UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

(Exact name of registrant as specified in charter)

60 State Street, Boston, MA 02109

(Address of principal executive offices) (ZIP code)

Christopher J. Kelley, Amundi Asset Management, Inc.,

60 State Street, Boston, MA 02109

(Name and address of agent for service)

Registrant's telephone number, including area code:

Date of reporting period:

Item 1. Report to Stockholders.

(a) The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

Pioneer Securitized Income Fund

Class A / SIFFX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Securitized Income Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class A | $95 | 0.90% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class A shares at NAV returned 11.88%. For the same period, the Fund’s broad-based benchmark, the Bloomberg U.S. Aggregate Bond Index, returned 5.10%. The performance benchmark, the Bloomberg U.S. Securitized MBS/ABS/CMBS Index, returned 5.07% over the period.

The Fund’s returns relative to the performance benchmark benefited from allocations to non-agency mortgage-backed securities (RMBS), collateralized loan obligations (CLO), asset-backed securities, U.S. government agency mortgage-backed securities, and commercial mortgage-backed securities (CMBS).

Both sector allocation and security selection contributed to the Fund’s returns relative to the performance benchmark.

Residential mortgage credit generated positive returns for the year and was the strongest performing sector as US housing prices remained resilient despite still-elevated mortgage rates. The portfolio’s allocation to residential credit-risk-transfer securities was the strongest contributing subsector.

Asset-backed securities (ABS) were an overall contributor to total return and relative returns versus the performance benchmark for the year led by a strong showing from the portfolio’s auto ABS exposure. As corporate spreads tightened during the year, so did auto ABS spreads. The elevated short-end of the yield curve benefited many of the ABS subsector’s short duration exposure.

The portfolio’s exposure to CMBS contributed over the year to returns relative to the performance benchmark, with the securities’ high coupons and discount prices leading to gains despite broadly waning investor appetite for CMBS securities with any collateral tied to retail or office.

The only notable detractor from performance was the Fund's U.S. Treasury futures (derivatives held in the Fund to hedge against interest rate risk) which decreased in value as rates rallied during the period.

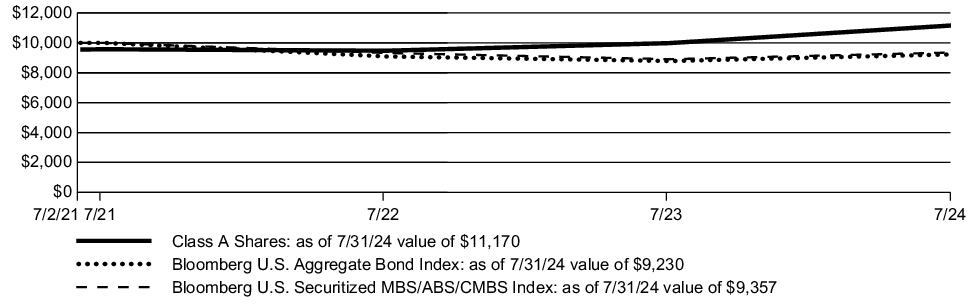

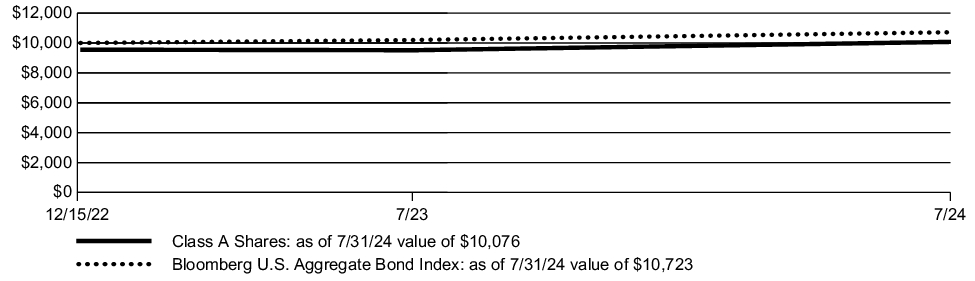

Fund Performance

The line graph below shows the change in value of a $10,000 investment made in Class A shares of the Fund at public offering price during the periods shown, compared to that of the Bloomberg U.S. Aggregate Bond Index and the Bloomberg U.S. Securitized MBS/ABS/CMBS Index.

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | Since Inception* |

| Class A (with sales charge) | 6.85% | 3.66%) |

| Class A (without sales charge) | 11.88% | 5.23%) |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | (2.26)% |

| Bloomberg U.S. Securitized MBS/ABS/CMBS Index | 5.07% | (1.95)% |

* | Performance of Class A shares shown in the graph above is from the inception of Class A shares on 7/2/21 through 7/31/24. Index information shown in the graph above is from 7/31/21 through 7/31/24. |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $86,676,905% |

| Total number of portfolio holdings | $194%^^ |

| Total advisory fee paid | $4,736% |

| Portfolio turnover rate | $30% |

^^ | Excluding short-term investments and all derivative contracts except for options purchased. |

PORTFOLIO DIVERSIFICATION

(as of July 31, 2024)*

| Asset Backed Securities | 38.6% |

| Collateralized Mortgage Obligations | 33.1% |

| U.S. Government and Agency Obligations | 17.4% |

| Commercial Mortgage-Backed Securities | 10.8% |

| Corporate Bonds | 0.1% |

* | As a percentage of total investments excluding short‑term investments and all derivative contracts except for options purchased. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Securitized Income Fund

Class Y / SYFFX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Securitized Income Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class Y | $69 | 0.65% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class Y shares at NAV returned 12.16%. For the same period, the Fund’s broad-based benchmark, the Bloomberg U.S. Aggregate Bond Index, returned 5.10%. The performance benchmark, the Bloomberg U.S. Securitized MBS/ABS/CMBS Index, returned 5.07% over the period.

The Fund’s returns relative to the performance benchmark benefited from allocations to non-agency mortgage-backed securities (RMBS), collateralized loan obligations (CLO), asset-backed securities, U.S. government agency mortgage-backed securities, and commercial mortgage-backed securities (CMBS).

Both sector allocation and security selection contributed to the Fund’s returns relative to the performance benchmark.

Residential mortgage credit generated positive returns for the year and was the strongest performing sector as US housing prices remained resilient despite still-elevated mortgage rates. The portfolio’s allocation to residential credit-risk-transfer securities was the strongest contributing subsector.

