Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 1-32913

VeraSun Energy Corporation

(Exact name of registrant as specified in its charter)

| South Dakota | 20-3430241 | |

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification Number) |

| 110 N. Minnesota Ave, Suite 300 | ||

| Sioux Falls, SD | 57104 | |

| (Address of principal executive offices) | (Zip Code) |

605-978-7000

(Registrant’s telephone number, including area code)

NONE

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The number of shares of Common Stock outstanding on October 29, 2008 was 158,568,110.

Table of Contents

SEPTEMBER 30, 2008

INDEX TO FORM 10-Q

| PAGE NO. | ||

Item 1 —Financial Statements | ||

| 3 | ||

| 4 | ||

| 5 | ||

| 6 | ||

Item 2 —Management’s Discussion and Analysis of Financial Condition and Results of Operations | 42 | |

Item 3 —Quantitative and Qualitative Disclosures About Market Risk | 60 | |

Item 4 —Controls and Procedures | 63 | |

Item 1 —Legal Proceedings | 63 | |

Item 1A —Risk Factors | 63 | |

Item 2 —Unregistered Sales of Equity Securities and Use of Proceeds | 77 | |

Item 5 —Other Information | 77 | |

Item 6 —Exhibits | 77 | |

| 79 | ||

2

Table of Contents

| ITEM 1. | FINANCIAL STATEMENTS |

CONDENSED CONSOLIDATED BALANCE SHEETS

| September 30, 2008 | |||||||

| (unaudited) | December 31, 2007 | ||||||

| (dollars in thousands, except per share data) | |||||||

Assets | |||||||

Current Assets | |||||||

Cash and cash equivalents | $ | 9,326 | $ | 110,942 | |||

Restricted cash | 14,828 | — | |||||

Short-term investments | — | 43,175 | |||||

Trade receivables, less allowance for doubtful accounts of $419 and $95 in 2008 and 2007, respectively | 147,469 | 51,294 | |||||

Inventories | 183,107 | 107,912 | |||||

Prepaid expenses and other assets | 61,704 | 63,597 | |||||

Derivative financial instruments | 1,294 | 12,627 | |||||

Deferred income taxes | 3,787 | — | |||||

Total current assets | 421,515 | 389,547 | |||||

Goodwill | — | 169,629 | |||||

Other intangible assets | 33,803 | 21,668 | |||||

Other long-term assets | 13,623 | 15,572 | |||||

Debt issuance costs, net | 17,784 | 15,478 | |||||

| 65,210 | 222,347 | ||||||

Property and equipment, net | 2,426,136 | 1,251,612 | |||||

| $ | 2,912,861 | $ | 1,863,506 | ||||

Liabilities and Shareholders’ Equity | |||||||

Current Liabilities | |||||||

Current maturities of long-term debt | $ | 1,524,958 | $ | 16,774 | |||

Accounts payable | 173,547 | 120,814 | |||||

Accrued expenses and other liabilities | 85,289 | 11,138 | |||||

Derivative financial instruments | 14,512 | 11,299 | |||||

Deferred income taxes | — | 1,869 | |||||

Total current liabilities | 1,798,306 | 161,894 | |||||

Long-term debt, less current maturities | 10,931 | 888,696 | |||||

Deferred income taxes | 4,896 | 51,564 | |||||

Other long-term liabilities | 27,204 | 5,621 | |||||

Total long-term liabilities | 43,031 | 945,881 | |||||

Commitments and Contingencies | |||||||

Minority interest in consolidated subsidiary | 900 | — | |||||

Shareholders’ Equity | |||||||

Preferred stock, $0.01 par value; authorized 25,000,000 shares; none issued or outstanding | — | — | |||||

Common stock, $0.01 par value; authorized 350,000,000 and 250,000,000 shares at September 30, 2008, and December 31, 2007, respectively; 158,568,427 and 92,948,664 shares issued and outstanding as of September 30, 2008 and December 31, 2007, respectively | 1,586 | 929 | |||||

Additional paid-in capital | 1,397,485 | 638,606 | |||||

Retained (deficit) earnings | (328,447 | ) | 116,196 | ||||

| 1,070,624 | 755,731 | ||||||

| $ | 2,912,861 | $ | 1,863,506 | ||||

See Notes to Condensed Consolidated Financial Statements.

3

Table of Contents

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||||

| (dollars in thousands, except per share data) | ||||||||||||||||

Net sales | $ | 1,084,467 | $ | 221,868 | $ | 2,616,110 | $ | 535,934 | ||||||||

Cost of goods sold | (1,262,380 | ) | (198,474 | ) | (2,686,949 | ) | (470,811 | ) | ||||||||

Lower of cost or market adjustment | (40,107 | ) | — | (40,107 | ) | — | ||||||||||

Gross profit (loss) | (218,020 | ) | 23,394 | (110,946 | ) | 65,123 | ||||||||||

Startup expenses | 2,719 | 1,675 | 9,421 | 3,257 | ||||||||||||

Restructuring charge | 110 | — | 2,114 | — | ||||||||||||

Selling, general and administrative expenses | 21,280 | 9,862 | 48,961 | 28,211 | ||||||||||||

Goodwill impairment | 263,332 | — | 263,332 | — | ||||||||||||

Long-lived asset impairment | 121,218 | — | 121,218 | — | ||||||||||||

Total operating expenses | 408,659 | 11,537 | 445,046 | 31,468 | ||||||||||||

Operating income (loss) | (626,679 | ) | 11,857 | (555,992 | ) | 33,655 | ||||||||||

Other income (expense): | ||||||||||||||||

Interest expense | (28,692 | ) | (12,016 | ) | (55,006 | ) | (19,947 | ) | ||||||||

Interest income | 73 | 5,523 | 1,621 | 14,430 | ||||||||||||

Gain on extinguishment of debt | 3,743 | — | 3,743 | — | ||||||||||||

Other income | 576 | 4 | 1,290 | 36 | ||||||||||||

| (24,300 | ) | (6,489 | ) | (48,352 | ) | (5,481 | ) | |||||||||

Income (loss) before income taxes and minority interest | (650,979 | ) | 5,368 | (604,344 | ) | 28,174 | ||||||||||

Income tax provision (benefit) | (174,851 | ) | (2,425 | ) | (159,676 | ) | 5,557 | |||||||||

Income (loss) before minority interest | (476,128 | ) | 7,793 | (444,668 | ) | 22,617 | ||||||||||

Minority interest in net loss of subsidiary, net of income taxes | 19 | — | 25 | — | ||||||||||||

Net income (loss) | $ | (476,109 | ) | $ | 7,793 | $ | (444,643 | ) | $ | 22,617 | ||||||

Per share data: | ||||||||||||||||

Income (loss) per common share - basic | $ | (3.03 | ) | $ | 0.09 | $ | (3.28 | ) | $ | 0.29 | ||||||

Basic weighted average number of common shares | 157,135,926 | 85,177,689 | 135,660,386 | 79,329,665 | ||||||||||||

Income (loss) per common share - diluted | $ | (3.03 | ) | $ | 0.09 | $ | (3.28 | ) | $ | 0.27 | ||||||

Diluted weighted average number of common and common equivalent shares | 157,135,926 | 88,157,051 | 135,660,386 | 83,472,558 | ||||||||||||

See Notes to Condensed Consolidated Financial Statements.

