UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities

Exchange Act of 1934

(Amendment No. )

Filed by the Registranto Filed by a Party other than the Registrantþ

Check the appropriate box:

o Preliminary Proxy Statement

o Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

o Definitive Proxy Statement

þ Definitive Additional Materials;

o Soliciting Material Pursuant to §240.14a-12

THE PHOENIX COMPANIES, INC.

(Name of the Registrant as Specified In Its Charter)

OLIVER PRESS PARTNERS, LLC

OLIVER PRESS INVESTORS, LLC

AUGUSTUS K. OLIVER

CLIFFORD PRESS

DAVENPORT PARTNERS, L.P.

JE PARTNERS, L.P.

OLIVER PRESS MASTER FUND, L.P.

JOHN CLINTON

CARL SANTILLO

(Name(s) of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| þ | No fee required. |

| | |

| o | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

| | (1) | Title of each class of securities to which transaction applies: N/A |

| | (2) | Aggregate number of securities to which transaction applies: N/A |

| | (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined): N/A |

| | (4) | Proposed maximum aggregate value of transaction: N/A |

| | (5) | Total fee paid: N/A |

| |

| o | Fee paid previously with preliminary materials. |

| |

| o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| | (1) | Amount Previously Paid: N/A |

| | (2) | Form, Schedule or Registration Statement No.: N/A |

| | (3) | Filing Party: N/A |

| | (4) | Date Filed: N/A |

| |

Attached as Exhibit 1 are soliciting materials posted to http://www.raisethephoenix.com.

Oliver Press Partners, LLC

Raise the Phoenix

The Situation

Dear Fellow Phoenix Companies Shareholder:

We are writing to you as a shareholder of The Phoenix Companies, Inc. In the next few weeks, you will be receiving materials related to the 2008 Annual Meeting of Phoenix’s shareholders, which has been scheduled to take place on May 2, 2008.

You may be aware that our investment firm, Oliver Press Partners, LLC, owns nearly 5.7 million shares of The Phoenix Companies and is one of the company’s three largest shareholders. We are leading an initiative to elect three new independent Directors to the Board. Collectively, these nominees have substantial insurance industry expertise and significant stock ownership, so their interests are aligned with yours. They would bring an independent perspective that would help to focus the Board on the best interests of shareholders and policyholders like you.

We are very concerned about the direction in which Phoenix is heading as discussed in this letter and believe that this year it is particularly important that you vote for the election of new Directors to halt any further decline in the company’s fortunes and to prevent further deterioration in the ratings of Phoenix Life Insurance Company or its affiliates. Oliver Press Partners urges you to take advantage of this opportunity to change the composition of the Board, and believes this change will benefit all shareholders.

HISTORY OF THE PHOENIX COMPANIES

You may remember that The Phoenix Companies converted from a mutual insurance company to a public company through an Initial Public Offering at $17.50 per share on June 19, 2001. At that time, existing policyholders of the Phoenix Home Life Mutual Insurance Company received 54% of the shares in the company, and new public shareholders purchased the remaining 46%.

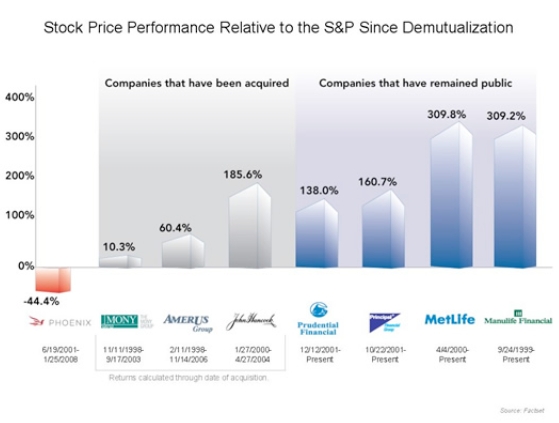

PHOENIX COMPANIES SHARES HAVE DECLINED BY 37% SINCE 2001

Unfortunately, since becoming a public company, the price of Phoenix’s stock has declined substantially. On March 7, 2008, it closed at $10.91 per share, a decline of 37% over the past nearly seven years. During this same general period, the stocks of other life insurance companies that converted from mutual to stock ownership have appreciated handsomely. The following graph shows the performance of other life insurance companies that converted from mutual to stock ownership in this period from the date of the conversion through the present or the date of sale of the company, where applicable.

