GUGGENHEIMINVESTMENTS.COM/GOF

... YOUR WINDOW TO THE LATEST, MOST UP-TO-DATE INFORMATION ABOUT GUGGENHEIM STRATEGIC OPPORTUNITIES FUND

The shareholder report you are reading right now is just the beginning of the story. Online at guggenheiminvestments.com/gof, you will find:

• Daily, weekly and monthly data on share prices, net asset values, distributions and more

• Portfolio overviews and performance analyses

• Announcements, press releases and special notices

• Fund and adviser contact information

Guggenheim Partners Investment Management, LLC and Guggenheim Funds Investment Advisors, LLC are continually updating and expanding shareholder information services on the Fund’s website in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed and the results of our efforts. It is just one more small way we are working to keep you better informed about your investment in the Fund.

DEAR SHAREHOLDER

We thank you for your investment in the Guggenheim Strategic Opportunities Fund (the “Fund”). This report covers the Fund’s performance for the 12-month period ended May 31, 2019.

The Fund’s investment objective is to maximize total return through a combination of current income and capital appreciation. The Fund pursues a relative value-based investment philosophy. The Fund’s sub-adviser seeks to combine a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies.

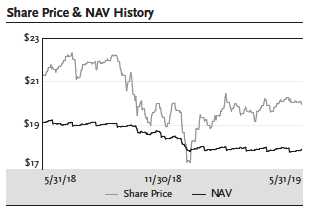

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the 12-month period ended May 31, 2019, the Fund provided a total return based on market price of 4.94% and a total return based on NAV of 5.43%. As of May 31, 2019, the Fund’s market price of $19.96 represented a premium of 11.45% to its NAV of $17.91. NAV return includes the deduction of management fees, operating expenses, and all other Fund expenses.

Past performance is not a guarantee of future results. All NAV returns include the deduction of management fees, operating expenses, and all other Fund expenses. The market price of the Fund’s shares fluctuates from time to time, and it may be higher or lower than the Fund’s NAV.

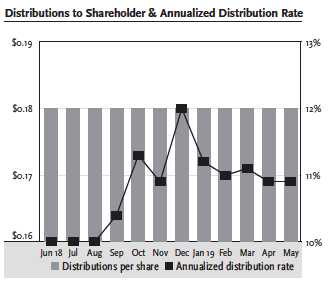

From June 2018 through May 2019, the Fund paid a monthly distribution of $0.1821 per share. The latest distribution represents an annualized distribution rate of 10.95% based on the Fund’s closing market price of $19.96 on May 31, 2019. The Fund’s distribution rate is not constant and the amount of distributions, when declared by the Fund’s Board of Trustees, is subject to change based on the performance of the Fund. Please see Note 2(f) on page 57 for more information on distributions for the period.

Guggenheim Funds Investment Advisors, LLC (the “Adviser”) serves as the investment adviser to the Fund. Guggenheim Partners Investment Management, LLC (“GPIM” or the “Sub-Adviser”) serves as the Fund’s investment sub-adviser and is responsible for the management of the Fund’s portfolio of investments. Each of the Adviser and the Sub-Adviser is an affiliate of Guggenheim Partners, LLC (“Guggenheim”), a global diversified financial services firm.

We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 93 of this report. When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the monthly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at the greater of NAV per share or 95% of the market price per share. The DRIP provides a cost-effective means to accumulate additional shares and enjoy the benefits of compounding returns over time. Since the Fund endeavors to maintain a stable monthly distribution, the DRIP effectively provides an income averaging technique which causes shareholders to accumulate a larger number of Fund shares when the market price is depressed than when the price is higher.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 3| | |

DEAR SHAREHOLDER (Unaudited) continued | May 31, 2019 |

To learn more about the Fund’s performance and investment strategy, we encourage you to read the Questions & Answers section of this report, which begins on page 5. You’ll find information on Guggenheim’s investment philosophy, views on the economy and market environment, and detailed information about the factors that impacted the Fund’s performance.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at guggenheiminvestments.com/gof.

Sincerely,

Guggenheim Funds Investment Advisors, LLC

Guggenheim Strategic Opportunities Fund

June 30, 2019

4 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

QUESTIONS & ANSWERS (Unaudited) | May 31, 2019 |

Guggenheim Strategic Opportunities Fund (“Fund”) is managed by a team of seasoned professionals at Guggenheim Partners Investment Management, LLC (“GPIM”). This team includes B. Scott Minerd, Chairman of Guggenheim Investments and Global Chief Investment Officer; Anne B. Walsh, CFA, JD, Senior Managing Director and Chief Investment Officer, Fixed Income; Steven H. Brown, CFA, Managing Director and Portfolio Manager; and Adam Bloch, Managing Director and Portfolio Manager. In the following interview, the investment team discusses the market environment and the Fund’s performance for the 12-month period ended May 31, 2019.

What is the Fund’s investment objective and how is it pursued?

The Fund seeks to maximize total return through a combination of current income and capital appreciation. The Fund pursues a relative value-based investment philosophy, which utilizes quantitative and qualitative analysis.

The Fund seeks to combine a credit-managed fixed-income portfolio with access to a diversified pool of alternative investments and equity strategies. The Fund seeks to achieve its investment objective by investing in a wide range of fixed-income and other debt and senior-equity securities (“Income Securities”) selected from a variety of credit qualities and sectors, including, but not limited to, corporate bonds, loans and loan participations, structured finance investments, U.S. government and agency securities, mezzanine and preferred securities and convertible securities, and in common stocks, limited liability company interests, trust certificates, and other equity investments (“Common Equity Securities”), exposure to which is obtained primarily by investing in exchange-traded funds (“ETFs”) that Guggenheim believes offer attractive yield and/or capital appreciation potential, including employing a strategy of writing (selling) covered call and put options on such equities. Guggenheim believes the volatility of the Fund can be reduced by diversifying across a large number of sectors and securities, some of which historically have not been highly correlated to one another.

Under normal market conditions:

| • | The Fund may invest without limitation in fixed-income securities rated below investment grade (commonly referred to as “junk bonds”); the Fund may invest in below-investment grade income securities of any rating; |

| • | The Fund may invest up to 20% of its total assets in non-U.S. dollar denominated fixed-income securities of corporate and governmental issuers located outside the U.S., including up to 10% of total assets in fixed-income securities of issuers located in emerging markets; |

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 5| | |

QUESTIONS & ANSWERS (Unaudited) continued | May 31, 2019 |

| • | The Fund may invest up to 50% of its total assets in common equity securities, and the Fund may invest in ETFs or other investment funds that track equity market indices and/or through derivative instruments that replicate the economic characteristics of exposure to Common Equity Securities; and |

| • | The Fund may invest up to 30% of its total assets in investment funds that primarily hold (directly or indirectly) investments in which the Fund may invest directly, of which amount up to 30% of the Fund’s total assets may be invested in investment funds that are registered as investment companies under the Investment Company Act of 1940 (the “1940 Act”) to the extent permitted by applicable law and related interpretations of the staff of the U.S. Securities and Exchange Commission. |

Guggenheim’s process for determining whether to buy a security is a collaborative effort between various groups including: (i) economic research, which focus on key economic themes and trends, regional and country-specific analysis, and assessments of event-risk and policy impacts on asset prices, (ii) the Portfolio Construction Group, which utilize proprietary portfolio construction and risk modeling tools to determine allocation of assets among a variety of sectors, (iii) its Sector Specialists, who are responsible for identifying investment opportunities in particular securities within these sectors, including the structuring of certain securities directly with the issuers or with investment banks and dealers involved in the origination of such securities, and (iv) portfolio managers, who determine which securities best fit the Fund based on the Fund’s investment objective and top-down sector allocations. In managing the Fund, Guggenheim uses a process for selecting securities for purchase and sale that is based on intensive credit research and involves extensive due diligence on each issuer, region and sector. Guggenheim also considers macroeconomic outlook and geopolitical issues.

The Fund may use financial leverage to finance the purchase of additional securities. Although financial leverage may create an opportunity for increased return for shareholders, it also results in additional risks and can magnify the effect of any losses. There is no assurance that the strategy will be successful. If income and gains earned on securities purchased with the financial leverage proceeds are greater than the cost of the financial leverage, common shareholders’ return will be greater than if financial leverage had not been used. Conversely, if the income or gains from the securities purchased with the proceeds of financial leverage are less than the cost of the financial leverage, common shareholders’ return will be less than if financial leverage had not been used.

6 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

QUESTIONS & ANSWERS (Unaudited) continued | May 31, 2019 |

What were the significant events over the 12-month period ended May 31, 2019 affecting Guggenheim’s view of the economy and market environment?

The U.S. Federal Reserve (“Fed”) was on a preset path to continue tightening monetary policy into 2019 until a confluence of factors drove market weakness in the fourth quarter of 2018, including a bear market in oil, risks of higher import tariffs, regulator warnings about the excesses in corporate credit, and concerns about tighter monetary policy. Adding to the pile was a government shutdown that showed no sign of resolution heading into 2019. As these events exposed the dying tailwinds to growth, the market awoke to the fact that there may be too much leverage in the system to handle an unfavorable economic environment. Risk assets were punished, with equity indexes almost entering a bear market and credit spreads moving sharply wider. The Fed initially failed to reassure markets that it would stem a collapse in asset prices, but the market seems to have forced the Fed’s hand.

A dovish pivot by both the Fed and the European Central Bank to start 2019 alleviated the perceived risk that the central banks were headed for irreversible policy mistakes and may even support a rebound in economic growth in both regions later this year. In the 12 months ended May 31, 2019, the yield on the two-year Treasury fell 50 basis points, from 2.4% to 1.9% and the yield on the 10-year Treasury fell from 2.9% to 2.1%.

