||||||||

| 17,000 | American International Group, Inc. | 1,159,910 | |||||||||

| 76,000 | Bank of America Corp. | 3,507,400 | |||||||||

| 37,000 | Bank of New York Co., Inc. (The) | 1,178,450 | |||||||||

| 62,333 | Citigroup, Inc. | 3,025,020 | |||||||||

| 15,000 | Equity Residential, REIT | 586,800 | |||||||||

| 34,000 | Fannie Mae | 1,659,540 | |||||||||

| 11,500 | Franklin Resources, Inc. | 1,081,115 | |||||||||

| 44,677 | ING Groep NV, ADR | 1,555,653 | |||||||||

| 74,490 | J.P. Morgan Chase & Co. | 2,956,508 | |||||||||

| 23,200 | Lincoln National Corp. | 1,230,296 | |||||||||

| 30,000 | Merrill Lynch & Company, Inc. | 2,031,900 | |||||||||

| 37,000 | Northern Trust Corp. | 1,917,340 | |||||||||

| 45,000 | Old Republic International Corp. | 1,181,700 | |||||||||

| 38,000 | PNC Financial Services Group, Inc. | 2,349,540 | |||||||||

| 56,600 | St. Paul Travelers Cos, Inc. (The) | 2,528,322 | |||||||||

| 26,000 | SunTrust Banks, Inc. | 1,891,760 | |||||||||

| 52,000 | Washington Mutual, Inc. | 2,262,000 | |||||||||

| 22,900 | Wells Fargo & Co. | 1,438,807 | |||||||||

| 16,400 | Willis Group Holdings, Ltd. | 605,816 | |||||||||

| 34,610,237 | |||||||||||

| Health Care (9.0%) | |||||||||||

| 29,200 | Abbott Laboratories | 1,151,356 | |||||||||

| 43,600 | Bristol-Myers Squibb Co. | 1,001,928 | |||||||||

| 17,000 | Cigna Corp. | 1,898,900 | |||||||||

| 25,000 | HCA, Inc. | 1,262,500 | |||||||||

| 17,400 | Johnson & Johnson | 1,045,740 | |||||||||

| 61,000 | Merck & Co., Inc. | 1,940,410 | |||||||||

| 51,000 | Pfizer, Inc. | 1,189,320 | |||||||||

| 15,000 | Wyeth | 691,050 | |||||||||

| 10,181,204 | |||||||||||

| Shares or Principal Amount | Fair Value | ||||||||||

| COMMON STOCKS — (continued) | |||||||||||

| Industrials (7.4%) | |||||||||||

| 15,000 | CSX Corp. | $ | 761,550 | ||||||||

| 9,500 | Emerson Electric Co. | 709,650 | |||||||||

| 31,000 | General Electric Co. | 1,086,550 | |||||||||

| 18,900 | Parker-Hannifin Corp. | 1,246,644 | |||||||||

| 3,500 | Phelps Dodge Corp. | 503,545 | |||||||||

| 27,600 | Pitney Bowes, Inc. | 1,166,100 | |||||||||

| 47,000 | Raytheon Co. | 1,887,050 | |||||||||

| 14,000 | Textron, Inc. | 1,077,720 | |||||||||

| 8,438,809 | |||||||||||

| Information Technology (8.3%) | |||||||||||

| 25,400 | Automatic Data Processing, Inc. | 1,165,606 | |||||||||

| 29,000 | First Data Corp. | 1,247,290 | |||||||||

| 82,200 | Hewlett-Packard Co. | 2,353,386 | |||||||||

| 4,800 | IBM Corp. | 394,560 | |||||||||

| 40,000 | Microsoft Corp. | 1,046,000 | |||||||||

| 87,000 | Nokia Corp., ADR | 1,592,100 | |||||||||

| 96,000 | Time Warner, Inc. | 1,674,240 | |||||||||

| 9,473,182 | |||||||||||

| Materials (4.9%) | |||||||||||

| 17,000 | Air Products & Chemicals, Inc. | 1,006,230 | |||||||||

| 41,000 | Alcoa, Inc. | 1,212,370 | |||||||||

| 5,000 | E.I. DuPont de Nemours & Co. | 212,500 | |||||||||

| 39,800 | Sonoco Products Co. | 1,170,120 | |||||||||

| 30,000 | Weyerhaeuser Co. | 1,990,200 | |||||||||

| 5,591,420 | |||||||||||

| Telecommunication Services (5.0%) | |||||||||||

| 72,399 | AT&T, Inc. | 1,773,052 | |||||||||

| 36,800 | BellSouth Corp. | 997,280 | |||||||||

| 60,000 | Sprint Nextel Corp. | 1,401,600 | |||||||||

| 52,000 | Verizon Communications, Inc. | 1,566,240 | |||||||||

| 5,738,172 | |||||||||||

| Utilities (5.3%) | |||||||||||

| 16,000 | Dominion Resources, Inc. | 1,235,200 | |||||||||

| 30,000 | Duke Energy Corp. | 823,500 | |||||||||

| 38,200 | National Fuel Gas Co. | 1,191,458 | |||||||||

| 70,000 | NiSource, Inc. | 1,460,200 | |||||||||

| 6,450 | SCANA Corp. | 254,001 | |||||||||

| 59,910 | Xcel Energy, Inc. | 1,105,939 | |||||||||

| 6,070,298 | |||||||||||

| Total Common Stocks (Cost $90,964,299) | 110,646,901 | ||||||||||

| REPURCHASE AGREEMENT (2.7%) | |||||||||||

| $ | 3,042,954 | U.S. Bank N.A., 4.05%, dated 12/30/05, maturing 1/3/06, with a maturity value of $3,044,323 (Collateralized fully by U.S. Government Agencies) | 3,042,954 | ||||||||

