UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21777

John Hancock Funds III

(Exact name of registrant as specified in charter)

601 Congress Street, Boston, Massachusetts 02210

(Address of principal executive offices) (Zip code)

George M. Boyd

Senior Counsel and Assistant Vice President

601 Congress Street

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-663-4204

| Date of fiscal year end: | February 28 |

| Date of reporting period: | August 31, 2006 |

ITEM 1. REPORT TO SHAREHOLDERS.

| TABLE OF CONTENTS |

| Managers' report |

| page 2 |

| A look at performance |

| page 6 |

| Your expenses |

| page 8 |

| Fund’s investments |

| page 1 0 |

| Financial statements |

| page 1 8 |

| For more information |

| page 40 |

CEO corner

To Our Shareholders,

The future has arrived at John Hancock Funds.

We have always been firm believers in the powerful role the Internet can play in providing fund information to our shareholders and prospective investors. Recently, we launched a redesigned, completely overhauled Web site that is more visually pleasing, easier to navigate and, most importantly, provides more fund information and learning tools without overwhelming the user.

Not long after we embarked on this major project, a study was released by the Investment Company Institute, the mutual fund industry’s main trade group, which found that an overwhelming majority of shareholders consider the Internet the “wave of the future” for accessing fund information.

Our new site sports fresher and faster ways to access account information. New innovations allow investors to view funds by risk level, track the performance of the John Hancock funds of their choice or sort funds by Morningstar, Inc.’s star ratings. Investors who own a John Hancock fund through a qualified retirement plan and don’t pay sales charges when making a purchase have the option of sorting by a “Load Waived” Morningstar Rating, thereby creating an apples-to-apples comparison with no-load funds that may also be available in their retirement plan.

The new site also has more educational tools and interactive modules to educate and assist investors with their financial goals, from college savings to retirement planning. A new “I want to…” feature allows investors to check performance, invest more money, update personal information or download prospectuses and forms quickly and easily.

In another of our ongoing efforts to provide our shareholders with top-notch service, we also redesigned our shareholder reports, as you may have noticed with this report. We hope the larger size, more colorful cover and redesigned presentation of the commentary and data tables will draw you in and make them easier to read.

After you’ve read your shareholder report, we encourage you to visit our new Web site — www.jhfunds.com — and take a tour. It’s easy, fast and fun and allows you to be in control of what you see and do. In short, it’s the wave of the future!

Sincerely,

Keith F. Hartstein,

President and Chief Executive Officer

This commentary reflects the CEO’s views as of August 31, 2006. They are subject to change at any time.

Your fund at a glance

The Fund seeks long-term capital growth by typically investing in U.S. companies that issue stocks included in the Russell 1000 Index and in companies with size and growth characteristics similar to those of companies with stocks in the Index.

From inception June 12, 2006

► U.S. stocks posted decent gains as the threat of higher interest rates seemed to fade.

► The Fund’s performance was aided by the more defensive names in the health care and grocery chain segments.

► Momentum stocks suffered and were the biggest detractors from the Fund’s returns.

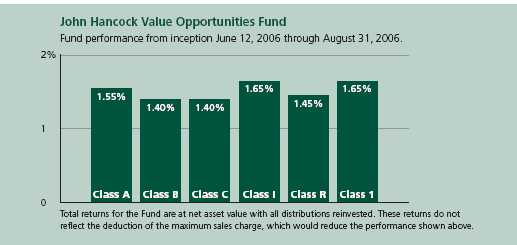

John Hancock Intrinsic Value Fund

Fund performance from inception June 12, 2006 through August 31, 2006

Total returns for the Fund are at net asset value with all distributions reinvested. These returns do not reflect the deduction of the maximum sales charge, which would reduce the performance shown above.

| Top 10 holdings | |

| Pfizer, Inc. | 5.5% |

| Citigroup, Inc. | 4.7% |

| Verizon Communications, Inc. | 4.3% |

| AT&T, Inc. | 3.9% |

| Merck & Company, Inc. | 3.6% |

| American International Group, Inc. | 2.9% |

| Fannie Mae | 2.3% |

| Home Depot, Inc. | 2.2% |

| Altria Group, Inc. | 1.9% |

| Morgan Stanley | 1.7% |

As a percentage of net assets on August 31, 2006.

1

SCORECARD

Managers’ report

John Hancock

Intrinsic Value Fund

Despite increased stock market volatility prompted by uncertainty over the economy, interest rates and geopolitical events, U.S. stocks as a whole posted decent gains for the period spanning the Fund’s inception on June 12, 2006, to its semiannual period end on August 31, 2006. The period began just weeks after newly appointed Federal Reserve Board Chairman Ben Bernanke rattled investors by seeming to imply that inflation pressures were mounting and, as a result, interest rates would move higher than the market might previously have anticipated. Equity investors worried that the Fed might raise rates too much and trigger a recession. But beginning in mid-July, stocks staged an impressive rally that accelerated in early August, when the Fed opted not to increase interest rates again for the first time in two years. Against this macroeconomic backdrop, large-company stocks performed in line with their smaller cap counterparts, foreign equities performed better than those in the U.S., and value stocks trumped growth stocks.

Performance

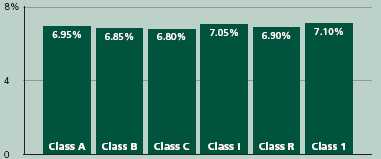

From its inception on June 12, 2006 through August 31, 2006, John Hancock Intrinsic Value Fund’s Class A, Class B, Class C, Class I, Class R and Class 1 shares returned 6.95%, 6.85%, 6.80%, 7.05%, 6.90% and 7.10%, respectively, at net asset value. By comparison, the Russell 1000 Value Index returned 7.15% and the average large value fund returned 6.09% at net asset value, according to Morningstar, Inc.1

| INVESTMENT | PERIOD’S PERFORMANCE AND WHAT’S BEHIND THE NUMBERS | |

| Merck | ▲ | Bounces back in response to stronger-than-expected sales |

| Kroger | ▲ | Shares rise as investors gravitate to defensive names |

| Home Depot | ▼ | Housing market slowdown prompts worries over future profits |

2

Portfolio Managers, Grantham, Mayo, Van Otterloo & Co. LLC (GMO)

Sam Wilderman, Ed Choi, Donna Murphy, Chuck Joyce and Tara Oliver

“During this abbreviated period,

our best performers were

generated by our valuation

discipline.”

Strategy explained

Since the Fund is new, we are continuing to build our positions, using our time-tested investment process. Although many managers use a single methodology to select stocks, we use two independent disciplines to select stocks for the Fund: valuation and momentum. Over two-thirds of stocks in this portfolio are bought based on valuation. We seek quality companies that are selling for less than their worth with the expectation that they will remain profitable, eventually regain favor in the market and generate above-average returns. Although traditional measures of a stock’s cheapness, such as price-to-book (P/B) or price-to-earnings (P/E) ratios may help investors determine if a company’s stock price is low, such measures do not distinguish between high-quality and low-quality companies. We believe high-quality companies are worth a premium because they can sustain a competitive advantage an d continue to grow over the long term.

The remaining stocks in the Fund are considered “momentum” stocks; that is, we select value stocks that are experiencing price appreciation and/or positive earnings revisions. This momentum typically follows a decline relative to the market. We’ve determined that stocks whose prices have declined for six months, then advanced for 12 months, will tend to continue rising for another 12 to 18 months. Price momentum enables portfolios to benefit from short-term swings in earnings and investor sentiment.

Because momentum and valuation tools tend to perform differently across various market and economic cycles, the Fund’s combination of the two disciplines results in greater diversification in the portfolio. Diversification

3 Intrinsic Value Fund

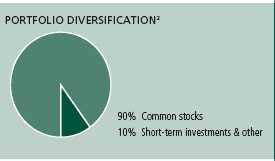

SECTOR DISTRIBUTION2

| Financial | 29% |

| Consumer, | |

| non-cyclical | 23% |

| Consumer, cyclical | 13% |

| Communications | 11% |

| Industrial | 5% |

| Energy | 4% |

| Technology | 4% |

| Mortgage securities | 4% |

| Basic materials | 1% |

| Utilities | 0.3% |

may help to lower the Fund’s risk level. We also employ a number of other risk control techniques. We typically hold more than 300 common stocks, so that the Fund’s performance isn’t overly dependent on the fortunes of one or a handful of companies. We give more weight to large-cap companies with strong balance sheets and high profit margins. Finally, we limit our holdings by economic sector and company size within the large-cap universe.

Leaders and laggards

During this abbreviated period, our best performers were generated by our valuation discipline. In particular, we saw gains from companies whose shares had been beaten up in prior periods but rallied in response to investors’ growing appetite for defensive stocks — shares of companies whose sales and profits tend to continue to grow even while the broader economy slows. Leading the pack were our stakes in large drug companies Merck & Company, Inc. and Pfizer, Inc. Merck’s net profit rose substantially and the company raised its profit forecast for the full year, helped by strong sales of cholesterol drug Zocor. Pfizer posted strong earnings in August, thanks in large part to stronger-than-expected sales of Lipitor, the anti-cholesterol medication that is one of the best-selling drugs in the world. Investors also cheered a management change and shake-up in the executive suite. A growing move toward defensive stocks also helped our shares in grocery store chains The Kroger Company and Safeway, Inc. Our holdings in Ford Motor Company contributed to performance, as investors looked to the stock as an interesting value play.