4

Table of Contents

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

| Nine Months Ended September 30, | ||||||||

| 2008 | 2007 | |||||||

| (dollars in thousands) | ||||||||

Cash Flows from Operating Activities | ||||||||

Net income (loss) | $ | (444,643 | ) | $ | 22,617 | |||

Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | ||||||||

Goodwill impairment | 263,332 | — | ||||||

Deferred income taxes | (150,460 | ) | 11,017 | |||||

Long-lived asset impairment | 121,218 | — | ||||||

Depreciation | 53,381 | 11,120 | ||||||

Lower of cost or market adjustment | 40,107 | |||||||

Change in derivative financial instruments | 21,100 | 3,198 | ||||||

Stock-based compensation expense | 6,311 | 4,356 | ||||||

Accretion of contracts and long-term debt fair valued during purchase accounting | (4,518 | ) | — | |||||

Gain on extinguishment of debt | (3,743 | ) | — | |||||

Amortization of other intangible assets | 3,273 | — | ||||||

Amortization of debt issuance cost and debt discount | 2,253 | 1,357 | ||||||

Gain on disposal of equipment | (370 | ) | (82 | ) | ||||

Accretion of deferred revenue | (147 | ) | (71 | ) | ||||

Minority interest in net loss of subsidiary | (25 | ) | — | |||||

Excess tax benefits from share-based payment arrangements | — | (8,424 | ) | |||||

Changes in current assets and liabilities, net of effects of business aquisition | ||||||||

Trade receivables | (38,794 | ) | (2,928 | ) | ||||

Inventories | (17,397 | ) | (29,193 | ) | ||||

Prepaid expenses and other assets | 13,405 | (3,335 | ) | |||||

Accounts payable | 52,486 | 39,476 | ||||||

Accrued expenses and other liabilities | 4,669 | 24,538 | ||||||

Net cash (used in) provided by operating activities | (78,562 | ) | 73,646 | |||||

Cash Flows from Investing Activities | ||||||||

Purchases of property and equipment | (264,991 | ) | (303,241 | ) | ||||

Acquisitions, net of transaction costs | 44,359 | (242,775 | ) | |||||

Proceeds from the sale of short-term investments | 43,175 | — | ||||||

Change in restricted cash | (14,828 | ) | — | |||||

Proceeds from sales of property and equipment | 1,300 | 6 | ||||||

Payments for other long-term assets and liabilities | (382 | ) | (6,496 | ) | ||||

Net cash used in investing activities | (191,367 | ) | (552,506 | ) | ||||

Cash Flows from Financing Activities | ||||||||

Proceeds from long-term debt | 195,445 | 471,367 | ||||||

Principal payments on long-term debt | (21,004 | ) | — | |||||

Debt issuance costs paid | (3,779 | ) | (11,539 | ) | ||||

Cost of registering equity securities | (2,127 | ) | (5 | ) | ||||

Net effect of the exercise of stock options | (222 | ) | — | |||||

Excess tax benefits from share-based payment arrangements | — | 8,424 | ||||||

Net proceeds from the issuance of 2,934,747 shares of common stock | — | 12,784 | ||||||

Net cash provided by financing activities | 168,313 | 481,031 | ||||||

Net (decrease) increase in cash and cash equivalents | (101,616 | ) | 2,171 | |||||

Cash and Cash Equivalents | ||||||||

Beginning of period | 110,942 | 318,049 | ||||||

End of period | $ | 9,326 | $ | 320,220 | ||||

See Notes to Condensed Consolidated Financial Statements.

5

Table of Contents

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

Note 1. Nature of Business and Basis of Presentation

Nature of Business

VeraSun Energy Corporation, a South Dakota corporation, together with its subsidiaries, is one of the largest ethanol producers in the United States based on production capacity, according to Renewable Fuels Association (“RFA”) data. VeraSun focuses primarily on the production and sale of ethanol and its co-products.

Basis of Presentation and Going Concern Considerations

The accompanying condensed consolidated balance sheet as of December 31, 2007 has been derived from audited consolidated financial statements. The unaudited condensed consolidated financial statements present the accounts of VeraSun Energy Corporation, a South Dakota corporation, and its wholly-owned subsidiaries, including, since April 1, 2008 (see Note 2), US BioEnergy Corporation (“US BioEnergy”), and US BioEnergy’s joint venture Big River Resources Grinnell, LLC (“Grinnell”). Except as the context requires or as stated otherwise, “VeraSun,” the “Company,” “we,” “us” and “our” refer to VeraSun Energy Corporation, its subsidiaries and Grinnell, collectively. The unaudited interim condensed consolidated financial statements of VeraSun reflect all recurring and non-recurring adjustments that are, in the opinion of our management, necessary for a fair presentation of VeraSun’s consolidated financial position, results of operations and cash flows. Refer to Note 3 “Goodwill and Other Identifiable Intangible Assets,” Note 4 “Impairment of Long-Lived Assets” and Note 6 “Inventories” for information on non-recurring adjustments. The results for the nine months ended September 30, 2008 are not necessarily indicative of the results that may be expected for a full fiscal year. Certain information and note disclosures normally included in annual consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) have been condensed or omitted pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”), although the Company believes that the disclosures made are adequate to make the information not misleading. These condensed consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements and notes thereto included in its annual report for the year ended December 31, 2007 filed on Form 10-K with the SEC.

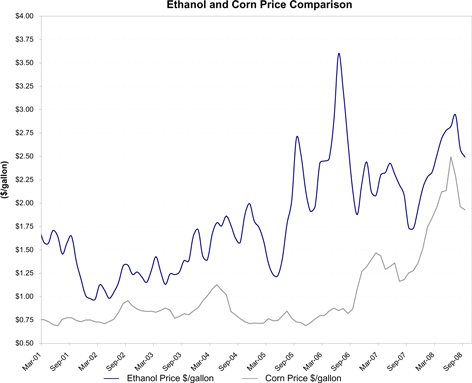

During the third quarter of 2008, the Company suffered a significant loss from operations as a result of various factors including dramatic changes in corn costs and falling ethanol prices. Subsequent to September 30, 2008, we continue to suffer operating losses primarily due to the relative prices of ethanol and corn. Such losses,combined with worsening capital market conditions and a tightening of trade credit, resulted in severe constraints on the Company’s liquidity position. Faced with these constraints, on October 31, 2008, VeraSun Energy Corporation and 24 of its subsidiaries, which include all of VeraSun Energy Corporation’s material subsidiaries, filed voluntary petitions for relief (collectively, the “Bankruptcy Filing”) under Chapter 11 (“Chapter 11”) of the United States Bankruptcy Code (the “Bankruptcy Code”) with the United States Bankruptcy Court for the District of Delaware (the “Bankruptcy Court”). VeraSun intends to continue to operate its business as debtor-in-possession under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code and orders of the Bankruptcy Court. See Note 15 “Subsequent Events,” for details regarding the Bankruptcy Filing and the Chapter 11 cases. The accompanying unaudited condensed consolidated financial statements have been prepared assuming we will continue as a going concern, which assumes continuity of operations and realization of assets and satisfaction of liabilities in the ordinary course of business. Our ability to continue as a going concern is dependent upon, among other things, (i) our ability to secure adequate debtor-in-possession financing; (ii) our ability to comply with the terms and conditions of any debtor-in-possession financing and any cash collateral order entered by the Bankruptcy Court in connection with the Chapter 11 cases; (iii) our ability to maintain adequate cash on hand; (iv) our ability to generate cash from operations; (v) our ability to obtain confirmation of and to consummate a plan of reorganization under the Bankruptcy Code; (vi) the cost, duration and outcome of the reorganization process; and (vii) our ability to achieve profitability. Uncertainty as to the outcome of these factors raises substantial doubt about the Company’s ability to continue as a going concern. We are currently evaluating various courses of action to address the operational and liquidity issues the Company is facing and are in the process of attempting to secure debtor-in-possession financing, as described in Note 15, and formulating plans for improving operations. There can be no assurance that any of these efforts will be successful. The accompanying consolidated financial statements do not include any adjustments that might result should we be unable to continue as a going concern.

American Institute of Certified Public Accountants Statement of Position 90-7, “Financial Reporting by Entities in Reorganization under the Bankruptcy Code” (SOP 90-7), which is applicable to companies in Chapter 11, generally does not change the manner in which financial statements are prepared. However, it does require that the financial statements for periods subsequent to the filing of the Chapter 11 petition distinguish transactions and events that are directly associated with the reorganization from the ongoing operations of the business. Revenues, expenses (including professional fees), realized gains and losses, and provisions for losses that can be directly associated with the reorganization and restructuring of the business must be reported separately as

6

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

reorganization items in the consolidated statements of operations beginning in the quarter ending December 31, 2008. The consolidated balance sheet must distinguish pre-petition liabilities subject to compromise from both those pre-petition liabilities that are not subject to compromise and from post-petition liabilities. Liabilities that may be affected by the plan must be reported at the amounts expected to be allowed, even if they may be settled for lesser amounts. In addition, cash provided by reorganization items must be disclosed separately in the condensed consolidated statement of cash flows. VeraSun adopted SOP 90-7 effective on October 31, 2008 and will segregate those items as outlined above for all reporting periods subsequent to such date.