| Total Repurchase Agreement (Cost $3,042,954) | 3,042,954 | ||||||||||

| Total Investments (Cost $94,007,253) — 100.0% | 113,689,855 | ||||||||||

| Net other assets (liabilities) — 0.0% | (41,859 | ) | |||||||||

| NET ASSETS — 100.0% | $ | 113,647,996 | |||||||||

See accompanying notes to schedules of portfolio investments and notes to the financial statements.

11

BB&T Mid Cap Growth VIF

Schedule of Portfolio Investments

December 31, 2005

| Shares | Fair Value | ||||||||||

| COMMON STOCKS (92.5%) | |||||||||||

| Consumer Discretionary (12.6%) | |||||||||||

| 9,850 | Abercrombie & Fitch Co., Class A | $ | 642,023 | ||||||||

| 11,550 | Advance Auto Parts, Inc. (a) | 501,963 | |||||||||

| 10,000 | Carter's, Inc. (a) | 588,500 | |||||||||

| 14,400 | Chico's FAS, Inc. (a) | 632,592 | |||||||||

| 17,100 | Coach, Inc. (a) | 570,114 | |||||||||

| 5,700 | Getty Images, Inc. (a) | 508,839 | |||||||||

| 3,625 | Harman International Industries, Inc. | 354,706 | |||||||||

| 6,500 | Starwood Hotels & Resorts Worldwide, Inc. | 415,090 | |||||||||

| 28,000 | Urban Outfitters, Inc. (a) | 708,680 | |||||||||

| 4,922,507 | |||||||||||

| Energy (13.1%) | |||||||||||

| 7,300 | Arch Coal, Inc. | 580,350 | |||||||||

| 15,000 | Cal Dive International, Inc. (a) | 538,350 | |||||||||

| 9,700 | Cameco Corp. | 614,883 | |||||||||

| 19,700 | Chesapeake Energy Corp. | 625,081 | |||||||||

| 15,600 | Cooper Cameron Corp. (a) | 645,840 | |||||||||

| 16,000 | Grant Prideco, Inc. (a) | 705,920 | |||||||||

| 5,950 | National-Oilwell Varco, Inc. (a) | 373,065 | |||||||||

| 8,100 | Peabody Energy Corp. | 667,602 | |||||||||

| 10,300 | Rowan Cos., Inc. | 367,092 | |||||||||

| 1 | XTO Energy, Inc. | 44 | |||||||||

| 5,118,227 | |||||||||||

| Financials (8.3%) | |||||||||||

| 9,700 | Affiliated Managers Group, Inc. (a) | 778,425 | |||||||||

| 27,000 | Ameritrade Holding Corp. (a) | 648,000 | |||||||||

| 1,950 | Chicago Mercantile Exchange Holdings, Inc. | 716,606 | |||||||||

| 6,000 | Legg Mason, Inc. | 718,140 | |||||||||

| 5,500 | T. Rowe Price Group, Inc. | 396,165 | |||||||||

| 3,257,336 | |||||||||||

| Health Care (16.1%) | |||||||||||

| 6,100 | Aetna, Inc. | 575,291 | |||||||||

| 13,500 | Caremark Rx, Inc. (a) | 699,165 | |||||||||

| 12,250 | Celgene Corp. (a) | 793,800 | |||||||||

| 4,600 | Cerner Corp. (a) | 418,186 | |||||||||

| 11,700 | Covance, Inc. (a) | 568,035 | |||||||||

| 9,500 | Coventry Health Care, Inc. (a) | 541,120 | |||||||||

| 16,000 | Dade Behring Holdings, Inc. | 654,240 | |||||||||

| 8,000 | Genzyme Corp. (a) | 566,240 | |||||||||

| 8,400 | Humana, Inc. (a) | 456,372 | |||||||||

| 9,100 | Omnicare, Inc. | 520,702 | |||||||||

| 13,400 | ResMed, Inc. (a) | 513,354 | |||||||||

| 6,306,505 | |||||||||||

| Industrials (13.2%) | |||||||||||

| 9,500 | Canadian Pacific Railway, Ltd. | 398,525 | |||||||||

