iM DBi Managed Futures Strategy ETF

iM DBi Hedge Strategy ETF

Semi-Annual Report

June 30, 2020

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Fund’s website, www.imglobalpartner.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or a bank) or, if you are a direct investor, by calling 1-888-898-1041, sending an e-mail request to contact@imglobalpartner.com, or by enrolling at www.imglobalpartner.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund you can call 1-888-898-1041 or send an e-mail request to contact@imglobalpartner.com to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held with the fund complex if you invest directly with the Fund.

iM DBi ETFs

Table of Contents

| iM DBi Managed Futures Strategy ETF | | |

| Composition of Consolidated Schedule of Investments | | 3 |

| Consolidated Schedule of Investments | | 4 |

| Consolidated Schedule of Open Futures Contracts | | 5 |

| iM DBi Hedge Strategy ETF | | |

| Composition of Schedule of Investments | | 6 |

| Schedule of Investments | | 7 |

| Schedule of Open Futures Contracts | | 8 |

| Consolidated Statements of Assets and Liabilities | | 9 |

| Consolidated Statements of Operations | | 10 |

| Consolidated Statements of Changes in Net Assets | | 11 |

| Consolidated Financial Highlights | | 13 |

| Consolidated Notes to Financial Statements | | 15 |

| Expense Example | | 46 |

| Notice to Shareholders | | 48 |

| Notice of Privacy Policy and Practices | | 49 |

iM DBi Managed Futures Strategy ETF

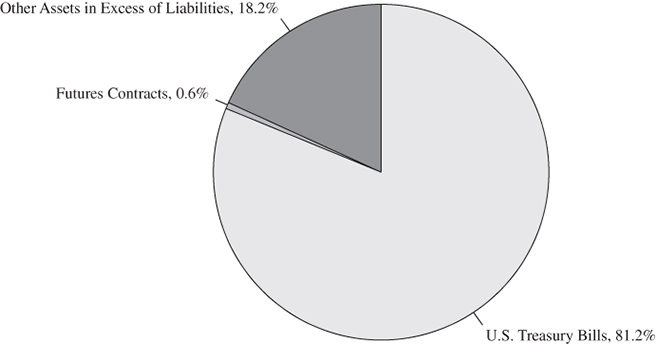

| COMPOSITION OF CONSOLIDATED SCHEDULE OF INVESTMENTS |

| at June 30, 2020 (Unaudited) |

Percentages represent market value as a percentage of net assets.

iM DBi Managed Futures Strategy ETF

| CONSOLIDATED SCHEDULE OF INVESTMENTS |

| at June 30, 2020 (Unaudited) |

| | | Principal | | | | |

| SHORT-TERM INVESTMENTS – 81.2% | | Amount | | | Value | |

| U.S. Treasury Bills – 81.2% (b)(c) | | | | | | |

| 0.090%, 07/02/2020 | | $ | 1,842,000 | | | $ | 1,841,996 | |

| 0.105%, 07/09/2020 | | | 111,000 | | | | 110,997 | |

| 0.120%, 07/23/2020 | | | 62,000 | | | | 61,996 | |

| 0.126%, 08/27/2020 | | | 605,000 | | | | 604,883 | |

| 0.126%, 09/10/2020 | | | 2,586,000 | | | | 2,585,375 | |

| 0.131%, 09/17/2020 | | | 449,000 | | | | 448,874 | |

| 0.127%, 09/24/2020 | | | 193,000 | | | | 192,945 | |

| 0.137%. 10/01/2020 | | | 372,000 | | | | 371,872 | |

| 0.143%, 10/08/2020 | | | 2,587,000 | | | | 2,586,022 | |

| 0.141%, 10/15/2020 (a) | | | 309,000 | | | | 308,870 | |

| 0.146%, 10/22/2020 | | | 855,000 | | | | 854,624 | |

| 0.150%, 11/05/2020 (a) | | | 348,000 | | | | 347,822 | |

| 0.146%, 11/12/2020 | | | 109,000 | | | | 108,942 | |

| 0.143%, 11/19/2020 (a) | | | 150,000 | | | | 149,914 | |

| 0.147%, 11/27/2020 | | | 2,920,000 | | | | 2,918,187 | |

| 0.146%, 12/03/2020 (a) | | | 750,000 | | | | 749,548 | |

| 0.146%, 12/10/2020 (a) | | | 1,163,000 | | | | 1,162,254 | |

| 0.141%, 12/17/2020 (a) | | | 208,000 | | | | 207,861 | |

| 0.153%, 12/24/2020 | | | 278,000 | | | | 277,803 | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | | | | |

| (Cost $15,892,747) | | | | | | | 15,890,785 | |

| TOTAL INVESTMENTS | | | | | | | | |

| (Cost $15,892,747) | | | | | | | 15,890,785 | |

| Other Assets in Excess of Liabilities – 18.8% | | | | | | | 3,682,768 | |

| TOTAL NET ASSETS – 100.0% | | | | | | $ | 19,573,553 | |

Percentages are stated as a percent of net assets.

| (a) | All or a portion of this security is held by the iM DBi Cayman Managed Futures Subsidiary. |

| (b) | Zero coupon bond. The effective yield to maturity is listed. |

| (c) | All or a portion of this security is held as collateral for certain futures contracts. |

The accompanying notes are an integral part of these financial statements.

iM DBi Managed Futures Strategy ETF

CONSOLIDATED SCHEDULE OF OPEN FUTURES CONTRACTS(a) |

| at June 30, 2020 (Unaudited) |

| | Number of | | | | | | | | | Unrealized | |

| | Contracts | Settlement | | Notional | | | | | | Appreciation | |

Description | Purchased/(Sold) | Month | | Amount | | | Value | | | (Depreciation) | |

| Purchased Contracts: | | | | | | | | | | | |

| U.S. Treasury 10-Year | | | | | | | | | | | |

| Note Futures | 51 | Sep-20 | | $ | 7,082,745 | | | $ | 7,097,766 | | | $ | 15,021 | |

| U.S. Treasury 10-Year | | | | | | | | | | | | | | |

| Ultra Bond Futures | 45 | Sep-20 | | | 7,062,825 | | | | 7,086,796 | | | | 23,971 | |

| MSCI Emerging Market | | | | | | | | | | | | | | |

| Index Futures | 28 | Sep-20 | | | 1,390,043 | | | | 1,379,979 | | | | (10,064 | ) |

| Japanese Yen | | | | | | | | | | | | | | |

| Currency Futures | 27 | Sep-20 | | | 3,155,855 | | | | 3,128,963 | | | | (26,892 | ) |

| MSCI EAFE | | | | | | | | | | | | | | |

| Index Futures | 11 | Sep-20 | | | 965,283 | | | | 978,119 | | | | 12,836 | |

| U.S. Treasury Long | | | | | | | | | | | | | | |

| Bond Futures | 8 | Sep-20 | | | 1,418,656 | | | | 1,428,500 | | | | 9,844 | |

| U.S. Treasury Ultra | | | | | | | | | | | | | | |

| Bond Futures | 7 | Sep-20 | | | 1,516,727 | | | | 1,527,094 | | | | 10,367 | |

| S&P 500 E-mini | | | | | | | | | | | | | | |

| Index Futures | 2 | Sep-20 | | | 310,653 | | | | 309,020 | | | | (1,633 | ) |

| Gold 100 Oz. | | | | | | | | | | | | | | |

| Futures (b) | 18 | Aug-20 | | | 3,148,703 | | | | 3,240,900 | | | | 92,197 | |

| WTI Crude | | | | | | | | | | | | | | |

| Futures (b) | 10 | Sep-20 | | | 402,564 | | | | 393,400 | | | | (9,164 | ) |

| | | | | | | | | | | | | | 116,483 | |

| Contracts Sold: | | | | | | | | | | | | | | |

| U.S. Treasury 2-Year | | | | | | | | | | | | | | |

| Note Futures | (20) | Sep-20 | | | (4,413,867 | ) | | | (4,416,562 | ) | | | (2,695 | ) |

| 90-day Euro-Dollar | | | | | | | | | | | | | | |

| Futures | (18) | Dec-21 | | | (4,489,432 | ) | | | (4,491,000 | ) | | | (1,568 | ) |

| Euro FX | | | | | | | | | | | | | | |

| Currency Futures | (17) | Sep-20 | | | (2,396,497 | ) | | | (2,391,368 | ) | | | 5,129 | |

| 30-day Fed | | | | | | | | | | | | | | |

| Fund Futures | (8) | Oct-20 | | | (3,331,572 | ) | | | (3,332,100 | ) | | | (528 | ) |

| | | | | | | | | | | | | | 338 | |

| | | | | | | | | | | | | $ | 116,821 | |

| (a) | Societe Generale is the counterparty for all Open Futures Contracts held by the Fund and the iM DBi Cayman Managed Futures Subsidiary at June 30, 2020. |

| (b) | Contract held by the iM DBi Cayman Managed Futures Subsidiary. |

The accompanying notes are an integral part of these financial statements.

