UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21700

Tortoise North American Energy Corporation

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

11550 Ash Street, Suite 300, Leawood, KS 66211

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

David J. Schulte

11550 Ash Street, Suite 300, Leawood, KS 66211

(Name and address of agent for service)

11550 Ash Street, Suite 300, Leawood, KS 66211

(Name and address of agent for service)

913-981-1020

Registrant's telephone number, including area code

Registrant's telephone number, including area code

Date of fiscal year end: November 30

Date of reporting period: May 31, 2011

Item 1. Report to Stockholders.

Company at a Glance

Tortoise North American Energy Corp. (NYSE: TYN) is a non-diversified closed-end investment company focused primarily on investing in equity securities of companies in the energy sector with their primary operations in North America, including oil and gas exploitation, energy infrastructure and energy shipping companies. Our investments are primarily in Master Limited Partnerships (MLPs) and their affiliates, but may also include Canadian royalty and income trusts, common stock, debt and other securities issued by energy companies that are not MLPs.

Investment Goals: Yield, Growth and Quality

TYN seeks a high level of total return with an emphasis on current distributions paid to stockholders.

In seeking to achieve yield, we target distributions to our stockholders that are roughly equal to the underlying yield on a direct investment in MLPs. In order to accomplish this, we maintain our strategy of investing primarily in companies in the energy sector with attractive current yields and growth potential.

We seek to achieve distribution growth as revenues of our underlying companies grow with the economy, with the population and through rate increases. This revenue growth generally leads to increased operating profits, and when combined with internal expansion projects and acquisitions, is expected to provide attractive growth in distributions to us.

TYN seeks to achieve quality by investing in companies operating energy infrastructure assets that are critical to the North American economy. Often these assets would be difficult to replicate. We also back experienced management teams with successful track records. By investing in TYN, our stockholders have access to a portfolio that is diversified through geographic regions and across product lines, including natural gas, natural gas liquids, crude oil and refined products.

About U.S. Energy Infrastructure Master Limited Partnerships (MLPs)

MLPs are limited partnerships whose units trade on public exchanges such as the New York Stock Exchange (NYSE), the NYSE Alternext US and the NASDAQ. Buying MLP units makes an investor a limited partner in the MLP. There are currently approximately 70 MLPs in the market, mostly in industries related to energy and natural resources. We invest primarily in MLPs in the energy infrastructure sector. Energy infrastructure MLPs are engaged in the transportation, storage and processing of crude oil, natural gas and refined products from production points to the end users.

TYN Investment Features

We provide stockholders an alternative to investing directly in MLPs and their affiliates. We offer investors the opportunity to receive an attractive distribution return with a historically low return correlation to returns on stocks and bonds.

Additional features include:

- One Form 1099 per stockholder at the end of the year, multiple K-1s and multiple state filings for individual partnership investments;

- A professional management team, with more than 120 years combined investment experience;

- The ability to access investment grade credit markets to enhance stockholder return; and

- Access to direct placements and other investments not available through the public market.

June 16, 2011

Dear Fellow Stockholders,

Recently one of our investment committee members referred to pipelines as “boring” and we were questioned as to how could the assets that help fuel our nation’s economy be boring? Rightly put, if you are using Merriam-Webster’s definition of boring as “dull” or “drab.” However, if you think about it, boring in investing can be anything but boring — it can mean stability, predictability and longevity. In the words of Paul Samuelson, the Nobel Prize winning economist, “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.”

In our philosophy of focusing on yield, growth and quality over the long term, pipelines are boring — not because of what they do — but because they provide such an essential and predictable service to our daily lives. It is with this mindset that we continue to focus our investments on long-haul, fee-based pipeline MLPs that offer stable and growing distribution potential with a modest risk profile.

Master Limited Partnership Sector Review and Outlook

Political unrest in Libya and summer-like temperatures in the U.S. pushed commodity prices higher through the end of the fiscal quarter. As a result, the strongest relative performers within the MLP sector continued to be the more commodity-sensitive companies. The Tortoise Upstream MLP IndexTM posted a total return of 0.5 percent and 15.1 percent for the three months and six months ended May 31, 2011, respectively. In comparison, the Tortoise Long Haul Pipelines MLP IndexTM had a total return of (3.4) percent and 4.2 percent for the same three and six month periods, respectively. The fundamentals supporting the underlying cash flows across the entire MLP sector remain strong.

The acquisition market continued to be active with more than $14 billion of activity in 2011 fiscal year-to-date as large integrated and independent oil and gas companies continued to divest midstream and upstream assets to MLPs. Likewise, equity capital markets remained open, with MLP companies issuing nearly $13 billion during the same period, including $1 billion in direct placements. In addition, five MLP IPOs have closed in 2011 with three others in registration with the SEC.

As we approach the summer, many of us are looking forward to driving or flying to our favorite summer vacation destination. The crude oil and refined product pipeline operators that provide the infrastructure to support our travel activities have regulated revenues that will reflect an annual rate increase this summer. Effective July 1, 2011, petroleum pipelines regulated by the Federal Energy Regulatory Commission (FERC) will increase rates by 6.8 percent. This inherent partial inflation hedge should help offset any higher costs and continue to position these regulated assets well in a higher inflationary environment.

Company Performance Review and Outlook

Our total return based on market value (including the reinvestment of distributions) for the 2011 second fiscal quarter ended May 31, 2011, was (2.8) percent as compared to the Tortoise MLP Total Return Index™ of (2.2) percent during the same period. For the six months ended May 31, 2011, our market-based total return was 2.9 percent as compared to the Tortoise MLP Total Return Index of 6.9 percent. Lastly, the ratio of TYN’s debt as a percentage of our total assets was 12.8 percent as of May 31, 2011, which reflects one of the lowest levels of leverage in the MLP closed-end fund sector.

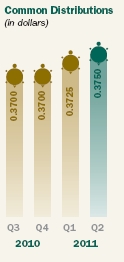

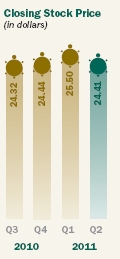

We paid a distribution of $0.3750 per common share ($1.50 annualized) to our stockholders on June 1, 2011, a 0.7 percent increase from our prior quarterly distribution of $0.3725. This represents an annualized yield of 6.1 percent based on the fiscal quarter closing price of $24.41. Our payout ratio of distributions to distributable cash flow (DCF) for the second fiscal quarter was 94.4 percent. For tax purposes, we currently expect 75 to 100 percent of TYN’s 2011 distributions will be characterized as qualified dividend income, with the remainder characterized as return of capital. A final determination of the characterization will be made in January 2012.

TYN helped finance energy infrastructure sector growth with the completion of two direct placements totaling $8 million during the fiscal quarter. Through these investments, we acquired common units in Regency Energy Partners LP and Crestwood Midstream Partners, LP which used the proceeds to help finance acquisitions in natural gas liquids pipeline/storage and natural gas gathering assets, respectively.

Additional information about our financial performance is available in the Management’s Discussion of this report.

Conclusion

We believe TYN offers a diversified portfolio investing across the entire MLP sector with a disciplined management focus on Yield, Growth, and Quality.

Thank you for your investment.

Sincerely,

The Managing Directors

Tortoise Capital Advisors, L.L.C.

The adviser to Tortoise North American Energy Corp.

Tortoise Capital Advisors, L.L.C.

The adviser to Tortoise North American Energy Corp.

|  |  |

| H. Kevin Birzer | Zachary A. Hamel | Kenneth P. Malvey |

|  | |

| Terry Matlack | David J. Schulte |

2011 2nd Quarter Report 1

Key Financial Data (Supplemental Unaudited Information) (dollar amounts in thousands unless otherwise indicated) |

The information presented below regarding Distributable Cash Flow and Selected Operating Ratios is supplemental non-GAAP financial information, which we believe is meaningful to understanding our operating performance. The Selected Operating Ratios are the functional equivalent of EBITDA for non-investment companies, and we believe they are an important supplemental measure of performance and promote comparisons from period-to-period. Supplemental non-GAAP measures should be read in conjunction with our full financial statements.