| 24,500 | Gol-Linhas Aereas Inteligentes, ADR | 691,145 | |||||||||

| 9,300 | Goodrich Corp. | 382,230 | |||||||||

| 10,300 | JLG Industries, Inc. | 470,298 | |||||||||

| 18,300 | Joy Global, Inc. | 732,000 | |||||||||

| 16,700 | Monster Worldwide, Inc. (a) | 681,694 | |||||||||

| 11,400 | Precision Castparts Corp. | 590,634 | |||||||||

| 6,800 | Rockwell Automation, Inc. | 402,288 | |||||||||

| Shares or Principal Amount | Fair Value | ||||||||||

| COMMON STOCKS — (continued) | |||||||||||

| Industrials — (continued) | |||||||||||

| 8,750 | UTI Worldwide, Inc. | $ | 812,350 | ||||||||

| 5,161,164 | |||||||||||

| Information Technology (21.9%) | |||||||||||

| 16,950 | Advanced Micro Devices, Inc. (a) | 518,670 | |||||||||

| 11,300 | Amphenol Corp., Class A | 500,138 | |||||||||

| 11,400 | ATI Technologies, Inc. (a) | 193,686 | |||||||||

| 13,300 | AutoDesk, Inc. | 571,235 | |||||||||

| 10,500 | Broadcom Corp., Class A (a) | 495,075 | |||||||||

| 26,500 | CNET Networks, Inc. (a) | 389,285 | |||||||||

| 17,500 | Cognizant Technology Solutions Corp., Class A (a) | 881,125 | |||||||||

| 32,000 | Comverse Technology, Inc. (a) | 850,880 | |||||||||

| 14,800 | Harris Corp. | 636,548 | |||||||||

| 31,700 | Intersil Corp., Class A | 788,696 | |||||||||

| 19,700 | Jabil Circuit, Inc. (a) | 730,673 | |||||||||

| 14,000 | Marvell Technology Group, Ltd. (a) | 785,260 | |||||||||

| 27,500 | MEMC Electronic Materials, Inc. (a) | 609,675 | |||||||||

| 13,400 | Varian Semiconductor Equipment Associates, Inc. (a) | 588,662 | |||||||||

| 8,539,608 | |||||||||||

| Materials (2.5%) | |||||||||||

| 18,700 | Airgas, Inc. | 615,230 | |||||||||

| 7,750 | Florida Rock Industries, Inc. | 380,215 | |||||||||

| 995,445 | |||||||||||

| Telecommunication Services (4.8%) | |||||||||||

| 43,000 | American Tower Corp., Class A (a) | 1,165,300 | |||||||||

| 16,600 | NII Holdings, Inc. (a) | 725,088 | |||||||||

| 1,890,388 | |||||||||||

| Total Common Stocks (Cost $25,441,356) | 36,191,180 | ||||||||||

| EXCHANGE TRADED FUNDS (4.3%) | |||||||||||

| 17,700 | iShares Russell Midcap Growth Index Fund | 1,664,508 | |||||||||

| Total Exchange Traded Funds (Cost $1,633,913) | 1,664,508 | ||||||||||

| REPURCHASE AGREEMENT (3.6%) | |||||||||||

| $ | 1,408,006 | U.S. Bank N.A., 4.05%, dated 12/30/05, maturing 1/3/06, with a maturity value of $1,408,640 (Collateralized fully by U.S. Government Agencies) | 1,408,006 | ||||||||

| Total Repurchase Agreement (Cost $1,408,006) | 1,408,006 | ||||||||||

| Total Investments (Cost $28,483,275) — 100.4% | 39,263,694 | ||||||||||

| Net other assets (liabilities) — (0.4)% | (173,196 | ) | |||||||||

| NET ASSETS — 100.0% | $ | 39,090,498 | |||||||||

See accompanying notes to schedules of portfolio investments and notes to the financial statements.