Asset-backed securities (ABS) were an overall contributor to total return and relative returns versus the performance benchmark for the year led by a strong showing from the portfolio’s auto ABS exposure. As corporate spreads tightened during the year, so did auto ABS spreads. The elevated short-end of the yield curve benefited many of the ABS subsector’s short duration exposure.

The portfolio’s exposure to CMBS contributed over the year to returns relative to the performance benchmark, with the securities’ high coupons and discount prices leading to gains despite broadly waning investor appetite for CMBS securities with any collateral tied to retail or office.

The only notable detractor from performance was the Fund's U.S. Treasury futures (derivatives held in the Fund to hedge against interest rate risk) which decreased in value as rates rallied during the period.

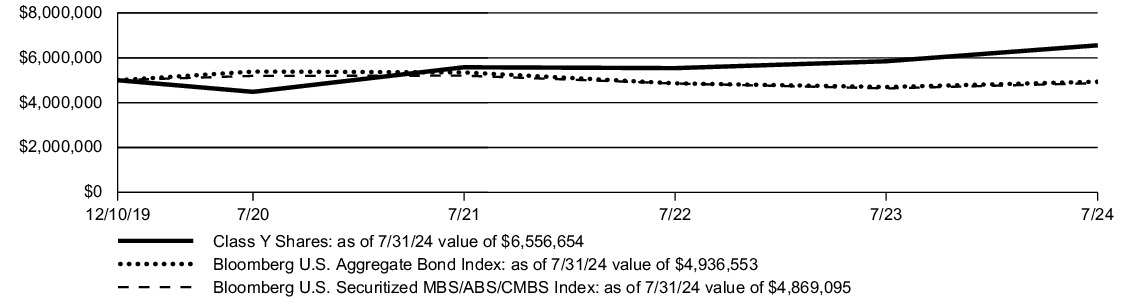

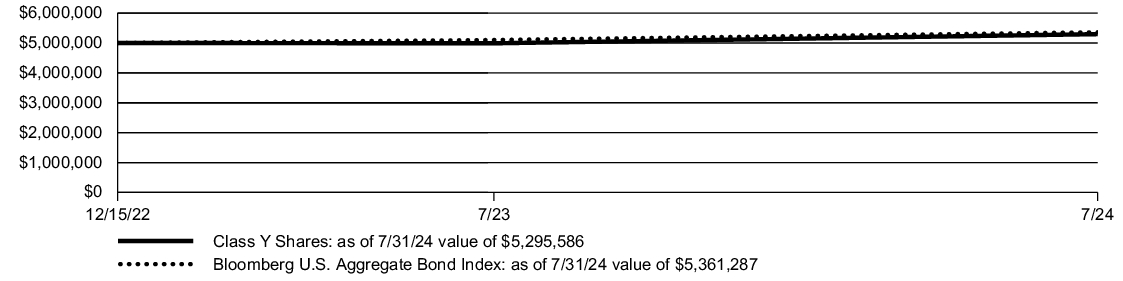

Fund Performance

The line graph below shows the change in value of a $5 Million investment made in Class Y shares of the Fund during the periods shown, compared to that of the Bloomberg U.S. Aggregate Bond Index and the Bloomberg U.S. Securitized MBS/ABS/CMBS Index.

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | Since Inception* |

| Class Y | 12.16% | 6.01%) |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | (0.26)% |

| Bloomberg U.S. Securitized MBS/ABS/CMBS Index | 5.07% | (0.51)% |

* | Performance of Class Y shares shown in the graph above is from the inception of Class Y shares on 12/10/19 through 7/31/24. Index information shown in the graph above is from 12/31/19 through 7/31/24. |

The Fund acquired the assets and liabilities of Pioneer Securitized Income Fund (the “Predecessor Fund”) on June 30, 2021 (the “Reorganization”). As a result of the Reorganization, the Predecessor Fund’s performance and financial history became the performance and financial history of the Fund. The performance of Class Y shares of the Fund is the performance of the common shares of the Predecessor Fund for periods prior to the Reorganization, and has not been restated to reflect any differences in expenses.

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $86,676,905% |

| Total number of portfolio holdings | $194%^^ |

| Total advisory fee paid | $4,736% |

| Portfolio turnover rate | $30% |

^^ | Excluding short-term investments and all derivative contracts except for options purchased. |

PORTFOLIO DIVERSIFICATION

(as of July 31, 2024)*

| Asset Backed Securities | 38.6% |

| Collateralized Mortgage Obligations | 33.1% |

| U.S. Government and Agency Obligations | 17.4% |

| Commercial Mortgage-Backed Securities | 10.8% |

| Corporate Bonds | 0.1% |

* | As a percentage of total investments excluding short‑term investments and all derivative contracts except for options purchased. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Multi-Asset Income Fund

Class A / PMAIX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Multi-Asset Income Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class A | $88 | 0.83% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class A shares at NAV returned 11.56%. For the same period, the Fund’s broad-based benchmarks, the MSCI All Country World NR Index (MSCI ACWI) and the Bloomberg U.S. Aggregate Bond Index, returned 17.02% and 5.10%, respectively. The performance benchmark, a blended benchmark (35% MSCI All Country World NR Index and 65% Bloomberg U.S. Aggregate Bond Index), returned 9.22% over the period.

Security selection and sector allocation both contributed positively to benchmark relative performance in the period, mainly due to positions in several international bank stocks as well as individual opportunities in industrials, energy, and information technology stocks. Fixed income selection and allocations to U.S. Treasury securities, securitized investments, and investment grade corporate bonds also contributed positively to benchmark relative performance.

The largest detractor from performance were positions in index futures, as a result of the positive performance of the equity markets during the period. The Fund maintains a significant position in equity-linked notes. The Fund holds positions in index futures in an effort to reduce risk associated with the equity-linked notes. Within fixed income, the Fund's overweight allocation to U.S. government agency bonds detracted from benchmark relative performance.

