UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

|

Investment Company Act file number 811-21940 EIP Investment Trust (Exact name of registrant as specified in charter) c/o Energy Income Partners, LLC 49 Riverside Avenue Westport, CT 06880 (Address of principal executive offices) (Zip code) Linda Longville c/o Energy Income Partners, LLC 49 Riverside Avenue Westport, CT 06880 (Name and address of agent for service) Registrant’s telephone number, including area code: 203-349-8232 Date of fiscal year end: December 31 Date of reporting period: December 31, 2015 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

EIP Growth and Income Fund

December 31, 2015 Annual Report

EIP Growth and Income Fund

You should carefully consider the investment objectives, risks, charges, and expenses of the Fund before making an investment decision. The private placement memorandum contains this and other information - please read it carefully before investing or sending money. Except as noted, numbers in the private placement memorandum are unaudited. To obtain a copy of the private placement memorandum, please call (203) 349-8232.

EIP Growth and Income Fund

To Our Shareholders:

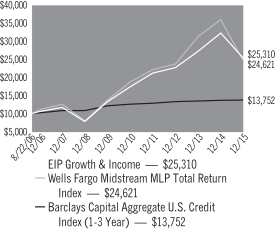

I am pleased to submit this Annual Report for the EIP Growth and Income Fund (the “Fund”) for the year ended December 31, 2015. For the year ended December 31, 2015, the Fund’s total return was -21.54%. For the year ended December 31, 2014, the Fund’s total return was +18.69%.

The Fund’s primary strategy is investing in publicly traded energy infrastructure companies with high dividend payouts that offer attractive yields and have the opportunity to grow. A large portion of our equity investment opportunities are publicly traded partnerships known as Master Limited Partnerships (“MLPs”). These securities represent just under 25% of the Fund’s total assets, which is the maximum allowable for mutual funds under current tax diversification rules. The remainder of our equity portfolio is invested in securities with similar characteristics to the energy related MLPs, such as MLP affiliates, Yield Corporations (YieldCos) and pipeline and power utilities in the U.S. and Canada.

The Fund’s bond portfolio, when applicable, is invested in high quality corporate bonds with a weighted average maturity of 18 months or less or a coupon that floats with prevailing interest rates. All of our corporate bonds must have an AA rating or better, or an equivalent rating from Moody’s or, if unrated, have been determined by Energy Income Partners, LLC to be of similar quality, at the time they are put into the portfolio unless they are issued by an energy company, in which case the bond must have an investment grade rating or higher. As of June 30, 2015, we liquidated our bond portfolio. Our reverse repurchase agreement counterparty, through which we obtain leverage, terminated our relationship. We continue to explore other options for leverage.

Benchmarks:

We believe the following benchmarks provide appropriate comparisons of the Fund’s performance:

| | | | |

| | | Total Return

1/1/15-

12/31/15 | |

| Wells Fargo Midstream MLP Total Return Index | | | -31.50% | |

| Barclays Capital Aggregate U.S. Credit Index (1-3 year) | | | 0.85% | |

| | | | |

| | | Total Return

1/1/14-

12/31/14 | |

| Wells Fargo Midstream MLP Total Return Index | | | 15.07% | |

| Barclays Capital Aggregate U.S. Credit Index (1-3 year) | | | 1.12% | |

Wells Fargo Midstream MLP Total Return Index. We believe the portion of our portfolio invested in MLPs and other energy equities may be compared to the Wells Fargo Midstream MLP Total Return Index. We use this index rather than a broader MLP index as our investment style tends to focus the portfolio in MLPs involved in pipeline transportation, storage, terminaling and processing of petroleum and natural gas. These activities are commonly known as “midstream” as opposed to oil and gas production (“upstream”) and refining and marketing (“downstream”). The upstream and downstream parts of the energy industry are the customers of the midstream companies. And while much of the equity portion of the portfolio is not invested in midstream MLPs per se, their business characteristics are similar: a heavy weighting in North American midstream operations and a high payout ratio.

Barclays Capital Aggregate U.S. Credit Index. The Barclays Capital Aggregate U.S. Credit Index (1-3 year) is an index of corporate bonds with an average duration of about 1.9 years and an average credit quality between Moody’s assigned A1 to A2 ratings (Source: Barclays Capital Inc.). While slightly longer in duration and lower in credit quality, we believe that over time, this index is the best benchmark for how we run the bond portion of our portfolio, when applicable.

MLPs and Other Equities

The Fund’s equity portfolio significantly outperformed the Wells Fargo Midstream MLP Total Return Index in 2015. Throughout the year, weakness in oil and gas prices weighed heavily on sentiment across the energy sector and the MLP asset class. The significant outperformance of the portfolio in comparison to this index was driven by three main factors: 1) diversification of the portfolio across multiple asset classes such as YieldCos and pipeline and power utilities in the U.S. and Canada, 2) the avoidance of commodity exposure and 3) valuation discipline.

As measured by the Wells Fargo Midstream MLP Total Return Index, the total return for MLPs for the year ended December 31, 2015 was -31.50%. This return reflects an initial yield of about 4.67% and share depreciation of about 36.17%. We believe

Results of a Hypothetical $10,000 Investment

EIP Growth & Income is net of all fees and expenses.

The Wells Fargo Midstream MLP Total Return Index consists of 56 energy MLPs and represents the Midstream sub-sector of the Wells Fargo MLP Composite Index. The index is calculated by S&P using a float-adjusted market capitalization methodology. Unlike the Fund, the index does not incur fees and expenses.

The Barclays Capital Aggregate U.S. Credit Index (1-3 year) is an index of corporate bonds with an average duration of about 1.9 years and an average credit quality of between Moody’s assigned A1 to A2 ratings. Unlike the Fund, the index does not incur fees and expenses.

The graph is provided for illustrative purposes only and should not be relied on when making an investment decision regarding the Fund. A discussion of the risk factors involved in an investment in the Fund is contained in the prospectus and SAI, which should be read thoroughly before undertaking any investment in the Fund.

EIP Growth and Income Fund

RETURNS FOR YEAR ENDED 12/31/15

Average Annual Total Returns

| | | | |

| One Year | | | -21.54% | |

| Five Years | | | 7.79% | |

| Since Inception | | | 10.43% | |

Inception Date 08/22/06

The performance data quoted represents past performance and does not guarantee future results. The performance stated may have been due to extraordinary market conditions, which may not be duplicated in the future. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of the fund will fluctuate so that an investor’s shares, when sold, may be worth more or less than the original cost. Calculations do not reflect the deduction in taxes that a shareholder would pay on fund distributions or the redemption of shares. Calculations assume reinvestment of dividends and capital gain distributions. To obtain more recent performance data, please contact the Energy Income Partners Information Center at (203) 349-8232.

EIP Growth and Income Fund

the MLP structure and a high payout ratio are only suitable for a narrow set of long-lived assets that have stable non-cyclical cash flows, such as regulated pipelines or other infrastructure assets that are legal or natural monopolies. By comparison, the Wells Fargo Midstream MLP Total Return Index tends to have more cyclical exposure that has been negatively affected by falling oil and gas prices versus the Fund’s portfolio. For oil and natural gas systems, the supply-end is more cyclical while the demand-end is more non-cyclical driven by inelastic consumption. The Fund’s portfolio has always been tilted to the demand-end of the system with a significant portion of the portfolio invested in utilities, while the index is much more exposed to the supply-end of the system with a larger weighting in gathering and processing assets that directly serve oil and gas producers. Over the last 12 months, the per-share cash distributions of energy-related MLPs has declined about 12.6% (Source: Alerian Capital Management). This compares to the weighted average distribution growth of 2.8% for the portfolio.

Our valuation discipline also contributed to the Fund’s significant outperformance of the portfolio relative to the Wells Fargo Midstream MLP Total Return Index. Over the past few years, there were a significant number of MLPs and MLP general partner issues that have been experiencing much higher than average growth due in large part to the acquisition of “drop down” assets from the parent entity (usually the general partner or GP) to the child entity (usually the limited partner or LP). The schedule of drop downs was so well telegraphed that it was clear to anyone paying attention that growth would be high for some number of years, which is why the valuations of these situations got stratospherically high. Some had price-to-earnings ratios higher than 50x and enterprise value-to-EBITDA ratios above 25x. With the massive swing we have seen in sentiment and the resulting reduction in the price of the LP units, there has been a dramatic reduction in the accretion of these drop down acquisitions and an even more dramatic drop in those stratospheric valuations. We are cautious about putting high growth, high valuation positions into the portfolio as the valuation can decline before the growth slows, for reasons that are unforeseen. The result is a portfolio that has less dividend growth but also less valuation risk.