12

BB&T Large Company Growth VIF

Schedule of Portfolio Investments

December 31, 2005

| Shares | Fair Value | ||||||||||

| COMMON STOCKS (95.6%) | |||||||||||

| Consumer Discretionary (9.2%) | |||||||||||

| 3,397 | Chico's FAS, Inc. (a) | $ | 149,230 | ||||||||

| 3,671 | Coach, Inc. (a) | 122,391 | |||||||||

| 2,300 | eBay, Inc. (a) | 99,475 | |||||||||

| 3,933 | Hershey Co., (The) | 217,298 | |||||||||

| 5,814 | Home Depot, Inc. | 235,351 | |||||||||

| 6,410 | Kohl's Corp. (a) | 311,526 | |||||||||

| 1,855 | Lowe's Companies, Inc. | 123,654 | |||||||||

| 1,594 | Nike, Inc., Class B | 138,343 | |||||||||

| 17,297 | Starbucks Corp. (a) | 519,084 | |||||||||

| 2,174 | Target Corp. | 119,505 | |||||||||

| 3,049 | Williams Sonoma, Inc. (a) | 131,564 | |||||||||

| 2,167,421 | |||||||||||

| Consumer Staples (8.8%) | |||||||||||

| 3,182 | Altria Group, Inc. | 237,759 | |||||||||

| 5,749 | Coca-Cola Co. | 231,742 | |||||||||

| 8,753 | PepsiCo, Inc. | 517,127 | |||||||||

| 9,033 | Procter & Gamble Co. | 522,830 | |||||||||

| 11,936 | Wal-Mart Stores, Inc. | 558,605 | |||||||||

| 2,068,063 | |||||||||||

| Energy (5.6%) | |||||||||||

| 3,737 | Anadarko Petroleum Corp. | 354,081 | |||||||||

| 5,136 | Apache Corp. | 351,919 | |||||||||

| 6,270 | Baker Hughes, Inc. | 381,090 | |||||||||

| 3,842 | ConocoPhillips | 223,528 | |||||||||

| 1,310,618 | |||||||||||

| Financials (4.8%) | |||||||||||

| 4,399 | American International Group, Inc. | 300,143 | |||||||||

| 2,355 | CIT Group, Inc. | 121,942 | |||||||||

| 2,553 | Franklin Resources, Inc. | 240,008 | |||||||||

| 1,890 | Goldman Sachs Group, Inc. (The) | 241,372 | |||||||||

| 3,699 | PNC Financial Services Group, Inc. | 228,709 | |||||||||

| 1,132,174 | |||||||||||

| Health Care (20.2%) | |||||||||||

| 6,940 | Abbott Laboratories | 273,644 | |||||||||

| 6,253 | Amgen, Inc. (a) | 493,112 | |||||||||

| 5,865 | Caremark Rx, Inc. (a) | 303,748 | |||||||||

| 2,385 | Genentech, Inc. (a) | 220,613 | |||||||||

| 2,870 | Genzyme Corp. (a) | 203,139 | |||||||||

| 5,502 | Gilead Sciences, Inc. (a) | 289,570 | |||||||||

| 11,846 | Johnson & Johnson | 711,944 | |||||||||

| 4,449 | Medco Health Solutions, Inc. (a) | 248,254 | |||||||||

| 8,608 | Medtronic, Inc. | 495,562 | |||||||||

| 5,400 | Novartis AG, ADR | 283,392 | |||||||||

| 9,865 | Pfizer, Inc. | 230,052 | |||||||||

| 6,811 | UnitedHealth Group, Inc. | 423,236 | |||||||||

| 3,056 | Wellpoint, Inc. (a) | 243,838 | |||||||||

| 7,140 | Wyeth | 328,940 | |||||||||

| 4,749,044 | |||||||||||

| Industrials (17.3%) | |||||||||||

| 4,514 | Boeing Co. | 317,063 | |||||||||

| 6,201 | Caterpillar, Inc. | 358,232 | |||||||||

| Shares or Principal Amount | Fair Value | ||||||||||

| COMMON STOCKS — (continued) | |||||||||||

| Industrials — (continued) | |||||||||||

| 2,245 | Danaher Corp. | $ | 125,226 | ||||||||

| 6,296 | Dow Chemical Co. (The) | 275,891 | |||||||||

| 1,406 | FedEx Corp. | 145,366 | |||||||||

| 28,213 | General Electric Co. | 988,866 | |||||||||

| 3,300 | Honeywell International, Inc. | 122,925 | |||||||||

| 2,892 | Illinois Tool Works, Inc. | 254,467 | |||||||||

| 11,774 | National Semiconductor Corp. | 305,889 | |||||||||

| 2,415 | Phelps Dodge Corp. | 347,446 | |||||||||

| 4,661 | Precision Castparts Corp. | 241,486 | |||||||||

| 3,158 | United Parcel Service, Inc., Class B | 237,324 | |||||||||

| 6,096 | United Technologies Corp. | 340,827 | |||||||||

| 4,061,008 | |||||||||||

| Information Technology (28.8%) | |||||||||||

| 4,941 | 3M Co. | 382,928 | |||||||||

| 1,887 | Apple Computer, Inc. (a) | 135,656 | |||||||||

| 30,747 | Cisco Systems, Inc. (a) | 526,389 | |||||||||

| 12,768 | Corning, Inc. (a) | 251,019 | |||||||||

| 7,767 | Dell, Inc. (a) | 232,932 | |||||||||

| 8,530 | EMC Corp. (a) | 116,179 | |||||||||

| 605 | Google, Inc . (a) | 250,990 | |||||||||

| 6,442 | IBM Corp. | 529,532 | |||||||||

| 31,504 | Intel Corp. | 786,340 | |||||||||

| 37,536 | Microsoft Corp. | 981,567 | |||||||||

| 9,956 | Monster Worldwide, Inc. (a) | 406,404 | |||||||||

| 19,939 | Motorola, Inc. | 450,422 | |||||||||

| 10,094 | Nokia Corp., ADR | 184,720 | |||||||||

| 30,800 | Oracle Corp. (a) | 376,068 | |||||||||

| 6,100 | QUALCOMM, Inc. | 262,788 | |||||||||

| 11,579 | Texas Instruments, Inc. | 371,339 | |||||||||

| 23,776 | Time Warner, Inc. | 414,653 | |||||||||

| 3,116 | Yahoo!, Inc. (a) | 122,085 | |||||||||

| 6,782,011 | |||||||||||

| Telecommunication Services (0.9%) | |||||||||||

| 9,423 | Sprint Nextel Corp. | 220,121 | |||||||||

| Total Common Stocks (Cost $20,175,360) | 22,490,460 | ||||||||||

| REPURCHASE AGREEMENT (4.4%) | |||||||||||

| $ | 1,026,296 | U.S. Bank N.A., 4.05% dated 12/30/05, maturing 1/3/06, with a maturity value of $1,026,758 (Collateralized fully by U.S. Government Agencies) | 1,026,296 | ||||||||

| Total Repurchase Agreement (Cost $1,026,296) | 1,026,296 | ||||||||||

| Total Investments (Cost $21,201,656) — 100.0% | 23,516,756 | ||||||||||

| Net other assets (liabilities) — 0.0% | 6,415 | ||||||||||

| NET ASSETS — 100.0% | $ | 23,523,171 | |||||||||

See accompanying notes to schedules of portfolio investments and notes to the financial statements.

