UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21777

John Hancock Funds III

(Exact name of registrant as specified in charter)

601 Congress Street, Boston, Massachusetts 02210

(Address of principal executive offices) (Zip code)

Gordon M. Shone

Treasurer

601 Congress Street

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-663-3000

| Date of fiscal year end: | February 28 |

| Date of reporting period: | August 31, 2007 |

ITEM 1. REPORT TO SHAREHOLDERS.

| TABLE OF CONTENTS | ||

| Your fund at a glance | ||

| page 1 | ||

| Managers’ report | ||

| page 2 | ||

| A look at performance | ||

| page 6 | ||

| Your expenses | ||

| page 8 | ||

| Fund’s investments | ||

| page 10 | ||

| Financial statements | ||

| page 18 | ||

| Notes to financial | ||

| statements | ||

| page 28 | ||

| For more information | ||

| page 40 | ||

CEO corner

To Our Shareholders,

Volatility returned to the U.S. stock market in the six-month period ended August 31, 2007; however, stocks still posted a strong gain of 5.70%, as measured by the Standard & Poor’s 500 Index. The market experienced a particularly sharp downturn in August, as the subprime mortgage market’s woes increased. Rising defaults and an ensuing credit crunch caused heightened fears about their potential impact on U.S. economic growth. Foreign markets felt some ripple effects from the subprime issue, but they continued nonetheless to benefit from solid economic growth and outperformed the U.S. market in this period.

During this period of volatility, the U.S. stock market also passed a significant milestone — the broad Standard & Poor’s 500 Index climbed beyond the record it had set seven years ago. From its peak in March 2000, the stock market spiraled downward three consecutive years, bottoming in 2002. The upturn began in 2003, and the market has advanced each year since, finally setting a new high for the first time on May 30, 2007. During that period, the S&P 500 Index experienced five significant short-term sell-offs of 6% or more, with the August subprime-induced meltdown being the most recent.

This nearly complete market cycle highlights the importance of two investment principles you have heard us speak of often: diversification and patience. By allocating your investments among different asset classes, investment styles and portfolio managers, you are likely to be well represented through all phases of a complete market cycle, with the winners helping to cushion the fall of the losers.

The challenge for investors with a diversified portfolio is to properly evaluate your investments to tell the difference between an underperforming manager and an out-of-favor style, while also understanding the role each investment plays in your portfolio. That’s where your financial professional can provide true value. He or she can help you make those assessments and also counsel patience, because a properly diversified portfolio by its very nature will typically have something lagging or out of favor — a concept that can be difficult to live with, but necessary to embrace. If everything in your portfolio is “working,” then you are not truly diversified, but rather are leveraged to the current market and the flavor of the day. If so, you are bound to be out of step in the near future.

The recent volatility in the securities markets has prompted many investors to question how long this type of market cycle will last. History tells us it will indeed end and that when it does, today’s leaders may well turn into laggards and vice versa. The subprime mortgage market woes are just the latest example of why investors should be both patient and well-diversified. For with patience and a diversified portfolio, it could be easier to weather the market’s twists and turns and reach your long-term goals.

Sincerely,

Keith F. Hartstein,

President and Chief Executive Officer

This commentary reflects the CEO’s views as of August 31, 2007. They are subject to change at any time.

Your fund at a glance

The Fund seeks long-term capital growth by typically investing in U.S. companies that issue stocks included in the Russell 1000 Index and in companies with size and value characteristics similar to those of companies with stocks in the Index.

Over the last six months

► Despite heightened volatility, the broad U.S. market, as measured by the S&P 500 Index, gained ground.

► The services, retail and manufacturing sectors detracted from Fund performance, while technology and financials added value.

► The Fund's momentum discipline was able to capitalize on the rising broad market.

| Top 10 holdings | ||||

| Exxon Mobil Corp. | 7.9% | Home Depot, Inc. | 2.7% | |

| Citigroup, Inc. | 4.7% | Chevron Corp. | 2.7% | |

| Verizon Communications, Inc. | 3.7% | Federal National Mortgage Assn. | 2.4% | |

| Pfizer, Inc. | 3.5% | AT&T, Inc. | 2.4% | |

| Merck & Company, Inc. | 3.1% | Wal-Mart Stores, Inc. | 2.2% | |

As a percentage of net assets on August 31, 2007.

1

Managers’ report

John Hancock

Intrinsic Value Fund

U.S. investors entered the six-month review period on March 1, 2007 still reeling from the market’s late-February swoon. Their big question was whether the recent fall was the beginning of a major correction or just a brief hiccup in the middle of a bull market. Though some of the concerns surrounding the decline — including the first sign of trouble in subprime mortgages — were still present, investors appeared to shake them off. Less than two months into the review period, the Standard & Poor’s 500 Index had recovered all of its lost ground, entering the summer poised to continue its ascent. With historically-low market volatility, the continuation of strong corporate profits and a glut of private equity deals fueled by ubiquitous financial liquidity, there seemed to be almost no ceiling to the market’s potential. Hopes for a smooth summer, however, would turn out to be short-lived.

Beginning in July, as many market indexes touched record highs, credit concerns similar to those seen in February flared up again. Distress in subprime mortgages quickly spilled over into the broader credit and equity markets. Just weeks after the S&P 500 Index set an all-time high, the Federal Reserve began injecting liquidity into a faltering financial system in an attempt to stem the turmoil taking place in the credit market. As equity market volatility returned with a vengeance, investor tolerance for risk abated and the broad market indexes plunged lower in the first days of August. And while hopes for a Federal Reserve rate

SCORECARD

| INVESTMENT | PERIOD’S PERFORMANCE ... AND WHAT’S BEHIND THE NUMBERS | ||

| Exxon Mobil | ▲ | Benefited from rising oil prices over the period | |

| Forest Laboratories | ▼ | Promising stroke medication failed late-stage trials | |

| Kohl’s | ▼ | Fund’s overweight position hurt when same-store sales declined | |

2

From the Grantham, Mayo, Van Otterloo & Co. LLC (GMO)

Portfolio Management Team

cut helped stabilize things somewhat, investors ended the review period much in the same way they began it — wondering whether the market would rally again or if risk aversion was here to stay. Despite the volatility, the S&P 500 Index posted gains in the six-month period.

Looking at performance

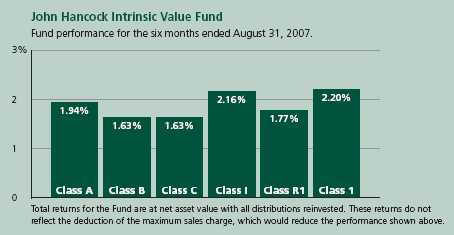

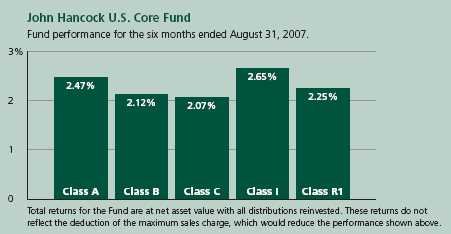

For the six months ended August 31, 2007, John Hancock Intrinsic Value Fund’s Class A, Class B, Class C, Class I, Class R1 and Class 1 shares returned 1.94%, 1.63%, 1.63%, 2.16%, 1.77% and 2.20%, respectively, at net asset value. By comparison, the Russell 1000 Value Index returned 2.76%, while the average large value fund monitored by Morningstar, Inc. gained 3.81% .1 Keep in mind that your returns will differ from those listed above if you were not invested in the Fund for the entire period or did not reinvest all distributions. See pages six and seven for historical performance information.

“Despite the volatility, the S&P

500 Index posted gains in the

six-month period.”

In a generally rising market, our primary stock selection tools — valuation and momentum — performed differently. Valuation, which determines the positioning for the majority of this Fund’s assets, was the key driver of the relative performance shortfall. The late-period market turmoil notwithstanding, the period as a whole was dominated by strong investor appetite for risky, lower-quality stocks — securities that our valuation discipline found overvalued. The lower-risk, higher-quality securities that our valuation discipline found attractive underperformed for much of the period in a risk-oriented market. While these higher-quality selections fared better later in the period as risk aversion returned, they still finished the period in negative territory.

Intrinsic Value Fund

3

Our momentum discipline was able to capitalize on the rising broad market. The discipline is designed to identify stocks that have performed well recently and appear poised to continue outperforming. With this orientation, the momentum discipline was able to add value during the period by selecting many of the leading performers and following their outperformance. The discipline also benefited from its underweight position in financial company stocks, leaving it less exposed to the spreading troubles from subprime mortgages.

Services, retail and manufacturing limit gains

The sector detracting most from performance during the period was services, where our stock selection negatively impacted the Fund’s returns. For example, an overweight position in Gannett Company, Inc. detracted from relative returns as shares fell after an earnings report triggered worries about the state of the company’s newspaper business. Our valuation model continues to find the company attractive and maintains its overweight position.

Retail was another sector detracting from the Fund’s performance because of our overweight position. For example, an overweight position in Wal-Mart Stores, Inc. detracted from relative returns as shares fell amid short-term concerns about a lower quarterly profit report. Home Depot, Inc. also struggled during the period, as worries about weakness in the housing sector sent shares lower. Our valuation model continues to find each of these high-quality companies attractive and maintains overweight positions in both.

