UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21910

Claymore Exchange-Traded Fund Trust 2

(Exact name of registrant as specified in charter)

227 West Monroe Street, Chicago, 60606

(Address of principal executive offices) (Zip code)

Amy J. Lee

227 West Monroe Street, Chicago, 60606

(Name and address of agent for service)

Registrant's telephone number, including area code: (312) 827-0100

Date of fiscal year end: May 31

Date of reporting period: June 1, 2016 - May 31, 2017

Item 1. Reports to Stockholders.

The registrant's annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the "Investment Company Act"), is as follows:

GUGGENHEIMINVESTMENTS.COM

. . . YOUR ROAD TO THE LATEST, MOST UP-TO-DATE INFORMATION

The shareholder report you are reading right now is just the beginning of the story. Online at guggenheiminvestments.com, you will find:

| • | Daily and historical fund pricing, fund returns, portfolio holdings and characteristics, and distribution history. |

| | |

| • | Investor guides and fund fact sheets. |

| | |

| • | Regulatory documents including a prospectus and copies of shareholder reports. |

Guggenheim Funds Distributors, LLC is constantly updating and expanding shareholder information services on each Fund’s website, in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more small way we are working to keep you better informed about your investment.

| Contents | | |

| | | |

| Dear Shareholder | 3 | |

| | | |

| Economic and Market Overview | 4 | |

| | | |

| Management Discussion of Fund Performance | 6 | |

| | | |

| Risks and Other Considerations | 13 | |

| | | |

| Performance Report and Fund Profile | 14 | |

| | | |

| Fees and Expenses | 25 | |

| | | |

| Schedules of Investments | 27 | |

| | | |

| Statements of Assets and Liabilities | 47 | |

| | | |

| Statements of Operations | 49 | |

| | | |

| Statements of Changes in Net Assets | 51 | |

| | | |

| Financial Highlights | 55 | |

| | | |

| Notes to Financial Statements | 62 | |

| | | |

| Report of Independent Registered Public | | |

| Accounting Firm | 70 | |

| | | |

| Other Information | 71 | |

| | | |

| Approval of Advisory Agreements – Claymore | | |

| Exchange-Traded Fund Trust 2 | 72 | |

| | | |

| Information on Board of Trustees and Officers | 77 | |

| | | |

| Trust Information | 81 | |

| | | |

| Guggenheim Investments Privacy Policies | 82 | |

| | | |

| About the Trust Adviser | Back Cover | |

DEAR SHAREHOLDER

Guggenheim Funds Investment Advisors, LLC (the “Investment Adviser”) is pleased to present the annual shareholder report for several of our exchange-traded funds (“ETFs” or “Funds”). This report covers performance of the Funds for the 12 months ended May 31, 2017.

The Investment Adviser is part of Guggenheim Investments, which represents the investment management businesses of Guggenheim Partners, LLC (“Guggenheim”), a global diversified financial services firm.

Guggenheim Funds Distributors, LLC, the distributor of the Funds, is committed to providing investors with innovative investment solutions; as of the date of this report, we offer ETFs with a wide range of domestic and global themes, as well as closed-end funds and unit investment trusts. We have built on the investment management strengths of Guggenheim Investments and worked with a diverse group of index providers to create some of the most distinctive ETFs available.

To learn more about economic and market conditions over the last year and the objective and performance of each ETF, we encourage you to read the Economic and Market Overview section of the report, which follows this letter, and the Management Discussion of Fund Performance for each ETF, which begins on page 6.

Sincerely,

Donald Cacciapaglia

President and Chief Executive Officer

Claymore Exchange-Traded Fund Trust 2

June 30, 2017

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 3 |

| ECONOMIC AND MARKET OVERVIEW (Unaudited) | May 31, 2017 |

The period was marked by significant events in the political sphere, both in the U.S. and globally. Late last June, Britain’s vote to depart the European Union shocked world markets, distressing the many market participants who had positioned themselves for the opposite outcome. The result was a sharp, but brief market sell off at the end of the second quarter of 2016.

With the election of Donald Trump, the market began anticipating that reduced regulation and fiscal stimulus would lead to stronger economic growth in the U.S. and globally. With the potential to finance some of this stimulus increased Treasury issuance, nominal interest rates climbed higher by the end of 2016.

By spring 2017, markets were reassessing their optimistic economic outlooks after not seeing much progress on the legislative front. This helped bond prices to stabilize and the yield curve to flatten. With the rate rise in June and the U.S. Federal Reserve’s (the “Fed”) announcement about reducing the size of its balance sheet, after the period ended, investors may see increased Treasury market volatility through the rest of the year.

Still, the global macroeconomic environment remains positive. China has stabilized, Europe is recovering, corporate earnings in the United States are rising, confidence measures are strong, and a U.S. recession appears unlikely before 2019. However, tracking estimates for first-quarter real Gross Domestic Product (“GDP”) growth gradually fell throughout the quarter despite strong gains in consumer and business sentiment since the election. GDP increased at an annual rate of 1.4% in the first quarter of 2017. The prospects for quarterly U.S. GDP growth are better going forward, and we expect a bounce back in the second quarter.

Our medium-term growth outlook has dimmed marginally as a result of the minimal progress seen to date on the Trump administration’s fiscal policy initiatives. The ongoing struggle to create a healthcare bill has sapped early legislative momentum, and tax reform shows that work still needs to be done to put the agenda into effect in a timely manner—meaning markets may come to realize that the Trump rally may be long on promise and short on delivery.

With the Fed set to continue raising interest rates—possibly at a faster pace than that the market is pricing in—the shape of the yield curve going forward will remain a major theme in many portfolios. In addition to another potential rate hike this year, the Fed may raise rates three to four more times in 2018. The Fed’s strategy to reduce its balance sheet could pressure yields higher in the short end and belly of the curve, which is where most of the new Treasury issuance is likely to come. At the long end, rates are likely to stay low for some time. Recall that the last time the 10-year Treasury note traded below 3%, it lasted nearly 22 years (June 1934 through March 1956.)

By many measures, the stock and bond markets have rarely been more expensive and more stable than in the second quarter of 2017. High-yield bonds were trading near their narrowest-ever spreads relative to Treasuries in May 2017. At the same time, U.S. stock market indexes are continuing to reach new highs while the Chicago Board Options Exchange Volatility Index (VIX), which measures option-implied S&P 500 volatility, is near its lowest level since 1993. The amount of complacency built into the markets argues for caution.

For the 12 months ended May 31, 2017, the Standard & Poor’s 500® (“S&P 500”) Index* returned 17.47%. The MSCI Europe-Australasia-Far East (“EAFE”) Index* returned 16.44%. The return of the MSCI Emerging Markets Index* was 27.41%.

In the bond market, the Bloomberg Barclays U.S. Aggregate Bond Index* posted a 1.58% return for the period, while the Bloomberg Barclays U.S. Corporate High Yield Index* returned 13.58%. The return of the Bloomberg Barclays 1-3 Month U.S. Treasury Bill Index* was 0.40% for the 12-month period.

The opinions and forecasts expressed may not actually come to pass. This information is subject to change at any time, based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

| |

| 4 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| ECONOMIC AND MARKET OVERVIEW (Unaudited) continued | May 31, 2017 |

*Index Definitions

All indices described below are unmanaged and reflect no expenses. It is not possible to invest directly in any index.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, mortgage-backed securities or “MBS” (agency fixed-rate and hybrid adjustable-rate mortgage, or “ARM”, pass-throughs), asset-backed securities (“ABS”), and commercial mortgage-backed securities (“CMBS”) (agency and non-agency).

The Bloomberg Barclays U.S. Corporate High Yield Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB +/BB + or below.

The Bloomberg Barclays 1-3 month U.S. Treasury Bill Index tracks the performance of the U.S. Treasury Bills with a remaining maturity of one to three months. U.S. Treasury Bills, which are short-term loans to the U.S. government, are full-faith-and-credit obligations of the U.S. Treasury and are generally regarded as being free of any risk of default.