Growing uncertainty around import tariffs has weighed on consumers’ outlook for income, business, and labor market conditions and has caused growth projections to slow. Consequently, by May 2019 markets had priced in multiple rate cuts by the Fed in 2019 and through 2020, as the Fed has made extending the business cycle a priority. Investors may be tempted to go down in quality in anticipation of a Fed-induced rally in credit. However, history suggests that credit spreads tend to widen when the Fed is lowering interest rates. Our posture remains defensive in the face of likely rate cuts starting in July.

How did the Fund perform for the 12 months ended May 31, 2019?

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the 12-month period ended May 31, 2019, the Fund provided a total return based on market price of 4.94% and a total return based on NAV of 5.43%. As of May 31, 2019, the Fund’s market price of $19.96 represented a premium of 11.45% to its NAV of $17.91. NAV return includes the deduction of management fees, operating expenses, and all other Fund expenses. As of May 31, 2018, the Fund’s market price of $21.29 represented a premium of 11.35% to its NAV of $19.12. The market value of the Fund’s shares fluctuates from time to time and may be higher or lower than the Fund’s NAV. Past performance is not a guarantee of future results.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 7| | |

QUESTIONS & ANSWERS (Unaudited) continued | May 31, 2019 |

What were the Fund’s distributions?

From June 2018 through May 2019, the Fund paid a monthly distribution of $0.1821 per share. The latest distribution represents an annualized distribution rate of 10.95% based on the Fund’s closing market price of $19.96 on May 31, 2019. The Fund’s distribution rate is not constant and the amount of distributions, when declared by the Fund’s Board of Trustees, is subject to change based on the performance of the Fund. Please see Note 2(f) on page 57 for more information on distributions for the period.

For the year ended May 31, 2019, approximately 55.0% of the distributions were characterized as ordinary income, 3.4% were characterized as long-term capital gains and 41.6% were characterized as a return of capital. The Fund will provide a Form 1099-DIV each calendar year that will explain the character of these distributions for U.S. federal income tax purposes.

How did other markets perform in this environment for the 12-month period ended May 31, 2019?

| | |

Index | Total Return |

| Bloomberg Barclays U.S. Aggregate Bond Index | 6.40% |

| Bloomberg Barclays U.S. Aggregate Bond 1-3 Year Index | 3.72% |

| Bloomberg Barclays U.S. Corporate High Yield Index | 5.51% |

| Credit Suisse Leveraged Loan Index | 4.02% |

| ICE Bank of America Merrill Lynch Asset Backed Security Master BBB-AA Index | 5.60% |

| S&P 500 Index | 3.78% |

Discuss performance over the period.

During the period, the Fund saw positive performance primarily attributable to the portfolio’s carry, despite broadly wider spreads over the period. Carry refers to the income received from portfolio investments over a defined period. Carry from bank loans, high yield corporate bonds, and nonAgency residential mortgage backed securities (“non-Agency RMBS”) were the largest drivers of return.

We are cognizant of the growing risk of negative credit events related to the turn in the credit cycle. We remain focused on limiting spread duration to help protect against price volatility. Volatility spiked in the fourth quarter of 2018 amid risks of higher import tariffs, warnings about the excesses in corporate credit, and concerns about tighter monetary policy. The Fund has gradually pared back its allocation to credit and high yield in particular, while increasing allocation to higher quality investments.

Bank loans contributed to overall performance for the period primarily via carry, but technical dynamics have changed given the Fed’s pivot.

8 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

QUESTIONS & ANSWERS (Unaudited) continued | May 31, 2019 |

High yield corporate bonds made a round trip from late 2018 to early 2019, aided by the Fed’s dovish pivot in December and a benign default environment. We reduced our exposure though as uncertainty in later stages of the credit cycle has been accompanied by higher volatility in lower-quality assets. With spreads still near cycle tights, history suggests returns could be more tepid in the upcoming months, with risks skewed to the downside.

The Fund increased its allocation to non-Agency RMBS. We hold a constructive view on the sector as healthy housing fundamentals and improving borrower performance support the sector. Strong demand and muted new home construction have pushed inventories to historically low levels, in turn boosting home values. Against this backdrop, ongoing credit curing of legacy mortgage-backed securities borrowers should result in improved prepayments and loss rates on bonds.

Collateralized loan obligation (“CLO”) debt also added to the Fund’s return. Credit performance in underlying bank loans remains solid, though cyclical and idiosyncratic risk concerns are increasing.

Asset-backed securities (“ABS”) remained stable and performed well during the period, led by Aircraft ABS where spreads were largely unchanged.

The covered call allocation marginally detracted from total return over the 12-month period. The allocation was reduced in May in line with our broader plan to protect the portfolio and shareholders from future drawdowns.

What was the impact of derivatives on Fund performance?

The Fund uses derivatives for its covered call strategy and for various hedging purposes, such as currency forward contracts to fully hedge exchange rate risk in the purchase of government securities of foreign countries. It also uses them to obtain exposure to indexes that track various equity market sectors.

Index futures contributed to performance for the period. The covered call strategy detracted from performance during the period.

Currency forward contracts are used to fully hedge FX rate movement on non-USD denominated positions in the portfolio. The appreciation in foreign-denominated sovereign debt assets more than offset the cost of hedging these assets in U.S. dollar terms.

The Fund also purchased a credit hedge via credit default swaps in Q4 2018 to reduce portfolio spread duration and help protect shareholders from a drawdown. As spreads tightened in 2019, the credit hedge detracted from performance.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 9| | |

QUESTIONS & ANSWERS (Unaudited) continued | May 31, 2019 |

Discuss the Fund’s approach to duration.

Although the Fund has no set policy regarding portfolio duration or maturity, the Fund maintained a generally low-duration at period’s end.

Discuss the Fund’s use of leverage.

In light of our defensive posturing, the Fund employed virtually no leverage over the period as the Fund started with leverage of 0.30% of managed assets (including the proceeds of leverage) at May 31, 2018 and ended with zero. The minimal use of leverage during this period had a negligible impact on the Fund’s return. The purpose of leverage (borrowing and reverse repurchase agreements) is to fund the purchase of additional securities that may provide increased income and potentially greater appreciation to common shareholders than could be achieved from an unlevered portfolio. Leverage results in greater NAV volatility and entails more downside risk than an unleveraged portfolio.

Guggenheim employs leverage through two vehicles: reverse repurchase agreements, under which the Fund temporarily transfers possession of portfolio securities and receives cash which can be used for additional investments, and a committed financing facility through a leading financial institution.

There is no guarantee that the Fund’s leverage strategy will be successful. The Fund’s use of leverage may cause the Fund’s NAV and market price of common shares to be more volatile and can magnify the effect of any losses.

Index Definitions

Indices are unmanaged and reflect no expenses. It is not possible to invest directly in an index.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including U.S. Treasuries, government-related and corporate securities, mortgage-backed securities or “MBS” (agency fixed-rate and hybrid adjustable-rate mortgage, or “ARM”, pass-throughs), ABS, and commercial mortgage-backed securities (“CMBS”) (agency and non-agency).

The Bloomberg Barclays U.S. Aggregate Bond 1-3 Year Index measures the performance of publicly issued investment grade corporate, U.S. Treasury and government agency securities with remaining maturities of one to three years.

The Bloomberg Barclays U.S. Corporate High Yield Index measures the U.S. dollar-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB +/BB + or below.

10 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

QUESTIONS & ANSWERS (Unaudited) continued | May 31, 2019 |

The Credit Suisse Leveraged Loan Index is an index designed to mirror the investable universe of the U.S.-dollar-denominated leveraged loan market.

The ICE Bank of America Merrill Lynch Asset Backed Security Master BBB-AA Index is a subset of The ICE BofA/ML U.S. Fixed Rate Asset Backed Securities Index including all securities rated AA1 through BBB3, inclusive.

The Standard & Poor’s 500 (“S&P 500”) Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad economy, representing all major industries and is considered a representation of the U.S. stock market.

Risks and Other Considerations

Investing involves risk, including the possible loss of principal and fluctuation of value. The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are expressed for informational purposes only and are subject to change at any time, based on market and other conditions, and may not come to pass. These views may differ from views of other investment professionals at Guggenheim and should not be construed as research, investment advice or a recommendation of any kind regarding the fund or any issuer or security, do not constitute a solicitation to buy or sell any security and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation or particular needs of any specific investor.

The views expressed in this report may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass. Actual results or events may differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include general economic conditions such as inflation, recession and interest rates.

There can be no assurance that the Fund will achieve its investment objectives or that any investment strategies or techniques discussed herein will be effective. The value of the Fund will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value.

As part of its investment strategy, the Fund utilizes short sales and a variety of derivative instruments. These investments involve, to varying degrees, elements of market risk and risks in excess of amounts recognized in the Statement of Assets and Liabilities. Valuation and accounting treatment of these instruments can be found under Significant Accounting Policies in Note 2 of these Notes to Financial Statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 11| | |

QUESTIONS & ANSWERS (Unaudited) continued | May 31, 2019 |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown.

Please see guggenheiminvestments.com/gof for a detailed discussion of the Fund’s risks and considerations.