Principles of Consolidation

The accompanying condensed consolidated financial statements include the accounts of VeraSun Energy Corporation and its subsidiaries. All intercompany balances and transactions have been eliminated on consolidation. See Note 2 for disclosures related to acquisitions in the second quarter of 2008 and the third quarter of 2007.

Reclassifications

The accompanying consolidated financial statements contain certain reclassifications to conform to the presentation used in the current period. The reclassification had no impact on shareholders’ equity, working capital, gross profit or net income.

Revenue Recognition

Revenue from the production of ethanol and distillers grains is recorded when title transfers to customers. Shipping and handling charges to customers are included in revenues. In accordance with our marketing agreements with Provista Renewable Fuels Marketing, LLC (“Provista”) that terminated in August 2008, certain sales from April 1, 2008 through August 31, 2008 were recorded when products were shipped from our production facilities, net of commissions retained by Provista. Our sales of ethanol, with the exception of sales from our plants in Bloomingburg, Ohio; Linden, Indiana; Marion, South Dakota; and Albion, Nebraska, which are recognized upon shipment from these plants, net of commissions retained by Cargill, Inc. and Archer-Daniels-Midland Co. under marketing agreements, are now recognized upon delivery to our customers at terminals or other locations.

We receive incentives to produce ethanol from state and federal entities. In accordance with the terms of these arrangements, incentive income is recognized when we produce ethanol or blend ethanol with gasoline to produce E85. For the three and nine months ending September 30, 2008, incentive revenue was $1,663 and $7,017 respectively, compared to $1,134 and $2,571 for the three and nine months ended September 30, 2007, respectively.

Net sales to three customers represented approximately 22%, 15%, and 12% of the Company’s net sales for the nine months ended September 30, 2008. At September 30, 2008, accounts receivable balance from these customers accounted for 43% of total trade receivable.

Derivatives and Hedging Activities

Derivatives are recognized on the balance sheet at their fair value and are included in the accompanying balance sheets as “Derivative financial instruments”. On the date the derivative contract is entered into, the Company may designate the derivative as a hedge of a forecasted transaction or of the variability of cash flows to be received or paid related to a recognized asset or liability (“cash flow” hedge). Changes in the fair value of a derivative that is highly effective and that is designated and qualifies as a cash flow hedge are recorded in other comprehensive income, net of tax effect, until earnings are affected by the variability of cash flows (e.g., when periodic settlements on a variable rate asset or liability are recorded in earnings). Changes in the fair value of undesignated derivative instruments are reported in current period earnings.

Prior to September 1, 2008, in connection with the execution of forward purchase contracts, the Company normally elected to create a hedging relationship by selling an exchange traded futures contract as an offsetting position. In this situation, the forward purchase contract was designated to be valued at market price until delivery was made against the contract. During the third quarter of 2008, the Company chose to exit a majority of offsetting futures contracts due to unacceptable margin exposure. The corresponding forward purchase contracts are continuing to be marked to market until their settlement. The Company has elected not to establish hedging relationships for forward purchase contracts executed during the third quarter of 2008 subsequent to August 31, 2008. Since the Company has elected the normal purchase normal sale exception, forward purchase contracts not hedged are not subject to accounting requirements under SFAS 133—Accounting for Derivative Instruments and Hedging Activities and, accordingly, are not marked to market. In circumstances where we estimate that our cash contract value cannot be recovered through the sale of ethanol, we record a loss on the contract classified as “Lower of cost or market adjustment” in the accompanying condensed consolidated statements of operations and the resulting liability classified as accrued expenses in the accompanying condensed consolidated balance sheet. Losses are calculated using a lower of cost or market approach, similar to inventory.

7

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

The Company continues to formally document all relationships between hedging instruments and hedged items, as well as its risk-management objectives and strategy for undertaking various hedged transactions. This process includes linking all derivatives that are designated as cash flow hedges to specific assets and liabilities on the balance sheet or to specific firm commitments or forecasted transactions. The Company also formally assesses, both at the hedge’s inception and on an ongoing basis, whether the derivatives that are used in hedging transactions are highly effective in offsetting changes in cash flows of hedged items.

When hedge accounting is discontinued because it is probable that a forecasted transaction will not occur, the derivative will continue to be carried on the balance sheet at its fair value, and gains and losses that were accumulated in other comprehensive income will be recognized immediately in earnings. In all other situations in which hedge accounting is discontinued, the derivative will be carried at its fair value on the balance sheet, with subsequent changes in its fair value recognized in current-period income. The Company’s derivative positions related to corn are undesignated instruments where changes in the fair value of these economic hedges are included in cost of goods sold in the income statements. Income statement effects of unleaded gasoline futures contracts and natural gas futures contracts are included in net sales and cost of goods sold, respectively.

The Company recorded corn related derivatives losses of $118,584 and $114,316 during the three months and nine months ended September 30, 2008, respectively, compared to gains of $13,724 and $5,674 for the three months ended and nine months ended September 30, 2007, respectively. The losses are attributable to unrealized mark-to-market open positions of forward purchase and futures contracts, realized hedging losses on exiting futures contracts, and settled forward purchase contracts. Unrealized mark-to-market losses accounted for $42,254 and $12,275 of this derivative loss for the three months and nine months ended September 30, 2008, respectively, compared to no gain or loss and $72 for the three months and nine months ended September 30, 2007. Losses due to realized positions account for $76,330 and $102,041 for the three months and nine months ended September 30, 2008, respectively, compared to a net gain of $13,724 and $5,602 for the three months and nine months ended September 30, 2007, respectively. These losses are included in Cost of goods sold.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect (i) the reported amounts of assets and liabilities, (ii) the disclosure of contingent assets and liabilities at the date of the financial statements, and (iii) the reported amounts of revenues and expenses during the reporting period.

We use estimates and assumptions in accounting for the following significant matters, among others:

| • | Allowances for doubtful accounts |

| • | Inventory valuation and allowances |

| • | Valuation of acquired assets and liabilities |

| • | Fair value of derivative financial instruments and related hedged items |

| • | Accrued losses on forward purchase and sales contracts |

| • | Useful lives of property and equipment and intangible assets |

| • | Asset retirement obligations |

| • | Goodwill and other long-lived asset impairments |

| • | Accounting for assets to be sold and related purchase order obligations |

| • | Contingencies |

| • | Fair value of options and restricted stock granted under our stock-based compensation plans |

8

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

| • | Tax related items |

Actual results may differ from previously estimated amounts, and such differences may be material to our condensed consolidated financial statements. We periodically review estimates and assumptions, and the effects of revisions are reflected in the period in which the revision is made. The revisions to estimates or assumptions during the periods presented in the accompanying condensed consolidated financial statements were not considered to be significant.

Recently Issued Accounting Pronouncements:

In February 2008, the FASB issued “Effective Date of FASB Statement No. 157” FASB Staff Position (FSP) No. 157-2 (FSP No. 157-2). FSP No. 157-2 delays the effective date of SFAS No. 157 until fiscal years beginning after November 15, 2008, for fair value measurements of non-financial assets and non-financial liabilities, except for items that are recognized or disclosed at fair value in an entity’s financial statements on a recurring basis (at least annually).

As of January 1, 2008, the Company adopted SFAS No. 157 for all assets and liabilities measured at fair value except for non-financial assets and non-financial liabilities measured at fair value on a non-recurring basis, as permitted by FSP No. 157-2. The adoption did not have a material impact on the Company’s consolidated financial statements. For additional discussion and SFAS No. 157 required disclosures see Note 7 to these condensed consolidated financial statements.