The MSCI China Index is a capitalization-weighted index that monitors the performance of stocks from the country of China.

The MSCI EAFE Index is a capitalization weighted measure of stock markets in Europe, Australasia and the Far East.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market performance in the global emerging markets.

The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure equity market performance of developed markets. The MSCI World Index (Net) is calculated with net dividends reinvested.

The Standard & Poor’s (“S&P 500”) Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad economy, representing all major industries and is considered a representation of U.S. stock market.

The S&P/TSX Composite Index is a capitalization-weighted index. The index is designed to measure performance of the broad Canadian economy through changes in the aggregate market value of stocks representing all major industries.

The S&P Global Timber & Forestry Index is comprised of 25 of the largest publicly traded companies engaged in the ownership, management, or the upstream supply chain of forests and timberlands. These may be forest products companies, timber REITs, paper products companies, paper packaging companies, or agricultural product companies that are engaged in the ownership, management, or the upstream supply chain of forests and timberlands.

Industry Sectors

Comments about industry sectors in these fund commentaries are based on Bloomberg Barclays industry classifications.

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 5 |

| MANAGEMENT DISCUSSION OF FUND PERFORMANCE (Unaudited) | May 31, 2017 |

ENY Guggenheim Canadian Energy Income ETF

Fund Overview

The Guggenheim Canadian Energy Income ETF, NYSE Arca ticker: ENY (the “Fund”) seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of an equity index called the S&P/TSX Canadian High Income Energy Index (the “Index”). The Index includes the constituent stocks of the S&P/TSX Composite Index that are classified as energy companies, according to the Global Industry Classification Standard (“GICS”), and that also meet specific yield requirements.

The Fund will invest at least 80% of its total assets in securities that comprise the Index. The Fund generally will invest in all of the stocks comprising the Index in proportion to their weightings in the Index.

Fund Performance

All Fund returns cited–whether based on net asset value (“NAV”) or market price–assume the reinvestment of all distributions. This report discusses the annual fiscal period ended May 31, 2017.

On a market price basis, the Fund generated a total return of -0.01%, which included a decrease in market price over the period to $8.09 on May 31, 2017, from $8.33 on May 31, 2016. On an NAV basis, the Fund generated a total return of 0.36%, which included a decrease in NAV over the period to $8.14 on May 31, 2017, from $8.35 on May 31, 2016. At the end of the period the Fund’s shares were trading at a market price discount to NAV, which is to be expected from time to time. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses.

For underlying index and broad Canadian equity market comparison purposes, the underlying Index returned 1.66%, and the S&P/TSX Composite Index returned 8.82% for the 12-month period ended May 31, 2017.

The Fund made the following quarterly distributions per share during the annual period ended May 31, 2017, which were characterized as ordinary income.

| Month | | Distribution per Share | |

| June 2016 | | $ | 0.0693 | |

| September | | $ | 0.0658 | |

| December | | $ | 0.0742 | |

| March 2017 | | $ | 0.0463 | |

| Total | | $ | 0.2556 | |

Performance Attribution

Since nearly all of the Fund’s portfolio is invested in the energy sector, the return of this sector was the major source of the Fund’s positive NAV return for the 12-month period ended May 31, 2017.

Positions that contributed the most to return included Veresen, Inc., Alberta-based energy infrastructure company involved in pipelines, natural gas and power generation; Suncor Energy, Inc., a Canadian integrated energy company that specializes in production of synthetic crude from oil sands; and TransCanada Corp., network of natural gas and crude oil pipelines, along with wind, solar and nuclear power facilities (6.1%, 5.4%, and 5.3%, respectively, of the Fund’s long-term investments at period end).

Positions that detracted the most included Crescent Point Energy Corp., an oil and gas company based in Calgary, Alberta; Peyto Exploration & Development Corp., an explorer and producer of unconventional natural gas in Alberta’s Deep Basin; and ARC Resources Ltd., a Canadian oil and gas producer (4.3%, 4.3%, and 4.6%, respectively, of the Fund’s long-term investments at period end).

| |

| 6 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| MANAGEMENT DISCUSSION OF FUND PERFORMANCE (Unaudited) continued | May 31, 2017 |

TAO Guggenheim China Real Estate ETF

Fund Overview

The Guggenheim China Real Estate ETF, NYSE Arca ticker: TAO (the “Fund”) seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of an equity index called the AlphaShares China Real Estate Index (the “Index”).

The Index is designed to measure and monitor the performance of the investable universe of publicly-traded companies and real estate investment trusts (“REITs”) which are open to foreign ownership and derive a majority of their revenues from real estate development, management, and/or ownership of property in China or the Special Administrative Regions of China, such as Hong Kong, and Macau. The Index was created by AlphaShares, LLC and is maintained by Standard & Poor’s.

The Fund will invest at least 90% of its total assets in common stock, American Depositary Receipts (“ADRs”), American Depositary Shares (“ADSs”), Global Depositary Receipts (“GDRs”), and International Depositary Receipts (“IDRs”) that comprise the Index and depositary receipts representing common stocks included in the Index (or underlying securities representing the ADRs, ADSs, GDRs, and IDRs included in the Index). The Fund generally will invest in all of the securities comprising the Index in proportion to their weightings in the Index.

Fund Performance

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. This report discusses the annual fiscal period ended May 31, 2017.

On a market price basis, the Fund generated a total return of 36.26%, which included an increase in market price over the period to $25.14 on May 31, 2017, from $18.83 on May 31, 2016. On an NAV basis, the Fund generated a total return of 34.94%, which included an increase in NAV over the period to $25.02 on May 31, 2017, from $18.92 on May 31, 2016. At the end of the period the Fund’s shares were trading at a market price premium to NAV, which is to be expected from time to time. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses.

For underlying index and market comparison purposes, the Index returned 35.92% and the MSCI China Index returned 30.60% for the 12-month period ended May 31, 2017.

The Fund made a distribution of $0.4027 per share on December 30, 2016, which was characterized as ordinary income.

Performance Attribution

Nearly all of the Fund’s investments are in the real estate sector. For the 12-month period ended May 31, 2017, that sector contributed the most to return.

Positions that contributed the most to the Fund’s return included Country Garden Holdings Co. Ltd., a property development company based in Guangdong Province; China Wharf Holdings Ltd., which operates businesses in property investment and development, and communications, media, and entertainment; and China Evergrande Group, a property developer in Guangdong that sell apartments to upper- and middle-income dwellers (5.5%, 5.1%, and 3.9%, respectively, of the Fund’s long-term investments at period end).

Positions that detracted the most from the Fund’s return included China Logistics Property Holdings Co. Ltd., which constructs warehouses and provides leasing services to logistic firms (0.4% of the Fund’s long-term investments at period end); Swire Pacific Ltd.—Class A, a London-based conglomerate that operates in the property development, aviation, beverage, and marine services industries (3.1% of the Fund’s long-term investments at period end); and China New City Commercial Development Ltd., a commercial property developer, owner, and operator with a focus on developing integrated commercial complexes in sub-city centers of second-tier cities in the Yangtze River Delta Region (not held in the Fund’s portfolio at period end).

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 7 |

| MANAGEMENT DISCUSSION OF FUND PERFORMANCE (Unaudited) continued | May 31, 2017 |

HAO Guggenheim China Small Cap ETF

Fund Overview

The Guggenheim China Small Cap ETF, NYSE Arca ticker: HAO (the “Fund”) seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of an equity index called the AlphaShares China Small Cap Index (the “Index”).

The Index is designed to measure and monitor the performance of publicly traded mainland China-based small-capitalization companies. The Index was created by AlphaShares, LLC (“AlphaShares”) and is maintained by Standard & Poor’s. For inclusion in the Index, AlphaShares defines small-capitalization companies as those companies with a maximum $1.5 billion float-adjusted market capitalization.