This material is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

12 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

FUND SUMMARY (Unaudited) | May 31, 2019 |

| | |

Fund Statistics | |

| Share Price | $19.96 |

| Net Asset Value | $17.91 |

| Premium to NAV | 11.45% |

| Net Assets ($000) | $641,825 |

AVERAGE ANNUAL TOTAL RETURNS FOR THE

PERIOD ENDED MAY 31, 2019

| | | | | |

| | One | Three | Five | Ten |

| | Year | Year | Year | Year |

| Guggenheim Strategic Opportunities Fund | | | | |

| NAV | 5.43% | 13.02% | 9.13% | 15.68% |

| Market | 4.94% | 16.61% | 9.99% | 17.61% |

Performance data quoted represents past performance, which is no guarantee of future results and current performance may be lower or higher than the figures shown. All NAV returns include the deduction of management fees, operating expenses and all other Fund expenses. The deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares is not reflected in the total returns. For the most recent month-end performance figures, please visit guggenheiminvestments.com/gof. The investment return and principal value of an investment will fluctuate with changes in market conditions and other factors so that an investor’s shares, when sold, may be worth more or less than their original cost.

| | |

Ten Largest Holdings | (% of Total Net Assets) |

| Government of Japan, 07/01/19 | 3.2% |

| Federative Republic of Brazil, 10/01/19 | 1.7% |

| Federative Republic of Brazil, 01/01/20 | 1.0% |

| Government of Japan, 07/08/19 | 0.9% |

| TSGE, 6.25% | 0.8% |

| Lehman XS Trust Series, 2.61% | 0.8% |

| LSTAR Securities Investment Trust, 4.19% | 0.8% |

| Golub Capital Partners CLO Ltd., 4.67% | 0.7% |

| AIM Aviation Finance Ltd., 5.07% | 0.7% |

| Encore Capital Group, Inc., 5.63% | 0.6% |

| Top Ten Total | 11.2% |

“Ten Largest Holdings” excludes any temporary cash or derivative investments.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 13| | |

FUND SUMMARY (Unaudited) continued | May 31, 2019 |

| | |

Portfolio Breakdown | % of Net Assets |

Investments | |

| Senior Floating Rate Interests | 36.1% |

| Asset-Backed Securities | 18.2% |

| Corporate Bonds | 15.3% |

| Collateralized Mortgage Obligations | 12.5% |

| Foreign Government Debt | 8.2% |

| U.S. Treasury Bills | 4.2% |

| Money Market Fund | 3.0% |

| Other | 4.2% |

Total Investments | 101.7% |

| Corporate Bonds Sold Short | -0.6% |

| Call Options Written | 0.0%* |

| Put Options Written | 0.0%* |

| Other Assets & Liabilities, net | -1.1% |

Net Assets | 100.0% |

Holdings diversification and holdings are subject to change daily. For more information, please visit guggenheiminvestments.com/gof. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results.

* Less than 0.1%.

14 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

FUND SUMMARY (Unaudited) continued | May 31, 2019 |

Portfolio breakdown is subject to change daily. For more information, please visit guggenheiminvestments.com/gof. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results. All or a portion of the above distributions may be characterized as a return of capital. For the year ended May 31, 2019, 55.0% of the distributions were characterized as ordinary income, 3.4% of the distributions were categorized as long-term capital gains and 41.6% of the distributions were characterized as return of capital.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 15| | |

FUND SUMMARY (Unaudited) continued | May 31, 2019 |

Portfolio Composition by Quality Rating1

| | |

| | % of Total |

Rating | Investments |

Investments | |

| AAA | 2.0% |

| AA | 0.4% |

| A | 3.3% |

| BBB | 6.0% |

| BB | 7.8% |

| B | 17.6% |

| CCC | 2.4% |

| CC | 1.9% |

| D | 0.1% |

NR2 | 44.5% |

Other Instruments | |

| Other | 14.0% |

Total Investments: | 100.0% |

| | |

| 1 | Source: BlackRock Solutions. Credit quality ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest). All rated securities have been rated by Moody’s, Standard & Poor’s (“S&P”), or Fitch, each of which is a Nationally Recognized Statistical Rating Organization (“NRSRO”). For purposes of this presentation, when ratings are available from more than one agency, the highest rating is used. Guggenheim Investments has converted Moody’s and Fitch ratings to the equivalent S&P rating. Security ratings are determined at the time of purchase and may change thereafter. |

| 2 | NR securities do not necessarily indicate low credit quality. |

16 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS | May 31, 2019 |

| | | |

| | Shares | Value |

| |

COMMON STOCKS† – 0.4% | | |

Utilities – 0.1% | | |

TexGen Power LLC†† | 22,219 | $ 870,252 |

| |

Consumer, Non-cyclical – 0.1% | | |

Chef Holdings, Inc.*,†††,1 | 4,789 | 602,648 |

Targus Group International Equity, Inc.†††,1,2 | 12,989 | 28,515 |

Total Consumer, Non-cyclical | | 631,163 |

| |

Consumer, Cyclical – 0.1% | | |

ATD New Holdings, Inc.*,†† | 13,571 | 434,272 |

| |

Energy – 0.1% | | |

SandRidge Energy, Inc.*,14 | 39,565 | 272,603 |

| Approach Resources, Inc.* | 14,929 | 3,192 |

Titan Energy LLC*,14 | 9,603 | 125 |

Total Energy | | 275,920 |

| |

Communications – 0.0% | | |

Cengage Learning Acquisitions, Inc.*,†† | 11,126 | 127,026 |

| |

Technology – 0.0% | | |

Qlik Technologies, Inc. – Class A*,†††,1 | 56 | 62,173 |

Qlik Technologies, Inc.*,†††,1 | 3,600 | – |

Qlik Technologies, Inc. – Class B*,†††,1 | 13,812 | – |

Total Technology | | 62,173 |

| |

Industrial – 0.0% | | |

BP Holdco LLC*,†††,1,2 | 55,076 | 19,447 |

Vector Phoenix Holdings, LP*,†††,1 | 55,076 | 4,609 |

Total Industrial | | 24,056 |

Total Common Stocks | | |

| (Cost $3,320,312) | | 2,424,862 |

| |

PREFERRED STOCKS†† – 0.3% | | |

Financial – 0.2% | | |

Public Storage 5.40%3 | 41,000 | 1,048,370 |

AgriBank FCB 6.88%3,5 | 4,000 | 423,000 |

Total Financial | | 1,471,370 |

| |

Industrial – 0.1% | | |

Lytx Holdings, LLC 11.50%†††,1,3 | 559 | 559,157 |

Total Preferred Stocks | | |

| (Cost $1,902,157) | | 2,030,527 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 17| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Shares | Value |

| |

WARRANTS††† – 0.0% | | |

Lytx, Inc.*,1 | 26 | $ 131 |

Total Warrants | | |

| (Cost $–) | | 131 |

| |

MONEY MARKET FUND† – 3.0% | | |

Dreyfus Treasury Securities Cash Management – Institutional Shares 2.24%6 | 19,089,706 | 19,089,706 |

Total Money Market Fund | | |

| (Cost $19,089,706) | | 19,089,706 |

| | Face | |

| | Amount~ | |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% | | |

Industrial – 8.3% | | |

| Alion Science & Technology Corp. | | |

| 6.94% (1 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 08/19/21 | 3,341,940 | 3,346,117 |

| Dynasty Acquisition Co. | | |

| 6.60% (3 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 04/06/26 | 3,000,000 | 3,004,679 |

| Tronair Parent, Inc. | | |

| 7.56% (1 Month USD LIBOR + 4.75% and 12 Month USD LIBOR + 4.75%, | | |

| Rate Floor: 5.75%) due 09/08/23 | 3,135,878 | 2,916,367 |

| PT Intermediate Holdings III LLC | | |

| 6.50% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 12/09/24 | 2,582,783 | 2,485,929 |

| 10.50% (1 Month USD LIBOR + 8.00%, Rate Floor: 9.00%) due 12/08/25 | 400,000 | 384,000 |

| American Bath Group LLC | | |

| 6.85% (3 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 09/30/23 | 2,694,647 | 2,677,806 |

| Capstone Logistics | | |

| 6.94% (1 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 10/07/21 | 2,613,814 | 2,592,041 |

| ILPEA Parent, Inc. | | |

| 7.19% (1 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 03/02/23 | 2,548,726 | 2,529,610 |

| WP CPP Holdings LLC | | |

| 6.34% (1 Month USD LIBOR + 3.75% and 3 Month USD LIBOR + 3.75%, | | |

| Rate Floor: 4.75%) due 04/30/25 | 2,368,100 | 2,366,134 |

| STS Operating, Inc. (SunSource) | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 12/11/24 | 2,063,943 | 2,050,177 |

| Tank Holdings Corp. | | |

| 6.68% (1 Month USD LIBOR + 4.00%, 3 Month USD LIBOR + 4.00% and | | |

| 12 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 03/26/26 | 2,000,000 | 2,003,500 |

| Sundyne Us Purchaser, Inc. | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 05/15/26 | 2,000,000 | 1,995,000 |

| II-VI Incorporated | | |

| due 05/07/26 | 2,000,000 | 1,983,760 |

| Transcendia Holdings, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 05/30/24 | 1,970,063 | 1,733,655 |

| Bioplan / Arcade | | |

| 7.19% (1 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 09/23/21 | 1,862,931 | 1,730,197 |

See notes to financial statements.