Detracting from Fund returns was the fact that we were significantly underweighted relative to the index in some strong-performing energy stocks, which were among the market’s best performers during the period. We also were hurt by some of our momentum plays. Weak performers included home improvement stores Home Depot, Inc. and Lowe’s Companies, Inc., which both slumped as the housing market cooled.

4 Intrinsic Value Fund

“Since we remain very wary of risk, we

will continue to focus on high-quality

companies that we believe can best

weather a market and/or economic

downturn.”

Outlook

The summer stock market rally and the Fed’s decision to pause its interest-rate-raising cycle after 17 consecutive quarter-point hikes since June 2004, appear to have provided investors with reasons for optimism. By the end of the period, stocks overall seemed “priced for perfection,” with investors betting that economic growth would remain moderate and sustainable and that inflation would be contained. But we believe this optimism is likely overblown and that the market is significantly underpricing risk. The investment landscape is always fraught with any number of risks, be it higher-than-expected inflation and interest rates, slower-than-expected economic growth or geopolitical events. But we believe that the economy and financial systems are so highly levered at the moment that even the smallest unfavorable development could result in a significant repricing of risk, meaning that risk ier assets would underperform. Since we remain very wary of risk, we will continue to focus on high-quality companies that we believe can best weather a market and/or economic downturn.

This commentary reflects the views of the portfolio management team through the end of the Fund’s period discussed in this report. The team’s statements reflect their own opinions. As such, they are in no way guarantees of future events and are not intended to be used as investment advice or a recommendation regarding any specific security. They are also subject to change at any time as market and other conditions warrant.

1 Figures from Morningstar, Inc. include reinvested dividends and do not take into account sales charges. Actual load-adjusted performance is lower.

2 As a percentage of net assets on August 31, 2006.

5 Intrinsic Value Fund

A look at performance

| For the period ending August 31, 2006 | ||

| Cumulative total returns | ||

| with maximum sales charge (POP) | ||

| Inception | Since | |

| Class | date | inception |

| A | 6-12-06 | 1.62% |

| B | 6-12-06 | 1.85 |

| C | 6-12-06 | 5.80 |

| I1 | 6-12-06 | 7.05 |

| R1 | 6-12-06 | 6.90 |

| 11 | 6-12-06 | 7.10 |

Performance figures assume all distributions are reinvested. Returns with maximum sales charge reflect a sales charge on Class A shares of 5%, and the applicable contingent deferred sales charge (CDSC) on Class B and Class C shares. The Class B shares’ CDSC declines annually between years 1–6 according to the following schedule: 5, 4, 3, 3, 2, 1%. No sales charge will be assessed after the sixth year. Class C shares held for less than one year are subject to a 1% CDSC. Sales charge is not applicable for Class I, Class R and Class 1 shares.

The returns reflect past results and should not be considered indicative of future performance. The return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Due to market volatility, the Fund’s current performance may be higher or lower than the performance shown. For performance data current to the most recent month-end, please call 1-800-225-5291 or visit the Fund’s Web site at www.jhfunds.com.

The performance table above and the chart on the next page do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The Fund’s performance results reflect any applicable expense reductions, without which the expenses would increase and results would have been less favorable.

Since inception performance is calculated with an opening price (prior day’s close) on the inception date.

1 For certain types of investors as described in the Fund’s Class I, Class R and Class 1 share prospectuses.

6 Intrinsic Value Fund

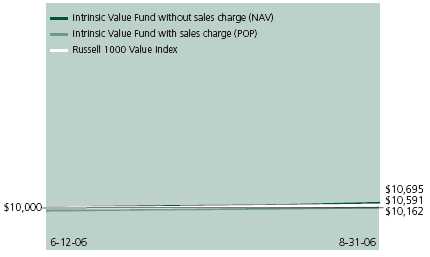

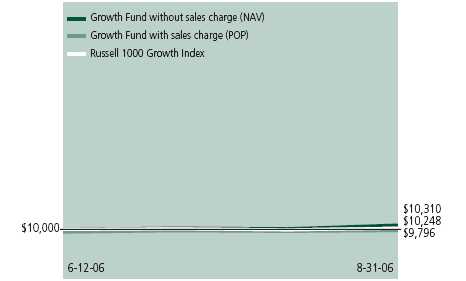

Growth of $10,000

This chart shows what happened to a hypothetical $10,000 investment in Class A shares for the period indicated. For comparison, we’ve shown the same investment in the Russell 1000 Value Index.

| With maximum | ||||

| Class | Period beginning | Without sales charge | sales charge | Index |

| B | 6-12-06 | $10,685 | $10,185 | $10,591 |

| C | 6-12-06 | 10,680 | 10,580 | 10,591 |

| I 1 | 6-12-06 | 10,705 | 10,705 | 10,591 |

| R1 | 6-12-06 | 10,690 | 10,690 | 10,591 |

| 11 | 6-12-06 | 10,710 | 10,710 | 10,715 |

Assuming all distributions were reinvested for the period indicated, the table above shows the value of a $10,000 investment in the Fund’s Class B, Class C, Class I, Class R and Class 1 shares, respectively, as of August 31, 2006. Performance of the classes will vary based on the difference in sales charges paid by shareholders investing in the different classes and the fee structure of those classes.

Russell 1000 Value Index is an unmanaged index containing those securities in the Russell 1000 Index with a less-than-average growth orientation.

It is not possible to invest directly in an index. Index figures do not reflect sales charges which would have resulted in lower values if they did.

1 For certain types of investors as described in the Fund’s Class I, Class R and Class 1 share prospectuses.

7 Intrinsic Value Fund

Your expenses

These examples are intended to help you understand your ongoing operating expenses.

Understanding Fund expenses

As a shareholder of the Fund, you incur two types of costs:

■ Transaction costs which include sales charges (loads) on purchases or redemptions (varies by share class), minimum account fee charge, etc.

■ Ongoing operating expenses including management fees, distribution and service fees (if applicable) and other Fund expenses.

We are going to present only your ongoing operating expenses here.

Actual expenses/actual returns

This example is intended to provide information about your Fund’s actual ongoing operating expenses, and is based on your Fund’s actual return. It assumes an account value of $1,000.00 on June 12, 2006, with the same investment held until August 31, 2006.

| Account value | Ending value | Expenses paid during period | |

| on 6-12-06 | on 8-31-06 | ended 8-31-061 | |

| Class A | $1,000.00 | $1,069.50 | $3.10 |

| Class B | 1,000.00 | 1,068.50 | 4.65 |

| Class C | 1,000.00 | 1,068.00 | 4.65 |

| Class I | 1,000.00 | 1,070.50 | 2.17 |

| Class R | 1,000.00 | 1,069.00 | 3.83 |

| Class 1 | 1,000.00 | 1,071.00 | 2.07 |

Together with the value of your account, you may use this information to estimate the operating expenses that you paid over the period. Simply divide your account value at August 31, 2006 by $1,000.00, then multiply it by the “expenses paid” for your share class from the table above. For example, for an account value of $8,600.00, the operating expenses should be calculated as follows:

8 Intrinsic Value Fund

Hypothetical example for comparison purposes

This table allows you to compare your Fund’s ongoing operating expenses with those of any other fund. It provides an example of the Fund’s hypothetical account values and hypothetical expenses based on each class’ actual expense ratio and an assumed 5% annual return before expenses (which is not your Fund’s actual return). It assumes an account value of $1,000.00 on June 12, 2006, with the same investment held until August 31, 2006. Look in any other fund shareholder report to find its hypothetical example and you will be able to compare these expenses.

| Account value | Ending value | Expenses paid during period | |

| on 6-12-06 | on 8-31-06 | ended 8-31-061 | |

| Class A | $1,000.00 | $1,008.00 | $3.01 |

| Class B | 1,000.00 | 1,006.50 | 4.51 |

| Class C | 1,000.00 | 1,006.50 | 4.51 |

| Class I | 1,000.00 | 1,008.90 | 2.11 |

| Class R | 1,000.00 | 1,007.30 | 3.71 |

| Class 1 | 1,000.00 | 1,009.00 | 2.01 |

Remember, these examples do not include any transaction costs, such as sales charges; therefore, these examples will not help you to determine the relative total costs of owning different funds. If transaction costs were included, your expenses would have been higher. See the prospectus for details regarding transaction costs.

1 Expenses are equal to the Fund's annualized expense ratio of 1.35%, 2.05%, 2.05%, 0.95%, 1.70% and 0.90% for Class A, Class B, Class C, Class I, Class R and Class 1, respectively, multiplied by the average account value over the period, multiplied by the number of days in the inception period /365 or 366 (to reflect the one-half year period).