The Fund will invest at least 90% of its total assets in common stock, American Depositary Receipts (“ADRs”), American Depositary Shares (“ADSs”), Global Depositary Receipts (“GDRs”), and International Depositary receipts (“IDRs”) that comprise the Index and depositary receipts representing common stocks included in the Index (or underlying securities representing the ADRs, ADSs, GDRs, and IDRs included in the Index). The Fund generally will invest in all of the securities comprising the Index in proportion to their weightings in the Index.

Fund Performance

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. This report discusses the annual fiscal period ended May 31, 2017.

On a market price basis, the Fund generated a total return of 17.13%, which included an increase in market price over the period to $24.97 on May 31, 2017, from $22.04 on May 31, 2016. On an NAV basis, the Fund generated a total return of 18.05%, which included an increase in NAV over the period to $25.20 on May 31, 2017, from $22.06 on May 31, 2016. At the end of the period the Fund’s shares were trading at a market price discount to NAV, which is to be expected from time to time. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses.

For underlying index and broad market comparison purposes, the Index returned 18.72% and the MSCI China Index returned 30.60% for the 12-month period ended May 31, 2017.

The Fund made a distribution of $0.7553 per share on December 30, 2016, which was characterized as ordinary income.

Performance Attribution

For the 12-month period ended May 31, 2017, the real estate sector was the largest contributor to the Fund’s return, followed by the materials sector. The consumer staples sector was the only detractor from return; the telecommunications services sector contributed least.

Positions that contributed the most to the Fund’s return included Sunac China Holdings Ltd., which focuses on large-scale property developments in Tianjin and other cities; China Lodging Group Ltd. ADR, a leading hotel operator and franchisor in China under 12 brand names; and Kingboard Chemical Holdings Ltd., a laminate manufacturer (1.3%, 1.1%, and 1.1%, respectively, of the Fund’s long-term investments at period end).

Positions that detracted the most from the Fund’s return included 58.com, Inc. ADR—Class A, which operates the largest online marketplace serving local merchants and consumers in China; Tech Pro Technology Development Ltd., an investment holding company principally engaged in the manufacture and sale of Light Emitting Diode (LED) lighting products and accessories; and China Huishan Dairy Holdings Co. Ltd., a dairy farm operator (none held in the Fund’s portfolio at period end).

| |

| 8 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| MANAGEMENT DISCUSSION OF FUND PERFORMANCE (Unaudited) continued | May 31, 2017 |

FRN Guggenheim Frontier Markets ETF

Fund Overview

The Guggenheim Frontier Markets ETF, NYSE Arca ticker: FRN (the “Fund”), seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of the BNY Mellon New Frontier Index (the “Index”).

The Index is composed of all liquid (as defined by the criteria set forth below) American depositary receipts (“ADRs”), global depositary receipts (“GDRs”), and local securities of certain countries that are represented in the Index. The Index tracks the performance of ADRs listed on a U.S. exchange, GDRs traded on the London Stock Exchange (“LSE”), and ordinary share classes of equity securities listed on exchanges in Frontier Market countries (as defined below).

The Bank of New York Mellon, the Fund’s Index provider (“BNY Mellon” or the “Index Provider”), categorizes countries as “Frontier Market” based upon an evaluation of gross domestic product growth, per capita income growth, experienced and expected inflation rates, privatization of infrastructure, and social inequalities. These countries currently are: Argentina*, Bahrain*, Bangladesh*, Bulgaria, Croatia, Cyprus, Jordan*, Kazakhstan*, Kenya, Kuwait, Latvia, Lithuania, Morocco, Nigeria, Oman, Pakistan, Panama, Romania, Sri Lanka*, Tunisia*, Vietnam and Zambia (* denotes that such country must have an eligible class in a developed or emerging market).

The universe of potential Index constituents includes all liquid ADRs, GDRs, and ordinary shares which meet certain criteria with respect to trading volume and market capitalization. Potential Index constituents include securities with free-float market capitalizations greater than $250 million, which may include securities of all categories of market capitalizations, as defined by the Index Provider. The Fund also may invest directly in other exchange-traded funds (“ETFs”) that provide exposure to securities similar to those securities in which the Fund may directly invest.

Fund Performance

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. This report discusses the annual period ended May 31, 2017.

On a market price basis, the Fund generated a total return of 26.20%, which included an increase in market price over the period to $13.74 on May 31, 2017, from $11.33 on May 31, 2016. On an NAV basis, the Fund generated a total return of 24.72%, which included an increase in NAV over the period to $13.76 on May 31, 2017, from $11.48 on May 31, 2016. At the end of the period the Fund’s shares were trading at a market price discount to NAV, which is to be expected from time to time. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses.

The Index returned 27.30% and the MSCI Emerging Markets Index returned 27.41% for the 12-month period ended May 31, 2017.

The Fund made a distribution of $0.4702 per share on December 30, 2016, which was characterized as ordinary income.

Performance Attribution

For the 12-month period ended May 31, 2017, the financials sector was the largest contributor to return, followed by the industrials sector. The consumer staples sector was the only detractor from return; the health care sector contributed least.

Positions that contributed the most to the Fund’s return included MercadoLibre, Inc. an Argentine online marketplace dedicated to e-commerce and online auctions; Copa Holdings, S.A.—Class A, which provides international airline passenger and cargo service; and KAZ Minerals Plc, a copper company focused on large scale, low cost open pit mining in Kazakhstan (6.3%, 4.9%, and 2.3%, respectively, of the Fund’s long-term investments at period end).

Positions that detracted the most from the Fund’s return included Nigerian Breweries Plc, a large brewing company that serves the Nigerian market and exports to other parts of West Africa (2.8% of the Fund’s long-term investments at period end); Zenith Bank Plc, a Nigerian multinational financial services provider (not held in the Fund’s portfolio at period end); and Equity Bank Ltd., is a financial services provider headquartered in Nairobi, Kenya (not held in the Fund’s portfolio at period end).

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 9 |

| MANAGEMENT DISCUSSION OF FUND PERFORMANCE (Unaudited) continued | May 31, 2017 |

HGI Guggenheim International Multi-Asset Income ETF

Fund Overview

The Guggenheim International Multi-Asset Income ETF, NYSE Arca ticker: HGI (the “Fund”) seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of an index called the Zacks International Multi-Asset Income Index (the “Index”).

The Index is comprised of approximately 150 securities selected, based on investment and other criteria, from a universe of international companies, global real estate investment trusts (“REITs”), master limited partnerships (“MLPs”), Canadian royalty trusts, and American Depositary Receipts (“ADRs”) of emerging market companies and U.S. listed closed-end funds that invest in international companies, and at all times is comprised of at least 40% non-U.S. securities. The companies in the universe are selected using a proprietary strategy developed by Zacks Investment Research, Inc.

The Fund will invest at least 90% of its total assets in securities that comprise the Index and underlying securities representing the ADRs included in the Index. The Fund generally will invest in all of the securities comprising the Index in proportion to their weightings in the Index.

Fund Performance

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. This report discusses the annual fiscal period ended May 31, 2017.

On a market price basis, the Fund generated a total return of 18.69%, which included an increase in market price over the period to $16.79 on May 31, 2017, from $14.66 on May 31, 2016. On an NAV basis, the Fund generated a total return of 18.09%, which included an increase in NAV over the period to $16.81 on May 31, 2017, from $14.75 on May 31, 2016. At the end of the period the Fund’s shares were trading at a market price discount to NAV, which is to be expected from time to time. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses.

For underlying index and broad market comparison purposes, the Index returned 18.36% and the MSCI EAFE Index returned 16.44% for the 12-month period ended May 31, 2017.