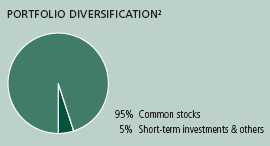

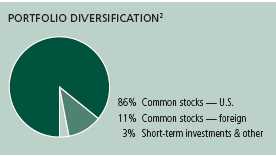

| SECTOR DISTRIBUTION2 | |

| Financial | 23% |

| Consumer non-cyclical | 18% |

| Consumer cyclical | 16% |

| Energy | 13% |

| Communications | 10% |

| Technology | 5% |

| Industrial | 4% |

| Government | 2% |

| Basic materials | 2% |

| Mortgage securities | 1% |

Also detracting from performance was the manufacturing sector. Our underweight position drove the negative relative returns. An underweight in General Electric Company was particularly detrimental, as the company’s shares advanced during the period after it reported strong quarterly earnings and increased its stock buyback plan.

Technology and financials add value

On the positive side, our aversion to risky companies did pay off in certain sectors. In particular, as we mentioned earlier, our underweight position in the financial sector was helpful to returns, as we were able to add value during the period

Intrinsic Value Fund

4

by owning less of this risky sector as troubles in the credit market stemming from subprime mortgages drove financial shares lower. For example, having either underweighted or no positions in JPMorgan Chase & Company and Lehman Brothers Holdings added value in a period in which investors sold off financial companies. Though some of our financial holdings, like National City Corp., detracted from returns, the underweight position made this sector a strong contributor to overall relative returns. Another sector adding to relative returns was technology, where strong stock selection helped add value. One strong performer was our overweight of Intel Corp., as the company’s shares rose during a period in which large-cap technology stocks were among the market leaders.

“Valuation, which determines

the positioning for the majority

of this Fund’s assets, was

the key driver of the relative

performance shortfall.”

Outlook

The market volatility at the end of the period left investors wondering if the bull market has finally come to an end. The upcoming months will show whether the market’s recent trend toward risk aversion — especially in the troubled sub-prime mortgage sector — will persist or if risk-taking will resume in full force. The Fund remains overweight in higher-quality stocks and we believe it is well positioned to face further volatility in the market.

This commentary reflects the views of the portfolio management team through the end of the Fund’s period discussed in this report. The team’s statements reflect their own opinions. As such, they are in no way guarantees of future events and are not intended to be used as investment advice or a recommendation regarding any specific security. They are also subject to change at any time as market and other conditions warrant.

1 Figures from Morningstar, Inc. include reinvested dividends and do not take into account sales charges. Actual load-adjusted performance is lower.

2 As a percentage of net assets on August 31, 2007.

Intrinsic Value Fund

5

A look at performance

For the periods ended August 31, 2007

| Average annual returns | Cumulative total returns | |||||||||

| with maximum sales charge (POP) | with maximum sales charge (POP) | |||||||||

| Inception | Since | Since | ||||||||

| Class | date | 1-year | 5-year | 10-year | inception | 6-month | 1-year | 5-year | 10-year | inception |

| A | 6-12-06 | 4.28% | — | — | 9.33% | –3.14% | 4.28% | — | — | 11.57% |

| B | 6-12-06 | 4.02 | — | — | 10.06 | –3.37 | 4.02 | — | — | 12.49 |

| C | 6-12-06 | 8.07 | — | — | 13.24 | 0.63 | 8.07 | — | — | 16.49 |

| I1 | 6-12-06 | 10.23 | — | — | 14.43 | 2.16 | 10.23 | — | — | 18.00 |

| R1 1 | 6-12-06 | 9.37 | — | — | 13.58 | 1.77 | 9.37 | — | — | 16.91 |

| 11 | 6-12-06 | 10.25 | — | — | 14.50 | 2.20 | 10.25 | — | — | 18.07 |

Performance figures assume all distributions are reinvested. Public offering price (POP) figures reflect maximum sales charge on Class A shares of 5%, and the applicable contingent deferred sales charge (CDSC) on Class B and Class C shares. The Class B shares’ CDSC declines annually between years 1 to 6 according to the following schedule 5, 4, 3, 3, 2, 1%. No sales charge will be assessed after the sixth year. Class C shares held for less than one year are subject to a 1% CDSC. Sales charge is not applicable for Class I, Class R1 and Class 1 shares.

The expense ratios of the Fund, both net (including any fee waivers or expense limitations) and gross (excluding any fee waivers or expense limitations), are set forth according to the most recent publicly available Prospectuses for the Fund and may differ from the expense ratios disclosed in the Financial Highlights tables in this report. The waivers and expense limitations are contractual at least until 6-30-08. The net expenses are as follows: Class A — 1.34%, Class B — 2.04%, Class C — 2.04%, Class I — 0.95%, Class R1 — 1.69%, Class 1 — 0.90% . Had the fee waivers and expense limitations not been in place, the gross expenses would be as follows: Class A — 1.94%, Class B — 9.00%, Class C — 10.08%, Class I — 17.60%, Class R1 — 20.85%, Class 1 — 1.44% .

The returns reflect past results and should not be considered indicative of future performance. The return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Due to market volatility, the Fund’s current performance may be higher or lower than the performance shown. For performance data current to the most recent month-end, please call 1-800-225-5291 or visit the Fund’s Web site at www.jhfunds.com.

The performance table above and the chart on the next page do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Fund’s performance results reflect any applicable expense reductions, without which the expenses increase and results would have been less favorable.

Performance is calculated with an opening price (prior day’s close) on the inception date.

1 For certain types of investors as described in the Fund’s Class I, Class R1 and Class 1 share prospectuses.

Intrinsic Value Fund

6

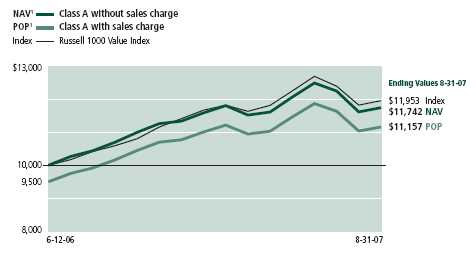

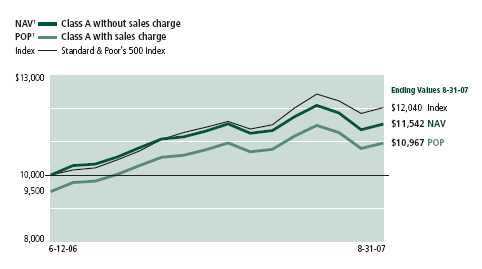

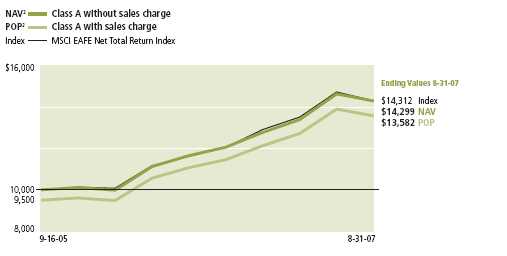

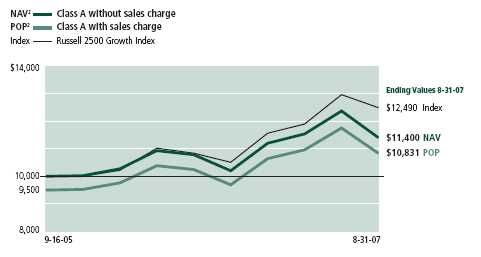

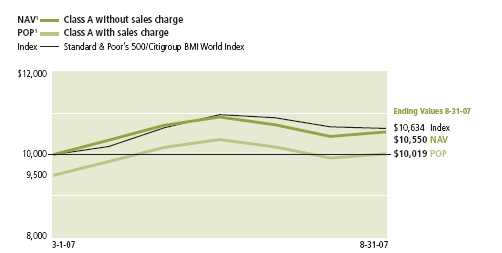

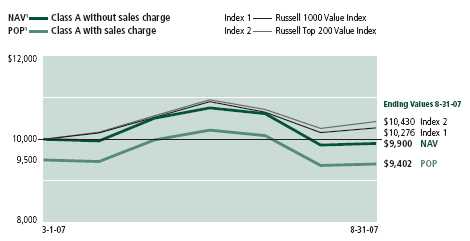

Growth of $10,000

This chart shows what happened to a hypothetical $10,000 investment in Intrinsic Value Fund Class A shares for the period indicated. For comparison, we’ve shown the same investment in the Russell 1000 Value Index.

| With maximum | ||||

| Class | Period beginning | Without sales charge | sales charge | Index |

| B | 6-12-06 | $11,649 | $11,249 | $11,953 |

| C2 | 6-12-06 | 11,649 | 11,649 | 11,953 |

| I3 | 6-12-06 | 11,800 | 11,800 | 11,953 |

| R1 3 | 6-12-06 | 11,691 | 11,691 | 11,953 |

| 13 | 6-12-06 | 11,807 | 11,807 | 11,953 |

Assuming all distributions were reinvested for the period indicated, the table above shows the value of a $10,000 investment in the Fund’s Class B, Class C, Class I, Class R1 and Class 1 shares, respectively, as of August 31, 2007. Performance of the classes will vary based on the difference in sales charges paid by shareholders investing in the different classes and the fee structure of those classes.

Russell 1000 Value Index is an unmanaged index containing those securities in the Russell 1000 Index with a less-than-average growth orientation.

It is not possible to invest directly in an index. Index figures do not reflect sales charges, which would have resulted in lower values if they did.

1 NAV represents net asset value and POP represents public offering price.

2 No contingent deferred sales charge applicable.

3 For certain types of investors as described in the Fund’s Class I, Class R1 and Class 1 share prospectuses.

Intrinsic Value Fund

7

Your expenses

These examples are intended to help you understand your ongoing operating expenses.

Understanding fund expenses

As a shareholder of the Fund, you incur two types of costs:

■ Transaction costs which include sales charges (loads) on purchases or redemptions (varies by share class), minimum account fee charge, etc.

■ Ongoing operating expenses including management fees, distribution and service fees (if applicable) and other fund expenses.

