9united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-21853

Northern Lights Variable Trust

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450, Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

The Corporation Trust Company

1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2600

Date of fiscal year end: 12/31

Date of reporting period: 12/31/22

Item 1. Reports to Stockholders.

TOPS® Target Range™ Portfolio

A series of the Northern Lights Variable Trust

Annual Report

December 31, 2022

Distributed by Northern Lights Distributors, LLC

Member FINRA

A Message from the TOPS® Portfolio Management Team

End of Year 2022 Market Commentary

2022 – A Year of Survival

While we hope there were bright spots in 2022 for each of us, overall, it was a tough year for many investors. For stocks and bonds, 2022 was seemingly a year of survival. The S&P 500 Index (the “S&P 500”) fell 18.1% for the year, the 3rd worst year for the S&P 500 going back to 1980. Average bond investors did not fare much better, as the Bloomberg U.S. Aggregate Bond Index (the “U.S. Aggregate Bond Index”) lost 13.1%. Going back to 1976, this is the worst return for the U.S. Aggregate Bond Index and only the 5th negative annual return over that period. The next closest was a -3% loss in 1994.

With 2022 creating so many hurdles, many professional managers struggled as well. According to Bloomberg, there are 865 actively managed stock mutual funds domiciled in the U.S. with at least $1 Billion in assets. On average, those 865 mutual funds lost -19% in 2022. Likewise, a 60/40 mix of the S&P 500 and U.S. Aggregate Bond Index would have returned a loss of about 16.1%

We often discuss investment markets using the term “cycles.” As the literal meaning would connotate, markets tend to follow certain cycles for various lengths of time. The pervasive cycle of outperformance of large cap growth U.S. stocks, primarily tech stocks, lasted for about a decade. When the tide receded for growth stocks, the exceptionally high valuations revealed risk levels higher than most investors were willing to take. Further, the long cycle of growth outperformance was fueled by abnormally low interest rates and extremely high access to capital. We believe, the next decade may look very different.

As we look out to the next 10 years, we see an environment where the Federal Reserve (the “Fed”) may be much less accommodating than the last 10 years. The era of the “Fed Put”, the Fed bailing out markets at every slip, seems to be over for now. At least for the next few years, higher interest rates should significantly increase the cost of capital for growth companies. Also, investors will likely ask for more concrete results when the risk-free rate (U.S. Treasury yield) is providing returns over 4%. This may have been a contributor as Tesla saw its stock price fall -65% in 2022, followed by Apple and Microsoft, at -26.3% and -27.9% respectively. Despite these significant retractions, valuations for large cap growth stocks remain higher than most of the other major asset classes we maintain exposure to.

Given what we know, and the modeling we employ regarding what we do not know for sure, we believe our TOPS strategies are well positioned for the next 10 years. Importantly, we are encouraged by the higher yields available for fixed income holdings and the historically attractive valuations for many of our asset classes, such as small cap, mid cap, international and emerging markets. Additionally, we highlight the continued historically strong valuation of the U.S. Dollar (USD). If the USD were to weaken in 2023 (or throughout the next cycle), it would be a boost to the returns of our international investments.

After discussing Q4 2022 financial market results, we will address three general themes important to TOPS portfolio returns and strategies:

| 1) | It is all about the Fed |

| 2) | If we have a 2023 recession, what will it look like? |

| 3) | What’s in store for stocks and bonds in 2023? |

Year-To-Date Markets Review

Equity indexes saw positive returns in the fourth quarter. Value stocks (S&P 500 Value) outperformed growth stocks (S&P 500 Growth), returning +13.6% and +1.4%, respectively. Midcap (S&P 400, +10.8%) outperformed both small cap equities (S&P 600, +9.2%) and large cap equities (S&P 500, +7.6%). Developed international (MSCI EAFE) returned +17.3%, outpacing emerging markets (MSCI Emerging Markets), which returned +9.7%. Natural resources (S&P GSSI NA Natural Resources) and real estate (MSCI World Real Estate) were both positive as well in the fourth quarter, up +18.3% and +5.6%, respectively.

Even with a positive fourth quarter, most equity indexes were still negative for the year. The exception is natural resources with the S&P GSSI Natural Resources Index providing +34.1% returns in 2022. Value stocks (S&P 500 Value) returned -5.2% and significantly outperformed growth stocks (S&P 500 Growth), which returned -29.4%. Midcap (S&P 400, -13.1%) outperformed both small cap equities (S&P 600, -16.1%) and large cap equities (S&P 500, -18.1%). Developed international (MSCI EAFE) returned -14.5% this year, outpacing emerging markets (MSCI Emerging Markets) which returned -7.0%. Real estate (MSCI World Real Estate) was down -25.1% in 2022.

Like equity returns, we also started to see positive fixed income returns in the fourth quarter. The Bloomberg U.S. Aggregate Bond Index had a +1.9% return for the quarter, while the Bloomberg U.S. TIPS Index was up +2.0%. Credit (ICE BofA U.S. Corporate Index, +3.5%) outperformed government (ICE BofA U.S. Treasury Index, +0.7%). High yield (Solactive USD High Yield Corporates, +4.2%), investment grade corporates (iBoxx USD Liquid Investment Grade Index, +4.2%), and international bond indexes (Bloomberg Global Aggregate ex-USD, +0.1%) were also positive. The 10-year U.S. Treasury yield increased from 3.83% to 3.88% in the fourth quarter.

For the year, we saw credit (ICE BofA U.S. Corporate Index, -15.4%) underperformed government (ICE BofA U.S. Treasury Index, -12.9%), and shorter duration holdings outperform longer duration holdings. This was seen in both credit markets, with the Bloomberg U.S. Corporate 1-3 year (-3.3%), and government markets, Bloomberg U.S. Treasury 1-3 Year (-3.8%), where the shorter duration indexes outperformed the previously mentioned full duration indexes. Even with positive fourth quarter returns, high yield (Solactive USD High Yield Corporates, -11.0%), international bond indexes (Bloomberg Global Aggregate ex-USD, -12.7%), and investment grade corporates (iBoxx USD Liquid Investment Grade Index, -17.9%) remained negative for the year. Over the course of 2022, the 10-year U.S. Treasury yield increased from 1.52% to 3.88%.

It is all about the Fed

As we discussed throughout 2022, the Federal Reserve remains in the economic driver seat. The Fed is carrying out a tightening monetary policy in an effort to cool high levels of inflation. For stock investors, a major fear is that a strong labor market may force the Fed to maintain high (and/or increasing) interest rates until they push the economy into recession (directly or indirectly).

As we model this situation, we are consistently asking ourselves, what can go right and what can go wrong? Ultimately, there are many inputs of varying impact which will decide the highest level of the Fed Funds Rate (called the terminal rate) and the amount of time it stays there. Levels of inflation, employment and wage growth will likely be the most impactful inputs.

Just after the end of the year, we got the December jobs numbers. According to the Wall Street Journal, “Employers added 223,000 jobs in December, the smallest gain in two years, the Labor Department said Friday. Average hourly earnings were up 4.6% in December from the previous year, the narrowest increase since mid-2021, and down from a March peak of 5.6%.” The report could be considered Goldilocks, not too hot and not too cool.