In February 2007, the FASB issued “The Fair Value Option for Financial Assets and Financial Liabilities — Including an Amendment of FASB Statement No. 115” (SFAS No. 159), which provides companies with an option to measure, at specified election dates, many financial instruments and certain other items at fair value that are not currently measured at fair value. A company that adopts SFAS No. 159 will report unrealized gains and losses on items for which the fair value option has been elected in earnings at each subsequent reporting date. This statement also establishes presentation and disclosure requirements designed to facilitate comparisons between entities that choose different measurement attributes for similar types of assets and liabilities. This statement is effective for fiscal years beginning after November 15, 2007. Effective January 1, 2008, the Company adopted SFAS No. 159 but did not elect fair value as an alternative.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations.” This statement significantly changes the financial accounting and reporting of business combination transactions. The provisions of this statement are to be applied prospectively to business combination transactions in the first annual reporting period beginning on or after December 15, 2008. The Company is currently assessing the impact of the adoption this will have on our consolidated financial statements.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements”, (SFAS No. 160), which amends Accounting Research Bulletin No. 51. SFAS No. 160 improves the relevance, comparability, and transparency of financial information provided to investors by requiring all entities to report noncontrolling (minority) interests in subsidiaries as equity in the consolidated financial statements. This statement is effective for fiscal years beginning after December 15, 2008, and early adoption is not permitted. The provisions of this standard must be applied retrospectively upon adoption. The Company has assessed SFAS No. 160 and has determined that the impact of the adoption of this statement will result in minority interest being reported as a component of shareholders’ equity, but separate from VeraSun Energy Corporation’s equity.

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities” (“SFAS No. 161”). The new standard is intended to improve financial reporting about derivative instruments and hedging activities by requiring enhanced disclosures to enable investors to better understand their effects on an entity’s financial position, financial performance, and cash flows. It is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008, with early application encouraged. We do not expect the adoption of SFAS No. 161 to have a material impact on our consolidated financial statements. However, we are still in the process of evaluating the impact of adopting SFAS No. 161.

In April 2008, the FASB released FSP No. 142-3, “Determination of the Useful Life of Intangible Assets. “ This FSP requires entities to disclose information for recognized intangible assets that enable users of financial statements to understand the extent to which expected future cash flows associated with intangible assets are affected by the entity’s intent or ability to renew or extend the arrangement associated with the intangible asset. This FSP also amends the factors an entity should consider in developing the renewal or extension assumptions used in determining the useful life of recognized intangible assets under SFAS No. 142, “Goodwill and Other Intangible Assets.” This FSP will be applied prospectively only to intangible assets acquired after the FSP’s effective date, but the disclosure requirements will be applied prospectively to all intangible assets as of the FSP’s effective date. This FSP is effective for fiscal years beginning after December 15, 2008 and early adoption is not permitted. The Company is currently assessing the impact the adoption of the FSP will have on its consolidated financial statements.

9

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

In September 2008, the FASB issued FSP No. 133-1 and FIN 45-4, “Disclosures about Credit Derivatives and Certain Guarantees: An Amendment of FASB Statement No. 133 and FASB Interpretation No. 45; and Clarification of the Effective Date of FASB Statement No. 161.” This FSP is intended to improve disclosures about credit derivatives by requiring more information about the potential adverse effects of changes in credit risk on the financial position, financial performance, and cash flows of the sellers of credit derivatives. This FSP amends FASB Statement No. 133, Accounting for Derivative Instruments and Hedging Activities, to require disclosures by sellers of credit derivatives, including credit derivatives embedded in hybrid instruments. This FSP also amends FASB Interpretation (FIN) No. 45, Guarantor’s Accounting and Disclosure Requirements for Guarantees, Including Indirect Guarantees of Indebtedness to Others, to require an additional disclosure about the current status of the payment/performance risk of a guarantee. The provisions of the FSP that amend Statement 133 and FIN 45 are effective for reporting periods (annual or interim) ending after November 15, 2008. Finally, this FSP clarifies the effective date in SFAS No. 161. The disclosures required by SFAS No. 161 should be provided for any reporting period (annual or quarterly interim) beginning after November 15, 2008. This clarification of the effective date of SFAS No. 161 is effective upon issuance of the FSP. The Company is currently assessing the impact the adoption of the FSP will have on its consolidated financial statements.

Note 2. Business Combinations

US BioEnergy Acquisition

On April 1, 2008, the Company acquired 100% of the outstanding common stock of US BioEnergy for an aggregate purchase price of $757,645, consisting of the value of the common stock issued, stock option awards under which approximately 1.8 million shares of common stock are issuable upon the future exercise of the stock options and transaction costs. Under the merger agreement, 0.81 shares of the Company’s common stock were issued for each outstanding share of US BioEnergy common stock. This transaction is referred to in this document as the “US BioEnergy Acquisition.” The existing VeraSun shares remained outstanding and represented approximately 60 percent of the shares outstanding after the acquisition. A breakdown of the aggregated purchase price is as follows:

Number of shares of US BioEnergy common stock outstanding at the closing date of the merger (in thousands) | 79,986 | ||||||

Exchange ratio | 0.81 | ||||||

Shares of VeraSun issued (in thousands) | 64,789 | ||||||

| Multiplied by VeraSun’s weighted average stock price for the period two business days before and three business days after the November 29, 2007 announcement of acquisition | $ | 11.36 | $ | 736,001 | |||

| Fair value of VeraSun’s stock options issued in exchange for US BioEnergy’s stock options outstanding as of the closing date of the merger | 14,664 | ||||||

Other, including VeraSun’s transaction (registering and issuing) costs | 8,397 | ||||||

Less: Cost of registering equity securities | (1,417 | ) | |||||

Purchase price | $ | 757,645 | |||||

The fair value of VeraSun’s options issued in exchange for US BioEnergy’s stock options was determined using the Black-Scholes option pricing model with the following assumptions: dividend yield of 0.0%; expected volatility of 65%; risk-free rate of 3.0%; and an expected life of 6.9 years.

The acquisition was an opportunity for two leading companies in the renewable fuels industry to capitalize on synergies and provide value for shareholders. It also underscored the commitment of each company to execute on its growth strategy to become a large-scale, low-cost ethanol producer. The merger was expected to create a unique and stronger business platform by improving access to capital and allowing the combined company to leverage technology and operating experience across its entire plant fleet.

The excess of purchase price over the estimated fair value of identifiable net assets acquired was classified as goodwill. The major factors that contributed to goodwill included the expected future profitability of US BioEnergy, the market position of US BioEnergy, its existing facilities and plants under construction given their geographic locations, and its successful track record of plant start-ups and completions. Refer to Note 3 for the Company’s goodwill impairment evaluation performed as of the end of the third quarter of fiscal year 2008.

10

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

Through the US BioEnergy Acquisition, the Company acquired five operating ethanol production facilities: Albert City, Iowa, with a capacity of 110 MMGY; Woodbury, Michigan, with a capacity of 50 MMGY; Central City and Ord, Nebraska, with capacities of 100 MMGY and 50 MMGY, respectively; and Marion, South Dakota, with a capacity of 110 MMGY. The Hankinson, North Dakota facility, with a capacity of 110 MMGY, was completed in June of 2008 and became operational on July 21, 2008. The Dyersville, Iowa facility, with a capacity of 110 MMGY, became operational on September 5, 2008. The start-up of the Janesville, Minnesota facility, which is expected to have a capacity of 110 MMGY, has been delayed indefinitely because the financing necessary to continue construction and start-up activities, which we had anticipated would be available under existing project financing and credit lines, has not been forthcoming due to the Bankruptcy Filing (see Note 15). US BioEnergy’s primary products are ethanol and distillers grains, which it derives from corn. At the acquisition date, all ethanol produced by US BioEnergy was sold to Provista, an ethanol marketing company owned by CHS, Inc, except ethanol produced at the Marion, South Dakota facility, which is sold to Archer-Daniels–Midland Co. Effective August 31, 2008, the Company terminated its marketing agreement with Provista.