| 2010 | 2011 | |||||||||||||||||||

| Q2(1) | Q3(1) | Q4(1) | Q1(1) | Q2(1) | ||||||||||||||||

| Total Distributions Received from Investments | ||||||||||||||||||||

| Distributions received from master limited partnerships | $ | 2,424 | $ | 2,497 | $ | 2,556 | $ | 2,666 | $ | 2,736 | ||||||||||

| Dividends paid in stock | 413 | 381 | 393 | 404 | 364 | |||||||||||||||

| Dividends from common stock | 187 | 189 | 188 | 191 | 190 | |||||||||||||||

| Interest and dividend income | 103 | 96 | 95 | 48 | 46 | |||||||||||||||

| Other income | — | — | — | 22 | 60 | |||||||||||||||

| Total from investments | 3,127 | 3,163 | 3,232 | 3,331 | 3,396 | |||||||||||||||

| Operating Expenses Before Leverage Costs and Current Taxes | ||||||||||||||||||||

| Advisory fees, net of expense reimbursement | 369 | 387 | 419 | 459 | 498 | |||||||||||||||

| Other operating expenses | 141 | 133 | 126 | 128 | 129 | |||||||||||||||

| 510 | 520 | 545 | 587 | 627 | ||||||||||||||||

| Distributable cash flow before leverage costs and current taxes | 2,617 | 2,643 | 2,687 | 2,744 | 2,769 | |||||||||||||||

| Leverage costs(2) | 266 | 261 | 260 | 257 | 260 | |||||||||||||||

| Current income tax expense | 8 | 9 | 9 | 3 | 9 | |||||||||||||||

| Distributable Cash Flow(3) | $ | 2,343 | $ | 2,373 | $ | 2,418 | $ | 2,484 | $ | 2,500 | ||||||||||

| Distributions paid on common stock | $ | 2,321 | $ | 2,326 | $ | 2,330 | $ | 2,345 | $ | 2,361 | ||||||||||

| Distributions paid on common stock per share | 0.3700 | 0.3700 | 0.3700 | 0.3725 | 0.3750 | |||||||||||||||

| Payout percentage for period(4) | 99.1 | % | 98.0 | % | 96.4 | % | 94.4 | % | 94.4 | % | ||||||||||

| Net realized gain (loss), net of income taxes, for the period | (74 | ) | 8,475 | (810 | ) | 636 | 7,040 | |||||||||||||

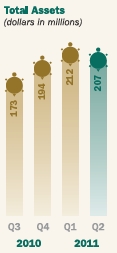

| Total assets, end of period | 158,277 | 173,158 | 193,819 | 211,932 | 207,450 | |||||||||||||||

| Average total assets during period(5) | 163,427 | 171,026 | 185,678 | 202,187 | 211,556 | |||||||||||||||

| Leverage(6) | 21,850 | 24,200 | 25,400 | 24,700 | 26,500 | |||||||||||||||

| Leverage as a percent of total assets | 13.8 | % | 14.0 | % | 13.1 | % | 11.7 | % | 12.8 | % | ||||||||||

| Net unrealized appreciation, net of income taxes, end of period | 38,653 | 40,510 | 56,146 | 67,646 | 58,667 | |||||||||||||||

| Net assets, end of period | 133,412 | 141,622 | 154,289 | 163,963 | 159,100 | |||||||||||||||

| Average net assets during period(7) | 138,900 | 142,460 | 151,466 | 158,748 | 162,099 | |||||||||||||||

| Net asset value per common share | 21.26 | 22.53 | 24.51 | 26.04 | 25.27 | |||||||||||||||

| Market value per common share | 23.65 | 24.32 | 24.44 | 25.50 | 24.41 | |||||||||||||||

| Shares outstanding | 6,274,149 | 6,285,310 | 6,295,750 | 6,295,750 | 6,295,750 | |||||||||||||||

| Selected Operating Ratios(8) | ||||||||||||||||||||

| As a Percent of Average Total Assets | ||||||||||||||||||||

| Total distributions received from investments | 7.59 | % | 7.34 | % | 6.98 | % | 6.68 | % | 6.37 | % | ||||||||||

| Operating expenses before leverage costs and current taxes | 1.24 | % | 1.21 | % | 1.18 | % | 1.18 | % | 1.18 | % | ||||||||||

| Distributable cash flow before leverage costs and current taxes | 6.35 | % | 6.13 | % | 5.80 | % | 5.50 | % | 5.19 | % | ||||||||||

| As a Percent of Average Net Assets | ||||||||||||||||||||

| Distributable cash flow(3) | 6.69 | % | 6.61 | % | 6.40 | % | 6.35 | % | 6.12 | % | ||||||||||

| (1) | Q1 is the period from December through February. Q2 is the period from March through May. Q3 is the period from June through August. Q4 is the period from September through November. | |

| (2) | Leverage costs include interest expense and other recurring leverage expenses. | |

| (3) | “Net investment income (loss), before income taxes” on the Statement of Operations is adjusted as follows to reconcile to Distributable Cash Flow (DCF): increased by the return of capital on MLP distributions, the value of paid-in-kind distributions, distributions included in direct placement discounts, and amortization of debt issuance costs; and decreased by current taxes paid. | |

| (4) | Distributions paid as a percentage of Distributable Cash Flow. | |

| (5) | Computed by averaging month-end values within each period. | |

| (6) | Leverage consists of long-term debt obligations and short-term borrowings. | |

| (7) | Computed by averaging daily values within each period. | |

| (8) | Annualized for periods less than one full year. Operating ratios contained in our Financial Highlights are based on average net assets. |

2 Tortoise North American Energy Corp.

Management’s Discussion (Unaudited) |

Overview

Tortoise North American Energy Corp.’s (“TYN” or the “Company”) investment objective is to seek a high level of total return for our stockholders, with an emphasis on distribution income paid to stockholders. Our investment strategy requires us to invest at least 80 percent of our total assets in equity securities of companies in the energy sector with their primary operations in North America, including energy infrastructure, oil and gas exploitation and energy shipping companies. The equity securities of the energy companies purchased by TYN consist primarily of interests in MLPs. MLPs are publicly traded partnerships whose equity interests are traded in the form of units on public exchanges, such as the NYSE or NASDAQ. We invest primarily in MLPs through public market and private purchases. While we are a registered investment company under the Investment Company Act of 1940, as amended (the “1940 Act”), we are not a “regulated investment company” for federal tax purposes. Our distributions do not typically generate unrelated business taxable income (“UBTI”) and our stock may therefore be suitable for holding by pension funds, IRAs and mutual funds, as well as taxable accounts. Tortoise Capital Advisors, L.L.C. serves as our investment adviser.

Company Update

Market values of our MLP investments declined in May from year-to-date highs earlier in the quarter resulting in an overall decrease in total assets of $4.5 million during the quarter. Distribution increases from our MLP investments were in-line with our expectations while the increase in average total assets during the quarter resulted in increased asset-based expenses. Total leverage as a percent of total assets increased during the quarter as a result of increased leverage and a decline in investment values. Our distributable cash flow (“DCF”) remained strong and we increased our quarterly distribution to $0.375 per share. Subsequent to quarter-end, we refinanced the outstanding senior notes which matured on June 17, 2011 and our bank credit facility. Additional information on these events and results of our operations are discussed in more detail below.

Critical Accounting Policies

The financial statements are based on the selection and application of critical accounting policies, which require management to make significant estimates and assumptions. Critical accounting policies are those that are both important to the presentation of our financial condition and results of operations and require management’s most difficult, complex, or subjective judgments. Our critical accounting policies are those applicable to the valuation of investments, tax matters and certain revenue recognition matters as discussed in Note 2 in the Notes to Financial Statements.

Determining Distributions to Stockholders

Our portfolio generates cash flow from which we pay distributions to stockholders. Our Board of Directors considers our distributable cash flow (“DCF”) in determining distributions to stockholders. Our Board of Directors reviews the distribution rate quarterly, and may adjust the quarterly distribution throughout the year. Our goal is to declare what we believe to be sustainable increases in our regular quarterly distributions with increases safely covered by earned DCF. We have targeted to pay at least 95 percent of DCF on an annualized basis.

Determining DCF

DCF is simply distributions received from investments less expenses. The total distributions received from our investments include the amount received by us as cash distributions from MLPs, paid-in-kind distributions, and dividend and interest payments. The total expenses include current or anticipated operating expenses, leverage costs and current income taxes (excluding taxes generated from realized gains). Realized gains, expected tax benefits and deferred taxes are not included in our DCF.

The Key Financial Data table discloses the calculation of DCF and should be read in conjunction with this discussion. The difference between distributions received from investments in the DCF calculation and total investment income as reported in the Statement of Operations, is reconciled as follows: the Statement of Operations, in conformity with U.S. generally accepted accounting principles (“GAAP”), recognizes distribution income from MLPs and common stock on their ex-dates, whereas the DCF calculation reflects distribution income on their pay dates; GAAP recognizes that a significant portion of the cash distributions received from MLPs are characterized as a return of capital and therefore excluded from investment income, whereas the DCF calculation includes the return of capital; and distributions received from investments in the DCF calculation include the value of dividends paid-in-kind (additional stock or MLP units), whereas such amounts are not included as income for GAAP purposes, and includes distributions related to direct investments when the purchase price is reduced in lieu of receiving cash distributions. The treatment of expenses in the DCF calculation also differs from what is reported in the Statement of Operations. In addition to the total operating expenses, including expense reimbursement, as disclosed in the Statement of Operations, the DCF calculation reflects interest expense, other leverage expenses as well as current taxes paid on net investment income. A reconciliation of Net Investment Loss, before Income Taxes to DCF is included below.

