| Benchmark | DBIQ Optimum Yield | |

| index: | Diversified Commodity | |

| Index Excess ReturnTM | ||

| Inception: | Feb. 3, 2006 | |

| Total expense | 0.89% | |

ratio: | ||

| AUM: | $3.01 billion | |

| (as of June 29, 2018) | ||

Category:

| Commodities

| |

| Issuer Free Writing Prospectus dated |

| August 15, 2018. |

| Filed pursuant to Rule 433. |

Registration number333-223891.

|

Source: Bloomberg L.P., as of June 30, 2018.PastPerformance does not guarantee future results. An investment cannot be made directly into an index.

Source: Bloomberg L.P., June 1, 2008 to June 30, 2018.Past performance does not guarantee future results. Emerging markets are represented by the MSCI Emerging Markets Index, developed markets are represented by the MSCI EAFE Index, US equities are represented by the S&P 500 Index and US bonds are represented by the Bloomberg Barclays US Aggregate Bond Index. An investment cannot be made directly into an index.

| Fund in Focus Invesco DB Commodity Index Tracking Fund |

| Key features | ||

∎

| Portfolio solution to hedge against inflation | |

| ∎ | Commodities as a key portfolio diversifier | |

| ∎ | Diversified exposure to broad basket of commodities | |

∎

| Optimize roll yield return potential

| |

Portfolio solution to hedge against inflation

Inflation is the increase in the amount of currency required to purchase goods and services. Commodities can help protect investment portfolios against inflation because they represent the value of the goods, not the value of the currency. Unlike stocks, bonds, or Treasury inflation protected securities (TIPS), commodities historically have a strong positive correlation to inflation.

10-year correlation to inflation1

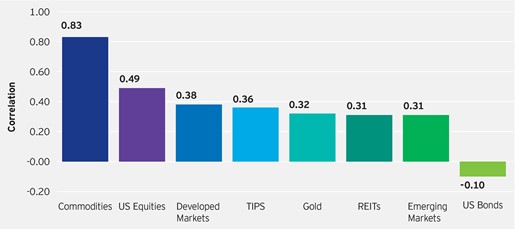

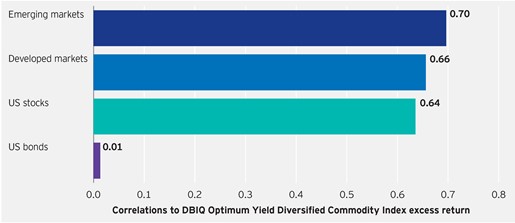

Commodities as a key portfolio diversifier

As illustrated in the chart below, commodities have historically demonstrated limited correlation to US stocks and bonds, and developed and emerging markets. The history of moderate correlation meant that commodities were typically less influenced by market dynamics, thus offering potential diversification benefits when incorporated into traditional allocation models.

Commodities correlation

| 1 | Inflation is measured by changes in the Consumer Price Index (CPI). Correlation is the degree to which two investments have historically moved in relation to each other. Asset classes were represented by the following indexes respectively: Commodities: DBIQ Optimum Yield Diversified Commodity Excess ReturnTM; TIPS: ICE BofAML US Inflation-Linked Treasury Index; Gold: Gold Spot Fix pm; REITs: MSCI US REIT Index; Emerging markets: MSCI Emerging Markets Index; Developed markets: MSCI EAFE Index; US equities: S&P 500 Index; and US bonds: Bloomberg Barclays US Aggregate Bond Index. |

Not FDIC Insured | May Lose Value | No Bank Guarantee

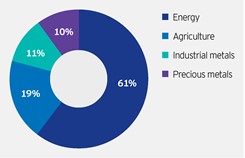

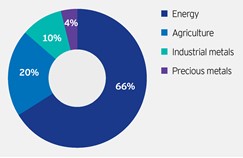

Diversified exposure to broad basket of commodities

DBC is one of the largest and most liquid broad-based commodity ETFs in the US today, based on current AUM and average daily volume. Its underlying index, DBIQ Optimum Yield Diversified Commodity Index Excess Return (DBIQ Index), offers diversified exposure to 14 commodities. DBC maintains robust exposure to energy opportunities while offering expanded exposure to other asset classes, including precious metals. Target weights for annual rebalancing are shown below.