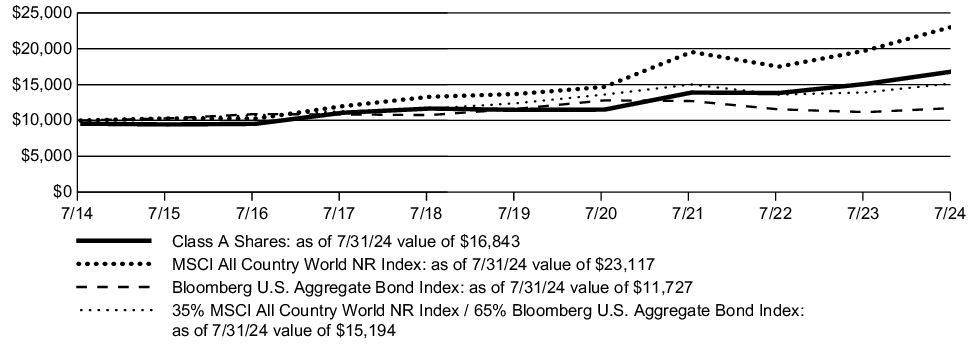

Fund Performance

The line graph below shows the change in value of a $10,000 investment made in Class A shares of the Fund at public offering price during the periods shown, compared to that of the MSCI All Country World NR Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (65% MSCI All Country World NR Index and 35% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class A (with sales charge) | 6.57% | 6.98% | 5.35% |

| Class A (without sales charge) | 11.56% | 7.98% | 5.84% |

| MSCI All Country World NR Index | 17.02% | 11.05% | 8.74% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 35% MSCI All Country World NR Index / 65% Bloomberg U.S. Aggregate Bond Index | 9.22% | 4.13% | 4.27% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $3,623,720,285% |

| Total number of portfolio holdings | $491%^^ |

| Total advisory fee paid | $13,905,080% |

| Portfolio turnover rate | $62% |

^^ | Excluding short‑term investments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Financials | 27.3% |

| U.S. Government | 12.2% |

| Energy | 10.3% |

| Information Technology | 9.8% |

| Basic Materials | 7.8% |

| Health Care | 6.3% |

| Consumer Discretionary | 4.6% |

| Industrials | 4.6% |

| Mortgage Securities | 3.9% |

| Asset Backed Securities | 2.8% |

| Utilities | 2.6% |

| Communication Services | 2.6% |

| Consumer, Cyclical | 1.3% |

| Consumer, Non-cyclical | 1.2% |

| Consumer Staples | 1.2% |

| Foreign Government | 1.0% |

| Closed-End Funds | 0.3% |

| Real Estate | 0.2% |

* | As a percentage of total investments excluding short‑term investments and all derivative contracts except for options purchased. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Multi-Asset Income Fund

Class C / PMACX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Multi-Asset Income Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class C | $169 | 1.60% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class C shares at NAV returned 10.64%. For the same period, the Fund’s broad-based benchmarks, the MSCI All Country World NR Index (MSCI ACWI) and the Bloomberg U.S. Aggregate Bond Index, returned 17.02% and 5.10%, respectively. The performance benchmark, a blended benchmark (35% MSCI All Country World NR Index and 65% Bloomberg U.S. Aggregate Bond Index), returned 9.22% over the period.

Security selection and sector allocation both contributed positively to benchmark relative performance in the period, mainly due to positions in several international bank stocks as well as individual opportunities in industrials, energy, and information technology stocks. Fixed income selection and allocations to U.S. Treasury securities, securitized investments, and investment grade corporate bonds also contributed positively to benchmark relative performance.

The largest detractor from performance were positions in index futures, as a result of the positive performance of the equity markets during the period. The Fund maintains a significant position in equity-linked notes. The Fund holds positions in index futures in an effort to reduce risk associated with the equity-linked notes. Within fixed income, the Fund's overweight allocation to U.S. government agency bonds detracted from benchmark relative performance.

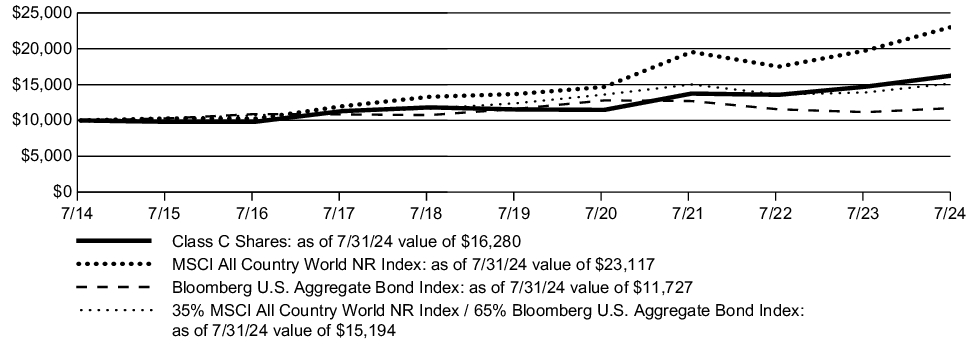

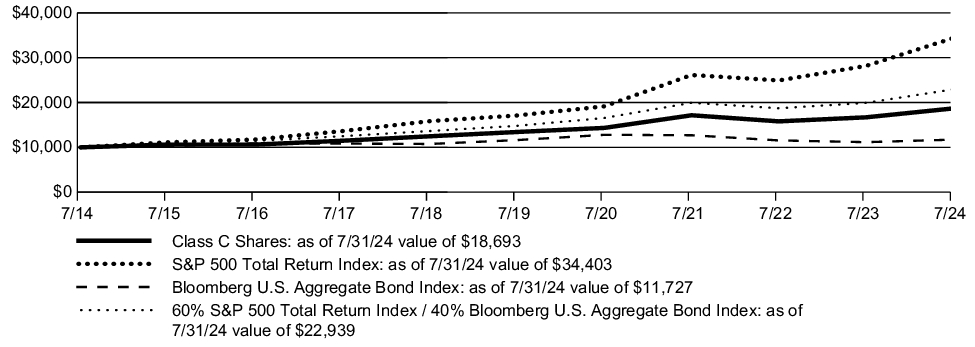

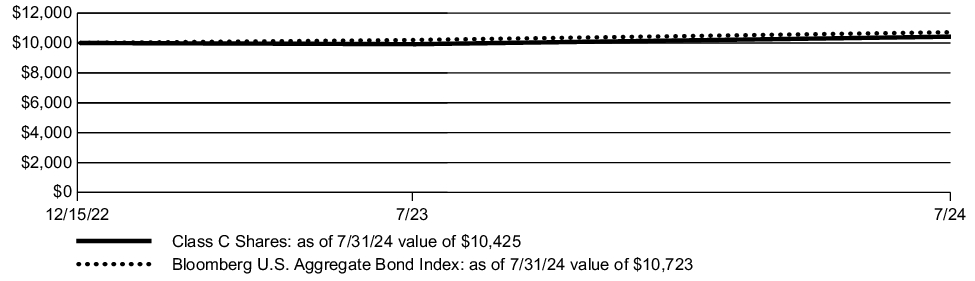

Fund Performance

The line graph below shows the change in value of a $10,000 investment made in Class C shares of the Fund during the periods shown, compared to that of the MSCI All Country World NR Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (65% MSCI All Country World NR Index and 35% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class C (with contingent deferred sales charge) | 9.64% | 7.14% | 4.99% |