iM DBi Hedge Strategy ETF

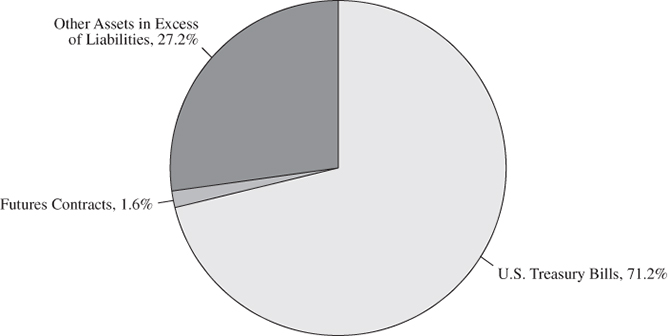

| COMPOSITION OF SCHEDULE OF INVESTMENTS |

| at June 30, 2020 (Unaudited) |

Percentages represent market value as a percentage of net assets.

iM DBi Hedge Strategy ETF

| SCHEDULE OF INVESTMENTS |

| at June 30, 2020 (Unaudited) |

| | | Principal | | | | |

| SHORT-TERM INVESTMENTS – 71.2% | | Amount | | | Value | |

| U.S. Treasury Bills – 71.2% (a)(b) | | | | | | |

| 0.105%, 07/09/2020 | | $ | 253,000 | | | $ | 33,990 | |

| 0.120%, 07/23/2020 | | | 495,000 | | | | 252,993 | |

| 0.118%, 07/30/2020 | | | 30,000 | | | | 494,967 | |

| 0.131%, 09/17/2020 | | | 1,036,000 | | | | 29,997 | |

| 0.135%, 09/22/2020 | | | 34,000 | | | | 1,035,708 | |

| 0.127%, 09/24/2020 | | | 1,171,000 | | | | 1,170,668 | |

| 0.137%, 10/01/2020 | | | 129,000 | | | | 128,956 | |

| 0.143%, 10/08/2020 | | | 655,000 | | | | 654,752 | |

| 0.141%, 10/15/2020 | | | 202,000 | | | | 201,915 | |

| 0.142%, 10/22/2020 | | | 274,000 | | | | 273,880 | |

| 0.150%, 11/05/2020 | | | 253,000 | | | | 252,871 | |

| 0.146%, 11/12/2020 | | | 363,000 | | | | 362,808 | |

| 0.143%, 11/19/2020 | | | 101,000 | | | | 100,942 | |

| 0.147%, 11/27/2020 | | | 251,000 | | | | 250,844 | |

| 0.146%, 12/03/2020 | | | 260,000 | | | | 259,843 | |

| 0.146%, 12/10/2020 | | | 94,000 | | | | 93,940 | |

| 0.141%, 12/17/2020 | | | 111,000 | | | | 110,926 | |

| 0.153%, 12/24/2020 | | | 138,000 | | | | 137,902 | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | | | | |

| (Cost $5,848,565) | | | | | | | 5,847,902 | |

| TOTAL INVESTMENTS | | | | | | | | |

| (Cost $5,848,565) | | | | | | | 5,847,902 | |

| Other Assets in Excess of Liabilities – 28.8% | | | | | | | 2,369,717 | |

| TOTAL NET ASSETS – 100.0% | | | | | | $ | 8,217,619 | |

Percentages are stated as a percent of net assets.

| (a) | Zero coupon bond. The effective yield to maturity is listed. |

| (b) | All or a portion of this security is held as collateral for certain futures contracts. |

The accompanying notes are an integral part of these financial statements.

iM DBi Hedge Strategy ETF

SCHEDULE OF OPEN FUTURES CONTRACTS(a) |

| at June 30, 2020 (Unaudited) |

| | Number of | | | | | | | | | Unrealized | |

| | Contracts | Settlement | | Notional | | | | | | Appreciation | |

Description | Purchased/(Sold) | Month | | Amount | | | Value | | | (Depreciation) | |

| Purchased Contracts: | | | | | | | | | | | |

| MSCI Emerging Market | | | | | | | | | | | |

| Index Futures | 66 | Sep-20 | | $ | 3,174,111 | | | $ | 3,252,810 | | | $ | 78,699 | |

| U.S. Dollar | | | | | | | | | | | | | | |

| Index Futures | 16 | Sep-20 | | | 1,544,363 | | | | 1,557,584 | | | | 13,221 | |

| U.S. Treasury 2-Year | | | | | | | | | | | | | | |

| Note Futures | 14 | Sep-20 | | | 3,090,762 | | | | 3,091,594 | | | | 831 | |

| 90-day Euro-Dollar | | | | | | | | | | | | | | |

| Futures | 12 | Dec-21 | | | 2,992,995 | | | | 2,994,000 | | | | 1,005 | |

| Russel 2000 E-mini | | | | | | | | | | | | | | |

| Futures | 11 | Sep-20 | | | 804,330 | | | | 790,680 | | | | (13,650 | ) |

| MSCI EAFE | | | | | | | | | | | | | | |

| Index Futures | 10 | Sep-20 | | | 867,087 | | | | 889,200 | | | | 22,113 | |

| U.S. Treasury Long | | | | | | | | | | | | | | |

| Bond Futures | 7 | Sep-20 | | | 1,239,883 | | | | 1,249,938 | | | | 10,055 | |

| Nasdaq 100 E-mini | | | | | | | | | | | | | | |

| Futures | 6 | Sep-20 | | | 1,208,864 | | | | 1,217,670 | | | | 8,806 | |

| U.S. Treasury Ultra | | | | | | | | | | | | | | |

| Bond Futures | 5 | Sep-20 | | | 1,081,017 | | | | 1,090,781 | | | | 9,764 | |

| S&P Mid Cap 400 | | | | | | | | | | | | | | |

| E-mini Futures | 4 | Sep-20 | | | 739,643 | | | | 711,640 | | | | (28,003 | ) |

| | | | | | | | | | | | | | 102,841 | |

| Contracts Sold: | | | | | | | | | | | | | | |

| Euro FX Currency | | | | | | | | | | | | | | |

| Futures | (11) | Sep-20 | | | (1,564,839 | ) | | | (1,547,356 | ) | | | 17,483 | |

| British Pound | | | | | | | | | | | | | | |

| Currency Futures | (4) | Sep-20 | | | (318,037 | ) | | | (309,925 | ) | | | 8,112 | |

| Japanese Yen | | | | | | | | | | | | | | |

| Currency Futures | (3) | Sep-20 | | | (350,393 | ) | | | (347,663 | ) | | | 2,730 | |

| Canadian Dollar | | | | | | | | | | | | | | |

| Currency Futures | (3) | Sep-20 | | | (223,068 | ) | | | (220,860 | ) | | | 2,208 | |

| | | | | | | | | | | | | | 30,533 | |

| | | | | | | | | | | | | $ | 133,374 | |

| (a) | Mizuho Securities USA LLC is the counterparty for all Open Futures Contracts held by the Fund at June 30, 2020. |

The accompanying notes are an integral part of these financial statements.

iM DBi ETFs

| STATEMENTS OF ASSETS AND LIABILITIES |

| at June 30, 2020 (Unaudited) |

| | | iM DBi Managed | | | | |

| | | Futures Strategy ETF | | | iM DBi Hedge | |

| | | (Consolidated) | | | Strategy ETF | |

| Assets: | | | | | | |

| Investments, at value (cost of $15,892,747 | | | | | | |

| and $5,848,565, respectively) | | $ | 15,890,785 | | | $ | 5,847,902 | |

| Cash | | | 1,766,226 | | | | 658,508 | |

| Deposits with broker for futures (Note 2) | | | 1,926,739 | | | | 1,713,966 | |

| Total assets | | | 19,583,750 | | | | 8,220,376 | |

| | | | | | | | | |

| Liabilities: | | | | | | | | |

| Payable for investment management fees | | | 10,197 | | | | 2,757 | |

| Total liabilities | | | 10,197 | | | | 2,757 | |

| | | | | | | | | |

| Net assets | | $ | 19,573,553 | | | $ | 8,217,619 | |

| | | | | | | | | |

| Net assets consist of: | | | | | | | | |

| Paid in capital | | $ | 19,676,753 | | | $ | 9,779,150 | |

| Total distributable earnings | | | (103,200 | ) | | | (1,561,531 | ) |

| Net assets | | $ | 19,573,553 | | | $ | 8,217,619 | |

| | | | | | | | | |

| Net Asset Value: | | | | | | | | |

| Net assets | | $ | 19,573,553 | | | $ | 8,217,619 | |

| Shares outstanding^ | | | 800,000 | | | | 325,000 | |

| Net asset value, offering | | | | | | | | |

| and redemption price per share | | $ | 24.47 | | | $ | 25.28 | |

| ^ | $0.01 par value, unlimited number of shares authorized. |

The accompanying notes are an integral part of these financial statements.