Industry Review

MLP equity issuance slowed 48% in 2015 to $18.4 billion compared to $35.3 billion in 2014. Reduced activity can be attributed to weak MLP equity markets as many indexes were down sharply year-over-year. There were 9 IPOs that raised $4.9 billion during 2015 compared to 20 MLP IPOs that raised $7.7 billion in 2014. Total MLP debt transactions are down 11% to $37.1 billion for 2015, which compares to $41.8 billion for 2014 according to Barclays.

Over the long term, the total return proposition of owning non-cyclical energy related infrastructure MLPs, YieldCos and utilities has been and continues to be their yield plus their growth. In our opinion, the better positioned MLPs, YieldCos and utilities not only have non-cyclical cash flows but also conservative balance sheets, modest and/or flexible organic growth commitments and liquidity on their revolving lines of credit. Cyclical cash flows will always be unpredictable in our view, making them a poorer fit with a steady dividend obligation. Over the last few years, the majority of MLP IPOs were companies whose primary business is the production of oil and gas, shipping, refining or natural gas gathering and processing. While some of these MLPs have quality assets and competent management teams, they have more risk associated with the cyclical nature of their businesses. We have written about the dangers of this trend in the past, and remain vigilant about limiting our exposure to MLPs with cyclical cash flows.

Sincerely,

James Murchie

President

EIP Growth and Income Fund

The views expressed in this commentary reflect those of the Fund’s portfolio management team as of December 31, 2015. Any such views are subject to change at any time based on market or other conditions, and the Fund disclaims any responsibility to update such views. These views are not intended to be a forecast of future events, a guarantee of future results or advice. Because investment decisions for the Fund are based on numerous factors, these views may not be relied upon as an indication of trading intent on behalf of the Fund. The information contained herein has been prepared from sources believed to be reliable, but is not guaranteed by the Fund as to its accuracy or completeness. Past performance is not indicative of future results. Performance information provided above assumes the reinvestment of interest, dividends and other earnings. There is no assurance that the Fund’s investment objectives will be achieved.