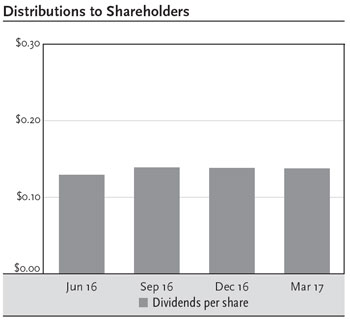

The Fund made the following quarterly distributions per share during the annual period ended May 31, 2017, which were characterized as ordinary income.

| Month | | Distribution per Share | |

| June 2016 | | $ | 0.1289 | |

| September | | $ | 0.1390 | |

| December | | $ | 0.1380 | |

| March 2017 | | $ | 0.1372 | |

| Total | | $ | 0.5431 | |

Performance Attribution

For the 12-month period ended May 31, 2017, the financials sector was the largest contributor to return, followed by the industrials sector. The energy sector was the only detractor from return.

Positions that contributed the most to the Fund’s return included Qiwi Plc ADR—Class B, a provider of payment services in Russia and the CIS; Man Wah Holdings Ltd., a Chinese furniture and bedding manufacturer; and Braskem S.A. Preferred ADR—Class A, a Brazilian petrochemical company (2.3%, 2.0%, and 1.3%, respectively, of the Fund’s long-term investments at period end).

Positions that detracted the most from the Fund’s return included Crescent Point Energy Corp., an oil and gas company based in Calgary, Alberta, Canada (0.6% of the Fund’s long-term investments at period end); PLDT, Inc. ADR, the largest telecommunications and digital services company in the Philippines (not held in the Fund’s portfolio at period end); and DRDGOLD Ltd. ADR, a South African gold producer (0.6% of the Fund’s long-term investments at period end).

| |

| 10 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| MANAGEMENT DISCUSSION OF FUND PERFORMANCE (Unaudited) continued | May 31, 2017 |

CUT Guggenheim MSCI Global Timber ETF

Fund Overview

The Guggenheim MSCI Global Timber ETF, NYSE Arca ticker: CUT (the “Fund”) seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of an equity index called the MSCI ACWI IMI Timber Select Capped Index (the “Index”).

The MSCI ACWI IMI Timber Select Capped Index is designed to measure the performance of securities that are engaged in the ownership and management of forests and timberlands and production of finished products which use timber as raw material. These companies include companies that produce forest products, paper products and paper packaging products, and real estate investment trusts (“REITs”) that own and/or manage timberland. Index constituents must be constituents of the MSCI ACWI Investable Market Index, a rules-based index that measures equity market performance of developed and emerging markets.

The Fund will invest at least 90% of its total assets in common stock, American depositary receipts (“ADRs”) and global depositary receipts (“GDRs”) that comprise the Index and depositary receipts representing common stocks included in the Index (or underlying securities representing the ADRs and GDRs included in the Index). The Fund generally will invest in all of the securities comprising the Index in proportion to their weightings in the Index.

Fund Performance

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. This report discusses the annual fiscal period ended May 31, 2017.

On a market price basis, the Fund generated a total return of 19.09%, which included an increase in market price over the period to $27.52 on May 31, 2017, from $23.59 on May 31, 2016. On an NAV basis, the Fund generated a total return of 19.09%, which included an increase in NAV over the period to $27.57 on May 31, 2017, from $23.63 on May 31, 2016. At the end of the period the Fund’s shares were trading at a market price discount to NAV, which is to be expected from time to time. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses.

The MSCI ACWI IMI Timber Select Capped Index returned 19.23% for the 12-month period ended May 31, 2017. The S&P Global Timber and Forestry Index returned 26.94%; and the MSCI World Index returned 16.42%. The STOXX® Europe TMI (Total Market Index) Forestry & Paper Index returned 42.58%. It is a market-capitalization weighted index of all companies in the Forestry & Paper sector of the STOXX Europe TMI.

The Fund made a distribution of $0.5152 per share on December 30, 2016, which was characterized as ordinary income.

Performance Attribution

Most of the Fund’s portfolio is invested in the materials sector, and it was the major contributor to the Fund’s return for the 12-month period ended May 31, 2017. The Fund also has positions in the financials sector, which contributed to return for the period.

Positions that contributed the most to the Fund’s return included UPM-Kymmene Oyj, a Finnish forest industry company; WestRock Co., an American corrugated packaging company; and Packaging Corporation of America, a manufacturer of containerboard and corrugated packaging (5.1%, 5.0%, and 4.9%, respectively, of the Fund’s long-term investments at period end).

Positions detracting the most from the Fund’s return included Bemis Company, Inc., global manufacturer of flexible packaging products and pressure-sensitive materials; Huhtamaki Oyj, a Finnish global food packaging concern; and Stella-Jones, Inc., a North American manufacturer of pressure treated wood products (2.1%, 1.8%, and 0.8%, respectively, of the Fund’s long-term investments at period end).

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 11 |

| MANAGEMENT DISCUSSION OF FUND PERFORMANCE (Unaudited) continued | May 31, 2017 |

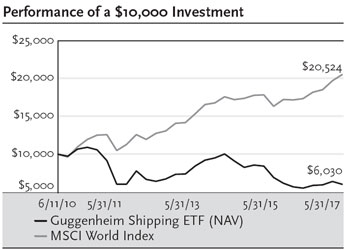

SEA Guggenheim Shipping ETF

Fund Overview

The Guggenheim Shipping ETF, NYSE Arca ticker: SEA (the “Fund”) seeks investment results that correspond generally to the performance, before the Fund’s fees and expenses, of an equity index called the Dow Jones Global Shipping IndexSM (the “Index”).

The Index is designed to measure the performance of high-dividend paying companies in the global shipping industry. CME Group Index Services, LLC (the “Index Provider”) uses a rules-based methodology to rank companies by yield that are involved in the shipping industry globally that primarily transport goods and materials. The Index Provider considers a company to be in the shipping industry if its revenues are derived primarily from shipping activities (excluding companies solely involved in transporting passengers). The Index Provider determines whether a company is “high-dividend paying” by ranking it relative to other companies in the shipping industry based upon indicated annual yield (most recent distribution annualized and divided by the current share price). The companies in the Index may be located in any country, including those classified as emerging markets.

The Fund will at all times invest at least 90% of its total assets in common stock, American Depositary Receipts (“ADRs”), Global Depositary Receipts(“GDRs”), and master limited partnerships (“MLPs”) that comprise the Index and the underlying stocks of the ADRs and GDRs in the Index. The Fund generally will invest in all of the securities comprising the Index in proportion to their weightings in the Index.

Fund Performance

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. This report discusses the annual fiscal period ended May 31, 2017.

On a market price basis, the Fund generated a total return of 1.79%, which included a decrease in market price over the period to $11.49 on May 31, 2017, from $12.00 on May 31, 2016. On an NAV basis, the Fund generated a total return of 1.83%, which included a decrease in NAV over the period to $11.50 on May 31, 2017, from $12.01 on May 31, 2016. At the end of the period the Fund’s shares were trading at a market price discount to NAV, which is to be expected from time to time. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses.

For underlying index and broad market comparison purposes, the Index returned 0.76% and the MSCI World Index returned 16.42% for the 12-month period ended May 31, 2017.

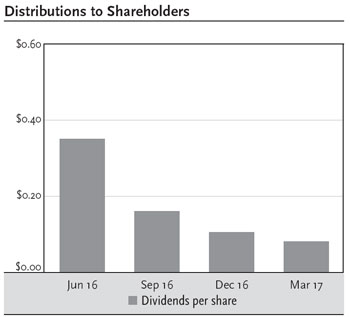

The Fund made the following quarterly distributions per share during the annual period ended May 31, 2017, which were characterized as ordinary income.

| Month | | Distribution per Share | |

| June 2016 | | $ | 0.3503 | |

| September | | $ | 0.1603 | |

| December | | $ | 0.1059 | |

| March 2017 | | $ | 0.0810 | |

| Total | | $ | 0.6975 | |

Performance Attribution

Most of the Fund’s portfolio is invested in the energy and the industrials sectors; the industrials sector contributed to return, while the energy sector detracted.