Intrinsic Value Fund 9

F I N A N C I A L S T A T E M E N T S

Fund’s investments

Securities owned by the Fund on 8-31-06 (unaudited)

This schedule is divided into two main categories: common stocks and short-term investments. Common stocks are further broken down by industry group. Short-term investments, which represent the Fund’s cash position, are listed last.

| Issuer | Shares | Value |

| Common stocks 93.80% | $15,725,218 | |

| (Cost $14,775,702) | ||

| Aerospace 0.24% | 40,086 | |

| Northrop Grumman Corp. | 600 | 40,086 |

| Agriculture 0.30% | 49,404 | |

| Archer-Daniels-Midland Company | 1,200 | 49,404 |

| Aluminum 0.39% | 65,757 | |

| Alcoa, Inc. | 2,300 | 65,757 |

| Apparel & Textiles 0.99% | 165,217 | |

| Jones Apparel Group, Inc. | 1,000 | 31,300 |

| Liz Claiborne, Inc. | 1,200 | 44,844 |

| Mohawk Industries, Inc. * | 400 | 28,352 |

| Polo Ralph Lauren Corp., Class A | 200 | 11,798 |

| VF Corp. | 700 | 48,923 |

| Auto Parts 0.73% | 122,351 | |

| AutoZone, Inc. * | 200 | 18,060 |

| Johnson Controls, Inc. | 900 | 64,737 |

| O’Reilly Automotive, Inc. * | 1,000 | 29,690 |

| TRW Automotive Holdings Corp. * | 400 | 9,864 |

| Auto Services 0.31% | 52,461 | |

| AutoNation, Inc. * | 2,700 | 52,461 |

| Automobiles 1.22% | 204,885 | |

| Ford Motor Company | 18,600 | 155,682 |

| PACCAR, Inc. | 900 | 49,203 |

| Banking 5.08% | 852,123 | |

| AmSouth Bancorp. | 600 | 17,190 |

| Bank of America Corp. | 4,000 | 205,880 |

| Bank of New York Company, Inc. | 1,500 | 50,625 |

| BB&T Corp. | 1,300 | 55,640 |

| Comerica, Inc. | 1,600 | 91,600 |

| Cullen Frost Bankers, Inc. | 200 | 11,792 |

| Fifth Third Bancorp. | 500 | 19,670 |

| 10 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Banking (continued) | ||

| First Horizon National Corp. | 500 | $19,090 |

| Golden West Financial Corp. | 300 | 22,647 |

| Huntington Bancshares, Inc. | 1,000 | 23,920 |

| KeyCorp | 2,200 | 80,938 |

| National City Corp. | 6,300 | 217,854 |

| US Bancorp | 1,100 | 35,277 |

| Biotechnology 0.16% | 27,585 | |

| Applera Corp. | 900 | 27,585 |

| Broadcasting 0.32% | 53,291 | |

| CBS Corp., Class B | 1,400 | 39,970 |

| News Corp. | 700 | 13,321 |

| Building Materials & Construction 0.36% | 60,564 | |

| American Standard Companies, Inc. | 400 | 16,708 |

| Masco Corp. | 1,600 | 43,856 |

| Business Services 1.28% | 214,231 | |

| Affiliated Computer Services, Inc., Class A * | 700 | 35,938 |

| Cendant Corp. | 5,000 | 9,650 |

| Computer Sciences Corp. * | 500 | 23,690 |

| Convergys Corp. * | 1,300 | 27,131 |

| Electronic Data Systems Corp. | 500 | 11,915 |

| First Data Corp. | 900 | 38,673 |

| Manpower, Inc. | 400 | 23,644 |

| Pitney Bowes, Inc. | 1,000 | 43,590 |

| Cellular Communications 0.03% | 4,676 | |

| Motorola, Inc. | 200 | 4,676 |

| Chemicals 0.23% | 38,016 | |

| PPG Industries, Inc. | 600 | 38,016 |

| Computers & Business Equipment 2.93% | 490,958 | |

| CDW Corp. | 200 | 11,660 |

| Dell, Inc. * | 3,400 | 76,670 |

| Hewlett-Packard Company | 7,700 | 281,512 |

| Ingram Micro, Inc., Class A * | 1,600 | 28,800 |

| International Business Machines Corp. | 700 | 56,679 |

| Lexmark International, Inc. * | 200 | 11,214 |

| Tech Data Corp. * | 700 | 24,423 |

| Construction Materials 0.15% | 24,708 | |

| Martin Marietta Materials, Inc. | 300 | 24,708 |

| Containers & Glass 0.08% | 12,529 | |

| Smurfit-Stone Container Corp. * | 1,100 | 12,529 |

| 11 Intrinsic Value Fund See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Crude Petroleum & Natural Gas 1.57% | $263,755 | |

| Apache Corp. | 600 | 39,168 |

| Devon Energy Corp. | 700 | 43,743 |

| Marathon Oil Corp. | 600 | 50,100 |

| Occidental Petroleum Corp. | 2,000 | 101,980 |

| Sunoco, Inc. | 400 | 28,764 |

| Electrical Equipment 0.10% | 16,430 | |

| Emerson Electric Company | 200 | 16,430 |

| Electrical Utilities 0.27% | 44,602 | |

| CenterPoint Energy, Inc. | 1,600 | 23,120 |

| Edison International | 100 | 4,364 |

| FirstEnergy Corp. | 300 | 17,118 |

| Electronics 0.31% | 51,824 | |

| Agilent Technologies, Inc. * | 300 | 9,648 |

| Arrow Electronics, Inc. * | 500 | 13,950 |

| Synopsys, Inc. * | 900 | 17,064 |

| Teleflex, Inc. | 200 | 11,162 |

| Financial Services 17.45% | 2,925,960 | |

| Bear Stearns Companies, Inc. | 200 | 26,070 |

| CIT Group, Inc. | 300 | 13,518 |

| Citigroup, Inc. | 15,900 | 784,665 |

| E*TRADE Financial Corp. * | 1,300 | 30,667 |

| Federal Home Loan Mortgage Corp. | 3,800 | 241,680 |

| Federal National Mortgage Association | 7,300 | 384,345 |

| Fiserv, Inc. * | 400 | 17,668 |

| Goldman Sachs Group, Inc. | 1,000 | 148,650 |

| JPMorgan Chase & Company | 5,700 | 260,262 |

| Lehman Brothers Holdings, Inc. | 1,300 | 82,953 |

| Mellon Financial Corp. | 1,700 | 63,291 |

| Merrill Lynch & Company, Inc. | 2,100 | 154,413 |

| Morgan Stanley | 4,300 | 282,897 |

| PNC Financial Services Group, Inc. | 2,100 | 148,659 |

| State Street Corp. (c) | 700 | 43,260 |

| Washington Mutual, Inc. | 5,800 | 242,962 |

| Food & Beverages 1.67% | 280,516 | |

| Dean Foods Company * | 700 | 27,734 |

| Kraft Foods, Inc., Class A | 2,800 | 94,948 |

| Pepsi Bottling Group, Inc. | 400 | 14,004 |

| PepsiAmericas, Inc. | 500 | 11,495 |

| Sara Lee Corp. | 3,100 | 51,553 |

| Starbucks Corp. * | 800 | 24,808 |

| Tyson Foods, Inc., Class A | 3,800 | 55,974 |

| Healthcare Products 0.42% | 71,126 | |

| Johnson & Johnson | 1,100 | 71,126 |

| 12 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Healthcare Services 3.53% | $592,416 | |