DBIQ Index

| S&P GSCI Index

|

Source: Bloomberg L.P., index weights as of June 29, 2018. Totals may not add up to 100% due to rounding.

Optimize roll yield return potential

One component of the fund’s total return is roll return generated by rolling from a short-term futures contract to a longer-term futures contract. Roll return, impacted by the shape of the futures curve, is negative when the markets are in contango and positive when markets are in backwardation.

Conventional commodity indexes tend to implement a rigid front-month only roll process where the index simply rolls to the next available contract, which is the $102.00 contract in the example below. In a contango market, this contract is at the steepest part of the curve and would lead to the highest annual roll cost of $24.00. In contrast, the fund’s underlying index seeks to minimize the effects of negative roll cost by applying the Optimum Yield “OY” formula. The OY formula replaces expiring futures contracts with new contracts expiring in the month that will generate the highest “implied roll yield” which would be the $108.00 contract and minimize the annual cost to $8.00.

Contango

For illustrative purposes only

Backwardation

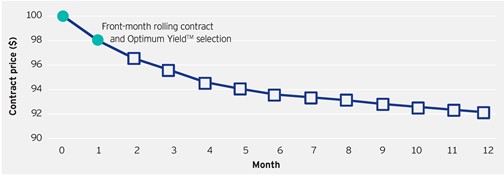

In backwardated markets, the OY formula (like the front-month rolling method) would roll into the $98.00 contract to lock in the steepest part of the curve and maximize the roll return.

For illustrative purposes only

Contango is when the front-month contract is trading at a lower price than contracts expiring in later months.

Backwardation is when the front-month contract is trading at a higher price than contracts expiring in later months.

Month

| Price

| Annual roll cost

| ||||||||

| 0 | 100.00 | |||||||||

| 1 | 102.00 | -$24.00 | ||||||||

| 2 | 103.50 | -$21.00 | ||||||||

| 3 | 104.50 | -$18.00 | ||||||||

| 4 | 105.50 | -$16.50 | ||||||||

| 5 | 106.00 | -$14.40 | ||||||||

| 6 | 106.50 | -$13.00 | ||||||||

| 7 | 106.75 | -$11.57 | ||||||||

| 8 | 107.00 | -$10.50 | ||||||||

| 9 | 107.25 | -$9.67 | ||||||||

| 10 | 107.50 | -$9.00 | ||||||||

| 11 | 107.75 | -$8.45 | ||||||||

| 12 | 108.00 | -$8.00 | ||||||||

Month

| Price

| Annual roll return

| ||||||||

| 0 | 100.00 | |||||||||

| 1 | 98.00 | $24.00 | ||||||||

| 2 | 96.50 | $21.00 | ||||||||

| 3 | 95.50 | $18.00 | ||||||||

| 4 | 94.50 | $16.50 | ||||||||

| 5 | 94.00 | $14.40 | ||||||||

| 6 | 93.50 | $13.00 | ||||||||

| 7 | 93.25 | $11.57 | ||||||||

| 8 | 93.00 | $10.50 | ||||||||

| 9 | 92.75 | $9.67 | ||||||||

| 10 | 92.50 | $9.00 | ||||||||

| 11 | 92.25 | $8.45 | ||||||||

| 12 | 92.00 | $8.00 | ||||||||

| DBC is offered by Invesco, an ETF industry innovator and smart beta pioneer. In addition to DBC, we offer a suite of commodity ETFs to give investors access to products that seek commodity exposure on a global level. |