iM DBi ETFs

| STATEMENTS OF OPERATIONS |

| For the Six-Months Ended June 30, 2020 (Unaudited) |

| | | iM DBi Managed | | | | |

| | | Futures Strategy ETF | | | iM DBi Hedge | |

| | | (Consolidated) | | | Strategy ETF | |

| Investment Income: | | | | | | |

| Interest | | $ | 88,873 | | | $ | 55,173 | |

| Total investment income | | | 88,873 | | | | 55,173 | |

| | | | | | | | | |

| Expenses: | | | | | | | | |

| Management fees (Note 5) | | | 86,768 | | | | 53,278 | |

| Total expenses | | | 86,768 | | | | 53,278 | |

| Net investment income | | | 2,105 | | | | 1,895 | |

| | | | | | | | | |

| Realized and unrealized | | | | | | | | |

| gain (loss) on investments: | | | | | | | | |

| Net realized gain (loss) on: | | | | | | | | |

| Investments | | | 11,906 | | | | 10,963 | |

| Futures | | | (372,060 | ) | | | (1,692,935 | ) |

| Net change in unrealized | | | | | | | | |

| appreciation (depreciation) on: | | | | | | | | |

| Investments | | | (1,596 | ) | | | (933 | ) |

| Futures | | | (60,752 | ) | | | 133,070 | |

| Net realized and unrealized | | | | | | | | |

| loss on investments | | | (422,502 | ) | | | (1,549,835 | ) |

| Net decrease in net assets | | | | | | | | |

| resulting from operations | | $ | (420,397 | ) | | $ | (1,547,940 | ) |

The accompanying notes are an integral part of these financial statements.

iM DBi Managed Futures Strategy ETF

| CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS |

| |

| | | Six Months Ended | | | | |

| | | June 30, 2020 | | | Fiscal Period Ended | |

| | | (Unaudited) | | | December 31, 2019* | |

| Operations: | | | | | | |

| Net investment income | | $ | 2,105 | | | $ | 99,991 | |

| Net realized gain (loss) on investments | | | | | | | | |

| and futures contracts | | | (360,154 | ) | | | 1,565,311 | |

| Net change in unrealized appreciation (depreciation) | | | | | | | | |

| on investments and futures contracts | | | (62,348 | ) | | | 177,207 | |

| Net increase (decrease) in net assets | | | | | | | | |

| resulting from operations | | | (420,397 | ) | | | 1,842,509 | |

| | | | | | | | | |

| Distributions to Shareholders: | | | | | | | | |

| Distributable earnings | | | (15,194 | ) | | | (1,715,439 | ) |

| Total distributions | | | (15,194 | ) | | | (1,715,439 | ) |

| | | | | | | | | |

| Capital Share Transactions: | | | | | | | | |

| Proceeds from shares sold | | | 12,075,848 | | | | 25,609,090 | |

| Payment for shares redeemed | | | (10,435,721 | ) | | | (7,367,143 | ) |

| Net increase in net assets | | | | | | | | |

| from capital share transactions | | | 1,640,127 | | | | 18,241,947 | |

| Total increase in net assets | | | 1,204,536 | | | | 18,369,017 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of period | | | 18,369,017 | | | | — | |

| End of period | | $ | 19,573,553 | | | $ | 18,369,017 | |

| | | | | | | | | |

| Change in Shares Outstanding: | | | | | | | | |

| Shares sold | | | 475,000 | | | | 1,000,000 | |

| Shares redeemed | | | (400,000 | ) | | | (275,000 | ) |

| Net increase in shares outstanding | | | 75,000 | | | | 725,000 | |

| * | The iM DBi Managed Futures Strategy ETF commenced operations on May 7, 2019. |

The accompanying notes are an integral part of these financial statements.

iM DBi Hedge Strategy ETF

| STATEMENTS OF CHANGES IN NET ASSETS |

| |

| | | Six Months Ended | | | | |

| | | June 30, 2020 | | | Fiscal Period Ended | |

| | | (Unaudited) | | | December 31, 2019* | |

| Operations: | | | | | | |

| Net investment income | | $ | 1,895 | | | $ | 2,621 | |

| Net realized loss on investments | | | | | | | | |

| and futures contracts | | | (1,681,972 | ) | | | (1 | ) |

| Net change in unrealized appreciation | | | | | | | | |

| on investments and futures contracts | | | 132,137 | | | | 574 | |

| Net increase (decrease) in net assets | | | | | | | | |

| resulting from operations | | | (1,547,940 | ) | | | 3,194 | |

| | | | | | | | | |

| Distributions to Shareholders: | | | | | | | | |

| Distributable earnings | | | (14,173 | ) | | | (2,612 | ) |

| Total distributions | | | (14,173 | ) | | | (2,612 | ) |

| | | | | | | | | |

| Capital Share Transactions: | | | | | | | | |

| Proceeds from shares sold | | | 3,773,653 | | | | 16,249,065 | |

| Payment for shares redeemed | | | (10,243,568 | ) | | | — | |

| Net increase (decrease) in net assets | | | | | | | | |

| from capital share transactions | | | (6,469,915 | ) | | | 16,249,065 | |

| Total increase (decrease) in net assets | | | (8,032,028 | ) | | | 16,249,647 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of period | | | 16,249,647 | | | | — | |

| End of period | | $ | 8,217,619 | | | $ | 16,249,647 | |

| | | | | | | | | |

| Change in Shares Outstanding: | | | | | | | | |

| Shares sold | | | 150,000 | | | | 650,000 | |

| Shares redeemed | | | (475,000 | ) | | | — | |

| Net increase (decrease) in shares outstanding | | | (325,000 | ) | | | 650,000 | |

| * | The iM DBi Hedge Strategy ETF commenced operations on December 17, 2019. |

The accompanying notes are an integral part of these financial statements.

iM DBi Managed Futures Strategy ETF

| CONSOLIDATED FINANCIAL HIGHLIGHTS |

| |

For a capital share outstanding throughout each period

| | | Six Months Ended | | | May 7, 2019* | |

| | | June 30, 2020 | | | through | |

| | | (Unaudited) | | | December 31, 2019 | |

| Net Asset Value – Beginning of Period | | $ | 25.34 | | | $ | 25.00 | |

| | | | | | | | | |

| Income (Loss) from Investment Operations: | | | | | | | | |

Net investment income1 | | | 0.00 | | | | 0.15 | |

| Net realized and unrealized | | | | | | | | |

| gain (loss) on investments | | | (0.85 | ) | | | 2.55 | |

| Total from investment operations | | | (0.85 | ) | | | 2.70 | |

| | | | | | | | | |

| Less Distributions: | | | | | | | | |

| Distributions from net investment income | | | (0.02 | ) | | | (0.11 | ) |

| Distributions from net realized gains | | | — | | | | (2.25 | ) |

| Total distributions | | | (0.02 | ) | | | (2.36 | ) |

| | | | | | | | | |

| Net Asset Value – End of Period | | $ | 24.47 | | | $ | 25.34 | |

| | | | | | | | | |

| Total Return | | (3.37 | )%^ | | 10.76 | %^ |

| | | | | | | | | |

| Ratios and Supplemental Data: | | | | | | | | |

| Net assets, end of period (thousands) | | $ | 19,574 | | | $ | 18,369 | |

| Ratio of operating expenses to average net assets | | | 0.85 | %+ | | | 0.85 | %+ |

| Ratio of net investment income to average net assets | | | 0.02 | %+ | | | 0.84 | %+ |

| Portfolio turnover rate | | 0 | %^ | | 0 | %^ |

| * | Commencement of operations was May 7, 2019. |

| + | Annualized |

| ^ | Not Annualized |

1 | The net investment income per share was calculated using the average shares outstanding method. |

The accompanying notes are an integral part of these financial statements.

iM DBi Hedge Strategy ETF

For a capital share outstanding throughout each period

| | | Six Months Ended | | | December 17, 2019* | |

| | | June 30, 2020 | | | through | |

| | | (Unaudited) | | | December 31, 2019 | |

| Net Asset Value – Beginning of Period | | $ | 25.00 | | | $ | 25.00 | |

| | | | | | | | | |

| Income (Loss) from Investment Operations: | | | | | | | | |

Net investment income1 | | | 0.00 | | | | 0.00 | 2 |

| Net realized and unrealized gain on investments | | | 0.30 | | | | 0.00 | 2 |

| Total from investment operations | | | 0.30 | | | | 0.00 | |

| | | | | | | | | |

| Less Distributions: | | | | | | | | |

| Distributions from net investment income | | | (0.02 | ) | | | 0.00 | 2 |

| Total distributions | | | (0.02 | ) | | | 0.00 | |

| | | | | | | | | |

| Net Asset Value – End of Period | | $ | 25.28 | | | $ | 25.00 | |

| | | | | | | | | |

| Total Return | | 1.23 | %^ | | 0.01 | %^ |

| | | | | | | | | |

| Ratios and Supplemental Data: | | | | | | | | |

| Net assets, end of period (thousands) | | $ | 8,218 | | | $ | 16,250 | |

| Ratio of operating expenses to average net assets | | | 0.85 | %+ | | | 0.85 | %+ |

| Ratio of net investment income to average net assets | | | 0.03 | %+ | | | 0.48 | %+ |

| Portfolio turnover rate | | 0 | %^ | | 0 | %^ |

| * | Commencement of operations was December 17, 2019. |

| + | Annualized |

| ^ | Not Annualized |

1 | The net investment income per share was calculated using the average shares outstanding method. |

2 | Amount represents less than $0.01. |

The accompanying notes are an integral part of these financial statements.