Distributions Received from Investments

Our ability to generate cash is dependent on the ability of our portfolio of investments to generate cash flow from their operations. In order to maintain and grow distributions to our stockholders, we evaluate each holding based upon its contribution to our investment income, our anticipation of its growth rate, and its risk relative to other potential investments.

We concentrate on investments we believe can expect an increasing demand for services from economic and population growth. We seek well-managed businesses with hard assets and stable recurring revenue streams.

Total distributions received from our investments for the 2nd quarter 2011 was approximately $3.4 million, an increase of 2.0 percent as compared to 1st quarter 2011. The increase in distributions received from 1st quarter 2011 primarily reflects distribution increases from our MLP investments and the receipt of a one-time commitment fee of $60,000 related to a direct MLP investment completed during the quarter.

Expenses

We incur two types of expenses: (1) operating expenses, consisting primarily of the advisory fee, and (2) leverage costs. On a percentage basis, operating expenses before leverage costs and current taxes were an annualized 1.18 percent of average total assets for the 2nd quarter 2011 as compared to 1.24 percent for the 2nd quarter 2010 and 1.18 percent for the 1st quarter 2011. The decrease in our operating expense ratio as compared to 2nd quarter 2010 is the result of decreased fixed costs that were partially offset by a reduction in the advisory fee waiver and spread over a larger asset base.

Advisory fees for the 2nd quarter 2011 increased 8.5 percent from 1st quarter 2011 as a result of increased average managed assets for the quarter as discussed above. While the contractual advisory fee of 1.00 percent of average monthly managed assets remains unchanged, the Adviser waived an amount equal to 0.10 percent of average managed assets through December 31, 2010, and has agreed to a waiver of 0.05 percent of average managed assets for the period from January 1, 2011 through December 31, 2011. Other operating expenses for 2nd quarter 2011 were relatively unchanged as compared to 1st quarter 2011.

2011 2nd Quarter Report 3

Management’s Discussion (Unaudited) (Continued) |

Leverage costs consist of the direct interest expense on our Tortoise Notes and short-term credit facility and other expenses, including rating agency fees and commitment fees. Total leverage costs were approximately $260,000 for the 2nd quarter 2011, a slight increase from 1st quarter 2011 due to a slight increase in the utilization of our bank credit facility during the quarter.

The weighted average annual rate of our leverage at May 31, 2011 was 3.80 percent. This rate includes balances on our bank credit facility which accrue interest at a variable rate equal to one-month LIBOR plus 1.25 percent. Our weighted average rate may vary in future periods as a result of changes in LIBOR, the utilization of our credit facility and as our leverage matures or is redeemed. Additional information on our leverage is disclosed below in Liquidity and Capital Resources and in our Notes to Financial Statements.

Distributable Cash Flow

For 2nd quarter 2011, our DCF was approximately $2.5 million, an increase of 0.6 percent as compared to 1st quarter 2011. The change is the net result of increased distributions and expenses as outlined above. We declared a distribution of $2.4 million, or $0.375 per share, on May 9, 2011. This is an increase of 1.4 percent as compared to the per share distribution paid for 2nd quarter 2010 and a 0.7 percent increase compared to 1st quarter 2011.

Our dividend payout ratio as a percentage of DCF decreased from 99.1 percent for 2nd quarter 2010 to 94.4 percent for 2nd quarter 2011. A payout of less than 100 percent of DCF provides cushion for on-going management of the portfolio, changes in leverage costs and other expenses. An on-going payout ratio in excess of 100 percent will, over time, erode the earning power of a portfolio and may lead to lower distributions or portfolio managers taking on more risk than they otherwise would.

Net investment loss before income taxes on the Statement of Operations is adjusted as follows to reconcile to DCF for 2011 YTD and the 2nd quarter 2011 (in thousands):

| 2011 YTD | 2nd Qtr 2011 | |||||||

| Net Investment Loss, before Income Taxes | $ | (1,060 | ) | $ | (875 | ) | ||

| Adjustments to reconcile to DCF: | ||||||||

| Dividends paid in stock | 768 | 364 | ||||||

| Return of capital on distributions | 5,262 | 3,015 | ||||||

| Distribution included in direct placement discount | 16 | — | ||||||

| Amortization of debt issuance costs | 10 | 5 | ||||||

| Current income tax expenses | (12 | ) | (9 | ) | ||||

| DCF | $ | 4,984 | $ | 2,500 | ||||

We had total assets of $207 million at quarter-end. Our total assets reflect the value of our investments, which are itemized in the Schedule of Investments. It also reflects cash, interest and receivables and any expenses that may have been prepaid. During 2nd quarter 2011, total assets decreased by approximately $4.5 million. This change was primarily the result of a $6.1 million decrease in the value of our investments as reflected by the change in realized and unrealized gains on investments (excluding return of capital on distributions), net sales of portfolio securities during the quarter and an increase in cash available to pay down short-term borrowings.

Total leverage outstanding at May 31, 2011 was $26.5 million, an increase of $1.8 million as compared to February 28, 2011. Outstanding leverage is comprised of $15 million in senior notes and $11.5 million outstanding under the credit facility. Total leverage represented 12.8 percent of total assets, an increase from 11.7 percent of total assets at February 28, 2011 and a decrease from 13.8 percent of total assets at May 31, 2010. Subsequent to quarter-end, we refinanced the $15 million fixed-rate senior notes which matured on June 17, 2011 and the balance on our bank credit facility by entering into a margin loan facility. The new secured facility allows us to borrow up to $40 million and has a 270-day rolling term. Interest accrues on the margin facility at a rate equal to 1-month LIBOR plus 0.85 percent and unused balances are subject to a fee of 0.25 percent. We expect to enter into interest rate swaps in an attempt to reduce a portion of the interest rate risk from our leveraged capital structure. Our leverage as a percent of total assets remains below our long-term target level of 20 percent of total assets. This allows the opportunity to add leverage when compelling investment opportunities arise. Temporary increases to up to 25 percent of our total assets may be permitted, provided that such leverage is consistent with the limits set forth in the 1940 Act, and that such leverage is expected to be reduced over time in an orderly fashion to reach our long-term target. Our leverage ratio is impacted by increases or decreases in MLP values, issuance of equity and/or the sale of securities where proceeds are used to reduce leverage.

We have used leverage to acquire securities consistent with our investment philosophy. The terms of our leverage are governed by regulatory and contractual asset coverage requirements that arise from the use of leverage. Additional information on our leverage and asset coverage requirements is discussed in Note 9 in the Notes to Financial Statements. Our coverage ratio is updated each week on our Web site at www.tortoiseadvisors.com.

Taxation of our Distributions and Income Taxes

We invest in partnerships which generally have larger distributions of cash than the accounting income which they generate. Accordingly, the distributions include a return of capital component for accounting and tax purposes. Distributions declared and paid by us in a year generally differ from taxable income for that year, as such distributions may include the distribution of current year taxable income or return of capital.

The taxability of the distribution you receive depends on whether we have annual earnings and profits. If so, those earnings and profits are first allocated to preferred shares (if any) and then to the common shares.

In the event we have earnings and profits allocated to our common shares, all or a portion of our distribution will be taxable at the 15 percent Qualified Dividend Income (“QDI”) rate, assuming various holding requirements are met by the stockholder. The 15 percent QDI rate is currently effective through 2012. The portion of our distribution that is taxable may vary for either of two reasons: first, the characterization of the distributions we receive from MLPs could change annually based upon the K-1 allocations and result in less return of capital and more in the form of income. Second, we could sell an MLP investment and realize a gain or loss at any time. It is for these reasons that we inform you of the tax treatment after the close of each year as the ultimate characterization of our distributions is undeterminable until the year is over.

For tax purposes, distributions to common stockholders for the fiscal year ended 2010 were 30 percent qualified dividend income and 70 percent return of capital. A holder of our common stock would reduce their cost basis for income tax purposes by 70 percent of the total distributions they received in 2010. This information is reported to stockholders on Form 1099-DIV and is available on our Web site at www.tortoiseadvisors.com. For book purposes, the source of distributions to common stockholders for the fiscal year ended 2010 was 100 percent return of capital. We currently estimate that 75 to 100 percent of 2011 distributions will be characterized as qualified dividend income for tax purposes, with the remaining percentage characterized as return of capital. Final determination will be made after the completion of our fiscal year.