In response to the numbers, BMO reminded us, “the Fed has assumed that a strong labor market would lead to excessive wage growth which, in turn, would lead to inflation pressures.” Maybe though, we can thread the needle and have inflation cool even as jobs remain robust. For this to happen, wage growth must remain tame. These numbers, along with recent highly publicized layoffs in the tech arena, are encouraging investors that the Fed may back off a bit in response to the Goldilocks report. However, there are still about 1.8 jobs per each unemployed worker, according to Lazard. Likewise, Labor Force Participation numbers remain at the lowest levels since the 1970s, other than the depths of the pandemic of course. Both facts would typically place upward pressure on wages.

The next Fed policy meeting starts January 31st. Currently, markets are pricing in an equal probability of a 0.25% or 0.50% rate increase at the meeting. Before that meeting, important inflation figures, called the Consumer Price Index (CPI), will be released on January 12th. Fortunately, inputs to the CPI number seem to be trending lower, including gas prices, used car prices, residential rent, goods prices, and retail prices.

As the Fed saga of 2022 enters another year, we continue the search for the soft landing, the opportunity for inflation to subside without a significant recession. The Fed has outlined that their path is going to be data driven and take a while, so patience is necessary. As noted in previous messages, though, we believe stocks will be leading indicators and eventually lead coming out of any economic slowdown.

If we have a 2023 recession, what will it look like?

The word recession can strike fear for investors. However, recessions do happen, and they are likely a necessary evil in the longer-term success of economies. Economists believe we are more likely than not to have a recession in 2023. In Bloomberg’s December survey of economists, the consensus estimate was a 70% chance of recession in 2023, up from 65% in November. The story is much bigger than whether we experience a recession though. The key for markets will be the type of recession we get (if one develops). Will it be short or long? Deep or shallow? Broad or rolling?

A recession which is short, shallow, and rolling looks very different from a recession which is long, deep, and broad. Obviously, there are many different combinations between as well. A recession which is short, shallow, and rolling could have little impact on stocks. Actually, stocks may respond positively, as a mellow recession would potentially be better than what is currently priced into stocks. We do not believe stocks have priced in a long, deep, and broad recession. If a long, deep, and broad recession materializes, we believe this will have a negative short-term impact on stock prices.

It is impossible for anyone to confidently predict whether a recession is coming or not, let alone what that recession will look like. According to our research, we feel there is at least a 50% chance we see a recession in 2023. However, we believe stock prices are already reflecting some recessionary concerns and the likelihood of a long, deep, and broad recession is quite low.

Regardless of whether we experience a recession in 2023, we believe our allocations remain appropriate for our long-term investors. Now that 2023 is starting, stock valuations are already starting to reflect earnings in 2024 and beyond, which look pretty good at this point. Ultimately, earnings are the fuel for stocks. Over the next 12-24 months, we are likely to see analysts making meaningful adjustments to earnings expectations, as the Fed saga plays out and the recession question gets answered. While 2023 may in fact turn out to be another “year of survival”, longer-term investors should be rewarded for that risk.

What’s in store for stocks and bonds in 2023?

For quite a long time, we highlighted the relatively high valuations U.S. large cap stocks were recording. As expected, given the concerns of the year, 2022 resulted in “blowing off the froth” on stock valuations. Valuations, which were well above average, fell closer to average for large caps. The story was different for small caps, mid-caps, international and emerging markets though. For these markets, valuations started the decline at lower levels. So, these markets blew off a much smaller amount of froth before they hit averages and are now hovering well below average.

How does this impact 2023? Well, as mentioned earlier, there is no guarantee 2023 will be the end of the current Fed saga. Successful investing typically requires patience, and 2023 may test the patience of all of us. On the other hand, if the Fed is successful in corralling inflation and delivering a soft landing, the expected bounce in securities may be led by some of the markets which currently exhibit more attractive valuations.

Historically, small cap stocks have tended to lead coming out of bear markets, international stocks boast attractive valuations, and there is potential for USD trends to revert. These factors lead us to believe some of these asset classes have a viable opportunity for strong performance when “risk on” shifts into gear. Included in our analysis, and relative focus on diversified asset classes, is the concern it could be another tough year for tech stocks, and it might be a bold time to bargain shop for vanity brands, such as Tesla, etc. Many of these darlings remain highly valued, even after major pullbacks from astronomic price levels.

TOPS Portfolio Strategies

We cannot say we are sad to see 2022 go. Our 20th year of managing portfolios (as a firm) was one of the toughest we have had. While still paling in comparison to the challenges of the financial crisis in 2008, 2022 provided unique trials. That being said, from a relative perspective, 2022 was a very strong year for our portfolios overall. An accountant’s job is not to bring your tax bill to zero; their job is to professionally execute a strategy which provides the best overall result, accounting for risk and return of tax strategies. Our role is similar in many ways; in that vein, we are pleased with what we were able to provide in a year of survival.

Now that we have survived 2022, we live to fight another day. With the confidence of our investors, we will continue to strive to deliver results to the best of our abilities. Thank you to all our investors for your confidence in us throughout the storm of 2022, and your confidence in us leading up to 2023, which provided us the opportunity to fight for you last year.

Summary of the Target Range™ (TR) Strategy

The TOPS® Target Range Fund, is a unique fund which follows the methodology of the innovative TOPS® Global Equity Target Range™ Index. The Fund is managed by Valmark Advisers, Inc and Milliman Financial Risk Management, LLC.

TR provides investors with the unique opportunity to participate in equity markets, with downside protection. To provide this experience, the fund typically enters into 1-year options investments each January (around the 3rd week of the month) on SPY (S&P 500 ETF- Large Cap U.S. stocks), IWM (Russell 2000 ETF – Mid/Small Cap U.S. Stocks), EFA (EAFE ETF – International Developed Markets), and EEM (MSCI Emerging Markets – Emerging Markets Stocks).

As options expire in late January, the full investment period from January 2022 was not yet over as of the time of this report. In January 2023, options contracts purchased in 2022 expire and new options contracts expiring in 2024 will be purchased through a process called the annual roll.

Here is some Q&A you might find helpful regarding TR:

Is there anything you need to do regarding the annual roll?

As a current shareholder of TR, there is no action needed on your part. TR is designed to be used as a long-term holding and automatically go through these annual rolls, like how many portfolios go through an annual rebalance. The roll is scheduled to occur each year automatically going forward.

What happens on the annual roll?

Upon the annual roll (when options expire the third week of January each year) a new bull call spread options package is typically purchased with exposure to SPY, IWM, EFA and EEM. 50% of the options exposure is typically allocated to cover SPY (U.S. Large Cap Stocks), 20% to IWM (U.S. Mid/Small Cap U.S. Stocks) 20% to EFA (International Developed Markets) and 10% to EEM (Emerging Markets Stocks). Based on those proportions, GTR purchases a target 15% in-the-money long call option and sells a target 15% out-of-the money call option. This creates the call spread, with a Target Range™ of +/- 15% at initial reset.

What can I expect for the next 12 months holding GTR?

We feel the market conditions for the January 2024 roll are particularly attractive for TR, as TR benefits from higher interest rates in 2023. On 1/17/2022, the 3-month U.S. Treasury was paying 0.17% and on 1/29/2023, it was paying 4.72%. Since the majority of assets are typically invested in short-term fixed income investments, these higher yields should lead to higher portfolio interest overall.

For the roll period ending in 2023, after the end of the period covered by this report, TR finished near the lower protection level for the period. This shows TR performed in line with our expectations. If stocks would have stayed at their lows for the year, TR would have outperformed significantly. As it turned out, TR provided appropriate returns, with less risk and volatility than the underlying long only ETF exposures.