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS |

| at June 30, 2020 (Unaudited) |

NOTE 1 – ORGANIZATION

Manager Directed Portfolios Trust (the “Trust”) is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company consisting of multiple series, and was organized as a Delaware statutory trust on April 4, 2006. These financial statements include the iM DBi Managed Futures Strategy ETF and the iM DBi Hedge Strategy ETF (each a “Fund” and collectively, the “Funds”). The Funds are both actively managed exchange-traded funds that are non-diversified series of the Trust. The iM DBi Managed Futures Strategy ETF commenced operations on May 7, 2019 and the iM DBi Hedge Strategy ETF commenced operations on December 17, 2019. iM Global Partner US LLC (“iM Global” or the “Advisor”) serves as the investment advisor to the Funds. Dynamic Beta investments, LLC (the “Sub-Advisor”) serves as the sub-advisor to the Funds. As an investment company, the Funds follow the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 Financial Services – Investment Companies. The investment objective of the Funds is to seek long-term capital appreciation.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Funds. These policies are in conformity with U.S. generally accepted accounting principles (“GAAP”).

| | A. | Security Valuation: All investments in securities are recorded at their estimated fair value, as described in Note 3. |

| | | |

| | B. | Consolidation of Subsidiary: The iM DBi Managed Futures Strategy ETF may invest up to 10% of its total assets in the iM DBi Cayman Managed Futures Subsidiary (the “Subsidiary”). The Subsidiary, which is organized under the laws of the Cayman Islands, is wholly-owned and controlled by the iM DBi Managed Futures Strategy ETF. The financial statements of the iM DBi Managed Futures Strategy ETF include the operations of the Subsidiary. All intercompany accounts and transactions have been eliminated in consolidation. The Subsidiary acts as an investment vehicle in order to invest in commodity-linked derivative instruments consistent with the Fund’s investment objectives and policies. The iM DBi Managed Futures Strategy ETF had 5.18% of its total assets invested in the Subsidiary as of June 30, 2020. |

| | | |

| | | The Subsidiary is an exempted Cayman Islands investment company and as such is not subject to Cayman Islands taxes at the present time. For U.S. income tax purposes, the Subsidiary is a Controlled Foreign Corporation (“CFC”) not subject to U.S. income taxes. As a wholly-owned CFC, however, the Subsidiary’s net income and capital gains, if any, will be included each year in the Fund’s investment company taxable income. |

| | | |

| | C. | Federal Income Taxes: It is the Funds’ policy to comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

| | | companies and to distribute substantially all of their taxable income to its shareholders. Therefore, no federal income or excise tax provisions are required. |

| | | |

| | | The Funds recognize the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Funds’ tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions expected to be taken in the Funds’ 2019 and 2020 tax returns. The Fund’s identify its major tax jurisdictions as U.S. Federal and the state of Delaware. |

| | | |

| | | The Subsidiary is classified as a CFC under Subchapter N of the Internal Revenue Code. Therefore, the iM DBi Managed Futures Strategy ETF is required to increase its taxable income by its share of the Subsidiary’s income. Net investment loss of the Subsidiary cannot be deducted by the iM DBi Managed Futures Strategy ETF in the current period nor carried forward to offset taxable income in future periods. |

| | | |

| | D. | Securities Transactions, Income and Distributions: Securities transactions are accounted for on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost. Interest income is recorded on an accrual basis. Dividend income and distributions to shareholders are recorded on the ex-dividend date. Discounts and premiums on fixed income securities are amortized/accreted using the effective interest method. |

| | | |

| | | The Funds distribute substantially all of their net investment income, if any, quarterly, and net realized capital gains, if any, annually. Distributions from net realized gains for book purposes may include short-term capital gains. All short-term capital gains are included in ordinary income for tax purposes. The amount of dividends and distributions to shareholders from net investment income and net realized capital gains is determined in accordance with federal income tax regulations, which may differ from GAAP. To the extent these book/tax differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax treatment. |

| | | |

| | E. | Use of Estimates: The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets during the reporting period. Actual results could differ from those estimates. |

| | | |

| | F. | Reclassification of Capital Accounts: GAAP requires that certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. |

| | | |

| | G. | Events Subsequent to the Fiscal Period End: In preparing the financial statements as of June 30, 2020, management considered the impact of subsequent events for potential recognition or disclosure in the financial statements. |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

| | H. | Foreign Securities and Currency: Investment securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts at the date of valuation. Purchases and sales of investment securities and income and expense items denominated in foreign currencies are translated into U.S. dollar amounts on the respective dates of such transactions. |

| | | |

| | | The Funds do not isolate the portion of reported net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the Funds’ books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the fair values of assets and liabilities, other than investments in securities at period end, resulting from changes in exchange rates. |

| | | |

| | I. | CFTC Regulation: Because of the nature of its investments, the Funds are subject to regulation under the Commodities Exchange Act, as amended (the “CEA”), as a commodity pool and each of the Advisor and Sub-Adviser is subject to regulation under the CEA as a commodity pool operator (“CPO”), as those terms are defined under the CEA. The Advisor and Sub-Adviser are regulated by the CFTC, the National Futures Association and the U.S. Securities and Exchange Commission (“SEC”) and are subject to each regulator’s disclosure requirements. The CFTC has adopted rules that are intended to harmonize certain CEA disclosure requirements with SEC disclosure requirements. |

| | | |

| | J. | Futures Contracts: Investments in futures contracts obligate a Fund and the clearing broker to settle monies on a daily basis representing changes in the prior days “mark-to-market” of the open contracts. If a Fund has unrealized appreciation the clearing broker would credit the Fund’s account with an amount equal to appreciation and conversely if a Fund has unrealized depreciation the clearing broker would debit the Fund’s account with an amount equal to depreciation. These daily cash settlements are also known as “variation margin.” Variation margin is recognized as a receivable and/or payable for “Variation margin on futures contracts” on the Statements of Assets and Liabilities. |

| | | |

| | | During the period the futures contract is open, changes in the value of a contract are recognized as an unrealized gain or loss by “marking-to-market” on a daily basis to reflect the changes in market value of the contract, which is recognized as a component of “Change in net unrealized appreciation/depreciation on futures” on the Statements of Operations. When the contract is closed or expired, a Fund records a realized gain or loss equal to the difference between the value of the contract on the closing date and value of the contract when originally entered into, which is recognized as a component of “Net realized gain (loss) on futures” on the Statements of Operations. |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

| | K. | Deposits with Broker: When trading derivative instruments, such as forward or futures contracts, the Funds and the Subsidiary are only required to post initial or variation margin with the exchange or clearing broker. The use of margin in trading these instruments has the effect of creating leverage, which can expose the Funds to substantial gains or losses occurring from relatively small price changes in the value of the underlying instrument and can increase the volatility of the Funds’ returns. Volatility is a statistical measure of the dispersion of returns of an investment, where higher volatility generally indicates greater risk. |

| | | |

| | | Upon entering into a futures contract, and to maintain the Funds’ open positions in futures contracts, the Funds would be required to deposit with their custodian or futures broker in a segregated account in the name of the futures broker an amount of cash, U.S. government securities, suitable money market instruments, or other liquid securities, known as “initial margin.” The margin required for a particular futures contract is set by the exchange on which the contract is traded, and may be significantly modified from time to time by the exchange during the term of the contract. Futures contracts are customarily purchased and sold on margins that may range upward from less than 5% of the value of the contract being traded. |