| Class C (without contingent deferred sales charge) | 10.64% | 7.14% | 4.99% |

| MSCI All Country World NR Index | 17.02% | 11.05% | 8.74% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 35% MSCI All Country World NR Index / 65% Bloomberg U.S. Aggregate Bond Index | 9.22% | 4.13% | 4.27% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $3,623,720,285% |

| Total number of portfolio holdings | $491%^^ |

| Total advisory fee paid | $13,905,080% |

| Portfolio turnover rate | $62% |

^^ | Excluding short‑term investments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Financials | 27.3% |

| U.S. Government | 12.2% |

| Energy | 10.3% |

| Information Technology | 9.8% |

| Basic Materials | 7.8% |

| Health Care | 6.3% |

| Consumer Discretionary | 4.6% |

| Industrials | 4.6% |

| Mortgage Securities | 3.9% |

| Asset Backed Securities | 2.8% |

| Utilities | 2.6% |

| Communication Services | 2.6% |

| Consumer, Cyclical | 1.3% |

| Consumer, Non-cyclical | 1.2% |

| Consumer Staples | 1.2% |

| Foreign Government | 1.0% |

| Closed-End Funds | 0.3% |

| Real Estate | 0.2% |

* | As a percentage of total investments excluding short‑term investments and all derivative contracts except for options purchased. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Multi-Asset Income Fund

Class K / PMFKX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Multi-Asset Income Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class K | $57 | 0.54% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class K shares at NAV returned 11.84%. For the same period, the Fund’s broad-based benchmarks, the MSCI All Country World NR Index (MSCI ACWI) and the Bloomberg U.S. Aggregate Bond Index, returned 17.02% and 5.10%, respectively. The performance benchmark, a blended benchmark (35% MSCI All Country World NR Index and 65% Bloomberg U.S. Aggregate Bond Index), returned 9.22% over the period.

Security selection and sector allocation both contributed positively to benchmark relative performance in the period, mainly due to positions in several international bank stocks as well as individual opportunities in industrials, energy, and information technology stocks. Fixed income selection and allocations to U.S. Treasury securities, securitized investments, and investment grade corporate bonds also contributed positively to benchmark relative performance.

The largest detractor from performance were positions in index futures, as a result of the positive performance of the equity markets during the period. The Fund maintains a significant position in equity-linked notes. The Fund holds positions in index futures in an effort to reduce risk associated with the equity-linked notes. Within fixed income, the Fund's overweight allocation to U.S. government agency bonds detracted from benchmark relative performance.

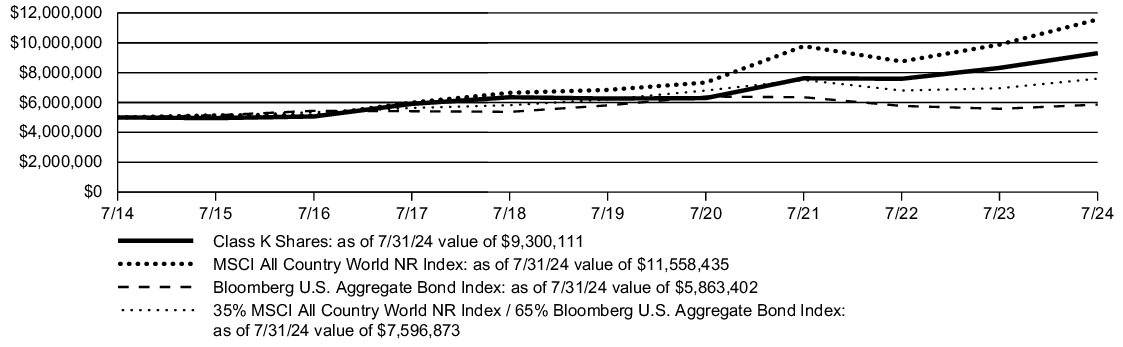

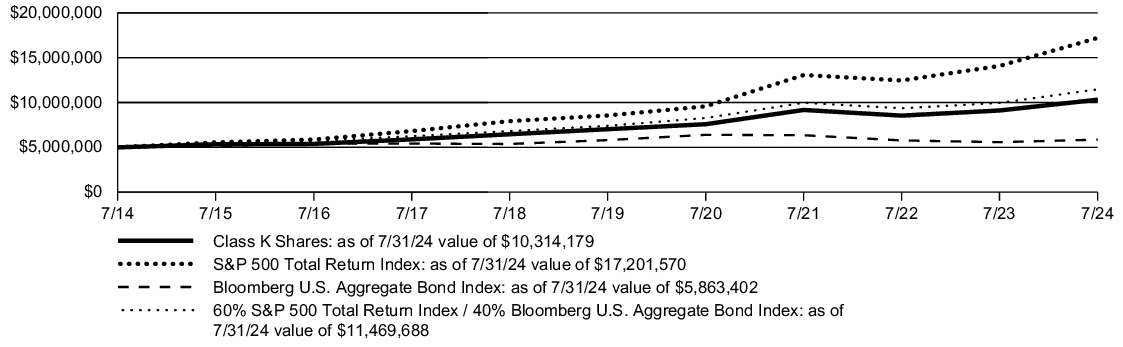

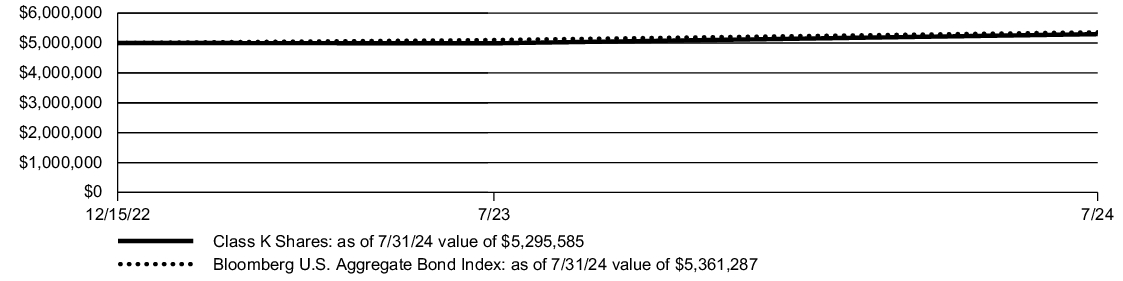

Fund Performance

The line graph below shows the change in value of a $5 Million investment made in Class K shares of the Fund during the periods shown, compared to that of the MSCI All Country World NR Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (65% MSCI All Country World NR Index and 35% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class K | 11.84% | 8.21% | 6.40% |