We are going to present only your ongoing operating expenses here.

Actual expenses/actual returns

This example is intended to provide information about your fund’s actual ongoing operating expenses, and is based on your fund’s actual return. It assumes an account value of $1,000.00 on March 1, 2007, with the same investment held until August 31, 2007.

| Account value | Ending value | Expenses paid during period | |

| on 3-1-07 | on 8-31-07 | ended 8-31-071 | |

| Class A | $1,000.00 | $1,019.40 | $6.85 |

| Class B | 1,000.00 | 1,016.30 | 10.44 |

| Class C | 1,000.00 | 1,016.30 | 10.44 |

| Class I | 1,000.00 | 1,021.60 | 4.83 |

| Class R1 | 1,000.00 | 1,017.70 | 8.67 |

| Class 1 | 1,000.00 | 1,022.00 | 4.57 |

Together with the value of your account, you may use this information to estimate the operating expenses that you paid over the period. Simply divide your account value at August 31, 2007 by $1,000.00, then multiply it by the “expenses paid” for your share class from the table above. For example, for an account value of $8,600.00, the operating expenses should be calculated as follows:

Intrinsic Value Fund

8

Hypothetical example for comparison purposes

This table allows you to compare your fund’s ongoing operating expenses with those of any other fund. It provides an example of the Fund’s hypothetical account values and hypothetical expenses based on each class’s actual expense ratio and an assumed 5% annualized return before expenses (which is not your fund’s actual return). It assumes an account value of $1,000.00 on March 1, 2007, with the same investment held until August 31, 2007. Look in any other fund shareholder report to find its hypothetical example and you will be able to compare these expenses.

| Account value | Ending value | Expenses paid during period | |

| on 3-1-07 | on 8-31-07 | ended 8-31-07 1 | |

| Class A | $1,000.00 | $1,018.35 | $6.85 |

| Class B | 1,000.00 | 1,014.78 | 10.43 |

| Class C | 1,000.00 | 1,014.78 | 10.43 |

| Class I | 1,000.00 | 1,020.36 | 4.82 |

| Class R1 | 1,000.00 | 1,016.54 | 8.67 |

| Class 1 | 1,000.00 | 1,020.61 | 4.57 |

Remember, these examples do not include any transaction costs, such as sales charges; therefore, these examples will not help you to determine the relative total costs of owning different funds. If transaction costs were included, your expenses would have been higher. See the prospectus for details regarding transaction costs.

1 Expenses are equal to the Fund’s annualized expense ratio of 1.35%, 2.06%, 2.06%, 0.95%, 1.71% and 0.90% for Class A, Class B, Class C, Class I, Class R1, and Class 1 respectively, multiplied by the average account value over the period, multiplied by the number of days in the inception period /365 or 366 (to reflect the one-half year period).

Intrinsic Value Fund

9

F I N A N C I A L S T A T E M E N T S

Fund’s investments

Securities owned by the Fund on 8-31-07 (unaudited)

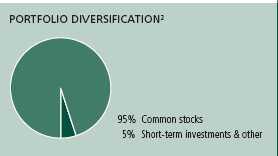

This schedule is divided into three main categories: common stocks, short-term investments and repurchase agreements. Common stocks are further broken down by industry group. Repurchase agreements, which represent the Fund’s cash position, are listed last.

| Issuer | Shares | Value |

| Common stocks 95.95% | $20,591,726 | |

| (Cost $19,365,375) | ||

| Aerospace 0.56% | 120,698 | |

| General Dynamics Corp. | 700 | 54,992 |

| Northrop Grumman Corp. | 600 | 47,304 |

| Raytheon Company | 300 | 18,402 |

| Aluminum 0.15% | 32,877 | |

| Alcoa, Inc. | 900 | 32,877 |

| Apparel & Textiles 1.14% | 245,012 | |

| Cintas Corp. | 300 | 10,995 |

| Coach, Inc. * | 400 | 17,812 |

| Jones Apparel Group, Inc. | 1,400 | 26,866 |

| Liz Claiborne, Inc. | 1,800 | 61,506 |

| Mohawk Industries, Inc. * | 200 | 17,462 |

| NIKE, Inc., Class B | 400 | 22,536 |

| VF Corp. | 1,100 | 87,835 |

| Auto Parts 0.53% | 114,132 | |

| Autoliv, Inc. | 500 | 28,685 |

| AutoZone, Inc. * | 300 | 36,387 |

| Johnson Controls, Inc. | 200 | 22,620 |

| O’Reilly Automotive, Inc. * | 400 | 14,216 |

| TRW Automotive Holdings Corp. * | 400 | 12,224 |

| Auto Services 0.42% | 90,909 | |

| AutoNation, Inc. * | 3,200 | 60,736 |

| Avis Budget Group, Inc. * | 1,300 | 30,173 |

| Automobiles 1.90% | 407,657 | |

| Ford Motor Company * | 23,000 | 179,630 |

| General Motors Corp. | 3,800 | 116,812 |

| PACCAR, Inc. | 1,300 | 111,215 |

| Banking 5.43% | 1,165,229 | |

| Bank of America Corp. | 8,600 | 435,848 |

| BB&T Corp. | 2,200 | 87,406 |

| Comerica, Inc. | 2,200 | 122,716 |

See notes to financial statements

Intrinsic Value Fund

10

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Banking (continued) | ||

| Downey Financial Corp. | 200 | $11,318 |

| Fifth Third Bancorp | 1,100 | 39,259 |

| First Horizon National Corp. (a) | 1,400 | 42,952 |

| Huntington BancShares, Inc. | 1,000 | 17,210 |

| KeyCorp | 2,500 | 83,250 |

| National City Corp. | 8,000 | 215,280 |

| US Bancorp | 3,400 | 109,990 |

| Broadcasting 0.66% | 141,621 | |

| CBS Corp., Class B | 3,200 | 100,832 |

| Liberty Media Corp. — Capital, Series A * | 300 | 32,697 |

| News Corp., Class A | 400 | 8,092 |

| Building Materials & Construction 0.41% | 87,588 | |

| American Standard Companies, Inc. | 400 | 14,732 |

| Masco Corp. | 2,800 | 72,856 |

| Business Services 0.94% | 201,495 | |

| Affiliated Computer Services, Inc., Class A * | 500 | 25,015 |

| Computer Sciences Corp. * | 500 | 27,975 |

| First Data Corp. | 1,200 | 39,864 |

| Fiserv, Inc. * | 600 | 27,912 |

| Moody’s Corp. | 200 | 9,170 |

| NCR Corp. * | 200 | 9,954 |

| Pitney Bowes, Inc. | 700 | 31,269 |

| R.R. Donnelley & Sons Company | 600 | 21,492 |

| Unisys Corp. * | 1,200 | 8,844 |

| Cable and Television 1.13% | 241,610 | |

| Comcast Corp., Class A * | 3,950 | 103,056 |

| Time Warner, Inc. | 7,300 | 138,554 |

| Chemicals 1.17% | 251,263 | |

| Albemarle Corp. | 600 | 24,282 |

| Dow Chemical Company | 1,900 | 80,997 |

| Eastman Chemical Company | 400 | 26,704 |

| Lubrizol Corp. | 200 | 12,716 |

| Lyondell Chemical Company | 400 | 18,544 |

| PPG Industries, Inc. | 1,200 | 88,020 |

| Colleges & Universities 0.33% | 70,650 | |

| Career Education Corp. * | 900 | 26,730 |

| ITT Educational Services, Inc. * | 400 | 43,920 |

| Computers & Business Equipment 3.14% | 674,224 | |

| CDW Corp. * | 200 | 17,214 |

| Cisco Systems, Inc. * | 2,700 | 86,184 |

| Dell, Inc. * | 5,300 | 149,725 |

| EMC Corp. * | 2,900 | 57,014 |

See notes to financial statements

Intrinsic Value Fund

11

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Computers & Business Equipment (continued) | ||

| Hewlett-Packard Company | 1,800 | $88,830 |

| Ingram Micro, Inc., Class A * | 1,600 | 31,424 |

| International Business Machines Corp. (a) | 1,500 | 175,035 |

| Lexmark International, Inc. * | 800 | 29,808 |

| Tech Data Corp. * | 1,000 | 38,990 |

| Construction Materials 0.21% | 45,743 | |

| Louisiana-Pacific Corp. (a) | 600 | 11,238 |

| Sherwin-Williams Company | 500 | 34,505 |

| Cosmetics & Toiletries 0.34% | 73,198 | |

| International Flavors & Fragrances, Inc. | 500 | 25,115 |

| Kimberly-Clark Corp. | 700 | 48,083 |

| Crude Petroleum & Natural Gas 0.70% | 149,318 | |

| Apache Corp. | 400 | 30,952 |

| Devon Energy Corp. | 700 | 52,717 |

| Occidental Petroleum Corp. | 900 | 51,021 |

| Sunoco, Inc. | 200 | 14,628 |

| Electrical Utilities 1.05% | 225,075 | |

| American Electric Power Company, Inc. | 1,200 | 53,376 |

| CenterPoint Energy, Inc. (a) | 600 | 9,732 |

| CMS Energy Corp. | 600 | 9,792 |

| Edison International | 500 | 26,355 |

| Entergy Corp. | 900 | 93,258 |

| Pinnacle West Capital Corp. | 300 | 11,952 |

| Xcel Energy, Inc. | 1,000 | 20,610 |

| Electronics 0.31% | 66,990 | |

| Arrow Electronics, Inc. * | 400 | 16,784 |

| Avnet, Inc. * | 600 | 23,586 |

| Synopsys, Inc. * | 400 | 10,928 |

| Tyco Electronics, Ltd. * | 450 | 15,692 |

| Energy 0.05% | 11,006 | |

| Sempra Energy | 200 | 11,006 |

| Financial Services 11.99% | 2,573,779 | |

| American Capital Strategies, Ltd. (a) | 300 | 12,387 |

| AmeriCredit Corp. * | 600 | 10,386 |

| Bank of New York Mellon Corp. | 1,115 | 45,079 |

| Citigroup, Inc. | 21,500 | 1,007,920 |

| Countrywide Financial Corp. | 1,600 | 31,760 |

| Discover Financial Services * | 2,200 | 50,908 |

| Federal Home Loan Mortgage Corp. | 4,600 | 283,406 |

| Federal National Mortgage Association | 8,000 | 524,880 |

| JP Morgan Chase & Company | 2,600 | 115,752 |

| Merrill Lynch & Company, Inc. | 1,500 | 110,550 |

| Morgan Stanley (c) | 4,000 | 249,480 |

See notes to financial statements

Intrinsic Value Fund

12

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Financial Services (continued) | ||