| | | |

| | | At June 30, 2020, the iM DBi Managed Futures Strategy ETF and Subsidiary, collectively, had $1,926,739 in cash and cash equivalents on deposit with brokers for futures, which are presented on the Fund’s consolidated statement of assets and liabilities. At June 30, 2020, the iM DBi Hedge Strategy ETF had $1,713,966 in cash and cash equivalents on deposit with brokers for futures, which are presented on the Fund’s statement of assets and liabilities. |

| | | |

| | | If the price of an open futures contract changes (by increase in underlying instrument or index in the case of a sale or by decrease in the case of a purchase) so that the loss on the futures contract reaches a point at which the margin on deposit does not satisfy margin requirements, a broker will require an increase in the margin. However, if the value of a position increases because of favorable price changes in the futures contract so that the margin deposit exceeds the required margin, a broker will pay the excess to the Funds. |

| | | |

| | | These subsequent payments, called “variation margin,” to and from the futures broker, are made on a daily basis as the price of the underlying assets fluctuate making the long and short positions in the futures contract more or less valuable, a process known as “marking to the market.” The Fund expects to earn interest income on any margin deposits. |

| | | |

| | L. | Counterparty, Credit and Market Risk: Many of the protections afforded to participants on some organized exchanges, such as the performance guarantee of an exchange clearing house, might not be available in connection with over-the-counter transactions or off-exchange transactions. Therefore, in those instances in which the Funds enter into such transactions, the Funds will be subject to the risk |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

| | that its counterparty will be unable or unwilling to perform its obligations under the transactions and that the Funds will sustain losses. Over-the-counter (“OTC”) and off-exchange transactions have greater liquidity risk, and often do not have liquidity beyond the counterparty to the instrument. In general, there is less government regulation and supervision of transactions in the OTC markets or off-exchange than of transactions entered into on organized exchanges. Furthermore, if any futures commission merchant, broker-dealer, or financial institution holding the Funds’ assets were to become bankrupt or insolvent, it is possible that the Funds would be able to recover only a portion, or in certain circumstances, none of their assets held by such bankrupt or insolvent entity. |

| | |

| | The risk that an issuer, guarantor or liquidity provider of an instrument (including the counterparty to an OTC position) held by the Funds will be unable or unwilling to perform its obligations is considered credit risk. It includes the risk that one or more of the securities will be downgraded by a credit rating agency; generally, lower rated issuers have higher credit risks. Credit risk also includes the risk that an issuer or guarantor of a security, or a bank or other financial institution that has entered into a repurchase agreement with the Funds, may default on its payment or repurchase obligation, as the case may be. Credit risk generally is inversely related to credit quality. To the extent that the Funds invest in derivative or other over-the-counter transactions, including forward contracts, the Funds may be exposed to a credit risk with respect to the parties with whom it trades and may also bear the risk of settlement default. These risks may differ materially from those entailed in exchange- traded transactions, which generally are backed by clearing organization guarantees, daily marking-to-market and settlement, and segregation and minimum capital requirements applicable to intermediaries. Transactions entered into directly between two counterparties generally do not benefit from such protections and expose the parties to the risk of counterparty default. |

| | |

| | The market value of a security or instrument may fluctuate, sometimes rapidly and unpredictably. These fluctuations, which are often referred to as “volatility,” may cause a security or instrument to be worth less than it was worth at an earlier time. Recent turbulence in financial markets and reduced liquidity in credit and fixed income markets may negatively affect many issuers, which may have an adverse effect on the Funds. Market risk may affect a single issuer, industry, commodity, sector of the economy, or the market as a whole. Market risk is common to most investments – including stocks, bonds, derivatives and commodities, and the mutual funds that invest in them. The risk of bonds can vary significantly depending upon factors such as issuer and maturity. The bonds of some companies may be riskier than the stocks of others. |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

NOTE 3 – SECURITIES VALUATION

The Funds have adopted authoritative fair value accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value, a discussion of changes in valuation techniques and related inputs during the period, and expanded disclosure of valuation levels for major security types. These inputs are summarized in the three broad levels listed below:

| | Level 1 – | Unadjusted, quoted prices in active markets for identical assets or liabilities that the Funds have the ability to access at the date of measurement. |

| | | |

| | Level 2 – | Other significant observable inputs (including, but not limited to, quoted prices in active markets for similar instruments, quoted prices in markets that are not active for identical or similar instruments, and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets, such as interest rates, prepayment speeds, credit risk curves, default rates, and similar data). |

| | | |

| | Level 3 – | Significant unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

Following is a description of the valuation techniques applied to the Funds’ major categories of assets and liabilities measured at fair value on a recurring basis.

Debt Securities: Debt securities, including corporate bonds, asset-backed securities, mortgage-backed securities, municipal bonds, U.S. Treasuries, and U.S. government agency issues, are generally valued at market on the basis of valuations furnished by an independent pricing service that utilizes both dealer-supplied valuations and formula-based techniques. The pricing service may consider recently executed transactions in securities of the issuer or comparable issuers, market price quotations (where observable), bond spreads, and fundamental data relating to the issuer. In addition, the model may incorporate market observable data, such as reported sales of similar securities, broker quotes, yields, bids, offers, and reference data. Certain securities are valued primarily using dealer quotations. To the extent these securities are actively traded and valuation adjustments are not applied, they are categorized in level 2 of the fair value hierarchy.

Futures: Futures contracts are valued at the settlement price on the exchange on which they are principally traded. Futures are generally categorized as Level 1 of the fair value hierarchy.

Registered Investment Companies: Investments in registered investment companies (e.g., mutual funds) are generally priced at the ending NAV provided by the applicable registered investment company’s service agent and will be classified in Level 1 of the fair value hierarchy.

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

Short-Term Debt Securities: Short-term debt instruments having a maturity of less than 60 days are valued at the evaluated mean price supplied by an approved pricing service. Pricing services may use various valuation methodologies including matrix pricing and other analytical pricing models as well as market transactions and dealer quotations. In the absence of prices from a pricing service, the securities will be priced in accordance with the procedures adopted by the Board. Short-term debt securities are generally classified in Level 1 or Level 2 of the fair market hierarchy depending on the inputs used and market activity levels for specific securities.

The Board has delegated day-to-day valuation issues to a Valuation Committee of the Trust which, as of June 30, 2020, was comprised of officers of the Trust. The function of the Valuation Committee is to value securities where current and reliable market quotations are not readily available, or the closing price does not represent fair value, by following procedures approved by the Board. These procedures consider many factors, including the type of security, size of holding, trading volume and news events. All actions taken by the Valuation Committee are subsequently reviewed and ratified by the Board.

Depending on the relative significance of the valuation inputs, fair valued securities may be classified in either level 2 or level 3 of the fair value hierarchy.

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

The following is a summary of the fair valuation hierarchy of the Funds’ consolidated investments and other financial instruments as of June 30, 2020:

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Managed Futures Strategy ETF | | | | | | | | | | | | |

| ASSETS: | | | | | | | | | | | | |

| Short-Term Investments | | $ | — | | | $ | 15,890,785 | | | $ | — | | | $ | 15,890,785 | |

| Total Investments in Securities | | | — | | | | 15,890,785 | | | | — | | | | 15,890,785 | |

| Other Financial Instruments* | | | | | | | | | | | | | | | | |

| Futures | | $ | 169,365 | | | $ | — | | | $ | — | | | $ | 169,365 | |

LIABILITIES: | | | | | | | | | | | | | | | | |

| Other Financial Instruments* | | | | | | | | | | | | | | | | |

| Futures | | $ | (52,544 | ) | | $ | — | | | $ | — | | | $ | (52,544 | ) |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Hedge Strategy ETF | | | | | | | | | | | | |

| ASSETS: | | | | | | | | | | | | |

| Short-Term Investments | | $ | — | | | $ | 5,847,902 | | | $ | — | | | $ | 5,847,902 | |

| Total Investments in Securities | | | — | | | | 5,847,902 | | | | — | | | | 5,847,902 | |

| Other Financial Instruments* | | | | | | | | | | | | | | | | |

| Futures | | $ | 175,027 | | | $ | — | | | $ | — | | | $ | 175,027 | |

| LIABILITIES: | | | | | | | | | | | | | | | | |

| Other Financial Instruments* | | | | | | | | | | | | | | | | |

| Futures | | $ | (41,653 | ) | | $ | — | | | $ | — | | | $ | (41,653 | ) |

| * | Other financial instruments are derivative instruments not reflected in the Schedule of Investments, such as futures. Futures are reflected as the unrealized appreciation (depreciation) on the instrument. |

NOTE 4 – DERIVATIVE INSTRUMENTS

During the six months ended June 30, 2020, the Funds invested in Derivative Instruments such as futures contracts and forward currency contracts in order to pursue their futures strategies. The Derivative Instruments for the Managed Futures Strategy ETF are not designated as hedging instruments. The Managed Futures Strategy ETF employs long and short positions in derivatives, primarily futures contracts and forward contracts, across the broad asset classes of equities, fixed income, currencies and, through the Subsidiary, commodities. Fund positions in those contracts are determined based on a proprietary, quantitative model – the Dynamic Beta Engine – that seeks to identify the main drivers of performance by approximating the current asset allocation of a selected pool of the largest commodity trading advisor hedge funds (“CTA”), which are hedge funds that use futures or forward contracts to achieve their investment objectives. The Dynamic Beta Engine analyzes recent historical performance in order to estimate the current asset allocation of a selected pool of the largest CTAs. The Sub-Adviser relies exclusively on the model and does not have discretion to override the model-determined asset allocation or portfolio weights. The Sub-Adviser will periodically review whether instruments should be added to or removed from the model in order to improve the model’s efficiency. The model’s asset allocation is limited to asset classes that are traded on U.S.-based exchanges. Based on this analysis, the Managed Futures Strategy ETF will invest in an optimized portfolio of long and short positions in domestically-traded, liquid derivative contracts selected from a pool of the most liquid derivative contracts, as determined by the Sub-Adviser.