As mentioned, 2023 provides a nice opportunity for TR. Compared to the 2022 roll, the options package should be slightly costlier by an estimated roughly 1%. This is due to higher interest rates, which raise the cost of the options slightly. However, the rate for the 3-month U.S. Treasury on January 19, 2023 (for the roll this year) is paying 4.72%. So, we feel the net effect of higher interest could benefit our investors by several percent in the roll period starting in January 2023.

For the year ending 12/31/2022, the TOPS Target Range Fund finished down a little over -19% (see performance information for each share class and period included in this report). This performance was in line with expectations, given market trajectory. A unique aspect of 2022 particularly, was that the market was down significantly between 1/1/2022 and the 1/19/2022 roll date of the fund. This caused the fund to be down about -4.65% for the year before the roll date, leading the fund to fall greater than -15% for the calendar year. As a reminder, the 15% Target Range bull call spread is run from the 3rd week in January to the following 3rd week in January, not on a calendar year cycle.

The MSCI EAFE® Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada. As of June 2007 the MSCI EAFE Index consisted of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

The MSCI Emerging Markets Index is a free float-adjusted, market capitalization-weighted index designed to measure the combined equity market performance of the materials sector of emerging markets countries. Component securities include those of chemical companies, construction materials companies, containers and packaging companies, metals and mining companies, and paper and forest products companies.

The S&P 500® Index is an unmanaged composite of 500 large capitalization companies. This index is widely used by professional investors as a performance benchmark for large-cap stocks.

The S&P Growth Index represents the growth companies of the S&P 500 Index.

The S&P MidCap 400® measures the mid-cap segment of the U.S.equity market. The index is designed to be an investable portfolio of companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

The S&P SmallCap 600® measures the small cap segment of the U.S. equity market. The index is designed to be an investable portfolio of companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

The Bloomberg U.S. Aggregate Bond Index is weighted according to market capitalization, which means the securities represented in the index are weighted according to the market size of the bond category. Treasury securities, mortgage-backed securities (“MBS”) foreign bonds, government agency bonds and corporate bonds are some of the categories included in the index. The bonds represented are medium term with an average maturity of about 4.57 years. In all, the index represents about 8,200 fixed-income securities with a total value of approximately $15 trillion (about 43% of the total U.S. bond market).

The Bloomberg U.S. Treasury Inflation Protected Securities Index (“TIPS”) Index includes all publicly issued, U.S. Treasury inflation-protected securities that have at least one year remaining to maturity, are rated investment grade, and have $250 million or more of outstanding face value.

You cannot invest directly in an index and unmanaged index returns do not reflect any fees, expenses or sales charges. Past Performance is no guarantee of future results. Past performance does not guarantee future results, and current performance may be lower or higher than the data quoted.

5174-NLD-02012023

TOPS® Target Range™ Portfolio

Portfolio Review (Unaudited)

December 31, 2022

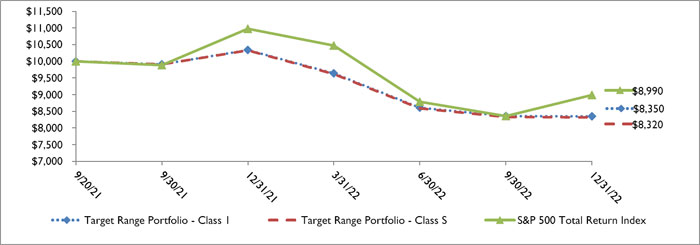

The Portfolio’s Average Annual Total Return through December 31, 2022*, as compared to its benchmark:

| | | Performance Since |

| | One Year | Inception (9/20/21) |

| Target Range Portfolio | | |

| Class 1 | -19.24% | -13.14% |

| Class 2 | -19.24% | -13.14% |

| Class S | -19.46% | -13.39% |

| S&P 500 Total Return Index ** | -18.11% | -7.98% |

| * | The performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Portfolio distributions or on the redemption of Portfolio shares as well as other charges and expenses of the insurance contract, or separate account. Per the fee table in the most recent prospectus, the Portfolio’s total annual operating expense ratios including acquired fund fees and expenses, for Class 1, Class 2, and Class S are 0.52%, 0.77% and 0.97%, respectively. For performance information current to the most recent month-end, please call 1-855-572-5945. |

| ** | The S&P 500 Total Return Index is an unmanaged market capitalization-weighted index of 500 of the largest capitalized U.S. domiciled companies. Index returns assume reinvestment of dividends. Investors may not invest in the index directly; unlike the Portfolio’s returns, the Index does not reflect any fees or expenses. |

Comparison of the Change in Value of a $10,000 Investment

| Holdings by Asset Class as of December 31, 2022 | | % of Net Assets | |

| Exchange-Traded Funds - Fixed Income | | | 67.8 | % |

| Short-Term Investments | | | 30.2 | % |

| Call Options Purchased | | | 1.0 | % |

| Other Assets in Excess of Liabilities | | | 1.0 | % |

| | | | 100.0 | % |

Please refer to the Schedule of Investments in this annual report for a detailed listing of the Portfolio’s holdings.

| TOPS® Target Range™ Portfolio |

| Schedule of Investments |

| December 31, 2022 |

| Shares | | | | | Fair Value | |

| | | | | EXCHANGE-TRADED FUNDS — 67.8% | | | | |

| | | | | FIXED INCOME - 67.8% | | | | |

| | 31,225 | | | Goldman Sachs Access Treasury 0-1 Year ETF | | $ | 3,113,445 | |

| | 41,525 | | | iShares 0-3 Month Treasury Bond ETF(a) | | | 4,158,313 | |

| | 34,078 | | | SPDR Bloomberg 1-3 Month T-Bill ETF | | | 3,117,115 | |

| | 53,022 | | | Vanguard Short-Term Treasury ETF(a) | | | 3,065,732 | |

| | | | | | | | 13,454,605 | |

| | | | | | | | | |

| | | | | TOTAL EXCHANGE-TRADED FUNDS (Cost $13,523,365) | | | 13,454,605 | |

| | | | | | | | | |

| Shares | | | | | Fair Value | |

| | | | | SHORT-TERM INVESTMENTS — 30.2% | | | | |

| | | | | MONEY MARKET FUNDS - 30.2% | | | | |

| | 5,998,855 | | | STIT - Government & Agency Portfolio, Institutional Class, 4.21% (Cost $5,998,855)(b) | | | 5,998,855 | |

| | | | | | | | Expiration | | Exercise | | | | | | | |

| Contracts(c) | | | | | Broker/Counterparty | | Date | | Price | | | Notional Value | | | Fair Value | |

| | | | | CALL OPTIONS PURCHASED - 1.0% | | | | | | | | | | | | | | | | |

| | 599 | | | iShares MSCI EAFE ETF | | SOC | | 01/20/2023 | | $ | 67 | | | $ | 3,931,836 | | | $ | 41,411 | |

| | 472 | | | iShares MSCI Emerging Markets ETF | | SOC | | 01/20/2023 | | | 42 | | | | 1,788,880 | | | | 1,420 | |

| | 227 | | | iShares Russell 2000 ETF | | SOC | | 01/20/2023 | | | 180 | | | | 3,957,972 | | | | 41,269 | |

| | 258 | | | SPDR S&P 500 ETF Trust | | SOC | | 01/20/2023 | | | 390 | | | | 9,866,694 | | | | 114,036 | |

| | | | | TOTAL CALL OPTIONS PURCHASED (Cost - $2,076,415) | | | | | | | 198,136 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | TOTAL INVESTMENTS - 99.0% (Cost $21,598,635) | | | | | | $ | 19,651,596 | |