| PNC Financial Services Group, Inc. | 300 | $21,111 |

| Washington Mutual, Inc. | 3,000 | 110,160 |

| Food & Beverages 2.60% | 558,785 | |

| Coca-Cola Enterprises, Inc. | 1,100 | 26,202 |

| ConAgra Foods, Inc. | 2,200 | 56,562 |

| Corn Products International, Inc. | 300 | 13,560 |

| General Mills, Inc. | 700 | 39,116 |

| Kraft Foods, Inc., Class A | 5,022 | 161,005 |

| Pepsi Bottling Group, Inc. | 700 | 24,213 |

| PepsiAmericas, Inc. | 500 | 14,800 |

| Pilgrim’s Pride Corp. | 300 | 12,177 |

| Sara Lee Corp. | 2,600 | 43,212 |

| The Coca-Cola Company | 1,600 | 86,048 |

| Tyson Foods, Inc., Class A | 3,800 | 81,890 |

| Forest Products 0.16% | 34,085 | |

| Weyerhaeuser Company | 500 | 34,085 |

| Gas & Pipeline Utilities 0.04% | 9,420 | |

| NiSource, Inc. | 500 | 9,420 |

| Healthcare Products 1.07% | 230,385 | |

| Bausch & Lomb, Inc. | 100 | 6,320 |

| Covidien, Ltd. * | 450 | 17,924 |

| Johnson & Johnson | 1,100 | 67,969 |

| Patterson Companies, Inc. * | 600 | 22,068 |

| Stryker Corp. | 800 | 53,440 |

| Zimmer Holdings, Inc. * | 800 | 62,664 |

| Healthcare Services 2.70% | 578,807 | |

| Cardinal Health, Inc. | 1,400 | 95,732 |

| Coventry Health Care, Inc. * | 200 | 11,474 |

| Express Scripts, Inc. * | 1,000 | 54,750 |

| Lincare Holdings, Inc. * | 600 | 21,594 |

| McKesson Corp. | 3,400 | 194,514 |

| Medco Health Solutions, Inc. * | 300 | 25,635 |

| Quest Diagnostics, Inc. | 600 | 32,850 |

| UnitedHealth Group, Inc. | 2,200 | 110,022 |

| WellPoint, Inc. * | 400 | 32,236 |

| Holdings Companies/Conglomerates 1.76% | 377,039 | |

| General Electric Company | 9,700 | 377,039 |

| Homebuilders 0.67% | 144,130 | |

| Centex Corp. | 1,100 | 31,801 |

| D.R. Horton, Inc. | 500 | 7,555 |

| KB Home (a) | 700 | 21,238 |

| Lennar Corp., Class A (a) | 1,200 | 33,924 |

See notes to financial statements

Intrinsic Value Fund

13

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Homebuilders (continued) | ||

| M.D.C. Holdings, Inc. | 400 | $17,796 |

| Pulte Homes, Inc. | 500 | 8,320 |

| Toll Brothers, Inc. * | 1,100 | 23,496 |

| Hotels & Restaurants 1.03% | 220,040 | |

| McDonald’s Corp. | 4,300 | 211,775 |

| Starbucks Corp. * | 300 | 8,265 |

| Household Products 0.15% | 31,779 | |

| Energizer Holdings, Inc. * | 300 | 31,779 |

| Industrial Machinery 0.16% | 35,431 | |

| Deere & Company | 100 | 13,606 |

| Ingersoll-Rand Company, Class A | 200 | 10,386 |

| Pall Corp. | 300 | 11,439 |

| Insurance 9.18% | 1,969,294 | |

| ACE, Ltd. | 500 | 28,880 |

| Aetna, Inc. | 2,900 | 147,639 |

| AFLAC, Inc. | 1,900 | 101,289 |

| Allstate Corp. | 6,300 | 344,925 |

| Ambac Financial Group, Inc. | 800 | 50,256 |

| American International Group, Inc. | 5,800 | 382,800 |

| Chubb Corp. | 300 | 15,339 |

| CIGNA Corp. | 1,200 | 62,016 |

| Commerce Group, Inc. | 400 | 12,752 |

| Conseco, Inc. * | 1,200 | 16,872 |

| First American Corp. | 700 | 29,281 |

| Hartford Financial Services Group, Inc. | 300 | 26,673 |

| Lincoln National Corp. | 100 | 6,088 |

| MBIA, Inc. | 1,500 | 90,000 |

| MetLife, Inc. | 900 | 57,645 |

| MGIC Investment Corp. | 800 | 24,128 |

| Nationwide Financial Services, Inc., Class A | 400 | 21,408 |

| Old Republic International Corp. | 1,600 | 29,104 |

| PMI Group, Inc. | 1,000 | 31,680 |

| Progressive Corp. | 2,100 | 42,714 |

| Protective Life Corp. | 400 | 16,720 |

| Prudential Financial, Inc. | 800 | 71,824 |

| Radian Group, Inc. | 600 | 10,584 |

| SAFECO Corp. | 800 | 46,416 |

| The Travelers Companies, Inc. | 3,200 | 161,728 |

| Torchmark Corp. | 900 | 55,404 |

| Transatlantic Holdings, Inc. | 200 | 14,166 |

| UnumProvident Corp. | 2,900 | 70,963 |

See notes to financial statements

Intrinsic Value Fund

14

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| International Oil 11.88% | $2,550,680 | |

| Anadarko Petroleum Corp. | 1,100 | 53,878 |

| Chevron Corp. | 6,500 | 570,440 |

| ConocoPhillips | 2,900 | 237,481 |

| Exxon Mobil Corp. | 19,700 | 1,688,881 |

| Internet Retail 0.11% | 23,262 | |

| Expedia, Inc. * | 500 | 14,925 |

| IAC/InterActiveCorp. * | 300 | 8,337 |

| Internet Software 0.05% | 10,725 | |

| McAfee, Inc. * | 300 | 10,725 |

| Leisure Time 0.41% | 88,505 | |

| Brunswick Corp. | 800 | 20,120 |

| Carnival Corp. | 1,500 | 68,385 |

| Liquor 0.23% | 49,400 | |

| Anheuser-Busch Companies, Inc. | 1,000 | 49,400 |

| Manufacturing 0.52% | 110,813 | |

| Danaher Corp. | 400 | 31,064 |

| Harley-Davidson, Inc. | 800 | 43,032 |

| Honeywell International, Inc. | 300 | 16,845 |

| Tyco International, Ltd. | 450 | 19,872 |

| Medical-Hospitals 0.14% | 30,273 | |

| Tenet Healthcare Corp. * | 2,700 | 9,153 |

| Universal Health Services, Inc., Class B | 400 | 21,120 |

| Office Furnishings & Supplies 0.07% | 14,208 | |

| OfficeMax, Inc. | 400 | 14,208 |

| Petroleum Services 0.13% | 27,404 | |

| Valero Energy Corp. | 400 | 27,404 |

| Pharmaceuticals 7.76% | 1,665,449 | |

| Abbott Laboratories | 700 | 36,337 |

| AmerisourceBergen Corp. | 2,400 | 114,840 |

| Forest Laboratories, Inc. * | 1,700 | 63,971 |

| King Pharmaceuticals, Inc. * | 1,400 | 21,042 |

| Merck & Company, Inc. | 13,100 | 657,227 |

| Pfizer, Inc. | 30,600 | 760,104 |

| Watson Pharmaceuticals, Inc. * | 400 | 11,928 |

| Photography 0.19% | 40,005 | |

| Eastman Kodak Company | 1,500 | 40,005 |

| Publishing 1.18% | 253,216 | |

| Gannett Company, Inc. | 3,600 | 169,200 |

| McGraw-Hill Companies, Inc. | 400 | 20,184 |

| The New York Times Company, Class A (a) | 1,400 | 30,772 |

| Tribune Company | 1,200 | 33,060 |

See notes to financial statements

Intrinsic Value Fund

15

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Real Estate 0.25% | $52,811 | |