EIP Growth and Income Fund

December 31, 2015

Schedule of Investments

| | | | | | | | |

Shares | | | | | Fair

Value | |

| | | | | | | | |

|

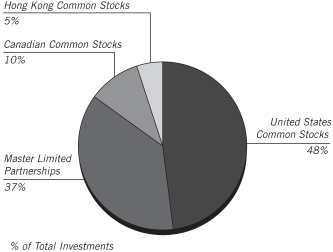

| | UNITED STATES COMMON STOCKS – 35.64% | |

| | | | Energy – 11.20% | | | | |

| | 44,628 | | | Enbridge Energy Management, LLC (a) | | $ | 996,543 | |

| | 35,240 | | | Kinder Morgan, Inc. | | | 525,781 | |

| | 3,000 | | | Spectra Energy Corp. | | | 71,820 | |

| | 5,000 | | | TransCanada Corp. | | | 162,950 | |

| | | | | | | | |

| | | | | | | 1,757,094 | |

| | | | | | | | |

| | | | Financial – 1.05% | | | | |

| | 721 | | | CorEnergy Infrastructure Trust, REIT | | | 10,697 | |

| | 8,300 | | | InfraREIT, Inc., REIT | | | 153,550 | |

| | | | | | | | |

| | | | | | | 164,247 | |

| | | | | | | | |

| | | | Utilities – 23.39% | | | | |

| | 2,000 | | | Alliant Energy Corp. | | | 124,900 | |

| | 6,000 | | | American Electric Power Co., Inc. | | | 349,620 | |

| | 3,000 | | | American Water Works Co., Inc. | | | 179,250 | |

| | 5,000 | | | Aqua America, Inc. | | | 149,000 | |

| | 2,500 | | | Atmos Energy Corp. | | | 157,600 | |

| | 2,300 | | | Chesapeake Utilities Corp. | | | 130,525 | |

| | 5,000 | | | CMS Energy Corp. | | | 180,400 | |

| | 100 | | | Dominion Resources, Inc. | | | 6,764 | |

| | 5,700 | | | Eversource Energy | | | 291,099 | |

| | 4,000 | | | Exelon Corp. | | | 111,080 | |

| | 3,000 | | | IDACORP, Inc. | | | 204,000 | |

| | 3,600 | | | National Grid PLC, Sponsored ADR | | | 250,344 | |

| | 6,300 | | | New Jersey Resources Corp. | | | 207,648 | |

| | 4,325 | | | ONE Gas Inc. | | | 216,985 | |

| | 10,500 | | | Public Service Enterprise Group, Inc. | | | 406,245 | |

| | 5,300 | | | SCANA Corp. | | | 320,597 | |

| | 2,250 | | | Sempra Energy | | | 211,523 | |

| | 2,200 | | | Southern Co. | | | 102,938 | |

| | 2,000 | | | Xcel Energy, Inc. | | | 71,820 | |

| | | | | | | | |

| | | | | | | 3,672,338 | |

| | | | | | | | |

| | | | Total United States Common Stocks | | | | |

| | | | (Cost $6,241,850) | | | 5,593,679 | |

| | | | | | | | |

| | | | | | | | |

|

| | MASTER LIMITED PARTNERSHIPS – 27.28% | |

| | | | Consumer Cyclicals – 1.28% | | | | |

| | 1,900 | | | AmeriGas Partners, LP | | $ | 65,113 | |

| | 6,100 | | | Westlake Chemical Partners LP | | | 135,298 | |

| | | | | | | | |

| | | | | | | 200,411 | |

| | | | | | | | |

| | | | Energy – 26.00% | | | | |

| | 3,800 | | | Alliance Holdings GP, LP | | | 76,684 | |

| | 8,000 | | | Alliance Resource Partners, LP | | | 107,920 | |

| | 19,500 | | | Columbia Pipeline Partners LP | | | 340,860 | |

| | 27,438 | | | Enterprise Products Partners, LP | | | 701,864 | |

| | 5,800 | | | EQT Midstream Partners, LP | | | 437,668 | |

| | 13,258 | | | Holly Energy Partners, LP | | | 412,854 | |

| | 16,000 | | | Nextera Energy Partners, LP (b) | | | 477,600 | |

| | 16,000 | | | Plains All American Pipeline, LP | | | 369,600 | |

| | 13,900 | | | Spectra Energy Partners, LP | | | 663,030 | |

| | 1,900 | | | Tallgrass Energy Partners LP | | | 78,299 | |

| | 4,000 | | | Targa Resources Partners, LP | | | 66,120 | |

| | 4,009 | | | TC Pipelines, LP | | | 199,287 | |

| | 5,600 | | | TransMontaigne Partners, LP | | | 149,856 | |

| | | | | | | | |

| | | | | | | 4,081,642 | |

| | | | | | | | |

| | | | Total Master Limited Partnerships | | | | |

| | | | (Cost $4,783,655) | | | 4,282,053 | |

| | | | | | | | |

|

| | CANADIAN COMMON STOCKS – 7.20% | |

| | | | Energy – 1.34% | | | | |

| | 13,100 | | | Inter Pipeline Ltd, LP | | | 210,270 | |

| | | | | | | | |

| | | | Utilities – 5.86% | | | | |

| | 9,400 | | | Atco Ltd/Canada, Class I | | | 242,524 | |

| | 3,000 | | | Canadian Utilities, Ltd., Class A | | | 69,249 | |

| | 4,000 | | | Emera, Inc. | | | 124,969 | |

| | 16,100 | | | Enbridge Income Fund Holdings, Inc. | | | 326,142 | |

| | 5,400 | | | Keyera Corp. | | | 157,118 | |

| | | | | | | | |

| | | | | | | 920,002 | |

| | | | | | | | |

| | | | Total Canadian Common Stocks | | | | |

| | | | (Cost $1,463,789) | | | 1,130,272 | |

| | | | | | | | |

|

| | HONG KONG COMMON STOCKS – 3.45% | |

| | | | Energy – 1.17% | | | | |

| | 20,100 | | | Power Assets Holdings LLC, ADR | | | 183,915 | |

| | | | Industrial – 2.28% | | | | |

| | 7,700 | | | Cheung Kong Infrastructure Holdings Ltd, ADR | | | 356,677 | |

| | | | | | | | |

| | | | Total Hong Kong Common Stocks | | | | |

| | | | (Cost $461,114) | | | 540,592 | |

| | | | | | | | |

|

| | Warrants – 0.00% | |

| | | | Energy – 0.00% | | | | |

| | 4,480 | | | Kinder Morgan, Inc., Strike Price | |

| | | | $40.00, Exp. 05/25/17 (a) | | | 269 | |

| | | | | | | | |

| | | | Total Warrants | | | | |

| | | | (Cost $8,534) | | | 269 | |

| | | | | | | | |

| Total Investments – 73.57% | | | | |

| (Cost $12,958,942)* | | | 11,546,865 | |

| | | | | | | | |

| Other Assets in Excess of Liabilities – 26.43% | | | 4,148,349 | |

| | | | | | | | |

| Net Assets – 100.00% | | $ | 15,695,214 | |

| | | | | | | | |

See accompanying Notes to Financial Statements.

3

EIP Growth and Income Fund

December 31, 2015

Schedule of Investments – continued

| | * | | Aggregate cost for federal tax purposes is $13,064,723 |

| | (a) | | Non-income producing security. |

| | (b) | | Organized as a limited partnership and has elected to be treated as a corporation for U.S. federal income tax purposes. |

| | ADR | | American Depositary Receipt |

| | REIT | | Real Estate Investment Trust |

The amount of $63,942 in cash was segregated with the counterparty, Credit Suisse, to cover margin requirements for the following open futures contracts as of December 31, 2015:

| | | | | | | | | | | | |

| Short Futures Outstanding | | Number of

Contracts | | | Notional

Amount1 | | | Unrealized

Appreciation | |

| Canadian Dollar (03/16) | | | 23 | | | $ | 1,692,476 | | | $ | 28,886 | |

| | 1 | | The notional amount represents the U.S. value of the contract as of the day of the opening of the transaction or latest contract reset date. |

The amount of $807,259 in cash was segregated with the custodian to cover the following total return equity swaps outstanding at December 31, 2015:

Credit Suisse is the counterparty to the below total return equity swaps.

| | | | | | | | | | | | | | |

Long Total

Return Equity Swaps | | Pay

Rate | | Expiration

Date | | | Notional

Amount2 | | | Unrealized

Appreciation | |

| Atmos Energy Corp. | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | $ | 18,477 | | | $ | 425 | |

| | | | |

| Dominion Resources, Inc. | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 370,440 | | | | 11,768 | |

| | | | |

| Enbridge, Inc. (Canada) | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 86,604 | | | | 6,281 | |

| | | | |

| Enterprise Products Partners, LP | | 1 month

LIBOR + 150

basis points | | | 2/24/2016 | | | | 295,944 | | | | 41,493 | |

| | | | |

| Eversource Energy | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 39,776 | | | | 1,392 | |

| ITC Holdings Corp. | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | $ | 48,906 | | | $ | 2,092 | |

| | | | |

| Magellan Midstream Partners, LP | | 1 month

LIBOR + 150

basis points | | | 2/24/2016 | | | | 185,690 | | | | 24,725 | |

| | | | |

| Nextera Energy, Inc. | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 394,880 | | | | 20,464 | |

| | | | |

| Plains All American Pipeline, LP | | 1 month

LIBOR + 150

basis points | | | 2/24/2016 | | | | 79,480 | | | | 12,861 | |

| | | | |

| Sempra Energy | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 157,760 | | | | 3,161 | |

| | | | |

| Tallgrass Energy Partners, LP | | 1 month

LIBOR + 150

basis points | | | 2/24/2016 | | | | 69,020 | | | | 13,349 | |

| | | | |

| TransCanada Corp. (Canada) | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 372,780 | | | | (13,680 | ) |

| | | | |

| UGI Corp. | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 45,290 | | | | 2,268 | |

| | | | |

| WEC Energy Corp. | | 1 month

LIBOR + 100

basis points | | | 2/24/2016 | | | | 339,456 | | | | 9,266 | |

| | | | | | | | | | | | | | |

| | | | | | | | $ | 2,504,503 | | | $ | 135,865 | |

| | | | | | | | | | | | | | |

| | 2 | | The notional amount represents the U.S. value of the contract as of the day of the opening of the transaction or latest contract reset date. |

| | 3 | | Amounts include $8,051 of net dividends and financing costs. |

See accompanying Notes to Financial Statements.

4

EIP Growth and Income Fund

December 31, 2015

Statement of Assets and Liabilities

| | | | |

| |

ASSETS: | | | | |

Investments, at value (Cost $12,958,942) | | $ | 11,546,865 | |

Cash and cash equivalents | | | 3,221,762 | |

Restricted cash | | | 871,201 | |

Swaps (premium paid $0) | | | 149,545 | |

Foreign currency, at value (Cost $1,257) | | | 1,261 | |

Receivables: | | | | |

Investments sold | | | 153,165 | |

Dividends and interest | | | 54,425 | |

Fund shares subscribed (Note 5) | | | 11,773,779 | |

Due from broker – variation margin on futures contracts | | | 28,886 | |

Prepaid expenses | | | 59,436 | |

| | | | |

Total assets | | | 27,860,325 | |

| | | | |

| |

LIABILITIES: | | | | |

Swaps (premium received $0) | | | 13,680 | |

| Payables: | | | | |

Fund shares redeemed (Note 5) | | | 11,914,201 | |

Professional fees | | | 162,162 | |

Investment advisory fees (Note 3) | | | 13,118 | |

Accounting and administration fees (Note 3) | | | 36,271 | |

Transfer agent fees | | | 12,074 | |

Custodian fees | | | 7,349 | |

Printing expense | | | 6,006 | |

Trustees fees and related expenses (Note 3) | | | 250 | |

| | | | |

Total liabilities | | | 12,165,111 | |

| | | | |

| |

NET ASSETS | | $ | 15,695,214 | |

| | | | |

| |

NET ASSETS CONSIST OF: | | | | |

Par value ($0.01 per share) | | $ | 11,433 | |

Paid-in-capital | | | 33,232,531 | |

Accumulated undistributed net investment loss | | | (395,882 | ) |

Accumulated net realized loss on investments, swaps, futures contracts and foreign currency transactions | | | (15,905,554 | ) |

Net unrealized depreciation on investments, swaps, futures contracts and foreign currency translations | | | (1,247,314 | ) |

| | | | |

| | $ | 15,695,214 | |

| | | | |

Shares outstanding (unlimited number of shares authorized) | | | 1,143,314 | |

| | | | |

Net Asset Value, offering and redemption price per share (net assets/shares outstanding) | | $ | 13.73 | |

| | | | |

See accompanying Notes to Financial Statements.

5

EIP Growth and Income Fund

Statement of Operations For the Year Ended December 31, 2015

| | | | |

| |

INVESTMENT INCOME: | | | | |

Dividends | | $ | 374,394 | |

Less: foreign taxes withheld | | | (20,947 | ) |

Interest | | | 18,101 | |

| | | | |

Total investment income | | | 371,548 | |

| | | | |

| |

EXPENSES: | | | | |

Investment advisory fees (Note 3) | | | 202,845 | |

Professional fees | | | 324,861 | |

Administration fees (Note 3) | | | 186,226 | |

Trustees fees and related expenses (Note 3) | | | 70,469 | |

Transfer agent fees (Note 3) | | | 48,148 | |

Interest expense (Note 2) | | | 23,079 | |

Custodian fees | | | 23,596 | |

Printing expenses | | | 11,324 | |

Insurance expense | | | 81,013 | |

Other expenses | | | 31,648 | |

| | | | |

Total expenses | | | 1,003,209 | |

| | | | |

NET INVESTMENT LOSS | | | (631,661 | ) |

| | | | |

| |

NET REALIZED AND UNREALIZED GAIN/(LOSS) | | | | |

NET REALIZED GAIN/(LOSS) ON: | | | | |

Investments | | | 730,539 | |

Swaps | | | (606,616 | ) |

Futures contracts | | | 406,634 | |

Foreign currency transactions | | | (22,637 | ) |

| | | | |

Net realized gain | | | 507,920 | |

| | | | |

NET CHANGE IN UNREALIZED APPRECIATION/DEPRECIATION ON: | | | | |

Investments | | | (4,288,462 | ) |

Swaps | | | (371,790 | ) |

Futures contracts | | | (15,259 | ) |

Foreign currency translations | | | 23 | |

| | | | |

Net change in unrealized appreciation/depreciation | | | (4,675,488 | ) |

| | | | |

NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | | | (4,167,568) | |

| | | | |

| |

NET DECREASE IN NET ASSETS FROM OPERATIONS | | $ | (4,799,229) | |

| | | | |

See accompanying Notes to Financial Statements.