| | | | | CALL OPTIONS WRITTEN - 0.0% (Proceeds - $88,027) | | | | | | | (843 | ) |

| | | | | OTHER ASSETS IN EXCESS OF LIABILITIES- 1.0% | | | | | | | 198,876 | |

| | | | | NET ASSETS - 100.0% | | | | | | $ | 19,849,629 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | Expiration | | Exercise | | | | | | | |

| Contracts(c) | | | | | Broker/Counterparty | | Date | | Price | | | Notional Value | | | Fair Value | |

| | | | | CALL OPTIONS WRITTEN- 0.0%(d) | | | | | | | | | | | | | | | | |

| | 599 | | | iShares MSCI EAFE ETF | | SOC | | 01/20/2023 | | $ | 90 | | | $ | 3,931,836 | | | $ | 600 | |

| | 472 | | | iShares MSCI Emerging Markets ETF | | SOC | | 01/20/2023 | | | 57 | | | | 1,788,880 | | | | — | |

| | 227 | | | iShares Russell 2000 ETF | | SOC | | 01/20/2023 | | | 240 | | | | 3,957,972 | | | | 114 | |

| | 258 | | | SPDR S&P 500 ETF Trust | | SOC | | 01/20/2023 | | | 525 | | | | 9,866,694 | | | | 129 | |

| | | | | TOTAL CALL OPTIONS WRITTEN (Proceeds - $88,027) | | | | | | | 843 | |

ETF - Exchange-Traded Fund

MSCI - Morgan Stanley Capital International

S&P - Standard & Poor’s

SOC - Societe Generale

SPDR - Standard & Poor’s Depositary Receipt

| (a) | All or part of these securities were held as collateral for call options written as of December 31, 2022. Total collateral for call options written is $337,714 in securities and $189,083 in cash. |

| (b) | Rate disclosed is the seven day effective yield as of December 31, 2022. |

| (c) | Each option contract allows the holder of the option to purchase or sell 100 shares of the underlying security. |

| (d) | Percentage rounds to greater than (0.1%). |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Statement of Assets and Liabilities |

| December 31, 2022 |

| Assets: | | | | |

| Investments in securities, at cost | | $ | 21,598,635 | |

| Investments in securities, at value | | $ | 19,651,596 | |

| Deposits with Broker | | | 189,083 | |

| Interest and dividends receivable | | | 28,837 | |

| Total Assets | | | 19,869,516 | |

| Liabilities: | | | | |

| Due to Custodian | | | 523 | |

| Options written, at value (premiums received $88,027) | | | 843 | |

| Payable for Portfolio shares redeemed | | | 539 | |

| Accrued investment advisory fees | | | 5,733 | |

| Accrued distribution (12b-1) fees | | | 7,693 | |

| Payable to related parties and administrative service fees | | | 4,556 | |

| Total Liabilities | | | 19,887 | |

| Net Assets | | $ | 19,849,629 | |

| | | | | |

| Components of Net Assets: | | | | |

| Paid-in capital | | $ | 21,630,811 | |

| Accumulated loss | | | (1,781,182 | ) |

| Net Assets | | $ | 19,849,629 | |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Statement of Assets and Liabilities (Continued) |

| December 31, 2022 |

| Class 1 Shares: | | | | |

| Net assets | | $ | 8 | |

| Total shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 1 | |

| | | | | |

| Net asset value, offering and redemption price per share (Net assets ÷ Total shares of beneficial interest outstanding) | | $ | 8.35 | (a) |

| | | | | |

| Class 2 Shares: | | | | |

| Net assets | | $ | 8 | |

| Total shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 1 | |

| | | | | |

| Net asset value, offering and redemption price per share (Net assets ÷ Total shares of beneficial interest outstanding) | | $ | 8.35 | (a) |

| | | | | |

| Class S Shares: | | | | |

| Net assets | | $ | 19,849,613 | |

| Total shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | | | 2,384,401 | |

| | | | | |

| Net asset value, offering and redemption price per share (Net assets ÷ Total shares of beneficial interest outstanding) | | $ | 8.32 | |

| (a) | NAV does not recalculate due to rounding of net assets. |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Statement of Operations |

| For the Year Ended December 31, 2022 |

| Investment Income: | | | | |

| Dividend income | | $ | 161,345 | |

| Interest income | | | 85,902 | |

| Total Investment Income | | | 247,247 | |

| Expenses: | | | | |

| Investment advisory fees | | | 43,373 | |

| Distribution fees (12b-1) | | | | |

| Class S Shares | | | 54,326 | |

| Related parties and administrative service fees | | | 18,905 | |

| Total Expenses | | | 116,604 | |

| Net Investment Income | | | 130,643 | |

| | | | | |

| Realized and Unrealized Gain (Loss) on Investments and Options Written: | | | | |

| Net realized gain (loss) on: | | | | |

| Investments | | | (56,984 | ) |

| Options written | | | 5,478 | |

| Total net realized loss | | | (51,506 | ) |

| Net change in unrealized appreciation (depreciation) on: | | | | |

| Investments | | | (1,972,338 | ) |

| Options written | | | 85,810 | |

| Total unrealized depreciation | | | (1,886,528 | ) |

| Net Realized and Unrealized Loss on Investments and Options Written | | | (1,938,034 | ) |

| Net Decrease in Net Assets Resulting from Operations | | $ | (1,807,391 | ) |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Statements of Changes in Net Assets |

| | | Year Ended | | | Period Ended | |

| | | December 31, 2022 | | | December 31, 2021 (a) | |

| Increase (Decrease) in Net Assets: | | | | | | | | |

| From Operations: | | | | | | | | |

| Net investment income (loss) | | $ | 130,643 | | | $ | (870 | ) |

| Net realized gain (loss) on investments and options written | | | (51,506 | ) | | | 116 | |

| Distributions of realized gains by underlying investment companies | | | — | | | | 302 | |

| Net change in unrealized appreciation (depreciation) on investments and options written | | | (1,886,528 | ) | | | 26,673 | |

| Net increase (decrease) in net assets resulting from operations | | | (1,807,391 | ) | | | 26,221 | |

| From Distributions to Shareholders: | | | | | | | | |

| Total Distributions Paid | | | | | | | | |

| Class 1 | | | (0 | ) (b) | | | — | |

| Class 2 | | | (0 | ) (b) | | | — | |

| Class S | | | (478 | ) | | | — | |

| Total distributions to shareholders | | | (478 | ) | | | — | |

| From Shares of Beneficial Interest: | | | | | | | | |

| Proceeds from shares sold | | | | | | | | |

| Class 1 | | | — | | | | 750,000 | |

| Class 2 | | | — | | | | 10 | |

| Class S | | | 21,732,256 | | | | 175,471 | |

| Reinvestment of distributions | | | | | | | | |

| Class 1 | | | 0 | (b) | | | — | |

| Class 2 | | | 0 | (b) | | | — | |

| Class S | | | 478 | | | | — | |

| Cost of shares redeemed | | | | | | | | |

| Class 1 | | | (684,526 | ) | | | — | |

| Class S | | | (292,292 | ) | | | (50,120 | ) |

| Net increase in net assets from share transactions of beneficial interest | | | 20,755,916 | | | | 875,361 | |

| Total Increase In Net Assets | | | 18,948,047 | | | | 901,582 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of year/period | | | 901,582 | | | | — | |