The acquired assets of the US BioEnergy Acquisition have been included in the condensed consolidated balance sheet as of September 30, 2008, and the operations of US BioEnergy are included in the Company’s condensed consolidated statement of operations beginning April 1, 2008.

In accordance with Statement of Financial Accounting Standards No. 141, “Business Combinations,” the Company recorded this acquisition using the purchase method of accounting. The purchase price has been allocated to tangible and identifiable intangible assets acquired and liabilities assumed based on their respective fair values as of April 1, 2008. The excess purchase price over the fair value of tangible and intangible assets acquired and liabilities assumed was recorded as goodwill, of which approximately $21,000 was considered deductible for tax purposes. Adjustments have been made to the preliminary allocation as reported as of June 30, 2008, primarily relating to the finalizing the fair value of property, plant, and equipment, fair value of identifiable intangibles, fair value of various ethanol, distiller, and rail car contracts, tax incentive credits, and transaction cost. The adjustments had an impact of decreasing goodwill by $3,447, increasing other non-current assets by $1,328, decreasing property, plant, and equipment by $520, decreasing other long-term liabilities, deferred tax liability, and minority interest in consolidated subsidiary by $300, $97, and $2,989, respectively. The following sets forth the allocation of the purchase consideration:

Cash | $ | 51,339 | |

Other current assets | 142,917 | ||

Property, plant and equipment | 1,068,830 | ||

Intangible assets | 55,694 | ||

Goodwill | 98,326 | ||

Other non-current assets | 7,899 | ||

Total assets acquired | 1,425,005 | ||

Current liabilities, excluding current maturities on long-term debt | 85,055 | ||

Long-term debt | 460,979 | ||

Deferred tax liability | 101,314 | ||

Other long-term liabilities | 19,087 | ||

Minority interest in consolidated subsidiary | 925 | ||

Total liabilities assumed | 667,360 | ||

Net assets acquired | $ | 757,645 | |

ASA Acquisition

On August 17, 2007, we closed on a transaction with ASAlliances Biofuels, LLC (“ASAlliances”). Under a Unit Purchase Agreement, we purchased all of the equity interests in ASA OpCo Holdings, LLC (“ASA Holdings”) from ASAlliances for an aggregate purchase price of $683,997. Of this amount, we issued 13,801,384 shares of our common stock valued at $194,323, and paid $250,000 of cash to the seller at closing, and $6,310 for transaction fees and expenses. The balance of the purchase price consisted of $233,364 of indebtedness owed by ASA Holdings and its subsidiaries, ASA Albion, LLC, ASA Bloomingburg, LLC and ASA Linden, LLC, which remained outstanding after the closing under a Credit Agreement, dated February 6, 2006 among ASA Holdings, ASA Albion, LLC, ASA Bloomingburg, LLC and ASA Linden, LLC, as borrowers, and WestLB AG, New York branch, as administrative agent for the lenders and the lenders named therein (“Senior Credit Facility”). We also agreed to register under

11

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

applicable securities laws, within 180 days of the acquisition date, the shares issued in the transaction. ASA Holdings owns companies with three bio-refineries and developmental rights to two sites. This transaction is referred to in this document as the “ASA Acquisition”.

The 13,801,384 shares of common stock issued in connection with the ASA Acquisition were valued at $194,323 based on the weighted average of the Company’s stock price two days before and two days after July 22, 2007, the date of the acquisition agreement and announcement of the transaction. The preliminary determination of goodwill acquired in the ASA Acquisition was $163,500. In June 2008, a purchase price reduction of $4,623 was determined due to a delay in the start-up of the Bloomingburg, Ohio facility. This adjustment was converted into a 648,000 reduction in the shares issued. This adjustment was recognized as a reduction in goodwill and shareholders’ equity as of June 30, 2008. Refer to Note 3 for the Company’s goodwill impairment evaluation performed during the third quarter of fiscal year 2008.

Pro Forma Results

The following table provides unaudited pro forma consolidated results of operations for the three and nine months ended September 30, 2008 and 2007, as though the ASA Acquisition and the US BioEnergy Acquisition had occurred as of the beginning of the respective fiscal years. The pro forma results include certain purchase accounting adjustments with respect to the acquired tangible and intangible assets. However, pro forma results do not include any anticipated costs savings or other effects of the planned integration. Accordingly, such amounts are not necessarily indicative of the results if the acquisition had occurred on the dates indicated or that may result in the future.

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||

Pro forma results: | ||||||||||||||

Net sales | $ | 1,084,467 | $ | 384,111 | $ | 2,824,994 | $ | 1,024,973 | ||||||

Net income (loss) | (476,109 | ) | 10,325 | (441,152 | ) | 36,613 | ||||||||

Basic net income (loss) per share | (3.03 | ) | 0.06 | (2.81 | ) | 0.22 | ||||||||

Diluted net income (loss) per share | (3.03 | ) | 0.06 | (2.81 | ) | 0.22 | ||||||||

Note 3. Goodwill and Other Identifiable Intangible Assets

Goodwill

Changes to goodwill for the nine months ended September 30, 2008 were as follows:

| Total | ||||

Balance as of December 31, 2007 | $ | 169,629 | ||

US BioEnergy acquisition (see note 2) | 98,326 | |||

ASA purchase price adjustment (see note 2) | (4,623 | ) | ||

Impairment charge | (263,332 | ) | ||

Balance as of September 30, 2008 | $ | — | ||

In accordance with Statement of Financial Accounting Standards No. 142, “Goodwill and Other Intangible Assets” (“SFAS 142”), the Company performs an annual impairment evaluation as of October 1st or performs an interim evaluation if triggering events have occurred. In accordance with Statement of Financial Accounting Standards No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets” (“SFAS 144”), the Company performs an impairment evaluation of long-lived assets if triggering events occur.

During the second quarter of fiscal 2008, the Company performed an interim impairment evaluation of its goodwill, other identifiable intangible assets and all its long-lived assets due to triggering events as in the sustained decrease in the Company’s stock price relative to the book value of the Company coupled with a significant issuance of common stock, pursuant to a merger with US

12

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

BioEnergy. No impairment was recorded during this impairment test as the fair value of the enterprise value was more than its carrying value. The Company also concluded that no impairment to its identifiable intangible assets and all its long-lived assets had occurred on the April 1st test date.

As of the end of the third quarter of fiscal 2008, the Company performed another interim impairment evaluation of its goodwill, other identifiable intangible assets and all its long-lived assets due to factors deemed by management to have constituted an impairment triggering event during the third quarter. The triggering event was the further sustained decrease in the Company stock price relative to the book value of the Company and declining gross margins leading to the substantial net loss incurred during the quarter.

For purposes of testing goodwill, the Company estimated the fair value of the enterprise utilizing several fair value measurement techniques, including two market estimates and one income estimate, and using relevant data available through and as of September 30, 2008. Under the market approaches, the fair value of the enterprise was estimated based upon the fair value of invested capital for VeraSun, as well as a separate comparison to revenue and earnings before interest, taxes, depreciation, and amortization (“EBITDA”) multiples for similar publicly traded companies in the renewable energy industry. Under the income approach, the fair value of the enterprise was estimated based upon the present value of estimated future cash flows for VeraSun. The income approach is dependent on a number of critical management assumptions including estimates of ethanol and distiller sales price, corn and natural gas cost, appropriate discount rates and other relevant assumptions. The Company considered the approaches described above and determined the income statement approach provided the best estimate of our enterprise fair value. The enterprise fair value was less than the entity’s carrying value, and, therefore, the Company was required to perform step two of the SFAS 142 goodwill impairment testing methodology.

In step two of the impairment test, the Company determined the implied fair value of goodwill by allocating the fair value of the reporting unit determined in step one to all the assets and liabilities of the Company, including any recognized and unrecognized intangible assets, as if the reporting unit had been acquired in a business combination and the fair value of the reporting unit was the price paid to acquire the reporting unit. The Company’s step two analysis resulted in no implied fair value of goodwill, and, therefore, the Company recognized an impairment charge of $263,332 for the three and nine months ended September 30, 2008, representing a write-off of the entire amount of the Company’s previously recorded goodwill.