18 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Industrial – 8.3% (continued) | | |

| Foundation Building Materials Holding Company LLC | | |

| 5.44% (1 Month USD LIBOR + 3.00%, Rate Floor: 3.00%) due 08/13/25 | 1,745,625 | $ 1,723,805 |

| API Holdings III Corp. | | |

| 6.70% (3 Month USD LIBOR + 4.25%, Rate Floor: 4.25%) due 05/11/26 | 1,600,000 | 1,594,000 |

| National Technical | | |

8.74% (1 Month USD LIBOR + 6.25%, Rate Floor: 7.25%) due 06/12/21†††,1 | 1,380,703 | 1,335,830 |

| Avison Young (Canada), Inc. | | |

| 7.54% (1 Month USD LIBOR + 5.00%, 3 Month USD LIBOR + 5.00% and | | |

| 2 Month USD LIBOR + 5.00%, Rate Floor: 5.00%) due 01/31/26 | 1,296,750 | 1,270,815 |

| Charter Nex US, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 05/16/24 | 1,200,000 | 1,195,800 |

| Savage Enterprises LLC | | |

| 6.97% (1 Month USD LIBOR + 4.50%, Rate Floor: 4.50%) due 08/01/25 | 1,140,750 | 1,143,602 |

| Duran, Inc. | | |

| 6.63% (3 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 12/20/24 | 548,505 | 532,050 |

| 6.58% (3 Month USD LIBOR + 4.00%, Rate Floor: 4.75%) due 03/29/24 | 500,285 | 485,276 |

| Bhi Investments LLC | | |

11.63% (3 Month USD LIBOR + 8.75%, Rate Floor: 9.75%) due 02/28/25†††,1 | 1,000,000 | 987,500 |

| Diversitech Holdings, Inc. | | |

| 10.10% (3 Month USD LIBOR + 7.50%, Rate Floor: 8.50%) due 06/02/25 | 1,000,000 | 977,500 |

| Pelican Products, Inc. | | |

| 5.97% (1 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 05/01/25 | 992,500 | 972,650 |

| Hillman Group, Inc. | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 05/30/25 | 994,987 | 968,620 |

| Arctic Long Carriers | | |

| 6.93% (1 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 05/18/23 | 982,500 | 950,569 |

| ProAmpac PG Borrower LLC | | |

| 11.02% (3 Month USD LIBOR + 8.50%, Rate Floor: 9.50%) due 11/18/24 | 1,000,000 | 942,500 |

| YAK MAT (YAK ACCESS LLC) | | |

| 12.44% (1 Month USD LIBOR + 10.00%, Rate Floor: 10.00%) due 07/10/26 | 1,000,000 | 862,500 |

| Fortis Solutions Group LLC | | |

6.93% (1 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 12/15/23†††,1 | 585,904 | 585,904 |

6.95% (1 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 12/15/23†††,1 | 241,045 | 241,045 |

| SLR Consulting Ltd. | | |

6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 06/23/25†††,1 | 793,980 | 775,342 |

6.43% (1 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 05/23/25†††,1 | 21,800 | 21,288 |

| Thermon Group Holdings, Inc. | | |

| 6.24% (1 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 10/30/24 | 750,342 | 751,279 |

| TAMKO Building Products, Inc. | | |

| due 05/31/26 | 750,000 | 746,250 |

| Dimora Brands, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 08/24/24 | 486,563 | 473,791 |

| Hayward Industries, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 08/05/24 | 295,987 | 288,588 |

Total Industrial | | 53,625,476 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 19| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Consumer, Cyclical – 7.7% | | |

| Accuride Corp. | | |

| 7.85% (3 Month USD LIBOR + 5.25%, Rate Floor: 6.25%) due 11/17/23 | 3,394,063 | $ 3,046,171 |

| EG Finco Ltd. | | |

| 6.60% (3 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 02/07/25 | 2,772,006 | 2,718,867 |

| 8.75% (3 Month EURIBOR + 7.75%, Rate Floor: 8.75%) due 04/20/26 | EUR 249,505 | 280,233 |

| Titan AcquisitionCo New Zealand Ltd. | | |

| 6.83% (3 Month USD LIBOR + 4.25%, Rate Floor: 4.25%) due 05/01/26 | 2,800,000 | 2,796,500 |

| Big Jack Holdings LP | | |

| 5.69% (1 Month USD LIBOR + 3.25%, Rate Floor: 4.25%) due 04/05/24 | 2,136,965 | 2,078,198 |

| CH Holding Corp. | | |

| 5.97% (1 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 02/05/26 | 2,000,000 | 2,002,500 |

| K & N Parent, Inc. | | |

| 7.19% (1 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 10/20/23 | 1,947,900 | 1,917,065 |

| Boot Barn Holdings, Inc. | | |

| 7.10% (3 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 06/29/23 | 1,765,000 | 1,756,175 |

| Midas Intermediate Holdco II LLC | | |

| 5.35% (3 Month USD LIBOR + 2.75%, Rate Floor: 3.75%) due 08/18/21 | 1,783,028 | 1,729,538 |

| BBB Industries, LLC | | |

| 6.97% (1 Month USD LIBOR + 4.50%, Rate Floor: 4.50%) due 08/01/25 | 1,642,747 | 1,636,587 |

| Blue Nile, Inc. | | |

| 9.02% (3 Month USD LIBOR + 6.50%, Rate Floor: 7.50%) due 02/17/23 | 1,825,000 | 1,606,000 |

| BGIS (BIFM CA Buyer, Inc.) | | |

| due 05/27/26 | 1,600,000 | 1,596,000 |

| CPI Acquisition, Inc. | | |

| 7.35% (3 Month USD LIBOR + 4.50%, Rate Floor: 6.50%) due 08/17/22 | 2,021,782 | 1,589,626 |

| Touchtunes Interactive Network | | |

| 7.19% (1 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 05/28/21 | 1,561,797 | 1,548,131 |

| Power Solutions (Panther) | | |

| 5.93% (1 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 04/30/26 | 1,550,000 | 1,537,414 |

| 1-800 Contacts | | |

| 5.69% (1 Month USD LIBOR + 3.25%, Rate Floor: 4.25%) due 01/22/23 | 1,546,301 | 1,528,905 |

| Comet Bidco Ltd. | | |

| 7.52% (3 Month USD LIBOR + 5.00%, Rate Floor: 6.00%) due 09/30/24 | 1,485,038 | 1,462,762 |

| EnTrans International, LLC | | |

| 8.44% (1 Month USD LIBOR + 6.00%, Rate Floor: 6.00%) due 11/01/24 | 1,471,875 | 1,449,797 |

| SHO Holding I Corp. | | |

| 7.58% (3 Month USD LIBOR + 5.00%, Rate Floor: 6.00%) due 10/27/22 | 1,202,542 | 1,136,402 |

| 6.45% (2 Month USD LIBOR + 4.00% and 3 Month USD LIBOR + 4.00%, | | |

Rate Floor: 4.00%) due 10/27/21†††,1 | 314,000 | 296,187 |

| Zephyr Bidco Ltd. | | |

| 8.23% (1 Month GBP LIBOR + 7.50%, Rate Floor: 7.50%) due 07/23/26 | GBP 1,100,000 | 1,377,841 |

| Alexander Mann | | |

| 7.93% (1 Month USD LIBOR + 5.50%, Rate Floor: 5.50%) due 08/11/25 | 1,300,000 | 1,248,000 |

| WESCO | | |

6.68% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 06/14/24†††,1 | 1,167,500 | 1,162,616 |

See notes to financial statements.

20 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Consumer, Cyclical – 7.7% (continued) | | |

| Apro LLC | | |

| 6.43% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 08/08/24 | 1,160,000 | $ 1,160,000 |

| SMG US Midco 2, Inc. | | |

| 5.44% (1 Month USD LIBOR + 3.00%, Rate Floor: 3.00%) due 01/23/25 | 990,000 | 980,407 |

| 9.44% (1 Month USD LIBOR + 7.00%, Rate Floor: 7.00%) due 01/23/26 | 125,000 | 126,250 |

| AT Home Holding III | | |

| 6.08% (3 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 06/03/22 | 1,104,249 | 1,090,446 |

| Galls LLC | | |

8.73% (2 Month USD LIBOR + 6.25%, Rate Floor: 7.25%) due 01/31/25†††,1 | 936,209 | 927,675 |

| 9.48% (1 Month USD LIBOR + 6.25% and Commercial Prime Lending Rate + | | |

5.25%, Rate Floor: 7.25%) due 01/31/24†††,1 | 110,526 | 99,323 |

8.73% (1 Month USD LIBOR + 6.25%, Rate Floor: 7.25%) due 01/31/25†††,1 | 27,630 | 27,378 |

| Cast & Crew Payroll LLC | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 02/09/26 | 1,000,000 | 1,004,750 |

| IBC Capital Ltd. | | |

| 6.36% (3 Month USD LIBOR + 3.75%, Rate Floor: 3.75%) due 09/11/23 | 990,000 | 975,150 |

| Nellson Nutraceutical | | |

| 6.85% (3 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 12/23/21 | 822,489 | 764,914 |

| Checkers Drive-In Restaurants, Inc. | | |

| 6.78% (1 Month USD LIBOR + 4.25% and 3 Month USD LIBOR + 4.25%, | | |

| Rate Floor: 5.25%) due 04/25/24 | 1,007,991 | 745,913 |

| Belk, Inc. | | |

| 7.29% (3 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 12/12/22 | 781,764 | 621,995 |

| NES Global Talent | | |

| 8.08% (3 Month USD LIBOR + 5.50%, Rate Floor: 6.50%) due 05/11/23 | 622,159 | 619,048 |

| Truck Hero, Inc. | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 3.75%) due 04/22/24 | 649,436 | 616,964 |

| Aimbridge Acquisition Co., Inc. | | |

| 6.24% (1 Month USD LIBOR + 3.75%, Rate Floor: 3.75%) due 02/02/26 | 500,000 | 501,250 |

| American Tire Distributors, Inc. | | |

| 8.52% (3 Month USD LIBOR + 6.00%, Rate Floor: 7.00%) due 09/01/23 | 425,232 | 420,980 |

| 9.98% (1 Month USD LIBOR + 7.50%, Rate Floor: 8.50%) due 09/01/24 | 83,280 | 78,342 |

| Drive Chassis (DCLI) | | |

| 10.83% (3 Month USD LIBOR + 8.25%, Rate Floor: 8.25%) due 04/10/26 | 500,000 | 480,000 |

| Leslie’s Poolmart, Inc. | | |

| 5.98% (2 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 08/16/23 | 463,627 | 449,222 |

| Outcomes Group Holdings, Inc. | | |

| 6.02% (1 Month USD LIBOR + 3.50% and 3 Month USD LIBOR + 3.50%, | | |

| Rate Floor: 3.50%) due 10/24/25 | 200,000 | 197,166 |

| Argo Merchants | | |

| 6.35% (3 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 12/06/24 | 149,632 | 148,043 |

| Petco Animal Supplies, Inc. | | |

| 5.83% (3 Month USD LIBOR + 3.25%, Rate Floor: 4.25%) due 01/26/23 | 98,977 | 75,364 |