| End of year/period | | $ | 19,849,629 | | | $ | 901,582 | |

| (a) | The TOPS® Target Range™ Portfolio commenced operations on September 20, 2021. |

| (b) | Represents less than $1. |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Statements of Changes in Net Assets (Continued) |

| | | Year Ended | | | Period Ended | |

| | | December 31, 2022 | | | December 31, 2021 (a) | |

| SHARE ACTIVITY | | | | | | | | |

| Class 1 | | | | | | | | |

| Shares Sold | | | — | | | | 75,000 | |

| Shares Reinvested | | | 0 | (b) | | | — | |

| Shares Redeemed | | | (74,999 | ) | | | — | |

| Net increase (decrease) in shares of beneficial interest outstanding | | | (74,999 | ) | | | 75,000 | |

| | | | | | | | | |

| Class 2 | | | | | | | | |

| Shares Sold | | | — | | | | 1 | |

| Shares Reinvested | | | 0 | (b) | | | — | |

| Net increase in shares of beneficial interest outstanding | | | 0 | (b) | | | 1 | |

| | | | | | | | | |

| Class S | | | | | | | | |

| Shares Sold | | | 2,406,351 | | | | 17,119 | |

| Shares Reinvested | | | 55 | | | | — | |

| Shares Redeemed | | | (34,133 | ) | | | (4,991 | ) |

| Net increase in shares of beneficial interest outstanding | | | 2,372,273 | | | | 12,128 | |

| (a) | The TOPS® Target Range™ Portfolio commenced operations on September 20, 2021. |

| (b) | Represents less than one share |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Financial Highlights |

| Selected data based on a share outstanding throughout each year/period indicated. |

| | | Class 1 Shares | |

| | | Year Ended | | | Period Ended | |

| | | December 31, 2022 | | | December 31, 2021 (a) | |

| Net asset value, beginning of year/period | | $ | 10.35 | | | $ | 10.00 | |

| Income (loss) from investment operations: | | | | | | | | |

| Net investment loss (b)(c) | | | (0.01 | ) | | | (0.01 | ) |

| Net realized and unrealized gain (loss) on investments and options written | | | (1.99 | ) | | | 0.36 | |

| Total income (loss) from investment operations | | | (2.00 | ) | | | 0.35 | |

| Less distributions from: | | | | | | | | |

| Net realized gain | | | (0.00 | ) (g) | | | — | |

| Total distributions | | | (0.00 | ) (g) | | | — | |

| Net asset value, end of year/period | | $ | 8.35 | (h) | | $ | 10.35 | |

| Total return (d) | | | (19.24 | )% | | | 3.50 | % (i)(j) |

| Ratios and Supplemental Data: | | | | | | | | |

| Net assets, end of year/period (e) | | $ | 8.00 | | | $ | 776,202 | |

| Ratio of expenses to average net assets (f) | | | 0.50 | % | | | 0.45 | % (k) |

| Ratio of net investment loss to average net assets (c)(f) | | | (0.06 | )% | | | (0.33 | )% (k) |

| Portfolio turnover rate | | | 46 | % | | | 14 | % (j) |

| (a) | The TOPS® Target Range™ Portfolio Class 1 commenced operations on September 20, 2021. |

| (b) | Net investment loss has been calculated using the average shares method, which more appropriately presents the per share data for the year/period. |

| (c) | Recognition of net investment loss by the Portfolio is affected by the timing of the declaration of dividends by the underlying investment companies in which the Portfolio invests. |

| (d) | Total returns are historical and assume changes in share price and reinvestment of dividends and capital gains distributions, if any. |

| (e) | Rounded net assets, not truncated. |

| (f) | Does not include the expenses of the underlying investment companies in which the Portfolio invests. |

| (g) | Amount represents less than $0.01 per share. |

| (h) | NAV does not recalculate due to rounding of net assets. |

| (i) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Financial Highlights |

| Selected data based on a share outstanding throughout each year/period indicated. |

| | | Class 2 Shares | |

| | | Year Ended | | | Period Ended | |

| | | December 31, 2022 | | | December 31, 2021 (a) | |

| Net asset value, beginning of year/period | | $ | 10.35 | | | $ | 10.00 | |

| Income (loss) from investment operations: | | | | | | | | |

| Net investment income (loss) (b) (c) | | | 0.06 | | | | (0.00 | ) (h) |

| Net realized and unrealized gain (loss) on investments and options written | | | (2.06 | ) | | | 0.35 | |

| Total income (loss) from investment operations | | | (2.00 | ) | | | 0.35 | |

| Less distributions from: | | | | | | | | |

| Net realized gain | | | (0.00 | ) (h) | | | — | |

| Total distributions | | | (0.00 | ) (h) | | | — | |

| Net asset value, end of year/period (d) | | $ | 8.35 | | | $ | 10.35 | |

| Total return (e) | | | (19.24 | )% | | | 3.50 | % (i)(j) |

| Ratios and Supplemental Data: | | | | | | | | |

| Net assets, end of year/period (f) | | $ | 8 | | | $ | 10 | |

| Ratio of expenses to average net assets (g) | | | 0.75 | % | | | 0.70 | % (k) |

| Ratio of net investment income (loss) to average net assets (c) (g) | | | 0.19 | % | | | (0.08 | )% (k) |

| Portfolio turnover rate | | | 46 | % | | | 14 | % (j) |

| (a) | The TOPS® Target Range™ Portfolio Class 2 commenced operations on September 20, 2021. |

| (b) | Net investment income (loss) has been calculated using the average shares method, which more appropriately presents the per share data for the year/period. |

| (c) | Recognition of net investment income (loss) by the Portfolio is affected by the timing of the declaration of dividends by the underlying investment companies in which the Portfolio invests. |

| (d) | NAV does not recalculate due to rounding of net assets. |

| (e) | Total returns are historical and assume changes in share price and reinvestment of dividends and capital gains distributions, if any. |

| (f) | Rounded net assets, not truncated. |

| (g) | Does not include the expenses of the underlying investment companies in which the Portfolio invests. |

| (h) | Amount represents less than $0.01 per share. |

| (i) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Financial Highlights |

| Selected data based on a share outstanding throughout each year/period indicated. |

| | | Class S Shares | |

| | | Year Ended | | | Period Ended | |

| | | December 31, 2022 | | | December 31, 2021 (a) | |

| Net asset value, beginning of year/period | | $ | 10.34 | | | $ | 10.00 | |

| Income (loss) from investment operations: | | | | | | | | |

| Net investment income (loss) (b)(c) | | | 0.09 | | | | (0.02 | ) |

| Net realized and unrealized gain (loss) on investments and options written | | | (2.11 | ) | | | 0.36 | |

| Total income (loss) from investment operations | | | (2.02 | ) | | | 0.34 | |

| Less distributions from: | | | | | | | | |

| Net realized gain | | | (0.00 | ) (f) | | | — | |

| Total distributions | | | (0.00 | ) (f) | | | — | |

| Net asset value, end of year/period | | $ | 8.32 | | | $ | 10.34 | |

| Total return (d) | | | (19.46 | )% | | | 3.40 | % (g)(h) |

| Ratios and Supplemental Data: | | | | | | | | |

| Net assets, end of year/period (000’s) | | $ | 19,850 | | | $ | 125 | |

| Ratio of expenses to average net assets (e) | | | 0.95 | % | | | 0.90 | % (i) |

| Ratio of net investment income (loss) to average net assets (c)(e) | | | 1.08 | % | | | (0.76 | )% (i) |

| Portfolio turnover rate | | | 46 | % | | | 14 | % (h) |

| (a) | The TOPS® Target Range™ Portfolio Class S commenced operations on September 20, 2021. |

| (b) | Net investment income (loss) has been calculated using the average shares method, which more appropriately presents the per share data for the year/period. |

| (c) | Recognition of net investment income (loss) by the Portfolio is affected by the timing of the declaration of dividends by the underlying investment companies in which the Portfolio invests. |

| (d) | Total returns are historical and assume changes in share price and reinvestment of dividends and capital gains distributions, if any. |

| (e) | Does not include the expenses of the underlying investment companies in which the Portfolio invests. |

| (f) | Amount represents less than $0.01 per share. |

| (g) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

See accompanying notes to financial statements.