6

EIP Growth and Income Fund

Statement of Changes in Net Assets

| | | | | | | | |

| | | Year ended

December 31,

2015 | | | Year ended

December 31,

2014 | |

OPERATIONS: | | | | | | | | |

Net investment loss | | $ | (631,661 | ) | | $ | (712,605 | ) |

Net realized gain on investments, swaps, futures contracts and foreign currency transactions | | | 507,920 | | | | 6,514,791 | |

Net change in unrealized depreciation on investments, swaps, futures contracts and foreign currency translations | | | (4,675,488 | ) | | | (798,439 | ) |

| | | | | | | | |

Net increase (decrease) in net assets from operations | | | (4,799,229 | ) | | | 5,003,747 | |

| | | | | | | | |

| | |

Distributions to shareholders from: | | | | | | | | |

Net investment income | | | (103,685 | ) | | | (2,160,985 | ) |

| | | | | | | | |

Total distributions | | | (103,685 | ) | | | (2,160,985 | ) |

| | | | | | | | |

| | |

Capital share transactions: | | | | | | | | |

Proceeds from sales of Fund shares | | | 14,238,677 | | | | 277,000 | |

Proceeds from reinvestment of distributions | | | 103,262 | | | | 2,018,015 | |

Cost of shares redeemed | | | (17,964,737 | ) | | | (15,954,246 | ) |

| | | | | | | | |

Net decrease in net assets from capital share transactions | | | (3,622,798 | ) | | | (13,659,231 | ) |

| | | | | | | | |

Total decrease in net assets | | | (8,525,712 | ) | | | (10,816,469 | ) |

| | | | | | | | |

NET ASSETS: | | | | | | | | |

Beginning of year | | | 24,220,926 | | | | 35,037,395 | |

End of year | | $ | 15,695,214 | | | $ | 24,220,926 | |

| | | | | | | | |

Undistributed net investment loss | | $ | (395,882 | ) | | $ | (461,803 | ) |

| | | | | | | | |

See accompanying Notes to Financial Statements.

7

EIP Growth and Income Fund

Statement of Cash Flows For the Year Ended December 31, 2015

| | | | |

| |

Operating Activities | | | | |

Net decrease in net assets from operations | | $ | (4,799,229 | ) |

| |

Adjustments to Net Decrease in Net Assets from Operations | | | | |

Purchase of investment securities | | | (10,004,087 | ) |

Sales of investment securities | | | 23,727,511 | |

Net realized gain on investments | | | (730,539 | ) |

Litigation gain | | | 2,785 | |

Net change in unrealized appreciation/depreciation on investments | | | 4,288,462 | |

Net change in unrealized appreciation/depreciation on foreign currency translations | | | (8 | ) |

Net change in swap appreciation/depreciation | | | 371,790 | |

Net premium bond amortization | | | 9,070 | |

Return of capital received from investments in master limited partnerships | | | 367,129 | |

Decrease in restricted cash | | | 38,367 | |

Decrease in investments purchased payable | | | (183,744 | ) |

Decrease in investments sold receivable | | | 728,368 | |

Net decrease in due from broker-variation margin on futures contracts | | | 15,259 | |

Decrease in prepaid expenses | | | 38,457 | |

Increase in dividends and interest receivable | | | (25,905 | ) |

Decrease in interest expense payable | | | (1,284 | ) |

Decrease in trustee fees and related expenses payable | | | (788 | ) |

Increase in accounting and administration fees payable | | | 16,415 | |

Increase in custodian fees payable | | | 303 | |

Increase in transfer agent fees payable | | | 7,323 | |

Decrease in printing expense payable | | | (578 | ) |

Decrease in investment advisory fee payable | | | (6,910 | ) |

Decrease in professional fees payable | | | (402 | ) |

Decrease in swaps payable | | | (9,619 | ) |

Decrease in other payables | | | (7,454 | ) |

| | | | |

Net cash provided by operating activities | | | 13,840,692 | |

| | | | |

| |

Cash Flows for Financing Activities | | | | |

Net decrease in reverse repurchase agreements | | | (9,248,125 | ) |

Proceeds from shares sold | | | 2,464,898 | |

Payment of shares redeemed | | | (6,050,536 | ) |

Cash distributions to shareholders | | | (423 | ) |

| | | | |

Net cash used in financing activities | | | (12,834,186 | ) |

| | | | |

Net increase in unrestricted cash and foreign currency | | | 1,006,506 | |

Beginning of Year(1) | | $ | 2,216,517 | |

| | | | |

End of Year(1) | | $ | 3,223,023 | |

| | | | |

| |

Supplemental Disclosure: | | | | |

Cash paid for interest expense | | $ | 24,363 | |

| | | | |

| (1) | The amount represents an investment in a money market sweep which is included in cash and cash equivalents, and foreign currency, if any, on the Statements of Assets and Liabilities. |

See accompanying Notes to Financial Statements.

8

EIP Growth and Income Fund

Financial Highlights

The financial highlights table is intended to help you understand the Fund’s financial performance for the periods shown. Certain information reflects financial results for a share outstanding throughout each period. The total returns in the table represent the rate that an investor would have earned (or lost) on an investment in the Fund (assuming reinvestment of all dividends and distributions).

| | | | | | | | | | | | | | | | | | | | |

| | | Year

Ended

12/31/15 | | | Year

Ended

12/31/14 | | | Year

Ended

12/31/13 | | | Year

Ended

12/31/12 | | | Year

Ended

12/31/11 | |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 17.62 | | | $ | 16.37 | | | $ | 14.51 | | | $ | 14.43 | | | $ | 13.04 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Income from investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss(a) | | | (0.50 | ) | | | (0.44 | ) | | | (0.29 | ) | | | (0.29 | ) | | | (0.31 | ) |

Net realized and unrealized gain/(loss) on investments | | | (3.30 | ) | | | 3.41 | | | | 3.16 | | | | 1.29 | | | | 3.05 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | (3.80 | ) | | | 2.97 | | | | 2.87 | | | | 1.00 | | | | 2.74 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Distributions paid to shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.09 | ) | | | (1.72 | ) | | | (1.01 | ) | | | (0.92 | ) | | | (1.35 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total from distributions | | | (0.09 | ) | | | (1.72 | ) | | | (1.01 | ) | | | (0.92 | ) | | | (1.35 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net increase (decrease) in net asset value | | | (3.89 | ) | | | 1.25 | | | | 1.86 | | | | 0.08 | | | | 1.39 | |

| | | | | | | | | | | | | | | | | | | | |

Net asset value, end of year | | $ | 13.73 | | | $ | 17.62 | | | $ | 16.37 | | | $ | 14.51 | | | $ | 14.43 | |

| | | | | | | | | | | | | | | | | | | | |

Total return | | | (21.54 | )% | | | 18.69 | % | | | 20.06 | % | | | 7.03 | % | | | 21.62 | % |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (in 000’s) | | $ | 15,695 | | | $ | 24,221 | | | $ | 35,037 | | | $ | 40,574 | | | $ | 41,437 | |

Ratios of expenses to average net assets: | | | | | | | | | | | | | | | | | | | | |

Operating expenses excluding interest expense | | | 4.83 | % | | | 3.63 | % | | | 2.71 | % | | | 2.66 | % | | | 2.90 | % |

Operating expenses including interest expense | | | 4.95 | % | | | 3.87 | % | | | 2.90 | % | | | 2.84 | % | | | 3.17 | % |

Ratios of net investment loss to average net assets | | | (3.11 | )% | | | (2.47 | )% | | | (1.64 | )% | | | (1.92 | )% | | | (2.21 | )% |

Portfolio turnover rate | | | 49 | % | | | 25 | % | | | 102 | % | | | 51 | % | | | 69 | % |

| (a) | Per share investment income has been calculated using the average shares method. |

See accompanying Notes to Financial Statements.