Total Consumer, Cyclical | | 49,612,095 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 21| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Technology – 7.5% | | |

| Cologix Holdings, Inc. | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 3.75%) due 03/20/24 | 3,150,000 | $ 3,001,950 |

| 11.50% (Commercial Prime Lending Rate + 6.00%, Rate Floor: 7.00%) due 03/20/25 | 750,000 | 719,535 |

| Planview, Inc. | | |

7.69% (1 Month USD LIBOR + 5.25%, Rate Floor: 6.25%) due 01/27/23†††,1 | 1,965,000 | 1,965,000 |

12.19% (1 Month USD LIBOR + 9.75%, Rate Floor: 10.75%) due 07/27/23†††,1 | 900,000 | 908,604 |

| TIBCO Software, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 12/04/20 | 2,647,273 | 2,641,767 |

| Nimbus Acquisitions Bidco Ltd. | | |

| 7.25% (3 Month GBP LIBOR + 6.25%, Rate Floor: 7.25%) (in-kind rate was | | |

1.00%) due 07/15/21†††,1,7 | GBP 1,668,571 | 2,097,343 |

| 8.77% (3 Month USD LIBOR + 6.25%, Rate Floor: 7.25%) (in-kind rate was | | |

1.00%) due 07/15/21†††,1,7 | 423,111 | 415,256 |

| Datix Bidco Ltd. | | |

7.12% (6 Month USD LIBOR + 4.50%, Rate Floor: 4.50%) due 04/21/25†††,1 | 2,001,644 | 1,984,821 |

10.37% (6 Month USD LIBOR + 7.75%, Rate Floor: 7.75%) due 04/27/26†††,1 | 300,111 | 297,364 |

| GlobalFoundries, Inc. | | |

| due 05/22/26 | 2,250,000 | 2,227,500 |

| LANDesk Group, Inc. | | |

| 6.72% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 01/20/24 | 2,227,083 | 2,210,847 |

| Ministry Brands LLC | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 12/02/22 | 2,184,786 | 2,173,862 |

| Bullhorn, Inc. | | |

9.27% (3 Month USD LIBOR + 6.75%, Rate Floor: 7.75%) due 11/21/22†††,1 | 1,757,639 | 1,750,043 |

9.28% (3 Month USD LIBOR + 6.75%, Rate Floor: 7.75%) due 11/21/22†††,1 | 420,976 | 419,157 |

| EIG Investors Corp. | | |

| 6.27% (1 Month USD LIBOR + 3.75% and 3 Month USD LIBOR + 3.75%, | | |

| Rate Floor: 4.75%) due 02/09/23 | 2,076,450 | 2,067,625 |

| Cvent, Inc. | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 11/29/24 | 1,980,000 | 1,956,082 |

| Brave Parent Holdings, Inc. | | |

| 6.58% (2 Month USD LIBOR + 4.00% and 3 Month USD LIBOR + 4.00%, | | |

| Rate Floor: 4.00%) due 04/18/25 | 1,885,750 | 1,885,750 |

| Dun & Bradstreet | | |

| 7.43% (1 Month USD LIBOR + 5.00%, Rate Floor: 5.00%) due 02/06/26 | 1,750,000 | 1,745,625 |

| Park Place Technologies LLC | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 03/29/25 | 1,076,910 | 1,067,035 |

| 10.44% (1 Month USD LIBOR + 8.00%, Rate Floor: 9.00%) due 03/29/26 | 680,723 | 668,810 |

| MRI Software LLC | | |

| 7.94% (1 Month USD LIBOR + 5.50%, Rate Floor: 6.50%) due 06/30/23 | 1,493,378 | 1,478,445 |

| 8.10% (3 Month USD LIBOR + 5.50%, Rate Floor: 6.50%) due 06/30/23 | 20,444 | 20,240 |

| 7.93% (1 Month USD LIBOR + 5.50% and 3 Month USD LIBOR + 5.50%, | | |

Rate Floor: 6.50%) due 06/30/23†††,1 | 14,000 | 13,095 |

| 24-7 Intouch, Inc. | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 4.25%) due 08/25/25 | 1,492,500 | 1,417,875 |

See notes to financial statements.

22 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Technology – 7.5% (continued) | | |

| Refinitiv (Financial & Risk US Holdings, Inc.) | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 3.75%) due 10/01/25 | 1,396,500 | $ 1,360,498 |

| Transact Holdings, Inc. | | |

| 7.33% (3 Month USD LIBOR + 4.75%, Rate Floor: 4.75%) due 04/30/26 | 1,350,000 | 1,343,250 |

| Advanced Computer Software | | |

| 7.22% (1 Month USD LIBOR + 4.75%, Rate Floor: 4.75%) due 05/31/24 | 1,319,458 | 1,316,713 |

| Optiv, Inc. | | |

| 5.69% (1 Month USD LIBOR + 3.25%, Rate Floor: 4.25%) due 02/01/24 | 1,261,706 | 1,171,809 |

| Lytx, Inc. | | |

9.19% (1 Month USD LIBOR + 6.75%, Rate Floor: 7.75%) due 08/31/23†††,1 | 1,142,376 | 1,122,358 |

| Project Boost Purchaser LLC | | |

| due 06/01/26 | 1,000,000 | 996,250 |

| Project Accelerate Parent, LLC | | |

| 6.70% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 01/02/25 | 990,000 | 990,000 |

| Greenway Health LLC | | |

| 6.35% (3 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 02/16/24 | 989,924 | 861,234 |

| Aspect Software, Inc. | | |

| 7.47% (1 Month USD LIBOR + 5.00%, Rate Floor: 6.00%) due 01/15/24 | 1,022,669 | 840,634 |

| Informatica LLC | | |

| 5.69% (1 Month USD LIBOR + 3.25%, Rate Floor: 3.25%) due 08/05/22 | 800,000 | 799,000 |

| Jaggaer | | |

| 6.44% (1 Month USD LIBOR + 4.00% and Commercial Prime Lending | | |

| Rate + 3.00%, Rate Floor: 5.00%) due 12/28/24 | 597,232 | 588,273 |

| Ping Identity Corp. | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 01/24/25 | 496,250 | 494,389 |

| Misys Ltd. | | |

| 6.10% (3 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 06/13/24 | 397,869 | 389,235 |

| Solera LLC | | |

6.38% (1 Month USD LIBOR + 4.50%, Rate Floor: 4.50%) due 03/03/21†††,1 | 345,610 | 328,518 |

| Peak 10 Holding Corp. | | |

| 6.10% (3 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 08/01/24 | 247,487 | 228,307 |

| Targus Group International, Inc. | | |

due 05/24/16†††,1,2,12 | 155,450 | — |

Total Technology | | 47,964,099 |

| |

Consumer, Non-cyclical – 4.8% | | |

| WIRB – Copernicus Group, Inc. | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 08/15/22 | 3,306,993 | 3,290,458 |

| Springs Window Fashions | | |

| 10.93% (1 Month USD LIBOR + 8.50%, Rate Floor: 8.50%) due 06/15/26 | 1,350,000 | 1,285,875 |

| 6.68% (1 Month USD LIBOR + 4.25%, Rate Floor: 4.25%) due 06/15/25 | 1,120,428 | 1,075,611 |

| Endo Luxembourg Finance Co. | | |

| 6.75% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.00%) due 04/29/24 | 2,267,737 | 2,184,126 |

| Civitas Solutions, Inc. | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 4.25%) due 03/09/26 | 2,000,000 | 2,003,760 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 23| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Consumer, Non-cyclical – 4.8% (continued) | | |

| Immucor, Inc. | | |

| 7.60% (3 Month USD LIBOR + 5.00%, Rate Floor: 6.00%) due 06/15/21 | 1,965,000 | $ 1,955,175 |

| PlayPower, Inc. | | |

| 7.98% (3 Month USD LIBOR + 5.50%, Rate Floor: 5.50%) due 05/08/26 | 1,850,000 | 1,852,313 |

| Arctic Glacier Group Holdings, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 03/20/24 | 1,772,602 | 1,762,268 |

| ScribeAmerica Intermediate Holdco LLC (Healthchannels) | | |

| 6.97% (1 Month USD LIBOR + 4.50%, Rate Floor: 4.50%) due 04/03/25 | 1,636,495 | 1,618,084 |

| MDVIP LLC | | |

| 6.68% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 11/14/24 | 1,481,250 | 1,473,844 |

| California Cryobank | | |

| 6.60% (3 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 08/06/25 | 1,443,872 | 1,436,653 |

| Hearthside Group Holdings LLC | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 4.00%) due 05/23/25 | 1,446,375 | 1,426,487 |

| BCPE Eagle Buyer LLC | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 03/18/24 | 1,471,477 | 1,416,297 |

| Tecbid US, Inc. | | |

| 6.85% (3 Month USD LIBOR + 4.25%, Rate Floor: 4.25%) due 07/25/24 | 988,890 | 986,418 |

| Affordable Care Holding | | |

| 7.23% (2 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 10/24/22 | 970,000 | 940,900 |

| Give and Go Prepared Foods Corp. | | |

| 6.85% (3 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 07/29/23 | 827,400 | 756,037 |

| CPI Holdco LLC | | |

| 6.08% (3 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 03/21/24 | 694,684 | 693,815 |

| CTI Foods Holding Co. LLC | | |

| 9.58% (3 Month USD LIBOR + 7.00%, Rate Floor: 8.00%) due 05/03/24 | 468,529 | 468,529 |

| 10.58% (3 Month USD LIBOR + 8.00%, Rate Floor: 9.00%) due 05/03/24 | 190,901 | 181,356 |

| Moran Foods LLC | | |

| 8.60% (3 Month USD LIBOR + 6.00%, Rate Floor: 7.00%) due 12/05/23 | 1,197,449 | 621,177 |

| Certara, Inc. | | |

| 6.10% (3 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 08/15/24 | 616,132 | 612,281 |

| Avantor, Inc. | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 11/21/24 | 519,053 | 518,835 |

| Packaging Coordinators Midco, Inc. | | |

| 6.61% (3 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 06/30/23 | 507,580 | 506,311 |

| Hoffmaster Group, Inc. | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 11/21/23 | 441,031 | 439,928 |

| Kar Nut Products Company | | |

6.93% (1 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 03/31/23†††,1 | 374,907 | 371,913 |

| Sierra Acquisition, Inc. | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 11/11/24 | 299,244 | 297,000 |

| Affordable Care Holdings Corp. | | |

| 7.23% (2 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 10/24/22 | 246,856 | 239,450 |

See notes to financial statements.