The unrealized gain or loss we have in the portfolio is reflected in the Statement of Assets and Liabilities. At May 31, 2011, our investments are valued at $205 million, with an adjusted cost of $131.1 million. The $73.9 million difference reflects unrealized appreciation that would be realized for financial statement purposes if those investments were sold at those values. The Statement of Assets and Liabilities also reflects either a net deferred tax liability or net deferred tax asset depending primarily upon unrealized gains (losses) on investments, realized gains (losses) on investments, capital loss carryforwards and net operating losses. At May 31, 2011, the balance sheet reflects a net deferred tax liability of approximately $18.7 million or $2.98 per share. Accordingly, our net asset value per share represents the amount which would be available for distribution to stockholders after payment of taxes. Details of our deferred taxes are disclosed in Note 5 in our Notes to Financial Statements.

4 Tortoise North American Energy Corp.

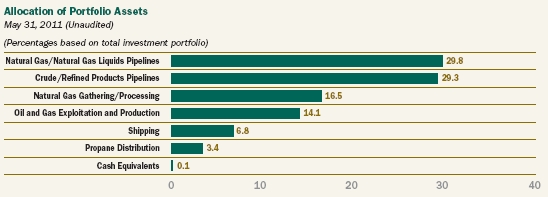

Schedule of Investments May 31, 2011 |

| (Unaudited) |

| Shares | Fair Value | |||||

| Master Limited Partnerships and | ||||||

| Related Companies — 121.1%(1) | ||||||

| Crude/Refined Products Pipelines — 37.8%(1) | ||||||

| United States — 37.8%(1) | ||||||

| Buckeye Partners, L.P. | 150,200 | $ | 9,530,190 | |||

| Enbridge Energy Management, L.L.C.(2) | 175,001 | 5,428,533 | ||||

| Enbridge Energy Partners, L.P. | 159,600 | 4,901,316 | ||||

| Holly Energy Partners, L.P. | 73,300 | 4,033,699 | ||||

| Kinder Morgan Management, LLC(2) | 181,318 | 11,834,649 | ||||

| Magellan Midstream Partners, L.P. | 142,400 | 8,410,144 | ||||

| NuStar Energy L.P. | 98,000 | 6,218,100 | ||||

| Plains All American Pipeline, L.P. | 107,600 | 6,697,024 | ||||

| Sunoco Logistics Partners L.P. | 33,000 | 2,791,800 | ||||

| Tesoro Logistics LP | 13,168 | 327,093 | ||||

| 60,172,548 | ||||||

| Natural Gas/Natural Gas Liquids Pipelines — 38.5%(1) | ||||||

| United States — 38.5%(1) | ||||||

| Boardwalk Pipeline Partners, LP | 297,500 | 8,657,250 | ||||

| Duncan Energy Partners L.P. | 11,200 | 465,024 | ||||

| El Paso Pipeline Partners, L.P. | 174,740 | 6,005,814 | ||||

| Energy Transfer Equity, L.P. | 140,100 | 5,903,814 | ||||

| Energy Transfer Partners, L.P. | 205,200 | 9,749,052 | ||||

| Enterprise Products Partners L.P. | 296,100 | 12,329,604 | ||||

| Niska Gas Storage Partners LLC | 67,100 | 1,302,411 | ||||

| ONEOK Partners, L.P. | 65,500 | 5,458,770 | ||||

| PAA Natural Gas Storage, L.P. | 38,071 | 861,166 | ||||

| PAA Natural Gas Storage, L.P.(3) | 46,718 | 1,010,510 | ||||

| Spectra Energy Partners, LP | 93,700 | 2,998,400 | ||||

| TC PipeLines, LP | 74,400 | 3,434,304 | ||||

| Williams Partners L.P. | 57,061 | 3,019,668 | ||||

| 61,195,787 | ||||||

| Natural Gas Gathering/Processing — 21.2%(1) | ||||||

| United States — 21.2%(1) | ||||||

| Chesapeake Midstream Partners, L.P. | 47,604 | 1,249,129 | ||||

| Copano Energy, L.L.C. | 210,100 | 7,050,956 | ||||

| Crestwood Midstream Partners LP(2)(3) | 82,800 | 2,019,492 | ||||

| DCP Midstream Partners, LP | 51,500 | 2,087,295 | ||||

| MarkWest Energy Partners, L.P. | 136,100 | 6,467,472 | ||||

| Regency Energy Partners LP | 144,700 | 3,644,993 | ||||

| Regency Energy Partners LP(3) | 250,000 | 6,010,000 | ||||

| Targa Resources Partners LP | 152,200 | 5,260,032 | ||||

| 33,789,369 | ||||||

| Oil and Gas Exploitation and Production — 18.1%(1) | ||||||

| United States — 18.1%(1) | ||||||

| Encore Energy Partners LP | 132,100 | 2,936,583 | ||||

| EV Energy Partners, L.P. | 124,700 | 6,902,145 | ||||

| Legacy Reserves, LP | 120,600 | 3,844,728 | ||||

| Linn Energy, LLC | 270,300 | 10,503,858 | ||||

| Pioneer Southwest Energy Partners L.P. | 150,900 | 4,628,103 | ||||

| 28,815,417 | ||||||

| Propane Distribution — 4.3%(1) | ||||||

| United States — 4.3%(1) | ||||||

| Inergy, L.P. | 185,700 | 6,887,613 | ||||

| Shipping — 1.2%(1) | ||||||

| Republic of the Marshall Islands — 1.2%(1) | ||||||

| Teekay LNG Partners L.P. | 53,500 | 1,907,810 | ||||

| Total Master Limited Partnerships and | ||||||

| Related Companies (Cost $121,999,192) | 192,768,544 | |||||

| Common Stock — 7.6%(1) | ||||||

| Shipping — 7.6%(1) | ||||||

| Republic of the Marshall Islands — 7.6%(1) | ||||||

| Golar LNG Partners LP | 91,000 | 2,518,880 | ||||

| Navios Maritime Partners L.P. | 238,000 | 4,545,800 | ||||

| Teekay Offshore Partners L.P. | 174,650 | 5,073,583 | ||||

| Total Common Stock (Cost $8,990,100) | 12,138,263 | |||||

| Short-Term Investment — 0.1%(1) | ||||||

| United States Investment Company — 0.1%(1) | ||||||

| Fidelity Institutional Money Market Portfolio — | ||||||

| Class I, 0.16%(4) (Cost $112,162) | 112,162 | 112,162 | ||||

| Total Investments — 128.8%(1) | ||||||

| (Cost $131,101,454) | 205,018,969 | |||||

| Other Assets and Liabilities — (19.4%)(1) | (30,918,929 | ) | ||||

| Long-Term Debt Obligations — (9.4%)(1) | (15,000,000 | ) | ||||

| Total Net Assets Applicable to | ||||||

| Common Stockholders — 100.0%(1) | $ | 159,100,040 | ||||

| (1) | Calculated as a percentage of net assets applicable to common stockholders. | |

| (2) | Security distributions are paid-in-kind. | |

| (3) | Restricted securities have been fair valued in accordance with procedures approved by the Board of Directors and have a total fair value of $9,040,002, which represents 5.7% of net assets. See Note 7 to the financial statements for further disclosure. | |

| (4) | Rate reported is the current yield as of May 31, 2011. |

See accompanying Notes to Financial Statements.

2011 2nd Quarter Report 5

Statement of Assets & Liabilities May 31, 2011 |

| (Unaudited) |

| Assets | ||||

| Investments at fair value (cost $131,101,454) | $ | 205,018,969 | ||

| Cash | 2,284,528 | |||

| Receivable for Adviser expense reimbursement | 17,424 | |||

| Prepaid expenses and other assets | 129,008 | |||

| Total assets | 207,449,929 | |||

| Liabilities | ||||

| Payable to Adviser | 348,472 | |||

| Distributions payable to common stockholders | 2,360,906 | |||

| Accrued expenses and other liabilities | 385,972 | |||

| Current tax liability | 16,368 | |||

| Deferred tax liability | 18,738,171 | |||

| Short-term borrowings | 11,500,000 | |||

| Long-term debt obligations | 15,000,000 | |||

| Total liabilities | 48,349,889 | |||

| Net assets applicable to common stockholders | $ | 159,100,040 | ||

| Net Assets Applicable to Common Stockholders Consist of: | ||||

| Capital stock, $0.001 par value; 6,295,750 shares issued and | ||||

| outstanding (100,000,000 shares authorized) | $ | 6,296 | ||

| Additional paid-in capital | 111,562,444 | |||

| Accumulated net investment loss, net of income taxes | (514,007 | ) | ||

| Accumulated net realized loss, net of income taxes | (10,621,778 | ) | ||

| Net unrealized appreciation of investments, net of income taxes | 58,667,085 | |||