9

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements

1. ORGANIZATION

EIP Growth and Income Fund (the “Fund”) is a diversified, open-end management investment company. The Fund commenced operations on August 22, 2006. The Fund is currently the sole series of EIP Investment Trust (the “Trust”), a Delaware statutory trust. The Fund is managed by Energy Income Partners, LLC (the “Manager”). At this time, the Fund is currently not making a public offering of the shares. Fund shares are available only to certain unregistered investment companies through a “master/feeder” arrangement pursuant to Section 12(d)(1)(e) of the Investment Company Act of 1940, as amended (the “1940 Act”) and certain other accredited investors.

The Fund’s primary investment objective is to seek a high level of total shareholder return that is balanced between current income and growth. As a secondary objective, the Fund will seek low volatility. Under normal market conditions, the Fund’s investments will be concentrated in the securities of one or more issuers conducting their principal business activities in the Energy Industry. The Energy Industry is defined as enterprises connected to the exploration, development, production, gathering, transportation, processing, storing, refining, distribution, mining or marketing of natural gas, natural gas liquids (including propane), crude oil, refined petroleum products, electricity, coal or other energy sources.

2. SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company that follows the accounting and reporting guidance of Accounting Standards Codification Topic 946 applicable to Investment Companies. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements and which are in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for investment companies. The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Security Valuation: For purposes of valuing investment securities, readily marketable portfolio securities listed on any exchange or the National Association of Securities Dealers Automated Quotation System (“NASDAQ”) Global Market are valued, except as indicated below, at the last sale price or the NASDAQ official closing price as determined by NASDAQ on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean between the most recent bid and asked price on such day. Portfolio securities traded on more than one securities exchange are valued at the last sale price on the business day of which such value is being determined at the close of the exchange representing the principal market for such securities. Investments initially valued in currencies other than the U.S. dollar are converted to U.S. dollars using exchange rates obtained from independent pricing services. As a result, the net asset value (“NAV”) of the Fund’s shares may be affected by changes in the value of currencies in relation to the U.S. dollar. The value of securities traded in markets outside of the United States or denominated in currencies other than the U.S. dollar may be affected significantly on a day that the New York Stock Exchange (“NYSE”) is closed and an investor is not able to purchase or redeem shares.

Equity securities traded in the over-the-counter (“OTC”) market, but excluding securities trading on the NASDAQ Global Market, are valued at the closing bid prices, if held long, or at the closing asked prices, if held short. Debt securities are priced based upon valuations provided by independent, third-party pricing agents. These third-party pricing agents may employ methodologies that utilize actual market transactions, broker-dealer supplied valuation, or other electronic data processing techniques. Such techniques generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations. If reliable market quotations are not readily available with respect to a portfolio security held by the Fund, including any illiquid securities, or if a valuation is deemed inappropriate, the fair value of such security will be determined under procedures adopted by the Board of Trustees of the Trust (the “Board”) in a manner that most fairly reflects market value of the security on the valuation date as described below.

Financial futures contracts traded on exchanges are valued at their last sale price. Swap agreements are valued utilizing quotes received daily by the Fund’s pricing service.

The use of fair value pricing by the Fund indicates that a readily available market quotation is unavailable (such as when the exchange on which a security trades does not open for the day due to extraordinary circumstances and no other market prices are available or when events occur after the close of a relevant market and prior to the close of the NYSE that materially affect the value of an asset) and in such situations the Board (or the Manager, acting at the Board’s direction) will estimate the value of a security using available information. In such situations, the values assigned to such securities may not necessarily represent the amounts which might be realized upon their sale. The use of fair value pricing by the Fund will be governed by valuation procedures adopted by the Trust’s Board, and in accordance with the provisions of the 1940 Act.

10

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued

Fair Value Measurement: The inputs and valuation techniques used to measure fair value of the Fund’s net assets are summarized into three levels as described in the hierarchy below:

| | • Level 1 – | unadjusted quoted prices in active markets for identical assets or liabilities |

| | • Level 2 – | other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, evaluation pricing, etc.) |

| | • Level 3 – | significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. Transfers in and out of levels are recognized at market value at the end of the period. A summary of the values of each investment in each level as of December 31, 2015 is as follows:

| | | | | | | | | | | | | | | | |

| | | Total Fair Value at

12/31/2015 | | | Level 1 Quoted Price | | | Level 2 Significant Observable Inputs | | | Level 3 Significant Unobservable Inputs | |

ASSETS | | | | | | | | | | | | | | | | |

United States Common Stocks* | | $ | 5,593,679 | | | $ | 5,593,679 | | | $ | — | | | $ | — | |

Master Limited Partnerships* | | | 4,282,053 | | | | 4,282,053 | | | | — | | | | — | |

Canadian Common Stocks* | | | 1,130,272 | | | | 1,130,272 | | | | — | | | | — | |

Hong Kong Common Stocks* | | | 540,592 | | | | 183,915 | | | | 356,677 | | | | — | |

Cash and Cash Equivalents, Restricted Cash and

Foreign Currency | | | 4,094,224 | | | | 4,094,224 | | | | — | | | | — | |

Warrants* | | | 269 | | | | 269 | | | | — | | | | — | |

Derivatives | | | | | | | | | | | | | | | | |

Equity Contracts | | | 145,266 | | | | — | | | | 145,266 | | | | — | |

Foreign Currency Exchange Contracts | | | 28,886 | | | | 28,886 | | | | — | | | | — | |

Total | | | 15,815,241 | | | | 15,313,298 | | | | 501,943 | | | | — | |

LIABILITIES | | | | | | | | | | | | | | | | |

Derivatives | | | | | | | | | | | | | | | | |

Equity Contracts | | | 13,680 | | | | — | | | | 13,680 | | | | — | |

Total | | $ | 13,680 | | | $ | — | | | $ | 13,680 | | | $ | — | |

| * | See Schedule of Investments detail for industry breakout. |

The Fund did not have any transfers in and out of Level 1 and Level 2 during the year ended December 31, 2015.

The Fund held no securities or financial instruments during 2015, which were measured at fair value using Level 3 inputs.

At the end of each calendar quarter, management evaluates the Level 2 and 3 assets and liabilities, if applicable, for changes in liquidity, including but not limited to: whether a broker is willing to execute at the quoted price, the depth and consistency of prices from third party services, and the existence of contemporaneous, observable trades in the market. Additionally, management evaluates the Level 1 and 2 assets and liabilities on a quarterly basis for changes in listings or delistings on national exchanges. Due to the inherent uncertainty of determining the fair value of investments that do not have a readily available market value, the fair value of the Fund’s investments may fluctuate from period to period.

Additionally, the fair value of investments may differ significantly from the values that would have been used had a ready market existed for such investments and may differ materially from the values the Fund may ultimately realize. Further, such investments may be subject to legal and other restrictions on resale or otherwise less liquid than publicly traded securities.

MLP Common Units: Master Limited Partnership (“MLP”) common units represent limited partnership interests in the MLP. Common units are generally listed and traded on U.S. securities exchanges or OTC with their value fluctuating predominantly based on the success of the MLP. Unlike owners of common stock of a corporation, owners of MLP common units have limited voting rights and have no ability to annually elect directors. MLPs generally distribute all available cash flow (cash flow from operations less maintenance capital expenditures) in the form of quarterly distributions. Common unit holders have first priority to receive quarterly cash distributions up to

11

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued

the minimum quarterly distribution and have arrearage rights. In the event of liquidation, common unit holders have preference over subordinated units, but not debt holders or preferred unit holders, to the remaining assets of the MLP.