| Annaly Capital Management, Inc., REIT | 2,300 | 32,407 |

| iStar Financial, Inc., REIT | 300 | 10,980 |

| Thornburg Mortgage, Inc., REIT (a) | 800 | 9,424 |

| Retail Grocery 1.98% | 424,901 | |

| Safeway, Inc. | 5,500 | 174,515 |

| SUPERVALU, Inc. | 1,400 | 59,010 |

| The Kroger Company | 7,200 | 191,376 |

| Retail Trade 9.16% | 1,965,218 | |

| Abercrombie & Fitch Company, Class A | 200 | 15,740 |

| American Eagle Outfitters, Inc. | 400 | 10,332 |

| Bed Bath & Beyond, Inc. * | 800 | 27,712 |

| Big Lots, Inc. * | 900 | 26,793 |

| BJ’s Wholesale Club, Inc. * | 900 | 31,500 |

| Dillard’s, Inc., Class A | 100 | 2,374 |

| Dollar Tree Stores, Inc. * | 1,700 | 73,865 |

| Family Dollar Stores, Inc. | 1,200 | 35,136 |

| Foot Locker, Inc. | 500 | 8,355 |

| Gap, Inc. | 2,600 | 48,776 |

| Home Depot, Inc. | 15,300 | 586,143 |

| Kohl’s Corp. * | 900 | 53,370 |

| Lowe’s Companies, Inc. | 8,900 | 276,434 |

| Rite Aid Corp. *(a) | 6,300 | 31,941 |

| Staples, Inc. | 1,100 | 26,125 |

| Target Corp. | 2,400 | 158,232 |

| The TJX Companies, Inc. | 700 | 21,343 |

| Tiffany & Company | 200 | 10,266 |

| Walgreen Company | 1,100 | 49,577 |

| Wal-Mart Stores, Inc. | 10,800 | 471,204 |

| Semiconductors 1.46% | 313,332 | |

| Intel Corp. | 10,000 | 257,500 |

| KLA-Tencor Corp. | 400 | 22,988 |

| Novellus Systems, Inc. * | 1,200 | 32,844 |

| Software 0.50% | 108,156 | |

| Compuware Corp. * | 2,000 | 16,220 |

| Microsoft Corp. | 3,200 | 91,936 |

| Telecommunications Equipment & Services 3.84% | 824,156 | |

| Polycom, Inc. * | 800 | 24,248 |

| Verizon Communications, Inc. | 19,100 | 799,908 |

See notes to financial statements

Intrinsic Value Fund

16

F I N A N C I A L S T A T E M E N T S

| Issuer | Shares | Value |

| Telephone 2.57% | $550,607 | |

| AT&T, Inc. | 12,727 | 507,425 |

| CenturyTel, Inc. | 900 | 43,182 |

| Tires & Rubber 0.04% | 8,298 | |

| Goodyear Tire & Rubber Company * | 300 | 8,298 |

| Tobacco 0.60% | 129,657 | |

| Altria Group, Inc. | 1,300 | 90,233 |

| UST, Inc. | 800 | 39,424 |

| Toys, Amusements & Sporting Goods 0.44% | 94,605 | |

| Hasbro, Inc. | 900 | 25,389 |

| Mattel, Inc. | 3,200 | 69,216 |

| Trucking & Freight 0.36% | 76,776 | |

| FedEx Corp. | 700 | 76,776 |

| Principal | ||

| Issuer, description, maturity date | amount | Value |

| Short-term investments 0.83% | $178,406 | |

| (Cost $178,406) | ||

| John Hancock Cash Investment Trust (c) | $178,406 | 178,406 |

| Repurchase agreements 3.89% | $836,000 | |

| (Cost $836,000) | ||

| Repurchase Agreement with State Street Corp. dated 08-31-07 at | ||

| 4.60% to be repurchased at $836,427 on 09-04-07, collateralized | ||

| by $885,000 FederalHome Loan Mortgage Corp., 4.00%, due | ||

| 06-12-13 (valued at $854,025, including interest) | $836,000 | 836,000 |

| Total investments (Cost $20,379,781) 100.67% | $21,606,132 | |

| Other assets in excess of liabilities (0.67%) | (144,621) | |

| Total net assets 100.00% | $21,461,511 | |

Percentages are stated as a percent of net assets.

REIT Real Estate Investment Trust

* Non-income-producing.

(a) All or a portion of this security was out on loan.

(c) Investment is an affiliate of the Trust’s adviser or subadviser.

See notes to financial statements

Intrinsic Value Fund

17

F I N A N C I A L S T A T E M E N T S

Financial statements

Statement of assets and liabilities 8-31-07 (unaudited)

This Statement of Assets and Liabilities is the Fund’s balance sheet. It shows the value of what the Fund owns, is due and owes. You’ll also find the net asset value and the maximum offering price per share.

| Assets | |

| Investments, at value (cost $19,365,375) | |

| including $174,908 of securities loaned (Note 2) | $20,591,726 |

| Repurchase agreement, at value (cost $836,000) | 836,000 |

| Investments in affiliated issuers, at value (cost $178,406) | 178,406 |

| Total investments, at value (cost $20,379,781) | 21,606,132 |

| Cash | 85 |

| Cash collateral at broker for futures contracts | 40,000 |

| Receivable for fund shares sold | 12,865 |

| Dividends and interest receivable | 47,353 |

| Receivable for futures variation margin | 6,040 |

| Receivable due from adviser | 43,329 |

| Other assets | 6,761 |

| Total assets | 21,762,565 |

| Liabilities | |

| Payable for fund shares repurchased | 93,762 |

| Payable upon return of securities loaned (Note 2) | 178,406 |

| Payable to affiliates | |

| Fund administration fees | 42 |

| Transfer agent fees | 266 |

| Distribution and service fees | 347 |

| Other payables and accrued expenses | 28,231 |

| Total liabilities | 301,054 |

| Net assets | |

| Capital paid-in | $18,978,631 |

| Undistributed net investment income | 155,850 |

| Accumulated undistributed net realized gain on | |

| investments and future contracts | 1,119,686 |

| Net unrealized appreciation on investments and future contracts | 1,207,344 |

| Net assets | $21,461,511 |

See notes to financial statements

Intrinsic Value Fund

18

F I N A N C I A L S T A T E M E N T S

Statement of assets and liabilities (continued)

| Net asset value per share | |

| Based on net asset values and shares outstanding — the Fund has an | |

| unlimited number of shares authorized with no par value. | |

| Class A ($20,242,210 ÷ 875,426 shares) | $23.12 |

| Class B ($431,204 ÷ 18,743 shares)1 | $23.01 |

| Class C ($396,951 ÷ 17,254 shares)1 | $23.01 |

| Class I ($155,385 ÷ 6,700 shares) | $23.19 |

| Class R1 ($117,690 ÷ 5,109 shares) | $23.032 |

| Class 1($118,071 ÷ 5,090 shares) | $23.20 |

| Maximum offering price per share | |

| Class A3 ($23.12 ÷ 95%) | $24.34 |

1 Redemption price per share is equal to the net asset value less any applicable contingent deferred sales charge.

2 Net assets and shares outstanding have been rounded for presentation purposes. The net asset value is as reported August 31, 2007.

3 On single retail sales of less than $50,000. On sales of $50,000 or more and on group sales the offering price is reduced.

See notes to financial statements

Intrinsic Value Fund

19

F I N A N C I A L S T A T E M E N T S

Statement of operations For the period ended 8-31-07 (unaudited)1

This Statement of Operations summarizes the Fund’s investment income earned and expenses incurred in operating the Fund. It also shows net gains (losses) for the period stated.

| Investment income | |

| Dividends | $243,172 |

| Interest | 19,461 |

| Total investment income | 262,633 |

| Expenses | |

| Investment management fees (Note 3) | 85,434 |

| Distribution and service fees (Note 3) | 35,585 |

| Transfer agent fees (Note 3) | 8,281 |

| Fund administration fees (Note 3) | 3,061 |

| Audit and legal fees | 52,631 |

| Blue sky fees (Note 3) | 45,994 |

| Custodian fees | 12,056 |

| Registration and filing fees | 11,622 |

| Printing and postage fees (Note 3) | 5,196 |

| Trustees’ fees (Note 3) | 612 |

| Miscellaneous | 200 |

| Total expenses | 260,672 |

| Less expense reductions (Note 3) | (110,303) |

| Net expenses | 150,369 |

| Net investment income | 112,264 |

| Realized and unrealized gain (loss) | |

| Net realized gain on | |

| Investments | 742,043 |

| Futures contracts | 41,072 |

| 783,115 | |

| Change in net unrealized appreciation (depreciation) of | |

| Investments | (496,100) |

| Futures contracts | (15,650) |

| (511,750) | |

| Net realized and unrealized gain | 271,365 |

| Increase in net assets from operations | $383,629 |

1 Semiannual period from 3-1-07 to 8-31-07.

See notes to financial statements

Intrinsic Value Fund

20

F I N A N C I A L S T A T E M E N T S

Statement of changes in net assets

These Statements of Changes in Net Assets show how the value of the Fund’s net assets has changed during the last two periods. The difference reflects earnings less expenses, any investment gains and losses, distributions, if any, paid to shareholders and the net of Fund share transactions.

| Period | Period | |

| ended | ended | |

| 2-28-071 | 8-31-072 | |

| Increase (decrease) in net assets | ||

| From operations | ||

| Net investment income | $143,510 | $112,264 |

| Net realized gain | 526,061 | 783,115 |

| Change in net unrealized appreciation (depreciation) | 1,719,094 | (511,750) |

| Increase in net assets resulting from operations | 2,388,665 | 383,629 |

| Distributions to shareholders | ||

| From net investment income | ||

| Class A | (108,035) | — |

| Class B | (1,017) | — |

| Class C | (762) | — |

| Class I | (985) | — |

| Class R1 | (620) | — |

| Class 1 | (914) | — |

| From net realized gain | ||

| Class A | (179,361) | — |

| Class B | (3,802) | — |

| Class C | (2,850) | — |

| Class I | (1,241) | — |

| Class R1 | (1,118) | — |

| Class 1 | (1,118) | — |

| Total distributions | (301,823) | — |

| From Fund share transactions | 18,224,388 | 766,652 |

| Total increase | 20,311,230 | 1,150,281 |

| Net assets | ||

| Beginning of period | — | 20,311,230 |

| End of period3 | $20,311,230 | $21,461,511 |

1 Period from 6-12-06 (commencement of operations) to 2-28-07.

2 Semiannual period from 3-1-07 to 8-31-07. Unaudited.

3 Includes undistributed net investment income of $43,586 and $155,850, respectively.

See notes to financial statements

Intrinsic Value Fund

21

F I N A N C I A L S T A T E M E N T S

Financial highlights

The Financial Highlights show how the Fund’s net asset value for a share has changed since the end of the previous period.