| Contact us to learn more: |

| Financial Advisors |

| 800.983.0903 |

| Registered Investment Advisors and Institutions |

866.406.5693

|

TheDBIQ Optimum Yield Diversified CommodityIndex Excess ReturnTMis composed of futures contracts on 14 heavily traded commodities across the energy, precious metals, industrial metals and agriculture sectors. The S&P GSCI Indexmeasures the performance of commodities over time. TheConsumer Price Index (CPI) measures the prices consumers pay for a basket of consumer-based goods and services. The BloombergBarclays US Aggregate Bond Index represents the US investment-grade,fixed-rate bond market. The Gold Spot Fix PM establishes the price per ounce of gold at 3 p.m. London time as deemed by the five members of the London Gold Pool. The five members determine where supply meets demand for the bank’s entire pending buy and sell orders to find a price balance. The ICE BofAML US Inflation-LinkedTreasury Index is an unmanaged index comprised of US Treasury Inflation-Protected Securities with at least $1 billion in outstanding face value and a remaining term to final maturity of greater than one year. TheMSCI Emerging Markets Index represents stocks of developing countries.The MSCI EAFE Index represents stocks of Europe, Australasia and the Far East. TheMSCI US REIT Index is an unmanaged index considered representative of real estate equity performance. The index is computed using the gross return, which does not withhold taxes fornon-resident investors.

Risk Information

This fund is not suitable for all investors due to the speculative nature of an investment based upon the fund’s trading which takes place in very volatile markets. Because an investment in futures contracts is volatile, such frequency in the movement in market prices of the underlying futures contracts could cause large losses. Please see the prospectus for additional risk disclosures.

The shares of the fund are not deposits, interests in or obligations of Deutsche Bank AG, Deutsche Bank AG London Branch, Deutsche Bank Securities Inc., Deutsche Investment Management Americas Inc. or any of their respective subsidiaries or affiliates or any other bank

(collectively, the “DB Parties”) and are not guaranteed by the DB Parties.

Shares are not individually redeemable and owners of the shares may acquire those shares from the fund and tender those shares for redemption to the fund in creation unit aggregations only, typically consisting of 200,000 shares.

DBIQ Optimum Yield Diversified Commodity Index Excess Return™ (the “Index”) is a product of Deutsche Bank AG and/or its affiliates. Information regarding this Index is reprinted with permission. © Copyright 2018. Deutsche Bank®, DB™, DBIQ®, and DBIQ Optimum Yield Diversified Commodity Index Excess Return™ are trademarks or service marks of Deutsche Bank AG and have been licensed for use for certain purposes by Invesco Capital Management LLC, an affiliate of Invesco Distributors, Inc. The fund is not sponsored, endorsed, sold or promoted by DB Parties or their third party licensors and none of such parties makes any representation, express or implied, regarding the advisability of investing in the fund, nor do such parties have any liability for errors, omissions, or interruptions in the Index. As the index provider, Deutsche Bank AG is licensing certain trademarks, the underlying Index and trade names which are composed by Deutsche Bank AG without regard to the Index, this product or any investor.

Invesco Capital Management LLC and Invesco Distributors, Inc. are not affiliated with Deutsche Investment Management Americas Inc.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

Beta is a measure of risk representing how a security is expected to respond to general market movements. Smart Beta represents an alternative and selection index based methodology that seeks to outperform a benchmark or reduce portfolio risk, both in active or passive vehicles. Smart beta funds may underperformcap-weighted benchmarks and increase portfolio risk.

Diversification does not ensure a profit or eliminate the risk of loss.

Invesco Capital Management LLC, investment adviser and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

Commodities and futures generally are volatile and are not suitable for all investors.

Please review the prospectus for break-even figures for the fund.

Shares in the fund are not FDIC insured, may lose value and have no bank guarantee.

The value of the shares of the fund relate directly to the value of the futures contracts and other assets held by the fund and any fluctuation in the value of these assets could adversely affect an investment in the fund’s shares.

The fund is speculative and involves a high degree of risk. An investor may lose all or substantially all of an investment in the fund.

The fund is not a mutual fund or any other type of Investment Company within the meaning of the Investment Company Act of 1940, as amended, and is not subject to regulation thereunder.

The issuer has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the issuer, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling toll-free1-800-983-0903.

Note: Not all products available through all firms or in all jurisdictions.

invesco.com/us 800 983 0903 P-DBC-FIF-1 08/18 Invesco Distributors, Inc. US8627