| MSCI All Country World NR Index | 17.02% | 11.05% | 8.74% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 35% MSCI All Country World NR Index / 65% Bloomberg U.S. Aggregate Bond Index | 9.22% | 4.13% | 4.27% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance shown for Class K shares for the period prior to the commencement of operations of Class K shares on December 1, 2014, is the net asset value performance of the Fund’s Class A shares, which has not been restated to reflect any differences in expenses, including Rule 12b-1 fees applicable to Class A shares. Since fees for Class A shares generally are higher than those of Class K shares, the performance of Class K shares prior to their inception on December 1, 2014, would have been higher than the performance shown. For the period beginning December 1, 2014, the actual performance of Class K shares is reflected.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $3,623,720,285% |

| Total number of portfolio holdings | $491%^^ |

| Total advisory fee paid | $13,905,080% |

| Portfolio turnover rate | $62% |

^^ | Excluding short‑term investments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Financials | 27.3% |

| U.S. Government | 12.2% |

| Energy | 10.3% |

| Information Technology | 9.8% |

| Basic Materials | 7.8% |

| Health Care | 6.3% |

| Consumer Discretionary | 4.6% |

| Industrials | 4.6% |

| Mortgage Securities | 3.9% |

| Asset Backed Securities | 2.8% |

| Utilities | 2.6% |

| Communication Services | 2.6% |

| Consumer, Cyclical | 1.3% |

| Consumer, Non-cyclical | 1.2% |

| Consumer Staples | 1.2% |

| Foreign Government | 1.0% |

| Closed-End Funds | 0.3% |

| Real Estate | 0.2% |

* | As a percentage of total investments excluding short‑term investments and all derivative contracts except for options purchased. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Multi-Asset Income Fund

Class R / PMFRX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Multi-Asset Income Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class R | $122 | 1.16% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class R shares at NAV returned 11.10%. For the same period, the Fund’s broad-based benchmarks, the MSCI All Country World NR Index (MSCI ACWI) and the Bloomberg U.S. Aggregate Bond Index, returned 17.02% and 5.10%, respectively. The performance benchmark, a blended benchmark (35% MSCI All Country World NR Index and 65% Bloomberg U.S. Aggregate Bond Index), returned 9.22% over the period.

Security selection and sector allocation both contributed positively to benchmark relative performance in the period, mainly due to positions in several international bank stocks as well as individual opportunities in industrials, energy, and information technology stocks. Fixed income selection and allocations to U.S. Treasury securities, securitized investments, and investment grade corporate bonds also contributed positively to benchmark relative performance.

The largest detractor from performance were positions in index futures, as a result of the positive performance of the equity markets during the period. The Fund maintains a significant position in equity-linked notes. The Fund holds positions in index futures in an effort to reduce risk associated with the equity-linked notes. Within fixed income, the Fund's overweight allocation to U.S. government agency bonds detracted from benchmark relative performance.

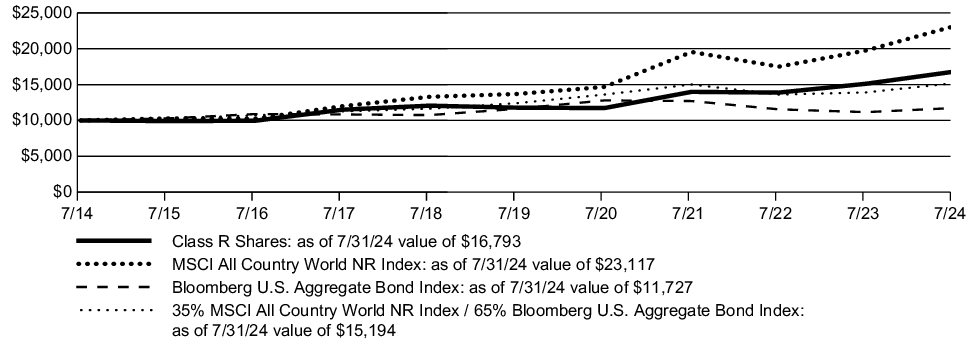

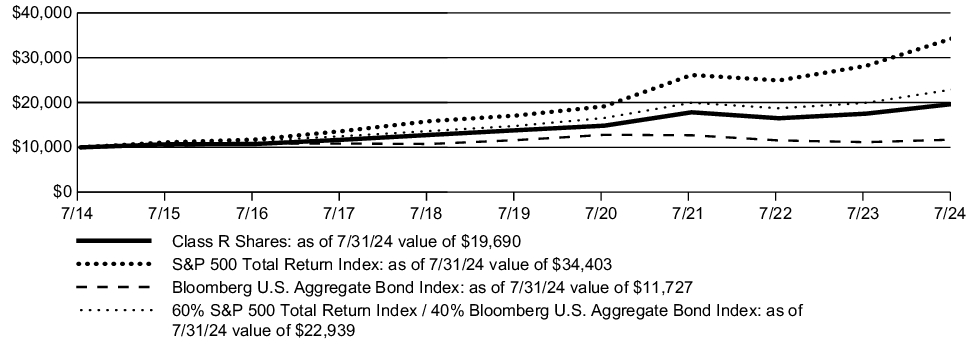

Fund Performance

The line graph below shows the change in value of a $10,000 investment made in Class R shares of the Fund during the periods shown, compared to that of the MSCI All Country World NR Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (65% MSCI All Country World NR Index and 35% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class R | 11.10% | 7.35% | 5.32% |

| MSCI All Country World NR Index | 17.02% | 11.05% | 8.74% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 35% MSCI All Country World NR Index / 65% Bloomberg U.S. Aggregate Bond Index | 9.22% | 4.13% | 4.27% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance shown for Class R shares for the period prior to the commencement of operations of Class R shares on December 1, 2014, is based on the performance of Class A shares, reduced to reflect the higher distribution and service fees of Class R shares. For the period beginning December 1, 2014, the actual performance of Class R shares is reflected.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $3,623,720,285% |

| Total number of portfolio holdings | $491%^^ |

| Total advisory fee paid | $13,905,080% |

| Portfolio turnover rate | $62% |

^^ | Excluding short‑term investments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Financials | 27.3% |

| U.S. Government | 12.2% |

| Energy | 10.3% |

| Information Technology | 9.8% |

| Basic Materials | 7.8% |

| Health Care | 6.3% |

| Consumer Discretionary | 4.6% |

| Industrials | 4.6% |

| Mortgage Securities | 3.9% |

| Asset Backed Securities | 2.8% |

| Utilities | 2.6% |

| Communication Services | 2.6% |

| Consumer, Cyclical | 1.3% |

| Consumer, Non-cyclical | 1.2% |

| Consumer Staples | 1.2% |

| Foreign Government | 1.0% |

| Closed-End Funds | 0.3% |

| Real Estate | 0.2% |

* | As a percentage of total investments excluding short‑term investments and all derivative contracts except for options purchased. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Multi-Asset Income Fund