13

BB&T Capital Manager Equity VIF

Schedule of Portfolio Investments

December 31, 2005

| Shares | Fair Value | ||||||||||

| INVESTMENT COMPANIES (99.9%) | |||||||||||

| 432,590 | BB&T Equity Index Fund, Class A | $ | 3,629,430 | ||||||||

| 416,286 | BB&T International Equity Fund, Institutional Class | 4,204,486 | |||||||||

| 632,624 | BB&T Large Company Growth Fund, Institutional Class | 5,820,140 | |||||||||

| 475,413 | BB&T Large Company Value Fund, Institutional Class | 8,695,304 | |||||||||

| 99,177 | BB&T Mid Cap Growth Fund, Institutional Class (a) | 1,334,918 | |||||||||

| 163,034 | BB&T Mid Cap Value Fund, Institutional Class | 2,002,055 | |||||||||

| 56,293 | BB&T Small Company Growth Fund, Institutional Class (a) | 853,958 | |||||||||

| Shares | Fair Value | ||||||||||

| INVESTMENT COMPANIES — (continued) | |||||||||||

| 89,284 | BB&T Small Cap Fund, Institutional Class | $ | 1,279,442 | ||||||||

| 865,285 | BB&T U.S. Treasury Money Market Fund, Institutional Class | 865,285 | |||||||||

| Total Investment Companies (Cost $27,080,066) | 28,685,018 | ||||||||||

| Total Investments (Cost $27,080,066) — 99.9% | 28,685,018 | ||||||||||

| Net other assets (liabilities) — 0.1% | 36,990 | ||||||||||

| NET ASSETS — 100.0% | $ | 28,722,008 | |||||||||

See accompanying notes to schedules of portfolio investments and notes to the financial statements.

14

BB&T Special Opportunities Equity VIF

Schedule of Portfolio Investments

December 31, 2005

| Shares | Fair Value | ||||||||||

| COMMON STOCKS (89.7%) | |||||||||||

| Commercial Services (6.8%) | |||||||||||

| 54,500 | Cendant Corp. | $ | 940,125 | ||||||||

| 44,900 | WCI Communities, Inc. (a) | 1,205,565 | |||||||||

| 2,145,690 | |||||||||||

| Consumer Discretionary (20.4%) | |||||||||||

| 20,500 | Anheuser-Busch Companies, Inc. | 880,680 | |||||||||

| 46,450 | Comcast Corp., Class A (a) | 1,205,842 | |||||||||

| 16,500 | Costco Wholesale Corp. | 816,255 | |||||||||

| 10,000 | Hain Celestial Group, Inc. (a) | 211,600 | |||||||||

| 65,340 | News Corp., Class A | 1,016,037 | |||||||||

| 43,100 | Smithfield Foods, Inc. (a) | 1,318,860 | |||||||||

| 22,200 | YUM! Brands, Inc. | 1,040,736 | |||||||||

| 6,490,010 | |||||||||||

| Energy (15.0%) | |||||||||||

| 16,800 | Apache Corp. | 1,151,136 | |||||||||

| 19,900 | CONSOL Energy, Inc. | 1,297,082 | |||||||||

| 20,600 | Pioneer Natural Resources Co. | 1,056,162 | |||||||||

| 34,600 | Weatherford International, Ltd. (a) | 1,252,520 | |||||||||

| 4,756,900 | |||||||||||

| Financials (8.2%) | |||||||||||

| 2,600 | Markel Corp. (a) | 824,330 | |||||||||

| 11,000 | MBIA, Inc. | 661,760 | |||||||||

| 18,000 | Wells Fargo & Co. | 1,130,940 | |||||||||

| 2,617,030 | |||||||||||

| Health Care (13.2%) | |||||||||||

| 111,448 | Emdeon Corp. (a) | 942,850 | |||||||||

| 18,900 | Laboratory Corporation of America Holdings (a) | 1,017,765 | |||||||||

| 28,000 | Manor Care, Inc. | 1,113,560 | |||||||||

| 60,503 | MedCath Corp. (a) | 1,122,331 | |||||||||

| 4,196,506 | |||||||||||

| Shares or Principal Amount | Fair Value | ||||||||||

| COMMON STOCKS — (continued) | |||||||||||

| Industrials (7.6%) | |||||||||||

| 16,000 | L-3 Communications Holdings, Inc. | $ | 1,189,600 | ||||||||

| 17,500 | PACCAR, Inc. | 1,211,525 | |||||||||

| 2,401,125 | |||||||||||

| Information Technology (18.5%) | |||||||||||

| 42,400 | Activision, Inc. (a) | 582,576 | |||||||||

| 175,880 | ARM Holdings PLC, ADR | 1,092,215 | |||||||||

| 49,200 | ATI Technologies, Inc. (a) | 835,908 | |||||||||

| 17,000 | Fair Issac Corp. | 750,890 | |||||||||

| 27,840 | First Data Corp. | 1,197,398 | |||||||||

| 33,000 | Packeteer, Inc. (a) | 256,410 | |||||||||

| 66,400 | Symantec Corp. (a) | 1,162,000 | |||||||||

| 5,877,397 | |||||||||||

| Total Common Stocks (Cost $25,531,936) | 28,484,658 | ||||||||||

| REPURCHASE AGREEMENT (10.7%) | |||||||||||

| $ | 3,403,712 | U.S. Bank N.A., 4.05%, dated 12/30/05, maturing 1/3/06, with a maturity value of $3,405,244 (Collateralized fully by U.S. Government Agencies) | 3,403,712 | ||||||||