As a result of the impairment testing described above and in Note 4, the Company’s goodwill and certain long-lived assets were recorded at fair value. In accordance with FASB Staff Position No. 157-2, Effective Date of FASB Statement No. 157, the Company has not applied SFAS 157 to the determination of the fair value of these assets. However, the provisions of SFAS 157 were applied to the determination of the fair value of financial assets and financial liabilities that were part of the SFAS 142 step two goodwill fair value determination.

Other intangible assets

Other intangible assets as of September 30, 2008 and December 31, 2007 are as follows:

| September 30, 2008 | December 31, 2007 | ||||||||||||||||||||

| Gross Carrying Value | Accumulated Amortization | Impairment | Net Carrying Value | Gross Carrying Value | Accumulated Amortization | Net Carrying Value | |||||||||||||||

Favorable corn procurement agreements | $ | 41,794 | $ | 17,179 | $ | 22,278 | $ | 2,337 | — | — | — | ||||||||||

Vendor supply arrangements | 20,370 | 937 | — | 19,433 | $ | 20,370 | $ | 228 | $ | 20,142 | |||||||||||

Customer relationships | 13,900 | 1,867 | — | 12,033 | — | — | — | ||||||||||||||

Non-compete agreements | 1,740 | 911 | 829 | — | 1,740 | 214 | 1,526 | ||||||||||||||

Total | $ | 77,804 | $ | 20,894 | $ | 23,107 | $ | 33,803 | $ | 22,110 | $ | 442 | $ | 21,668 | |||||||

The Company completed an impairment evaluation of these other intangible assets as of September 30, 2008 due to triggering events described in the preceding paragraphs. The Company determined that the fair value of the favorable corn procurement agreements and non-compete agreements was less than their carrying value. The fair value of the favorable corn procurement agreements was determined based upon a lower of cost or market analysis of the corn contracts acquired and marked to fair value as part of the US BioEnergy Acquisition on April 1, 2008. Implied fair value of the non-compete agreements was determined based on the Company’s decision not to enforce these non-compete agreements.

Based on the lower of cost or market analysis, the Company recorded an impairment charges on favorable corn procurement contracts of $22,278 for the three months ended September 30, 2008. The total impairment charge was recorded in the statement of operations as “Long-lived asset impairment”. The impairment of other identifiable intangible assets was determined as of the September 30, 2008 test date in accordance with SFAS No. 144. See Note 4 for information regarding impairment of the Company’s long-lived assets.

13

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

All other intangible assets are amortizable and the weighted-average amortization periods related to these amortizable intangible assets are as follows:

| (In years) | Weighted-average Amortization Period | |

Favorable corn procurement agreements | 3 | |

Vendor supply arrangements | 20 | |

Customer relationships | 4 |

The weighted-average amortization period for all amortizable intangibles on a combined basis is 16 years.

The Company’s aggregate amortization expense was $9,434 and $20,452 for the three and nine months ended September 30, 2008 and $112 for the three and nine month periods ended September 30, 2007, respectively. Based on current levels of amortizable intangible assets, estimated annual amortization expense is expected to be $1,188 in the fourth quarter of 2008, $6,800 in 2009, $5,040 in 2010, $3,984 in 2011, $1,694 in 2012 and $1,019 in 2013.

Note 4. Impairment of Long-Lived Assets

Long-lived asset impairment charges for the three and nine months ended September 30, 2008 were as follows:

| Total | |||

Impairment of property, plant, and equipment | $ | 92,961 | |

Impairment of investment in economic development bonds | 5,150 | ||

Impairment of favorable corn procurement agreements (see Note 3) | 22,278 | ||

Impairment of non-compete agreements (see Note 3) | 829 | ||

| $ | 121,218 | ||

As of the end of the third quarter of fiscal 2008, the Company performed an impairment test of its long-lived assets due to the triggering events mentioned in Note 3.

We evaluated the recoverability of property, plant and equipment in accordance with SFAS No. 144. For purposes of testing impairment of its long-lived assets at September 30, 2008, the Company determined whether the carrying amount of its long-lived assets was recoverable by comparing the carrying amount to the sum of the undiscounted cash flows expected to result from the use and eventual disposition of the assets. If the carrying value of the assets exceeded the expected cash flows, the Company estimated the fair value of these assets to determine whether an impairment existed. The estimated undiscounted cash flows were dependent on a number of critical management assumptions, including estimates of future capacity, crush margin, corn, natural gas and other inputs, operating costs and other relevant assumptions. If estimates of fair value were required, fair value was estimated using the market approach. Asset appraisals and recent transactions for similar assets were considered by the Company in its market value determination less any transaction or disposal cost the Company might occur.

Based on the recoverability analysis on certain properties, the Company recorded an impairment charge of $92,961 for the three months ended September 30, 2008 to reflect the write-down of such assets to fair market value and an estimated amount to settle open purchase orders. The Company also recorded an impairment charge of $5,150 relating to the value of economic development bonds in connection with the Reynolds, Indiana facility. The total impairment charge was recorded in the statement of operations as “Long-lived asset impairment”.

See the disclosure under the heading “Other intangible assets” in Note 3 for information regarding long-lived asset impairment charges relating to favorable corn procurement agreements and non-compete agreements.

14

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

Due to corn and crude oil price volatility, tight credit markets, the volatility of the Company’s stock price and the resulting decline in its market capitalization and the uncertain economic environment, as well as other uncertainties, the Company can provide no assurance that a material impairment charge to remaining intangible assets and all long lived assets will not occur in a future period. The Company will continue to monitor circumstances and events in future periods to determine whether additional interim long-lived asset impairment testing is warranted.

Note 5. Restructuring Activities

In conjunction with the US BioEnergy Acquisition, the Company has combined corporate headquarters in Sioux Falls, South Dakota, and has recorded a restructuring charge related to severance payments to existing VeraSun employees.

Restructuring costs for the first nine months of 2008 were as follows:

| Balance at | Nine months ended September 30, 2008 | Cumulative Drawdowns | Balance at | ||||||||||||||||||

| December 31, | Cash | Non-cash | September 30, | ||||||||||||||||||

| 2007 | Charges | Reversals | Totals | Payments | Charges | 2008 | |||||||||||||||

Personnel and severance costs: | $ | — | $ | 2,114 | $ | — | $ | 2,114 | $ | 2,114 | $ | — | $ | — | |||||||

Total | $ | — | $ | 2,114 | $ | — | $ | 2,114 | $ | 2,114 | $ | — | $ | — | |||||||

All restructuring charges and cash payments for the three and nine months ended September 30, 2008 consisted of personnel and severance costs. At year-end 2007, VeraSun expected to reduce headcount by 16 employees. As of September 30, 2008 the Company had reduced headcount by 17 employees as part of its restructuring actions.

There were no costs associated with restructuring activities for the three and nine month periods ended September 30, 2007.

Note 6. Inventories

Corn, chemicals, supplies and work in process inventories are stated at the lower of cost or market on the first-in, first-out method. Ethanol and distillers grains are stated at the lower of average cost or market.

A summary of inventories as of September 30, 2008 and December 31, 2007 is as follows:

| September 30, | December 31, | |||||

| 2008 | 2007 | |||||

Ethanol | $ | 108,237 | $ | 56,199 | ||

Corn | 22,572 | 27,637 | ||||

Work in process | 21,643 | 7,859 | ||||

Supplies | 16,149 | 11,341 | ||||

Chemicals | 7,948 | 2,743 | ||||

Distillers grains | 6,558 | 2,133 | ||||

| $ | 183,107 | $ | 107,912 | |||

Lower of cost or market adjustment for the three and nine months ended September 30, 2008 was as follows:

| Total | |||

Loss on forward corn contracts and purchase commitments | $ | 27,240 | |

Lower of cost or market adjustment for inventory on hand | 12,867 | ||

| $ | 40,107 | ||

15

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

The Company had entered into forward corn purchase contracts and multi-year corn purchase agreements under which it is required to take delivery at the contract price. Currently, some of these contract prices are above current market prices for corn. Given the declining ethanol price, upon taking delivery under these contracts, the Company would incur a loss. Accordingly, the Company recorded a loss on these purchase commitments aggregating to $27,240 for both three months and nine months ended September 30, 2008. The loss was recorded in “Lower of cost or market adjustments” on the condensed consolidated statement of operations. The amount of the loss was determined by applying a methodology similar to that used in the impairment evaluation with respect to inventory. Given the uncertainty of future ethanol prices, this loss may or may not be recovered, and further losses on the outstanding purchase commitments could be recorded in future periods.