Cash and Cash Equivalents: The Fund maintains cash in a bank deposit account that, at times, may exceed federally insured limits. The Fund has not experienced any losses in such accounts and does not believe it is exposed to any significant credit risk on such bank deposits. The Fund considers investments in money market sweep accounts and short-term highly liquid investments with maturities of 90 days or less (when acquired) to be cash equivalents. Cash equivalents are carried at cost. As of December 31, 2015, the Fund held $3,221,762 of BNY Mellon Cash Reserve included in cash and cash equivalents on the Statement of Assets and Liabilities.

Restricted Cash: Restricted cash includes amounts required to be segregated with the Fund’s custodian or brokers as collateral for the Fund’s derivatives as shown on the Schedule of Investments. Segregated cash collateral is recorded at its carrying amount which represents fair value.

Reverse Repurchase Agreements: One method by which the Fund may incur leverage is through the use of reverse repurchase agreements. In a reverse repurchase agreement, the Fund sells securities to a bank, securities dealer or one of their respective affiliates and agrees to repurchase such securities on demand or on a specified future date and at a specified price, including an implied interest payment. During the period between the sale and the forward purchase, the Fund will continue to receive principal and interest payments on the securities sold and also have the opportunity to earn a return on the securities furnished by the counterparty. Reverse repurchase agreements involve the risk that the buyer of the securities sold by the Fund might be unable to deliver them when the Fund seeks to repurchase such securities. If the buyer of the securities under the reverse repurchase agreement files for bankruptcy or becomes insolvent, the buyer or a trustee or receiver may receive an extension of time to determine whether to enforce the Fund’s obligation to repurchase the securities, and the Fund’s use of the proceeds of the reverse repurchase agreement may effectively be restricted pending that decision. The Fund will segregate on its books assets in an amount at least equal to its obligations, marked to market daily, under any reverse repurchase agreement or take other permissible actions to cover its obligations. The use of leverage involves risks of increased volatility of the Fund’s investment portfolio, among others. In certain cases, the Fund may be required to sell securities with a value significantly in excess of the cash received by the Fund from the buyer. In certain reverse repurchase agreements, the buyer may require excess cover of the Fund’s obligation. If the buyer files for bankruptcy or becomes insolvent, the Fund may lose the value of the securities in excess of the cash received. In addition, many reverse repurchase agreements are short-term in duration (often overnight), and the counterparty may refuse to “roll over” the agreement to the next period, in which case the Fund may temporarily lose the ability to incur leverage through the use of reverse repurchase agreements and may need to dispose of a significant portion of its assets in a short time period.

Reverse repurchase transactions are entered into by the Trust under Master Repurchase Agreements (“MRA”), which may permit the Trust, under certain circumstances, including an event of default (such as bankruptcy or insolvency), to offset payables and/or receivables under the MRA and create one single net payment due to or from the Trust. With reverse repurchase transactions, typically the counterparty, as purchaser of securities, is permitted to sell, re-pledge, or use the financial assets acquired in the transaction. Pursuant to the terms of the MRA, the Trust typically sells securities with a market value in excess of the repurchase price to be paid by the Trust upon the maturity of the transaction. Upon a bankruptcy or insolvency of the MRA counterparty, the Trust may be deemed an unsecured creditor with respect to claims against the counterparty for recovery of the value of securities in excess of the repurchase price. There is a risk for any unsecured claims against the counterparty that its payment may be substantially delayed and may not be paid in full in a bankruptcy or other insolvency proceeding. In addition, bankruptcy or insolvency laws of a particular jurisdiction may impose restrictions on or prohibitions against rights of offset in the event of the MRA counterparty’s bankruptcy or insolvency.

The Fund closed the reverse repurchase agreements as of the period ending June 30, 2015. The Fund did not enter into reverse repurchase transactions during the period July 1, 2015 to December 31, 2015 or have any reverse repurchase agreements outstanding at December 31, 2015.

| | | | |

| |

Maximum amount outstanding during the period | | $ | 9,248,125 | |

| |

Average amount outstanding during the period* | | $ | 9,180,763 | |

| |

Average shares outstanding during the period* | | | 1,364,405 | |

| |

Average debt per share outstanding during the period* | | | $6.73 | |

| * | The average amount outstanding during the period was calculated by adding the cash received under reverse repurchase agreements at the end of each day and dividing the sum by the number of days in the six months ended June 30, 2015, the period in which the reverse repurchased agreements were held. |

The reverse repurchase agreements are executed daily based on the previous day’s terms. The accrued interest and maturity amounts are payable at the time the reverse

12

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued

repurchase agreement is not renewed or the terms of the agreement are renegotiated. Interest accrues on a daily basis from the initial opening date or last interest payment date, if an interest payment has been made for the respective repurchase agreement.

Implied interest rates ranged from 0.50% to 0.75% during the six months ended June 30, 2015, on cash received under reverse repurchase agreements. Interest expense for the year ended December 31, 2015 aggregated $23,079, which is included in the Statement of Operations under “Interest Expense.”

Short Sales of Securities: The Fund may enter into short sale transactions. A short sale is a transaction in which the Fund sells securities it does not own (but has or may have borrowed) in anticipation of a decline in the market price of the securities. To complete a short sale, the Fund may arrange through a broker to borrow the securities to be delivered to the buyer. The proceeds received by the Fund for the short sale are retained by the broker until the Fund replaces the borrowed securities. In borrowing the securities to be delivered to the buyer, the Fund becomes obligated to replace the securities borrowed at their market price at the time of replacement, whatever that price may be. The Fund did not enter into any short sale transactions during the year ended December 31, 2015.

Disclosures about Derivative Instruments and Hedging Activities: The following is a table summarizing the fair value of derivatives held at December 31, 2015 by primary risk exposure:

| | | | | | | | | | | | |

| | | Asset Derivatives | | | Liability Derivatives | |

Derivatives not accounted for

| | | | | | | | | | | | |

| | | Statement of Assets

and Liabilities Location | | Fair Value | | | Statement of Assets

and Liabilities Location | | Fair Value | |

| Foreign Currency Exchange Contracts | | Due from broker-variation margin on future contracts | | $ | 28,886 | | | Due to broker-unrealized depreciation on future contracts | | $ | — | |

| | | | |

Equity Contracts | | Swaps | | | 149,545 | | | Swaps | | | 13,680 | |

| | | | | | | | | | | | |

| | | | |

Total | | | | $ | 178,431 | | | | | $ | 13,680 | |

| | | | | | | | | | | | |

The effect of Derivative Instruments on the Statement of Operations for the year ended December 31, 2015:

| | | | | | | | | | |

Derivatives not accounted for

as hedging instruments | | Location of Gain/(Loss)

on Derivatives

Recognized in Income | | Net Realized Gain/

(Loss) on Derivatives

Recognized in Income | | | Net Change in Unrealized

Appreciation/

Depreciation on

Derivatives

Recognized in Income | |

| | | |

Foreign Currency Exchange Contracts | | Net realized gain/(loss) on futures contracts/Net change in unrealized appreciation/depreciation on futures contracts | | $ | 406,634 | | | $ | (15,259 | ) |

| | | |

Equity Contracts | | Net realized gain/(loss) on swaps/Net change in unrealized appreciation/depreciation on swaps | | | (606,616 | ) | | | (371,790 | ) |

| | | | | | | | | | |

| | | |

Total | | | | $ | (199,982 | ) | | $ | (387,049 | ) |

| | | | | | | | | | |

In order to better define its contractual rights and to secure rights that will help the Fund mitigate its counterparty risk, the Fund may enter into an International Swaps and Derivatives Association, Inc. Master Agreement (“ISDA Master Agreement”) or similar agreement with its derivative contract counterparties. An ISDA Master Agreement is a bilateral agreement between a Fund and a counterparty that governs OTC derivatives and foreign exchange contracts and typically contains, among other things, collateral posting terms and netting provisions that apply in the event of a default and/or termination event. Under an ISDA Master Agreement, the Fund may, under certain circumstances, offset with the counterparty certain payables and/or receivables with collateral held and/or posted to create one single payment. The provisions of the ISDA Master Agreement typically permit a single net payment by the non-defaulting party in the event of default (close-out netting), including the bankruptcy or insolvency of the counterparty. Note, however, that bankruptcy or insolvency laws of a particular jurisdiction may

13

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued

impose restrictions on or prohibitions against the right of offset in bankruptcy, insolvency or other events.