| Total Repurchase Agreement (Cost $3,403,712) | 3,403,712 | ||||||||||

| Total Investments (Cost $28,935,648) — 100.4% | 31,888,370 | ||||||||||

| Net other assets (liabilities) — (0.4)% | (120,128 | ) | |||||||||

| NET ASSETS — 100.0% | $ | 31,768,242 | |||||||||

See accompanying notes to schedules of portfolio investments and notes to the financial statements.

15

BB&T Total Return Bond VIF

Schedule of Portfolio Investments

December 31, 2005

| Principal Amount | Fair Value | ||||||||||

| CORPORATE BONDS (40.1%) | |||||||||||

| Aerospace & Defense (0.5%) | |||||||||||

| $ | 85,000 | Raytheon Co., 6.15%, 11/1/08 | $ | 88,215 | |||||||

| Airlines (0.6%) | |||||||||||

| 125,000 | Southwest Airlines Co., 5.25%, 10/1/14 | 121,219 | |||||||||

| Auto — Cars/Light Trucks (0.7%) | |||||||||||

| 125,000 | DaimlerChrysler NA Holdings, 4.875%, 6/15/10 | 122,048 | |||||||||

| Banking & Financial Services (32.5%) | |||||||||||

| 87,000 | Associates Corp. NA, 6.25%, 11/1/08 | 90,121 | |||||||||

| 355,000 | Bank of America Commercial Mortgage, Inc., Series 2004-6, Class A5, 4.81%, 12/10/42 | 346,119 | |||||||||

| 155,000 | Bank of America Corp., 4.25%, 10/1/10 | 150,723 | |||||||||

| 184,000 | Centex Home Equity, Series 2005-C, Class AF6, 4.64%, 6/25/35 | 178,782 | |||||||||

| 345,000 | Chase Funding Mortgage Loan Asset-Backed, Series 2003-4, Class 1A5, 5.42%, 5/25/33 | 345,104 | |||||||||

| 500,000 | Chase Issuance Trust, Series 2005-A1, Class A1, 4.38%, 12/15/10 (c)* | 500,050 | |||||||||

| 82,000 | CIT Group, Inc., 5.00%, 2/13/14 | 80,209 | |||||||||

| 200,000 | CIT Group, Inc., Series MTN, 4.73%, 9/20/07* | 200,661 | |||||||||

| 490,000 | Countrywide Asset-Backed Certificates, Series 2004-3, Class 3A3, 4.76%, 8/25/34 (c)* | 491,375 | |||||||||

| 284,000 | Countrywide Asset-Backed Certificates, Series 2005-4, Class 3AV2, 4.59%, 10/25/35 (c)* | 284,050 | |||||||||

| 250,000 | CS First Boston Mortgage Securities Corp., Series 2004-C1, Class A2, 3.52%, 1/15/37 | 241,005 | |||||||||

| 182,000 | Gatx Financial Corp., 5.125%, 4/15/10 | 180,201 | |||||||||

| 166,000 | GE Capital Commercial Mortgage Corp., Series 2005-C4, Class A4, 5.33%, 11/10/45 | 168,962 | |||||||||

| 173,912 | GE Capital Commercial Mortgage Corp., Series 2001-3, Class A1, 5.56%, 6/10/38 | 175,602 | |||||||||

| 310,000 | GE Capital Commercial Mortgage Corp., Series 2004-C1, Class A2, 3.915%, 11/10/38 | 297,767 | |||||||||

| 184,000 | General Motors Acceptance Corp., 6.75%, 12/1/14 | 165,530 | |||||||||

| 130,000 | Goldman Sachs Group, Inc., 4.125%, 1/15/08 | 128,004 | |||||||||

| 175,000 | Household Automotive Trust, Series 2005-1, Class A4, 4.35%, 6/18/12 | 172,122 | |||||||||

| 150,000 | HSBC Finance Corp., 4.75%, 7/15/13 | 144,927 | |||||||||

| 265,000 | Lehman Brothers Holdings, Series MTNG, 4.80%, 3/13/14 | 258,744 | |||||||||

| 190,000 | Merrill Lynch & Co., 6.00%, 2/17/09 | 195,935 | |||||||||

| 170,000 | Morgan Stanley, 4.25%, 5/15/10 | 164,326 | |||||||||

| 251,602 | Residential Asset Mortgage Products, Inc., Series 2003-RZ5, Class A3, 3.80%, 7/25/30 | 250,607 | |||||||||