| Cardinal Health, Inc. | 2,200 | 148,324 |

| Express Scripts, Inc. * | 600 | 50,448 |

| Health Net, Inc. * | 800 | 33,448 |

| Lincare Holdings, Inc. * | 300 | 11,109 |

| McKesson Corp. | 3,400 | 172,720 |

| Quest Diagnostics, Inc. | 400 | 25,712 |

| UnitedHealth Group, Inc. | 2,900 | 150,655 |

| Holdings Companies/Conglomerates 1.29% | 215,592 | |

| General Electric Company | 5,200 | 177,112 |

| Loews Corp. | 1,000 | 38,480 |

| Homebuilders 0.63% | 105,677 | |

| Centex Corp. | 500 | 25,475 |

| KB Home | 400 | 17,104 |

| Lennar Corp., Class A | 600 | 26,904 |

| M.D.C. Holdings, Inc. | 200 | 8,558 |

| Pulte Homes, Inc. | 500 | 14,835 |

| Ryland Group, Inc. | 300 | 12,801 |

| Hotels & Restaurants 0.31% | 52,342 | |

| Brinker International, Inc. | 600 | 23,082 |

| Wyndham Worldwide Corp. * | 1,000 | 29,260 |

| Household Appliances 0.48% | 80,910 | |

| Whirlpool Corp. | 1,000 | 80,910 |

| Household Products 0.26% | 43,061 | |

| Energizer Holdings, Inc. * | 200 | 13,372 |

| Newell Rubbermaid, Inc. | 1,100 | 29,689 |

| Industrial Machinery 0.52% | 86,489 | |

| Cummins, Inc. | 100 | 11,482 |

| Deere & Company | 300 | 23,430 |

| Flowserve Corp. * | 200 | 10,228 |

| Parker-Hannifin Corp. | 200 | 14,810 |

| Terex Corp. * | 300 | 13,179 |

| W.W. Grainger, Inc. | 200 | 13,360 |

| Insurance 9.99% | 1,674,937 | |

| Aetna, Inc. | 300 | 11,181 |

| AFLAC, Inc. | 3,000 | 135,210 |

| Allstate Corp. | 800 | 46,352 |

| Ambac Financial Group, Inc. | 600 | 51,954 |

| American Financial Group, Inc. | 600 | 28,032 |

| American International Group, Inc. | 7,700 | 491,414 |

| Amerus Group Company | 300 | 20,340 |

| Aon Corp. | 1,800 | 62,226 |

| CIGNA Corp. | 400 | 45,228 |

| Commerce Group, Inc. | 400 | 11,916 |

13 Intrinsic Value Fund See notes to financial statements

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Insurance (continued) | ||

| Conseco, Inc. * | 600 | $12,420 |

| Fidelity National Financial, Inc. | 1,300 | 52,299 |

| First American Corp. | 700 | 28,434 |

| Hanover Insurance Group, Inc. | 400 | 17,800 |

| Hartford Financial Services Group, Inc. | 200 | 17,172 |

| Lincoln National Corp. | 900 | 54,630 |

| Marsh & McLennan Companies, Inc. | 500 | 13,080 |

| MBIA, Inc. | 1,100 | 67,793 |

| MetLife, Inc. | 800 | 44,024 |

| MGIC Investment Corp. | 400 | 23,148 |

| Nationwide Financial Services, Inc., Class A | 400 | 19,364 |

| Old Republic International Corp. | 1,600 | 33,440 |

| PMI Group, Inc. | 400 | 17,296 |

| Principal Financial Group, Inc. | 400 | 21,296 |

| Progressive Corp. | 2,100 | 51,639 |

| Protective Life Corp. | 400 | 18,412 |

| Prudential Financial, Inc. | 400 | 29,364 |

| Radian Group, Inc. | 400 | 23,952 |

| St. Paul Travelers Companies, Inc. | 1,700 | 74,630 |

| Torchmark Corp. | 700 | 43,547 |

| Transatlantic Holdings, Inc. | 200 | 12,284 |

| UnumProvident Corp. | 2,800 | 53,060 |

| W.R. Berkley Corp. | 1,200 | 42,000 |

| International Oil 1.27% | 212,977 | |

| Anadarko Petroleum Corp. | 2,700 | 126,657 |

| ConocoPhillips | 1,000 | 63,430 |

| Hess Corp. | 500 | 22,890 |

| Leisure Time 0.07% | 11,860 | |

| Walt Disney Company | 400 | 11,860 |

| Life Sciences 0.07% | 11,436 | |

| Pharmaceutical Product Development, Inc. | 300 | 11,436 |

| Manufacturing 0.55% | 92,974 | |

| Eaton Corp. | 400 | 26,600 |

| Harley-Davidson, Inc. | 400 | 23,404 |

| Snap-on, Inc. | 500 | 21,850 |

| SPX Corp. | 400 | 21,120 |

| Medical-Hospitals 0.14% | 23,578 | |

| Health Management Associates, Inc., Class A | 600 | 12,546 |

| Tenet Healthcare Corp. * | 1,400 | 11,032 |

| Metal & Metal Products 0.14% | 22,939 | |

| Reliance Steel & Aluminum Company | 700 | 22,939 |

| Office Furnishings & Supplies 0.31% | 51,576 | |

| Office Depot, Inc. * | 1,400 | 51,576 |

| 14 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Paper 0.18% | $30,741 | |

| International Paper Company | 500 | 17,385 |

| Temple-Inland, Inc. | 300 | 13,356 |

| Petroleum Services 1.37% | 230,078 | |

| Exxon Mobil Corp. | 3,400 | 230,078 |

| Pharmaceuticals 11.03% | 1,849,843 | |

| AmerisourceBergen Corp. | 2,800 | 123,648 |

| Barr Pharmaceuticals, Inc. * | 200 | 11,300 |

| Bristol-Myers Squibb Company | 4,000 | 87,000 |

| Caremark Rx, Inc. | 400 | 23,176 |

| Forest Laboratories, Inc. * | 900 | 44,982 |

| King Pharmaceuticals, Inc. * | 2,500 | 40,550 |

| Merck & Company, Inc. | 14,900 | 604,195 |

| Pfizer, Inc. | 33,200 | 914,992 |

| Photography 0.29% | 48,921 | |

| Eastman Kodak Company | 2,300 | 48,921 |

| Publishing 0.52% | 86,389 | |

| Gannett Company, Inc. | 1,300 | 73,905 |

| Tribune Company | 400 | 12,484 |

| Railroads & Equipment 0.56% | 94,246 | |

| Burlington Northern Santa Fe Corp. | 800 | 53,560 |

| Norfolk Southern Corp. | 200 | 8,546 |

| Union Pacific Corp. | 400 | 32,140 |

| Real Estate 0.16% | 26,750 | |

| Realogy Corp. * | 1,250 | 26,750 |

| Retail Grocery 2.87% | 480,555 | |

| Safeway, Inc. | 6,300 | 194,859 |

| SUPERVALU, Inc. | 2,000 | 57,120 |

| The Kroger Company | 9,600 | 228,576 |

| Retail Trade 6.87% | 1,151,141 | |

| Abercrombie & Fitch Company, Class A | 200 | 12,906 |

| Bed Bath & Beyond, Inc. * | 800 | 26,984 |

| Best Buy Company, Inc. | 300 | 14,100 |

| BJ’s Wholesale Club, Inc. * | 900 | 23,715 |

| Borders Group, Inc. | 500 | 9,565 |

| Circuit City Stores, Inc. | 400 | 9,444 |

| Costco Wholesale Corp. | 800 | 37,432 |

| Dollar General Corp. | 1,500 | 19,290 |

| Dollar Tree Stores, Inc. * | 900 | 25,902 |

| Family Dollar Stores, Inc. | 1,300 | 33,241 |

| Gap, Inc. | 1,400 | 23,534 |

| Home Depot, Inc. | 10,700 | 366,903 |

| Lowe’s Companies, Inc. | 6,200 | 167,772 |

15 Intrinsic Value Fund See notes to financial statements

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Retail Trade (continued) | ||

| Rent-A-Center, Inc. * | 500 | $13,550 |

| Staples, Inc. | 700 | 15,792 |

| The TJX Companies, Inc. | 1,100 | 29,425 |

| Tiffany & Company | 500 | 15,800 |

| Walgreen Company | 1,300 | 64,298 |

| Wal-Mart Stores, Inc. | 5,400 | 241,488 |

| Sanitary Services 0.14% | 23,996 | |

| Waste Management, Inc. | 700 | 23,996 |

| Semiconductors 0.23% | 38,077 | |

| Intel Corp. | 1,300 | 25,402 |

| Intersil Corp., Class A | 500 | 12,675 |

| Software 0.22% | 36,567 | |

| BEA Systems, Inc. * | 1,500 | 20,595 |

| BMC Software, Inc. * | 600 | 15,972 |

| Steel 0.23% | 39,096 | |

| Nucor Corp. | 800 | 39,096 |

| Telephone 9.99% | 1,674,356 | |

| ALLTEL Corp. | 400 | 21,684 |

| AT&T, Inc. | 20,800 | 647,504 |

| BellSouth Corp. | 4,700 | 191,384 |

| CenturyTel, Inc. | 1,500 | 59,730 |

| Qwest Communications International, Inc. * | 3,600 | 31,716 |

| Verizon Communications, Inc. | 20,300 | 714,154 |

| Windstream Corp. | 620 | 8,184 |

| Tobacco 2.03% | 340,777 | |

| Altria Group, Inc. | 3,700 | 309,061 |

| UST, Inc. | 600 | 31,716 |

| Toys, Amusements & Sporting Goods 0.10% | 16,956 | |

| Mattel, Inc. | 900 | 16,956 |

| Travel Services 0.14% | 24,112 | |

| Sabre Holdings Corp. | 1,100 | 24,112 |

| Trucking & Freight 0.72% | 120,798 | |

| Fedex Corp. | 1,000 | 101,030 |

| Ryder Systems, Inc. | 400 | 19,768 |

| 16 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

| Principal | ||

| Issuer, description, maturity date | amount | Value |

| Repurchase agreements 5.37% | $901,000 | |

| (Cost $901,000) | ||

| Repurchase Agreement with State Street Corp. — Dated | ||

| 8/31/2006 at 3.95% to be repurchased at $901,099 on | ||

| 9/1/2006, collateralized by $945,000 Federal National | ||

| Mortgage Association, 4.25% due 8/15/2010 (valued | ||

| at $920,194, including interest) (c) | $901,000 | $901,000 |

| Total investments (cost $15,676,702) (99.17%) | $16,626,218 | |

| Other assets in excess of liabilities 0.83% | 138,497 | |

| Total net assets 100.00% | $16,764,715 | |

* Non-income producing.