| CLASS A SHARES | ||

| Period ended | 2-28-071 | 8-31-072 |

| Per share operating performance | ||

| Net asset value, beginning of period | $20.00 | 22.68 |

| Net investment income3 | 0.18 | 0.12 |

| Net realized and unrealized | ||

| gain on investments | 2.85 | 0.32 |

| Total from investment operations | 3.03 | 0.44 |

| Less distributions | ||

| From net investment income | (0.13) | — |

| From net realized gain | (0.22) | — |

| (0.35) | — | |

| Net asset value, end of period | $22.68 | 23.12 |

| Total return4,5,6 (%) | 15.19 | 1.94 |

| Ratios and supplemental data | ||

| Net assets, end of period | ||

| (in millions) | $19 | $20 |

| Ratio of net expenses to average | ||

| net assets7 (%) | 1.34 | 1.35 |

| Ratio of gross expenses to average | ||

| net assets7,8 (%) | 1.94 | 2.02 |

| Ratio of net investment income | ||

| to average net assets7 (%) | 1.13 | 1.05 |

| Portfolio turnover6 (%) | 32 | 26 |

See notes to financial statements

Intrinsic Value Fund

22

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS B SHARES | ||

| Period ended | 2-28-071 | 8-31-072 |

| Per share operating performance | ||

| Net asset value, beginning of period | $20.00 | $22.64 |

| Net investment income3 | 0.07 | 0.04 |

| Net realized and unrealized | ||

| gain on investments | 2.85 | 0.33 |

| Total from investment operations | 2.92 | 0.37 |

| Less distributions | ||

| From net investment income | (0.06) | — |

| From net realized gain | (0.22) | — |

| (0.28) | — | |

| Net asset value, end of period | $22.64 | $23.01 |

| Total return4,5,6 (%) | 14.61 | 1.63 |

| Ratios and supplemental data | ||

| Net assets, end of period | ||

| (in millions) | —9 | — 9 |

| Ratio of net expenses to average | ||

| net assets7 (%) | 2.04 | 2.05 |

| Ratio of gross expenses to average | ||

| net assets7,8 (%) | 9.00 | 6.74 |

| Ratio of net investment income | ||

| to average net assets7 (%) | 0.42 | 0.35 |

| Portfolio turnover6 (%) | 32 | 26 |

See notes to financial statements

Intrinsic Value Fund

23

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS C SHARES | ||

| Period ended | 2-28-071 | 8-31-07 2 |

| Per share operating performance | ||

| Net asset value, beginning of period | $20.00 | $22.64 |

| Net investment income3 | 0.06 | 0.04 |

| Net realized and unrealized | ||

| gain on investments | 2.86 | 0.33 |

| Total from investment operations | 2.92 | 0.37 |

| Less distributions | ||

| From net investment income | (0.06) | — |

| From net realized gain | (0.22) | — |

| (0.28) | — | |

| Net asset value, end of period | $22.64 | $23.01 |

| Total return4,5,6 (%) | 14.61 | 1.63 |

| Ratios and supplemental data | ||

| Net assets, end of period | ||

| (in millions) | —9 | —9 |

| Ratio of net expenses to average | ||

| net assets7 (%) | 2.04 | 2.05 |

| Ratio of gross expenses to average | ||

| net assets7,8 (%) | 10.08 | 8.20 |

| Ratio of net investment income | ||

| to average net assets7 (%) | 0.37 | 0.35 |

| Portfolio turnover6 (%) | 32 | 26 |

See notes to financial statements

Intrinsic Value Fund

24

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS I SHARES | ||

| Period ended | 2-28-071 | 8-31-072 |

| Per share operating performance | ||

| Net asset value, beginning of period | $20.00 | $22.70 |

| Net investment income3 | 0.24 | 0.17 |

| Net realized and unrealized | ||

| gain on investments | 2.86 | 0.32 |

| Total from investment operations | 3.10 | 0.49 |

| Less distributions | ||

| From net investment income | (0.18) | — |

| From net realized gain | (0.22) | — |

| (0.40) | — | |

| Net asset value, end of period | $22.70 | $23.19 |

| Total return4,5,6 (%) | 15.50 | 2.16 |

| Ratios and supplemental data | ||

| Net assets, end of period | ||

| (in millions) | —9 | —9 |

| Ratio of net expenses to average | ||

| net assets7 (%) | 0.95 | 0.95 |

| Ratio of gross expenses to average | ||

| net assets7,8 (%) | 17.60 | 14.74 |

| Ratio of net investment income | ||

| to average net assets7 (%) | 1.53 | 1.45 |

| Portfolio turnover6 (%) | 32 | 26 |

See notes to financial statements

Intrinsic Value Fund

25

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS R1 SHARES | ||

| Period ended | 2-28-071 | 8-31-072 |

| Per share operating performance | ||

| Net asset value, beginning of period | $20.00 | $22.63 |

| Net investment income3 | 0.12 | 0.08 |

| Net realized and unrealized | ||

| gain on investments | 2.85 | 0.32 |

| Total from investment operations | 2.97 | 0.40 |

| Less distributions | ||

| From net investment income | (0.12) | — |

| From net realized gain | (0.22) | — |

| (0.34) | — | |

| Net asset value, end of period | $22.63 | $23.03 |

| Total return4,5,6 (%) | 14.88 | 1.77 |

| Ratios and supplemental data | ||

| Net assets, end of period | ||

| (in millions) | —9 | —9 |

| Ratio of net expenses to average | ||

| net assets7 (%) | 1.69 | 1.71 |

| Ratio of gross expenses to average | ||

| net assets7,8 (%) | 20.85 | 17.98 |

| Ratio of net investment income | ||

| to average net assets7 (%) | 0.78 | 0.70 |

| Portfolio turnover6 (%) | 32 | 26 |

See notes to financial statements

Intrinsic Value Fund

26

F I N A N C I A L S T A T E M E N T S

Financial highlights

| CLASS 1 SHARES | ||

| Period ended | 2-28-071 | 8-31-072 |

| Per share operating performance | ||

| Net asset value, beginning of period | $20.00 | $22.70 |

| Net investment income3 | 0.25 | 0.18 |

| Net realized and unrealized | ||

| gain on investments | 2.85 | 0.32 |

| Total from investment operations | 3.10 | 0.50 |

| Less distributions | ||

| From net investment income | (0.18) | — |

| From net realized gain | (0.22) | — |

| (0.40) | — | |

| Net asset value, end of period | $22.70 | $23.20 |

| Total return4,5,6 (%) | 15.53 | 2.20 |

| Ratios and supplemental data | ||

| Net assets, end of period | ||

| (in millions) | —9 | —9 |

| Ratio of net expenses to average | ||

| net assets7 (%) | 0.90 | 0.90 |

| Ratio of gross expenses to average | ||

| net assets7,8 (%) | 1.44 | 1.58 |

| Ratio of net investment income | ||

| to average net assets7 (%) | 1.58 | 1.50 |

| Portfolio turnover6 (%) | 32 | 26 |

1 Class A, Class B, Class C, Class I, Class R1 and Class 1 shares began operations on 6-12-06.

2 Semiannual period from 3-1-07 to 8-31-07. Unaudited.

3 Based on the average of the shares outstanding.

4 Assumes dividend reinvestment.

5 Total returns would have been lower had certain expenses not been reduced during the periods shown.

6 Not annualized.

7 Annualized.

8 Does not take into consideration expense reductions during the periods shown.

9 Less than $500,000.

See notes to financial statements

Intrinsic Value Fund

27

Notes to financial statements (unaudited)

1. Organization

John Hancock Intrinsic Value Fund (the Fund) is a newly organized non-diversified series of John Hancock Funds III (the Trust). The Trust was established as a Massachusetts business trust on June 9, 2005. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end investment management company. The investment objective of the Fund is to seek long-term capital growth.

John Hancock Life Insurance Company of New York (John Hancock New York) is a wholly owned subsidiary of John Hancock Life Insurance Company (U.S.A.) (John Hancock USA). John Hancock USA and John Hancock New York are indirect wholly owned subsidiaries of The Manufacturers Life Insurance Company (Manulife), which in turn is a wholly owned subsidiary of Manulife Financial Corporation (MFC), a publicly traded company. MFC and its subsidiaries are known collectively as “Manulife Financial.”

John Hancock Investment Management Services, LLC (the Adviser), a Delaware limited liability company controlled by John Hancock USA, serves as investment adviser for the Trust and John Hancock Funds, LLC (the Distributor), a Delaware limited liability company, an affiliate of the Adviser, serves as principal underwriter.

The Board of Trustees has authorized the issuance of multiple classes of shares of the Fund, including classes designated as Class A, Class B, Class C, Class I, Class R1, Class 1, Class 3 and Class NAV shares. The shares of each class represent an interest in the same portfolio of investments of the Fund, and have equal rights as to voting, redemptions, dividends and liquidation, except that certain expenses, subject to the approval of the Board of Trustees, may be applied differently to each class of shares in accordance with current regulations of the Securities and Exchange Commission (SEC) and the Internal Revenue Service. Shareholders of a class that bear distribution and service expenses under the terms of a distribution plan have exclusive voting rights to that distribution plan. Class B shares will convert to Class A shares eight years after purchase.