24 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Consumer, Non-cyclical – 4.8% (continued) | | |

| Diamond (BC) B.V. | | |

| 5.58% (2 Month USD LIBOR + 3.00% and 3 Month USD LIBOR + 3.00%, | | |

| Rate Floor: 3.00%) due 09/06/24 | 249,369 | $ 221,315 |

| Acosta, Inc. | | |

| 5.41% (1 Month USD LIBOR + 3.25% and Commercial Prime Lending | | |

| Rate + 2.25%, Rate Floor: 3.25%) due 09/26/19 | 419,974 | 173,504 |

Total Consumer, Non-cyclical | | 30,809,720 |

| |

Basic Materials – 2.5% | | |

| ICP Industrial, Inc. | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 11/03/23 | 2,472,915 | 2,460,551 |

| PetroChoice Holdings | | |

| 7.58% (2 Month USD LIBOR + 5.00% and 3 Month USD LIBOR + 5.00%, | | |

| Rate Floor: 6.00%) due 08/19/22 | 2,035,017 | 2,022,298 |

| American Rock Salt Company LLC | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 03/21/25 | 1,980,000 | 1,971,743 |

| GrafTech Finance, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 02/12/25 | 1,664,194 | 1,649,633 |

| Niacet Corp. | | |

| 6.94% (1 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 02/01/24 | 1,612,827 | 1,604,763 |

| Big River Steel LLC | | |

| 7.60% (3 Month USD LIBOR + 5.00%, Rate Floor: 6.00%) due 08/23/23 | 1,539,842 | 1,541,767 |

| US Salt LLC | | |

| 7.19% (1 Month USD LIBOR + 4.75%, Rate Floor: 4.75%) due 01/16/26 | 1,000,000 | 997,500 |

| LTI Holdings, Inc. | | |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 09/06/25 | 995,000 | 945,668 |

| Niacet B.V. | | |

| 5.50% (1 Month EURIBOR + 4.50%, Rate Floor: 5.50%) due 02/01/24 | EUR 758,977 | 843,968 |

| Pregis Holding I Corp. | | |

| 6.10% (3 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 05/20/21 | 471,165 | 457,030 |

| ASP Chromaflo Dutch I B.V. | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 11/20/23 | 452,222 | 449,396 |

| Ranpak | | |

| 9.69% (1 Month USD LIBOR + 7.25%, Rate Floor: 8.25%) due 10/03/22 | 417,407 | 414,277 |

| ASP Chromaflo Intermediate Holdings, Inc. | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 11/20/23 | 347,778 | 345,604 |

| Vectra Co. | | |

| 5.69% (1 Month USD LIBOR + 3.25%, Rate Floor: 3.25%) due 03/08/25 | 149,623 | 142,984 |

| PMHC II, Inc. (Prince) | | |

| 6.15% (1 Month USD LIBOR + 3.50%, 12 Month USD LIBOR + 3.50% and | | |

| 3 Month USD LIBOR + 3.50%, Rate Floor: 4.50%) due 03/29/25 | 98,000 | 89,425 |

| Noranda Aluminum Acquisition Corp. | | |

8.00% (3 Month USD LIBOR + 4.50%, Rate Floor: 5.75%) due 02/28/1912 | 517,932 | 1,295 |

Total Basic Materials | | 15,937,902 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 25| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Communications – 2.1% | | |

| Trader Interactive | | |

8.94% (1 Month USD LIBOR + 6.50%, Rate Floor: 7.50%) due 06/17/24†††,1 | 2,725,034 | $ 2,690,982 |

| Conterra Ultra Broadband Holdings, Inc. | | |

| 6.99% (3 Month USD LIBOR + 4.50%, Rate Floor: 4.50%) due 04/30/26 | 2,000,000 | 2,002,500 |

| Houghton Mifflin Co. | | |

| 5.44% (1 Month USD LIBOR + 3.00%, Rate Floor: 4.00%) due 05/28/21 | 2,011,062 | 1,923,923 |

| Market Track LLC | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 06/05/24 | 2,112,375 | 1,922,261 |

| Imagine Print Solutions LLC | | |

| 7.19% (1 Month USD LIBOR + 4.75%, Rate Floor: 5.75%) due 06/21/22 | 1,960,000 | 1,675,800 |

| Flight Bidco, Inc. | | |

| 9.94% (1 Month USD LIBOR + 7.50%, Rate Floor: 7.50%) due 07/23/26 | 1,300,000 | 1,277,250 |

| 5.94% (1 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 07/23/25 | 350,000 | 345,040 |

| Resource Label Group LLC | | |

| 7.09% (3 Month USD LIBOR + 4.50%, Rate Floor: 5.50%) due 05/26/23 | 1,329,652 | 1,249,873 |

| Mcgraw-Hill Global Education Holdings LLC | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 05/04/22 | 485,800 | 460,675 |

| Cengage Learning Acquisitions, Inc. | | |

| 6.68% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 06/07/23 | 189,419 | 180,117 |

Total Communications | | 13,728,421 |

| |

Financial – 1.4% | | |

| Aretec Group, Inc. | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 4.25%) due 10/01/25 | 1,695,750 | 1,666,074 |

| Jefferies Finance LLC | | |

| due 05/21/26 | 1,550,000 | 1,546,606 |

| StepStone Group LP | | |

| 6.44% (1 Month USD LIBOR + 4.00%, Rate Floor: 5.00%) due 03/27/25 | 1,485,000 | 1,481,288 |

| Virtu Financial, Inc. | | |

| 6.13% (3 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 03/01/26 | 1,450,000 | 1,450,450 |

| Alliant Holdings Intermediate LLC | | |

| 5.70% (1 Month USD LIBOR + 3.25%, Rate Floor: 3.25%) due 05/09/25 | 1,000,000 | 985,830 |

| due 05/09/25 | 100,000 | 97,325 |

| Assetmark Financial Holdings, Inc. | | |

| 6.10% (3 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 11/14/25 | 723,188 | 724,091 |

| Jane Street Group LLC | | |

| 5.44% (1 Month USD LIBOR + 3.00%, Rate Floor: 3.00%) due 08/25/22 | 500,000 | 497,500 |

| Northstar Financial Services LLC | | |

| 5.69% (1 Month USD LIBOR + 3.25% and 1 Month USD LIBOR + 3.50%, | | |

| Rate Floor: 4.00%) due 05/25/25 | 392,341 | 386,781 |

| National Financial Partners Corp. | | |

| 5.44% (1 Month USD LIBOR + 3.00%, Rate Floor: 3.00%) due 01/08/24 | 100,000 | 97,188 |

Total Financial | | 8,933,133 |

See notes to financial statements.

26 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

SENIOR FLOATING RATE INTERESTS††,4 – 36.1% (continued) | | |

Utilities – 1.0% | | |

| Oregon Clean Energy LLC | | |

| 6.19% (1 Month USD LIBOR + 3.75%, Rate Floor: 4.75%) due 03/01/26 | 2,500,000 | $ 2,500,000 |

| Carroll County Energy LLC | | |

| 6.10% (3 Month USD LIBOR + 3.50%, Rate Floor: 3.50%) due 02/16/26 | 1,600,000 | 1,608,000 |

| Panda Power | | |

| 9.10% (3 Month USD LIBOR + 6.50%, Rate Floor: 7.50%) due 08/21/20 | 1,462,846 | 1,323,876 |

| EIF Channelview Cogeneration LLC | | |

| 6.69% (1 Month USD LIBOR + 4.25%, Rate Floor: 5.25%) due 05/03/25 | 908,517 | 914,577 |

Total Utilities | | 6,346,453 |

| |

Energy – 0.8% | | |

| Permian Production Partners LLC | | |

| 8.43% (1 Month USD LIBOR + 6.00%, Rate Floor: 7.00%) due 05/20/24 | 1,828,750 | 1,682,450 |

| SeaPort Financing LLC | | |

| 7.94% (1 Month USD LIBOR + 5.50%, Rate Floor: 5.50%) due 10/31/25 | 1,496,250 | 1,481,287 |

| Summit Midstream Partners, LP | | |

| 8.44% (1 Month USD LIBOR + 6.00%, Rate Floor: 7.00%) due 05/13/22 | 1,202,220 | 1,190,197 |

| Gavilan Resources LLC | | |

| 8.43% (1 Month USD LIBOR + 6.00%, Rate Floor: 7.00%) due 03/01/24 | 990,000 | 733,838 |

Total Energy | | 5,087,772 |

Total Senior Floating Rate Interests | | |

| (Cost $237,008,051) | | 232,045,071 |

| |

ASSET-BACKED SECURITIES†† – 18.2% | | |

Collateralized Loan Obligations – 11.9% | | |

| Golub Capital Partners CLO Ltd. | | |

2018-36A, 4.67% (3 Month USD LIBOR + 2.10%, Rate Floor: 0.00%) due 02/05/314,8 | 5,000,000 | 4,612,574 |