| 408,000 | Residential Asset Securities Corp., Series 2005-KS6, Class A2, 4.53%, 7/25/35 (c)* | 407,814 | |||||||||

| 147,000 | Synovus Financial, 4.875%, 2/15/13 | 144,383 | |||||||||

| 200,000 | Wachovia Corp., 4.28%, 10/28/08* | 199,979 | |||||||||

| 140,000 | Wachovia Corp., 4.375%, 6/1/10 | 136,951 | |||||||||

| 6,100,053 | |||||||||||

| Telecommunications (4.1%) | |||||||||||

| 175,000 | America Movil SA de CV, 5.75%, 1/15/15 | 175,595 | |||||||||

| 320,000 | Motorola, Inc., 7.50%, 5/15/25 | 385,028 | |||||||||

| 200,000 | Sprint Capital Corp., 6.875%, 11/15/28 | 218,538 | |||||||||

| 779,161 | |||||||||||

| Principal Amount | Fair Value | ||||||||||

| CORPORATE BONDS — (continued) | |||||||||||

| Utilities (1.7%) | |||||||||||

| $ | 215,000 | American Electric Power, Series C, 5.375%, 3/15/10 | $ | 216,731 | |||||||

| 105,000 | General Electric Co., 5.00%, 2/1/13 | 104,945 | |||||||||

| 321,676 | |||||||||||

| Total Corporate Bonds (Cost $7,590,167) | 7,532,372 | ||||||||||

| MORTGAGE-BACKED SECURITIES (33.2%) | |||||||||||

| Federal Home Loan Mortgage Corp. (7.6%) | |||||||||||

| 795,375 | 6.00%, 10/1/19, Pool # G11679 | 811,633 | |||||||||

| 94,665 | 5.50%, 11/1/20, Pool # J02711 | 95,239 | |||||||||

| 166,833 | 4.50%, 6/1/35, Pool # G01842 | 156,962 | |||||||||

| 152,766 | 5.50%, 7/1/35, Pool # A36540 | 151,397 | |||||||||

| 121,706 | 6.00%, 7/1/35, Pool # A36304 | 122,936 | |||||||||

| 91,001 | 5.50%, 12/1/35, Pool # A40359 | 90,186 | |||||||||

| 1,428,353 | |||||||||||

| Federal National Mortgage Assoc. (17.2%) | |||||||||||

| 134,396 | 4.50%, 10/1/18, Pool # 752030 | 130,782 | |||||||||

| 90,659 | 5.50%, 11/1/20, Pool # 843972 | 91,250 | |||||||||

| 1,451,321 | 5.50%, 1/1/34, Pool # 757571 | 1,437,367 | |||||||||

| 351,628 | 6.50%, 9/1/34, Pool # 796569 | 360,765 | |||||||||

| 505,313 | 6.00%, 2/1/35, Pool # 735269 | 510,114 | |||||||||

| 125,019 | 6.00%, 5/1/35, Pool # 821037 | 126,207 | |||||||||

| 256,470 | 7.00%, 6/1/35, Pool # 255820 | 267,597 | |||||||||

| 132,227 | 5.00%, 9/1/35, Pool # 757857 | 128,122 | |||||||||

| 89,399 | 6.00%, 11/1/35, Pool # 843803 | 90,249 | |||||||||

| 93,186 | 6.00%, 11/1/35, Pool # 817636 | 94,072 | |||||||||

| 3,236,525 | |||||||||||

| Government National Mortgage Assoc. (8.4%) | |||||||||||

| 1,590,000 | 5.00%, 1/1/36 (b) | 1,568,634 | |||||||||

| Total Mortgage-Backed Securities (Cost $6,281,141) | 6,233,512 | ||||||||||

| MUNICIPAL BONDS (2.2%) | |||||||||||

| Illinois (0.4%) | |||||||||||

| 85,000 | Illinois State, 3.75%, 6/1/12 | 79,865 | |||||||||

| New York (0.5%) | |||||||||||

| 100,000 | Sales Tax Asset Receivables Corp., Series B, 4.06%, 10/15/10, FGIC | 96,694 | |||||||||

| Oregon (0.5%) | |||||||||||

| 95,000 | Oregon School Boards Association, 4.76%, 6/30/28, AMBAC | 89,122 | |||||||||

| Texas (0.8%) | |||||||||||

| 155,000 | Brownsville Texas Utility System, Series B, 4.92%, 9/1/14, AMBAC | 154,525 | |||||||||

| Total Municipal Bonds (Cost $424,345) | 420,206 | ||||||||||

| U.S. GOVERNMENT AGENCIES (13.9%) | |||||||||||

| Federal Home Loan Bank (4.4%) | |||||||||||

| 200,000 | 4.25%, 9/28/06, Callable 3/28/06 @ 100* | 199,767 | |||||||||

| 150,000 | 4.25%, 3/24/08, Callable 3/24/06 @ 100 | 148,260 | |||||||||

| 220,000 | 3.75%, 8/15/08 | 214,770 | |||||||||

| 245,000 | Series FB11, 5.875%, 2/15/11 | 255,989 | |||||||||

| 818,786 | |||||||||||

Continued

16

BB&T Total Return Bond VIF

Schedule of Portfolio Investments — (continued)