PHOENIX STOCK UNDERPERFORMS ITS COMPETITORS

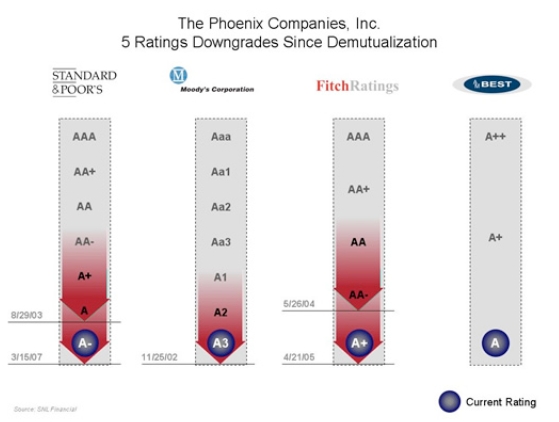

Not only has Phoenix’s stock price fallen, but the company’s insurance rating has been downgraded on five separate occasions since the IPO by major rating agencies, which affects the security of its policies. As the following graph reveals, the financial strength (“claims paying”) rating is now much lower than it was before the conversion from a mutual to a public stock company.

PHOENIX COMPANIES INSURANCE RATING DOWNGRADED FIVE TIMES

DONA YOUNG’S POTENTIAL $49 MILLION PAYOUT

While shareholders and policyholders have suffered declining performance and ratings, the management of the company has been generously paid. Phoenix’s 2008 Proxy statement, which you will shortly be receiving from the company, reveals that Chief Executive Officer Dona Young:

- had her total compensation for 2007 increased to $4.9 million, during a year in which the company’s stock price fell 25.3% .

- now has a total package of compensation arrangements that would pay her no less than $49[1] million if she left the company. This payment would include her current accumulated $12.8 million of pension benefits, $9.1 million of deferred compensation and additional Board approved arrangements providing a further $27.0 million of severance, other compensation, benefits and perquisites. The compensation arrangements are valid in the event she were terminated by the Company after a change-incontrol, she were to choose to leave the Company for “good reason” after a change-in-control (as defined in her change-in-control agreement) [2] or she were to choose to leave the Company voluntarily within 30 days after the first anniversary of a change-in-control.

At The Phoenix Companies, this compensation generosity is not limited to the CEO. This year’s Phoenix Proxy statement reveals that the Board has permitted the “Supplemental” pension plan for current and retired senior management and select employees to grow to $141 million. This plan is a direct unfunded liability of the company that ranks ahead of shareholders.

We believe it is clear that the Board of Directors has failed to exercise effective and responsible oversight on your behalf. Instead, shareholders have been left with losses, policyholders have been left with downgraded ratings for their policies and management has been enriched.

We believe that The Phoenix Companies needs new Directors who will bring accountability to management. Therefore we are proposing three Directors, Carl Santillo, John Clinton, and Augustus Oliver for election at this year’s annual meeting. These candidates all have significant insurance or financial experience. We believe that, collectively, they have deeper, more substantive industry expertise than the three incumbent Board members that we are seeking to replace, who have all been members of the Board’s Compensation Committee during the period that the compensation packages discussed in this letter were approved.