Positions that contributed most to the Fund’s return included A.P. Moller-Maersk AS—Class B, a Danish business conglomerate with activities in the transport & logistics and energy sectors; Kawasaki Kisen Kaisha Ltd., an integrated logistics company known as the “K” Line; and Golar LNG Partners LP, which owns and operates floating storage and regasification units and LNG carriers (24.0%, 6.3%, and 3.6%, respectively, of the Fund’s long-term investments at period end).

Positions that detracted the most from the Fund’s return included Nordic American Tankers Ltd., which owns 33 crude oil tankers; Seaspan Corp., an independent owner and manager of containerships; and Teekay Offshore Partners LP, an international provider of marine transportation, oil production, storage, long-distance towing and other services to the oil industry (2.7%, 2.0%, and 1.6%, respectively, of the Fund’s long-term investments at period end).

| |

| 12 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| RISKS AND OTHER CONSIDERATIONS (Unaudited) | May 31, 2017 |

The views expressed in this report reflect those of the portfolio managers and Guggenheim Investments only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any kind. The material may also contain forward-looking statements that involve risk and uncertainty, and there is no guarantee they will come to pass.

This information does not represent an offer to sell securities of the Funds and it is not soliciting an offer to buy securities of the Funds. An investment in the various Guggenheim Investments ETFs is subject to certain risks and other considerations. Below are some general risks and considerations associated with investing in the Funds, which may cause you to lose money, including the entire principal that you invest. Please refer to the individual ETF prospectus for a more detailed discussion of the Fund-specific risks and considerations.

Equity Risk: The value of the equity securities held by the Funds may fall due to general market and economic conditions, perceptions regarding the industries in which the issuers of securities held by the Funds participate, or factors relating to specific companies in which the Funds invest.

Foreign Investment Risk: Investing in non-U.S. issuers may involve unique risks such as currency, political, and economic risk, as well as less market liquidity, generally greater market volatility and less complete financial information than for U.S. issuers.

Small- and Medium-Sized Company Risk: Investing in securities of these companies involves greater risk as their stocks may be more volatile and less liquid than investing in more established companies. These stocks may have returns that vary, sometimes significantly, from the overall stock market.

Non-Correlation Risk: The Funds’ return may not match the return of the Index including, but not limited to, operating expenses and costs in buying and selling securities to reflect changes in the Index. The Funds may not be fully invested at times. If the Funds utilize a sampling approach or futures or other derivative positions, their return may not correlate with the Index return, as would be the case if they purchased all of the stocks with the same weightings as the Index.

Passive Management Risk: The Funds are not “actively” managed. Therefore, they would not necessarily sell a stock because the stock’s issuer was in financial trouble unless that stock is removed from the Index.

Issuer-Specific Changes: The value of an individual security or particular type of security can be more volatile than the market as a whole and can perform differently from the value of the market as a whole. The value of securities of smaller issuers can be more volatile than that of larger issuers.

Industry Risk: If its Index is comprised of issuers in a particular industry or sector, a Fund would therefore be focused in that industry or sector. Accordingly, that Fund may be subject to more risks than if it were broadly diversified over numerous industries and sectors of the economy.

Non-Diversified Fund Risk: Certain Funds are considered non-diversified and can invest a greater portion of assets in securities of individual issuers than a diversified fund. As a result, changes in the market value of a single investment could cause greater fluctuations in share price than would occur in a diversified fund.

Emerging Markets Risk (excluding CUT, FRN, HGI, TAO, HAO and SEA): Investment in securities of issuers based in developing or “emerging markets” countries entails all of the risks of investing in securities of non-U.S. issuers, as previously described, but to a heightened degree.

Canadian Risk (ENY and HGI): Investing in Canadian royalty trusts and stocks listed on the TSX are subject to: Commodity Exposure Risk, Reliance on Exports Risk, U.S. Economic Risk and Structural Risk (Political Risk).

Master Limited Partnership (MLP) Risk (FRN, SEA and HGI): Investments in securities of MLPs involve risks that differ from an investment in common stock. Holders of the units of MLPs have more limited control and limited rights to vote on matters affecting the partnership. There are also certain tax risks associated with an investment in units of MLPs.

China Investment Risk (HAO and TAO): Investing in securities of Chinese companies involves additional risks, including, but not limited to: the economy of China differs, often unfavorably, from the U.S. economy in such respects as structure, general development, government involvement, wealth distribution, rate of inflation, growth rate, allocation of resources and capital reinvestment, among others; the central government has historically exercised substantial control over virtually every sector of the Chinese economy through administrative regulation and/or state ownership; and actions of the Chinese central and local government authorities continue to have a substantial effect on economic conditions in China.

REIT Risk (HGI, TAO and CUT): Investments in securities of real estate companies involve risks. These risks include, among others, adverse changes in national, state or local real estate conditions; obsolescence of properties; changes in the availability, cost and terms of mortgage funds; and the impact of changes in environmental laws.

Risks of Investing In Other Investment Companies (HGI): Investments in securities of other investment companies involve risks, including, among others, the fact that shares of other investment companies are subject to the management fees and other expenses of those companies, and the purchase of shares of some investment companies (in the case of closed-end investment companies) may sometimes require the payment of substantial premiums above the value of such companies’ portfolio securities or net asset values.

Risks of Investing in Frontier Securities (FRN): Investment in securities in emerging markets countries involves risks not associated with investments in securities in developed countries, including risks associated with expropriation and/or nationalization, political or social instability, armed conflict, the impact on the economy as a result of civil war, religious or ethnic unrest and the withdrawal or non-renewal of any license enabling the Fund to trade in securities of a particular country, confiscatory taxation, restrictions on transfers of assets, lack of uniform accounting, auditing and financial reporting standards, less publicly available financial and other information, diplomatic development which could affect U.S. investments in those countries and potential difficulties in enforcing contractual obligations. Frontier countries generally have smaller economies or less developed capital markets than traditional emerging markets, and, as a result, the risk of investing in emerging markets countries are magnified in frontier countries.

As of the date of this report, a significant percentage of the BNY Mellon New Frontier Index is comprised of securities of companies from Kuwait, Morocco and Pakistan. To the extent that the Index is focused on securities of any one country, including Kuwait, Morocco or Pakistan, the value of the Index will be especially affected by adverse developments in such country, including the risks described above.

Securities Lending Risk: Although each Fund will receive collateral in connection with all loans of its securities holdings, the Funds would be exposed to a risk of loss should a borrower default on its obligation to return the borrowed securities (e.g., the loaned securities may have appreciated beyond the value of the collateral held by the Fund). In addition, the Funds will bear the risk of loss of any cash collateral that they invest.

In addition to the risks described, there are certain other risks related to investing in the Funds. These risks are described further in the Prospectus and Statement of Additional Information and at guggenheiminvestments.com/etf.

This material is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 13 |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) | May 31, 2017 |

ENY Guggenheim Canadian Energy Income ETF

| Fund Statistics | | | |

| Share Price | | $ | 8.09 |

| Net Asset Value | | $ | 8.14 |

| Discount to NAV | | | -0.61% |

| Net Assets ($000) | | $ | 24,596 |

AVERAGE ANNUAL TOTAL RETURNS FOR THE

PERIOD ENDED May 31, 2017 |

| | | | | | | | | Since |

| | | One | | Three | | Five | | Inception |

| | | Year | | Year | | Year | | (07/03/07) |

| Guggenheim Canadian | | | | | | | | |

| Energy Income ETF | | | | | | | | |

| NAV | | 0.36% | | -18.20% | | -8.53% | | -7.45% |

| Market | | -0.01% | | -18.50% | | -8.51% | | -7.51% |

| Sustainable Canadian | | | | | | | | |

| Energy Income | | | | | | | | |

| Index S&P/TSX/ | | | | | | | | |

| Canadian High | | | | | | | | |

| Income Energy | | | | | | | | |

| Index | | 1.66% | | -17.37% | | -8.09%1 | | -6.41%1 |

| S&P/TSX | | | | | | | | |

| Composite | | | | | | | | |

| Index | | 8.82% | | -2.66% | | 3.44% | | 1.33% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Since inception returns assume a purchase of the Fund at the initial share price of $25.05 per share for share price returns or initial net asset value (NAV) of $25.05 per share for NAV returns. Returns for periods of less than one year are not annualized.