| Net assets applicable to common stockholders | $ | 159,100,040 | ||

| Net Asset Value per common share outstanding | ||||

| (net assets applicable to common stock, | ||||

| divided by common shares outstanding) | $ | 25.27 | ||

| Statement of Operations Period from December 1, 2010 through May 31, 2011 |

| (Unaudited) |

| Investment Income | ||||

| Distributions from master limited partnerships | $ | 5,385,903 | ||

| Less return of capital on distributions | (5,262,148 | ) | ||

| Net distributions from master limited partnerships | 123,755 | |||

| Dividend income | 380,594 | |||

| Interest income | 93,518 | |||

| Dividends from money market mutual funds | 52 | |||

| Other income | 82,163 | |||

| Total Investment Income | 680,082 | |||

| Operating Expenses | ||||

| Advisory fees | 1,015,646 | |||

| Professional fees | 96,065 | |||

| Administrator fees | 40,628 | |||

| Directors’ fees | 33,957 | |||

| Stockholder communication expenses | 32,816 | |||

| Fund accounting fees | 19,047 | |||

| Registration fees | 12,456 | |||

| Stock transfer agent fees | 5,833 | |||

| Custodian fees and expenses | 5,495 | |||

| Other operating expenses | 10,668 | |||

| Total Operating Expenses | 1,272,611 | |||

| Leverage Expenses | ||||

| Interest expense | 502,604 | |||

| Amortization of debt issuance costs | 9,664 | |||

| Other leverage expenses | 14,027 | |||

| Total Leverage Expenses | 526,295 | |||

| Total Expenses | 1,798,906 | |||

| Less expense reimbursement by Adviser | (58,975 | ) | ||

| Net Expenses | 1,739,931 | |||

| Net Investment Loss, before Income Taxes | (1,059,849 | ) | ||

| Current tax expense | (17,479 | ) | ||

| Deferred tax benefit | 397,319 | |||

| Income tax benefit, net | 379,840 | |||

| Net Investment Loss | (680,009 | ) | ||

| Realized and Unrealized Gain on Investments | ||||

| Net realized gain on investments, before income taxes | 12,161,134 | |||

| Deferred tax expense | (4,485,026 | ) | ||

| Net realized gain on investments | 7,676,108 | |||

| Net unrealized appreciation of investments, before income taxes | 3,993,366 | |||

| Deferred tax expense | (1,472,754 | ) | ||

| Net unrealized appreciation of investments | 2,520,612 | |||

| Net Realized and Unrealized Gain on Investments | 10,196,720 | |||

| Net Increase in Net Assets Applicable to Common Stockholders | ||||

| Resulting from Operations | $ | 9,516,711 | ||

See accompanying Notes to Financial Statements.

6 Tortoise North American Energy Corp.

Statement of Changes in Net Assets |

| Period from | ||||||||

| December 1, 2010 | ||||||||

| through | Year Ended | |||||||

| May 31, 2011 | November 30, 2010 | |||||||

| (Unaudited) | ||||||||

| Operations | ||||||||

| Net investment loss | $ | (680,009 | ) | $ | (540,554 | ) | ||

| Net realized gain on investments | 7,676,108 | 3,023,685 | ||||||

| Net unrealized appreciation of investments | 2,520,612 | 33,743,451 | ||||||

Net increase in net assets applicable to common stockholders resulting from operations | 9,516,711 | 36,226,582 | ||||||

| Distributions to Common Stockholders | ||||||||

| Net investment income | — | — | ||||||

| Return of capital | (4,706,073 | ) | (9,293,612 | ) | ||||

| Total distributions to common stockholders | (4,706,073 | ) | (9,293,612 | ) | ||||

| Capital Stock Transactions | ||||||||

Issuance of 33,090 common shares from reinvestment of distributions to stockholders | — | 747,127 | ||||||

Net increase in net assets applicable to common stockholders from capital stock transactions | — | 747,127 | ||||||

| Total increase in net assets applicable to common stockholders | 4,810,638 | 27,680,097 | ||||||

| Net Assets | ||||||||

| Beginning of period | 154,289,402 | 126,609,305 | ||||||

| End of period | $ | 159,100,040 | $ | 154,289,402 | ||||

Undistributed (accumulated) net investment income (loss), net of income taxes, end of period | $ | (514,007 | ) | $ | 166,002 | |||

See accompanying Notes to Financial Statements.

2011 2nd Quarter Report 7

Statement of Cash Flows Period from December 1, 2010 through May 31, 2011 |

| (Unaudited) |

| Cash Flows from Operating Activities | ||||

| Distributions received from master limited partnerships | $ | 5,385,903 | ||

| Interest and dividend income received | 483,118 | |||

| Purchases of long-term investments | (29,847,912 | ) | ||

| Proceeds from sales of long-term investments | 29,244,363 | |||

| Interest received on securities sold | 153,653 | |||

| Purchases of short-term investments, net | (13,976 | ) | ||

| Other income received | 82,097 | |||

| Interest expense paid | (499,487 | ) | ||

| Income taxes paid | (16,110 | ) | ||

| Operating expenses paid | (1,199,000 | ) | ||

| Net cash provided by operating activities | 3,772,649 | |||

| Cash Flows from Financing Activities | ||||

| Advances from revolving line of credit | 20,450,000 | |||

| Repayments on revolving line of credit | (19,350,000 | ) | ||

| Distributions paid to common stockholders | (2,588,121 | ) | ||

| Net cash used in financing activities | (1,488,121 | ) | ||

| Net change in cash | 2,284,528 | |||

| Cash — beginning of period | — | |||

| Cash — end of period | $ | 2,284,528 | ||

| Reconciliation of net increase in net assets applicable to | ||||

| common stockholders resulting from operations to net cash | ||||

| provided by operating activities | ||||

| Net increase in net assets applicable to common | ||||

| stockholders resulting from operations | $ | 9,516,711 | ||

| Adjustments to reconcile net increase in net assets | ||||

| applicable to common stockholders resulting from | ||||

| operations to net cash provided by operating activities: | ||||

| Purchases of long-term investments | (29,847,912 | ) | ||

Return of capital on distributions received | 5,262,148 | |||

| Purchases of short-term investments, net | (13,976 | ) | ||

| Proceeds from sales of long-term investments | 29,242,506 | |||

| Deferred tax expense | 5,560,461 | |||

| Net unrealized appreciation of investments | (3,993,366 | ) | ||

| Net realized gain on investments | (12,161,200 | ) | ||

| Amortization of market premium, net | 11,045 | |||

| Amortization of debt issuance costs | 9,664 | |||

| Changes in operating assets and liabilities: | ||||

| Decrease in interest and dividend receivable | 151,596 | |||

| Decrease in receivable for investments sold | 1,857 | |||

| Increase in prepaid expenses and other assets | (23,017 | ) | ||

| Increase in current tax liability | 1,368 | |||

| Increase in payable to Adviser, net of | ||||

| expense reimbursement | 43,301 | |||

| Increase in accrued expenses and other liabilities | 11,463 | |||

| Total adjustments | (5,744,062 | ) | ||

| Net cash provided by operating activities | $ | 3,772,649 | ||

See accompanying Notes to Financial Statements.

8 Tortoise North American Energy Corp.

Financial Highlights |

| Period from | ||||||||||||||||||||||||

| December 1, 2010 | Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | |||||||||||||||||||

| through | November 30, | November 30, | November 30, | November 30, | November 30, | |||||||||||||||||||

| May 31, 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||||||||

| (Unaudited) | ||||||||||||||||||||||||

| Per Common Share Data(1) | ||||||||||||||||||||||||

| Net Asset Value, beginning of period | $ | 24.51 | $ | 20.22 | $ | 10.78 | $ | 27.25 | $ | 23.70 | $ | 23.95 | ||||||||||||

| Income (Loss) from Investment Operations | ||||||||||||||||||||||||

| Net investment income (loss)(2) | (0.11 | ) | (0.09 | ) | 0.25 | 0.43 | 0.72 | 0.61 | ||||||||||||||||

| Net realized and unrealized gain (loss) on investments(2) | 1.62 | 5.86 | 10.67 | (15.14 | ) | 4.47 | 0.55 | |||||||||||||||||

| Total income (loss) from investment operations | 1.51 | 5.77 | 10.92 | (14.71 | ) | 5.19 | 1.16 | |||||||||||||||||

| Distributions to Preferred Stockholders | ||||||||||||||||||||||||

| Net investment income | — | — | — | — | (0.12 | ) | (0.06 | ) | ||||||||||||||||

| Net realized gain | — | — | — | — | (0.07 | ) | (0.01 | ) | ||||||||||||||||

| Return of capital | — | — | — | (0.17 | ) | — | — | |||||||||||||||||

| Total distributions to preferred stockholders | — | — | — | (0.17 | ) | (0.19 | ) | (0.07 | ) | |||||||||||||||

| Distributions to Common Stockholders | ||||||||||||||||||||||||

| Net investment income | — | — | — | — | (0.90 | ) | (0.69 | ) | ||||||||||||||||