| TOPS® Target Range™ Portfolio |

| Notes to Financial Statements |

| December 31, 2022 |

The TOPS® Target Range™ Portfolio (the “Portfolio”) is a non-diversified series of shares of beneficial interest of Northern Lights Variable Trust (the “Trust”), a statutory trust organized on November 2, 2005 under the laws of the State of Delaware and registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Portfolio is intended to be a funding vehicle for variable annuity contracts and flexible premium variable life insurance policies offered by the separate accounts of various insurance companies. The assets of the Portfolio are segregated and a shareholder’s interest is limited to the Portfolio in which shares are held. The Portfolio pays its own expenses. The Portfolio seeks to provide capital appreciation, with a secondary objective of hedging risk. The Portfolio commenced operations on September 20, 2021.

The Portfolio currently offers three classes of shares: Class 1 Shares, Class 2 Shares, and Class S Shares. Each class of shares of the Portfolio has identical rights and privileges except with respect to arrangements pertaining to shareholder servicing or distribution, class-related expenses, voting rights on matters affecting a single class of shares, and the exchange privilege of each class of shares. The Portfolio’s share classes differ in the fees and expenses charged to shareholders. The Portfolio’s income, expenses (other than class specific distribution fees) and realized and unrealized gains and losses are allocated proportionately each day based upon the relative net assets of each class.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Portfolio in the preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. The Portfolio is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946 “Financial Services – Investment Companies”, including Accounting Standards Update 2013-08.

Securities Valuation – Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the primary exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price (“NOCP”). In the absence of a sale, such securities shall be valued at the mean between the current bid and ask prices on the primary exchange on the day of valuation. The independent pricing service does not distinguish between smaller-sized bond positions known as “odd lots” and larger institutional-sized bond positions known as “round lots”. The Portfolio may fair value a particular bond if the advisor does not believe that the round lot value provided by the independent pricing service reflects fair value of the Portfolio’s holding. Short-term debt obligations having 60 days or less remaining until maturity, at time of purchase, may be valued at amortized cost. Options contracts listed on a securities exchange or board of trade (not including Index Options contracts) for which market quotations are readily available shall be valued at the last quoted sales price or, in the absence of a sale, at the mean between the current bid and ask prices on the valuation date. Index Options listed on a securities exchange or board of trade for which market quotations are readily available shall be valued at the mean between the current bid and ask prices on the valuation date.

Valuation of Fund of Funds – The Portfolio may invest in portfolios of open-end investment companies. Open-end investment companies are valued at their respective net asset values as reported by such investment companies. Open-end investment companies value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value based on the methods established by the boards of directors or trustees of the open-end investment companies.

| TOPS® Target Range™ Portfolio |

| Notes to Financial Statements (Continued) |

| December 31, 2022 |

The Portfolio may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities are valued using the “fair value” procedures approved by the Board. The Board has designated the adviser as its valuation designee (the “Valuation Designee”) to execute these procedures. The Board may also enlist third party consultants such as a valuation specialist at a public accounting firm, valuation consultant or financial officer of a security issuer on an as-needed basis to assist the Valuation Designee in determining a security-specific fair value. The Board is responsible for reviewing and approving fair value methodologies utilized by the Valuation Designee, approval of which shall be based upon whether the Valuation Designee followed the valuation procedures established by the Board.

Fair Valuation Process – The applicable investments are valued by the Valuation Designee pursuant to valuation procedures established by the Board. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source); (ii) securities for which, in the judgment of the Valuation Designee, the prices or values available do not represent the fair value of the instrument; factors which may cause the Valuation Designee to make such a judgment include, but are not limited to, the following: only a bid price or an asked price is available; the spread between bid and asked prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading; (iii) securities determined to be illiquid; and (iv) securities with respect to which an event that affects the value thereof has occurred (a “significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to a Portfolio’s calculation of its net asset value .. Specifically, interests in commodity pools or managed futures pools are valued on a daily basis by reference to the closing market prices of each futures contract or other asset held by a pool, as adjusted for pool expenses. Restricted or illiquid securities, such as private investments or non-traded securities are valued based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If a current bid from such independent dealers or other independent parties is unavailable, the Valuation Designee shall determine the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Portfolio’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii) the level of recent trades of similar or comparable securities; (ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Portfolio utilizes various methods to measure the fair value of all of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Portfolio has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument in an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Portfolio’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

| TOPS® Target Range™ Portfolio |

| Notes to Financial Statements (Continued) |

| December 31, 2022 |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following tables summarize the inputs used as of December 31, 2022 for the Portfolio’s investments measured at fair value:

| TOPS® Target Range™ Portfolio | | | | | | | | | | | | |

| Assets* | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Exchange-Traded Funds | | $ | 13,454,605 | | | $ | — | | | $ | — | | | $ | 13,454,605 | |

| Short-Term Investment | | | 5,998,855 | | | | — | | | | — | | | | 5,998,855 | |

| Call Options Purchased | | | — | | | | 198,136 | | | | — | | | | 198,136 | |

| Total | | $ | 19,453,460 | | | $ | 198,136 | | | $ | — | | | $ | 19,651,596 | |

| | | | | | | | | | | | | | | | | |

| Liabilities | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Call Options Written | | $ | — | | | $ | 843 | | | $ | — | | | $ | 843 | |

The Portfolio did not hold any Level 3 securities during the year ended December 31, 2022.

| * | Refer to the Schedule of Investments for security classifications. |

Security Transactions and Related Income – Security transactions are accounted for on the trade date. Interest income is recognized on an accrual basis. Discounts are accreted and premiums are amortized on securities purchased over the lives of the respective securities. Dividend income is recorded on the ex-dividend date. Realized gains or losses from sales of securities are determined by comparing the identified cost of the security lot sold with the net sales proceeds.

Dividends and Distributions to Shareholders – Dividends from net investment income and distributions from net realized capital gains if any, are declared and paid annually. Dividends and distributions to shareholders are recorded on the ex-date and are determined in accordance with federal income tax regulations, which may differ from GAAP. These “book/tax” differences are considered either temporary (e.g., deferred losses, capital loss carryforwards) or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences do not require reclassification. These reclassifications have no effect on net assets, results from operations or net asset value per share of the Portfolio.

Federal Income Tax – It is the Portfolio’s policy to continue to qualify as a regulated investment company by complying with the provisions of the Internal Revenue Code that are applicable to regulated investment companies and to distribute substantially all of its taxable income and net realized gains to shareholders. Therefore, no federal income tax provision is required.