The S&P/TSX Composite is the headline index for the Canadian equity market. It is the broadest in the S&P/TSX family and is the basis for multiple sub-indices.The referenced indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

Per the most recent prospectus, the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 0.87%. In the Financial Highlights section of this Annual Report, the Fund’s annualized net operating expense ratio was 0.66% while the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 0.90%. There is a contractual fee waiver currently in place for this Fund through December 31, 2019 to the extent necessary in keeping the Fund’s operating expense ratio from exceeding 0.65% of average net assets per year. Some expenses fall outside of this expense cap and actual expenses may be higher than 0.65%. Without this expense cap, actual returns would be lower. Please see the Financial Highlights for recent expense ratios.

| Country Diversification |

| | % of Long-Term |

| Country | Investments |

| Canada | 100.0% |

| Ten Largest Holdings | | (% of Total Net Assets) |

| Veresen, Inc. | | 6.1% |

| Keyera Corp. | | 5.5% |

| Suncor Energy, Inc. | | 5.4% |

| PrairieSky Royalty Ltd. | | 5.3% |

| TransCanada Corp. | | 5.3% |

| Pembina Pipeline Corp. | | 5.2% |

| AltaGas Ltd. | | 5.0% |

| Inter Pipeline Ltd. | | 4.9% |

| Enbridge, Inc. | | 4.9% |

| Canadian Natural Resources Ltd. | | 4.6% |

| Top Ten Total | | 52.2% |

“Ten Largest Holdings” excludes any temporary cash investments.

| 1 | Benchmark returns reflect the blended return of the Sustainable Canadian Energy Income Index from 7/3/07 – 7/31/13 and the return of the S&P/TSX Canadian High Income Energy Index, net of foreign withholding taxes, from 8/1/13 – 5/31/17. |

| |

| 14 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

ENY Guggenheim Canadian Energy Income ETF continued

This graph compares a hypothetical $10,000 investment in the Fund, made at its inception, with a similar investment in the Standard and Poor’s Toronto Stock Exchange Composite Index (S&P/TSX Composite Index). Results include the reinvestment of all dividends and capital gains. Past performance is no guarantee of future results. The S&P/TSX Composite Index is a capitalization-weighted index. The index is designed to measure performance of the broad Canadian economy through changes in the aggregate market value of stocks representing all major industries. It is not possible to invest directly in the S&P/TSX Composite Index. Investment return and principal value will fluctuate with changes in market conditions and other factors and Fund shares, when redeemed, may be worth more or less than their original investment.

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 15 |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

TAO Guggenheim China Real Estate ETF

| Fund Statistics | | | |

| Share Price | | $ | 25.14 |

| Net Asset Value | | $ | 25.02 |

| Premium to NAV | | | 0.48% |

| Net Assets ($000) | | $ | 44,038 |

| AVERAGE ANNUAL TOTAL RETURNS FOR THE |

| PERIOD ENDED MAY 31, 2017 |

| | | | | Since |

| | One | Three | Five | Inception |

| | Year | Year | Year | (12/18/07) |

| Guggenheim China | | | | |

| Real Estate ETF | | | | |

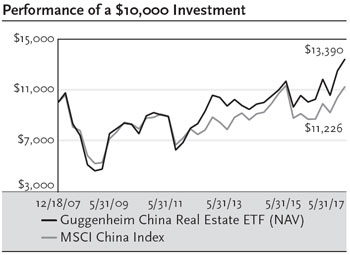

| NAV | 34.94% | 10.20% | 11.52% | 3.14% |

| Market | 36.26% | 10.57% | 11.62% | 3.18% |

| AlphaShares China | | | | |

| Real Estate | | | | |

| Index | 35.92% | 10.66% | 12.08% | 3.84% |

| MSCI China | | | | |

| Index | 30.60% | 8.38% | 8.90% | 1.24% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Since inception returns assume a purchase of the Fund at the initial share price of $23.50 per share for share price returns or initial net asset value (NAV) of $23.50 per share for NAV returns. Returns for periods of less than one year are not annualized.

The MSCI China Index is a capitalization-weighted index that measures the performance of large- and mid-cap securities in the Chinese equity markets and includes representation across China H shares, B shares, Red chips and P chips. The referenced indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

Per the most recent prospectus, the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 1.15%. In the Financial Highlights section of this Annual Report, the Fund’s annualized net operating expense ratio was 0.70% while the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 0.99%. There is a contractual fee waiver currently in place for this Fund through December 31, 2019 to the extent necessary in keeping the Fund’s operating expense ratio from exceeding 0.65% of average net assets per year. Some expenses fall outside of this expense cap and actual expenses may be higher than 0.65%. Without this expense cap, actual returns would be lower. Please see the Financial Highlights for recent expense ratios.

| Portfolio Breakdown | % of Net Assets |

| Financial | 87.3% |

| Diversified | 9.5% |

| Energy | 1.7% |

| Consumer, Cyclical | 0.7% |

| Industrial | 0.4% |

| Total Common Stocks | 99.6% |

| Securities Lending Collateral | 2.0% |

| Total Investments | 101.6% |

| Other Assets & Liabilities, net | -1.6% |

| Net Assets | 100.0% |

| Ten Largest Holdings | (% of Total Net Assets) |

| Country Garden Holdings Company Ltd. | 5.5% |

| Wharf Holdings Ltd. | 5.0% |

| Hongkong Land Holdings Ltd. | 5.0% |

| Henderson Land Development Company Ltd. | 4.8% |

| China Resources Land Ltd. | 4.8% |

| Link REIT | 4.8% |

| Sun Hung Kai Properties Ltd. | 4.7% |

| Cheung Kong Property Holdings Ltd. | 4.6% |

| China Overseas Land & Investment Ltd. | 4.4% |

| New World Development Company Ltd. | 4.2% |

| Top Ten Total | 47.8% |

“Ten Largest Holdings” excludes any temporary cash investments.

This graph compares a hypothetical $10,000 investment in the Fund, made at its inception, with a similar investment in the MSCI China Index. Results include the reinvestment of all dividends and capital gains. Past performance is no guarantee of future results. The MSCI China Index is a capitalization-weighted index that monitors the performance of stocks from the country of China. The referenced index is unmanaged. It is not possible to invest directly in the MSCI China Index. Investment return and principal value will fluctuate with changes in market conditions and other factors and Fund shares, when redeemed, may be worth more or less than their original investment.

| |

| 16 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

HAO Guggenheim China Small Cap ETF

| Fund Statistics | | | |

| Share Price | | $ | 24.97 |

| Net Asset Value | | $ | 25.20 |

| Discount to NAV | | | -0.91% |

| Net Assets ($000) | | $ | 85,687 |

| AVERAGE ANNUAL TOTAL RETURNS FOR THE |

| PERIOD ENDED MAY 31, 2017 |

| | | | | Since |

| | One | Three | Five | Inception |

| | Year | Year | Year | (01/30/08) |

| Guggenheim China | | | | |

| Small Cap ETF | | | | |

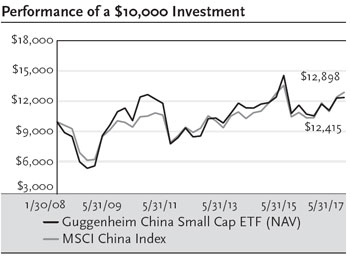

| NAV | 18.05% | 3.81% | 7.45% | 2.34% |

| Market | 17.13% | 3.55% | 7.22% | 2.24% |

| AlphaShares China | | | | |

| Small Cap | | | | |

| Index | 18.72% | 1.68% | 6.31% | 2.33% |

| MSCI China | | | | |

| Index | 30.60% | 8.38% | 8.90% | 2.76% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Since inception returns assume a purchase of the Fund at the initial share price of $24.34 per share for share price returns or initial net asset value (NAV) of $24.34 per share for NAV returns. Returns for periods of less than one year are not annualized.