Futures contracts and forward contracts are contractual agreements to buy or sell a particular currency, commodity or financial instrument at a pre-determined price in the future. The Managed Futures Strategy ETF takes long positions in derivative contracts that provide exposure to various asset classes, sectors and/or markets that the Fund expects to rise in value, and takes short positions in asset classes, sectors or and/or markets that the Fund expects to fall in value. Currently, the Managed Futures Strategy

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

ETF expects to limit its investments to highly-liquid, domestically-traded contracts that the Sub-Adviser believes exhibit the highest correlation to what the Sub-Adviser perceives to be the core positions of the target hedge funds. Such core positions are generally long and short positions in domestically-traded derivative contracts viewed as highly liquid by the Sub-Adviser.

The Hedge Strategy ETF employs long and short positions in futures contracts to gain exposure to global equity markets, while using fixed income securities and /U.S. currency derivatives to mitigate risk. The long and short positions in the futures contracts are determined by the Fund’s sub-adviser, using a proprietary, quantitative model – the Dynamic Beta Engine. The Dynamic Beta Engine is designed to identify the main drivers of performance of a diversified portfolio of the largest Equity Hedge funds, which are hedge funds that typically employ fundamental analysis to buy or sell short individual equity securities to achieve their respective investment objectives. The sub-adviser has conducted extensive research into the drivers of performance of such hedge funds and concluded that individual security selection by the target hedge funds can deliver alpha over time through shifts in asset allocation among major equity markets. In other words, if fundamentally-driven hedge fund managers collectively determine that stocks in emerging markets are more attractive than those in developed markets, the Dynamic Beta Engine can identify this and shift asset allocation exposures accordingly.

Based on this model, the Fund will invest in an optimized portfolio of long and short positions in domestically-traded, liquid futures contracts, as determined by the Sub-Adviser. This process is repeated monthly, with all positions rebalanced at that time. The Dynamic Beta Engine analyzes recent historical performance in order to estimate the current asset allocation of a selected pool of Equity Hedge funds. The Sub-Adviser relies exclusively on the model and does not have discretion to override the model-determined asset allocation or portfolio weights. Investing in a limited number of highly liquid futures contracts and monthly rebalancing is expected to keep transaction costs low relative to Equity Hedge funds that invest in dozens or hundreds of underlying investments and must pay to loan stocks when they sell short a security.

Equity Hedge fund managers take long positions in stocks that are expected to increase in value and short positions in stocks that are expected to decrease in value. The returns of the strategy are expected to be correlated to equity markets over a full market cycle, because these managers tend to keep a long equity bias, but with lower drawdowns than major equity indices. The Hedge Strategy ETF will invest in a limited number of highly-liquid, domestically-traded futures contracts that the Sub-Adviser believes exhibit the highest correlation to what the Sub-Adviser perceives to be the core positions of the target Equity Hedge funds. Unlike Equity Hedge fund managers, the Fund will not invest in individual equity securities. Such core positions are generally long and short positions in domestically-traded derivative contracts viewed as highly liquid by the Sub-Adviser.

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

The Funds may have gross notional exposure, which is defined as the sum of the notional exposure of both long and short derivative positions across the Funds, that approximates the current asset allocation and matches the risk profile of a diversified pool of the largest CTAs and Equity Hedge funds. The Investment Company Act of 1940, as amended (the “1940 Act”), and the rules and interpretations thereunder, impose certain limitations on the Funds’ ability to use leverage. Under normal market conditions, the Sub-Adviser, on average, will target an annualized volatility level for the Fund of 8-10%.

The Sub-Adviser will, in an effort to reduce certain risks (e.g., volatility of returns), limit the Fund’s gross notional exposure on certain futures contracts whose returns are expected to be particularly volatile. In addition to these specific exposure limits, the Sub-Adviser will use quantitative methods to assess the level of risk for the Fund.

There are significant risks associated with the Funds’ use of futures contracts, including the following: (1) the success of a hedging strategy may depend on the Sub-Adviser’s ability to predict movements in the prices of individual securities, fluctuations in markets and movements in interest rates; (2) there may be an imperfect or no correlation between the changes in market value of the instruments held by the Fund and the prices of futures; (3) there may not be a liquid secondary market for a futures contract; (4) trading restrictions or limitations may be imposed by an exchange; and (5) government regulations may restrict trading in futures contracts. In addition, some strategies reduce the Fund’s exposure to price fluctuations, while others tend to increase its market exposure.

The Funds have adopted derivative instruments disclosure standards, in order to enable the investor to understand how and why an entity used derivatives, how derivatives are accounted for, and how derivative instruments affect an entity’s results of operations and financial position.

Statement of Assets and Liabilities – Values of Derivative Instruments as of June 30, 2020

Managed Futures Strategy ETF

| |

| Asset Derivatives | |

| | | Statement of Assets and | | | |

| | | Liabilities Location | | Value | |

| Commodity Contracts – Futures* | | Unrealized appreciation | | | |

| | | on futures contracts** | | $ | 92,197 | |

| Equity Contracts – Futures* | | Unrealized appreciation | | | | |

| | | on futures contracts** | | | 12,836 | |

| Foreign Exchange Contracts – Futures* | | Unrealized appreciation | | | | |

| | | on futures contracts** | | | 5,129 | |

| Interest Rate Contracts – Futures* | | Unrealized appreciation | | | | |

| | | on futures contracts** | | | 59,203 | |

| Total | | | | $ | 169,365 | |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

| |

| Liability Derivatives | |

| | | Statement of Assets and | | | |

| | | Liabilities Location | | Value | |

| Commodity Contracts – Futures* | | Unrealized depreciation | | | |

| | | on futures contracts** | | $ | 9,164 | |

| Equity Contracts – Futures* | | Unrealized depreciation | | | | |

| | | on futures contracts** | | | 11,697 | |

| Foreign Exchange Contracts – Futures* | | Unrealized depreciation | | | | |

| | | on futures contracts** | | | 28,460 | |

| Interest Rate Contracts – Futures* | | Unrealized depreciation | | | | |

| | | on futures contracts** | | | 3,223 | |

| Total | | | | $ | 52,544 | |

| * | | Includes cumulative appreciation/depreciation as reported on the Consolidated Schedule of Open Futures Contracts. |

| ** | | Included in total distributable earnings on the Consolidated Statement of Assets and Liabilities. |

Hedge Strategy ETF

| |

| Asset Derivatives | |

| | | Statement of Assets and | | | |

| | | Liabilities Location | | Value | |

| Equity Contracts – Futures* | | Unrealized appreciation | | | |

| | | on futures contracts** | | $ | 120,631 | |

| Foreign Exchange Contracts – Futures* | | Unrealized appreciation | | | | |

| | | on futures contracts** | | | 30,533 | |

| Interest Rate Contracts – Futures* | | Unrealized appreciation | | | | |

| | | on futures contracts** | | | 23,863 | |

| Total | | | | $ | 175,027 | |

| | | | | | | |

| | | Liability Derivatives | |

| | | Statement of Assets and | | | | |

| | | Liabilities Location | | Value | |

| Equity Contracts – Futures* | | Unrealized depreciation | | | | |

| | | on futures contracts** | | $ | 13,650 | |

| Foreign Exchange Contracts – Futures* | | Unrealized depreciation | | | | |

| | | on futures contracts** | | | — | |

| Interest Rate Contracts – Futures* | | Unrealized depreciation | | | | |

| | | on futures contracts** | | | 28,003 | |

| Total | | | | $ | 41,653 | |

| * | | Includes cumulative appreciation/depreciation as reported on the Schedule of Open Futures Contracts. |

| ** | | Included in total distributable earnings on the Statement of Assets and Liabilities. |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