The Portfolio will recognize the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Portfolio’s tax position and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax year ended December 31, 2021 or expected to be taken in the Portfolio’s December 31, 2022 year-end tax return. The Portfolio identified its major tax jurisdictions as U.S. federal, Ohio and foreign jurisdictions where the Portfolio makes significant investments. The Portfolio is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

| TOPS® Target Range™ Portfolio |

| Notes to Financial Statements (Continued) |

| December 31, 2022 |

Option Transactions – The Porfolio is subject to equity price risk in the normal course of pursuing its investment objectives and may purchase or sell options to help hedge against risk. When a portfolio writes put and call options, an amount equal to the premium received is included in the Statement of Assets and Liability as a liability. The amount of the liability is subsequently marked-to-market to reflect the current market value of the option. If an option expires on its stipulated expiration date or if a portfolio enters into a closing purchase transaction, a gain or loss is realized. If a written call option is exercised, a gain or loss is realized for the sale of the underlying security and the proceeds from the sale are increased by the premium originally received. As writer of an option, the Portfolio has no control over whether the option will be exercised and, as a result, retain the market risk of an unfavorable change in the price of the security underlying the written option.

Put options are purchased to hedge against a decline in the value of securities held in the Portfolio’s Schedule of Investments. If such a decline occurs, the put options will permit the Portfolio to sell the securities underlying such options at the exercise price, or to close out the options at a profit. The premium paid for a put or call option plus any transaction costs will reduce the benefit, if any, realized by the Portfolio upon exercise of the option, and, unless the price of the underlying security rises or declines sufficiently, the option may expire worthless to the Portfolio. In addition, in the event that the price of the security in connection with which an option was purchased moves in a direction favorable to the Portfolio, the benefits realized by the Portfolio as a result of such favorable movement will be reduced by the amount of the premium paid for the option and related transaction costs. Written and purchased options are non-income producing securities. With purchased options, there is minimal counterparty risk to the Portfolio since these options are exchange-traded and the exchange’s clearinghouse, as counterparty to all exchange-traded options, guarantees against a possible default.

Impact of Derivatives on the Statement of Assets and Liabilities and Statement of Operations

The following is a summary of the location of derivative investments on the Portfolio’s Statement of Asset and Liabilities as of December 31, 2022:

| | | | | Statement of Assets and Liabilities | | | | |

| | Contract Type/Primary Risk Exposure | | | Location | | | Fair Market Value | |

| | Call Options Purchased Equity Risk | | | Investments in securities, at value | | | $ | 198,136 | |

| | Call Options Written Equity Risk | | | Options written, at value | | | | (843 | ) |

| | Total | | | | | | $ | 197,293 | |

The following is a summary of the location of derivative investments on the Portfolio’s Statement of Operations for the year ended December 31, 2022:

| | | | | | | | | | | Realized and Unrealized Gain | |

| | | | | | | | Location of Gain (Loss) on Derivatives | | | (Loss) on Derivatives | |

| | Derivative Investment Type | | | Primary Risk Exposure | | | recognized in income | | | recognized in income | |

| | Call Options Purchased | | | Equity Risk | | | Net realized loss on investments | | | $ | (40,894 | ) |

| | Call Options Written | | | Equity Risk | | | Net realized gain on options written | | | | 5,478 | |

| | Total | | | | | | | | | $ | (35,416 | ) |

| | | | | | | | | | | | | |

| | Call Options Purchased | | | Equity Risk | | | Net change in unrealized depreciation on investments | | | $ | (1,905,383 | ) |

| | Call Options Written | | | Equity Risk | | | Net change in unrealized appreciation on options written | | | | 85,810 | |

| | Total | | | | | | | | | $ | (1,819,573 | ) |

The notional value of the derivative instruments outstanding as of December 31, 2022, as disclosed in the Schedule of Investments and the amounts realized and changes in unrealized gains and losses on derivative instruments during the year, as disclosed above and within the Statement of Operations, serve as indicators of the volume of derivative activity for the Portfolio.

| TOPS® Target Range™ Portfolio |

| Notes to Financial Statements (Continued) |

| December 31, 2022 |

Offsetting of Financial Assets and Derivative Liabilities –

| | | | | | | | | Gross Amounts Not Offset in the Statement of | | | | |

| Liabilities: | | | | | | | | Assets & Liabilities | | | | |

| | | | | | | | | | | | | | | | |

| | | | | | Net Amounts of | | | | | | | | | | |

| | | Gross Amounts Offset | | | Liabilities Presented | | | | | | | | | | |

| | | in the Statement of | | | in the Statement of | | | | | | Cash Collateral | | | | |

| Description | | Assets & Liabilities (1) | | | Assets & Liabilities | | | Financial Instruments (2) | | | Received | | | Net Amount | |

| Options Written | | $ | — | | | $ | 843 | | | $ | 843 | | | $ | — | | | $ | — | |

| (1) | Written options at value as presented in the Schedule of Investments. |

| (2) | The amount is limited to the derivative liability balance and, accordingly, does not include excess collateral pledged. |

Exchange Traded Funds – The Portfolio may invest in exchange traded funds (“ETFs”). An ETF is a type of open-end fund, however, unlike a mutual fund, its shares are bought and sold on a securities exchange at market price and only certain financial institutions called authorized participants may buy and redeem shares of the ETF at net asset value. ETF shares can trade at either a premium or discount to net asset value. Each ETF like a mutual fund is subject to specific risks depending on the type of strategy (actively managed or passively tracking an index) and the composition of its underlying holdings. Investing in an ETF involves substantially the same risks as investing directly in the ETF’s underlying holdings. ETFs pay fees and incur operating expenses, which reduce the total return earned by the ETFs from their underlying holdings. An ETF may not achieve its investment objective or execute its investment strategy effectively, which may adversely affect the Portfolio’s performance.

Expenses – Expenses of the Trust that are directly identifiable to a specific portfolio are charged to that portfolio. Expenses, which are not readily identifiable to a specific portfolio, are allocated in such a manner as deemed equitable, taking into consideration the nature and type of expense and the relative sizes of the portfolios in the Trust.

Indemnification – The Trust indemnifies its officers and Trustees for certain liabilities that may arise from the performance of their duties to the Trust. Additionally, in the normal course of business, the Portfolio enters into contracts that contain a variety of representations and warranties which provide general indemnities. The Portfolio’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Portfolio that have not yet occurred. However, based on experience, the Portfolio expects the risk of loss due to these warranties and indemnities to be remote.

| 3. | INVESTMENT TRANSACTIONS |

For the year ended December 31, 2022, cost of purchases and proceeds from sales of portfolio securities, other than short-term investments and government securities, amounted to $16,601,260 and $3,598,833, respectively.

| 4. | INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES |

ValMark Advisers, Inc. serves as the Portfolio’s investment advisor (the “Advisor”). The Advisor has engaged Milliman Financial Risk Management, LLC as the Portfolio’s sub-advisor (the “Sub-Advisor”). Pursuant to an advisory agreement with the Trust, the Advisor, on behalf of the Portfolio, under the oversight of the Board, directs the daily investment operations of the Portfolio and supervises the performance of administrative and professional services provided by others. As compensation for its services and the related expenses borne by the Advisor, the Portfolio pays the Advisor a management fee, computed on average daily net assets and accrued daily and paid monthly, at an annual rate of 0.35% of the Portfolio’s average daily net assets. Pursuant to a sub-advisory agreement, the Advisor pays the Sub-Advisor a fee, which is computed and accrued daily and paid monthly. For the year ended December 31, 2022, the Advisor earned $43,373 in advisory fees.

| TOPS® Target Range™ Portfolio |

| Notes to Financial Statements (Continued) |

| December 31, 2022 |

The Trust, with respect to the Portfolio, has adopted the Trust’s Master Distribution and Shareholder Servicing Plan (“12b-1 Plan” or “Plan”) for Class 2 shares and Class S shares. The fee is calculated at an annual rate of 0.25% and 0.45% of the average daily net assets attributable to Portfolio’s Class 2 shares and Class S shares, respectively, and is paid to Northern Lights Distributors, LLC (the “Distributor”) to provide compensation for ongoing shareholder servicing and distribution related activities and/or maintenance of the Portfolio’s shareholder accounts, not otherwise required to be provided by the Advisor. For the year ended December 31, 2022, the Portfolio paid $54,326 in distribution fees under the Plan.