| Net realized gain | — | — | — | (0.10 | ) | (0.55 | ) | (0.12 | ) | |||||||||||||||

| Return of capital | (0.75 | ) | (1.48 | ) | (1.48 | ) | (1.49 | ) | — | (0.46 | ) | |||||||||||||

| Total distributions to common stockholders | (0.75 | ) | (1.48 | ) | (1.48 | ) | (1.59 | ) | (1.45 | ) | (1.27 | ) | ||||||||||||

| Underwriting discounts and offering costs on issuance of common | ||||||||||||||||||||||||

| and preferred stock(3) | — | — | — | — | — | (0.07 | ) | |||||||||||||||||

| Net Asset Value, end of period | $ | 25.27 | $ | 24.51 | $ | 20.22 | $ | 10.78 | $ | 27.25 | $ | 23.70 | ||||||||||||

| Per common share market value, end of period | $ | 24.41 | $ | 24.44 | $ | 19.49 | $ | 9.25 | $ | 23.10 | $ | 22.38 | ||||||||||||

| Total Investment Return Based on Market Value(4) | 2.94 | % | 33.62 | % | 131.66 | % | (55.98 | )% | 9.28 | % | (5.39 | )% | ||||||||||||

| Supplemental Data and Ratios | ||||||||||||||||||||||||

| Net assets applicable to common stockholders, end of period (000’s) | $ | 159,100 | $ | 154,289 | $ | 126,609 | $ | 49,716 | $ | 125,702 | $ | 109,326 | ||||||||||||

| Average net assets (000’s) | $ | 160,442 | $ | 141,986 | $ | 80,041 | $ | 113,045 | $ | 125,379 | $ | 114,338 | ||||||||||||

| Ratio of Expenses to Average Net Assets(5) | ||||||||||||||||||||||||

| Advisory fees | 1.27 | % | 1.19 | % | 1.13 | % | 1.50 | % | 1.45 | % | 1.32 | % | ||||||||||||

| Other expenses | 0.32 | 0.38 | 1.01 | 0.48 | 0.40 | 0.59 | ||||||||||||||||||

| Expense reimbursement | (0.07 | ) | (0.12 | ) | (0.12 | ) | (0.23 | ) | (0.29 | ) | (0.32 | ) | ||||||||||||

| Subtotal | 1.52 | 1.45 | 2.02 | 1.75 | 1.56 | 1.59 | ||||||||||||||||||

| Leverage expenses (6) | 0.66 | 0.75 | 1.17 | 3.71 | 2.01 | 1.49 | ||||||||||||||||||

| Income tax expense (benefit)(7) | 6.97 | 13.10 | (4.70 | ) | 0.06 | 0.02 | 0.01 | |||||||||||||||||

| Total expenses | 9.15 | % | 15.30 | % | (1.51 | )% | 5.52 | % | 3.59 | % | 3.09 | % | ||||||||||||

See accompanying Notes to Financial Statements.

2011 2nd Quarter Report 9

Financial Highlights (Continued) |

| Period from | ||||||||||||||||||||||||

| December 1, 2010 | Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | |||||||||||||||||||

| through | November 30, | November 30, | November 30, | November 30, | November 30, | |||||||||||||||||||

| May 31, 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||||||||

| (Unaudited) | ||||||||||||||||||||||||

| Ratio of net investment income (loss) to average net assets | ||||||||||||||||||||||||

| before expense reimbursement(5)(6) | (0.92 | )% | (0.50 | )% | 1.82 | % | 1.51 | % | 2.37 | % | 2.14 | % | ||||||||||||

| Ratio of net investment income (loss) to average net assets | ||||||||||||||||||||||||

| after expense reimbursement(5)(6) | (0.85 | )% | (0.38 | )% | 1.94 | % | 1.74 | % | 2.66 | % | 2.46 | % | ||||||||||||

| Portfolio turnover rate(5) | 28.62 | % | 27.89 | % | 41.90 | % | 36.69 | % | 16.06 | % | 12.01 | % | ||||||||||||

| Short-term borrowings, end of period (000’s) | $ | 11,500 | $ | 10,400 | $ | 5,900 | — | $ | 9,600 | $ | 7,000 | |||||||||||||

| Long-term debt obligations, end of period (000’s) | $ | 15,000 | $ | 15,000 | $ | 15,000 | $ | 15,000 | $ | 40,000 | $ | 40,000 | ||||||||||||

| Preferred stock, end of period (000’s) | — | — | — | $ | 10,000 | $ | 15,000 | $ | 15,000 | |||||||||||||||

| Per common share amount of long-term debt obligations outstanding, | ||||||||||||||||||||||||

| end of period | $ | 2.38 | $ | 2.38 | $ | 2.40 | $ | 3.25 | $ | 8.67 | $ | 8.67 | ||||||||||||

| Per common share amount of net assets, excluding long-term debt obligations, | ||||||||||||||||||||||||

| end of period | $ | 27.65 | $ | 26.89 | $ | 22.61 | $ | 14.03 | $ | 35.92 | $ | 32.37 | ||||||||||||

| Asset coverage, per $1,000 of principal amount of long-term debt obligations | ||||||||||||||||||||||||

| and short-term borrowings(8) | $ | 7,004 | $ | 7,074 | $ | 7,058 | $ | 4,981 | $ | 3,837 | $ | 3,645 | ||||||||||||

| Asset coverage ratio of long-term debt obligations and short-term borrowings(8) | 700 | % | 707 | % | 706 | % | 498 | % | 384 | % | 365 | % | ||||||||||||

| Asset coverage, per $25,000 liquidation value per share of preferred stock(9) | — | — | — | $ | 74,716 | $ | 73,646 | $ | 69,083 | |||||||||||||||

| Asset coverage ratio of preferred stock(9) | — | — | — | 299 | % | 295 | % | 276 | % | |||||||||||||||

| (1) | Information presented relates to a share of common stock outstanding for the entire period. | |

| (2) | The per common share data for the years ended November 30, 2010, 2009, 2008, 2007 and 2006 do not reflect the change in estimate of investment income and return of capital, for the respective period. See Note 2F to the financial statements for further disclosure. | |

| (3) | Represents the issuance of preferred stock for the year ended November 30, 2006. | |

| (4) | Not annualized for periods less than one full year. Total investment return is calculated assuming a purchase of common stock at the beginning of the period and a sale at the closing price on the last day of the period reported (excluding broker commissions). The calculation also assumes reinvestment of distributions at actual prices pursuant to the Company’s dividend reinvestment plan. | |

| (5) | Annualized for periods less than one full year. | |

| (6) | The expense ratios and net investment income (loss) ratios do not reflect the effect of distributions to preferred stockholders. |

| (7) | The Company accrued $17,479, $39,097, $(28,837), $68,509, $22,447 and $13,225 for the period from December 1, 2010 through May 31, 2011 and the years ended November 30, 2010, 2009, 2008, 2007 and 2006, respectively, for current foreign and excise tax (benefit) expense. For the period from December 1, 2010 through May 31, 2011 and the year ended November 30, 2010, the Company accrued $5,560,461 and $18,559,864, respectively, in net deferred income tax expense. For the year ended November 30, 2009, the Company accrued $3,732,366 in net deferred income tax benefit, which included $5,488,509 of deferred income tax benefit for the timing differences at December 1, 2008 when the Company converted to a taxable corporation. | |

| (8) | Represents value of total assets less all liabilities and indebtedness not represented by long-term debt obligations, short-term borrowings and preferred stock at the end of the period divided by long-term debt obligations and short-term borrowings outstanding at the end of the period. | |

| (9) | Represents value of total assets less all liabilities and indebtedness not represented by long-term debt obligations, short-term borrowings and preferred stock at the end of the period divided by long-term debt obligations, short-term borrowings and preferred stock outstanding at the end of the period. |

See accompanying Notes to Financial Statements.

10 Tortoise North American Energy Corp.

Notes to Financial Statements (Unaudited) May 31, 2011 |

1. Organization

Tortoise North American Energy Corporation (the “Company”) was organized as a Maryland corporation on January 13, 2005, and is a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Company’s investment objective is to seek a high level of total return with an emphasis on distribution income paid to stockholders. The Company seeks to provide its stockholders with a vehicle to invest in a portfolio consisting primarily of publicly traded U.S. master limited partnerships (“MLPs”), including oil and gas exploitation, energy infrastructure and energy shipping companies. The Company commenced operations on October 31, 2005. The Company’s stock is listed on the New York Stock Exchange under the symbol “TYN.”

2. Significant Accounting Policies

A. Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amount of assets and liabilities, recognition of distribution income and disclosure of contingent assets and liabilities at the date of the financial statements. Actual results could differ from those estimates.