Margin requirements are established by the broker or clearing house for exchange traded and centrally cleared derivatives, such as futures contracts, or by agreement between the Fund and the counterparty in the case of OTC derivatives. For the Fund, its OTC swap counterparty required an initial collateral balance equaling 25% of the initial notional value of the swaps for the year ended December 31, 2015. Additional collateral requirements are calculated by netting the mark to market amount for each transaction and comparing that amount to the value of any collateral currently pledged by the Fund to the counterparty (and vice versa). In the case of exchange traded and centrally cleared derivatives, for which the broker or clearing house establishes minimum margin requirements, brokers can ask for margining in excess of the minimum established by the relevant clearing house in certain circumstances. For financial reporting purposes, cash collateral that has been pledged to cover obligations of the Fund and cash collateral received from the counterparty, if any, is reported separately on the Statement of Assets and Liabilities as Restricted Cash. In the case of OTC derivatives, generally the amount of collateral due from or to a party has to exceed a minimum threshold before a transfer is made. To the extent amounts due to the Fund from its counterparties are not fully collateralized, contractually or otherwise, the Fund bears the risk of loss from counterparty non-performance. See Note 6 “Counterparty Risk”. The Fund’s ISDA Master Agreement provides for the bilateral right of counterparties to terminate derivative contracts prior to maturity due to certain defined Events of Default (including but not limited to failure to pay or deliver or breach of agreement) or defined Termination Events (including but not limited to illegality, tax events or credit events), which could cause the Funds to accelerate payment of any net liability owed to the counterparty.

For financial reporting purposes, the Fund does not offset derivative assets and liabilities that are subject to netting arrangements in the Statement of Assets and Liabilities.

Offsetting of Financial Assets and Derivative Assets:

The following table presents the Fund's derivative assets by type net of amounts available for offset under a MNA and net of the related collateral received by the Fund as of December 31, 2015:

| | | | | | | | | | | | | | | | |

| | | | | | | Gross Amounts not offset in the Statement of Assets and Liabilities | | | | |

| Description | | Gross Amounts of Assets Presented in Statement of Assets and Liabilities | | Derivatives Available for Offset | | Non-cash

Collateral

Received | | | Cash Collateral Received | | | Net Amounts1 | |

| Total Return Equity Swaps | | $ 149,545 | | $ (13,680) | | | $ — | | | | $ — | | | | $ 135,865 | |

| | | | | | | | | | | | | | | | |

Offsetting of Financial Liabilities and Derivative Liabilities:

The following table presents the Fund's derivative liabilities by type net of amounts available for offset under a MNA and net of the related collateral pledged by the Fund as of December 31, 2015:

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Gross Amounts not offset in the Statement of Assets and Liabilities | | | | |

| Description | | Gross Amounts of Liabilities Presented in Statement of Assets and Liabilities | | | Derivatives Available for Offset | | | Non-cash

Collateral

Pledged | | | Cash

Collateral Pledged | | | Net Amounts2 | |

Total Return Equity Swaps | | $ | 13,680 | | | | $ (13,680 | ) | | $ | — | | | | $ — | | | | $ — | |

| | | | | | | | | | | | | | | | | | | | |

| 1 | Net amount represents the net amount receivable from the counterparty in the event of default. |

| 2 | Net amount represents the net amount payable to the counterparty in the event of default. |

Futures Contracts: The Fund is subject to foreign currency exchange rate risk in the normal course of pursuing its investment objectives. The Fund may purchase or sell futures contracts to hedge against foreign currency exchange risk or for any other purpose permitted by applicable law. The purchase of futures contracts may be more efficient or cost effective than actually buying the underlying securities or assets. A futures contract is an agreement between two parties to buy and sell an instrument at a set price on a future date and is exchange-traded. Upon entering into a futures contract, the Fund is required to pledge to the broker an amount of cash, U.S. Government

14

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued

securities or other high-quality debt securities equal to the minimum “initial margin” requirements of the exchange or the broker. Pursuant to a contract entered into with a futures commission merchant, the Fund agrees to receive from or pay to the firm an amount of cash equal to the cumulative daily fluctuation in the value of the contract. Such receipts or payments are known as “variation margin” and are recorded by the Fund as unrealized gains or losses. When the contract is closed, the Fund records a gain or loss equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed. The Fund will cover its current obligations under futures contracts by the segregation of liquid assets or by entering into offsetting transactions or owning positions covering its obligations. The risks of entering into futures contracts include the possibility that there may be an illiquid market and that a change in the value of the contracts may not correlate with changes in the value of the underlying securities or assets. The Fund’s maximum foreign currency exchange rate risk on those futures contracts where the underlying currency is long is an amount equal to the notional amount of the related contracts. During the year ended December 31, 2015, the Fund held no futures contracts where the underlying currency is long. The Fund’s maximum foreign currency exchange rate risk on those futures contracts where the underlying currency is short is theoretically unlimited. However, if effectively hedged, any loss would be offset in unrealized foreign currency gains of securities denominated in the same currency. For the year ended December 31, 2015, the Fund’s average volume of futures activity was $2,473,218 based on the quarterly notional amount. The notional amount represents the U.S. value of the contracts as of the day of the opening of the transaction.

Currency Hedging Transactions: The Fund may engage in certain transactions intended to hedge the Fund’s exposure to currency risks, including without limitation buying or selling options or futures, entering into forward foreign currency contracts, currency swaps or options on currency and currency futures and other derivative transactions. Hedging transactions can be expensive and have risks, including the imperfect correlation between the value of such instruments and the underlying assets, the possible default of the other party to the transaction or illiquidity of the derivatives instruments.

Foreign Currency Translations: The accounting records of the Fund are maintained in U.S. dollars. The Fund may purchase securities that are denominated in foreign currencies. Investment securities and other assets and liabilities denominated in foreign currency are translated into U.S. dollars at the current exchange rates. Purchases and sales of securities, income and expenses are translated into U.S. dollars at the exchange rates on the dates of the respective transactions.

Although the net assets of the Fund are calculated using the foreign exchange rates and market values at the close of the period, the Fund does not isolate that portion of the results of operations arising as a result of changes in the foreign exchange rates from the fluctuations arising from changes in the market prices of securities held at the end of the period. Similarly, the Fund does not isolate the effect of changes in foreign exchange rates from the fluctuations arising from changes in the market prices of long-term portfolio securities sold during the period. Accordingly, these foreign exchange gains or losses are included in the reported net realized and unrealized gain/(loss) on investments shown on the Statement of Operations.

Net realized gains or losses on foreign currency transactions represent net foreign exchange gains or losses from the holding of foreign currencies, currency gains or losses realized between the trade date and settlement date on securities transactions, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent amounts actually received or paid. Net unrealized currency gains or losses from valuing foreign currency denominated assets and liabilities (other than investments) at period end exchange rates are reflected as a component of net change in unrealized appreciation/depreciation on foreign currency transactions shown on the Statement of Operations.

Swap Agreements: The Fund is subject to equity price risk in the normal course of pursuing its investment objectives. The Fund may enter into swap agreements as a substitute for purchasing equity securities of issuers in the Energy Industry as defined in Note 1 above, to achieve the same exposure as it would by engaging in short sales transactions of energy securities, to hedge its currency exposure or for any other purpose permitted by applicable law. A swap is a financial instrument that typically involves the exchange of cash flows between two parties on specified dates (settlement dates) where the cash flows are based on agreed-upon prices, rates, etc. In a typical equity swap agreement, one party agrees to pay another party the return on a security or basket of securities in return for a specified interest rate. By entering into swaps, the Fund can gain exposure to a security without actually purchasing the underlying asset. Swap agreements involve both the risk associated with the investment in the security as well as the risk that the performance of the security, including any dividends, will not exceed the interest that the Fund will be committed

15

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued

to pay under the swap. Swaps are individually negotiated. Swap agreements may increase or decrease the overall volatility of the investments of the Fund and its net asset value. The performance of swap agreements may be affected by a change in the specific interest rate, security, currency, or other factors that determine the amounts of payments due to and from the Fund. The Fund will cover its current obligations under swap agreements by the segregation of liquid assets or by entering into offsetting transactions or owning positions covering its obligations. A swap agreement would expose the Fund to the same equity price risk as it would have if the underlying equity securities were purchased. The regulation of swaps and futures transactions in the United States is a rapidly changing area of law and is subject to modification by government and judicial action. The effect of any future regulatory change on the Fund is impossible to predict, but could be substantial and adverse.