In addition, certain affiliates of the Distributor provide services to the Portfolio as follows:

Ultimus Fund Solutions, LLC (“UFS”), an affiliate of the Distributor, provides administration, fund accounting, and transfer agent services to the Trust. Pursuant to the terms of an administrative servicing agreement with UFS, the Portfolio pays to UFS a monthly fee for all operating expenses of the Portfolio, which is calculated by the Portfolio on its average daily net assets. Operating expenses include but are not limited to Fund Accounting, Fund Administration, Transfer Agency, Legal Fees, Audit Fees, Compliance Services, Shareholder Reporting Expenses, Trustees Fees and Custody Fees.

For the year ended December 31, 2022, the Trustees received fees in the amount of $16,577 on behalf of the Portfolio.

The approved entities may be affiliates of UFS and the Distributor. Certain Officers of the Trust are also Officers of UFS, and are not paid any fees directly by the Portfolio for serving in such capacities.

Northern Lights Compliance Services, LLC (“NLCS”), an affiliate of UFS and the Distributor, provides a Chief Compliance Officer to the Trust, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Trust. Under the terms of such agreement, NLCS receives customary fees from UFS under the administrative servicing agreement.

Blu Giant, LLC (“Blu Giant”), an affiliate of UFS and the Distributor, provides EDGAR conversion and filing services as well as print management services for the Portfolio on an ad-hoc basis. For the provision of these services, BluGiant receives customary fees from UFS under the administrative servicing agreement.

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of the Portfolio creates presumption of the control of the Portfolio, under Section 2(a)(9) of the 1940 Act. As of December 31, 2022, Minnesota Life Insurance Company held 100% of the voting securities of the Portfolio. The Trust has no knowledge as to whether all or any portion of the shares owned of record are also owned beneficially.

| 6. | DISTRIBUTIONS TO SHAREHOLDERS AND TAX COMPONENTS OF CAPITAL |

The table below represents aggregate cost for federal tax purposes for the Portfolio as of December 31, 2022 and differs from market value by net unrealized appreciation/depreciation which consisted of:

| | | | | | | | | | Tax Net | |

| Cost of Federal | | | Unrealized | | | Unrealized | | | Unrealized | |

| Tax Purposes | | | Appreciation | | | Depreciation | | | Depreciation | |

| $ | 21,540,120 | | | $ | 89,893 | | | $ | (1,979,260 | ) | | $ | (1,889,367 | ) |

As of December 31, 2022, the components of accumulated earnings/(deficit) on a tax basis were as follows:

| Undistributed | | | Undistributed | | | Post October Loss | | | Capital Loss | | | Other | | | Unrealized | | | Total | |

| Ordinary | | | Long-Term | | | and | | | Carry | | | Book/Tax | | | Appreciation/ | | | Accumulated | |

| Income | | | Gains | | | Late Year Loss | | | Forwards | | | Differences | | | (Depreciation) | | | Earnings/(Deficits | |

| $ | 130,467 | | | $ | — | | | $ | (754 | ) | | $ | (21,528 | ) | | $ | — | | | $ | (1,889,367 | ) | | $ | (1,781,182 | ) |

| TOPS® Target Range™ Portfolio |

| Notes to Financial Statements (Continued) |

| December 31, 2022 |

The difference between book basis and tax basis accumulated net realized gains/losses, and unrealized appreciation/depreciation from investments is primarily attributable to the tax deferral of losses on wash sales.

Capital losses incurred after October 31 within the fiscal year are deemed to arise on the first business day of the following fiscal year for tax purposes. The Portfolio incurred and elected to defer such capital losses of $754.

At December 31, 2022, the Portfolio had capital loss carry forwards for federal income tax purposes available to offset future capital gains as follows:

| Short-Term | | | Long-Term | | | Total | | | CLCF Utilized | |

| $ | 21,528 | | | $ | — | | | $ | 21,528 | | | $ | — | |

| 7. | UNDERLYING INVESTMENT IN OTHER INVESTMENT COMPANIES |

The Portfolio currently seeks to achieve its investment objectives by investing its assets in underlying funds. As of December 31, 2022, the percentage of the Portfolio’s net assets invested in the STIT - Government & Agency Portfolio, Institutional Class was 30.2%. (the “Security”). The Portfolio may sell its investments in this Security at any time if the Advisor determines that it is in the best interest of the Portfolio and its shareholders to do so.

The performance of the Portfolio will be directly affected by the performance of this investment. The annual report of the Security, along with the report of the independent registered public accounting firm is included in the respective Security’s N-CSR’s available at www.sec.gov.

Subsequent events after the date of the Statement of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has determined that no events or transactions occurred requiring adjustment or disclosure in the financial statements.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of the Northern Lights Variable Trust and Shareholders of TOPS Target Range Portfolio

Opinion on the Financial Statements and Financial Highlights

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of TOPS Target Range Portfolio, one of the portfolios constituting the Northern Lights Variable Trust (the “Portfolio”) as of December 31, 2022, the related statement of operations for the year then ended, the statements of changes in net assets and the financial highlights for the year ended December 31, 2022 and the period from September 20, 2021 (commencement of operations) through December 31, 2021, and the related notes. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Portfolio as of December 31, 2022, and the results of its operations for the year then ended, the changes in its net assets and the financial highlights for the year ended December 31, 2022 and the period from September 20, 2021 (commencement of operations) through December 31, 2021 in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Portfolio’s management. Our responsibility is to express an opinion on the Portfolio’s financial statements and financial highlights based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Portfolio in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. The Portfolio is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Portfolio’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. Our procedures included confirmation of securities owned as of December 31, 2022, by correspondence with the custodian and brokers; when replies were not received from broker, we performed other auditing procedures. We believe that our audit provides a reasonable basis for our opinion.

Costa Mesa, California

February 23, 2023

We have served as the auditor of one or more TOPS Portfolios investment companies since 2019.

| TOPS® Target Range™ Portfolio |

| Expense Example (Unaudited) |

| December 31, 2022 |

As a shareholder of the TOPS® Target Range™ Portfolio, you incur ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2022 through December 31, 2022.

Actual Expenses

The “Actual” columns in the table below provides information about actual account values and actual expenses. You may use the information below together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The “Hypothetical” columns in the table below provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the period. You may use this information to compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, or other expenses charged by your insurance contract or separate account. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | Hypothetical |

| | | | | | | | | | | (5% return before |

| | | | | | | Actual | | expenses) |

| | | | | | | | | |

| | | Portfolio’s | | Beginning | | Ending | | Expenses | | Ending | | Expenses |

| | | Annualized | | Account | | Account | | Paid | | Account | | Paid |

| | | Expense | | Value | | Value | | During | | Value | | During |