B. Investment Valuation

The Company primarily owns securities that are listed on a securities exchange or over-the-counter market. The Company values those securities at their last sale price on that exchange or over-the-counter market on the valuation date. If the security is listed on more than one exchange, the Company uses the price from the exchange that it considers to be the principal exchange on which the security is traded. Securities listed on the NASDAQ will be valued at the NASDAQ Official Closing Price, which may not necessarily represent the last sale price. If there has been no sale on such exchange or over-the-counter market on such day, the security will be valued at the mean between the last bid price and last ask price on such day.

The Company may invest up to 50 percent of its total assets in restricted securities. Restricted securities are subject to statutory and contractual restrictions on their public resale, which may make it more difficult to obtain a valuation and may limit the Company’s ability to dispose of them. Investments in restricted securities and other securities for which market quotations are not readily available will be valued in good faith by using fair value procedures approved by the Board of Directors. Such fair value procedures consider factors such as discounts to publicly traded issues, time until conversion date, securities with similar yields, quality, type of issue, coupon, duration and rating. If events occur that affect the value of the Company’s portfolio securities before the net asset value has been calculated (a “significant event”), the portfolio securities so affected will generally be priced using fair value procedures.

An equity security of a publicly traded company acquired in a direct placement transaction may be subject to restrictions on resale that can affect the security’s liquidity and fair value. Such securities that are convertible or otherwise will become freely tradable will be valued based on the market value of the freely tradable security less an applicable discount. Generally, the discount will initially be equal to the discount at which the Company purchased the securities. To the extent that such securities are convertible or otherwise become freely tradable within a time frame that may be reasonably determined, an amortization schedule may be used to determine the discount.

The Company generally values debt securities at prices based on market quotations for such securities, except those securities purchased with 60 days or less to maturity are valued on the basis of amortized cost, which approximates market value.

C. Foreign Currency Translation

For foreign currency, investments in foreign securities, and other assets and liabilities denominated in a foreign currency, the Company translates these amounts into U.S. dollars on the following basis:

| (1) | market value of investment securities, assets and liabilities at the current rate of exchange on the valuation date and | |

| (2) | purchases and sales of investment securities, income and expenses at the relevant rates of exchange on the respective dates of such transactions. | |

The Company does not isolate that portion of gains and losses on investments that is due to changes in the foreign exchange rates from that which is due to changes in market prices of equity securities.

D. Forward Foreign Currency Contracts

The Company may enter into forward foreign currency contracts as economic hedges related to specific transactions. All commitments are “marked-to-market” daily at the applicable foreign exchange rate, and any resulting unrealized gains or losses are recorded in the Statement of Operations. The Company recognizes realized gains or losses at the time forward contracts are extinguished.

E. Foreign Withholding Taxes

The Company may be subject to taxes imposed by countries in which it invests with respect to its investment in issuers existing or operating in such countries. Such taxes are generally based on income earned. The Company accrues such taxes when the related income is earned.

F. Security Transactions and Investment Income

Security transactions are accounted for on the date the securities are purchased or sold (trade date). Realized gains and losses are reported on an identified cost basis. Interest income is recognized on the accrual basis, including amortization of premiums and accretion of discounts. Dividend and distribution income is recorded on the ex-dividend date. Distributions from MLPs are generally comprised of income and return of capital from the MLPs. The Company allocates distributions between investment income and return of capital based on estimates made at the time such distributions are received. Such estimates are based on information provided by each MLP and other industry sources. These estimates may subsequently be revised based on actual allocations received from MLPs after their tax reporting periods are concluded, as the actual character of these distributions is not known until after the fiscal year end of the Company.

For the period from December 1, 2009 through November 30, 2010, the Company estimated the allocation of investment income and return of capital for the distributions received from MLPs within the Statement of Operations. For this period, the Company had estimated approximately 16 percent of total distributions as investment income and approximately 84 percent as return of capital.

2011 2nd Quarter Report 11

Notes to Financial Statements (Unaudited) (Continued) |

Subsequent to November 30, 2010, the Company reallocated the amount of investment income and return of capital it recognized for the period from December 1, 2009 through November 30, 2010 based on the 2010 tax reporting information received from the individual MLPs. This reclassification amounted to a decrease in pre-tax net investment income of approximately $534,000 or $0.085 per share ($337,000 or $0.053 per share, net of deferred tax benefit); an increase in unrealized appreciation of investments of approximately $512,000 or $0.081 per share ($323,000 or $0.051 per share, net of deferred tax expense) and an increase in realized gains of approximately $22,000 or $0.004 per share ($14,000 or $0.002 per share, net of deferred tax expense) for the period from December 1, 2010 through May 31, 2011.

Subsequent to the period ended February 28, 2011, the Company reallocated the amount of investment income and return of capital recognized in the current fiscal year based on its revised 2011 estimates, after considering the final allocations for 2010. This reclassification amounted to a decrease in pre-tax net investment income of approximately $134,000 or $0.021 per share ($85,000 or $0.013 per share, net of deferred tax benefit); an increase in unrealized appreciation of investments of approximately $263,000 or $0.042 per share ($166,000 or $0.026 per share, net of deferred tax expense) and a decrease in realized gains of approximately $129,000 or $0.021 per share ($81,000 or $0.013 per share, net of deferred tax expense).

G. Distributions to Stockholders

Distributions to common stockholders are recorded on the ex-dividend date. The Company may not declare or pay distributions to its common stockholders if it does not meet asset coverage ratios required under the 1940 Act or the rating agency guidelines for its debt and preferred stock (if any) following such distribution. The character of distributions to stockholders made during the year may differ from their ultimate characterization for federal income tax purposes. Distributions paid to stockholders in excess of investment company taxable income and net realized capital gains will be treated as a return of capital to the stockholders. For book purposes, the source of the Company’s distributions to common stockholders for the year ended November 30, 2010 and the period ended May 31, 2011 was 100 percent return of capital. For tax purposes, the Company’s distributions for the year ended November 30, 2010 were approximately 30 percent qualified dividend income and 70 percent return of capital. The tax character of distributions paid to common stockholders in the current year will be determined subsequent to November 30, 2011.

H. Federal Income Taxation

From the Company’s inception through November 30, 2008, the Company qualified as a regulated investment company (“RIC”) under the U.S. Internal Revenue Code of 1986, as amended (the “Code”). Effective December 1, 2008, the Company is treated as a taxable corporation for federal and state income tax purposes. The Company is obligated to pay federal and state income taxes on its taxable income. Currently, the highest regular marginal federal income tax rate for a corporation is 35 percent; however, the Company anticipates a marginal effective rate of 34 percent due to expectations of the level of taxable income relative to the federal graduated tax rates, including the tax rate anticipated when temporary differences reverse. The Company may be subject to a 20 percent federal alternative minimum tax on its federal alternative minimum taxable income to the extent that its alternative minimum tax exceeds its regular federal income tax.

The Company invests in MLPs, which generally are treated as partnerships for federal income tax purposes. As a limited partner in the MLPs, the Company reports its allocable share of the MLP’s taxable income in computing its own taxable income. The Company’s tax expense or benefit is included in the Statement of Operations based on the component of income or gains (losses) to which such expense or benefit relates. Deferred income taxes reflect the net effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. A valuation allowance is recognized if, based on the weight of available evidence, it is more likely than not that some portion or all of the deferred income tax asset will not be realized.

I. Offering and Debt Issuance Costs

Offering costs related to the issuance of common and preferred stock are charged to additional paid-in capital when the stock is issued. Debt issuance costs related to long-term debt obligations are capitalized and amortized over the period the debt is outstanding.

J. Derivative Financial Instruments

The Company may use derivative financial instruments (principally interest rate swap and forward foreign currency contracts) to manage interest rate and currency risks. The Company has established policies and procedures for risk assessment and the approval, reporting and monitoring of derivative financial instrument activities. The Company does not hold or issue derivative financial instruments for speculative purposes. All derivative financial instruments are recorded at fair value with changes in fair value during the reporting period, and amounts accrued under the agreements, included as unrealized gains or losses in the accompanying Statement of Operations. Cash settlements under the terms of the interest rate swap and forward foreign currency contracts and termination of such contracts are recorded as realized gains or losses in the accompanying Statement of Operations. The Company did not hold any derivative financial instruments during the period ended May 31, 2011.

K. Indemnifications

Under the Company’s organizational documents, its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the Company. In addition, in the normal course of business, the Company may enter into contracts that provide general indemnification to other parties. The Company’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Company that have not yet occurred, and may not occur. However, the Company has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

L. Recent Accounting Pronouncement

In May 2011, the FASB issued ASU No. 2011-04 “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements” in GAAP and the International Financial Reporting Standards (“IFRSs”). ASU No. 2011-04 amends FASB ASC Topic 820, Fair Value Measurements and Disclosures, to establish common requirements for measuring fair value and for disclosing information about fair value measurements in accordance with GAAP and IFRSs. ASU No. 2011-04 is effective for fiscal years beginning after December 15, 2011 and for interim periods within those fiscal years. Management is currently evaluating these amendments and does not believe they will have a material impact on the Company’s financial statements.