(c) Investment is an affiliate of the Trust's subadvisor or custodian bank.

17 Intrinsic Value Fund See notes to financial statements

F I N A N C I A L S T A T E M E N T S

Financial statements

Statement of assets and liabilities 8-31-06 (unaudited)

This Statement of Assets and Liabilities is the Fund’s balance sheet. It shows the value of what the Fund owns, is due and owes. You’ll also find the net asset value and the maximum offering price per share.

| Assets | |

| Investments, at value (Cost $14,775,702) | $15,725,218 |

| Repurchase agreements, at value (Cost $901,200) | 901,000 |

| Cash | 36,634 |

| Receivable for shares sold | 78,069 |

| Dividends and interest receivable | 29,621 |

| Receivable for futures variation margin | 250 |

| Other assets | 28,765 |

| Total assets | 16,799,557 |

| Liabilities | |

| Payable for shares repurchased | 150 |

| Payable to affiliates | |

| Transfer agent fees | 6,822 |

| Fund administration fees | 208 |

| Service fees | 55 |

| Other payables and accrued expenses | 27,607 |

| Total liabilities | 34,842 |

| Net assets | |

| Capital paid-in | 15,696,113 |

| Accumulated undistributed net realized gain on investments and futures contracts | 55,766 |

| Unrealized appreciation on investments and futures contracts | 964,727 |

| Undistributed net investment income | 48,109 |

| Net assets | $16,764,715 |

| Net asset value per share | |

| Based on net asset values and shares outstanding — the Fund has an | |

| unlimited number of shares authorized with no par value. | |

| Class A ($15,938,484 ÷ 744,986 shares) | $21.39 |

| Class B ($210,685 ÷ 9,861 shares) | $21.37 |

| Class C ($282,801 ÷ 13,237 shares) | $21.36 |

| Class I ($118,778 ÷ 5,547 shares) | $21.41 |

| Class R ($106,890 ÷ 5,000 shares) | $21.38 |

| Class 1 ($107,077 ÷ 5,000 shares) | $21.42 |

| Maximum offering price per share | |

| Class Aa ($21.39 ÷ 95%) | $22.52 |

a On single retail sales of less than $50,000. On sales of $50,000 or more and on group sales the offering price is reduced.

18 Intrinsic Value Fund See notes to financial statements

F I N A N C I A L S T A T E M E N T S

Statement of operations For the period ended 8-31-06a (unaudited).

This Statement of Operations summarizes the Fund’s investment income earned and expenses incurred in operating the Fund. It also shows net gains (losses) for the period stated.

| Investment income | |

| Dividends | $83,473 |

| Interest | 11,574 |

| Total investment income | 95,047 |

| Expenses | |

| Investment management fees (Note 3) | 26,925 |

| Distribution and service fees (Note 3) | 10,784 |

| Transfer agent fees (Note 3) | 6,822 |

| Fund administration fees (Note 3) | 209 |

| Blue sky fees (Note 3) | 20,404 |

| Audit and legal fees | 16,710 |

| Custodian fees | 9,047 |

| Printing and postage fees (Note 3) | 4,881 |

| Trustees’ fees (Note 3) | 111 |

| Miscellaneous | 215 |

| Total expenses | 96,108 |

| Less expense reductions (Note 3) | (49,170) |

| Net expenses | 46,938 |

| Net investment income | 48,109 |

| Realized and unrealized gain | |

| Net realized gain on | |

| Investments | 43,350 |

| Futures contracts | 12,416 |

| Change in net unrealized appreciation of | |

| Investments | 949,516 |

| Futures contracts | 15,211 |

| Net realized and unrealized gain | 1,020,493 |

| Increase in net assets from operations | $1,068,602 |

a Period from 6-12-06 (commencement of operations) to 8-31-06.

19 Intrinsic Value Fund See notes to financial statements

F I N A N C I A L S T A T E M E N T S

Statement of changes in net assets

This Statement of Changes in Net Assets shows how the value of the Fund’s net assets has changed during the last period. The difference reflects earnings less expenses, any investment gains and losses, distributions, if any, paid to shareholders and the net of Fund share transactions.

| Period | |

| endeda | |

| 8-31-06 | |

| Increase in net assets | |

| From operations | |

| Net investment income | $48,109 |

| Net realized gain | 55,766 |

| Change in net unrealized appreciation | 964,727 |

| Increase in net assets resulting from operations | 1,068,602 |

| From Fund share transactions | 15,696,113 |

| Net assets | |

| Beginning of period | — |

| End of periodb | $16,764,715 |

a Period from 6-12-06 (commencement of operations) to 8-31-06. Unaudited.

b Includes undistributed net investment income of $48,109.

| 20 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

Financial highlights

The Financial highlights show how the Fund’s net asset value for a share has changed since the end of the previous period.

| CLASS A SHARES | |

| Period ended | 8-31-06a,b |

| Per share operating performance | |

| Net asset value, beginning of period | $20.00 |

| Net investment incomeh | 0.06 |

| Net realized and unrealized | |

| gain on investments | 1.33 |

| Total from investment operations | 1.39 |

| Net asset value, end of period | $21.39 |

| Total return (%) | 6.95l,m |

| Ratios and supplemental data | |

| Net assets, end of period | |

| (in millions) | $16 |

| Ratio of net expenses to average | |

| net assets (%) | 1.35r |

| Ratio of gross expenses to average | |

| net assets (%) | 2.31r |

| Ratio of net investment income | |

| to average net assets (%) | 1.40r |

| Portfolio turnover (%) | 8m |

21 Intrinsic Value Fund See notes to financial statements

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS B SHARES | |

| Period ended | 8-31-06a,b |

| Per share operating performance | |

| Net asset value, beginning of period | $20.00 |

| Net investment incomeh | 0.03 |

| Net realized and unrealized | |

| gain on investments | 1.34 |

| Total from investment operations | 1.37 |

| Net asset value, end of period | $21.37 |

| Total return (%) | 6.85l,m |

| Ratios and supplemental data | |

| Net assets, end of period | |

| (in millions) | —i |

| Ratio of net expenses to average | |

| net assets (%) | 2.05r |

| Ratio of gross expenses to average | |

| net assets (%) | 16.56r |

| Ratio of net investment income | |

| to average net assets (%) | 0.74r |

| Portfolio turnover (%) | 8m |

| 22 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

| Financial highlights | |

| CLASS C SHARES | |

| Period ended | 8-31-06a,b |

| Per share operating performance | |

| Net asset value, beginning of period | $20.00 |

| Net investment incomeh | 0.03 |

| Net realized and unrealized | |

| gain on investments | 1.33 |

| Total from investment operations | 1.36 |

| Net asset value, end of period | $21.36 |

| Total return (%) | 6.80l,m |

| Ratios and supplemental data | |

| Net assets, end of period | |

| (in millions) | —i |

| Ratio of net expenses to average | |

| net assets (%) | 2.05r |

| Ratio of gross expenses to average | |

| net assets (%) | 14.67r |

| Ratio of net investment income | |

| to average net assets (%) | 0.59r |

| Portfolio turnover (%) | 8m |

23 Intrinsic Value Fund See notes to financial statements

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS I SHARES | |

| Period ended | 8-31-06a,b |

| Per share operating performance | |

| Net asset value, beginning of period | $20.00 |

| Net investment incomeh | 0.08 |

| Net realized and unrealized | |

| gain on investments | 1.33 |

| Total from investment operations | 1.41 |

| Net asset value, end of period | $21.41 |

| Total return (%) | 7.05l,m |

| Ratios and supplemental data | |

| Net assets, end of period | |

| (in millions) | —i |

| Ratio of net expenses to average | |

| net assets (%) | 0.95r |

| Ratio of gross expenses to average | |

| net assets (%) | 18.10r |

| Ratio of net investment income | |

| to average net assets (%) | 1.81r |

| Portfolio turnover (%) | 8m |

| 24 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS R SHARES | |

| Period ended | 8-31-06a,b |

| Per share operating performance | |

| Net asset value, beginning of period | $20.00 |

| Net investment incomeh | 0.05 |

| Net realized and unrealized | |

| gain on investments | 1.33 |

| Total from investment operations | 1.38 |

| Net asset value, end of period | $21.38 |

| Total return (%) | 6.90l,m |

| Ratios and supplemental data | |

| Net assets, end of period | |

| (in millions) | —i |

| Ratio of net expenses to average | |

| net assets (%) | 1.70r |

| Ratio of gross expenses to average | |

| net assets (%) | 20.47r |

| Ratio of net investment income | |

| to average net assets (%) | 1.06r |

| Portfolio turnover (%) | 8m |

| 25 | Intrinsic Value Fund | See notes to financial statements |

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS 1 SHARES | |

| Period ended | 8-31-06a,b |

| Per share operating performance | |

| Net asset value, beginning of period | $20.00 |

| Net investment incomeh | 0.08 |

| Net realized and unrealized | |

| gain on investments | 1.34 |

| Total from investment operations | 1.42 |

| Net asset value, end of period | $21.42 |

| Total return (%) | 7.10l,m |

| Ratios and supplemental data | |

| Net assets, end of period | |

| (in millions) | —i |

| Ratio of net expenses to average | |

| net assets (%) | 0.90r |

| Ratio of gross expenses to average | |

| net assets (%) | 1.72r |

| Ratio of net investment income | |

| to average net assets (%) | 1.85r |

| Portfolio turnover (%) | 8m |

a Class A, Class B, Class C, Class I, Class R and Class 1 shares began operations on 6-12-06.

b Unaudited.

h Based on the average of the shares outstanding.

i Less than $500,000.

l Total returns would have been lower had certain expenses not been reduced during the period shown.

m Not annualized.

r Annualized.