Class Y / PMFYX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Multi-Asset Income Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class Y | $68 | 0.64% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class Y shares at NAV returned 11.80%. For the same period, the Fund’s broad-based benchmarks, the MSCI All Country World NR Index (MSCI ACWI) and the Bloomberg U.S. Aggregate Bond Index, returned 17.02% and 5.10%, respectively. The performance benchmark, a blended benchmark (35% MSCI All Country World NR Index and 65% Bloomberg U.S. Aggregate Bond Index), returned 9.22% over the period.

Security selection and sector allocation both contributed positively to benchmark relative performance in the period, mainly due to positions in several international bank stocks as well as individual opportunities in industrials, energy, and information technology stocks. Fixed income selection and allocations to U.S. Treasury securities, securitized investments, and investment grade corporate bonds also contributed positively to benchmark relative performance.

The largest detractor from performance were positions in index futures, as a result of the positive performance of the equity markets during the period. The Fund maintains a significant position in equity-linked notes. The Fund holds positions in index futures in an effort to reduce risk associated with the equity-linked notes. Within fixed income, the Fund's overweight allocation to U.S. government agency bonds detracted from benchmark relative performance.

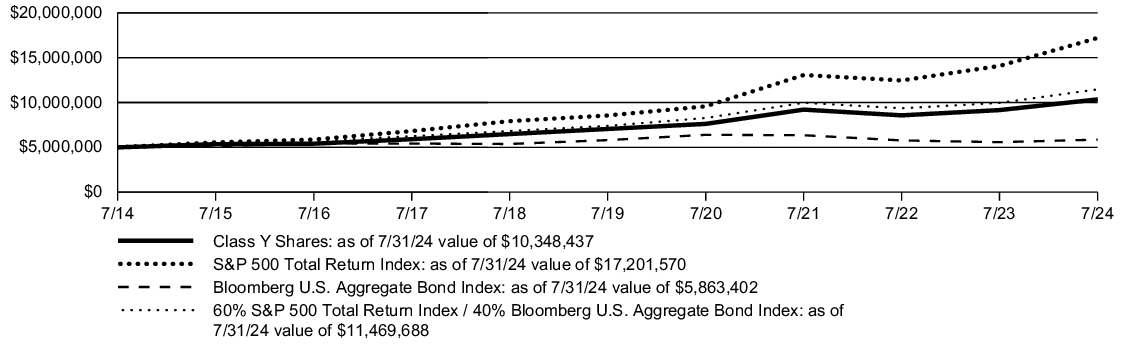

Fund Performance

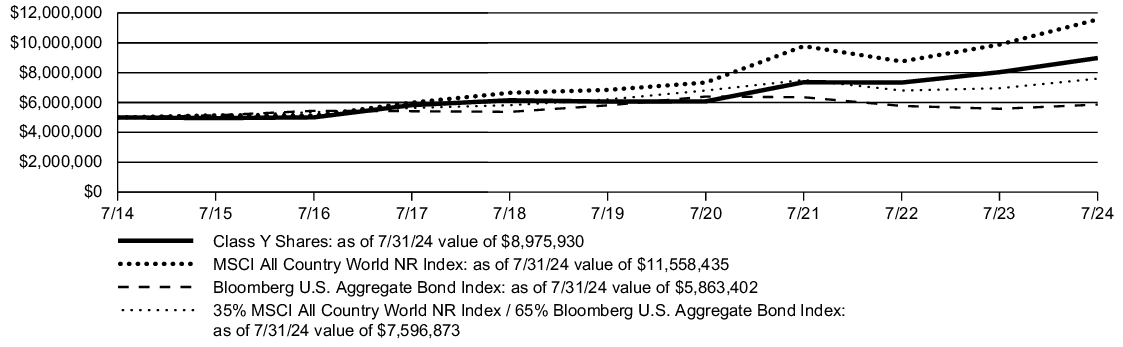

The line graph below shows the change in value of a $5 Million investment made in Class Y shares of the Fund during the periods shown, compared to that of the MSCI All Country World NR Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (65% MSCI All Country World NR Index and 35% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class Y | 11.80% | 8.16% | 6.03% |

| MSCI All Country World NR Index | 17.02% | 11.05% | 8.74% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 35% MSCI All Country World NR Index / 65% Bloomberg U.S. Aggregate Bond Index | 9.22% | 4.13% | 4.27% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $3,623,720,285% |

| Total number of portfolio holdings | $491%^^ |

| Total advisory fee paid | $13,905,080% |

| Portfolio turnover rate | $62% |

^^ | Excluding short‑term investments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Financials | 27.3% |

| U.S. Government | 12.2% |

| Energy | 10.3% |

| Information Technology | 9.8% |

| Basic Materials | 7.8% |

| Health Care | 6.3% |

| Consumer Discretionary | 4.6% |

| Industrials | 4.6% |

| Mortgage Securities | 3.9% |

| Asset Backed Securities | 2.8% |

| Utilities | 2.6% |

| Communication Services | 2.6% |

| Consumer, Cyclical | 1.3% |

| Consumer, Non-cyclical | 1.2% |

| Consumer Staples | 1.2% |

| Foreign Government | 1.0% |

| Closed-End Funds | 0.3% |

| Real Estate | 0.2% |

* | As a percentage of total investments excluding short‑term investments and all derivative contracts except for options purchased. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Balanced ESG Fund

Class A / AOBLX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Balanced ESG Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class A | $99 | 0.93% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class A shares at NAV returned 12.85%. For the same period, the Fund’s broad-based benchmarks, the Standard & Poor's 500 (S&P 500) Total Return Index and the Bloomberg U.S. Aggregate Bond Index, returned 22.15% and 5.10%, respectively. The performance benchmark, a blended benchmark (60% S&P 500 Total Return Index and 40% Bloomberg U.S. Aggregate Bond Index), returned 15.16% over the period.