12 Tortoise North American Energy Corp.

Notes to Financial Statements (Unaudited) (Continued) |

3. Concentration of Risk

Under normal conditions, the Company will have at least 80 percent of its total assets in equity securities of companies in the energy sector with their primary operations in North America (“Energy Companies”). Energy Companies include companies that derive more than 50 percent of their revenues from transporting, processing, storing, distributing or marketing natural gas, natural gas liquids, electricity, coal, crude oil or refined petroleum products, or exploring, developing, managing or producing such commodities. The Company may invest up to 50 percent of its total assets in restricted securities. In determining application of these policies, the term “total assets” includes assets obtained through leverage. Companies that primarily invest in a particular sector may experience greater volatility than companies investing in a broad range of industry sectors. The Company may, for defensive purposes, temporarily invest all or a significant portion of its assets in investment grade securities, short-term debt securities and cash or cash equivalents. To the extent the Company uses this strategy, it may not achieve its investment objective.

4. Agreements

The Company has entered into an Investment Advisory Agreement with Tortoise Capital Advisors, L.L.C. (the “Adviser”). Under the terms of the agreement, the Company pays the Adviser a fee equal to an annual rate of 1.00 percent of the Company’s average monthly total assets (including any assets attributable to leverage) minus accrued liabilities (other than debt entered into for purposes of leverage and the aggregate liquidation preference of outstanding preferred stock, if any) (“Managed Assets”), in exchange for the investment advisory services provided. The Adviser has contractually agreed to waive fees in an amount equal to an annual rate of 0.10 percent of the Company’s average monthly Managed Assets for the period from January 1, 2009 through December 31, 2010 and to waive fees in an amount equal to an annual rate of 0.05 percent of the Company’s average monthly Managed Assets from January 1, 2011 through December 31, 2011.

U.S. Bancorp Fund Services, LLC serves as the Company’s administrator. The Company pays the administrator a monthly fee computed at an annual rate of 0.04 percent of the first $1,000,000,000 of the Company’s Managed Assets, 0.01 percent on the next $500,000,000 of Managed Assets and 0.005 percent on the balance of the Company’s Managed Assets.

Computershare Trust Company, N.A. serves as the Company’s transfer agent and registrar and Computershare Inc. serves as the Company’s dividend paying agent and agent for the automatic dividend reinvestment plan.

U.S. Bank, N.A. serves as custodian of the Company’s cash and investment securities. The Company pays the custodian a monthly fee computed at an annual rate of 0.004 percent of the Company’s portfolio assets, plus portfolio transaction fees.

5. Income Taxes

Deferred income taxes reflect the net tax effect of temporary differences between the carrying amount of assets and liabilities for financial reporting and tax purposes. Components of the Company’s deferred tax assets and liabilities as of May 31, 2011, are as follows:

| Deferred tax assets: | ||

| Net operating loss carryforwards | $ | 5,144,237 |

| Capital loss carryforwards | 6,863,836 | |

| Organization costs | 49,204 | |

| State of Kansas credit | 4,055 | |

| 12,061,332 | ||

| Deferred tax liabilities: | ||

| Basis reduction of investment in MLPs | 3,538,734 | |

| Net unrealized gains on investment securities | 27,260,769 | |

| 30,799,503 | ||

| Total net deferred tax liability | $ | 18,738,171 |

At May 31, 2011, a valuation allowance was not deemed necessary because the Company believes it is more likely than not that there is an ability to realize its deferred tax assets through future taxable income of the appropriate character. Any adjustments to such estimates will be made in the period such determination is made. The Company’s policy is to record interest and penalties on uncertain tax positions as part of tax expense. As of May 31, 2011, the Company had no uncertain tax positions and no penalties and interest were accrued. Tax years subsequent to the year ending November 30, 2006 remain open to examination by federal and state tax authorities.

Total income tax expense differs from the amount computed by applying the federal statutory income tax rate of 34 percent to net investment loss and net realized and unrealized gains on investments for the period ended May 31, 2011, as follows:

| Application of statutory income tax rate | $ | 5,132,181 |

| State income taxes, net of federal tax benefit | 434,726 | |

| Foreign tax expense, net of federal tax benefit | 11,033 | |

| Total income tax expense | $ | 5,577,940 |

Total income taxes are computed by applying the federal statutory rate plus a blended state income tax rate.

For the period from December 1, 2010 through May 31, 2011, the components of income tax expense include current foreign tax expense (for which the federal tax benefit is reflected in deferred tax expense) of $17,479 and deferred federal and state income tax expense (net of federal tax benefit) of $5,126,238 and $434,223, respectively.

The Company acquired all of the net assets of Tortoise Gas and Oil Corporation (“TGO”) on September 14, 2009 in a tax-free reorganization under Section 368(a)(1)(C) of the Internal Revenue Code. As of November 30, 2010, the Company had a net operating loss for federal income tax purposes of approximately $13,000,000. This includes a net operating loss of $7,900,000 from TGO. The net operating loss may be carried forward for 20 years. If not utilized, this net operating loss will expire as follows: $2,700,000, $5,200,000, $2,000,000, and $3,100,000 in the years ending November 30, 2027, 2028, 2029 and 2030, respectively. Utilization of the net operating loss from TGO is further subject to Section 382 limitations of the Internal Revenue Code, which limit tax attributes subsequent to ownership changes.

2011 2nd Quarter Report 13

Notes to Financial Statements (Unaudited) (Continued) |

As of November 30, 2010, the Company had a capital loss carryforward of approximately $27,400,000 which may be carried forward for 5 years. This amount includes a capital loss of $4,000,000 from TGO. If not utilized, the capital loss will expire as follows: $2,700,000, $16,600,000, and $8,100,000 in the years ending November 30, 2012, 2013 and 2014, respectively. The amount of deferred tax asset for these items at May 31, 2011 also includes amounts for the period from December 1, 2010 through May 31, 2011. For corporations, capital losses can only be used to offset capital gains and cannot be used to offset ordinary income.

As of May 31, 2011, the aggregate cost of securities for federal income tax purposes was $121,506,217. The aggregate gross unrealized appreciation for all securities in which there was an excess of fair value over tax cost was $83,650,383, the aggregate gross unrealized depreciation for all securities in which there was an excess of tax cost over fair value was $137,631 and the net unrealized appreciation was $83,512,752.

6. Fair Value of Financial Instruments

Various inputs are used in determining the value of the Company’s investments. These inputs are summarized in the three broad levels listed below:

| Level 1 — | quoted prices in active markets for identical investments | |

| Level 2 — | other significant observable inputs (including quoted prices for similar investments, market corroborated inputs, etc.) | |

| Level 3 — | significant unobservable inputs (including the Company’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following table provides the fair value measurements of applicable Company assets by level within the fair value hierarchy as of May 31, 2011. These assets are measured on a recurring basis.

| Fair Value at | ||||||||||||

| Description | May 31, 2011 | Level 1 | Level 2 | Level 3 | ||||||||

| Equity Securities: | ||||||||||||

| Common Stock(a) | $ | 12,138,263 | $ | 12,138,263 | $ | — | $ | — | ||||

| Master Limited Partnerships | ||||||||||||

| and Related Companies(a) | 192,768,544 | 183,728,542 | 9,040,002 | — | ||||||||

| Total Equity Securities | 204,906,807 | 195,866,805 | 9,040,002 | — | ||||||||

| Other: | ||||||||||||

| Short-Term Investment(b) | 112,162 | 112,162 | — | — | ||||||||

| Total Other | 112,162 | 112,162 | — | — | ||||||||

| Total | $ | 205,018,969 | $ | 195,978,967 | $ | 9,040,002 | $ | — | ||||

| (a) | All other industry classifications are identified in the Schedule of Investments. |

| (b) | Short-term investment is a sweep investment for cash balances in the Company at May 31, 2011. |

Valuation Techniques

In general, and where applicable, the Company uses readily available market quotations based upon the last updated sales price from the principal market to determine fair value. This pricing methodology applies to the Company’s Level 1 investments.

An equity security of a publicly traded company acquired in a private placement transaction without registration under the Securities Act of 1933, as amended (the “1933 Act”), is subject to restrictions on resale that can affect the security’s fair value. If such a security is convertible into publicly-traded common shares, the security generally will be valued at the common share market price adjusted by a percentage discount due to the restrictions and categorized as Level 2 in the fair value hierarchy. If the security has characteristics that are dissimilar to the class of security that trades on the open market, the security will generally be valued and categorized as Level 3 in the fair value hierarchy.