December 31, 2005

| Principal Amount | Fair Value | ||||||||||

| U.S. GOVERNMENT AGENCIES — (continued) | |||||||||||

| Federal Home Loan Mortgage Corp. (3.2%) | |||||||||||

| $ | 100,000 | 3.75%, 2/25/08, Callable 2/25/06 @ 100* | $ | 99,371 | |||||||

| 196,000 | 4.625%, 8/15/08, Callable 8/15/06 @ 100 | 194,994 | |||||||||

| 210,000 | 4.125%, 7/12/10 | 204,782 | |||||||||

| 109,000 | 5.50%, 8/20/19, Callable 8/20/07 @ 100 | 108,142 | |||||||||

| 607,289 | |||||||||||

| Federal National Mortgage Assoc. (4.7%) | |||||||||||

| 385,000 | 6.625%, 11/15/10 | 416,054 | |||||||||

| 439,000 | 6.00%, 5/15/11 | 464,302 | |||||||||

| 880,356 | |||||||||||

| Student Loan Marketing Assoc. (1.6%) | |||||||||||

| 150,000 | Series MTNA, 4.28%, 1/25/08* | 150,096 | |||||||||

| 150,000 | Series MTNA, 4.00%, 1/15/09 | 145,970 | |||||||||

| 296,066 | |||||||||||

| Total U.S. Government Agencies (Cost $2,614,263) | 2,602,497 | ||||||||||

| U.S. TREASURY BONDS (9.5%) | |||||||||||

| 455,000 | 8.875%, 8/15/17 | 632,272 | |||||||||

| 314,000 | 7.875%, 2/15/21 | 424,955 | |||||||||

| 283,000 | 7.25%, 8/15/22 | 368,541 | |||||||||

| 300,000 | 6.25%, 8/15/23 | 358,242 | |||||||||

| Total U.S. Treasury Bonds (Cost $1,790,054) | 1,784,010 | ||||||||||

| U.S. TREASURY NOTES (0.9%) | |||||||||||

| 167,000 | 4.50%, 11/15/10 | 167,900 | |||||||||

| Total U.S. Treasury Notes (Cost $166,661) | 167,900 | ||||||||||

| Principal Amount | Fair Value | ||||||||||

| REPURCHASE AGREEMENT (7.5%) | |||||||||||

| $ | 1,409,886 | U.S. Bank N.A., 4.05%, dated 12/30/05, maturing 1/3/06, with a maturity value of $1,410,520 (Collateralized fully by U.S. Government Agencies) | $ | 1,409,886 | |||||||

| Total Repurchase Agreement (Cost $1,409,886) | 1,409,886 | ||||||||||

| Total Investments (Cost $20,276,517) — 107.3% | 20,150,383 | ||||||||||

| Net other assets (liabilities) — (7.3)% | (1,373,668 | ) | |||||||||

| NET ASSETS — 100.0% | $ | 18,776,715 | |||||||||

See accompanying notes to schedules of portfolio investments and notes to the financial statements.

17

Schedule of Portfolio Investments

Notes to Schedules of Portfolio Investments

December 31, 2005

(a) Represents non-income producing security.

(b) Represents a security purchased on a when-issued basis. At December 31, 2005, total cost of investments purchased on a when-issued basis for the BB&T Total Return Bond VIF was $1,552,304.

(c) Represents that all or a portion of the security was pledged as collateral for securities purchased on a when-issued basis.

* The interest rate for this variable rate note, which will change periodically, is based either on the prime rate or an index of market rates. The reflected rate is the rate in effect as of December 31, 2005. The maturity date reflected is the final maturity date.

ADR — American Depository Receipt.

AMBAC — Insured by AMBAC Indemnity Corp.

FGIC — Insured by Financial Guaranty Insurance Corp.

REIT — Real Estate Investment Trust.

See accompanying notes to financial statements.

18

(This page has been left blank intentionally.)

19

BB&T Variable Insurance Funds

Statements of Assets and Liabilities

December 31, 2005

| BB&T Large Cap Value VIF | BB&T Mid Cap Growth VIF | BB&T Large Company Growth VIF | BB&T Capital Manager Equity VIF | BB&T Special Opportunities Equity VIF | BB&T Total Return Bond VIF | ||||||||||||||||||||||

| Assets: | |||||||||||||||||||||||||||

| Investments: | |||||||||||||||||||||||||||

| Unaffiliated investments, at cost | $ | 90,964,299 | $ | 27,075,269 | $ | 20,175,360 | $ | — | $ | 25,531,936 | $ | 18,866,631 | |||||||||||||||

| Investment in affiliates, at cost | — | — | — | 27,080,066 | — | — | |||||||||||||||||||||

| Total investments, at cost | 90,964,299 | 27,075,269 | 20,175,360 | 27,080,066 | 25,531,936 | 18,866,631 | |||||||||||||||||||||

| Unrealized appreciation (depreciation) | 19,682,602 | 10,780,419 | 2,315,100 | 1,604,952 | 2,952,722 | (126,134 | ) | ||||||||||||||||||||

| Investments, at value | 110,646,901 | 37,855,688 | 22,490,460 | 28,685,018 | 28,484,658 | 18,740,497 | |||||||||||||||||||||