The Fund’s maximum equity price risk to meet its future payments under long swap agreements outstanding as of December 31, 2015 is equal to the total notional amount as shown on the Schedule of Investments. The Fund’s maximum equity price risk to meet its future payments under short swap agreements outstanding is theoretically unlimited. For the year ended December 31, 2015, the average volume of long Total Return Equity Swaps was $4,481,509 based on the quarterly notional amount. For the year ended December 31, 2015, the Fund held no short Total Return Equity Swaps. The notional amount represents the U.S. value of the contracts as of the day of the opening of the transaction or latest contract reset date.

Options Contracts: The Fund is subject to equity price risk in the normal course of pursuing its investment objectives. The Fund may enter into option contracts in order to hedge against potential adverse price movements in the value of portfolio assets, as a temporary substitute for selling selected investments, to lock in the purchase price of a security or currency which it expects to purchase in the near future, as a temporary substitute for purchasing selected investments, to enhance potential gain, and for any other purpose permitted by applicable law. An option contract is a contract in which the writer of the option grants the buyer of the option the right to purchase from (call option), or sell to (put option), the writer a designated instrument at a specified price within a specified period of time. Certain options, including options on indices, would require cash settlement by the Fund if the option is exercised.

The liability representing the Fund’s obligation under an exchange-traded written option or investment in a purchased option is valued at the last sale price or, in the absence of a sale on such day, the mean between the closing bid and ask prices on such day or at the most recent asked price (bid for purchased options) if no bid and asked prices are available. OTC written or purchased options are valued using dealer supplied quotations. Gain or loss is recognized when the option contract expires or is closed.

If the Fund writes a covered call option, the Fund forgoes, in exchange for the premium, the opportunity to profit during the option period from an increase in the market value of the underlying security above the exercise price. If the Fund writes a put option it accepts the risk of a decline in the market value of the underlying security below the exercise price. OTC options have the risk of the potential inability of counterparties to meet the terms of their contracts. The Fund’s maximum equity price risk for purchased options is limited to the premium initially paid. In addition, certain risks may arise upon entering into option contracts including the risk that an illiquid secondary market will limit the Fund’s ability to close out an option contract prior to the expiration date and that a change in the value of the option contract may not correlate exactly with changes in the value of the securities or currencies hedged. For the year ended December 31, 2015, the Fund did not hold any option contracts.

Securities Transactions and Investment Income: Securities transactions are recorded on a trade date basis. Realized gain and loss from securities transactions are recorded on the specific identified cost basis. Dividend income is recognized on the ex-dividend date. Dividend income on foreign securities is recognized as soon as the Fund is informed of the ex-dividend date. Distributions received in excess of income are recorded as a reduction of cost of investments and/or as a realized gain. Interest income is recognized on the accrual basis. All discounts/premiums are accreted/amortized using the effective yield method.

Dividends and Distributions: At least annually, the Fund intends to distribute all or substantially all of its investment company taxable income (computed without regard to the deduction for dividends paid), if any, and net capital gain, if any. The tax treatment and characterization of the Fund’s distributions may vary significantly from time to time because of the varied nature of the Fund’s investments. The Fund will reinvest distributions in additional shares of the Fund unless a shareholder has written to request distributions, in whole or in part, in cash.

The tax character of distributions paid during the calendar year ended December 31, 2015 was as follows:

| | | | |

Ordinary Income | | $ | 103,685 | |

Long-Term Capital Gains | | $ | — | |

The tax character of distributions paid during the calendar year ended December 31, 2014 was as follows:

| | | | |

Ordinary Income | | $ | 2,160,985 | |

Long-Term Capital Gains | | $ | — | |

16

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued

The Fund is considered a nonpublicly offered regulated investment company (“RIC”) under the Internal Revenue Code of 1986, as amended (the “Code”). Thus, certain expenses of the Fund, including the investment advisory fee, are subject to special rules that can affect certain shareholders of the Fund (generally individuals and entities that compute their taxable income in the same manner as an individual). In particular, such a shareholder’s pro rata portion of the affected expenses for the calendar year (but generally reduced by the Fund’s net operating loss, if any, for its tax year ending within the calendar year), will be taxable to such shareholder as an additional dividend and such shareholder will be treated as having paid its pro rata share of the affected expenses itself. If such a shareholder itemizes its deductions, it generally should be entitled to take an offsetting deduction for its share of the affected expenses, subject, however, to the 2% “floor” on miscellaneous itemized deductions. These expenses will not be deductible for the purposes of calculating alternative minimum tax.

The Fund has a tax year end of June 30. As of June 30, 2015, the components of distributable earnings on a tax basis and other tax attributes were as follows:

| | | | |

Undistributed Ordinary Income | | $ | 103,685 | |

Capital Loss Carryforward | | $ | 14,874,804 | |

Post October Loss – Capital & Foreign Currency | | $ | 5,430 | |

Taxable income and capital gains are determined in accordance with U.S. federal income tax rules, which may differ from accounting principles generally accepted in the United States of America. These differences are primarily due to differing treatments of income and gains on various investment securities held by the Fund, timing differences and differing characterization of distributions made by the Fund.

Permanent book and tax accounting differences relating to the tax year ended June 30, 2015 have been reclassified to reflect a decrease in undistributed net investment loss of $801,267, an increase in accumulated net realized loss on investments of $704,979 and a decrease in paid-in-capital of $96,288. These differences are primarily due to passive loss limitations, pass through taxable income from investments and swap character reclasses. Net assets were not affected by this reclassification.

Capital Loss Carryforward: As of June 30, 2015, the following capital loss carryforwards are available to reduce taxable income arising from future net realized gains on investments, if any, to the extent permitted by the Internal Revenue Code:

| | | | |

| Year of Expiration | | | |

| |

2018 | | Total | |

| $14,874,804 | | $ | 14,874,804 | |

During the tax year ended June 30, 2015, the Fund utilized $2,652,707 of capital loss carryforwards expiring in 2018.

Federal Income Tax: The Fund intends to qualify each year for taxation as a RIC eligible for treatment under the provisions of Subchapter M of the Code. If the Fund so qualifies and satisfies certain distribution requirements, the Fund will not be subject to federal income tax on income and gains distributed in a timely manner to its shareholders in the form of dividends or capital gain dividends.

As of December 31, 2015, the cost of securities and gross unrealized appreciation and depreciation for all securities on a tax basis was as follows:

| | | | |

Total Cost of Investments | | $ | 13,064,723 | |

| | | | |

Gross Unrealized Appreciation

on Investments | | $ | 570,816 | |

Gross Unrealized Depreciation

on Investments | | | (2,088,674 | ) |

| | | | |

Net Unrealized Depreciation

on Investments | | $ | (1,517,858 | ) |

| | | | |

Management has analyzed the Fund’s tax positions taken on federal income tax returns for all open tax years and has concluded that no provision for federal income tax is required in the Fund’s financial statements.

The Fund files U.S. federal and Connecticut state tax returns. No income tax returns are currently under examination. The Fund’s U.S. federal tax returns and Connecticut state tax returns remain open for examination for the tax years ended June 30, 2015, June 30, 2014, June 30, 2013 and June 30, 2012.

Expenses: The Fund will pay all of its own expenses incurred in its operations. Expenses are recorded on an accrual basis.

3. INVESTMENT ADVISORY FEE, ADMINISTRATION FEE AND

OTHER RELATED PARTY TRANSACTIONS

Pursuant to an investment advisory agreement, Energy Income Partners, LLC, serves as the Fund’s investment manager with responsibility for the management of the Fund’s investment portfolio, subject to the supervision of the Board of the Trust. For providing such services, the Fund pays to the Manager a fee, computed and paid monthly at the annual rate of 1% of the average daily net assets of the Fund.

During the 2015 calendar year, the Bank of New York Mellon served as custodian for the Fund and had custody of all securities and cash of the Fund and attended to the collection of principal and income and payment for and collection of proceeds of securities bought and sold by the Fund.

17

EIP Growth and Income Fund

December 31, 2015

Notes to Financial Statements – continued