Class 1 shares are sold only to certain exempt separate accounts of John Hancock USA and John Hancock New York.

The Adviser and affiliates of John Hancock USA owned 736,437, 5,088, 5,077 and 5,089 shares of beneficial interest of Class A, Class I, Class R1 and Class 1, respectively, on August 31, 2007.

2. Significant accounting policies

In the preparation of the financial statements, the Fund follows the policies described below. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results may differ from these estimates.

Security valuation

The net asset value of the shares of Class A, Class B, Class C, Class I, Class R1 and Class 1 of the Fund is determined daily as of the close of the New York Stock Exchange (NYSE), normally at 4:00 p.m., Eastern Time. Short-term debt instruments with remaining maturities of 60 days or less are valued at amortized cost, and thereafter assume a constant amortization to maturity of any discount or premium, which approximates market value. Investments in John Hancock Cash Investments Trust (JHCIT), an affiliate of John Hancock Advisers, LLC (JHA),

Intrinsic Value Fund

28

a wholly owned subsidiary of John Hancock Financial Services, Inc., a subsidiary of MFC, are valued at their net asset value each business day. All other securities held by the Fund are valued at the last sale price or official closing price (closing bid price or last evaluated quote if no sale has occurred) as of the close of business on a principal securities exchange (domestic or foreign) on which they trade or, lacking any sales, at the closing bid price. Securities traded only in the over-the- counter market are valued at the last bid price quoted by brokers making markets in the securities at the close of trading. Securities for which there are no such quotations, principally debt securities, are valued based on the valuation provided by an independent pricing service, which utilizes both dealer-supplied and electronic data processing techniques, which take into account factors such as institutional-size trading in similar grou ps of securities, yield, quality, coupon rate, maturity, type of issue, trading characteristics and other market data.

Other assets and securities for which no such quotations are readily available are valued at their fair value as determined in good faith under consistently applied procedures established by and under the general supervision of the Board of Trustees. Generally, trading in non-U.S. securities is substantially completed each day at various times prior to the close of trading on the NYSE. The values of such securities used in computing the net asset value of a Fund’s shares are generally determined as of such times. Occasionally, significant events that affect the values of such securities may occur between the times at which such values are generally determined and the close of the NYSE. Upon such an occurrence, these securities will be valued at their fair value as determined in good faith under consistently applied procedures established by and under the general supervision of the Board of Trustees.

Repurchase agreements

The Fund may enter into repurchase agreements. When the Fund enters into a repurchase agreement through its custodian, it receives delivery of securities, the amount of which at the time of purchase and each subsequent business day is required to be maintained at such a level that the market value is generally at least 102% of the repurchase amount. The Fund will take constructive receipt of all securities underlying the repurchase agreements it has entered into until such agreements expire. If the seller defaults, the Fund would suffer a loss to the extent that proceeds from the sale of underlying securities were less than the repurchase amount. The Fund may enter into repurchase agreements maturing within seven days with domestic dealers, banks or other financial institutions deemed to be creditworthy by the Adviser. Collateral for certain tri-party repurchase agreements is held at the custodian bank in a segregated account for the benefit of the Fund and the counterparty.

Security transactions and related investment income

Investment security transactions are accounted for on a trade date plus one basis for daily net asset value calculations. However, for financial reporting purposes, investment transactions are reported on trade date. Interest income is accrued as earned. Dividend income is recorded on the ex-dividend date. Foreign dividends are recorded on the ex-date or when the Fund becomes aware of the dividends from cash collections. Discounts/ premiums are accreted/amortized for financial reporting purposes. Non-cash dividends are recorded at the fair market value of the securities received. Debt obligations may be placed in a non-accrual status and related interest income may be reduced by ceasing current accruals and writing off interest receivables when the collection of all or a portion of interest has become doubtful, based upon consistently applied procedures.

From time to time, the Fund may invest in Real Estate Investment Trusts (REITs) and as a result, will estimate the components of distributions from these securities.

Intrinsic Value Fund

29

Distributions from REITs received in excess of income are recorded as a reduction of cost of investments and/or as a realized gain.

The Fund uses the First In, First Out method for fixed-income securities and Highest Cost, First Out for all other securities for determining realized gain or loss on investments for both financial and federal income tax reporting purposes.

Multi-class allocations

All income, expenses (except for class-specific expenses) and realized and unrealized gains (losses) are allocated to each class of shares based upon the relative net assets of each class.

Dividends to shareholders from net investment income are determined at a class level and distributions from capital gains are determined at a Fund level.

Expense allocation

Expenses are allocated based on the relative share of net assets of the Fund at the time the expense was incurred. Class-specific expenses, such as distribution (Rule 12b-1) fees, are accrued daily and charged directly to the respective share classes.

Securities lending

The Fund may lend securities in amounts up to 33 1 / 3% of the Fund’s total assets. Such loans are callable at any time and are at all times fully secured by cash, cash equivalents or securities issued or guaranteed by the U.S. government or its agencies or instrumentalities, marked to market on a daily basis. The Fund may bear the risk of delay in recovery of, or even of rights in, the securities loaned should the borrower of the securities fail financially. The Fund receives compensation for lending its securities either in the form of fees or by retaining a portion of interest on the investment of any cash received as collateral. The Fund invests in cash collateral received in connection with securities lending transactions in JHCIT, a Delaware common law trust and an affiliated fund. JHCIT is exempt from registration under Section 3(c)(7) of the 1940 Act (pursuant to exemptive order issued by the SEC) and is managed by the Adviser, for which the Adviser receives an investment advisory fee of 0.04% of the average daily net assets of JHCIT.

All collateral received will be in an amount equal to at least 100% of the market value of the loaned securities and is intended to be maintained at that level during the period of the loan. The market value of the loaned securities is determined at the close of business of the Fund and any additional required collateral is delivered to the Fund the next business day. During the loan period, the Fund continues to retain rights of ownership, including dividends and interest of the loaned securities. At August 31, 2007, the Fund loaned securities having a market value of $174,908 collateralized by securities in the amount of $178,406.

Futures

The Fund may purchase and sell financial futures contracts and options on those contracts. The Fund invests in contracts based on financial instruments such as U.S. Treasury Bonds or Notes or on securities indexes, such as the Standard & Poor’s 500 Index, in order to hedge against a decline in the value of securities owned by the Fund.

Initial margin deposits required upon entering into futures contracts are satisfied by the delivery of specific securities or cash as collateral to the broker (the Funds’ agent in acquiring the futures position). If the position is closed out by taking an opposite position prior to the settlement date of the futures contract, a final determination of variation margin is made, cash is required to be paid to or released by the broker, and the Fund realizes a gain or loss.

When the Fund sells a futures contract based on a financial instrument, the Fund becomes obligated to deliver that kind of instrument at an agreed upon date for a specified price. The Fund realizes a gain or loss depending on whether the price of an offsetting purchase is less or more than the price of the initial sale or on whether the price of an offsetting sale is more or less than the price of the initial purchase. The Fund could be exposed to risks if it could not close out futures positions because of an illiquid secondary market or the inability of counterparties to meet the terms of their contracts. Futures contracts are valued at the

Intrinsic Value Fund

30

The following is a summary of open futures contracts on August 31, 2007:

| NUMBER OF | UNREALIZED | |||

| OPEN CONTRACTS | CONTRACTS | POSITION | EXPIRATION | DEPRECIATION |

| S&P 500 Index | 8 | Long | Sep 2007 | ($19,007) |

quoted daily settlement prices established by the exchange on which they trade.

Federal income taxes

The Fund qualifies as a “regulated investment company” by complying with the applicable provisions of the Internal Revenue Code and will not be subject to federal income tax on taxable income that is distributed to shareholders. Therefore, no federal income tax provision is required.

New accounting pronouncements

In June 2006, Financial Accounting Standards Board (FASB) Interpretation No. 48, Accounting for Uncertainty in Income Taxes (the Interpretation), was issued and is effective for fiscal years beginning after December 15, 2006, and is to be applied to all open tax years as of the effective date. This Interpretation prescribes a minimum threshold for financial statement recognition of the benefit of a tax position taken or expected to be taken in a tax return and requires certain expanded disclosures. Management has evaluated the application of this Interpretation to the Fund and does not believe there is a material impact resulting from the adoption of this Interpretation on the Fund’s financial statements.

In September 2006, FASB Standard No. 157, Fair Value Measurements (FAS 157), was issued and is effective for fiscal years beginning after November 15, 2007. FAS 157 defines fair value, establishing a framework for measuring fair value and expands disclosure about fair value measurements. Management is currently evaluating the application of FAS 157 to the Fund and its impact, if any, resulting from the adoption of FAS 157 on the Fund’s financial statements.

Distribution of income and gains

The Fund records distributions to shareholders from net investment income and net realized gains, if any, on the ex-dividend date. During the period ended February 28, 2007, the tax character of distributions paid was as follows: ordinary income $270,360 and long-term capital gains $31,463. Distributions paid by the Fund with respect to each class of shares are calculated in the same manner, at the same time and are in the same amount, except for the effect of expenses that may be applied differently to each class.

Such distributions on a tax basis, are determined in conformity with income tax regulations, which may differ from accounting principles generally accepted in the United States of America. Distributions in excess of tax basis earnings and profits, if any, are reported in the Fund’s financial statements as a return of capital.

Capital accounts

The Fund reports the undistributed net investment income and accumulated undistributed net realized gain (loss) accounts on a basis approximating amounts available for future tax distributions (or to offset future taxable realized gains when a capital loss carryforward is available). Accordingly, the Fund may periodically make reclassifications among certain capital accounts without affecting its net asset value.