WE NEED YOU TO VOTE FOR NEW DIRECTORS TO PROTECT YOUR INVESTMENT AND SAFEGUARD YOUR POLICY

You might be surprised to learn that the current Board and senior executives of Phoenix — including CEO Dona Young —collectively own barely half of one percent of the stock of the company. In fact, several incumbent directors do not own even a single share of Phoenix stock. The directors that we are proposing have meaningful ownership and interests fully aligned with yours. The election of Directors will take place at Phoenix’s Annual Meeting of shareholders on May 2, 2008. This meeting will provide an important opportunity for you to vote for new, independent Directors.In the next few weeks, you will receive materials from us showing you how to vote for the new Directors on the WHITE card. Please note that these materials will be separate from the materials you receive from The Phoenix Companies, recommending that you vote for their incumbent directors. We encourage you not to return any Blue card that Phoenix may send to you.

Remember, the Board of The Phoenix Companies does not appoint its Directors, they must be elected by shareholders. This year you have a real choice, and can vote for new Directors nominated by Oliver Press Partners who are independent and aligned with your interests.

In order to cast your vote for the new Directors, you can simply complete theWHITE proxy card that you will receive shortly and return it as instructed. In the meanwhile, you can learn more about Phoenix’s performance issues, our proposals to address these issues, and our Board candidates atwww.RaiseThePhoenix.com.

We appreciate your support, and if you need assistance or have any questions, please call our Proxy Solicitor, MacKenzie Partners, Inc., toll-free at (800) 322-2885 or collect at (212) 929-5500.

| Sincerely | | |

| |  |

| Augustus K. Oliver | | Clifford Press |

If you have any questions or require assistance in voting your WHITE proxy card, please call MacKenzie Partners at the phone numbers listed below.

105 Madison Avenue

New York, NY 10016

proxy@mackenziepartners.com

Call Collect: (212) 929-5500

or Toll Free: (800) 322-2885

ADDITIONAL INFORMATION

Oliver Press Partners, LLC (“Oliver Press”) filed a preliminary proxy statement with the Securities and Exchange Commission (the “SEC”). Oliver Press will prepare and file with the SEC a definitive proxy statement and may file other solicitation materials. THE PHOENIX COMPANIES, INC.’S SHAREHOLDERS ARE URGED TO READ THE PROXY STATEMENT AND OTHER DOCUMENTS RELATED TO THE 2008 ANNUAL MEETING WHEN THEY BECOME AVAILABLE, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. THESE MATERIALS WILL BE AVAILABLE AT NO CHARGE ON THE SEC’S WEB SITE AT HTTP://WWW.SEC.GOV. Shareholders may also obtain free copies of the proxy statement and other documents filed by Oliver Press in connection with the annual meeting by directing a request to: MacKenzie Partners, Inc. by calling Toll-Free (800) 322-2885 or by e-mail atphoenixproxy@mackenziepartners.com.

OLIVER PRESS PARTICIPANT INFORMATION

IN ACCORDANCE WITH RULE 14A-12(A)(1)(I) OF THE SECURITIES EXCHANGE ACT OF 1934, AS AMENDED, INFORMATION REGARDING THE IDENTITY OF THE PERSONS WHO MAY, UNDER SEC RULES, BE DEEMED TO BE PARTICIPANTS IN THE SOLICITATION OF SHAREHOLDERS AND THEIR INTERESTS ARE SET FORTH IN THE PRELIMINARY PROXY STATEMENT THAT WAS FILED BY OLIVER PRESS WITH THE SEC.

| | | |

| [1] | A description of Dona Young’s change-in-control agreement is contained in Phoenix’s proxy statement. |

| |

| [2] | Includes Pension, Supplemental Pension, Excess Investment Plan, Deferred Restricted Stock Units, Deferred Dividends, Base Severance, Incentive Severance, 2007 Annual Incentive, 2005-2007 LTIP, 2006-2008 LTIP, 2007-2009 LTIP, Unvested Performance-Contingent RSU’s, Unvested Service-Based RSU’s, Unvested Stock Options, Incremental Non-Qualified Company Match, Non-Qualified Pension Lump Sum, and 280G Tax Gross-Up (for excise taxes on Excess Parachute Payments). The $12.8 million of pension benefits and $9.1 million of deferred compensation are payable independent of the occurrence of a change-incontrol. |

| |