During the three and nine month periods ended September 30, 2008, we recorded an inventory valuation impairment of $12,867 attributable primarily to decreases in market prices of corn and ethanol. The inventory valuation impairment was recorded in ”Lower of cost or market adjustment” on the condensed consolidated statement of operations.

Note 7. Fair Value Disclosure

Effective January 1, 2008, the Company adopted the provisions of SFAS No. 157 for assets and liabilities recognized at fair value on a recurring basis. SFAS No. 157 establishes a framework for measuring fair value and requires enhanced disclosures about assets and liabilities carried at fair value.

As defined in SFAS No. 157, fair value is the price that would be received to sell an asset or paid to transfer a liability in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants at the measurement date. SFAS No. 157 establishes a fair value hierarchy, which prioritizes the inputs used in measuring fair value into three broad levels as follows:

Level 1 – Quoted prices are available in active markets for identical assets or liabilities as of the reported date. The types of assets and liabilities included in Level 1 are highly liquid and actively traded instruments with quoted prices, such as equities listed by the New York Stock Exchange and commodity derivative contracts listed on the Chicago Board of Trade.

Level 2 – Pricing inputs are other than quoted prices in active markets, but are either directly or indirectly observable as of the reported date. The types of assets and liabilities included in Level 2 are typically either comparable to actively traded securities or contracts, or priced with models using highly observable inputs, such as commodity options priced using observable forward prices.

Level 3 – Significant inputs to pricing have little or no observability as of the reporting date. The types of assets and liabilities included in Level 3 are those with inputs requiring significant management judgment or estimation, such as the complex and subjective models and forecasts used to determine the fair value of financial transmission rights.

The following table presents the fair value hierarchy for those assets and liabilities measured at fair value on a recurring basis as of September 30, 2008. As required by SFAS No. 157, financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. The Company’s assessment of the significance of a particular input to the fair value measurement requires judgment and may affect the valuation of fair value assets and liabilities and their placement within the fair value hierarchy levels.

| Significant other | Significant | |||||||||||

| Total Carrying | Quoted prices in | observable | unobservable | |||||||||

| Value at | active markets | inputs | inputs | |||||||||

| September 30, 2008 | (Level 1) | (Level 2) | (Level 3) | |||||||||

Assets | ||||||||||||

Derivative financial instruments assets* | $ | 2,994 | $ | 2,364 | $ | 630 | $ | — | ||||

Liabilities | ||||||||||||

Derivative financials instrument liabilities* | $ | 17,593 | $ | — | $ | 17,593 | $ | — | ||||

| * | Derivative financial instruments assets and liabilities with the same counter party have been shown net in the accompanying balance sheet and long-term derivative financial instruments liabilities of $1,381 is included in other long-term liabilities. |

16

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

The Company enters into various commodity derivative instruments, including forward contracts, futures, options, swaps and other over-the-counter agreements. The fair value of the Company’s commodity derivatives is determined using unadjusted quoted prices for identical instruments on the applicable exchange in which VeraSun transacts. When quoted prices for identical instruments are not available, VeraSun uses forward price curves derived from market price quotations. Market price quotations are obtained from independent energy brokers, exchanges, direct communication with market participants and actual transactions executed by VeraSun. This methodology also applies to those derivative contract commitments which were made by US BioEnergy prior to the April 1, 2008 acquisition by VeraSun. Market price quotations for certain inputs are generally readily obtainable for the applicable term of VeraSun’s outstanding commodity derivative instruments and, therefore, VeraSun’s forward price curves for those locations and periods reflect observable market quotes.

Note 8. Long-Term Debt and Credit Facility

The Bankruptcy Filing, on October 31, 2008, resulted in an event of default under substantially all of VeraSun’s pre-petition long-term debt, summarized in the table below, with the exception of the tax increment revenue note, community redevelopment revenue bonds, and other debt consisting of capital leases and economic development loans. In light of the Bankruptcy Filing, the affected long-term debt obligations are reflected on the unaudited condensed consolidated balance sheet as of September 30, 2008 under current maturities of long-term debt, and no further borrowings are available under the related credit facilities. Under section 362 of the Bankruptcy Code, however, the acceleration provisions applicable to those debt obligations are generally unenforceable, and any remedies that may exist related to the events of default described above are stayed. For details on the impact of the Bankruptcy Filing and a discussion of the Company’s debtor-in-possession financing, see Note 15 “Subsequent Events”.

The following table summarizes the Company’s pre-petition long-term debt:

| September 30, | December 31, | |||||||

| 2008 | 2007 | |||||||

9 3/8% senior notes due 2017 (a) | $ | 437,000 | $ | 450,000 | ||||

Senior credit facility (b) | 266,750 | 240,946 | ||||||

AgStar construction loans (d) | 237,785 | — | ||||||

9 7/8% senior secured notes due 2012 (a) | 210,000 | 210,000 | ||||||

AgStar senior secured term loans (d) | 166,587 | — | ||||||

UBS credit facility due 2011 (c) | 108,795 | — | ||||||

Marion credit facility (e) | 88,394 | — | ||||||

AgStar revolving term loans (d) | 54,763 | — | ||||||

Revolving loans (d) (e) | 13,442 | — | ||||||

Tax increment revenue note (g) | 5,000 | 5,000 | ||||||

Community redevelopment revenue bonds (f) | 3,203 | — | ||||||

Other | 3,415 | 2,546 | ||||||

Total | 1,595,134 | 908,492 | ||||||

Less unamortized discount | (2,661 | ) | (3,022 | ) | ||||

Less unamortized discount associated with US BioEnergy Acquisition (h) | (56,584 | ) | — | |||||

Less current maturities of long-term debt | (1,524,958 | ) | (16,774 | ) | ||||

Long-term debt | $ | 10,931 | $ | 888,696 | ||||

At September 30, 2008, the Company was in the process of addressing certain conditions that could have, with the passage of time or receipt of notice, resulted in events of default under certain of the Company’s credit facilities. The Company’s Chapter 11 Bankruptcy filing on October 31, 2008 stayed the possible impact of such conditions.

17

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

(a) Senior Notes

In May 2007, the Company issued $450,000 aggregate principal amount of unsecured Senior Notes due 2017 (the “2017 Notes”) at 99.5% of face value. The 2017 Notes bear interest at a fixed rate of 9.375% per annum and are recorded net of unamortized debt discount of $2,300. The 2017 Notes mature on June 1, 2017. They may be redeemed at any time prior to June 1, 2012 by paying a make-whole premium and may be redeemed at any time after June 1, 2012 at specified redemption prices. Interest on the 2017 Notes is paid on a semi-annual basis on June 1 and December 1 of each year beginning on December 1, 2007. Total remaining principal balance as of September 30, 2008 was $437,000.

In August 2008, the Company extinguished $13,000 of principal and $282 of accrued interest outstanding on the 2017 Notes in exchange for 1,428,299 shares of the Company’s common stock. In connection with the extinguishment, the Company recorded a gain on extinguishment of debt in the amount of $3,743 for the three month ended September 30, 2008. The gain was computed by deducting the market price of the stock issued, as of the date issued, from the carrying value of the debt extinguished. Such amount included the write-off of unamortized debt issuance cost, unamortized debt discount, and transaction cost totalling $440.