3. Investment advisory and other agreements

Advisory fees

The Trust has entered into an Investment Advisory Agreement with the Adviser. The Adviser is responsible for managing the corporate and business affairs of the Trust and for selecting and compensating subadvisers to handle the investment of the assets of the Fund, subject to the supervision of the Trust’s Board of Trustees. Under the Advisory Agreement, the Fund pays a monthly management fee to the Adviser equivalent, on an annual basis, to the sum of: (a) 0.78% of the first $500,000,000 of the Fund’s aggregate daily net assets; (b) 0.76% of the next $500,000,000 of the Fund’s aggregate daily net assets; (c) 0.75% of the next $1,500,000,000 of the Fund’s aggregate daily

Intrinsic Value Fund

31

net assets; and (d) 0.74% of the Fund’s aggregate daily net assets in excess of $2,500,000,000. Aggregate net assets include the net assets of the Fund and Intrinsic Value Trust, a series of John Hancock Trust and the Intrinsic Value Fund, a series of John Hancock Funds II. The Adviser has a subadvisory agreement with Grantham, Mayo, Van Otterloo & Co. LLC. The Fund is not responsible for payment of the subadvisory fees.

Expense reimbursements

The Adviser has agreed contractually to reimburse for certain fund level expenses that exceed 0.08% of the average annual net assets, or to make a payment to a specific class of shares of the Fund in an amount equal to the amount by which the expenses attributable to such class of shares (excluding taxes, portfolio brokerage commissions, interest, litigation and indemnification expenses and other extraordinary expenses not incurred in the ordinary course of the Fund’s business and fees under any agreement or plans of the Fund dealing with services for shareholders and others with beneficial interests in shares of the Fund) exceed the percentage of average annual net assets (on an annualized basis) attributable as follows: 1.35% for Class A, 2.05% for Class B, 2.05% for Class C, 0.95% for Class I, 1.45% for Class R1 and 0.90% for Class 1. Accordingly, the expense reductions related to this expense limitation amounted to $69,037, $10,825, $10,468, $9,720, $9,847 and $406 for Class A, Class B, Class C, Class I, Class R1 and Class 1, respectively, for the period ended August 31, 2007. This expense reimbursement shall continue in effect until June 30, 2008 and thereafter until terminated by the Adviser on notice to the Trust.

Administration fees

The Fund has an agreement with the Adviser that requires the Fund to reimburse the Adviser for all expenses associated with providing the administrative, financial, accounting and recordkeeping services of the Fund, including the preparation of all tax returns, annual, semiannual and periodic reports to shareholders and the preparation of all regulatory reports. These expenses are allocated based on the relative net assets of each class. The compensation for the period amounted to $3,061 with an effective rate of 0.03% of the Fund’s average daily net asset value.

Distribution plan

The Trust has a Distribution Agreement with the Distributor. The Fund has adopted Distribution Plans with respect to Class A, Class B, Class C, Class R1 and Class 1, pursuant to Rule 12b-1 under the 1940 Act, to reimburse the Distributor for the services it provides as distributor of shares of the Fund. Accordingly, the Fund makes monthly payments to the Distributor at an annual rate not to exceed 0.30%, 1.00%, 1.00%, 0.50% and 0.05% of average daily net asset value of Class A, Class B, Class C, Class R1 and Class 1, respectively. A maximum of 0.25% of such payments may be service fees, as defined by the Conduct Rules of Financial Industry Regulatory Authority (formerly the National Association of Securities Dealers). Under the Conduct Rules, curtailment of a portion of the Fund’s 12b-1 payments could occur under certain circumstances. In addition, under a Service Plan for Class R1 shares, the Fund pays up to 0.25% of Class R1 a verage daily net asset value for certain other services.

Sales charges

Class A shares are assessed up-front sales charges of up to 5.00% of net asset value of such shares. During the period ended August 31, 2007, the Fund was informed that the Distributor received net up-front sales charges of $88,410 with regard to sales of Class A shares. Of this amount, $14,523 was retained and used for printing prospectuses, advertising, sales literature and other purposes, $73,154 was paid as sales commissions to unrelated broker-dealers and $733 was paid as sales commissions to sales personnel of Signator Investors, Inc. (Signator Investors), a related broker-dealer, an indirect subsidiary of MFC.

Class B shares that are redeemed within six years of purchase are subject to a contingent deferred sales charge (CDSC) at declining rates, beginning at 5.00% of the lesser of the current market value at the time of redemption or the original purchase cost of the shares being redeemed. Class C shares that are redeemed within one year of purchase

Intrinsic Value Fund

32

are subject to a CDSC at a rate of 1.00% of the lesser of the current market value at the time of redemption or the original purchase cost of the shares being redeemed. Proceeds from the CDSCs are paid to the Distributor and are used, in whole or in part, to defray its expenses for providing distribution-related services to the Fund in connection with the sale of Class B and Class C shares. During the period ended August 31, 2007, CDSCs received by JH Funds amounted to $49 for Class B shares and $103 for Class C shares.

Transfer agent fees

The Fund has a Transfer Agency Agreement with John Hancock Signature Services, Inc. (Signature Services), an indirect subsidiary of MFC. For Class A, Class B, Class C, Class I and Class R1 shares, the Fund pays a monthly transfer agent fee at an annual rate of 0.05% of each class’ average daily net assets, plus a fee based on the number of shareholder accounts and reimbursement for certain out-of-pocket expenses. Expenses not directly attributable to a particular class of shares are aggregated and allocated to each class on the basis of its relative net asset value.

Signature Services has agreed to limit the transfer agent fees so that such fees do not exceed 0.20% annually of Class A, Class B, Class C, Class I and Class R1 share average daily net assets. This agreement is effective until December 31, 2007. Signature Services reserves the right to terminate this limitation in the future. Accordingly, there were no transfer agent fee reductions for Class A, Class B, Class C, Class I and Class R1 shares, respectively, during the period ended August 31, 2007.

Expenses under the agreements described above for the period ended August 31, 2007, were as follows:

| Distribution and | Transfer | Blue sky | Printing and | |

| Share class | service fees | agent fees | fees | postage fees |

| Class A | $31,076 | $7,411 | $9,424 | $4,427 |

| Class B | 2,315 | 463 | 9,157 | 176 |

| Class C | 1,708 | 342 | 9,211 | 41 |

| Class I | — | 35 | 9,101 | 166 |

| Class R1 | 455 | 30 | 9,101 | 378 |

| Class 1 | 31 | — | — | 8 |

| Total | 35,585 | 8,281 | 45,994 | 5,196 |

Trustees’ fees

The Trust compensates each Trustee who is not an employee of the Adviser or its affiliates. Total Trustees’ expenses are allocated to the Fund based on its average daily net asset value.

4. Guarantees and indemnifications

Under the Trust’s organizational documents, its Officers and Trustees are indemnified against certain liability arising out of the performance of their duties to the Trust. Additionally, in the normal course of business, the Trust enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Trust that have not yet occurred. However, based on experience, the Trust believes the risk of loss to be remote.

5. Line of credit

The Fund has entered into an agreement which enables it to participate in a $100 million unsecured committed line of credit with State Street Corporation. Borrowings will be made solely to temporarily finance the repurchase of capital shares. Interest is charged to the Fund based on its borrowings at a rate per annum equal to the Federal Funds rate plus 0.50%. In addition, a commitment fee of 0.07% per annum, payable at the end of each calendar

Intrinsic Value Fund

33

quarter, based on the average daily-unused portion of the line of credit, is charged to the Fund on a prorated basis based on average net assets. For the period ended August 31, 2007, there were no borrowings under the line of credit.

6. Capital shares

Share activities for the Fund for the periods ended February 28, 2007 and August 31, 2007, were as follows:

| Period ended 2-28-07 1 | Period ended 8-31-072 | |||

| Shares | Amount | Shares | Amount | |

| Class A | ||||

| Sold | 838,725 | $17,032,947 | 60,561 | $1,429,482 |

| Distributions reinvested | 12,374 | 281,144 | — | — |

| Repurchased | (4,497) | (101,945) | (31,737) | (747,591) |

| Net increase | 846,602 | $17,212,146 | 28,824 | $681,891 |

| Class B | ||||

| Sold | 25,686 | $554,475 | 4,340 | $104,542 |

| Distributions reinvested | 201 | 4,563 | — | — |

| Repurchased | (5,219) | (119,072) | (6,265) | (151,835) |

| Net increase (decrease) | 20,668 | $439,966 | (1,925) | ($47,293) |

| Class C | ||||

| Sold | 23,486 | $503,103 | 5,938 | $138,311 |

| Distributions reinvested | 135 | 3,064 | — | — |

| Repurchased | (10,948) | (251,638) | (1,357) | (31,481) |

| Net increase | 12,673 | $254,529 | 4,581 | $106,830 |

| Class I | ||||

| Sold | 5,547 | 111,000 | 1,055 | $25,224 |

| Distributions reinvested | 98 | 2,226 | — | — |

| Net increase | 5,645 | 113,226 | 1,055 | $25,224 |

| Class R1 | ||||

| Sold | 5,033 | 100,750 | — | — |

| Distributions reinvested | 76 | 1,738 | — | — |

| Net increase | 5,109 | 102,488 | — | — |

| Class 1 | ||||

| Sold | 5,000 | $100,000 | — | — |

| Distributions reinvested | 90 | 2,033 | — | — |

| Net increase | 5,090 | $102,033 | — | — |

| Net increase | 895,787 | $18,224,388 | 32,535 | $766,652 |

1 Period from 6-12-06 (commencement of operations) to 2-28-07.

2 Semiannual period from 3-1-07 to 8-31-07. Unaudited.

7. Investment transactions