26 Intrinsic Value Fund See notes to financial statements

Notes to financial statements (unaudited)

1. Organization

John Hancock Intrinsic Value Fund (the “Fund”) is a newly organized non-diversified series of John Hancock Funds III (the “Trust”). The Trust was established as a Massachusetts business trust on June 9, 2005. The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end investment management company. The investment objective of the Fund is to seek long-term capital growth.

John Hancock Life Insurance Company of New York (“John Hancock New York”) is a wholly owned subsidiary of John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”). John Hancock USA and John Hancock New York are indirect wholly owned subsidiaries of The Manufacturers Life Insurance Company (“Manulife”), which in turn is a wholly owned subsidiary of Manulife Financial Corporation (“MFC”), a publicly traded company. Manulife Financial Corporation and its subsidiaries are known collectively as “Manulife Financial.”

John Hancock Investment Management Services, LLC (the “Adviser”) is the Adviser to the Trust. John Hancock Funds, LLC (the “Distributor”), a Delaware limited liability company controlled by John Hancock USA, serves as principal underwriter and is a wholly owned subsidiary of the Adviser.

Class 1 shares are sold only to certain exempt separate accounts of John Hancock USA and John Hancock New York.

The Board of Trustees has authorized the issuance of multiple classes of shares of the Fund, including classes designated as Class A, Class B, Class C, Class I, Class R and Class 1 shares. The shares of each class represent an interest in the same portfolio of investments of the Fund, and have equal rights as to voting, redemptions, dividends and liquidation, except that certain expenses, subject to the approval of the Board of Trustees, may be applied differently to each class of shares in accordance with current regulations of the Securities and Exchange Commission and the Internal Revenue Service. Shareholders of a class that bear distribution and service expenses under the terms of a distribution plan have exclusive voting rights to that distribution plan.

The Adviser and other subsidiaries of John Hancock USA owned 725,000 Class A shares, 5,000 Class B shares, 5,000 Class C shares, 5,000 Class I shares, 5,000 Class R shares and 5,000 Class 1 shares of beneficial interest of the Fund on August 31, 2006.

2. Significant accounting policies

In the preparation of the financial statements, the Fund follows the policies described below. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results may differ from these estimates.

Security valuation

The net asset value of the shares of the Fund is determined daily as of the close of the New York Stock Exchange, normally at 4:00 P.M. Eastern time. Short-term debt instruments with remaining maturities of 60 days or less are valued at amortized cost, and thereafter assume a constant amortization to maturity of any discount or premium, which approximates market value. Investments in State Street Navigator Securities Lending Prime Portfolio are valued at their net asset value each business day. All other securities held by the Fund are valued at the last sale price or official closing price (closing bid price or last evaluated quote if no sale has occurred) as of the close

27 Intrinsic Value Fund

of business on a principal securities exchange (domestic or foreign) or, lacking any sales, at the closing bid price. Securities traded only in the over-the-counter market are valued at the last bid price quoted by brokers making markets in the securities at the close of trading. Fund securities for which there are no such quotations, principally debt securities, are valued based on the valuation provided by an independent pricing service, which utilizes both dealer-supplied and electronic data processing techniques.

Other assets and securities for which no such quotations are readily available are valued at their fair value as determined in good faith under consistently applied procedures established by and under the general supervision of the Board of Trustees. Generally, trading in non-U.S. securities is substantially completed each day at various times prior to the close of trading on the New York Stock Exchange. The values of such securities used in computing the net asset value of a Fund’s shares are generally determined as of such times. Occasionally, significant events that affect the values of such securities may occur between the times at which such values are generally determined and the close of the New York Stock Exchange. In such events, these securities will then be valued at their fair value as determined in good faith under consistently applied procedures established by and under the general supervision of the Board of Trustees.

In deciding whether to make a fair value adjustment to the price of a security, the Trustees or their designee may review a variety of factors, including, developments in foreign markets, the performance of U.S. securities markets and the performance of instruments trading in U.S. markets that represent foreign securities and baskets of foreign securities. The Fund may also fair value securities in other situations, for example, when a particular foreign market is closed, but the Fund is calculating the net asset value. In view of these factors, it is likely that Fund investing significant amounts of assets in securities in foreign markets will be fair valued more frequently than a fund investing significant amounts of assets in frequently traded, U.S. exchange listed securities of large capitalization U.S. issuers.

For purposes of determining when fair value adjustments may be appropriate with respect to the Fund investing in securities in foreign markets that close prior to the New York Stock Exchange, the Fund will, on an ongoing basis, monitor for “significant market events.” A significant market event may be a certain percentage change in the value of an index or of certain exchange traded funds (“ETFs”) that track foreign markets in which the Fund has significant investments. If a significant market event occurs due to a change in the value of the index or of ETFs, the pricing for the Fund will promptly be reviewed and potential adjustments to the net asset value will be recommended to the Trust’s Pricing Committee, where applicable.

Fair value pricing of securities is intended to help ensure that the net asset value of the Fund’s shares reflects the value of the Fund’s securities as of the close of the New York Stock Exchange (as opposed to a value which is no longer accurate as of such close), thus limiting the opportunity for aggressive traders to purchase shares of the Fund at deflated prices, reflecting stale security valuations, and to promptly sell such shares at a gain. However, a security’s valuation may differ depending on the method used for determining value and no assurance can be given that fair value pricing of securities will successfully eliminate all potential opportunities for such trading gains.

Repurchase agreements

The Fund may enter into repurchase agreements. When the Fund enters into a repurchase agreement through its custodian, it receives delivery of securities, the amount of which at the time of purchase and each subsequent business day is required to be maintained at such a level that the market value is generally at least 102% of the repurchase amount. The Fund will take constructive receipt of all securities underlying the repurchase agreements it has entered into until such agreements expire. If the seller defaults, the Fund would suffer a loss to the extent that proceeds from the sale of underlying securities were less than the repurchase amount. The Fund may enter into repurchase agreements maturing within seven days with domestic

28 Intrinsic Value Fund

dealers, banks or other financial institutions deemed to be creditworthy by the Adviser. Collateral for certain tri-party repurchase agreements is held at the custodian bank in a segregated account for the benefit of the Fund and the counterparty.

Security transactions and related investment income

Investment security transactions are accounted for on a trade date plus one basis for daily net asset value calculations. However for financial reporting purposes, investment transactions are reported on trade date. Interest income is accrued as earned. Dividend income is recorded on the ex-dividend date. Foreign dividends are recorded on the ex-date or as soon after the ex-date that the Fund becomes aware of such dividends, net of all taxes. Discounts/premiums are accreted/amortized for financial reporting purposes. Non-cash dividends are recorded at the fair market value of the securities received. Debt obligations may be placed in a non-accrual status and related interest income may be reduced by ceasing current accruals and writing off interest receivables when the collection of all or a portion of interest has become doubtful, based upon consistently applied procedures.

From time to time, the Fund may invest in Real Estate Investment Trusts (“REITs”) and as a result, will estimate the components of distributions from these securities. Distributions from REITs received in excess of income are recorded as a reduction of cost of investments and/or as a realized gain.

The Fund uses the First In, First Out method for fixed income securities and Highest Cost, First Out for all other securities for determining realized gain or loss on investments for both financial and federal income tax reporting purposes.

Multi-class operations

All income, expenses (except for class-specific expenses) and realized and unrealized gains (losses) are allocated to each class of shares based upon the relative net assets of each class. Dividends to shareholders from net investment income are determined at a class level and distributions from capital gains are determined at a Fund level.

Expense allocation

Expenses are allocated based on the relative share of net assets of the Fund at the time the expense was incurred. Class-specific expenses, such as distribution (Rule 12b-1) fees, are accrued daily and charged directly to the respective share classes.

Futures

The Fund may purchase and sell financial futures contracts and options on those contracts. The Fund invests in contracts based on financial instruments such as U.S. Treasury Bonds or Notes on securities indices such as the Standard & Poor’s 500 Index (the “S&P 500 Index”), in order to hedge against a decline in the value of securities owned by the Fund.