The Senior Secured Notes due 2012 (the “2012 Notes”), principal amount of $210,000, bear interest at 9.875% per annum, payable semi-annually on June 15 and December 15 of each year, and mature on December 15, 2012. They may be redeemed at any time at specified redemption prices. The 2012 Notes and the 2017 Notes are guaranteed by the Company’s existing subsidiaries, other than ASA Holdings and its subsidiaries and US BioEnergy and its subsidiaries, and any future restricted subsidiaries that guaranty any of the Company’s or any subsidiary guarantor’s other indebtedness. The 2012 Notes are secured on a first priority basis by liens on substantially all of VeraSun Energy Corporation’s assets and the assets of the subsidiary guarantors other than accounts receivable, inventory and commodities accounts, and the cash proceeds therefrom.

The indentures governing the 2012 Notes and the 2017 Notes contain restrictive covenants which, among other things, limit the Company’s ability (subject to exceptions) to (a) make restricted payments (which limits redemption of capital stock, voluntary debt repayments, and investments); (b) incur additional debt; (c) engage in transactions with shareholders and affiliates; (d) pay dividends and other payments restrictions affecting subsidiaries; (e) incur liens on assets; (f) sell assets; and (g) engage in unrelated businesses.

(b) Senior Credit Facility

In connection with the ASA Acquisition, the Senior Credit Facility, as amended, remained in effect and provides for aggregate borrowings of up to $275,000 in two tranches: Tranche A for up to $175,000 and Tranche B for up to $100,000. Borrowings under the Senior Credit Facility must be used for the development, engineering, construction and operation of the Company’s Linden, Albion and Bloomingburg plants.

At December 31, 2007, the Company had borrowed $153,567 and $87,379 under the Senior Credit Facility in the form of Tranche A and Tranche B construction loans, respectively. On March 15, 2008, the Company converted the two tranches into term notes in the amounts of $175,000 and $100,000 respectively. Amounts borrowed and repaid under the Senior Credit Facility may not be re-borrowed. The Company paid quarterly commitment fees of 0.5% per annum on the average daily unused amount of the construction loan commitments under the Senior Credit Facility. The Company also pays agent fees of $125 per year.

Tranche A loans bear interest, at the Company’s option, at the administrative agent’s base rate (which is the higher of the federal funds effective rate and the administrative agent’s prime rate) plus 1.5% per annum or a Eurodollar rate based on LIBOR plus 2.5% per annum. Tranche B loans bear interest, at the Company’s option, at the administrative agent base rate plus 3.5% per annum or a Eurodollar rate based on LIBOR plus 4.5% per annum. The interest rate as of September 30, 2008 was 6.2% and 8.2% for Tranche A loans and Tranche B loans, respectively. The interest rate as of December 31, 2007 was 7.7% and 10.1% for Tranche A loans and Tranche B loans, respectively.

The obligations under the Senior Credit Facility are secured by the assets of ASA Holdings and its subsidiaries and a pledge made by VeraSun Energy Corporation of all of the equity interests in ASA Holdings.

The Tranche A term loan is payable in equal quarterly installments of principal of $2,625, and the Tranche B term loan is payable in equal quarterly installments of principal of $1,500, plus accrued interest in accordance with the terms of the Senior Credit Facility, with the balance in each case payable at maturity on June 30, 2014.

The Senior Credit Facility requires the Company to prepay the term loans each quarter. Among other such prepayment requirements, the Company must prepay a percentage of excess cash flows, if any, generated from the Linden, Albion and Bloomingburg plants. The Company did not make any prepayment on the Senior Credit Facility for the three and nine months ended September 30, 2008.

18

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

The Senior Credit Facility contains various covenants that, among other restrictions, limit ASA Holdings’ ability and the ability of its subsidiaries to make distributions and pay dividends; incur indebtedness and swap and hedge obligations; grant or assume liens; make certain investments; change the nature of their business; issue equity interests not pledged to the lenders; and sell, transfer, assign or convey assets, or engage in certain mergers or acquisitions.

As part of the covenant requirements when the construction loans were converted to term notes, the Company is required to restrict a certain amount of cash representing principal and interest payments on the outstanding Senior Credit Facility. Restricted cash as of September 30, 2008 includes $9,500 related to this requirement.

(c) UBS Credit Facility

On May 30, 2008, the Company entered into a Credit Agreement (the “Credit Facility”) with UBS Securities LLC, UBS AG, Stamford Branch, and UBS Loan Finance LLC. The Credit Agreement provides up to $125,000 of revolving credit subject to a borrowing base. The borrowing base is a formula based on eligible inventory and receivables, minus certain reserves. All obligations under the Credit Facility are secured by the VeraSun’s inventory and accounts receivable. Advances under the Credit Facility may be used for general corporate purposes, including permitted acquisitions. Subject to collateral availability, the Credit Facility also permits the Company to advance funds to VeraSun Reynolds, LLC and, in an initial amount not to exceed $40,000, to other subsidiaries of the Company. At September 30, 2008, the Company’s borrowing base was $140,854, and the Company had borrowed $108,795 under the Credit Facility at an average interest rate of 6.5%.

The Company is in the process of transferring certain letters of credit to the Credit Facility. As of September 30, 2008, UBS required the Company to restrict a certain amount of cash until all the letters of credit were transferred. Restricted cash as of September 30, 2008 includes $1,525 related to this requirement.

(d) AgStar Credit Facilities

On April 1, 2008, the Company assumed various credit facilities with AgStar as an administrative agent and as a lender, and a group of other lenders as part of the US BioEnergy Acquisition. As of September 30, 2008, $459,135 was outstanding with AgStar, which was comprised of the following:

| • | $237,785 of construction loans bearing interest of 3.15% above the one-month LIBOR, interest payable quarterly; |

| • | $83,136 of senior secured term loans bearing interest of 2.90% above the one-month LIBOR, with monthly principal and interest payments through February 2012 and September 2012; |

| • | $83,451 of senior secured term loans bearing interest of 3.25% above the one-month LIBOR, with monthly principal and interest payments through November 2011 and March 2012; and |

| • | $54,763 of revolving term loans bearing interest ranging from 2.90% to 3.25% above the one-month LIBOR, interest payable monthly, due on various dates ranging through November 2011 to September 2012. |

In addition, the Company had availability of $16,525 under seasonal revolving loans, bearing interest of 3.1% above the one-month LIBOR, interest payable monthly with outstanding principal balance due May 2009, that are available for working capital needs of which $6,442 were outstanding as of September 30, 2008, and $3,475 was used for letters of credit.

All of the AgStar senior secured term loans contain incentive based pricing that is based on levels of equity, which will reduce the interest rate ranging from 150 to 300 basis points above the one-month LIBOR rate. These agreements, each of which is associated with a particular ethanol plant, require quarterly payments of up to $5,000 annually based on excess cash flow calculations reducing the principal balance.

The Company has various construction retainage and payables relating to the construction of the Hankinson, Janesville and Dyersville facilities. As of September 30, 2008, there was approximately $57,715 of construction funding available under the AgStar credit facility, of which $11,496 was used for outstanding letters of credit. In light of the Bankruptcy Filing, no further borrowings are available under this credit facility.

19

Table of Contents

VERASUN ENERGY CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (unaudited)

(dollars in thousands, except for per share data)

(e) Marion Credit Facilities

US Bio Marion, LLC (“US Bio Marion”), which became a subsidiary of the Company as a result of the US BioEnergy Acquisition, at the time of the acquisition had outstanding construction loan from Dougherty Funding LLC (“Dougherty”) relating to the Marion, South Dakota facility (“Marion”). As of April 1, 2008, there was $79,800 of outstanding Marion construction loan borrowings bearing interest of 4.00% above the three-month LIBOR, interest payable monthly with outstanding principal balance due May 2009. On June 1, 2008 the outstanding Marion constructions loans were converted into a term note in the amount of $90,000 requiring monthly amortized payments of principal and interest sufficient to amortize the remaining unpaid principal balance to a maturity date of March 31, 2013. The term loan is secured by substantially all of the assets of US Bio Marion. As of September 30, 2008, outstanding borrowings under the Marion term note were $88,394.