Security selection in the equity portfolio was the primary detractor from benchmark relative performance in the period, mainly due to weaker relative selection in the information technology sector. An overweight to Asset Backed Securities and Collateralized Mortgage Obligations also detracted from relative returns.

Sector allocation decisions contributed to Fund performance overall due to an underweight to U.S. Treasury Securities and U.S. Government Agency-issued Mortgage-Backed Securities. Additionally, security selection in corporate bonds was additive to relative returns.

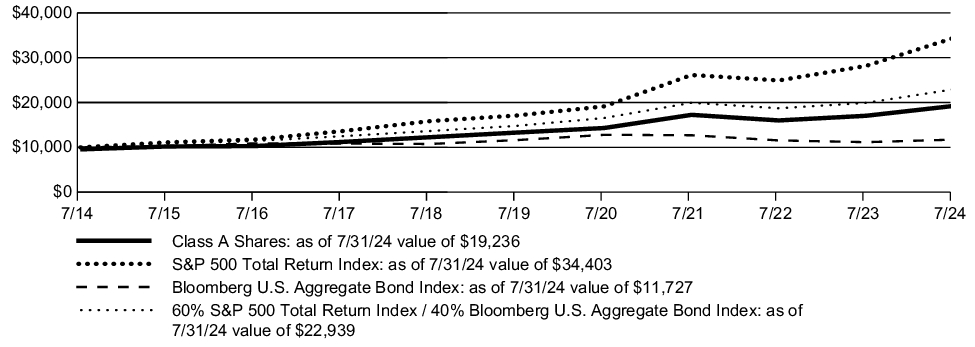

Fund Performance

The line graph below shows the change in value of a $10,000 investment made in Class A shares of the Fund at public offering price during the periods shown, compared to that of the S&P 500 Total Return Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (60% S&P 500 Total Return Index and 40% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class A (with sales charge) | 7.76% | 6.67% | 6.76% |

| Class A (without sales charge) | 12.85% | 7.66% | 7.25% |

| S&P 500 Total Return Index | 22.15% | 15.00% | 13.15% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 60% S&P 500 Total Return Index / 40% Bloomberg U.S. Aggregate Bond Index | 15.16% | 9.16% | 8.66% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $426,709,956% |

| Total number of portfolio holdings | $678%^^ |

| Total advisory fee paid | $2,043,303% |

| Portfolio turnover rate | $33% |

^^ | Excluding short-term investments, TBA sale commitments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Information Technology | 17.7% |

| U.S. Government | 17.0% |

| Financials | 14.1% |

| Health Care | 9.6% |

| Industrials | 8.0% |

| Communication Services | 6.7% |

| Energy | 4.5% |

| Basic Materials | 4.0% |

| Mortgage Securities | 3.9% |

| Consumer Discretionary | 3.5% |

| Consumer Staples | 3.0% |

| Asset Backed Securities | 2.9% |

| Real Estate | 1.5% |

| Consumer, Cyclical | 1.2% |

| Consumer, Non-cyclical | 0.9% |

| Utilities | 0.9% |

| Affiliated Closed-End Fund∞ | 0.3% |

| Foreign Government | 0.2% |

| Government | 0.1% |

* | As a percentage of total investments excluding short‑term investments, TBA sale commitments and all derivative contracts except for options purchased. |

∞ | Pioneer ILS Interval Fund is an affiliated closed-end fund managed by Amundi Asset Management US, Inc. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Balanced ESG Fund

Class C / PCBCX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Balanced ESG Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class C | $178 | 1.68% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class C shares at NAV returned 11.95%. For the same period, the Fund’s broad-based benchmarks, the Standard & Poor's 500 (S&P 500) Total Return Index and the Bloomberg U.S. Aggregate Bond Index, returned 22.15% and 5.10%, respectively. The performance benchmark, a blended benchmark (60% S&P 500 Total Return Index and 40% Bloomberg U.S. Aggregate Bond Index), returned 15.16% over the period.

Security selection in the equity portfolio was the primary detractor from benchmark relative performance in the period, mainly due to weaker relative selection in the information technology sector. An overweight to Asset Backed Securities and Collateralized Mortgage Obligations also detracted from relative returns.

Sector allocation decisions contributed to Fund performance overall due to an underweight to U.S. Treasury Securities and U.S. Government Agency-issued Mortgage-Backed Securities. Additionally, security selection in corporate bonds was additive to relative returns.

Fund Performance

The line graph below shows the change in value of a $10,000 investment made in Class C shares of the Fund during the periods shown, compared to that of the S&P 500 Total Return Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (60% S&P 500 Total Return Index and 40% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class C (with contingent deferred sales charge) | 10.95% | 6.84% | 6.45% |

| Class C (without contingent deferred sales charge) | 11.95% | 6.84% | 6.45% |

| S&P 500 Total Return Index | 22.15% | 15.00% | 13.15% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 60% S&P 500 Total Return Index / 40% Bloomberg U.S. Aggregate Bond Index | 15.16% | 9.16% | 8.66% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $426,709,956% |

| Total number of portfolio holdings | $678%^^ |

| Total advisory fee paid | $2,043,303% |

| Portfolio turnover rate | $33% |

^^ | Excluding short-term investments, TBA sale commitments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Information Technology | 17.7% |

| U.S. Government | 17.0% |

| Financials | 14.1% |

| Health Care | 9.6% |

| Industrials | 8.0% |

| Communication Services | 6.7% |

| Energy | 4.5% |

| Basic Materials | 4.0% |

| Mortgage Securities | 3.9% |

| Consumer Discretionary | 3.5% |

| Consumer Staples | 3.0% |

| Asset Backed Securities | 2.9% |

| Real Estate | 1.5% |

| Consumer, Cyclical | 1.2% |

| Consumer, Non-cyclical | 0.9% |

| Utilities | 0.9% |

| Affiliated Closed-End Fund∞ | 0.3% |

| Foreign Government | 0.2% |

| Government | 0.1% |

* | As a percentage of total investments excluding short‑term investments, TBA sale commitments and all derivative contracts except for options purchased. |

∞ | Pioneer ILS Interval Fund is an affiliated closed-end fund managed by Amundi Asset Management US, Inc. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants

On March 25, 2024, Ernst & Young LLP (the “Prior Auditor”) resigned as the independent registered public accounting firm of the Fund. There were no disagreements with the Prior Auditor during the two most recent fiscal years and the subsequent interim period through March 25, 2024.

On March 25, 2024, the Audit Committee of the Board approved, and on March 25, 2024, the Board approved, Deloitte & Touche LLP as the independent registered accounting firm of the Fund for fiscal periods ending after March 25, 2024.