Upon entering into futures contracts, the Fund is required to deposit with a broker an amount, termed the initial margin, which typically represents a certain percentage of the purchase price indicated in the futures contract. Payments to and from the broker, known as variation margin, are required to be made on a daily basis as the price of the futures contract fluctuates, making the long or short positions in the contract more or less valuable. If the position is closed out by taking an opposite position prior to the settlement date of the futures contract, a final determination of variation margin is made, cash is required to be paid to or released by the broker, and the Fund realizes a gain or loss.

When the Fund sells a futures contract based on a financial instrument, the Fund becomes obligated to deliver that kind of instrument at an agreed upon date for a specified price. The Fund realizes a gain or loss depending on whether the price of an offsetting purchase is less or more than the price of the initial sale or on whether the price of an offsetting sale is more or less than the price of the initial purchase. The Fund could be exposed to risks if it could not close out futures positions because of an illiquid secondary market or the inability of counterparties to meet the terms of their contracts. Futures contracts are valued at the quoted daily settlement prices established by the exchange on which they trade.

29 Intrinsic Value Fund

| The following is a summary of open futures contracts on August 31, 2006: | ||||

| NUMBER OF | UNREALIZED | |||

| OPEN CONTRACTS | CONTRACTS | POSITION | EXPIRATION | APPRECIATION |

| S&P 500 Index | 2 | Long | Sep 2006 | $15,211 |

Federal income taxes

The Fund qualifies as a “regulated investment company” by complying with the applicable provisions of the Internal Revenue Code and will not be subject to federal income tax on taxable income that is distributed to shareholders. Therefore, no federal income tax provision is required.

New accounting pronouncements

In June 2006, Financial Accounting Standards Board (“FASB”) Interpretation No. 48, Accounting for Uncertainty in Income Taxes (the “Interpretation”) was issued, and is effective for fiscal years beginning after December 15, 2006 and is to be applied to all open tax years as of the effective date. The Interpretation prescribes a minimum threshold for financial statement recognition of the benefit of a tax position taken or expected to be taken in a tax return, and requires certain expanded disclosures. Management is currently evaluating the application of the Interpretation to the Fund, and has not at this time quantified the impact, if any, resulting from the adoption of the Interpretation on the Fund’s financial statements.

In September 2006, FASB Standard No. 157, Fair Value Measurements (“FAS 157”) was issued, and is effective for fiscal years beginning after November 15, 2007. FAS 157 defines fair value, establishing a framework for measuring fair value and expands disclosure about fair value measurements. Management is currently evaluating the application of FAS 157 to the Fund, and its impact, if any, resulting from the adoption of FAS 157 on the Fund’s financial statements.

Distribution of income and gains

The Fund records distributions to shareholders from net investment income and net realized gains, if any, on the ex-dividend date. Distributions paid by the Fund with respect to each class of shares are calculated in the same manner, at the same time and are in the same amount, except for the effect of expenses that may be applied differently to each class. Such distributions, on a tax basis, are determined in conformity with income tax regulations, which may differ from accounting principles generally accepted in the United States of America. Distributions in excess of tax basis earnings and profits, if any, are reported in the Fund’s financial statements as a return of capital.

Capital accounts

The Fund reports the undistributed net investment income and accumulated undistributed net realized gain (loss) accounts on a basis approximating amounts available for future tax distributions (or to offset future taxable realized gains (loss) when a capital loss carryforward is available). Accordingly, the Fund may periodically make reclassifications among certain capital accounts without affecting its net asset value.

3. Investment advisory and other agreements Advisory fees

The Trust has entered into an Investment Advisory Agreement with the Adviser. The Adviser is responsible for managing the corporate and business affairs of the Trust and for selecting and compensating subadvisers to handle the investment and reinvestment of the assets of the Fund, subject to the supervision of the Board of Trustees. Under the Advisory Agreement the Fund pays a monthly management fee to the Adviser equivalent, on an annual basis, to the sum of: (a) 0.78% of the first $500,000,000 of the Fund’s aggregate daily net assets; (b) 0.76% of the next $500,000,000 of the Fund’s aggregate daily net assets; (c) 0.75% of the next $1,500,000,000 of the Fund’s aggregate daily net assets; and (d) 0.74% of the Fund’s aggregate daily net assets in excess of $2,500,000,000. Aggregate net assets include the net assets of the Fund

30 Intrinsic Value Fund

and Intrinsic Value Trust, a series of John Hancock Trust. John Hancock Trust is an open-end investment company advised by the Adviser and distributed by the Distributor. The Fund is not responsible for payment of the subadvisory fees.

Expense reimbursements

The Adviser has agreed contractually to reimburse for certain fund level expenses that exceed 0.08% of the average annual net assets, or to make a payment to a specific class of shares of the Fund in an amount equal to the amount by which the expenses attributable to such class of shares (excluding taxes, portfolio brokerage commissions, interest, litigation and indemnification expenses and other extraordinary expenses not incurred in the ordinary course of the Fund’s business and fees under any agreement or plans of the Fund dealing with services for shareholders and others with beneficial interests in shares of the Fund) exceed the percentage of average annual net assets (on an annualized basis) attributable as follows: 1.35% for Class A, 2.05% for Class B, 2.05% for Class C, 0.95% for Class I, 1.45% for Class R and 0.90% for Class 1. Accordingly, the expense reductions related to this expense limitation amounted to $185, $31,681, $4,340, $4,227, $4,239 and $4,498 for Class A, Class B, Class C, Class I, Class R and Class 1, respectively, for the period ended August 31, 2006. This expense reimbursement shall continue in effect until June 30, 2007 and thereafter until terminated by the Adviser on notice to the Trust.

Administration fees

The Fund has an agreement with the Adviser that requires the Fund to reimburse the Adviser for all expenses associated with providing the administrative, financial, accounting and recordkeeping services of the Fund, including the preparation of all tax returns, annual, semi-annual and periodic reports to shareholders and the preparation of all regulatory reports.

Distribution plan

The Trust has a Distribution Agreement with the Distributor, a wholly owned subsidiary of the Adviser. The Fund has adopted Distribution Plans with respect to Class A, Class B, Class C, Class R and Class 1, pursuant to Rule 12b-1 under the 1940 Act, to reimburse the Distributor for the services it provides as distributor of shares of the Fund. Accordingly, the Fund makes monthly payments to the Distributor at an annual rate not to exceed 0.30%, 1.00%, 1.00%, 0.50% and 0.05% of average daily net asset value of Class A, Class B, Class C, Class R and Class 1, respectively. A maximum of 0.25% of such payments may be service fees, as defined by the Conduct Rules of the National Association of Securities Dealers. Under the Conduct Rules, curtailment of a portion of the Fund’s 12b-1 payments could occur under certain circumstances. In addition, under a Service Plan for Class R shares, the Fund pays up to 0.25% of Class R average daily n et asset value for certain other services.

Sales charges

Class A shares are assessed up-front sales charges of up to 5.00% of net asset value of such shares. During the period ended August 31, 2006, the Fund was informed that the Distributor received net up-front sales charges of $7,127 with regard to sales of Class A shares. Of this amount, $1,242 was retained and used for printing prospectuses, advertising, sales literature and other purposes, $5,885 was paid as sales commissions to unrelated broker-dealers.

Class B shares that are redeemed within six years of purchase are subject to a contingent deferred sales charge (“CDSC”) at declining rates, beginning at 5.00% of the lesser of the current market value at the time of redemption or the original purchase cost of the shares being redeemed. Class C shares that are redeemed within one year of purchase are subject to a CDSC at a rate of 1.00% of the lesser of the current market value at the time of redemption or the original purchase cost of the shares being redeemed. Proceeds from the CDSCs are paid to the Distributor and are used, in whole or in part, to defray its expenses for providing distribution-related services to the Fund in connection with the sale of Class B and Class C shares. During the period ended August 31, 2006, the Fund was informed that the Distributor received no CDSCs for Class B and Class C shares.

31 Intrinsic Value Fund

Transfer agent fees

The Fund has a Transfer Agency Agreement with John Hancock Signature Services, Inc. (“Signature Services”), an indirect subsidiary of MFC. For Class A, Class B, Class C, Class I and Class R shares, the Fund pays a monthly transfer agent fee at an annual rate of 0.05% of each class’s average daily net assets, plus a fee based on the number of shareholder accounts and reimbursement for certain out-of-pocket expenses. Expenses not directly attributable to a particular class of shares are aggregated and allocated to each class on the basis of its relative net asset value.