2018-39A, 4.79% (3 Month USD LIBOR + 2.20%, Rate Floor: 2.20%) due 10/20/284,8 | 2,500,000 | 2,459,882 |

2018-25A, 4.47% (3 Month USD LIBOR + 1.90%, Rate Floor: 1.90%) due 05/05/304,8 | 2,500,000 | 2,437,104 |

2017-16A, 5.77% (3 Month USD LIBOR + 3.00%, Rate Floor: 0.00%) due 07/25/294,8 | 1,500,000 | 1,457,758 |

| Diamond CLO Ltd. | | |

2018-1A, 6.29% (3 Month USD LIBOR + 3.70%, Rate Floor: 3.70%) due 07/22/304,8 | 3,000,000 | 2,930,496 |

2018-1A, 5.19% (3 Month USD LIBOR + 2.60%, Rate Floor: 2.60%) due 07/22/304,8 | 2,500,000 | 2,428,969 |

| Mountain Hawk II CLO Ltd. | | |

2018-2A, 4.94% (3 Month USD LIBOR + 2.35%, Rate Floor: 0.00%) due 07/20/244,8 | 3,000,000 | 3,002,007 |

2013-2A, 5.74% (3 Month USD LIBOR + 3.15%, Rate Floor: 0.00%) due 07/22/244,8 | 1,750,000 | 1,750,031 |

| Fortress Credit Opportunities IX CLO Ltd. | | |

2017-9A, 5.17% (3 Month USD LIBOR + 2.65%, Rate Floor: 0.00%) due 11/15/294,8 | 4,000,000 | 3,868,758 |

| Marathon CRE Ltd. | | |

2018-FL1, 5.44% (1 Month USD LIBOR + 3.00%, Rate Floor: 3.00%) due 06/15/284,8 | 3,000,000 | 3,006,070 |

| FDF I Ltd. | | |

2015-1A, 6.88% due 11/12/308 | 2,000,000 | 1,997,480 |

2015-1A, 7.50% due 11/12/309 | 1,000,000 | 988,758 |

| FDF II Ltd. | | |

2016-2A, 7.70% due 05/12/319 | 3,000,000 | 2,971,997 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 27| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

ASSET-BACKED SECURITIES†† – 18.2% (continued) | | |

Collateralized Loan Obligations – 11.9% (continued) | | |

| Dryden 50 Senior Loan Fund | | |

2017-50A, due 07/15/308,10 | 3,555,000 | $ 2,762,903 |

| Denali Capital CLO XI Ltd. | | |

2018-1A, 4.74% (3 Month USD LIBOR + 2.15%, Rate Floor: 0.00%) due 10/20/284,8 | 2,400,000 | 2,399,805 |

| DRSLF | | |

due 01/15/3110 | 2,998,799 | 2,278,488 |

| Newstar Commercial Loan Funding LLC | | |

2017-1A, 7.73% (3 Month USD LIBOR + 5.10%, Rate Floor: 0.00%) due 03/20/274,8 | 2,000,000 | 2,001,390 |

2017-1A, 6.13% (3 Month USD LIBOR + 3.50%, Rate Floor: 0.00%) due 03/20/274,8 | 250,000 | 250,156 |

| Avery Point VI CLO Ltd. | | |

2018-6A, 4.57% (3 Month USD LIBOR + 2.00%, Rate Floor: 0.00%) due 08/05/274,8 | 2,000,000 | 1,972,207 |

| MP CLO VIII Ltd. | | |

2018-2A, 4.48% (3 Month USD LIBOR + 1.90%, Rate Floor: 0.00%) due 10/28/274,8 | 2,000,000 | 1,951,749 |

| Carlyle Global Market Strategies CLO Ltd. | | |

2012-3A, due 01/14/328,10 | 2,600,000 | 1,889,698 |

| TPG Real Estate Finance Issuer Ltd. | | |

2018-FL1, 5.13% (1 Month USD LIBOR + 2.70%, Rate Floor: 2.70%) due 02/15/354,8 | 1,800,000 | 1,806,791 |

| Exantas Capital Corporation Ltd. | | |

2018-RSO6, 4.93% (1 Month USD LIBOR + 2.50%, Rate Floor: 2.50%) due 06/15/354,8 | 1,800,000 | 1,799,992 |

| Hunt CRE Ltd. | | |

2017-FL1, 5.74% (1 Month USD LIBOR + 3.30%, Rate Floor: 0.00%) due 08/15/344,8 | 1,800,000 | 1,793,174 |

| Avery Point II CLO Ltd. | | |

2013-3X COM, due 01/18/2510 | 2,399,940 | 1,765,507 |

| Cent CLO 19 Ltd. | | |

2013-19A, 5.88% (3 Month USD LIBOR + 3.30%, Rate Floor: 0.00%) due 10/29/254,8 | 1,750,000 | 1,749,209 |

| Treman Park CLO Ltd. | | |

2015-1A, due 10/20/288,10 | 2,000,000 | 1,738,434 |

| Monroe Capital CLO Ltd. | | |

2017-1A, 6.19% (3 Month USD LIBOR + 3.60%, Rate Floor: 0.00%) due 10/22/264,8 | 1,750,000 | 1,709,321 |

| OHA Credit Partners IX Ltd. | | |

2013-9A, due 10/20/258,10 | 2,000,000 | 1,664,724 |

| Voya CLO Ltd. | | |

2013-1A, due 10/15/308,10 | 3,000,000 | 1,601,949 |

| Atlas Senior Loan Fund IX Ltd. | | |

2018-9A, due 04/20/288,10,14 | 2,600,000 | 1,387,493 |

| Ladder Capital Commercial Mortgage Trust | | |

2017-FL1, 6.03% (1 Month USD LIBOR + 3.60%, Rate Floor: 3.60%) due 09/15/344,8 | 1,350,000 | 1,344,244 |

| Babson CLO Ltd. | | |

2014-IA, due 07/20/258,10 | 3,000,000 | 984,747 |

2012-2A, due 05/15/238,10 | 2,000,000 | 24,400 |

| NewStar Clarendon Fund CLO LLC | | |

2015-1A, 6.93% (3 Month USD LIBOR + 4.35%, Rate Floor: 0.00%) due 01/25/274,8 | 1,000,000 | 1,000,364 |

| Marathon CLO V Ltd. | | |

2013-5A, due 11/21/278,10 | 3,566,667 | 996,295 |

See notes to financial statements.

28 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

ASSET-BACKED SECURITIES†† – 18.2% (continued) | | |

Collateralized Loan Obligations – 11.9% (continued) | | |

| Jackson Mill CLO Ltd. | | |

2018-1A, 4.45% (3 Month USD LIBOR + 1.85%, Rate Floor: 1.85%) due 04/15/274,8 | 1,000,000 | $ 980,588 |

| KVK CLO Ltd. | | |

2013-1A, due 01/14/288,10,14 | 2,300,000 | 894,744 |

| Venture XIII CLO Ltd. | | |

2013-13A, due 09/10/298,10 | 1,500,000 | 845,671 |

| Dryden 41 Senior Loan Fund | | |

2015-41A, due 04/15/318,10 | 1,250,000 | 818,750 |

| Dryden 37 Senior Loan Fund | | |

2015-37A, due 01/15/318,10 | 1,050,000 | 797,790 |

| Great Lakes CLO Ltd. | | |

2014-1A, due 10/15/298,10 | 1,153,846 | 743,753 |

| West CLO Ltd. | | |

2013-1A, due 11/07/258,10 | 1,350,000 | 274,077 |

Total Collateralized Loan Obligations | | 76,140,297 |

| |

Transport-Aircraft – 3.6% | | |

| Apollo Aviation Securitization Equity Trust | | |

2018-1A, 5.44% due 01/16/388 | 2,631,919 | 2,697,965 |

2017-1A, 5.93% due 05/16/428 | 2,605,706 | 2,693,664 |

| 2016-2, 7.87% due 11/15/41 | 1,032,075 | 1,032,751 |

| 2016-2, 5.93% due 11/15/41 | 560,230 | 565,338 |

2016-1A, 6.50% due 03/17/368,11 | 525,934 | 538,849 |

| AIM Aviation Finance Ltd. | | |

2015-1A, 5.07% due 02/15/408 | 4,207,595 | 4,255,386 |

| AASET 2018-2 US Ltd. | | |

2018-2A, 5.43% due 11/18/388 | 2,862,614 | 2,919,641 |

| Willis Engine Securitization Trust II | | |

2012-A, 5.50% due 09/15/378,11 | 2,140,803 | 2,202,995 |

| KDAC Aviation Finance Ltd. | | |

2017-1A, 4.21% due 12/15/428 | 1,679,411 | 1,710,417 |

| Falcon Aerospace Limited | | |

2017-1, 6.30% due 02/15/428 | 1,640,899 | 1,697,255 |

| Castlelake Aircraft Securitization Trust | | |

due 12/31/30†††,1,17 | 3,054,105 | 1,137,663 |

| Stripes Aircraft Ltd. | | |

2013-1 A1, 5.94% due 03/20/23††† | 1,131,999 | 1,109,449 |

| Turbine Engines Securitization Ltd. | | |

2013-1A, 6.38% due 12/13/489 | 470,691 | 406,996 |

| Airplanes Pass Through Trust | | |

| 2001-1A, 3.01% (1 Month USD LIBOR + 0.55%, Rate Floor: 0.55%) | | |

due 03/15/19†††,4,9,12 | 6,677,317 | 129,373 |

Total Transport-Aircraft | | 23,097,742 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 29| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