Availability of Additional Information

You can find additional information about the Fund, including the Fund's prospectus, financial information, holdings and proxy voting information, at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1‑800‑225‑6292.

Important notice to shareholders

In order to reduce expenses, we will deliver a single copy of prospectuses, proxies, financial reports and other communications to shareholders with the same residential address, provided they have the same last name or we reasonably believe them to be members of the same family. Unless we are notified otherwise, we will continue to send recipients only one copy of these materials for as long as they remain a shareholder of the Fund. If you would like to receive individual mailings, please call 1-800-225-6292 and we will begin sending you separate copies of these materials within 30 days after receiving your request.

Pioneer Balanced ESG Fund

Class K / PCBKX

ANNUAL SHAREHOLDER REPORT | July 31, 2024

This annual shareholder report contains important information about Pioneer Balanced ESG Fund (“Fund”) for the period of August 1, 2023 to July 31, 2024. You can find additional information about the Fund at https://www.amundi.com/usinvestors/Resources/Shareholder-Reports. You can also request this information by contacting us at 1-800-225-6292. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last year?

(Based on a hypothetical $10,000 investment)

| Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

| Class K | $66 | 0.62% |

How did the Fund perform last year and what affected the Fund performance?

For the fiscal year ended July 31, 2024, the Fund’s Class K shares at NAV returned 13.19%. For the same period, the Fund’s broad-based benchmarks, the Standard & Poor's 500 (S&P 500) Total Return Index and the Bloomberg U.S. Aggregate Bond Index, returned 22.15% and 5.10%, respectively. The performance benchmark, a blended benchmark (60% S&P 500 Total Return Index and 40% Bloomberg U.S. Aggregate Bond Index), returned 15.16% over the period.

Security selection in the equity portfolio was the primary detractor from benchmark relative performance in the period, mainly due to weaker relative selection in the information technology sector. An overweight to Asset Backed Securities and Collateralized Mortgage Obligations also detracted from relative returns.

Sector allocation decisions contributed to Fund performance overall due to an underweight to U.S. Treasury Securities and U.S. Government Agency-issued Mortgage-Backed Securities. Additionally, security selection in corporate bonds was additive to relative returns.

Fund Performance

The line graph below shows the change in value of a $5 Million investment made in Class K shares of the Fund during the periods shown, compared to that of the S&P 500 Total Return Index, the Bloomberg U.S. Aggregate Bond Index, and the blended benchmark (60% S&P 500 Total Return Index and 40% Bloomberg U.S. Aggregate Bond Index).

| AVERAGE ANNUAL TOTAL RETURN | 1 Year | 5 Years | 10 Years |

| Class K | 13.19% | 7.98% | 7.51% |

| S&P 500 Total Return Index | 22.15% | 15.00% | 13.15% |

| Bloomberg U.S. Aggregate Bond Index | 5.10% | 0.19% | 1.61% |

| 60% S&P 500 Total Return Index / 40% Bloomberg U.S. Aggregate Bond Index | 15.16% | 9.16% | 8.66% |

Call 1-800-225-6292 or visit https://www.amundi.com/usinvestors/Resources/Shareholder-Reports for the most recent month-end performance results. Current performance may be lower or higher than the performance data quoted.

The performance shown for Class K shares for the period prior to the commencement of operations of Class K shares on December 1, 2015, is the net asset value performance of the Fund’s Class A shares, which has not been restated to reflect any differences in expenses, including Rule 12b-1 fees applicable to Class A shares. Since fees for Class A shares generally are higher than those of Class K shares, the performance of Class K shares prior to their inception on December 1, 2015, would have been higher than the performance shown. For the period beginning December 1, 2015, the actual performance of Class K shares is reflected.

The performance data quoted represents past performance, which is no guarantee of future results.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares.

KEY FUND STATISTICS

(as of July 31, 2024)

| Fund net assets | $426,709,956% |

| Total number of portfolio holdings | $678%^^ |

| Total advisory fee paid | $2,043,303% |

| Portfolio turnover rate | $33% |

^^ | Excluding short-term investments, TBA sale commitments and all derivative contracts except for options purchased. |

SECTOR DISTRIBUTION

(as of July 31, 2024)*

| Information Technology | 17.7% |

| U.S. Government | 17.0% |

| Financials | 14.1% |

| Health Care | 9.6% |

| Industrials | 8.0% |

| Communication Services | 6.7% |

| Energy | 4.5% |

| Basic Materials | 4.0% |

| Mortgage Securities | 3.9% |

| Consumer Discretionary | 3.5% |

| Consumer Staples | 3.0% |

| Asset Backed Securities | 2.9% |

| Real Estate | 1.5% |

| Consumer, Cyclical | 1.2% |

| Consumer, Non-cyclical | 0.9% |

| Utilities | 0.9% |

| Affiliated Closed-End Fund∞ | 0.3% |

| Foreign Government | 0.2% |

| Government | 0.1% |

* | As a percentage of total investments excluding short‑term investments, TBA sale commitments and all derivative contracts except for options purchased. |

∞ | Pioneer ILS Interval Fund is an affiliated closed-end fund managed by Amundi Asset Management US, Inc. |

Material Fund Changes

Amundi Asset Management US, Inc. (the “Adviser”), the Fund’s investment adviser, is currently an indirect, wholly-owned subsidiary of Amundi. On July 9, 2024, Amundi announced that it had entered into a definitive agreement with Victory Capital Holdings, Inc. (“Victory Capital”) to combine the Adviser with Victory Capital, and for Amundi to become a strategic shareholder of Victory Capital (the “Transaction”). Victory Capital is headquartered in San Antonio, Texas. The closing of the Transaction is subject to certain regulatory approvals and other conditions. There is no assurance that the Transaction will close.

The closing of the Transaction would cause the Fund’s current investment advisory agreement with the Adviser to terminate. Under the terms of the Transaction, the Fund’s Board of Trustees will be asked to approve a reorganization of the Fund into a corresponding, newly established Victory Fund advised by Victory Capital Management Inc., an affiliate of Victory Capital. The proposed reorganization of the Fund would be sought in connection with the closing of the Transaction. If approved by the Board, the proposal to reorganize the Fund will be submitted to the shareholders of the Fund for their approval. There is no assurance that the Board or the shareholders of the Fund will approve the proposal to reorganize the Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by December 1, 2024 at https://www.amundi.com/usinvestors/Products/Mutual-Funds or upon request at 1-800-225-6292.

Changes in Accountants