The MSCI China Index is a capitalization-weighted index that measures the performance of large- and mid-cap securities in the Chinese equity markets and includes representation across China H shares, B shares, Red chips and P chips. The referenced index is unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

Per the most recent prospectus, the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 0.87%. In the Financial Highlights section of this Annual Report, the Fund’s annualized net operating expense ratio was 0.75% while the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 0.90%. There is a contractual fee waiver currently in place for this Fund through December 31, 2019 to the extent necessary in keeping the Fund’s operating expense ratio from exceeding 0.70% of average net assets per year. Some expenses fall outside of this expense cap and actual expenses may be higher than 0.70%. Without this expense cap, actual returns would be lower. Please see the Financial Highlights for recent expense ratios.

| Portfolio Breakdown | % of Net Assets |

| Financial | 21.7% |

| Industrial | 17.3% |

| Consumer, Non-cyclical | 17.0% |

| Consumer, Cyclical | 15.4% |

| Basic Materials | 8.6% |

| Communications | 6.7% |

| Technology | 5.4% |

| Other | 7.3% |

| Total Long-Term Investments | 99.4% |

| Securities Lending Collateral | 10.9% |

| Total Investments | 110.3% |

| Other Assets & Liabilities, net | -10.3% |

| Net Assets | 100.0% |

| Ten Largest Holdings | (% of Total Net Assets) |

| Sunac China Holdings Ltd. | 1.3% |

| TravelSky Technology Ltd. — Class H | 1.2% |

| Kingboard Chemical Holdings Ltd. | 1.1% |

| Xinyi Glass Holdings Ltd. | 1.0% |

| China Lodging Group Ltd. ADR | 1.0% |

| Autohome, Inc. ADR | 1.0% |

| Yangzijiang Shipbuilding Holdings Ltd. | 1.0% |

| Sihuan Pharmaceutical Holdings Group Ltd. | 1.0% |

| Beijing Capital International Airport Company Ltd. — Class H | 0.9% |

| Sinopec Shanghai Petrochemical Company Ltd. — Class H | 0.9% |

| Top Ten Total | 10.4% |

“Ten Largest Holdings” excludes any temporary cash investments.

This graph compares a hypothetical $10,000 investment in the Fund, made at its inception, with a similar investment in the MSCI China Index. Results include the reinvestment of all dividends and capital gains. Past performance is no guarantee of future results. The MSCI China Index is a capitalization-weighted index that monitors the performance of stocks from the country of China. The index is unmanaged. It is not possible to invest directly in the MSCI China Index. Investment return and principal value will fluctuate with changes in market conditions and other factors and Fund shares, when redeemed, may be worth more or less than their original investment.

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 17 |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

FRN Guggenheim Frontier Markets ETF

| Fund Statistics | | | |

| Share Price | | $ | 13.74 |

| Net Asset Value | | $ | 13.76 |

| Discount to NAV | | | -0.15% |

| Net Assets ($000) | | $ | 63,834 |

| AVERAGE ANNUAL TOTAL RETURNS FOR THE |

| PERIOD ENDED MAY 31, 2017 |

| | | | | Since |

| | One | Three | Five | Inception |

| | Year | Year | Year | (06/12/08) |

| Guggenheim Frontier | | | | |

| Markets ETF | | | | |

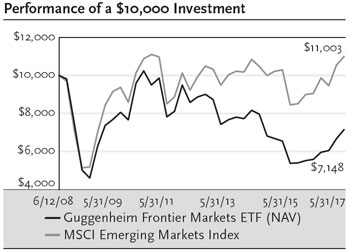

| NAV | 24.72% | -3.60% | -3.32% | -3.66% |

| Market | 26.20% | -3.77% | -3.52% | -3.67% |

| BNY Mellon | | | | |

| New Frontier | | | | |

| Index | 27.30% | -1.51% | -1.90% | -2.57% |

| MSCI Emerging | | | | |

| Markets | | | | |

| Index | 27.41% | 1.62% | 4.54% | 1.07% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Since inception returns assume a purchase of the Fund at the initial share price of $24.34 per share for share price returns or initial net asset value (NAV) of $24.34 per share for NAV returns. Returns for periods of less than one year are not annualized.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The referenced indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

Per the most recent prospectus, the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 1.28%. In the Financial Highlights section of this Annual Report, the Fund’s annualized net operating expense ratio was 0.70% while the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 1.17%. There is a contractual fee waiver currently in place for this Fund through December 31, 2019 to the extent necessary in keeping the Fund’s operating expense ratio from exceeding 0.65% of average net assets per year. Some expenses fall outside of this expense cap and actual expenses may be higher than 0.65%. Without this expense cap, actual returns would be lower. Please see the Financial Highlights for recent expense ratios.

| Country Diversification |

| | | % of Long-Term |

| Country | | Investments |

| Kuwait | | 13.3% |

| Morocco | | 9.9% |

| Pakistan | | 9.5% |

| Nigeria | | 9.4% |

| Romania | | 9.4% |

| Vietnam | | 9.1% |

| Argentina | | 8.3% |

| Other | | 31.1% |

| Total Long-Term Investments | | 100.0% |

| Ten Largest Holdings | | (% of Total Net Assets) |

| MercadoLibre, Inc. | | 6.3% |

| Guaranty Trust Bank plc | | 5.1% |

| Copa Holdings S.A. — Class A | | 4.9% |

| National Bank of Kuwait SAKP | | 3.5% |

| Aroundtown Property Holdings plc | | 3.4% |

| Banca Transilvania S.A. | | 3.3% |

| Safaricom Ltd. | | 3.0% |

| Nigerian Breweries plc | | 2.8% |

| Vietnam Dairy Products JSC | | 2.6% |

| YPF S.A. ADR | | 2.5% |

| Top Ten Total | | 37.4% |

“Ten Largest Holdings” excludes any temporary cash investments.

This graph compares a hypothetical $10,000 investment in the Fund, made at its inception, with a similar investment in the MSCI Emerging Markets Index. Results include the reinvestment of all dividends and capital gains. Past performance is no guarantee of future results. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. It is not possible to invest directly in the MSCI Emerging Market Index. Investment return and principal value will fluctuate with changes in market conditions and other factors and Fund shares, when redeemed, may be worth more or less than their original investment.

| |

| 18 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

HGI Guggenheim International Multi-Asset Income ETF

| Fund Statistics | | | |

| Share Price | | $ | 16.79 |

| Net Asset Value | | $ | 16.81 |

| Discount to NAV | | | -0.12% |

| Net Assets ($000) | | $ | 15,132 |

| AVERAGE ANNUAL TOTAL RETURNS FOR THE |

| PERIOD ENDED MAY 31, 2017 |

| | | | | Since |

| | One | Three | Five | Inception |

| | Year | Year | Year | (07/11/07) |

| Guggenheim | | | | |

| International | | | | |

| Multi-Asset | | | | |

| Income ETF | | | | |

| NAV | 18.09% | -1.49% | 6.29% | 0.23% |

| Market | 18.69% | -1.73% | 6.21% | 0.21% |

| Zacks International | | | | |

| Multi-Asset | | | | |

| Income | | | | |

| Index | 18.36% | -1.49% | 6.34% | 0.56% |

| MSCI EAFE | | | | |

| Index | 16.44% | 1.53% | 10.21% | 0.87% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Since inception returns assume a purchase of the Fund at the initial share price of $24.98 per share for share price returns or initial net asset value (NAV) of $24.98 per share for NAV returns. Returns for periods of less than one year are not annualized.