The Effect of Derivative Instruments on the Statements of Operations for the six months ended June 30, 2020

Managed Futures Strategy ETF

Amount of Realized Gain (Loss) on Derivatives

| | | Futures Contracts | |

| Commodity Contracts | | $ | 73,530 | |

| Equity Contracts | | | (3,008,935 | ) |

| Foreign Exchange Contracts | | | (458,212 | ) |

| Interest Rate Contracts | | | 3,021,557 | |

| Total | | $ | (372,060 | ) |

Change in Unrealized Appreciation (Depreciation) on Derivatives

| | | Futures Contracts | |

| Commodity Contracts | | $ | 59,175 | |

| Equity Contracts | | | (323,453 | ) |

| Foreign Exchange Contracts | | | 7,740 | |

| Interest Rate Contracts | | | 195,786 | |

| Total | | $ | (60,752 | ) |

Hedge Strategy ETF

Amount of Realized Gain (Loss) on Derivatives

| | | Futures Contracts | |

| Equity Contracts | | $ | (2,840,886 | ) |

| Foreign Exchange Contracts | | | 108,169 | |

| Interest Rate Contracts | | | 1,039,782 | |

| Total | | $ | (1,692,935 | ) |

Change in Unrealized Appreciation (Depreciation) on Derivatives

| | | Futures Contracts | |

| Equity Contracts | | $ | 22,328 | |

| Foreign Exchange Contracts | | | 84,713 | |

| Interest Rate Contracts | | | 26,029 | |

| Total | | $ | 133,070 | |

Volume Disclosures

The average monthly notional amount outstanding of futures during the six months ended June 30, 2020 were as follows:

| | | iM DBi Managed | | | iM DBi Hedge | |

| Long Positions | | Futures Strategy ETF | | | Strategy ETF | |

| Futures | | $ | 3,966,180 | | | $ | 2,257,932 | |

| Short Positions | | | | | | | | |

| Futures | | $ | (4,050,346 | ) | | $ | (512,160 | ) |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

Offsetting Assets and Liabilities

Managed Futures Strategy ETF

The Funds are subject to various Master Netting Arrangements, which govern the terms of certain transactions with select counterparties. The Master Netting Arrangements allow the Funds to close out and net their total exposure to a counterparty in the event of a default with respect to all the transactions governed under a single agreement with a counterparty. The Master Netting Arrangements also specify collateral posting arrangements at pre-arranged exposure levels. Under the Master Netting Arrangements, collateral is routinely transferred if the total net exposure to certain transactions (net of existing collateral already in place) governed under the relevant Master Netting Arrangement with a counterparty in a given account exceeds a specified threshold depending on the counterparty and the type of Master Netting Arrangement.

The table below, as of June 30, 2020, discloses both gross information and net information about instruments and transactions eligible for offset in the Consolidated Statements of Assets and Liabilities, and instruments and transactions that are subject to an agreement similar to a master netting agreement as well as amounts related to collateral held at clearing brokers and counterparties. For financial reporting purposes, the Funds do not offset derivative assets and liabilities, and any related collateral received or pledged, on the Consolidated Statements of Assets and Liabilities, except in the case of futures contracts for the Managed Futures Strategy ETF.

Assets

| | | | | Gross Amounts not offset | |

| | | | | in the Consolidated Statement | |

| | | | | of Assets and Liabilities | |

| | | | Net | | | |

| | | Gross | Amounts | | | |

| | | Amounts | Presented | | | |

| | | Offset in the | in the | | | |

| | Gross | Consolidated | Consolidated | | | |

| | Amounts of | Statement of | Statement of | | | |

| Description / | Recognized | Assets and | Assets and | Financial | Collateral | Net |

Counterparty | Assets | Liabilities | Liabilities | Instruments | Received | Amount |

| Futures contracts* | | | | | | |

| Societe Generale | $169,365 | $(52,544) | $116,821 | $ — | $ — | $116,821 |

| | $169,365 | $(52,544) | $116,821 | $ — | $ — | $116,821 |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

Liabilities

| | | | | Gross Amounts not offset | |

| | | | | in the Consolidated Statement | |

| | | | | of Assets and Liabilities | |

| | | | Net | | | |

| | | Gross | Amounts | | | |

| | | Amounts | Presented | | | |

| | | Offset in the | in the | | | |

| | Gross | Consolidated | Consolidated | | | |

| | Amounts of | Statement of | Statement of | | | |

| Description / | Recognized | Assets and | Assets and | Financial | Collateral | Net |

Counterparty | Liabilities | Liabilities | Liabilities | Instruments | Pledged | Amount |

| Futures contracts* | | | | | | |

| Societe Generale | $52,544 | $(52,544) | $ — | $ — | $ — | $ — |

| | $52,544 | $(52,544) | $ — | $ — | $ — | $ — |

| * | Cumulative appreciation/ depreciation on futures contracts is reported in the consolidated schedule of open futures contracts. Variation margin and receivable/payable for unsettled open futures contracts presented above, if any, is presented in the Consolidated Statements of Assets and Liabilities. |

In some instances, the collateral amounts disclosed in the tables were adjusted due to the requirement to limit the collateral amounts to avoid the effect of overcollateralization. Actual collateral received/pledged may be more than the amounts disclosed herein.

Hedge Strategy ETF

Assets

| | | | | Gross Amounts not offset | |

| | | | | in the Consolidated Statement | |

| | | | | of Assets and Liabilities | |

| | | | Net | | | |

| | | Gross | Amounts | | | |

| | | Amounts | Presented | | | |

| | | Offset in the | in the | | | |

| | Gross | Consolidated | Consolidated | | | |

| | Amounts of | Statement of | Statement of | | | |

| Description / | Recognized | Assets and | Assets and | Financial | Collateral | Net |

Counterparty | Assets | Liabilities | Liabilities | Instruments | Received | Amount |

| Futures contracts* | | | | | | |

| Mizuho | $175,027 | $(41,653) | $133,374 | $ — | $ — | $133,374 |

| | $175,027 | $(41,653) | $133,374 | $ — | $ — | $133,374 |

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

Liabilities

| | | | | Gross Amounts not offset | |

| | | | | in the Consolidated Statement | |

| | | | | of Assets and Liabilities | |

| | | | Net | | | |

| | | Gross | Amounts | | | |

| | | Amounts | Presented | | | |

| | | Offset in the | in the | | | |

| | Gross | Consolidated | Consolidated | | | |

| | Amounts of | Statement of | Statement of | | | |

| Description / | Recognized | Assets and | Assets and | Financial | Collateral | Net |

Counterparty | Liabilities | Liabilities | Liabilities | Instruments | Pledged | Amount |

| Futures contracts* | | | | | | |

| Mizuho | $41,653 | $(41,653) | $ — | $ — | $ — | $ — |

| | $41,653 | $(41,653) | $ — | $ — | $ — | $ — |

| * | Cumulative appreciation/ depreciation on futures contracts is reported in the consolidated schedule of open futures contracts. Variation margin and receivable/payable for unsettled open futures contracts presented above, if any, is presented in the Statements of Assets and Liabilities. |

In some instances, the collateral amounts disclosed in the tables were adjusted due to the requirement to limit the collateral amounts to avoid the effect of overcollateralization. Actual collateral received/pledged may be more than the amounts disclosed herein.

NOTE 5 – INVESTMENT ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

The Trust has entered into an Investment Advisory Agreement (the “Advisory Agreement”) with the Advisor. Under the Advisory Agreement, the Advisor provides a continuous investment program for the Funds’ assets in accordance with their investment objectives, policies and limitations, and oversees the day-to-day operations of the Funds subject to the supervision of the Board, including the Trustees who are not “interested persons” of the Trust as defined in the 1940 Act (the “Independent Trustees”).

Pursuant to the Advisory Agreements between the Trust, on behalf of the Funds, and iM Global, the Funds pay a unified management fee to the Advisor, which is calculated daily and paid monthly, at an annual rate of 0.85% of the Funds average daily net assets. Under the Investment Advisory Agreement, the Advisor has agreed to pay all expenses of the Funds except for interest charges on any borrowings, dividends and other expenses on securities sold short, taxes, brokerage commissions and other expenses incurred in placing orders for the purchase and sale of securities and other investment instruments, acquired fund fees and expenses, accrued deferred tax liability, extraordinary expenses, distribution fees and expenses paid by the Funds under any distribution plan adopted pursuant to Rule 12b-1 under the 1940 Act, and the unified management fee payable to the Advisor. iM Global, in turn, compensates the Funds’ sub-adviser from the management fee it receives.