Signature Services has agreed to limit the transfer agent fees so that such fees do not exceed 0.20% annually of Class A, Class B, Class C, Class I and Class R share average daily net assets. This agreement is effective until December 31, 2006. Signature Services reserves the right to terminate this limitation in the future. Accordingly, there were no transfer agent fees reductions for Class A, Class B, Class C, Class I and Class R shares, respectively, during the period ended August 31, 2006.

| Expenses under the agreements described above for the period ended August 31, 2006, were as follows: | ||||

| Distribution and | Transfer | Printing and | ||

| Share Class | service fees | agent | Blue sky | postage |

| Class A | $9,950 | $6,634 | $4,276 | $4,705 |

| Class B | 299 | 60 | 4,032 | 37 |

| Class C | 356 | 71 | 4,032 | 39 |

| Class I | — | 12 | 4,032 | 36 |

| Class R | 168 | 45 | 4,032 | 32 |

| Class 1 | 11 | — | — | 32 |

| Total | $10,784 | $6,822 | $20,404 | $4,881 |

Trustees’ fees

The Trust compensates each Trustee who is not an employee of the Adviser or its affiliates. Total Trustees’ expenses are allocated to the Fund based on its average daily net asset value.

4. Guarantees and indemnifications

Under the Trust’s organizational documents, its Officers and Trustees are indemnified against certain liability arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred. However, based on experience, the Trust believes the risk of loss to be remote.

5. Line of credit

The Fund has entered into an agreement which enables them to participate in a $100 million unsecured committed line of credit with State Street Bank & Trust Company. Borrowings will be made solely to temporarily finance the repurchase of capital shares. Interest is charged to the Fund based on its borrowings at a rate per annum equal to the Federal Funds rate plus 0.50% . In addition, a commitment fee of 0.07% per annum, payable at the end of each calendar quarter, based on the average daily-unused portion of the line of credit, is charged to the Fund on a prorated basis based on average net assets. For the period ended August 31, 2006 there was no borrowings under the line of credit.

32 Intrinsic Value Fund

6. Capital shares

Share activities for the Fund for the period ended August 31, 2006 were as follows:

| Period ended 8-31-06a | ||

| Shares | Amount | |

| Class A shares | ||

| Sold | 745,482 | $14,923,582 |

| Repurchased | (496) | (10,305) |

| Net increase (decrease) | 744,986 | $14,914,277 |

| Class B shares | ||

| Sold | 9,861 | $201,789 |

| Net increase (decrease) | 9,861 | $201,789 |

| Class C shares | ||

| Sold | 13,237 | $270,047 |

| Net increase (decrease) | 13,237 | $270,047 |

| Class I shares | ||

| Sold | 5,547 | $111,000 |

| Net increase (decrease) | 5,547 | $111,000 |

| Class R shares | ||

| Sold | 5,000 | $100,000 |

| Net increase (decrease) | 5,000 | $100,000 |

| Class 1 shares | ||

| Sold | 5,000 | $100,000 |

| Net increase (decrease) | 5,000 | $100,000 |

| Net increase (decrease) | 783,631 | $15,696,113 |

| aPeriod from 6-12-06 (commencement of operations) to 8-31-06. Unaudited. | ||

33 Intrinsic Value Fund

7. Investment transactions

Purchases and proceeds from sales or maturities of securities, other than short- term securities and obligations of the U.S. government, during the period ended August 31, 2006, aggregated $15,887,543 and $1,155,191, respectively.

The cost of investments owned on August 31, 2006, including short-term investments, for federal income tax purposes, was $15,676,702. Gross unrealized appreciation and depreciation of investments aggregated $1,175,580 and $226,064, respectively, resulting in net unrealized appreciation of $949,516.

8. Federal income tax information

Federal income tax regulations may differ from generally accepted accounting principles and income and capital gain distributions determined in accordance with tax regulations may differ from net investment income and realized gains recognized for financial reporting purposes.

34 Intrinsic Value Fund

Evaluation of Advisory and Subadvisory Agreements by the Board of Trustees

This section describes the evaluation by the Board of Trustees of the Advisory Agreement and each of the Subadvisory Agreements.

Evaluation by the Board of Trustees The Board, including all of the Trustees who are not “interested persons” as defined in the Investment Company Act of 1940, as amended (the “Independent Trustees”), is responsible for selecting the Trust’s investment adviser, John Hancock Investment Management Services, LLC (the “Adviser” or “JHIMS”), approving the Adviser’s selection of subadvisers for each series of the Trust (the “Funds”) and approving the Trust’s advisory and sub-advisory agreements (and any sub-subadvisory agreements), their periodic continuation and any amendments. Consistent with SEC rules, the Board regularly evaluates the Trust’s advisory and subadvisory (and sub-subadvisory) arrangements, including consideration of the factors listed below. The Board may also consider other factors (including conditions and trends prevailing generally in the econom y, the securities markets and the industry) and does not treat any single factor as determinative, and each Trustee may attribute different weights to different factors. The Board is furnished with an analysis of its fiduciary obligations in connection with its evaluation and, throughout the evaluation process, the Board is assisted by counsel for the Trust and the Independent Trustees are also separately assisted by independent legal counsel. The factors regularly considered by the Board are:

1. the nature, extent and quality of the services to be provided by the Adviser to the Trust and by the subadvisers to the Funds;

2. the investment performance of the Funds and their subadvisers;

3. the extent to which economies of scale would be realized as a Fund grows and whether fee levels reflect these economies of scale for the benefit of Trust shareholders;

4. the costs of the services to be provided and the profits to be realized by the Adviser and its affiliates (including any subadvisers that are affiliated with the Adviser) from the Adviser’s relationship with the Trust; and

5. comparative services rendered and comparative advisory and subadvisory fee rates.

The Board believes that information relating to all these factors is relevant to its evaluation of the Trust’s advisory agreement. With respect to its evaluation of subadvisory agreements (including sub-subadvisory agreements) the Board believes that, in view of the Trust’s “manager-of managers” advisory structure, the costs of services to be provided and the profits to be realized by those subadvisers that are not affiliated with the Adviser from their relationship with the Trust generally are not a material factor to the Board’s consideration of subadvisory agreements because such fees are paid to sub-advisers by the Adviser and not by the Funds, and because the Board relies on the ability of the Adviser to negotiate such subadvisory fees at arms-length.

In evaluating subadvisory arrangements, the Board also considers other material business relationships that unaffiliated sub-advisers and their affiliates have with the Adviser or its affiliates, including the involvement by certain affiliates of certain subadvisers in the distribution of financial products, including shares of the Trust, offered by the Adviser and other affiliates of the Adviser (“Material Relationships”).

Approval of Advisory Agreement

At its meeting on September 21, 2005, the Board, including all the Independent Trustees, approved the Advisory Agreement between the Trust and JHIMS with respect to each of the Funds.

In approving the Advisory Agreement, and with reference to the factors which it regularly considers, the Board:

(1) (a) considered the high value to the Trust of continuing the relationship with JHIMS as the Trust’s Adviser to the other John Hancock Funds, the skills and competency with which JHIMS

35

has in the past managed the affairs and subadvisory relationships of other funds in the complex, JHIMS’s oversight and monitoring of subadvisers’ investment performance and compliance programs including its timelines in responding to performance issues and the qualifications of JHIMS’s personnel,

(b) considered JHIMS’s compliance policies and procedures and its responsiveness to regulatory changes and mutual fund industry developments, and

(c) JHIMS’s administrative capabilities, including its ability to supervise the other service providers for the Funds and concluded that JHIMS may reasonably be expected to ably perform its services under the Advisory Agreement.

(2) reviewed the investment performance of portfolios that are managed comparable to the Funds; the comparative performance of their respective benchmarks; and JHIMS’ analysis of such performance and its plans and recommendations regarding the Trust’s subadvisory arrangements generally and with respect to the Funds; and concluded that each of the comparably managed funds has performed well or within a range that the Board deemed competitive, and that JHIMS may reasonably be expected to ably monitor the performance of the Funds and their subadvisers;

(3) reviewed the Trust’s advisory fee structure and the incorporation therein of any subadvisory fee breakpoints in the advisory fees charged and concluded (i) that to the extent that Funds have subadvisory fees with breakpoints, those breakpoints are reflected as breakpoints in the advisory fees for Funds, (ii) that all Funds with a subadviser that is not affiliated with the Adviser have subadvisory fees which are the product of arms-length negotiations between the Adviser and the subadviser and which in many, but not all, cases contain breakpoints, and (iii) that, although economies of scale cannot be measured with precision, these arrangements permit shareholders of Funds with advisory fee breakpoints to benefit from economies of scale if those Funds grow;

(4) (a) reviewed the financial statements of JHIMS and John Hancock Life Insurance Company (U.S.A.) (“JHLICO (U.S.A.)”;

(b) reviewed the anticipated profitability of the JHIMS’s relationship with the Funds in terms of the fees it expects to receive with respect to the Funds and whether JHIMS has the financial ability to provide a high level of services to the Funds,

(c) considered that JHIMS derives reputational and other indirect benefits from providing advisory services to the Funds, and

(d) noted that JHIMS will pay the sub-advisory fees out of the advisory fees JHIMS receives from the Funds and concluded that the advisory fees paid by the Trust with respect to the Funds are not unreasonable in light of such information; and

(5) reviewed comparative information with respect to the advisory fee rates and concluded that the anticipated advisory fees for the Funds are within the range of those incurred by other comparable funds and that the advisory structure for the Funds is thus competitive within the industry.