The MSCI EAFE Index measures the performance for a diverse range of global stock markets within Europe, Australasia and the Far East. The referenced index is unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

Per the most recent prospectus, the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 1.13%. In the Financial Highlights section of this Annual Report, the Fund’s annualized net operating expense ratio was 0.70% while the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 1.37%. There is a contractual fee waiver currently in place for this Fund through December 31, 2019 to the extent necessary in keeping the Fund’s operating expense ratio from exceeding 0.65% of average net assets per year. Some expenses fall outside of this expense cap and actual expenses may be higher than 0.65%. Without this expense cap, actual returns would be lower. Please see the Financial Highlights for recent expense ratios.

| Country Diversification |

| | | % of Long-Term |

| Country | | Investments |

| United States | | 15.1% |

| Japan | | 13.8% |

| United Kingdom | | 11.6% |

| France | | 7.9% |

| Cayman Islands | | 4.8% |

| China | | 4.0% |

| Netherlands | | 3.9% |

| Other | | 38.9% |

| Total Long-Term Investments | | 100.0% |

| Ten Largest Holdings | | (% of Total Net Assets) |

| QIWI plc ADR | | 2.3% |

| Huaneng Power International, Inc. ADR | | 2.1% |

| Man Wah Holdings Ltd. | | 2.0% |

| ChipMOS Technologies, Inc. | | 1.7% |

| Koninklijke KPN N.V. | | 1.5% |

| Hopewell Highway Infrastructure Ltd. | | 1.5% |

| Societe Generale S.A. | | 1.5% |

| BNP Paribas S.A. | | 1.4% |

| Lloyds Banking Group plc | | 1.4% |

| Braskem S.A. ADR | | 1.3% |

| Top Ten Total | | 16.7% |

“Ten Largest Holdings” excludes any temporary cash investments.

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 19 |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

HGI Guggenheim International Multi-Asset Income ETF continued

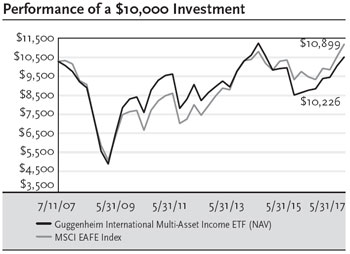

This graph compares a hypothetical $10,000 investment in the Fund, made at its inception, with a similar investment in the MSCI EAFE Index. Results include the reinvestment of all dividends and capital gains. Past performance is no guarantee of future results. The Morgan Stanley Capital International EAFE Index (“MSCI EAFE Index”) measures the performance for a diverse range of global stock markets within Europe, Australasia and the Far East. The referenced indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees, or expenses.

| |

| 20 l CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

CUT Guggenheim MSCI Global Timber ETF

| Fund Statistics | | | |

| Share Price | | $ | 27.52 |

| Net Asset Value | | $ | 27.57 |

| Discount to NAV | | | -0.18% |

| Net Assets ($000) | | $ | 190,203 |

| AVERAGE ANNUAL TOTAL RETURNS FOR THE |

| PERIOD ENDED MAY 31, 2017 | | |

| | | | | Since |

| | One | Three | Five | Inception |

| | Year | Year | Year | (11/09/07) |

| Guggenheim MSCI | | | | |

| Global Timber ETF | | | | |

| NAV | 19.09% | 5.00% | 13.93% | 3.00% |

| Market | 19.09% | 5.00% | 13.83% | 2.98% |

| MSCI ACWI IMI Timber | | | | |

| Select Capped | | | | |

| Index/Beacon | | | | |

| Global | | | | |

| Timber | | | | |

| Index | 19.23% | 5.17%1 | 14.42%1 | 4.08%1 |

| MSCI World | | | | |

| Index | 16.42% | 5.73% | 12.41% | 3.93% |

| S&P Global Timber & | | | | |

| Forestry | | | | |

| Index | 26.94% | 7.40% | 13.68% | 2.19% |

| STOXX® Europe | | | | |

| TMI Forestry & | | | | |

| Paper | | | | |

| Index | 42.58% | 14.96% | 24.99% | 5.88% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Since inception returns assume a purchase of the Fund at the initial share price of $24.91 per share for share price returns or initial net asset value (NAV) of $24.91 per share for NAV returns. Returns for periods of less than one year are not annualized.

The Morgan Stanley Capital International (MSCI) World Index measures performance from a diverse range of global stock markets, including the U.S., Canada, Europe, Australia, New Zealand, and the Far East.

The S&P Global Timber & Forestry Index is comprised of 25 of the largest publicly traded companies engaged in the ownership, management or the upstream supply chain of forests and timberlands. These may be forest products companies, timber REITs, paper products companies, paper packaging companies, or agricultural product companies that are engaged in the ownership, management or the upstream supply chain of forests and timberlands.

The STOXX® Europe TMI Forestry & Paper Index is a market capitalization weighted index of all companies in the Forestry & Paper sector of the STOXX Europe TMI index. Using the market standard ICB (Industry Classification Benchmark), companies with primary revenue sources from the Forestry & Paper sector are selected from the STOXX Europe TMI universe, which covers 95 percent of the free float market capitalization across 18 Western European countries (Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom).

The referenced indices are unmanaged and not available for direct investment. Index performance does not reflect transaction costs, fees or expenses.

Per the most recent prospectus, the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 0.75%. In the Financial Highlights section of this Annual Report, the Fund’s annualized net operating expense ratio was 0.57% while the Fund’s annualized gross operating expense ratio, gross of any fee waivers or expense reimbursements, was 0.70%. There is a contractual fee waiver currently in place for this Fund through December 31, 2019 to the extent necessary in keeping the Fund’s operating expense ratio from exceeding 0.55% of average net assets per year. Some expenses fall outside of this expense cap and actual expenses may be higher than 0.55%. Without this expense cap, actual returns would be lower. Please see the Financial Highlights for recent expense ratios.

| Country Diversification |

| | | % of Long-Term |

| Country | | Investments |

| United States | | 44.7% |

| Finland | | 11.1% |

| South Africa | | 8.6% |

| Australia | | 6.3% |

| Japan | | 5.1% |

| Canada | | 4.7% |

| Brazil | | 4.3% |

| Other | | 15.2% |

| Total Long-Term Investments | | 100.0% |

| 1 | Benchmark returns reflect the blended return of the Beacon Global Timber Index from 11/09/07 – 05/19/16 and the return of the MSCI ACWI IMI Timber Select Capped Index from 05/20/16 – 05/31/17. |

| |

| CLAYMORE EXCHANGE-TRADED FUND TRUST 2 ANNUAL REPORT l 21 |

| PERFORMANCE REPORT AND FUND PROFILE (Unaudited) continued | May 31, 2017 |

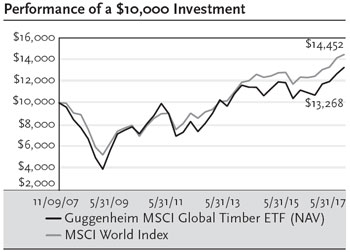

CUT Guggenheim MSCI Global Timber ETF continued

| Ten Largest Holdings | (% of Total Net Assets) |

| International Paper Co. | 5.1% |

| UPM-Kymmene Oyj | 5.1% |

| Weyerhaeuser Co. | 5.0% |

| Amcor Ltd. | 5.0% |

| WestRock Co. | 5.0% |

| Packaging Corporation of America | 4.8% |

| Mondi plc | 4.8% |

| Sealed Air Corp. | 4.3% |

| Avery Dennison Corp. | 3.8% |

| Stora Enso Oyj — Class R | 3.5% |

| Top Ten Total | 46.4% |

“Ten Largest Holdings” excludes any temporary cash investments.