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

Dynamic Beta investments, LLC, serves as the sub-adviser to the Funds. Pursuant to a Sub-Advisory Agreement between the Advisor and the Sub-Adviser (the “Sub-Advisory Agreement”), the Sub-Adviser manages the investment program for the Funds, including the purchase, retention and disposition of investments in the Funds’ portfolio, in accordance with the Funds’ investment objectives, policies and restrictions. The Advisor has ultimate responsibility to oversee the Sub-Adviser and recommend to the Board of Trustees its hiring, termination, and replacement. In this capacity, the Advisor, among other things: (i) monitors the compliance of the Sub-Adviser with the investment objectives and related policies of the Funds; (ii) reviews the performance of the Sub-Adviser; and (iii) reports periodically on such performance to the Board of Trustees. The Sub-Adviser is paid a sub-advisory fee by the Advisor for its services as sub-adviser to the Funds. The Advisor is a minority owner of the Sub-Adviser.

U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services, LLC (“Fund Services” or the “Administrator”) acts as the Funds’ Administrator under an Administration Agreement. The Administrator prepares various federal and state regulatory filings, reports and returns for the Funds; prepares reports and materials to be supplied to the Trustees; monitors the activities of the Funds’ custodian, transfer agent and accountants; coordinates the preparation and payment of the Funds’ expenses and reviews the Funds’ expense accruals. Fund Services also serves as the fund accountant and transfer agent to the Funds. Vigilant Compliance, LLC serves as the Chief Compliance Officer to the Funds. U.S. Bank N.A., an affiliate of Fund Services, serves as the Funds’ custodian.

For the six months ended June 30, 2020, the Managed Futures Strategy ETF and the Hedge Strategy ETF paid $2,311 and $3,456, respectively, in brokerage commissions from portfolio transactions to U.S. Bank N.A., an affiliate of the Distributor.

Quasar Distributors, LLC (the “Distributor”) acts as the Funds’ principal underwriter in a continuous public offering of the Funds shares. The Distributor is an affiliate of the Administrator. A Trustee of the Trust is deemed to be an interested person of the Trust due to his former position with the Distributor.

Certain officers of the Funds are employees of the Administrator and are not paid any fees by the Funds for serving in such capacities.

NOTE 6 – SECURITIES TRANSACTIONS

For the six months ended June 30, 2020, the cost of purchases and the proceeds from sales of securities, excluding short-term securities, were as follows:

| | | Purchases | | | Sales | |

| Managed Futures Strategy ETF | | $ | — | | | $ | — | |

| Hedge Strategy ETF | | $ | — | | | $ | — | |

There were no purchases or sales of long-term U.S. Government securities.

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

NOTE 7 – SHARE TRANSACTIONS

Shares of the Funds are listed and traded on NYSE Arca, Inc. Market prices for the shares may be different from their NAV. The Funds issue and redeem shares on a continuous basis at NAV generally in blocks of 25,000 shares, called “Creation Units.” The Funds generally issue and redeem Creation Units in exchange for a designated amount of U.S. cash and/or a portfolio of securities closely approximating the holdings of the Funds. Once created, shares generally trade in the secondary market at market prices that change throughout the day. Except when aggregated in Creation Units, shares are not redeemable securities of the Funds. Shares of the Funds may only be purchased or redeemed by certain financial institutions (“Authorized Participants”). An Authorized Participant is either (i) a broker-dealer or other participant in the clearing process through the Continuous Net Settlement System of the National Securities Clearing Corporation or (ii) a Depository Trust Company participant and, in each case, must have executed a Participant Agreement with the Distributor. Most retail investors do not qualify as Authorized Participants nor have the resources to buy and sell whole Creation Units. Therefore, they are unable to purchase or redeem shares directly from the Funds. Rather, most retail investors may purchase shares in the secondary market with the assistance of a broker and are subject to customary brokerage commissions or fees.

The Funds currently offer one class of shares, which has no front-end sales load, no deferred sales charge, and no redemption fee. A fixed transaction fee is imposed for the transfer and other transaction costs associated with the purchase or sale of Creation Units. The standard fixed transaction fee for the Funds are $250, payable to the Custodian. The fixed transaction fee may be waived on certain orders if the Funds’ Custodian has determined to waive some or all of the costs associated with the order, or another party, such as the Advisor, has agreed to pay such fee. In addition, a variable fee may be charged on all cash transactions or substitutes for Creation Units of up to a maximum of 2% as a percentage of the value of the Creation Units subject to the transaction. There were no variable fees received during the period. The Funds may issue an unlimited number of shares of beneficial interest, with $0.01 par value.

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

NOTE 8 – INCOME TAXES AND DISTRIBUTIONS TO SHAREHOLDERS

As of December 31, 2019, the Funds’ most recent fiscal period, the components of accumulated earnings/(losses) on a tax basis were as follows:

| | | Managed Futures | | | Hedge | |

| | | Strategy ETF | | | Strategy ETF | |

| Cost of investments | | $ | 14,566,286 | | | $ | 13,293,068 | |

| Gross unrealized appreciation | | | 24,283 | | | | 474 | |

| Gross unrealized depreciation | | | (791 | ) | | | (204 | ) |

| Net unrealized depreciation | | | 23,492 | | | | 270 | |

| Undistributed ordinary income | | | 123,670 | | | | 130 | |

| Undistributed long-term capital gain | | | 185,230 | | | | 182 | |

| Total distributable earnings | | | 308,900 | | | | 312 | |

| Other accumulated gains/(losses) | | | — | | | | — | |

| Total accumulated earnings/(losses) | | $ | 332,392 | | | $ | 582 | |

As of December 31, 2019, the Funds had no short-term or long-term tax basis capital losses to offset future capital gains.

The tax character of distributions paid during the six months ended June 30, 2020 and fiscal period ended December 31, 2019 was as follows:

| | | Six Months Ended | | | | |

| | | June 30, 2020 | | | Fiscal Year Ended | |

| | | (Unaudited) | | | December 31, 2019 | |

| Managed Futures Strategy ETF | | | | | | |

| Ordinary income | | $ | 15,194 | | | $ | 735,072 | |

| Long-term capital gains | | | — | | | | 980,367 | |

| | | | | | | | | |

| Hedge Strategy ETF | | | | | | | | |

| Ordinary income | | $ | 14,173 | | | $ | 2,612 | |

| Long-term capital gains | | | — | | | | — | |

NOTE 9 – PRINCIPAL RISKS

Below are summaries of some, but not all, of the principal risks of investing in the Funds, each of which could adversely affect each Fund’s NAV, market price, yield, and total return. Further information about investment risks are available in each Fund’s prospectus and Statement of Additional Information.

Managed Futures Strategy ETF

Recent Market Events; Market Risk: The risk that the market value of a security may go up or down in response to many factors including the historical and prospective earnings of the issuer, the value of its assets, general economic conditions, interest rates, investor perceptions and market liquidity. Price changes may be temporary or last for extended

iM DBi ETFs

| CONSOLIDATED NOTES TO FINANCIAL STATEMENTS (Continued) |

| at June 30, 2020 (Unaudited) |

periods. Market risk may affect a single issuer, industry, sector of the economy or the market as a whole. U.S. and international markets experienced significant volatility in recent months and years due to a number of economic, political and global macro factors including the impact of the coronavirus as a global pandemic and related public health issues, growth concerns in the U.S. and overseas, uncertainties regarding interest rates, trade tensions and the threat of tariffs imposed by the U.S. and other countries. In particular, the spread of the novel coronavirus worldwide has resulted in disruptions to supply chains and customer activity, stress on the global healthcare system, rising unemployment claims, quarantines, cancellations, market declines, the closing of borders, restrictions on travel and widespread concern and uncertainty. Health crises and related political, social and economic disruptions caused by the spread of the recent coronavirus outbreak may also exacerbate other pre-existing political, social and economic risks in certain countries. It is not possible to know the extent of these impacts, and they may be short term or may last for an extended period of time. These developments as well as other events, such as the U.S. presidential election, could result in further market volatility and negatively affect financial asset prices, the liquidity of certain securities and the normal operations of securities exchanges and other markets, despite government efforts to address market disruptions. In addition, the Fund may face challenges with respect to its day-to-day operations if key personnel of the Advisor or other service providers are unavailable due to quarantines and restrictions on travel related to the coronavirus outbreak. Global economies and financial markets are increasingly interconnected, which increases the probabilities that conditions in one country or region might adversely impact issues in a different country or region.

Managed Futures Strategy Risk: In seeking to achieve its investment objective, the Fund will utilize various investment strategies that involve the use of complex investment techniques, and there is no guarantee that these strategies will succeed. The use of such strategies and techniques may subject the Fund to greater volatility and loss. There can be no assurance that utilizing a certain approach or model will achieve a particular level of return or reduce volatility and loss.