ASSET-BACKED SECURITIES†† – 18.2% (continued) | | |

Whole Business – 1.0% | | |

| TSGE | | |

2017-1, 6.25% due 09/25/31†††,1 | 5,000,000 | $ 5,196,757 |

| Wingstop Funding LLC | | |

2018-1, 4.97% due 12/05/488 | 1,000,000 | 1,045,600 |

Total Whole Business | | 6,242,357 |

| |

Collateralized Debt Obligations – 0.7% | | |

| Anchorage Credit Funding 1 Ltd. | | |

2015-1A, 6.30% due 07/28/308 | 3,000,000 | 2,970,826 |

| Anchorage Credit Funding 4 Ltd. | | |

2016-4A, 5.50% due 02/15/358 | 1,000,000 | 1,007,236 |

| Highland Park CDO I Ltd. | | |

2006-1A, 3.05% (3 Month USD LIBOR + 0.40%, Rate Floor: 0.00%) due 11/25/514,9,14 | 297,271 | 294,263 |

Total Collateralized Debt Obligations | | 4,272,325 |

| |

Insurance – 0.3% | | |

| LTCG Securitization Issuer LLC | | |

2018-A, 4.59% due 06/15/488 | 2,123,412 | 2,140,557 |

| |

Infrastructure – 0.3% | | |

| Secured Tenant Site Contract Revenue Notes Series | | |

2018-1A, 5.92% due 06/15/488 | 1,981,666 | 1,971,287 |

| |

Diversified Payment Rights – 0.2% | | |

| Bib Merchant Voucher Receivables Ltd. | | |

4.18% due 04/07/28†††,1 | 1,100,000 | 1,151,589 |

| |

Financial – 0.1% | | |

| NCBJ | | |

2015-1A, 5.88% due 07/08/22†††,1 | 1,023,953 | 1,031,244 |

| |

Transport-Container – 0.1% | | |

| Global SC Finance II SRL | | |

2013-1A, 2.98% due 04/17/288 | 783,333 | 779,460 |

Total Asset-Backed Securities | | |

| (Cost $122,754,920) | | 116,826,858 |

| |

CORPORATE BONDS†† – 15.3% | | |

Financial – 5.6% | | |

| QBE Insurance Group Ltd. | | |

7.50% due 11/24/435,8 | 3,000,000 | 3,273,000 |

| Bank of America Corp. | | |

6.50%3,5 | 2,000,000 | 2,175,000 |

6.30%3,5 | 1,000,000 | 1,095,000 |

| Springleaf Finance Corp. | | |

| 7.13% due 03/15/26 | 1,550,000 | 1,625,097 |

| 6.13% due 03/15/24 | 1,500,000 | 1,556,250 |

See notes to financial statements.

30 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

CORPORATE BONDS†† – 15.3% (continued) | | |

Financial – 5.6% (continued) | | |

| BBC Military Housing-Navy Northeast LLC | | |

6.30% due 10/15/4914 | 2,900,000 | $ 3,078,664 |

| American Equity Investment Life Holding Co. | | |

| 5.00% due 06/15/27 | 2,950,000 | 2,990,621 |

| Citizens Financial Group, Inc. | | |

5.50%3,5 | 2,500,000 | 2,506,250 |

| Macquarie Group Ltd. | | |

5.03% due 01/15/305,8 | 2,000,000 | 2,164,526 |

| Assurant, Inc. | | |

| 4.90% due 03/27/28 | 1,950,000 | 2,078,323 |

| Fort Knox Military Housing Privatization Project | | |

5.82% due 02/15/528 | 1,928,096 | 2,058,971 |

| CNB Financial Corp. | | |

5.75% due 10/15/265,9 | 2,000,000 | 2,037,860 |

| Atlas Mara Ltd. | | |

| 8.00% due 12/31/20 | 2,200,000 | 1,927,000 |

| Hunt Companies, Inc. | | |

6.25% due 02/15/268 | 1,675,000 | 1,555,656 |

| Newmark Group, Inc. | | |

| 6.13% due 11/15/23 | 1,450,000 | 1,483,117 |

| Jefferies Finance LLC / JFIN Company-Issuer Corp. | | |

7.25% due 08/15/248 | 1,500,000 | 1,470,000 |

| GEO Group, Inc. | | |

| 5.88% due 10/15/24 | 600,000 | 556,500 |

| 5.88% due 01/15/22 | 300,000 | 296,250 |

| 5.13% due 04/01/23 | 275,000 | 258,500 |

| 6.00% due 04/15/26 | 100,000 | 91,750 |

| Fort Benning Family Communities LLC | | |

6.09% due 01/15/518 | 729,341 | 819,639 |

| Pacific Beacon LLC | | |

5.63% due 07/15/518,14 | 695,353 | 721,598 |

| Hospitality Properties Trust | | |

| 5.25% due 02/15/26 | 158,000 | 165,970 |

| CoreCivic, Inc. | | |

| 4.75% due 10/15/27 | 125,000 | 110,625 |

| Icahn Enterprises, LP / Icahn Enterprises Finance Corp. | | |

| 5.88% due 02/01/22 | 50,000 | 50,438 |

Total Financial | | 36,146,605 |

| |

Energy – 1.9% | | |

| Hess Corp. | | |

| 5.60% due 02/15/41 | 1,550,000 | 1,565,955 |

| 6.00% due 01/15/40 | 1,000,000 | 1,062,264 |

| 7.13% due 03/15/33 | 500,000 | 597,441 |

See notes to financial statements.

GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT l 31| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

CORPORATE BONDS†† – 15.3% (continued) | | |

Energy – 1.9% (continued) | | |

| Bruin E&P Partners LLC | | |

8.88% due 08/01/238 | 1,825,000 | $ 1,637,938 |

| Indigo Natural Resources LLC | | |

6.88% due 02/15/268 | 1,750,000 | 1,570,625 |

| Husky Energy, Inc. | | |

| 4.00% due 04/15/24 | 900,000 | 919,036 |

| 3.95% due 04/15/22 | 600,000 | 613,355 |

| Sunoco Logistics Partners Operations, LP | | |

| 4.25% due 04/01/24 | 1,000,000 | 1,032,541 |

| American Midstream Partners Limited Partnership / American Midstream Finance Corp. | | |

9.50% due 12/15/218 | 895,000 | 868,150 |

| EQT Corp. | | |

| 8.13% due 06/01/19 | 800,000 | 800,000 |

| Buckeye Partners, LP | | |

| 4.35% due 10/15/24 | 750,000 | 744,315 |

| Unit Corp. | | |

| 6.63% due 05/15/21 | 500,000 | 470,000 |

| Basic Energy Services, Inc. | | |

10.75% due 10/15/238 | 500,000 | 395,000 |

| Schahin II Finance Co. SPV Ltd. | | |

5.88% due 09/25/228,12 | 1,216,133 | 121,613 |

Total Energy | | 12,398,233 |

| |

Industrial – 1.9% | | |

| Encore Capital Group, Inc. | | |

5.63% due 08/11/24††† | 4,000,000 | 3,972,450 |

| Dynagas LNG Partners Limited Partnership / Dynagas Finance, Inc. | | |

| 6.25% due 10/30/19 | 1,800,000 | 1,702,170 |

| Reynolds Group Issuer Incorporated / Reynolds Group Issuer LLC / | | |

| Reynolds Group Issuer Luxembourg | | |

6.10% (3 Month USD LIBOR + 3.50%) due 07/15/214,8 | 1,225,000 | 1,229,594 |

| 5.75% due 10/15/20 | 436,098 | 436,774 |

| Intertape Polymer Group, Inc. | | |

7.00% due 10/15/268 | 1,450,000 | 1,479,000 |

| Princess Juliana International Airport Operating Company N.V. | | |

5.50% due 12/20/279 | 1,528,550 | 1,424,425 |

| Cleaver-Brooks, Inc. | | |

7.88% due 03/01/238 | 650,000 | 624,000 |

| Grinding Media Inc. / MC Grinding Media Canada Inc. | | |

7.38% due 12/15/238 | 500,000 | 465,000 |

| Glenn Pool Oil & Gas Trust | | |

6.00% due 08/02/21††† | 451,519 | 448,600 |

| Great Lakes Dredge & Dock Corp. | | |

| 8.00% due 05/15/22 | 376,000 | 395,740 |

Total Industrial | | 12,177,753 |

See notes to financial statements.

32 l GOF l GUGGENHEIM STRATEGIC OPPORTUNITIES FUND ANNUAL REPORT| | |

SCHEDULE OF INVESTMENTS continued | May 31, 2019 |

| | | |

| | Face | |

| | Amount~ | Value |

| |

CORPORATE BONDS†† – 15.3% (continued) | | |

Consumer, Cyclical – 1.8% | | |

| Exide Technologies | | |

11.00% (in-kind rate was 7.00%) due 04/30/227,8,14 | 2,504,083 | $ 2,053,348 |

| 10.75% due 10/31/21 | 732,227 | 710,260 |

| HP Communities LLC | | |

6.16% due 09/15/538,14 | 1,000,000 | 1,193,856 |

6.82% due 09/15/538,14 | 960,145 | 1,099,378 |

| Williams Scotsman International, Inc. | | |

6.88% due 08/15/238 | 1,650,000 | 1,650,000 |

| Panther BF Aggregator 2 Limited Partnership / Panther Finance Company, Inc. | | |

8.50% due 05/15/278 | 1,500,000 | 1,496,250 |

| Titan International, Inc. | | |

| 6.50% due 11/30/23 | 1,550,000 | 1,328,157 |

| JB Poindexter & Company, Inc. | | |

7.13% due 04/15/268 | 1,100,000 | 1,122,000 |

| Party City Holdings, Inc. | | |

6.63% due 08/01/268 | 875,000 | 870,625 |

Total Consumer, Cyclical | | 11,523,874 |

| |

Basic Materials – 1.4% | | |

| BHP Billiton Finance USA Ltd. | | |

6.75% due 10/19/755,8 | 2,450,000 | 2,749,071 |

| Yamana Gold, Inc. | | |

| 4.95% due 07/15/24 | 2,560,000 | 2,652,928 |

| Eldorado Gold Corp. | | |